Omitted Variable Bias Methods of Economic Investigation Lecture 7 1.

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 1/23

1

Impact of Economic Variables onImpact of Economic Variables on

Stock PricesStock Prices

A Research Paper by

Prof. Rana Abdul Qudous

Fariha Shoukat Malik

Prof. Dr. M. Iqbal Saif

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 2/23

2

Abstract

The objective of this paper is to analyze the relationship

between stock prices and certain relevant macroeconomic

variables. These variables include money supply, exports,

foreign exchange rate, industrial production and interest

rate. The study covers a period of 10 Years from January 1,

2000 to December 31, 2009. The results indicate that all

macroeconomic variables

««««««««««««««««««««««««««««««««««««««««««««««««««

«««««««««««««««««««««««««

«««««««««««««««««««««««««

«««..

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 3/23

3

Stock market is an enigma for many people who think that

it has something to do with riches only whereas may

believes it is a heaven for gamblers and is not related to

common man in any sense.

Stock market is a place where we can buy or sell shares and

securities. Stock market can be easily understood by

dividing it into primary and secondary markets. Primary

market is where companies and government issue share

and securities to the public to finance their operations. This

way savings of the people are channelized to productive

ventures.

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 4/23

4

Secondary markets provide the investors an opportunity to selltheir shares and securities to other investors. These trades are

facilitated by the brokers who charge a commission for the order

executed by them on behalf of their clients. Stock exchanges like

Karachi Stock Exchange and Lahore Stock Exchange are

secondary markets.

Pakistan has three stock exchanges. Karachi Stock Exchange,

Lahore Stock Exchange and Islamabad Stock Exchange. Karachi

Stock Exchange(KSE) is the oldest stock exchange of the country.

It was incorporated on March, 1949. It started with 5 companieswith a paid up capital of Rs. 37 Million(.44 Million USD) and now

the market capitalization is equal to 26.48 Billion US Dollar with

651 companies listed on the Exchange

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 5/23

5

It has four indices ie. KSE 100 index, KSE 30, KMI 30 andKSE All Shares Index. KSE 100 Index is most represented

index of the Pakistani stock market. The KSE-100 Index was

introduced in November, 1991 and was recomposed in

November 1994. This index showed a return of 40.19% for

the year 2007.

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 6/23

6

Purpose of the Study

The focus of this study is to analyze the relationship between

stock prices and certain relevant macroeconomic variables

and whether these variables can be used to predict stock

pries in Pakistan?. These variables include money supply,

export, foreign exchange rate and interest. The stock prices

are represented by KSE-100 index.

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 7/23

7

Stock Prices and Interest Rates:

The perception concerning the relationship between interest

rates and equity prices is well recognized, signifying that anincrease in interest rates increases the opportunity cost of

holding money and thus substituted by interest bearing

securities, which then cause a fall in equity prices. Another

argument is that when interest rate increases, it increases the

cost of production and decreases the profits of the companywhich, thus, reduces the prices of shares.

Economic VariablesEconomic Variables

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 8/23

8

Increase in industrial production decreases production cost

due to fixed cost element because fixed cost remains fixed andit is only the variable cost which is added. So per unit cost is

decreased. This leads to higher profit margins and ultimately

increase in stock price.

Industrial production index and Stock Prices:

Economic VariablesEconomic Variables

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 9/23

9

Increase in money supply bring essentially needed liquidity to

the market. Due to availability of the money, trading activity in

the market is increased which results into increase in stock

prices. Moreover, increase in money supply bring inflation,

which is rise in prices. Along with prices of the goods, price of

shares and securities is also increased.

Stock Prices and Money Supply:

Economic VariablesEconomic Variables

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 10/23

10

Change in foreign exchange rate affects the market in two

ways. If the currency is depreciated, stock will be available

to the potential international investor at a cheaper rate.Whereas those who have already invested will fear a

decrease in their return, thus, there will a higher trading

activity affecting stock prices with a change in currency

value.

Stock Prices and Exchange rate:

Economic VariablesEconomic Variables

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 11/23

11

Exports brings much needed foreign exchange to the country

which has a healthy impact on the economy. The exporting

companies enjoys tax concessions and lower rate of interest onloans meant for export purpose. This way their profit margin

is increased. These companies charge a better price from their

customers in advanced countries and consequently the profits

are increased. So increase in exports leads to the increase in

stock prices

Stock Prices and Exports

Economic VariablesEconomic Variables

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 12/23

12

Model

The stock prices are dependent variable hypothesized to be

influenced by independent variables. These independent

variables are set up as log of Foreign Exchange Rate referredto as eXCH, log of interest as iNT, log of industrial

production as iPR, log of money supply as mSUP, and log of

export as eXP. Whereas log of stock prices are referred to as

sTKP

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 13/23

13

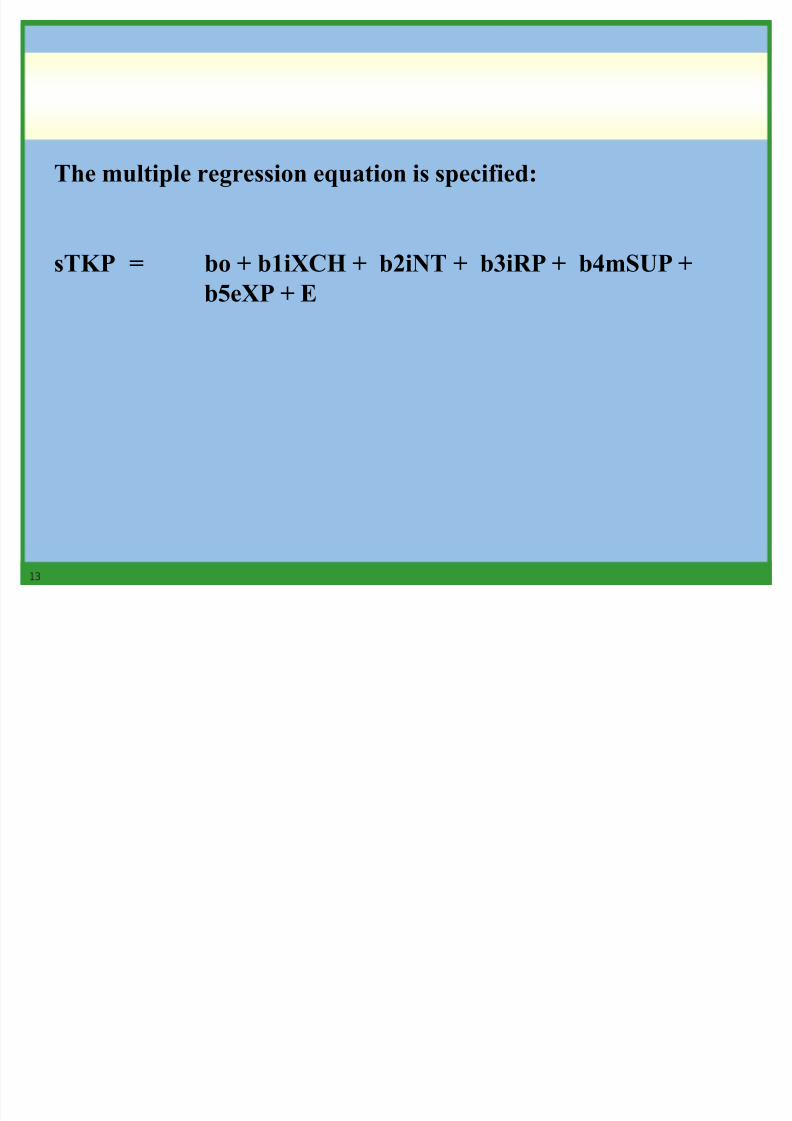

The multiple regression equation is specified:

sTKP = bo + b1iXCH + b2iNT + b3iRP + b4mSUP +

b5eXP + E

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 14/23

14

Where

bo = a constant

b1 = regression coefficient that measures the

sensitivity of sTKP to iXCH

b2 = regression coefficient that measures the

sensitivity of sTKP to iNT

b3 = regression coefficient that measures the

sensitivity of sTKP to iRP

b4 = regression coefficient that measures the

sensitivity of sTKP to mSUPb5 = regression coefficient that measures the

sensitivity of sTKP to eXP

E = Error Term

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 15/23

15

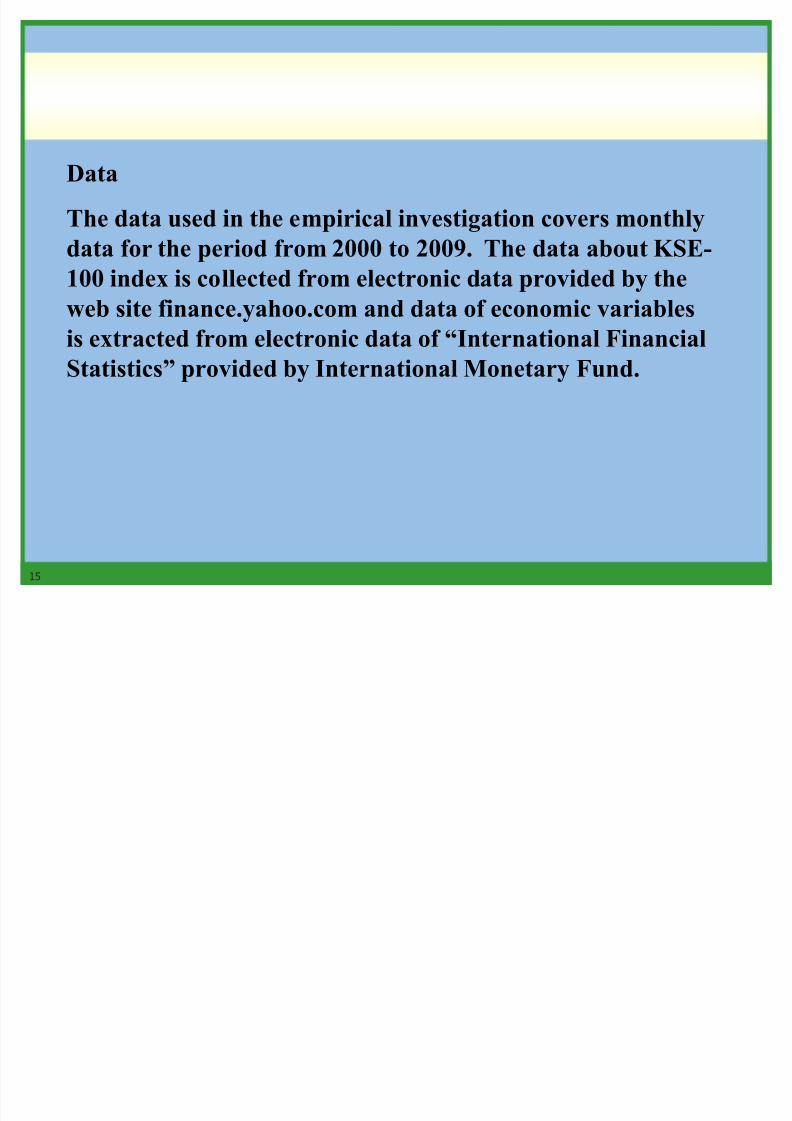

Data

The data used in the empirical investigation covers monthly

data for the period from 2000 to 2009. The data about KSE-

100 index is collected from electronic data provided by theweb site finance.yahoo.com and data of economic variables

is extracted from electronic data of ³International Financial

Statistics´ provided by International Monetary Fund.

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 16/23

16

Analytical Framework

A systematic approach for data analysis was used. The

Augmented Dickey-Fuller (ADF) Test was applied to check

the stationarity of the data. Useful inference can be drawn if the time series consists of stationary data. A data series is

considered to be stationary if its mean and variance are

constant over time and the value of covariance between two

time periods depends only on the lag between the two time

periods and not on the actual time at which the covariance iscomputed. Linear regression was used to quantify the

strength of relationship between stock prices and other

independent variables.

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 17/23

17

Data Analysis

Conclusion

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 18/23

18

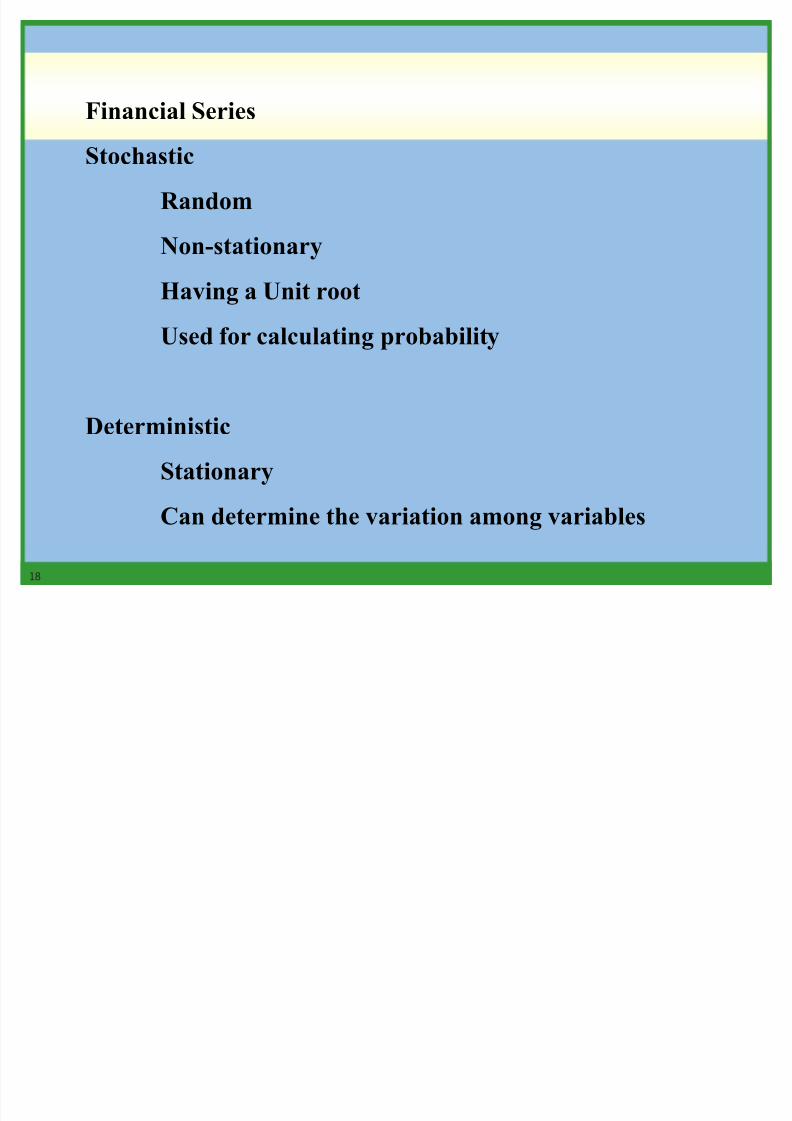

Financial Series

Stochastic

Random

Non-stationary

Having a Unit root

Used for calculating probability

Deterministic

Stationary

Can determine the variation among variables

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 19/23

19

Unit Root Test

For series considered as stationary t-stat < 5% CV

If series is not statinary then take its natural log return

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 20/23

20

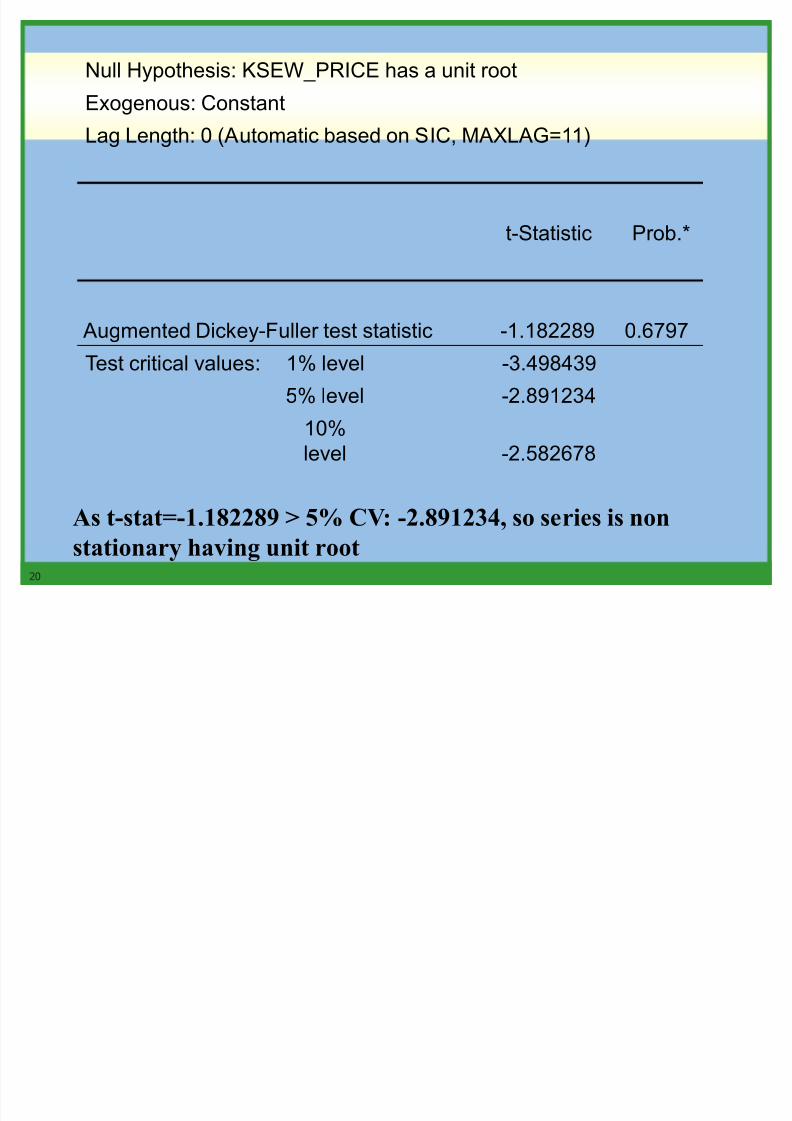

Null Hypothesis: KSEW_PRICE has a unit root

Exogenous: Constant

Lag Length: 0 (Automatic based on SIC, MAXLAG=11)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -1.182289 0.6797

Test critical values: 1% level -3.498439

5% level -2.891234

10%

level -2.582678

As t-stat=-1.182289 > 5% CV: -2.891234, so series is non

stationary having unit root

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 21/23

21

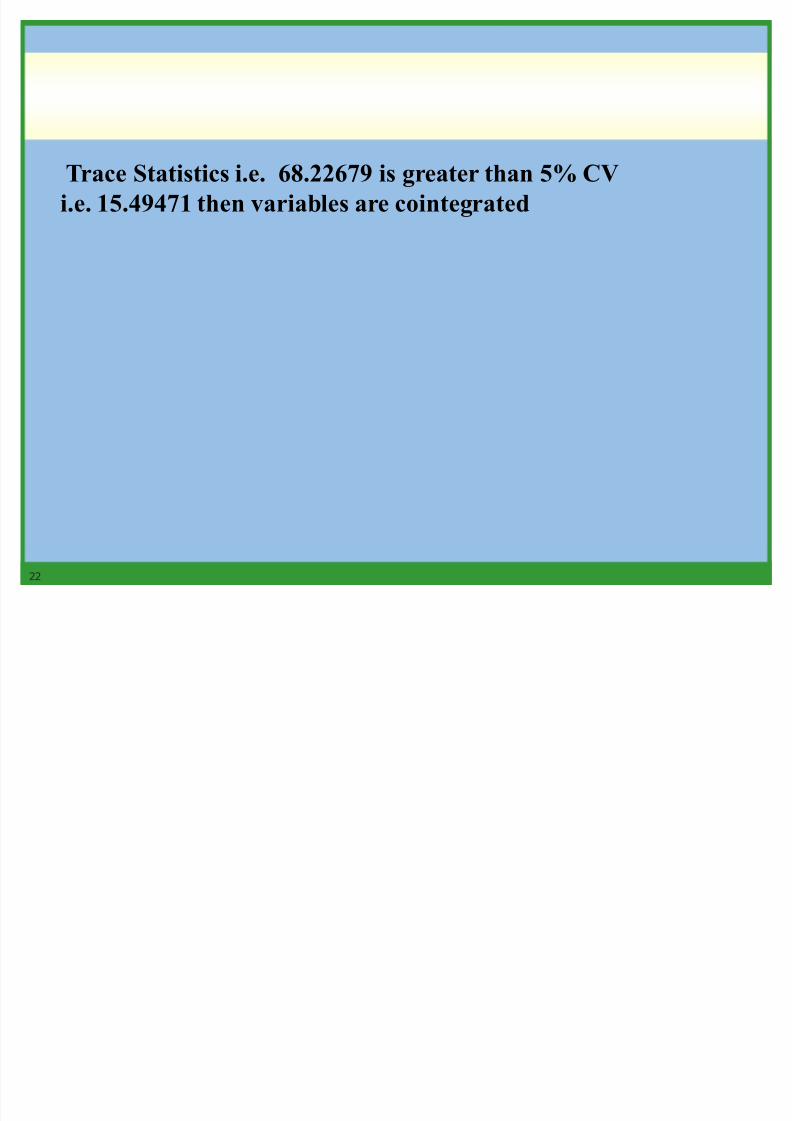

Unrestricted Cointegration Rank Test (Trace)

Hypothesi

zed Trace 0.05

No. of CE(s)

Eigenvalue Statistic

CriticalValue Prob.**

None * 0.329454 68.22679 15.49471 0.000

At most 1 0.211774 25.46290 3.841466 0.000

Cointegration

If Trace Statistics is less than 5% CV then variables are not

cointegrated

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 22/23

22

Trace Statistics i.e. 68.22679 is greater than 5% CV

i.e. 15.49471 then variables are cointegrated

8/6/2019 (ASSIGNMENT)+Economic Variable

http://slidepdf.com/reader/full/assignmenteconomic-variable 23/23

23

GrangerCausality Test

If F-statistics is large and the probability value is close to0 then the variableGranger causes the other variable.

Null Hypothesis:Observation

F-

Statistic

Probability

eXCH does not Granger

Cause sTKP 118 0.488 0.6150sTKP does not Granger Cause

eXCH 0.616 0.5415