Attracting Private Capital to The Electricity Sector

30

Tonci Bakovic 1 Tonci Bakovic Attracting Private Capital to The Electricity Sector -regulatory challenges and lessons- January 2012 Washington DC Presented by: Tonci Bakovic Chief Energy Specialist International Finance Corporation

Transcript of Attracting Private Capital to The Electricity Sector

Tonci Bakovic 1

To

nci B

ako

vic

Attracting Private Capital to The Electricity Sector -regulatory challenges and lessons-

January 2012

Washington DC

Presented by:

Tonci Bakovic

Chief Energy Specialist

International Finance Corporation

Tonci Bakovic 2

The findings, interpretations, and conclusions expressed in this presentation

are entirely those of the author and should not be attributed in any manner to

the International Finance Corporation or to the World Bank Group or to

members of its Board of Executive Directors or the countries they represent.

Disclaimer

-This presentation cannot be quoted without permission-

Tonci Bakovic

Tonci Bakovic 3

1. Capital Attraction – two decades of reform and privatization

2. Change Trends

3. Regulatory Lessons Learned and Best Practices

4. Country Case Studies Bolivia, Macedonia, Argentina, Chile, Brazil, Romania, Albania, Turkey, India

5. Summary – Best Practices

6. Suggested Reading

Table of Contents

“If you have ten thousand regulations you destroy all respect for the law.” Winston Churchill

Tonci Bakovic 4

0

5000

10000

15000

20000

25000

30000

35000

40000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

East Asia & Pacific

Europe & Central Asia

Latin America & Caribbean

Middle East & North Africa

South Asia

Sub-Saharan Africa

Tonci Bakovic

Latin America

Privatizations

Indian Ultramega

Projects

Brazil Boom

Eastern Europe

Privatizations

Asian IPPs

$ Capital Attraction

Two Decades of Reform (1990-2011)

Privatizations, Concessions, Green Field Projects

Source : World Bank and PPIAF, PPI Project Database. (http://ppi.worldbank.org) Date: 01/23/2012

Total Investment Commitments in Power USD 000

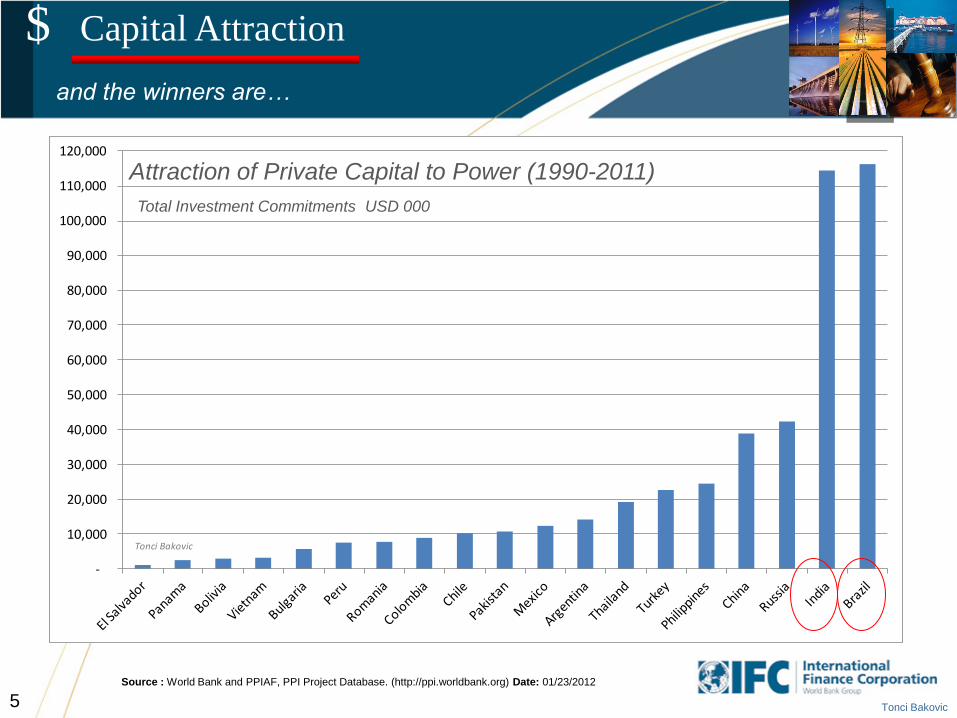

Tonci Bakovic 5

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

Tonci Bakovic

$ Capital Attraction

Attraction of Private Capital to Power (1990-2011)

Total Investment Commitments USD 000

Source : World Bank and PPIAF, PPI Project Database. (http://ppi.worldbank.org) Date: 01/23/2012

and the winners are…

Tonci Bakovic 6 Source : World Bank and PPIAF, PPI Project Database. (http://ppi.worldbank.org) Date: 01/23/2012

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

$110,000

Concession

Divestiture

Greenfield

Tonci Bakovic

$ Capital Attraction

Attraction of Private Capital to Power (1990-2011)

Concessions, Divestitures or Privatizations, Green Field Projects USD 000

Indian Ultramega (Gov Guarantee)

Russian Privatization (Generation)

Brazil (Concessions +

Greenfield)

Distribution privatized in all countries with exception of: -Vietnam

-Thailand

-China

-Mexico

Tonci Bakovic 7

101 106

238 253 260 262 288334 343 347

392 418 433 461 464 477 492

601

699

1,660

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

KOE ROE Varna Ban Dob M old Star Olt Sof Ded Tit ESM VSE Dem SSE Ed Em Elm ZSE M Sud

Ukr Ukr Bulg Rom Rom Rom Bulg Rom Bulg Hung Hung M acd Slovk Hung Slovk Hung Hung Hung Slovk Rom

Avg E.Europe Avg Lat.America Avg.Brazil T.Bakovic

EV= [(amount paid for equity) + (debt assumed * % bought)]

Post-World Bank PRG

PRG = Partial Risk Guarantee

$ Capital Attraction

Eastern Europe - Prices Paid for Discos (US$/customer)

Attraction of Private Capital to the Regulated Business

Brazil an outlier ?

Disco = Distribution Company

T Bakovic

Tonci Bakovic

How the Sector Structure Has Evolved

G1 G2 G3 G4

TRANSMISSION COMPANY

LTC/Spot

DISTRIBUTION COMPANIES AND LARGE USERS

END USERS

LTC = LONG TERM CONTRACT

LTC/Spot LTC/Spot LTC/Spot

LTC/Spot

Source: T Bakovic

G

T

D

Vertical Integrated

UTILITY (Monopoly)COMPETITION and Choice

ifrompriceofferP

offeredquantityofferQ

ifromprocuredquantityQwhere

QofferQQand

demandQtosubject

PQMinimize

i

i

i

iii

n

i i

i

n

i i

)(

0),(

,

1

1

Cost Plus = O&M + Dep + r (Assets)

Competitive MktMonopoly

T Bakovic

CHANGE TRENDS

8

Tonci Bakovic

Private participation and competition

CHANGE TRENDS

Latin

American

Model

Asian (IPP)

ModelIndonesia

Pakistan

Thailand

Philippines

MexicoFrance, Italy

South Africa

Portugal

Morocco

Uruguay

Chile

Argentina

El Salvador

Panama

Guatemala

Peru

Colombia

AustraliaNew Zealand

Cote d’Ivoire

Cameroon

Low

Competition

and

Regulatory

Reform

Private ParticipationLow High

High

Uganda

Philippines

Turkey

Argentina

Norway

USARussia

Brazil

Egypt

Vietnam

Source: T Bakovic

Bulgaria

Romania

Slovakia

Hungary

Poland,

India

UK

China,

Turkey

Ghana

UK +

9

Do you know where you are going to….

Tonci Bakovic

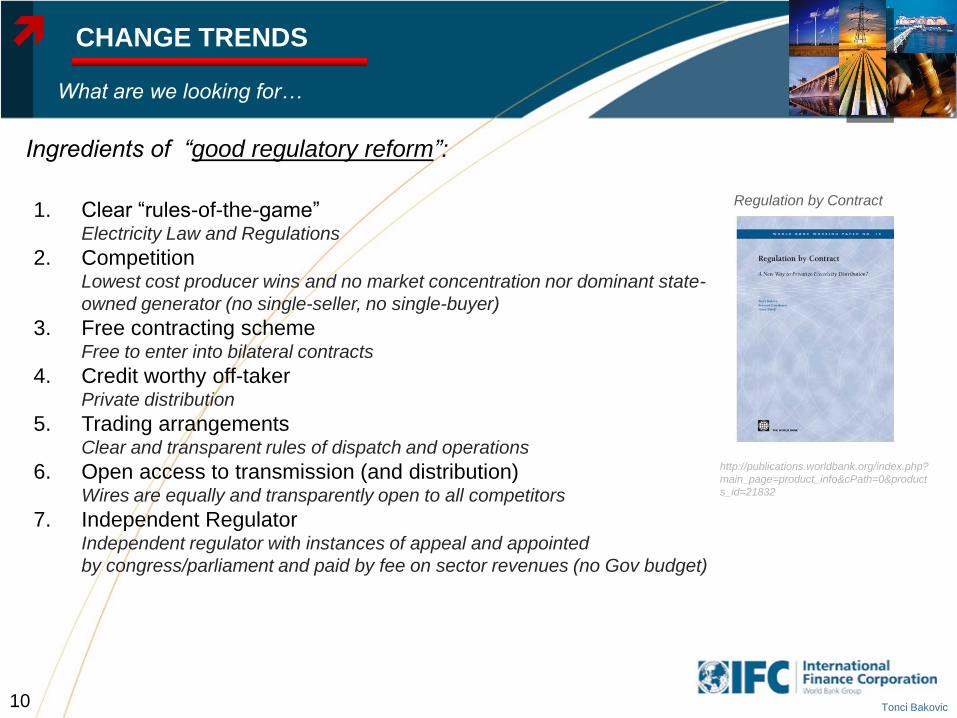

Ingredients of “good regulatory reform”:

1. Clear “rules-of-the-game” Electricity Law and Regulations

2. Competition Lowest cost producer wins and no market concentration nor dominant state-

owned generator (no single-seller, no single-buyer)

3. Free contracting scheme Free to enter into bilateral contracts

4. Credit worthy off-taker Private distribution

5. Trading arrangements Clear and transparent rules of dispatch and operations

6. Open access to transmission (and distribution) Wires are equally and transparently open to all competitors

7. Independent Regulator Independent regulator with instances of appeal and appointed

by congress/parliament and paid by fee on sector revenues (no Gov budget)

CHANGE TRENDS

10

http://publications.worldbank.org/index.php?

main_page=product_info&cPath=0&product

s_id=21832

Regulation by Contract

What are we looking for…

Tonci Bakovic 11

0

20

40

60

80

100

120

140

160

US$

/MW

h

Taxes

Distribution

Transmission

Generation

T Bakovic

First Question: Do tariffs cover costs…?

Second Question: Do we want to maximize sale revenues to the Treasury or do we want to minimize

tariff impact to customers ?

Third Question: How sustainable are the tariff increases required by the privatization policy ?

Tariff

Components

Lessons Learned and Best Practices

Checklist before embarking on reform/privatization

Tonci Bakovic 12

~50% Power Purchase Costs (PPC)

~50% Distribution Margin (VAD)

~2/3 RAB related

Lessons Learned and Best Practices

Pass-Through and Asset Valuation

RAB = Regulated Asset Base

Total Tariff

Key Regulatory Issues:

-Promote competition

-Respect free-market price determination

-PPC passthrough mechanism

Key Regulatory Issues:

-Asset revaluation

-WACC determination

-Allowed losses passthrough

-Allowed bad-debt passthrough

-X-factor determination

-Quality of Service Regulations

-Forex indexation

-Supply margin determination

Ge

ne

ratio

n P

rice

s

Dis

tributio

n T

ariff

Tonci Bakovic

If you achieve

competition at the

wholesale level then

you only need to

regulate the “wires-

business”

Tonci Bakovic

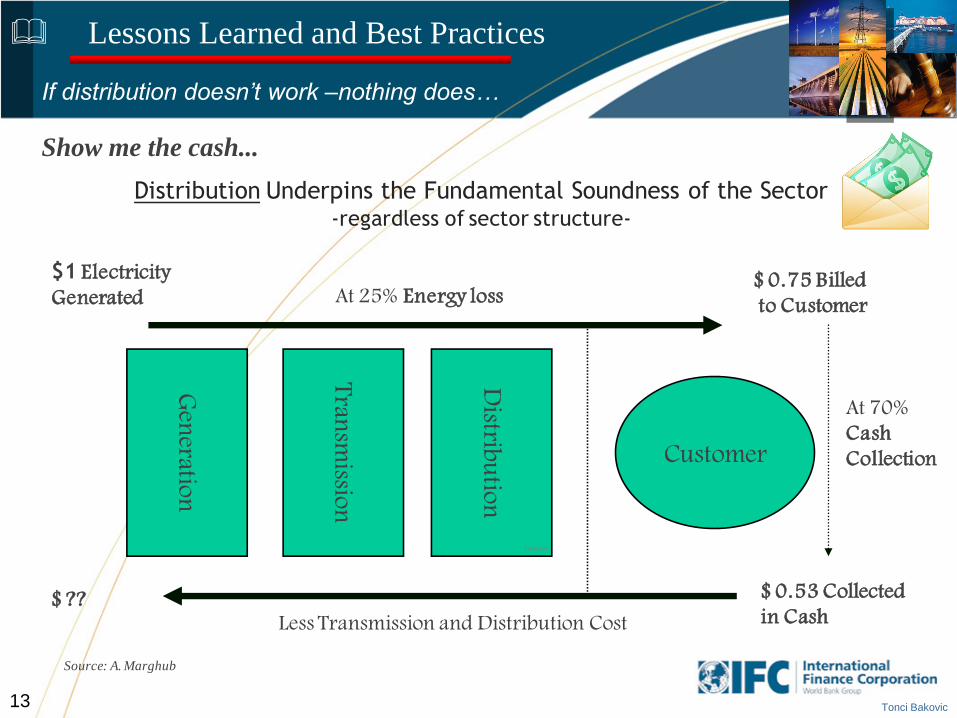

Gen

eration

Customer

Tran

smissio

n

Distrib

utio

n

$ 0.53 Collected

in Cash

$1 Electricity

Generated At 25% Energy loss$ 0.75 Billed

to Customer

At 70%

Cash

Collection

Less Transmission and Distribution Cost$ ??

Distribution Underpins the Fundamental Soundness of the Sector-regardless of sector structure-

Source: A. Marghub

T Bakovic

Show me the cash...

Lessons Learned and Best Practices

If distribution doesn‟t work –nothing does…

13

Tonci Bakovic 14

RAB Depreciation

Regulated Return on RAB

Operating costs

Cost of distribution losses

Regulated Revenues

Projected Demand

For Regulatory Period

Distribution Tariff

(indexed to inflation during

regulatory period)

RAB Depreciation

Regulated Return on RAB

Operating costs

Cost of distribution losses

Regulated Revenues

Projected Demand

For Regulatory Period

Distribution Tariff

(indexed to inflation during

regulatory period)

RRt = OCt + Depnt + [RABt x RRR] + DLt

RRt = Regulated revenues

OCt = Operating costs (in real terms). “Controllable” costs (O&M costs, commercial and administrative costs, labor cost) and “non-controllable” costs ( taxes, royalties)

Depnt = Depreciation of the RAB

RABt = Regulatory Asset Base. RAB is based on the enterprise value paid for the disco assets at privatization, plus the future capital expenditure approved by Regulator, plus

the annual working capital needs (e.g. capped at 1/8 of the revenues). RAB is depreciated annually and adjusted for inflation at the end of each regulatory period.

RRR = Regulated rate of return determined using a pre-tax Capital Asset Pricing Methodology (CAPM). This value remains constant for each regulatory year in the regulatory

period [e.g. the RRR can be set at 12%, in real terms, for the First Regulatory Period (FRP) and 10% for the Second Regulatory Period (SRP)]

DLt = Cost to purchase the energy that does not get distributed to the end consumers due to commercial and technical losses in the network. (e.g. allowed losses for the

beginning of the FRP are 13%)

Lessons Learned and Best Practices

Typical Components of the Distribution Tariff

PCAPt = PCAPt-1 x (1 + CPI – X)

customers

RRt

#PCAPt

Source: Tonci Bakovic

Tonci Bakovic

An asset based business…

Tonci Bakovic 15

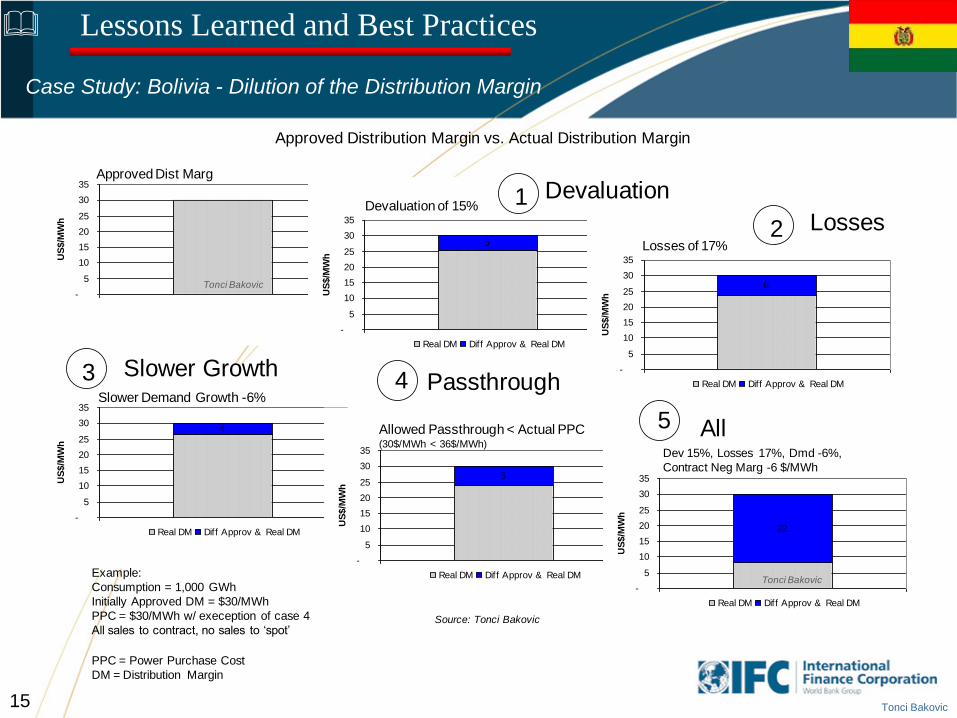

Case Study: Bolivia - Dilution of the Distribution Margin

Lessons Learned and Best Practices

-

5

10

15

20

25

30

35

1

US

$/M

Wh

5

-

5

10

15

20

25

30

35

1

US

$/M

Wh

Real DM Diff Approv & Real DM

6

-

5

10

15

20

25

30

35

1

US

$/M

Wh

Real DM Diff Approv & Real DM

4

-

5

10

15

20

25

30

35

1

US

$/M

Wh

Real DM Diff Approv & Real DM

6

-

5

10

15

20

25

30

35

1

US

$/M

Wh

Real DM Diff Approv & Real DM

22

-

5

10

15

20

25

30

35

1

US

$/M

Wh

Real DM Diff Approv & Real DM

Devaluation of 15%

Losses of 17%

Slower Demand Growth -6%

Allowed Passthrough < Actual PPC(30$/MWh < 36$/MWh)

Dev 15%, Losses 17%, Dmd -6%,

Contract Neg Marg -6 $/MWh

Approved Dist Marg

PPC = Power Purchase Cost

DM = Distribution Margin

Approved Distribution Margin vs. Actual Distribution Margin

1

2

3 4

Devaluation

Losses

Slower GrowthPassthrough

Example:

Consumption = 1,000 GWh

Initially Approved DM = $30/MWh

PPC = $30/MWh w/ exeception of case 4

All sales to contract, no sales to „spot‟

All5

Source: Tonci Bakovic

Tonci Bakovic

Tonci Bakovic

Tonci Bakovic 16

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan-

06

Feb-

06

Mar-

06

Apr-

06

May-

06

Jun-

06

Jul-

06

Aug-

06

Sep-

06

Oct-

06

Nov-

06

Dec-

06

Jan-

07

Feb-

07

Mar-

07

Apr-

07

1 month 3 months 6 months 9 months

Estimated Bill Collections Rates as % of Monthly Invoices

Sample: Starting Retail Tariff After Privatization

• Difficult for regulator to add capex to the asset base

• Company trying to improve efficiencies (reduce

O&M, improve collections, reduce losses)

• Privatization restrictions on employee reductions

• Trying to shift share of VAD that is going to O&M

and losses to the asset base (capex)

• Chicken-and-egg issue since you need capex to

improve efficiency (reduce losses, increase

collections)

Performance Improvement Higher Capex

Larger RAB Higher Tariff

2.99

0.11

0.99

0.33

0.46

0.42

0.34

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Eu

rocen

t/kW

h

Pow er Purchase Cost Transmission ChargeO&M Costs DepreciationReturn on RAB Allow ed LossesExcess Losses

Net

Distribution

Margin

€2.2 cent/kWh

Power Purchase

Cost Tariff

€3.1 cent/kWh

Excess

Losses

Retail

Tariff: €5.3

cent/kWh

Lessons Learned and Best Practices

Macedonia: Losses vs Capex

Tonci Bakovic

Tonci Bakovic RAB = Regulated Asset Base

Tonci Bakovic

Single Buyer stops delivering electricity to cover losses

Import wholesale mkt prices at 7 euro-cent/kWh

Only 11% losses allowed for pass-through

Actual losses in 2008 are 21%

Current scenario already shows losses at regulated wholesale prices

Revised scenario shows losses at import wholesale mkt prices

3.06 3.06

0.11 0.11

1.12 1.12

0.33 0.330.46 0.46

0.44 0.44

0.410.93

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Eu

roc

en

t/kW

h

Power Purchase Cost Transmission Charge O&M Costs

Depreciation Return on RAB Allowed Losses

Excess Losses

Net

Distribution

Margin

€2.2 cent/kWh

Power Purchase

Cost Tariff

€3.1 cent/kWh

Excess

Losses at

market prices

ESM Retail

Tariff: €5.3

cent/kWh

Excess

Losses at regulated

prices

Current

Scenario

Revised

Scenario

Macedonia: Single Buyer and Pass-through of Losses

Lessons Learned and Best Practices

Tonci Bakovic

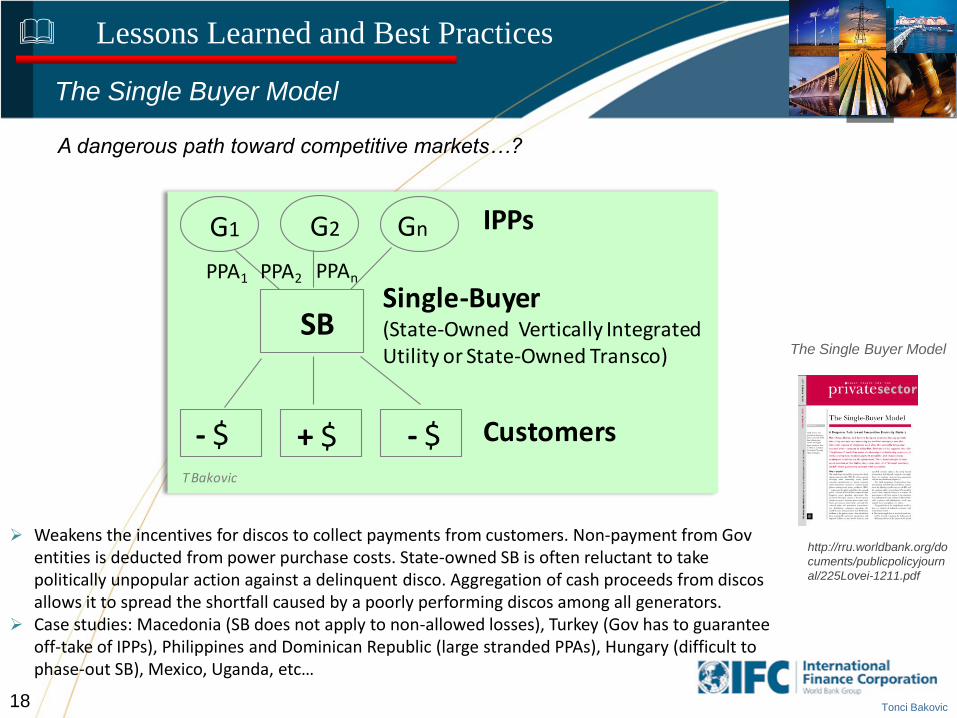

+ $- $ - $

? $

G1 G2 Gn

Single-Buyer

T Bakovic

Not enough cash to meet capex needs or debt service

17

Tonci Bakovic

The Single Buyer Model

Lessons Learned and Best Practices

A dangerous path toward competitive markets…?

+ $- $ - $

SB

G1 G2 Gn

Single-Buyer(State-Owned Vertically Integrated Utility or State-Owned Transco)

IPPs

Customers

PPA1 PPA2 PPAn

T Bakovic

Weakens the incentives for discos to collect payments from customers. Non-payment from Gov entities is deducted from power purchase costs. State-owned SB is often reluctant to take politically unpopular action against a delinquent disco. Aggregation of cash proceeds from discos allows it to spread the shortfall caused by a poorly performing discos among all generators.

Case studies: Macedonia (SB does not apply to non-allowed losses), Turkey (Gov has to guarantee off-take of IPPs), Philippines and Dominican Republic (large stranded PPAs), Hungary (difficult to phase-out SB), Mexico, Uganda, etc…

http://rru.worldbank.org/do

cuments/publicpolicyjourn

al/225Lovei-1211.pdf

The Single Buyer Model

18

Tonci Bakovic 19

Source: Electricity Association Argentina + Edelap

Effect of Devaluation – Residential Tariffs US$/kWh

Effect of Devaluation – Industrial Tariffs US$/kWh

Lessons Learned and Best Practices

Argentina: Devaluation and No Indexation

- Argentina Post 2001

Tonci Bakovic 20

Where:

Dollar Price: Average price of the exchange rate for the US Dollar, for the last thirty days, published by the Central Bank.

DOL0 : Average Exchange rate for the US Dollar, published by the Central Bank (Chilean$/US$).

D1 : Custom Duty applicable to electro-mechanical equipment at the Iquique Extension Free Zone.

D10 : Current Custom Duty applicable to electro-mechanical equipment at the Iquique Extension Free Zone

ISS & IPM : Salary & Wholesale Prices indexes published by INE for the third month before the Indexation is calculated.

ISS0 & IPM0 : Base values for the ISS and the IPM

0.11*

IPM

IPM0.1*

ISS

ISS.790*

D1

D+1*

DOL

PriceDollar *Price BaseCapacity =Capacity Price

0010

1

0

Chile: Indexation, Indexation, Indexation

Capacity Node Price in Chilean Pesos (79% xrate & import duties, 10% salary index, 11% wholesale price index)

Where :

Dollar Price: Average price of the exchange rate for the US Dollar, for the last thirty days, published by the Central Bank.

DOL0 : Average Exchange rate for the US Dollar, published by the Central Bank (Chilean $/US$).

D2 : Custom Duty aplicable to electro-mechanical equipment in Antofagasta.

D20 : Current Custom Duty aplicable to electro-mechanical equipment in Antofagasta

PPDA : Price for Light Diesel in Antofagasta, (in $/m3).

PPDA0 : Current Price for Light Diesel in Antofagasta (in $/m3

PFOA : Price for Fuel Oil Nº6 in Antofagasta, ($/ton)

PFOA0 : Current price for Fuel Oil Nº6 in Antofagasta (en $/ton)

The fuel prices to be used in the indexatión formulas will be the purchase prices, net of IVA (sale tax).

0020

2

0 PFOA

PFOA*0.00

PPDA

PPDA*0.00.001*

D 1

D 1 *

DOL

PriceDollar *PriceEnergy Base=Energy Price

Energy Node Price in Chilean Pesos (100% indexed to import components: xrate + import duties)

Note: Wholesale Energy Prices get Adjusted Every 6 Months Based on Expected Spot Forecast for Next 48 Months

%10Price BaseCapacity

Price) BaseCapacity -Capacity (Price ifAdjust

Lessons Learned and Best Practices

%10PriceEnergy Base

Price)Energy Base -Energy (Price ifAdjust

Indexation Algorithm for Hydro

Devil is in the Details

Tonci Bakovic 21

DoDIB4

IPCuoIPCuIB3

IPMNoIPMN*OB2)(IB2

IPCoIPC*OB1)(IB1*CDBTo= CDBT

In which:

CDBT: Cost of Distribution in Low Voltage $Chilean/kW-month

D: Index of imported products where D= Tc * (1+Ta) where Tc corresponds to the average price of the exchange rate for the US Dollar, for

the month before the last, published by the Central Bank, and Ta corresponds to the custom duty applicable to electro mechanical

equiptment

IPC: Consumer Price Index published by INE for the third month before the month when the tariffs will be applied

IPMN: Wholesale Price Index published by INE for the third month before the month when the tariffs will be applied

IPCu: Copper Price Index calculated as the average monthly price for the last 12 months of the price of Copper in the London Mercantile

Exchange

IAi and OAi: Weights applied to each service area

CFE: Fixed Charges; billing and metering $Chilean/client-month

DoD*B*0.07

IPCuoIPCu*0.10

IPMNoIPMN*.430

IPCoIPC*.400*3.811=CDBT

Cost of Distribution (17% indexed to import components: xrate + import duties)

IPMNoIPMN*FE2

IPCoIPC*FE1*CFEo= CFE CC

Fixed Charges

IPMNoIPMN*.180

IPCoIPC*.820*371.25= CFE

Lessons Learned and Best Practices

In the past also indexed to salary index (IRH) published by INE (IRH and IPMN ~20% each in the CDBT, and 70% and 30% -respectively- in the CFE)

IRHo

IRH*OB5)(IB5. ......*CDBTo= CDBT

INE = National Statistics Institute

IRHo

IRH*FE2 IPMNo

IPMN*FE1*CFEo= CFE CC

Chile: Distribution Tariff Indexation

Devil is in the Details

Tonci Bakovic 22

Spot Prices, Seasonal Passthrough and Smoothing Scrow Account

Argentina‟s MEM 1999-2003

Lessons Learned and Best Practices

Argentina: Collapse of „Pass-Though‟ Mechanism

-40.00

-30.00

-20.00

-10.00

0.00

10.00

20.00

30.00

40.00

1999 2000 2001 2002 2003

Mo

no

mic

Sp

ot

Pri

ce (

$/M

Wh

)

-400.00

-300.00

-200.00

-100.00

0.00

100.00

200.00

300.00

400.00

Bala

nce S

mo

oth

ing

Fu

nd

($)

Seasonal Avg Spot Balance Smoothing Fund

Source: ADEERA

http://www.regulationbodyofknowledge.or

g/documents/001.pdf

Pass Through of Power

Purchase Costs

Is your passthrough

mechanism

sustainable…?

Tonci Bakovic 23

http://siteresources.worldbank.org/INTENE

RGY/Resources/335544-

1111615897422/EnergyWorkingNotes2.pdf

- What should be the new

asset-base at the end of

the regulatory period ?

Book Value

Replacement

Value

Market

Value

3,000 $/cust

1,000 $/cust

400 $/cust

Tonci Bakovic

Brazil: Percentage premium of market

value over minimum sale price

(distribution privatizations)

Lessons Learned and Best Practices

Brazil: Asset Revaluation (RAB)

Source: The Regulatory Challenge of Asset Valuation.

Vivien Foster and Pedro Antmann

RAB = Regulatory Asset Base

The Regulatory Challenge

of Asset Valuation

Tonci Bakovic 24

S1 S2 S4 S5

Disco

Regulated Customers Eligible Customers „Grey‟ Customers

SOLR

?

Lessons Learned and Best Practices

Romania: The Supplier of Last Resort

Exerting the Right to Choose

Generators

Suppliers

Tariffs Prices

SOLR = Supplier of Last Resort

will PPC be allowed a

full passthrough ?

what is the regulated

supply-margin?

can customers leave

and come back at any

time?

who is in charge for

stopping supply in

case of no payment?

PPC = Power Purchase Costs

Why me…?

Tonci Bakovic 25

Prior to privatization, the GOA entered into a Partial Risk Guarantee (PRG) Agreement with

IBRD in May 2009 for an amount of up to EUR 60 million ensuring that the regulatory

framework committed to in the pre-privatization phase will be preserved and not changed

unilaterally following the privatization

The PRG backstops the Government‟s debt obligation to a commercial bank (Citibank) who

issued the Letter of Credit (LC) that may be drawn by OSSH to compensate for a resulting loss

of revenue upon a non-compliance by ERE or the Government relating to the distribution tariff

formula, the full pass-through of the electricity costs and the timely approval of the tariffs

The PRG covers the first three regulatory periods until the end of 2014

Following any LC drawings, the Ministry of Finance is obligated to pay the withdrawn amount

to IBRD within 12-18 months

The PRG recognizes the compensation mechanism and the option of the Government to limit

the tariff increase at 15% (in real terms) and therefore as long as the tariff increase is at 15% +

inflation (if required), the LC cannot be withdrawn

• If the event is not remedied within

review/cure periods in the Government

Support Agreement (GSA), OSSH is

entitled to draw under the LC and the LC

amount is reduced by the amount of

drawing

• If this is disputed by the Government, the

claim will be referred to international

arbitration and in the mean time OSSH can

continue to draw provisional payments by

posting security in favor of the Government

Lessons Learned and Best Practices

Albania: Partial Risk Guarantee (PRG)

Source: World Bank

www-

wds.worldbank.org/.../280900

Mitigatingrisk0EMS0no.05.pdf

The World Bank Partial

Risk Guarantee

Tonci Bakovic

26

Lessons Learned and Best Practices

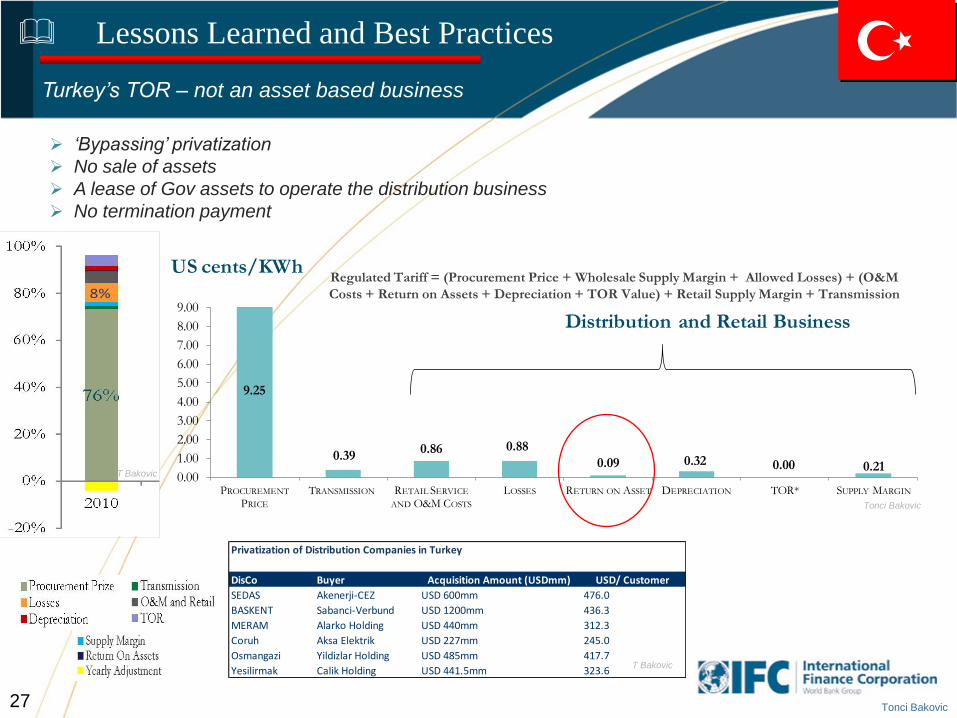

Turkey‟s Transfer of Operating Rights (TOR scheme)

Source: TEDAS

Tonci Bakovic 27

8%8%

7%3%

2.5%

T BakovicT Bakovic

9.25

0.390.86 0.88

0.09 0.32 0.00 0.210.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

PROCUREMENT

PRICE

TRANSMISSION RETAIL SERVICE

AND O&M COSTS

LOSSES RETURN ON ASSET DEPRECIATION TOR* SUPPLY MARGIN

US cents/KWh

Distribution and Retail Business

77.1% 2.7% 0%7.3% 1.7%3.2% 0.8%7.2%

Tonci Bakovic

Lessons Learned and Best Practices

Turkey‟s TOR – not an asset based business

„Bypassing‟ privatization

No sale of assets

A lease of Gov assets to operate the distribution business

No termination payment

Privatization of Distribution Companies in Turkey

1000

DisCo Buyer Acquisition Amount (USDmm) USD/ Customer

SEDAS Akenerji-CEZ USD 600mm 476.0

BASKENT Sabanci-Verbund USD 1200mm 436.3

MERAM Alarko Holding USD 440mm 312.3

Coruh Aksa Elektrik USD 227mm 245.0

Osmangazi Yildizlar Holding USD 485mm 417.7

Yesilirmak Calik Holding USD 441.5mm 323.6T Bakovic

Regulated Tariff = (Procurement Price + Wholesale Supply Margin + Allowed Losses) + (O&M

Costs + Return on Assets + Depreciation + TOR Value) + Retail Supply Margin + Transmission

Tonci Bakovic

28

India‟s Franchise Model

Green = Private

Black = Public

Hybrid Single Buyer Model and Power Exchange

Gov supports the creation of private power exchanges mainly to encourage captive generation

(cogen) to inject into the grid

Companies must prepay 2-days before transacting on exchange

Distribution “franchising” model gets implemented by some states given difficulties implementing

privatization

Lessons Learned and Best Practices

IPP1

Industry

State1

IPP2

IPPn

IPP3

State2

Staten

PTC

IEX

PXI

Private Power Exchanges(~2% of transactions)

(Pre-Pay Before Trade)

Single Buyer Mega Projects(Guarantees Off-Take)

Industry

Staten

Private Bilateral Contract

Traders

T Bakovic

Cogen

D1

D2

2 Discos Private(others franchising some localities)

Private Bilateral Cont.

“Franchise” Model:Locality/Region operation, within State distribution concession, awarded to private operators based on loss reduction and collection improvement targets.

38% of Consumption

Private Industry

Fed Gencos

State Gencos

Tonci Bakovic 29

Establish a fair mechanism to set-up the limits and a ‘smoothing mechanism’ of the power

purchase costs (pass-through)

Length of concession should be at least 30 years

In case of intervention or concession lapse, a clear ‘asset-transfer-mechanism’ must be established

indicating how the ‘terminal value’ of the concession will be determined

Establish clear and measurable quality standards in the concession and/or regulations and the

corresponding penalty levels

Obtain a technical audit of the starting distribution losses and agree on a realistic loss reduction

program for –at least- the first two regulatory periods. Audited losses should be disclosed at the

data-room before privatization

Clearly indicate and obtain regulatory approval for the investment program for the first regulatory

period

Clearly indicate the upper limit of the efficiency factor X -in at least the initial two regulatory

periods

Obtain an audit of the starting ‘accounts receivable’ of the disco and clearly indicate how much of

those receivables are ‘bad debt’. Audited bad-debt should be disclosed at the data-room before

privatization.

Clearly indicate who will have the responsibility to be SOLR and how ‘grey customers’ will be

treated

Avoid an intermediate ‘single-buyer’-between Generation and Distribution

Do not leave anything for approval post-privatization

– discount from purchase value information not provided at time of sale

Lessons Learned and Best Practices

Wish list…

Tonci Bakovic 30

The Regulatory Challenge of Asset Valuation: A Case Study from the Brazilian Electricity Distribution Sector

(Vivien Foster and Pedro Antmann)

Pass Through of Power Purchase Costs. Regulatory Challenges and International Practices (Beatriz Arizu,

Luiz Maurer, and Bernard Tenenbaum)

Mitigating Regulatory Risk for Distribution Privatization – The World Bank Partial Risk Guarantee (Pankaj

Gupta, Ranjit Lamech, Farida Mazhar, Joseph Wright)

The Single-Buyer Model: A Dangerous Path toward Competitive Electricity Markets (Laszlo Lovei)

The Regulation of Investment in Utilities Concepts and Applications (Ian Alexander, Clive Harris)

Regulation by Contract: A New Way to Privatize Electricity Distribution? (Tonci Bakovic, Bernard

Tenenbaum and Fiona Woolf)

Recommended Reading

World Bank Group – Two Decades of Regulatory Lessons