ASIA-PACIFIC ENERGY MARKETS AND ROSNEFT Vladivostok, 3 … · ASIA-PACIFIC ENERGY MARKETS AND...

15

ASIA-PACIFIC ENERGY MARKETS AND ROSNEFT POTENTIAL Igor Sechin Chairman of the Management Board OJSC Rosneft Vladivostok, 3-5 September 2015

Transcript of ASIA-PACIFIC ENERGY MARKETS AND ROSNEFT Vladivostok, 3 … · ASIA-PACIFIC ENERGY MARKETS AND...

ASIA-PACIFIC ENERGY

MARKETS AND ROSNEFT POTENTIAL

Igor Sechin

Chairman of the Management Board

OJSC Rosneft

Vladivostok, 3-5 September 2015

The information contained in this presentation was prepared by the Company. Conclusions made herein are based on the information

collected as of the moment of the material preparation and may be changed without further notice. The Company relies on the

information obtained from sources considered to be reliable; nevertheless, it does not warrant the accuracy or completion thereof.

Such materials contain statements as to future events and explanations which may be considered as a forecast of such events. Any

statements made in these materials not being factual findings shall be deemed to be forward-looking statements associated with known

and unknown risks, uncertainties and other factors due to which our actual results, outcomes and achievements may significantly differ

from any future results, outcomes and achievements reported in or assumed by such forward-looking statements. We do not assume

any obligations as to updating any forward-looking statements contained herein so that they could reflect actual results, changes in

assumptions or in factors affecting such statements.

This presentation is not an offer to sell or encouragement to subscribe or buy any securities. It is understood that neither provision of this

report / presentation underlies any contract or obligation of any kind. The information contained herein shall not be considered, for any

purposes, to be complete, accurate or unprejudiced. The information contained herein is subject to verification, completion or change.

The content of this presentation has not be verified. Accordingly, we have not and will not make, on behalf of the Company, its

shareholders, directors, officials or employees or other persons, any representations or warranties, expressly indicated or implied, with

regard to accuracy, completeness, or objectivity of the information or conclusions contained herein. None of the directors of the

Company, its shareholders, officials, employees, or any other persons assume any liability for any losses of any kind which may be

incurred as a result of the use of such presentation or content hereof or otherwise in connection with this presentation.

2 IMPORTANT NOTICE

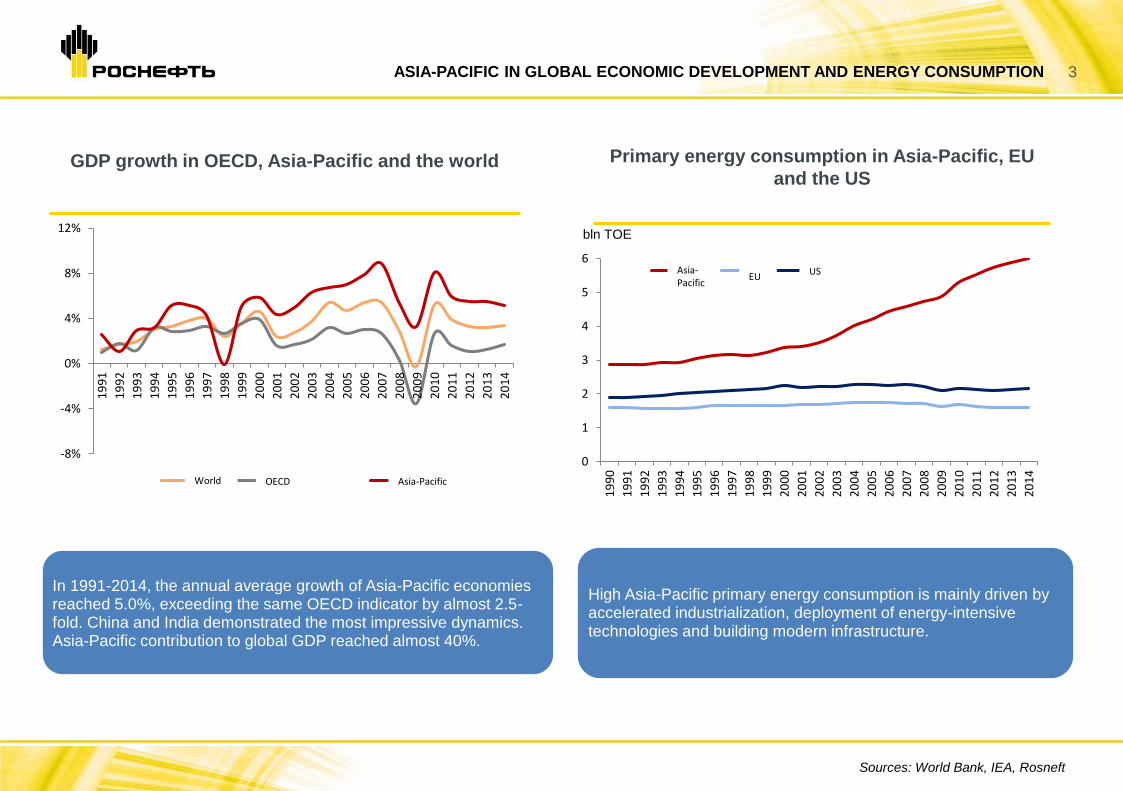

In 1991-2014, the annual average growth of Asia-Pacific economies reached 5.0%, exceeding the same OECD indicator by almost 2.5-fold. China and India demonstrated the most impressive dynamics. Asia-Pacific contribution to global GDP reached almost 40%.

High Asia-Pacific primary energy consumption is mainly driven by accelerated industrialization, deployment of energy-intensive technologies and building modern infrastructure.

Sources: World Bank, IEA, Rosneft

ASIA-PACIFIC IN GLOBAL ECONOMIC DEVELOPMENT AND ENERGY CONSUMPTION 3

GDP growth in OECD, Asia-Pacific and the world Primary energy consumption in Asia-Pacific, EU

and the US

-8%

-4%

0%

4%

8%

12%

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Мир Развитые страны АТР

0

1

2

3

4

5

6

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

АТР ЕС США

bln TOE

World OECD Asia-Pacific

Asia-Pacific

EU US

Crude oil production and consumption in Asia-

Pacific (excluding Russia) Natural gas production and consumption in Asia-

Pacific (excluding Russia)

In the middle of the 90s, Asia-Pacific own crude output (excl. Russia) accounted for 50% of the regional oil consumption. In 2014, its share reduced to 32%, and, according to Company forecasts, will drop further to 21% by 2030.

In 2014, Asia-Pacific own gas supplies accounted for 72% of the regional gas consumption.

According to Rosneft forecast, gas consumption in Asia-Pacific will grow to 1 200 mln toe by 2030, with imported gas accounting for over 40% of the supply.

ENERGY SHORTAGE IN ASIA-PACIFIC

Source: World Bank, IEA, Rosneft

4

0

10

20

30

40

50

60

70

0

200

400

600

800

1000

1200

1400

1600

1800

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

20

13

20

16

20

19

20

22

20

25

20

28

% mln t

Потребление

Производство

Самообеспеченность нефтью (правая шкала)

2014

40

50

60

70

80

90

100

0

200

400

600

800

1000

1200

1400

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

20

13

20

16

20

19

20

22

20

25

20

28

% mln TOE

Потребление

Производство

Самообеспеченность газом (правая шкала)

2014

Production

Consumption

Self-sufficiency in crude oil (right scale)

Production

Consumption

Self-sufficiency in gas (right scale)

5 RUSSIAN OIL - AN OPTIMAL SOURCE OF ENERGY SUPPLY FOR ASIA-PACIFIC

6 TOP 10 COUNTRIES IN TERMS OF GAS AND OIL RESERVES

Sources: BP Statistical Review 2015, EIA, Ministry of Natural Resources,

Zarubezhgeologia, USGS, Rosneft

TOP 10 COUNTRIES IN TERMS OF CRUDE OIL RESERVES, BLN BBL TOP 10 COUNTRIES IN TERMS OF GAS RESERVES, TLN CUB. M

* incl. shale gas

** incl. 4.5 trln cub. m of shale gas

* incl. 257 bln bbl of extra heavy crude oil

** incl. 170 bln bbl of bitumen

*** incl. 10 bln bbl of shale oil

7 UPSTREAM PROJECTS IN EAST SIBERIA ARE COMPETITIVE

VS. OTHER PROJECTS IN ASIA-PACIFIC

PROFIT / CAPITAL EXPENDITURES RATIO

0,0

0,5

1,0

1,5

2,0

2,5

Чая

нд

ин

ско

е

Ко

выкт

ин

ско

е

Ван

кор

Мес

соях

ско

е

Юр

убче

но

То

хом

ско

е

Ср

едн

ебо

ту

об

ин

ско

е

Суз

уньс

кое

и

Тагу

льс

кое

Вер

хнеч

он

ско

е

Сах

али

н-1

Сах

али

н-2

Wh

eats

ton

e L

NG

Qu

een

slan

d L

NG

AP

LNG

Gla

dst

on

e LN

G

Arr

ow

LN

G

Evan

s Sh

oal

Plu

to L

NG

1

Gre

ater

Su

nri

se

Tan

ggu

h L

NG

San

ga S

anga

Pu

guan

g

D6

MB

A

SHW

E

Vie

tnam

Gas

Россия Австралия Индонезия Китай Индия Мья нма

Вье тнам

2012 2015 средняя 2012 средняя 2015

INTERNAL RATE OF RETURN

0%5%

10%15%20%25%30%35%40%45%50%

Чая

нд

ин

ско

е

Ко

выкт

ин

ско

е

Ван

кор

Мес

соях

ско

е

Юр

убче

но

То

хом

ско

е

Ср

едн

ебо

ту

об

ин

ско

е

Суз

уньс

кое

и

Тагу

льс

кое

Вер

хнеч

он

ско

е

Сах

али

н-1

Сах

али

н-2

Wh

eats

ton

e L

NG

Qu

een

slan

d L

NG

AP

LNG

Gla

dst

on

e LN

G

Arr

ow

LN

G

Evan

s Sh

oal

Plu

to L

NG

1

Gre

ater

Su

nri

se

Tan

ggu

h L

NG

San

ga S

anga

Pu

guan

g

D6

MB

A

SHW

E

Vie

tnam

Gas

Россия Австралия Индонезия Китай Индия Мья нма

Вье тнам

2012 2015 средняя 2012 средняя 2015

Russia Australia Indonesia

China

India

Myanmar

Vietnam

average

average

average

average

Russia Australia Indonesia

China

India

Myanmar

Vietnam

Cha

ya

din

sko

e

Ko

vyktin

sko

e

Va

nko

r

Me

sso

ya

kh

sko

e

Yu

rub

ch

en

o-

To

kh

om

sko

e

Sre

dn

eb

otu

ob

.

Ve

rkh

ne

ch

onskoe

Sa

kh

alin

-1

Su

zu

nsko

e a

nd

T

ag

uls

ko

e

Sa

kh

alin

-2

Cha

ya

din

sko

e

Ko

vyktin

sko

e

Va

nko

r

Yu

rub

ch

en

o-

To

kh

om

sko

e

Su

zu

nsko

e a

nd

Ta

gu

lsko

e

Sa

kh

alin

-1

Sa

kh

alin

-2

Me

sso

ya

kh

sko

e

Sre

dn

eb

otu

ob

.

Ve

rkh

ne

ch

onskoe

Source: Institute of Economics and Finance (IEF), Goldman Sachs

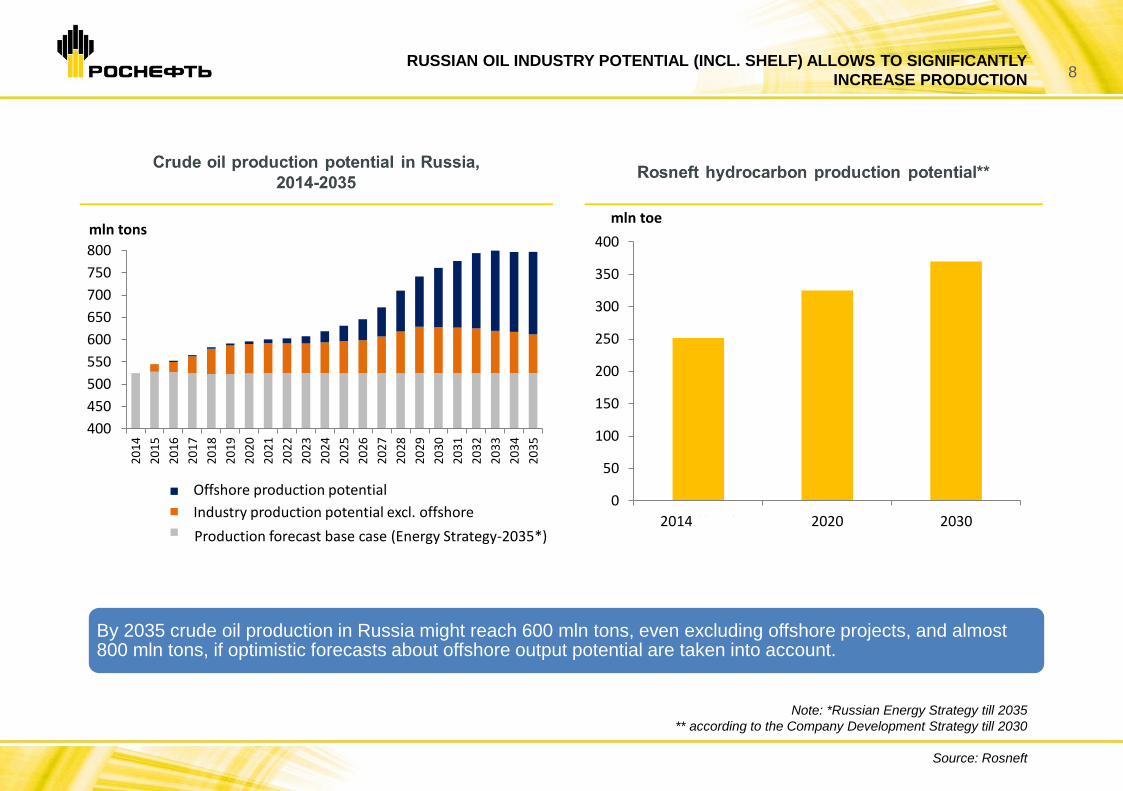

8 RUSSIAN OIL INDUSTRY POTENTIAL (INCL. SHELF) ALLOWS TO SIGNIFICANTLY

INCREASE PRODUCTION

400

450

500

550

600

650

700

750

800

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

mln tons

Потенциал шельфовой добычи

Потенциал добычи отрасли без учета шельфа

Базовый прогноз добычи (ЭС-2035*)

0

50

100

150

200

250

300

350

400

2014 (факт) 2020 2030

млн тнэ

By 2035 crude oil production in Russia might reach 600 mln tons, even excluding offshore projects, and almost 800 mln tons, if optimistic forecasts about offshore output potential are taken into account.

Note: *Russian Energy Strategy till 2035

** according to the Company Development Strategy till 2030

Source: Rosneft

1

mln toe

Offshore production potential

Industry production potential excl. offshore

Production forecast base case (Energy Strategy-2035*)

9 RUSSIA – MAJOR GLOBAL HYDROCARBON PRODUCTION CENTRE

2016-2017

LAUNCHING SUZUN AND

VOSTOCHNO-

MESSOYAKHSKOYE

VladIvostok

Russkoye

Suzun

Tagulskoye

Lodochnoye

Taas-Yuryakh Yurubcheno-Tokhomskoye

Moscow

Verkhnechonskoye

Production – 7.7 mmtpa

Suzun

Production – 4.5 mmtpa

Taas-Yuryakh

(Srednebotuobinskoye) – 2nd stage

Production – 4.2 mmtpa

Yurubcheno-Tokhomskoye

Production – 5.0 mmtpa

Tagulskoye

Production– 4.8 mmtpa

Lodochnoye

Production – 2.0 mmtpa

Vankor

Production – 22.0 mmtpa

Northern tip of Chaivo

Verkhnechonskoye

Kyumbinskoye

Production – 3.0 mmtpa (50%

Rosneft share) Kyumbinskoye

Vankor

*Production at plateau

**Onshore projects

Source: Rosneft

2020+

EASTERN FIELDS REACHING

PRODUCTION OF 40 MLN TONS

2018+

TAAS-YURYAKH (2ND STAGE),

YURUBCHENO-TOKHOMSKOYE,

RUSSKOYE, TAGULSKOYE,

LODOCHNOYE

Cooperation opportunities: bringing financial and technology partners to implement major projects –Taas-Yurakh, Yurubcheno-Tokhomskoye, Vankor cluster

10 ROSNEFT GAS BUSINESS POTENTIAL IN EASTERN RUSSIA

Zabaikalsk

Иркутск

Blagoveschensk

Srednebotuobinskoye

Nizhnejerbinskiy

Srednebiryukskoiy

Verkhnechonskoye

Yurubcheno-Tokhomskoye

Kuyumbinskoye

Agaleyevskoye

Exploration areas near Sobinskoye

Savostyanova

Lisovskiy

Sanarskoye

Bratskoye

Chayandinskoye

Kovyktinskoye

Danilovskoiye

641

307

181

9597

Юг Красноярского края

Иркутская обл.

Респ. Саха-Якутия

Сахалинская обл. (включая шельф)

Доля в Сахалине-1 (20%)

ONSHORE GAS IN EASTERN RUSSIA

>1 trln cub. m of gas reserves and c. 0.8 trln cub. m of

gas resources

Ongoing large-scale exploration program – 6 fields

discovered in 3 years

Gas reserves monetization is a strong catalyst for the

regional development

SAKHALIN GAS - FAR EAST LNG (100%)

Project reserve base – 0.6 trln cub. m of Rosneft and

Sakhalin-1 gas

Intensive exploration works on the Okhotsk Sea offshore

licenses granted by the government

LNG plant and infrastructure planned capacity is 5 mmtpa

with potential expansion to 10 mmtpa

Commissioning is scheduled post 2020

The project drives infrastructure building and new jobs

creation

1.3 trln cub.

m

Map of key Company assets in the region

Company’s reserves in the region (С1+С2)

South of the Krasnoyarsk region

Irkutsk region

Republic of Sakha-Yakutiya

Sakhalin region (incl. shelf)

Sakhalin-1 share (20%)

11 OFFSHORE EXPLORATION AND APPRAISAL IN THE FAR EAST

19 areas are under exploration and appraisal

9 areas are being explored together with

partners

9 areas are open for potential cooperation

AGGREGATE RECOVERABLE

RESERVES, ROSNEFT SHARE:

oil+ condensate - 117 mln tons

gas – 183 bln cub. m

AGGREGATE AREA POTENTIAL:

(DeGolyer & MacNaughton and

Rosneft estimate)

oil+condensate – 10.7 bln tons

gas - 10 trln cub. m

2014 RESULTS:

Aero-gravity-magnetic survey – 155 thous. km

2D seismic survey – 14.3 thous. km

Electric prospecting – 1 300 km

3D seismic survey – 1 500 sq. km

Drilling – 1 exploration well

OFFSHORE EXPLORATION INVESTMENT IN THE

FAR EAST FEDERAL DISTRICT:

2014 – 10.4 bln RUB

2015E – 13.7 bln RUB

2016-2019E – 210.2 bln RUB

LICENSES FOR 26 OFFSHORE AREAS IN THE FAR EAST FEDERAL

DISTRICT

12 CREATION OF NEW INDUSTRIAL CLUSTER BASED ON

SHIP-BUILDING COMPLEX ZVEZDA

Construction of an integrated ship-building

complex located in the Bolshoy Kamen and

Pyatj Okhotnikov bays

I construction stage

2012 – 2019

in the Bolshoy Kamen bay

Medium

shipbuilding site

II construction stage

2018 – 2022

in the Bolshoy Kamen bay

Ultra-large

shipbuilding site

III construction stage

2021 – 2024

in the Pyatj Okhotnikov

bay

Offshore shipbuilding

site

Project cost: 145.5 bln RUB

Main customers of vessels and marine

equipment:

local oil and gas companies and Russian maritime

shipping companies, incl. Rosneft, Gazprom,

Sovkomflot, NOVATEK, etc.

Planned workplaces ~ 7 500 jobs

Bolshoy Kamen bay Pyatj Okhotnikov bay

ROSNEFT DEMAND FOR DRILLING RIGS AND SUPPORT VESSELS FOR

EXPLORATION DRILLING

ROSNEFT DEMAND FOR SEISMIC SURVEY AND SUPPORT VESSELS

0

20

40

60

80

100

120

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Support vessels

Semi-submersible floating drillingrigs

Jackup drilling rigs

0

20

40

60

80

2016 2017 2018 2019 2020 2021 2022 2023

Support vessels

3D seismic vessels

2D seismic vessels

13 DEVELOPING INTEGRATED PETROCHEMICAL BUSINESS IN EASTERN RUSSIA

Angarsk petrochemicals company Refining volume: 10.4 mln tons Investment: 84 bln RUB Upgrade completion: 2017 Light yields: 65%

Achinsk refinery Refining volume: 6.9 mln tons Investment: 98 bln RUB Upgrade completion: 2017 Light yields: 88%

Angarsk polymers plant Petrochemicals (olefins): 0.7 mln tons Investment: 52 bln RUB Upgrade completion: post 2020

Komsomolsk refinery Refining volume: 8.0 mln tons Investment: 78 bln RUB Upgrade completion: 2018 Light yields: 83%

Vostochnaya petrochemicals company (FEPCO)

Refining volume: 12mln tons Construction completion: I stage in 2020, II stage in 2022 Conversion rate > 95% Petrochemicals (feedstock): 3.4 mln tons

Achinsk refinery

Komsomolsk refinery

Sakhalin LNG

Krasnoyarsk

Irkutsk Angarsk polymers plant Khabarovsk

Vladivostok Angarsk petrochemicals company Vostochnyaya

pertochemicals company

* - based on historical costs and Company business plan for 2015-19.

Developing modern petrochemical clusters. Investments into existent refining assets upgrades ~315* bln RUB

Rosneft priority – supplying regional markets with quality motor fuel and entering Asia-Pacific markets with high value-adding products

14 FEPCO PROJECT – MODERN REFINING AND PETROCHEMICAL COMPLEX

FEPCO Mongolia

China Japan South Korea

Russia

High quality motor fuels for the Company’s retail network

Gasoil , jet fuel, polyethylene, polypropylene, etc..

ESPO oil pipeline

Promising fields in East Siberia

FEPCO is located near largest sales markets

(Primorsk area – >50% fuel demand of the Far East

federal district; Asia-Pacific)

I stage: refining – 12 mmtpa

II stage: petrochemicals – 3.4 mmtpa

MOTOR FUEL PRODUCTION:

I, II stages – 8.5 mln tons

PETROCHEMICALS PRODUCTION:

I, II stages – 3.0 mln tons

Project status – preparing project documentation for the 1st and 2nd project stages, carrying out engineering surveys. Completion in 2016

Cooperation opportunities – attracting an investor/ partner into the project

117997, Moscow, Sofiyskaya emb., 26/1

Teleaphone: +7 (499) 517-88-99

Fax: +7 (499) 517-72-35

E-mail: [email protected]

CONTACT INFORMATION