Automotive Industry v1

40

Automobile Industry: TFAE RAKSHIT JHUNJHUNWALA 111 OMKAR MALAGE 114 ANKITESH MATHUR 115 HARSH MEHTA 117 NIKESH SOLANKI 123 CHINTAN SHAH 126

-

Upload

harsh-mehta -

Category

Documents

-

view

227 -

download

0

Transcript of Automotive Industry v1

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 1/43

Automobile

Industry: TFAE

RAKSHIT JHUNJHUNWALA 111 OMKAR MALAGE 114

ANKITESH MATHUR 115 HARSH MEHTA 117

NIKESH SOLANKI 123 CHINTAN SHAH 126

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 2/43

CONTENT

INDUSTRY OVERVIEW

HYBRID CAR TECHNOLOGY

BOTTLENECKS HAZARDS & RISKS

POTENTIALS & BARRIERS

COMPETITORS

COST OF IMPLEMENTATION

VERTICAL INTEGRATION & VENDOR MANAGEMENT

FUTURE SPACE

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 3/43

Automobiles: Review

Disparate Technologies

Long Age of Evolution

Showcases advances in Science & Engineering – „Men‟s Best MadeMachine‟

Seminal Development > Bessemer Steel Process, Internal Combustion

Engine, Machine Tooling, Petroleum Refining

Modern Automobiles are result of clustering of hundreds of suchtechnologies

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 4/43

Technologies involved..

Fuel &Transmissio

nElectronics

Energy &Material

Resources

Aerodynamics &

StructuralDesign

Mechanics &

Electrics

Computing &

Processing

Rather itswise to ask what‟s notinvolved..

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 5/43

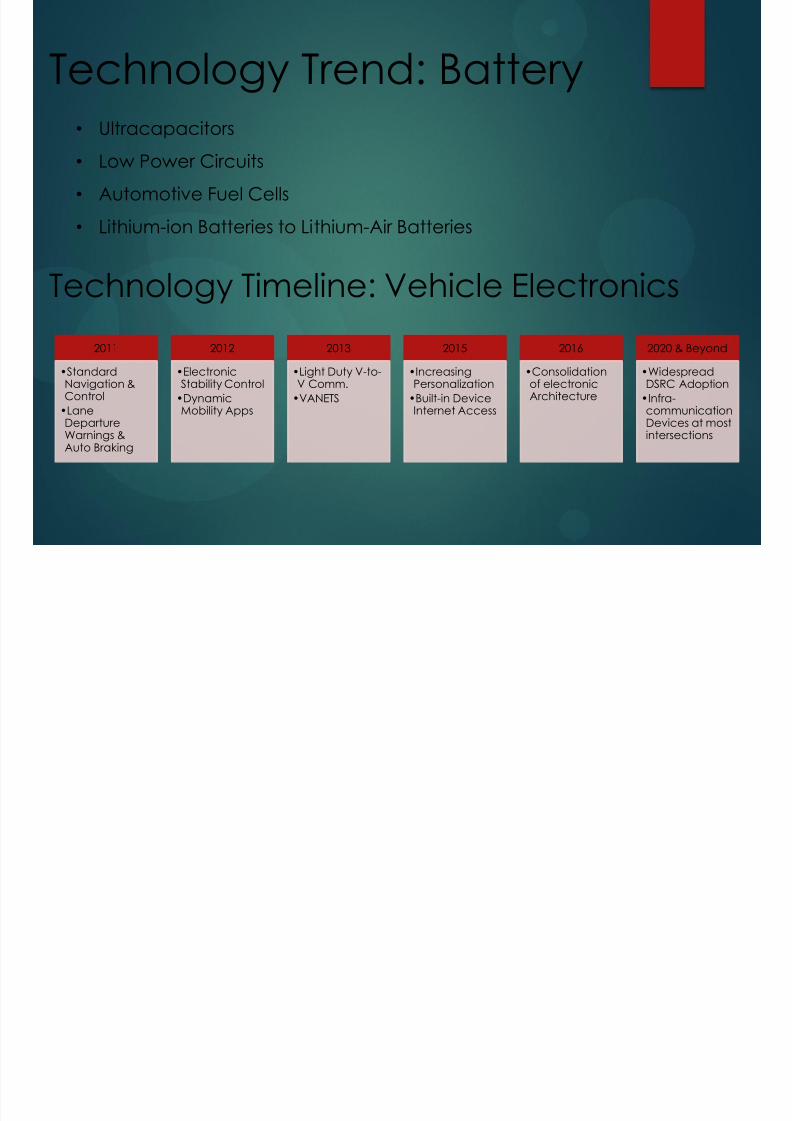

Technology Trend: Battery

Technology Timeline: Vehicle Electronics

• Ultracapacitors

• Low Power Circuits

• Automotive Fuel Cells

• Lithium-ion Batteries to Lithium-Air Batteries

2011

•Standard

Navigation &Control

•LaneDepartureWarnings &Auto Braking

2012

•Electronic

Stability Control•DynamicMobility Apps

2013

•Light Duty V-to-

V Comm.•VANETS

2015

•Increasing

Personalization•Built-in DeviceInternet Access

2016

•Consolidation

of electronicArchitecture

2020 & Beyond

•Widespread

DSRC Adoption•Infra-communicationDevices at mostintersections

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 6/43

Hybrid CarsCASE FOR DISCUSSION

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 7/43

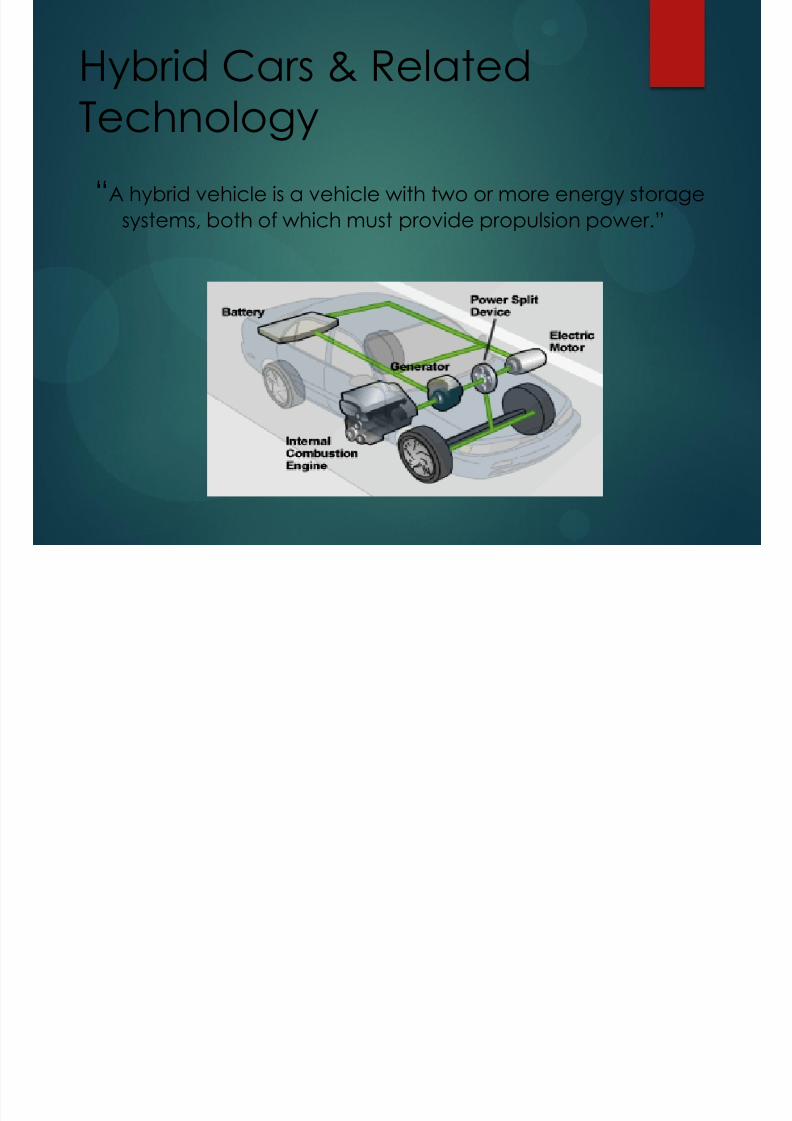

Hybrid Cars & Related

Technology“A hybrid vehicle is a vehicle with two or more energy storage

systems, both of which must provide propulsion power.”

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 8/43

IdleStop/Start

RegenerativeBraking

Electric-only

mode(Engine off)

Power boost

Self-chargingbattery

Low Emissions

Low FuelConsumption

Features

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 9/43

What Does the Market (People)Want?

A significant and growing percentage of customersindicate a willingness to buy an environmentally

friendly vehicle

If, and only if, all other attributes are EQUAL

or Better

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 10/43

Significant fuel economy improvement.

Major reduction in exhaust emissions.

No new infrastructure needs (e.g. fuelling stations).

No perceived difference by customer in vehicle performance,handling, etc.

A competitive price to encourage adoption.

Hybrid Technology Design

Objectives

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 11/43

PROCESS & TECHNOLOGY

Vehicle equipped with either an internal combustion engine(ICE) and an electrical motor powered by electrical batteries.

Today‟s HEVs are an emerging technology in the automotivemarket, with manufacturers designing and producing hybridsystems for passenger cars, light-duty vehicles, heavy dutyvehicles, and even locomotives.

The improved efficiency of HEVs over conventional (i.e. non-hybrid) vehicle is achieved by operating a smaller (moreefficient) ICE within a narrower, more efficient operationalspeed/power band and using an electric engine and electricalstorage (i.e. the battery) to balance the performance energy

requirements.

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 12/43

PROCESS & TECHNOLOGY

In general, in the current-generation HEVs, the combustionengine provides the main power during long-distance drive whilethe electrical motor can either complement the ICE or power thevehicle in electric- only mode (as long as energy is available fromthe battery) during the urban service, where the ICE is lessefficient.

The battery charge is provided by regenerative braking andexcess energy from the ICE (stored when the vehicle has lower power requirements).

Improving battery capacity and technology may enable longer electric drive range and reduce the need for the ICEcontribution. New- generation HEVs include batteriesrechargeable from the grid.

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 13/43

Cost Benefit View

The hybrid vehicles can benefit from the best features of bothconventional ICE vehicles and electric vehicles.

Hybrids offer drive range and rapid refueling the same asconventional vehicles, and provide high efficiency at low loads,potentially better acceleration, environmental benefits and 25-40% CO2 emissions saving as compared to conventional vehicles.

The HEVs cost however is higher. This is largely due to the highprice of the battery.

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 14/43

Advantages

Significant fuel economy improvement

Low carbon / alternative fuels

Major reduction in exhaust emissions

No new infrastructure needs (e.g. fuelling stations)

No perceived difference by customer in vehicle performance,handling, etc.

Socio-economic & Environmental Benefits

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 15/43

Disadvantages

Heavier

Threat to first responders

High Maintenance &Repair Cost

Underpowered & lowtorque

Harmful extent ofelectromagnetic fields

to human health

Hybrid Technology is costly.

Acceleration is not exhilarating.

High battery cost (to bereplaced after completing80000 miles, cost : $5000-8000)

Light weight body materialsmake it more vulnerable toserious damage.

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 16/43

BOTTLENECKS

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 17/43

BOTTLENECKS

Battery : Availability & Cost of batteries as thebiggest bottleneck to production.

Production pollution Panasonic EV Energy, the company that supplies

nickel metal hydride batteries to Toyota for theeg : Prius - 500,000 packs per year

Poor consumer understanding The public have concerns about the maturity of the

technology, and the availability and adequacy ofafter-sales service. This is mostly attributed to poor understanding of the technology status

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 18/43

HAZARDS & RISKS

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 19/43

Hazards and Risks

High VoltageStandard cars circulate 12 volts of electric power from thebattery through the alternator. Hybrid cars circulates 276 voltsin total, most of which powers the electric motor. Potential ofaccidents are high.

Electromagnetic fields

A driver's proximity to that field could pose a long-termhealth risk.

BatteriesA hybrid's batteries contin potent chemicals designed tostore and produce electricity.

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 20/43

Hazards and risks

SilenceThe lack of sound gives blind or distractedpeople less warning for an approaching car.

Complex softwareHybrid vehicles depend on complex enginemanagement systems that automaticallyswitch between the car's electric andgasoline engines. The complexity of thesoftware constitutes one risk posed by hybrids.

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 21/43

POTENTIALS & BARRIERS

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 22/43

POTENTIAL & BARRIERS

Major drivers for performance and costs

Inherent benefits of the vehicles, such as lower fuel consumption,

emissions and noise, are making them more attractive toconsumers.

Equally, producers and manufacturers are incentivised by a greenimage that can enhance their brand against competitors.

A high uptake of HEVs may lead to important benefits such asreduced emissions and use of fossil fuels in road transport,decarbonisation of the transport sector, and the consequentreduced dependence on foreign.

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 23/43

POTENTIAL & BARRIERS

Role of legislation

Various countries such as the US, Spain and Japan have setambitious targets for the future deployment of hybrids.

These targets form a major component of national andinternational policies for tackling climate change.

In particular, Europe is subject to an array of regulations that restrictthe emissions of the automotive sector.

Technological developments, further refinement and advancedmaterials will deliver improved performance through greater efficiency and hence lower CO2 emissions.

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 24/43

POTENTIAL & BARRIERS

Market Potential and Prospects

By the end of 2009, the world-wide sales of hybrid vehicles had reached

around 2.7 million (some 1% of global sales), with 1.6 million in the US, 870thousand in Japan and 237 thousand in Europe.

The vast majority of these sales were by Toyota/Lexus (around 2 million)

A recent study conducted by JPMorgan predicts that by 2020 some 11.3million hybrids will be sold annually (over 13% of all vehicles sold).

The future deployment and commercialisation of hybrid vehiclesessentially depends upon substantial improvements and reduced pricesin battery technology, but also in electric motors and power electronics

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 25/43

POTENTIAL & BARRIERS

Barriers to Development and Deployment

The high price of HEVs is certainly an inhibiting factor for their

widespread adoption.

A reduction in the costs of battery technology is essential for the HEVs tofurther penetrate into the market.

However other factors also play a large role in the future deployment ofHEVs:

External markets

Poor consumer understanding

Environmental impacts

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 26/43

Competitors

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 27/43

Sorcehttp://www.fueleconomy.gov/feg/Find.do?action=sbs&id=32484&id=33010&id=33083&id=32053

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 28/43

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 29/43

COST OFIMPLEMENTATION

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 30/43

Cost of Implementation

• Current commercial Hybrid Vehicles must compete against the mature

technologies of conventional vehicles

•

Tough Competition with Diesel based traditional and conventional cars.

• Nickel-Metal Hybrid batteries still account for roughly half of the extra

cost of a hybrid vehicle, despite their cost have been almost halving

over the last 10 years.

• The battery cost is expected to level during the next 5 years, as the

production benefits from economies of scale and large volumes

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 31/43

Cost of Implementation

• But leveling process may be offset by the rising cost of nickel.

• The new Li-ion batteries use cheaper raw materials and offer the

same economies of scale as production volumes increase.

• The two battery technologies are expected to be the same price by

2014; however Li-ion has the advantage of low temperature

performance, with better energy and power density

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 32/43

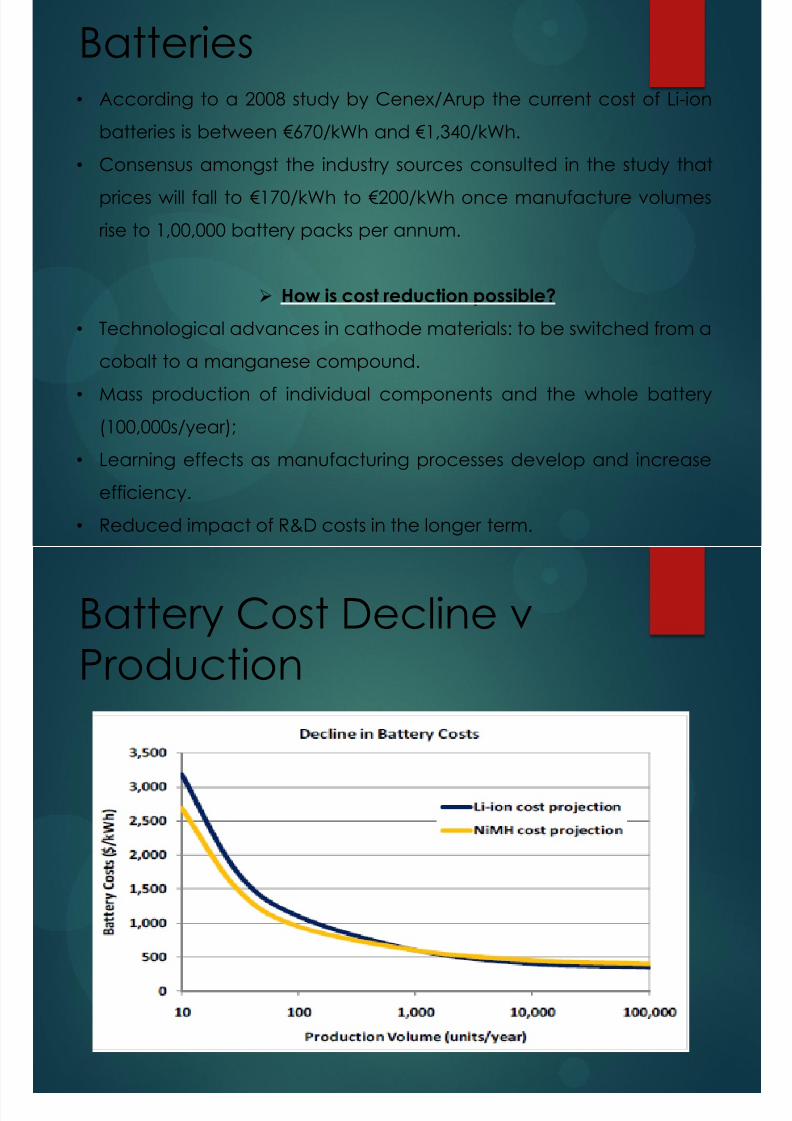

Batteries• According to a 2008 study by Cenex/Arup the current cost of Li-ion

batteries is between €670/kWh and €1,340/kWh.

• Consensus amongst the industry sources consulted in the study that

prices will fall to €170/kWh to €200/kWh once manufacture volumes

rise to 1,00,000 battery packs per annum.

How is cost reduction possible?

• Technological advances in cathode materials: to be switched from a

cobalt to a manganese compound.

• Mass production of individual components and the whole battery

(100,000s/year);

• Learning effects as manufacturing processes develop and increase

efficiency.

• Reduced impact of R&D costs in the longer term.

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 33/43

Battery Cost Decline v

Production

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 34/43

VERTICAL INTEGRATION &VENDOR MANAGEMENT

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 35/43

Vertical Integration -

Toyota

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 36/43

Solar Based Plug-in

Stations

• Toyota wanted to vertically integrate by launching Solar based Plug-

in Stations at 21 cities in Japan.• This integration helps Toyota for new range of vehicles in Hybrid

sector post Prius.

• Will understand Consumer Behavior towards Hybrid cars.

•

Can explore new age technological horizons with help of Batteryoperated cars.

TECHNOLOGY

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 37/43

TECHNOLOGY – OUTSOURCED Or NOT?• Hybrid technology is generally not sourced and is built in house.

• Car manufacturers like Toyota and Ford build their hybridtechnologies in house and compete against each other.

VENDOR MANAGEMENT

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 38/43

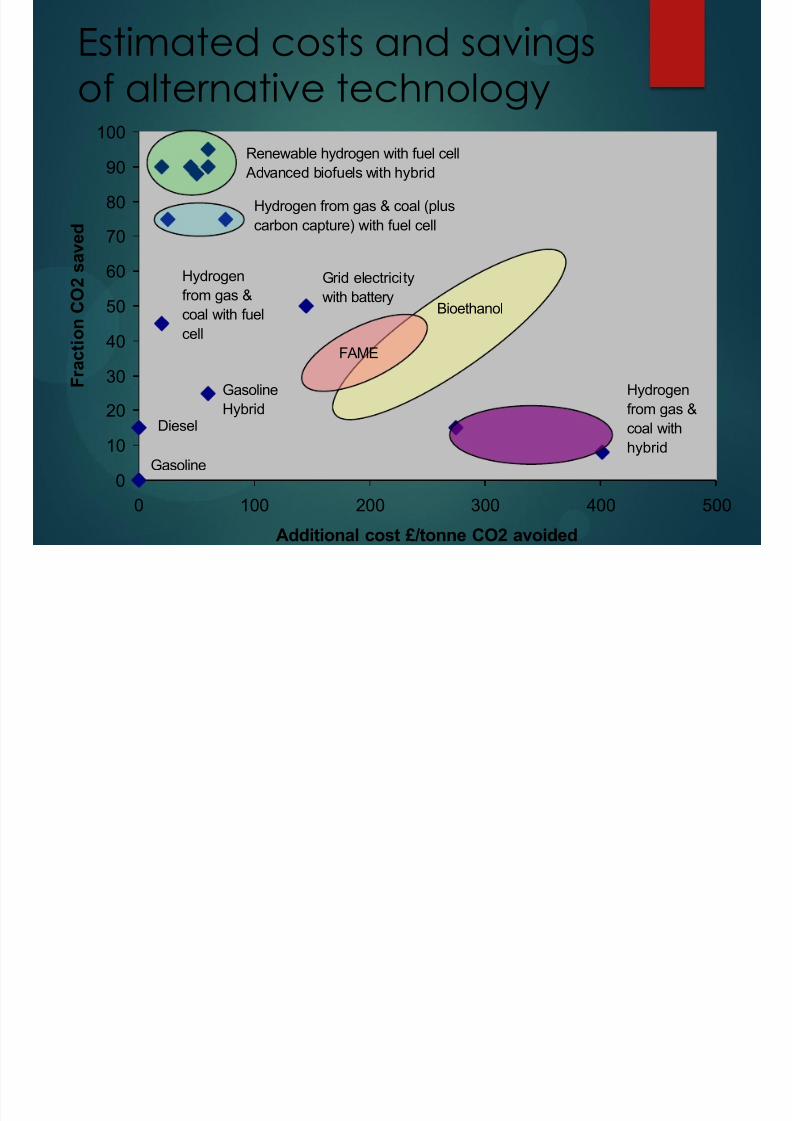

0

10

20

30

40

50

60

70

80

90

100

0 100 200 300 400 500

Additional cost £/tonne CO2 avoided

F r a c t i o n C O 2 s a

v e d

Renewable hydrogen with fuel cell

Advanced biofuels with hybrid

Hydrogen from gas & coal (plus

carbon capture) with fuel cell

Grid electricity

with battery

FAME

Bioethanol

GasolineHybrid

Hydrogenfrom gas &

coal with

hybrid

Diesel

Gasoline

Hydrogen

from gas &

coal with fuel

cell

Estimated costs and savingsof alternative technology

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 39/43

“If you don’t make the system now, as Toyota continues to make

hybrids much cheaper and in greater numbers, the others won’t be able

to catch up.”

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 40/43

Future evolution of Hybrid Technology

Prius: gasoline FINE-S: hydrogen

Engine Fuel Cell

Secondarybattery

Motor

Powercontrol unit

Powercontrol unit

Secondarybattery

Motor

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 41/43

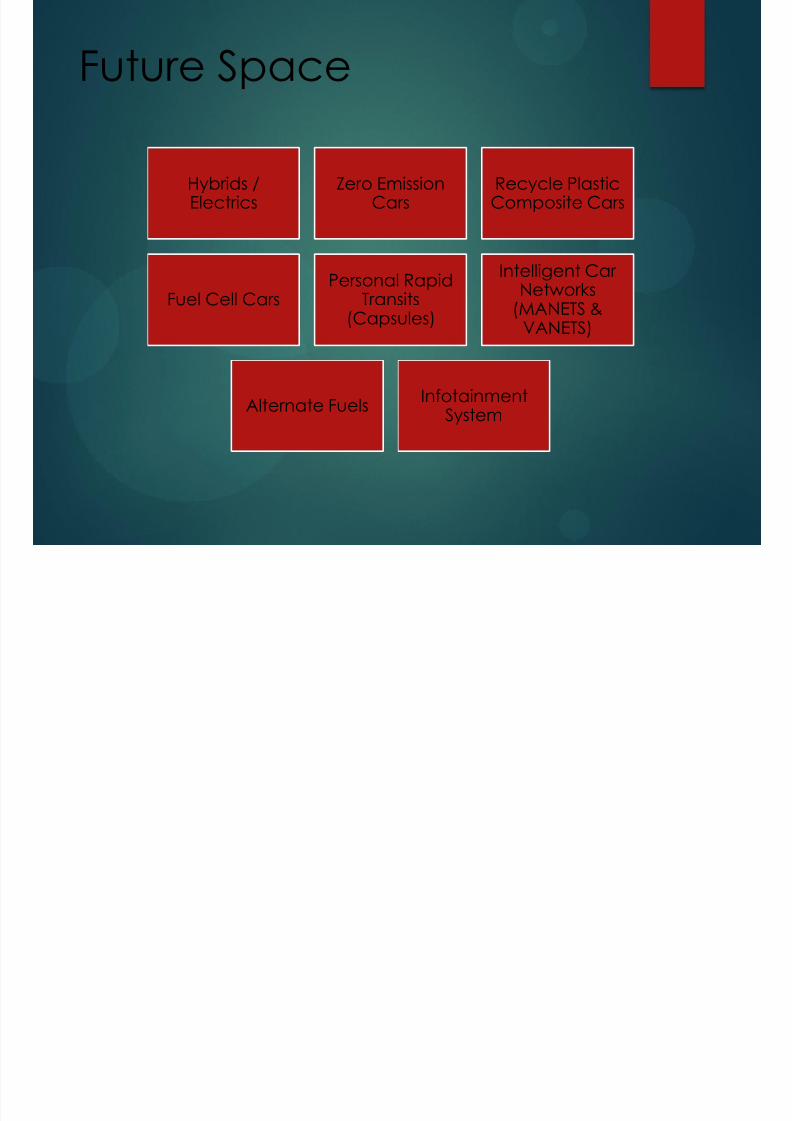

Future Space

Hybrids /Electrics

Zero EmissionCars

Recycle PlasticComposite Cars

Fuel Cell CarsPersonal Rapid

Transits(Capsules)

Intelligent Car Networks

(MANETS &VANETS)

Alternate FuelsInfotainment

System

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 42/43

Technology offers the potential to significantly reducegreenhouse gas emissions from road transport – butresponsible vehicle use will also be an important contributor

The range of fuel and vehicle technology options are wide–

most vehicle manufacturers believe hybrid technology is animportant step in the evolution of technology to zero emissionvehicles

Low carbon technologies come at a financial premium and

current incentives are inadequate to change the attitudes andpurchasing behaviours of most consumers

The transition to a low carbon future needs a partnershipapproach the LowCVP is delivering.

Summary

7/29/2019 Automotive Industry v1

http://slidepdf.com/reader/full/automotive-industry-v1 43/43

THANK YOU!!!!!