IAS37 - Provisions, Contingent Liabilities and Contingent ...

Upload

linette-porterCategory

view

222download

3

Asset Pricing

Zheng Zhenlong

Ch3. Contingent Claims Markets

18:08

Asset Pricing

Zheng ZhenlongBrief introduction

• In the frame of complete market, we look forward to see the equation p=E(mx) more intuitive.

• The structure is as follows: Contingent Claims Risk-Neutral Probabilities Investors Again Risk Sharing State Diagram and Price Function

18:08

Asset Pricing

Zheng Zhenlong3.1 Contingent Claims

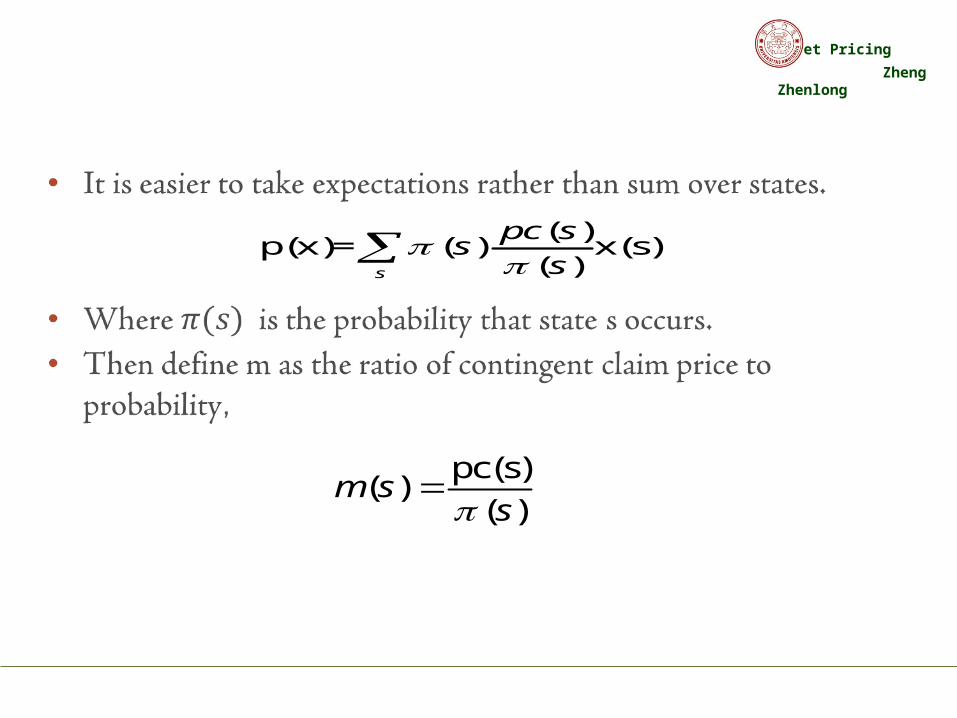

• A contingent claim is a security that pays one dollar (or one unit of the consumption good) in one state s only tomorrow.

• pc(s) is the price today of the contingent claim. (状态价格)

Asset Pricing

Zheng ZhenlongComplete market

p(x)= ( )x(s)s

pc s

Asset Pricing

Zheng Zhenlong

( )p(x)= ( ) x(s)

( )s

pc ss

s

pc(s)( )

( )m s

s

Asset Pricing

Zheng Zhenlong

Conclusion about discount factor

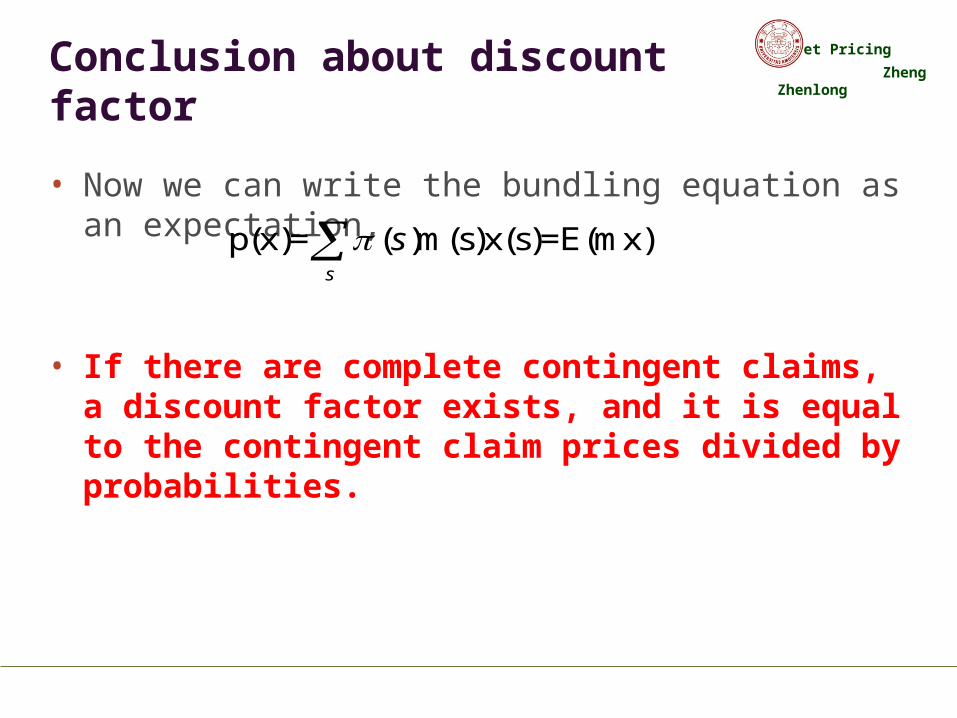

• Now we can write the bundling equation as an expectation,

• If there are complete contingent claims, a discount factor exists, and it is equal to the contingent claim prices divided by probabilities.

p(x)= ( )m(s)x(s)=E(mx)s

s

Asset Pricing

Zheng ZhenlongExpand to infinite space

• In general, we posit states of nature ω that can take continuous (uncountably infinite) values in a space Ω. In this case, the sums become integrals, and we have to use some measure to integrate over Ω. Thus, scaling contingent claims prices by some probability-like object is unavoidable.

Asset Pricing

Zheng Zhenlong

3.2 Risk- neutral probabilities

( )( )

( )

( ) ( ) ( ) ( ) ( ),

( )( ) ( ) ( ) ( )

( )

s

s

f

pc ss

pc s

pc s m s s pc s E m

m ss s R m s s

E m

Asset Pricing

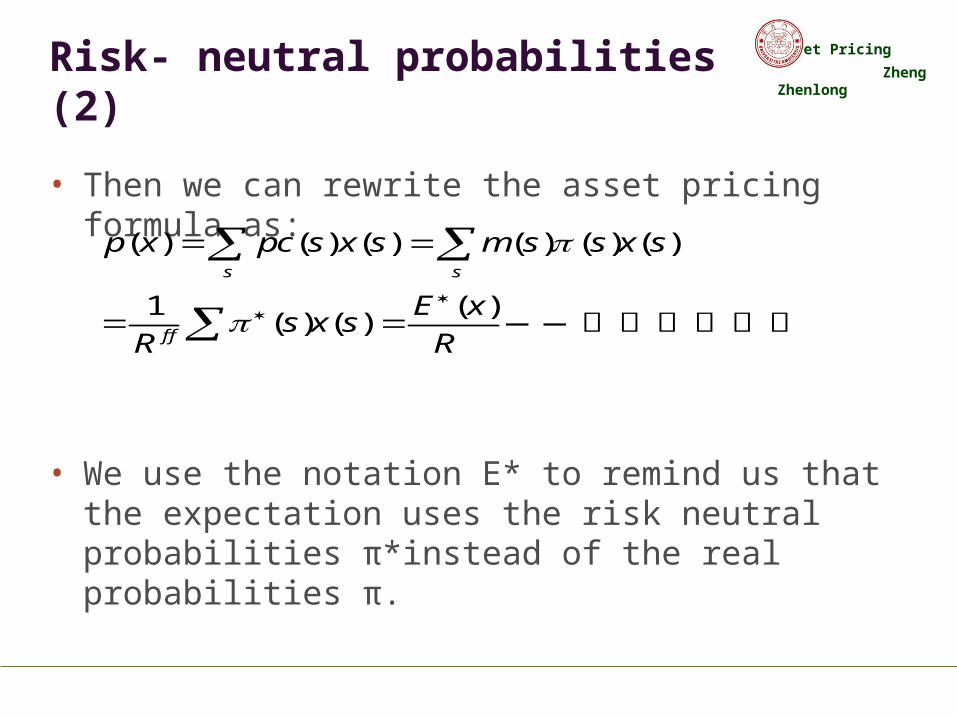

Zheng ZhenlongRisk- neutral probabilities (2)

• Then we can rewrite the asset pricing formula as:

• We use the notation E* to remind us that the expectation uses the risk neutral probabilities π*instead of the real probabilities π.

( ) ( ) ( ) ( ) ( ) ( )

1 ( )( ) ( )

s s

f f

p x pc s x s m s s x s

E xs x s

R R

——风险中性定价

Asset Pricing

Zheng Zhenlong

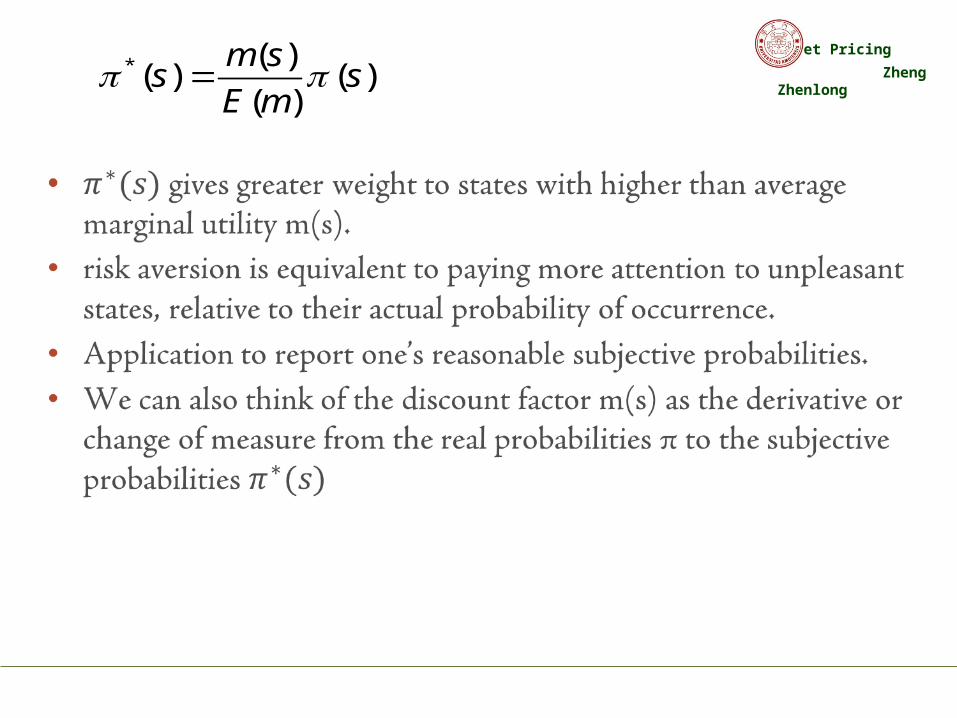

* ( )( ) ( )

( )

m ss s

E m

Asset Pricing

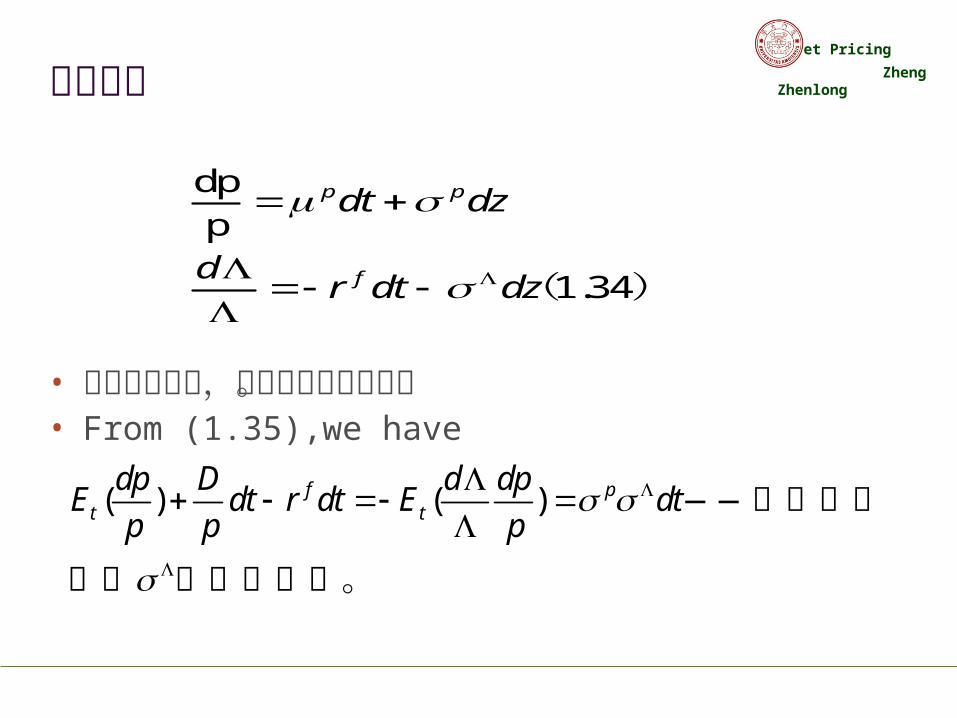

Zheng Zhenlong连续时间

• 在完全市场中,两者的风险源相同。• From (1.35),we have

1.34

p p

f

dt dz

dr dt dz

dpp

( )

( ) ( )f pt t

dp D d dpE dt r dt E dt

p p p

——超额收益

可见 是风险价格。

Asset Pricing

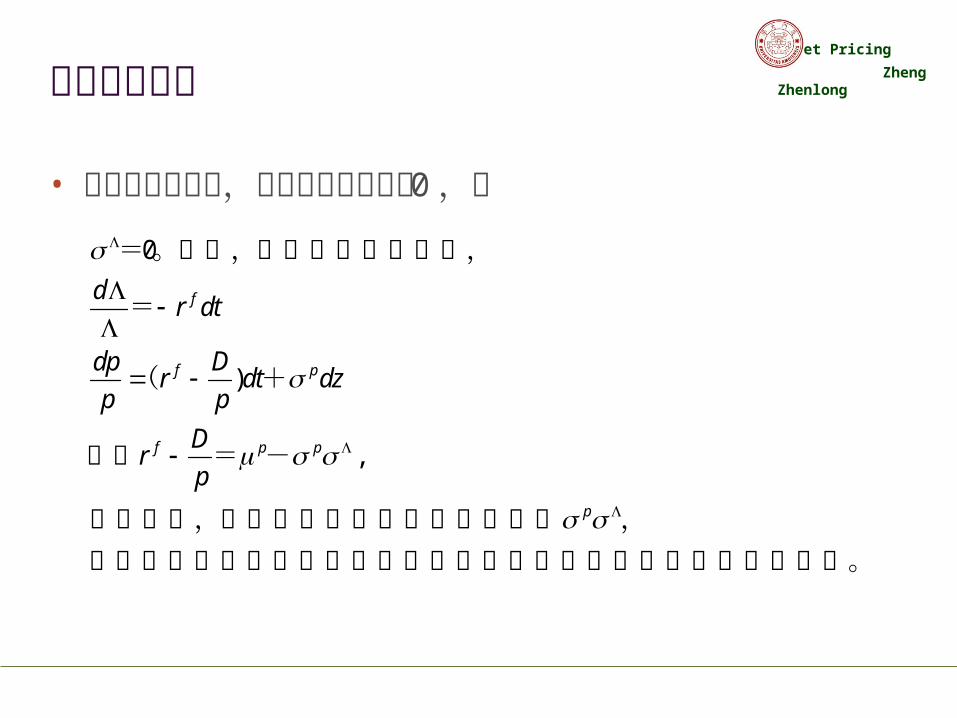

Zheng Zhenlong风险中性定价

• 在风险中性世界,风险价格必须等于 0 ,即

0

)

,

f

f p

f p p

p

dr dt

dp Dr dt dz

p p

Dr

p

=。这样,在风险中性世界中,

=

( +

由于 = -

也就是说,我们只要把价格的偏移率减少 ,并去掉随机贴现因子的扰动项就可以得到风险中性世界的随机过程。

Asset Pricing

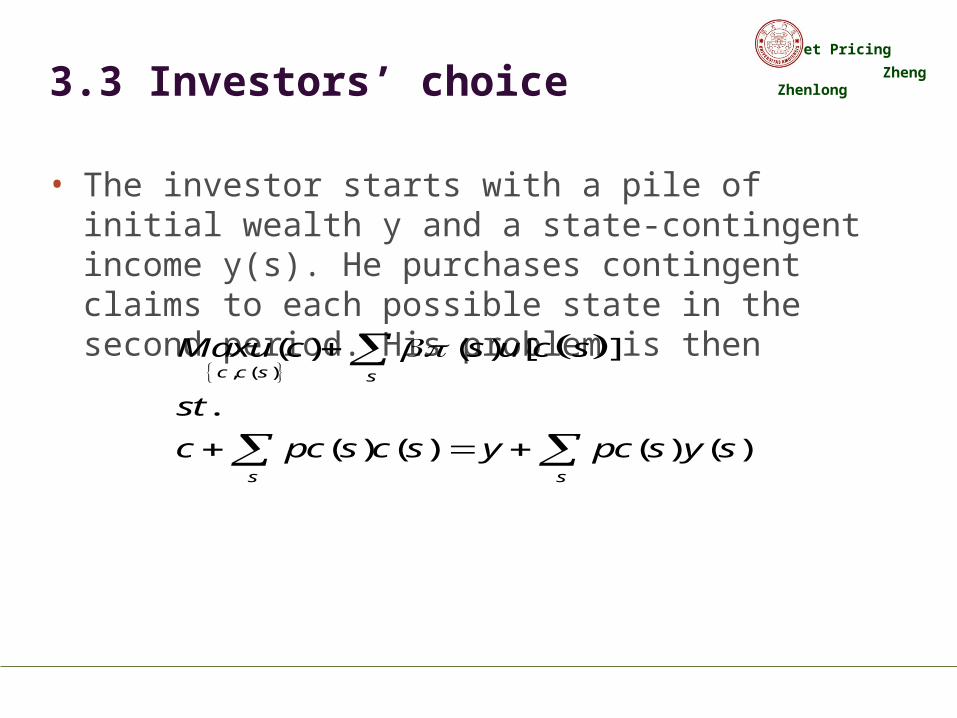

Zheng Zhenlong3.3 Investors’ choice

• The investor starts with a pile of initial wealth y and a state-contingent income y(s). He purchases contingent claims to each possible state in the second period. His problem is then

, ( )( ) ( ) [ ]

.

( ) ( ) ( ) ( )

c c s s

s s

Maxu c s u c s

st

c pc s c s y pc s y s

Asset Pricing

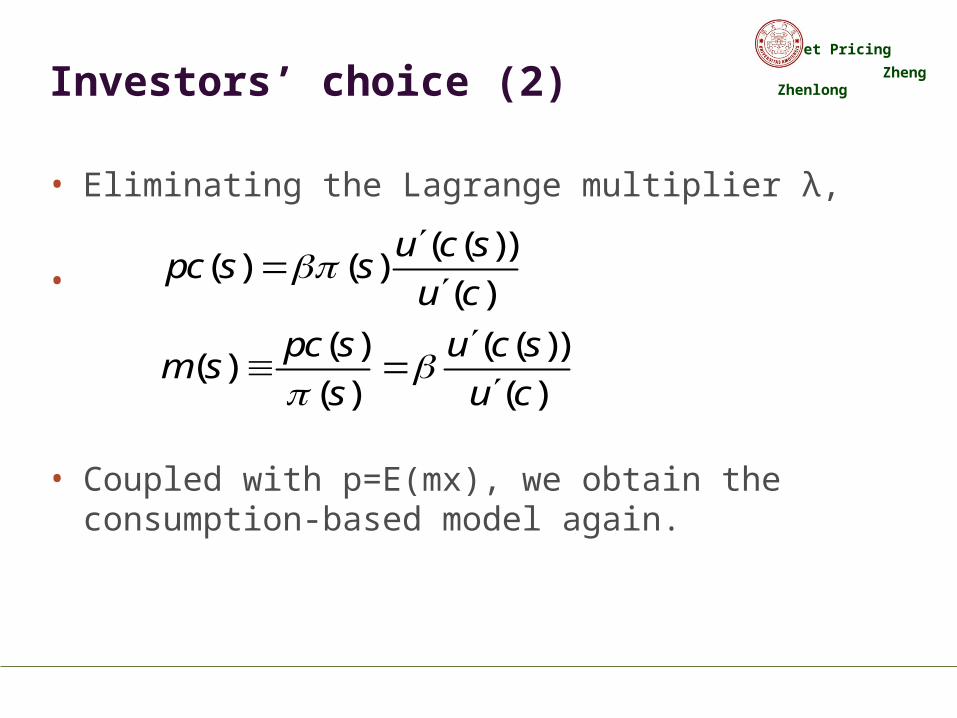

Zheng ZhenlongInvestors’ choice (2)

• Eliminating the Lagrange multiplier λ,

•

• Coupled with p=E(mx), we obtain the consumption-based model again.

( ( ))( ) ( )

( )

( ) ( ( ))( )

( ) ( )

u c spc s s

u c

pc s u c sm s

s u c

Asset Pricing

Zheng Zhenlong

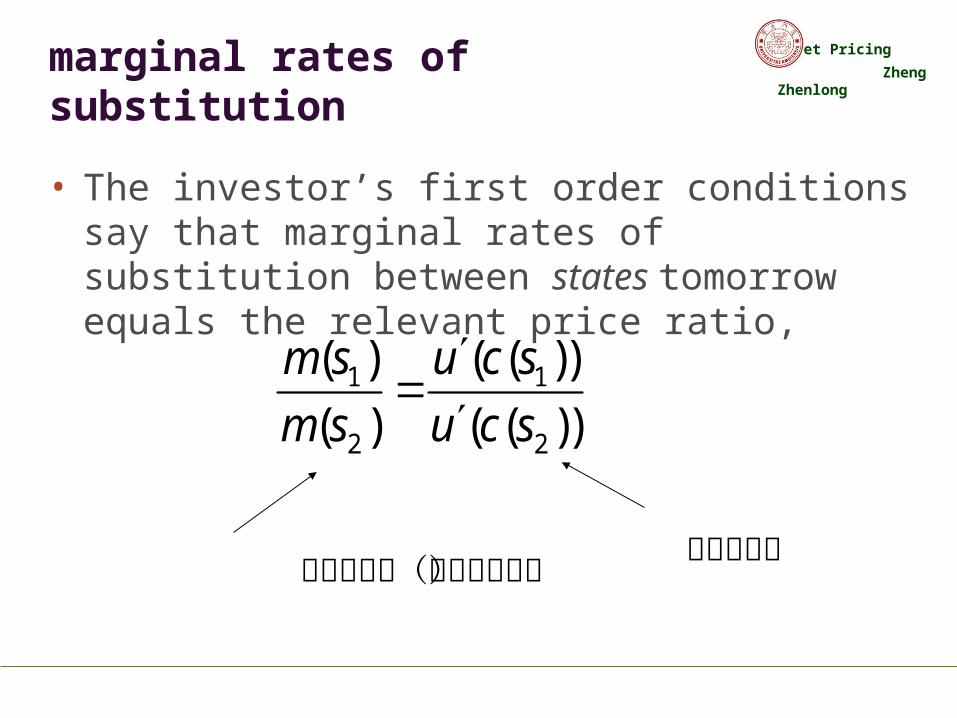

marginal rates of substitution

• The investor’s first order conditions say that marginal rates of substitution between states tomorrow equals the relevant price ratio,

边际替代率相对价格比(经概率调整)

1 1

2 2

( ) ( ( ))

( ) ( ( ))

m s u c s

m s u c s

Asset Pricing

Zheng Zhenlong

Economics behind this approach to asset pricing (figure 3.1)

Asset Pricing

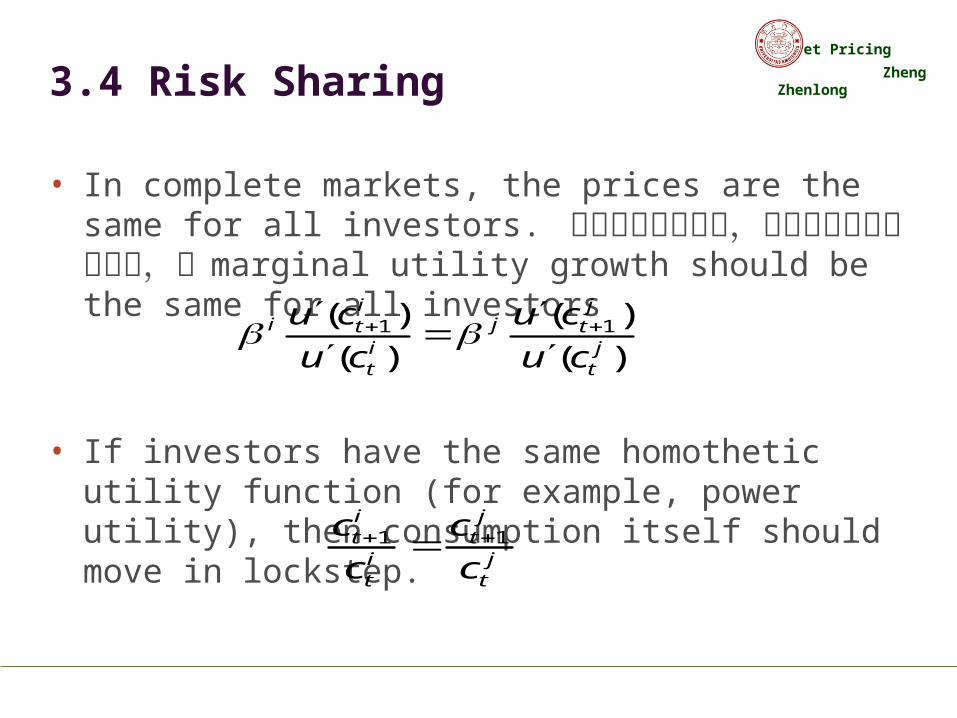

Zheng Zhenlong3.4 Risk Sharing

• In complete markets, the prices are the same for all investors. 如果信息是透明的,每个人都知道客观概率,则 marginal utility growth should be the same for all investors

• If investors have the same homothetic utility function (for example, power utility), then consumption itself should move in lockstep.

1 1( ) ( )

( ) ( )

i ji jt t

i jt t

u c u c

u c u c

1 1i jt ti jt t

c c

c c

Asset Pricing

Zheng ZhenlongRisk Sharing (2)

• It means that shocks to consumption are perfectly correlated across individuals.

• It doesn’t say that expected consumption growth should be equal; it says that consumption growth should be equal ex post.

• In a complete contingent claims market, all investors share all risks, so when any shock hits, it hits us all equally (after insurance payments).

Asset Pricing

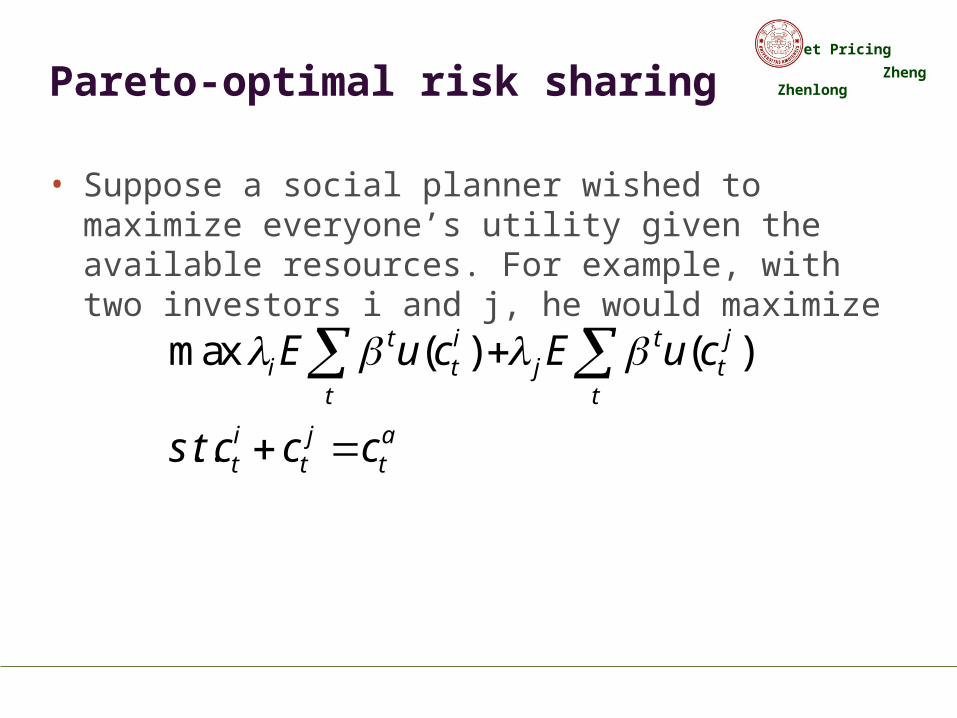

Zheng ZhenlongPareto-optimal risk sharing

• Suppose a social planner wished to maximize everyone’s utility given the available resources. For example, with two investors i and j, he would maximize

max ( ) ( )

. .

t i t ji t j t

t t

i j at t t

E u c E u c

s t c c c

Asset Pricing

Zheng Zhenlong

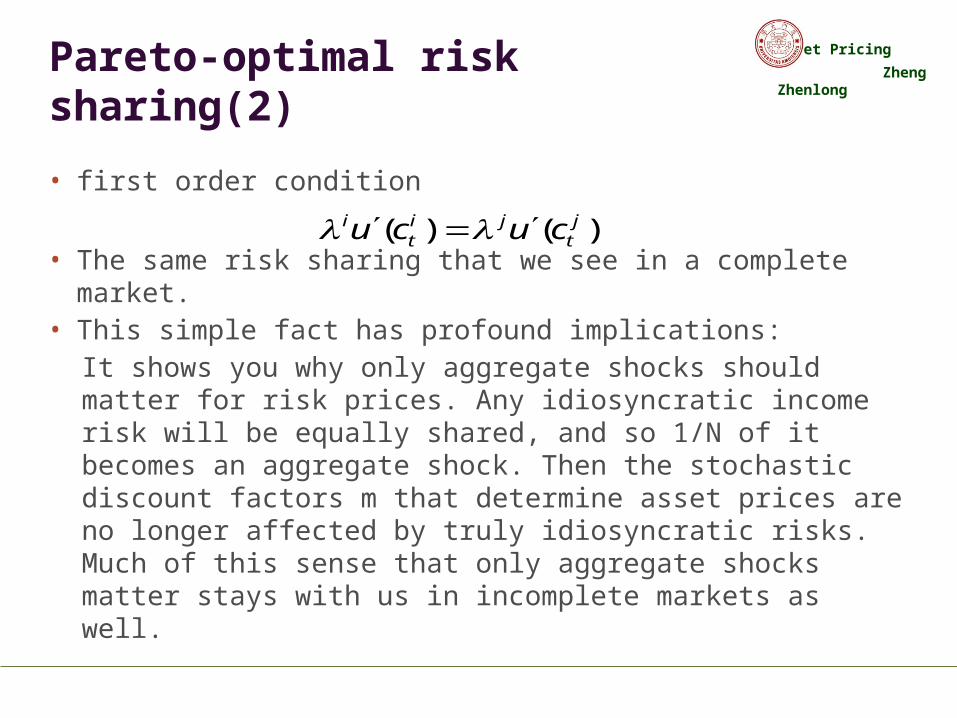

Pareto-optimal risk sharing(2)

• first order condition

• The same risk sharing that we see in a complete market.

• This simple fact has profound implications:It shows you why only aggregate shocks should matter for risk prices. Any idiosyncratic income risk will be equally shared, and so 1/N of it becomes an aggregate shock. Then the stochastic discount factors m that determine asset prices are no longer affected by truly idiosyncratic risks. Much of this sense that only aggregate shocks matter stays with us in incomplete markets as well.

( ) ( )i i j jt tu c u c

Asset Pricing

Zheng ZhenlongSub-markets for risk sharing:

• Insurance market• bond market• stock market

Asset Pricing

Zheng Zhenlong

Reasons for individual consumptions not move in lockstep• The real economy does not yet have complete

markets or full risk sharing.• Different utility functions• Different value of individual impatient

coefficients.

Asset Pricing

Zheng Zhenlong

3.5 State Diagram and Price Function

'[ (1) (2) ( )]pc pc pc pc S '[ (1) (2) ( )]x x x x S

Asset Pricing

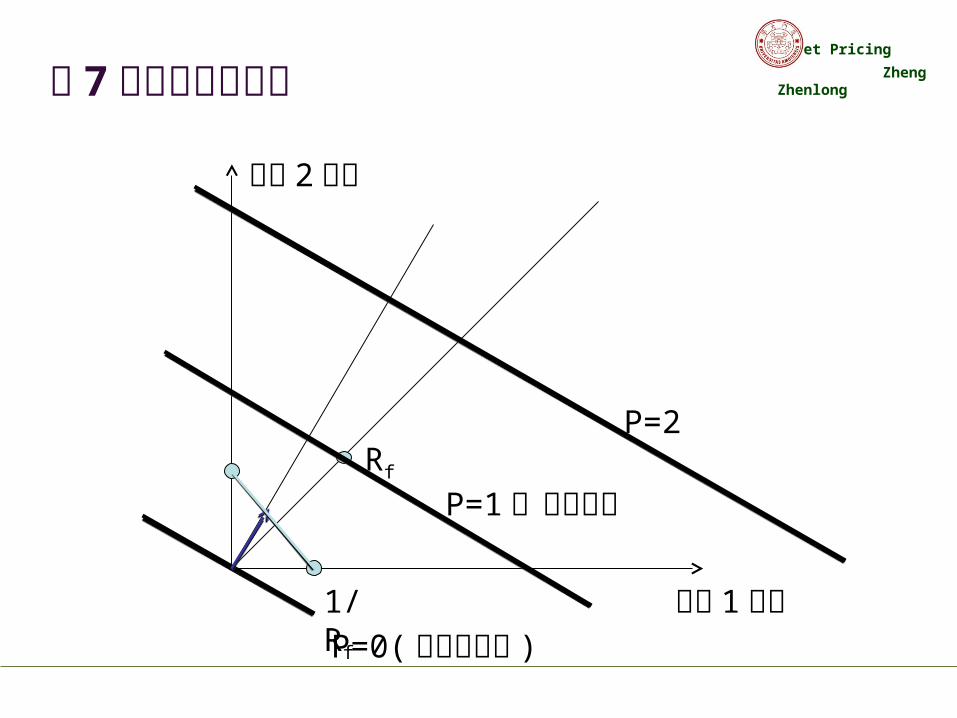

Zheng Zhenlong图 7 状态价格与回报

P=0(超额收益率 )

Rf

P=2

P=1(收益率)

状态 1回报

状态 2回报

1/Rf

Asset Pricing

Zheng Zhenlong

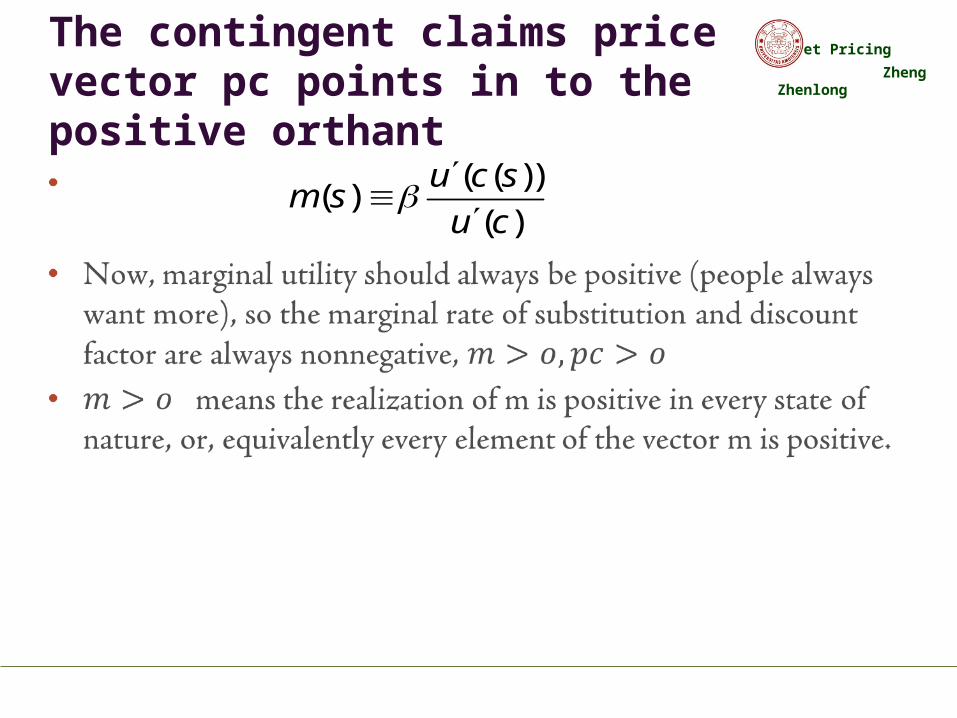

The contingent claims price vector pc points in to the positive orthant

( ( ))( )

( )

u c sm s

u c

Asset Pricing

Zheng Zhenlongpc线的斜率

• 在经概率调整后的状态偏好中性世界中, pc(1)=pc(2),因此 pc 线是 45 度线。

• 在现实生活中,投资者对不同状态的偏好不同。投资者越爱好(经概率调整)某种状态的 PAYOFF ,该状态的 PC就越高。在上图中, pc(1)<pc(2), 所以 pc 线较陡。

Asset Pricing

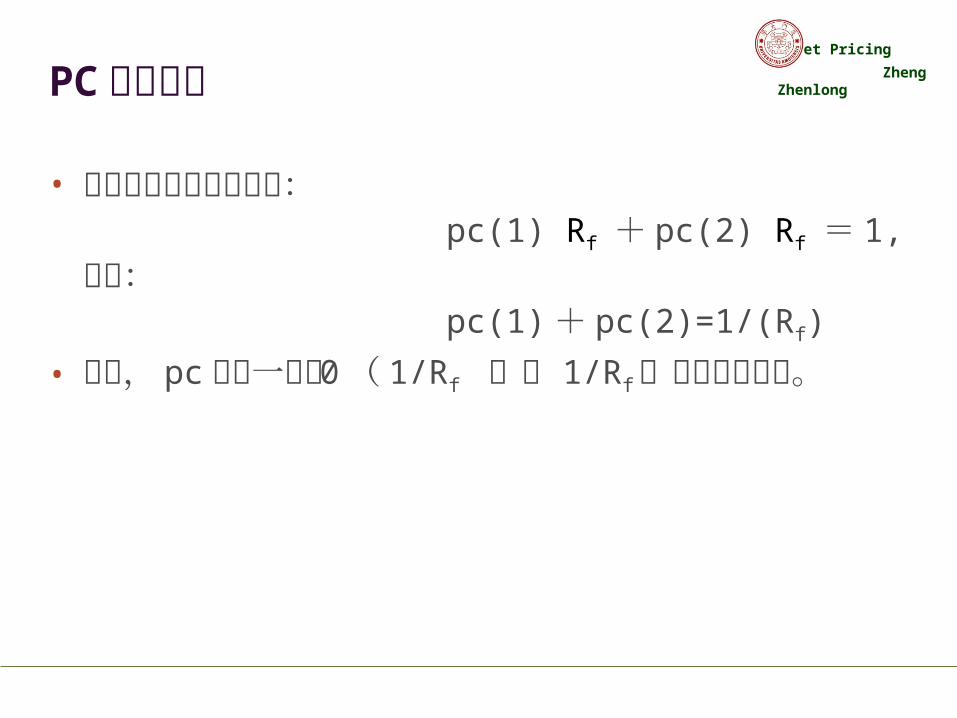

Zheng ZhenlongPC线的长度

• 对无风险资产定价可知: pc(1) Rf + pc(2) Rf = 1, 可得: pc(1)+ pc(2)=1/(Rf)

• 可见, pc 向量一定在 0 ( 1/Rf )( 1/Rf )这个三角形中。

Asset Pricing

Zheng Zhenlong

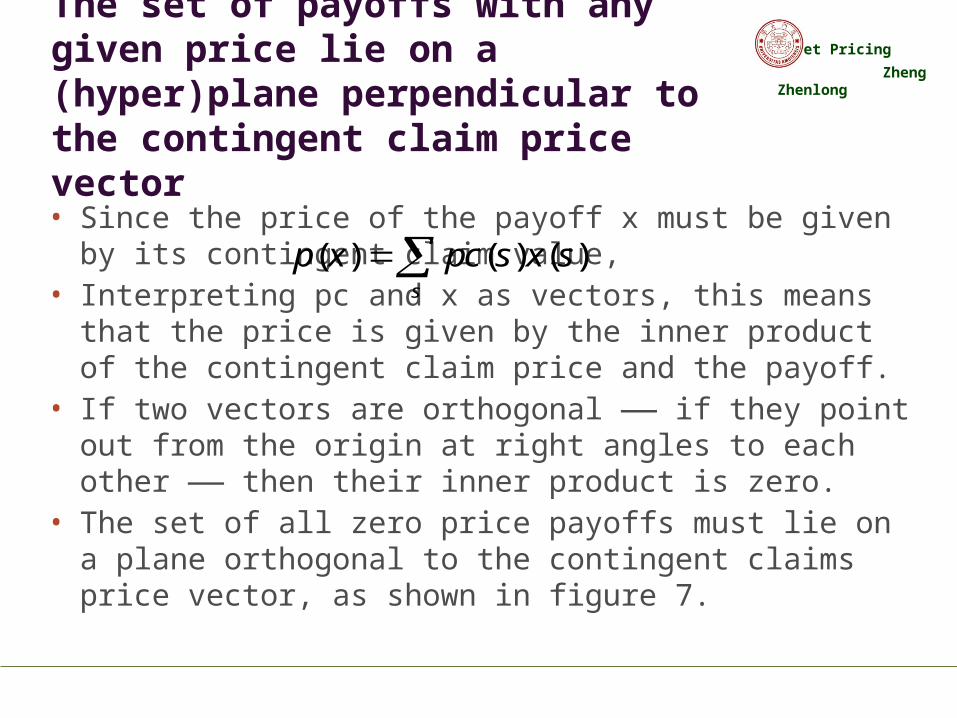

The set of payoffs with any given price lie on a (hyper)plane perpendicular to the contingent claim price vector

• Since the price of the payoff x must be given by its contingent claim value,

• Interpreting pc and x as vectors, this means that the price is given by the inner product of the contingent claim price and the payoff.

• If two vectors are orthogonal —— if they point out from the origin at right angles to each other —— then their inner product is zero.

• The set of all zero price payoffs must lie on a plane orthogonal to the contingent claims price vector, as shown in figure 7.

( ) ( ) ( )s

p x pc s x s

Asset Pricing

Zheng Zhenlong

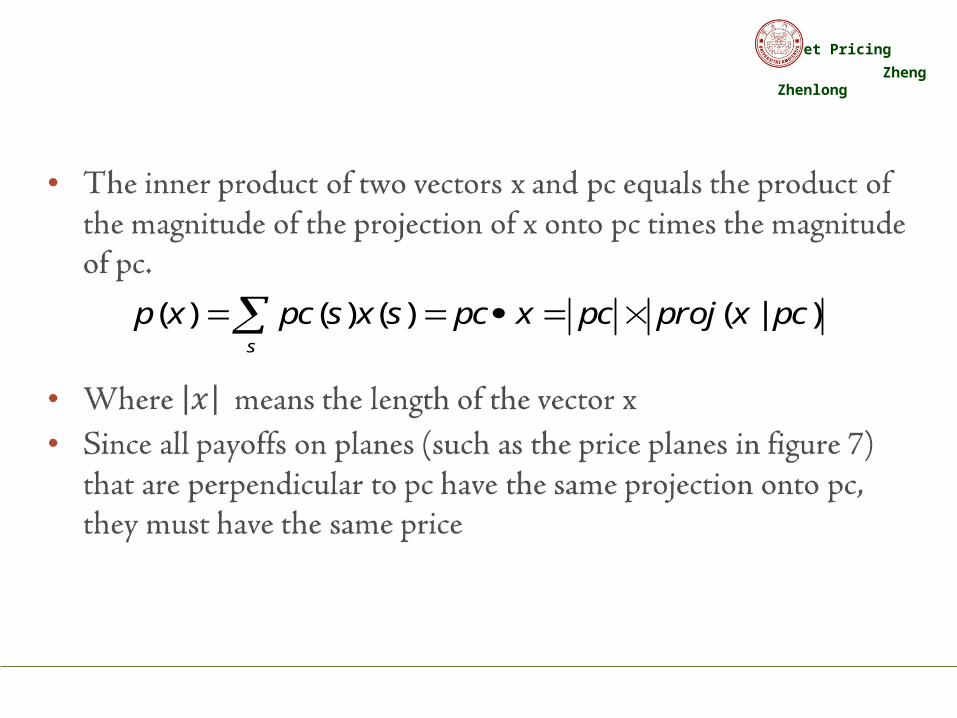

( ) ( ) ( ) ( | )s

p x pc s x s pc x pc proj x pc

Asset Pricing

Zheng Zhenlong

Asset Pricing

Zheng Zhenlong

• Planes of constant price move out linearly, and the origin x= 0 must have a price of zero.

• If payoff y= 2x, then its price is twice the price of x

( ) ( ) ( ) ( )2 ( ) 2 ( )s s

p y pc s y s pc s x s p x

Asset Pricing

Zheng Zhenlong

( ) ( ) ( )p ax by ap x bp y

Asset Pricing

Zheng Zhenlong

Asset Pricing

Zheng Zhenlong