Aswath Damodaran Valuationpeople.stern.nyu.edu/adamodar/pdfiles/ovhds/val.pdfAswath Damodaran 189...

54

Aswath Damodaran 186 Valuation Aswath Damodaran

Transcript of Aswath Damodaran Valuationpeople.stern.nyu.edu/adamodar/pdfiles/ovhds/val.pdfAswath Damodaran 189...

Asw

ath Dam

odaran186

Valuation

Asw

ath Dam

odaran

Asw

ath Dam

odaran187

First P

rinciples

Invest in projects that yield a return greater than the minim

umacceptable hurdle rate.•

The hurdle rate should be higher for riskier projects and reflect the

financing mix used - ow

ners’ funds (equity) or borrowed m

oney (debt)

•R

eturns on projects should be measured based on cash flow

s generatedand the tim

ing of these cash flows; they should also consider both positive

and negative side effects of these projects.

Choose a financing m

ix that minim

izes the hurdle rate and matches the

assets being financed.

If there are not enough investments that earn the hurdle rate, return the

cash to stockholders.•

The form

of returns - dividends and stock buybacks - will depend upon

the stockholders’ characteristics.

Objective: M

aximize the V

alue of the Firm

Asw

ath Dam

odaran188

Discounted C

ashflow V

aluation: Basis for

Approach

•w

here,

•n =

Life of the asset

•C

Ft =

Cashflow

in period t

•r =

Discount rate reflecting the riskiness of the estim

ated cashflows

Value =

C

Ft

(1+

r) tt=

1

t=n

∑

Asw

ath Dam

odaran189

Equity V

aluation

The value of equity is obtained by discounting expected cashflow

s toequity, i.e., the residual cashflow

s after meeting all expenses, tax

obligations and interest and principal payments, at the cost of equity,

i.e., the rate of return required by equity investors in the firm.

where,

CF to E

quityt = E

xpected Cashflow

to Equity in period t

ke = C

ost of Equity

The dividend discount m

odel is a specialized case of equity valuation,and the value of a stock is the present value of expected futuredividends.

Value of E

quity=

C

F to E

quityt

(1+

ke ) t

t=1

t=n

∑

Asw

ath Dam

odaran190

Firm

Valuation

The value of the firm

is obtained by discounting expected cashflows to

the firm, i.e., the residual cashflow

s after meeting all operating

expenses and taxes, but prior to debt payments, at the w

eightedaverage cost of capital, w

hich is the cost of the different components

of financing used by the firm, w

eighted by their market value

proportions.

where,

CF to Firm

t = E

xpected Cashflow

to Firm in period t

WA

CC

= W

eighted Average C

ost of Capital

Value of F

irm=

C

F to F

irmt

(1+

WA

CC

) tt=1

t=n

∑

Asw

ath Dam

odaran191

Generic D

CF

Valuation M

odel

Cash

flow

sF

irm: P

re-debt cash flowE

quity: After debt

cash flows

Exp

ected G

row

thF

irm: G

rowth in

Operating E

arningsE

quity: Grow

th in N

et Income/E

PS

CF

1C

F2

CF

3C

F4

CF

5

Forever

Firm

is in stable growth:

Grow

s at constant rateforever

Term

inal Value

CF

n.........

Disco

un

t Rate

Firm

:Cost of C

apital

Equity: C

ost of Equity

Value

Firm

: Value of F

irm

Equity: V

alue of Equity

DIS

CO

UN

TE

D C

AS

HF

LOW

VA

LUA

TIO

N

Len

gth

of P

eriod

of H

igh

Gro

wth

Asw

ath Dam

odaran192

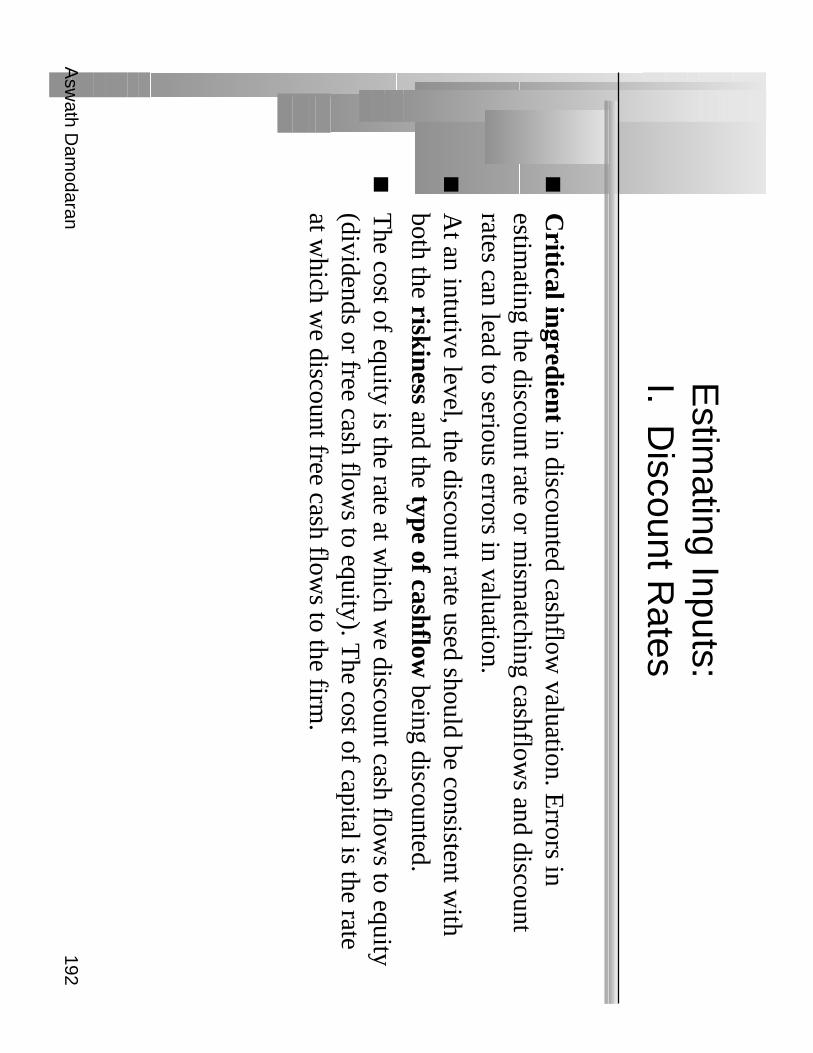

Estim

ating Inputs:I. D

iscount Rates

Critical ingredient in discounted cashflow

valuation. Errors in

estimating the discount rate or m

ismatching cashflow

s and discountrates can lead to serious errors in valuation.

At an intutive level, the discount rate used should be consistent w

ithboth the riskiness and the type of cashflow

being discounted.

The cost of equity is the rate at w

hich we discount cash flow

s to equity(dividends or free cash flow

s to equity). The cost of capital is the rate

at which w

e discount free cash flows to the firm

.

Asw

ath Dam

odaran193

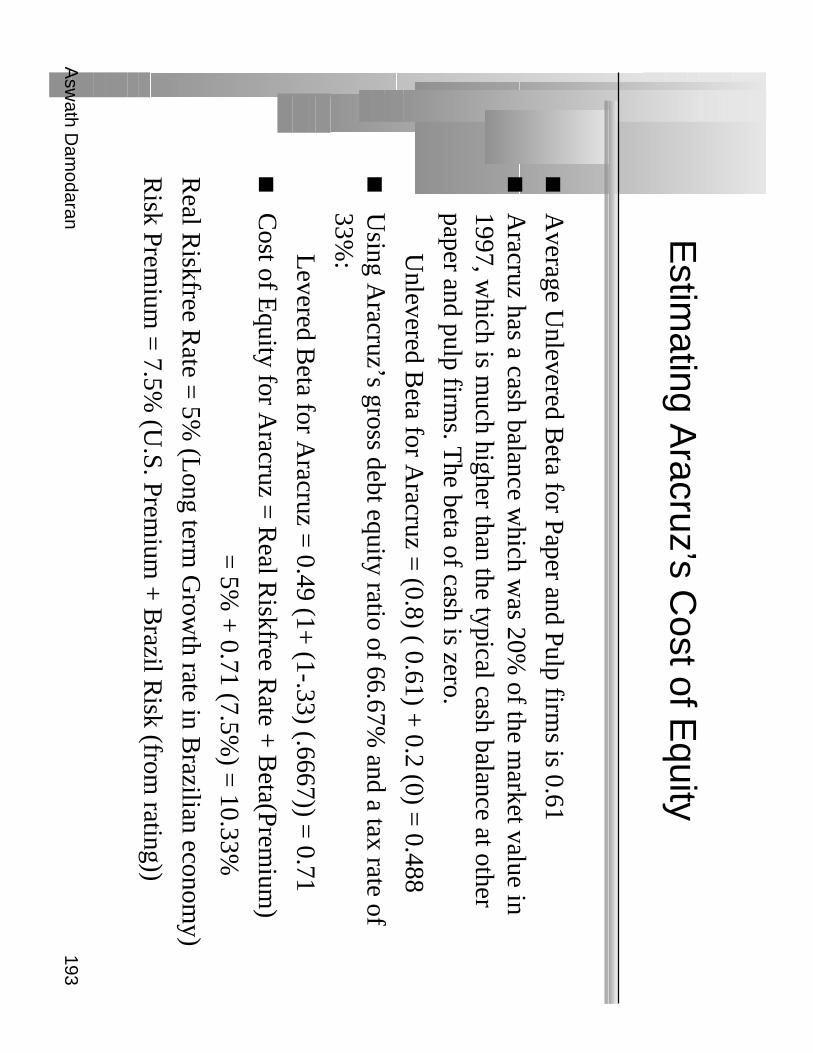

Estim

ating Aracruz’s C

ost of Equity

Average U

nlevered Beta for Paper and Pulp firm

s is 0.61

Aracruz has a cash balance w

hich was 20%

of the market value in

1997, which is m

uch higher than the typical cash balance at otherpaper and pulp firm

s. The beta of cash is zero.

Unlevered B

eta for Aracruz =

(0.8) ( 0.61) + 0.2 (0) =

0.488

Using A

racruz’s gross debt equity ratio of 66.67% and a tax rate of

33%:Levered B

eta for Aracruz =

0.49 (1+ (1-.33) (.6667)) =

0.71

Cost of E

quity for Aracruz =

Real R

iskfree Rate +

Beta(Prem

ium)

= 5%

+ 0.71 (7.5%

) = 10.33%

Real R

iskfree Rate =

5% (L

ong term G

rowth rate in B

razilian economy)

Risk Prem

ium =

7.5% (U

.S. Premium

+ B

razil Risk (from

rating))

Asw

ath Dam

odaran194

Estim

ating Cost of E

quity: Deutsche B

ank

Deutsche B

ank is in two different segm

ents of business - comm

ercialbanking and investm

ent banking.

To estim

ate its comm

ercial banking beta, we w

ill use the average betaof com

mercial banks in G

ermany.

To estim

ate the investment banking beta, w

e will use the average bet

of investment banks in the U

.S and U.K

.

Com

parable Firm

sA

verage Beta

Weight

Com

mercial B

anks in Germ

any0.90

90%

U.K

. and U.S. investm

ent banks1.30

10%

Beta for D

eutsche Bank =

0.9 (.90) + 0.1 (1.30)=

0.94

Cost of E

quity for Deutsche B

ank (in DM

) = 7.5%

+ 0.94 (5.5%

)

= 12.67%

Asw

ath Dam

odaran195

Review

ing Disney’s C

osts of Equity &

Debt

Business

Unlevered

D/E

Ratio

Levered

Riskfree

Risk

Cost of

Beta

Beta

Rate

Premium

Equity

Creative C

ontent1.25

20.92%1.42

7.00%5.50%

14.80%

Retailing

1.5020.92%

1.707.00%

5.50%16.35%

Broadcasting

0.9020.92%

1.027.00%

5.50%12.61%

Them

e Parks1.10

20.92%1.26

7.00%5.50%

13.91%

Real E

state0.70

59.27%0.92

7.00%5.50%

12.31%

Disney

1.0921.97%

1.257.00%

5.50%13.85%

Disney’s C

ost of Debt (based upon rating) =

7.50%

Asw

ath Dam

odaran196

Estim

ating Cost of C

apital: Disney

Equity•

Cost of E

quity =13.85%

•M

arket Value of E

quity =

$50.88 Billion

•E

quity/(Debt+

Equity ) =

82%

Debt

•A

fter-tax Cost of debt =

7.50% (1-.36) =

4.80%

•M

arket Value of D

ebt =$ 11.18 B

illion

•D

ebt/(Debt +

Equity) =

18%

Cost of C

apital = 13.85%

(.82)+4.80%

(.18) = 12.22%

Asw

ath Dam

odaran197

II. Estim

ating Cash F

lows

Cash F

lows

To E

quityT

o Firm

The S

trict View

Dividends +

Stock B

uybacks

The B

roader View

Net Incom

e- N

et Cap E

x (1-Debt R

atio)- C

hg WC

(1 - Debt R

atio)= F

ree Cashflow

to Equity

EB

IT (1-t)

- ( Cap E

x - Depreciation)

- Change in W

orking Capital

= Free C

ashflow to F

irm

Asw

ath Dam

odaran198

Estim

ating FC

FE

next year: Aracruz

All inputs are per share num

bers:

Earnings

BR

0.222

- (CapE

x-Depreciation)*(1-D

R)

BR

0.042

-Chg. W

orking Capital*(1-D

R)

BR

0.018

Free Cashflow

to Equity

BR

0.170

Earnings: Since A

racruz’s 1996 earnings are “abnormally” low

, I usedthe average earnings per share from

1992 to 1996.

Capital E

xpenditures per share next year = 0.24 B

R/share

Depreciation per share next year =

0.18 BR

/share

Change in W

orking Capital =

0.03 BR

/share

Debt R

atio = 39%

Asw

ath Dam

odaran199

Estim

ating FC

FF

: Disney

EB

IT =

$5,559 Million

Capital spending =

$ 1,746 Million

Depreciation =

$ 1,134 Million

Increase in Non-cash W

orking capital = $ 617 M

illion

Estim

ating FCFF

EB

IT (1-t)

$ 3,558

+ D

epreciation $ 1,134

- Capital E

xpenditures $ 1,746

- Change in W

C $ 617

= FC

FF

$ 2,329 Million

Asw

ath Dam

odaran200

Application T

est: Estim

ating your firm’s

FC

FF

Estim

ate the FCFF for your firm

in its most recent financial year:

In general,If using statem

ent of cash flows

EB

IT (1-t)

EB

IT (1-t)

+ D

epreciation+

Depreciation

- Capital E

xpenditures+

Capital E

xpenditures

- Change in N

on-cash WC

+ C

hange in Non-cash W

C

= FC

FF=

FCFF

Estim

ate the dollar reinvestment at your firm

:

Reinvestm

ent = E

BIT

(1-t) - FCFF

Asw

ath Dam

odaran201

Choosing a C

ash Flow

to Discount

When you cannot estim

ate the free cash fllows to equity or the firm

,the only cash flow

that you can discount is dividends. For financialservice firm

s, it is difficult to estimate free cash flow

s. For Deutsche

Bank, w

e will be discounting dividends.

If a firm’s debt ratio is not expected to change over tim

e, the free cashflow

s to equity can be discounted to yield the value of equity. ForA

racruz, we w

ill discount free cash flows to equity.

If a firm’s debt ratio m

ight change over time, free cash flow

s to equitybecom

e cumbersom

e to estimate. H

ere, we w

ould discount free cashflow

s to the firm. For D

isney, we w

ill discount the free cash flow to

the firm.

Asw

ath Dam

odaran202

III. Expected G

rowth

Expected G

rowth

Net Incom

eO

perating Income

Retention R

atio=1 - D

ividends/Net

Income

Return on E

quityN

et Income/B

ook Value of

Equity

X

Reinvestm

ent R

ate = (Net C

ap E

x + C

hg in W

C/E

BIT

(1-t)

Return on C

apital =E

BIT

(1-t)/Book V

alue of C

apitalX

Asw

ath Dam

odaran203

Expected G

rowth in E

PS

gE

PS =

Retained E

arningst-1 / N

It-1 * RO

E=

Retention R

atio * RO

E=

b * RO

E•

Proposition 1: The expected grow

th rate in earnings for a company

cannot exceed its return on equity in the long term.

Asw

ath Dam

odaran204

Estim

ating Expected G

rowth in E

PS

: Disney,

Aracruz and D

eutsche Bank

Com

panyR

OE

Retention

Exp.

Forecast

Retention

Exp

Ratio

Grow

thR

OE

Ratio

Grow

th

Disney

24.95%77.68%

19.38%25%

77.68%19.42%

Aracruz

2.22%65.00%

1.44%13.91%

65.00%9.04%

Deutsche B

ank7.25%

39.81%2.89%

14.00%45.00%

6.30%

RO

E: R

eturn on Equity for m

ost recent year

Forecasted RO

E =

Expected R

OE

for the next 5 years•

For Disney, forecasted R

OE

is expected to be close to current RO

E

•For A

racruz, the average RO

E betw

een 1994 and 1996 is used, since 1996w

as a abnormally bad year

•For D

eutsche Bank, the forecast R

OE

is set equal to the average RO

E for

Germ

an banks

Asw

ath Dam

odaran205

RO

E and Leverage

RO

E =

RO

C +

D/E

(RO

C - i (1-t))

where,

RO

C =

(EB

IT (1 - tax rate)) / B

ook Value of C

apital

= E

BIT

(1- t) / Book V

alue of Capital

D/E

= B

V of D

ebt/ BV

of Equity

i = Interest E

xpense on Debt / B

ook Value of D

ebt

t = T

ax rate on ordinary income

Note that B

V of C

apital = B

V of D

ebt + B

V of E

quity.

Asw

ath Dam

odaran206

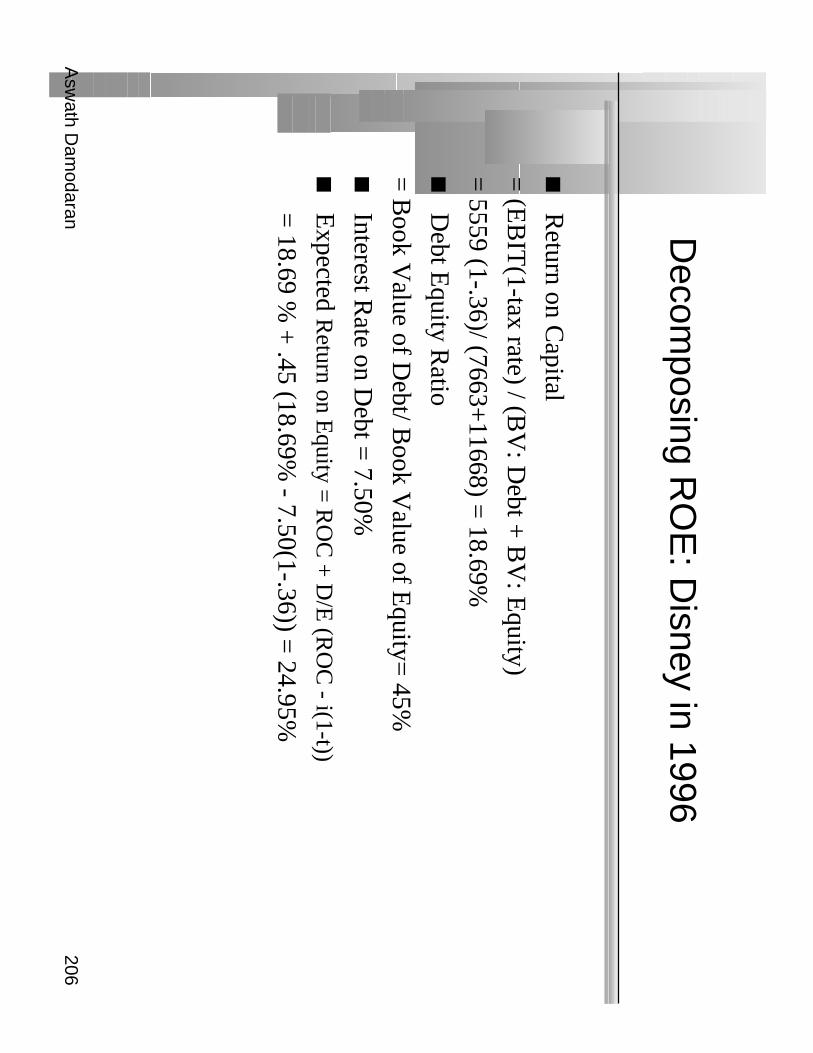

Decom

posing RO

E: D

isney in 1996

Return on C

apital

= (E

BIT

(1-tax rate) / (BV

: Debt +

BV

: Equity)

= 5559 (1-.36)/ (7663+

11668) = 18.69%

Debt E

quity Ratio

= B

ook Value of D

ebt/ Book V

alue of Equity=

45%

Interest Rate on D

ebt = 7.50%

Expected R

eturn on Equity =

RO

C +

D/E

(RO

C - i(1-t))

=

18.69 % +

.45 (18.69% - 7.50(1-.36)) =

24.95%

Asw

ath Dam

odaran207

Expected G

rowth in E

BIT

And F

undamentals

Reinvestm

ent Rate and R

eturn on Capital

gE

BIT

= (N

et Capital E

xpenditures + C

hange in WC

)/EB

IT(1-t) * R

OC

= R

einvestment R

ate * RO

C

Proposition 2: No firm

can expect its operating income to grow

overtim

e without reinvesting som

e of the operating income in net capital

expenditures and/or working capital.

Proposition 3: The net capital expenditure needs of a firm

, for a givengrow

th rate, should be inversely proportional to the quality of itsinvestm

ents.

Asw

ath Dam

odaran208

Estim

ating Grow

th in EB

IT: D

isney

Actual reinvestm

ent rate in 1996 = (N

et Cap E

x+ C

hg in WC

)/ EB

IT (1-t)

•N

et Cap E

x in 1996 = (1745-1134)

•C

hange in Working C

apital = 617

•E

BIT

(1- tax rate) = 5559(1-.36)

•R

einvestment R

ate = (1745-1134+

617)/(5559*.64)= 34.5%

Forecasted Reinvestm

ent Rate =

50%

Return on C

apital =20%

(Higher than this year’s 18.69%

)

Expected G

rowth in E

BIT

=.5(20%

) = 10%

The forecasted reinvestm

ent rate is much higher than the actual

reinvestment rate in 1996, because it includes projected acquisition.

Betw

een 1992 and 1996, adding in the Capital C

ities acquisition to allcapital expenditures w

ould have yielded a reinvestment rate of roughly

50%.

Asw

ath Dam

odaran209

Application T

est: Estim

ating Expected

Grow

th

Estim

ate the following:

•T

he reinvestment rate for your firm

•T

he after-tax return on capital

•T

he expected growth in operating incom

e, based upon these inputs

Asw

ath Dam

odaran210

IV. G

etting Closure in V

aluation

A publicly traded firm

potentially has an infinite life. The value is

therefore the present value of cash flows forever.

Since we cannot estim

ate cash flows forever, w

e estimate cash flow

sfor a “grow

th period” and then estimate a term

inal value, to capture thevalue at the end of the period:

Value =

C

Ft

(1+

r) tt

=1

t=∞

∑

Value =

C

Ft

(1+

r) tT

erminal V

alue

(1+

r)t=

1

t=N

N+

∑

Asw

ath Dam

odaran211

Stable G

rowth and T

erminal V

alue

When a firm

’s cash flows grow

at a “constant” rate forever, the presentvalue of those cash flow

s can be written as:

Value =

Expected C

ash Flow N

ext Period / (r - g)

where,

r = D

iscount rate (Cost of E

quity or Cost of C

apital)

g = E

xpected growth rate

This “constant” grow

th rate is called a stable growth rate and cannot

be higher than the growth rate of the econom

y in which the firm

operates.

While com

panies can maintain high grow

th rates for extended periods,they w

ill all approach “stable growth” at som

e point in time.

When they do approach stable grow

th, the valuation formula above

can be used to estimate the “term

inal value” of all cash flows beyond.

Asw

ath Dam

odaran212

Grow

th Patterns

A key assum

ption in all discounted cash flow m

odels is the period ofhigh grow

th, and the pattern of growth during that period. In general,

we can m

ake one of three assumptions:

•there is no high grow

th, in which case the firm

is already in stable growth

•there w

ill be high growth for a period, at the end of w

hich the growth rate

will drop to the stable grow

th rate (2-stage)

•there w

ill be high growth for a period, at the end of w

hich the growth rate

will decline gradually to a stable grow

th rate(3-stage)

The assum

ption of how long high grow

th will continue w

ill dependupon several factors including:•

the size of the firm (larger firm

-> shorter high grow

th periods)

•current grow

th rate (if high -> longer high grow

th period)

•barriers to entry and differential advantages (if high ->

longer growth

period)

Asw

ath Dam

odaran213

Length of High G

rowth P

eriod

Assum

e that you are analyzing two firm

s, both of which are enjoying

high growth. T

he first firm is E

arthlink Netw

ork, an internet serviceprovider, w

hich operates in an environment w

ith few barriers to entry

and extraordinary competition. T

he second firm is B

iogen, a bio-technology firm

which is enjoying grow

th from tw

o drugs to which it

owns patents for the next decade. A

ssuming that both firm

s are well

managed, w

hich of the two firm

s would you expect to have a longer

high growth period?

Earthlink N

etwork

Biogen

Both are w

ell managed and should have the sam

e high growth period

Asw

ath Dam

odaran214

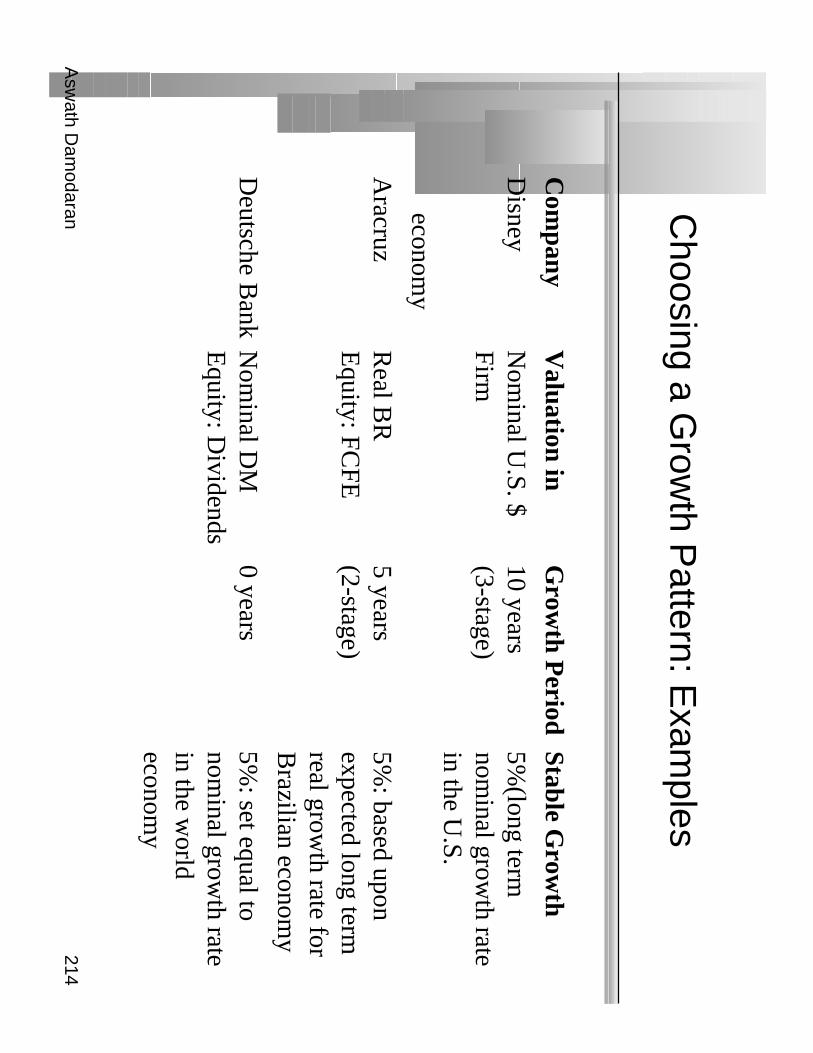

Choosing a G

rowth P

attern: Exam

ples

Com

panyV

aluation in G

rowth P

eriodStable G

rowth

Disney

Nom

inal U.S. $

10 years5%

(long term

Firm(3-stage)

nominal grow

th ratein the U

.S.econom

y

Aracruz

Real B

R5 years

5%: based upon

Equity: FC

FE(2-stage)

expected long termreal grow

th rate forB

razilian economy

Deutsche B

ankN

ominal D

M0 years

5%: set equal to

Equity: D

ividendsnom

inal growth rate

in the world

economy

Asw

ath Dam

odaran215

Firm

Characteristics as G

rowth C

hanges

Variable

High G

rowth F

irms tend to

Stable Grow

th Firm

s tend to

Risk

be above-average riskbe average risk

Dividend Payout

pay little or no dividendspay high dividends

Net C

ap Ex

have high net cap exhave low

net cap ex

Return on C

apitalearn high R

OC

(excess return)earn R

OC

closer to WA

CC

Leverage

have little or no debthigher leverage

Asw

ath Dam

odaran216

Estim

ating Stable G

rowth Inputs

Start with the fundam

entals:•

Profitability measures such as return on equity and capital, in stable

growth, can be estim

ated by looking at–

industry averages for these measure, in w

hich case we assum

e that this firm in

stable growth w

ill look like the average firm in the industry

–cost of equity and capital, in w

hich case we assum

e that the firm w

ill stopearning excess returns on its projects as a result of com

petition.

•L

everage is a tougher call. While industry averages can be used here as

well, it depends upon how

entrenched current managem

ent is and whether

they are stubborn about their policy on leverage (If they are, use currentleverage; if they are not; use industry averages)

Use the relationship betw

een growth and fundam

entals to estimate

payout and net capital expenditures.

Asw

ath Dam

odaran217

Estim

ating Stable P

eriod Net C

ap Ex

gE

BIT

= (N

et Capital E

xpenditures + C

hange in WC

)/EB

IT(1-t) * R

OC

= R

einvestment R

ate * RO

C

Moving term

s around,

Reinvestm

ent Rate =

gE

BIT / R

eturn on Capital

For instance, assume that D

isney in stable growth w

ill grow 5%

andthat its return on capital in stable grow

th will be 16%

. The

reinvestment rate w

ill then be:

Reinvestm

ent Rate for D

isney in Stable Grow

th = 5/16 =

31.25%

In other words,

•the net capital expenditures and w

orking capital investment each year

during the stable growth period w

ill be 31.25% of after-tax operating

income.

Asw

ath Dam

odaran218

Valuation: D

eutsche Bank

Sustainable growth at D

eutsche Bank =

RO

E * R

etention Ratio

= 14%

(.45) = 6.30%

{ I used the normalized num

bers for this]

Cost of equity =

7.5% +

0.94 (5.5%) =

12.67%.

Current D

ividends per share = 2.61 D

M

Model U

sed:•

Stable Grow

th (Large firm

; Grow

th is close to stable growth already)

•D

ividend Discount M

odel (FCFE

is tough to estimate)

Valuation

•E

xpected Dividends per Share next year =

2.61 DM

(1.063) = 2.73 D

M

•V

alue per Share = 2.73 D

M / (.1267 - .063) =

42.89 DM

Deutsche B

ank was trading for 119 D

M on the day of this analysis.

Asw

ath Dam

odaran219

What does the valuation tell us?

Stock is tremendously overvalued: T

his valuation would suggest that

Deutsche B

ank is significantly overvalued, given our estimates of

expected growth and risk.

Dividends m

ay not reflect the cash flows generated by D

eutsche Bank.

TheFC

FE could have been significantly higher than the dividends

paid.

Estim

ates of growth and risk are w

rong: It is also possible that we

have underestimated grow

th or overestimated risk in the m

odel, thusreducing our estim

ate of value.

Asw

ath Dam

odaran220

Valuation: A

racruz Cellulose

The current earnings per share for A

racruz Cellulose is 0.044 B

R.

These earnings are abnorm

ally low. T

o normalize earnings, w

e use theaverage earnings per share betw

een 1994 and 1996 of 0.204 BR

pershare as a m

easure of the normalized earnings per share.

Model U

sed:•

Real valuation (since inflation is still in double digits)

•2-Stage G

rowth (Firm

is still growing in a high grow

th economy)

•FC

FE D

iscount Model (D

ividends are lower than FC

FE: See D

ividendsection)

Asw

ath Dam

odaran221

Aracruz C

ellulose: Inputs for Valuation

High G

rowth P

haseStable G

rowth P

hase

Length

5 yearsForever, after year 5

Expected G

rowth

Retention R

atio * RO

E5%

(Real G

rowth R

ate in Brazil)

= 0.65 * 13.91%

= 8.18%

Cost of E

quity5%

+ 0.71 (7.5%

) = 10.33%

5% +

1(7.5%) =

12.5%

(Beta =

0.71; Rf =

5%)

(Assum

es beta moves to 1)

Net C

apital Expenditures

Net capital ex grow

s at same

Capital expenditures are assum

ed rate as earnings. N

ext year, to be 120%

of depreciation

capital ex will be 0.24 B

R

and deprec’n will be 0.18 B

R.

Working C

apital32.15%

of Revenues;

32.15% of R

evenues;

Revenues grow

at same rate as earnings in both periods.

Debt R

atio39.01%

of net capital ex and working capital investm

ents come

from debt.

Asw

ath Dam

odaran222

Aracruz: E

stimating F

CF

E for next 5 years

12

34

5T

erminal

Earnings

BR

0.222 B

R 0.243

BR

0.264 B

R 0.288 B

R 0.314 B

R 0.330

- (CapE

x-Depreciation)*(1-D

R)

BR

0.042 B

R 0.046

BR

0.050 B

R 0.055 B

R 0.060 B

R 0.052

-Chg. W

orking Capital*(1-D

R)

BR

0.010 B

R 0.011

BR

0.012 B

R 0.013 B

R 0.014 B

R 0.008

Free Cashflow

to Equity

BR

0.170 B

R 0.186

BR

0.202 B

R 0.221 B

R 0.241 B

R 0.269

Present Value

BR

0.154 B

R 0.152

BR

0.150 B

R 0.149 B

R 0.147

The present value is com

puted by discounting the FCFE

at the currentcost of equity of 10.33%

.

Asw

ath Dam

odaran223

Aracruz: E

stimating T

erminal P

rice and Value

per share

The term

inal value at the end of year 5 is estimated using the FC

FE in

the terminal year.

•T

he FCFE

in year 6 reflects the drop in net capital expenditures after year5.

•T

erminal V

alue = 0.269/(.125-.05) =

3.59 BR

•V

alue per Share = 0.154 +

0.152 + 0.150 +

0.149 + 0.147 +

3.59/1.10335

= 2.94 B

R

The stock w

as trading at 2.40 BR

in September 1997.

The value per share is based upon norm

alized earnings. To the extent

that it will take som

e time to get to norm

al earnings, discount thisvalue per share back to the present at the cost of equity of 10.33%

.

Asw

ath Dam

odaran224

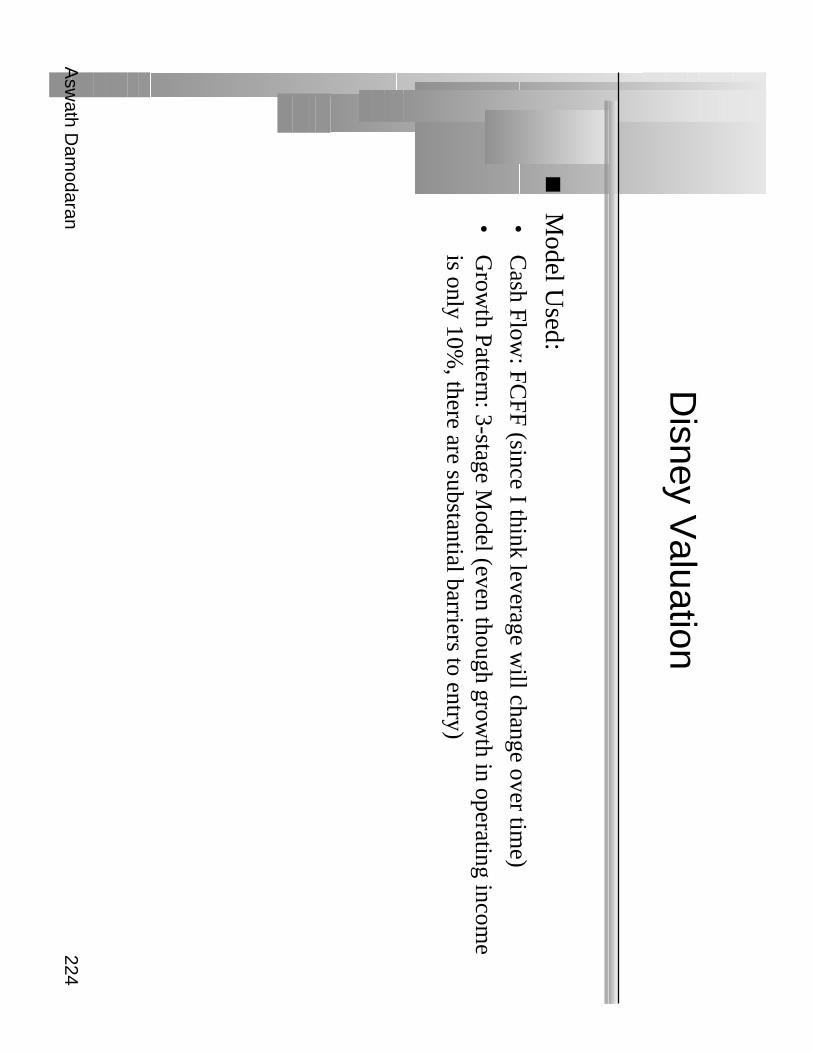

Disney V

aluation

Model U

sed:•

Cash Flow

: FCFF (since I think leverage w

ill change over time)

•G

rowth Pattern: 3-stage M

odel (even though growth in operating incom

eis only 10%

, there are substantial barriers to entry)

Asw

ath Dam

odaran225

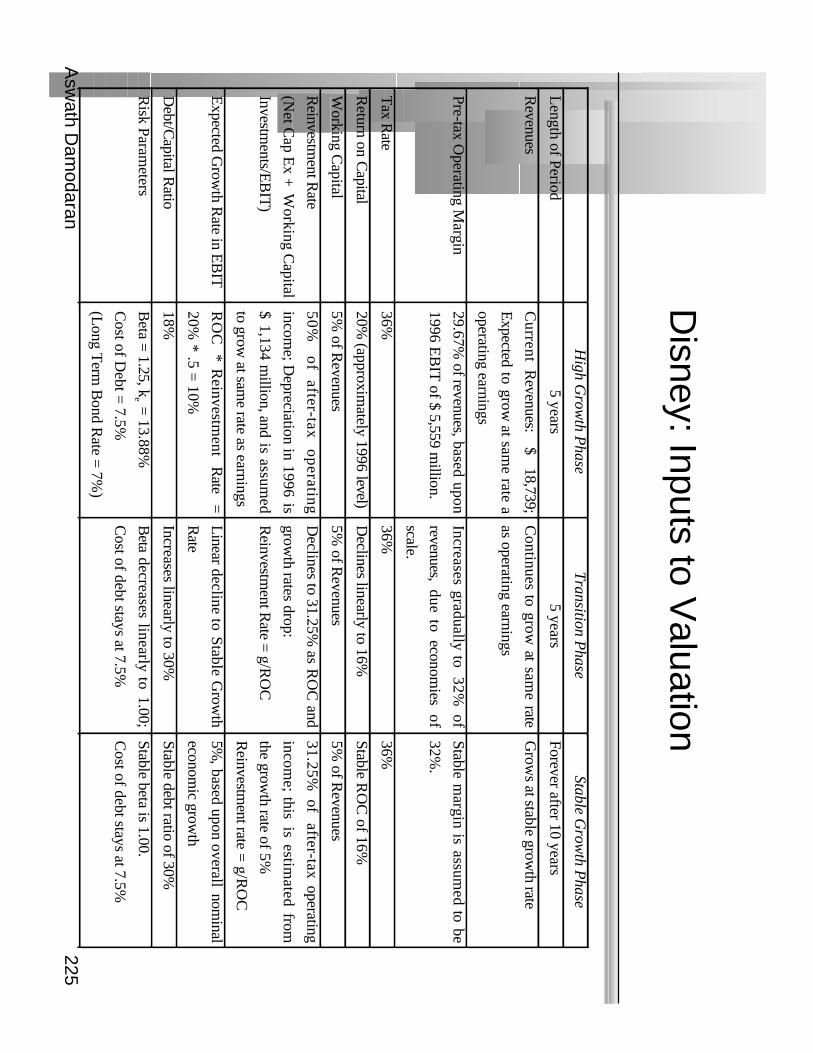

Disney: Inputs to V

aluation

High G

rowth P

haseT

ransition Phase

Stable Grow

th Phase

Length of Period

5 years5 years

Forever after 10 years

Revenues

Current R

evenues: $

18,739;

Expected to grow

at same rate a

operating earnings

Continues to grow

at same rate

as operating earnings

Grow

s at stable growth rate

Pre-tax Operating M

argin29.67%

of revenues, based upon

1996 EB

IT of $ 5,559 m

illion.

Increases gradually to 32%

of

revenues, due to economies of

scale.

Stable margin is assum

ed to be

32%.

Tax R

ate36%

36%36%

Return on C

apital20%

(approximately 1996 level)

Declines linearly to 16%

Stable RO

C of 16%

Working C

apital5%

of Revenues

5% of R

evenues5%

of Revenues

Reinvestm

ent Rate

(Net C

ap Ex +

Working C

apital

Investments/E

BIT

)

50%

of after-tax

operating

income; D

epreciation in 1996 is

$ 1,134 m

illion, and is assumed

to grow at sam

e rate as earnings

Declines to 31.25%

as RO

C and

growth rates drop:

Reinvestm

ent Rate = g/R

OC

31.25% of

after-tax operating

income; this is estim

ated from

the growth rate of 5%

Reinvestm

ent rate = g/R

OC

Expected G

rowth R

ate in EB

ITR

OC

*

Reinvestm

ent R

ate =

20% * .5 =

10%

Linear decline to S

table Grow

th

Rate

5%, based upon overall nom

inal

economic grow

th

Debt/C

apital Ratio

18%Increases linearly to 30%

Stable debt ratio of 30%

Risk Param

etersB

eta = 1.25, ke =

13.88%

Cost of D

ebt = 7.5%

(Long T

erm B

ond Rate =

7%)

Beta decreases linearly to 1.00;

Cost of debt stays at 7.5%

Stable beta is 1.00.

Cost of debt stays at 7.5%

Asw

ath Dam

odaran226

Disney: F

CF

F E

stimates

Base

12

34

56

78

910

Expected G

rowth

10%10%

10%10%

10%9%

8%7%

6%5%

Revenues

$ 18,739 $ 20,613

$ 22,674 $ 24,942

$ 27,436 $ 30,179

$ 32,895 $ 35,527

$ 38,014 $ 40,295

$ 42,310

Oper. M

argin29.67%

29.67%29.67%

29.67%29.67%

29.67%30.13%

30.60%31.07%

31.53%32.00%

EB

IT $ 5,559

$ 6,115 $ 6,726

$ 7,399 $ 8,139

$ 8,953 $ 9,912

$ 10,871 $ 11,809

$ 12,706 $ 13,539

EB

IT (1-t)

$ 3,558 $ 3,914

$ 4,305 $ 4,735

$ 5,209 $ 5,730

$ 6,344 $ 6,957

$ 7,558 $ 8,132

$ 8,665

+ Depreciation

$ 1,134 $ 1,247

$ 1,372 $ 1,509

$ 1,660 $ 1,826

$ 2,009 $ 2,210

$ 2,431 $ 2,674

$ 2,941

- Capital E

xp. $ 1,754

$ 3,101 $ 3,411

$ 3,752 $ 4,128

$ 4,540 $ 4,847

$ 5,103 $ 5,313

$ 5,464 $ 5,548

- Change in W

C $ 94

$ 94 $ 103

$ 113 $ 125

$ 137 $ 136

$ 132 $ 124

$ 114 $ 101

= FC

FF $ 1,779

$ 1,966 $ 2,163

$ 2,379 $ 2,617

$ 2,879 $ 3,370

$ 3,932 $ 4,552

$ 5,228 $ 5,957

RO

C20%

20%20%

20%20%

20%19.2%

18.4%17.6%

16.8%16%

Reinv. R

ate50%

50%50%

50%50%

46.875%43.48%

39.77%35.71%

31.25%

Asw

ath Dam

odaran227

Disney: C

osts of Capital

Year

12

34

56

78

910

Cost of E

quity13.88%

13.88%13.88%

13.88%13.88%

13.60%13.33%

13.05%12.78%

12.50%

Cost of D

ebt4.80%

4.80%4.80%

4.80%4.80%

4.80%4.80%

4.80%4.80%

4.80%

Debt R

atio18.00%

18.00%18.00%

18.00%18.00%

20.40%22.80%

25.20%27.60%

30.00%

Cost of C

apital12.24%

12.24%12.24%

12.24%12.24%

11.80%11.38%

10.97%10.57%

10.19%

Asw

ath Dam

odaran228

Disney: T

erminal V

alue

The term

inal value at the end of year 10 is estimated based upon the

free cash flows to the firm

in year 11 and the cost of capital in year 11.

FCFF

11 = E

BIT

(1-t) - EB

IT (1-t) R

einvestment R

ate

= $ 13,539 (1.05) (1-.36) - $ 13,539 (1.05) (1-.36) (.3125)

= $ 6,255 m

illion

Note that the reinvestm

ent rate is estimated from

the cost of capital of16%

and the expected growth rate of 5%

.

Cost of C

apital in terminal year =

10.19%

Term

inal Value =

$ 6,255/(.1019 - .05) = $ 120,521 m

illion

Asw

ath Dam

odaran229

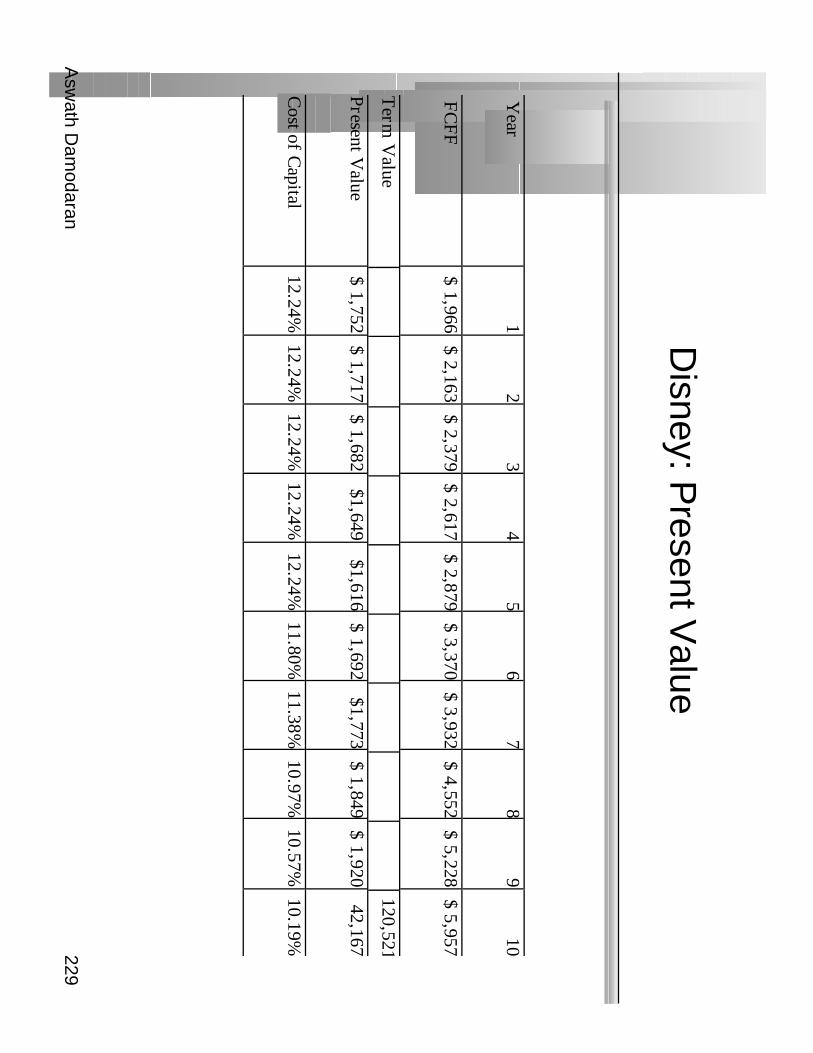

Disney: P

resent Value

Year

12

34

56

78

910

FC

FF

$ 1,966 $ 2,163

$ 2,379 $ 2,617

$ 2,879 $ 3,370

$ 3,932 $ 4,552

$ 5,228 $ 5,957

Term

Value

120,521

Present V

alue $ 1,752

$ 1,717 $ 1,682

$1,649 $1,616

$ 1,692 $1,773

$ 1,849 $ 1,920

42,167

Cost of C

apital12.24%

12.24%12.24%

12.24%12.24%

11.80%11.38%

10.97%10.57%

10.19%

Asw

ath Dam

odaran230

Present V

alue Check

The FC

FF and costs of capital are provided for all 10 years. Confirm

the present value of the FCFF in year 7.

Asw

ath Dam

odaran231

Disney: V

alue Per S

hare

Value of the Firm

=$ 57,817 m

illion

+ V

alue of Cash =

$ 0 (almost no non-operating cash)

- Value of D

ebt =$ 11,180 m

illion

= V

alue of Equity =

$ 46,637 million

/ Num

ber of Shares675.13

Value Per Share =

$ 69.08

Asw

ath Dam

odaran232

Cash

flow

to F

irmE

BIT

(1-t) : 3,558- N

t CpX

612- C

hg WC

617= F

CF

F 2,329

Exp

ected G

row

th

in E

BIT

(1-t).50*.20 =

.1010.00

%

1,9662,163

2,379 2,617

2,879

Forever

Stable G

rowth

g = 5%

; Beta =

1.00; D

/(D+

E) =

30%; R

OC

=16%

Reinvestm

ent Rate=

31.25%

Term

inal Value

10=

6255/(.1019-.05) = 120,52 1

Co

st of E

qu

ity13.85%

Co

st of D

ebt

(7%+

0.50%)(1-.36)

= 4.80%

Weig

hts

E =

82% D

= 18%

Discount at

Cost of C

apital (WA

CC

) = 13.85%

(0.82) + 4.8%

(0.18) = 12.22%

57,817- 11,180=

46,637P

er Share: 69.08

Riskfree R

ate:

Governm

ent Bond

Rate =

7%+

Beta

1.25X

Risk P

remiu

m5.5%

Unlevered B

eta for S

ectors: 1.09F

irm’s D

/ER

atio: 21.95%H

istorical US

P

remium

5.5%

Country R

iskP

remium

0%

Disney: A

Valuation

Reinvestm

ent Rate

50.00%R

eturn on Capital

20%

3,370 3,932

4,552 5,228

5,957

TransitionB

eta drops to 1.00D

ebt ratio rises to 30%

RO

C drops to 16%

Reinv. rate drops to 31.25%

Asw

ath Dam

odaran233

Th

e Investm

ent D

ecision

Invest in projects that yield a return

greater than the m

inimum

acceptablehurdle rate

Th

e Fin

ancin

g D

ecision

Choose a financing m

ix that

maxim

izes the value of the projectstaken, and

matches the assets

beingfinanced.

Th

e Divid

end

Decisio

nIf there are

not enoughinvestm

ents that earn the

hurdle rate, return the cash

tothe ow

ners

Current

EB

IT(1-t) =

$3,558 m

illion

Return on C

apital20.00%

Reinvestm

ent Rate

50%

Expected G

rowth =

RO

C * R

R=

.50 * 20%=

10%

Cost of C

apital12.22%

Determ

ine the business risk of the firm (B

eta, Default R

isk)

Equity:

Beta=

1.25D

ebt::D

efault Risk

In stable growth:

Reinvestm

ent Rate=

31.67%R

eturn on Capital = 16%

Beta =

1.00D

ebt Ratio =

30.00%C

ost of Capital =

10.19%

Transition tostable grow

thinputs

Year

EB

IT(1-t)

Reinvestm

entF

CF

FT

erminal V

aluePV

13,914

$ 1,947

$ 1,966

$ 1,752

$ 2

4,305$

2,142$

2,163$

1,717$

34,735

$ 2,356

$ 2,379

$ 1,682

$ 4

5,209$

2,343$

2,866$

1,649$

55,730

$ 2,851

$ 2,879

$ 1,616

$ 6

6,344$

2,974$

3,370$

1,692$

76,957

$ 2,762

$ 4,196

$ 1,773

$ 8

7,558$

3,006$

4,552$

1,849$

98,132

$ 2,904

$ 5,228

$ 1,920

$ 10

8,665$

2,708$

5,957$

120,521$

42,167$ 57,817$ $11,180

46,637$

69.08$

Value of D

isney =

= Value of E

quity - V

alue of Debt =

Value of D

isney/share =

Asw

ath Dam

odaran234

Relative V

aluation

In relative valuation, the value of an asset is derived from the pricing

of 'comparable' assets, standardized using a com

mon variable such as

earnings, cashflows, book value or revenues. E

xamples include --

•Price/E

arnings (P/E) ratios

–and variants (E

BIT

multiples, E

BIT

DA

multiples, C

ash Flow m

ultiples)

•Price/B

ook (P/BV

) ratios–

and variants (Tobin's Q

)

•Price/Sales ratios

Asw

ath Dam

odaran235

Multiples and F

undamenals

Gordon G

rowth M

odel:

Dividing both sides by the earnings,

Dividing both sides by the book value of equity,

If the return on equity is written in term

s of the retention ratio and theexpected grow

th rate

Dividing by the Sales per share,

P0=

DP

S1

r−

gn

P0

EP

S0=

PE

= P

ayout Ratio

*(1+

gn )

r-gn

P0

BV

0=

PB

V=

RO

E - g

n

r-gn

P0

BV

0=

PB

V=

RO

E*

Payout R

atio*

(1+

gn )

r-gn

P0

Sales0

=P

S=

Profit M

argin*

Payout R

atio*

(1+

gn )

r-gn

Asw

ath Dam

odaran236

Disney: R

elative Valuation

Com

panyP

EE

xpected Grow

thP

EG

King W

orld Productions10.4

7.00%1.49

Aztar

11.912.00%

0.99

Viacom

12.118.00%

0.67

All A

merican C

omm

unications15.8

20.00%0.79

GC

Com

panies20.2

15.00%1.35

Circus C

ircus Enterprises

20.817.00%

1.22

Polygram N

V A

DR

22.613.00%

1.74

Regal C

inemas

25.823.00%

1.12

Walt D

isney27.9

18.00%1.55

AM

C E

ntertainment

29.520.00%

1.48

Premier Parks

32.928.00%

1.18

Family G

olf Centers

33.136.00%

0.92

CIN

AR

Films

48.425.00%

1.94

Average

22.1918.56%

1.20

Asw

ath Dam

odaran237

Is Disney fairly valued?

Based upon the PE

ratio, is Disney under, over or correctly valued?

Under V

alued

Over V

alued

Correctly V

alued

Based upon the PE

G ratio, is D

isney under valued?

Under V

alued

Over V

alued

Correctly V

alued

Will this valuation give you a higher or low

er valuation than thediscounted C

F valutaion?

Higher

Low

er

Asw

ath Dam

odaran238

Relative V

aluation Assum

ptions

Assum

e that you are reading an equity research report where a buy

recomm

endation for a company is being based upon the fact that its PE

ratio is lower than the average for the industry. Im

plicitly, what is the

underlying assumption or assum

ptions being made by this analyst?

The sector itself is, on average, fairly priced

The earnings of the firm

s in the group are being measured consistently

The firm

s in the group are all of equivalent risk

The firm

s in the group are all at the same stage in the grow

th cycle

The firm

s in the group are of equivalent risk and have similar cash

flow patterns

All of the above

Asw

ath Dam

odaran239

First P

rinciples

Invest in projects that yield a return greater than the minim

umacceptable hurdle rate.•

The hurdle rate should be higher for riskier projects and reflect the

financing mix used - ow

ners’ funds (equity) or borrowed m

oney (debt)

•R

eturns on projects should be measured based on cash flow

s generatedand the tim

ing of these cash flows; they should also consider both positive

and negative side effects of these projects.

Choose a financing m

ix that minim

izes the hurdle rate and matches the

assets being financed.

If there are not enough investments that earn the hurdle rate, return the

cash to stockholders.•

The form

of returns - dividends and stock buybacks - will depend upon

the stockholders’ characteristics.

Objective: M

aximize the V

alue of the Firm