Asian Equities in the Year of the Monkey - · PDF fileAsian Equities in the Year of the Monkey...

38

February 2016 Bill Maldonado Global CIO, Equities & CIO, Asia-Pacific Asian Equities in the Year of the Monkey Presentation only intended for professional investors as defined by MIFID.

Transcript of Asian Equities in the Year of the Monkey - · PDF fileAsian Equities in the Year of the Monkey...

February 2016

Bill Maldonado

Global CIO, Equities & CIO, Asia-Pacific

Asian Equities in the Year of the Monkey

Presentation only intended for professional investors as defined by MIFID.

2

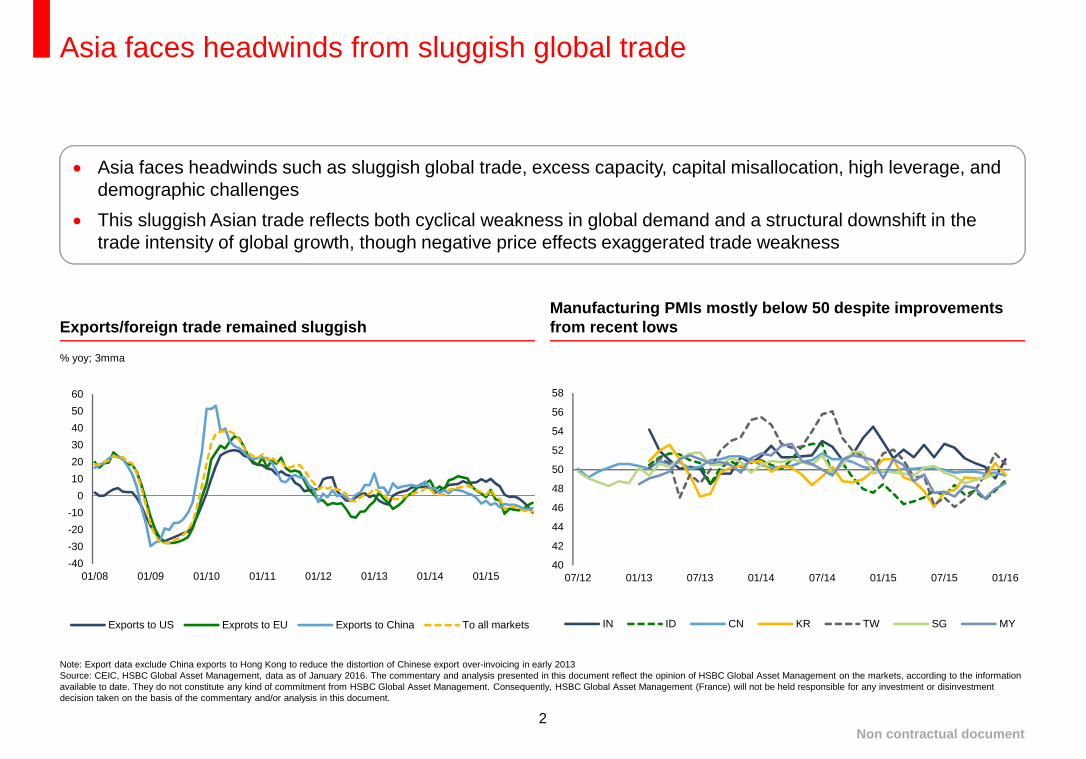

Asia faces headwinds from sluggish global trade

Note: Export data exclude China exports to Hong Kong to reduce the distortion of Chinese export over-invoicing in early 2013Source: CEIC, HSBC Global Asset Management, data as of January 2016. The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the informationavailable to date. They do not constitute any kind of commitment from HSBC Global Asset Management. Consequently, HSBC Global Asset Management (France) will not be held responsible for any investment or disinvestmentdecision taken on the basis of the commentary and/or analysis in this document.

40

42

44

46

48

50

52

54

56

58

07/12 01/13 07/13 01/14 07/14 01/15 07/15 01/16

IN ID CN KR TW SG MY

-40

-30

-20

-10

0

10

20

30

40

50

60

01/08 01/09 01/10 01/11 01/12 01/13 01/14 01/15

Exports to US Exprots to EU Exports to China To all markets

Asia faces headwinds such as sluggish global trade, excess capacity, capital misallocation, high leverage, anddemographic challenges

This sluggish Asian trade reflects both cyclical weakness in global demand and a structural downshift in thetrade intensity of global growth, though negative price effects exaggerated trade weakness

Exports/foreign trade remained sluggishManufacturing PMIs mostly below 50 despite improvementsfrom recent lows

% yoy; 3mma

Non contractual document

3

Relatively resilient services and consumption

Source: CEIC, HSBC Global Asset Management, data as of November 2015.The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment fromHSBC Global Asset Management. Consequently, HSBC Global Asset Management (France) will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in thisdocument.

-6

-4

-2

0

2

4

6

8

10

AU CN IN ID KR MY PH SG TW TH

% yoy

Manufacturing Services

Real GDP growth (1H15)

-60

-40

-20

0

20

40

60

80

100

120

01/08 01/09 01/10 01/11 01/12 01/13 01/14 01/15

CN IN ID MY PH TH KR

The services sector has help up relatively well as compared with manufacturing in most of Asia, barring a fewexceptions

Similarly, consumption has also proved to be more or less resilient with some high frequency data such as autosales recording a pick up in most Asian countries

Services sector growth held up relatively well Car sales also improved modestly in most countries

% yoy; 3mma

Non contractual document

4

External fundamentals in much better shape than prior to AFC

Source: CEIC, HSBC Global Asset Management, data as of September 2015.The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment fromHSBC Global Asset Management. Consequently, HSBC Global Asset Management (France) will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in thisdocument.

0

20

40

60

80

100

120

140

160

180

1990 1993 1996 1999 2002 2005 2008 2011 2014

CN IN ID KR MY PH TW TH

-15

-10

-5

0

5

10

15

CN HK IN ID KR MY PH TW TH VN

1994 1995 1996 2012 2013 2014

Most Asian countries now run current account surpluses as compared with deficits prior to the Asian financialcrisis (AFC)

Similarly, external debt-to-GDP ratio is lower now than prior to the AFC in most countries, proving that theseeconomies are less vulnerable at present

Current account surpluses vs deficits prior to AFC Lower external debt-to-GDP ratio

% of GDP% of GDP

Non contractual document

5

Inflation outlook remains benign

Source: CEIC, Bloomberg, HSBC Global Asset Management, data as of January 2016Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts, projections or targets. For illustrativepurpose only. The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitmentfrom HSBC Global Asset Management. Consequently, HSBC Global Asset Management (France) will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in thisdocument.

30

50

70

90

110

130

150

01/10 01/11 01/12 01/13 01/14 01/15 01/16

ID (6M) KR (12M) TH (12M) IN (12M) CN (3M) PH (12M)

Inflation remains low, even after accounting for some pass-through from currency weakness, amid soft globalcommodity prices, excess capacity and tepid domestic demand

Headline reading is likely to rise gradually, as the impact of the sharp decline in oil/commodity prices eases.However, inflation will likely remain benign

Inflation expectations are bottoming out in most countries

2010=100

Non contractual document

6

Meanwhile, real interest rates remain high in some countries

Note: real interest rates are deflated by 12-month forward CPI inflation expectationsSource: Bloomberg, CEIC, HSBC Global Asset Management, data as of December 2015. The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according tothe information available to date. They do not constitute any kind of commitment from HSBC Global Asset Management. Consequently, HSBC Global Asset Management (France) will not be held responsible for any investment ordisinvestment decision taken on the basis of the commentary and/or analysis in this document.

3M interbank rates

-4

-3

-2

-1

0

1

2

3

4

5

AU CH HK IN ID KR MY PH SG TW TH

End-2013 End-2014 End-2015

Currency depreciation helped loosen monetary conditions in some countries, but we think policymakers insome countries would still prefer a weaker currency

Despite monetary easing over the past 12 months across the region, real interest rates remained high on theback of disinflation. There is room for further easing in some countries

Real short-term interest rates remains high in some countries

% yoy

Non contractual document

What lies ahead?

8

Equity performance & rising rates – its about growth expectations

Source: Bloomberg, Nomura Strategy, HSBC Global Asset Management, as at December 2015. Past performance is not a reliable indicator of future performance

MSCI Asia ex Japan during 2004-06 Fed tightening

0

1

2

3

4

5

6

90

100

110

120

130

140

150

160

170

180

190

200

210

Jan-04 Jun-04 Nov-04 Apr-05 Sep-05 Feb-06 Jul-06 Dec-06 May-07

S&P 500 MSCI AC World MSCI AC Asia ex Japan Fed funds target rate (%, RHS)

Historical data shows that periods of rising interest rates are not necessarily bad for equities

Periods of inflation are often accompanied by strong growth, which is positive for equities

Non contractual document

9

Equity volatility is rising…

Source: Bloomberg, HSBC Global Asset Management, data as of 27 January 2016. Past performance is not a reliable indicator of future performance

0

10

20

30

40

50

60

70

80

90

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

MSCI Asia ex Japan 30-day annualised volatility 5-year average

Average in thefirst 5 years:

23%

Average in thesecond 5 years:15%

Equity volatility has increased in early 2016 but it remains low relative to its 10-year history

However macro risk indicators show that risk aversion is now above average and rising

Non contractual document

10

…But volatility creates opportunities in regional markets

Source: HSBC Global Asset Management, Bloomberg as of December 2015. Past performance is not a reliable indicator of future performance.

10

11

12

13

14

15

16

17

18

19

Dec-1

2

Feb-1

3

Ap

r-13

Jun

-13

Au

g-1

3

Oct

-13

Dec-1

3

Feb-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct

-14

Dec-1

4

Feb-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct

-15

Dec-1

5

0.4

0.45

0.5

0.55

0.6

Dec-1

2

Feb-1

3

Ap

r-13

Jun

-13

Au

g-1

3

Oct

-13

Dec-1

3

Feb-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct

-14

Dec-1

4

Feb-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct

-15

Dec-1

5

0.3

0.35

0.4

0.45

0.5

0.55

0.6

0.65

Dec-1

2

Feb-1

3

Ap

r-13

Jun

-13

Au

g-1

3

Oct

-13

Dec-1

3

Feb-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct

-14

Dec-1

4

Feb-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct

-15

Dec-1

5

8

8.5

9

9.5

10

10.5

11

11.5

12

12.5

Dec-1

2

Feb-1

3

Ap

r-13

Jun

-13

Au

g-1

3

Oct

-13

Dec-1

3

Feb-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct

-14

Dec-1

4

Feb-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct

-15

Dec-1

5

MSCI India MSCI Korea

MSCI Indonesia MSCI Taiwan

(in USD) (in USD)

(in USD) (in USD)

Non contractual document

11

Asian equity valuations still a big draw

Asia ex-Japan equity valuations are now at levels last seen during the global financial crisis

However, it’s hard to argue that the region’s fundamentals justify such low valuations

On a sector level, cyclicals appear to be very attractive when compared to defensive stocks

Asia ex-Japan equity valuations close to previous lows Cyclicals vs defensives P/B ratio gap widens

Price-to-book ratio

0.5

1.0

1.5

2.0

2.5

3.0

Dec-95 Dec-98 Dec-01 Dec-04 Dec-07 Dec-10 Dec-13

Asia ex-JP - Trailing PB

1.24xnow

1.23x inFeb 090.94x in

Aug 98

1.47x inJan 14

1.22x inMar 03

1.28x on24 Aug

1.19x inSep 01

12-month return:114%

12-month return:14%

12-month return:72%

12-month return:84%

Price-to-book ratio gap

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

Asia ex-JP Trailing PB - Cyclicals less Defensives

-0.74 Dec 2008

-0.59xnow

-0.82x Jul 2015

Non contractual document

Source: Credit Suisse, as of January 2016. Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet suchforecasts, projections or targets. For illustrative purpose only. The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the information available todate. They do not constitute any kind of commitment from HSBC Global Asset Management. Consequently, HSBC Global Asset Management (France) will not be held responsible for any investment or disinvestment decision taken onthe basis of the commentary and/or analysis in this document. Past performance is not a reliable indicator of future performance.

12

Valuations differ by sector – stock selection is key

Source: Factset, I/B/E/S, MSCI, Gloldman Sachs Global Investment Research as of January 2016. The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets,according to the information available to date. They do not constitute any kind of commitment from HSBC Global Asset Management. Consequently, HSBC Global Asset Management (France) will not be held responsible for anyinvestment or disinvestment decision taken on the basis of the commentary and/or analysis in this document. Past performance is not a reliable indicator of future performance.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

HealthC

are

Cons

Sta

p

Tele

com

Info

Tech

Insu

rance

Div

Fin

s

Cons

Dis

c

Indust

rials

Util

itie

s

Ba

nks

Mate

rials

En

erg

y

Pro

pert

y

Current PB Valuations

0.0

5.0

10.0

15.0

20.0

25.0

30.0

HealthC

are

Cons

Sta

p

Mate

rials

Tele

com

Indust

rials

Info

Tech

Insu

rance

Util

itie

s

En

erg

y

Pro

pert

y

Div

Fin

s

Cons

Dis

c

Ba

nks

Current PE valuation

Most sectors trading cheaply on a PB basis (ignoring the cyclicality of earnings)

We are UW expensive healthcare and staples stocks

We are OW property and consumer discretionary, which look cheap on both PE and PB basis

Too early to be investing into materials as earnings are still bottoming

Financials look cheap in terms of cyclical earnings

Asia Pacific ex Japan sector-wise 12-month forward PE/PB relatively to historical high/low

Non contractual document

13

Long term risk/return expectations point to Asian equities

Note: Global Fixed Income assets are shown hedged to USD. Local EM debt, Equity and Real Estate assets are shown unhedgedSource: HSBC Global Asset Management as at end December 2015. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way.

Cash US TIPSUK IL GiltsUS Tsy

UK GiltsGerman BundsJapan JGBs

US Corp

US HY

GBP CorpEUR Corp

EM Sovs USD

EM Credit US Equity

UK EquityJapan Equity

EM Equity

AC World Equity

Asia ex Japan Equity

Euro ABS

US 5y TsyUK 5y Gilts

Local EM Debt

Europe x UK Equity (H)UK Equity (H)

Japan Equity (H)

Canada Equity

Canada Equity (H)

Asia IG Credit

Asia HY Corporate

Global HY

0

1

2

3

4

5

6

7

8

9

10

0 2 4 6 8 10 12 14 16 18 20 22 24 26

Expected Volatility (%)

Sharpe Ratio = 0.25

Sharpe Ratio = 0.10

Expected Asset Class Returns (%, Nominal, USD)

In 2016, equities are the preferred asset class, especially over government bonds and cash

Current pecking order of asset classes

Non contractual document

14

SOE reform

Fiscal/tax reform

Financial reform

Capital market liberalisation/RMB internationalisation

Household registration system (Hukou) reform

Land reform

Relaxation of one-child policy

“One Belt, One Road” and Free-Trade Zones

China: Rebalancing the economy for sustainable growth

Preference for Asia anchored in fundamentals (ie reform agenda)

Source: HSBC Global Asset Management, data as of September 2015

Goods and services tax (GST)

Labour market reform

Diesel pricing deregulation

Coal and mining

Inflation-targeting/new monetary policy framework

Government transparency and ease of doing business

Aadhar/UID

“Make in India” and “Digital India”

India: Voted for change with strongest mandate in 30 years

Fiscal/fuel subsidy reform

Increasing spending on infrastructure

Increasing spending on health and education

Anti-corruption and better governance

Institutional reform to improve efficiency of SOEs

Reducing bureaucracy for business start-ups

Agriculture/rural development (including land reform)

Improving financial inclusion

Indonesia: Voted for redistribution and accelerated reform

Tax measures to encourage corporates to pay moredividends, raise wage or increase capex

Overhaul of the inflexible labour market

Regulatory reforms

Reform of the public pension system

Reform of the educational system

Nurturing the service sector

Economic democratisation (reform of chaebols)

Korea: Restructuring for stronger fundamentals

Non contractual document

15

Key drivers for Asian equities

Driver Outlook Impact for Equities

Monetary policy/higher interest rates Fed to normalize rates only as economy strengthens; remains data driven 0/+

Oil prices Oil prices now below long term fair value forecasts However, oversupply concerns may add to near term downward pressure Lower oil prices support consumer spending and corporate profit

+

Growth & inflation Inflation appears to be contained across the Asian region Current growth rate is unlikely to drive up inflation expectations in the near future

+

Macro uncertainty & geopolitical risk Uncertainty on China growth: hard landing unlikely despite slowing momentum Geopolitical risk in Europe, Middle East and China Sea unhelpful

-

Valuations Equity valuations are generally more attractive in Asia ex Japan vs. the developed world Defensive stocks are over valued; cyclical stocks remain attractive Earnings growth remains subdued but scope for upside surprises

+

Fragile Equilibrium Moderate growth/inflation mix likely to continue Periodic scares likely to trigger bouts of market volatility No cause for despondency or euphoria

0/+

Source: HSBC Global Asset ManagementFor illustrative purposes only, and should not be construed as a recommendation to buy or sell any investment. The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on themarkets, according to the information available to date. They do not constitute any kind of commitment from HSBC Global Asset Management. Consequently, HSBC Global Asset Management (France) will not be held responsible forany investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document.

Non contractual document

Where are the investment opportunities?

17

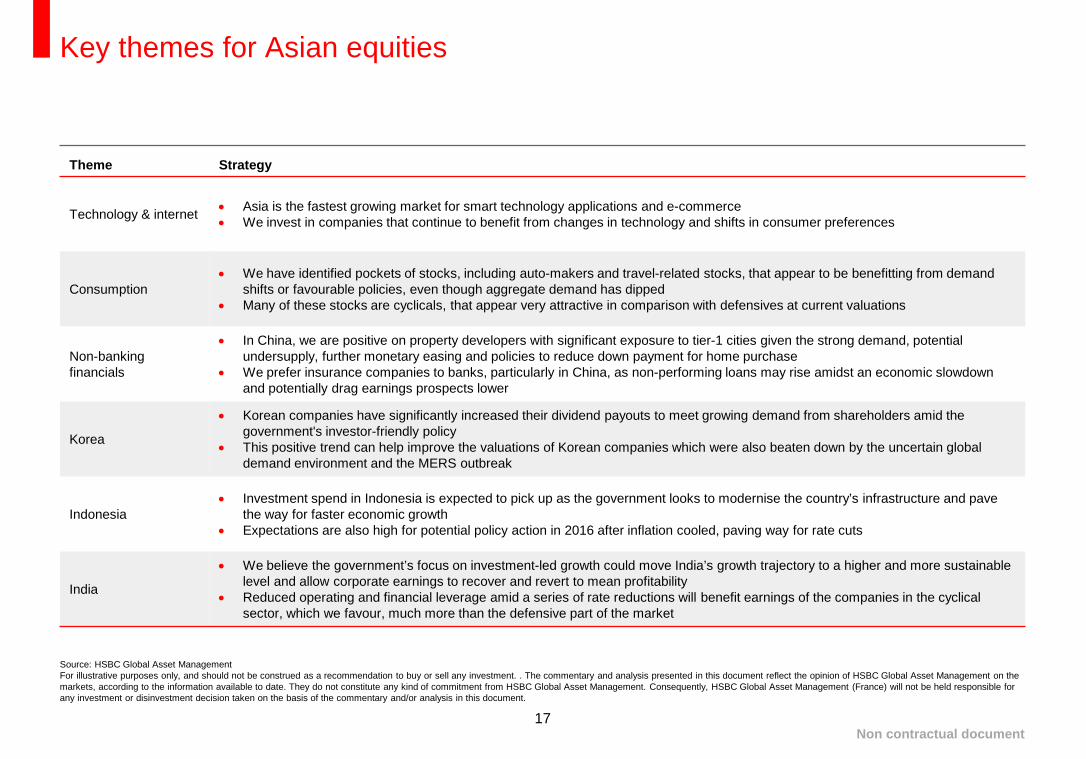

Key themes for Asian equities

Theme Strategy

Technology & internet Asia is the fastest growing market for smart technology applications and e-commerce We invest in companies that continue to benefit from changes in technology and shifts in consumer preferences

Consumption We have identified pockets of stocks, including auto-makers and travel-related stocks, that appear to be benefitting from demand

shifts or favourable policies, even though aggregate demand has dipped Many of these stocks are cyclicals, that appear very attractive in comparison with defensives at current valuations

Non-bankingfinancials

In China, we are positive on property developers with significant exposure to tier-1 cities given the strong demand, potentialundersupply, further monetary easing and policies to reduce down payment for home purchase

We prefer insurance companies to banks, particularly in China, as non-performing loans may rise amidst an economic slowdownand potentially drag earnings prospects lower

Korea

Korean companies have significantly increased their dividend payouts to meet growing demand from shareholders amid thegovernment's investor-friendly policy

This positive trend can help improve the valuations of Korean companies which were also beaten down by the uncertain globaldemand environment and the MERS outbreak

Indonesia Investment spend in Indonesia is expected to pick up as the government looks to modernise the country’s infrastructure and pave

the way for faster economic growth Expectations are also high for potential policy action in 2016 after inflation cooled, paving way for rate cuts

India

We believe the government’s focus on investment-led growth could move India’s growth trajectory to a higher and more sustainablelevel and allow corporate earnings to recover and revert to mean profitability

Reduced operating and financial leverage amid a series of rate reductions will benefit earnings of the companies in the cyclicalsector, which we favour, much more than the defensive part of the market

Source: HSBC Global Asset ManagementFor illustrative purposes only, and should not be construed as a recommendation to buy or sell any investment. . The commentary and analysis presented in this document reflect the opinion of HSBC Global Asset Management on themarkets, according to the information available to date. They do not constitute any kind of commitment from HSBC Global Asset Management. Consequently, HSBC Global Asset Management (France) will not be held responsible forany investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document.

Non contractual document

18

Investment opportunityTechnology-enabled consumption: China

Source: CEIC, HSBC Global Asset Management, data as of September 2015. For illustrative purposes only and should not be construed as a recommendation to buy or sell any investment.

0

2

4

6

8

10

12

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2007 2008 2009 2010 2011 2012 2013 2014

E-commerce (retail sales), rhs E-commerce (B2B), lhs

0

10

20

30

40

50

60

70

0

100

200

300

400

500

600

700

800

2006 2008 2010 2012 2014

No of Internet user (rural), lhs No of Internet user (urban), lhs

Internet penetration rate (rural), rhs Internet penetration rate (urban), rhs

In China’s 12th Five-Year Plan (2011-2015) includes plans to make China a global e-commerce leader

Smart technology and e-commerce are re-shaping the ways Chinese consumers purchase goods and services

The number of Internet users in China has grown rapidly, although the Internet penetration is still below 50%

The e-commerce market is becoming an increasinglyimportant channel for consumption The Internet market has grown rapidly

CNYtrn CNYtrn Million persons %

Non contractual document

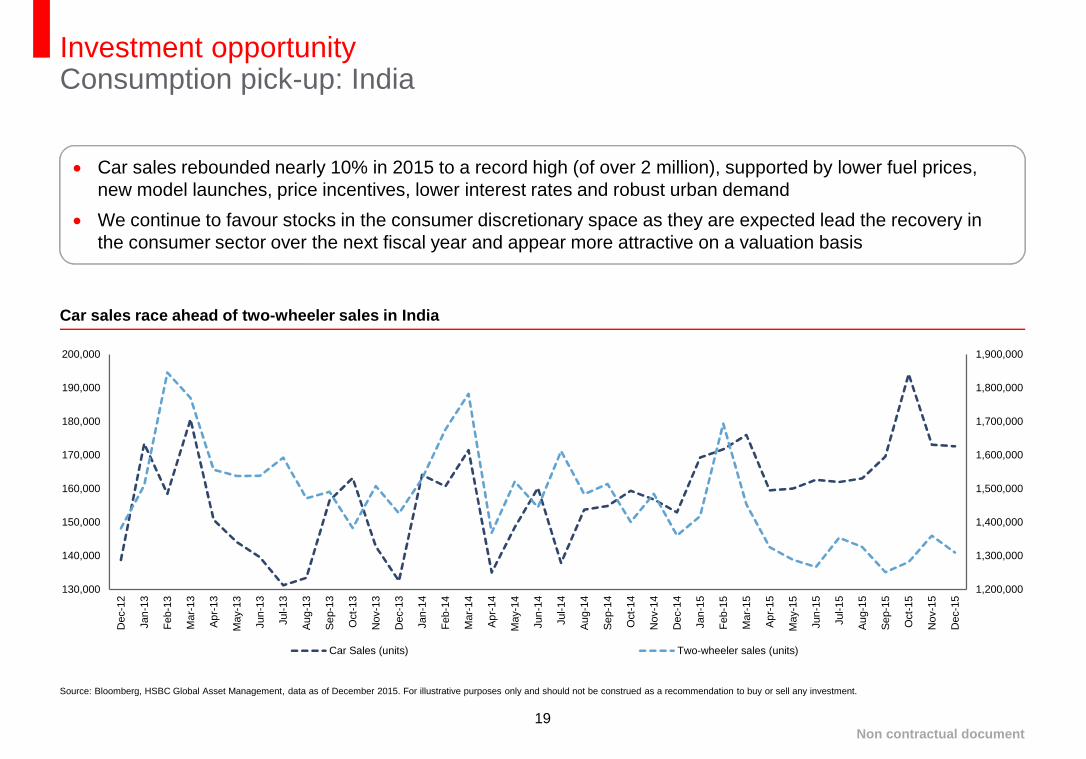

19

Investment opportunityConsumption pick-up: India

Source: Bloomberg, HSBC Global Asset Management, data as of December 2015. For illustrative purposes only and should not be construed as a recommendation to buy or sell any investment.

1,200,000

1,300,000

1,400,000

1,500,000

1,600,000

1,700,000

1,800,000

1,900,000

130,000

140,000

150,000

160,000

170,000

180,000

190,000

200,000

Dec-1

2

Jan

-13

Feb-1

3

Mar-

13

Ap

r-13

May-

13

Jun

-13

Jul-1

3

Au

g-1

3

Se

p-1

3

Oct

-13

Nov-1

3

Dec-1

3

Jan

-14

Feb-1

4

Mar-

14

Ap

r-14

May-

14

Jun

-14

Jul-1

4

Au

g-1

4

Se

p-1

4

Oct

-14

Nov-1

4

Dec-1

4

Jan

-15

Feb-1

5

Mar-

15

Ap

r-15

May-

15

Jun

-15

Jul-1

5

Au

g-1

5

Se

p-1

5

Oct

-15

Nov-1

5

Dec-1

5

Car Sales (units) Two-wheeler sales (units)

Car sales rebounded nearly 10% in 2015 to a record high (of over 2 million), supported by lower fuel prices,new model launches, price incentives, lower interest rates and robust urban demand

We continue to favour stocks in the consumer discretionary space as they are expected lead the recovery inthe consumer sector over the next fiscal year and appear more attractive on a valuation basis

Car sales race ahead of two-wheeler sales in India

Non contractual document

20

Investment opportunityReal Estate: Selective shortage in China

Source: Soufun, HSBC Global Asset Management, data as of November 2015. Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC accepts noliability for any failure to meet such forecasts, projections or targets. For illustrative purposes only and should not be construed as a recommendation to buy or sell any investment.

Great divergence among different tiers in the Chinese property market

We expect undersupply in tier-1 cities in 2016

Demand supply imbalance has lead to double digit price growth in tier 1 cities in 2015

Demand/supply ratioCumulative ASP change since Jun-2005

Year to November (based on Soufun data)

Tier 1 17.4%

Tier 2 6.9%

Tier 3 -2%

Non contractual document

21

Investment opportunityKorea: Improved dividend payouts, inexpensive valuations

Source: Credit Suisse as of December 2015Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts, projections or targets. For illustrative

purposes only and should not be construed as a recommendation to buy or sell any investment.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

Chin

a

Hong

Kon

g

India

Indonesi

a

Ko

rea

Mala

ysia

Ph

ilippin

es

Sin

ga

pore

Taiw

an

Thaila

nd

Asia

ex

Japan

2013 2014 2015e

-5%

5%

15%

25%

35%

45%

55%

65%

Chin

a

Hong

Kon

g

India

Indonesi

a

Ko

rea

Mala

ysia

Ph

ilippin

es

Sin

ga

pore

Taiw

an

Thaila

nd

Asia

ex

Japan

2013 2014 2015e

Dividend payout ratios have increased materially since 2013 and firms are conducting more share buy backs

Key driver of this change is agitation from Korea’s National Pension Service (NPS) which owns about 7% ofKorea’s equity market

This is a positive trend and re-rating catalyst for the market, which is trading at relatively low valuations

Korea’s dividend yield inches closer to regional rivals Dividend payout rose nearly 60% since 2013

Non contractual document

22

Investment opportunityIndonesia: Increased capex spending, rate cuts

Source: CEIC, Morgan Stanley as of December 2015. For illustrative purposes only and should not be construed as a recommendation to buy or sell any investment.

Capex spend on the rise as government looks to modernise the infrastructure and pave the way for fastereconomic growth

Further policy action expected in 2016 after Bank of Indonesia cut rates in January on moderating inflation

Government spending on the rise

Non contractual document

23

Investment opportunityIndia: Cyclical recovery-led growth

Source: Morgan Stanley as of December 2015. For illustrative purposes only and should not be construed as a recommendation to buy or sell any investment.

Industrial production Passenger car sales

Pick-up in high frequency data, including industrial production, consumption and capex, indicate that a cyclicalrecovery is underway, albeit at a slower pace than previously anticipated

Corporate earnings are expected to bounce back off their low base amid the ongoing growth recovery, reducedreal rates and other favourable macro economic factors that have put India in an advantageous position vis-à-vis other emerging markets

Improved high frequency data suggests recovery in domestic demand

Non contractual document

Focus on Asia ex Japan Small Caps

25

Asia ex-Japan small caps outperform the broad index over time…

Small caps tend to outperform in Asia over the long term

Asset class can underperform the broad index significantly in periods of extreme crisis

– Eg 1997 Asian financial crisis, 2000 bursting technology bubble, 2008 Global financial crisis

However, small caps are not just a bull market investment

Source: Bloomberg, data as at end-January 2016. For illustrative purposes only and does not constitute any investment recommendation. Past performance is not indicative of future performance

50

100

150

200

250

300

350

400

Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

MSCI Asia ex Japan MSCI Asia ex Japan Small Cap

Performance of small cap index vs broad index since the technology bubble, indexed at 100

Non contractual document

26

In 2015, Asia ex Japan small caps outperformed their large cap peers, despite the challenging investmentenvironment

The outperformance also highlights the diversification benefits of including Asia ex Japan small caps in aninvestor's broader portfolio

…and periodically amidst heightened volatility

Source: Bloomberg, data as of December 2015. For illustrative purposes only and does not constitute any investment recommendation. Past performance is not indicative of future performance

80

85

90

95

100

105

110

115

120

Dec-14 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15

MSCI Asia ex Japan Small Cap MSCI Asia ex Japan

Small caps beat out large caps in 2015

Non contractual document

27

Small cap market is much more diversified than large caps, where financials account for 30% of holdings

Structural opportunities emerging for sectors that used to be small – better access via small caps

0%

5%

10%

15%

20%

25%

30%

35%

Fin

anci

als

Consum

er

Dis

cre

tiona

ry

Info

rmatio

nT

ech

no

logy

Indust

rials

Healthca

re

Mate

rials

Consum

er

Sta

ple

s

Util

itie

s

Energ

y

Tele

com

munic

atio

nS

erv

ices

MSCI AC Asia ex Japan Small Cap Index MSCI AC Asia ex Japan Index

Outperformance is led by greater diversificationSmall cap investing is all about stock selection

Source: HSBC Global Asset Management, data as of end-December 2015. For illustrative purposes only and does not constitute any investment recommendation in the above-mentioned sectors or countries

Small cap has greater exposure to “New Asia” sectors

Non contractual document

28

Small cap investing is all about stock selectionGreat inefficiency = great opportunity

Notes: Small caps are defined as stocks with market cap>$100 million but <$2 billion1. Stock with 3 or more analysts covering it.Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts, projections or targets. For illustrativepurpose onlySource: Macquarie Research, data as of July 2015. For illustrative purposes only and does not constitute any investment recommendation. Past performance is not indicative of future performance

Activecoverage =

73.6%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Asia ex Japan Europe USA

Total no. small cap stocks Active sell-side coverage*

Activecoverage =

54.2%

Activecoverage =

34.6%

No. of stocks

Brokerage firms often emphasise large cap over small cap research

This lack of coverage is particularly stark in Asia and this creates inefficiencies – and opportunities

Fundamental research by experienced analysts is crucial

Small cap investing is about identifying and investing early in attractive companies

Lack of sell-side analyst coverage on Asia ex Japan small caps

1

Non contractual document

29

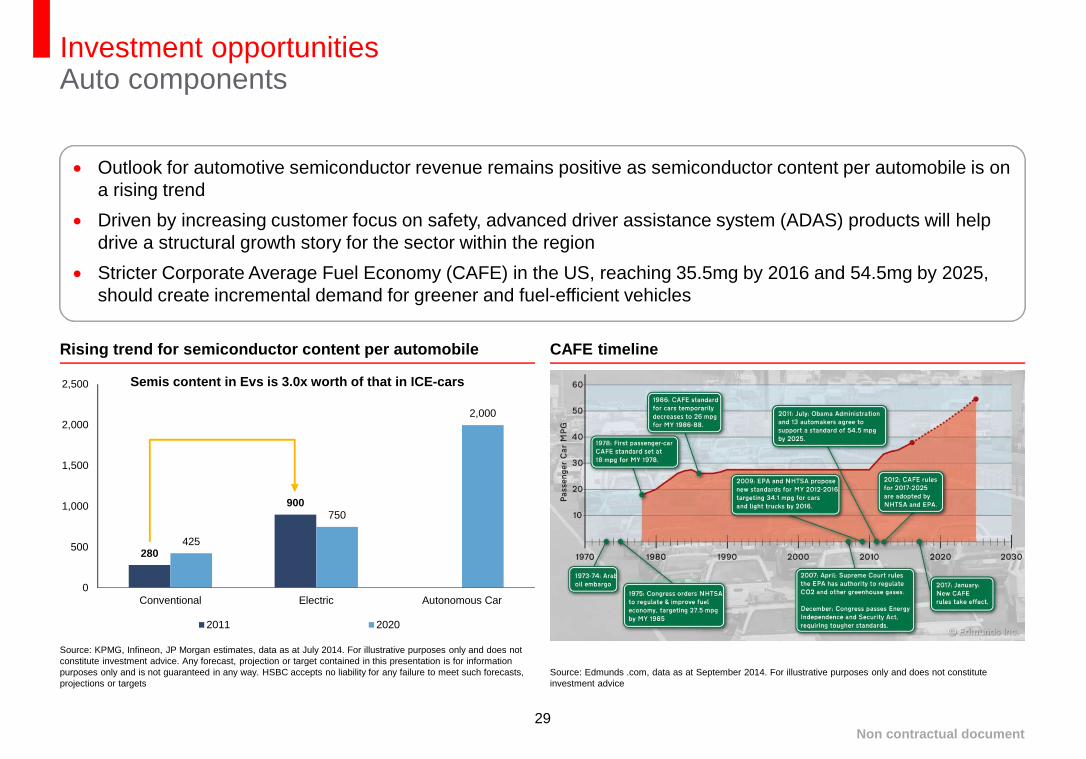

Outlook for automotive semiconductor revenue remains positive as semiconductor content per automobile is ona rising trend

Driven by increasing customer focus on safety, advanced driver assistance system (ADAS) products will helpdrive a structural growth story for the sector within the region

Stricter Corporate Average Fuel Economy (CAFE) in the US, reaching 35.5mg by 2016 and 54.5mg by 2025,should create incremental demand for greener and fuel-efficient vehicles

Investment opportunitiesAuto components

Source: Edmunds .com, data as at September 2014. For illustrative purposes only and does not constituteinvestment advice

Source: KPMG, Infineon, JP Morgan estimates, data as at July 2014. For illustrative purposes only and does notconstitute investment advice. Any forecast, projection or target contained in this presentation is for informationpurposes only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts,projections or targets

Rising trend for semiconductor content per automobile CAFE timeline

280

900

425

750

2,000

0

500

1,000

1,500

2,000

2,500

Conventional Electric Autonomous Car

2011 2020

Semis content in Evs is 3.0x worth of that in ICE-cars

Non contractual document

30

Even as China’s exports have cooled amid rising labour costs, countries like Vietnam, which benefit from amuch lower cost base, have expanded their share of apparel, footwear, textiles imports to the US

Vietnam will benefit from the Trans Pacific Partnership (TPP), with the US being a main drawcard in themultilateral agreement

Moreover Vietnam also has free trade agreements with Japan and the EU which provide a competitiveadvantage

Investment opportunitiesGlobal manufacturing hub: Vietnam

Source: International Trade Administration data as of October 2015. For illustrative purposes only and does notconstitute investment advice

Source: International Trade Administration data as of December 2015. For illustrative purposes only and does notconstitute investment advice.

10% 10% 10%9% 9% 8% 8%

10%12%

14%

22%

26%

31%32%

37%39%

38% 38% 37% 36% 36%

0% 0% 0% 0% 0% 0% 0%2%

4% 4% 4% 4%6%

7% 8% 8% 9% 9% 10%11% 12%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Share of US imports of apparel and textile

China (%) Vietnam (%)

66% 68% 69%71% 72% 73% 74%

76% 76%74%

72%69%

66%64%

1% 2% 3% 4% 5% 5% 6% 7% 8% 9% 10% 12%14%

16%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Share of US imports of footwear

China (%) Vietnam (%)

Vietnam’s increasing foothold in apparel and footwear imports

Non contractual document

31

Increased focus on environment – greater transparency on pollution at a provincial level

To meet PM2.5 reduction target by 2020

– Clean energies should rise to 27% of total consumption by 2020 (2012-13%)

– Annual coal consumption growth needs to be cut to 0.9%

UK experience: halved coal consumption and halved air pollution from 1950s-70s

Favorable policies to encourage faster capacity installation for solar (solar farm, BIPV) and wind farm operators

Investment opportunityAlternative energy: China

Source: BofA Merrill Lynch Global Research, data as at December 2015. For illustrative purpose only and does not constitute any investment recommendation in the above-mentioned sectorsAny forecast, projection or target contained in this presentation is for information purpose only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts, projections or targets

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2011 2012 2013 2014 2015 2016e 2017e 2018e 2019e 2020e

Thermal Hydro Nuclear Wind Solar Others/Biomass

China’s clean energy generation capacity on the rise

Non contractual document

32

Indian government has announced massive capacity addition targets – Scale up to 100,000 MW solar powerand 60,000 MW wind energy capacity by 2022

If achieved, this will put India among the top two renewable energy markets in the world, alongside China

Government plans to implement large-scale and small-scale solar and wind energy projects throughout thecountry through competitive auctions

Investment opportunityAlternative energy: India

Source: Deutsche Bank data as at December 2015. For illustrative purpose only and does not constitute any investment recommendation in the above-mentioned sectorsAny forecast, projection or target contained in this presentation is for information purpose only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts, projections or targets

24,376

60,000

4,347

100,000

0

20,000

40,000

60,000

80,000

100,000

120,000

Nov 15 2022 end

Wind Solar

CAGR – 14%

CAGR – 57%

E

India to step up alternative energy generation

Mega Watts (MW)

Non contractual document

33

Over the last two years the number of projects awarded has picked up in urban infrastructure segments suchas roads, buildings and metro projects

Given Modi government’s thrust on the infrastructure investment, we expect capex on urban infrastructureprojects to continue expanding

Investment opportunityUrban construction: India

Note:1. Y-o-y compares March-December 2015 with corresponding period of 2014Source: Emkay Research, data as at December 2015. For illustrative purpose only and does not constitute any investment recommendation in the above-mentioned sectorsAny forecast, projection or target contained in this presentation is for information purpose only and is not guaranteed in any way. HSBC accepts no liability for any failure to meet such forecasts, projections or targets. The commentaryand analysis presented in this document reflect the opinion of HSBC Global Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Global AssetManagement. Consequently, HSBC Global Asset Management (France) will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document.

Road projects awarded up 152.5% y-o-y1

Pick-up in National Highways Authority of India (NHAI)projects awarded

4,663

1,7351,234

643

3,360

5,058

6,380

1,1161,436

3,447

2,721

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 FY 14 FY 15 YTDFY 16

Length awarded

(Km)

Non contractual document

34

Investment opportunityValuations represent good buying opportunities

Note: SD= standard deviationSource: Bloomberg, HSBC Global Asset Management, data as of February 2016. For illustrative purposes only and does not constitute any investment recommendation. Past performance is not indicative of future performance

MSCI Taiwan small cap price-to-bookMSCI Indonesia small cap price-to-book

MSCI Singapore small cap price-to-book

Current valuations of some small cap markets are close to or lower than their historical averages

+1SD = 1.8x

Mean = 1.5x

-1SD = 1.2x

+1SD = 1.5x

-1SD = 1.2x

Mean = 1.3x

+1SD = 1.3x

Mean = 1.1x

-1SD = 0.95x

0.7

0.9

1.1

1.3

1.5

1.7

1.9

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Non contractual document

35

Investment opportunityCompelling valuations of HK/China equities

Source: Bloomberg. HSBC Global Asset Management . Data as of end January 2016. Past performance is not indicative of future performance.

0.58

1.41

1.22

0.83

1.06

0.87

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

P/B Average +1 SD -1SD

0.62

1.71

0.77

1.51

0.95

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

P/B Average +1SD -1SD

HK-listed Chinese and Hong Kong small caps are trading at very inexpensive valuations relative to their ownhistory and many of their larger cap counterparts (MSCI China – 1.2x P/B, MSCI Hong Kong – 1.05x P/B)

As small caps listed in Hong Kong form a very diversified universe of stocks, we can gain exposure tointeresting growth stories in China without buying into the A-share market

MSCI China Small Cap Price-to-book (x) MSCI Hong Kong Small Cap Price-to-book (x)

Non contractual document

Key risks and disclosures

37

Key risks

Investor sentiment may be susceptible to macro concerns

Investor should be reminded that investment in some of the developing Asian countries may involve specialconsiderations and risks. Below could affect adversely the economies of such countries or the value of theinvestment

– Political changes

– Government regulation

– Social instability

– Diplomatic development

– Global economic development etc

Emerging markets can be significantly more volatile than developed markets, so that the value of investmentsmay be subject to larger fluctuations

Currency movement and market condition may affect the value of investments

Non contractual document

38

Important information

This presentation is distributed by HSBC Global Asset Management (France) and is only intended for professional investors as defined by MIFID.The information contained herein is subject to change without notice. Allnon-authorised reproduction or use of this commentary and analysis will be the responsibility of the user and will be likely to lead to legal proceedings. This document has no contractual value and is not by any meansintended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The commentary and analysis presented in this document reflectthe opinion of HSBC Global Asset Management on the markets, according to the information available to date. They do not constitute any kind of commitment from HSBC Global Asset Management. Consequently,HSBC Global Asset Management (France) will not be held responsible for any investment or disinvestment decision taken on the basis of the commentary and/or analysis in this document. Any forecast, projection ortarget where provided is indicative only and is not guaranteed in any way. HSBC Global Asset Management (France) accepts no liability for any failure to meet such forecast, projection or target.

All data from HSBC Global Asset Management (France) unless otherwise specified. Any third party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

The performance figures displayed in the document relate to the past and past performance should not be seen as an indication of future returns. It is important to remember that the value of investments and any incomefrom them can go down as well as up and is not guaranteed. Capital is not guaranteed. Where overseas investments are held the rate of exchange may cause the value to go down as well as up. Investments inemerging markets are by their nature higher risk and potentially more volatile than those inherent in established markets. Funds that invest in securities listed on a stock exchange or market could be affected by generalchanges in the stock market. The value of investments can go down as well as up due to equity markets movements. Small and mid cap markets are occasionally affected by a temporary lack of liquidity; they may besubject to greater fluctuations than large cap markets and be more difficult for the fund manager to buy or sell.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used to create any financial instruments or products or any indices.The MSCI information is provided on an 'as is' basis and the user of this information assumes the entire risk of any use it may make or permit to be made of this information. Neither MSCI, any of its affiliates or any otherperson involved in or related to compiling, computing or creating the MSCI information (collectively, the 'MSCI Parties') makes any express or implied warranties or representations with respect to such information or theresults to be obtained by the use thereof, and the MSCI Parties hereby expressly disclaim all warranties (including, without limitation, all warranties of originality, accuracy, completeness, timeliness, non-infringement,merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental,punitive, consequential or any other damages (including, without limitation, lost profits) even if notified of, or if it might otherwise have anticipated, the possibility of such damages.

Important information for Luxembourg investors: HSBC entities in Luxembourg are regulated and authorised by the Commission de Surveillance du Secteur Financier (CSSF).

Important information for Swiss investorsThis presentation is intended exclusively towards qualified investors in the meaning of Art. 10 para 3, 3bis and 3ter of the Federal Collective Investment SchemesAct (CISA).

The above document has been approved for distribution/issue by the following entities :

HSBC Global Asset Management (France)

421 345 489 RCS Nanterre. Portfolio management company authorised by the French regulatory authority AMF (no. GP99026) with capital of 8.050.320 euros. Postal address: 75419 Paris cedex 08,France.Offices: Immeuble Coeur Défense, 110, esplanade du Général Charles de Gaulle, 92400 Courbevoie - La Défense 4 . (Website: www.assetmanagement.hsbc.com/fr).

HSBC Global Asset Management (Switzerland) Limited

Bederstrasse 49, P.O. Box, CH-8027 Zurich, Switzerland (Website: www.assetmanagement.hsbc.com/ch)

Non contractual document, updated in February 2016 - AMFR_Ext_89_2016

Copyright © 2016. HSBC Global Asset Management (France). All rights reserved.