Audit and Assurance Marking Insight

36

Audit and Assurance Marking Insight Flora Zheng 23 rd Feb. 2021

Transcript of Audit and Assurance Marking Insight

Auditand Assurance

Marking Insight

Flora Zheng

23rd Feb. 2021

© ACCA PUBLIC

Webinar agenda

1. How marking works at ACCA – marking team

2. General principles of AA marking

3. Overview of the marking of the progress test

© ACCA PUBLIC

1. How marking works at ACCA – marking team

Qualifications Technical

Adviser

Marking

Session Lead

Team Leader

Markers

Team Leader

Markers

Team Leader

Markers

© ACCA PUBLIC

2. General principles of AA marking (1/2)

• Suggested answers – are examples of strong answers

• Credit is given for any relevant answers

• No negative marking

• No marks lost for poor spelling or grammar

© ACCA PUBLIC

2. General principles of AA marking (2/2)

• Generally 1(SP) or 2 marks(resolve relevant issue) per relevant point

• Marking will reflect the intellectual level demanded by the task

requirements

• Using professional verbs in the audit procedure to obtain audit

evidence

© ACCA PUBLIC

3. Overview of the marking of the progress test

Q1 uses a very common style of requirement, namely to ‘calculate ratio for both

year and describe audit risks and explain the auditor’s response to each risk’.

Here the question called for SEVEN risks and responses.

The examiner advises that future candidates must take note that audit risk is and

will continue to be an important element of the syllabus and must be understood.

Candidates must also ensure that they include adequate question practice as part

of their revision of this key topic.

© ACCA PUBLIC

3. Overview of the marking of the progress test

Q2 is testing the ability of students to identify and analysis the strength and

weakness of the internal control system of the client, meanwhile in accordance

with the strength of the internal control system, assuming the control activities

have been operating effectively, students should state how to use TEST OF

CONTROL to obtain sufficiency and appropriate audit evidence.

© ACCA PUBLIC

3. Overview of the marking of the progress test

Q3 Audit evidence is the area of the syllabus that requires a description of the

work and evidence obtained by the auditor to meet the objectives of audit

engagements and the application of International Standards on Auditing.

A key requirement of this part of the syllabus is an ability to describe relevant audit

procedures for a particular class of transactions or account balances. Generally,

questions in this syllabus area will cover a variety of areas across both the

statement of profit or loss and statement of financial position.

© ACCA PUBLIC

3.1 Answer the requirement – Q1

© ACCA PUBLIC

3.1 Answer the requirement – Q1– analysis the requirement(1/3)

The 14 marks reflects the fact that each risk/response is worth 2 marks which will be

awarded as follows:

·For identification of each audit risk – ½ mark each

·For explanation of each risk – ½ mark

·For an appropriate auditor’s response to each risk – 1 mark

© ACCA PUBLIC

3.1 Answer the requirement – Q1– analysis the requirement(2/3)

·To explain an audit risk it is necessary to state the relevant financial statement

assertion that is affected (e.g. completeness/cut-off/valuation, etc) or whether

amounts could be over/under/misstated or the effect on inherent/ control/detection

risk.

·An auditor’s response is an approach the audit team will take to address the

identified risk; it does not have to be a detailed audit procedure. ‘Discuss with

management’ is not sufficient to deal with any identified risk. You will have to apply

your knowledge of audit procedures to provide a valid response which would

adequately address the risk identified.

© ACCA PUBLIC

3.1 Answer the requirement – Q1– analysis the requirement(3/3)

·As you will see when you look at the marked answers in this article, it is not possible

to achieve a pass mark to such questions by the mere statement of knowledge – it

must be tailored to the specific scenario provided.

© ACCA PUBLIC

3.1 Answer the requirement – Q3 – format of your answer

Audit risk Auditor’s response

© ACCA PUBLIC

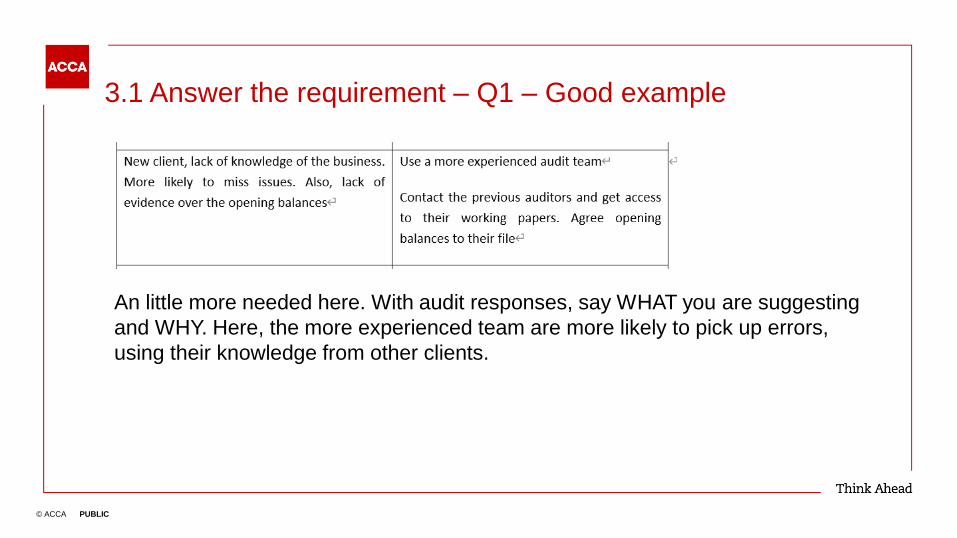

3.1 Answer the requirement – Q1 – Good example

An little more needed here. With audit responses, say WHAT you are suggesting

and WHY. Here, the more experienced team are more likely to pick up errors,

using their knowledge from other clients.

© ACCA PUBLIC

3.1 Answer the requirement – Q1 – Good example

TO make this even better – obtain documentary evidence.

© ACCA PUBLIC

3.1 Answer the requirement – Q1 – Good example

You scored a decent mark here – but could’ve dine even better by using the

numbers / ratios.

The question asked you to do this specifically, so you missed out on easy marks by

not using then.

© ACCA PUBLIC

3.1 Answer the requirement – Q1 – poor answer

Too vague to score credit. Say which tests you would perform to obtain evidence.

© ACCA PUBLIC

3.1 Answer the requirement – Q1 – poor answer

·This is a good point – going concern is an issue here.

·Better evidence for this would’ve been – deteriorating margins / liquidity ratios.

Quoting these would’ve earned you a full mark, rather than just a half.

·A bit vague. Better to say exactly what you would do e.g. ensure that all debt

covenants continue to be met, or that the business doesn’t run out of cash.

© ACCA PUBLIC

3.2 Answer the requirement – Q2-general principal

• Just knowing about control activities only is clearly insufficient.

• Exam is scenario based

• Exam technique is critical to passing-Students must learn to problem

solve

© ACCA PUBLIC

3.2 Answer the requirement – Q2(b)-analysis the requirement

·identify the benefit of the control activity can given to the client, cannot be too general

·identify the difference between the substantive procedure and test of control

·using professional verbs to state the audit procedure,

© ACCA PUBLIC

3.2 Answer the requirement –Q2(b) – Good example

© ACCA PUBLIC

3.2 Answer the requirement –Q2(b) – poor answer

Observation is a weak test here – it would only show you that the safe is being

used on that occasion, not that it was used throughout the year.

If it is an electronic safe – you could test this by obtaining the access logs, and

confirming that the till is used each night.

© ACCA PUBLIC

3.2 Answer the requirement –Q2(b) – poor answer

You’ve correctly picked out a strength here (daily transfer is overseen), but not

explained why it helps (more likely that any missing stores are picked up)

More detail needed here - how exactly would you test it? See the model answer.

© ACCA PUBLIC

3.2 Answer the requirement – Q2(c)-analysis the requirement

© ACCA PUBLIC

3.2 Answer the requirement –Q2(c) – Good example

© ACCA PUBLIC

3.2 Answer the requirement –Q2(c)– Poor answer

The requirement was to Identify and explain SIX DEFICIENCIES

½ mark for identifying (i.e. pick the deficiency out of the scenario, which you have done

well), ½ mark for explaining why it is a weakness (which you haven’t done)

Also, your answer falls short as you only picked out 3 issues, rather than the 6 that were

asked for.

© ACCA PUBLIC

3.2 Answer the requirement –Q2(c)– Poor answer

Weak recommendation, hence not scoring a mark.

The issue with anyone logging onto the till is that there is no audit trail of who served

a particular customer, increasing fraud risk.

The better recommendation is that each employee should have a till swipe card, so

that there is a log of who was on the till.

© ACCA PUBLIC

3.2 Answer the requirement –Q2(c)– Poor answer

You correctly picked out the issue, but didn’t explain it – so only scored half a mark.

Lack of segregation of duties means that this individual could commit a fraud and it

go undetected.

© ACCA PUBLIC

3.3 Answer the requirement – Q3

© ACCA PUBLIC

3.3 Answer the requirement – Q3– analysis the requirement(1/3)

·One mark would be awarded for each well described substantive procedure. Hence,

for each of these 6 or 5 mark requirements, you should aim to provide at least six or

five substantive procedures.

© ACCA PUBLIC

3.3 Answer the requirement – Q3– analysis the requirement(2/3)

·Care must be taken to address the specifics of the question; where the requirement

is to describe substantive procedures to address specific financial statement

assertions, such as valuation, any procedures that do not address this assertion

would not score any marks.

·If a requirement does not reference specific financial statement assertions, you must

read the requirement even more carefully to ensure that you answer the question set.

© ACCA PUBLIC

3.3 Answer the requirement – Q3– analysis the requirement(3/3)

·Details in the scenario were clearly headed ‘Trade payables’, and ‘Trade

receivables’. Careful reading of the scenario is always essential before writing an

answer.

Procedures which are not relevant to the requirement or the scenario will earn no

marks. Candidates must be prepared to tailor their knowledge of substantive

procedures to any area of the financial statements.

© ACCA PUBLIC

3.3 Answer the requirement – Q3 – Good example

© ACCA PUBLIC

3.3 Answer the requirement – Q3 – Good example

© ACCA PUBLIC

3.3 Answer the requirement – Q3 – poor answer

This isn’t really a substantive procedure – more of an understanding / test of

controls point.

When the requirement asks for substantive procedures, you need to suggest

tests that will tell you whether or not a year-end number is correct.

© ACCA PUBLIC

3.3 Answer the requirement – Q3 – poor answer

This won’t give any comfort over whether the year end receivables figure is

correctly stated.