Asset Allocation

226

Asset Allocation Principles A Resource for Private Investors 2002–2003

-

Upload

gujingjing -

Category

Documents

-

view

166 -

download

2

Transcript of Asset Allocation

Asset Allocation PrinciplesA Resource for Private Investors

2002–2003

Letter to Investors

To our investing clients:

We are pleased to present the enclosed selection of Asset Allocation Principles, High Net Worth Investment Tools,Investment Philosophy Concepts, and summaries of Classic Investment Readings. These essays are excerpted from thetwenty-one previously published issues of Financial Management Review and Outlook, a joint publication of MorganStanley Investment Management; the Morgan Stanley Individual Investor Group, including Investor Advisory Services andPrivate Wealth Management; and Morgan Stanley Investment Research.

Academic studies have shown that approximately 75% to 91% of the variance in returns from investing activity derivesfrom the asset allocation decision. Asset allocation has been a core discipline and an area of firmwide focus since thefounding of Morgan Stanley Investment Management (MSIM) over 20 years ago. In recent years, we have extendedthis emphasis to the investment needs, goals, and specific circumstances of affluent and High Net Worth family groups,private foundations, closely-held corporations, and related private investors.

Throughout this publication, our aim is to provide analysis, tools, and concepts of value to sophisticated investorsfacing important asset allocation decisions.

We want to emphasize our commitment to providing excellent service, superior quality investment advice, andfinancial solutions that meet the needs of substantial private investors.

We greatly appreciate the feedback from, and dialogue with, our private investing clients that these writings haveengendered.

BARTON M. BIGGSCHAIRMAN

MORGAN STANLEYINVESTMENT MANAGEMENT

MITCHELL M. MERINPRESIDENT AND CHIEF OPERATING OFFICER

MORGAN STANLEYINVESTMENT MANAGEMENT

JOHN H. SCHAEFERPRESIDENT AND CHIEF OPERATING OFFICER

MORGAN STANLEYINDIVIDUAL INVESTOR GROUP

MAYREE C. CLARKGLOBAL DIRECTORMORGAN STANLEY

PRIVATE WEALTH MANAGEMENT

-

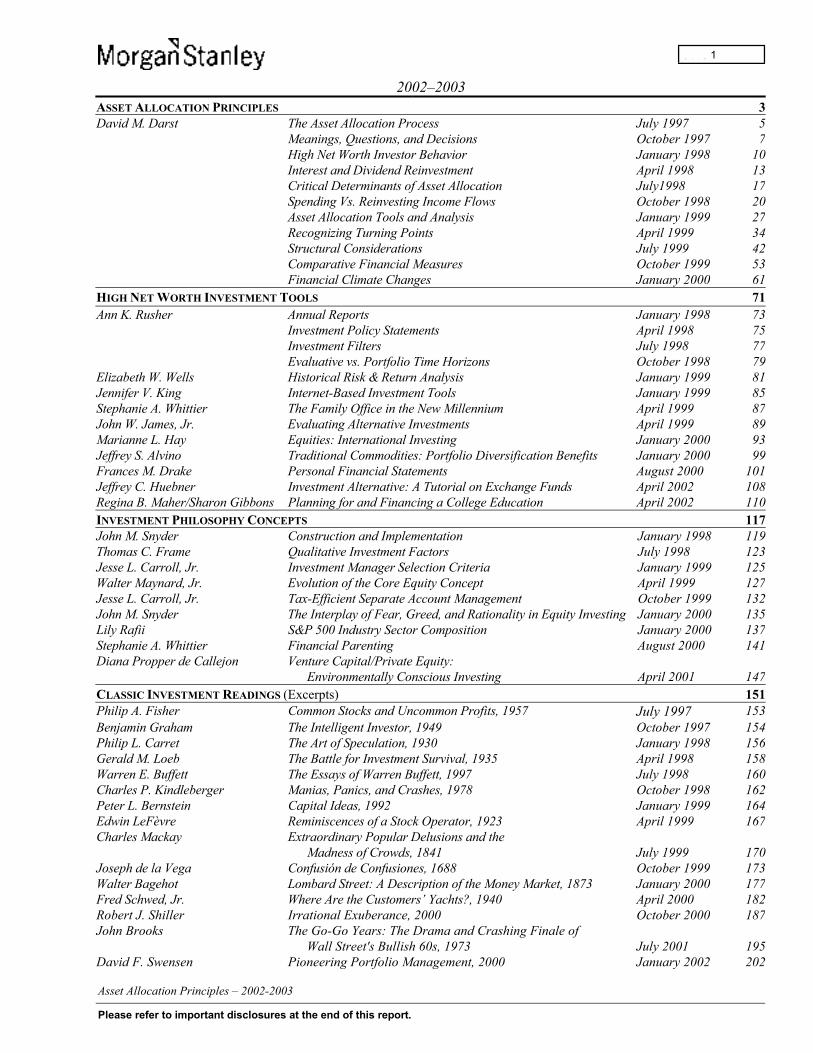

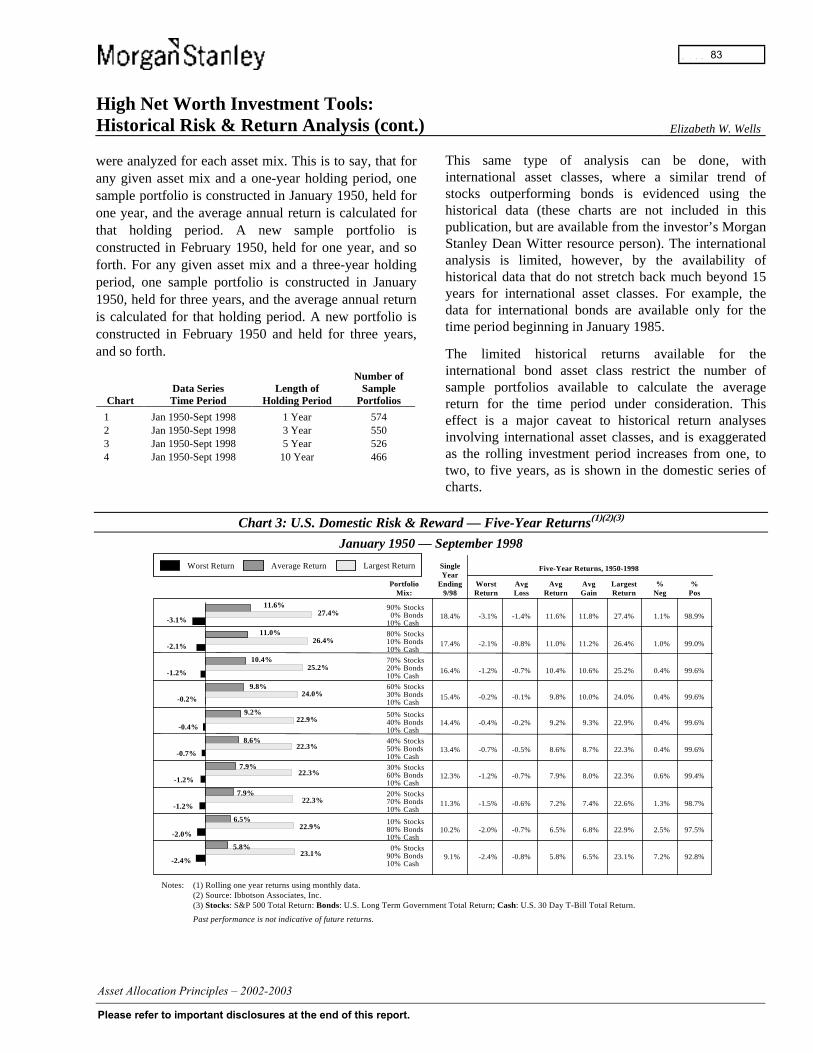

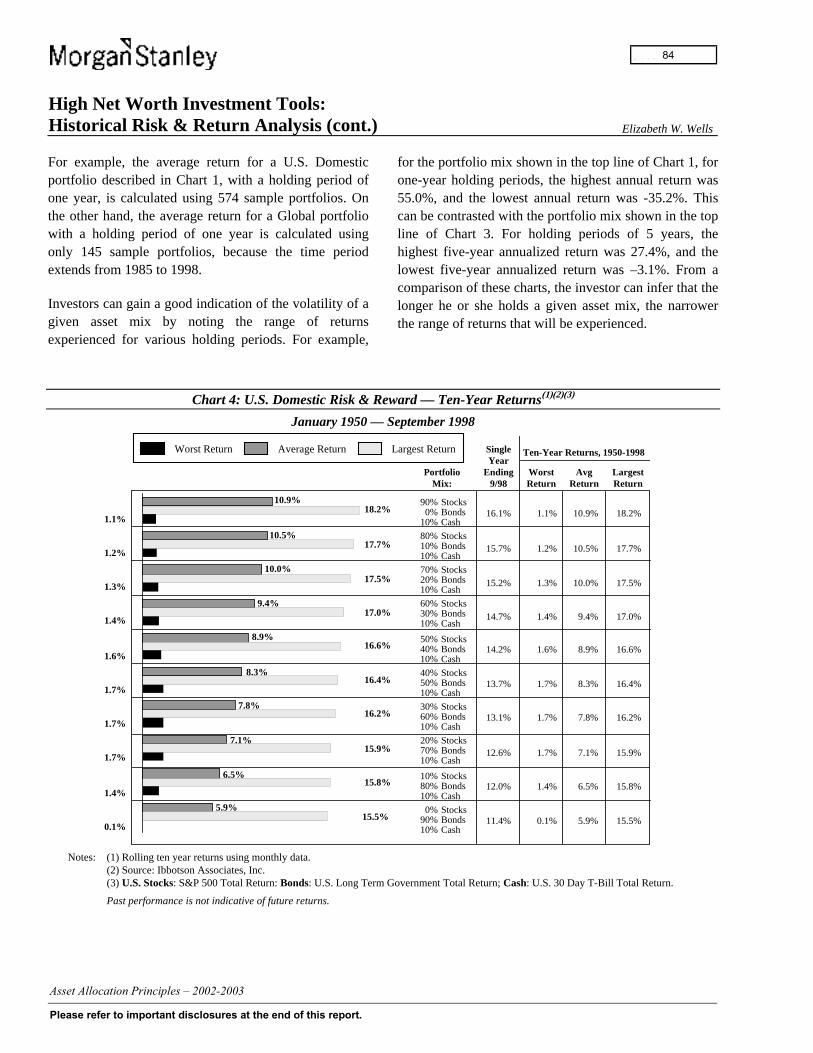

2002–2003ASSET ALLOCATION PRINCIPLES 3David M. Darst The Asset Allocation Process July 1997 5

Meanings, Questions, and Decisions October 1997 7High Net Worth Investor Behavior January 1998 10Interest and Dividend Reinvestment April 1998 13Critical Determinants of Asset Allocation July1998 17Spending Vs. Reinvesting Income Flows October 1998 20Asset Allocation Tools and Analysis January 1999 27Recognizing Turning Points April 1999 34Structural Considerations July 1999 42Comparative Financial Measures October 1999 53Financial Climate Changes January 2000 61

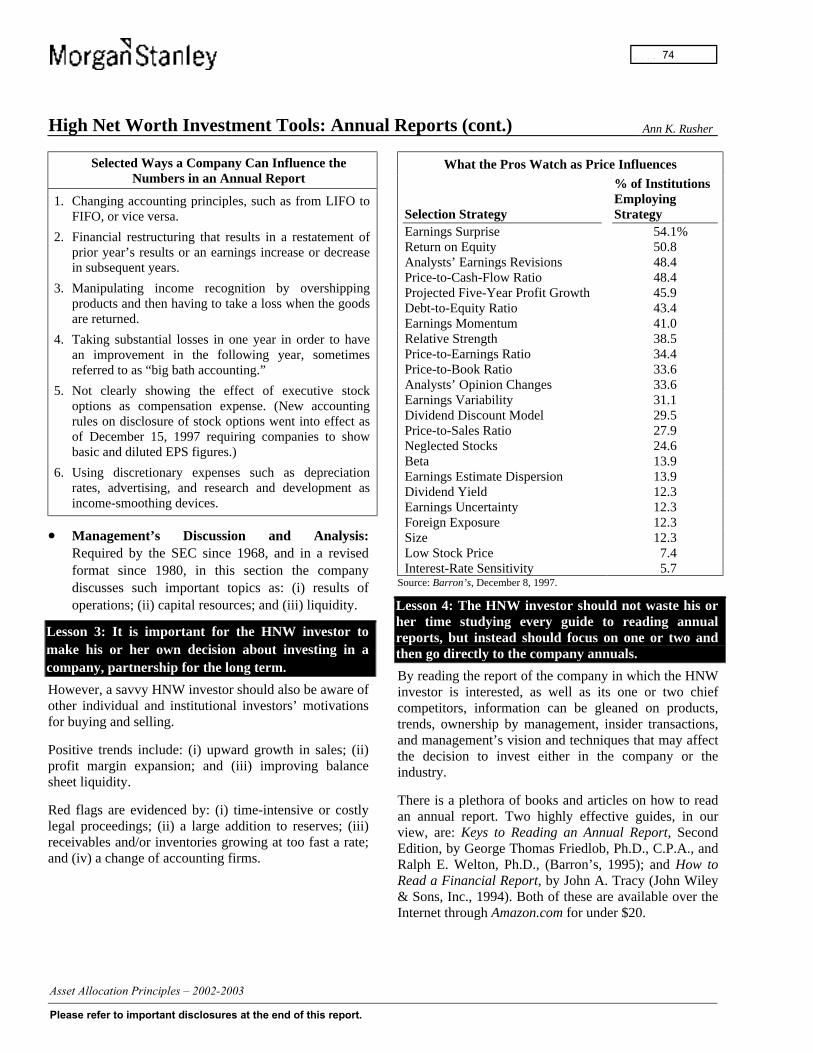

HIGH NET WORTH INVESTMENT TOOLS 71Ann K. Rusher Annual Reports January 1998 73

Investment Policy Statements April 1998 75Investment Filters July 1998 77Evaluative vs. Portfolio Time Horizons October 1998 79

Elizabeth W. Wells Historical Risk & Return Analysis January 1999 81Jennifer V. King Internet-Based Investment Tools January 1999 85Stephanie A. Whittier The Family Office in the New Millennium April 1999 87John W. James, Jr. Evaluating Alternative Investments April 1999 89Marianne L. Hay Equities: International Investing January 2000 93Jeffrey S. Alvino Traditional Commodities: Portfolio Diversification Benefits January 2000 99Frances M. Drake Personal Financial Statements August 2000 101Jeffrey C. Huebner Investment Alternative: A Tutorial on Exchange Funds April 2002 108Regina B. Maher/Sharon Gibbons Planning for and Financing a College Education April 2002 110INVESTMENT PHILOSOPHY CONCEPTS 117John M. Snyder Construction and Implementation January 1998 119Thomas C. Frame Qualitative Investment Factors July 1998 123Jesse L. Carroll, Jr. Investment Manager Selection Criteria January 1999 125Walter Maynard, Jr. Evolution of the Core Equity Concept April 1999 127Jesse L. Carroll, Jr. Tax-Efficient Separate Account Management October 1999 132John M. Snyder The Interplay of Fear, Greed, and Rationality in Equity Investing January 2000 135Lily Rafii S&P 500 Industry Sector Composition January 2000 137Stephanie A. Whittier Financial Parenting August 2000 141Diana Propper de Callejon Venture Capital/Private Equity:

Environmentally Conscious Investing April 2001 147CLASSIC INVESTMENT READINGS (Excerpts) 151Philip A. Fisher Common Stocks and Uncommon Profits, 1957 July 1997 153Benjamin Graham The Intelligent Investor, 1949 October 1997 154Philip L. Carret The Art of Speculation, 1930 January 1998 156Gerald M. Loeb The Battle for Investment Survival, 1935 April 1998 158Warren E. Buffett The Essays of Warren Buffett, 1997 July 1998 160Charles P. Kindleberger Manias, Panics, and Crashes, 1978 October 1998 162Peter L. Bernstein Capital Ideas, 1992 January 1999 164Edwin LeFèvre Reminiscences of a Stock Operator, 1923 April 1999 167Charles Mackay Extraordinary Popular Delusions and the

Madness of Crowds, 1841 July 1999 170Joseph de la Vega Confusión de Confusiones, 1688 October 1999 173Walter Bagehot Lombard Street: A Description of the Money Market, 1873 January 2000 177Fred Schwed, Jr. Where Are the Customers’ Yachts?, 1940 April 2000 182Robert J. Shiller Irrational Exuberance, 2000 October 2000 187John Brooks The Go-Go Years: The Drama and Crashing Finale of

Wall Street's Bullish 60s, 1973 July 2001 195David F. Swensen Pioneering Portfolio Management, 2000 January 2002 202

-

1

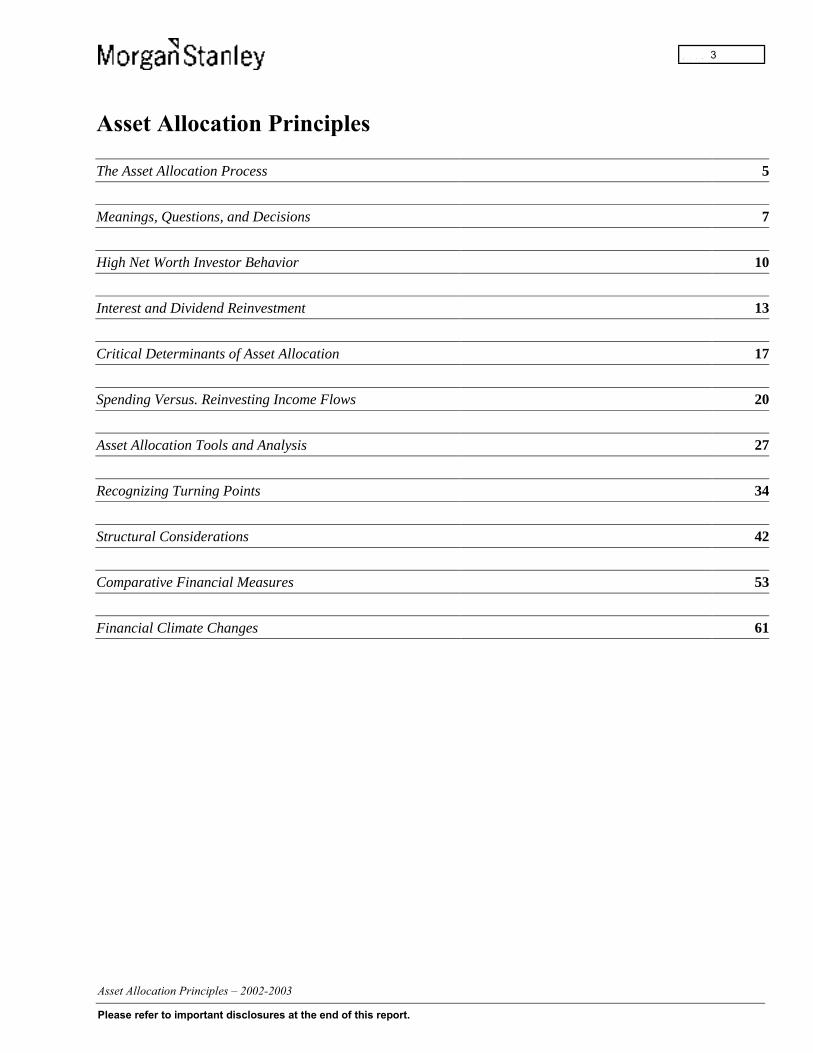

The Asset Allocation Process 5

Meanings, Questions, and Decisions 7

High Net Worth Investor Behavior 10

Interest and Dividend Reinvestment 13

Critical Determinants of Asset Allocation 17

Spending Versus. Reinvesting Income Flows 20

Asset Allocation Tools and Analysis 27

Recognizing Turning Points 34

Structural Considerations 42

Comparative Financial Measures 53

Financial Climate Changes 61

-

3

Asset Allocation Principles: The Asset Allocation Process David M. Darst

Asset allocation means different things to differentinvestor groups. For many institutional investors, assetallocation means: (i) calculating the rates of return from,standard deviations on, and correlations between, variousasset classes; (ii) running these variables through amean-variance optimization program to produce aselection of asset mixes having different risk-rewardprofiles; and (iii) analyzing and implementing someversion of the desired asset allocation in light of theinstitution’s goals, history, preferences, constraints, andother factors.

For High Net Worth private investors, asset allocationmay or may not include these formalized actions. In ourview, most important for private investors is the need topursue asset allocation with special attention to: (i) thetax status and after-tax implications of investments in agiven asset class; and (ii) the investor’s individualmotivations, personal circumstances, and cyclical andsecular market outlook.

Some, but by no means all, of the strategic issuesaffecting wealthy private investors’ asset allocationdecisions include: the timing and magnitude ofintergenerational income requirements; the ability tomeasure, withstand, and be adequately compensated forbearing risk or loss; absolute and relative performancegoals and benchmarks for measuring returns; theinfluence of one or more dominant investment positionsor significant non-tracked asset categories, such as art,

jewelry, or collectibles; and meaningful financialliabilities such as mortgage debt or margin borrowing.

After a thorough review of the High Net Worthinvestor’s financial profile and objectives, the assetallocation process can proceed in a multi-step process.First, assumptions need to be examined and then spelledout about future expected returns, risk, and thecorrelation of future returns between asset classes.Second, the investor and his or her advisor should selectthose asset classes which are appropriate in view of theinvestor’s profile and objectives and which have themaximum expected return for a given level of risk or,stated another way, the minimum risk for a given level ofreturn.

Next, the investor should establish a long-term assetallocation policy (the “Strategic Asset Allocation”)which reflects the optimal long-term benchmark aroundwhich future asset mixes might be expected to vary.Fourth, the investor should implement Tactical AssetAllocation decisions against the broad guidelines of theStrategic Asset Allocation. Fifth, the portfolio of assetsshould be periodically rebalanced, with sensitivity to thetax consequences of such rebalancing, to take account ofthe Strategic Asset Allocation framework. Last, theinvestor should review the Strategic Asset Allocationitself, from time to time, to ensure overallappropriateness given his or her circumstances, frame ofmind, the outlook for each of the respective asset classes,and the financial markets overall.

Quantitative and Qualitative Decision Framework

SpecifyAssumptions

Re: Asset Classes

ConductOngoingReview

SelectOptimum Asset

Classes

EstablishStrategic

Asset Allocation

ImplementTactical

Asset Allocation

RebalanceStrategic

Asset Allocation

-

5

Asset Allocation Principles: The Asset Allocation Process (cont.) David M. Darst

The history of wealthy individual investors’ focus onasset allocation can be divided into three broad phases.Traditionally, most U.S. private investors deployed theirportfolios according to overall perceived-wisdomguidelines reflecting the investment ethos of the age. Inthe 1930s, one version of these guidelines specified 60%in U.S. domestic bonds and 40% in U.S. stocks. A morerecent version of this standard asset mix, which prevailedfor quite some time, recommended 60% in stocks, 30%in bonds, and 10% in cash.

Beginning in the mid- to late 1980s, inspired by theactivities of certain institutional investors, a smallerproportion of wealthy individuals and family groupsbegan to shift some of their assets into venture capital,real estate, LBOs, oil and gas investments, andinternational and emerging markets equity and debt.

The third phase of private investors’ evolution in assetallocation has included exposure, generally throughfunds or managed accounts, to a variety of sophisticatedinvestment strategies known as market-neutral orabsolute-return strategies. In the equity realm, thesestrategies include warrant and convertible arbitrage,hedged closed-end fund and cross ownership arbitrage,synthetic security arbitrage, and other techniquesinvolving derivative instruments. In the fixed incomeworld, these strategies include futures, swaparrangements, credit risk and yield curve shapemispricings, and embedded and explicit optionstechniques.

It is important for individual investors to recognize thedistinctions among, and the valuation dynamicsunderlying, the three major super categories of assets, onwhich Robert J. Greer elaborated in a Winter 1997Journal of Portfolio Management article. The first assetgrouping consists of Capital Assets, such as equities andfixed income securities. Valuations of these assets aredetermined by the capitalization of cash flows fromprojected dividend, interest, and terminal valuepayments. The values of the second asset grouping,Consumable or Tradable Assets, such as oil, grains, andother commodities, are determined by the classical forcesof supply and demand. The valuations for the third assetgrouping, Store of Value Assets, such as art orcurrencies, are a function of what someone is willing topay for them. Some assets, such as real estate or gold, fitinto more than one of these groupings. Being aware ofthe distinctions between the value drivers in each assetgrouping, and the occasional tendency for markets tomisclassify assets (for example, treating stocks asConsumable Assets, or as Store of Value Assets) canhelp private investors in establishing a Strategic AssetAllocation framework, in implementing tactical assetallocation decisions, and even in selecting specificinvestments.

For further insights on the importance and mechanics of asset allocation,investors are referred to The Asset Allocation Process, by Barton M. Biggs,dated October 17, 1996.

-

6

Asset Allocation Principles: Meanings, Questions, and Decisions David M. Darst

For the tax-sensitive private investor, asset allocation hasseveral deeper meanings beyond the mathematicaloptimization of returns, standard deviations, andcorrelations. Very importantly, asset allocation is about(1) blending the underlying characteristics of a selectedset of asset classes to produce, in effect, a financial alloypossessing a more favorable risk/reward profile than anyof its component elements. Further, asset allocation isabout (2) recognizing and balancing trade-offs, chiefamong them being time horizon, protection goals, andexpected sources of return.

Asset allocation is also about (3) setting minimumand maximum percentages to ensure sufficientrepresentation, but not overconcentration, of investmentalternatives. Finally, asset allocation is centrally about(4) diversification, with the objective of aligning theexpected risk profile of the investor’s portfolio with hisor her own risk profile. Rather than attempting to timethe market in a limited number of asset classes, assetallocation seeks, through diversification, to providehigher returns with lower risk over a sufficiently longtime frame and appropriately compensate the investor forbearing nondiversifiable volatility.

Private investors face several critical questions anddecisions in the process of asset allocation. Theseinclude: (i) the ultimate length of the time horizon for theportfolio as a whole; (ii) the degree of volatility or valueimpairment the investor can withstand, in the aggregateand for specific investment categories; (iii) the desiredextent of principal protection versus purchasing powerprotection; (iv) the role and amount of core and non-coreasset classes; (v) the degree of patience and convictionthat can be maintained in the face of overall portfoliounderperformance relative to the performance of one ortwo asset classes; and, not to be minimized, (vi) theinvestor’s confidence level in the specific return, risk,and correlation projections on which asset allocationdecisions are based.

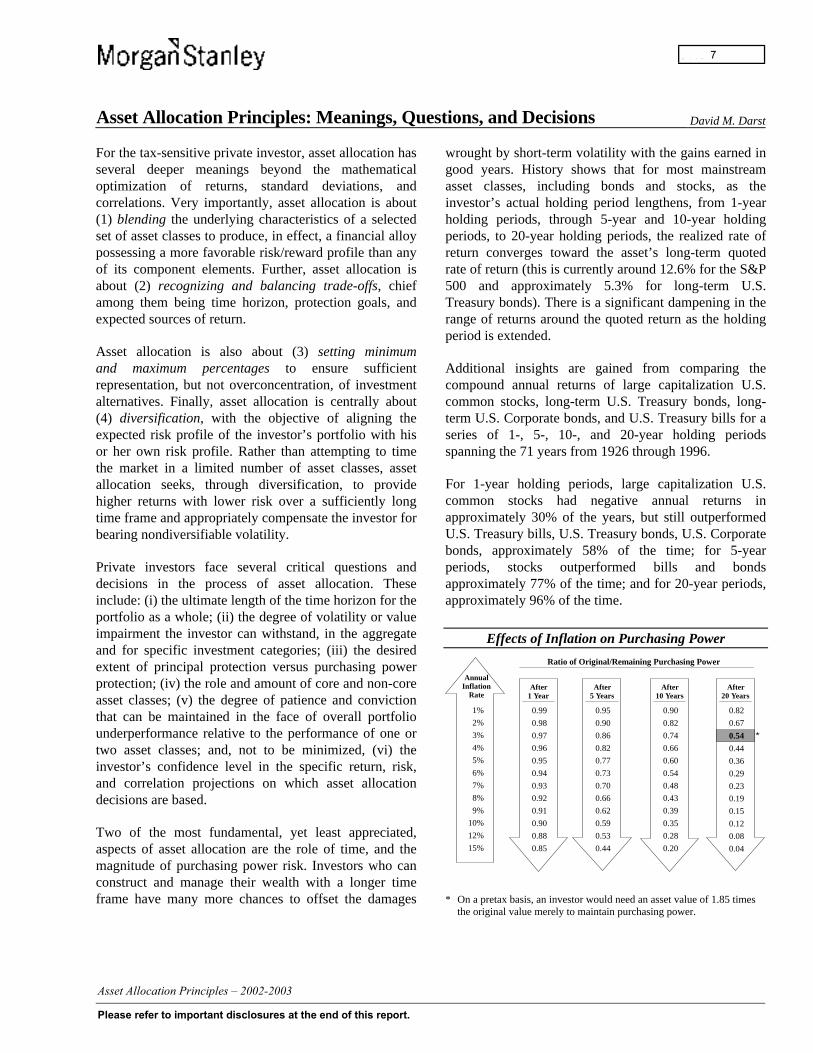

Two of the most fundamental, yet least appreciated,aspects of asset allocation are the role of time, and themagnitude of purchasing power risk. Investors who canconstruct and manage their wealth with a longer timeframe have many more chances to offset the damages

wrought by short-term volatility with the gains earned ingood years. History shows that for most mainstreamasset classes, including bonds and stocks, as theinvestor’s actual holding period lengthens, from 1-yearholding periods, through 5-year and 10-year holdingperiods, to 20-year holding periods, the realized rate ofreturn converges toward the asset’s long-term quotedrate of return (this is currently around 12.6% for the S&P500 and approximately 5.3% for long-term U.S.Treasury bonds). There is a significant dampening in therange of returns around the quoted return as the holdingperiod is extended.

Additional insights are gained from comparing thecompound annual returns of large capitalization U.S.common stocks, long-term U.S. Treasury bonds, long-term U.S. Corporate bonds, and U.S. Treasury bills for aseries of 1-, 5-, 10-, and 20-year holding periodsspanning the 71 years from 1926 through 1996.

For 1-year holding periods, large capitalization U.S.common stocks had negative annual returns inapproximately 30% of the years, but still outperformedU.S. Treasury bills, U.S. Treasury bonds, U.S. Corporatebonds, approximately 58% of the time; for 5-yearperiods, stocks outperformed bills and bondsapproximately 77% of the time; and for 20-year periods,approximately 96% of the time.

Effects of Inflation on Purchasing Power

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

12%

15%

AnnualInflation

Rate

0.99

0.98

0.97

0.96

0.95

0.94

0.93

0.92

0.91

0.90

0.88

0.85

After1 Year

0.95

0.90

0.86

0.82

0.77

0.73

0.70

0.66

0.62

0.59

0.53

0.44

After5 Years

0.90

0.82

0.74

0.66

0.60

0.54

0.48

0.43

0.39

0.35

0.28

0.20

After10 Years

After20 Years

Ratio of Original/Remaining Purchasing Power

0.82

0.67

0.54

0.44

0.36

0.29

0.23

0.19

0.15

0.12

0.08

0.04

*

* On a pretax basis, an investor would need an asset value of 1.85 timesthe original value merely to maintain purchasing power.

-

7

Asset Allocation Principles: Meanings, Questions, and Decisions (cont.) David M. Darst

Furthermore, the miracle of compound interest dependson the passage of time. For instance, of the increase inthe value of a 10%-compounding portfolio held for 20years, 11% of the total gain occurs in the first five years,17% in the second five years, 28% in the third five years,and fully 46% occurs in the final five years. Even atrelatively modest annual rates of inflation, over a 20-yeartime period, the effective loss in an investment’spurchasing power can be debilitating. As shown in thechart above, at an annual inflation rate of 3%, after 20years, the investor has lost 46% (1.00 minus 0.54) of hisor her original purchasing power on an investmentwhose principal value remains unchanged. Under such ascenario, the investor would need an asset value of 1.85times its original value merely to maintain purchasingpower. If taxes had to be paid, the required growthwould be even larger.

While there is no assurance that the annual inflation ratewill always average out to be a certain positive levelover long stretches of time, based on the experience ofthe modern era, purchasing power erosion has in the pastbeen a fact of life and is a significant risk that theinvestor should address squarely and prepare for.

For long-term investors, purchasing power risk is at leastas important, if not more so, as multi-period market pricevolatility risk. For short-term investors who do not havethe opportunity for good and bad years of investmentperformance to offset one another, market price volatilityrisk is usually more important than purchasing powerrisk.

The implications of time duration and purchasing powerrisk for asset allocation thus generally lead to greateremphasis: (i) in longer-term portfolios, on equities andequity-like assets which have relatively higher returnsand higher volatility; and (ii) in shorter-term portfolios,on principal-protected, interest-generating assets thathave relatively lower returns and lower volatility. Theseasset allocation guidelines for private investors aresummarized below:

InvestorCharacteristic

Factors tendingto emphasizeprincipal-protected,interest generatingassets

Factors tending toemphasize equity-likeassets with projectedprincipal growth buthigher volatility

Expected TimeHorizon

Short Horizon Long Horizon

Income Needs High and/orPredictable Needs

Low and/orUnpredictable Needs

Desired PurchasingPower Protection

Low PurchasingPower Protection

High PurchasingPower Protection

VolatilityTolerance

Low VolatilityTolerance

High VolatilityTolerance

Private investors who have specific incomerequirements, but who can adopt a long-term investmenthorizon, may prefer to (1) spend small amounts ofprincipal from a higher total return portfolio to augmentlower levels of actual income return, rather than (2)constructing a lower total income return portfolio thathas higher levels of actual income return. This policy hasbeen followed by a number of leading universityendowments, many of whom have developed guidelinesto keep any spending of income plus small amounts ofprincipal well below their portfolios’ annual total return.

It is worth noting several caveats concerning historicaland projected return data. Historical single-point assetclass and security returns covering several years or moreare in fact averages of varying — sometimes, widelyvarying — results experienced in the years comprisingthe period cited.

Similarly, future returns do not possess the degree ofcertainty or accuracy implied by a single-pointprojection. A more telling rate of return descriptionshould incorporate a range of plus or minus returns, andtheir associated probability, around the single-point

-

8

Asset Allocation Principles: Meanings, Questions, and Decisions (cont.) David M. Darst

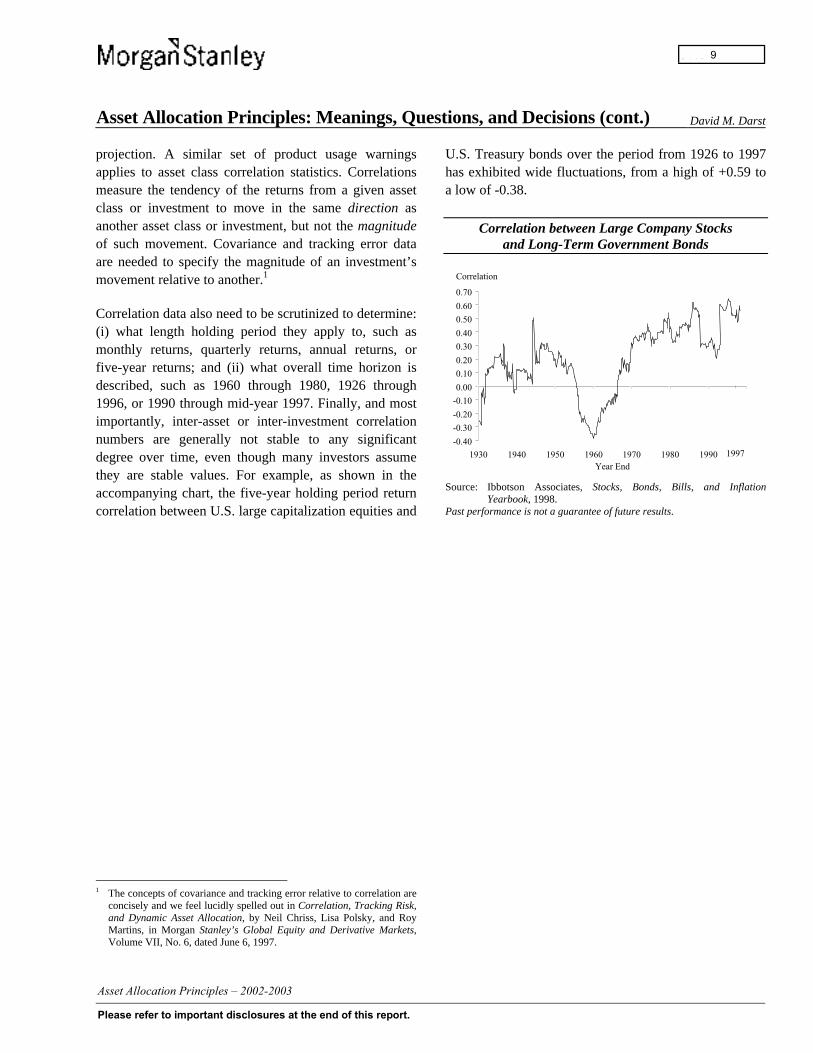

projection. A similar set of product usage warningsapplies to asset class correlation statistics. Correlationsmeasure the tendency of the returns from a given assetclass or investment to move in the same direction asanother asset class or investment, but not the magnitudeof such movement. Covariance and tracking error dataare needed to specify the magnitude of an investment’smovement relative to another.1

Correlation data also need to be scrutinized to determine:(i) what length holding period they apply to, such asmonthly returns, quarterly returns, annual returns, orfive-year returns; and (ii) what overall time horizon isdescribed, such as 1960 through 1980, 1926 through1996, or 1990 through mid-year 1997. Finally, and mostimportantly, inter-asset or inter-investment correlationnumbers are generally not stable to any significantdegree over time, even though many investors assumethey are stable values. For example, as shown in theaccompanying chart, the five-year holding period returncorrelation between U.S. large capitalization equities and

1 The concepts of covariance and tracking error relative to correlation are

concisely and we feel lucidly spelled out in Correlation, Tracking Risk,and Dynamic Asset Allocation, by Neil Chriss, Lisa Polsky, and RoyMartins, in Morgan Stanley’s Global Equity and Derivative Markets,Volume VII, No. 6, dated June 6, 1997.

U.S. Treasury bonds over the period from 1926 to 1997has exhibited wide fluctuations, from a high of +0.59 toa low of -0.38.

Correlation between Large Company Stocksand Long-Term Government Bonds

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

1930 1940 1950 1960 1970 1980 1990Year End

Correlation

1997

Source: Ibbotson Associates, Stocks, Bonds, Bills, and InflationYearbook, 1998.

Past performance is not a guarantee of future results.

-

9

Asset Allocation Principles: High Net Worth Investor Behavior David M. Darst

Asset allocation principles explore what it is about thenature, behavior, hopes, and fears of High Net Worth(HNW) investors that equips them well and/or poorly forthe crucial and challenging task of asset allocation.

Much has been made of the competitive disadvantage ofHNW investors in a global financial marketplacedominated by institutions. In the asset allocation process,it is commonly believed that institutional investors willoutperform HNW individuals due to institutions’superior access to investment research, corporatemanagements, trading media, quantitative tools, and, notleast, each other.

At the same time, High Net Worth private investorsappear to have several factors working in their favor.First, many HNW individuals are deeply grounded inknowledge of the business world — they know cycles ofcrops, of energy costs, of final-product prices; theyexperience companies as groups of people rather thanabstractions, as employees, suppliers, and customers; andthey possess an innate sense of corporate welfare andvalues, as a result of having to meet a payroll, expandmarket share, and maintain the viability of their ownenterprise.

Second, HNW investors are generally not answerable toartificial quarterly or annual demarcations of time, nor tothe dictates of committee-based thinking. If the privateinvestor so desires, he or she can withdraw from an assetclass altogether, or alternatively, ride through thevicissitudes of markets and leave valuable core long-term holdings undisturbed.

Third, individual investors are eminently capable —although not all HNW investors display these traits in theinvestment realm — of distance, objectivity, perspective,perception, independence, and clear thinking. Perhapsbecause it is their own funds that are at stake, HNWinvestors tend to experience the pain of losses moredeeply than they experience the pleasure of gains. Forsome, this can clarify; for others, this can cloud reason.

Fourth, HNW investors have essentially equal accesswith institutions to the great financial leveler: soundjudgment. In the asset allocation and investmentselection process, the characteristic that is most in shortsupply is not intelligence, data, or technology resources,it is judgment. Because individual investors andprofessional money managers may be gifted with, or

bereft of, good judgment, it is critical for the HNWinvestor to assess candidly whether or not he or she hasgood judgment; if not, an individual should not rest untila person possessed of good judgment can be found toprovide asset allocation advice.

A powerful testament to the force, effect, and success ofprivate individual investment was demonstrated in theworld of art on November 10, 1997, when the collectionof Victor and Sally Ganz was auctioned at Christie’s for$206.5 million. This total established the record for asingle-owner sale of art, surpassing the 1989 sale bySotheby’s of impressionist and modern paintingsbelonging to John Dorrance, Jr., for $123.4 million.

The Ganz couple’s holdings generated extraordinarilyhigh returns that are rare and difficult to achieve in anyasset class, but in the process, they left a legacy ofvaluable lessons for any serious investor. They (i) hadpassion and commitment to collecting art; (ii)concentrated and focused their efforts in a definedsphere; (iii) came to know their field of endeavor in greatdepth; (iv) bought with care, reflection, and analysis; and(v) exercised patience, letting time and longevity workfor them. Mr. Ganz’s first acquisition, Picasso’s Dream,was purchased in 1941 for $7,000 and sold at auction for$48.4 million. Over its 56-year holding period, thispainting generated a compound annual return of 17.1%before commissions and expenses,l an astoundingly highgrowth rate over such a long time frame. Anotherpainting by Picasso, Woman Seated in an Armchair(Eva), was bought in 1967 for $200,000 and auctioned30 years later for $24.7 million, producing an equallyuncommon and lofty compound annual return of 17.4%before commissions and expenses.1

In their asset allocation activity, HNW investors exhibitcertain behavior, often unwittingly, that can influence therealization of their investment goals. Since many of thesetraits derive from deep-seated human impulses, what isimportant in controlling and/or altering them is first and

1 After deduction of the auction house’s commission, which is 15% of the

first $50,000 and 10% of the remainder, the compound annual growthrate for Dream was 16.9%, and for Eva was 17.0%, before any annualexpenses for insurance and other carrying costs, which were notdisclosed.

-

10

Asset Allocation Principles: High Net Worth Investor Behavior (cont.) David M. Darst

foremost, the recognition of their potential existence. Anumber of these characteristics, some of which arecontradictory yet still encountered in the same investor,are set forth in the points below:

• Underestimate time horizons. Many privateinvestors specify a three- or five-year investmenttime horizon and invest with a short-termorientation, when in fact the investment time frameis 15 to 20 years or more.

• Attach too much significance to short-termresults. One key goal of asset allocation is todampen volatility and reduce risk through asset classdiversification. The benefits of such a program,which are usually purchased at the cost of loweroverall returns than the best-performing assetclasses, should be assessed over a sufficiently longperiod of time.

• Overemphasize volatility risk vs. purchasingpower risk. Particularly when the investor’s horizonextends to ten years or more, the erosion ofpurchasing power due to inflation can be significantin asset classes that maintain their nominal value.HNW investors need to address the risks of inflationvs. deflation and factor these considerations intotheir asset allocation strategy.

• Adopt a loss-averse mentality rather than a risk-averse mentality. Due to an antipathy toward losingmoney, many private investors will accept a“smooth” return of 10% (with low or no losses) overa series of market cycles, rather than a “bumpy”return of 15% (with occasional periods of testing,sometimes severe, in down years). After 15 years,

• the latter portfolio would be worth approximatelytwice the value of the former portfolio, but manyinvestors are not willing to stomach the volatility.

• Overestimate the ability to tolerate risk and/orilliquidity. In glaring contradiction to their loss-averse nature, a number of HNW investorscommonly forecast their loss-withstanding thresholdat a much higher level than the profound level ofdistress they feel when such losses — realized orunrealized — are actually experienced.

• Think in nominal terms rather than real terms.Assuming no change in interest rates and a 3%inflation rate, a private investor who placed $1million in tax-exempt bonds, and spent the interestincome each year, would have only $633,251 in realpurchasing power at the end of 15 years, eventhough the $1 million value remained whole innominal terms.

• Allow income needs to tilt the portfolio towarddividend/interest yield rather than total return.Wealth creation is a product of the compounding ofcapital over an appropriate time span; HNWinvestors with high current income needs shouldlook at the total return from an asset allocation mix,not merely the current yield level.

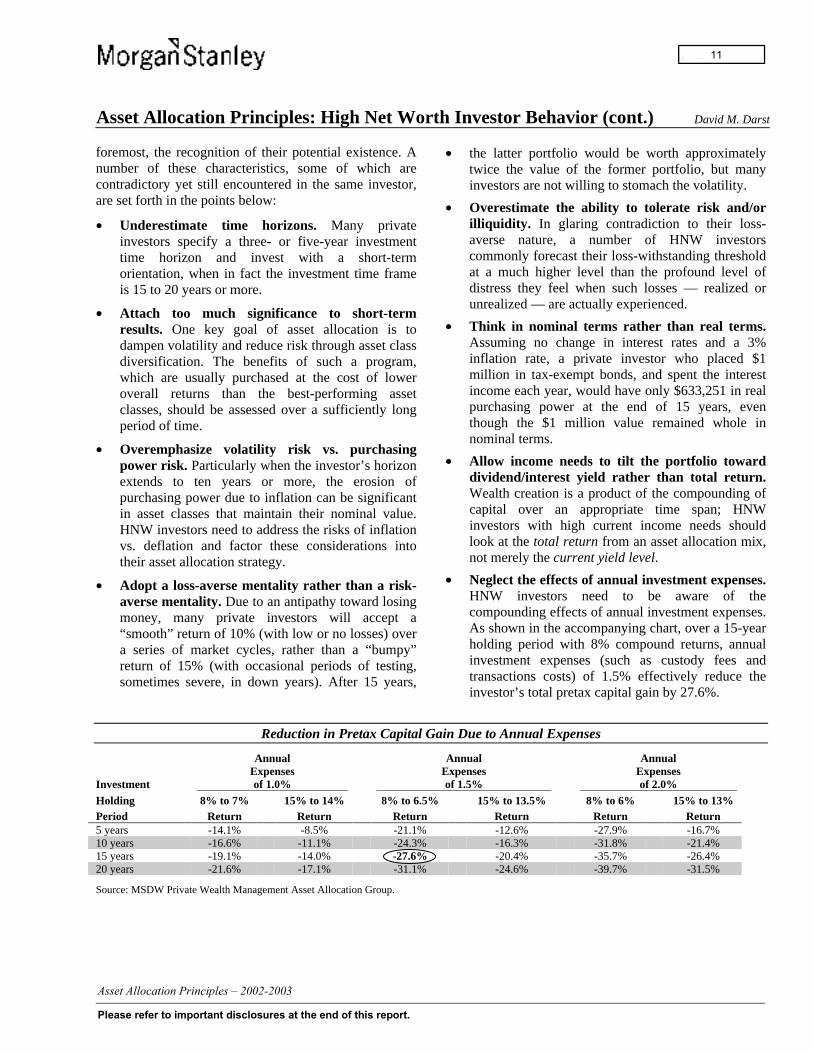

• Neglect the effects of annual investment expenses.HNW investors need to be aware of thecompounding effects of annual investment expenses.As shown in the accompanying chart, over a 15-yearholding period with 8% compound returns, annualinvestment expenses (such as custody fees andtransactions costs) of 1.5% effectively reduce theinvestor’s total pretax capital gain by 27.6%.

Reduction in Pretax Capital Gain Due to Annual Expenses

Investment

AnnualExpensesof 1.0%

AnnualExpensesof 1.5%

AnnualExpensesof 2.0%

Holding 8% to 7% 15% to 14% 8% to 6.5% 15% to 13.5% 8% to 6% 15% to 13%Period Return Return Return Return Return Return5 years -14.1% -8.5% -21.1% -12.6% -27.9% -16.7%10 years -16.6% -11.1% -24.3% -16.3% -31.8% -21.4%15 years -19.1% -14.0% -27.6% -20.4% -35.7% -26.4%20 years -21.6% -17.1% -31.1% -24.6% -39.7% -31.5%

Source: MSDW Private Wealth Management Asset Allocation Group.

-

11

Asset Allocation Principles: High Net Worth Investor Behavior (cont.) David M. Darst

• Desire insurance protection without facing thepremium costs of such protection. Privateinvestors need to recognize, and be willing to pay for(in the form of dampened overall return on theupside and the downside), asset classes which areincluded in a strategic asset allocation framework fordefensive, hedging, or insurance purposes.

• Project the most recent asset class returns andmeasure against the best-performingbenchmarks. Particularly after a series of successful(or unsuccessful) years of investment returns,individuals tend to expect such performance tocontinue indefinitely. At the same time, HNWinvestors want returns that match or exceed the top-performing indices or asset classes. In part, thesedesires, and the relative outperformance of the S&P500 index vs. a substantial majority of mutual fundsduring many years of the early- and mid-1990s, havefueled the dramatic expansion of assets in stock andbond index funds, from $2.1 billion in 1987 to$140.6 billion at the end of the third quarter in 1997.

• Experience wide swings in sentiment, confidence,and patience. Throughout recorded history, this ishuman nature. Over time, successful asset allocationcomes from the ability to distinguish cyclical andsecular movements, and act accordingly.

• Ignore asset allocation trade-offs. HNW privateinvestors should recognize the virtual impossibilityof finding an asset class that simultaneously meetsall the desired criteria: deep liquidity; stable,guaranteed principal values; high current yields; andcapital growth that consistently and substantiallyoutperforms inflation, taxes, and the popular indices.

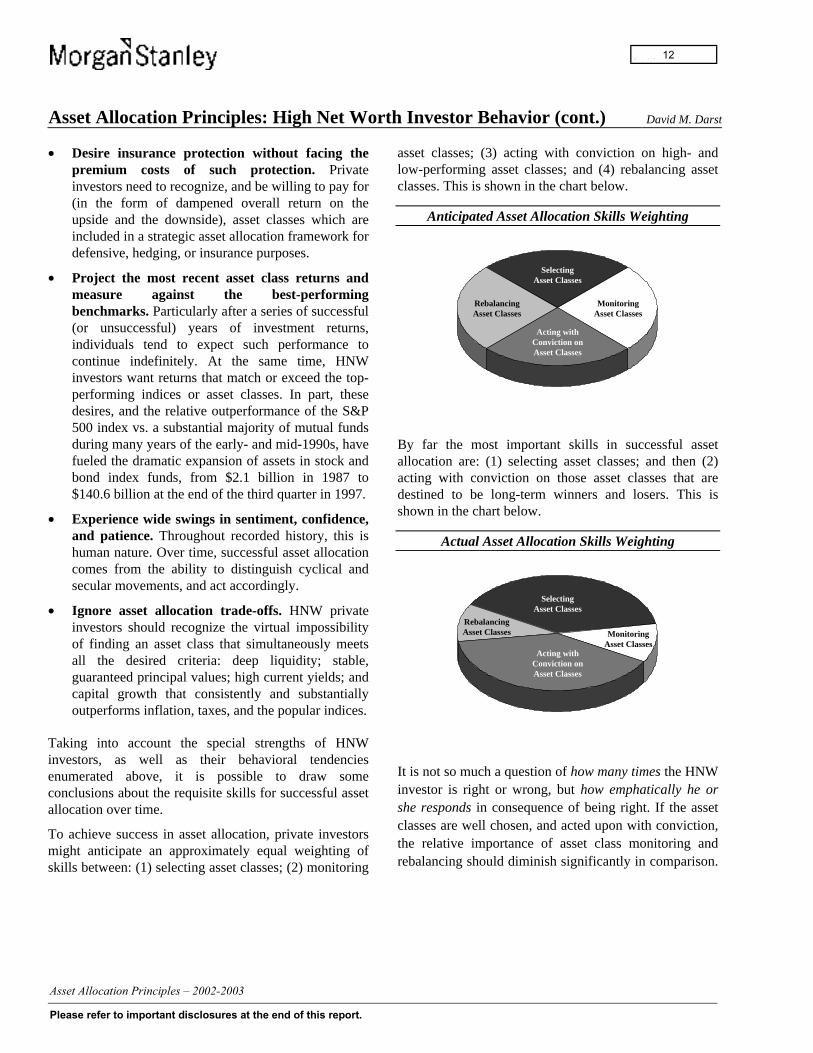

Taking into account the special strengths of HNWinvestors, as well as their behavioral tendenciesenumerated above, it is possible to draw someconclusions about the requisite skills for successful assetallocation over time.

To achieve success in asset allocation, private investorsmight anticipate an approximately equal weighting ofskills between: (1) selecting asset classes; (2) monitoring

asset classes; (3) acting with conviction on high- andlow-performing asset classes; and (4) rebalancing assetclasses. This is shown in the chart below.

Anticipated Asset Allocation Skills Weighting

MonitoringAsset Classes

RebalancingAsset Classes

SelectingAsset Classes

Acting withConviction onAsset Classes

By far the most important skills in successful assetallocation are: (1) selecting asset classes; and then (2)acting with conviction on those asset classes that aredestined to be long-term winners and losers. This isshown in the chart below.

Actual Asset Allocation Skills Weighting

MonitoringAsset Classes

RebalancingAsset Classes

SelectingAsset Classes

Acting withConviction onAsset Classes

It is not so much a question of how many times the HNWinvestor is right or wrong, but how emphatically he orshe responds in consequence of being right. If the assetclasses are well chosen, and acted upon with conviction,the relative importance of asset class monitoring andrebalancing should diminish significantly in comparison.

-

12

Asset Allocation Principles: Interest and Dividend Reinvestment David M. Darst

One of the most important, yet least appreciated, aspectsof investing in specific asset classes is the concept ofinterest and dividend reinvestment. For compounding towork its highly beneficial effects on portfolio valuesover time, attention must be paid to the necessity, theconsequences, and the challenges of investing couponpayments or dividends at sufficiently high rates of return.Spending such income flows, using them to pay taxes, orreinvesting them at low returns can significantly reducethe Realized Compound Yield and thus the total long-term asset value of a portfolio.

For High Net Worth investors, the reinvestment ofcoupon and dividend payments, in as tax-advantaged amanner as possible, is of vital importance in actuallyachieving the long-term quoted returns from debt orequity securities. This is particularly true, the longer theinvestment holding period and the higher the expectedcompound rates of return.

Coupon Reinvestment in Fixed Income Securities

The proportion of a fixed income security’s return that isrepresented by the reinvestment of interest couponsincreases: (i) the higher the coupon; (ii) the higher theinitial yield to maturity; and (iii) the longer the maturityof the instrument. For sufficiently high-coupon, longmaturity bonds, purchased at sufficiently high initialyields to maturity, the assumed reinvestment of interestcoupons, assumed to be at that same, high initial yield tomaturity, can account for a dramatically large share ofthe total funds received from an investment.

The Importance of Interest on Interest10% Annual Coupon Bond, 30-Year Maturity, 10% Yield to Maturity

5 Years 10 Years 20 Years 30 Years

$2,000

$6,000

10,000

14,000

18,000

$3,000 = 30 coupons x $100/coupon

$1,000 = Principal Repayment

30-year total = $17,449.40

Total FundsReceived

$13,444.40 = Reinvestment of Interest Coupons

Maturity

Source: MSDW Private Wealth Management Asset Allocation Group.

For example, as shown in the accompanying chart, for a$1,000 par value, 30-year, 10% annual coupon bond,purchased at a 10% yield to maturity, the total fundsreceived over the life of the bond amount to $17,449.40.Of this total, $1,000, or 5.7%, represents the repaymentof principal; $3,000, or 17.2%, represents 30 years’payment of $100 annual coupons; and $13,449.40, orfully 77.1%, represents the aggregate total generated bythe reinvestment of each $100 annual1 coupon at aninterest rate of exactly 10%.

Source of Funds Amount Percent of TotalPrincipal $1,000.00 5.7%Coupons $3,000.00 17.2%Coupon Reinvestment $13,449.40 77.1%Total $17,449.40 100.0%

As a percent of the total funds received from a 10%annual coupon bond purchased at a beginning yield levelof 10%, the importance of coupon reinvestment, alsoknown as interest on interest, ranges from 77.1% on a30-year bond, to 55.4% on a 20-year bond, to 22.8% on a10-year bond, to 6.9% on a 5-year bond. This is shownin the table below:

Annual Coupon Bonds Purchased at 10%and 5% Yields to Maturity

$1,000 Par Value Bonds

Percentage of Total Funds Received

Coupon

InitialYield to

MaturityYears toMaturity

Repaymentof

PrincipalInterestCoupons

Reinvestmentof InterestCoupons

TotalFunds

Received

10% 10% 5 62.1% 31.0% 6.9% $1,610.5110% 10% 10 38.6% 38.6% 22.8% 2,593.7410% 10% 20 14.9% 29.7% 55.4% 6,727.5010% 10% 30 5.7% 17.2% 77.1% 17,449.40

5% 5% 5 78.3% 19.6% 2.1% $1,276.285% 5% 10 61.4% 30.7% 7.9% 1,628.895% 5% 20 37.7% 37.7% 24.6% 2,653.305% 5% 30 23.1% 34.7% 42.2% 4,321.94

Source: MSDW Private Wealth Management Asset Allocation Group.

The table also demonstrates the diminished importanceof coupon reinvestment at lower coupon rates and initialyield levels. For instance, for a 30-year, 5% annualcoupon bond, purchased at a 5% initial yield to maturity,the reinvestment of interest coupons represents 42.2%, or$1,821.94, of the $4,321.94 in total funds received by theinvestor.

1 For the sake of simplicity, annual, rather than semiannual, coupons are

used in this analysis. For a $1,000 par value, 10% bond, with 60semiannual coupons of 5%, the total funds received amount to$18,679.19, of which $14,679.19, or 78.6%, represents the reinvestmentof interest coupons at an assumed rate of 10%.

-

13

Asset Allocation Principles: Interest and Dividend Reinvestment (cont.) David M. Darst

For short-maturity bonds, the importance of couponreinvestment is modest, regardless of coupon andbeginning yield level. For 5-year, 10% coupon bonds,purchased at a 10% yield to maturity, the reinvestment ofinterest coupons represents 6.9% of total funds received,and for 5-year, 5% coupon bonds, purchased at a 5%yield to maturity, the reinvestment of interest couponsrepresents only 2.1% of total funds received.

In practice, interest rates do not remain stable for theentire life of a 30-year bond, much less a bond of 20, 10,or even 5 years’ maturity. Investors are thus subject toone key form of reinvestment risk, or the chance thatcoupons (or principal) will not be able to be invested at arate equal to the bond’s original yield to maturity. Afurther complication for High Net Worth Investors stemsfrom the annual taxability of interest and dividendincome.

In response to these tax considerations, High Net Worthinvestors have sought, whenever possible, to own anysecurities that have a meaningful degree of reinvestmentrisk in tax-advantaged structures, such as a Foundationor a 401(k) plan. A tax-advantaged structure is especiallyimportant in the case of zero coupon bonds, whichotherwise incur taxes on the phantom interest incomethat is not paid in cash but which is considered by the taxauthorities to accrete each year.

Zero Coupon Bonds

Zero coupon bonds eliminate coupon reinvestment riskby means of the annual internal compounding of capitalvalues, to a final value for the bond (usually its $1,000par value). Zeros have been popular with low-tax or tax-advantaged investors seeking to lock in a specificcompounding rate of interest at the time of the bond’spurchase. In addition, some investors seek out zerocoupon bonds due to their high degree of capital valueresponsiveness in reaction to interest rate changes.

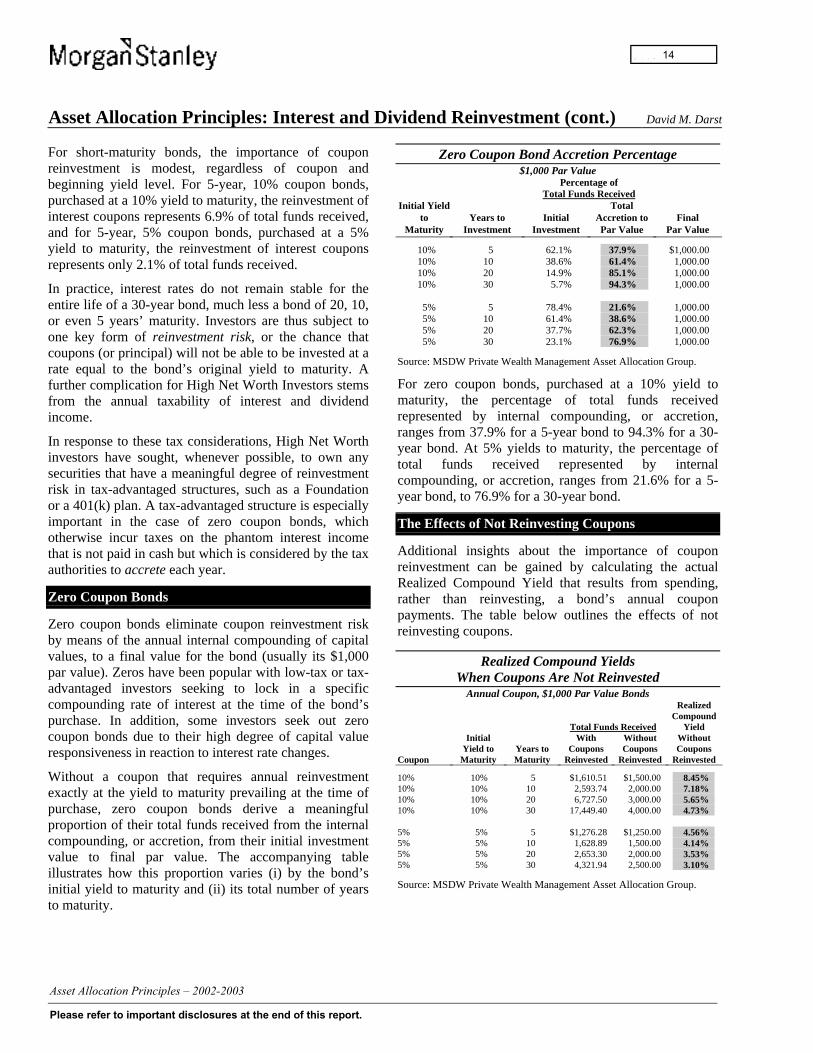

Without a coupon that requires annual reinvestmentexactly at the yield to maturity prevailing at the time ofpurchase, zero coupon bonds derive a meaningfulproportion of their total funds received from the internalcompounding, or accretion, from their initial investmentvalue to final par value. The accompanying tableillustrates how this proportion varies (i) by the bond’sinitial yield to maturity and (ii) its total number of yearsto maturity.

Zero Coupon Bond Accretion Percentage$1,000 Par Value

Percentage ofTotal Funds Received

Initial Yieldto

MaturityYears to

InvestmentInitial

Investment

TotalAccretion toPar Value

FinalPar Value

10% 5 62.1% 37.9% $1,000.0010% 10 38.6% 61.4% 1,000.0010% 20 14.9% 85.1% 1,000.0010% 30 5.7% 94.3% 1,000.00

5% 5 78.4% 21.6% 1,000.005% 10 61.4% 38.6% 1,000.005% 20 37.7% 62.3% 1,000.005% 30 23.1% 76.9% 1,000.00

Source: MSDW Private Wealth Management Asset Allocation Group.

For zero coupon bonds, purchased at a 10% yield tomaturity, the percentage of total funds receivedrepresented by internal compounding, or accretion,ranges from 37.9% for a 5-year bond to 94.3% for a 30-year bond. At 5% yields to maturity, the percentage oftotal funds received represented by internalcompounding, or accretion, ranges from 21.6% for a 5-year bond, to 76.9% for a 30-year bond.

The Effects of Not Reinvesting Coupons

Additional insights about the importance of couponreinvestment can be gained by calculating the actualRealized Compound Yield that results from spending,rather than reinvesting, a bond’s annual couponpayments. The table below outlines the effects of notreinvesting coupons.

Realized Compound YieldsWhen Coupons Are Not Reinvested

Annual Coupon, $1,000 Par Value Bonds

Total Funds Received

RealizedCompound

Yield

Coupon

InitialYield to

MaturityYears toMaturity

WithCoupons

Reinvested

WithoutCoupons

Reinvested

WithoutCoupons

Reinvested

10% 10% 5 $1,610.51 $1,500.00 8.45%10% 10% 10 2,593.74 2,000.00 7.18%10% 10% 20 6,727.50 3,000.00 5.65%10% 10% 30 17,449.40 4,000.00 4.73%

5% 5% 5 $1,276.28 $1,250.00 4.56%5% 5% 10 1,628.89 1,500.00 4.14%5% 5% 20 2,653.30 2,000.00 3.53%5% 5% 30 4,321.94 2,500.00 3.10%

Source: MSDW Private Wealth Management Asset Allocation Group.

-

14

Asset Allocation Principles: Interest and Dividend Reinvestment (cont.) David M. Darst

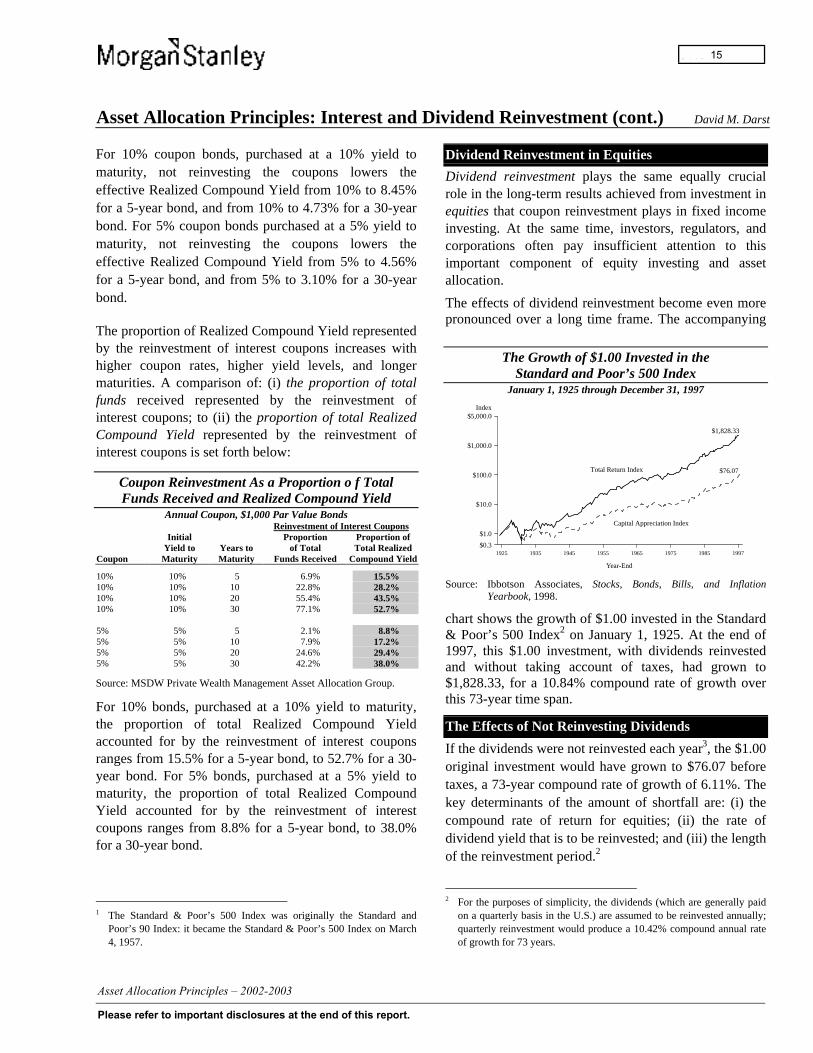

For 10% coupon bonds, purchased at a 10% yield tomaturity, not reinvesting the coupons lowers theeffective Realized Compound Yield from 10% to 8.45%for a 5-year bond, and from 10% to 4.73% for a 30-yearbond. For 5% coupon bonds purchased at a 5% yield tomaturity, not reinvesting the coupons lowers theeffective Realized Compound Yield from 5% to 4.56%for a 5-year bond, and from 5% to 3.10% for a 30-yearbond.

The proportion of Realized Compound Yield representedby the reinvestment of interest coupons increases withhigher coupon rates, higher yield levels, and longermaturities. A comparison of: (i) the proportion of totalfunds received represented by the reinvestment ofinterest coupons; to (ii) the proportion of total RealizedCompound Yield represented by the reinvestment ofinterest coupons is set forth below:1

Coupon Reinvestment As a Proportion o f TotalFunds Received and Realized Compound Yield

Annual Coupon, $1,000 Par Value BondsReinvestment of Interest Coupons

Coupon

InitialYield to

MaturityYears toMaturity

Proportionof Total

Funds Received

Proportion ofTotal Realized

Compound Yield

10% 10% 5 6.9% 15.5%10% 10% 10 22.8% 28.2%10% 10% 20 55.4% 43.5%10% 10% 30 77.1% 52.7%

5% 5% 5 2.1% 8.8%5% 5% 10 7.9% 17.2%5% 5% 20 24.6% 29.4%5% 5% 30 42.2% 38.0%

Source: MSDW Private Wealth Management Asset Allocation Group.

For 10% bonds, purchased at a 10% yield to maturity,the proportion of total Realized Compound Yieldaccounted for by the reinvestment of interest couponsranges from 15.5% for a 5-year bond, to 52.7% for a 30-year bond. For 5% bonds, purchased at a 5% yield tomaturity, the proportion of total Realized CompoundYield accounted for by the reinvestment of interestcoupons ranges from 8.8% for a 5-year bond, to 38.0%for a 30-year bond.

1 The Standard & Poor’s 500 Index was originally the Standard and

Poor’s 90 Index: it became the Standard & Poor’s 500 Index on March4, 1957.

Dividend Reinvestment in Equities

Dividend reinvestment plays the same equally crucialrole in the long-term results achieved from investment inequities that coupon reinvestment plays in fixed incomeinvesting. At the same time, investors, regulators, andcorporations often pay insufficient attention to thisimportant component of equity investing and assetallocation.

The effects of dividend reinvestment become even morepronounced over a long time frame. The accompanying

The Growth of $1.00 Invested in theStandard and Poor’s 500 Index

January 1, 1925 through December 31, 1997

1925 1935 1945 1955 1965 1975 1985 1997$0.3

$1.0

$10.0

$100.0

1000.0

5000.0Index

Year-End

$1,828.33

$76.07Total Return Index

Capital Appreciation Index

$5,000.0

$1,000.0

Source: Ibbotson Associates, Stocks, Bonds, Bills, and InflationYearbook, 1998.

chart shows the growth of $1.00 invested in the Standard& Poor’s 500 Index2 on January 1, 1925. At the end of1997, this $1.00 investment, with dividends reinvestedand without taking account of taxes, had grown to$1,828.33, for a 10.84% compound rate of growth overthis 73-year time span.

The Effects of Not Reinvesting Dividends

If the dividends were not reinvested each year3, the $1.00original investment would have grown to $76.07 beforetaxes, a 73-year compound rate of growth of 6.11%. Thekey determinants of the amount of shortfall are: (i) thecompound rate of return for equities; (ii) the rate ofdividend yield that is to be reinvested; and (iii) the lengthof the reinvestment period.2

2 For the purposes of simplicity, the dividends (which are generally paid

on a quarterly basis in the U.S.) are assumed to be reinvested annually;quarterly reinvestment would produce a 10.42% compound annual rateof growth for 73 years.

-

15

Asset Allocation Principles: Interest and Dividend Reinvestment (cont.) David M. Darst

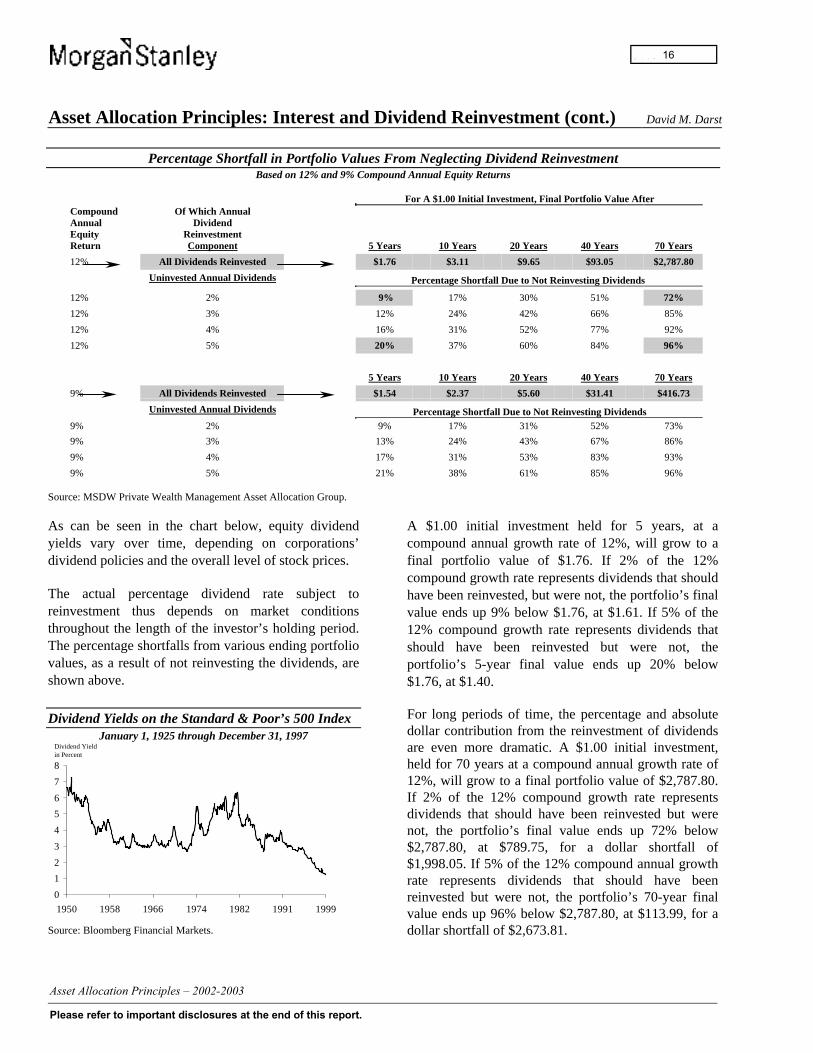

Percentage Shortfall in Portfolio Values From Neglecting Dividend ReinvestmentBased on 12% and 9% Compound Annual Equity Returns

For A $1.00 Initial Investment, Final Portfolio Value AfterCompoundAnnualEquityReturn

Of Which AnnualDividend

ReinvestmentComponent 5 Years 10 Years 20 Years 40 Years 70 Years

12% All Dividends Reinvested $1.76 $3.11 $9.65 $93.05 $2,787.80

Uninvested Annual Dividends Percentage Shortfall Due to Not Reinvesting Dividends

12% 2% 9% 17% 30% 51% 72%

12% 3% 12% 24% 42% 66% 85%

12% 4% 16% 31% 52% 77% 92%

12% 5% 20% 37% 60% 84% 96%

5 Years 10 Years 20 Years 40 Years 70 Years

9% All Dividends Reinvested $1.54 $2.37 $5.60 $31.41 $416.73

Uninvested Annual Dividends Percentage Shortfall Due to Not Reinvesting Dividends9% 2% 9% 17% 31% 52% 73%

9% 3% 13% 24% 43% 67% 86%

9% 4% 17% 31% 53% 83% 93%

9% 5% 21% 38% 61% 85% 96%

Source: MSDW Private Wealth Management Asset Allocation Group.

As can be seen in the chart below, equity dividendyields vary over time, depending on corporations’dividend policies and the overall level of stock prices.

The actual percentage dividend rate subject toreinvestment thus depends on market conditionsthroughout the length of the investor’s holding period.The percentage shortfalls from various ending portfoliovalues, as a result of not reinvesting the dividends, areshown above.

Dividend Yields on the Standard & Poor’s 500 IndexJanuary 1, 1925 through December 31, 1997

0

1

2

3

4

5

6

7

8

1950 1958 1966 1974 1982 1991 1999

Dividend Yieldin Percent

Source: Bloomberg Financial Markets.

A $1.00 initial investment held for 5 years, at acompound annual growth rate of 12%, will grow to afinal portfolio value of $1.76. If 2% of the 12%compound growth rate represents dividends that shouldhave been reinvested, but were not, the portfolio’s finalvalue ends up 9% below $1.76, at $1.61. If 5% of the12% compound growth rate represents dividends thatshould have been reinvested but were not, theportfolio’s 5-year final value ends up 20% below$1.76, at $1.40.

For long periods of time, the percentage and absolutedollar contribution from the reinvestment of dividendsare even more dramatic. A $1.00 initial investment,held for 70 years at a compound annual growth rate of12%, will grow to a final portfolio value of $2,787.80.If 2% of the 12% compound growth rate representsdividends that should have been reinvested but werenot, the portfolio’s final value ends up 72% below$2,787.80, at $789.75, for a dollar shortfall of$1,998.05. If 5% of the 12% compound annual growthrate represents dividends that should have beenreinvested but were not, the portfolio’s 70-year finalvalue ends up 96% below $2,787.80, at $113.99, for adollar shortfall of $2,673.81.

-

16

Asset Allocation Principles: Critical Determinants of Asset Allocation David M. Darst

Distilled to its purest form, asset allocation for High NetWorth investors is intended, among other objectives, tohelp answer four fundamental questions: (i) What is theproper mix between equities, fixed income securities,alternative investments, and cash equivalentinstruments? (ii) What is the proper mix betweendomestic and non-domestic securities? (iii) What is theproper reference currency, and the proper degree of non-reference currency exposure? and (iv) What is the properdivision of assets between publicly-traded and privateinvestments?

Critical Determinants of Asset Allocation

In developing an appropriate response to each of thesequestions, High Net Worth investors need to carefullyassess the critical determinants of asset allocation. Thesecritical determinants can be grouped under a few broadrubrics, analogous in some sense to the investor’s ownhighly individualized set of income statement factors,balance sheet factors, and off-balance sheet factors.

Each investor’s history, current situation, andexpectations for the future will shape the degree ofemphasis to be placed on these asset allocationdeterminants, as set forth below:

Income Statement Factors

• Tolerance for bearing risk or loss. An investor’sability to withstand losses in a given investmentposition or asset class is influenced by the severityof the loss in percentage and absolute terms, theduration of the loss, whether it is realized orunrealized, expected future price action, the pricebehavior of other investment instruments, generaleconomic conditions, and not least, the investor’sown emotional, financial, and psychological profile.

• Cyclical and secular market outlook. A highlyimportant influence on strategic and tactical assetallocation is the investor’s qualitatively- andquantitatively-driven sense of where markets aregoing, how long they will take to reach their pricetargets, and the pattern of price movements —stairstep, continuous, highly volatile, or an extendedwaiting period, followed by a sharp upward ordownward move.

• Confidence level in projections. One of the greatseparators of highly successful investors or asset

• allocators from less fortunate ones is the age-olddecision between conviction and flexibility.Investors who know they are right have the courageof their convictions; at the same time, investors whodiscover flaws in their own thinking must have theflexibility to face facts and reverse course ifnecessary.

• Investor’s and assets’ tax status. The High NetWorth investor's tax status — federal, state, local,and cross-border; income, capital gains, and estate;current and future — brings a crucial set of variablesto bear in structuring an optimal allocation of assets,as does the tax treatment of all the capital andincome flows from an investment.

Balance Sheet Factors

• Individual motivations and circumstances. It isworthwhile for the HNW investor to reflect on theultimate goals and objectives of the assets beingallocated — for whose benefit are the assets beinginvested? What do these assets mean in the contextof the beneficiaries’ other circumstances? In whatblocks of time does the investor reckon? Whatplanned commitments and unforeseen developmentsshould be allowed for?

• Influence of dominant investment positions. Assetallocation for High Net Worth investors should takeaccount of large existing or contractually-expectedinvestment positions, capital flows, options, andrestricted securities. At the same time, objectivityand rigorous analysis are required to weigh themerits and costs of retaining dominant investmentpositions vs. diversification of all or a portion ofthese positions into other asset classes.

• Financial requirements, liabilities, andcontingencies. Planned annual expenditure levels,margin debt, mortgages, and other liabilities affectthe asset allocation decision because the certainty ofsuch outlays often leads to the selection of assetclasses and investments having predictable paymentstreams to meet these obligations.

• Significant non-tracked assets. Many High NetWorth investors have a considerable portion of theiroverall wealth tied up in asset categories that are notincluded in conventional asset allocationframeworks. Such assets include: (i) royalty streamsfrom media-related, oil, gas, forestry, and mining

-

17

Asset Allocation Principles: Critical Determinants of Asset Allocation (cont.) David M. Darst

interests; (ii) art, collectibles, antiques, and jewelry;and (iii) ownership positions in family businesses,undeveloped land, and other real property.

Off-Balance Sheet Factors

• Ability to recognize and evaluate trade-offs. Webelieve the entire asset allocation process hinges onthe investor’s skill at recognizing and judging aseries of financial factors. How important is one setof factors compared with another set of factors? Forany given tradeoff, how much of the costs andbenefits of one variable has to be foregone in orderto obtain a more favorable cost-benefit profile inanother variable? Several of the most frequently-encountered asset allocation tradeoffs are listed inthe table below:

Asset Allocation Tradeoffs

Characteristic

Tending towardlower risk,

lower return vs.

Tending towardhigher risk,

higher return

Time Frame Short-term vs. Long-TermAsset Allocation Strategy Diversification vs. ConcentrationHarvesting/Consumption

of Returns Current vs. DeferredForm of Returns Income vs. Change in Capital ValuePattern of Returns Predictable vs. VariableAccess/Convertibility Liquid Investments vs. Illiquid Investments

• Goals and benchmarks for returns. We believeanother crucial determinant of a High Net Worthinvestor’s asset allocation is the universe of goalsthat his or her investment activity is intended toachieve, and the relative importance assigned toeach. These goals include safety of principal,protection of purchasing power, and specified levelsof annual pretax or after-tax returns. Prudence andrealism are essential in the selection of anappropriate absolute benchmark, or the constructionof a blended benchmark, against which theinvestor’s results are to be measured.

• Timing, nature, and size of portfolio outflows.When and in what form capital is to be returned tothe ultimate beneficiaries of the portfolio can causemeaningful shifts in asset allocation.

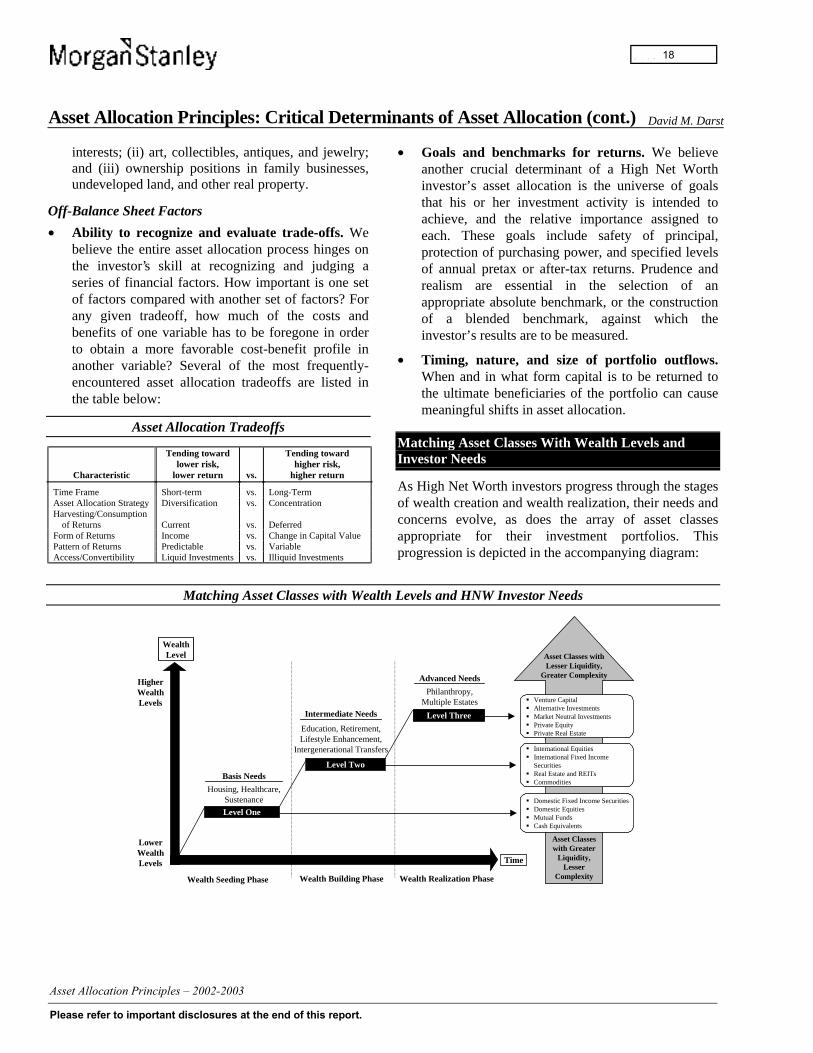

Matching Asset Classes With Wealth Levels andInvestor Needs

As High Net Worth investors progress through the stagesof wealth creation and wealth realization, their needs andconcerns evolve, as does the array of asset classesappropriate for their investment portfolios. Thisprogression is depicted in the accompanying diagram:

Matching Asset Classes with Wealth Levels and HNW Investor Needs

Wealth Seeding Phase Wealth Building Phase Wealth Realization Phase

LowerWealthLevels

HigherWealthLevels

Basis Needs

Intermediate Needs

Advanced Needs

Philanthropy,Multiple Estates

Education, Retirement,Lifestyle Enhancement,

Intergenerational Transfers

Housing, Healthcare,Sustenance

WealthLevel

Time

� Venture Capital� Alternative Investments� Market Neutral Investments� Private Equity� Private Real Estate

� International Equities� International Fixed Income

Securities� Real Estate and REITs� Commodities

� Domestic Fixed Income Securities� Domestic Equities� Mutual Funds� Cash Equivalents

Level One

Level Two

Level Three

Asset Classes withLesser Liquidity,

Greater Complexity

Asset Classeswith Greater

Liquidity,Lesser

Complexity

-

18

Asset Allocation Principles: Critical Determinants of Asset Allocation (cont.) David M. Darst

Wealth Seeding PhaseFor those individuals who are in the beginning — orwealth seeding — part of their wealth creation activity,basic needs are paramount and include: housing,healthcare, food, clothing, and insurance. If surpluscapital is available for investments, HNW investorsshould consider asset classes that are characterized by areasonable degree of liquidity and understandability.These asset classes generally include domestic equities,domestic fixed income securities, and cash equivalents,either directly or in mutual fund or partnership form.

Wealth Building PhaseAs individuals progress through the growth — or wealthbuilding — phase of their wealth creation activity, theirneeds expand, to include education, lifestyleenhancement, retirement, and intergenerational transfers.At the same time, although not in all cases, their range ofinvestible asset classes expands to include not only theabovementioned asset classes, but also internationalequities, international fixed income securities, real estateand REITs, and commodities.

Wealth Realization PhaseWhen individuals acquire significant wealth — in thewealth realization phase — through a liquidity eventsuch as a merger or acquisition, a securities offering, orinheritance, the circle of their needs may expand yetagain, to include philanthropy and the maintenance ofmultiple estates. In this phase, High Net Worth investorscan and should encompass an even broader range ofasset classes in addition to those considered byindividuals in the wealth seeding and wealth buildingphases. These more advanced asset classes may also becharacterized by a lower level of liquidity and asomewhat greater degree of complexity, and includeventure capital, alternative investments, market neutralinvestments, private equity, and private real estate.

Effects of Financial Market Environments on AssetAllocation and Investor Behavior

Financial market conditions can exert a powerfulinfluence not only on asset allocation, but also onprevailing approaches to investor behavior andinvestment strategy. For example, in a mature bullmarket for equities, cash as an asset class and markettiming are denigrated in favor of a virtually fullyinvested investment approach and a long-horizon, buy-

the-dips mentality toward stocks. The accompanyingchart presents a back-of-the-envelope estimate ofinvestors’ motives in a bull market compared with theirmotives in a bear market.

Behavioral Effects of Financial Market Environments

70%15%

15%

10%

60%

30%

Favorable FinancialMarket Environment

Unfavorable FinancialMarket Environment

Making Money

Diversification

Avoiding Losses

Avoiding Losses

Diversification

Making Money

Bull Market Motives Bear Market Motives

Effects on Investors

• Significant amounts of newly-createdindividual wealth

• Wide range of geographical, assetclass, and implementation strategies

• Heightened and frequentlyunrealistic investor expectations

• Investor satisfaction with existingfinancial intermediaries

• Explicit and implicit assumption ofrisk

• Equities, equity-like products, andmargin borrowing more important ininvestment mix

• Interest in performance investing,alternative investments, and absolutereturn strategies

• Proliferation of investmentmanagement boutiques, consultants,and third-party capital raisers

• Focus on capital appreciation

Effects on Investors

• Wealth reduction and less newly-created wealth

• Narrow range of geographical, assetclass, and implementation strategies

• Investor dissatisfaction withinvestment performance

• Investor flight to high-qualityfinancial intermediaries

• Emphasis on risk reduction, riskcontrol, and risk management

• Short- and intermediate-term fixedincome securities more important ininvestment mix

• Reduced interest in non-mainstreaminvestments

• Consolidation/closure of investmentmanagement boutiques, consultants,and third-party capital raisers

• Focus on capital preservation

The chart also contrasts some of the commonly-encountered effects of a favorable financial marketenvironment on asset allocation with those of anunfavorable financial market environment. In periods ofprolonged rising prices for financial assets, High NetWorth investors are willing to entertain a wider range ofgeographical, asset class, and implementation strategies.Amidst heightened expectations and risk assumption,investors tend to focus heavily on capital appreciation,equities and equity-like products, alternativeinvestments, and absolute return strategies.

In periods of prolonged falling financial asset prices,High Net Worth investors tend to concentrate on anarrowed range of geographical, asset class, andimplementation strategies. Investors’ primary focus istypically on capital preservation and mainstreaminvestments of a defensive character, such as short- andintermediate-term fixed income securities. Expectationsare restrained and risk awareness is crucial.

-

19

Asset Allocation Principles: Spending Versus Reinvesting Income Flows David M. Darst

A frequently encountered and highly important issue inthe asset allocation process revolves around theinvestor’s decision to spend, or alternatively to reinvest,some portion or all of the annual returns from aninvestment. The answer to this question is shaped in partby the investor’s own preferences and the timing of hisor her required capital flows, and in part by the level,pattern, and longevity of returns from a given asset class.

Consciously or unconsciously, investors often evaluatespending now versus in the future, not only in financiallyquantifiable terms, but also according to hard-to-definemeasures such as utility or enjoyment. In doing so,investors need to take account of the effects ofcompounding, inflation and deflation in the general pricelevel, and not least, psychological and highlyindividualized attitudes toward current and postponedgratification.

It is worthwhile to analyze the overall effect onintermediate cash flows — including those funds whichare spent, and the terminal value of a portfolio — of: (i)spending annual investment returns immediately afterthey have been earned; or (ii) reinvesting these returns atthe overall rate of return of the portfolio. The annualinvestment returns can be in the form of dividend orinterest income accrued or received, realized orunrealized capital gains, or some combination thereof.

The Effects of Spending vs. Reinvestment as aFunction of the Rate of Return

20-Year Investment Horizon, 20% Annual Returns

The first accompanying table shows the effects ofspending vs. reinvestment, of varying proportions ofannual returns for a $1,000 initial investment held for aperiod of 20 years with annual returns of 20%. It shouldbe pointed out that generating 20% returns for 20 years,while it has been achieved by some investors in certainasset categories, is an extraordinary accomplishment.Such rates of return, for so long, are relatively rare, evenfor performance-oriented investors in equities or fixed-income securities, much less for asset managers in lessefficient markets such as private equity or venturecapital. In the two immediately following sections, asimilar analysis has been carried out for 20-yearinvestment horizons using annual returns of 10% and5%, respectively.

Several simplifying assumptions have been made inorder to highlight some of the important principles whichderive from this analysis. For example, it is assumed, buthighly unlikely, that the investor can reinvest the annualreturns from his or her investments at exactly the samerate as the investment’s original rate of return — 20% inthe first table displayed here, 10% in the second table,and 5% in the third table. In addition, income taxes,capital gains taxes, inflation and deflation, andtransaction costs are not considered here. Any one ofthese factors can introduce meaningful subtleties into theconclusions.

-

20

Asset Allocation Principles: Spending Versus Reinvesting Income Flows (cont.) David M. Darst

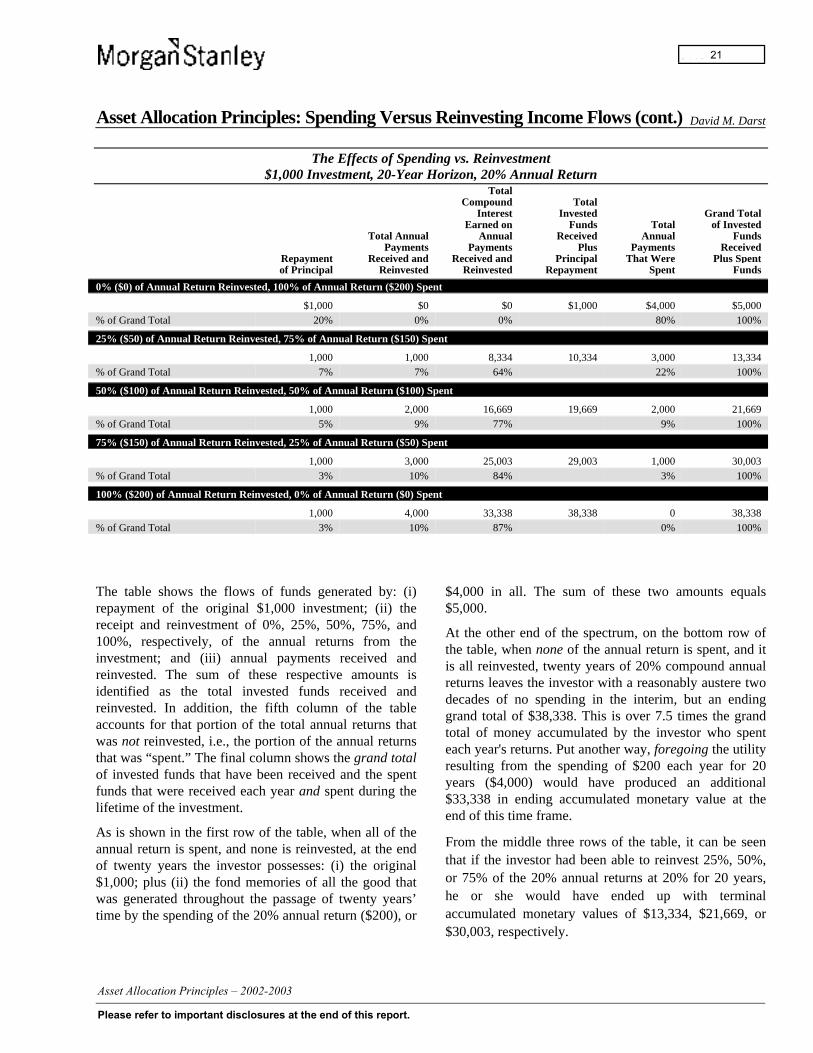

The Effects of Spending vs. Reinvestment$1,000 Investment, 20-Year Horizon, 20% Annual Return

TotalCompound Total

Interest Invested Grand TotalEarned on Funds Total of Invested

Total Annual Annual Received Annual FundsPayments Payments Plus Payments Received

Repayment Received and Received and Principal That Were Plus Spentof Principal Reinvested Reinvested Repayment Spent Funds

0% ($0) of Annual Return Reinvested, 100% of Annual Return ($200) Spent

$1,000 $0 $0 $1,000 $4,000 $5,000% of Grand Total 20% 0% 0% 80% 100%

25% ($50) of Annual Return Reinvested, 75% of Annual Return ($150) Spent

1,000 1,000 8,334 10,334 3,000 13,334% of Grand Total 7% 7% 64% 22% 100%

50% ($100) of Annual Return Reinvested, 50% of Annual Return ($100) Spent

1,000 2,000 16,669 19,669 2,000 21,669% of Grand Total 5% 9% 77% 9% 100%

75% ($150) of Annual Return Reinvested, 25% of Annual Return ($50) Spent

1,000 3,000 25,003 29,003 1,000 30,003% of Grand Total 3% 10% 84% 3% 100%

100% ($200) of Annual Return Reinvested, 0% of Annual Return ($0) Spent

1,000 4,000 33,338 38,338 0 38,338% of Grand Total 3% 10% 87% 0% 100%

The table shows the flows of funds generated by: (i)repayment of the original $1,000 investment; (ii) thereceipt and reinvestment of 0%, 25%, 50%, 75%, and100%, respectively, of the annual returns from theinvestment; and (iii) annual payments received andreinvested. The sum of these respective amounts isidentified as the total invested funds received andreinvested. In addition, the fifth column of the tableaccounts for that portion of the total annual returns thatwas not reinvested, i.e., the portion of the annual returnsthat was “spent.” The final column shows the grand totalof invested funds that have been received and the spentfunds that were received each year and spent during thelifetime of the investment.

As is shown in the first row of the table, when all of theannual return is spent, and none is reinvested, at the endof twenty years the investor possesses: (i) the original$1,000; plus (ii) the fond memories of all the good thatwas generated throughout the passage of twenty years’time by the spending of the 20% annual return ($200), or

$4,000 in all. The sum of these two amounts equals$5,000.

At the other end of the spectrum, on the bottom row ofthe table, when none of the annual return is spent, and itis all reinvested, twenty years of 20% compound annualreturns leaves the investor with a reasonably austere twodecades of no spending in the interim, but an endinggrand total of $38,338. This is over 7.5 times the grandtotal of money accumulated by the investor who spenteach year's returns. Put another way, foregoing the utilityresulting from the spending of $200 each year for 20years ($4,000) would have produced an additional$33,338 in ending accumulated monetary value at theend of this time frame.

From the middle three rows of the table, it can be seenthat if the investor had been able to reinvest 25%, 50%,or 75% of the 20% annual returns at 20% for 20 years,he or she would have ended up with terminalaccumulated monetary values of $13,334, $21,669, or$30,003, respectively.

-

21

Asset Allocation Principles: Spending Versus Reinvesting Income Flows (cont.) David M. Darst

The Effects of Spending vs. Reinvestment$1,000 Investment, 20-Year Horizon, 10% Annual Return

TotalCompound Total

Interest Invested Grand TotalEarned on Funds Total of Invested

Total Annual Annual Received Annual FundsPayments Payments Plus Payments Received

Repayment Received and Received and Principal That Were Plus Spentof Principal Reinvested Reinvested Repayment Spent Funds

0% ($0) of Annual Return Reinvested, 100% of Annual Return ($100) Spent

$1,000 $0 $0 $1,000 $2,000 $3,000% of Grand Total 33% 0% 0% 67% 100%

25% ($25) of Annual Return Reinvested, 75% of Annual Return ($75) Spent

1,000 500 932 2,432 1,500 3,932% of Grand Total 25% 13% 24% 38% 100%

50% ($50) of Annual Return Reinvested, 50% of Annual Return ($50) Spent

1,000 1,000 1,864 3,864 1,000 4,864% of Grand Total 21% 21% 37% 21% 100%

75% ($75) of Annual Return Reinvested, 25% of Annual Return ($25) Spent

1,000 1,500 2,796 5,296 500 5,796% of Grand Total 17% 26% 48% 9% 100%

100% ($100) of Annual Return Reinvested, 0% of Annual Return ($0) Spent

1,000 2,000 3,727 6,727 0 6,727% of Grand Total 15% 30% 55% 0% 100%

20-Year Investment Horizon, 10% Annual Returns

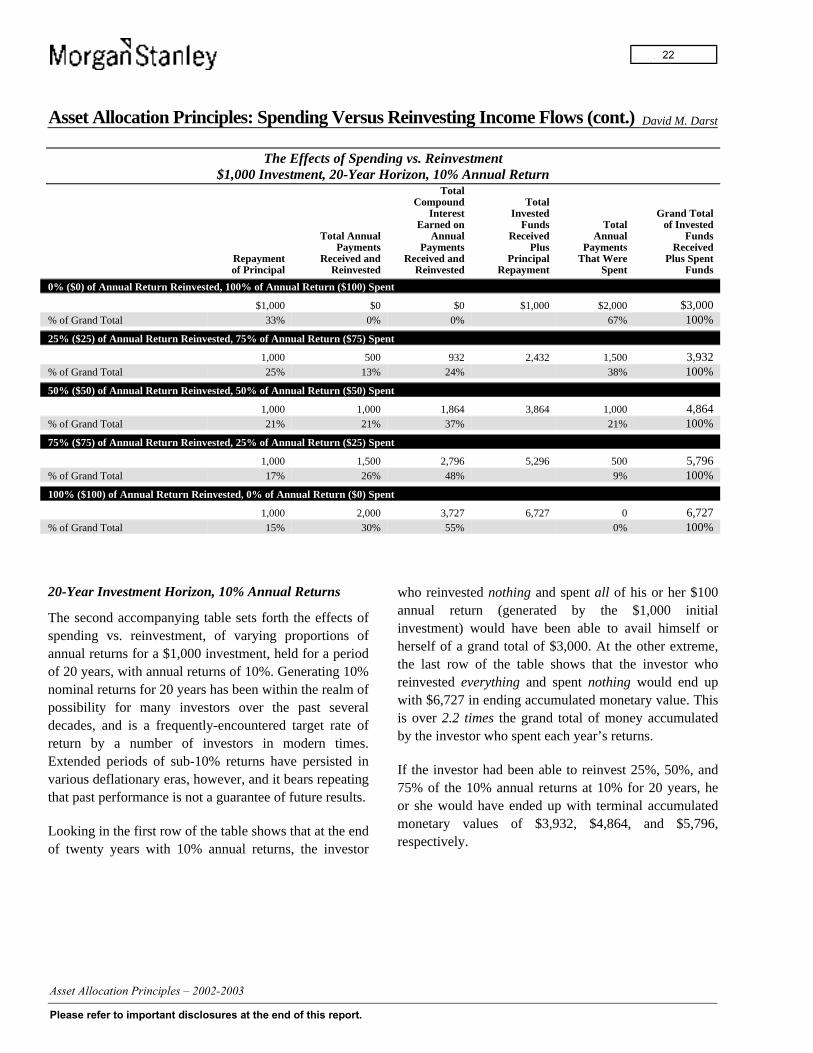

The second accompanying table sets forth the effects ofspending vs. reinvestment, of varying proportions ofannual returns for a $1,000 investment, held for a periodof 20 years, with annual returns of 10%. Generating 10%nominal returns for 20 years has been within the realm ofpossibility for many investors over the past severaldecades, and is a frequently-encountered target rate ofreturn by a number of investors in modern times.Extended periods of sub-10% returns have persisted invarious deflationary eras, however, and it bears repeatingthat past performance is not a guarantee of future results.

Looking in the first row of the table shows that at the endof twenty years with 10% annual returns, the investor

who reinvested nothing and spent all of his or her $100annual return (generated by the $1,000 initialinvestment) would have been able to avail himself orherself of a grand total of $3,000. At the other extreme,the last row of the table shows that the investor whoreinvested everything and spent nothing would end upwith $6,727 in ending accumulated monetary value. Thisis over 2.2 times the grand total of money accumulatedby the investor who spent each year’s returns.

If the investor had been able to reinvest 25%, 50%, and75% of the 10% annual returns at 10% for 20 years, heor she would have ended up with terminal accumulatedmonetary values of $3,932, $4,864, and $5,796,respectively.

-

22

Asset Allocation Principles: Spending Versus Reinvesting Income Flows (cont.) David M. Darst

The Effects of Spending vs. Reinvestment$1,000 Investment, 20-year Horizon, 5% Annual Return

TotalCompound Total

Interest Invested Grand TotalEarned on Funds Total of Invested

Total Annual Annual Received Annual FundsPayments Payments Plus Payments Received

Repayment Received and Received and Principal That Were Plus Spentof Principal Reinvested Reinvested Repayment Spent Funds

0% ($0) of Annual Return Reinvested, 100% of Annual Return ($50) Spent

$1,000 $0 $0 $1,000 $2,000 $2,000% of Grand Total 50% 0% 0% 50% 100%

25% ($12.50) of Annual Return Reinvested, 75% of Annual Return ($37.50) Spent

1,000 250 163 1,413 750 2,163% of Grand Total 45% 12% 8% 35% 100%

50% ($25) of Annual Return Reinvested, 50% of Annual Return ($25) Spent

1,000 500 327 1,827 500 2,327% of Grand Total 43% 21% 15% 21% 100%

75% ($37.50) of Annual Return Reinvested, 25% of Annual Return ($12.50) Spent

1,000 750 490 2,240 250 2,490% of Grand Total 40% 30% 20% 10% 100%

100% ($50) of Annual Return Reinvested, 0% of Annual Return ($0) Spent

1,000 2,000 653 2,653 0 2,653% of Grand Total 38% 38% 24% 0% 100%

20-Year Investment Horizon, 5% Annual Returns

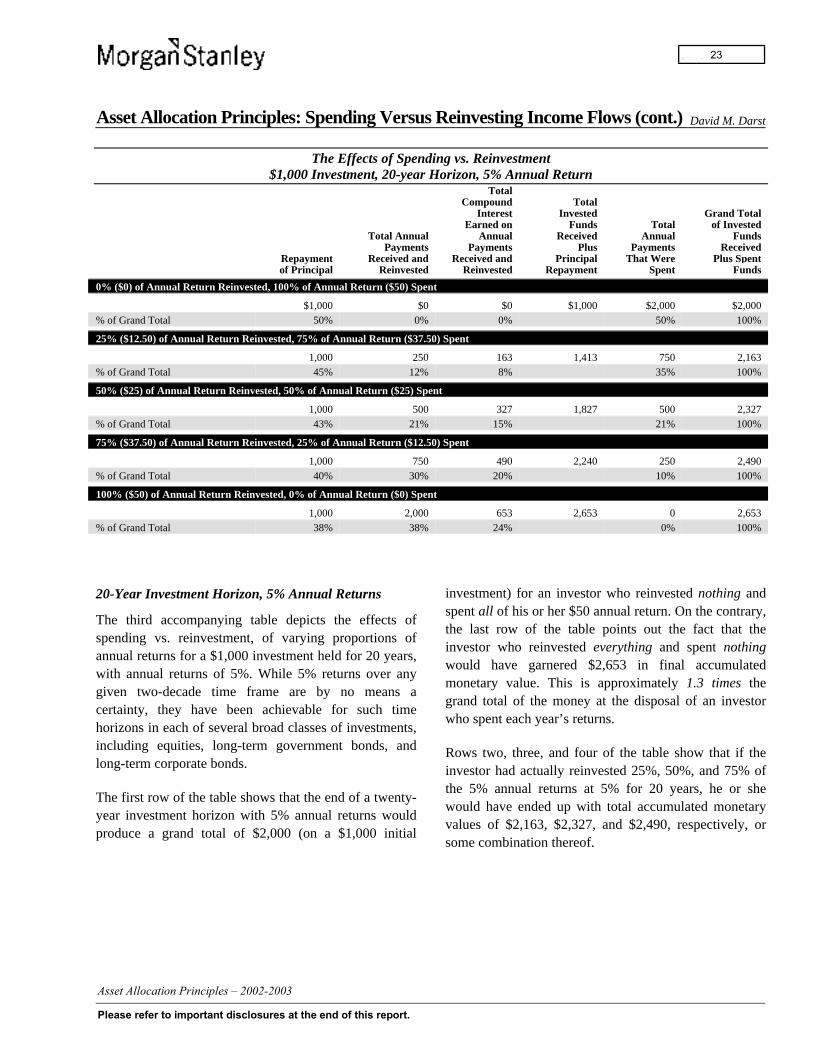

The third accompanying table depicts the effects ofspending vs. reinvestment, of varying proportions ofannual returns for a $1,000 investment held for 20 years,with annual returns of 5%. While 5% returns over anygiven two-decade time frame are by no means acertainty, they have been achievable for such timehorizons in each of several broad classes of investments,including equities, long-term government bonds, andlong-term corporate bonds.

The first row of the table shows that the end of a twenty-year investment horizon with 5% annual returns wouldproduce a grand total of $2,000 (on a $1,000 initial

investment) for an investor who reinvested nothing andspent all of his or her $50 annual return. On the contrary,the last row of the table points out the fact that theinvestor who reinvested everything and spent nothingwould have garnered $2,653 in final accumulatedmonetary value. This is approximately 1.3 times thegrand total of the money at the disposal of an investorwho spent each year’s returns.

Rows two, three, and four of the table show that if theinvestor had actually reinvested 25%, 50%, and 75% ofthe 5% annual returns at 5% for 20 years, he or shewould have ended up with total accumulated monetaryvalues of $2,163, $2,327, and $2,490, respectively, orsome combination thereof.

-

23

Asset Allocation Principles: Spending Versus Reinvesting Income Flows (cont.) David M. Darst

The Effects of Spending vs. Reinvestment$1,000 Investment, 10-year Horizon, 20% Annual Return

TotalCompound Total

Interest Invested Grand TotalEarned on Funds Total of Invested

Total Annual Annual Received Annual FundsPayments Payments Plus Payments Received

Repayment Received and Received and Principal That Were Plus Spentof Principal Reinvested Reinvested Repayment Spent Funds

0% ($0) of Annual Return Reinvested, 100% of Annual Return ($200) Spent

$1,000 $0 $0 $1,000 $2,000 $3,000% of Grand Total 33% 0% 0% 67% 100%

25% ($50.00) of Annual Return Reinvested, 75% of Annual Return ($150) Spent

1,000 500 798 2,298 1,500 3,798% of Grand Total 26% 13% 22% 39% 100%

50% ($100) of Annual Return Reinvested, 50% of Annual Return ($100) Spent

1,000 1,000 1,596 3,596 1,000 4,596% of Grand Total 22% 22% 34% 22% 100%

75% ($150) of Annual Return Reinvested, 25% of Annual Return ($50) Spent

1,000 1,500 2,394 4,894 500 5,394% of Grand Total 19% 28% 44% 9% 100%

100% ($200) of Annual Return Reinvested, 0% of Annual Return ($0) Spent

1,000 2,000 3,192 6,192 0 6,192% of Grand Total 16% 32% 52% 0% 100%

The Effects of Spending vs. Reinvestment as aFunction of the Investment Time Horizon

The fourth accompanying table shows the effects ofspending vs. reinvestment of varying proportions ofannual returns for a $1,000 investment, held for a periodof 10 years rather than 20 years, with annual returns of20%. It is worth repeating that 20% annual returns areextraordinarily high, and achieving such investmentperformance is rare, even if only for one decade, not two.

At the end of 10 years with 20% annual returns, theinvestor who reinvested nothing and spent all of his orher $200 annual return would have been able to availhimself or herself of a grand total of $3,000. Theinvestor who reinvested everything and spent nothingwould own $6,192 in ending accumulated monetaryvalue. This is just over 2 times the grand total of moneyat the disposal of an investor who spent each year’sreturns.

If the investor had reinvested 25%, 50% and 75% of the20% annual returns at 20% for 10 years, he or she wouldown ending accumulated monetary sums equal to$3,798, $4,596, and $5,394, respectively.

Implications of Spending vs. Reinvestment

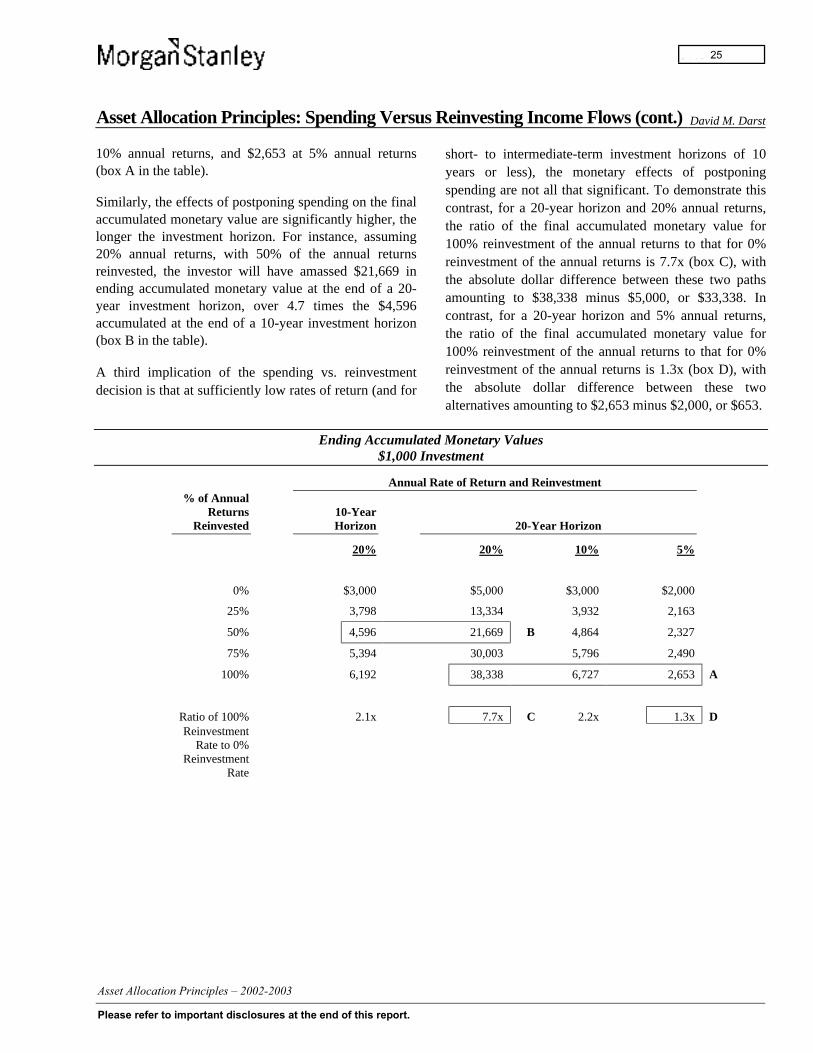

To illuminate some of the implications of the spendingvs. reinvestment decision, the fifth accompanying tablesets forth data drawn from the 20-year investments with20%, 10%, and 5% annual returns, and for comparison,the 10-year investment with 20% annual returns.

One key implication of the spending vs. reinvestmentdecision is that the final accumulated effects ofpostponing spending are dramatically higher, the higherthe reinvestment rate. For example, given a 20-yearinvestment horizon, with 100% of annual returnsreinvested, the final accumulated monetary valueamounts to $38,338 at 20% annual returns, $6,727 at

-

24

Asset Allocation Principles: Spending Versus Reinvesting Income Flows (cont.) David M. Darst

10% annual returns, and $2,653 at 5% annual returns(box A in the table).

Similarly, the effects of postponing spending on the finalaccumulated monetary value are significantly higher, thelonger the investment horizon. For instance, assuming20% annual returns, with 50% of the annual returnsreinvested, the investor will have amassed $21,669 inending accumulated monetary value at the end of a 20-year investment horizon, over 4.7 times the $4,596accumulated at the end of a 10-year investment horizon(box B in the table).

A third implication of the spending vs. reinvestmentdecision is that at sufficiently low rates of return (and for