August 2017 CLIENT BRIEFING - jegi.com · Client Briefing August 2017 ... team harmony is key. ......

8

Client Briefing August 2017 | 1 HUMAN CAPITAL MANAGEMENT SYMPOSIUM On July 12 th , JEGI hosted its 2017 Human Capital Management Symposium with partner S&P Global in New York City. This exclusive event brought together a select group of senior industry executives and investors for an engaging symposium on key topics and trends within the Human Capital Management sector. The event began with opening remarks by JEGI Founder & CEO, Wilma Jordan and a Human Capital Management overview from JEGI Managing Director & Co-Head of Technology Banking, Jeff Becker. Attendees then heard from Jean- Marc Laouchez, Global Managing Director, Strategy & Solutions, Korn Ferry Hay Group and Michael Vaughan, Managing Director & CEO of The Regis Company, in a fireside chat on the topic of Leadership & Talent Development for the New Economy. The evening concluded with a panel titled Looking Ahead: Real Future Growth Opportunities in HCM. Panelists included Robert Schultz, General Manager, IBM Talent Management Solutions, Matt Sigelman, CEO, Burning Glass Technologies, and Bryan Sherwood, Vice President, Talent Acquisition, S&P Global. The following articles contain insights from this event. IN THIS ISSUE @JordanEdmiston linkedin.com/company/jegi Follow us on Twitter Find us on LinkedIn (from left) Bryan Sherwood (S&P), Robert Schultz (IBM), Wilma Jordan (JEGI), Matt Sigelman (Burning Glass), Jeff Becker (JEGI), Jean-Marc Laouchez (Korn Ferry), Michael Vaughan (Regis Company) August 2017 CLIENT BRIEFING 1 JEGI’s HCM Symposium Overview 2 Looking Ahead: Real Future Growth Opportunities in HCM 2 Leadership & Talent Development for the New Economy 3 China Executive Summary 4 JEGI H1 2017 M&A Overview 8 Exceptional Transaction Experience JEGI Human Capital Management Symposium To register: www.outsellinc.com/signature-event-2017

Transcript of August 2017 CLIENT BRIEFING - jegi.com · Client Briefing August 2017 ... team harmony is key. ......

Client Briefing August 2017 | 1

HUMAN CAPITAL MANAGEMENT SYMPOSIUM

On July 12th, JEGI hosted its 2017 Human Capital Management Symposium with partner S&P Global in New York City. This exclusive event brought together a select group of senior industry executives and investors for an engaging symposium on key topics and trends within the Human Capital Management sector.

The event began with opening remarks by JEGI Founder & CEO, Wilma Jordan and a Human Capital Management overview from JEGI Managing Director & Co-Head of Technology Banking, Jeff Becker. Attendees then heard from Jean-Marc Laouchez, Global Managing Director, Strategy & Solutions, Korn Ferry Hay Group and Michael Vaughan, Managing Director & CEO of The Regis Company, in a fireside chat on the topic of Leadership & Talent Development for the New Economy. The evening concluded with a panel titled Looking Ahead: Real Future Growth Opportunities in HCM. Panelists included Robert Schultz, General Manager, IBM Talent Management Solutions, Matt Sigelman, CEO, Burning Glass Technologies, and Bryan Sherwood, Vice President, Talent Acquisition, S&P Global.

The following articles contain insights from this event.

IN THIS ISSUE

@JordanEdmiston

linkedin.com/company/jegi

Follow us on Twitter

Find us on LinkedIn

(from left) Bryan Sherwood (S&P), Robert Schultz (IBM), Wilma Jordan (JEGI), Matt Sigelman (Burning Glass), Jeff Becker (JEGI), Jean-Marc Laouchez (Korn Ferry), Michael Vaughan (Regis Company)

August 2017

CLIENT BRIEFING

1 JEGI’s HCM Symposium Overview

2 Looking Ahead: Real Future Growth Opportunities in HCM

2 Leadership & Talent Development for the New Economy

3 China Executive Summary

4 JEGI H1 2017 M&A Overview

8 Exceptional Transaction Experience

JEGI Human Capital Management Symposium

To register:www.outsellinc.com/signature-event-2017

(from left) Bryan Sherwood (S&P), Robert Schultz (IBM), Matt Sigelman (Burning Glass)

LEADERSHIP & TALENT DEVELOPMENT FOR THE NEW ECONOMY

2 | Client Briefing August 2017

• The expectations of HR leaders are changing – in a department that is often siloed between talent acquisition, benefits and development, these departments now need to holistically determine who has had an impact. We are near a convergence of HR and Learning.

• Hybridization suggests that the skills required for a job are changing rapidly, and we’re needing new sets of skills for specific positions. The talent exists, but we need to analyze and redefine the talent, due to the need for new skills.

• HR Analytics should be implemented as support to key framing questions – implementation itself will not solve any problems. Companies should be able to identify issues and then engage with, process and analyze the data to support employees in developing solutions. Avoid the trap of looking only at operational, process-oriented KPIs.

• HR data has been disappointing in the past, because it has been limited to the scope of what is available within an individual HR management system. Big data companies are able to generate granular, actionable insights, because they have access to billions of records.

• AI can help companies do a better job of defining the type of person they should be looking to fill a position. There has never been an analytical framework for success, a way to automate decisions, or a way to provide and process real data as it relates to recruiting and HR in general.

• AI can help companies optimize their business-as-usual processes through pattern analysis and driving engagement in otherwise tedious tasks.

• Collecting and analyzing both internal and external data develops a framework for shaping current and future talent, and in aligning investments in learning and development. Employers can determine the changing set of skills within each role and what learning and development processes they can implement to better support current employees.

• HR needs to become a strategy function versus the process function it has previously been. A lack of planning around employee engagement and employee experience can cause pain points within organizations.

• In analyzing data collected internally versus externally, companies can arbitrage their current workforce,

which is more effective from a time and resource standpoint than external recruitment.

• Company culture needs to drive retention. Current difficulties in external hiring exacerbate the urgent need for data and analytics, from which companies can learn how to drive engagement and development of their existing workforce.

• Employers should use data to look for employees who are capable and have certain predispositions, rather than those who have a specific set of acquired skills. Rather than pushing employees into superfluously created positions, determine their capabilities and then map them into applicable positions.

LOOKING AHEAD: REAL FUTURE GROWTH OPPORTUNITIES FOR HCM

Panelists discussed the latest trends and challenges facing HCM and how technology can help, and hinder, those issues; see key takeaways below.

Jeff Becker: Amid constant transformation, how can companies think about leadership development as it attributes to long-term success?

Jean-Marc Laouchez: Companies want to know how to lead in this digitally-driven environment. Traditional leaders use blended development: assessing who you are and what you need to do, combined with lessons and lectures. We’re seeing companies engage young

people in developing a vision for the future in hopes of understanding the next generation – we know that they want to be part of the solution. We work with them in defining where we want to go and what we want to achieve, which makes us stronger. Over time, we monitor progress and ensure that what was developed is happening, aligning meaning and being mindful about what they do, rather than forcing it upon them.

Michael Vaughan: One of the shifts we’re seeing is the model of skills. Previously, technology focused on the organization, and skills were developed around the job profiles required. Now, technologies are people-centric, because things change so quickly. What’s made people successful today may completely change in six months.

Continued on page 7 >

Jean-Marc Laouchez and Michael Vaughan provide key insights into the intersection of leadership, talent and learning development – getting the most out of the human capital that has been attracted to your organization.

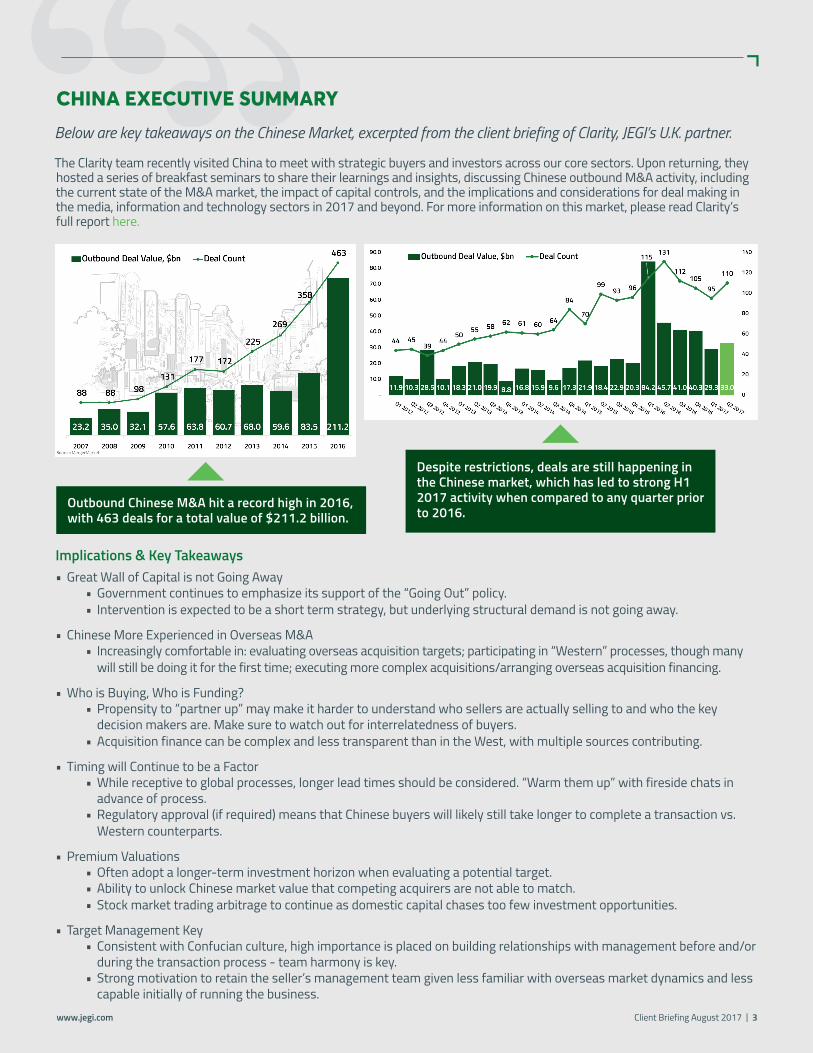

Outbound Chinese M&A hit a record high in 2016, with 463 deals for a total value of $211.2 billion.

Implications & Key Takeaways• Great Wall of Capital is not Going Away

• Government continues to emphasize its support of the “Going Out” policy.• Intervention is expected to be a short term strategy, but underlying structural demand is not going away.

• Chinese More Experienced in Overseas M&A• Increasingly comfortable in: evaluating overseas acquisition targets; participating in “Western” processes, though many

will still be doing it for the first time; executing more complex acquisitions/arranging overseas acquisition financing.

• Who is Buying, Who is Funding?• Propensity to “partner up” may make it harder to understand who sellers are actually selling to and who the key

decision makers are. Make sure to watch out for interrelatedness of buyers.• Acquisition finance can be complex and less transparent than in the West, with multiple sources contributing.

• Timing will Continue to be a Factor • While receptive to global processes, longer lead times should be considered. “Warm them up” with fireside chats in

advance of process.• Regulatory approval (if required) means that Chinese buyers will likely still take longer to complete a transaction vs.

Western counterparts.

• Premium Valuations• Often adopt a longer-term investment horizon when evaluating a potential target.• Ability to unlock Chinese market value that competing acquirers are not able to match.• Stock market trading arbitrage to continue as domestic capital chases too few investment opportunities.

• Target Management Key• Consistent with Confucian culture, high importance is placed on building relationships with management before and/or

during the transaction process - team harmony is key.• Strong motivation to retain the seller’s management team given less familiar with overseas market dynamics and less

capable initially of running the business.

Despite restrictions, deals are still happening in the Chinese market, which has led to strong H1 2017 activity when compared to any quarter prior to 2016.

Client Briefing August 2017 | 3www.jegi.com

CHINA EXECUTIVE SUMMARY

Below are key takeaways on the Chinese Market, excerpted from the client briefing of Clarity, JEGI’s U.K. partner.

The Clarity team recently visited China to meet with strategic buyers and investors across our core sectors. Upon returning, they hosted a series of breakfast seminars to share their learnings and insights, discussing Chinese outbound M&A activity, including the current state of the M&A market, the impact of capital controls, and the implications and considerations for deal making in the media, information and technology sectors in 2017 and beyond. For more information on this market, please read Clarity’s full report here.

Sources: JEGI Transaction Database and 451 Research LLC *Some of these deals are still pending

4 | Client Briefing August 2017

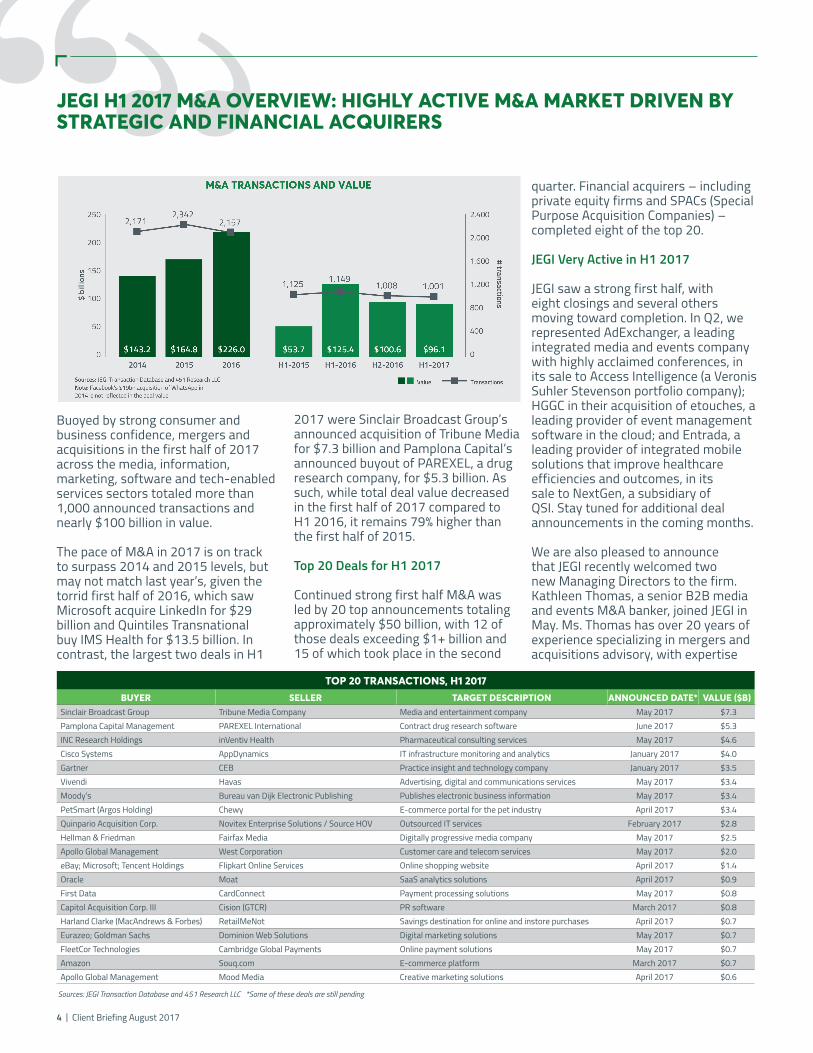

JEGI H1 2017 M&A OVERVIEW: HIGHLY ACTIVE M&A MARKET DRIVEN BY STRATEGIC AND FINANCIAL ACQUIRERS

2017 were Sinclair Broadcast Group’s announced acquisition of Tribune Media for $7.3 billion and Pamplona Capital’s announced buyout of PAREXEL, a drug research company, for $5.3 billion. As such, while total deal value decreased in the first half of 2017 compared to H1 2016, it remains 79% higher than the first half of 2015.

Top 20 Deals for H1 2017

Continued strong first half M&A was led by 20 top announcements totaling approximately $50 billion, with 12 of those deals exceeding $1+ billion and 15 of which took place in the second

Buoyed by strong consumer and business confidence, mergers and acquisitions in the first half of 2017 across the media, information, marketing, software and tech-enabled services sectors totaled more than 1,000 announced transactions and nearly $100 billion in value.

The pace of M&A in 2017 is on track to surpass 2014 and 2015 levels, but may not match last year’s, given the torrid first half of 2016, which saw Microsoft acquire LinkedIn for $29 billion and Quintiles Transnational buy IMS Health for $13.5 billion. In contrast, the largest two deals in H1

quarter. Financial acquirers – including private equity firms and SPACs (Special Purpose Acquisition Companies) – completed eight of the top 20.

JEGI Very Active in H1 2017

JEGI saw a strong first half, with eight closings and several others moving toward completion. In Q2, we represented AdExchanger, a leading integrated media and events company with highly acclaimed conferences, in its sale to Access Intelligence (a Veronis Suhler Stevenson portfolio company); HGGC in their acquisition of etouches, a leading provider of event management software in the cloud; and Entrada, a leading provider of integrated mobile solutions that improve healthcare efficiencies and outcomes, in its sale to NextGen, a subsidiary of QSI. Stay tuned for additional deal announcements in the coming months.

We are also pleased to announce that JEGI recently welcomed two new Managing Directors to the firm. Kathleen Thomas, a senior B2B media and events M&A banker, joined JEGI in May. Ms. Thomas has over 20 years of experience specializing in mergers and acquisitions advisory, with expertise

TOP 20 TRANSACTIONS, H1 2017BUYER SELLER TARGET DESCRIPTION ANNOUNCED DATE* VALUE ($B)

Sinclair Broadcast Group Tribune Media Company Media and entertainment company May 2017 $7.3Pamplona Capital Management PAREXEL International Contract drug research software June 2017 $5.3 INC Research Holdings inVentiv Health Pharmaceutical consulting services May 2017 $4.6Cisco Systems AppDynamics IT infrastructure monitoring and analytics January 2017 $4.0Gartner CEB Practice insight and technology company January 2017 $3.5Vivendi Havas Advertising, digital and communications services May 2017 $3.4Moody’s Bureau van Dijk Electronic Publishing Publishes electronic business information May 2017 $3.4PetSmart (Argos Holding) Chewy E-commerce portal for the pet industry April 2017 $3.4Quinpario Acquisition Corp. Novitex Enterprise Solutions / Source HOV Outsourced IT services February 2017 $2.8Hellman & Friedman Fairfax Media Digitally progressive media company May 2017 $2.5Apollo Global Management West Corporation Customer care and telecom services May 2017 $2.0eBay; Microsoft; Tencent Holdings Flipkart Online Services Online shopping website April 2017 $1.4Oracle Moat SaaS analytics solutions April 2017 $0.9First Data CardConnect Payment processing solutions May 2017 $0.8Capitol Acquisition Corp. III Cision (GTCR) PR software March 2017 $0.8Harland Clarke (MacAndrews & Forbes) RetailMeNot Savings destination for online and instore purchases April 2017 $0.7Eurazeo; Goldman Sachs Dominion Web Solutions Digital marketing solutions May 2017 $0.7FleetCor Technologies Cambridge Global Payments Online payment solutions May 2017 $0.7Amazon Souq.com E-commerce platform March 2017 $0.7Apollo Global Management Mood Media Creative marketing solutions April 2017 $0.6

Client Briefing August 2017 | 5www.jegi.com

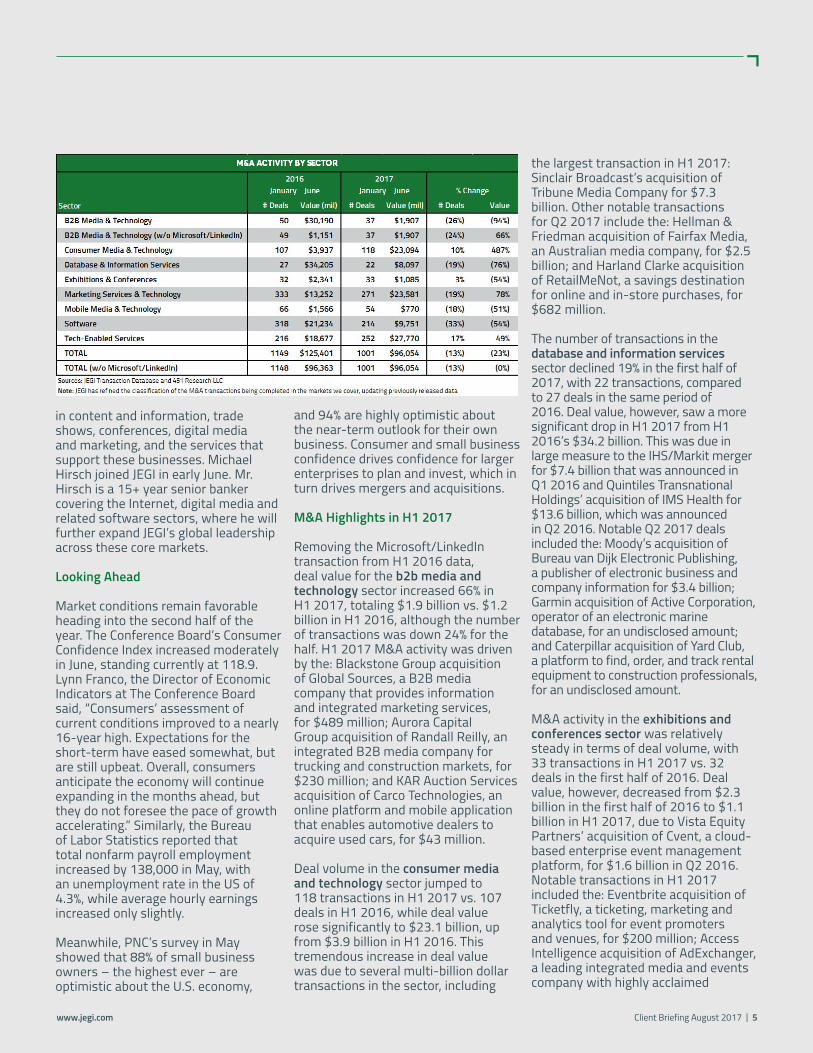

and 94% are highly optimistic about the near-term outlook for their own business. Consumer and small business confidence drives confidence for larger enterprises to plan and invest, which in turn drives mergers and acquisitions.

M&A Highlights in H1 2017

Removing the Microsoft/LinkedIn transaction from H1 2016 data, deal value for the b2b media and technology sector increased 66% in H1 2017, totaling $1.9 billion vs. $1.2 billion in H1 2016, although the number of transactions was down 24% for the half. H1 2017 M&A activity was driven by the: Blackstone Group acquisition of Global Sources, a B2B media company that provides information and integrated marketing services, for $489 million; Aurora Capital Group acquisition of Randall Reilly, an integrated B2B media company for trucking and construction markets, for $230 million; and KAR Auction Services acquisition of Carco Technologies, an online platform and mobile application that enables automotive dealers to acquire used cars, for $43 million.

Deal volume in the consumer media and technology sector jumped to 118 transactions in H1 2017 vs. 107 deals in H1 2016, while deal value rose significantly to $23.1 billion, up from $3.9 billion in H1 2016. This tremendous increase in deal value was due to several multi-billion dollar transactions in the sector, including

the largest transaction in H1 2017: Sinclair Broadcast’s acquisition of Tribune Media Company for $7.3 billion. Other notable transactions for Q2 2017 include the: Hellman & Friedman acquisition of Fairfax Media, an Australian media company, for $2.5 billion; and Harland Clarke acquisition of RetailMeNot, a savings destination for online and in-store purchases, for $682 million.

The number of transactions in the database and information services sector declined 19% in the first half of 2017, with 22 transactions, compared to 27 deals in the same period of 2016. Deal value, however, saw a more significant drop in H1 2017 from H1 2016’s $34.2 billion. This was due in large measure to the IHS/Markit merger for $7.4 billion that was announced in Q1 2016 and Quintiles Transnational Holdings’ acquisition of IMS Health for $13.6 billion, which was announced in Q2 2016. Notable Q2 2017 deals included the: Moody’s acquisition of Bureau van Dijk Electronic Publishing, a publisher of electronic business and company information for $3.4 billion; Garmin acquisition of Active Corporation, operator of an electronic marine database, for an undisclosed amount; and Caterpillar acquisition of Yard Club, a platform to find, order, and track rental equipment to construction professionals, for an undisclosed amount.

M&A activity in the exhibitions and conferences sector was relatively steady in terms of deal volume, with 33 transactions in H1 2017 vs. 32 deals in the first half of 2016. Deal value, however, decreased from $2.3 billion in the first half of 2016 to $1.1 billion in H1 2017, due to Vista Equity Partners’ acquisition of Cvent, a cloud-based enterprise event management platform, for $1.6 billion in Q2 2016. Notable transactions in H1 2017 included the: Eventbrite acquisition of Ticketfly, a ticketing, marketing and analytics tool for event promoters and venues, for $200 million; Access Intelligence acquisition of AdExchanger, a leading integrated media and events company with highly acclaimed

in content and information, trade shows, conferences, digital media and marketing, and the services that support these businesses. Michael Hirsch joined JEGI in early June. Mr. Hirsch is a 15+ year senior banker covering the Internet, digital media and related software sectors, where he will further expand JEGI’s global leadership across these core markets.

Looking Ahead

Market conditions remain favorable heading into the second half of the year. The Conference Board’s Consumer Confidence Index increased moderately in June, standing currently at 118.9. Lynn Franco, the Director of Economic Indicators at The Conference Board said, “Consumers’ assessment of current conditions improved to a nearly 16-year high. Expectations for the short-term have eased somewhat, but are still upbeat. Overall, consumers anticipate the economy will continue expanding in the months ahead, but they do not foresee the pace of growth accelerating.” Similarly, the Bureau of Labor Statistics reported that total nonfarm payroll employment increased by 138,000 in May, with an unemployment rate in the US of 4.3%, while average hourly earnings increased only slightly.

Meanwhile, PNC’s survey in May showed that 88% of small business owners – the highest ever – are optimistic about the U.S. economy,

6 | Client Briefing August 2017

conferences and media offerings, for an undisclosed sum; and HGGC acquisition of etouches, a leading provider of event management software in the cloud, for an undisclosed sum. JEGI represented AdExchanger and HGGC in the previously mentioned transactions.

The marketing services and technology sector continues to be very active, with 271 transactions accounting for $23.6 billion in value in H1 2017. Deal value increased more than 78% in H1 2017 over H1 2016, even though the number of deals decreased 19% for the sector in the first half of the year. Market research and consulting transactions accounted for 46% of deal value in the sector, with 40 deals worth nearly $11 billion. This sub-sector saw several multi-billion dollar deals including the: Pamplona Capital Management acquisition of PAREXEL International, a contract drug research organization, for $5.3 billion; and INC Research Holding acquisition of inVentiv Health, a provider of consulting services to pharmaceutical, biotechnology and healthcare industries worldwide, for $4.6 billion.

Agency deals accounted for just over 25% of deal value in the marketing services and technology sector, totalling roughly $6 billion for the first half of the year. The leading agency transaction in Q2 2017 was Vivendi’s

acquisition of Havas, provider of advertising, digital and communication services, for $3.4 billion.

Other notable transactions in Q1 2017 included the: Oracle acquisition of Moat, the SaaS analytics solution for brand advertisers and publishers, for $850 million; Wave Systems acquisition of Jive Software, a communication and collaboration solution that enhances marketing engagement and brand advocacy, for $462 million; Vector Capital acquisition of Experian’s Email and Cross-Channel Marketing Business, for $300 million; and Thales acquisition of Guavus, a big data analytics application for planning, operations, customer experience management and IOT, for $215 million.

M&A activity for the mobile media and technology sector declined in both deal volume and value in H2 2017, to 54 transactions and $770 million in value, compared to 66 deals and $1.6 billion in H1 2016. 2016 activity was driven by Microsoft’s $400 million acquisition of mobile application software developer Xamarin and several deals in the $50-100 million range. Notable Q2 2017 transactions included the: Sirius XM Holdings acquisition of Automatic Labs, operator of mobile phone based driver assist devices and applications, for $100 million; Quotient Technology

acquisition of Crisp Media, a mobile shopper activation company, for $57.2 million; and NextGen Healthcare Information Systems, a subsidiary of QSI, acquisition of Entrada, a leading provider of integrated mobile solutions that improve healthcare efficiencies and outcomes, for an undisclosed amount. JEGI represented Entrada in this transaction.

The software sector saw an approximate 33% decline in deal volume, with 214 transactions in H1 2017 vs. 318 in H1 2016. Deal value decreased as well, from $21.2 billion in H1 2016 to $9.8 billion in H1 2017. In Q2 2017, there were no $1+ billion transactions to offset the three $2+ billion transactions in Q2 2016. Notable deals in the second quarter of 2017 included the: Cisco Systems acquisition of Viptela, a WAN virtualization company, for $610 million; GTCR acquisition of Sage Payment Solutions, a provider of transaction procession software, SaaS and services, for $260 million; True Wind Capital Management acquisition of ARI Network Services, catalog management software and SaaS, for just over $130 million; and Francisco Partners acquisition of Insight Venture Partners portfolio company SmartBear Software, provider of application and API testing software, for an undisclosed amount.

The tech-enabled services sector led the first half of the year in terms of deal value, totaling $27.8 billion, up 49% over $18.7 billion from H1 2016. Deal volume also saw an uptick to 252 deals, compared to 216 in the same period of 2016. Notable transactions in Q2 2017 included the: Apollo Global Management acquisition of West Corporation, provider of customer care and telecom services for $2 billion; First Data acquisition of CardConnect, provider of payment processing solutions, for $769 million; FleetCor Technologies acquisition of Cambridge Global Payments, an online payment solutions provider, for $675 million; and Vista Equity Partners acquisition of Xactly, a cloud-based incentive compensation solution, for $577 million.

(from left) Michael Vaughan (Regis Company) , Jean-Marc Laouchez (Korn Ferry)

Client Briefing August 2017 | 7www.jegi.com

We analyzed trends in leadership skills over 10 years, and found that leaders are expected to learn upwards of 15 different competencies. Research tells us that we can only become proficient at two or three. Thus, there is a transition to looking at and measuring three core abilities: critical; creative; and systems thinking. Leadership development is becoming about teaching people how to learn: how to become better decision makers, problems solvers and collaborators.

Becker: How do you train and develop the next generation of leaders?

Vaughan: The hype around Millennials should actually be more about modality. Our needs are similar: be respected, add value and be viewed as adding value. How one learns might be different from the model – focus should be on the core of what a person needs rather than the age of that person. It’s about motivating people individually. We’re seeing a transformation in educating people on how to think, whether Millennials or Baby Boomers – learning how to learn, unlearn and relearn quickly; and learning how to think in ambiguous situations. We have been focusing on simulations for leaders, confronting them with business issues to see how they react, an approach that works across generations because it’s emotionally engaging and intellectually rigorous.

Laouchez: Many millennials are already leaders, and most Boomers will retire in the next 10 years. Millennials want respect, wellbeing and most importantly, they want purpose, which is why they must be involved in the solution. We need to recognize millennials are going to shape the way we will do business in the future. A blended learning process can help us guide them. Simulation is important, as is immersion into new experiences – observing how they think and act, then understanding their values and drivers. Now, we can look at their experiences, competencies, traits and personalities to understand who they really are and

LEADERSHIP & TALENT DEVELOPMENT FOR THE NEW ECONOMY (CONT.)

how they learn, so we can help them to be more effective.

Becker: How are you changing solutions and applying data to identify and develop talent and leaders?

Laouchez: A lot of activity formerly done by people is now done by systems, so leaders must decide whether to build a team or use an algorithm to solve a problem. This quickly emerging, fundamentally different way of operating an organization will impact the way we manage people and use analytics. Technology is being applied to everything across HCM – recruiting people, providing diagnostics on individual connectivity and engagement. This supports the learning process, as these diagnostics help us understand performance impact and promote progress, both for individuals and the organization.

Vaughan: Human intelligence is increasing, but artificial intelligence is surpassing it significantly. People in the field are nervous about this, but it’s led to some interesting approaches to human development. Cisco, for example, is discarding its learning and performance management systems, and putting people into situations to self-determine how they can add value to the organization. Look for platforms that emphasize the learning journey – assessments, simulations, classroom-style learning – all in one, so that data can be collected and compared against new AI tools. Platforms should also be open with APIs, a necessary part of the learning ecosystem in a digital world, to collect richer data sets.

Becker: Give us an example of these new approaches.

Laouchez: We are working on the concept of using data and analytics in the talent supply chain. In staffing a project, data can be used to ensure the right people are working on the right projects at the right cost. Over time, a learning process occurs, helping to optimize talent

management through an integrated link of what adds value for clients.

Vaughan: We are exploring how to ethically use simulations as a diagnostic tool in situations where companies are hiring people for the wrong positions and ultimately losing money. We have certain cases where this data helps people have self-generated insights, rather than simply measuring ability.

Becker: When are digital solutions more apropriate and when is face-to-face interaction still the best approach?

Vaughan: The issue right now is that we’re not sure what “digital” truly means. Are we throwing money into a digital market that’s really just a lot of consumption? Will it help us change our thinking and behaviors? We need to define digital and learn from the open-source community. In the learning space, we need an open-architecture ecosystem to make digital viable.

Laouchez: Strategically, humans have this untapped capability to use data and digital access to achieve full potential and make it available to whoever can use it. Therefore, there is a need to use digital transformation to service human beings in addition to finding talent to fulfill objectives, we should also determine how to fulfill objectives using the talent we have.

8 | Client Briefing August 2017

Wilma JordanFounder & [email protected]

Kathleen ThomasManaging [email protected]

Tolman [email protected]

Richard MeadManaging [email protected]

David ClarkManaging [email protected]

Jeff BeckerManaging [email protected]

Michael HirschManaging [email protected]

Sam BarthelmeManaging [email protected]

Adam [email protected]

Bill [email protected]

Amir AkhavanManaging [email protected]

Joseph SanbornManaging [email protected]

LONDONClarity, 90 Long Acre London WC2E 9RA +44 20 3402 4900 www.claritycp.com

NEW YORKJEGI,150 East 52nd Street18th FloorNew York, NY 10022 +1 212 754 0710 www.jegi.com

BOSTONJEGI, One Liberty Square11th FloorBoston, MA 02109+1 617 294 6555 www.jegi.com

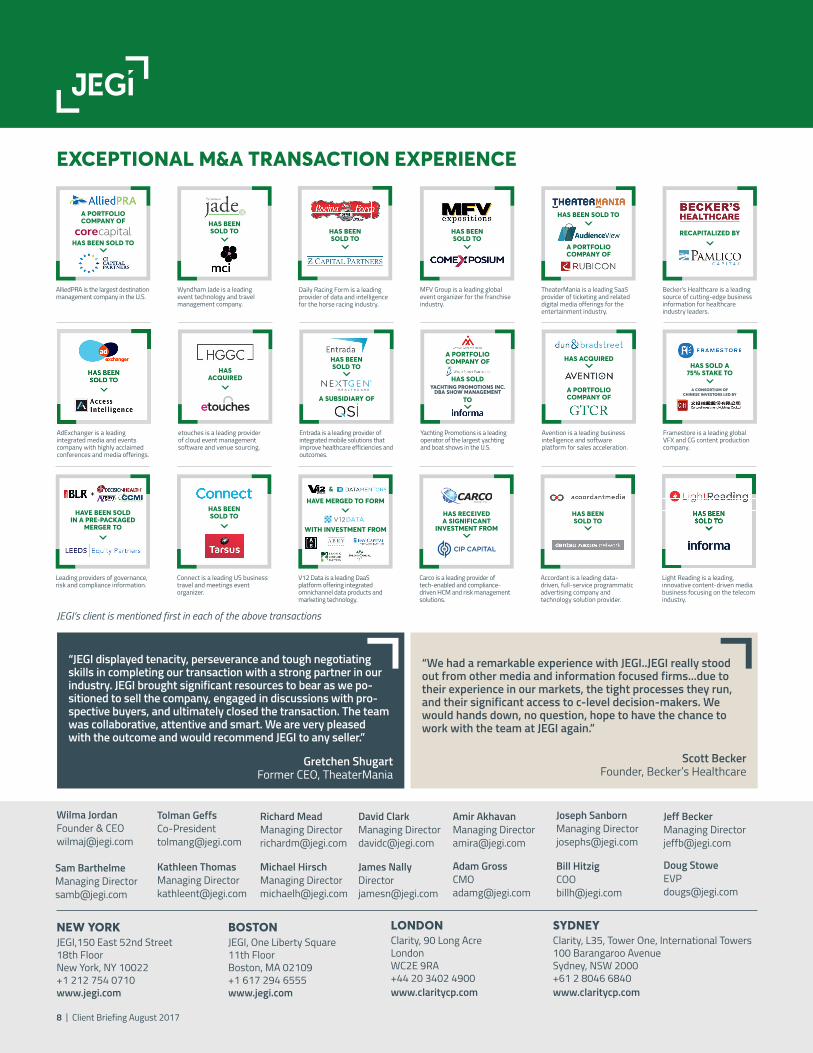

EXCEPTIONAL M&A TRANSACTION EXPERIENCE

JEGI’s client is mentioned first in each of the above transactions

Wyndham Jade is a leading event technology and travel management company.

HAS BEEN SOLD TO

etouches is a leading provider of cloud event management software and venue sourcing.

MFV Group is a leading global event organizer for the franchise industry.

TheaterMania is a leading SaaS provider of ticketing and related digital media offerings for the entertainment industry.

Becker’s Healthcare is a leading source of cutting-edge business information for healthcare industry leaders.

AdExchanger is a leading integrated media and events company with highly acclaimed conferences and media offerings.

HASACQUIRED

RECAPITALIZED BY

HAS BEEN SOLD TO

A PORTFOLIO COMPANY OF

HAS BEEN SOLD TO

Entrada is a leading provider of integrated mobile solutions that improve healthcare efficiencies and outcomes.

HAS BEEN SOLD TO

A SUBSIDIARY OF

Daily Racing Form is a leading provider of data and intelligence for the horse racing industry.

Framestore is a leading global VFX and CG content production company.

AlliedPRA is the largest destination management company in the U.S.

A PORTFOLIO COMPANY OF

HAS BEEN SOLD TO

Avention is a leading business intelligence and software platform for sales acceleration.

A PORTFOLIO COMPANY OF

HAS ACQUIRED

Yachting Promotions is a leading operator of the largest yachting and boat shows in the U.S.

A PORTFOLIO COMPANY OF

TO

HAS SOLDYACHTING PROMOTIONS INC.

DBA SHOW MANAGEMENT

HAS BEEN SOLD TO

HAS SOLD A 75% STAKE TO

A CONSORTIUM OFCHINESE INVESTORS LED BY

Doug [email protected]

“JEGI displayed tenacity, perseverance and tough negotiating skills in completing our transaction with a strong partner in our industry. JEGI brought significant resources to bear as we po-sitioned to sell the company, engaged in discussions with pro-spective buyers, and ultimately closed the transaction. The team was collaborative, attentive and smart. We are very pleased with the outcome and would recommend JEGI to any seller.”

Gretchen ShugartFormer CEO, TheaterMania

“We had a remarkable experience with JEGI..JEGI really stood out from other media and information focused firms...due to their experience in our markets, the tight processes they run, and their significant access to c-level decision-makers. We would hands down, no question, hope to have the chance to work with the team at JEGI again.”

Scott BeckerFounder, Becker’s Healthcare

James [email protected]

SYDNEYClarity, L35, Tower One, International Towers100 Barangaroo Avenue Sydney, NSW 2000 +61 2 8046 6840 www.claritycp.com

Connect is a leading US business travel and meetings event organizer.

Leading providers of governance, risk and compliance information.

HAS BEEN SOLD TOHAVE BEEN SOLD

IN A PRE-PACKAGEDMERGER TO

+

V12 Data is a leading DaaS platform offering integrated omnichannel data products and marketing technology.

&

HAVE MERGED TO FORM

WITH INVESTMENT FROM

Light Reading is a leading, innovative content-driven media business focusing on the telecom industry.

Accordant is a leading data-driven, full-service programmatic advertising company and technology solution provider.

HAS BEEN SOLD TO

Carco is a leading provider of tech-enabled and compliance-driven HCM and risk management solutions.

HAS RECEIVED A SIGNIFICANT

INVESTMENT FROM