Aviva UK: Winning In The UK November 2010

42

nn ng n e

-

Upload

aviva-group -

Category

Documents

-

view

221 -

download

0

Transcript of Aviva UK: Winning In The UK November 2010

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 1/42

nn ng n e

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 2/42

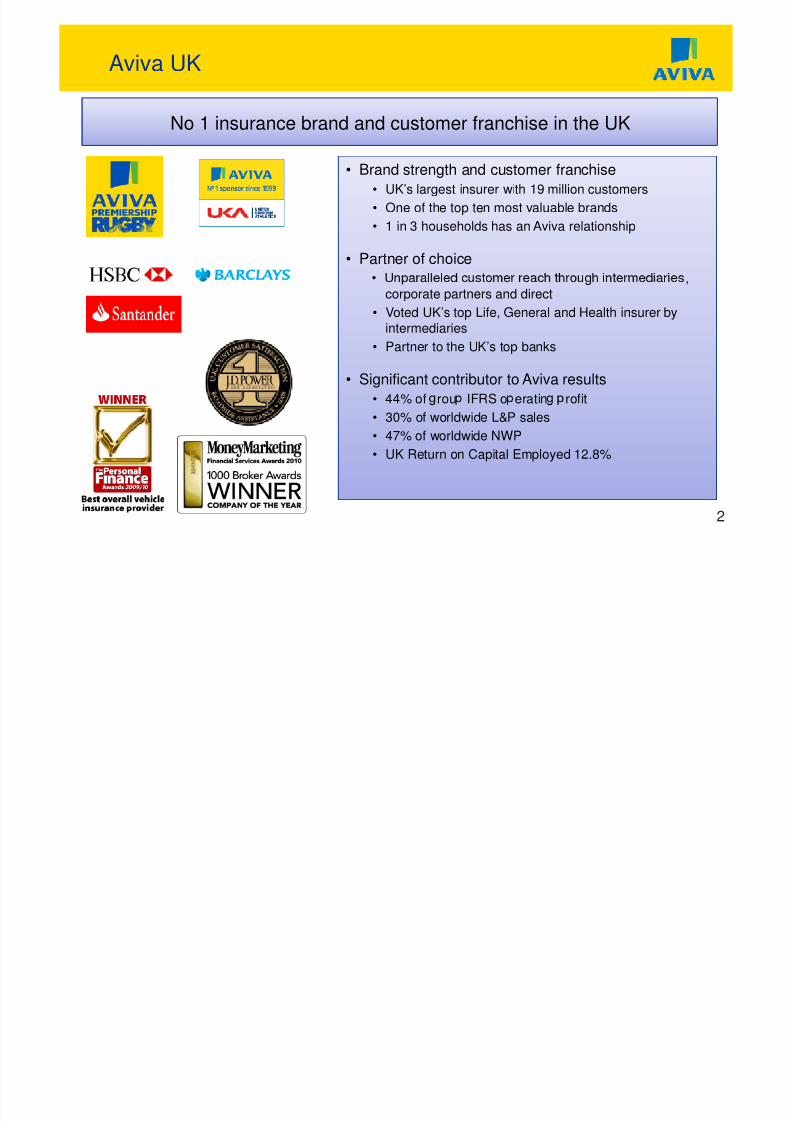

Aviva UK

No 1 insurance brand and customer franchise in the UK

No 1 insurance brand and customer franchise in the UK

• Brand strength and customer franchise

• UK’s largest insurer with 19 million customers• One of the top ten most valuable brands

• 1 in 3 households has an Aviva relationship

• Partner of choice

,

corporate partners and direct• Voted UK’s top Life, General and Health insurer by

intermediaries

• Partner to the UK’s top banks

• Significant contributor to Aviva results

• 44% of rou IFRS o eratin rofit

• 30% of worldwide L&P sales

• 47% of worldwide NWP

• UK Return on Capital Employed 12.8%

2

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 3/42

Aviva UK

CEO Aviva UKMark Hod es

UK Life CEOToby Strauss

UK GI CEODavid McMillan

UK Commercial

DirectorUK CRO

Craig ThorntonUK HRD

Rupert McNeil

3

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 4/42

Aviva UK

A unique opportunity for customers and shareholdersA unique opportunity for customers and shareholders

• Increase earnings from new and in-force business

• Capitalise on our multi-channel, multi-product strategy

• Win in an RDR world through strong brand andservice

• Underwriting and risk management capability

• Drive profitable growth

• Excellence in underwriting, claims management andcustomer service

• Expand profitably into business lines and segments

where underweight

UK

Drive outadditional

• Leverage brand to drive earnings from 19mcustomers

•

4

value

• Generate further cost and efficiency savings• Exploit capital diversification benefit

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 5/42

Aviva UK

A leading competitive positionA leading competitive position

750)

650

rofit* (£

450

erating

250

350

IF

RS o

50

150

HY201

-50

5

(253)

* HY 2010 IFRS operating profit or reported equivalent (£m)AXA operating profit includes UK and Ireland, RBS operating profit includes international businesses

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 6/42

Aviva UK

A unique opportunity for customers and shareholdersA unique opportunity for customers and shareholders

UK

Drive outadditional

6

value

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 7/42

UK Life today

Performance transformed over last 5 yearsPerformance transformed over last 5 years

FY 2005 HY 2010 +/-

Operating Expenses £941m £379m

FY 2005 Q3 2010 +/-

, ,

Life & Pensions margin 1.8% 3.5% +170bp

New business IRR 10.6% 15.1%

Payback (years) 9 7

+450bp

2

7

Capital Intensity 5.3% 2.7%

+260bp

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 8/42

UK Life today

We have driven substantive and permanent operational changeWe have driven substantive and permanent operational change

2005 Q3 2010

Systems rationalisation20 core admin systems 4 core admin systems

12,500 UK headcount(9 sites)

7,600 UK headcount(5 sites)

Site rationalisation

Over 5 million policies

98% of customeroperations in house

37% outsourced,16% offshoreFlexible cost base

Customer and Adviser Portale-commerce ca abilit

Distributor satisfaction41%

Distributor satisfaction76%

- --available on-line

Customer centric designCustomer satisfaction

38%Customer satisfaction

76%

8

Leadership and focus

Employee engagement

49%

Employee engagement

71%

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 9/42

UK Life today

An ambitious programme has transformed our operating expense baseAn ambitious programme has transformed our operating expense base

UK Life expense base• £211m reduction in underlying

£941m

£730m800

900

1,000

)

• Continuing to operate in linewith expense allowances

500

600

700

penses (£ • P&L benefit of £100m by end

of 2012 reflecting costreduction and growth

200

300

400

erating e

• Pension scheme closure

• UK procurement

0

2005 2010 Est.

O • E-commerce / self-service

9

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 10/42

UK Life today

A strong and diversified new business franchiseA strong and diversified new business franchise

Q3 2010 Mix(PVNBP) IRR Payback(Years) Margin CapitalIntensity

Pensions (inc. SIPP) 40% 12.8% 9 1.7% 3.5%

Bonds 17% 23.9% 6 1.5% 0.4%

Annuities 30% 22.2% 6 5.7% 2.0%

Protection 10% 13.9% 6 7.6% 8.7%

qu y e ease > . .

Life and Pensions Total 100% 15.1% 7 3.5% 2.7%

10

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 11/42

UK Life today

Proactive pricing actions driving up IRRProactive pricing actions driving up IRR

IRR

Pricing actions include:

• Reduced commission on

14%

15%

16% bonds, individual pensionsand GPPs

• Successful launch of

12%

13% adviser charging pensionsproduct

• Protection re- ricin from 2

9%

10%

months to 2 days

• Annuities re-pricing from 1month to 1 da ostcode

8%

FY 2005 MixMovement

ExpenseReduction

PricingActions

Q3 2010

pricing

• Improved reinsurance for

11

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 12/42

UK Life today

Experience broadly in line with long term assumptionsExperience broadly in line with long term assumptions

HY 2010

Persistency Shortterm

LongtermExperience

variances

Bonds

Protection

Mortality / Morbidity £12m

Management actions:

• Proactive management of bond

Persistency £(10)m

• Action on individual IFA accounts

• Protection la se alert for IFAs

Expenses £(8)m

• Improved customer and distributorcommunications

Total £(6)m

12IRR using short term persistency assumptions would be 14.8% vs. 15.1%

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 13/42

UK Life today

Growing IFRS operating profits from a base of £800m+ paGrowing IFRS operating profits from a base of £800m+ pa

150

200

250

(£m

)HY 2009 Operating profit £368m

HY 2010 Operating profit £463m

0

50

100

rating profi

(200)

(150)

(100)

IFRS op

Newbusinessmargin

Technicalmargin

Unitlinkedmargin

Participatingbusiness

Spreadmargin

Expectedreturn

Acquisitionexpenses

Adminexpenses

DAC

• Disciplined financial management of new business, costs and in-force book

• Reattribution benefit of £120m per year

• Resilient rofits in a low interest rate environment

13

• Generating £400m+ of net operating capital per annum

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 14/42

UK Life today

A strong competitive positionA strong competitive position

500

400

450

rofit (£m

250

300

350

erating

P

150

200

IF

RS Op

0

50

100

H1 2009 H2 2009 H1 2010

14

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 15/42

UK Life today

Consistent strategy and disciplined execution – delivered distinctive positionConsistent strategy and disciplined execution – delivered distinctive position

500

400

it HY 2010

300

ating Prof

100IFRS Ope

0

NBC HY 2010

15

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 16/42

UK Life market

Market growth and opportunityMarket growth and opportunity

The UK Life market is attractive:

• Demo ra hic trends and the demiseNumber of people aged 65

of defined benefit schemes willincrease the market by 30% over thenext 5 years

• UK retirement savings gap £318bn(1)

per year

• (2) .

• Ageing population creating

opportunities for new product

products e.g. Long term care

16(1) Source: “Mind the gap – quantifying Europe’s pensions gap,” Aviva & Deloitte, September 2010 (2) Source: Swiss Re Term and Health Watch 2010

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 17/42

UK Life looking forward

Winning positions in our chosen growth marketsWinning positions in our chosen growth markets

Sectors and Products 3 yr CAGRmarket IRR Est. marketposition b Current Competitive Focusforecast vol

Individual(0.5)% 13.5% 6* 8%

Provide service and defend

GPP +10% 12.0% 4 11% Move to Top 3

Bonds +3% 23.9% 2 11%e ec ve grow w ere

value

Annuities +17% 22.2% 1 20% Consolidate No1 position

Core Protection (1)% 20.7% 2 15% Move to clear No1 position

17

Equity Release (3)% N/A 1 48% Consolidate No1 position

* IPP 2nd

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 18/42

UK Life looking forward

Well placed to win in an RDR worldWell placed to win in an RDR world

Aviva UK Life channel & product analysis (NBC)* • To win in an RDR world requires:

• A strong brand

• Diverse distribution

• Well positioned products

• Excellent service

NBC by Product &Channel

IFA

Building

Socs

EBCs Retail Total

Bonds 3% 4% - - 7%

• Successfully launched RDRcompliant pensions products

• Well positioned in largely

Individual Pensions 10% 1% 1% - 12%

GPP 2% - 2% - 4%

Corporate pensions - - 1% - 1%

market

• IFA segmentation used to identify

winners

nnu es -

Protection 7% 9% 4% 1% 21%

Equity release 3% - - 2% 5%

• RDR resilient bancassurancerelationships growing

• Continue to build customer

RDR impact

Limited RDR impact

18•HY 2010

EBCs – Employee Benefit Consultants

capability through e-commerce

investment

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 19/42

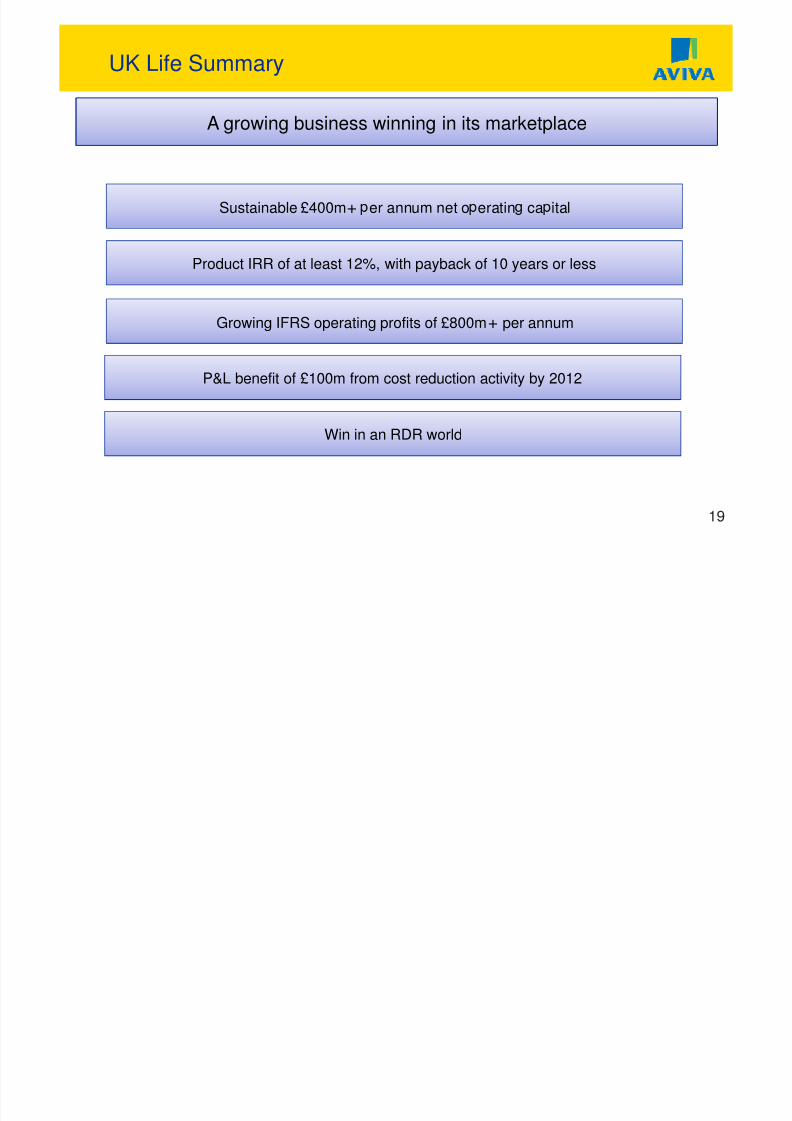

UK Life Summary

A growing business winning in its marketplaceA growing business winning in its marketplace

Sustainable £400m+ er annum net o eratin ca ital

Product IRR of at least 12%, with payback of 10 years or less

Growing IFRS operating profits of £800m+ per annum

P&L benefit of £100m from cost reduction activity by 2012

Win in an RDR world

19

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 20/42

Aviva UK

A unique opportunity for customers and shareholdersA unique opportunity for customers and shareholders

UK

Drive outadditional

20

value

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 21/42

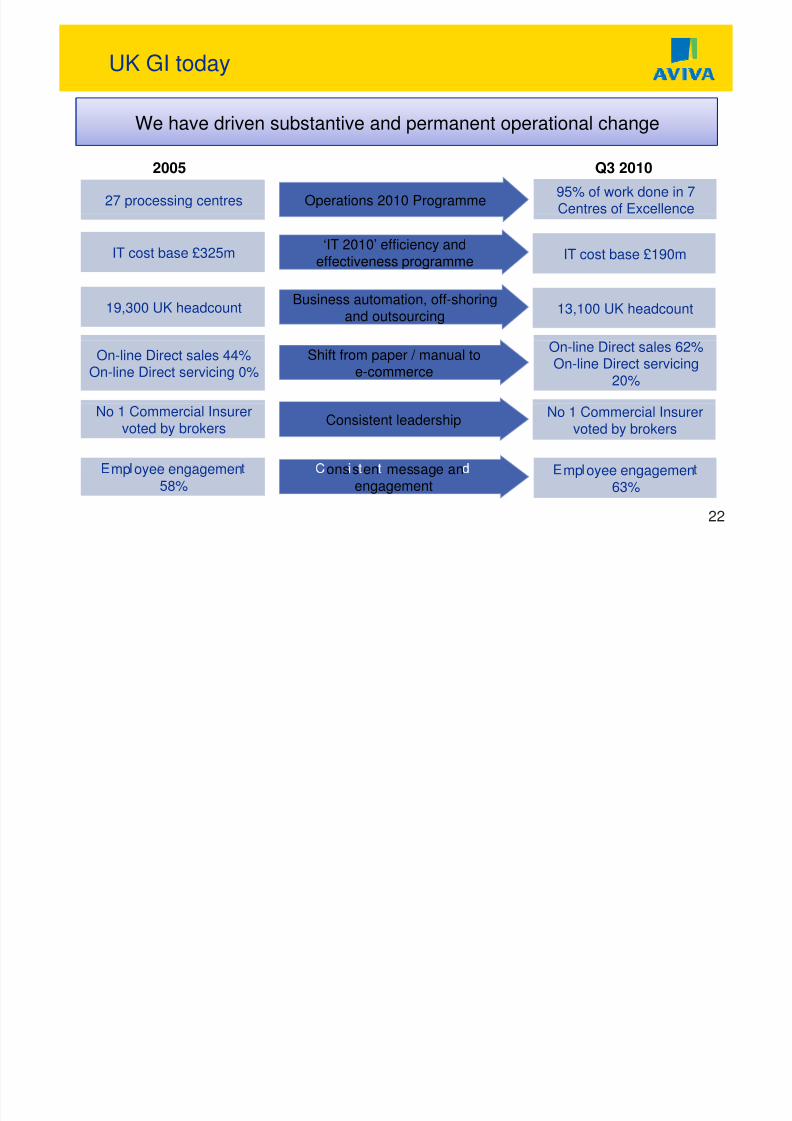

UK GI today

Leading distribution franchise and core insurance excellenceLeading distribution franchise and core insurance excellence

• A market leader with >10% share

•

• No1 for Commercial SME

• Two great direct brands - Aviva and RAC

LeadingDistributionFranchise

• No1 for GI Bancassurance

• Underwriting excellence and largest underwriting footprint(28 branches, 1,800 underwriters)

• Leading edge pricing (Aviva Risk Index “ARi”)

• 7 operational Centres of Excellence delivering scale and bestpractice

InsuranceExcellence

21

• Award winning service

• Purchasing power and claims supply chain management

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 22/42

UK GI today

We have driven substantive and permanent operational changeWe have driven substantive and permanent operational change

2005 Q3 2010

Operations 2010 Programme27 processing centres95% of work done in 7Centres of Excellence

IT cost base £325m‘IT 2010’ efficiency and

effectiveness programmeIT cost base £190m

19,300 UK headcount Business automation, off-shoringand outsourcing

13,100 UK headcount

Shift from paper / manual toe-commerce

On-line Direct sales 44%On-line Direct servicing 0%

On-line Direct sales 62%On-line Direct servicing

20%

Consistent leadershipNo 1 Commercial Insurer

voted by brokersNo 1 Commercial Insurer

voted by brokers

22

ons s en message an

engagement

mp oyee engagemen

58%

mp oyee engagemen

63%

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 23/42

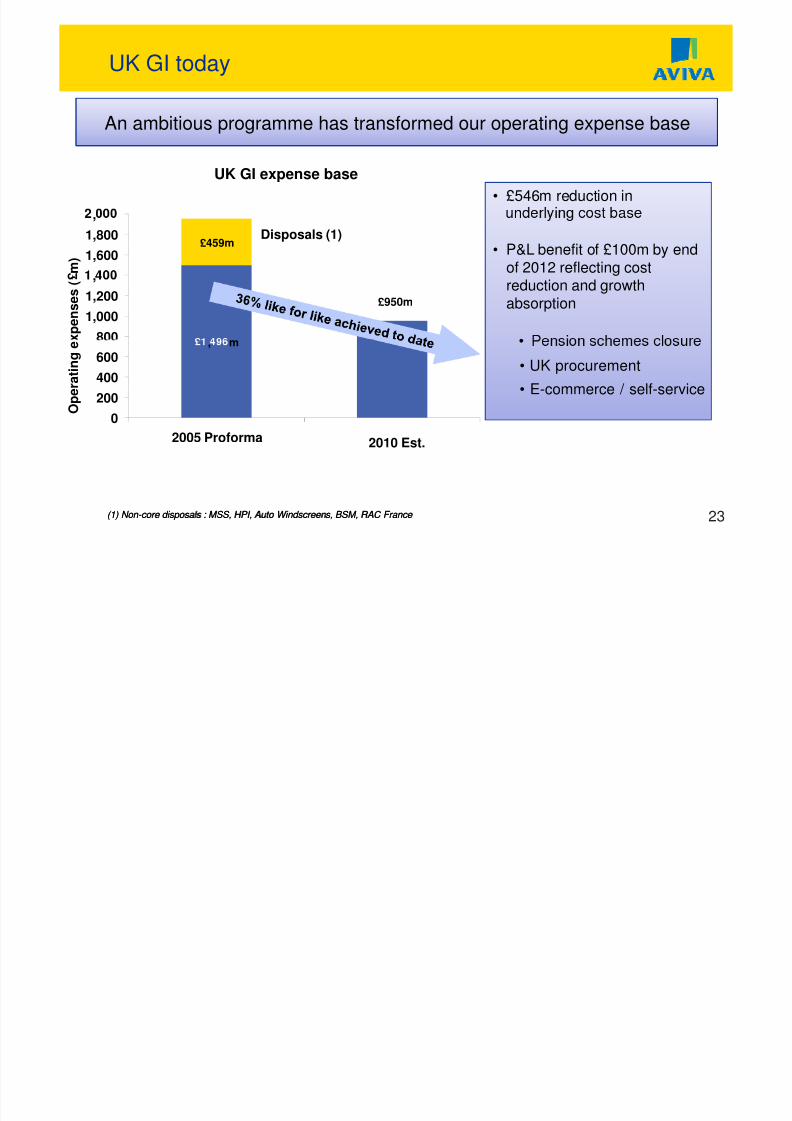

UK GI today

An ambitious programme has transformed our operating expense baseAn ambitious programme has transformed our operating expense base

• £546m reduction in

UK GI expense base

£459m1,600

1,800

,

m)

Disposals (1)

• P&L benefit of £100m by endof 2012 reflecting cost

£950m

800

1,0001,200

,

xpenses ( reduction and growth

absorption

, m

200

400

600

pe

rating e

• UK procurement

• E-commerce / self-service0

2005 Proforma

O

2010 Est.

(1) Non (1) Non- -core disposals : MSS, HPI, Auto Windscreens, BSM, RAC France core disposals : MSS, HPI, Auto Windscreens, BSM, RAC France 23

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 24/42

UK GI today

Active cycle managementActive cycle management

94%6,000

NWP and COR Actions to drive profitability

• 2003-06 rew volumes at attractive

98%5,000

CORs

• 2007-09 actions to maintain

profitability

102%

4,000• Exited unprofitable

relationships (Schemes, MGAs,

Partners)P (£m

)

COR

106%

3,000

• Focus on most profitable brokersegments (Club110 and B.I.G.)

• Disciplined underwriting and

N

2,000

2003 2004 2005 2006 2007 2008 2009

Aviva UK GI NWP Market COR (Source FSA returns) Aviva UK GI COR

sophisticated pricing (ARiimplemented, early creditor

pricing action)

24

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 25/42

UK GI today

UK GI has a strong competitive position compared to its peersUK GI has a strong competitive position compared to its peers

300

(£

m)

200

250

ting profit

100

150

IFRS op

er

0

50

HY10

(50)

Q3 YTD 2010 % COR 96

(253)

25

HY 2010 % COR 98 99 83 95 101 100 120

* HY 2010 IFRS operating profit or reported equivalent (£m)AXA operating profit and COR include UK and Ireland, RBS operating profit includes international businesses but COR is UK business only

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 26/42

UK GI today

High quality book with significantly improved current year profitabilityHigh quality book with significantly improved current year profitability

1,200

£mOperating profit • Underwriting, pricing and

claims handling delivering

800

1,000improving claims costs

• Reserving confirmed byregular independent reviews

200

400 • Distribution ratio reducedfrom 40% (2007) to 33%(2010 HY)

(200)

0

2005 2006 2007 2008 2009 HY 2010

Axis Title

Prior year Current year

• Profits relatively resilient tolow interest rate environment

96 95 106 99 99 98COR %Reported

26

Q3 YTD 2010 96

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 27/42

UK GI today

Core strengths in underwriting, pricing and claims managementCore strengths in underwriting, pricing and claims management

80%

5.7%

6.0%

26%

28%P

Reducing commercial lines claims frequency

Direct PM New Business Rating Vs Market

Hardening personal motor rates

20%

40%

5.1%

5.4%

22%

24%

oper t yM

oto

0%

AA Comp UKDI

4.8%20%2007 2008 2009 2010

Motor Property

“ ”Drivin commercial lines underwritin

2008 2009 2010

• Operational centres of excellence, poolingexpertise and best practice

• Claims intelligence team targeting organised

excellence:

• Local underwriting including “Bonusunderwriters”

fraud rings

• Strong litigation avoidance processes –

saving c£5k per claim

• rd

• Underwriting innovation (Hawkeye mapping

tool, Commercial Ari, flood data)

• Cleanse the book a continuous process

• own network

27

“poorest” performers

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 28/42

UK GI today

Personal lines – growing personal motor into a hardening marketPersonal lines – growing personal motor into a hardening market

1,600

’s)

Strong advertising Better risk selection

10% C

on Proportion of UKDI motor customers

800

uotes (000

5%

er si onR a

ARi risk group 2008 2010

1 - 3 28% 13%

0Q1 2009 Q3 2010

Qt e

4 - 7 39% 39%

8 - 10 33% 48%

Internet Conversion Rate Quotes

Improving fundamentalsUKDI Car - BI

ARi Risk Group 1 -3 4 - 7 8 - 10130

140

150

u

ency

Retention rate 68% 72% 78%

Cancellation rate 25% 11% 7%100

110

120

Indexed fre

28

Conversion rate 4% 11% 13%2005 2006 2007 2008 2009 2010

Accident Year

Aviva indexed frequency Third party working group

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 29/42

UK GI today

UK GI is growing profitablyUK GI is growing profitably

050

100 £m UK GI Net Written Premium• UKDI motor customer growth of

160,000 to Q3 2010

£1,053m

£1,029m

£1,050m

000

• ,Q3 2010 versus 150,000 for the

whole of 2009

•£996m

£937m

950

2,300 brokers

• Strong growth in commercialnew business, 2010 YTD up

£880m

£913m

850

900 £82m on 2009

• Commercial Property

persistency at the highest levels

800

s nce

• Successful re-entry intoCorporate Risks with projected

750

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010

29

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 30/42

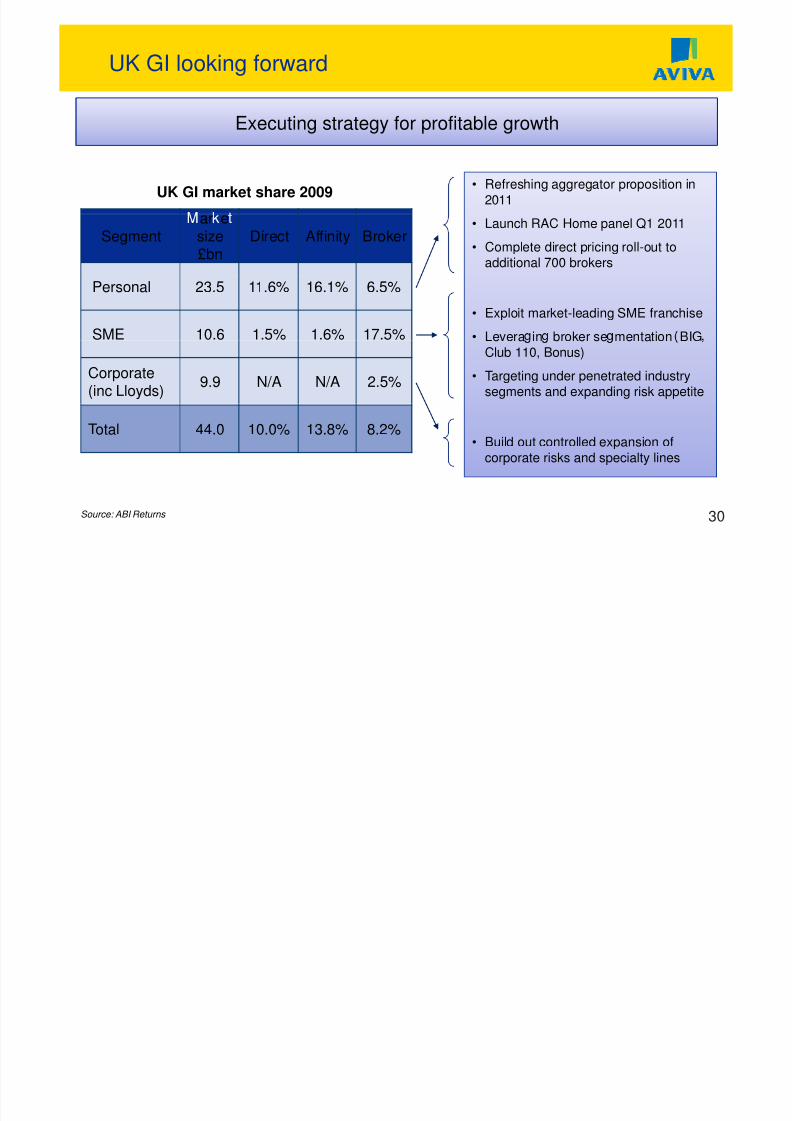

UK GI looking forward

Executing strategy for profitable growthExecuting strategy for profitable growth

UK GI market share 2009• Refreshing aggregator proposition in

2011

• Launch RAC Home panel Q1 2011

• Complete direct pricing roll-out toadditional 700 brokers

Segmentar esize£bn

Direct Affinity Broker

• Exploit market-leading SME franchise

• Levera in broker se mentation BIG

Personal 23.5 11.6% 16.1% 6.5%

SME 10.6 1.5% 1.6% 17.5%

Club 110, Bonus)

• Targeting under penetrated industry

segments and expanding risk appetite

Corporate

(inc Lloyds)

9.9 N/A N/A 2.5%

• Build out controlled expansion of

corporate risks and specialty lines

Total 44.0 10.0% 13.8% 8.2%

Source: ABI Returns 30

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 31/42

UK GI looking forward

Controlled expansion in corporate risks and specialty linesControlled expansion in corporate risks and specialty lines

Appetite extension - £6bn market

Eg:pabili

ty SME core business - £10bn market

UK Corporates

Property

Liability

C Eg:

Property

Liability

Motor and Fleet o or an ee

LocalAuthorities

D&O

Group PA

Engineering

Fidelity Guarantee

Marine

31Risk AppetiteLow

Construction

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 32/42

UK GI Summary

A strong business well positioned to win in its marketplaceA strong business well positioned to win in its marketplace

2011 UK General Insurance COR to be 97% or better

P&L benefit of £100m from cost reduction activity by 2012

Controlled expansion of risk appetite in Corporate and Specialty Lines

Scale and efficient claims management

32

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 33/42

Aviva UK

A unique opportunity for customers and shareholdersA unique opportunity for customers and shareholders

UK

Drive outadditional

33

value

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 34/42

Aviva UK

Diversification brings wide-ranging benefitsDiversification brings wide-ranging benefits

Brand• Integrated branding advantages

• GI advertising benefits the life business in the

CustomerDifferentiation

• Drive value from our shared customer base

Distribution• Ability to adapt to changing customer demands

• Leadershi in bancassurance

Cost &

Scale &efficiency • Exploit opportunities to combine common

Structural • Making best use of our capital and benefiting

,

advantage from the advantages of our diversified business

34

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 35/42

Aviva UK today

Outstanding brand awareness since launchOutstanding brand awareness since launch

63%

60%

70%

50%

rec ne

57%

39%

33%

40%

32% Scottish Widows

29%

20%20% 18% Legal & General

26% More Than

4%

11%

10%10%

an ar e

14% Esure

35YouGov Brand Index data – a Nationally representative daily sample of over 2000 people

0%

Dec '08 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 36/42

Aviva UK today

Common customer base brings significant opportunityCommon customer base brings significant opportunity

Household income• Similar customer profiles mean

insights can be exploited across

• Concentration on mid-marketcustomers brings both loyalty and

Pre-retired

stage

a grea er va ue

• 1.27 policy holding per customer

•Family

Non-family

Lif

products

• Broad product range covers all

36

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 37/42

Aviva UK today

No 1 bancassurance provider - the partner of choiceNo 1 bancassurance provider - the partner of choice

LIFE GI

Personal Commercial

• Proven ability to improve partnersales penetration - Santander

• Single relationship managerlines lines

Lloyds

building deep relationshipsacross all products – and co-

ordinated globally

Santander

opportunities

• Creation of unified IT platform

giving partners:

RBS

• Lower training and

integration costs

• Re-use data across Life /

CIS

GI products

• Higher cross-sales

• Bancassurance IRR of 15%

37

and COR of 96% YTD 2010

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 38/42

Aviva UK today

Scale benefits from UK modelScale benefits from UK model

• Over £700m reduction in

underlying cost baseUK ex ense base

£2.4bn2.5

3.0

)

• Significant shared servicesbenefits over the last 10 years– a third of cost base is

£1.7bn

1.5

2.0

enses (£b

• c. £275 million to NAV and atleast £50 million cost savings

0.5

1.0

rating exp pa rom e c osure o e

final salary pension schemes

• P&L benefit of £200m by end

0.0

2005 2010 Est.

Ope 2012 re ect ng cost re uct on

and growth absorption

38

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 39/42

Aviva UK today

Strong and disciplined focus on generation and allocation of capitalStrong and disciplined focus on generation and allocation of capitalStrong and disciplined focus on generation and allocation of capital

• UK region significant contributor to

Group economic capitaldiversification benefit

• Sustainable ongoing net capitalgeneration of £800m+ (excludingone offs) through:

• Reduction in UK Life newbusiness strain

£535m

• Benefits of reattribution

• Rigorous management of costs• Growing IFRS operating profits

2009 2010 Est.

39

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 40/42

Aviva UK

A unique opportunity for customers and shareholdersA unique opportunity for customers and shareholders

• Increase earnings from new and in-force business

• Capitalise on our multi-channel, multi-product strategy• Win in an RDR world through strong brand and

service

• Underwriting and risk management capability

• Drive profitable growth

• Excellence in underwriting, claims management andcustomer service

• Expand profitably into business lines and segmentswhere underweight

UK

Drive outadditional

• Leverage brand to drive earnings from 19m

customers

• Extend and deepen new bancassurance relationships

40

value

• Generate further cost and efficiency savings

• Exploit capital diversification benefit

A i UK fi i l

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 41/42

Aviva UK financial summary

A growing business exploiting its unique positionA growing business exploiting its unique position

+

Life product IRR of at least 12%, with payback of 10 years or less

2011 UK General Insurance COR to be 97% or better

P&L benefit of £200m from cost reduction activity by 2012

Increasing IFRS operating profit and ROCE

41

8/7/2019 Aviva UK: Winning In The UK November 2010

http://slidepdf.com/reader/full/aviva-uk-winning-in-the-uk-november-2010 42/42