August 2017 - Tidewater Midstream and … Tidewater is a High Growth Midstream Company NGL...

14

August 2017

Transcript of August 2017 - Tidewater Midstream and … Tidewater is a High Growth Midstream Company NGL...

August 2017

2

Forward Looking Information

Advisory

In the interests of providing Tidewater Midstream and Infrastructure Ltd. (“Tidewater” or the “Corporation”) shareholders andpotential investors with information regarding Tidewater, including management’s assessment of future plans and operationsrelating to the Corporation, this document contains certain statements and information that are forward-looking statements orinformation within the meaning of applicable securities legislation, and which are collectively referred to herein as “forward-looking statements”. Forward-looking statements in this document include, but are not limited to statements and tables(collectively “statements”) with respect to: the strategic acquisition and concurrent equity financing; subsequent acquisitions andstrategies for acquisitions, capital projects and expenditures; strategic initiatives; anticipated producer activity and industry trends;and anticipated performance. Readers are cautioned not to place undue reliance on forward-looking statements, as there can be noassurance that the plans, intentions or expectations upon which they are based will occur. By their nature, forward-lookingstatements involve numerous assumptions, as well as known and unknown risks and uncertainties, both general and specific, thatcontribute to the possibility that the predictions, forecasts, projections and other forward-looking statements will not occur andwhich may cause Tidewater’s actual performance and financial results in future periods to differ materially from any estimates orprojections of future performance or results expressed or implied by the forward-looking statements. These assumptions, risks anduncertainties include, among other things: receipt of third party, regulatory and governmental approvals and consents in respect ofthe strategic acquisition and concurrent equity financing; completion of the strategic acquisition and concurrent equity financing;Tidewater’s ability to successfully implement strategic initiatives and whether such initiatives yield the expected benefits; futureoperating results; fluctuations in the supply and demand for natural gas, NGLs, and iso-octane; assumptions regarding commodityprices; activities of producers, competitors and others; the weather; assumptions around construction schedules and costs, includingthe availability and cost of materials and service providers; fluctuations in currency and interest rates; credit risks; marketingmargins; potential disruption or unexpected technical difficulties in developing new facilities or projects; unexpected cost increasesor technical difficulties in constructing or modifying processing facilities; Tidewater’s ability to generate sufficient cash flow fromoperations to meet its current and future obligations; its ability to access external sources of debt and equity capital; changes inlaws or regulations or the interpretations of such laws or regulations; political and economic conditions; and other risks anduncertainties described from time to time in the reports and filings made with securities regulatory authorities by Tidewater.

Readers are cautioned that the foregoing list of important factors is not exhaustive. The forward-looking statements contained inthis document are made as of the date of this document or the dates specifically referenced herein. For additional informationplease refer to Tidewater’s public filings available on SEDAR at www.sedar.com. All forward-looking statements contained in thisdocument are expressly qualified by this cautionary statement.

Any financial outlook or future-oriented financial information, as defined by applicable securities legislation, has been approved bymanagement of Tidewater as of August 15, 2017. Such financial outlook or future-oriented financial information is provided for thepurpose of providing information about management's current expectations and goals relating to the future of Tidewater. Readersare cautioned that reliance on such information may not be appropriate for other purposes.

Non-GAAP Financial Measures: This presentation refers to “EBITDA” and “cash available for distribution” (CAFD), which do not haveany standardized meaning prescribed by generally accepted accounting principles in Canada (“GAAP”). We define EBITDA as meansearnings before interest, taxes, depreciation and amortization. We define “cash available for distribution” (CAFD) as the amount ofcash generated from operations, before changes in working capital and after deducting sustaining capital expenditures, scheduledprincipal repayments of debt and distributions to non-controlling interests.

2

3

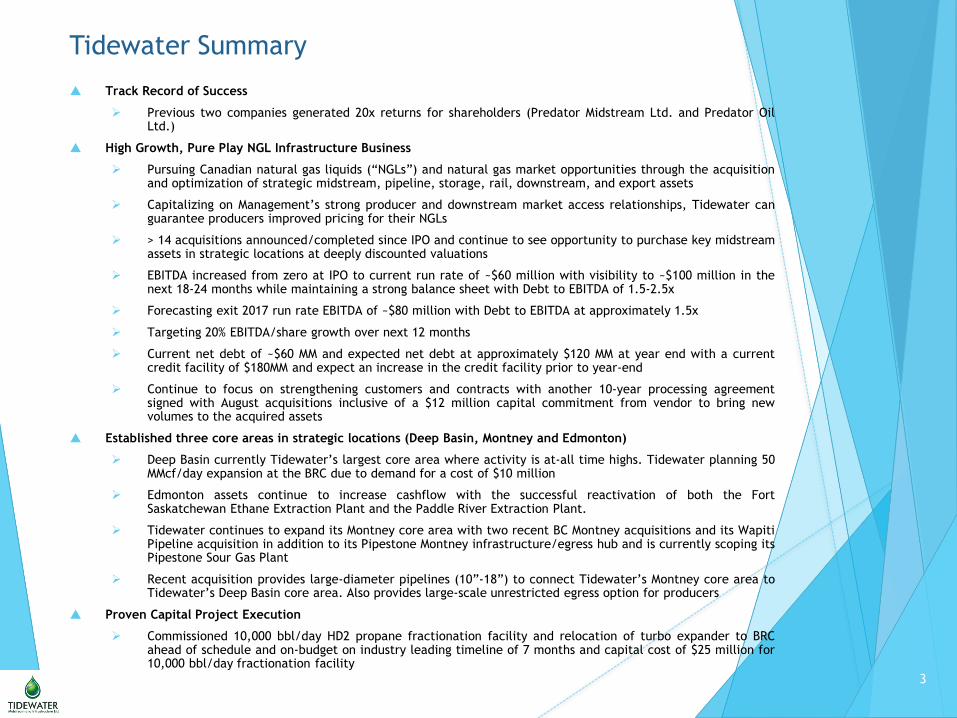

Track Record of Success

➢ Previous two companies generated 20x returns for shareholders (Predator Midstream Ltd. and Predator OilLtd.)

High Growth, Pure Play NGL Infrastructure Business

➢ Pursuing Canadian natural gas liquids (“NGLs”) and natural gas market opportunities through the acquisitionand optimization of strategic midstream, pipeline, storage, rail, downstream, and export assets

➢ Capitalizing on Management’s strong producer and downstream market access relationships, Tidewater canguarantee producers improved pricing for their NGLs

➢ > 14 acquisitions announced/completed since IPO and continue to see opportunity to purchase key midstreamassets in strategic locations at deeply discounted valuations

➢ EBITDA increased from zero at IPO to current run rate of ~$60 million with visibility to ~$100 million in thenext 18-24 months while maintaining a strong balance sheet with Debt to EBITDA of 1.5-2.5x

➢ Forecasting exit 2017 run rate EBITDA of ~$80 million with Debt to EBITDA at approximately 1.5x

➢ Targeting 20% EBITDA/share growth over next 12 months

➢ Current net debt of ~$60 MM and expected net debt at approximately $120 MM at year end with a currentcredit facility of $180MM and expect an increase in the credit facility prior to year-end

➢ Continue to focus on strengthening customers and contracts with another 10-year processing agreementsigned with August acquisitions inclusive of a $12 million capital commitment from vendor to bring newvolumes to the acquired assets

Established three core areas in strategic locations (Deep Basin, Montney and Edmonton)

➢ Deep Basin currently Tidewater’s largest core area where activity is at-all time highs. Tidewater planning 50MMcf/day expansion at the BRC due to demand for a cost of $10 million

➢ Edmonton assets continue to increase cashflow with the successful reactivation of both the FortSaskatchewan Ethane Extraction Plant and the Paddle River Extraction Plant.

➢ Tidewater continues to expand its Montney core area with two recent BC Montney acquisitions and its WapitiPipeline acquisition in addition to its Pipestone Montney infrastructure/egress hub and is currently scoping itsPipestone Sour Gas Plant

➢ Recent acquisition provides large-diameter pipelines (10”-18”) to connect Tidewater’s Montney core area toTidewater’s Deep Basin core area. Also provides large-scale unrestricted egress option for producers

Proven Capital Project Execution

➢ Commissioned 10,000 bbl/day HD2 propane fractionation facility and relocation of turbo expander to BRCahead of schedule and on-budget on industry leading timeline of 7 months and capital cost of $25 million for10,000 bbl/day fractionation facility

Tidewater Summary

4

Tidewater is a High Growth Midstream Company

NGL Connectivity Strategy

Acquire Strategic

Contracted

Infrastructure

Own key NGL/gas infrastructure and gas plants

with proximity to multiple transportation

options, coupled with take-or-pay and/or

reserve dedication agreements

Most recent acquisition was $51 million dollar

purchase price to acquire assets with > $900 million

of replacement value and generating 2018 EBITDA of

~ $10 million. Creating the backbone for the

Tidewater network between the Montney and Deep

Basin and includes 10 year reserve dedication

Optimize Through

Organic Investments

Enable Tidewater to own a strategic integrated

value chain from well head to end market

and/or tidewater

Significant opportunities within acquired assets to

continue to generate incremental EBITDA at > 20%

IRR

Recent acquisition includes large diameter pipelines

in both Montney and Deep Basin core areas and

create new egress options for producers

Increase Capabilities of

Infrastructure

Increase third party throughput and/or

improve liquids capture/pricing of NGLs for all

related parties

Commissioned 10,000 bbl/d fractionation facility on

industry leading timeline and cost in 7 months for

$25 MM

Relocation of existing acquired and idled turbo

expander and commenced expansion at BRC

Focused on building out large scale Montney

infrastructure and related egress

Enhance Logistics

Network & Market

Access Infrastructure

Various logistics infrastructure including rail,

pipelines and trucking

Various port and pipeline infrastructure to get

us to export markets

100 railcar NGL facility at Edmonton constructed on

time and on budget

Recent acquisition includes large sales meter which

is currently unrestricted creating immediate egress

options for Tidewater’s customers

1

2

3

4

5

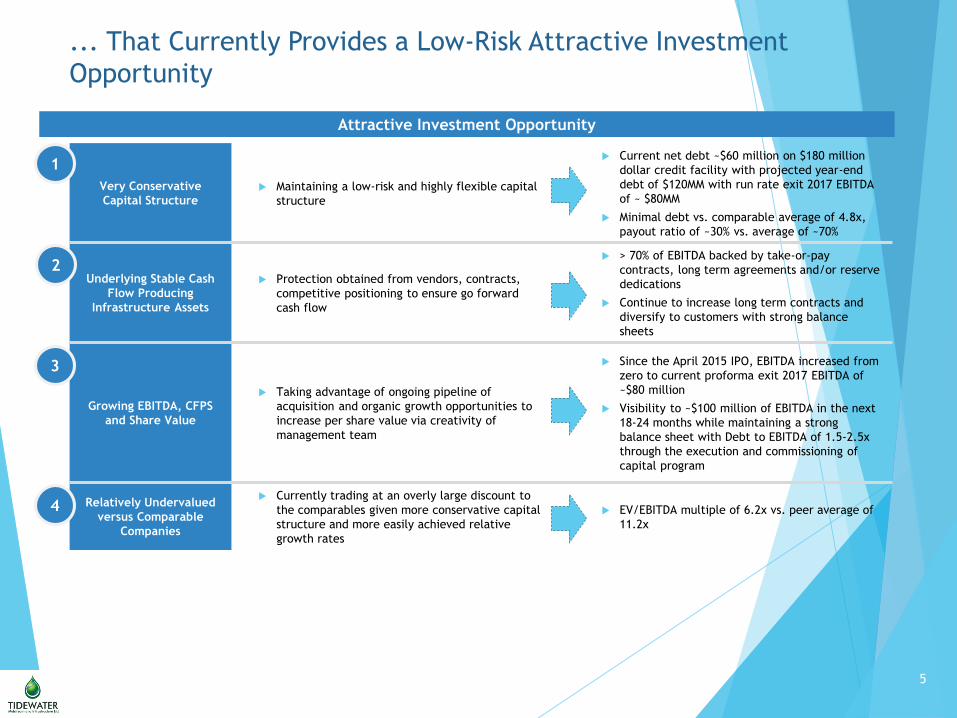

Very Conservative

Capital Structure Maintaining a low-risk and highly flexible capital

structure

Current net debt ~$60 million on $180 million

dollar credit facility with projected year-end

debt of $120MM with run rate exit 2017 EBITDA

of ~ $80MM

Minimal debt vs. comparable average of 4.8x,

payout ratio of ~30% vs. average of ~70%

Underlying Stable Cash

Flow Producing

Infrastructure Assets

Protection obtained from vendors, contracts,

competitive positioning to ensure go forward

cash flow

> 70% of EBITDA backed by take-or-pay

contracts, long term agreements and/or reserve

dedications

Continue to increase long term contracts and

diversify to customers with strong balance

sheets

Growing EBITDA, CFPS

and Share Value

Taking advantage of ongoing pipeline of

acquisition and organic growth opportunities to

increase per share value via creativity of

management team

Since the April 2015 IPO, EBITDA increased from

zero to current proforma exit 2017 EBITDA of

~$80 million

Visibility to ~$100 million of EBITDA in the next

18-24 months while maintaining a strong

balance sheet with Debt to EBITDA of 1.5-2.5x

through the execution and commissioning of

capital program

Relatively Undervalued

versus Comparable

Companies

Currently trading at an overly large discount to

the comparables given more conservative capital

structure and more easily achieved relative

growth rates

EV/EBITDA multiple of 6.2x vs. peer average of

11.2x

... That Currently Provides a Low-Risk Attractive Investment

Opportunity

Attractive Investment Opportunity

1

2

3

4

66

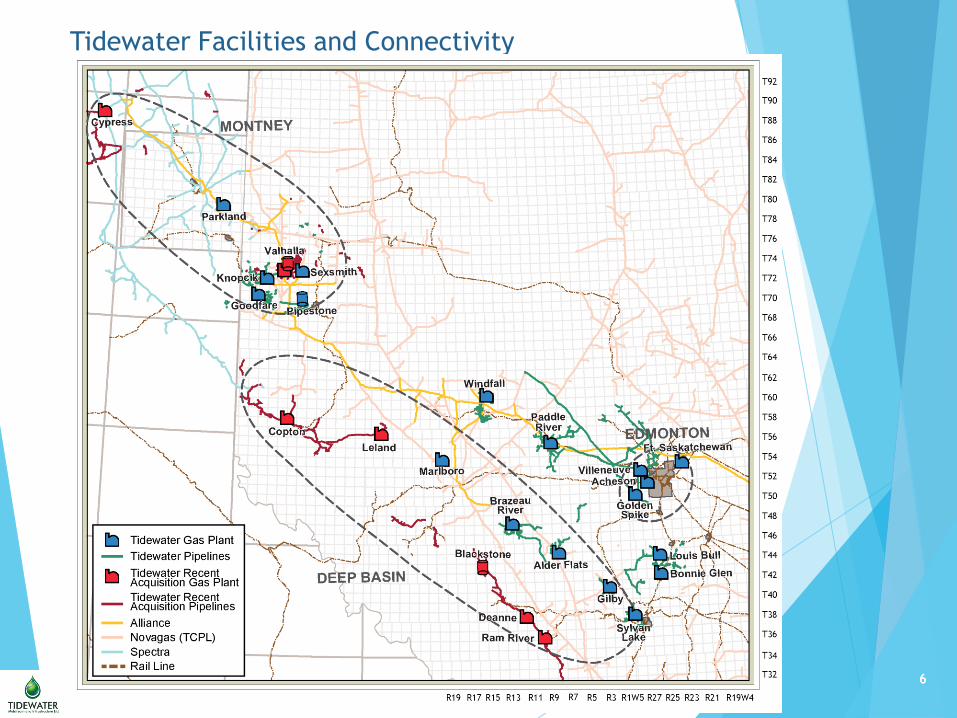

Tidewater Facilities and Connectivity

77

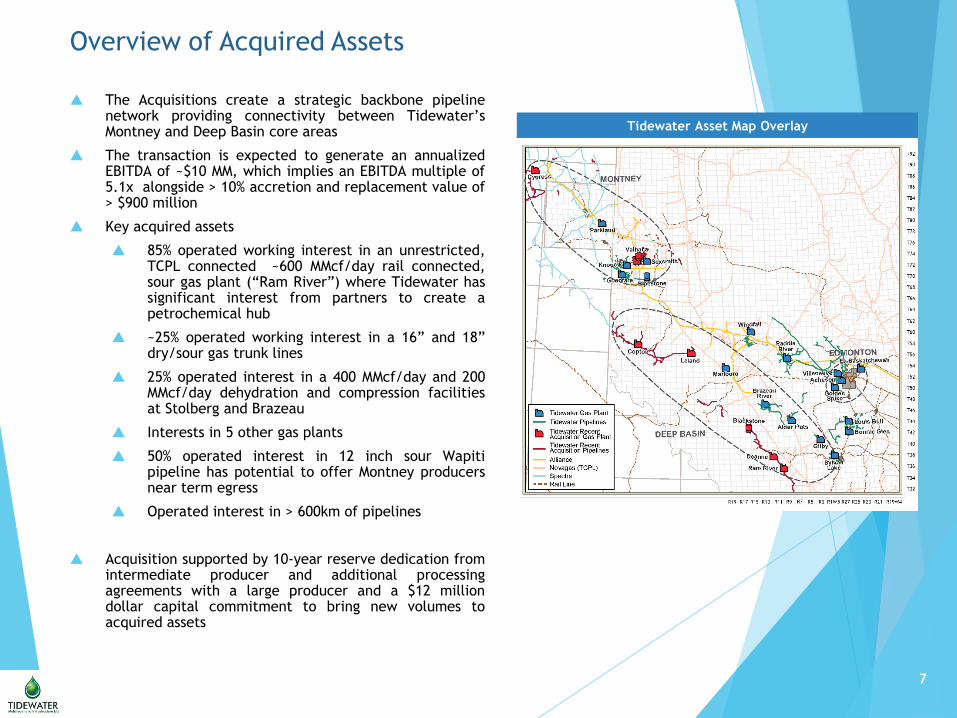

Overview of Acquired Assets

Tidewater Asset Map Overlay

The Acquisitions create a strategic backbone pipelinenetwork providing connectivity between Tidewater’sMontney and Deep Basin core areas

The transaction is expected to generate an annualizedEBITDA of ~$10 MM, which implies an EBITDA multiple of5.1x alongside > 10% accretion and replacement value of> $900 million

Key acquired assets

85% operated working interest in an unrestricted,TCPL connected ~600 MMcf/day rail connected,sour gas plant (“Ram River”) where Tidewater hassignificant interest from partners to create apetrochemical hub

~25% operated working interest in a 16” and 18”dry/sour gas trunk lines

25% operated interest in a 400 MMcf/day and 200MMcf/day dehydration and compression facilitiesat Stolberg and Brazeau

Interests in 5 other gas plants

50% operated interest in 12 inch sour Wapitipipeline has potential to offer Montney producersnear term egress

Operated interest in > 600km of pipelines

Acquisition supported by 10-year reserve dedication fromintermediate producer and additional processingagreements with a large producer and a $12 milliondollar capital commitment to bring new volumes toacquired assets

88

Overview of Deep Basin Assets

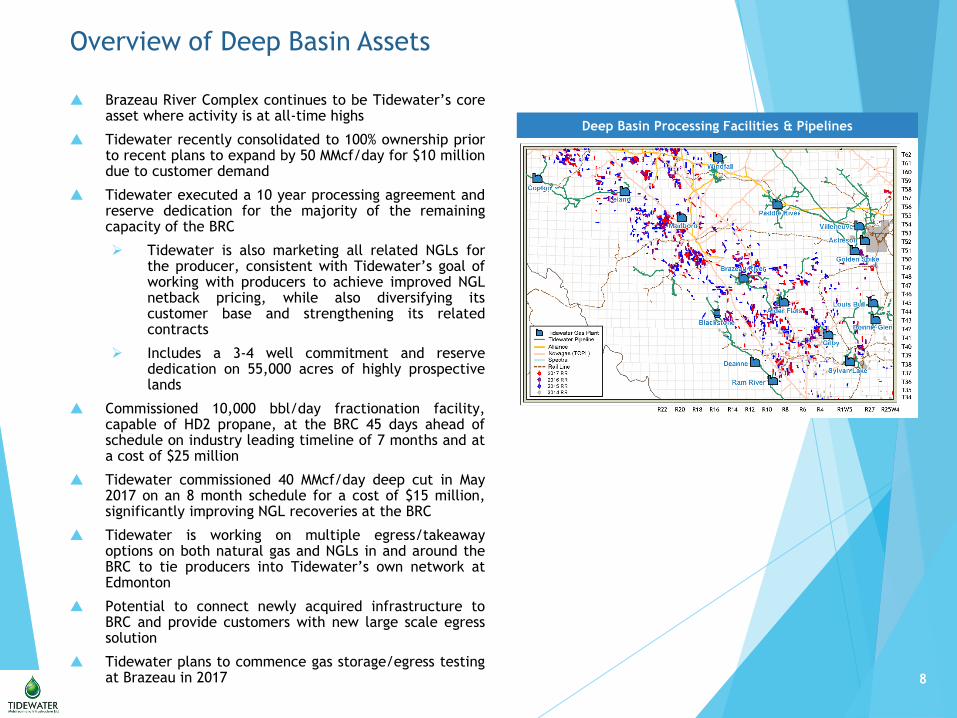

Deep Basin Processing Facilities & Pipelines

Brazeau River Complex continues to be Tidewater’s coreasset where activity is at all-time highs

Tidewater recently consolidated to 100% ownership priorto recent plans to expand by 50 MMcf/day for $10 milliondue to customer demand

Tidewater executed a 10 year processing agreement andreserve dedication for the majority of the remainingcapacity of the BRC

➢ Tidewater is also marketing all related NGLs forthe producer, consistent with Tidewater’s goal ofworking with producers to achieve improved NGLnetback pricing, while also diversifying itscustomer base and strengthening its relatedcontracts

➢ Includes a 3-4 well commitment and reservededication on 55,000 acres of highly prospectivelands

Commissioned 10,000 bbl/day fractionation facility,capable of HD2 propane, at the BRC 45 days ahead ofschedule on industry leading timeline of 7 months and ata cost of $25 million

Tidewater commissioned 40 MMcf/day deep cut in May2017 on an 8 month schedule for a cost of $15 million,significantly improving NGL recoveries at the BRC

Tidewater is working on multiple egress/takeawayoptions on both natural gas and NGLs in and around theBRC to tie producers into Tidewater’s own network atEdmonton

Potential to connect newly acquired infrastructure toBRC and provide customers with new large scale egresssolution

Tidewater plans to commence gas storage/egress testingat Brazeau in 2017

99

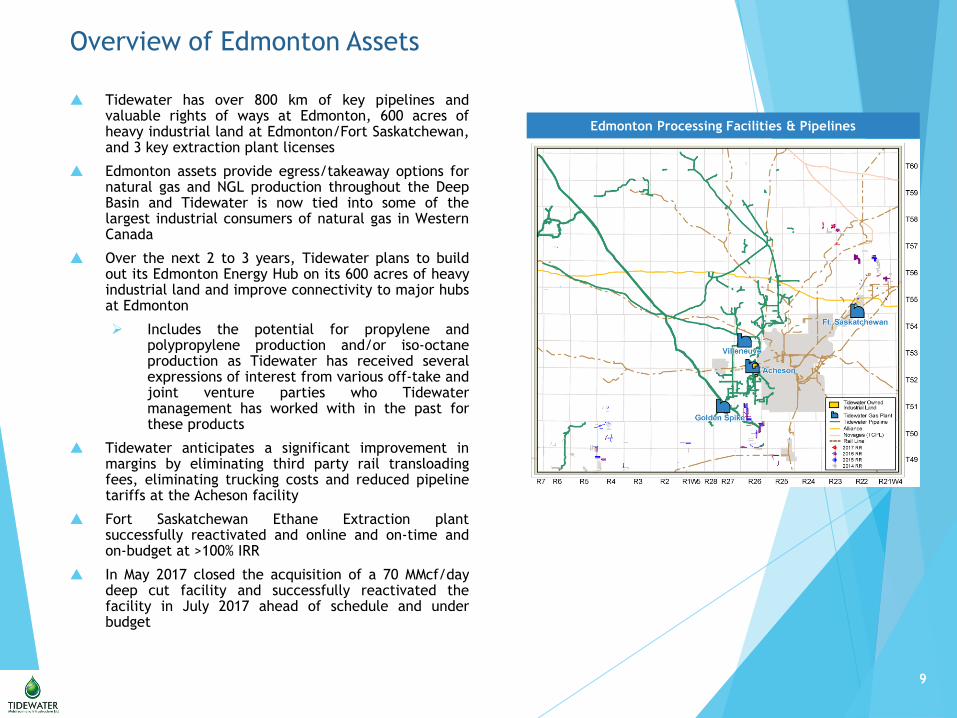

Overview of Edmonton Assets

Edmonton Processing Facilities & Pipelines

Tidewater has over 800 km of key pipelines andvaluable rights of ways at Edmonton, 600 acres ofheavy industrial land at Edmonton/Fort Saskatchewan,and 3 key extraction plant licenses

Edmonton assets provide egress/takeaway options fornatural gas and NGL production throughout the DeepBasin and Tidewater is now tied into some of thelargest industrial consumers of natural gas in WesternCanada

Over the next 2 to 3 years, Tidewater plans to buildout its Edmonton Energy Hub on its 600 acres of heavyindustrial land and improve connectivity to major hubsat Edmonton

➢ Includes the potential for propylene andpolypropylene production and/or iso-octaneproduction as Tidewater has received severalexpressions of interest from various off-take andjoint venture parties who Tidewatermanagement has worked with in the past forthese products

Tidewater anticipates a significant improvement inmargins by eliminating third party rail transloadingfees, eliminating trucking costs and reduced pipelinetariffs at the Acheson facility

Fort Saskatchewan Ethane Extraction plantsuccessfully reactivated and online and on-time andon-budget at >100% IRR

In May 2017 closed the acquisition of a 70 MMcf/daydeep cut facility and successfully reactivated thefacility in July 2017 ahead of schedule and underbudget

1010

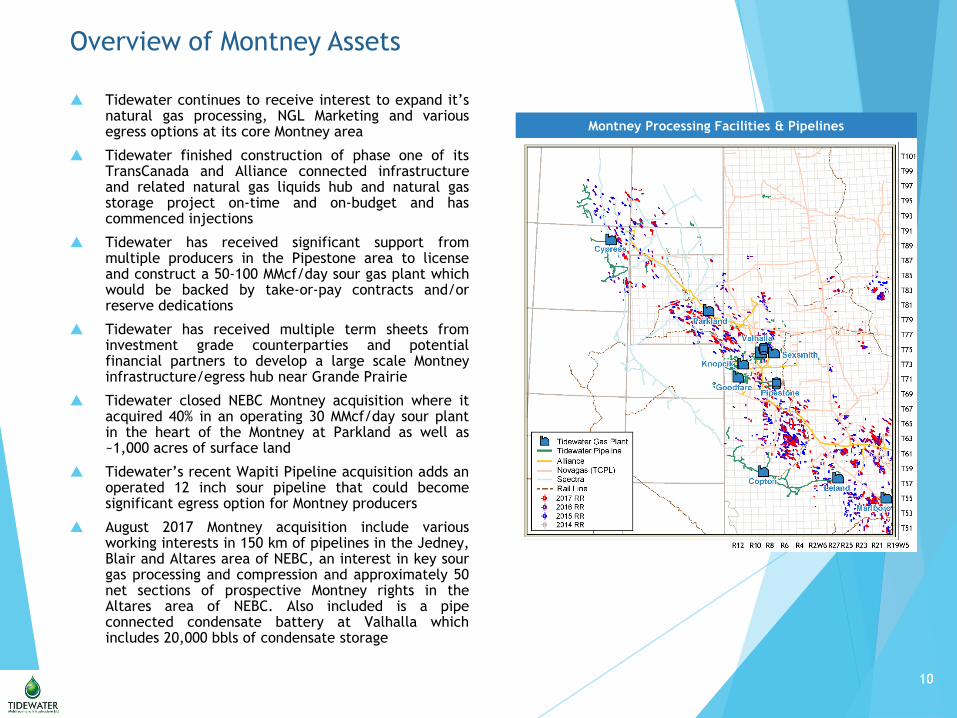

Overview of Montney Assets

Montney Processing Facilities & Pipelines

Tidewater continues to receive interest to expand it’snatural gas processing, NGL Marketing and variousegress options at its core Montney area

Tidewater finished construction of phase one of itsTransCanada and Alliance connected infrastructureand related natural gas liquids hub and natural gasstorage project on-time and on-budget and hascommenced injections

Tidewater has received significant support frommultiple producers in the Pipestone area to licenseand construct a 50-100 MMcf/day sour gas plant whichwould be backed by take-or-pay contracts and/orreserve dedications

Tidewater has received multiple term sheets frominvestment grade counterparties and potentialfinancial partners to develop a large scale Montneyinfrastructure/egress hub near Grande Prairie

Tidewater closed NEBC Montney acquisition where itacquired 40% in an operating 30 MMcf/day sour plantin the heart of the Montney at Parkland as well as~1,000 acres of surface land

Tidewater’s recent Wapiti Pipeline acquisition adds anoperated 12 inch sour pipeline that could becomesignificant egress option for Montney producers

August 2017 Montney acquisition include variousworking interests in 150 km of pipelines in the Jedney,Blair and Altares area of NEBC, an interest in key sourgas processing and compression and approximately 50net sections of prospective Montney rights in theAltares area of NEBC. Also included is a pipeconnected condensate battery at Valhalla whichincludes 20,000 bbls of condensate storage

11

Tidewater has a Solid Infrastructure Business With a Strengthening

Customer Base

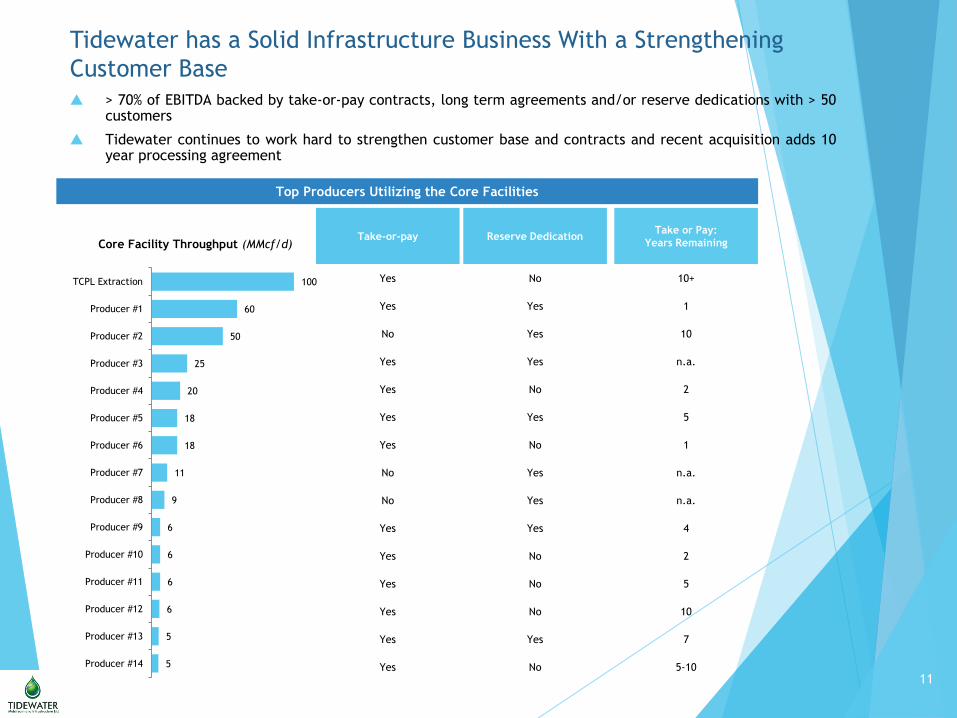

> 70% of EBITDA backed by take-or-pay contracts, long term agreements and/or reserve dedications with > 50customers

Tidewater continues to work hard to strengthen customer base and contracts and recent acquisition adds 10year processing agreement

Top Producers Utilizing the Core Facilities

Take-or-pay Reserve DedicationTake or Pay:

Years Remaining

Yes No 10+

Yes Yes 1

No Yes 10

Yes Yes n.a.

Yes No 2

Yes Yes 5

Yes No 1

No Yes n.a.

No Yes n.a.

Yes Yes 4

Yes No 2

Yes No 5

Yes No 10

Yes Yes 7

Yes No 5-10

Core Facility Throughput (MMcf/d)

5

5

6

6

6

6

9

11

18

18

20

25

50

60

100

Producer #14

Producer #13

Producer #12

Producer #11

Producer #10

Producer #9

Producer #8

Producer #7

Producer #6

Producer #5

Producer #4

Producer #3

Producer #2

Producer #1

TCPL Extraction

12

$54

$80

-

$24 $24 $26 $28 $28

$42 $42 $46

$49 $54 $54 $56 $58

$69 $71

$80 $80

$100

($5)

($25)

($17)($12)

$20

$25

$55

($23) ($21)

$20

$50

($15)

($2)

$16

$66 $66

$120 $120

$150

($30)

($20)

($10)

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

$160

IPO BRCAcquisition &

Financing

PipelineAcquisition

Peace RiverArch Gas Plant

Acquisition

Gas Plant &Propane

Acquisitions

Edmonton AreaInfrastrucutre

Acquisition

AltaGasAcquisition

$80.5 MMFinancing

Acheson Plant,Land andPipeline

Acquisition andRail Facility

BRC Infra.Acquisition

Remaining BRCInterest,Gathering

Pipelines, NatGas Storage

$69 MMFinancing

NEBCProcessing

Plant / NGLTrucking

Q4 ProcessingAgreement /

PembinaRestrictionsLifted / Fort

SaskatchewanReactivation /70 MMcf Deep

Cut + NGLPipeline

Acquisition &Reactivation

FractionationFacility &

Relocation ofTurbo

Expander /BRC Expansion

TransCanadaand AllianceConnected

Infrastructure

Acquisition Total RemainingCapital OverNext 12-24

Months

C$ M

illions

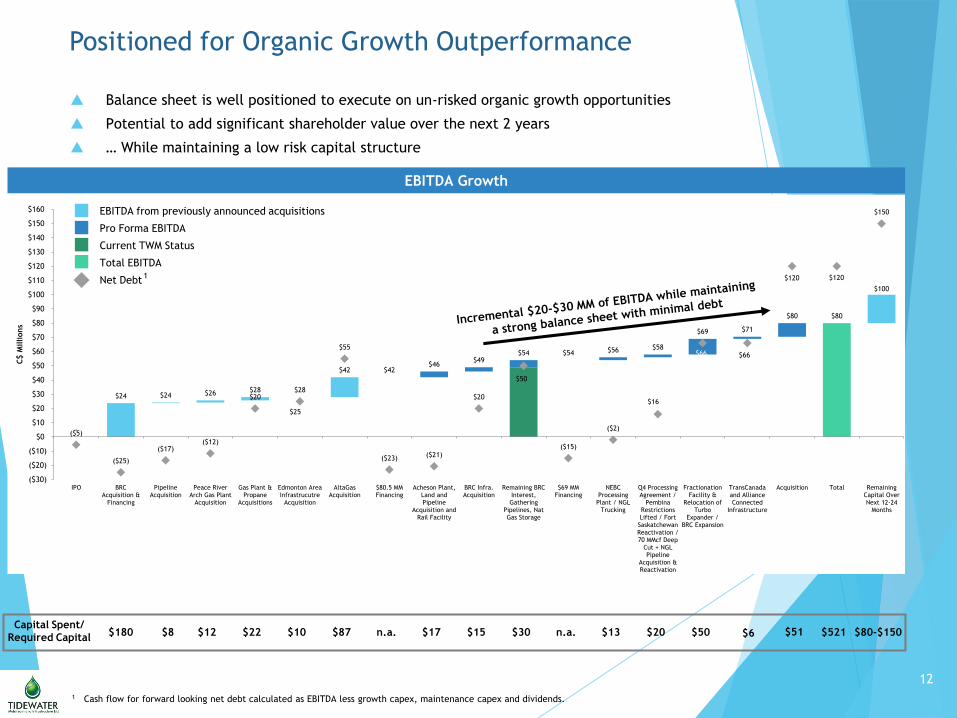

Positioned for Organic Growth Outperformance

Balance sheet is well positioned to execute on un-risked organic growth opportunities

Potential to add significant shareholder value over the next 2 years

… While maintaining a low risk capital structure

EBITDA Growth

EBITDA from previously announced acquisitions

Total EBITDA

Net Debt

Pro Forma EBITDA

Capital Spent/

Required Capital$180 $8 $12 $22 $10 $87 n.a. $17 n.a. $20 $50 $6 $521

Current TWM Status

$80-$150

1 Cash flow for forward looking net debt calculated as EBITDA less growth capex, maintenance capex and dividends.

1

$15 $30 $13 $51

13

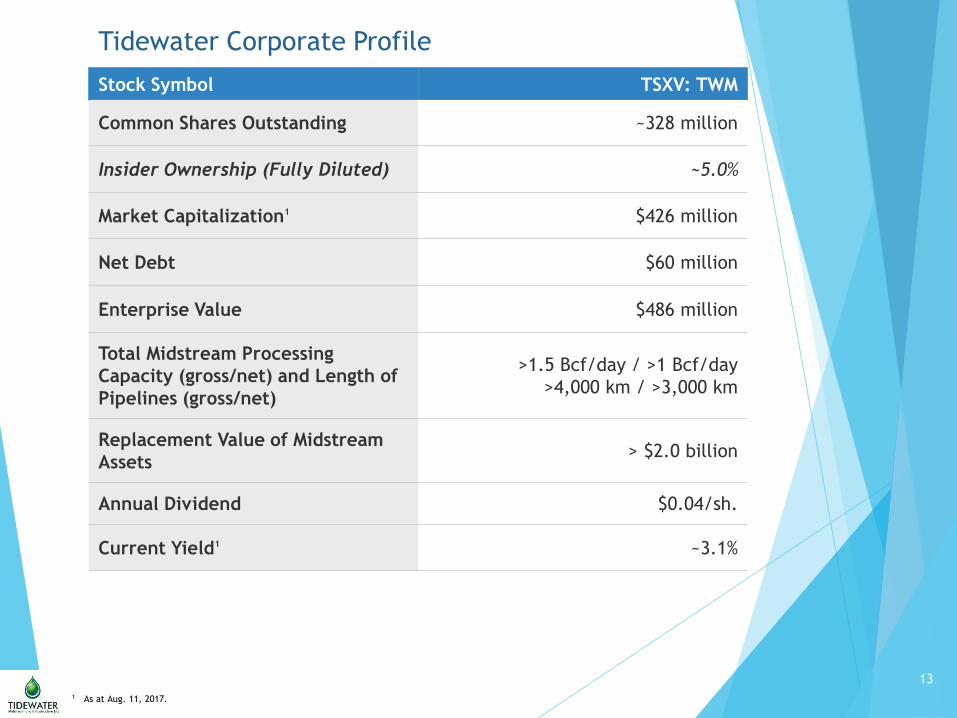

Stock Symbol TSXV: TWM

Common Shares Outstanding ~328 million

Insider Ownership (Fully Diluted) ~5.0%

Market Capitalization1 $426 million

Net Debt $60 million

Enterprise Value $486 million

Total Midstream Processing

Capacity (gross/net) and Length of

Pipelines (gross/net)

>1.5 Bcf/day / >1 Bcf/day

>4,000 km / >3,000 km

Replacement Value of Midstream

Assets> $2.0 billion

Annual Dividend $0.04/sh.

Current Yield1 ~3.1%

Tidewater Corporate Profile

1 As at Aug. 11, 2017.

14

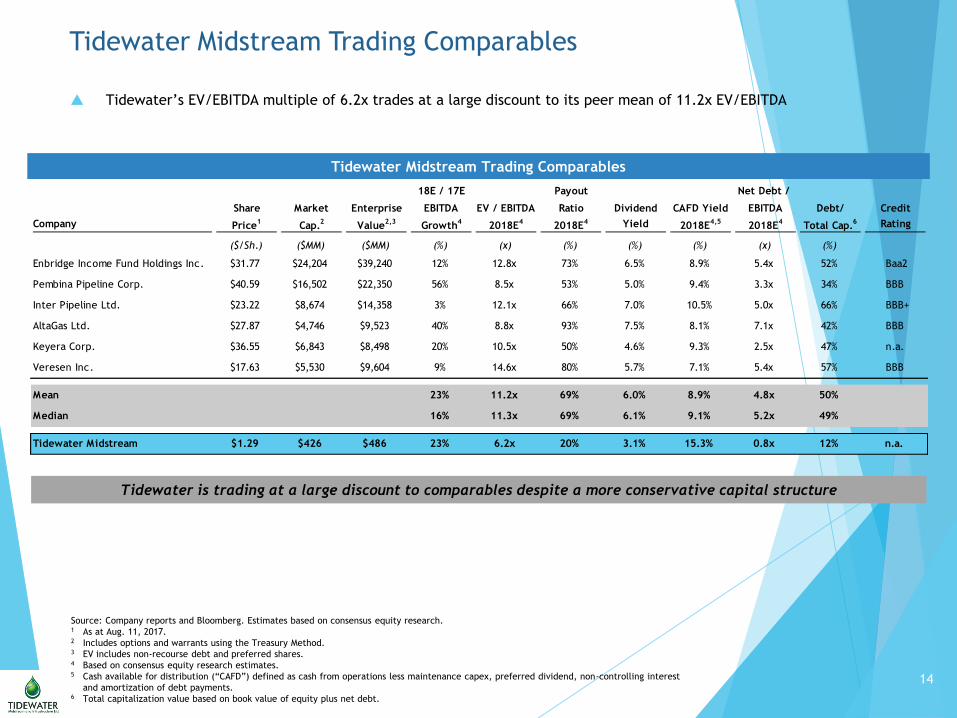

Tidewater Midstream Trading Comparables

Source: Company reports and Bloomberg. Estimates based on consensus equity research.1 As at Aug. 11, 2017.2 Includes options and warrants using the Treasury Method.3 EV includes non-recourse debt and preferred shares.4 Based on consensus equity research estimates.5 Cash available for distribution (“CAFD”) defined as cash from operations less maintenance capex, preferred dividend, non-controlling interest

and amortization of debt payments.6 Total capitalization value based on book value of equity plus net debt.

Tidewater is trading at a large discount to comparables despite a more conservative capital structure

Tidewater’s EV/EBITDA multiple of 6.2x trades at a large discount to its peer mean of 11.2x EV/EBITDA

Tidewater Midstream Trading Comparables

18E / 17E Payout Net Debt /

Share Market Enterprise EBITDA EV / EBITDA Ratio Dividend CAFD Yield EBITDA Debt/ Credit

Company Price1

Cap.2

Value2,3

Growth4

2018E4

2018E4 Yield 2018E

4,52018E

4Total Cap.

6 Rating

($/Sh.) ($MM) ($MM) (%) (x) (%) (%) (%) (x) (%)

Enbridge Income Fund Holdings Inc. $31.77 $24,204 $39,240 12% 12.8x 73% 6.5% 8.9% 5.4x 52% Baa2

Pembina Pipeline Corp. $40.59 $16,502 $22,350 56% 8.5x 53% 5.0% 9.4% 3.3x 34% BBB

Inter Pipeline Ltd. $23.22 $8,674 $14,358 3% 12.1x 66% 7.0% 10.5% 5.0x 66% BBB+

AltaGas Ltd. $27.87 $4,746 $9,523 40% 8.8x 93% 7.5% 8.1% 7.1x 42% BBB

Keyera Corp. $36.55 $6,843 $8,498 20% 10.5x 50% 4.6% 9.3% 2.5x 47% n.a.

Veresen Inc. $17.63 $5,530 $9,604 9% 14.6x 80% 5.7% 7.1% 5.4x 57% BBB

Mean 23% 11.2x 69% 6.0% 8.9% 4.8x 50%

Median 16% 11.3x 69% 6.1% 9.1% 5.2x 49%

Tidewater Midstream $1.29 $426 $486 23% 6.2x 20% 3.1% 15.3% 0.8x 12% n.a.