Automotive LNG Technology

18

Automotive LNG Technology Industrial Minerals - Frac Sands Conference September 24th, 2013

Transcript of Automotive LNG Technology

Automotive LNG Technology Industrial Minerals - Frac Sands Conference September 24th, 2013

2

© 2013 PLS Logistics Services

PLS Logistics Services

PLS is the leader in industrial

logistics management services – Outsourced logistics management

– Freight Brokerage

– $600mm Freight under management

– 1,000,000+ loads annually

Network Operations Centers: – Pittsburgh, Jacksonville, Houston

Energy Services Division – Energy.plslogistics.com

Network of 22,000 Carriers

PLS Shipment Network, 12 months ending June 2013

3

© 2013 PLS Logistics Services

Motor Carrier Transportation Market Trends

4

© 2013 PLS Logistics Services

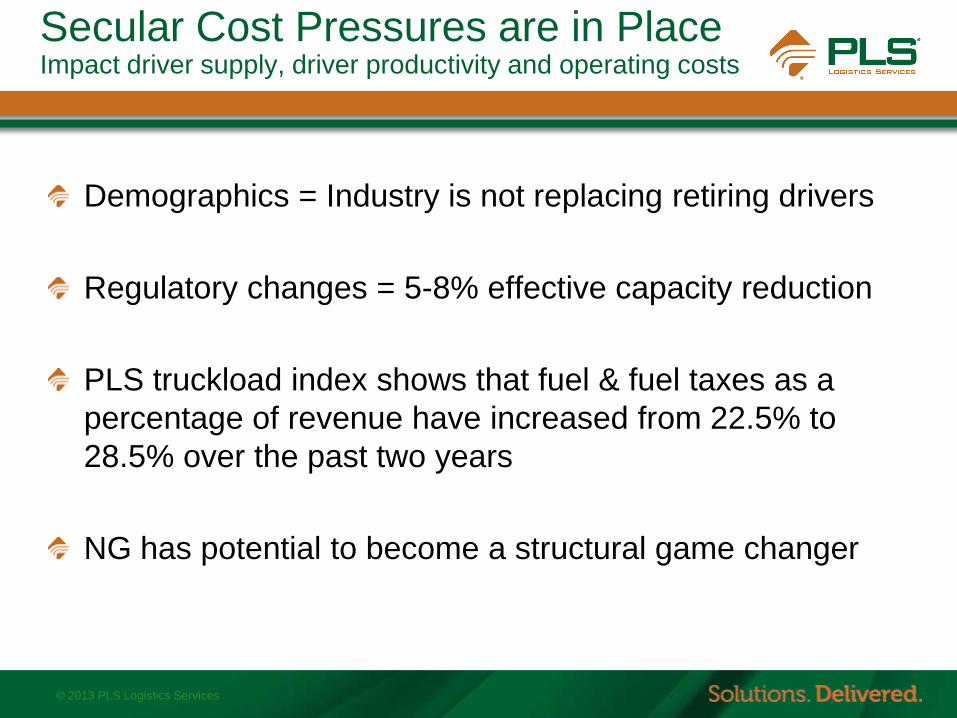

Secular Cost Pressures are in Place Impact driver supply, driver productivity and operating costs

Demographics = Industry is not replacing retiring drivers

Regulatory changes = 5-8% effective capacity reduction

PLS truckload index shows that fuel & fuel taxes as a

percentage of revenue have increased from 22.5% to

28.5% over the past two years

NG has potential to become a structural game changer

5

© 2013 PLS Logistics Services

Driver Shortage Major Constraint to Fleet Expansion

Source: Global Insight

6

© 2013 PLS Logistics Services

Diesel Fuel is a key cost

Range of fuel surcharge

7

© 2013 PLS Logistics Services

Average Rate Trends

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

JAN

20

10

FEB

MA

R

AP

R

MA

Y

JUN

JUL

AU

G

SEP

OC

T

NO

V

DEC

JAN

20

11

FEB

MA

R

AP

R

MA

Y

JUN

JUL

AU

G

SEP

OC

T

NO

V

DEC

JAN

20

12

FEB

MA

R

AP

R

MA

Y

JUN

JUL

AU

G

SEP

OC

T

NO

V

DEC

JAN

20

13

FEB

MA

R

AP

R

MA

Y

JUN

National Average Truckload Van & Flatbed Linehaul Rates Transcore's Truckload Rate Index

Van Contract Flatbed Contract

8

© 2013 PLS Logistics Services

Natural Gas Vehicles Adoption & Challenges in Over The Road Trucking

Technology

– NG Engines add $30,000- $80,000 to tractor costs

– LNG has driving range needed for over-the-road trucking

LNG Infrastructure

– Currently limited in the U.S.

• As of August, 75 LNG Stations (Source: DOE)

– America’s Natural Gas Highway

• CleanEnergy commitment to build a 150-station network by the end

of 2013

Trade-offs

– Additional Weight

– Lower power

– Increased maintenance

9

© 2013 PLS Logistics Services

PLS Carrier Survey: Natural Gas Vehicles 1Q 2013

10

© 2013 PLS Logistics Services

PLS Carrier Base Survey Titles/Roles of Survey Respondents

Source: PLS Logistics 2013 LNG Survey

11

© 2013 PLS Logistics Services

PLS Carrier Base Survey Fleet Sizes

Source: PLS Logistics 2013 LNG Survey

12

© 2013 PLS Logistics Services

PLS Carrier Base Survey Carrier View of LNG Impact in Over the Road Trucking

Source: PLS Logistics 2013 LNG Survey

13

© 2013 PLS Logistics Services

PLS Carrier Base Survey Carrier View of LNG Impact in Over the Road Trucking

Source: PLS Logistics 2013 LNG Survey

14

© 2013 PLS Logistics Services

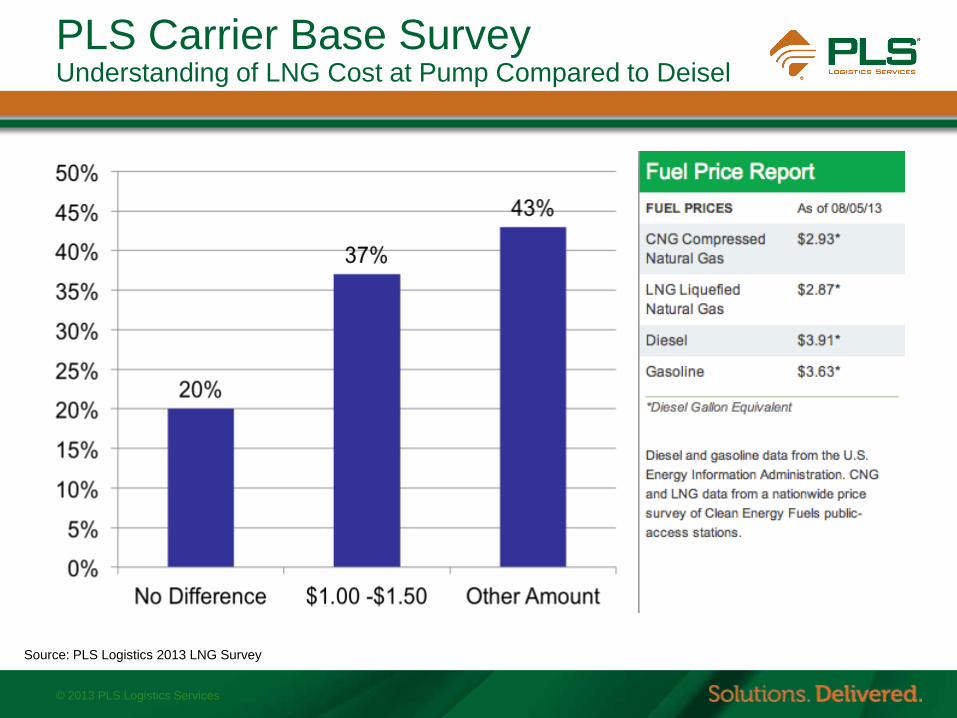

PLS Carrier Base Survey Understanding of LNG Cost at Pump Compared to Deisel

Source: PLS Logistics 2013 LNG Survey

15

© 2013 PLS Logistics Services

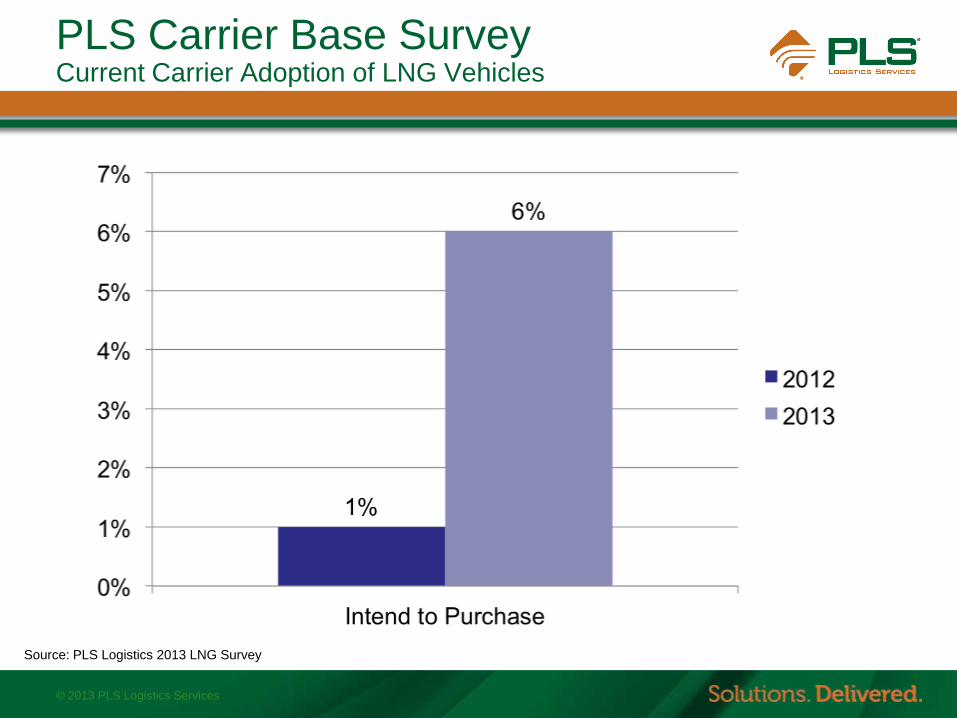

PLS Carrier Base Survey Current Carrier Adoption of LNG Vehicles

Source: PLS Logistics 2013 LNG Survey

16

© 2013 PLS Logistics Services

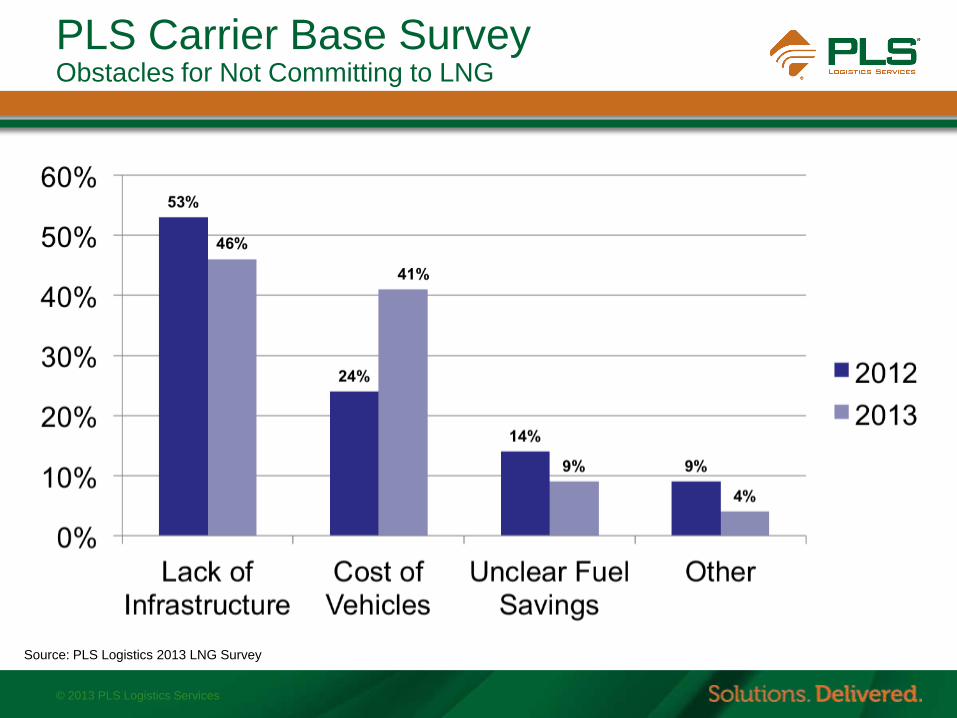

PLS Carrier Base Survey Obstacles for Not Committing to LNG

Source: PLS Logistics 2013 LNG Survey

17

© 2013 PLS Logistics Services

PLS Carrier Base Survey How Carriers View Shipper Perspective

Source: PLS Logistics 2013 LNG Survey

18

© 2013 PLS Logistics Services

Q&A

Visit us on the web at: energy.plslogistics.com

Michael Ceravolo

Director of Energy Services