Asian Olefins Update - Asia Petrochemical Industry Conference - Malaysia/Sub-committee...

31

Asia Petrochemical Industry Conference - 2004 Houston London Singapore Dubai Asian Olefins Update Asian Olefins Update Chemical Market Associates, Inc. Singapore Larry Tan Director, Asia Olefins Studies [email protected] Presented to the Raw Materials Committee (APIC 2004) Kuala Lumpur May 20, 2004

Transcript of Asian Olefins Update - Asia Petrochemical Industry Conference - Malaysia/Sub-committee...

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Asian Olefins Update Asian Olefins Update

Chemical Market Associates, Inc.SingaporeLarry Tan

Director, Asia Olefins [email protected]

Presented to the Raw Materials Committee (APIC 2004)

Kuala LumpurMay 20, 2004

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

State of Asia Petrochemical Industry• In midst of economic recovery • Global petrochemical markets

recovering from past poor profitability• Slow additions on new olefins capacity

till 2005• Asia crackers operating at higher cost

structure than 1990s• Competition from low cost Middle East

suppliers intense

• Dysfunctional pricingSource: Getty Images

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Asian Petchems Mired in Oversupply Since 1997

Asian Petchems Mired in Oversupply Since 1997

Weighted Average Earnings Before Interest & Tax

-100

-50

0

50

100

150

200

250

300

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

PlasticsMethanolChloralkaliAromaticsOlefins

“Reinvestment” Margin

Dollars per Ton

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

• Olefins Supply / Demand Overview

• China’s Impact on the Market • Update on Chinese Crackers

Investments• Issues Arising• Future Propylene Supply

Sources • Dysfunctional Contract Pricing

Mechanism in Asia

• Olefins Supply / Demand Overview

• China’s Impact on the Market • Update on Chinese Crackers

Investments• Issues Arising• Future Propylene Supply

Sources • Dysfunctional Contract Pricing

Mechanism in Asia

Asia Olefins UpdateAsia Olefins Update

Source: Getty Images

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

NE Asia Net Ethylene Equivalent Trade Imports To Exceed 8 Mil Tons by 2008

NE Asia Net Ethylene Equivalent Trade Imports To Exceed 8 Mil Tons by 2008

-9-8-7-6-5-4-3-2-101

98 99 00 01 02 03 04 05 06 07 08

Million TonsNet Exports

Net Imports

PolyethyleneEthyleneGlycol

VinylsOthers

StyrenicsNet Trade

Ethylene Net Equivalent Trade

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

SE Asia Ethylene Supply TighterSE Asia Ethylene Supply Tighter

-2

-1.5

-1

-0.5

0

0.5

1

98 99 00 01 02 03 04 05 06 07 08

Million Tons

Net Exports

Net Imports

PolyethyleneEthyleneGlycol

VinylsOthers

StyrenicsNet Trade

Ethylene Net Equivalent Trade

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

What About Propylene in Asia?

“Short, Shorter, Very Short!”

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

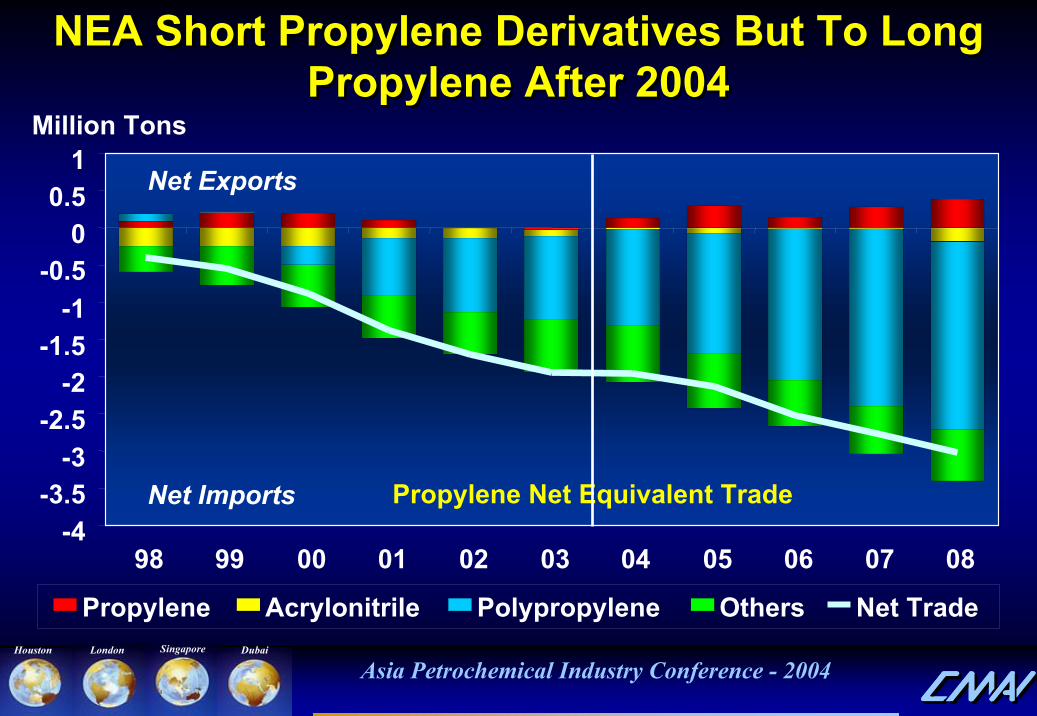

NEA Short Propylene Derivatives But To Long Propylene After 2004

NEA Short Propylene Derivatives But To Long Propylene After 2004

Propylene Acrylonitrile Polypropylene Others Net Trade

Million Tons

-4-3.5

-3-2.5

-2-1.5

-1-0.5

00.5

1

98 99 00 01 02 03 04 05 06 07 08

Net Exports

Net Imports Propylene Net Equivalent Trade

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

SE Asia Has Huge Propylene DeficitSE Asia Has Huge Propylene Deficit

Propylene Acrylonitrile Polypropylene Others Net Trade

-1.2-1

-0.8-0.6-0.4-0.2

00.20.40.6

98 99 00 01 02 03 04 05 06 07 08

Million Tons

Net Exports

Net Imports Propylene Net Equivalent Trade

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Why is China So Important Why is China So Important to Industry?to Industry?

• World’s fastest-growing market• Capturing 20-30% of investments• Becoming world’s factory

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

China’s Demand & Supply Growth Has Major Impact Globally

China’s Demand & Supply Growth Has Major Impact Globally

Global Cumulative Growth Demand

(2003 – 2013)PropyleneEthylene

SEA8%

RNEA4%

ROW73%

China15%

China24%

ROW61%

RNEA5%

SEA10%

Global Cumulative Capacity Expansion

(2003 – 2013)PropyleneEthylene

SEA8%

RNEA5%

ROW69%

China18%

China27%

ROW54%

RNEA8%

SEA11%

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

China Has Large Per Capita GDP Growth Potential

China Has Large Per Capita GDP Growth Potential

2003

China USA JapanJapan ThailandThailand S. KoreaS. Korea

Population, Mil 1,303 294 128 63 48

GDP*, Bil US$ 1,354 10,455 4,790 137 514

GDP* / Capita, US$ 1,040 35,570 37,500 2,180 10,700

• 2000 US$ Source: Getty Images

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Location 2003 % GDP

China’s Economic Growth Faster Than Rest of World

China’s Economic Growth Faster Than Rest of World

Annual Growth Rate (%)

– China– Taiwan– S. Korea– Japan– SEA Totals– India

– North America– Western Europe

• World

4.11.01.514.52.01.7

35.525.7100

2003 2003-2008

7.55.05.02.85.27.3

4.12.73.8

9.13.22.52.64.37.5

3.00.82.7

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

China Captures Foreign InvestmentChina Captures Foreign Investment

2002 Data

Mfg - 74%

Services - 12%

Real Estate/ Const. - 4%

Wholesale/ Retail - 4%

Agriculture/Food - 4%

Others - 2%

China - 8%ROW - 80%

Germany - 6%US - 5%

Japan - 1%

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Startup Status of New Ethylene Capacities and Expansions China / Taiwan

Formosa PC(Mai Liao: 1200 kta)

Company Startup TimingQilu PC 3Q ‘04BASF-YPC 1Q ’05BP-SECCO 2Q ’05Maoming PC Mid ’05Daqing PC 4Q ’06Lanzhou PC Mid ‘06Shell / CNOOC Mid ‘06Formosa 4Q ’06Fujian PC (ex-ExxonMobil) ~ ’10

Projects in Planning StageSinopec (800 kta, Wuhai) ~ ’10Zhenhai, Zhejiang (1,000 kta) ~ ’08-’10Shanghai 2nd Cracker (1,000 kta) ~ ’08-’10

BASF/Yangzhi PC(Nanjing; 600kta)

BP/SECCO(Shanghai; 900 kta)

Fujian PC / Aramco / Sinopec(Fujian; 800 kta)

Shell/CNOOC(Nanhai; 800 kta)

Maoming PCMaoming, +420 kta

Daqing PCDaiqing, +320 kta

Qilu PCShandong, +270 kta

Lanzhou PCGansu, +360 kta

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Ethylene Capacity Additions in China/ Taiwan CouldReach +7.5 Mil Tons by 2010

Qilu PC BASF-YPC BP-SECCOMaoming PC Daqing PC Lanzhou PCShell / CNOOC Formosa Fujian PC (Ex-ExxonMobil)Sinopec Zhenhai

0

2

4

6

8

3Q-04 1Q-05 2Q-05 3Q-05 4Q-05 1Q-06 2Q-06 3Q-06 4Q-06 2008 2009 2010

Mil Tons Per Year

5.7

7.5

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Sufficient Naphtha To Satisfy Ethylene Demand Growth?

Data suggest it is sufficient– +5.7 - 7.5 mil tons per year of NEA ethylene

capacity (by 2010) – Need +2.4 million barrels of crude / day – But Asia Pacific’s 20 million BPSD needs to be

expand by 12% (by end 2010)

Food for thought– Heavy fuels cracking and condensate splitters

opportunistic supply steps – Most big JV projects in China based on local

feedstocks• Some have feedstock flexibility

– Can port facilities handle imports of long haul ships ?

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Can China Handle Large Olefins Volume Imports?

Import Quantity Outlook— About 500 – 600 kta olefins import needed for

demand growth— Could grow to 600 - 900 kta if demand growth

is higher — Is this operationally feasible? Import facilities

could limit demand growth ?

Import Capability Overview— Currently can handle up 350 kta— New facilities raise capability to ~650 kta

• Dahua, Cangzhou (new SM terminal) in 2H ’04• Tianjin Dagu, Tianjin (VCM plant) in 1H ’05• Hebei Cangzhou (VCM plant) in 2H ‘05

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Re-Investment Cash Margins

Ethylene Margins Peak During ‘04-’06Ethylene Margins Peak During ‘04-’06

0

50

100

150

200

250

300

350

400

450

98 99 00 01 02 03 04 05 06 07 08

Dollars Per Ton

NAM Ethane NAM Light Naphtha WEP Naphtha SEA Naphtha

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Today’s Global Propylene MarketToday’s Global Propylene Market

SupplySteam Crackers

67%

Propane Dehydro.

2%

Others1%

FCC/Splitters30%

57.6 Million Metric Tons

Demand

Acrylonitrile10%

Propylene Oxide7%

Polypropylene64%

Others7%

Oxo Alcohols

8%

Cumene4%

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Today’s Asia Propylene MarketToday’s Asia Propylene Market

Supply

19.8 Million Metric Tons (in 2003)

DemandPolypropylene

68%

OxoAlcohols

7%

Cumene4%

PropyleneOxide

4%

Others5%

Acrylonitrile12%

Steam Crackers71%

FCC/Splitters

25%Dehydro4%

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Middle East / Asia Inter-Dependence

New M.E. Ethylene CapacityNew Asia Ethylene Demand New Asia Propylene Demand

New M.E. Propylene Capacity

3.0

2.0

1.0

0.0

1.0

2.0

3.0

4.0

1990 1995 2000 2005 2010

Million Metric Tons

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

How Will Propylene Supply Grow?

+3.4M Metathesis+1.8M PDH

+8.2M Steam Cracker

+9.3M Refinery

Million Metric Tons

50

55

60

65

70

75

80

85

2003 2004 2005 2006 2007 2008 2009 2010

2003 Base

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Where Is Global Propylene in the Future?

Where Is Global Propylene in the Future?

20102003

Steam Cracker59%

Refineries33% Dehydro

3%Metathesis & Others

5%

80.3 Million Metric Tons

Steam Cracker67%

Refineries30% Dehydro

2%Metathesis & Others

1%

57.6 Million Metric Tons

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

What is Asia Doing About Propylene Shortage?

Metathesis projects– Mitsui Chemicals, 140 kta propylene, middle ‘04

startup at Osaka, Japan – BP/ SECCO, 160 kta propylene, 2Q 2005 startup at

Shanghai, China– Others:

• Sumitomo Chemicals in Chiba, Japan• PCS, Singapore (200 kta; 2006)• Formosa PC, Kaohsiung, Taiwan (250 kta; end 2005)• Nippon Oil, Kawasaki Japan (150 kta; 2005)

Maximizing feedstock flexibility– Shell Nanhai cracker designed to crack heavy

feedstocks as well

Others – Deep Catalytic Cracking (Formosa PC)– Methanol-To-Olefins plant (Yihua Group planning to

build one in Inner Mongolia)

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Global Contract Prices Consistently Above Spot Prices in Long Market

• Spot prices are opportunistic sales

– In a long market, this is a last desperate seller’s price

• Pipeline suppliers committed capital to improve supply logistics

– Justifies a premium to spot price

• Asia contracts tied wholly to spot prices at disadvantage for sellers

– Buyers extract value from supply chain offering

• Dysfunctional pricing methodology

– 97% of contract business “influenced”by 3% of spot trade !

Ethylene Price Comparison*

300350400450500550600

USGC Europe Korea Taiwan Thailand

NEA Spot Price

NEA Spot Price

SEA Spot Price

Spot Price

$/ton

* 2002-2003 averages

Contract

Spot

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Global Contract Prices Consistently Below Spot Prices in Tight Market

* 2002-2003 averages

Contract

Spot

Propylene Price Comparison*

300350400450500550600

USGC Europe Korea Taiwan Thailand

Spot Price

Spot PriceNEASpotPrice

SE Asia Spot Price

NEASpotPrice

• In short markets, this is a last desperate buyer’s price

• Pipeline buyers give assurances of steady offtakes

– Justifies a discount to spot price

• Asia contracts tied wholly to spot prices at disadvantage to buyers

– Buyers not getting value for steady long term supply commitments

• Same dysfunctional methodology– Spot volumes represent around 2 % of

total Asia capacity (2003)

$/ton

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Summary• East Asia requires 900 kta of

monomer imports (from ‘03 –‘08)

• Demand and supply growth mainly in China & Taiwan

• China’s demand growth has large impact globally

• NE Asia to add 5.7 - 7.5 million tons of ethylene capacity by 2010

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

Summary• Issues arising

– Refining capacity needs to expand by about 12% by 2010 to supply the naphtha feedstock

– Chinese olefins import facilities could potentially limited demand growth

• Propylene supply tight and steam crackers loose “market share” in future

• Asia needs to price olefins based on longer term fundamentals

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai

A High Growth Region Needs Re-Investment EconomicsA High Growth Region Needs Re-Investment Economics

• CMAI to launch a new Asia Olefins Market Report in 3Q 2004

• Focus on more analysis of fundamental factors

– Cash costs– Derivatives’ margins– Dynamics of contract & spot

markets– Short term supply / demand– Arbitrage opportunities– International markets– Spot market

Fortnightly

Little Some Lots

Extend of Analysis

Market Report Frequency

Monthly

CMAI (Asia Olefins)

Company “I”Company “P”

CMAI (in MMR)

Company “D”

Companies “T”, “PC”, “N” etc

Weekly

None

Red - New ServiceWhite - Existing Service

Competitors’ Segmentation

Asia Petrochemical Industry Conference - 2004Houston London Singapore Dubai