ASIAN DEVELOPMENT BANK RRP: IND 29473 - adb.org – National Hydroelectric Power Corporation NTPC...

102

ASIAN DEVELOPMENT BANK RRP: IND 29473 REPORT AND RECOMMENDATION OF THE PRESIDENT TO THE BOARD OF DIRECTORS ON PROPOSED LOANS TO INDIA FOR THE MADHYA PRADESH POWER SECTOR DEVELOPMENT PROGRAM November 2001

-

Upload

hoangxuyen -

Category

Documents

-

view

224 -

download

2

Transcript of ASIAN DEVELOPMENT BANK RRP: IND 29473 - adb.org – National Hydroelectric Power Corporation NTPC...

ASIAN DEVELOPMENT BANK RRP: IND 29473

REPORT AND RECOMMENDATION

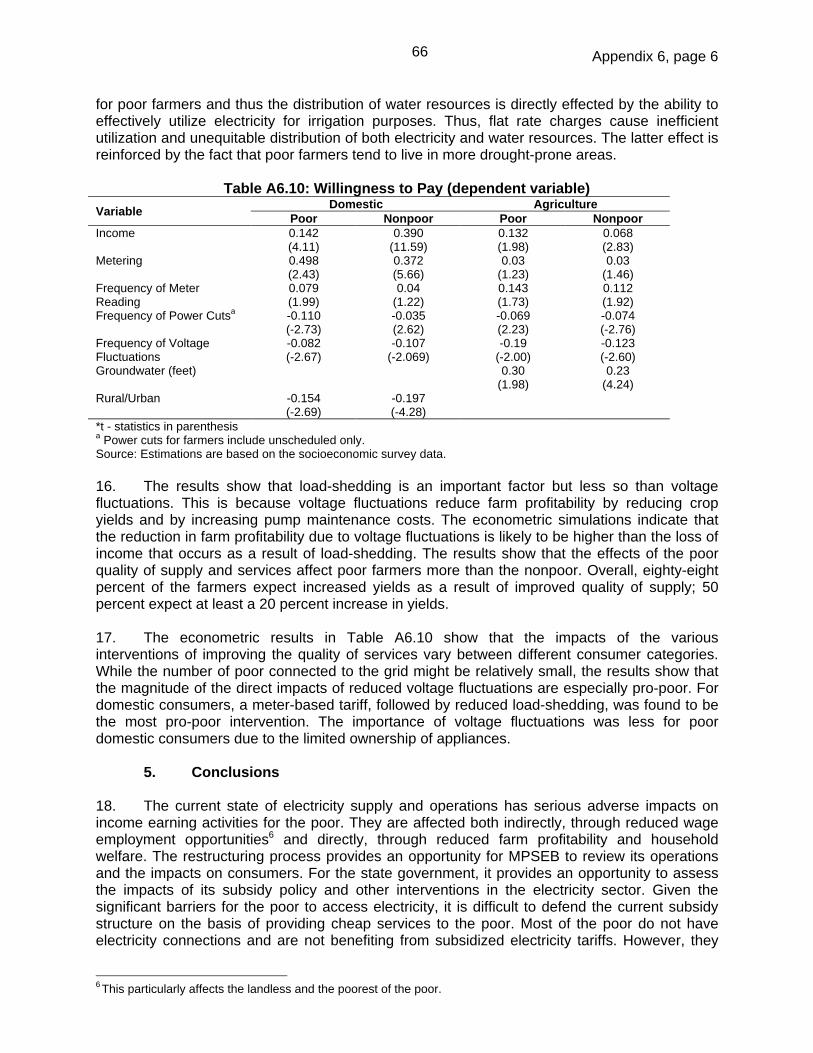

OF THE

PRESIDENT

TO THE

BOARD OF DIRECTORS

ON PROPOSED LOANS

TO

INDIA

FOR THE

MADHYA PRADESH POWER SECTOR DEVELOPMENT PROGRAM

November 2001

CURRENCY EQUIVALENTS(as of 1 November 2001)

Currency Unit − Indian Rupee (Re/Rs) Re1.00 = $0.0208

$1.00 = Rs47.98

In this report, an exchange rate of $1.00 = Rs0.47 was used forcalculation purposes. This was the prevailing rate during appraisal.

ABBREVIATIONS

ADB – Asian Development BankBMU – benefit monitoring unitCSEB – Chhattisgarh State Electricity BoardCIDA – Canadian International Development AgencyDFID – Department for International DevelopmentEISP – Energy Infrastructure Services ProjectERC – Electricity Regulatory CommissionHP – horsepowerHT – high tensionIEE – initial environmental examinationLIBOR – London interbank offered rateLT – low tensionMOU – memorandum of understandingMP – Madhya PradeshMPEB – Madhya Pradesh Electricity BoardMPG – Madhya Pradesh governmentMPPGCL – Madhya Pradesh Power Generation Company

LimitedMPPTCL – Madhya Pradesh Power Transmission Company

LimitedMPSEB – Madhya Pradesh State Electricity BoardMPSERC – Madhya Pradesh State Electricity Regulatory

CommissionNHPC – National Hydroelectric Power CorporationNTPC – National Thermal Power CorporationPFC – Power Finance CorporationPMU – project management unitPRA – participatory rapid appraisalSC/ST – scheduled caste/scheduled tribeSEB – State Electricity BoardSPU – strategic policy unitTA – technical assistanceT&D – transmission and distribution

NOTES

(i) The fiscal year (FY) of the Government ends on 31 March. FY before a calendaryear denotes the year in which the FY ends. Thus, FY2003 will start on 1 April2002 and end on 31 March 2003.

(ii) In this report, ‘$’ refers to US dollars.

WEIGHTS AND MEASURES

GWh – gigawatt-hour (1,000 megawatt-hours)kV – kilovolt (1,000 watts)kWh – kilowatt-hour (1,000 watt-hours)MW – megawatt (1,000 kilowatts)W – watt (unit of active power)

CONTENTS Page

LOAN AND PROGRAM SUMMARY ii

MAP viii

I. THE PROPOSAL 1

II. INTRODUCTION 1

III. THE SECTOR 2A. Macroeconomic Context 2B. Sector Description and Recent Performance 4C. Constraints and Issues 7D. State Government Objectives and Strategy 9E. External Assistance to the Sector 10F. ADB’s Operations and Strategy in the Sector 11

IV. THE SECTOR DEVELOPMENT PROGRAM 12A. Rationale 12B. Objectives and Scope 13C. Policy Framework and Actions 14D. The Investment Project 18E. Social and Environmental Measures 20

V. THE LOANS 22A. The Policy Loan 22B. The Investment Loan 25

VI. BENEFITS AND RISKS 32A. Expected Impacts 32B. Risks and Safeguards 35

VII. ASSURANCES 36A. Specific Assurances 36B. Conditions for Loan Effectiveness 38

VIII. RECOMMENDATION 39

APPENDIXES 40

ii

LOAN AND PROGRAM SUMMARY

Borrower India

The Proposal A sector development program (SDP) comprising a policy loan of$150 million and an investment loan of $200 million, for a total of$350 million from ordinary capital resources of the AsianDevelopment Bank (ADB) to support restructuring of the MadhyaPradesh Power Sector.

Rationale The SDP is designed to support the creation of an efficient, self-sustaining, and competitive power sector to provide sufficientquantity and quality of power to support the economic and socialdevelopment of Madhya Pradesh (MP). Given the complexity ofsector reforms, implementation will follow a phased approach overa period of time. The SDP supports the first stage of reforms thatlay the foundation for change and create an enabling environmentfor future private sector involvement through independent sectorregulation; institutional and organizational actions for improvedsector governance; establishment and gradual operationalizationof new sector companies; decisions about reconfigurating thedistribution segment, and managerial, financial, and operationalefficiency improvements in ongoing operations. These policyinitiatives will be supported by targeted physical investments toreduce system losses, improve operational and financialperformance, and increase the delivery capacity of the powersector to reap the benefits offered by sector restructuring.

The SDP seeks to assist in improving public and private resourceallocation in MP by increasing the operational efficiencies anddelivery capacity, and progressively reducing the demands on thestate budget for the power sector that have resulted in suboptimalallocation of public funds at the expense of other stateresponsibilities like education and health. This requiressimultaneous intervention at the policy level to provide thenecessary legal and institutional framework, and at the projectlevel to support critical investment components to ensure thesuccess of the reforms. Therefore, a mixed-modality SDP seekingto establish appropriate policies as well as supporting projectinvestments is considered the best instrument for supportingpower sector restructuring initiatives.

Classification Thematic: Economic GrowthGood Governance

iii

The Sector Development Program

Objectives and Scope The immediate objectives of the policy component (the Program)of the SDP are to (i) improve the policy environment andgovernance of the sector; (ii) initiate the establishment of acommercial and competitive business environment to promoteefficiency gains and loss reduction; (iii) improve the financialviability of the Madhya Pradesh State Electricity Board (MPSEB)through financial restructuring; and (iv) introduce a computerizedinformation and revenue management system.

Policy Frameworkand Actions The policy framework includes support for several actions.

The MP Vidyut Sudhar Adhiniyam, 2000 (the Reform Act), broughtinto force on 3 July 2001, is the most progressive in India to dateand includes provision for (i) restructuring MPSEB, (ii) mandatorymetering of all consumers; (iii) rationalizing tariffs so that allclasses of consumers will pay at least 75 percent of cost of supply(progressively phased over 5 years); (iv) allocating subsidies fromthe MP government (MPG) budget before subsidizing anycategory of consumers; (v) creating the MP State ElectricityRegulatory Commission (MPSERC); and (vi) referring disputeresolution between MPG and the MPSERC to the CentralElectricity Regulatory Commission rather than to the courts.

The existing MP Electricity Regulatory Commission was convertedinto the first MPSERC following the coming into force of theReform Act.

The generation, transmission, and distribution functions of MPSEBwill be corporatized and commercialized.

The MPSEB tariff structure will be rationalized and free powersupply in the state will be restricted.

The sector will undergo financial restructuring.

The Investment Project The investment component (the Project) of the SDP comprises sixcomponents:

A: 33 kilovolt (kV) and 11kV system improvements in Bhopal,Gwalior, Indore, Jabalpur, Khargone, Mandsaur, and Ujjain areas;

B: Conversion of selected low-voltage feeders supplyingagricultural pumps in selected divisions in Mandsaur andUjjain districts to 11kV operation;

iv

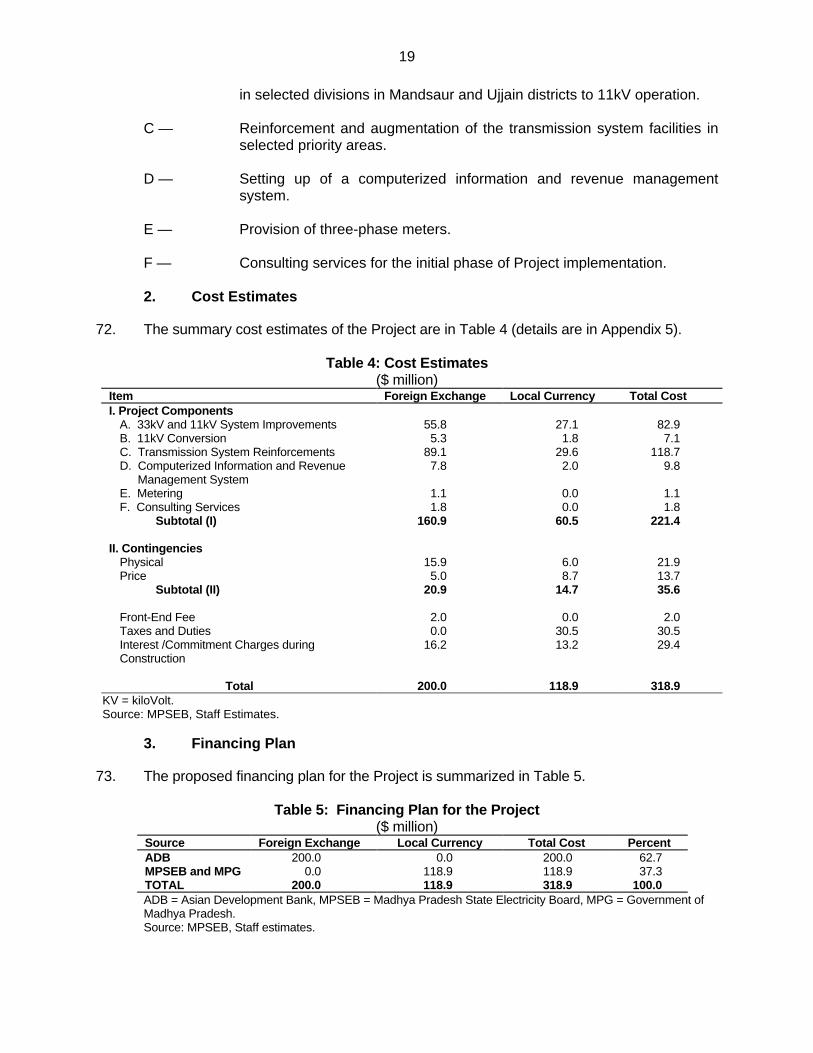

C: Reinforcement and augmentation of the transmission systemfacilities in selected priority areas of MP;

D: Setting up of a computerized information and revenuemanagement system;

E: Provision of three-phase meters; and

F: Consulting services for the initial phase of projectimplementation.

Cost Estimates The Project is estimated to cost $318.9 million equivalent,comprising $200.0 million in foreign exchange and $118.9 millionequivalent in local currency costs.

($ million)Financing Plan Source Foreign

Exchan geLocal

CurrencyTotalCost

Percent

ADB 200.0 0.0 200.0 62.7

MPSEB/MPG

0.0 118.9 118.9 37.3

Total 200.0 118.9 318.9 100.0

ADB = Asian Development Bank; MPG = Madhya Pradesh government,MPSEB = Madhya Pradesh State Electricity Board.

Environmental and Social Measures The Project is classified as Category B. An initial environmental

examination was undertaken and the summary is attached as acore appendix.

The poverty impact assessment for the SDP indicates that themandatory metering under the Reform Act is more beneficial forlow-income and poor households than the flat rate currentlycharged, since the per-unit charge is higher on a flat rate basis.Under the SDP, access to power connections by consumers livingbelow the poverty line will be facilitated through a scheme ofamortizing the upfront connection charges and associated feesover 12 months. Improved technical and nontechnical efficiencywill benefit all categories of consumers by improving supplyquality.

v

The Policy Loan

Loan Amountand Terms A loan of $150 million from ADB’s ordinary capital resources will

be provided under ADB’s LIBOR-based lending facility. The loanwill have a 15-year term, including a grace period of 3 years, aninterest rate to be determined in accordance with ADB’s LIBOR-based lending facility, including commitment charges and front-end fee. The Government will bear the foreign exchange risk onthe loan in accordance with its policy.

Program Periodand Tranching The period of the policy loan is December 2001 to June 2003. The

loan will be released in three tranches:

Tranche 1 of $65 million when (i) the Reform Act is in force;(ii) MPSERC awards the first tariff order; (iii) MP PowerGeneration Company Ltd. (MPPGCL), MP Power TransmissionCompany Ltd. (MPPTCL), and MP Power Distribution CompanyLtd. (MPPDCL) are incorporated and registered under the IndianCompanies Act, 1956; (iv) MPG and MPSEB agree on all thearrangements, with all outstanding dues paid, in accordance withthe memorandum of understanding; and (v) MPG issues an orderallowing MPSEB to disconnect all defaulting municipalities.

Tranche 2 of $40 million when (i) not less than 7,500 energy auditmeters are installed and operationalized; (ii) boards of directors forthe MPPGCL and MPPTCL are established with the majority ofmembers recruited in an open and transparent basis from outsidegovernment services; (iii) distribution reconfiguration is decided byMPG; (iv) MPG pays Rs2,000 million of total outstanding dues asof 31 March 2001 owed by municipalities to MPSEB; (v) asatisfactory debt restructuring plan of MPSEB is submitted; and(vi) second tariff filing is done by MPSEB before MPSERC.

Tranche 3 of $45 million when (i) all new distribution companiesare incorporated and registered under the Indian Companies Act;(ii) transfer scheme(s) are finalized; (iii) MPSEB assets aretransferred to MPPGCL, MPPTCL, and at least one of the newlyincorporated distribution companies, in accordance with thetransfer scheme(s); (iv) MPG pays Rs2,423 million of totaloutstanding dues as of 31 March 2001 owed by municipalities toMPSEB; and (v) third tariff filing is done by MPSEB beforeMPSERC.

Executing Agencies The Executing Agencies will be the Finance Department and theEnergy Department of MPG.

vi

Procurement The proceeds of the policy loan will finance the foreign exchangecosts (excluding local taxes and duties) of eligible items producedin and procured from ADB’s member countries.

Counterpart Funds Counterpart funds to be generated by the policy loan will betransferred from the Government to MPG under the normalarrangements for the transfer of external assistance and will betreated as an additionality to the Government’s transfers allocatedannually to MPG. Counterpart funds will be used by MPG, inaccordance with arrangements satisfactory to ADB, to support thefinancial restructuring of MPSEB and adjustment costs associatedwith the SDP, including (i) payment of outstanding municipalitiesand other local bodies dues, (ii) rationalization of electricity duty,(iii) set-off on dues of market borrowing of MPSEB to MPG,(iv) set-off of cross-liabilities between MPG and MPSEB, and(v) payment of debt obligations of MPSEB.

The Investment Loan

Loan Amountand Terms A loan of $200 million from ADB’s ordinary capital resources will

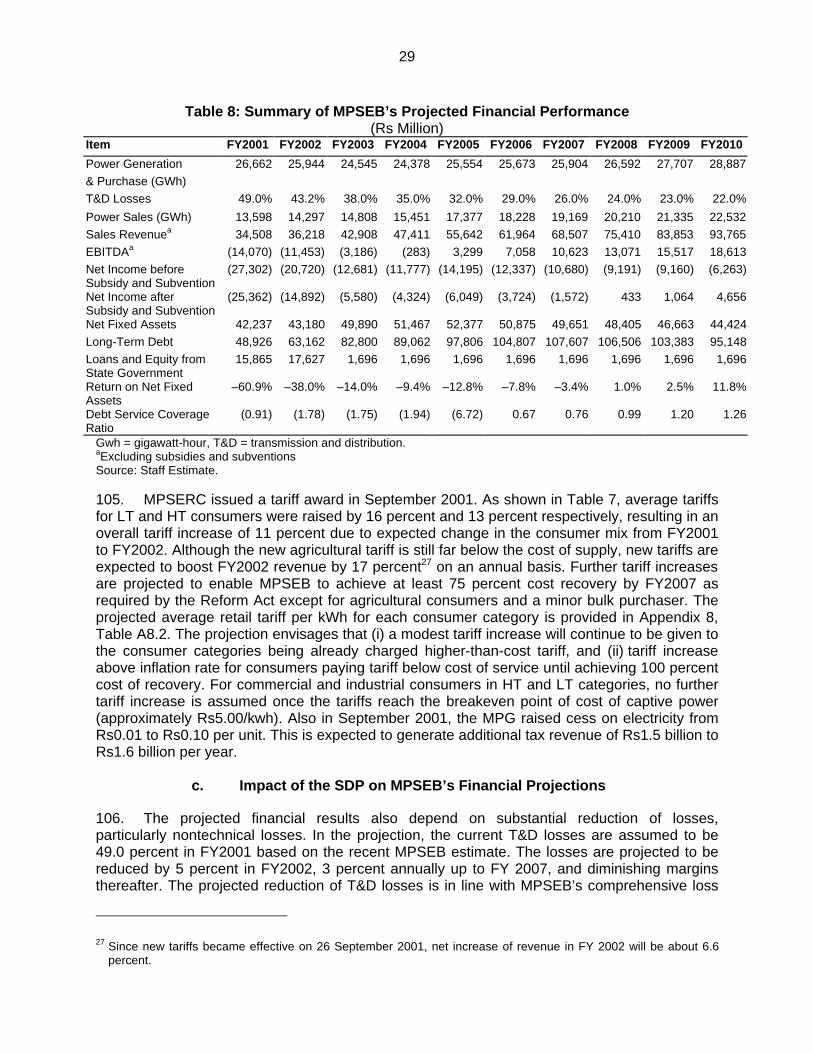

be provided under ADB’s LIBOR-based lending facility. Theinvestment loan will have a 20-year term, including a grace periodof 5 years, an interest rate determined in accordance with ADB’sLIBOR-based lending facility, a commitment charge of 0.75percent per annum, and a front-end fee of 1.0 percent. The loanproceeds will be transferred by the Government to MPG under itsnormal transfer arrangements. MPG will relend the loan proceedsto MPSEB at an interest rate of 12 percent with a term of 20years, including a grace period of 5 years. The Government willbear the foreign exchange risk on the loan in accordance with itspolicy.

ImplementationArrangements andExecuting Agency The Project will be executed by MPSEB (or its successor entities

with the prior approval of ADB). MPSEB, a statutory organizationcreated under the Government’s Electricity (Supply) Act 1948, ismanaged by a board appointed by MPG. Its successor entities willbe companies registered under the Companies’ Act, 1956 of theBorrower.

Procurement and Consulting Services Procurement of goods and services will be carried out in

accordance with ADB’s Guidelines for Procurement. Internationalconsultants will provide support for Project implementation and berecruited in accordance with ADB’s Guidelines on the Use ofConsultants. For implementation of component D, as also for

vii

benefit monitoring of the SDP, MPSEB will engage consultantsusing its own funds and procedures.

Time Frame Project implementation will commence in January 2002 and becompleted in December 2005. Disbursement under the projectloan will continue until June 2006.

Risks and Safeguards The major risks of the SDP are (i) regulatory risk, (ii) financialsituation of MPSEB, (iii) lack of adequate technical assistancesupport for outstanding analytical work, and (iv) operationalineffectiveness. These will be mitigated by (i) providingcomprehensive institutional strengthening and training forMPSERC, (ii) initiating comprehensive financial restructuring ofMPSEB with support from all stakeholders, (iii) solicitingcofinancing from bilateral assistance agencies and ADB providingadditional technical assistance funds, and (iv) changing andstrengthening organizational and management structures andpractices and effective follow-up mechanisms.

I. THE PROPOSAL

1. I submit for your approval the following Report and Recommendation on proposedassistance to India for the Madhya Pradesh Power Sector Development Program, that includes(i) a policy loan, and (ii) an investment loan.

II. INTRODUCTION

2. India’s economy has been growing by about 6 percent annually over the last six years.1

The country’s economic performance, however, does not necessarily imply that the economy isfully utilizing its growth potential. The slowing of economic reforms since the mid-1990shighlighted the major problems affecting the economy including severe infrastructurebottlenecks, widening fiscal deficits, poverty, and illiteracy. In particular, the deteriorating fiscalhealth of the central and state governments is significantly undermining the long-term growthpotential of the economy. Insufficient investments in physical infrastructure, both public andprivate, prevent the economy from reaping the benefits that are offered by market reforms andliberalization. This is particularly worrisome as empirical evidence on India strongly suggeststhat economic growth is the most effective path to sustained poverty reduction.

3. Under the Indian federal structure the states are responsible for a large number of vitalactivities, including infrastructure facilities, education, health, and law enforcement.Consequently, the fiscal health of the states is crucial for delivering these public services. Whilea large part of the states’ fiscal deficit is due to financial mismanagement and the priorityservicing of political interests, the inability of the states to recover the costs of their services is afurther reason for their poor fiscal health. For example, in the power sector, the inadequateaverage tariff base necessitates high budgetary subsidies to power utilities. As one result of thefiscal crunch, the electricity generation expansion target set for the Eighth Five-Year Plan(1992/97) fell short by 50 percent due primarily to inadequate investment at the state level. If notremedied, the unavailability of sufficient power will be the single most important constraint toeconomic development in the coming years and will thwart efforts to attract domestic andforeign investment.

4. Recognizing the importance of improving policymaking at the state level to enhancestructural reforms in India, in 1996 the Asian Development Bank (ADB) adopted a new strategyfor its operations in India directly targeting a portion of its assistance to selected states that havedemonstrated the political will to (i) undertake structural reforms in their macrofinances;(ii) improve their public resources management, (iii) restructure public sector enterprises; and(iv) undertake sectoral reforms. Gujarat was the first state chosen for this type of holistic support.ADB approved the first loan in December 1996.2 Based on the willingness and commitment ofthe Madhya Pradesh government (MPG) to reforms, the state of Madhya Pradesh (MP) wasincluded as the second focal state. Kerala was included as the third focal state and policydialogue has been initiated. The MPG and ADB agreed on a program to enhance resourceallocation to social sectors, improve fiscal capabilities, reform the public enterprise sector, andpromote an enabling environment for private sector participation in supporting infrastructure.The reform program was supported by the approval of the MP Public Resource ManagementProgram loan,3 which initiated power sector reform with ADB agreeing, in principal, to provide

1 CER: IND 200019: Country Economic Review , India, December 2000.2 Loan 1506-IND: Gujarat Public Sector Resource Management Program, for $250 million, approved on

18 December 1996.3 Loan 1717-IND: Madhya Pradesh Public Resource Management Program, for $250 million, approved on

14 December 1999.

2

targeted assistance for power sector development. The Power Sector Development Program(SDP) is included in the 2001 country program for India. The Fact-Finding Mission andAppraisal Mission were fielded during March-April 2001 and August-September 2001.4 Thisreport is based on the agreements reached during the missions.

III. THE SECTOR

A. Macroeconomic Context

1. Recent Macroeconomic Performance

5. In terms of area, MP was the largest state in India and fourth in population until it wasbifurcated into two states, MP and Chhattisgarh, on 1 November 2000, on the basis of the MPReorganization Act, 2000. Its rich deposits of coal, iron ore, limestone, and forest resourceswere the prime sources of industrial growth in the prebifurcated state. The major resource-tiedindustries were steel, cement, and newsprint. During the 1980’s, the state had three primaryattractions for many industrial units not based on local resources, such as chemical, electricalappliances, yarns, and garments: abundant land, no labor problems, and uninterrupted powersupply. Thus the state economy has shown robust growth averaging 4.4 percent since 1980/81,accelerating to 5 percent during 1990/96. The contribution of the primary sector in statedomestic product declined gradually over time and the contribution of services and industry roseconsistently. For example, the share of the primary sector declined from 43.4 percent in 1993/94to 39.6 percent in 1998/99. Similarly, the share of manufacturing and construction rose from21.4 percent to 23.0 percent during the same period.

6. However, the industrial growth situation has changed noticeably since 1995/96.Countrywide industrial recession and acute power shortages (almost 14 percent of the peakdemand in 1995/96) led to a sharp decline in industrial growth in MP.5 The growth rate of realnet state domestic product of registered manufacturing declined sharply from 7.1 percent in1994/95 to 4.4 percent in 1995/96, and 1.1 percent in 1996/97. Many industrial units wereforced to shutdown leading to large-scale unemployment. For example, the ferro alloys industrymade its debut in the state in 1989. The number of units rose to 22 by 1995. Power shortagescoupled with steep hikes in the power tariff after 1995 and strong market pressure due to thenew open import policy led to the closure of almost all of the 22 units as of 1999;6 and theirpower consumption reduced from 424 million units in 1995/96 to 17.34 in 1999/2000. Totalinvestment in these plants was about Rs2 billion and 20,000 workers were involved directly orindirectly. Similarly many designated economic growth centers in MP failed to promoteindustrialization due to the lack of proper infrastructure, such as roads, water, and street lightsetc. A recent small survey of constraints faced by small-and medium-sized enterprises in MP7

identifies lack of infrastructure, in particular shortage of electricity and its quality, followed by thepoor state of the roads.

4 The project team consisted of D. Graczyk, Senior Energy Sector Specialist and Mission Leader; IWEN; B. M.Karunaratne, Senior Project Engineer, IWEN; P. Ghosh, Senior Environment Specialist, ENVD; K. GerhaeusserSenior Programs Officer, PW2; S. Chander, Senior Project Engineer, IWEN; Y. L. Feng, Senior EnvironmentSpecialist, ENVD; M. Mitra, Senior Social Specialist, SOCD; T. Kimura, Energy Sector Specialist, IWEN; C. Litwin,Poverty Reduction Specialist, IWEN; V. S. Rekha, Counsel, OGC; and H. Mukhopadhyay, Macroeconomist, INRM.

5 The reasons for postreform industrial recession in India are still being debated. However, high lending rates, creditsqueeze, and political uncertainties are some of the important factors.

6 National Institute of Public Finance and Policy. 1999. Fiscal Industrial Incentives of the Government of MadhyaPradesh: Costs and Benefits. New Delhi.

7 TA 3338-IND: Capacity Building for Public Enterprises Reform and Social Safety Net in Madhya Pradesh, for$750,000, approved on 14 December 1999.

3

7. MP is one of the poorest states in India. In 1998/99, the per capita annual income wasRs7,350 (in constant prices) as compared with Rs9,739 at the all-India level. The percentage ofthe population living below the poverty line was 37.4 in 1999/2000, much higher than the all-India figure of 26.1 percent.

8. The new MP comprises roughly two thirds of the state before bifurcation, in terms of landarea and population, is industrially more diversified with a higher proportion of light andmanufacturing industries, and will have a higher per-capita income than the undivided state.However, the new MP has lost most of its natural and mineral resources to Chhattisgarh, andwill need to adopt a new strategy for stimulating industrial growth. Therefore, future plans forindustrialization in the new MP should primarily focus on promoting industries that are notresource-tied. States in India are competing to attract these industries. As decided by thecouncil of state finance ministers, all fiscal incentives for industrialization were ended byApril 2001. Thus, future industrialization will critically depend on adequate infrastructure facilitiesincluding power and good roads, as well as adequate education and health facilities to attractgrowth industries and their employees.

2. Macroeconomic Linkages of Power Sector Reform

9. Delays in reforms and the MPG policy of free power supply to a large proportion of itsagricultural and domestic consumers (para. 62) has brought the MP Electricity Board (MPEB)(para. 20) into a severe financial crisis. As a result, MPEB is unable to provide adequate power,which is the most important ingredient of growth in the state. Also, the state exchequer is losingpotential revenues that could have been mobilized from a financially strong electricity board. Forexample, in fiscal year (FY) 2001 MPEB’s dues from interest on MPG loans (Rs3.33 billion) andfor electricity duty (Rs3.31 billion), which MPEB collects on behalf of MPG, is estimated to beequivalent to almost 8 percent of the state’s own revenue (both tax and nontax), and 0.8 percentof the net state domestic product. However, as a result of misdirected power policies and anoncommercial tariff structure, MPG provides annual budgetary support for MPEB such as therural electrification subsidy, subsidy for free power supply, and fresh loans. And althoughMPEB’s dues are adjusted entirely against budgetary support, MPG’s unpaid subsidy to MPEBamounted to Rs23.3 billion as of March 2001. In 1996, MPG adjusted Rs7.9 billion by writing offits loans to MPEB, and in FY 1998 converted another Rs7 billion of its loans to equity to clearthe backlog of subsidy payment from the state budget to MPEB.

10. Although funds are not fully fungible, fiscal imbalances, budgetary allocations, and thefinancial deterioration of MPSEB are clearly linked, as state budget support to the power sectorcrowds out public expenditure and investments in alternative sectors more productive forpoverty reduction. The cash shortfall of MPSEB under a no-reform scenario is estimated atRs16.7 billion for FY2002. In terms of evaluating the opportunity cost of MPSEB’s cashrequirements, the cash shortfall translates into 32 percent of total social sector spending,including capital investments. In view of the state fiscal imbalances, the Government has beencompelled to finance budgetary support for the power sector through the banking sector. Thecash requirement of MPSEB would amount to 43 percent of the gross fiscal deficit. Furtherdeterioration of MPSEB would increase resource requirements from the banking sector andaffect the ability of the sector to lend for private sector investments, which are more productivefor economic growth. The macroeconomic linkages of the power sector reform are summarizedin Figure 1.

11. MPG support for the power sector is targeted primarily at operational subsidies insteadof supporting investments in system expansion to improve quantity, quality, and reliability of

4

supply or at least for adequate maintenance of existing assets. The electrification ratio forhouseholds in MP is about 42 percent, with less than 29 percent electrified in rural areas. Effortsby the state to increase private sector investment in power generation were undermined by theMPEB’s low credit rating. Recognizing its inability to fund the additional investments required inthe power sector, MPG has decided to reorganize the power sector to increase the self-financing capability with the objective of increasing the ability to allocate budget resources tosocial sectors.

Figure 1: Macroeconomic Linkages of Power Sector Reform

B. Sector Description and Recent Performance

1. Organization

12. India consists of 28 states8 and 7 union territories with a total population of over 1 billion.The organization of the power sector is determined by the country’s federal structure. All majorissues affecting the power sector require concurrent action by the central and stategovernments.

13. The central Government’s Ministry of Power provides overall guidance to the sectorthrough the Central Electricity Authority (CEA). The Government owns central power utilitiessuch as the National Thermal Power Corporation (NTPC), National Hydroelectric Power

8 Three new states, Chhattisgarh, Jharkhand, and Uttaranchal, were created in November 2000 through thebifurcation of Madhya Pradesh, Bihar, and Uttar Pradesh states, respectively.

Fiscal reliefto the stategovernment

Benefits to thereal sector

Higherrevenuegrowth

Higheremployment

Reduction inPoverty

Stabledemand for

mass-consumption

items

Higherexpenditure

on socialsectors

Highercapital

expenditure

Power Sector Reform

Increasedcredit available

for privatesector

5

Corporation (NHPC), Nuclear Power Corporation and the Powergrid Corporation of India(Powergrid), which are engaged in generation and interstate power transmission. The RuralElectrification Corporation and the Power Finance Corporation (PFC) are Government-ownedand dedicated to financing power sector activities. The Power Trading Corporation was recentlyestablished to be responsible for power trading for large independent power producers targetedto multistate purchases.

14. State governments control the rest of the sector through 17 state electricity boards(SEBs) and 12 electricity departments, which provide distribution facilities and set retail tariffswithin a state, and share responsibility with the central power sector agencies for powergeneration and transmission. The central agencies own and operate 32 percent of the country’stotal generation, while the SEBs and electricity departments have 64 percent of the total. Inaddition, five private utilities in urban agglomerations have a 4 percent share in powergeneration.

15. In 1998, the Electricity Regulatory Commission (ERC) Act was passed by the IndianParliament and in the same year the Central Electricity Regulatory Commission (CERC) wasestablished. The ERC Act gives CERC full autonomy to regulate central power utilities and toset bulk tariffs. The ERC Act also encourages the states to establish state electricity regulatorycommissions with full authority for state-level power utilities.

2. State Electricity Boards

16. The Indian Electricity Act of 1910 and the Electricity (Supply) Act of 1948 provide thelegal basis for the establishment and operation of SEBs. SEBs are typically vertically integratedentities owned by their respective state governments. While they are nominally independentfrom the state governments, their commercial and financial operations are subject to substantialintervention by these governments, in particular for tariff setting, metering policies, andelectrification targets. Most SEBs are ordered to provide free or highly subsidized power to theagriculture sector and to a substantial portion of domestic consumers. Continuous politicizationof the sector combined with a lack of commercial culture and accountability have resulted innegative internal cash generation by SEBs, impeded expansion of the power system, andrestrained adequate maintenance and rehabilitation of existing assets. As a result, the demand-supply gap has widened, and the quality of power supply has deteriorated in almost all parts ofthe country.

17. Recognizing the need to separate social obligations from commercial imperatives, somestates initiated power sector reforms in the mid-1990s and passed their own power sectorreform bills to provide a legal basis for SEB reorganization. The states that have reorganized, orare in the process of reorganizing, their power sectors are Orissa (1996), Haryana (1998),Andhra Pradesh (1999), Karnataka (1999), MP (2000), Rajasthan (2000), Uttar Pradesh (2000),Delhi (2001), and Gujarat (2001). The major objective of the state power sector reform is toincrease the sector’s self-generation of funds and to reduce its reliance on budget transfers fromthe state’s budget. Although each state has adopted a unique model of power reform, all modelsreflect in one way or the other the desire to distance the government from power sectoroperations.

3. Central Power Utilities

18. Until 1972, the SEBs were almost solely responsible for developing power generationand transmission within their states, but were unable to meet the rapidly increasing demand forelectricity. To improve the efficiency of generation, three central sector agencies — NTPC,

6

NHPC, and Nuclear Power Corporation — were established in 1975 to generate bulk power forsale to SEBs. In 1989, Powergrid was established as a transmission and dispatch company byamalgamating the transmission and dispatch assets of all central power sector agencies. Inaddition to these wholly owned companies, the Government also has shares in special-purposegenerating companies.

19. The central agencies, including NTPC, NHPC, and Powergrid, are seriously affected bythe poor financial health of most SEBs, as was evidenced several times in the past whenexcessive accounts receivable from SEBs seriously impaired the central agencies’ financialliquidity. To resolve this problem, NTPC has, in addition to restricting supply and obtainingGovernment appropriation to settle SEB debts, even resorted to taking over the SEB generationfacilities in settlement of accounts receivable.9 ADB’s two loans to Powergrid,10 restrictinvestments to SEBs that have a satisfactory payment record with Powergrid and makeprovisions for Powergrid to suspend power supply to delinquent SEBs.

4. Madhya Pradesh Power Sector

20. The MP power sector was operated by a vertically integrated monopoly, MPEB.Following the bifurcation of the state into MP and Chhattisgarh, in pursuance of subsection (4)of section 58 of the MP Reorganization Act, 2000, MPEB was succeeded by the MP StateElectricity Board (MPSEB) and the Chhattisgarh State Electricity Board (CSEB), both verticallyintegrated monopolies. As of 1 November 2000, the total installed capacity in the undividedstate of MP was 4,261 megawatt (MW). The division of generating capacity following thebifurcation is given in Table 1.

Table 1: Generation Plant Details (1999-2000)State Type Total

(megawatts)A. Madhya Pradesh (new) Thermal

HydroTotal (A)

2,148 7532,901

B. Chhattisgarh ThermalHydro

Total (B)

1,240 1201,360

C. Total (Old MP) ThermalHydro

Total (C)

3,388 8734,261

Central Allocation 1,521 Source: MPSEB.

21. Based on a provisional Government order, generation capacity was allocated betweenthe two states on the basis of asset location. Similarly, transmission assets, distribution regions,and project/asset-specific liabilities, including employees, would be split along geographic stateborders. However, non-project/asset-specific liabilities (including employees) would beapportioned on the basis of population leaving MPSEB to assume approximately 79 percent oftotal long-term debt of MPEB. Both states have requested the Government to reconsider its

9 As part of the agreement to change the executing agency for Loan 907-IND: Unchahar Thermal Power Project, for$160.0 million approved on 29 September 1988 to NTPC, ADB, the Government, the Uttar Pradesh government,and NTPC agreed to transfer title to the 420-MW Stage-I to NTPC. NTPC has since taken over the TalcherThermal Power Station from Orissa SEB, and the Tanda Thermal Power Station from Uttar Pradesh SEB in lieu ofdues owned by these states.

10 Loan 1405-IND: Power Transmission (Sector) Project, for $275 million, approved on 16 November 1995 andLoan 1764-IND: Power Transmission Improvement (Sector) Project, for $250 million, approved on 6 October 2000.

7

order. Nonetheless, MPSEB was already granted the right of first refusal for purchasing surpluspower from CSEB’s own production. The key indicators for the new MP’s power sector aregiven in Supplementary Appendix A.

22. From 1993 to 2000, power demand grew by a compounded 7.3 percent annually.However, annual growth rates fluctuated strongly due to the severe power shortagesexperienced from 1996 to 1998. Growth was also uneven between the different customercategories over the same period with high tension (HT) industrial consumers showing zerogrowth compared with a compounded 16 percent growth rate for agricultural consumers.

23. The size of load served, as well as the load mix, in the two new states differssignificantly from that of the undivided MP state (Table 2). As a result, the new MPSEB isexpected to be in a financially weaker position than erstwhile MPEB because (i) many high-profile industrial consumers reside in Chhattisgarh, (ii) 94 percent of agricultural consumersremain in the new MP, and (iii) allocation of 32 percent of generation capacity to Chhattisgarhwill leave the new MP with a more serious power shortage.

Table 2: Load Mix for MPSEB and MPEB in 1999-2000State Unit Domestic LT Agriculture HT Industry All Other TotalMadhya Pradesh MU 2,622.2 8,994.6 2,984.2 3,721.6 18,322.6(MPSEB) 14% 49% 16% 21% 100%Chhattisgarh MU 929.8 624.3 2,916.8 942.3 5,413.2

% 17% 12% 54% 17% 100%Total (MPEB) MU 3,552.0 9,618.9 5,901.0 4,663.9 23,735.8

% 15% 41% 25% 19% 100%HT = high tension, LT = low tension, MPEB = Madhya Pradesh Electricity Board, MU = million units.Source: MPSEB.

C. Constraints and Issues

24. Load Restrictions. Power demand grew by 6.4 percent in 1999/2000 and the peakdemand-supply gap in the same year is estimated at about 1,500 MW. This unserved, orsuppressed demand, results from planned (load relief) and unplanned (load shedding) cuts. Inresponse to the shortage, MPEB resorted to load restrictions for HT, low tension (LT), and ruralconsumers. Energy shortfall reached 1,060 gigawatt-hours in 1998/99 and is estimated to haveincreased to 1,552 gigawatt-hours for the year 1999/2000. Quality of supply has also sufferedas a result of overloaded transmission and distribution facilities; the system has been operatingat lower than normal frequency and voltage approximately 55 percent of the time. Transmission,distribution, and generation limitations are thus preventing the system from meeting demand.

25. Independent Power Producer Policy. In response to the growing supply gap, MPGinitiated a policy to invite private power producers and entered into power purchase agreementswith a total of 17 sponsors. However, none of the independent power producers has achievedfinancial closure yet due to MPEB’s insufficient escrow capacity11. In December 1999, theescrow capacity was reviewed and revised to 900 MW, which is only 35 percent of the capacityestimated 18 months earlier, pointing to the sector’s severe financial problems.

11 The term escrow used here refers to the deposition of the revenue stream from a specific revenue collectioncenter, e.g., a distribution unit, into a separate account in an identified bank, an escrow agent. In the power sectorthis mechanism is mostly used to guarantee payment of an independent power producer, to whom the primaryclaim on a revenue stream from a distribution zone is transferred or escrowed.

8

26. Tariff Structure and Subsidies. The financial problems of MPEB and its successorMPSEB are in large part due to an MPG policy (para. 62) to provide free power to single-pointconnections12 in urban and rural areas and for agricultural pump connections up to5 horsepower. Moreover, MPG instructed MPEB to supply almost free electricity to ruralelectricity cooperative committees (Rs0.07 per kWh) and to pursue a vigorous ruralelectrification program. This resulted in lopsided growth rates in the domestic and primarily theagriculture sectors at the expense of the industrial and commercial consumer categories.Industrial consumption was 82.7 percent of total energy consumption in 1970/71, but dropped toonly 20 percent of consumption in 1999/2000. During the same period, the percentage ofagricultural consumption went up from 3.4 percent to 41 percent.

27. With its high energy consumption, the agriculture sector contributed barely 6 percent oftotal MPEB revenue in 1999/2000, while the industry sector’s contribution was 43 percentcompared with 20 percent of consumption. In terms of average realization per kilowatt-hour(kWh), the agriculture sector accounted for Rs0.27 and the domestic sector for Rs0.93 ascompared with an average cost of supply of Rs3.03 per kWh (Table 3).

Table 3: Average Realization from Energy SoldFY1996 FY2000

Item %TotalConsumption

Average TariffRs/kWh

%TotalRevenue

%TotalConsumption

Average TariffRs/kWh

%TotalRevenue

Domestica 15 0.65 7 15 0.93 8

Irrigation/Agriculture

35 0.18 4 41 0.27 6

HT Industriesb 33 2.66 62 20 3.82 43

Ave.OverallSupply Cost

1.74 3.03

HT= high tension, kWh= kilowatt-hour, Rs= Indian Rupee.aIncludes single point consumers.bIncludes steel plants.Source: MPSEB.

28. This situation has resulted in (i) MPSEB not having resources to finance its systemexpansion to meet unserved demand; (ii) industrial consumers paying high tariffs that impairtheir competitiveness and consequently establishing their own generation facilities, erodingMPSEB’s consumer mix; and (iii) MPSEB being unable, without subsidies from the stategovernment, to earn a return on its investments as prescribed by law.

29. Captive Power. In direct response to the deficient quantity and quality of power supplycoupled with high tariffs, major industrial consumers have set up their own captive powergeneration plants. From 1995/96 to 1999/2000, growth of captive generation averaged 8.7percent per year, with the last two years being above 9.3 percent for a total of 1,390 MW ofinstalled captive capacity for MPEB. Of this, 671 MW or 48 percent is located in the territorysupplied by the new MPSEB. This represents considerable loss of revenues for MPSEB.

30. System Losses. From 1994/95 to 1998/99, transmission and distribution (T&D) losseshave varied within a range of 19.6 percent to 20.9 percent. Precise loss estimation is hamperedby the fact that currently only about 38 percent of energy input into the distribution system ismeasured due to the policy of free supply for designated agricultural and domestic consumers,

12 These are unmetered connections intended for operation of a single power outlet point only.

9

and the charging of a flat rate for several other consumer groups. In addition, a significantnumber of meters are defective and consumption of those customers also needs to beestimated.

31. Losses consist of two major types: technical and commercial. Estimation of technicallosses can be made rather precisely through load-flow analysis. Commercial losses aregenerally a function of the operation of the system; and can include theft, metering problems,and billing and collection inefficiencies. Given the current absence of energy audit and full end-user metering of agricultural customers, reestimation of consumption by MPSEB consultantsbased on connected load, supply restrictions, etc., provides strong evidence that agriculturalconsumption is gravely overstated and that losses are understated. This revised estimate showslosses of around 47 percent, of which 22 percent are considered technical and 25 percentcommercial. Reduction in technical losses generally requires significant investment; because ofthe financial constraint of MPSEB, the improvement in technical losses is expected to be slow.On the other hand, major improvement in nontechnical losses can be quickly achieved withconcerted management effort at much lower levels of investment.

D. State Government Objectives and Strategy

1. The Policy Framework

32. As a result of efforts made by the National Development Council13 the high-levelCommittee on Power was constituted in June 1993. In its report submitted in October 1994,the committee recommended (i) organizational reforms at the state level, consisting ofcommercialization and vertical and horizontal unbundling; (ii) large-scale involvement of theprivate sector in generation and distribution; (iii) depoliticizing electricity-tariff setting by creatingnational and regional tariff boards; and (iv) progressive phasing out of subsidies to agriculturalconsumers. These recommendations were renewed in the council meeting with Power ministersin October and December 1996, and are outlined in the Common Minimum National Action Planfor Power.

33. In response to the National Development Council’s recommendation, MPG appointed ahigh-level committee in 1996 to review the existing power sector situation and to suggestmeasures for its restructuring in the context of economic liberalization and introduction of privatecapital into the sector. Named after its chairman, the Tata Rao Committee issued Guidelines onRestructuring and Privatization of Power Sector and Power Tariff in January 1997. The majorrecommendations of the report were to (i) divide MPEB along functional lines, (ii) maintainMPEB as a holding company, (iii) establish a regulatory authority, (iv) allow private sectorinvestment in all functional areas, and (v) improve the financial and operational efficiency of thedistribution segment before inviting private sector investment. The report recommendedfundamental changes in the free supply of power to certain consumer segments, and that anysubsidies must be transparent and reimbursed to the utility on a timely basis. The Tata RaoCommittee advised against separating and privatizing urban area distribution from semiurbanand rural distribution, as this would leave the remaining public sector distribution segment highlynonviable. It also recommended maintaining uniform tariffs for each category of consumers, aslong as the areas continue to be MPEB subsidiaries.

13 India's highest political body, the council is chaired by the Prime Minister and comprises the chief ministers of all thestates in India.

10

E. External Assistance to the Sector

34. The power sector has received a major portion of India's external assistance. Of ADB’stotal Government-guaranteed lending to India amounting to $9.898 billion as of 31 October2001, 9 loans for $1.865 billion (18.8 percent) were approved for the power sector. The first fourprojects were for power generation; three were sector loans to support improvements in SEBefficiency and development of the national transmission grid; and the two most recent were forsector development to support the restructuring of a state’s power sector. In addition, under itsprivate sector operations, ADB has approved three loans and investments totaling $79.8 millionfor one captive transmission and two generation projects.14 Power subprojects have also beenconsidered for financing under ADB's private sector infrastructure facility15 and the InfrastructureDevelopment Finance Company.16 ADB also has approved $12.9 million for 21 technicalassistance (TA), mainly advisory, at both the national and state levels. The TAs have focusedon environmental and pollution control issues related to power generation, bulk transmissiontariffs, improved least-cost system planning, tariff studies at the retail level, improved technicaland commercial operations, power sector restructuring, and establishment of an independentregulatory authority. Previous ADB assistance to India’s power sector is listed in SupplementaryAppendix B.

35. The major funding source to the sector is the World Bank Group. The World Bank hassupported power generation, transmission, and distribution projects, including assistancedirected to SEBs. The World Bank is supporting power sector reforms in the states of AndhraPradesh, Haryana, Orissa, Rajasthan, and Uttar Pradesh. In Andhra Pradesh and UttarPradesh, power sector reform is viewed as part of overall reform of the state finances. ADBcoordinates with the World Bank on the geographical demarcation of state-level operations, aswell as to ensure overall complementarity of actions at both the central and state levels. ADBand the World Bank have concurrent ongoing operations for different projects with threeorganizations: PFC, Powergrid, and NTPC. Other major agencies funding the sector are theJapan Bank for International Cooperation, Kreditanstalt für Wiederaufbau for the Government ofGermany, Department for International Development of the United Kingdom (DFID), CanadianInternational Development Agency (CIDA), and United States Agency for InternationalDevelopment. Although the combined assistance of all aid agencies constitutes only about 8-10percent of the total investments in the sector, several key policy initiatives have been catalyzedas a result. Major external assistance provided to the power sector by other aid agencies is alsolisted in Supplementary Appendix B.

36. The Japan Bank for International Cooperation is supporting the expansion of publicsector generation, transmission, and distribution including rural electrification. It has nogeographic preferences.

37. DFID’s exclusive objective in providing assistance is poverty reduction. It is financingstudies for power sector restructuring in Andhra Pradesh, Haryana, and Orissa; and has noplans to participate in the financing of hardware other than in renewable energy systems. It is

14 Loan 7058/1036-IND: CESC Limited, for $17.8 million, approved on 4 October 1990; Loan 7082/1142-IND: CESCLimited II, for $32.0 million, approved on 13 December 1991; and Loan 7130/1499-IND: Balagarh Power CompanyLimited, for $15 million in equity and a loan for $25 million, approved on 5 December 1996.

15 Loans 1480/1481/1482-IND: Private Sector Infrastructure Facility, for a total of $300 million, approved on7 November 1996.

16 Investment 7138-IND: Infrastructure Development Finance Company, for $30 million equity investment, approvedon 14 October 1997. The loan amount was subsequently reduced to $15.463 million due to greater than expectedsubscription from the investors.

11

considering (i) cooperating with ADB to fund studies on power sector restructuring in MP andWest Bengal states; and (ii) assisting these states in other areas also, preferably in the "soft"sectors, like health and education.

38. The United States Agency for International Development has extensively supported andcontinues to support policy aspects of private sector participation. It has supported studies forstate sector reforms through PFC, and by providing grant assistance for energy management,conservation, and training.

39. CIDA assisted Kerala in conducting extensive studies for restructuring its power sector.ADB is following up on CIDA’s work through policy dialogue and preparation for a possible loanintervention. Together with the World Bank, CIDA is providing similar TA for power sectorreforms in Andhra Pradesh. In Madhya Pradesh, CIDA and ADB are cooperating andcoordinating closely in providing assistance to MPSEB and MPG for power sector reform. CIDAprovides the most bilateral assistance and is providing an umbrella TA to MPSEB through theEnergy Infrastructure Services Project (EISP). The EISP’s components include (i) rationalizingthe tariff structure; (ii) developing a power system master plan; (iii) supporting distributionreconfiguration and preparation of a grid code; (iv) restructuring MPSEB debt and preparingopening balance sheets for the new sector entities; (v) supporting capacity building for cross-cutting themes in environment, gender equality, socioeconomic analysis, and governance; and(vi) developing a poverty reduction strategy as it relates to energy availability for the poor(para. 50).

F. ADB’s Operations and Strategy in the Sector

1. Lessons Learned

40. ADB operations in India’s power sector have generally been successful from a projectpoint of view, i.e., the projects concerned have achieved their physical objectives. However,except for the ongoing loans to Powergrid and Gujarat (footnote 10),17 these projects were notdesigned to change the business environment, and sector performance continues to deteriorate.This was primarily on account of (i) political interference in tariff setting; (ii) rapid growth of thedemand for electricity, making conventional investment strategies unworkable; (iii) governmentrules and regulations and control of the SEBs that inhibited speedy decision making; and (iv) thenoncommercial setup of the sector, which did not generate the market for alternative players tostep in to bridge the gap between supply and demand.

41. Although the past strategy enabled ADB to support many projects, it spread ADB'sresources too thinly, with the result that it could not achieve its desired goal of policy reformswith its power sector borrowers. In most states, the power sector has been the largest recipientof state resources, in terms of subsidies as well as in terms of capital investments. Thus, macromanagement of the state's finances needs to be improved if the power sector is to besuccessfully turned around. Therefore, ADB is now assisting selected states with power sectorreforms, only in the context of a holistic change in their macroeconomic management.

2. Operational Strategy

42. ADB’s current operational strategy in India is to support efforts to achieve highersustainable economic growth to promote employment and reduce poverty. Its contribution to

17 Loans 1803/1804-IND: Gujarat Power Sector Development Program, for $350 million, approved on 13 December2000.

12

higher growth focuses on improving the supply-side efficiency of the economy, especially byreducing bottlenecks in key infrastructure sectors. Emphasis is on improving the policy,institutional, and regulatory framework to enhance the efficiency of public sector operations andto encourage private investment. Improving resource mobilization to finance the necessaryinvestments is a key component of ADB’s assistance, and includes support for the developmentof financial and capital markets, as well as for improving internal resource mobilization in thesector agencies and enhancing their creditworthiness. High priority is also given to assistingprojects that contribute to environmental improvement.

43. ADB's strategy for India was revised in 1996 to accommodate an urgent need for aportion of its assistance to be provided in a systematic and comprehensive way at thesubnational or state level. This need reflects the facts that (i) a geographic focus, together withthe ongoing selective sector focus, enables ADB to maximize its developmental impact both inthe states concerned and, through the demonstrational impact of its operations on other statesas well; (ii) state-level economic reforms, which have been lagging behind initiatives takenby the Government, need support and incentives; and (iii) the states have considerableautonomy and have major legislative, administrative, and fiscal responsibilities in manyeconomic and social sectors. Key elements of the subnational assistance include (i) improvingthe states' public resources management, (ii) reforming and restructuring public sectorenterprises to improve operating efficiencies, and (iii) supporting reforms in key infrastructuresectors with a view to increasing private investment (para. 4).

44. Reflecting ADB’s overall country strategy for India and in recognition of the dualisticstructure of India's power sector, ADB's strategy for the power sector, which has been pursuedin coordination with the World Bank, intends to operate at two levels. At the central level,assistance is provided to central power sector companies such as Powergrid (para. 18,footnote 10) and PFC18 with a view to supporting their commercialization and using them asagents to leverage reform in their client SEBs. Through its support to PFC, ADB seeks topromote power sector reforms in states that would currently not qualify for direct lendingoperations. At the state level, by considering assistance only for states that demonstrate thepolitical will to substantially restructure and commercialize their power sectors, and by assistingthem to actualize the reforms, ADB is building up the reform process from the grassroots.Improvements in the power sector will increase the fiscal space of the state governments andincrease their ability to allocate more resources for poverty reduction and socioeconomicdevelopment.

IV. THE SECTOR DEVELOPMENT PROGRAM

A. Rationale

45. The power sector has become one of the major budget items for MPG due to politicizedsector management. Despite receiving high annual subsidies, the sector has not been in aposition to meet the growing demand for power, and quality and reliability of power supply havedeteriorated. Political interference in tariff setting and sector operations had adverse impacts onthe operational and financial performance of the MPSEB, which finds itself in a severe financialcrisis. The lack of sufficient and reliable power is eroding MP’s competitiveness, and prevents itfrom attracting the same level of industrial investments as some of its neighboring states. At thesame time, the demands on the state budget for the power sector have resulted in suboptimalallocation of public funds at the expense of other state responsibilities like education and health,

18 Loan 1161-IND: Power Efficiency (Sector) Project, for $250 million, approved on 26 March 1992. The loan accountwas closed on 18 December 1998.

13

further undermining the state’s attractiveness as a location for new industrial developments,especially information technology and biotechnology, which are India’s future growth sectors.Restoring the sector’s financial viability and sustainability is a declared objective of MPG andthe SDP provides the basis for MPG to reform and restructure the power sector.

46. MPG adopted the recommendations of the Tata Rao Report as the base model forsector reform, namely, (i) functional unbundling of MPSEB, (ii) retention of MPSEB as a holdingcompany, (iii) establishment of a regulatory authority, and (iv) improvement of operational andfinancial efficiency of the distribution segment before inviting private sector investment.However, MPG found that given the complexity of the sector reforms to be undertaken,implementation should be phased. Stage I of the reforms will lay the foundation for change andcreate the conducive environment for future private sector involvement in the power sector19

(Appendix 1 provides a vision for the long-term sector model). In close dialogue with ADB, MPGdeveloped a detailed plan for stage I of the reform process that aims at creating an enablingenvironment and independent sector regulation; establishing new sector companies and theirgradual operationalization; deciding on reconfiguring the distribution segment; and improvingmanagerial, financial, and operational efficiency of its ongoing operations. Those policyinitiatives would be supported by targeted physical investments to reduce system losses andincrease the delivery capacity of the power sector to reap the benefits offered by sectorrestructuring. On the basis of the policy dialogue associated with the SDP, MPG submitted itsdevelopment policy letter (Appendix 2), which includes a policy matrix and memorandum ofunderstanding (MOU) between MPB and MPSEB. A detailed plan for stage I of the reformprocess is provided in Appendix 3.

47. The SDP is designed to support MPG’s long-term goal to ensure an efficient, self-sustaining, and competitive power sector to provide sufficient quantity and quality of power tosupport the state’s economic and social development. The SDP provides incentives forinstitutional and organizational actions for improved sector governance and the functionalunbundling of MPSEB, and in parallel supports physical investments to strengthen the capacityof the power system and to reduce technical and nontechnical losses to improve operationaland financial sector performance. The SDP seeks to improve public and private resourceallocation in MP by increasing MPSEB’s operational efficiencies and delivery capacity, andprogressively reducing the need for transfers from the state government budget. This requiressimultaneous intervention at the policy level to provide the necessary legal and institutionalframework, and at the project level, to support critical investment components to ensuresuccess of the reform. Therefore, a mixed-modality sector development program is consideredthe best instrument for supporting an initiative to restructure the power sector. The SDPconstitutes the first stage of the reform process, and will be followed by a second loanintervention upon successful implementation of the first stage of reforms.

B. Objectives and Scope

48. The immediate objectives of the SDP are to assist MPG and MPSEB to (i) improve thepolicy environment and governance of the sector; (ii) initiate the establishment of a commercialand competitive business environment to promote efficiency gains and loss reduction;(iii) improve the financial viability of the MPSEB through financial restructuring; (iv) improve thequality and quantity of supply by reinforcing, modernizing, and rehabilitating the T&D systems to

19 The India Country Strategy Program for 2003 includes TA for Increasing Private Sector Participation in ElectricityDistribution.

14

promote economic growth; (v) introduce a computerized information and revenue managementsystem; and (vi) pursue installation of meters.

49. Given the lack of creditworthiness of MPSEB to attract private capital and the parallelneed to meet the growing demand for energy, the sector reform and restructuring strategy mustfocus on enhancing the cash flow at the distribution end. In addition to rationalizing the tariffstructure, the SDP will (i) reduce T&D losses, (ii) pursue 100 percent metering, (iii) improvebilling and collection efficiency, and (iv) install efficient operational management of power sectorcompanies. To achieve these changes, autonomous functioning of the power sector alongcommercial lines, especially of the distribution functions, and independent sector regulation andcorporatization of the generation, transmission, and distribution functions of MPSEB, arerequired. The SDP is designed to assist MPG and MPSEB in achieving these objectives. TheSDP frameworks are provided in Appendix 4.

C. Policy Framework and Actions

50. During its deliberation of the Tata Rao Report, MPG recognized that irrespective of thechoice of the long-term sector model, a set of preparatory studies would be needed to optimizesector expansion, ensure its commercial viability, attract and optimize private capital investment,and establish benchmark performance for introducing competition. Consequently, MPGrequested ADB assistance for preparing and financing the MP Power Sector DevelopmentProject.20 The TA was designed as a cluster TA to include six studies, two financed by ADB andfour by CIDA.21 In addition, CIDA recently expanded the EISP scope to include funding ofactivities related to implementing stage I and preparing stage II of the power sector reforms(para. 39). ADB will coordinate the overall MP power sector reform program and CIDA isworking closely with ADB to implement the studies. The first TA subproject to be implementedreviewed electricity legislation and regulation, and included drafting of the MP Power SectorReform Bill and support for the selection of a base model for the restructured power sector.

51. In May 2000, an MOU was signed between the Union Ministry of Power and MPG. In theMOU both parties affirm their joint commitment to the reform of the power sector, and set outtime-bound reform measures to be implemented by MP and the implementation support to beprovided by the Government. The MOU outlines the objectives of the reform program: topromote the development of an efficient, commercially viable and competitive power supplyindustry, which will provide reliable and quality power at competitive prices to all consumers inthe state and which will support the industrial development in the State. The Governmentcommits to support the reforms by allocating additional power from central power stations; andproviding financial support for investment projects through Powergrid and PFC, and technicalconsulting assistance.

1. Governance

52. ADB had extensive policy dialogue with MPG and MPEB about the legislative frameworkand the need to constitute the regulatory authority under a separate state power sector bill and

20 TA 2980-IND: Technical Assistance to India for the Madhya Pradesh Power Sector Development Project, for$1,000,000, approved on 7 January 1998. The six studies include (i) preparation of a power system master plan(CIDA); (ii) preparation of a framework for rationalization of tariffs (CIDA); (iii) review of electricity legislation andregulation (ADB); (iv) solicitation for private sector implementation of a generation project (ADB); (v) technical andmanagerial upgrading of distribution profit centers (CIDA); and (vi) demandside management (CIDA).

21 Implementation of CIDA’s TA components was delayed due to then prevailing external environment. CIDA iscurrently implementing TA components (i) and (ii).

15

not under the ERC Act to ensure independence of the regulator. As a result of the policydialogue, the MP Vidyut Sudhar Adhiniyam, 2000 (the Reform Act) was brought into force on3 July 2001. The Reform Act is the most progressive in India to date and includes provision for(i) restructuring MPSEB, (ii) mandatory metering of all consumers, (iii) tariff rationalization sothat all classes of consumers will pay at least 75 percent of the cost of supply (progressivelyphased over 5 years), (iv) allocation of MPG budget subsidies before subsidizing any categoryof consumers, (v) creation of the MP State Electricity Regulatory Commission (MPSERC), and(vi) dispute resolution between MPG and MPSERC by reference to the CERC as againstreference to the courts. The Reform Act is primarily an enabling provision for reform and leavessufficient flexibility for the power sector structure to evolve with future policy decisions andoperational requirements. Its prescriptive elements, like mandatory metering and minimum tarifflevels, are aimed at reducing political interference and ensuring the commercial management ofpower sector operations.

53. The MP Electricity Regulatory Commission was established in June 1999 under the ERCAct and was recognized as the first MPSERC upon bringing the Reform Act into force.MPSERC is gradually increasing its role as a proactive sector stakeholder. It formed an advisorycommittee consisting of representatives of different consumer groups, labor unions,nongovernment organizations, academic and research bodies, and various governmentdepartments, and issued a tariff philosophy paper for discussion. Its first tariff award was madeafter holding extensive public hearings throughout MP involving questions and answer sessionswith MPSEB officials. Also, in response to MPG’s recent proposals for a state-wide, load-shedding schedule, MPSERC held several public consultations before issuing an order.

54. In relation to the selection of a model for the postreform power sector, two largestakeholder meetings were organized during 1999. Representatives from unions, the MPFederation of Industries, academia, MPG officials, Madhya Pradesh Electricity RegulatoryCommission, and MPEB staff attended the meetings. The workshops contributed significantly toan understanding of the objectives, strategies, challenges, and benefits of power sectorrestructuring, and increased the transparency of the reform process.

55. Both the MOU and the Reform Act define MPG’s long-term vision for the sector and setthe legal framework for restructuring. However, in the short-term, visible improvements in thepower sector can only be achieved by combining internal efficiency enhancements of the utilityand MPG actions to boost MPSEB’s financial viability.

56. To depoliticize sector management, open and transparent recruitment processes mustbe used to fill boards of directors and senior management positions of the new sectorcompanies. MPG has agreed to recruit experts from outside government services for functionalareas including finance, commercial, corporate planning, and information technology. Inrecognition of the importance of installing and maintaining commercial discipline in the sector,MPG has taken the leadership role and issued an order to appropriate at source outstandingdues of municipalities and other government bodies. MPG also committed to make futuresubsidy payments to MPSEB in cash on a monthly basis.

2. Reform Model and Institutional Arrangements

57. Details of the power sector model for stage I of reforms were decided upon by MPGthrough continuous policy dialogue with ADB. As recommended by the Tata Rao Report, MPGdecided to functionally segregate MPSEB into separate generation, transmission, and distributioncompanies incorporated under the Indian Companies’ Act, 1956, to conduct business on acommercial basis. MPSEB will remain as the holding company of the newly incorporated

16

companies, and will also act as the single buyer and system operator during the first stage ofpower sector reform. All generation assets of MPSEB will be transferred to the newly incorporatedgenerating company, and each of the plants will be operated as an independent profit center. Alltransmission assets will be transferred to the newly established transmission company and it willact as the wheeling agent for intrastate transmission activities.

58. Stage I of the reforms also has to contend with the continuous uncertainty overapportionment of liabilities and employees between the two states as a result of bifurcation. Thefinal apportionment will impact on MPG’s decision on transfer schemes (proposed to beprepared under ADB TA) that are a prerequisite for full operationalization of the new sectorcompanies. Further, MPG recognizes the importance of identifying and assessing any costsresulting from the transfer schemes early to be able to mitigate their impacts.

59. Detailed analytical work needs to be carried out before the final number of distributioncompanies can be decided upon. Moreover, the final decision on the number of distributioncompanies includes an element of political decision making about the extent of supportablecross-subsidization within and between the new distribution entities and the treatment ofpredominantly rural distribution areas. Therefore, MPG decided to retain the existing distributionregions under MPSEB as the holding company until a final decision has been reached ondistribution reconfiguration. ADB also initiated policy dialogue with MPG and MPSEB that someof the existing distribution circles should already start operating as independent profit centers toprovide practical experience and best practices before operationalization of the new distributioncompanies becomes effective. The most suitable candidates for the profit center approach arethose distribution circles whose facilities are proposed for upgrading and strengthening. MPSEBshould give priority to installing of meters for energy audit and for end-consumers in these circles;and fully delegate managerial powers to those circles as part of the overall internal efficiencyenhancement measures currently being implemented.

60. While principally open to divestment and private sector involvement in all three functionalareas, MPG wishes to make its decision based on full and detailed information about the currentoperational and financial situation and the business prospects of the power sector in themedium term. Learning from experiences made elsewhere, MPG will first establish the legal andregulatory framework and an enabling business environment to create certainty for investorsbefore soliciting private sector investments.

61. MPG recognizes the benefits of creating a formal coordination mechanism for the reformprocess since effective reform management will require that a strategic and program overviewbe maintained at the highest level throughout the reform process to ensure effective use ofresources and to establish priorities. MPG has set up an institutional framework for managingpower sector reform under the apex of the Steering Committee for Power Sector Reformchaired by the chief secretary. The members of the committee include the principal secretariesfor power, finance, law, and planning; secretary, finance; and chairman, MPSEB. In addition, thejoint secretary reforms, Union Ministry of Power, and director, ADB, Department of EconomicAffairs, have been included to ensure close coordination on power sector reforms. Reporting tothe committee is the Strategic Policy Unit (SPU) headed by the principal secretary, power. TheSPU is responsible for defining the critical path for reform and for preparing a time-boundimplementation plan and review mechanisms, keeping in mind the institutional, financial, andregulatory imperatives. The SPU includes representatives from MPSEB and the Power andFinance ministries of MPG, and coordinates with ADB and other assistance agencies in thesector. Power sector experts from outside the state and representatives of consumer groups areinvited to provide feedback and input to the SPU on an intermittent basis. The SPU shouldideally be supported by a professional implementation task force to analyze best practices and

17

present alternative scenarios considering local conditions. With the assistance of ADB, MPG iscurrently identifying external funding for the implementation task force and the SPU. DFID hasexpressed general interest in supporting both.

3. Restriction of Free Power Supply

62. With effect from 1 January 2001, a new MPG policy became effective reducing freesupply of power to agriculture consumers and single-point consumers. Under the new policyonly scheduled castes and scheduled tribes (SC/ST) consumers who are living below thepoverty line and with a monthly consumption of not more than 20 kWh will receive free powersupply under the single-point scheme. SC/ST agricultural consumers are now only eligible forfree electricity supply for pumps up to 5 horsepower if they have less than 1 hectare of irrigatedland. As a consequence of this policy, about 95 percent of agriculture consumers and75 percent of single-point consumers are now required to pay their electricity bills fully. MPSEBexpects annual revenues from the agriculture sector to increase by Rs1,610 million, and fromsingle-point connections up to Rs1,440 million once the new policy is fully implemented. Theprojected increase is equivalent to 19 percent of total revenues from LT consumers in FY2000.

4. Energy Audit and Metering

63. The MP Urja Vidheyak, 2001, or the MP Energy Act for the prohibition of unauthorizeduse of electricity; and the assessment, compounding, and recovery of arrears and dues toreduce losses caused by illegal abstraction, use, consumption, and pilferage of electricity wasenacted on 17 April 2001. A comprehensive energy audit comprising the installation of 7,500meters is being implemented on all feeders up to the 11 kilovolt (kV) level; electronic meters willbe provided to all HT consumers. This will allow MPSEB to record and compare the energyinput into a specific distribution feeder with the realized revenues coming from the same feeder.Grouping and accounting of consumers according to distribution feeder will be implemented aspart of the energy audit. In addition to allowing specific targeting of high loss zones for efficiencyimprovements, the energy audit is a fundamental ingredient for distribution reconfiguration andcorporatization/divestment to be carried out as part of sector reform.

64. While preparing for supplying and installing meters to all endusers, MPSEB haslaunched a campaign to regularize unmetered connections using self-assessment of electricityconsumption. Under the scheme, administrative requirements for official connections arerelaxed, and consumers are encouraged to self-assess their monthly electricity consumptionand make payments based on this assessment. Once meters have been installed theconnections will be billed based on the meter reading. The self-assessment campaign fulfillsthree objectives: (i) immediately increase MPSEB’s revenues, (ii) lower resistance to meterinstallation, and (iii) assist in detecting tampering of meters if metered consumption issubstantially lower than that self-assessed. It also benefits poorer consumers who until nowcould not obtain legal connections due to lack of titles to their land/housing. Under the newpolicy, proof of property titles is no longer a requirement for obtaining a connection fromMPSEB. After an interim period, all nonregistered connections will be levied with heavy finesand ultimately disconnected.

5. Internal Reforms

65. The self-assessment scheme is part of the comprehensive measures implemented byMPSEB to increase the internal operational efficiencies. Simplifying procedural hurdles to obtainofficial connections will reduce nonmonetary access barriers to the network, whilesimultaneously reducing illegal connections and thus system losses.

18

66. Introduction of grievance procedures to better respond to customer needs and toincrease public participation is another step toward a commercial and competitive power sector.MPSEB has formed grievance redress committees at district and subdivision levels headed byrepresentatives of MPSEB and the local community. In anticipation of the new businessenvironment, MPSEB has implemented measures to decentralize powers and to increaseMPSEB officers’ responsibility for incidents of theft in their jurisdiction. As part of the internalrestructuring, MPSEB banned all new recruitment and revised the retirement age from 60 to 58years starting in January 2001, which immediately reduced the number of employees by about1,200 (of a total of 67,000).

67. MPSEB recently delegated more operational responsibilities. Administrative,commercial, and financial responsibilities created on a graduated scale by MPSEB weredelegated to individual generating plants and distribution circles. For example, in an effort toincrease the number of high-profile customers, line extensions for HT consumers can now beapproved by superintending engineers, and for industrial consumers up to 5 MW by regionalchief engineers instead of requiring approval of MPSEB board members.

68. In response to the changes resulting from the sector reforms, MPSEB is adjusting itsorganizational set-up. MPSEB’s reform coordination structure mirrors MPG’s, in the sense thatMPSEB’s High-Level Reform Coordination Committee is supported by a coordinationcommittee, which in turn collaborates closely with the Corporate Planning Group, (thecounterparts for CIDA’s EISP), which acts as MPSEB’s resource center for coordination with thereform process and is equivalent to MPG’s implementation task force.