Asset & Debt Division in Divorce

22

Division of Property & Debts RETURN TO “ALL ABOUT” SERIES SLIDE Scott Baroway Mediation Partners 720-889-2808 Baroway@gmail. com

Transcript of Asset & Debt Division in Divorce

Division of Property & Debts

RETURN TO “ALL ABOUT” SERIES SLIDE

Scott Baroway Mediation Partners [email protected]

DISCLAIMER

2

No legal advice is given in this website. Nothing said in this website shall in anyway constitutes legal advice. Nothing on this or associated pages, documents, comments, answers, emails, or other communications should be taken as legal advice for any individual case or situation. All information presented is for informative purposes only and should not be considered legal advice in any way. Additionally, no attorney-client relationship is established by viewing any information on this website. If you believe you are here to get legal advice in any way, you should leave now. THIS WEBSITE IS FOR GENERAL INFORMATION PURPOSES ONLY.

No Warranties or Guaranties are made regarding accuracy of the information provided.

Equitable Distribution Defined

3

The division of marital property, “without regard to marital misconduct, in such proportions as the court deems just and equitable after considering all relevant factors...”

May consider economic fault in very limited circumstances

Colorado not a community property stateDivision is not necessarily 50-50 or equal“Dual Property” Equitable Distribution State

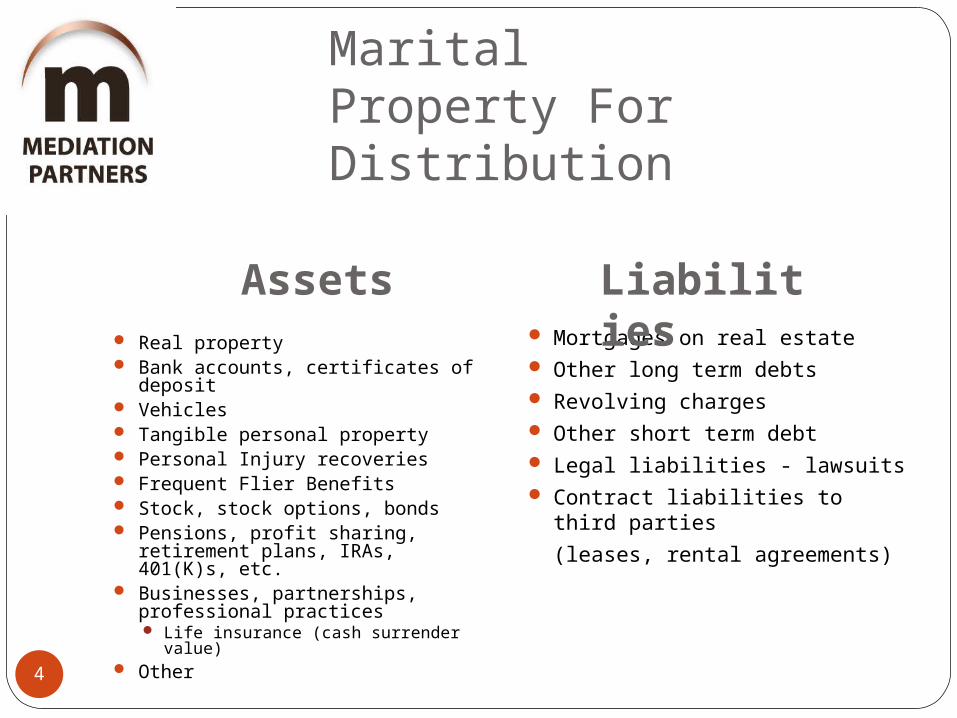

Marital Property For Distribution

4

Real property Bank accounts, certificates of

deposit Vehicles Tangible personal property Personal Injury recoveries Frequent Flier Benefits Stock, stock options, bonds Pensions, profit sharing,

retirement plans, IRAs, 401(K)s, etc.

Businesses, partnerships, professional practices Life insurance (cash surrender

value) Other

Mortgages on real estate Other long term debts Revolving charges Other short term debt Legal liabilities - lawsuits Contract liabilities to third

parties

(leases, rental agreements)

Assets Liabilities

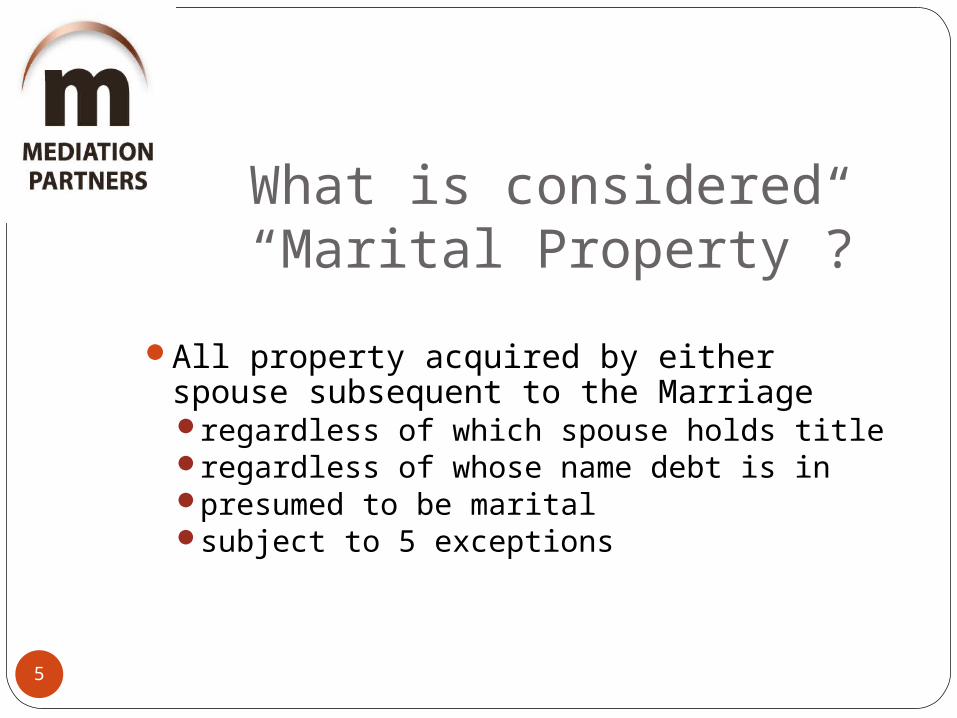

What is considered “Marital Property”?

5

All property acquired by either spouse subsequent to the Marriageregardless of which spouse holds titleregardless of whose name debt is inpresumed to be maritalsubject to 5 exceptions

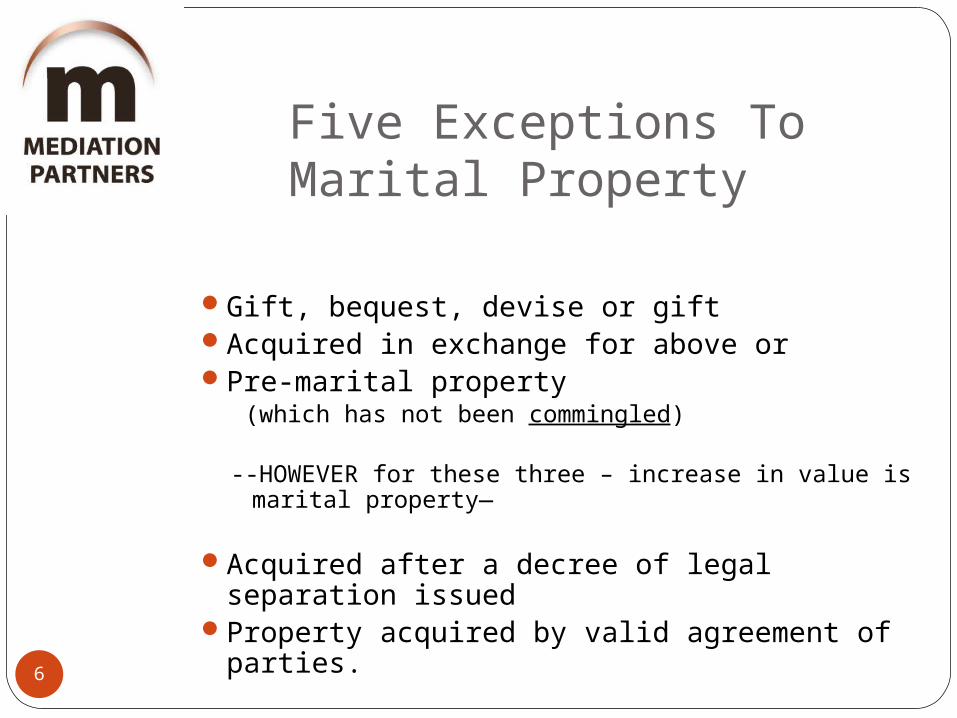

Five Exceptions To Marital Property

6

Gift, bequest, devise or giftAcquired in exchange for above or Pre-marital property

(which has not been commingled)

--HOWEVER for these three – increase in value is marital property—

Acquired after a decree of legal separation issued

Property acquired by valid agreement of parties.

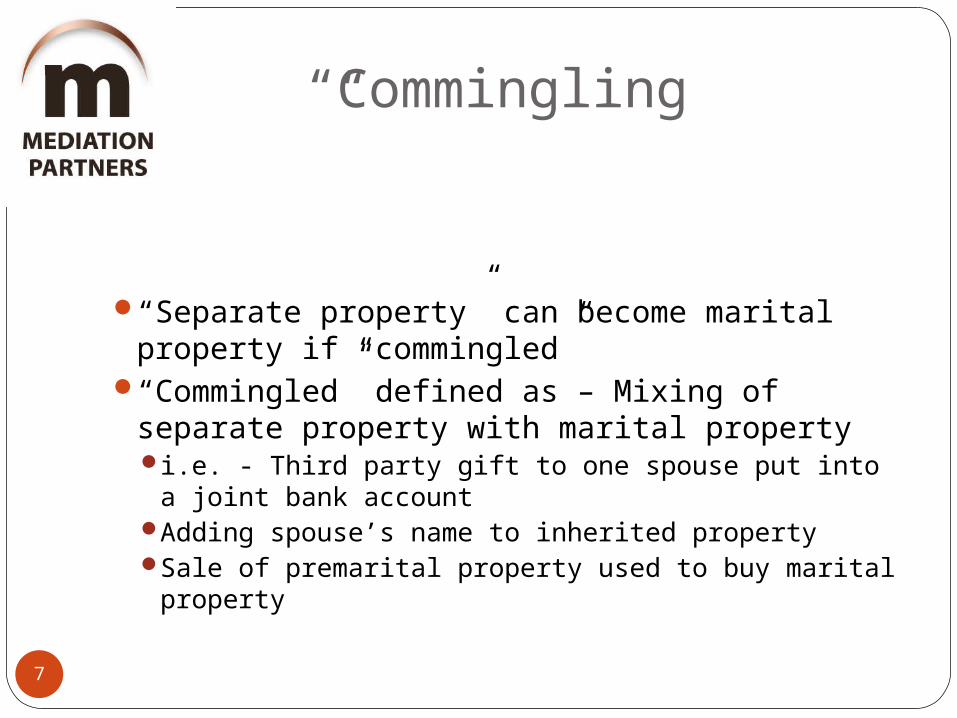

“Commingling”

7

“Separate property” can become marital property if “commingled”

“Commingled” defined as – Mixing of separate property with marital propertyi.e. - Third party gift to one spouse put into a joint

bank accountAdding spouse’s name to inherited propertySale of premarital property used to buy marital

property

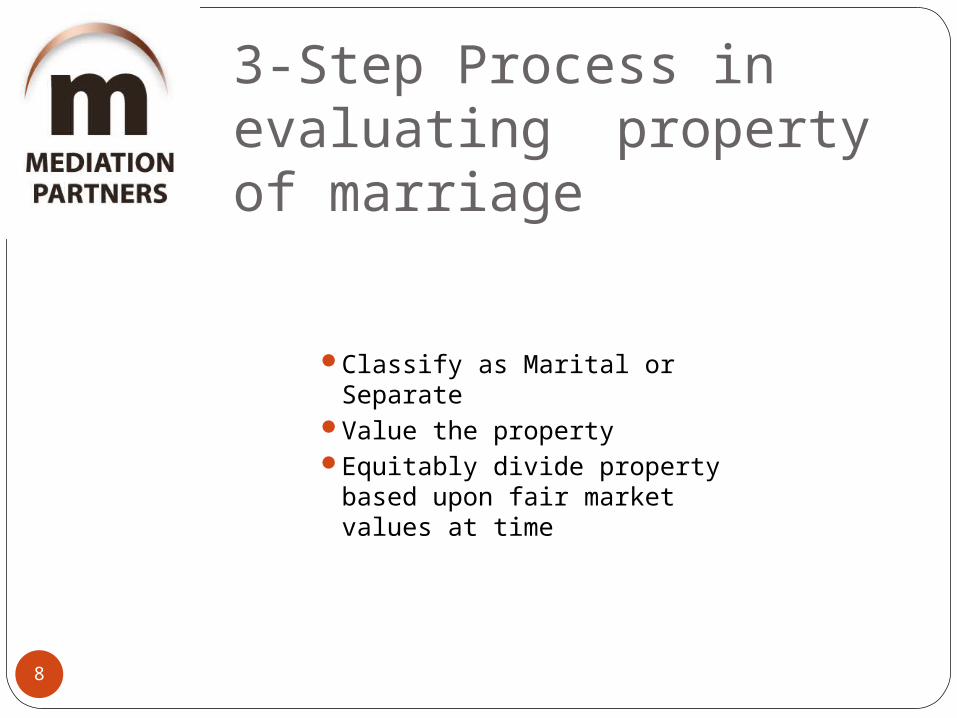

3-Step Process in evaluating property of marriage

8

Classify as Marital or SeparateValue the propertyEquitably divide property

based upon fair market values at time

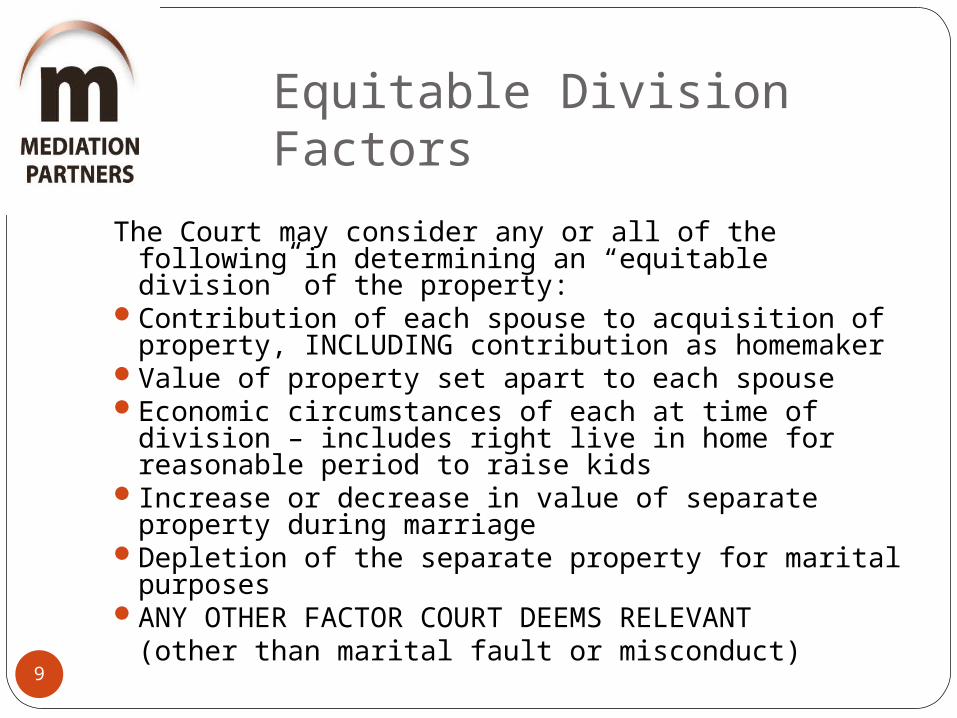

Equitable Division Factors

9

The Court may consider any or all of the following in determining an “equitable division” of the property:

Contribution of each spouse to acquisition of property, INCLUDING contribution as homemaker

Value of property set apart to each spouseEconomic circumstances of each at time of division

– includes right live in home for reasonable period to raise kids

Increase or decrease in value of separate property during marriage

Depletion of the separate property for marital purposes

ANY OTHER FACTOR COURT DEEMS RELEVANT(other than marital fault or misconduct)

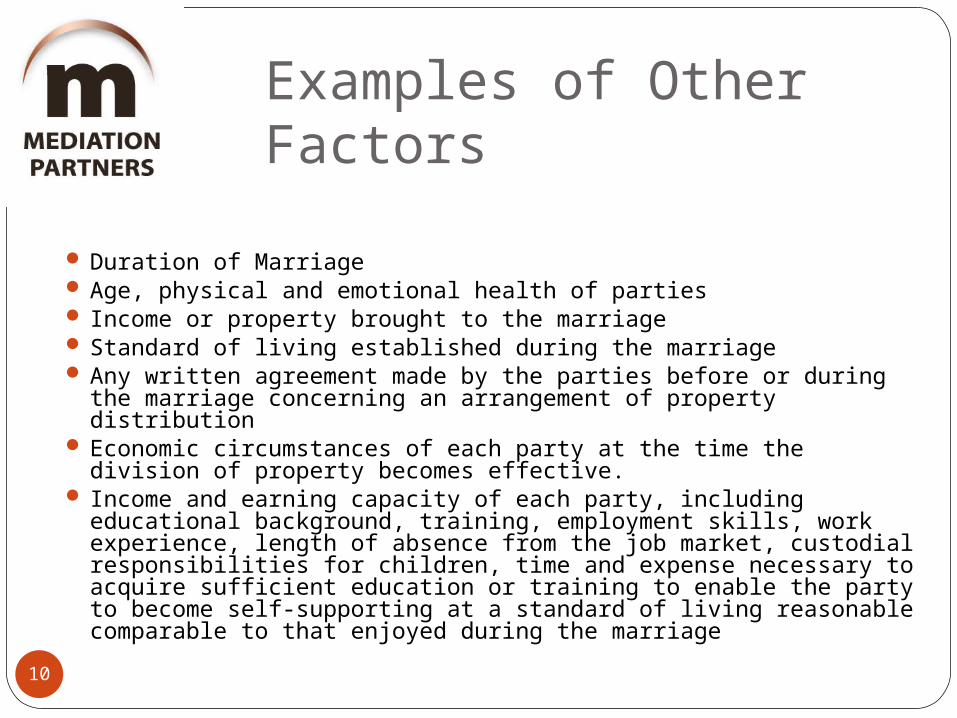

Examples of Other Factors

10

Duration of Marriage Age, physical and emotional health of parties Income or property brought to the marriage Standard of living established during the marriage Any written agreement made by the parties before or during the

marriage concerning an arrangement of property distribution Economic circumstances of each party at the time the division of

property becomes effective. Income and earning capacity of each party, including educational

background, training, employment skills, work experience, length of absence from the job market, custodial responsibilities for children, time and expense necessary to acquire sufficient education or training to enable the party to become self-supporting at a standard of living reasonable comparable to that enjoyed during the marriage

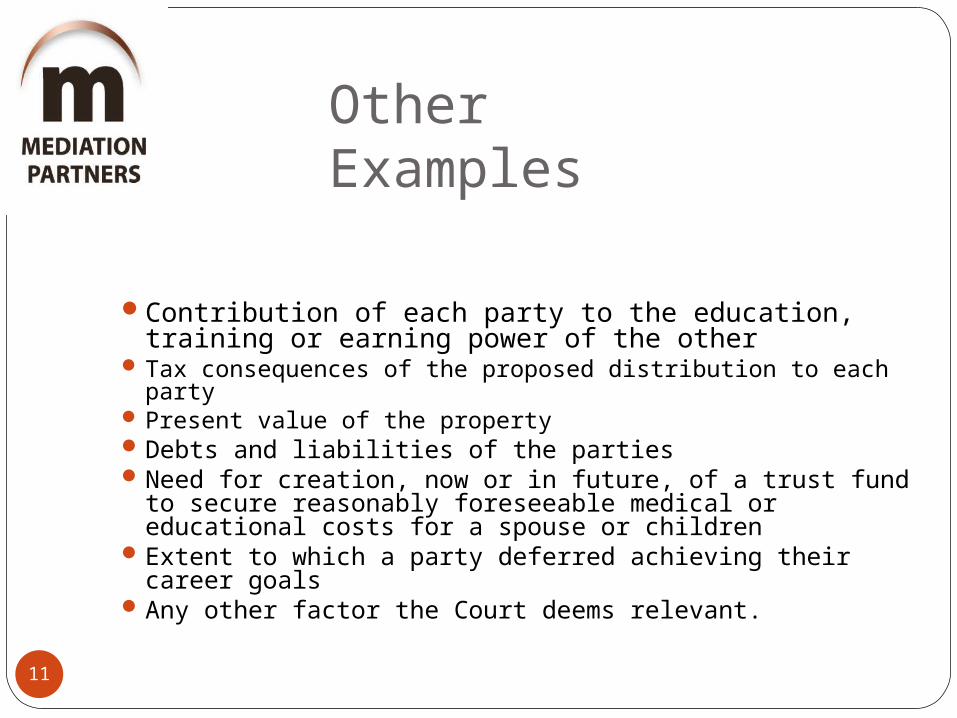

Other Examples

11

Contribution of each party to the education, training or earning power of the other

Tax consequences of the proposed distribution to each party Present value of the propertyDebts and liabilities of the partiesNeed for creation, now or in future, of a trust fund to

secure reasonably foreseeable medical or educational costs for a spouse or children

Extent to which a party deferred achieving their career goals

Any other factor the Court deems relevant.

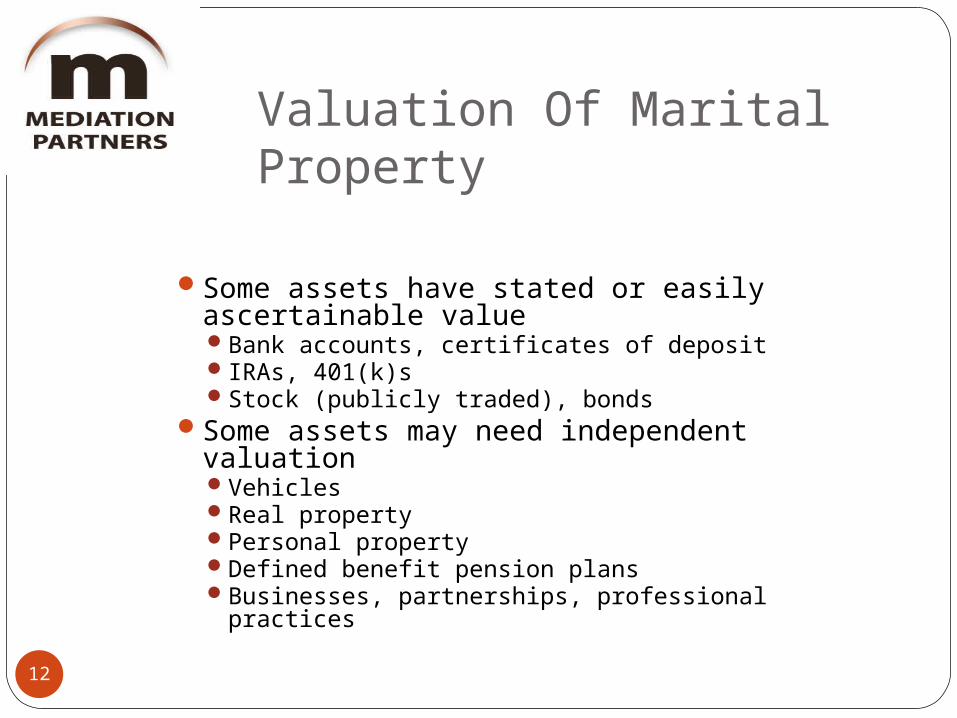

Valuation Of Marital Property

12

Some assets have stated or easily ascertainable valueBank accounts, certificates of depositIRAs, 401(k)sStock (publicly traded), bonds

Some assets may need independent valuationVehicles Real propertyPersonal propertyDefined benefit pension plansBusinesses, partnerships, professional practices

Valuation Methods

13

Publicly available informationVehicles – NADA Used Car book, Internet

sourcesSales of comparable real estate in your

neighborhoodUse of neutral expertsReal estate appraisersBusiness valuation expertsPension appraisers

OR MEDIATED AGREEMENT OF THE PARTIES

Marital Home

14

Colorado recognizes “desirability of awarding the family home or right to live therein for a reasonable period of time to the spouse with whom any children reside the majority of the time.”

However, may be cost prohibitive Spouse not awarded house my be obligated to pay

or assist in paying mortgage and delay equity cash value until future date.

Spouse in home – forced to reduce standard of living to keep home

OptionsSell homeKeep home

Offset against other assets or obligationsBuy-out over timeDeferred sale and deferred distribution of

equityFirst $250,000 of gain per spouse/former

spouse from sale of primary residence is tax exempt provided home used as primary residence 2 out of last 5 years

Stock Options Can Be Marital Property

15

Possible scenariosOptions acquired and vested during marriage Options acquired but not vested during

marriageOptions for past performanceOptions for future performance

Options acquired after marriage but granted for performance during marriage

Social Security Benefits

16

Not marital property subject to distributionCan be considered as an offset against other

marital assetsProtected from most creditors

Exception for payment of child support or alimonyYou’re entitled to your own benefits and may be

entitled to benefits as a former spouse if - Married for at least 10 years and divorced

for 2 yearsBoth parties at least 62 years old Not married when you apply for benefitsNot receiving Social Security spousal or survival benefits

based on someone else’s employment historyNeed to talk to specialist on this subject as law changes

Pensions Often Marital Property

17

Retirement benefits earned during marriagedeferred compensation for past employment

Marital propertypart earned from employment during the

marriage, ANDincreased value during marriageMilitary pension benefits earned during marriage

subject to special division rules

Pension Plan Valuation

18

Defined contribution plansvalue easy to determine comprised of the spouse’s contributions

plus those of the employerDefined benefit plans

value more complex to determine value is defined by the plan and not the

employee’s contributions

Date Of Valuation

19

Date of permanent orders hearing or date of decree

Spouses can agree on different date(s)Increases/decreases due to market conditions

Usually realized by both parties at time of actual distribution or sale (Major Issue now with Economy)

Distributing Pension Benefits

20

Two methodsImmediate offset – determine present value of benefit

and offset against other assets being distributedDeferred distribution – non-pension spouse receives

benefits when pension spouse is eligible for his/her benefits

Qualified Domestic Relations Order (QDRO)Judicial device for distributing pension benefits

Specialized and need expert to prepareUsually an added cost to mediation of $350-$500 per

pension plan being divided.

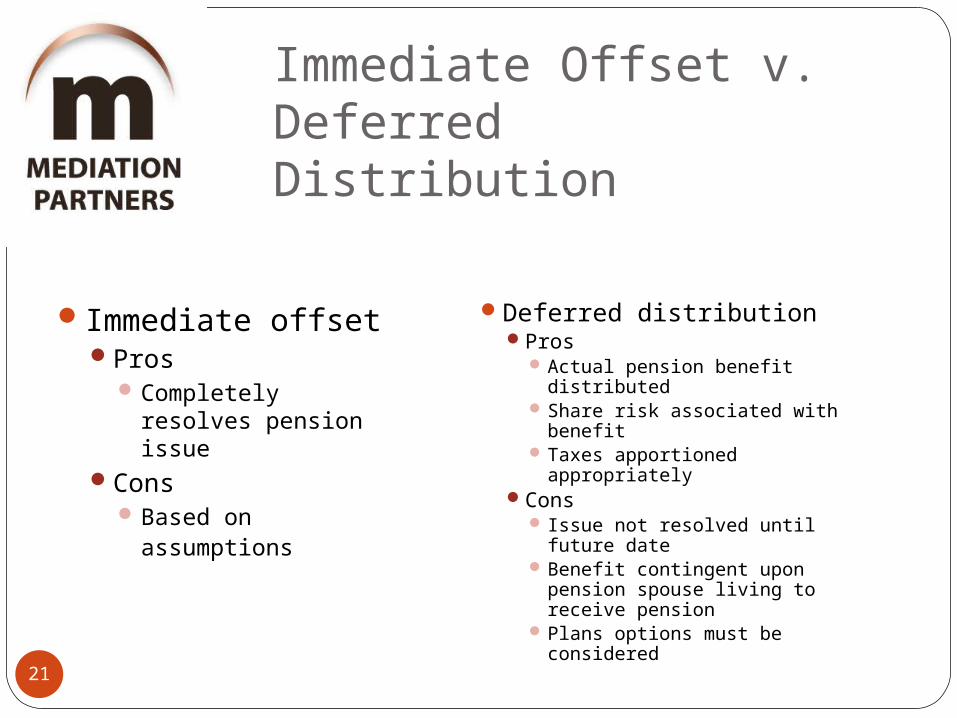

Immediate Offset v. Deferred Distribution

21

Immediate offsetPros

Completely resolves pension issue

ConsBased on

assumptions

Deferred distributionPros

Actual pension benefit distributed

Share risk associated with benefit

Taxes apportioned appropriately

Cons Issue not resolved until future

date Benefit contingent upon

pension spouse living to receive pension

Plans options must be considered

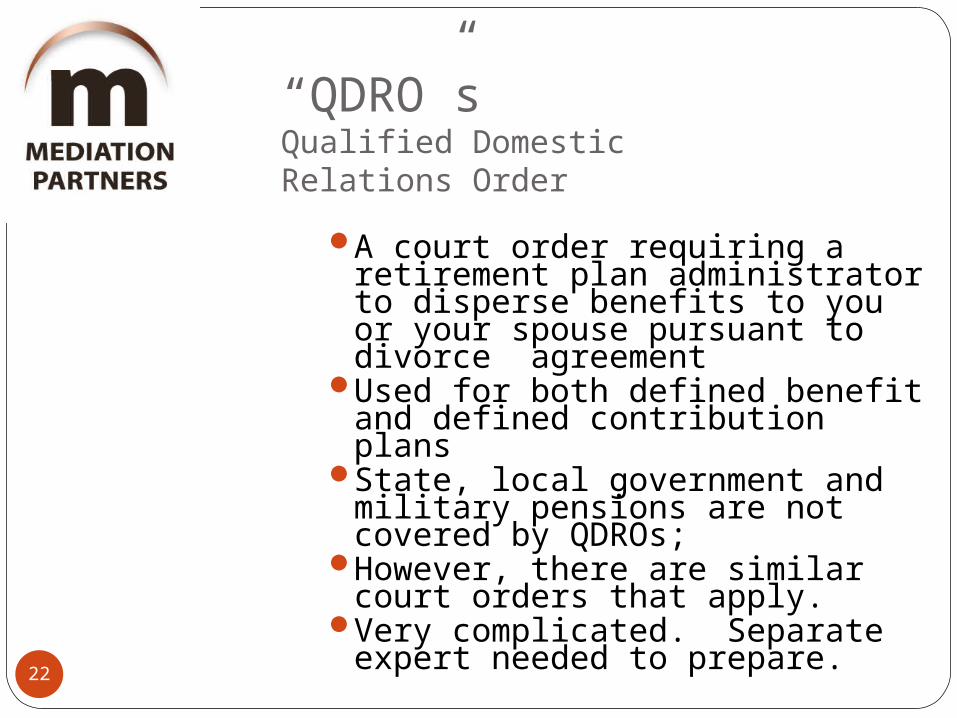

“QDRO”sQualified Domestic Relations Order

22

A court order requiring a retirement plan administrator to disperse benefits to you or your spouse pursuant to divorce agreement

Used for both defined benefit and defined contribution plans

State, local government and military pensions are not covered by QDROs;

However, there are similar court orders that apply.

Very complicated. Separate expert needed to prepare.