August 2000 CONTENTS - WordPress.com NINL and KMCL are under advance stage of implementation. MMTC,...

22

1 A REPORT ON EXPORT POTENTIAL OF GRANITES (With Special Reference to Minerals and Metals Trading Corporation, Visakhapatnam) Submitted to GITAM Institute of Foreign Trade and MMTC, Visakhapatnam Date: 11 th August 2000 P. Vijay Kumar CONTENTS CHAPTER – 1 State Trading Rational of State Trading Canalization of Imports & Exports Need for the Study Objectives of the Study Methodology of the Study Limitations of the Study CHAPTER – 2 MMTC – Past, Present & Future CHAPTER – 3 Granites Granite Deposits in India Table of Granite Deposits in India Granites Belt in South India CHAPTER – 4 Dimensional stone Granite – Indian Scenario Granite Exports from India Granite Exports from Visakhapatnam Competition in the International Market Problems faced by the Granite Industry in India Future of the Granite Industry SUGGESTIONS AND CONCLUSION APPENDIX List of varieties of Rough Granite Blocks List of Granite Exports from India List of Granite Exports from Visakhapatnam List of Customers Abroad List of Machinery Suppliers

Transcript of August 2000 CONTENTS - WordPress.com NINL and KMCL are under advance stage of implementation. MMTC,...

1

A REPORT ON EXPORT POTENTIAL OF GRANITES

(With Special Reference to Minerals and Metals Trading Corporation, Visakhapatnam)

Submitted to GITAM Institute of Foreign Trade and MMTC, Visakhapatnam

Date: 11th August 2000

P. Vijay Kumar

CONTENTS

CHAPTER – 1 State Trading Rational of State Trading Canalization of Imports & Exports Need for the Study Objectives of the Study Methodology of the Study Limitations of the Study CHAPTER – 2 MMTC – Past, Present & Future CHAPTER – 3 Granites Granite Deposits in India Table of Granite Deposits in India Granites Belt in South India CHAPTER – 4 Dimensional stone Granite – Indian Scenario Granite Exports from India Granite Exports from Visakhapatnam Competition in the International Market Problems faced by the Granite Industry in India Future of the Granite Industry SUGGESTIONS AND CONCLUSION APPENDIX List of varieties of Rough Granite Blocks List of Granite Exports from India List of Granite Exports from Visakhapatnam List of Customers Abroad List of Machinery Suppliers

2

CHAPTER – 1 State Trading

here is no precise definition of state trading. There are various types of government participation in foreign trade, all of which can be defined as state trading. For example, in the centrally planned economies, the entire foreign

trade is nationalized and is, therefore, conducted directly by government departments or government owned corporations. On the other hand, there are countries, which are essentially free enterprise economies but export and import of specific commodities are entrusted to Government Trading Organizations or departments. For example, import of raw and unmanufactured tobacco is a state monopoly in France, the government food agency of Japan regulates the import, export and internal distribution of rice, wheat and barley, the Australian Wheat Board has the exclusive rights for export of wheat. There are many such instances all over the world. The third variety of state trading is found in mixed economies like India. In India, the role of state trading is coming down with the coming up of liberalized policies; private sector participation in gaining momentum day by day. The government’s own trading corporations are, however, commercial entities registered under the Companies Act and have the same rights and obligations as any private sector firms. There are a number of such government trading organisations. Rationale of State Trading State Trading is restored for a number of reasons. In the centrally planned economies, foreign trade as a matter of state policy is nationalised. Foreign trade in those countries is to be conducted by state trading organisations because otherwise the central planning mechanism will not function properly. In the developed free enterprise economies, state trading sometimes is practiced as a source of revenue. That is why it is found that trade in products like alcohol and tobacco is subject to state monopoly. Similarly, trade in drugs and arms and ammunition is managed through state bodies in the interest of health and national security of the country. State trading in a number of agricultural products is quite common because state intervention is necessary to avoid large fluctuations in the prices and preventing deteriorating in the income of the agricultural producers.

State trading, however, is more commonly practiced in the developing economies. The reason behind this are varied. First, such countries may not have adequately developed private sector trading bodies, which can effectively participate in international commercial, and also project the national interest.

Secondly, the private sector bodies, though possessing adequate trading

expertise, will be solely motivated by profit consideration. However, it may be necessary from the national standpoint to promote new export items and cultivate new export markets even by sustaining short-term losses. This can be done only by governmental bodies having a development role and which are backed by the government so that financial losses do not hamper the pursuit of long-term objectives.

T

3

Thirdly, the centrally planned economies have emerged as important export markets for a large number of developing countries including India. Since the foreign trade of these countries is invariably conducted through state trading organisations, it is found that government trading bodies are in a better position to negotiate with their counterparties in the centrally planned economies.

Canalisation of Imports and Exports State participation in imports is generally motivated by some other considerations. These are:

1. To reap the advantages of bulk buying 2. To mop up any excess profit which the private sector firms might enjoy in

import business, and 3. To ensure proper internal distribution of the imported items and to maintain

stable domestic prices. The basic objectives of state trading in exports are as follows:

1. It is observed in the case of certain products that there was secular decline in the total value of exports. It was thought that a government trading organisation would be able to reverse this trend by concerted action.

2. In some cases, the inner competition among the Indian exporters was resulting in lower unit value realisation, entry of state trading organisation in the international market through which exports were to be canalized could result in the improvement of unit value realization.

3. Canalisation was also thought of as an instrument to improve the bargaining power of Indian exporters.

The major state trading organisations in India are:

1. The State Trading Corporation Limited (STC) 2. The Projects and Equipment Corporation of India Limited (PEC) 3. The Minerals and Metals Trading Corporation Limited (MMTC) 4. The Mica Trading Corporation of India Limited (MITCO) 5. The Tea Trading Corporation of India (TTCI) 6. Spices Trading Corporation Limited

Need for the study In the recent past, granite industry has established itself as a major earner of foreign exchange for the country. The Indian granite has significant presence in the South East Asian countries and also some European countries., but the potential of this industry is much deeper than it is today.

The Indian granite industry has not performed to its expected levels because of lack of information regarding availability of machinery, buyer’s abroad and suppliers of raw blocks domestically. The study intends to explore the potential of granite

4

exports from India by finding out the suppliers in India and buyers abroad so as to bridge the gap of unavailability for information.

Objectives of the Study

1. To find out the location of granites in India 2. To find out the varieties of granites available in different states 3. To find out the problems faced by the industry 4. To find out the foreign buyers of granites 5. To find out the machinery suppliers for granite processing units

Methodology of the Study The sources from which the data was collected can be divided into two:

1. Primary sources 2. Secondary sources

1. Primary Sources: Data was collected by meeting persons directly and interviewing

them. Various department heads like the Dy. Director of A.P. Mines and Geology, Visakhapatnam, H.O.D. of Department of Geology, Andhra Pradesh, were contacted personally and their views were recorded for use in the study.

2. Secondary Sources: A major part of the information was collected from secondary sources like books, journals and reports (such as the perspective plan of Visakhapatnam Port Trust – 2020).

Limitations of the Study

1. A part of the information is not disclosed due to some organizational constraints.

2. Latest information regarding exports were not available 3. Because of the vastness of the subject, an in-depth study was not possible.

Granite being a minor export component in the total array of Indian exports, data relating to it was not available even with the concerned department.

5

CHAPTER – 2 MMTC – Past, Present and Future

MTC, started in 1963, as a small canalizing agency for minerals and metals. Today, it is amongst the first to be awarded “The Golden Super Star Trading House” status in India and stands as a pre-eminent corporate entity with an

annual turnover of about US $ 1.2 billion. The company’s diverse trade activities encompass third country trade, joint ventures, link deals, etc., all of which are modern day foals of international trading. Its vast international trade network, which includes a wholly owned international subsidiary in Singapore, as well as two international offices in Tokyo & Dubai, spans more than 85 countries in Asia, Europe, Africa, Oceania and America, giving MMTC a global market coverage. An integrated global trader with bulk handling capabilities: A comprehensive infrastructure for bulk cargo handling, well developed arrangements for rail and road transportation, warehousing, port and shipping operations given MMTC complete control over trade logistics for export and import of over 15 million tonnes of bulk products annually. MMTC’s core competencies are in the field of minerals, metals and fertilizers, precious metals, gems and jewelry and agro products. The company’s countrywide domestic network is spread over 85 regional, sub-regional, port and filed officers, warehouses and procurement centers. Broad based activities beyond trading: The process of liberalization in India has taken MMTC from monopoly status to a competitive open market player making a strong thrust towards broad basing its sphere of activities while consolidating its core areas of business. MMTC has diversified for value addition and synergies its core strength of Iron Ore operations with Iron and Steel production. A joint venture company of MMTC Limited, Neelachal Ispat Nigam Limited (NINL) is setting up an integrated steel plant for manufacture of 3,00,000 tpa of steel wire rods, 3,20,000 tpa of steel billets and 4,90,000 tpa of basic grade pig iron at Jajpur, Orissa, which is extremely rich in Iron ore reserves. The entire requirement of metallurgical coke of 5,70,000 tpa and a part of the power requirement of 362 million units per annum wil be met through Konark Met Coke Limited (KMCL), another joint venture company promoted by MMTC, which is setting up a coke oven plant adjacent to the integrated steel plant. Both NINL and KMCL are under advance stage of implementation. MMTC, with its vast experience is procuring, marketing and selling of various minerals, metals and other commodities in domestic and overseas markets, is the sole and exclusive agent for procurement of all raw materials and services for NINL and KMCL; as also the sole and exclusive agent for marketing and sale of all the products in India and abroad.

M

6

India’s leading exporter of Minerals: A major global player in the minerals trade, MMTC is the single largest exporter of minerals from India. With its comprehensive infrastructure expertise to handle bulk minerals, the company provides full logistics support from procurement, quality control to guaranteed timely deliveries of minerals from different ports, through a wide network of regional and port offices in India, as well as international subsidiary and foreign offices. Biggest Importer of Metals: MMTC is India’s largest seller of imported Non-ferrous metals such as Copper, Aluminum, Zinc, Lead, Tin, Nickel and other minor metals such as Magnesium, Antimony, Silicon and Mercury, as also industrial raw materials like Asbestos, Steel and its products. MMTC imports quality products conforming to international specifications like ASTIM, BSS or LME approved brands. MMTC source its metals from suppliers including producers and traders throughout the world. Largest buyer of Fertilizers: Being the world’s second largest importer of fertilizers and the largest in India, MMTC has become a major fertilizer marketing company in India, through planned forward integration of its import activities with the direct marketing of Urea, DAP, MOP, Sulphur, Rock Phosphate, SSP, Sulphuric Acid, Liquid Ammonia, Ammonium Sulphate, etc., and other farming and agricultural inputs. Largest Bullion trader in the Indian Sub-Continent: MMTC is India’s largest importer of precious metals like gold and silver, handling about 50 mt of gold and 400 mt of silver. The company has opened a retail jewelry showroom at Maker Bhavan in Mumbai selling hall marked gold and studded jewelry. MMTC also operates a Duty Free jewelry sales outlet in the departure lounge at the International Airport, Mumbai. The company has an in-house assay and hallmarking unit and a medallion manufacturing facility at New Delhi. MMTC organizes major jewelry exhibitions in India and abroad. Leading player in Agro products: India offers a wide variety of agricultural products. MMTC is amongst the leading Indian exporter and importer of Agro products like Rice, Wheat Flour, Soya meal, Pulses, Sugar, Processed Foods and plantation products like Tea, Coffee, Jute and other products. MMTC also undertakes extensive operations in oilseed extracts. It also trades in edible oils. Coal and Hydrocarbons – Growth Potential Area: As new measures in post liberalization era, MMTC is diversifying, establishing and expanding into new areas of core competencies in the area of Coal and Hydrocarbons and has already got a firm footing in these activities. MMTC is supplying thermal coal to state electricity boards and power utilities. To cater to the needs of power sector, MMTC is already importing steam coal. MMTC has plans to import, in the near future, coking coal and metallurgical coke to cater to the needs of steel sector. Other products include Sko, Furnace oil, Bitumen, Naptha, LPG, LSMS, etc.

7

General Trading: Other general commodities like textiles, mulberry raw silk, building materials like granite, sand stone, cement, clinker, marine products, chemicals, drugs and pharmaceuticals, software exports, processed foods, mica and mica products, engineering items are also handled by MMTC.

8

CHAPTER – 3 Granites – Introduction:

ranite is a hard, coarse-grained rock that makes up a large part of every continent. Granite consists chiefly of three minerals – quartz, alkali feldspar and plagioclase feldspar. These minerals make granite white, pink, or light

gray. Granite also consists of small amounts of dark-brown, dark-green or black minerals, such as horn-blende and biotite mica. The grains of the minerals in granite are so large that they can easily be distinguished. Many grains measure more than 0.5 centimeter width. The minerals in granite are interlocked like the pieces of a Jigsaw Puzzle. As a result, granite is a strong, durable rock useful in the construction of buildings. Most granite can withstand weathering for centuries and can be polished smooth, making it especially suitable for columns, tombstones and momentous. Geologists classify granite as an igneous rock. They have concluded that most granite is formed by a slow coding and crystallization of molten material called magma. This magma has the same chemical composition as granite. It forms from rock that melts 25 to 40 kilometers below the surface of continents. These rocks melt at temperatures between 6500c and 6000 C. The magma rises because it is lighter than the surrounding solid rocks. As the magma rises, it cools, most granite magma cools slowly enough to form coarse crystals and it solidifies below the earth’s surface. Sometimes granite magma erupts from volcanoes and cools too quickly to form large crystals. The resulting rock, called Rhyolite, has the same mineral composition as granite but is fine grained. Experiments have shown that many kinds of rocks yield granite when they melt. Rocks melt in stages, and the minerals that form granite melt first, one of the reasons that granite is so abundant may be the ease with which granite magma forms. The continents consist largely of granite buried under sedimentary rock. Most granite appears where deeply buried rocks are brought to the surface of the earth by mountain building movements in the earth crust. Erosion removes the upper part of the mountains, exposing the granite under earth.

G

9

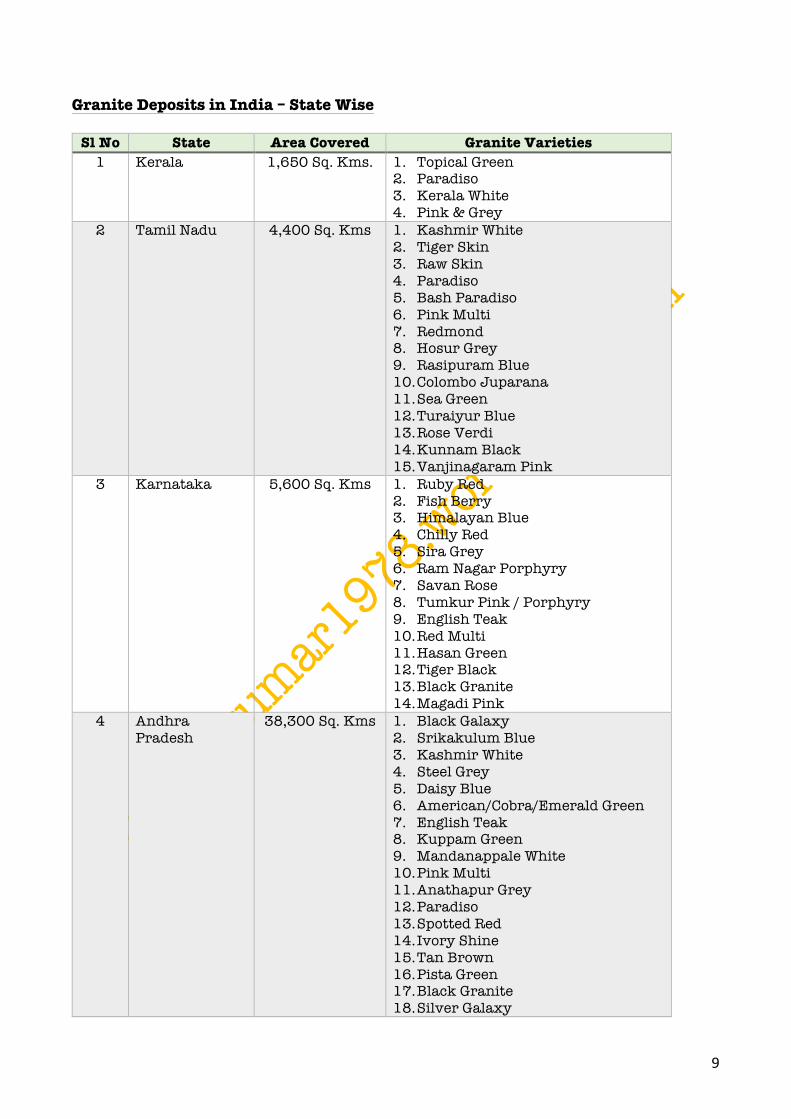

Granite Deposits in India – State Wise

Sl No State Area Covered Granite Varieties 1 Kerala 1,650 Sq. Kms.

1. Topical Green 2. Paradiso 3. Kerala White 4. Pink & Grey

2 Tamil Nadu 4,400 Sq. Kms

1. Kashmir White 2. Tiger Skin 3. Raw Skin 4. Paradiso 5. Bash Paradiso 6. Pink Multi 7. Redmond 8. Hosur Grey 9. Rasipuram Blue 10. Colombo Juparana 11. Sea Green 12. Turaiyur Blue 13. Rose Verdi 14. Kunnam Black 15. Vanjinagaram Pink

3 Karnataka 5,600 Sq. Kms 1. Ruby Red 2. Fish Berry 3. Himalayan Blue 4. Chilly Red 5. Sira Grey 6. Ram Nagar Porphyry 7. Savan Rose 8. Tumkur Pink / Porphyry 9. English Teak 10. Red Multi 11. Hasan Green 12. Tiger Black 13. Black Granite 14. Magadi Pink

4 Andhra Pradesh

38,300 Sq. Kms 1. Black Galaxy 2. Srikakulum Blue 3. Kashmir White 4. Steel Grey 5. Daisy Blue 6. American/Cobra/Emerald Green 7. English Teak 8. Kuppam Green 9. Mandanappale White 10. Pink Multi 11. Anathapur Grey 12. Paradiso 13. Spotted Red 14. Ivory Shine 15. Tan Brown 16. Pista Green 17. Black Granite 18. Silver Galaxy

10

5 Maharashtra 3,685 Sq. Kms 1. Grey Silk 2. Light Pink 3. Jhansi Red

6 Madhya Pradesh

6,720 Sq. Kms 1. Black Granite 2. Multicoloured Granite

7 Gujarat 812 Sq. Kms 1. Sonawadi Grey 2. Balaram Pink 3. Ajapur Galaxy 4. Chhapara Grey 5. Godh Grey 6. Dhori Pink 7. Khaleda Pink 8. Maharaja Tiger Black 9. Vaghor Grey

8 Rajasthan 30,000 Sq. Kms 1. Mokalsar Green 2. Nagina Green 3. Rasy Pink 4. Yellow Galaxy 5. Grey Granite 6. Blue Pearl 7. China Pink

9 Orissa 1,250 Sq. Kms 1. Berhampur Blue 2. Pink Granite 3. Silver Grey 4. Seaweed Green 5. Chilika Blue 6. Grey Ware 7. Red Pearl 8. Jeypore Black 9. Keonjhar Black

10 West Bengal 1,250 Sq. Kms 1. Bero Pink Porphyry 2. Spotty Ribbon Gneiss 3. Purulia Black 4. Chocolate Brown 5. Birbhum Pink 6. Spotty Black

11 Bihar 2,235 Sq. Kms 1. Tiger Skin 2. Mayurakshi Blue 3. Sawan Rose 4. English Teak 5. Black Granite (Black Chitah and

Black Zebra) 12 Uttar Pradesh 3,100 Sq. Kms 1. Ruby Red

2. Jhansi Red 3. Grey Granite 4. Black Granite

13 Haryana 105 Sq. Kms 1. Steel Grey 2. Porphyry Grey 3. Pink Granite 4. Deep Pink Granite 5. Purplish Granite Porphyry 6. Pink Porphyritic Granite

11

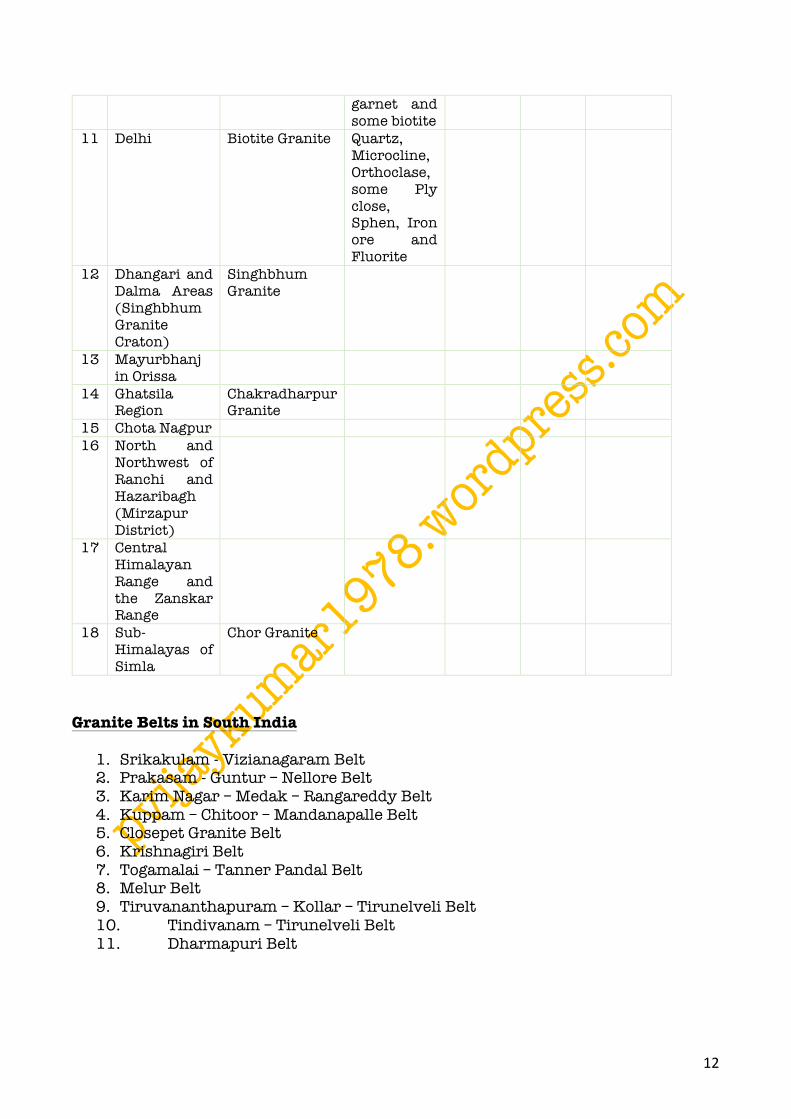

Granite Deposits in India – Block Wise

Sl No

Region Granite Name Mineral Content

Colour Area Features (if any)

1 N-S Band (N.N.W – S.S.E)

Closepet Granite

Quartz & Feldspar

Grey & Pink

15-25 Kms Width

Contains large amounts of feldspar

2 Western Regions (Vijayan Series) near Rajasthan

Tongala Granite Or Microdine Granite

Feldspar, Manazite, Torianite, Quartz, etc.

Pink Microdine being biotite-horn-blende gneisses of grade

3 Travancore and Tirunelveli

Microdine Granite

Quartz, Feldspar, Monazite, Thorinite, etc.

4 Berach Valley (between Chitoor and Bilwara)

Quartz, Orthoclase, Subordinate Microcline and a little of ferro Magnesian minerals

Pink to Reddish

10 miles long

Medium grained, non-faliated, non- porphyite granite

5 Alwar 6 Godhwar in

Jodhpur Hornblende Granite

Other names of the granites in this region are: Idar Granite, Jalor Granite and Siwani Granite

7 Sarangwa Quarries

More than 1.6 Kms long

8 Rajsamand 9 Jahazpur and

Sabalpura

10 Chilika Catchment in Orissa

Quartz with feldspar,

12

garnet and some biotite

11 Delhi Biotite Granite Quartz, Microcline, Orthoclase, some Ply close, Sphen, Iron ore and Fluorite

12 Dhangari and Dalma Areas (Singhbhum Granite Craton)

Singhbhum Granite

13 Mayurbhanj in Orissa

14 Ghatsila Region

Chakradharpur Granite

15 Chota Nagpur 16 North and

Northwest of Ranchi and Hazaribagh (Mirzapur District)

17 Central Himalayan Range and the Zanskar Range

18 Sub-Himalayas of Simla

Chor Granite

Granite Belts in South India

1. Srikakulam - Vizianagaram Belt 2. Prakasam - Guntur – Nellore Belt 3. Karim Nagar – Medak – Rangareddy Belt 4. Kuppam – Chitoor – Mandanapalle Belt 5. Closepet Granite Belt 6. Krishnagiri Belt 7. Togamalai – Tanner Pandal Belt 8. Melur Belt 9. Tiruvananthapuram – Kollar – Tirunelveli Belt 10. Tindivanam – Tirunelveli Belt 11. Dharmapuri Belt

13

CHAPTER – 4 Dimension Stone Granite – Indian Scenario

ndia, with an estimated resource of about 10,27,421 million cubic metres comprising over 160 shades of DSG, accounts for about 25% of the world’s granite reserves. Off the 300 varieties being traded in the world markets, nearly half of

them are from India. Commercially viable granite deposits are reported from A.P., Bihar, Gujurat, Karnataka, Madhya Pradesh, Maharashtra, Orissa, Rajasthan, Tamil Nadu, Uttar Pradesh and West Bengal. The industry is composed of the following four types of units.

1. Mining units 2. Polishing or Processing units 3. Exporting units 4. Manufacture of artifacts

The mining units are mainly located in the states of A.P., Karnataka, Tamil Nadu and Rajasthan. These units are operating under the purview of their respective state government department of mines and geology. The main activity of these units is to make raw granite blocks of various sizes depending upon the order placed by the other types of units – i.e. polishing units, export units or manufacturing of artifact units. The polishing units are also located mainly in the above mentioned states. These are mainly Export Oriented Units (EOUs) or units in Export Processing Zones (EPZs). These units buy raw granite blocks from the mining units and polish them. In the recent past these units have entered into many joint ventures and collaborations with foreign importers and polishing units located in foreign countries for supply of polishing machines. The cost of setting up a sophisticated state of the art granite polishing unit is nearly Rs. 65 million (Rs. 6.5 Crores). The exporting units are mainly concentrated near the port towns and cities. These units get orders from the buyers abroad and then procure granite domestically and export them to the buyers’ country. In India, there are numerous granite exporting units. These units are small in size and operations. They deal mainly with a particular kind of granite or granites. Granite blocks can be processed to be formed into various artifacts such as Elevation Pillars, Railing Pillars, Granite Cutlery, Monuments, Flower vases, Pedestals, Telephone Tables, etc. These artifacts are very attractive and are in great demand in the European countries. In India, a small number of firms are engaged in manufacture and trading of artifacts. Granite Exports from India The first export of granite (Black Granite) from India dates back to 1925 from Kuppam, Chitoor District, Andhra Pradesh to the United Kingdom for use as a

I

14

tombstone. Since then the Industry has made rapid strides, and today India ranks fifth in the world production of raw granite blocks and third in the export of the finished products. Indian granite exports are 40% to Japan, 39% to European countries, 7% to U.S.A., and the rest to other countries. During 1996-97, the granite industry earned Rs. 1,139 Crores against a production of 13,50,000 tonnes constituting 31.7% of the total world production. The exports registered an increase in 97-98 and stood at Rs. 1,468 Crores. Presently, there are about 200 export oriented grate cutting and polishing units and over 2,000 small-scale units spread over India. Exports of Granite Blocks from Visakhapatnam Port

Year Quantity (Metric Tonnes) Value (In Rs. Crores) 1992-93 12,252 N.A. 1993-94 53,964 N.A. 1994-95 64,723 N.A. 1995-96 85,189 N.A. 1996-97 75,315 N.A. 1997-98 65,171 46.80 1998-99 1,01,403 57.78

N.A. = Not Available Competition in the International Market The competition in the international market is intense. The competition for Indian granites is from countries such as Taiwan, Korea, Spain, South Africa, China, Thailand, Iran and Turkey. The units in these countries have huge capacities for processing granites, which helps reduce their cost of production, which in turn helps them to price their products cheaper than Indian exporters. This has led to fall in international market prices. The units in India are small and therefore are unable to reap the economies of scale. The domestic units do not have the resources to build brands or innovate new designs; this has led us to be recognized in the international market as only exporters of raw blocks rather than exporter of value-added products. Problems faced by the Granite Industry in India In the recent years, the granite industry in India has been facing severe problems. The performance of the export oriented undertakings (EOUs) of the granite industry has fallen short of expectations and unless measures are taken to infuse confidence and credibility in them in time, the industry will be plunged into deep crisis. The EOU scheme was ushered in with a view to encourage manufacturing of a range of quality products and to generate employment opportunities, policy changes at macro level

15

and procedural simplifications at the micro level were brought about to meet the goals. The growth of the granite EOUs was mostly between 1990 and 1996 and it was confined to Andhra Pradesh, Tamil Nadu and Karnataka. EOUs have provided better linkages with the domestic economy in terms of use of raw material and attracting FDI and sub-contracting. In the liberalized scenario, new schemes with extended benefits of duty-free imports appear to have diluted the attraction to EOUs. These and a host of other factors have affected the growth of the granite industry. Though the market for granite products abroad has registered an annual growth of 8 percent, the majority of the 100 percent granite EOUs, which went public, have not performed to expected levels. The reasons for non-performance have been mainly related to finance non-availability of quality raw blocks, fall in international prices and others. The granite industry in the country comprise the segment of rough blocks and value added products. Inadequate working capital has hit the majority of units, forcing them to work at reduced capacity. The granite trade operates largely on credit terms, which could be smooth only when there as adequate working capital. The interest burden also has added to the woes of the industry, rendering the products costly in comparison with international prices offered by countries having cheaper credit facilities. When the export of value added products was conceived, availability of raw material in sufficient quantities was envisaged. But the suppliers (quarry owners) of raw blocks preferred to export them to avail themselves of tax exemptions under Section 80 HHC as also to get assured payments. The situation rendered the availability of raw blocks for EOUs hitting their delivery schedules. The recent growth in competition from countries such as Taiwan, Korea, Spain, South Korea, China, Thailand, Iran and Turkey, which have huge capacities for processed granite has led to fall in international market prices. In addition, the small and medium domestic units, due to their low production costs, could export at a lesser price upsetting the position of 100 percent EOUs. Indian granite has substantial presence in South-East Asia, but the economic crisis in the region has hit demand. While foreign importers of raw blocks manager to get good quality materials, the local EOUs are starred of them. They also have to pay higher prices even for the material rejected by the importers. With competition remaining the driving force, the mineral development corporations of the State Government preferred to sell large size blocks to foreign customers. Since granite is a minor mineral, there is no uniform national policy, resulting in serious problems in procurement and movement of rough granite blocks from one state to another. The commerce ministry, on its part, has to establish linkages of rough granite blocks with export of products by processing units to ease matters. In the given circumstance, the industry wants the Government to reduce its export commitment for the next five years to achieve levels. The quarry leases need to be liberalized giving preference to 100 percent EOUs. Extension of tax exemptions under Section 80 HHC for the supply of raw blocks to EOUs, meeting of working capital requirement in full through revised norms and exemptions of EOUs from sales and turnover taxes for purchases made within the state are among the demands of the industry. The industry also needs website facilities for all EOUs as a promotional tool for the international market.

16

Future of the Granite Industry The future of the granite industry is bright provided the government takes necessary steps to boost exports. This optimism is based on the fact that nearly one-fourth of the granite reserves in the world are found in India and of the 300 varieties traded in the world 160 varieties are from India. The problem of non-performance by the industry is due to the lack of coordination among the various types of units (i.e. quarrying, polishing and manufacture of artifacts). These units are very small in size and operations. They do not have the necessary resources to pursue long-term strategies of brand building and exporting into new markets. The degree of innovation is also very less in India. The domestic granite industry, which is off-late showing interest to improve its image in the international market, has sought for the creation of a special fund for technological improvement of mining operations so that the current recovery of 5 to 10 percent can be increased to 25 percent. The granite industry felt that the technological upgradation was feasible only with access to machinery and tools which were available abroad. Now the government has permitted the 100 percent EOUs to import machines, tools and consumables to enable value addition. The present production can be doubled automatically with just one-time capital investment on machines and equipment. The industry has also pleaded for a uniform competitive royalty rates throughout the country. Another is the dead rent factor which the industry feels to be unreasonably high for the granite sector. But the above problems are likely to be solved by the recent formation of Granite Development Council. The government has established granite Development Council with representative from Industry and Government officials, with the aim to increase the exports to Rs. 2,000 crores. The Development Council decided to formulate a long-term approach for the next 20 years and evolve a national policy on Granites.

17

SUGGESTIONS AND CONCLUSION

rade in Granites is lucrative, and India has the comparative advantage in trading in Granites, because of its vast endowment of granite reserves. Since Granites are in great demand in the European Countries and also in the Middle

East, export of granites is attractive. This can be seen from the following calculations given below: -

Particulars Amount (Rs.)

Amount (Rs.)

Selling price of a tile of 1’ X 1’ of 10 mm thickness in International market

($ 4 per unit X 15,00,000 Units X Rs. 44/-)

Exchange rate between USD/INR = Rs. 44/-

26,40,00,000

Less: Cost price of a tile of 1’ X 1’ of 10 mm thickness in India

(Rs. 123 per unit X Rs. 15,00,000 Units)

18,45,00,000

Add: Port charges

(US $ 0.2187 X 2 X 3,000 X 44)

57,736

Add: Pilotage charges

(US $ 0.315 X 2 X 3,000 X 44)

83,160

Add: Wharfage charges

(32 X 30,00,000/1,000)

96,000

Add: Berth charges

(US $ 0.13618 X 44 X 3,000)

18,000

Add: Finance charges

46,12,500

Add: Transport, Admin & Miscellaneous costs 25,00,000 Total Cost 19,18,67,396

Profit 7,21,32,604 Note:

1. The calculations do not include the wagon hire charges from the supplier’s place to Visakhapatnam Port.

2. The calculation does not include the C&F agents fee, Customs duty payable at the port of shipment, freight charges payable to the Shippers.

3. The calculations are made assuming that the price quoted is under CFR terms. 4. The calculations are made assuming that the USD/INR rate is Rs. 44/- 5. The domestic selling price quote is the price of Galaxy variety of granite of

Srikakulam. 6. The approximate weight of a 1’ x 1’ tile is assumed to be 2 Kgs.

T

18

7. For a better understanding of the calculations made above, see the list of charges given in the Appendix.

MMTC with its solid infrastructure, efficient manpower and vast exposure to international markets is best suited to enter this business. It can also act as a link between the domestic suppliers and the foreign buyers by exporting on behalf of the supplier for commission. Both of these activities are going to bring additional revenue to MMTC with less cost and effort. Srikakulam, the largest granite belt in Andhra Pradesh, being near Visakhapatnam provides an excellent opportunity to source Granites. Srikakulam is endowed with wide varieties of granites and there are a number of small scale firms which are involved in mining and polishing of granites in this region. Considering the above, export of granites is a business which, I think, MMTC Visakhapatnam should include in its portfolio of trading.

19

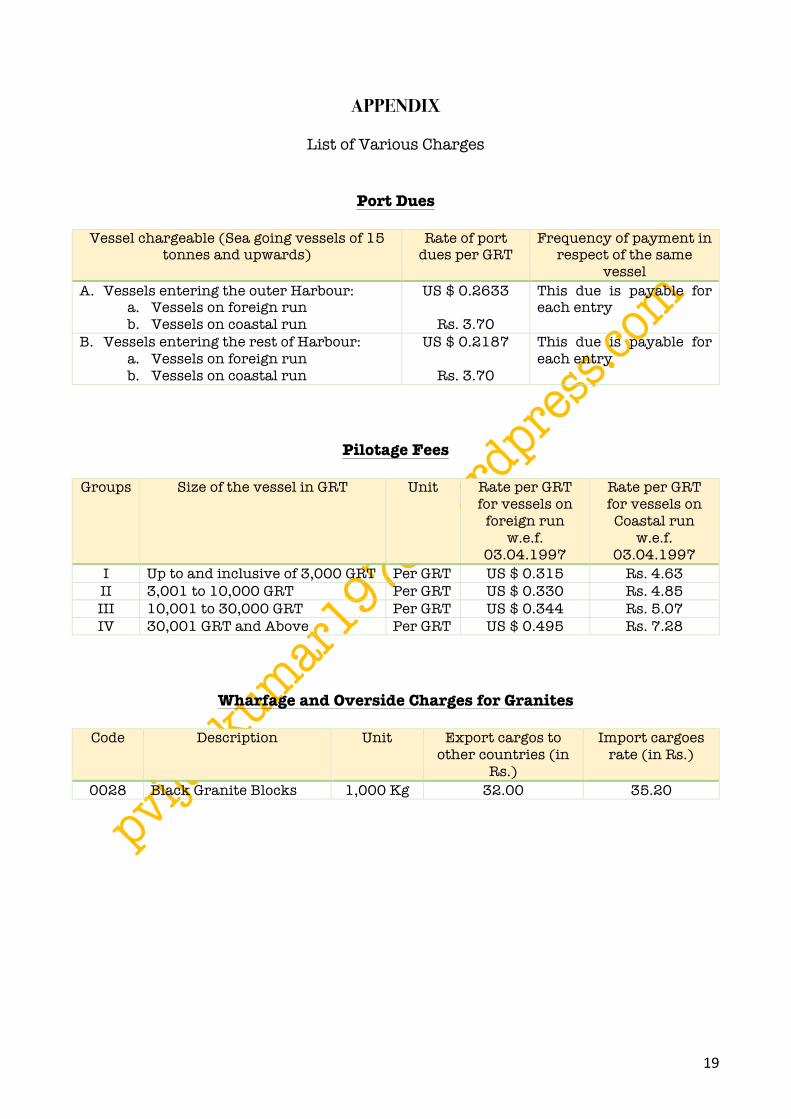

APPENDIX

List of Various Charges

Port Dues

Vessel chargeable (Sea going vessels of 15 tonnes and upwards)

Rate of port dues per GRT

Frequency of payment in respect of the same

vessel A. Vessels entering the outer Harbour:

a. Vessels on foreign run b. Vessels on coastal run

US $ 0.2633

Rs. 3.70

This due is payable for each entry

B. Vessels entering the rest of Harbour: a. Vessels on foreign run b. Vessels on coastal run

US $ 0.2187

Rs. 3.70

This due is payable for each entry

Pilotage Fees

Groups Size of the vessel in GRT Unit Rate per GRT for vessels on

foreign run w.e.f.

03.04.1997

Rate per GRT for vessels on

Coastal run w.e.f.

03.04.1997 I Up to and inclusive of 3,000 GRT Per GRT US $ 0.315 Rs. 4.63 II 3,001 to 10,000 GRT Per GRT US $ 0.330 Rs. 4.85 III 10,001 to 30,000 GRT Per GRT US $ 0.344 Rs. 5.07 IV 30,001 GRT and Above Per GRT US $ 0.495 Rs. 7.28

Wharfage and Overside Charges for Granites

Code Description Unit Export cargos to other countries (in

Rs.)

Import cargoes rate (in Rs.)

0028 Black Granite Blocks 1,000 Kg 32.00 35.20

20

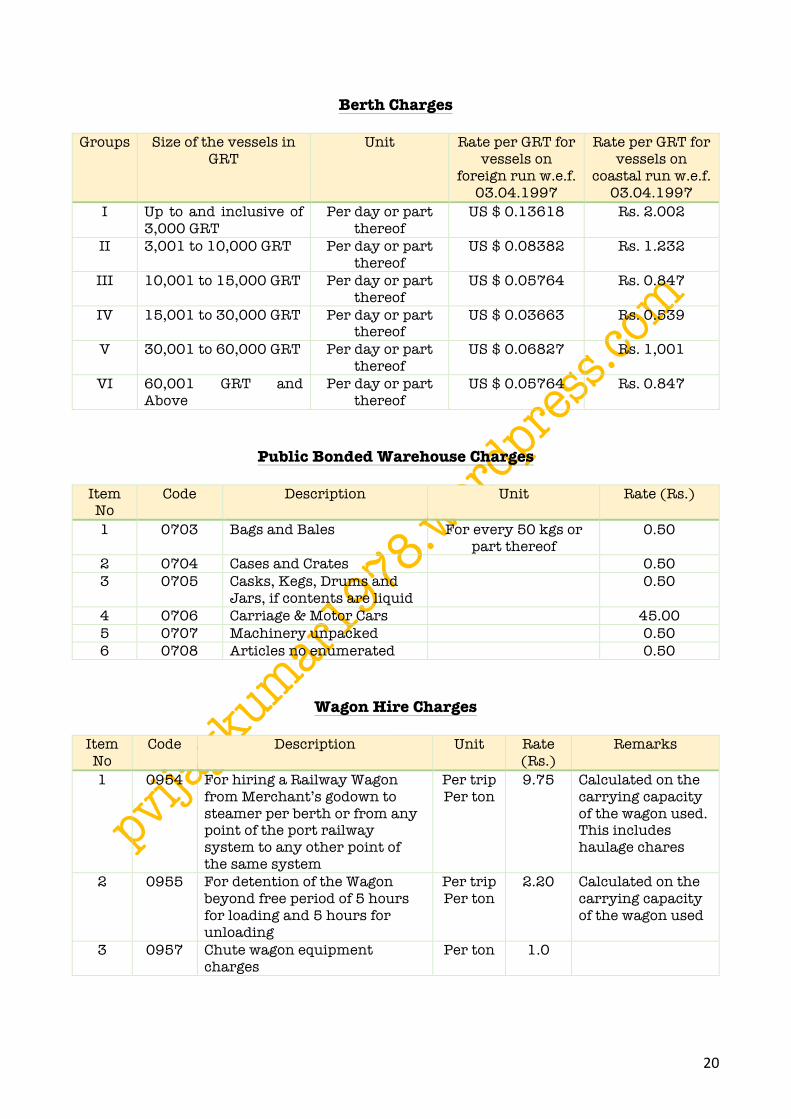

Berth Charges

Groups Size of the vessels in GRT

Unit Rate per GRT for vessels on

foreign run w.e.f. 03.04.1997

Rate per GRT for vessels on

coastal run w.e.f. 03.04.1997

I Up to and inclusive of 3,000 GRT

Per day or part thereof

US $ 0.13618 Rs. 2.002

II 3,001 to 10,000 GRT Per day or part thereof

US $ 0.08382 Rs. 1.232

III 10,001 to 15,000 GRT Per day or part thereof

US $ 0.05764 Rs. 0.847

IV 15,001 to 30,000 GRT Per day or part thereof

US $ 0.03663 Rs. 0.539

V 30,001 to 60,000 GRT Per day or part thereof

US $ 0.06827 Rs. 1,001

VI 60,001 GRT and Above

Per day or part thereof

US $ 0.05764 Rs. 0.847

Public Bonded Warehouse Charges

Item No

Code Description Unit Rate (Rs.)

1 0703 Bags and Bales For every 50 kgs or part thereof

0.50

2 0704 Cases and Crates 0.50 3 0705 Casks, Kegs, Drums and

Jars, if contents are liquid 0.50

4 0706 Carriage & Motor Cars 45.00 5 0707 Machinery unpacked 0.50 6 0708 Articles no enumerated 0.50

Wagon Hire Charges

Item No

Code Description Unit Rate (Rs.)

Remarks

1 0954 For hiring a Railway Wagon from Merchant’s godown to steamer per berth or from any point of the port railway system to any other point of the same system

Per trip Per ton

9.75 Calculated on the carrying capacity of the wagon used. This includes haulage chares

2 0955 For detention of the Wagon beyond free period of 5 hours for loading and 5 hours for unloading

Per trip Per ton

2.20 Calculated on the carrying capacity of the wagon used

3 0957 Chute wagon equipment charges

Per ton 1.0

21

List of Varieties of Rough Granite Blocks

Red Granites Multi-Colour Granites Blue Granites 1. Ruby Red 2. Sentinal Red 3. BMS Red 4. N.K. Red 5. BDG Red 6. Shahpur Red 7. Jhansi Red 8. K.R. Red 9. Jasmine Red

1. Kanakapura Multi-colour

2. Jupurna 3. Paradiso 4. Colombo Jupurna 5. Bash Paradiso 6. Red Multicolour 7. Sira Multicolour

1. Himalayan Blue 2. Vizag Blue 3. Arya Blue

Porphyry Granites Green Granites White Granites 1. Tumkur Pink 2. Green Rose 3. Queen Rose

1. Tropical Green (Dark Light)

2. Hassan Green 3. Sea Weed Green

1. White Galaxy 2. Kashmir White 3. Viscon White 4. Yedapadi White 5. Madanapalli White

Grey Granites Black Granites Yellow Granites 1. Sira Grey 2. Fish Belly Grey 3. Santhekalhalli Grey 4. Grey Galaxy

1. Black Galaxy 2. G-20 Black 3. Tiger Black 4. Warangal Black 5. Chamarajanagar Black 6. Kunnam Black

1. Sivakasi Yellow 2. Tiruvanamal Yellow

Other Granites 1. Indian Mahagony 2. Tiger Skin 3. Raw Skin 4. Diana Pink 5. Star Ruby (Cat’s Eye)

22

List of Granite Exporters from Vizag

1. M/s. Kunnam Granite Works 2. M/s. Sireesha Granites 3. M/s. Enterprising Enterprises 4. M/s. Apex Granite Exports 5. M/s. Hindustan Granites 6. Sree Venkateshwara Exports 7. M/s. Himalaya Granites 8. M/s. Ajay Mining Company 9. M/s. Primus Exports

List of Customers Abroad

1. Orient Sangyo Kaisha Ltd., Japan 2. Nissho Iwai Corporation Ltd., Japan 3. Mitsubishi Corporation Ltd., Japan 4. Marble Corporation, Japan 5. TAC Corporation, Japan 6. Magti Marble and Granite Trading Inc., Italy 7. Naturtein Verkaufs Gmbh, Germany 8. Cosmic Granites and Marbles Inc., USA 9. Stalian Impex (USA) Inc., USA 10. Kurz Natursteine Gmbh, Germany 11. Kreuzert Boemringer Gmbh, Germany 12. Selerie De la Lessee, Belgium 13. Branch Hot Hermant N.V. Belgium

List of Machinery Suppliers

1. Hensel Bayreuth, Germany 2. Fickert & Winterling, Germany 3. Ferriera Di Citadella 4. Wheel Abarator Allevard, France 5. Fabio Murga, Spain 6. Samick International Industries Co. Ltd., Korea 7. Diamant Boart, Italy 8. Italdimant, Italy 9. Toolgal Degania, Israel 10. Luna Abrasives, Italy

####### END OF REPORT #######