At the crossroads - Mirae Asset

61

Analysts who prepared this report are registered as research analysts in Indonesia but not in any other jurisdiction. PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT. Plantation At the crossroads Initiate coverage on the planation sector with a neutral stance Palm oil is one of vegetable oil which is consumed by people around the world. US Department of Agriculture (USDA) estimates 75% of palm oil is used for food and 25% for non-food purposes, such as biofuel. However, we expect clouded financial performance outlook of palm oil companies in the near horizon given lingering challenges. Our key concerns are: La Nina may potentially place negative impact on palm oil production while prolonged low commodity prices (in particular, crude oil) could keep palm oil less attractive. We initiate coverage on the plantation sector with a neutral call. We forecast global palm oil price to reach USD636/ton and USD674/ton in 2016F and 2017F, respectively. Our global palm oil projection is based on Brent crude oil price of USD45/barrel and USD47/barrel in 2016F and 2017F, respectively. Indonesia has a competitive advantage vs. Malaysia in terms of CPO supply Global palm oil production has been dominated by Indonesia and Malaysia which accounted for 85.4% of total global production (2015). Indonesia and Malaysia’s crude palm oil (CPO) production stood at 33.0mn tons and 20.5mn tons, respectively. We believe that Indonesia can maintain its position as the top-producer over the longer term on the back of improving oil palm yield and also larger oil palm plantation area compared to Malaysia. We predict that Indonesia’s palm oil production will reach 34.3mn tons and 35.7mn tons in 2016F and 2017F, respectively. We underscore that Indonesian palm production grew 6.8% CAGR from 2011 to 2015. Global palm oil consumption drivers are Indonesia and India We predict that global palm oil consumption will reach 63.3mn tons and 66.5mn tons in 2016F and 2017F, respectively, in-line with increasing population. Furthermore, we consider the key countries behind the robust global palm oil consumption to be Indonesia and India. Meanwhile, our key concern is that China’s palm oil consumption growth will decelerate, as the country’s vegetable oil consumption is shifting to rape and soybean oil. We predict that Indonesia’s palm oil consumption will reach 9.3mn tons and 10.0mn tons in 2016F and 2017F, respectively. We are less convinced that India would be independent from palm oil imports (chiefly due to the unfavorable geographic limitations) despite Indian government’s efforts to promote oil palm cultivation. Our top picks are LSIP and SSMS Within our plantation coverage, our top picks are: London Sumatra Indonesia (LSIP/ Buy) for its healthy balance sheet and Sawit Sumbermas Sarana (SSMS/ buy) for its high CPO yield. Meanwhile, we rate Sampoerna Agro (SGRO) a Hold due to its high interest expense burden and also call Astra Agro Lestrari (AALI) a Hold due to its old-age oil palm profile and diversification to the downstream business (which is expected to dilute its profitability margins). Risks to our call are 1) global CPO supply/demand imbalance, 2) volatility in global crude oil prices, 3) unpredictable regulation risks, 4) unexpected weather changes, and 5) weak infrastructure situations. Palm oil companies covered in this report Company name Ticker Rating TP (IDR) ROE (%) P/E (x) P/B (x) 2016F 2017F 2016F 2017F 2016F 2017F Astra Agro Lestari AALI HOLD 15,850 2.9 3.3 78.5 66.7 2.3 2.2 PP London Sumatra LSIP BUY 2,040 7.3 7.4 19.0 18.1 1.4 1.3 Sampoerna Agro SGRO HOLD 1,875 6.0 6.0 18.3 17.5 1.1 1.0 Sawit Sumbermas Sarana SSMS BUY 2,150 17.0 16.8 26.5 23.4 4.5 3.9 Source: Daewoo Securities Research Neutral (Initiate) Initiation August 30, 2016 PT Daewoo Securities Indonesia Agriculture Andy Wibowo Gunawan +62-21-515-1140 [email protected]

Transcript of At the crossroads - Mirae Asset

Analysts who prepared this report are registered as research analysts in Indonesia but not in any other jurisdiction. PLEASE SEE

ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Plantation At the crossroads

Initiate coverage on the planation sector with a neutral stance

Palm oil is one of vegetable oil which is consumed by people around the world. US

Department of Agriculture (USDA) estimates 75% of palm oil is used for food and 25%

for non-food purposes, such as biofuel. However, we expect clouded financial

performance outlook of palm oil companies in the near horizon given lingering

challenges. Our key concerns are: La Nina may potentially place negative impact on palm

oil production while prolonged low commodity prices (in particular, crude oil) could keep

palm oil less attractive. We initiate coverage on the plantation sector with a neutral call.

We forecast global palm oil price to reach USD636/ton and USD674/ton in 2016F and

2017F, respectively. Our global palm oil projection is based on Brent crude oil price of

USD45/barrel and USD47/barrel in 2016F and 2017F, respectively.

Indonesia has a competitive advantage vs. Malaysia in terms of CPO supply

Global palm oil production has been dominated by Indonesia and Malaysia which

accounted for 85.4% of total global production (2015). Indonesia and Malaysia’s crude

palm oil (CPO) production stood at 33.0mn tons and 20.5mn tons, respectively. We

believe that Indonesia can maintain its position as the top-producer over the longer term

on the back of improving oil palm yield and also larger oil palm plantation area compared

to Malaysia. We predict that Indonesia’s palm oil production will reach 34.3mn tons and

35.7mn tons in 2016F and 2017F, respectively. We underscore that Indonesian palm

production grew 6.8% CAGR from 2011 to 2015.

Global palm oil consumption drivers are Indonesia and India

We predict that global palm oil consumption will reach 63.3mn tons and 66.5mn tons in

2016F and 2017F, respectively, in-line with increasing population. Furthermore, we

consider the key countries behind the robust global palm oil consumption to be

Indonesia and India. Meanwhile, our key concern is that China’s palm oil consumption

growth will decelerate, as the country’s vegetable oil consumption is shifting to rape and

soybean oil. We predict that Indonesia’s palm oil consumption will reach 9.3mn tons and

10.0mn tons in 2016F and 2017F, respectively. We are less convinced that India would

be independent from palm oil imports (chiefly due to the unfavorable geographic

limitations) despite Indian government’s efforts to promote oil palm cultivation.

Our top picks are LSIP and SSMS

Within our plantation coverage, our top picks are: London Sumatra Indonesia (LSIP/ Buy)

for its healthy balance sheet and Sawit Sumbermas Sarana (SSMS/ buy) for its high CPO

yield. Meanwhile, we rate Sampoerna Agro (SGRO) a Hold due to its high interest

expense burden and also call Astra Agro Lestrari (AALI) a Hold due to its old-age oil palm

profile and diversification to the downstream business (which is expected to dilute its

profitability margins). Risks to our call are 1) global CPO supply/demand imbalance, 2)

volatility in global crude oil prices, 3) unpredictable regulation risks, 4) unexpected

weather changes, and 5) weak infrastructure situations.

Palm oil companies covered in this report

Company name Ticker Rating TP

(IDR)

ROE (%) P/E (x) P/B (x)

2016F 2017F 2016F 2017F 2016F 2017F

Astra Agro Lestari AALI HOLD 15,850 2.9 3.3 78.5 66.7 2.3 2.2

PP London Sumatra LSIP BUY 2,040 7.3 7.4 19.0 18.1 1.4 1.3

Sampoerna Agro SGRO HOLD 1,875 6.0 6.0 18.3 17.5 1.1 1.0

Sawit Sumbermas Sarana SSMS BUY 2,150 17.0 16.8 26.5 23.4 4.5 3.9

Source: Daewoo Securities Research

Neutral (Initiate)

Initiation

August 30, 2016

PT Daewoo Securities Indonesia

Agriculture

Andy Wibowo Gunawan

+62-21-515-1140

Plantation

2

August 30, 2016

Daewoo Securities Indonesia Research

Palm oil at glance

Palm oil is an important, yet versatile vegetable oil which is used by raw materials for both food

and non-food industries. US Department of Agriculture (USDA) estimates that 75% of palm oil is

used for food, and the remaining 25% for non-food. Palm oil can be extracted from both the fruit

(mesocarp) and the seed (kernel). Crude palm oil (CPO) is extracted from the mesocarp and is

mainly used for cooking purposes, while palm kernel oil is extracted from the kernel and is mainly

used in non-edible products such as detergents, cosmetics and plastics.

Quick facts about palm oil:

1. Palm oil trees can grow up to 20 meters tall with an average life of 25 years.

2. Palm oil tress grow across or 10 degrees north or south of the equator.

3. The tree starts to bear fresh fruit bunches (FFB) after three years.

4. Palm oil can be harvested every 12 months of the year.

Figure 1. Cross section of an oil palm fruit Figure 2. Palm oil usage

Source: Centre for International Forestry Research, Daewoo Securities Research

Source: USDA, Daewoo Securities Research

Figure 3. Fresh fruit bunch picture Figure 4. Palm oil tree

Source: greenstokmedia.com, Daewoo Securities Research

Source: tdg24.com, Daewoo Securities Research

A young palm tree produces about 30 leaves a year. Established palms over 10 years produce

about 20 leaves a year. The flowers are produced in dense clusters and each individual flower is

small, with three sepals and three petals. The palm fruit takes five to six months to mature from

pollination to maturity. It is reddish, about the size of a large plum, and grows in large bunches.

Each fruit is covered up with an oily, fleshy outer layer (the pericarp), with a single seed (the palm

kernel), which is also rich in oil. When ripe, each fruit bunch weighs between 5–30kg depending on

the age.

75

25

Food

Non-food

(%)

Plantation

3

August 30, 2016

Daewoo Securities Indonesia Research

Oil palms generally begin to produce fruits three years after being planted in the fields with

commercial harvest able to be commenced six months later. However, the yield of an oil palm is

relatively low at this stage. As the oil palm continues to mature, its yield increases and it reaches

peak production during ages from 7 to 13 years old. Yield starts to gradually decrease after 14

years. The typical commercial lifespan of an oil palm is approximately 25 years.

Fully mature oil palms produce 18 to 30 metric tons of FFB per hectare. The yield depends on a

variety of factors, including age, seed quality, soil and climatic conditions, quality of plantation

management and the timely harvesting and processing of FFB. The ripeness of FFB harvested is

critical in maximizing the quality and quantity of palm oil extracted. Harvested fruits must be

processed within 24 hours to minimize the build-up of free fatty acids (FFA).

Figure 5. Palm oil yield & age profile Figure 6. CPO usage based on FFA

Source: Palmoilworld, Daewoo Securities Research

Source: Nippon-cnpc, Daewoo Securities Research

Milling of FFB takes place within 24 hours from the harvesting of FFB. They are initially transferred

to the palm oil mills for sterilization by applying high-pressure steam, whereupon the palm fruits

are enzyme-deactivated and separated from the palm bunches.

After steaming, the palm fruitlets are crushed in a pressing machine to obtain CPO and palm kernel.

Waste and water is then cleared and separated from the CPO by means of a centrifuge. The

cleared crude palm oil emerging from the centrifuge is then sent for refining while the palm kernel

nut is sent for crushing. The empty fruit bunches and liquid waste arising from the processing are

recycled as fertilizer in the plantations.

Figure 7. Palm oil supply chain

Source: Alibaba, Daewoo Securities Research

Palm oil mill

High FFA CPO

(FFA: 20% - 30% )

CPO

(FFA: <5% )Palm acid oil (PAO)

(FFA: >30% )

Non Food Food Non Food

Plantation

4

August 30, 2016

Daewoo Securities Indonesia Research

Indonesia to maintain its position as the top producer

Global palm oil production had been dominated by Indonesia and Malaysia which accounted to

85.4% of global total production by 2015. Last year, Indonesia and Malaysia produced 33.0mn tons

and 20.5mn tons respectively. Rewinding back to 1980, Indonesia palm oil production represented

a mere 14.3% of total global production (702,000 tons), while Malaysia dominated up to 51.9% of

total global production (2.5mn tons). 26 years later, Indonesia overtook the first place as the top

global palm oil producer. The mainly reason was dramatically increased area under plantation.

In terms of amount, Indonesia’s palm oil production jumped more than double to 33.0mn tons in

2015, compared to a decade ago which stood at 13.6mn tons. Meanwhile, Malaysia palm oil

production increased to 20.5mn tons in 2015, from 15.2mn tons in 2005. This was mainly because

Indonesia has larger plantation area compared to Malaysia. All in all, Indonesia is expected to

produce more than 40.0mn tons of palm oil by 2020 without any expansion plans, according to

Indonesia Sustainable Palm Oil (ISPO). Furthermore, smallholders palm oil plantation in Indonesia is

known to own an average farm size of 4.0~ 6.0 ha which would equate to an aggregate total of

1.0mn ha~ 1.5mn ha across the nation.

Figure 8. Indonesia & Malaysia palm oil production trends Figure 9. Indonesia the first rank as producer since 2006

Source: Bloomberg, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

Indonesia oil palm yield improved, despite lower than Malaysia

By 2015, Indonesia oil palm yield had increased to 3.7ton/ha – an improvement by 0.6ton/ha

compared to 1979. However this improvement fell slightly below Malaysian oil palm yield which

stood at 3.8ton/ha, last year. We ascribe the more sophisticated cultivation technique to be one of

the reasons why Malaysian oil palm yield was higher than Indonesia. Meanwhile, younger palm oil

age in Indonesia is another reason why Indonesian oil palm yield was lower, in our view. We

consider Malaysia’s early palm oil cultivation (vs. Indonesia) to be a key advantage of its stellar yield.

Figure 10. Malaysia has higher palm oil yield Figure 11. However Indonesia palm oil yield improved

Source: USDA, MPOB, Daewoo Securities Research

Source: USDA, Utrecht University, Daewoo Securities Research

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

('000 tons) Indonesia Malaysia

-

20.0

40.0

60.0

80.0

100.0

120.0

(%) Indonesia Malaysia Others

3.7

3.8

3.6

3.7

3.7

3.8

3.8

3.9

3.9

Indonesia Malaysia

(ton/ha)

3.1

3.6

3.5 3.5

3.7

2.8

2.9

3

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8

1979 1989 1999 2005 2015

(ton/ha)

Plantation

5

August 30, 2016

Daewoo Securities Indonesia Research

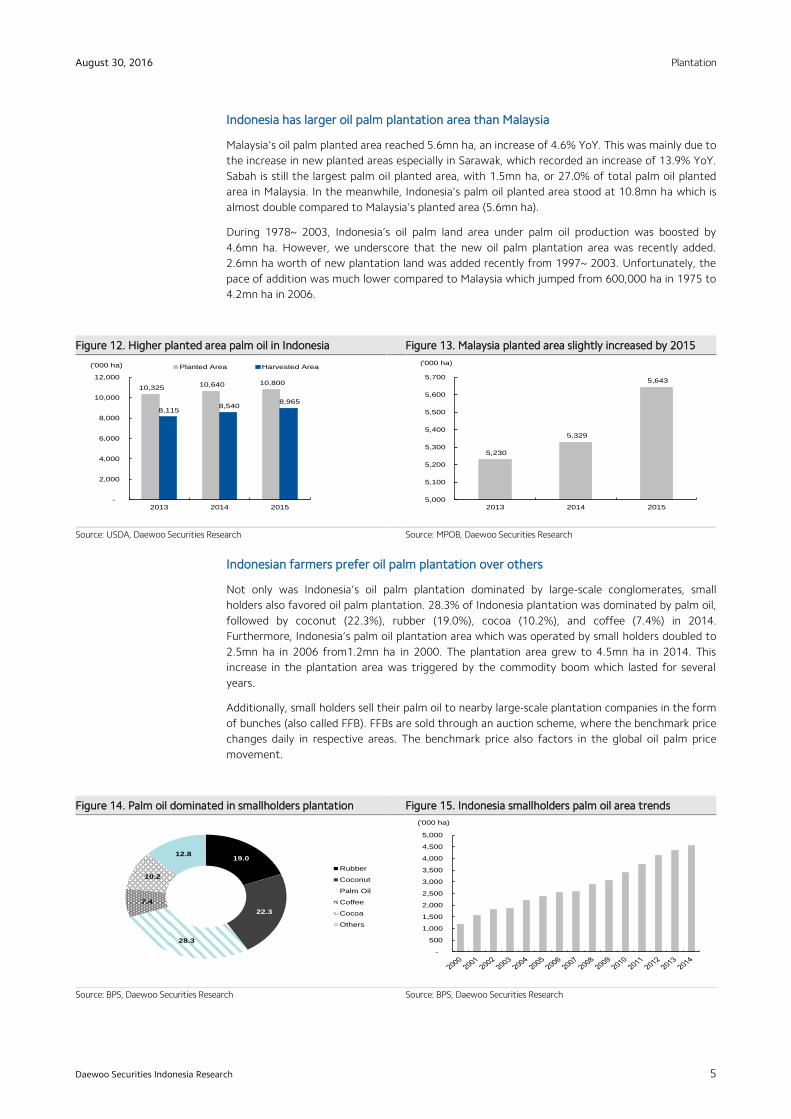

Indonesia has larger oil palm plantation area than Malaysia

Malaysia’s oil palm planted area reached 5.6mn ha, an increase of 4.6% YoY. This was mainly due to

the increase in new planted areas especially in Sarawak, which recorded an increase of 13.9% YoY.

Sabah is still the largest palm oil planted area, with 1.5mn ha, or 27.0% of total palm oil planted

area in Malaysia. In the meanwhile, Indonesia’s palm oil planted area stood at 10.8mn ha which is

almost double compared to Malaysia’s planted area (5.6mn ha).

During 1978~ 2003, Indonesia’s oil palm land area under palm oil production was boosted by

4.6mn ha. However, we underscore that the new oil palm plantation area was recently added.

2.6mn ha worth of new plantation land was added recently from 1997~ 2003. Unfortunately, the

pace of addition was much lower compared to Malaysia which jumped from 600,000 ha in 1975 to

4.2mn ha in 2006.

Figure 12. Higher planted area palm oil in Indonesia Figure 13. Malaysia planted area slightly increased by 2015

Source: USDA, Daewoo Securities Research

Source: MPOB, Daewoo Securities Research

Indonesian farmers prefer oil palm plantation over others

Not only was Indonesia’s oil palm plantation dominated by large-scale conglomerates, small

holders also favored oil palm plantation. 28.3% of Indonesia plantation was dominated by palm oil,

followed by coconut (22.3%), rubber (19.0%), cocoa (10.2%), and coffee (7.4%) in 2014.

Furthermore, Indonesia’s palm oil plantation area which was operated by small holders doubled to

2.5mn ha in 2006 from1.2mn ha in 2000. The plantation area grew to 4.5mn ha in 2014. This

increase in the plantation area was triggered by the commodity boom which lasted for several

years.

Additionally, small holders sell their palm oil to nearby large-scale plantation companies in the form

of bunches (also called FFB). FFBs are sold through an auction scheme, where the benchmark price

changes daily in respective areas. The benchmark price also factors in the global oil palm price

movement.

Figure 14. Palm oil dominated in smallholders plantation Figure 15. Indonesia smallholders palm oil area trends

Source: BPS, Daewoo Securities Research

Source: BPS, Daewoo Securities Research

10,325 10,640 10,800

8,115 8,540

8,965

-

2,000

4,000

6,000

8,000

10,000

12,000

2013 2014 2015

('000 ha) Planted Area Harvested Area

5,230

5,329

5,643

5,000

5,100

5,200

5,300

5,400

5,500

5,600

5,700

2013 2014 2015

('000 ha)

19.0

22.3

28.3

7.4

10.2

12.8

Rubber

Coconut

Palm Oil

Coffee

Cocoa

Others

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

('000 ha)

Plantation

6

August 30, 2016

Daewoo Securities Indonesia Research

Cooperation with external parties to secure FFB stocks

Occasionally, palm oil companies experience supply shortage in FFBs. Thus, palm oil companies

must secure FFBs from third parties to keep the mills running. However, purchase from third

parties is unsustainable and thus cannot be a long-term resolution. Hence, palm oil companies

additionally secure their long-term FFB supplies through cooperation with local farmers who reside

around the plantation area. This cooperation is called plasma scheme. The following is an example

of a plasma cooperation scheme:

1. Bank will assess the capability of farmers (plasma)

2. Both parties will sign a MoU and explain the rights and obligations

3. After the signing of MoU, palm oil companies will provide debt facilities to finance the

plasma plantation

4. Plasma farmers will receive the funds from palm oil companies (nucleus)

5. Plasma farmers will pay installment to nucleus by selling their FFB to nucleus

Figure 16. Plasma plantation schemes flow

Source: Agrindo Group, Daewoo Securities Research

Figure 17. Plasma plantation work periods

Source: Agrindo Group, Daewoo Securities Research

BANK

Nucleus

(Palm Oil

Company)

Cooperative

Farmers

(Plasma)

Memorandum of

Understanding

1

2

3

4

5

Development Stage Mature Plantation Stage

Tolerance period Return period

0 – 5 year 6 – 13 year

Plantation

7

August 30, 2016

Daewoo Securities Indonesia Research

A stepping stone to securing new land bank

On May 20, 2011, Indonesian government released presidential instruction No.10/2011 on “The

postponement of issuance of new licenses and improving governance of primary resources natural

forest and peatland”. The presidential instruction had effectively imposed a 2-year moratorium on

new forest concession licenses. President Jokowi will also issue a moratorium policy for peatland

through instructional president, but it has yet to be declared. This new policy will place negative

implications on palm oil companies as it would be tougher to acquire new land-bank. That being

said, the new policy should act as a key obstacle for expansion of palm oil companies.

According to the Ministry of Agriculture, most of Indonesia peatland are located in Sumatra Island

which contributed to 43.2% of total peatland, followed by Kalimantan and Papua islands which

contributed 32.1% and 24.8%, respectively in 2011. In Indonesia, peatland is categorized into four

tiers based on the thickness of peatland soil. Tiers 1 is the lowest level which has 50 – 100cm of

thickness, whereas tiers 2, 3, and 4 have 101 – 200cm, 201 – 400cm and >400cm thickness,

respectively.

Figure 18. Sumatra peat-land spots Figure 19. Kalimantan peat-land spots

Source: Wetlands International, Daewoo Securities Research

Source: Wetland International, Daewoo Securities Research

Table 1. Indonesia pet-land area with its thickness (‘000 hectare)

Region Thickness Large (%) of total

D1 D2 D3 D4

Sumatra 1,767.3 1,707.8 1,243.0 1,718.6 6,436.6 43.2

Kalimantan 1,048.6 1,389.8 1,072.8 1,266.8 4,778.0 32.1

Papua 2,425.5 817.7 447.7 - 3,690.9 24.8

Total 5,241.4 3,915.3 2,763.5 2,985.4 14,905.6 100.0

Source: Indonesia Agriculture Ministry, Daewoo Securities Research

Plantation

8

August 30, 2016

Daewoo Securities Indonesia Research

After dry El Nino, will La Nina occur?

Last year, it was a dry season for Indonesia where palm oil production dropped more than 5% YoY

compared to previous periods. We ascribe this dryness to the El Nino phenomenon. El Nino is a

band of warm ocean water that develops in the central and east-central equatorial pacific. El Nino

is accompanied by high air pressure in the western pacific and low air pressure in the eastern

pacific. There have been approximately 30 El Nino events since 1900, with the 1982-83, 1997-98,

and 2014-16 events which were among the strongest in history.

Figure 20. Southern oscillation index trend

Source: NOAA, Daewoo Securities Research

However, some meteorologists elsewhere (i.e., Australia, USA & Indonesia) predict that the

chances of La Nina in 2016 has increased. According to Australian Bureau Meteorology (BOM),

climate models are indicating 50% possibility of the wet weather event emerging this year (La Nina

is the opposite of the dry El Nino).

We predict that it could further disrupt supply of palm oil this year, as we think La Nina could

cause logistic problems during harvesting seasons. Generally, as the plantation area’s earth is soft

nature, this acts as challenge for farmers to transport FFB down to the main road. Given Indonesia

and Malaysia are the largest palm oil producers, we believe the supply disruptions should drive

global palm oil prices higher.

Figure 21. Rainfall probability distribution Figure 22. Character rainfall probability distribution

Source: BMKG, Daewoo Securities Research

Source: BMKG, Daewoo Securities Research

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Jan-

90

Aug

-90

Mar

-91

Oct

-91

May

-92

Dec

-92

Jul-9

3

Feb-

94

Sep

-94

Apr

-95

Nov

-95

Jun-

96

Jan-

97

Aug

-97

Mar

-98

Oct

-98

May

-99

Dec

-99

Jul-0

0

Feb-

01

Sep

-01

Apr

-02

Nov

-02

Jun-

03

Jan-

04

Aug

-04

Mar

-05

Oct

-05

May

-06

Dec

-06

Jul-0

7

Feb-

08

Sep

-08

Apr

-09

Nov

-09

Jun-

10

Jan-

11

Aug

-11

Mar

-12

Oct

-12

May

-13

Dec

-13

Jul-1

4

Feb-

15

Sep

-15

Plantation

9

August 30, 2016

Daewoo Securities Indonesia Research

Palm oil dominated vegetable oils consumption around the world

Edible vegetable oils are some of the most crucial cooking oil ingredients in the world and the

world vegetable oil consumption increased continuously to 173.3mn tons in 2015, or 4.5% CAGR

2011-2015 which was in-line with the global population growth (0.7% CAGR 2011~ 2015). By 2015,

palm oil still dominated as the key vegetable oil consumption which accounted for 35.0% of total

global vegetable oil consumption, followed by soybean, canola, sunflower, and others which

represented 27.0%, 15.6%, 8.8% and 13.6%, respectively.

Figure 23. Global vegetables oil consumption Figure 24. Palm oil was the largest vegetables oil consumption

Source: Statista, Daewoo Securities Research

Source: Statista, Daewoo Securities Research

Global palm oil consumption will be driven by India & Indonesia

Overall, global palm oil consumption increased to 60.3mn tons, or up 5.2% CAGR during 2011 –

2015. This growth was triggered by higher consumption of palm oil in India, Indonesia, and

Eurozone which reached 10.1mn, 8.6mn, and 6.6mn tons, respectively. By contrast, Malaysia and

China palm oil consumption decreased by 5.1% and 1.8% CAGR during 2011 – 2015, respectively

to 3.4mn and 5.8mn tons. Malaysia and China palm oil consumption accounted for 5.6% and 9.5%

of total global consumption in 2015 (vs. 8.4% and 12.5% of total global consumption in 2011). In

addition, the decline in China’s palm oil consumption was largely due to higher soybean import,

which amounted to 81.7mn tons (+14.5% YoY) in 2015 compared to its previous year.

We believe that global palm oil consumption growth will be driven by India and Indonesia on the

back of robust population growth and rising biodiesel consumption in Indonesia. Therefore, we are

optimistic that global consumption of palm oil will reach 63.3mn tons and 66.5mn tons in 2016F

and 2017F, respectively. Meanwhile, our main concern is the potential sharp decline in China’s palm

oil consumption on the back of shifting to rape and soybean oil consumption.

Figure 25. Global palm oil consumption still grow Figure 26. Global portfolio consumption palm oil by 2015

Source: Bloomberg, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

35.0

27.0

15.6

8.8

13.6

Palm Oil

Soybean

Canola

Sunflower

Others

(%)

145.3

151.8

157.7

166.3

173.3

130.0

135.0

140.0

145.0

150.0

155.0

160.0

165.0

170.0

175.0

180.0

2011 2012 2013 2014 2015

(mn tons)

-

50.0

100.0

150.0

200.0

250.0

India Indonesia China Eurozone Malaysia Others

2011 2012 2013 2014 2015(%)

49,343

54,125 57,044 57,393

60,324

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2011 2012 2013 2014 2015

('000 tonnes)

Plantation

10

August 30, 2016

Daewoo Securities Indonesia Research

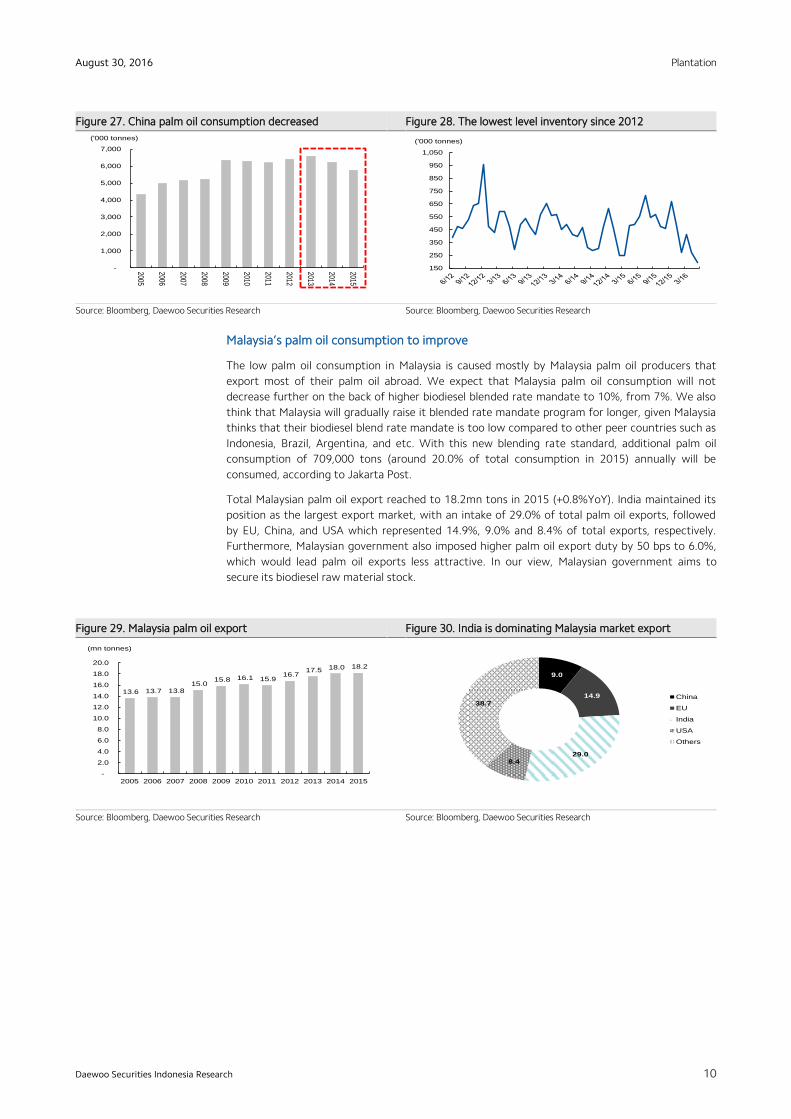

Figure 27. China palm oil consumption decreased Figure 28. The lowest level inventory since 2012

Source: Bloomberg, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

Malaysia’s palm oil consumption to improve

The low palm oil consumption in Malaysia is caused mostly by Malaysia palm oil producers that

export most of their palm oil abroad. We expect that Malaysia palm oil consumption will not

decrease further on the back of higher biodiesel blended rate mandate to 10%, from 7%. We also

think that Malaysia will gradually raise it blended rate mandate program for longer, given Malaysia

thinks that their biodiesel blend rate mandate is too low compared to other peer countries such as

Indonesia, Brazil, Argentina, and etc. With this new blending rate standard, additional palm oil

consumption of 709,000 tons (around 20.0% of total consumption in 2015) annually will be

consumed, according to Jakarta Post.

Total Malaysian palm oil export reached to 18.2mn tons in 2015 (+0.8%YoY). India maintained its

position as the largest export market, with an intake of 29.0% of total palm oil exports, followed

by EU, China, and USA which represented 14.9%, 9.0% and 8.4% of total exports, respectively.

Furthermore, Malaysian government also imposed higher palm oil export duty by 50 bps to 6.0%,

which would lead palm oil exports less attractive. In our view, Malaysian government aims to

secure its biodiesel raw material stock.

Figure 29. Malaysia palm oil export Figure 30. India is dominating Malaysia market export

Source: Bloomberg, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

13.6 13.7 13.8 15.0

15.8 16.1 15.9 16.7

17.5 18.0 18.2

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

(mn tonnes)

9.0

14.9

29.0 8.4

38.7 China

EU

India

USA

Others

150

250

350

450

550

650

750

850

950

1,050

('000 tonnes)

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

('000 tonnes)

Plantation

11

August 30, 2016

Daewoo Securities Indonesia Research

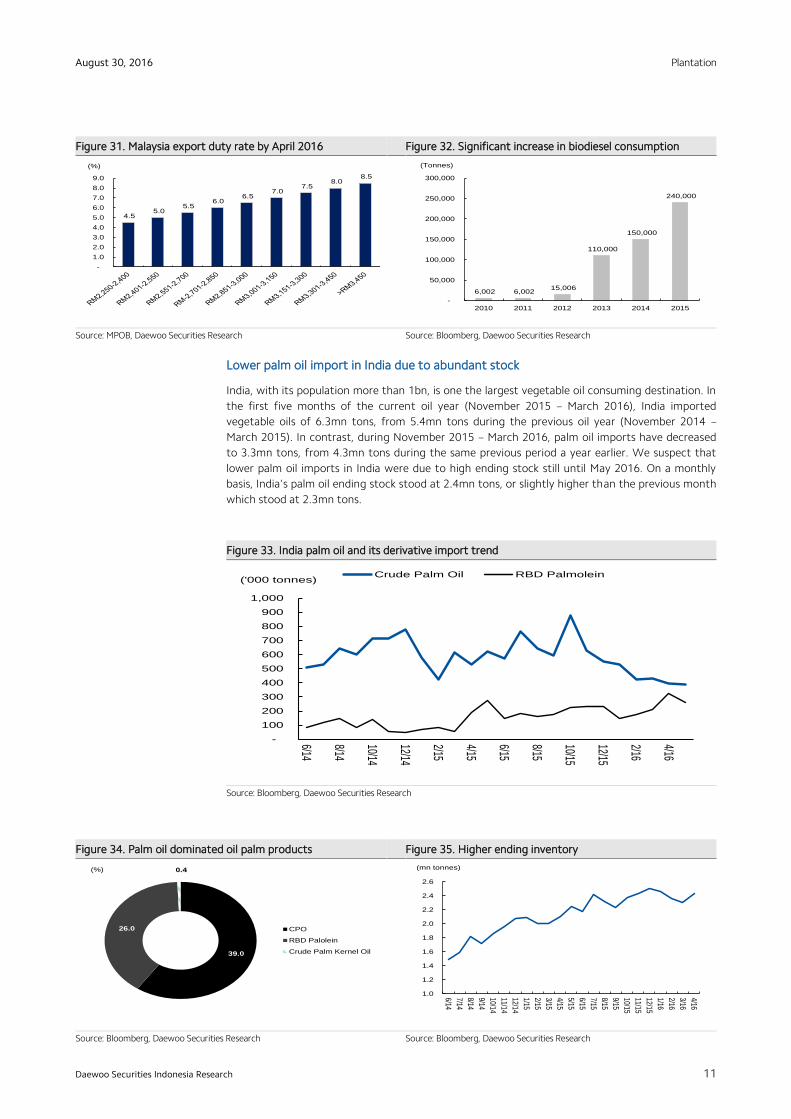

Figure 31. Malaysia export duty rate by April 2016 Figure 32. Significant increase in biodiesel consumption

Source: MPOB, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

Lower palm oil import in India due to abundant stock

India, with its population more than 1bn, is one the largest vegetable oil consuming destination. In

the first five months of the current oil year (November 2015 – March 2016), India imported

vegetable oils of 6.3mn tons, from 5.4mn tons during the previous oil year (November 2014 –

March 2015). In contrast, during November 2015 – March 2016, palm oil imports have decreased

to 3.3mn tons, from 4.3mn tons during the same previous period a year earlier. We suspect that

lower palm oil imports in India were due to high ending stock still until May 2016. On a monthly

basis, India’s palm oil ending stock stood at 2.4mn tons, or slightly higher than the previous month

which stood at 2.3mn tons.

Figure 33. India palm oil and its derivative import trend

Source: Bloomberg, Daewoo Securities Research

Figure 34. Palm oil dominated oil palm products Figure 35. Higher ending inventory

Source: Bloomberg, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

-

100

200

300

400

500

600

700

800

900

1,000

6/14

8/14

10/14

12/14

2/15

4/15

6/15

8/15

10/15

12/15

2/16

4/16

('000 tonnes)Crude Palm Oil RBD Palmolein

39.0

26.0

0.4

CPO

RBD Palolein

Crude Palm Kernel Oil

(%)

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

6/14

7/14

8/14

9/14

10/14

11/14

12/14

1/15

2/15

3/15

4/15

5/15

6/15

7/15

8/15

9/15

10/15

11/15

12/15

1/16

2/16

3/16

4/16

(mn tonnes)

4.5 5.0

5.5 6.0

6.5 7.0

7.5 8.0

8.5

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

(%)

6,002 6,002 15,006

110,000

150,000

240,000

-

50,000

100,000

150,000

200,000

250,000

300,000

2010 2011 2012 2013 2014 2015

(Tonnes)

Plantation

12

August 30, 2016

Daewoo Securities Indonesia Research

Can India break free from palm oil imports?

On the other hand, in order to bolster its edible oil security, India is aggressively pushing for oil

palm cultivation in the country despite its well documented deleterious socio-economy and

ecological impact. Furthermore, India’s edible oil import bill (around USD10bn in 2015) often

remains a focus for business and policy debates and once again policy makers have taken up the

gauntlet to make India self-sufficient in its edible oil requirements. On August 18, 2015, Prime

Minister Modi’s plan to commit USD1.5bn over three years pushed palm oil cultivation higher in

India. This stated target is to take India’s production of palm oil to 8mn tons. We are however less

optimistic that the target will be achieved in the longer term due to structural problems which has

been faced by India, while we believe that India is still a net importer of palm oil products.

Our first argument why India would be hard for India to meet its target in palm oil cultivation is

the unfavorable geographic location. As mentioned above, the ideal locations for oil palm trees are

within ten degrees latitude north and south equator. However, India’s geographic location is not

near the equatorial zone. The geographic location is also related with a climate of a country, while

major India’s climate is four-seasons which definitely it is not appropriate for palm oil tree

cultivation. In addition, long gestation period for palm oil is also our concern because farmers

would have to wait for four years for the trees in India to start yielding FFB.

Figure 36. India geography above equatorial zone

Source: Google maps, Daewoo Securities Research

Table 2. Oil palm plantation area in India (hectares)

State Potential Area Covered Area

Andaman & Nicobar - 1,593

Andhra Pradesh 400,000 96,563

Assam - 10

Chhattisgarh 40,000 -

Goa 2,000 874

Gujarat 90,000 2,175

Karnataka 250,000 18,906

Kerala 6,500 5,501

Maharashtra - 1,000

Mizoram 61,000 7,881

Orissa 25,000 3,775

Tamil Nadu 162,000 16,394

Tripura - 530

West Bengal - -

Total 1,036,500 155,202

Source: Chadha committee, Daewoo Securities Research

Plantation

13

August 30, 2016

Daewoo Securities Indonesia Research

How about Indonesia palm oil consumption?

Indonesia palm oil consumption jumped fourfold over the last two decades to 8.6mn tons in 2015.

This amazing growth was chiefly driven by increased population which reached 256mn people in

2015, from 198mn people in 1995. More than 50% of palm oil was used for cooking oil and

remaining was used for the margarine, and biodiesel. We believe that Indonesia’s palm oil

consumption will reach 9.3mn tons and 10.0mn tons in 2016F and 2017F, respectively on the back

of steady population growth and higher biodiesel consumption.

Figure 37. Indonesia palm oil consumption in-line with population

Source: Bloomberg, Daewoo Securities Research

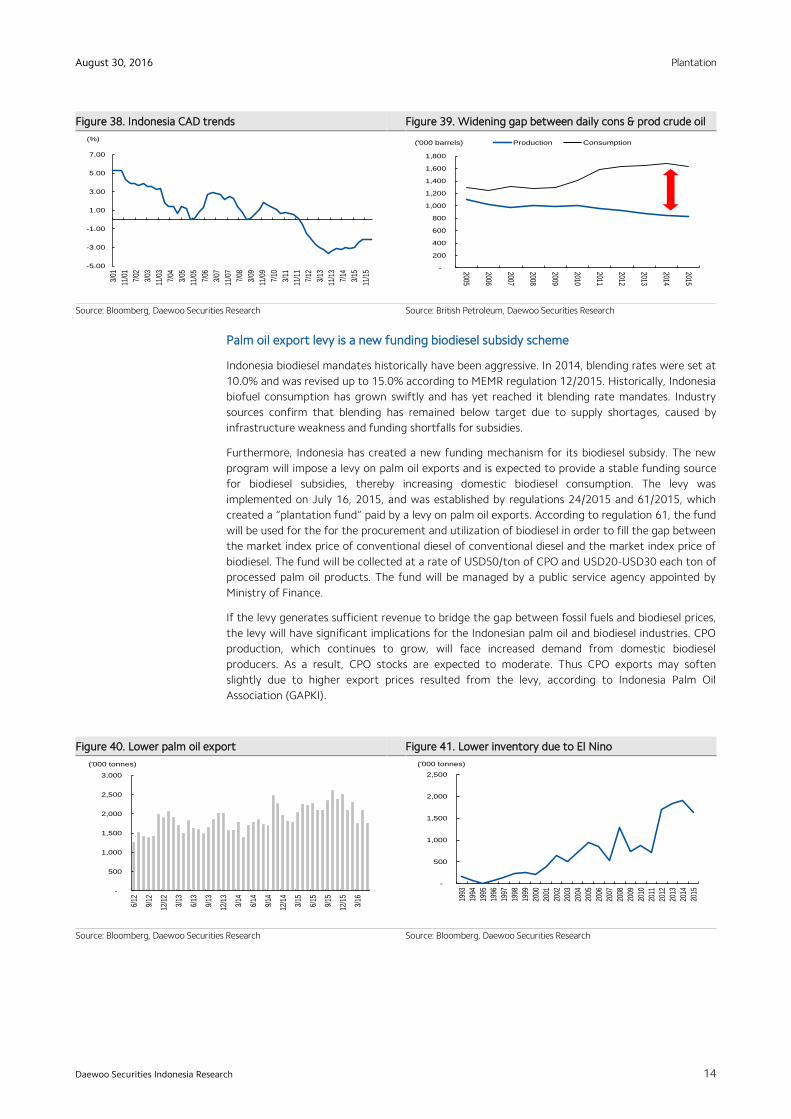

Palm oil is one of the biofuel alternatives for Indonesia

Since 1Q12 Indonesia’s current account deficit (CAD) to GDP crossed the negative territory

beginning with -0.51% and gradually fell deeper to -3.62% in 3Q13. Since the trough, Indonesia’s

CAD to GDP has gradually improved to -2.12% by 1Q16. Our assessment is that the current

account deficit was mainly driven by higher crude oil import stemming from increased car sales

which led to higher gasoline consumption. Indonesia’s daily crude oil consumption increased to

1.6mn barrels/day in 2015 from 1.3mn barrels/day in 2005. Meanwhile, daily production of crude

oil decreased to 825,000barrels/day in 2015, from 1.1mn barrels/day in a decade earlier. Because

of this structural problem, Indonesian government began to promote biodiesel as one of the fuel

alternatives which is mainly taken from palm oil. Indonesia’s biofuel policy is governed by a number

of regulations and decrees. Government regulation 1/2006 was an important first step for the

development of biofuels in Indonesia. In 2008, Indonesian government created a biofuel blending

rate mandate through Ministry of Energy & Mineral (MEMR) regulation 32. The blending rate

mandate regulation has been revised several times, most recently through MEMR regulation 12,

released in March 2015. Additionally, biofuel is energy made from living matter, usually plants.

Bioethanol, biogas and biodiesel are types of biofuels.

Biodiesel is used in standard diesel engine and is thus distinct from the vegetable and waste oils

converted for diesel engines. Biodiesel can be used alone, or blended with petro diesel in any

proportions. Biodiesel blends also can be used as heating oil. Blends of biodiesel and conventional

hydrocarbon-based diesel are products most commonly distributed for use in the retail diesel fuel

marketplace. Much of the world uses a system known as the “B” factor to state the amount of

biodiesel in any fuel mix. A 100% biodiesel is referred to as B100, A 20% of biodiesel and 80%

petro-diesel is labeled B20, and so on. A 55% of biodiesel can be used from palm oil and remaining

be used from other vegetable oils such as soybean, rapeseed, and etc.

50

100

150

200

250

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

(mn people)('000 tonnes)

Indonesia CPO Consumption Population

Plantation

14

August 30, 2016

Daewoo Securities Indonesia Research

Figure 38. Indonesia CAD trends Figure 39. Widening gap between daily cons & prod crude oil

Source: Bloomberg, Daewoo Securities Research

Source: British Petroleum, Daewoo Securities Research

Palm oil export levy is a new funding biodiesel subsidy scheme

Indonesia biodiesel mandates historically have been aggressive. In 2014, blending rates were set at

10.0% and was revised up to 15.0% according to MEMR regulation 12/2015. Historically, Indonesia

biofuel consumption has grown swiftly and has yet reached it blending rate mandates. Industry

sources confirm that blending has remained below target due to supply shortages, caused by

infrastructure weakness and funding shortfalls for subsidies.

Furthermore, Indonesia has created a new funding mechanism for its biodiesel subsidy. The new

program will impose a levy on palm oil exports and is expected to provide a stable funding source

for biodiesel subsidies, thereby increasing domestic biodiesel consumption. The levy was

implemented on July 16, 2015, and was established by regulations 24/2015 and 61/2015, which

created a “plantation fund” paid by a levy on palm oil exports. According to regulation 61, the fund

will be used for the for the procurement and utilization of biodiesel in order to fill the gap between

the market index price of conventional diesel of conventional diesel and the market index price of

biodiesel. The fund will be collected at a rate of USD50/ton of CPO and USD20-USD30 each ton of

processed palm oil products. The fund will be managed by a public service agency appointed by

Ministry of Finance.

If the levy generates sufficient revenue to bridge the gap between fossil fuels and biodiesel prices,

the levy will have significant implications for the Indonesian palm oil and biodiesel industries. CPO

production, which continues to grow, will face increased demand from domestic biodiesel

producers. As a result, CPO stocks are expected to moderate. Thus CPO exports may soften

slightly due to higher export prices resulted from the levy, according to Indonesia Palm Oil

Association (GAPKI).

Figure 40. Lower palm oil export Figure 41. Lower inventory due to El Nino

Source: Bloomberg, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

('000 barrels) Production Consumption

-5.00

-3.00

-1.00

1.00

3.00

5.00

7.00

3/01

11/0

1

7/02

3/03

11/0

3

7/04

3/05

11/0

5

7/06

3/07

11/0

7

7/08

3/09

11/0

9

7/10

3/11

11/1

1

7/12

3/13

11/1

3

7/14

3/15

11/1

5

(%)

-

500

1,000

1,500

2,000

2,500

3,000

6/12

9/12

12/1

2

3/13

6/13

9/13

12/1

3

3/14

6/14

9/14

12/1

4

3/15

6/15

9/15

12/1

5

3/16

('000 tonnes)

-

500

1,000

1,500

2,000

2,500

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

('000 tonnes)

Plantation

15

August 30, 2016

Daewoo Securities Indonesia Research

Changing in the reference rate of biodiesel

Indonesian biodiesel producers incurred heavy losses following the 2014 drop in crude oil prices.

This led to the abandonment of previous subsidy programs in February 2015 and the enactment of

a new biofuels price index formula in March 2015 through MEMR regulation 726/2015. Previously,

Indonesia’s biodiesel reference price was based on the Mean of Platts Singapore (MOPS) price.

According to MEMR 726, the MOPS price has been replaced by the current market price of CPO.

The new price formula covers biodiesel production costs and a 3% of margin. The government

expects the new biofuels price index formula to more accurately reflect market dynamics. Post

notes that revisions to the reference price have been ongoing throughout 2015, and as a result,

biofuel subsidies have not been provided for most of the calendar year. The reference price

formula is critical in determining the size of the payment subsidy to bridge the gap between

biodiesel and diesel, and therefore it is critical to meeting the new mandates. With this

implementation of the palm oil levy in July, the Indonesian Biofuel Producers Association expects

that the subsidy will be fully implemented in September at a 15% blended rate.

Figure 42. Crude oil price trend

Source: Bloomberg, Daewoo Securities Research

Indonesia biodiesel consumption outlook

The new biofuels mandatory program is expected to increase domestic biodiesel consumption. If

Indonesia continues on track with its blending mandate, it can consume 2.7bn liters in 2016F

(2015: 1.45bn liters), according to USDA. Under the new regulation, targeted blending rate for the

transportation and industrial sectors was lifted from 10% to 15% as of April 2015. However, some

concerns have been raised by industry associations and state electricity operator (PLN) regarding

the 25% targeted blending rate for electricity, noting that the mandated blend rate exceeds the

capacity of their generators.

Figure 43. Indonesia biodiesel consumption trend Figure 44. Biodiesel mandatory target history

Source: USDA, Daewoo Securities Research

Source: USDA, Daewoo Securities Research

220 258

670

1,048

1,600

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2010 2011 2012 2013 2014

(mn liters)

1,076 1,297

1,641

2,017

4,000

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2010 2011 2012 2013 2014

(mn liters)

-

20.0

40.0

60.0

80.0

100.0

120.0

11/1

0

3/11

7/11

11/1

1

3/12

7/12

11/1

2

3/13

7/13

11/1

3

3/14

7/14

11/1

4

3/15

7/15

11/1

5

3/16

(USD/barrel) WTI Brent

Plantation

16

August 30, 2016

Daewoo Securities Indonesia Research

Global palm oil prices outlook?

Global palm oil consumption is expected to increase and we expect supply disruption on the back

of La Nina. At the same time, we believe that global palm oil price movement shows positive

correlation with global crude oil price. We suspect that biofuel production has created a new

linkage between crude oil and palm oil. As a natural resource that is not renewable, market has

been concerned about the declining crude oil reserves; given crude oil is one of human needs which

cannot be discharged in our daily lives. Thus, during the search for new energy alternatives that

can be renewable, it turns out that palm oil can be used as an alternative to cater energy needs in

the future. We predict that global palm oil will reach USD636/ton and USD674/ton in 2016F and

2017F, respectively. Our global palm oil prediction is based on crude oil (Brent crude) price outlook

of USD45.0/barrel and USD47.0/barrel in 2016F and 2017F, respectively.

A 2016 survey of the academic literature finds that “most major oil price dating back to 1973 was

largely explained by shifts in the demand for crude oil”. As the global economy expands, so does

demand for crude oil. On supply side, crude oil is dependent on geological discovery, the legal and

tax framework for oil extraction, the cost of extraction, the availability and cost of technology for

extraction, and the political situation in oil-producing countries.

Figure 45. Strong correlation between palm oil price and Brent crude oil

Source: Bloomberg, Daewoo Securities Research

Figure 46. Vegetables oil price trend

Source: MPOB, Daewoo Securities Research

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

1/06

7/06

1/07

7/07

1/08

7/08

1/09

7/09

1/10

7/10

1/11

7/11

1/12

7/12

1/13

7/13

1/14

7/14

1/15

7/15

1/16

(USD/ton) Palm Oil Soybean Rapessed Oil

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

12/1

0

4/11

8/11

12/1

1

4/12

8/12

12/1

2

4/13

8/13

12/1

3

4/14

8/14

12/1

4

4/15

8/15

12/1

5

4/16

(%) CPO Brent

Plantation

17

August 30, 2016

Daewoo Securities Indonesia Research

Astra Agro Lestari (AALI IJ)

The old dinosaur

Initiate coverage on AALI with a Hold rating

We initiate coverage on Astra Agro Lestari (AALI) with a Hold rating and target price of

IDR15,850. AALI is the largest oil palm plantation area under our plantation coverage,

however, we believe that AALI will find it challenging to organically grow due to its old age

oil palm profile and its diversification to downstream business which offers lower gross

margin compared to upstream palm oil business (AALI’s gross margin for downstream: 4%

vs upstream: 23%). AALI has secured IDR4.8tr funds through the recent rights issue, which

will be used to reduce its USD debt exposures. While we are less optimistic that the

proceeds from the new shares issuance will boost AALI’s net profit margin going forward,

we believe reduced leverage should act as a positive impact on its share price.

Old plantation profile, a drag on productivity

A large portion of AALI’s plantation profile is old aged which represents 59.1% of the total

planted area. Our view is that this will squeeze FFB yield over the longer horizon. AALI’s

average plantation age stood at 14.7 years in 2015 (vs. 14.2 years in 2011). We suspect this

old age profile will rise further as moratorium in new oil palm plantation will act as a key

hurdle for the company to acquire new land bank. We forecast that AALI’s FFB yield will

reach 21.7 ton/ha and 21.5 ton/ha in 2016F and 2017F, respectively. As a consequence, FFB

harvest from external parties (plasma & smallholders) will dominate AALI’s FFB harvest, in

our view. We are factoring in external parties’ FFB harvest to reach 4.20mn tons and

4.84mn tons in 2016F and 2017F. FFB harvest from external parties will weaken AALI’s CPO

and palm kernel extraction, given nucleus plantation is more efficient.

Improving in solvability could not help a much boost profitability margin

As a large portion of its proceeds from the recent rights issue will be used to pay off its

existing USD denominated debt, we believe AALI’s balance sheet will turn healthier. We are

modeling AALI’s net debt-to-equity ratio to reach 0.3x throughout 2016F and 2017F, down

from 0.6x in 2015. However, we are concern that AALI’s profitability margin will remain

challenged on the back of its focus on downstream business. Overall, we predict that AALI

gross, operating and net profit margin will reach 19.8%, 10.4% and 4.1%, from 23.6%,

14.2%, and 4.7% in 2015.

Valuations and target price at IDR15,850

We derive our target price of IDR15,850 on AALI using our DCF approach, assuming WACC

of 10.2% and terminal growth of 5.0% and PE target. In addition, we factored in the right

issue impact to deriving our valuation. Risks to our call are 1) sudden price spike/plunge in

global palm oil prices, 2) unexpected weather changes, 3) crude oil price fluctuations, and 4)

regulation risks.

FY (Dec.) 12/13 12/14 12/15 12/16F 12/17F

Revenue (IDRbn) 12,675.0 16,305.8 13,059.2 11,246.8 14,401.7

Gross profit (IDRbn) 4,081.9 4,951.8 3,082.1 2,227.7 2,731.5

Operating profit (IDRbn) 3,004.5 3,722.4 1,853.2 1,169.4 1,376.3

NP (IDRbn) 1,801.4 2,503.7 619.1 461.3 542.9

EPS (IDR) 935.9 1,300.8 321.7 202.8 238.7

BPS (IDR) 5,334.8 6,150.3 6,078.2 7,028.0 7,176.8

P/E (x) 25.6 17.8 47.0 78.5 66.7

ROE (%) 17.5 21.2 5.3 2.9 3.3

ROA (%) 12.0 13.5 2.9 2.0 2.2

Note: NP refers to net profit attributable to controlling interests

Source: Company data, Daewoo Securities Indonesia Research estimates

Agriculture

(Initiate) Hold

Target Price (12M, IDR) 15,850

Share Price (8/29/16, IDR) 15,925

Expected Return -0.5%

OP (16F, IDRbn) 1,169

Consensus OP (16F, IDRbn) 2,249

EPS Growth (16F, %) -37.0

Market EPS Growth (16F, %) 122.2

P/E (16F, x) 78.5

Market P/E (16F, x) 19.6

JCI (8/29/2016) 5,370.8

Market Cap (IDRbn) 30,650.7

Shares Outstanding (mn) 1,924.7

Free Float (%) 20.3

Foreign Ownership (%) 4.6

Beta (5Y) 1.0

52-Week Low (IDR) 13,126

52-Week High (IDR) 21,058

(%) 1M 6M 12M

Absolute 9.8 12.5 -7.5

Relative 6.9 0.0 -28.3

Plantation

18

August 30, 2016

Daewoo Securities Indonesia Research

Old age plantation profile dominates

As the one of the key crude palm oil (CPO) producers in Indonesia, AALI’s oil palm plantation is

spreading across Indonesia in Sumatera, Kalimantan, and Sulawesi regions. We note that AALI is

the only CPO operator with our CPO universe which has oil palm plantation exposure in Sulawesi.

AALI’s total mature oil palm area (nucleus and plasma) reached 258,536 ha in 2015, from 217,343

ha in 2011.

However, AALI’s immature plantation area decreased by 10,037 ha to 39,326 ha in 2015, from

49,363 ha in 2011. This reduction was largely due to the government’s moratorium policy of

opening new oil palm plantation implemented several years ago. In our opinion, AALI will find it

hard to organically grow as the government plans to extend its oil palm plantation moratorium. A

large portion of AALI’s plantation profile is old aged which represents 59.1% of the total planted

area. However, we note that AALI’s old aged plantation portfolio showed improvement (from 65%

(2012) to 59.1% (2015)) which was largely due to the replanting program which had been

implemented several years ago. Based on our discussion with AALI, the company is not expecting

to add new land banks (due to moratorium issue).

Figure 47. Old age profile dominated oil palm plantation Figure 48. Immature area down to 39,325ha in 2015

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

Old age plantation profile = lower FFB yield

The combination of old aged plantation profile and government’s moratorium on new palm

plantation, AALI’s average plantation age increased to 14.7 years in 2015 from 14.2 years in 2011.

We are concerned that AALI’s average age will rise further going forward and reach 14.8 years and

15.0 years in 2016F and 2017F, respectively. We also note that AALI’s FFB yield decreased further

to 21.7tons/ha in 2015, from 23.5tons/ha in 2012. Thus, we think that AALI’s FFB yield will only

reach 21.7ton/ha and 21.5ton/ha in 2016F and 2017F, respectively.

Figure 49. Average age stood at 14.7 years in 2015 Figure 50. FFB yield only reached 21.7 ton/ha in 2015

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

37.4 35.0 37.2 39.2 40.9

62.6 65.0 62.8 60.8 59.1

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2011 2012 2013 2014 2015

(%)

Productive Old Age

49,363

38,564

33,891

42,662 39,326

-

10,000

20,000

30,000

40,000

50,000

60,000

2011 2012 2013 2014 2015

(ha)

14.2 14.2

13.8

14.2

14.7

13.2

13.4

13.6

13.8

14.0

14.2

14.4

14.6

14.8

2011 2012 2013 2014 2015

(Years)

22.1

23.5

20.7

22.0

21.7

19.0

19.5

20.0

20.5

21.0

21.5

22.0

22.5

23.0

23.5

24.0

2011 2012 2013 2014 2015

(ton/ha)

Plantation

19

August 30, 2016

Daewoo Securities Indonesia Research

Both CPO and palm kernel extraction rates will decline further

In 2011, AALI’s CPO extraction rate stood at 22.6% while palm kernel extraction rate stood at

4.6%. By 2015, AALI’s CPO extraction rate decreased further and reached 21.6%, falling below its

5-year average at 22.1%. Furthermore, AALI’s palm kernel extraction rate had improved to 4.9%,

and gradually slipped to 4.6% in 2015. Looking forward, we predict that AALI’s CPO extraction rate

will reach 21.5% and 21.4% in 2016F and 2017F, respectively, on the back of larger contribution of

external party harvest. We underscore that CPO and palm kernel extraction rates of external

parties (plasma & smallholder plantation) generally have lower efficiencies compared to nucleus

plantation due to the fact that nucleus plantation has better cultivation management than

external parties. We also forecast AALI’s palm kernel extraction rate to reach 4.5% and 4.4% in

2016F and 2017F.

Figure 51. CPO extraction rate below 5-years average Figure 52. Palm kernel extraction rate down significantly

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

Lower CPO production outlook in 2016F

We predict that AALI’s FFB harvest to reach 7.82mn tons and 8.39mn tons in 2016F and 2017F,

respectively. Furthermore, FFB harvest will be dominated by external parties which are expected to

reach 4.20mn tons and 4.83mn tons in 2016F and 2017F. At the same time, FFB harvest from

nucleus plantation is expected to fall to 3.61mn tons and 3.56mn tons in 2016F and 2017F on the

back of old aged plantation profile. Overall, we predict that AALI’s CPO production to reach

1.68mn tons and 1.79mn tons in 2016F and 2017F, respectively.

Figure 53. External parties will dominate FFB harvest Figure 54. Lower CPO production outlook in 2016F

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

22.6

22.322.3

21.9

21.6

21.0

21.2

21.4

21.6

21.8

22.0

22.2

22.4

22.6

22.8

2011 2012 2013 2014 2015

(%)

5-years average4.8

4.9

4.8

4.7

4.6

4.5

4.5

4.6

4.6

4.7

4.7

4.8

4.8

4.9

4.9

5.0

2011 2012 2013 2014 2015

(%)

-

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

2013 2014 2015 2016F 2017F

('000 tonnes) Nucleus External Parties

1,400.0

1,450.0

1,500.0

1,550.0

1,600.0

1,650.0

1,700.0

1,750.0

1,800.0

1,850.0

2013 2014 2015 2016F 2017F

('000 tonnes)

Plantation

20

August 30, 2016

Daewoo Securities Indonesia Research

Sales and net profit to contract in 2016F

We predict that AALI’s CPO sales volume to increase to 1.26mn tons and 1.44mn tons in 2016F

and 2017F, respectively (vs. 1.04mn tons in 2015). Meanwhile, we are less optimistic that AALI’s

revenue growth will expand due to moderate outlook in global palm oil prices. Therefore, we

predict that AALI’s revenue will only reach IDR11.3tr and IDR14.4tr in 2016F and 2017F,

respectively (-13.9% YoY and +28.1% YoY). On the bottom-line, we estimate AALI’s net profit to

reach IDR461.3bn and IDR542.9bn in 2016F and 2017F, respectively (-25.5% YoY and +17.7% YoY).

Figure 55. Higher CPO sales volume outlook Figure 56. Negative growth revenue in 2016F

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

Diversification to downstream will hamper AALI’s profitability over the long-term

In January 2015, the company had acquired a 50.0% in KL-Kepong Plantation Holdings Sdn, Bhd

which focuses more on downstream palm oil business. This refinery is located in Dumai, Riau

province. Yet, we are pessimistic that AALI’s profitability will improve over the long-term, given

CPO downstream business only offers thin gross margin at 4.0% compared to the upstream

business which yields 23.6%. We predict AALI’s gross, operating and net profit margins will decline

to 19.8%, 10.4% and 4.1% in 2016F.

Figure 57. Downstream business has lower gross margin Figure 58. Profitability margin

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2013 2014 2015 2016F 2017F

('000 tonnes)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2013 2014 2015 2016F 2017F

(%)Gross Operating Net Profit

23.6

4.0

-

5.0

10.0

15.0

20.0

25.0

Upstream Downstream

(%)

-100.0

-80.0

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

2013 2014 2015 2016F 2017F

(%)Revenue Net profit

Plantation

21

August 30, 2016

Daewoo Securities Indonesia Research

Figure 59. Lower net debt equity after right issue Figure 60. Improves in interest coverage ratio

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

Figure 61. ROE stand at single digit Figure 62. ROA will improve after 2016F

Source: Company data, Daewoo Securities Research

Source: Company data, Daewoo Securities Research

Figure 63. Current ratio will at 1.0x in 2016F & 2017F Figure 64. Lower capex going forward

Source: Company data, Daewoo Securities Research

Source: Bloomberg, Daewoo Securities Research

12.0

13.5

2.92.0 2.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2013 2014 2015 2016F 2017F

(%)

17.5

21.2

5.3

2.9 3.3

0.0

5.0

10.0

15.0

20.0

25.0

2013 2014 2015 2016F 2017F

(%)

0.5

0.6

0.8

1.0 1.0

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2013 2014 2015 2016F 2017F

(x)

0.2

0.3

0.6

0.30.3

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

2013 2014 2015 2016F 2017F

(x)

41.538.7

14.8

22.124.1

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2013 2014 2015 2016F 2017F

(x)

2,861.5

3,278.2

2,586.3

915.4

682.1

-

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

2013 2014 2015 2016F 2017F

(IDR bn)

Plantation

22

August 30, 2016

Daewoo Securities Indonesia Research

Valuation

We use DCF approach to derive AALI’s 12-months forward target price at IDR13,350 with WACC

of 10.2% and terminal growth of 5.0%. Our target price reflects 78.2x and 66.4x P/E in 2016F and

2017F. We also use discounted to equity value by 60.0% with the assumption that AALI’s oil palm

productive profile only remains 40.0% of the total planted area.

Table 3. DCF valuation assumption

WACC (%)

Equity portion of capital 75.1

Ke 12

Debt portion of capital 24.9

Kd 4.7

Average WACC 10.2

Terminal value

Perpetual growth rate 5.0

Wacc-g 5.2

NPV 8,732.3

PV of TV 72,230.6

Net debt -5,024.9

Equity value 75,938.0

Equity value 30,375.2

Shares Outstanding (bn shares) 2.275

DCF Weighted 40.0%

PE Weighted 60.0%

DCF Target Price 13,352

PE Target Price 2,506

Blended Target Price 15,858

Source: Daewoo Securities Research

Figure 65. PE band

Source: Bloomberg, Daewoo Securities Research

0

5

10

15

20

25

30

35

9/11

12/1

1

3/12

6/12

9/12

12/1

2

3/13

6/13

9/13

12/1

3

3/14

6/14

9/14

12/1

4

3/15

6/15

9/15

12/1

5

3/16

6/16

(x)

Plantation

23

August 30, 2016

Daewoo Securities Indonesia Research

AALI at a glance

Company profile

AALI is a subsidiary of PT Astra International Tbk which was established in 1980, engages in the

agribusiness, specifically in the management of oil palm plantation and the production of palm oil.

The company manages oil palm plantation with locations spread over Sumatra, Kalimantan, and

Sulawesi, producing to meet the demands of both the domestic and export markets.

In 1997, the company became public by listing its shares on the Indonesia Stock Exchange.

Currently, public ownership of the shares reached 20.3% (out of 1.57bn shares in circulation) at

the end of 2015. In addition to strengthening its position at the upstream sector by managing an

area more than 200,000 hectare comprising nucleus and plasma plantation, the company has also

been strengthening its palm oil downstream business. Owning a palm oil refinery, PT Tanjung

Sarana Lestari in the Mamuju Utara regency, West Sulawesi and 50% shares in PT Kreasijaya

Adhikarya in Dumai, Riau Province, has significantly strengthened the company competitiveness

advantages in palm oil business chain.

Figure 66. AALI brief history

Source: Company data, Daewoo Securities Research

Figure 67. AALI’s ownership structure before right issue

Source: Company data, Daewoo Securities Research

Established in

1988, namely PT

Suryaraya

Cakrawala

Changed its

name to PT Astra

Agro Niaga in

1989

Merge between

PT Astra Agro

Niaga and

Suryaraya

Bahtera and

changed to PT

Astra Agro Lestari

in 1997

Go public in 1997

Plantation

24

August 30, 2016

Daewoo Securities Indonesia Research

Management

AALI is managed by an experienced management team. The profiles of the management team are

presented below as we cited from AALI’s annual report:

Prijono Sugiarto (President Commissioner)

An Indonesian citizen, he has been appointed as president commissioner of the company

since 2010. Currently, he is also PT Astra International Tbk (ASII) president director since

March 2010, president commissioner of PT United Tractors Tbk (UNTR), PT Astra Honda

Motor and PT Menara Astra. Previously, he was a director of ASII (2001 – 2010) and sales

engineering manager of Daimier-Benz Indonesia. He holds a diploma degree in

mechanical engineering from the University of A. Sc. Konstanz, German in 1984 and also

diploma degree in business administration from the University of A. Sc. Bochum, German

in 1986.

Chiew Sin Cheok (Vice President Commissioner)

A Malaysian citizen, he has been the vice president commissioner of the company since

2007. He is also commissioner of ASII and PT Astra Otoparts Tbk (AUTO), a member of

the advisory committee of PT Tunas Ridean Tbk (TURI) and alternate director of Cycle &

Carriage Bintang. He is on the Board of Governors of the Keswick Foundation, a

charitable body in Hong Kong. He graduated from the London School of Economics and

Political Science with a bachelor science degree and obtained a Master of Management

Scinece degree from the Imperial College of Science & Technology, London.

Johannes Loman (Commissioner)

An Indonesian citizen, he is appointed as a Commissioner of the Company in 14 April

2015. He is also a Commissioner of PT Musashi Auto Parts Indonesia, PT Showa Indonesia

Manufacturing since 2009 and PT Federal International Finance since 2007. In addition,

he also serves as President Commissioner of PT Suryaraya Rubberindo Industries, Vice

President Commissioner PT Astra Otopart Tbk, Executive Vice President Director in PT

Astra Honda Motor and Director in PT Astra International Tbk. He joined Astra in 1984

and previously held the position of CEO Honda Sales Operation, CEO Daihatsu Sales

Operation, Marketing Director of PT Astra Daihatsu Motor and PT Astra Honda Motor.

He graduated from the Parahyangan Catholic University in 1984.

Anugerah Pekerti (Independent Commissioner)

An Indonesian citizen, he has been an Independent Commissioner of the Company since

April 2011. Currently he serves as Independent Commissioner of UNTR and PT Samudera

Indonesia Tbk (SMDR), member of the Advisory Board of the National Human Rights

Commission and advisor to the Indonesian Physics Olympic Team. He was a lecturer at

the PPM Management Institute from 1968 and its President Director in 1988-1998. Since

1998 he has been actively involved in the implementation of good corporate governance

in various companies and non-profit organizations. He graduated from the Universitas

Indonesia in 1967, majoring in Psychology and acquired his Doctor of Philosophy degree

in Business Administration from the University of Southern California, USA in 1985.

Soemadi Djoko Moerdjono Brotodiningrat (Independent Commissioner)

Indonesian citizen, he was appointed as the Independent Commissioner of the Company

in April 2015. Currently, Soemadi is entrusted to head Indonesian Delegation to the EFTA

Indonesia Comprehensive Economic Partnership Agreement negotiation. He also serves

as Advisor on International Affairs to the Defense Minister and is a member of the Asia-

Europe Foundation Board of Governors and a lecturer at the Foreign Affairs Ministry’s

Center for Education and Training. Soemadi graduated from Department of International

Relations, Faculty of Social & Political Sciences, Gadjah Mada University in Yogyakarta in

1965 and from the Institut International d’Administration Publique–Section Diplomatique,

Paris in 1969.

Plantation

25

August 30, 2016

Daewoo Securities Indonesia Research

Widya Wiryawan (President Director)

An Indonesian citizen, he has been the Company President Director since May 2007.

Currently he also serves as a Director of ASII since May 2008. He joined Astra Group in PT

ASII in 1994. Previously, he served as Finance Director of PT Federal International Finance

(1997 - 2000), Finance Director of AUTO (2000-2005) and appointed as Vice President

Director of PT AUTO in 2006. He graduated from Bogor Institute of Agriculture and

holds a Master of Business Administration from the University of Sydney, Australia.

Rudy (Independent Director)

An Indonesian citizen, he has been the Company Director since April 2013 and he was

appointed as the Company Independent Director since 14 April 2015. Previously he

served as a Finance Director of PT Asuransi Astra Buana (2009 – 2013) and Chief

Corporate Planning and Strategy of PT Astra International Tbk (2007 - 2009). He joined

Astra Group in 2000 and started his career in PT Charoen Pokphand Indonesia Tbk, Inti

Salim Corpora and PT Trimegah Securities. He graduated from University of Trisakti

majoring in Economic and holds a Master of Applied Finance from the University of

Melbourne, Australia.

Bambang Palgoenadi (Director)

An Indonesian citizen, he has been the Company Director since May 2000. He served as

the project leader in implementation of the plantation information system of the Astra

Agro Lestari Group (1995-1996) and served as the Company Deputy Director for

Production (1996 - 1998). He joined the Company in 1981. He completed his education

at the Bogor Institute of Agriculture in 1981, majoring in Agricultural Technology.

Juddy Arianto (Director)

An Indonesian citizen, he has been the Company Director since May 2007. He was

President Director of PT Menara Terus Makmur (2005 - 2007), he served as Director of

Federal Nittan Industries (2001-2004), previously appointed as Division Head of Bearing

Production of PT SKF Indonesia (1984-2000). He joined Astra Group in 1983. He

graduated from Universitas of Indonesia, majoring in Metallurgy.

Joko Supriyono (Director)

An Indonesian citizen, he has been a Company Director since May 2007. At the Company,

he was Deputy Director of Plantations and Mills Operation (2005 - 2007), he served as

Area Director (2002 - 2005), Division Head of Human Resources (2000 - 2002) and as

Personnel Department Head (1999 - 2000) after previously serving as Training &

Recruitment Department Head (1996 - 1997). He joined the Company in 1995 as

Training Department staff. He was an Instructor of Quality Management Consultant of

PT Wahana Kendali Mutu (1994 - 1995) and was Head of Afdeling at PT Perkebunan

Nusantara II, Medan (1986 - 1993). He graduated from Gadjah Mada University,

Yogyakarta majoring in Agriculture.

Jamal Abdul Nasser (Director)

An Indonesian citizen, he has been the Company Director since April 2011. Previously he

served as the Company Director of PT Denso Indonesia from 2008, after serving as the

Director of PT Kayaba Indonesia and PT Toyoda Gosei Safety System Indonesia. He joined

Astra Group in 1985 and started his career in PT SKF Indonesia, PT Federal Adiwira Serasi

and PT Adiwira Presisi Industri. He had served as Division Head of PT Astra Otoparts Tbk

in 2003 and was appointed as Deputy Chief Operation Officer in 2007. He graduated

from Bogor Institute of Agriculture in 1982, majoring in Agricultural Mechanization.

Plantation

26

August 30, 2016

Daewoo Securities Indonesia Research

Profit & Loss

Balance sheet

Year end Dec 31 (IDRbn) 2015 2016E 2017E 2018E

Year end Dec 31 (IDRbn) 2015 2016E 2017E 2018E

Revenue 13,059.2 11,246.8 14,401.7 16,371.1

Current assets

Cost of goods sold -9,977.1 -9,019.0 -11,670.2 -13,037.1

Cash & equivalents 294.4 275.1 185.6 184.3

Gross profit 3,082.1 2,227.7 2,731.5 3,334.0

Short-term financial asset - - - -

SG&A -1,228.9 -1,058.4 -1,355.3 -1,540.6

Account receivable 88.0 75.8 97.1 110.3

EBIT (Adj.) 1,853.2 1,169.4 1,376.3 1,793.4

Inventory 1,691.6 1,529.1 1,978.6 2,210.4

EBIT 1,853.2 1,169.4 1,376.3 1,793.4

Other current assets 740.1 572.4 689.9 898.5

Net interest income (loss) -97.7 -24.8 -27.1 -35.4

Non-current assets

Income (loss) from associcates 0.0 0.0 0.0 0.0

Net fixed assets 9,361.7 11,097.0 10,994.3 11,092.7

Others -579.9 -268.8 -318.4 -345.9

Investment 109.2 109.2 109.2 109.2

Recurring profit 1,175.5 875.8 1,030.8 1,412.1

Other long-term assets 9,227.3 9,423.5 10,260.2 11,217.7

Income tax -479.8 -357.5 -420.7 -576.4 Total assets 21,512.4 23,082.1 24,314.9 25,823.2

Net profit 619.1 461.3 542.9 743.7 Current liabilities

Net profit (Controlling Interest) 695.7 518.3 610.0 835.7 Account payable 733.5 663.1 858.0 958.5

Short-term debt 700.0 200.0 300.0 700.0

Growth & margins 2015 2016E 2017E 2018E Other current liabilities 2,088.6 1,538.4 1,704.7 1,948.7

Revenue growth -19.9 -13.9 28.1 13.7 Non-current liabilities

Gross profit growth -37.8 -27.7 22.6 22.1 Long-term debt 5,708.0 4,200.0 4,500.0 4,700.0

EBIT growth -50.2 -36.9 17.7 30.3 Other long-term liabilities 583.5 494.3 627.5 727.8

Net profit growth -75.3 -25.5 17.7 37.0 Total liabilities 9,813.6 7,095.8 7,990.3 9,035.0

EPS growth -75.3 -37.0 17.7 37.0 Controlling interests 11,284.8 15,572.3 15,910.6 16,374.2

Gross margin 23.6 19.8 19.0 20.4 Non-controlling Interest 414.0 414.0 414.0 414.0

EBIT margin 14.2 10.4 9.6 11.0 Shareholder's equity 11,698.8 15,986.3 16,324.6 16,788.1

Net profit margin 4.7 4.1 3.8 4.5 BVPS (IDR) 6,078.2 7,028.0 7,176.8 7,380.6

Cash Flow (Summarized)

Ratio analysis

Year end Dec 31 (IDRbn) 2015 2016E 2017E 2018E

Year end Dec 31 2015 2016E 2017E 2018E

Cash flow from operations

ROE (%) 5.3 2.9 3.3 4.4

Net profit 619.1 461.3 542.9 743.7

ROA (%) 2.9 2.0 2.2 2.9

Depr. & amortization 885.1 -1,250.2 814.7 847.3

Inventory days 17.0 17.0 17.0 17.0

Others -398.3 42.4 48.8 -64.7

Receivables days 2.5 2.5 2.5 2.5

Change in working capital -643.4 104.2 -275.8 -144.5

Payable days 26.8 26.8 26.8 26.8

Cash flow from investing

Net debt/equity (x) 0.6 0.3 0.3 0.4

Capital expenditure -2,189.5 -915.4 -682.1 -904.8

Interest cover (x) 14.8 22.1 24.1 28.0

Others -1,239.2 234.1 -866.8 -998.3

Cash flow from financing

Dividends -743.3 -173.8 -204.5 -280.2

Increase in equity -4.1 4,000.0 0.0 0.0

Increase in debt 3,305.9 -2,432.8 400.0 700.0

Others 90.9 -89.2 133.2 100.2

Beginning cash 611.2 294.4 275.1 185.6

Ending cash 294.4 275.1 185.6 184.3

Source: Company data, Daewoo Securities Research

Plantation

27

August 30, 2016

Daewoo Securities Indonesia Research