ASEAN-CER Integration Partnership Forum Kuala Lumpur Saturday 25 June 2011.

66

ASEAN-CER Integration Partnership Forum Kuala Lumpur Saturday 25 June 2011

-

Upload

hector-goodwin -

Category

Documents

-

view

214 -

download

1

Transcript of ASEAN-CER Integration Partnership Forum Kuala Lumpur Saturday 25 June 2011.

ASEAN-CERIntegration Partnership Forum

Kuala Lumpur

Saturday 25 June 2011

Overview of Economic Integration Between Australia and New Zealand:

What HappenedHow it Happened

Presentation forIntegration Partnership ForumKuala Lumpur, 25 June 2011

Robert ScollayAPEC Study Centre

University of Auckland

Australia-New Zealand Economic Integration

• A Success Story But

• Success did not come easily– especially in the early years

• Always more to be done

• Focus first on manufactures, agriculture and services followed

• Free movement of labour – a “given” throughout the process one of the cornerstones of ANZ economic integration

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

NZ

$ m

illio

ns

June years

New Zealand's total merchandise trade with Australia since CER took effect

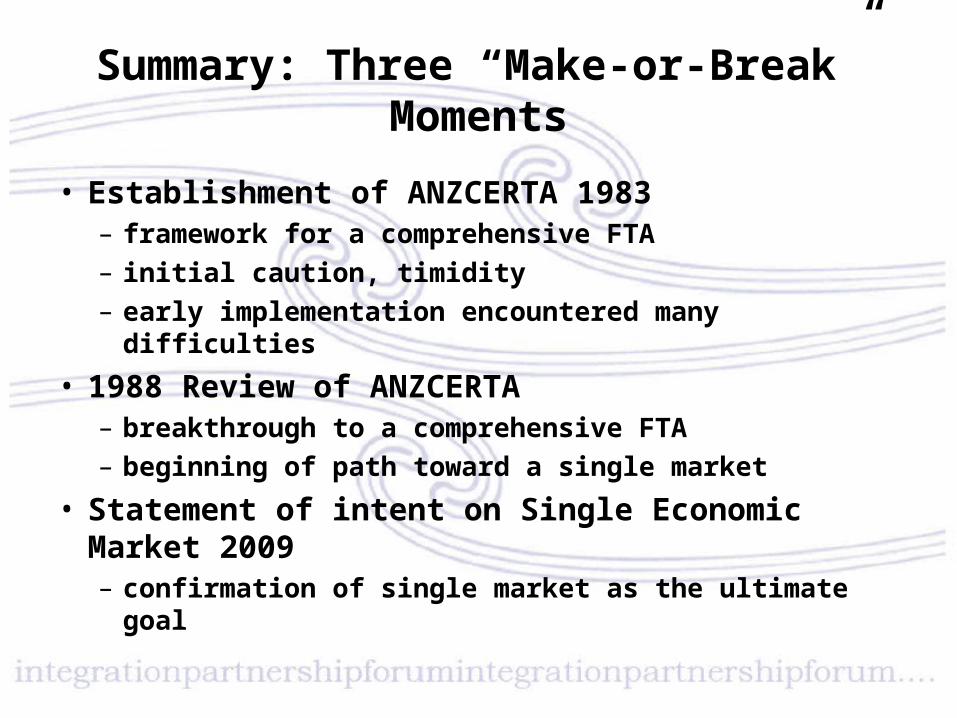

Summary: Three “Make-or-Break” Moments

• Establishment of ANZCERTA 1983– framework for a comprehensive FTA

– initial caution, timidity

– early implementation encountered many difficulties

• 1988 Review of ANZCERTA– breakthrough to a comprehensive FTA

– beginning of path toward a single market

• Statement of intent on Single Economic Market 2009– confirmation of single market as the ultimate goal

Before ANZCERTA……

..there was

•the original NAFTA (NZ-Australia FTA)– Positive list

– Limited coverage

– Increasingly difficult to extend

– Reached end of useful life by early 1980s

First “Make-or-Break” Moment: Establishment of ANZCERTA 1983

• Negative list agreement for free trade in goods• Furiously opposed by manufacturers (“Free Trade with Australia – A Step Too Far”)• Very cautious initially

– extensive negative list, special arrangements for agricultural products– lengthy phase-out periods for tariffs and NZ’s QRs– investment deliberately excluded, no coverage of services

• Initial implementation: difficult with some bickeringbut meantime– both countries began embracing comprehensive economic reform,

including unilateral MFN tariff reduction programmes– business gradually became more enthusiastic

(“CER – The Way Ahead”)

Second “Make-or-Break” Moment:1988 Review of ANZCERTA

• “End of the FTA Phase”– acceleration of free trade in goods – extension to free trade in services on negative list

basis

• “Beginning of the Single Market Phase”– elimination of anti-dumping on trans-Tasman trade– commitment on working to harmonise customs and

quarantine procedures– initial agreement on government procurement

Gradual Accumulation of Building Blocks for the Single Market

• 1990s– agreement on standards, accreditation, quality assurance– joint accreditation system for conformity assessment (JASANZ)– joint food standards and food standards authority– mutual recognition of standards and occupational qualifications (TTMRA)– enhanced arrangements on government procurement– double tax agreement– work on business law harmonisation– flow-on issues related to people movement addressed (eligibility for

welfare benefits, state-funded medical treatment, pensions; cost implications for each government)

– services• most remaining sectors progressively removed from the negative list• implementation issues addressed in some sectors

• Early mid-2000s: – single market concept placed on the agenda– focus on business law, competition and securities regulation issues– progress relatively slow– ANZ Leadership Forum began meeting 2004

• focusing support of business leaders in both countries

Third “Make-or-Break” Moment:Commitment to a Single Economic Market

• Joint Statement of Intent on SEM 2009– strong focus in initial work programme on competition and

regulatory issues (including enforcement), also IP– some elements completed, others nearing completion– other important issues remain to be resolved

• Major recent developments– adoption of new rules of origin 2009 (switch from RVC to CTC)– Treaty on Court Proceedings and Regulatory Enforcement 2009– Investment Protocol 2011

• beginning to fill a major gap in integration arrangements• progress on investment previously held back by various concerns over

– precedent setting– relation to broader investment policies– erosion of tax bases via application of dividend imputation provisions in both countries

How It HappenedFeatures of the Australia-NZ Integration Process

Leadership and Process•Political leadership at highest level (PMs) was crucial at “make-or-break” moments•Maintaining momentum through “ups and downs” facilitated by– close working relations at official level across many

government functions– periodic setting of broad objectives to be pursued

through well-defined processes•Objectives specified in broad terms rather than as detailed blueprints– often outcome focused

ASEAN – CER Integrated Partnership Forum

Evolution of CER to SEM

Geoff MillerPrincipal Adviser, Markets Group, Department

of the Treasury, Australia

Single Economic Market

“a geographic area comprising two or more countries in which there is no significant discrimination in the markets of each country arising from differences in the policies and regulations adopted by each country”

Scope of the SEM

• Business law (cross-border insolvency, company registration, mutual recognition of securities offerings);

• Prudential regulation (seamless banking, insurance, banking crisis and failure management);

• Superannuation (portability, interaction between the retirement income systems);

• Taxation (double tax agreements)

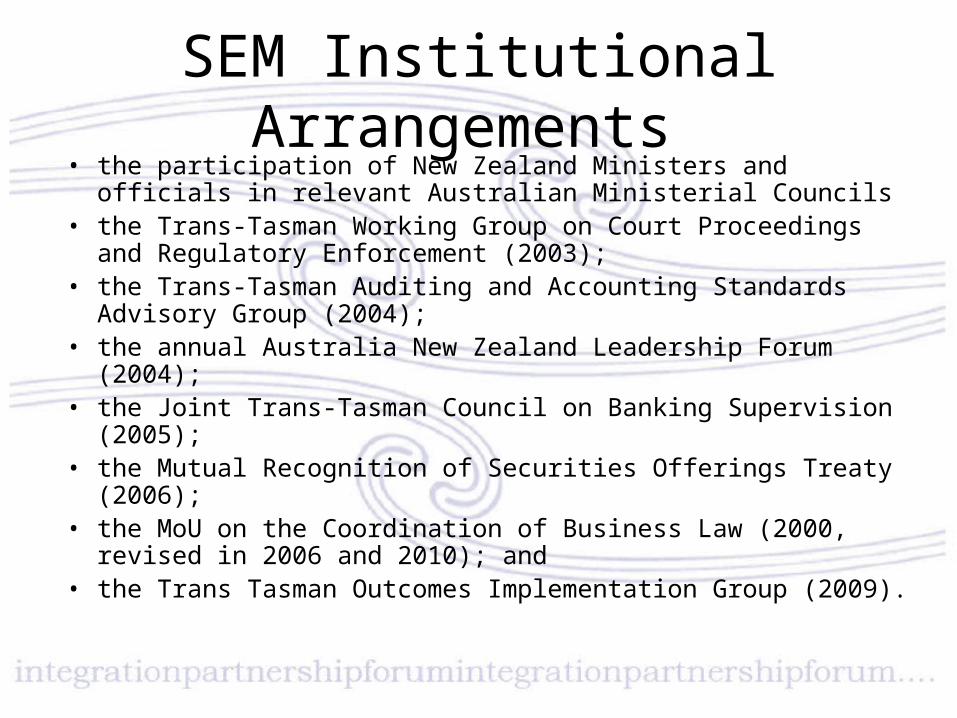

SEM Institutional Arrangements • the participation of New Zealand Ministers and officials in relevant

Australian Ministerial Councils• the Trans-Tasman Working Group on Court Proceedings and

Regulatory Enforcement (2003); • the Trans-Tasman Auditing and Accounting Standards Advisory

Group (2004); • the annual Australia New Zealand Leadership Forum (2004);• the Joint Trans-Tasman Council on Banking Supervision (2005); • the Mutual Recognition of Securities Offerings Treaty (2006); • the MoU on the Coordination of Business Law (2000, revised in

2006 and 2010); and• the Trans Tasman Outcomes Implementation Group (2009).

Memorandum of Understanding

• SEM is governed by the Memorandum of Understanding between the Government of New Zealand and the Government of Australia on the Coordination of Business Law

• The MOU sets out a framework of principles and a range of shared practical outcomes for developing cross border economic initiatives.

Memorandum of Understanding

• Original MOU signed in 1988 as the MOU on Business Law Harmonisation

• In 2000 old MOU replaced by a MOU on the Coordination of Business Law

• MOU on the Coordination of Business Law was revised and resigned in 2006 and 2010.

Vision of a single economic market

• No focus or sense of unity in purpose

• Harder to achieve legislative harmony

• Seemingly intractable issues around differing legal systems or sovereignty issues

• Time for a new approach

A new approach to the SEM

• Not identical laws but shared outcomes

• Shared outcomes could be achieved in any way each country felt necessary or appropriate

• In August 2009, a Joint Statement of Intent: Single Economic Market Outcomes Framework together with a framework of principles and outcomes proposals

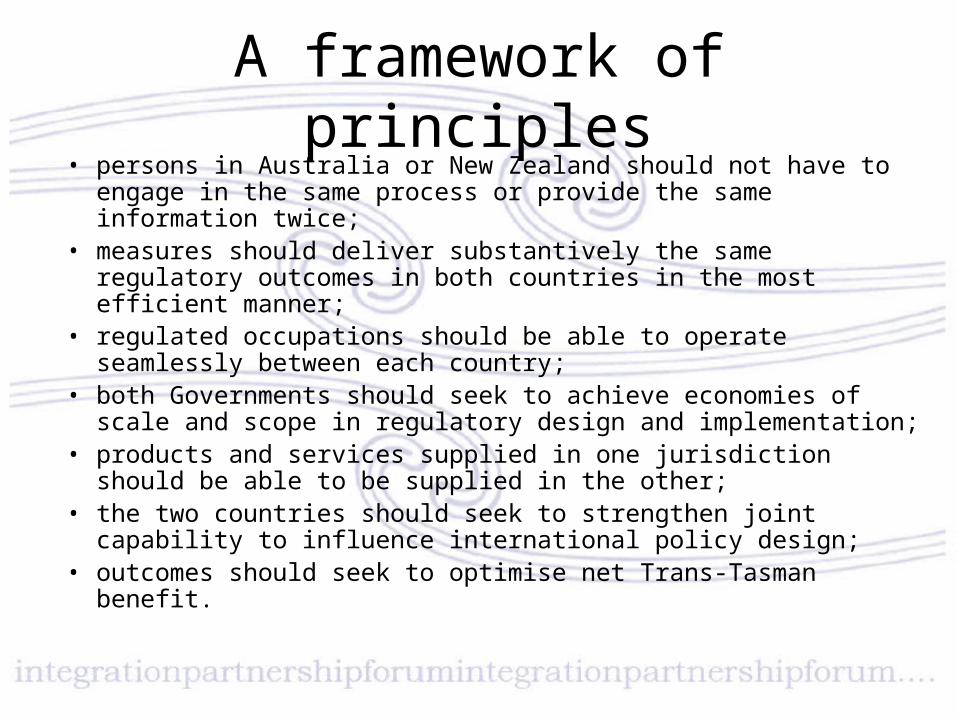

A framework of principles• persons in Australia or New Zealand should not have to engage in the

same process or provide the same information twice;• measures should deliver substantively the same regulatory outcomes

in both countries in the most efficient manner;• regulated occupations should be able to operate seamlessly between

each country;• both Governments should seek to achieve economies of scale and

scope in regulatory design and implementation;• products and services supplied in one jurisdiction should be able to be

supplied in the other;• the two countries should seek to strengthen joint capability to

influence international policy design; • outcomes should seek to optimise net Trans-Tasman benefit.

The work program

• Insolvency law• Financial reporting policy• Financial services policy• Competition policy• Business reporting• Corporations law• Personal property securities law• Intellectual property law• Consumer policy

Trans-Tasman Outcomes Implementation Group

• Ensure that the necessary processes are in place to advance the work;

• Monitor progress towards meeting the agreed outcomes;

• Identify areas of risk and seek to resolve issues;

• Report regularly to both Governments on progress in achieving the outcomes; and

• Make appropriate recommendations in relation to any changes to the initial list of proposed outcomes.

TTOIG website

www.treasury.gov.au/ttoig/

Case study Cross-border insolvency

• Australia adopted the United Nations Committee on International Trade Law (UNCITRAL) Model Law on Cross-Border Insolvency (Model Law) by passage of the Cross-Border Insolvency Act 2008

• New Zealand adopted the Model Law by its earlier legislation, the Insolvency (Cross-border) Act 2006

Case study Cross-border insolvency

• Although the Model Law provides an extremely flexible generic framework for governing cross-border insolvencies between countries with greatly differing legal systems, that flexibility can come at the cost of efficiency

• The pure legislative approach to harmonisation through model laws or strict alignment of laws did not lead to the expected harmonisation of regulation

Conclusion

• Aligning legislation in many cases would not and, in the case of Australia and New Zealand, did not result in regulatory harmonisation

• Harmonisation can occur when each country commits itself to achieving a shared outcome

• The mechanism for delivering that outcome is a means to an end, and not the outcome itself

A Business Perspective on Cross Border Agreements

Reflecting the Australia – New Zealand CER/SEM Experience

Kerry McDonald

Context for negotiations

• Business is the engine of an economy.

• It operates within the framework of government laws, policies and international agreements.

• This framework has a critical influence on the competitiveness and performance of business and strength of the economy.

• Business is now, of necessity, much more mobile, shifting investment readily in response to the competitiveness of different locations.

• Success in the intensively competitive globalized economy requires this.

• So, it is important, in terms of outcomes, that governments engage with business to understand its needs when developing the policy framework, including cross border agreements.

Related business perspectives

• As a businessman, when you understand what is possible you become impatient with anything less.

• In the modern World the speed of decision making has accelerated dramatically. A 90 to 180 day decision horizon often replaces one previously defined in years.

• It is often a struggle for policy makers to appreciate this.

The Evolution of the A-NZ Process

• The attitudes and role of business varied markedly through the process, with important implications for the rate of progress and the level of business support or frustration.

• 50 years ago, pre-globalisation the CER initiative was largely political, with some business support.

• Business generally was less outward looking, more reliant on subsidies and protection, and cautious.

• Over time both economies became more focused on reducing subsidies and increasing competition and competitiveness.

• In parallel, business became more engaged with and supportive of the CER process - but initially to maximize the gain for its home-base economy and minimize and loss of protection or other adverse impacts.

• Then, over the last 2 decades, with increasing globalisation and the rapid growth of Emerging Economies, the A-NZ business view shifted strongly, reflecting greater exposure to and awareness of international competition, it’s challenges and opportunities.

• It became a much more aligned, single view, across both economies, on steps needed to improve the competitiveness of both economies, in the face of globalisation – “we are in this together”!

• And, business became much more engaged and active with the CER/SEM processes, and increasingly impatient with slow-moving political leadership.

• The powerful unifying force was the competitive pressures in the market on both economies.

• It also sharpened the business focus on the domestic competitiveness benefits of leveraging off the CER/SEM change process to improve domestic policies and align them cross border.

• The CER/SEM processes became a vehicle for addressing domestic policy inefficiencies and barriers to competitiveness.

• The dominant business view became “we want the best, most efficient policy, whether it’s from Australia or NZ or elsewhere”.

• NZ business was apprehensive of A’s greater size, but increasingly focussed on the necessity and benefits of closer engagement with the larger economy.

• Some, mainly regulated, domestically focussed businesses, felt threatened and responded accordingly – but were a distinct minority.

The focus of the CER/SEM processes

• The initial focus was reducing trade barriers, especially tariffs.

• It evolved progressively to include non-tariff barriers and behind the border measures, such as standards, regulatory policies and processes, financial markets, investment, qualifications, tax harmonisation, etc.

• But, many of these changes were very slow and of limited scope.

• Post tariff reductions “behind the border” issues became more difficult as the benefits were more complex and domestic constituencies, which were less attuned to the importance of competitiveness, more resistant.

• On the other hand these issues, well handled, tended to have substantial competitiveness benefits.

The handbrake of politics

• As issues became more politically difficult progress slowed dramatically, in spite of the intense pressure on business to become more competitive, and from business for faster CER/SEM progress.

• In spite of the strong A-NZ business alignment post-CER progress has been slow.

The consequences

• CER meant major gains for business and the two economies, from tariff reductions and improved border processes and the increasing alignment of standards, financial markets, regulatory processes, and so on.

• In NZ, and perhaps to a lesser extent in Australia, it was part of a process of transformation to a more outwardly focussed, competitive economy.

• It probably also contributed to a closer social alignment, including in sport and culture – a stronger sense of shared opportunities and risks.

• In A-NZ business there is now a much stronger focus on the capability and performance of people, rather than their nationality.

• However, the slow pace of progress over at least the last decade has been costly for the two economies - probably NZ in particular.

• And the political reluctance was mirrored in the modest pace of domestic reform to improve competitiveness.

• The externally focussed, resource based sectors in the two economies are strong.

• This contrasts with the non-resource based parts of the two economies.

• In NZ’s case the output of the vital tradables sector (goods and services) peaked in about 2006 and has declined steadily since

• This reflects, to a substantial extent, a lack of competitiveness and the pressures of foreign competition.

• In this context, the very slow progress with CER/SEM initiatives is directly relevant.

• Such issues are not unique to Australia and New Zealand.

Session One: Q&A

Ambassador David Taylor

New Zealand

Services IntegrationExperiences of CER

Christopher FindlayUniversity of Adelaide

Why services integration matters

• Context of services industry development– Services sector grows with rising income levels –

demand and supply side factors

– But also there are new business models in services – supply chains matter like they do in goods

• Gains from international business– Gains from specialisation and access to variety

Why services integration matters (cont.)

• Costs in trading systems– Links to trade facilitation

• Participation matters– Value of reducing the costs of entering the trading

system

• Competition is the goal

Challenges of services reform

• Challenges• Nature of barriers

• Agencies involved,

• Continuing concerns about market failure, including the nature of competition

• How can trade agreements help?• Binding policy, guiding principles, schedules

• Concerns about diversion and competition

• Links to domestic reform

Approach in CER

• negative list• definitions• market access

• national treatment,

• access to the agreement• coverage of modes• mutual recognition• best endeavours

Assessments

• benchmark agreement compared to others– good coverage

– horizontal reservations not significant

– liberal rule of origin

– movement of people

• talking points– inscriptions, investment, business law

• impact studies – work in progress

Lessons

• Wider reform matters - services reform best driven by domestic reform agenda

• Leadership is important – define the goal

• Engagement from within – an important driver which can be mobilised

• Continuing process – as times change and shocks occur

Australia and New ZealandEstablishing joint bodies

Marc Mowbray-d’Arbela

Assistant SecretaryLegislative Review Branch

Department of Finance and Deregulation

Australia

Options for countries wishing to achieve a common approach to a particular activity

• Unilateral reform in one country to align its practices with another countryor

• Bilateral non-legally binding undertakingsor

• Bilateral legally binding commitments- such as the establishment of a joint body

Australia New Zealand Therapeutic Products Authority (Proposed)

• A joint body to replace 2 existing bodies

• Purpose – to regulate common standards for therapeutic goods in both countries

• Would have an enforcement role in both countries

Difficulties

• Involved both countries adjusting some of their normal internal approaches.

• Whole process took much longer and was more difficult than anticipated

Advantages

• Trade off was there would be considerable advantages for both countries

• Lower compliance costs for business

• Lower administration costs for both governments

• Increased regulatory effectiveness

• Greater strategic understanding

Lessons learned

1. Consider more than one option for cooperation

2. Don’t under-estimate the task

3. Differences between jurisdictions matter

4. Identify clear net benefits

5. Ensure clear political authority

Lessons learned

6. Agreements and decisions reached need to be scrupulously recorded

7. There is a need for dispute resolution mechanisms

8. Always bear in mind that the parties are sovereign nations and we have different political systems

Lessons learned

9. Seek and use specialist knowledge across respective bureaucracies

10. Apply existing organisational governance principles

Lessons learned

• Paper jointly developed in 2007 by New Zealand and Australia

• Title: “Arrangements for Facilitating Trans-Tasman Government Institutional Cooperation” – http://www.finance.gov.au/publications/arrangements-for-f

acilitating-trans-tasman-co-operation/index.html

Looking forward

• In most economic activity there will be a presumption in favour of cooperation

• Need to be alert for any unintended consequences for the other party

• Specifically, Australia and New Zealand recently agreed to resurrect the joint Therapeutic Products Authority project

CER/SEM: Lessons Learned

Simon Murdoch

Former Chief Executive, Department of Prime Minister and Cabinet

Former Secretary of Foreign Affairs and Trade

New Zealand

Integration Partnership Forum

Saturday 25 June 2011

Kuala Lumpur