Auditor Change During Listings: Effect on IPO Premiums PAPERS/JSSH Vol. 9 (2) Sep. 2001... ·...

9

PertanikaJ. Soc. Sci. & Hum. 9(2): 113- 121 (2001) ISSN: 0128-7702 © Universiti Putra Malaysia Press Auditor Change During Listings: Effect on IPO Premiums SHAMSHER MOHAMAD & HUSON JOHER Department of Accounting & Finance Faculty of Economics and Management Universiti Putra Malaysia 43400 UPM Serdang, Selangor Keywords: Audit quality, IPO Premium, ex-ante uncertainty ABSTRAK Kajian ini meneliti kaitan antara pulangan awal yang diperolehi dari penyenaraian syarikat di papan pertama dan kedua Bursa Saham Kuala Lumpur (BSKL) dengan syarikat audit yang digunakan dalam penyiapan dan penyemakan prospektus syarikat yang disenaraikan. Syarikat audit dibahagikan kepada dua kumpulan, iaitu syarikat yang ternama (Tier 1) dan syarikat yang tidak ternama (Bukan Tier 1). Diandaikan bahawa syarikat audit yang ternama akan memberi perkhidmatan audit yang berkualiti dan ini dapat mengurangkan tahap ketakpastian pelabur terhadap potensi syarikat yang hendak disenaraikan. Ini menyebabkan pulangan awal dari penyenaraian adalah lebih rendah jika dibandingkan dengan pulangan awal dari syarikat yang menggunakan perkidmatan audit dari syarikat audit yang tidak ternama. Penemuan kajian atas 213 syarikat yang disenaraikan di BSKL menunjukkan memang ada kecenderungan firma-firma yang hendak menyenaraikan saham-sahamnya di BSKL untuk menggunakan perkhimatan syarikat- syarikat audit yang ternama. Tidak terdapat perbezaan yang signifikan antara pulangan awal dari penyenaraian oleh syarikat yang menggunakan perkhidmatan syarikat audit yang ternama dengan yang tidak ternama. Walau bagaimanapun, pulangan awal syarikat-syarikat yang disenaraikan di papan kedua jauh lebih tinggi dari pulangan awal dari syarikat yang disenaraikan di papan pertama BSKL. Penemuan ini menunjukkan reputasi syarikat audit (iaitu sama ada ternama atau tidak) tidak berperanan sebagai penentu pulangan awal semasa penyenaraian. Penemuan ini secara keseluruhannya adalah tekal dengan penemuan daripada kajian yang lain (Shamsher 8c Annuar 1997) yang menunjukkan bahawa pelabur di BSKL tidak membezakan kualiti perkhidmatan audit yang diberikan oleh syarikat-syarikat audit yang ternama dan yang tidak ternama. ABSTRACT The study examined the relationship between choice of quality differentiated audit firm and initial return at listing. It is conjectured that the superior audit quality of Tier 1 audit firms helps to reduce ex-ante uncertainty and consequently reduces the initial premiums at listing. The findings show that there is an inclination for listed firms to engage Tier 1 audit firms, and no significant difference in the initial returns of IPOs firms audited by either Tier 1 or Non-Tier I audit firms were observed. However, higher significant initial returns for new issues were observed for Second Board firms relative to Main Board firms. The findings do not appear to suggest that the auditor reputation is a determinant of initial returns at listing. The findings are consistent with those documented by Shamsher and Annuar (1997) that investors are indifferent to the quality of audit service provided by Tier 1 and Non-Tier 1 audit firms. INTRODUCTION The change of auditors prior to listing has been an issue of interest among academics, investors, and management in developed economies due to its effect on underpricing or overpricing of the new issue. It is a statutory requirement in Malaysia for every company that goes public to engage the services of merchant banks to help them get listed. In the process, the companies are required to provide prospectus audited by independent auditors to verify the statements as being true and fair view of the company. The

Transcript of Auditor Change During Listings: Effect on IPO Premiums PAPERS/JSSH Vol. 9 (2) Sep. 2001... ·...

PertanikaJ. Soc. Sci. & Hum. 9(2): 113- 121 (2001) ISSN: 0128-7702© Universiti Putra Malaysia Press

Auditor Change During Listings: Effect on IPO Premiums

SHAMSHER MOHAMAD & HUSON JOHERDepartment of Accounting & Finance

Faculty of Economics and ManagementUniversiti Putra Malaysia

43400 UPM Serdang, Selangor

Keywords: Audit quality, IPO Premium, ex-ante uncertainty

ABSTRAKKajian ini meneliti kaitan antara pulangan awal yang diperolehi dari penyenaraian syarikat dipapan pertama dan kedua Bursa Saham Kuala Lumpur (BSKL) dengan syarikat audit yangdigunakan dalam penyiapan dan penyemakan prospektus syarikat yang disenaraikan. Syarikataudit dibahagikan kepada dua kumpulan, iaitu syarikat yang ternama (Tier 1) dan syarikat yangtidak ternama (Bukan Tier 1). Diandaikan bahawa syarikat audit yang ternama akan memberiperkhidmatan audit yang berkualiti dan ini dapat mengurangkan tahap ketakpastian pelaburterhadap potensi syarikat yang hendak disenaraikan. Ini menyebabkan pulangan awal daripenyenaraian adalah lebih rendah jika dibandingkan dengan pulangan awal dari syarikat yangmenggunakan perkidmatan audit dari syarikat audit yang tidak ternama. Penemuan kajian atas213 syarikat yang disenaraikan di BSKL menunjukkan memang ada kecenderungan firma-firmayang hendak menyenaraikan saham-sahamnya di BSKL untuk menggunakan perkhimatan syarikat-syarikat audit yang ternama. Tidak terdapat perbezaan yang signifikan antara pulangan awal daripenyenaraian oleh syarikat yang menggunakan perkhidmatan syarikat audit yang ternama denganyang tidak ternama. Walau bagaimanapun, pulangan awal syarikat-syarikat yang disenaraikan dipapan kedua jauh lebih tinggi dari pulangan awal dari syarikat yang disenaraikan di papanpertama BSKL. Penemuan ini menunjukkan reputasi syarikat audit (iaitu sama ada ternama atautidak) tidak berperanan sebagai penentu pulangan awal semasa penyenaraian. Penemuan inisecara keseluruhannya adalah tekal dengan penemuan daripada kajian yang lain (Shamsher 8cAnnuar 1997) yang menunjukkan bahawa pelabur di BSKL tidak membezakan kualiti perkhidmatanaudit yang diberikan oleh syarikat-syarikat audit yang ternama dan yang tidak ternama.

ABSTRACTThe study examined the relationship between choice of quality differentiated audit firm andinitial return at listing. It is conjectured that the superior audit quality of Tier 1 audit firms helpsto reduce ex-ante uncertainty and consequently reduces the initial premiums at listing. Thefindings show that there is an inclination for listed firms to engage Tier 1 audit firms, and nosignificant difference in the initial returns of IPOs firms audited by either Tier 1 or Non-Tier Iaudit firms were observed. However, higher significant initial returns for new issues were observedfor Second Board firms relative to Main Board firms. The findings do not appear to suggest thatthe auditor reputation is a determinant of initial returns at listing. The findings are consistentwith those documented by Shamsher and Annuar (1997) that investors are indifferent to thequality of audit service provided by Tier 1 and Non-Tier 1 audit firms.

INTRODUCTIONThe change of auditors prior to listing has beenan issue of interest among academics, investors,and management in developed economies dueto its effect on underpricing or overpricing ofthe new issue. It is a statutory requirement in

Malaysia for every company that goes public toengage the services of merchant banks to helpthem get listed. In the process, the companiesare required to provide prospectus audited byindependent auditors to verify the statements asbeing true and fair view of the company. The

Shamser Mohamad & Huson Joher

prospectus normally contains information onassets, historical profitability, economic prospects,investment plans and some form of profit forecastand dividends. The entrepreneurs usually disclosefavourable private information about the firm tothe potential investors so as to enhancemarketability of the offering without too muchoffer premium. To add more credibility to thebasic information provided in the prospectus,the management may engage the service ofreputable auditor. The reputation of theaccountants and auditors is potentially a signalingdevice for conveying the credibility of theinformation supplied to potential investors, sinceinvestors might not have any other resource toverify the information provided by a listing firm.It may also reduce uncertainty and therefore thelevel of premiums on the new listings, as investorsmight be willing to pay a higher offer price forthe shares offered if the audit firm is morereputable than the one engaged prior to goingpublic. Choice of quality differentiated auditfirm might provide a useful setting to ascertainwhether potential investors perceive the auditorchange as a signal of the level of uncertainty inthe new issue.

Though the information contained in theprospectus gives potentially useful informationto prospective investors there is also a great dealof uncertainty surrounding the pricing of IPO,which is further complicated given limiteddisclosures by companies prior to listing. In viewof the concern about the inherent risk associatedwith rapid expansion of business activities beingfinanced by the proceeds from a new issue, IPOrepresents a classic example of informationasymmetries between the pre-issue owners whoare the entrepreneurs and the investing public.Entrepreneurs have detailed information on thecompanies and their true worth whereas potentialinvestors have limited knowledge of the businessand its future economic prospects. Thusindependent auditors will serve as signalingdevice in validating entrepreneurs* claims basedon private information about the potential valueof the firm to stockholders. There is nodocumentation on this important issue in thisemerging Malaysian IPO market.

In view of the importance of the auditors'choice at listing, this paper examines the effectof choice of quality differentiated audit firms onthe IPO premiums of newly listed firms in theKuala JLumpur Stock Exchange (KLSE). The

hypothesised relationship between the choice ofquality-differentiated audit and the initial returnof the IPOs is investigated.

The findings have implications for corporatemanagement decisions, the auditing profession,investment adviser/banker and investors ingeneral. The documentation of the variousauditor choice and auditor switch and the effecton the initial return (market premium) fromofferings will assist the corporate decision makersto signal inside information to potential investorsbefore the listing. The findings would alsoprovide information to the audit professionregarding public's perception on the qualityand differentiation of quality of audit services.Investment adviser/banker would benefit fromthe understanding of choice of auditor as asignal of investment adviser/banker reputationand the pricing strategy of the new issues. Finally,the investing public could use this market signalin formulating price expectation of the newissues. Section 2 presents literature on the auditorcredibility and initial public offerings. Section 3provides discussion on methodology, datacollection and return measurement techniques.Section 4 provides discussion on findings andthe final section summarises the findings of thepaper.

REVIEW OF LITERATUREThe theory of the firm as amended to includeagency problem emphasises the importance ofauditing as a monitoring device (Jensen andMeckling 1976) to validate the management'suse of audited statements to convey a true andfair view of the company to the potential investorswho have very limited access to the company'sprivate information. DeAngelo (1981a;1981b)developed a demand and supply model for auditquality. Audit quality is defined as the probabilitythat an auditor will both discover the breach ofcontract (by the management and the investingpublic) and the ability to subsequently report it.An analogy from product differentiationhypothesis is that firms use auditor choice as asignaling device to reveal firm's desirablecharacteristic. Firms appear to signal ex-anteuncertainty by engaging the services of areputable audit firm. This signal is credible tothe market since the auditoris compensation ishigher exhibiting firm-specific reputation capital.Firms with favourable information would preferthe services of highly reputed auditors to reduce

114 Pertanika J. Soc. Sci. & Hum. Vol. 9 No. 2 2001

Auditor Change During Listings: Effect on IPO Premiums

uncertainty. A switch to a prestigious audit firmcan enhance audit services because of superiorindustry understanding, which help reduceuncertainty of the value of information infinancial statements. Management may seek areputable auditor in an attempt to install abetter monitoring system and enhance theprincipals' faith in the financial reporting system.This would also portray to the potentialshareholders the managementis integrity andgood stewardship of shareholders. It is widelyperceived that higher prestige audit firm hasgreater incentive not to perform low qualityaudit (DeAngelo 1981).

It is well documented in the literature thatsome companies replace their auditors beforegoing public for reasons of prestige, reputationand greater technical ability (Carpenter andStrawser 1971). The AICPA (1978) and Lurie(1977) examined the various reasons for auditorswitch and found that the larger and better-known audit firms were believed to encouragethe sales of their shares. Francis and Wilson(1988) documented that firms may change tohigher prestige audit firms (Big-Eight) to increasemarketability of the shares. It is also a commonpractice among Malaysian firms to employ morereputable auditors before listing. Huson et al.(2001) examined the wealth effect of auditorswitch among Malaysian listed firms. Theydocumented no evidence of significant wealtheffect from auditor switch announcement. Thus,auditor switch in this emerging capital marketconveys no information value associated withauditor switch.

Unlike the corporate announcement of ex-post events such as earnings, dividends, etc.,which reflect real change in corporateperformance about expected future prospect ofa company, auditor change is an event thatconveys no direct apparent economicinformation. Rather, the possible economic effectfrom such event is the signal associated withdifferent interpretation about the quality ofauditor switch by the investors at large (Hagigi etal 1993).

DeAngelo (1981a) found that financialstatement users do not directly observe the auditprocedure and have only limited informationabout the auditor contractual arrangement.However, they develop observable proxies foraudit procedures and auditor contractualarrangement, which are associated with audit

quality. De Angelo (1981b) argues that largerfirms have greater incentive to supply high qualityaudit services. It is also asserted that the size ofthe audit firm signals audit quality, since largerones have more clients and accordingly, morefuture quasi-rents will be lost if the auditor'sreputation is tarnished. Dopuch and Simunic(1982) assert that larger audit firms havedifferentiated themselves from other audit firmsin terms of higher audit quality. The assertionon size and quality of audit firms suggests thatlarger audit firms deliver higher quality auditsand are less likely to accede to client's pressureregarding the use of questionable accountingpolicies and practices. This is designed to buildconfidence on the financial statement from theauditors. If the company with a favourable privateinformation chooses to engage higher prestigeaudit firm, the market should react favourably.However, a switch to a lower prestige firm (non-Big-8) is viewed negatively due to the shiftingsignals of lesser quality standard (Hagigi et al.1993; Johnson and Lys 1990). Therefore, themarket would probably respond positively to theformer and negatively to the latter moves.

From the agency perspective, a company'saudited financial statements provide a means forowners to monitor the performance of the firm'smanagers. Financial statements that are certifiedby independent professional auditors provideassurance about reliability and credibility. Wallace(1980) suggests that increased credibility offinancial statements certified by credible auditorsreduce investors1 uncertainty about the reliabilityof the content of financial statements. Thissuggests that the price effect on shares fromauditor switch actually is a proxy for the qualityof information under strict professionalapplications of standards of a robust accountingenvironment. Thus, financial statements attestedto by a credible auditor provide believableattestation about the quality of informationcertified by the accounting professionrepresented by particular auditor to investors. Incontrast, financial statements that are audited bysmaller audit firms, which are less reputable,may not reduce investors' uncertainty about thewell being of a company. Hence, a costly searchby investors to evaluate the true and fair value ofthe company is perpetrated in such situations.Accordingly, market participants may lower theprice they are willing to pay for the securities ofsuch firms that switch to lower quality auditors.

PertanikaJ. Soc. Sci. 8c Hum. Vol. 9 No. 2 2001 115

Shamser Mohamad & Huson Joher

There are also conflicting opinions in somestudies. Contrary to the above arguments, someof earlier studies are based on the argumentthat professional standard imply homogeneityacross different size of audit firms such thataudit quality is independent of firm size. It wasfurther argued that audit quality is relativelyhomogeneous across audit firms assuming allaudit firms adhere to Generally AcceptedAccounting Principles (GAAPs) and GenerallyAccepted Auditing Standard (GAASs). However,Dopuch and Simunic (1982) argued that thatcredibility must be associated with an observablecharacteristic, such as brand name. Since thedetailed information of various audit firms arenot publicly disclosed, auditors need not beperceived to be homogeneous in the quality oftheir services. Such an attribute is difficult andcostly to develop as well as maintain, thus it musthave market value. Therefore, market for auditorsshould be characterized by productdifferentiation, as are all competitive producingunits. In other words, there is heterogeneityamong the audit firms. From the observed two-tier audit industry structure, Dopuch and Simunicinferred that higher prestige audit firm is morecredible than the others.

Auditor switch prior to the company goingpublic is fairly common and widely explained asone of management 's efforts to reduceuncertainty in emerging market. Carpenter andStrawser (1971) explained this phenomenon asnecessary to sell their offering at the highestpossible price. This widely held view suggeststhat the employment of a reputable audit firmwill increase the offer price of the new issue andinvestors may be predisposed to accept lowerreturns in exchange for greater certainty.

There is ample of evidence on underpricingof the firm's equity securities (Rock 1986; Beattyand Ritter 1986; Balvers et al 1988; and Allenmd Faulhaber 1989). Various explanations havebeen offered for the underpricing: for example,Baron (1982) proposed that the investmentbanker is 'better informed' than the issuingcompany as to the demand of issuing company'sissue and therefore the issuer underprice toensure success of the issue. Rock (1986) andBeatty and Ritter (1986) proposed two classes ofinvestors, 'informed' and 'uninformed' investorsare assumed to exist, and underpricing is toentice the informed investors to participate toreveal the value of the issue. These explanations

suggest that there is a positive relationshipbetween ex ante uncertainty and the underpricingof IPO.

With regard to choice of auditors at thetime of listing, Simunic and Stein (1987) suggestthat audit firm disassociated themselves bydifferentiation on the dimensions of controland credibility. Product line motivatesmanagement's auditor choice in IPO market.The form of the underwriter agreement, theproportion of common stocks held by outsidersafter the IPO, and a measure of uncertainty arerelated to the choice of which auditing firm ischosen. Beatty (1989) provides evidenceconsistent with Simunic and Stein (1987) thatlarger and less risky IPO clients tend to hire theBig Eight auditing firms.

Titman and Trueman (1986) suggests thatauditor quality provides useful information toinvestors to assess the value of the IPO firm.They showed analytically that an entrepreneurhas the incentive to choose level of auditorquality that correctly reveals the privateinformation about the firm. They suggest thatthe more reputable auditors charge a premiumprice for additional credibility they bring. Suchauditors are more likely to uncover and discloseadverse information about the firm.

DATA AND ANALYSISData

This study covers 213 firms listed on the mainsecond boards of KLSE over the period 1996 to2000. The information on offer price and thetraded price of these firms was extracted fromKLSE records, the company prospectus andannual reports. Information prior to listing, wasobtained from the Registrar of Companies(ROC). The Composite Index is used as a proxyof the market portfolio and the values of theindex were extracted from the daily diary ofKLSE.

To determine the impact of auditor switchprior to going public, the choice of auditors atthe time of listing was examined. Auditor changesthat occurred more than two financial periodsprior to the IPO were not considered.

•

Analysis

To determine the price impact of various auditorswitches, the audit firms are categorised into twocategories, the 'Big Eight* (and subsequently'Big Five') as Tier 1 audit firms and Non-Big

116 PertanikaJ. Soc. Sci. & Hum. Vol. 9 No. 2 2001

Auditor Change During Listings: Effect on IPO Premiums

(Non Tier 1) audit firms (Dopuch and Simunic1982). Tier 1 firms are used to proxy higherprestige audit firm with greater reputationalcapital, whereas the Non-tier 1 firms* proxy theless prestige audits firms with lesser reputationalcapital. To analyse the impact of auditor switchduring the issue, the data on auditors are sortedinto six groups in two different categories:

a. IPO xvith Auditor Switch1. Switch from no-Tier 1 audit firm to Tier 1

audit firm - upward switch.2. Switch from Tierl audit firm to Non-Tier 1

audit firm - downward switch,3. Switch from Tier 1 audit firm to another

Tier 1 audit firm - lateral switch.4. Switch from non-Tier 1 audit firm to another

Non-Tier 1 audit firm - lateral switch.

b. IPO with No Auditor Switch1. Remain with the same Tier 1 auditor2. Remain with the same Non-Tier 1 auditor

The IPO with no auditor switch serves as thecontrol group.

The initial return for a firm going public isdefined as the first day gross return to an investorwho acquires a share and sells at the closingprice on the first day of public trading.The initial return in percentage is:

Initial Return (IR)P — P1 MC IPO x 100%

(1)

Where PMC: Market price at the close of firsttrading day, and

P Ipo: IPO's offer price.The return on the market is computed for

the identical time period for each IPO. Themarket return in percentage is defined as:

KLCIMC - KLCLMarket Return (MR) = — - x 100%

KLCL,(2)

Where KLCIMC: Kuala Lumpur Composite Indexat the close of first trading day,and

KLCIp: Kuala Lumpur Composite Indexat the close of the previoustrading day.

The market adjusted initial return (MAIR)

is estimated for all categories of switch sample. Itis defined as the difference between the initialreturn on the new issue and the return on themarket, that is, MAIR • IR - MR. The averagemarket adjusted initial return (AMAIR) for eachgroup is computed.

SMAIRAMAIR =

N(3)

Where AMAIR : average market adjusted initialreturn of respective groups

MAIR : market adjusted initial returnof respective groups

Ng: number of firms in each of thegroups

It is hypothesized that the IPOs audited bythe Tier 1 auditor signals lesser ex ante uncertaintythan IPOs audited by Non-Tier 1 auditor, thusearning lower average initial returns (AIR),

AIR (Tier 1 auditors) < AIR (Non Tier 1 auditors)

Similarly, IPOs with downward auditor switch(i.e. switch from Tier 1 auditor to Non-Tier 1auditor) resulting an increases the ex anteuncertainty, thus earning a higher initial returns.

AIR (downward switch) > AIR (Tier 1 no switch)

However, for the price effect of IPOs withlateral auditor switches (i.e. Tier 1 auditor switchto another tier 1 auditor or Non-Tier 1 auditorswitch to another Non-Tier 1 auditor) is moreambiguous, and a mixed signal is expected.However, the initial returns of IPO with Non-Tier 1 lateral auditor switch are expected togenerate higher initial returns than the IPOwith Tier 1 lateral auditor switch. This could beexpressed as:

AIR (Non Tier 1 lateral switch) > AIR (Tier 1lateral switch)

The student-t statistics are used to test thestatistical significance of the observed values.

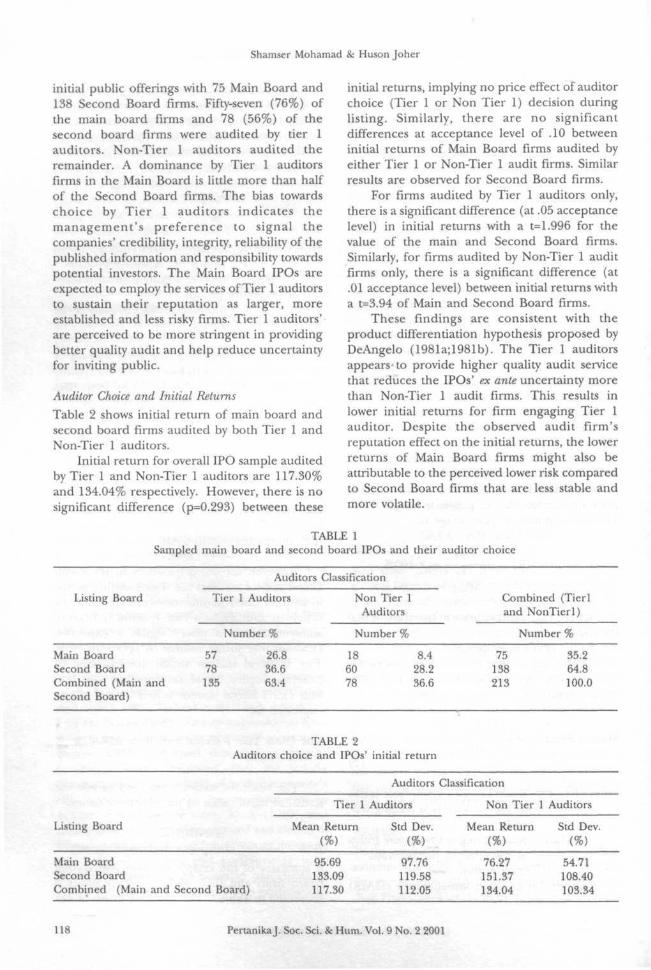

FINDINGSIPOs - Board of Listing and Auditor Choice

A summary of the sample of main and secondboard firms and their auditor classifications ispresented in Table 1. The sample consists of 213

PertanikaJ. Soc. Sci. & Hum. Vol. 9 No. 2 2001 117

Shamser Mohamad & Huson Joher

initial public offerings with 75 Main Board and138 Second Board firms. Fifty-seven (76%) ofthe main board firms and 78 (56%) of thesecond board firms were audited by tier 1auditors. Non-Tier 1 auditors audited theremainder. A dominance by Tier 1 auditorsfirms in the Main Board is little more than halfof the Second Board firms. The bias towardschoice by Tier 1 auditors indicates themanagement 's preference to signal thecompanies' credibility, integrity, reliability of thepublished information and responsibility towardspotential investors. The Main Board IPOs areexpected to employ the services of Tier 1 auditorsto sustain their reputation as larger, moreestablished and less risky firms. Tier 1 auditors'are perceived to be more stringent in providingbetter quality audit and help reduce uncertaintyfor inviting public.

Auditor Choice and Initial ReturnsTable 2 shows initial return of main board andsecond board firms audited by both Tier 1 andNon-Tier 1 auditors.

Initial return for overall IPO sample auditedby Tier 1 and Non-Tier 1 auditors are 117.30%and 134.04% respectively. However, there is nosignificant difference (p=0.293) between these

initial returns, implying no price effect of auditorchoice (Tier 1 or Non Tier 1) decision duringlisting. Similarly, there are no significantdifferences at acceptance level of .10 betweeninitial returns of Main Board firms audited byeither Tier 1 or Non-Tier 1 audit firms. Similarresults are observed for Second Board firms.

For firms audited by Tier 1 auditors only,there is a significant difference (at .05 acceptancelevel) in initial returns with a t-1.996 for thevalue of the main and Second Board firms.Similarly, for firms audited by Non-Tier 1 auditfirms only, there is a significant difference (at.01 acceptance level) between initial returns witha t=3.94 of Main and Second Board firms.

These findings are consistent with theproduct differentiation hypothesis proposed byDeAngelo (1981a;1981b). The Tier 1 auditorsappears to provide higher quality audit servicethat reduces the IPOs' ex ante uncertainty morethan Non-Tier 1 audit firms. This results inlower initial returns for firm engaging Tier 1auditor. Despite the observed audit firm'sreputation effect on the initial returns, the lowerreturns of Main Board firms might also beattributable to the perceived lower risk comparedto Second Board firms that are less stable andmore volatile.

TABLE 1Sampled main board and second board IPOs and their auditor choice

Listing Board

Main BoardSecond BoardCombined (Main andSecond Board)

Listing Board

Main BoardSecond BoardCombined (Main and

Auditors Classification

Tier 1 Auditors

Number %

57 26,878 36.6135 63.4

Non Tier 1Auditors

Number %

18 8.460 28.278 36.6

TABLE 2Auditors choice and IPOs' initial return

Auditors

Tier 1 Auditors

Mean Return Std Dev.(%) (%)

Second Board)

95.69 97.76133.09 119.58117.30 112.05

Combined (Tierland NonTierl)

Number %

75138213

Classification

Non Tier 1

Mean Return(%)

76.27151.37134.04

35.264.8100.0

Auditors

Std Dev.(%)

54.71108.40103.34

118 PertanikaJ. Soc. Sci. & Hum. Vol. 9 No. 2 2001

Auditor Change During Listings: Effect on IPO Premiums

IPOs and Auditor Changes

The distributional characteristics of variouscategories of auditor switch for the newly listedMain and Second board firms are presented inTable 3.

Table 3 shows that only 24 (about 18%)firms did change their auditors at the time oflisting, and majority of the change (18 out ofthe 24 firms) were in the upward switches (Non-Tier 1 to Tier 1) category. Seventeen of theupward switch firms were from the second board.Eighty-two percent of the sampled firms did notswitch auditors when listing. Of these, a majorityis from Second Board firms that engaged theservices of Tier 1 audit firms. The highproportion of no-switch firms may be due to acombination of factors.

The large numbers of IPOs wereincorporated shortly prior to the listing, thereforethe choice of auditors had been duly consideredand was not expected to change within such a

short time period. Possibly firms that wereincorporated for a long time, a majority of firmschanged their auditors earlier than two financialperiods prior to listing. In the process ofcomplying with the capital and profitperformance requirements, these firms switchedtheir auditors in anticipation of going publicthree years or five years ahead.

Auditor Switch and Initial ReturnsTable 4 summarizes the various categories ofauditor switch and their respective initial returns.

For the Main Board listings, the initialreturns for non-switch Tier 1 firms are larger(94.86%) than the initial returns of non-switchNon-Tier 1 firms (76.27%), the difference is notstatistically significant. However, the firms in theupward switch category recorded 142.40% initialreturns. For the Second Board, the Tier 1 non-switch firms generated 129% initial returns,which are lower than the non-switch Non-Tier 1

TABLE 3Auditors switch during IPOs

Type of Switches Main

No.

5600180

Board

%

26.290.000.008.450.00

SecondBoard

No.

6010

555

%

28.170.470.0025.822.35

Combined (Mainand Secondboard)

No.

11610735

%

54.460.470.0034.272.35

Tier 1 unchanged (no switch)Tier 1 to another Tier 1 (lateral switch)Tier 1 to Non Tier 1 (downward switch)Non Tier 1 unchanged (no switch)Non Tier 1 to another NonTier 1 (lateral switch)Non Tier 1

Total

to Tier 1 (upward switch) 1

75

0.47

35.21

17

138

7,98

64.79

18

213

8.45

100.00

TABLE 4

Type of Switches

Mean(

Main

Returns

Board

Std Dev. Mean1

Second

Returns(%)

Board

Std Dev.

Tier 1 unchanged (no switch)Tier 1 to another Tier 1 (lateral switch)Tier 1 to Non Tier 1 (downward switch)Non Tier 1 unchanged (no switch)Non Tier 1 to another Non Tier 1(lateral switch)Non Tier 1 to Tier 1 (upward switch)

94.8600

76.27

142.40

98.4400

54.710

129.1570.00

0149.58171.00

150.70

124.85

0102.26177.84

103.45

Total 75 35.21 138 64.79

PertanikaJ. Soc. Sci. 8c Hum. Vol. 9 No. 2 2001 119

Shamser Mohamad & Huson Joher

firms' returns of 149%; the difference is notstatistically significant. Firms that had upwardswitch (from Non-Tier 1 to Tier 1) recorded150% returns. These findings are basicallyinconsistent with the auditor reputationhypothesis, which postulates that firms auditedby reputable auditors should have lower initialreturns due to less uncertainty.

CONCLUSIONThis paper investigates the hypothesisedrelationship between the firms' choice of qualitydifferentiated audit firms (reputable (or Tier 1)and non-reputable (Non-Tier 1)) audit firmsand the initial returns at listing. The findingsappear to suggest that there is an inclination fornewly listed firms to engage Tier 1 audit firms,probably due to management's intention ofsignaling the firm's favourable privateinformation and credibility of the reportedfinancial information. Investment banker's andother advisors' prefer to engage Tier 1 auditorsto project a better image that could increase themarketability of the issue and reduce the risk ofunder-subscription.

The findings also show that there is nosignificant difference in the initial returns ofIPOs firms engaging Tier 1 and Non-Tier 1audit firms. However, there is a higher andsignificant initial return for Second Board firmsat listing compared to Main Board firms. Firmsthat had upward switch (Tier 2 to Tier 1) showedhigher returns as compared to lateral change inthe same tier, inconsistent with the auditorreputation hypothesis. This results, however,could be biased by the large number of newlylisted firms that did not switch auditors at listing,probably due to lack of time to make changesbefore listing, and/or have engaged Tier 1auditors at incorporation in anticipation oflisting. These results do not support the widelyheld view that firms that seek listing do switchauditors prior to their listing for positive marketsignaling. The results indicate that auditor'sreputation is not an important determinant ofthe IPOs initial return. These findings areconsistent to those documented by Shamsherand Annuar (1997) that investors are indifferentto the quality of audit services provided by Tier1 and Non-Tier 1 audit firms. It is highly probablethe differences in the listing board characteristicsare important determinant of initial returns atlisting.

REFERENCESALLEN, F. and G. R. FAULHABER. 1989. Signaling by

underpricing in the IPO market. Journal ofFinancial Economics 23: 303-323.

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS.

1978. Commission on Auditors' Responsibilities: Report, Conclusion and Recommendations.(AICPA 1978),

BALVERS, R. J., W, MCDONALD and R. E. MILLER.

1988. Underpricing of new issues and thechoice of auditor as a signal of investmentbanker reputation. The Accounting Review 63(4):605-622.

BARON, D. P. 1982. A model of the demand forinvestment banking advising and distributionservices for new issues. Journal of Finance37(September): 955-976.

BEATTY, R. P. and J. R. RITTER. 1986. Investment

banking, reputation, and the underpricing ofinitial public offerings. Journal of FinancialEconomics, 16(Jan/Feb): 213-232.

CARPENTER, C. G., and R. H. STRAWSER. 1971.

Displacement of auditor when the clients gopublic. Journal of Accountancy June: 55-58.

DE ANGELO, L. E. 1981a. Auditor size and auditquality. Journal of Accounting and EconomicsDecember: 183-199.

DE ANGELO L. E. 1981b. Auditor independent, lowballing, and disclosure regulation. Journal ofAccounting and Economies'. 113-127.

DOPUCH, N. and D. SIMUNIC. 1982. Competition in

Auditing : An Assessment. In Symposium onAuditing Research IV, Urbana : University ofIllinois.

FRANCIS, J. R., and E. R. WILSON. 1988. Auditor

changes : a joint test of theories relating toagency costs and auditor differentiation. TheAccounting Review 63(4): 663-683.

HAGIGI, M., B. D. KLUCER and D. SHIELDS. 1993.

Auditor change announcement and dispersionof investor expectations. Journal of BusinessFinance & Accounting 20(6): 787-802.

HUSON, J. A., M, SHAMSHER, M. ANNUAR, and M.

ARIFF. 2001. Auditor switch decision ofMalaysian listed firms: tests of determinantsand wealth effect. The Malaysian Capital MarketReview Forthcoming.

120 PertanikaJ. Soc. Sci. 8c Hum. Vol, 9 No. 2 2001

Auditor Change During Listings: Effect on IPO Premiums

JOHNSON, W. B. and T. LAS. 1990, Market for auditservice : evidence from voluntary auditorchange. Journal of Accounting and EconomicsJanuary: 281-308.

JENSEN, M. C. and W. MECKUNC. 1976. Theory of thefirm : managerial behaviour, agency cost andownership structure. Journal of FinancialEconomics 3: 305-360.

LURIE, A. G. 1977. Selecting your auditor. FinancialExecutive ]\x\y\ 50-58.

Rock, K. 1986. Why new issues are underpriced.Journal of Financial Economics 16(Jan/Feb): 187-212.

SHAMSHER, M, M.N. ANNUAR and M. ARIFF, 1993.

Underpricing and Signalling in the New ShareIssues Market. Stock Pricing in Malaysia -Corporate Financial and FinancialManagement, p. 98-118. Serdang : UniversityPutra Malaysia Press.

SHAMSHER, M. and M.N. ANNUAR. 1997. Auditingfirm reputation, ex ante uncertainty and theunderpricing of initial public offerings on thesecond board of Kuala Lumpur stock exchange: 1990-1995. Pertanika Journal of Social Scienceand Humanities 5(1 ):5; 59-64.

SIMUNIC, D. A. and M. STEIN. 1987. ProductDifferentiation in Auditing : Auditor Choice in theMarket for Unseasoned New Issues. Monographprepared for the Canadian Certified GeneralAccountant Research Foundation,

TITMAN, S. and B. TRUEMAN. 1986. Information qualityand the valuation of new issues. Journal ofAccounting and Economics June: 159-172.

WALLACE, W. A. 1980. The Economic Role of the Auditin Free and Regulated Market. New York : ToucheRoss & Co.

Received: 16 April 2001

PertanikaJ. Soc. Sci. & Hum. Vol. 9 No. 2 2001 121