Automotive Industry On Fast Track. Indian Automotive Industry India - An Overview Market and...

33

Automotive Industry On Fast Track

-

Upload

jonathan-watkins -

Category

Documents

-

view

231 -

download

3

Transcript of Automotive Industry On Fast Track. Indian Automotive Industry India - An Overview Market and...

Automotive Industry

On Fast Track

Indian Automotive Industry

India - An Overview

Market and Growth Potential

Players

Opportunities

Why India?

Contact in India

India - An Introduction

Population

States/UTs

Geographical Area

Languages recognised

Business language

Per Capita Income**

GDP**

Over 1 bn

35

3.3 mn sq kms

22

English

US$ 534

US$ 650 bn**(at factor cost & at current prices)

1USD=43.54 INR (as on July 4, 2005)Source:CSO Statistics

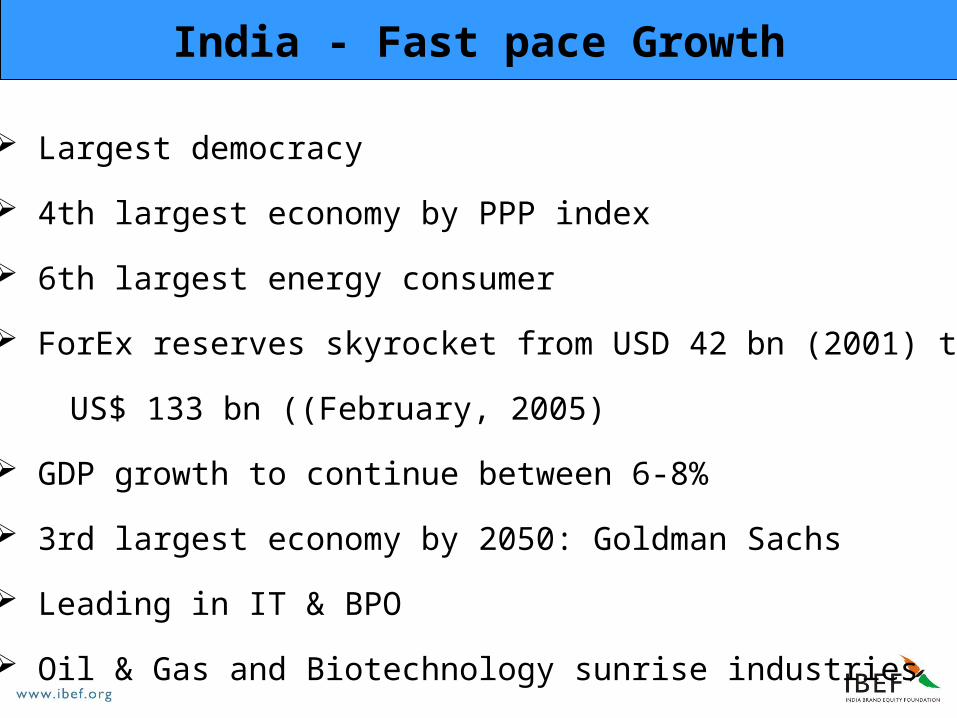

India - Fast pace Growth

Largest democracy

4th largest economy by PPP index

6th largest energy consumer

ForEx reserves skyrocket from USD 42 bn (2001) to

US$ 133 bn ((February, 2005)

GDP growth to continue between 6-8%

3rd largest economy by 2050: Goldman Sachs

Leading in IT & BPO

Oil & Gas and Biotechnology sunrise industries

India - Leading the world

Hero Honda - largest manufacturer of motorcycles

Moser Baer - among the top three media manufacturers

in the world

Pharmaceutical Industry - 4th largest in the world

Walmart, GAP, Hilfiger sources more than

USD 1bn worth apparel from India

100 Fortune 500 have set R&D facilities in India

including GE, Delphi, Eli Lilly, HP, Heinz and Daimler

Chrysler

Indian Automotive Industry

India - An Overview

Market and Growth Potential

Players

Opportunities

Why India?

Contact in India

Passenger Car Market

Projected CAGR 12.3%

Compact55%

Mid-size17% Mini

26%

Premium & Luxury

2%Executive

0%

Compact56%

Mid-size20%

Mini19%

Premium & Luxury

3%Executive

2%

2002-03 (A)

Total Units - 547,083

2007-08 (P)

Total Units - 975,703

Two Wheeler Market

Present estimated size 5.4 mn units per year CAGR (last 5 years) 10%

Average two-wheelers per 1000 people

India 27China 08

Auto Component Market

Estimated market size US$ 6.7 bn

Estimated market size (2012) US$ 17 bn

Projected CAGR 15%

16 Cos

237 Cos1 ~ 5 Mill US $

5 ~ 50 Mill US $

50 ~ 500 Mill US

$

149 Cos

Auto Component Industry Structure

Indian Automotive Industry

India - An Overview

Market and Growth Potential

Players

Opportunities

Why India?

Contact in India

Home to global players

Product PlayersCars/SUVs Suzuki, Honda, Toyota,

Mitsubishi, GM, Ford, Daimler-Chrysler, Skoda, Fiat, Hyundai, Tata, M&M

Two-wheelers TVS, Hero Honda, Bajaj, Yamaha, Kinetic, LML

CVs Tata, Ashok Leyland, Tatra, Eicher- Mitsubishi, Swaraj-Mazda, M&M, Volvo

Tractors Escorts, M&M, L&T, Punjab Tractors, New Holland, ITL-

Renault, John-Deere, Steyr

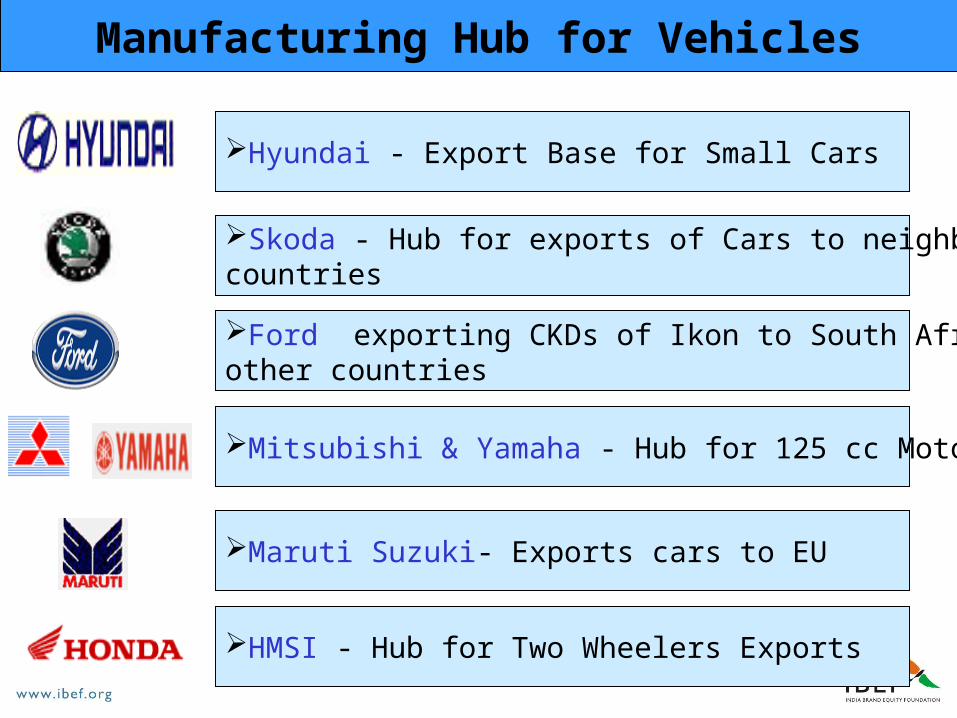

Manufacturing Hub for Vehicles

Hyundai - Export Base for Small Cars

Mitsubishi & Yamaha - Hub for 125 cc Motorcycles

HMSI - Hub for Two Wheelers Exports

Ford exporting CKDs of Ikon to South Africa &other countries

Maruti Suzuki- Exports cars to EU

Skoda - Hub for exports of Cars to neighbouring countries

Hyundai Motors India

Second largest player in passenger car market

Market Share 20%

Santro & Accent - Run away success stories

Made India its global sourcing base for small cars

Turnover (approx.) US$ 1 billion

Indian Automotive Industry

India - An Overview

Market and Growth Potential

Players

Opportunities

Why India?

Contact in India

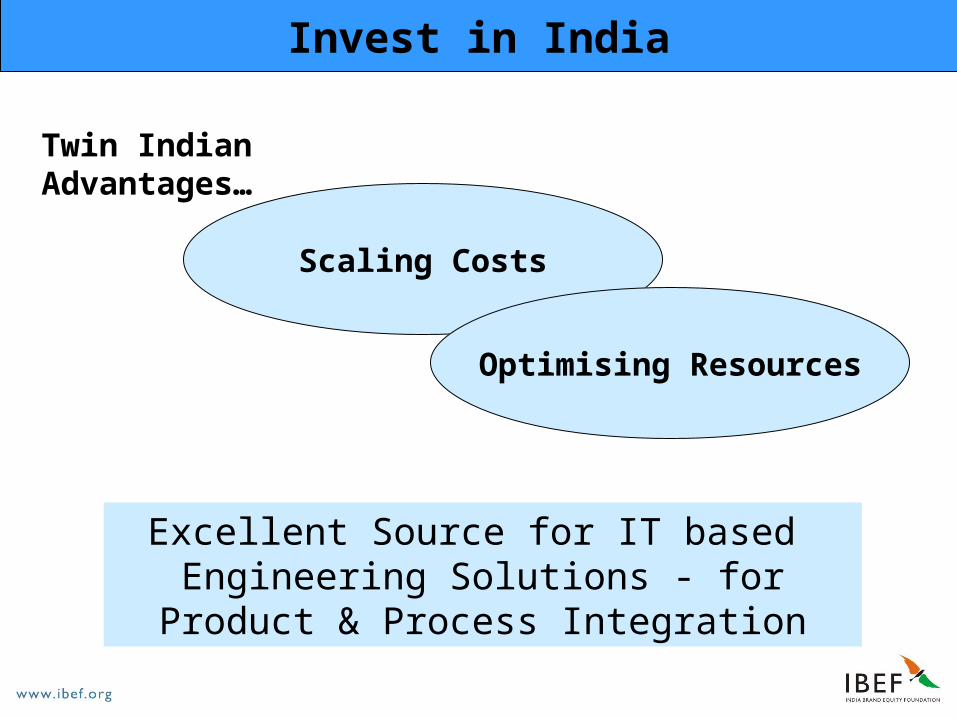

Invest in India

Excellent Source for IT based Engineering Solutions - for Product &

Process Integration

Scaling Costs

Optimising Resources

Twin Indian Advantages…

India - Manufacturing Hub for Components

Fiat sourcing components

Ford full fledged component sourcing team

Toyota Motors Global Hub for Transmissions

Daimler Chrysler sourcing > 70 million Euro

Export from India

0

5000

10000

15000

20000

25000

30000

35000

40000

HyundaiSantro

FordIkon

TataIndica

HyndaiAccent

Maruti800

(Suzuki)

No

. of

Un

its

FY 2003

FY 2004

Passenger Cars

Europe28%

Asia27%

America28%Australia

2%

Africa11%

Others4%

Export from India

Auto Components expand markets abroad

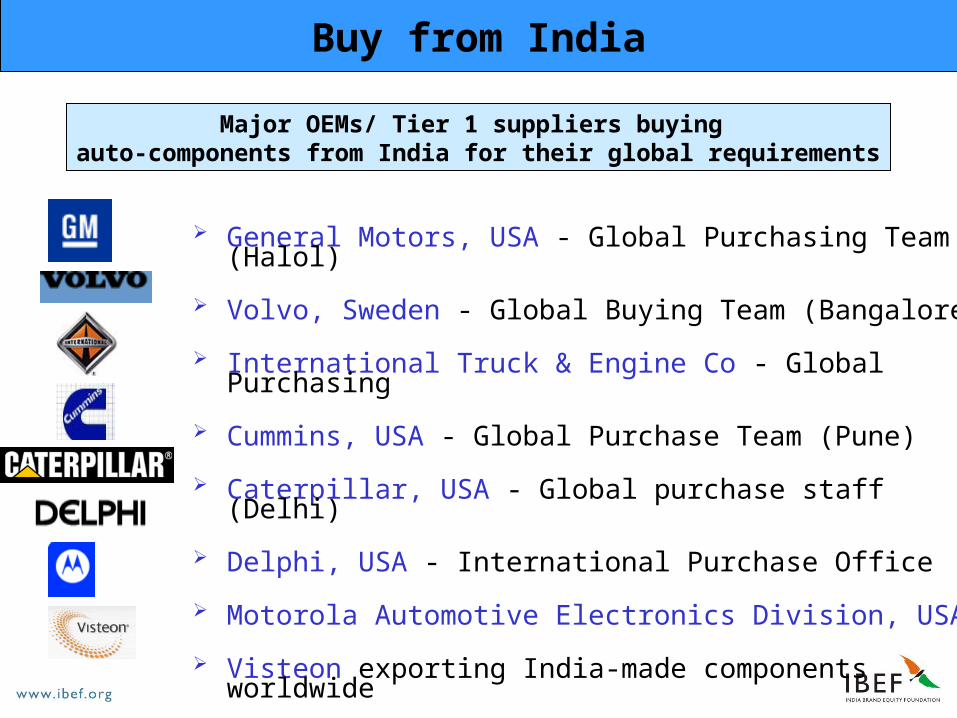

Buy from India

General Motors, USA - Global Purchasing Team (Halol)

Volvo, Sweden - Global Buying Team (Bangalore )

International Truck & Engine Co - Global Purchasing

Cummins, USA - Global Purchase Team (Pune)

Caterpillar, USA - Global purchase staff (Delhi)

Delphi, USA - International Purchase Office

Motorola Automotive Electronics Division, USA

Visteon exporting India-made components worldwide

Major OEMs/ Tier 1 suppliers buying auto-components from India for their global requirements

Sell to India

Low car penetration ratio 5 per thousand persons

This ratio projected to double by 2007-08

Large latent demand as…

Partner with India

OEMs leverage local manufacturers for

Contract Manufacturing

Mitsubishi and Ford tie-up with Hindustan Motors Kawasaki ties-up with Bajaj

Indian Automotive Industry

India - An Overview

Market and Growth Potential

Players

Opportunities

Why India?

Contact in India

Advantage India

5th Largest Commercial Vehicle Manufacturer in the World

4th Largest Car Market in Asia - crossed the 1 million mark

# 1 Global Motorcycle Manufacturer is in India

Largest Two-Wheeler Manufacturer in the World

2nd Largest Tractor Manufacturer in the World

Industry Milestones 2003-04

Car production crosses 1 million mark

Car exports cross US$ 1 million mark

Auto component exports cross US$ 1 bn mark

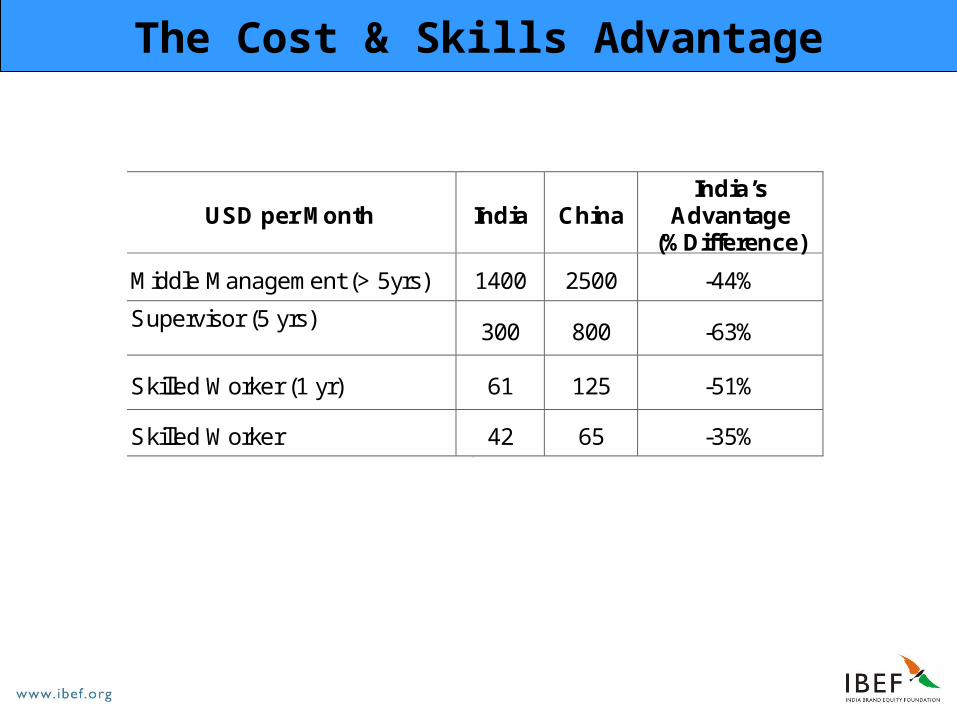

The Cost & Skills Advantage

USD per Month India ChinaIndia’s

Advantage(%Difference)

Middle Management (> 5yrs) 1400 2500 -44%

Supervisor (5 yrs)300 800 -63%

Skilled Worker (1 yr) 61 125 -51%

Skilled Worker 42 65 -35%42

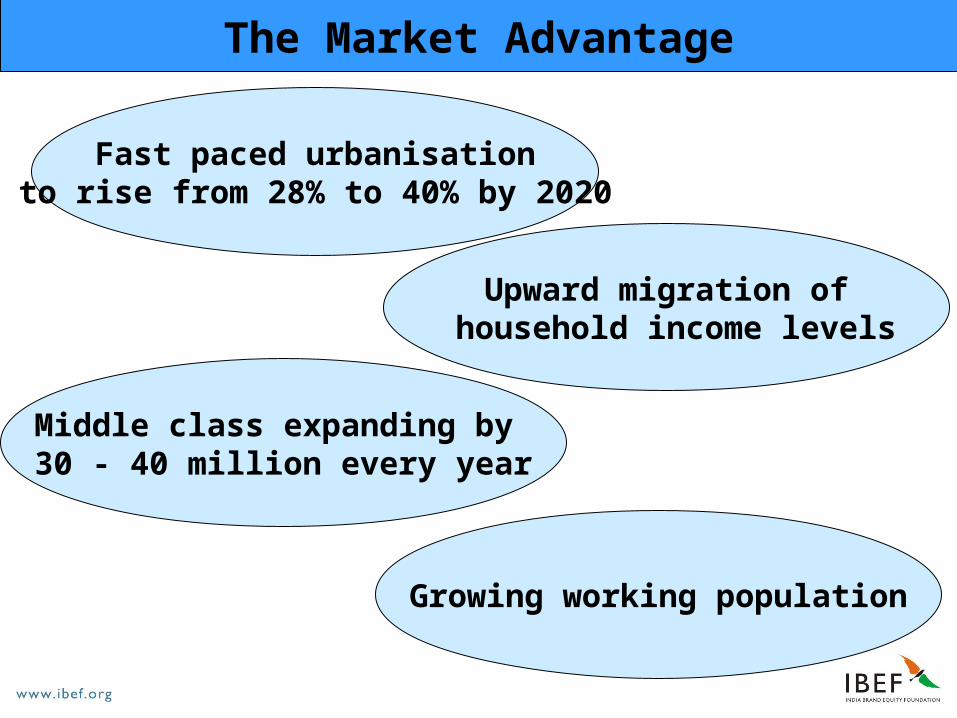

The Market Advantage

Fast paced urbanisationto rise from 28% to 40% by 2020

Middle class expanding by 30 - 40 million every year

Growing working population

Upward migration of household income levels

The Quality & Productivity Advantage

Auto Companies achieving high productivity through best practices:

T Q M T P M Six Sigma Toyota Production Systems / Lean

Companies growing in ranks can offer PPM levels of quality

The Policy Advantage

Auto Policy 2002 promotes an

integrated automotive sector

2001- Quantitative Restrictions were

removed

Incentives for R & D

Stringent environmental controls

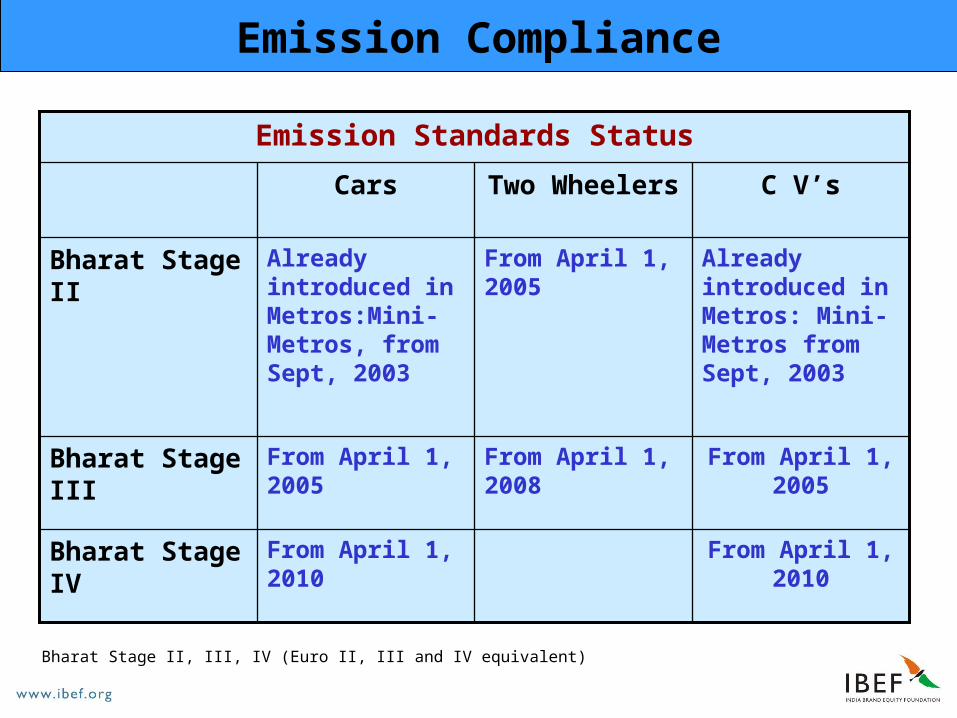

Emission Compliance

From April 1, 2010

From April 1, 2010

Bharat Stage IV

From April 1, 2005

From April 1, 2008

From April 1, 2005

Bharat Stage III

Already introduced in Metros: Mini-Metros from Sept, 2003

From April 1, 2005

Already introduced in Metros:Mini-Metros, from Sept, 2003

Bharat Stage II

C V’sTwo WheelersCars

Emission Standards Status

Bharat Stage II, III, IV (Euro II, III and IV equivalent)

Indian Automotive Industry

India - An Overview

Market and Growth Potential

Players

Opportunities

Why India?

Contact in India

Contact in India

Society of Indian Automobile Manufacturers (SIAM)

Core 4B, 5th Floor, India Habitat CentreLodi RoadNew Delhi - 110 003.India

Tel: 0091 11 24647810- 12, 24648555Fax: 0091 11 24648222

Contact in India

Automotive Component Manufacturers Association of India (ACMA)

6th FloorThe Capital Court,Olof Palme Marg, Munirka,New Delhi - 110 067

Tel.: 0091 11 2616 0315, 2617 5873, 2618 4479Fax: 0091 11 2616 0317E-mail: [email protected]: www.acmainfo.com