Ascendas Hospitality Trust Presentation of Roadshow...

33

Presentation of 1Q FY2013/14 Financial Results 7 August 2013 Ascendas Hospitality Trust Roadshow Presentation August 2013 Ascendas Hospitality Trust 2Q FY2013/14 Financial Results Presentation 12 November 2013

Transcript of Ascendas Hospitality Trust Presentation of Roadshow...

Presentation of 1Q FY2013/14

Financial Results

7 August 2013

Ascendas Hospitality Trust Roadshow Presentation

August 2013

Ascendas Hospitality Trust 2Q FY2013/14 Financial Results

Presentation

12 November 2013

2

Important Notice This presentation on A-HTRUST’s unaudited financial results for the second quarter ended 30 September 2013 (“2Q FY2013/14”) should be read in conjunction with A-HTRUST’s full financial statements, a copy of which is available on www.sgx.com or www.a-htrust.com.

This presentation may contain forward-looking statements that involve risks and uncertainties. Actual future performance, outcomes and results may differ materially from those expressed in forward-looking statements as a result of a number of risks, uncertainties and assumptions. Representative examples of these factors include (without limitation) general industry and economic conditions, interest rate trends, cost of capital and capital availability, competition from similar developments, shifts in expected levels of average daily room rates and occupancy, changes in operating expenses, including employee wages, benefits and training, property expenses and governmental and public policy changes and the continued availability of financing in the amounts and the terms necessary to support future business. You are cautioned not to place undue reliance on these forward looking statements, which are based on the Manager’s current view of future events. The value of securities in A-HTRUST (“Securities”) and the income derived from them, if any, may fall as well as rise. Securities are not obligations of, deposits in, or guaranteed by, the Manager or any of its affiliates. An investment in Securities is subject to investment risks, including the possible loss of the principal amount invested. Investors should note that they will have no right to request the Manager to redeem or purchase their Securities for so long as the Securities are listed on the SGX-ST. It is intended that investors and security holders of A-HTRUST may only deal in their Securities through trading on the SGX-ST. Listing of the Securities on the SGX-ST does not guarantee a liquid market for the Securities. The past performance of A-HTRUST is not necessarily indicative of the future performance of A-HTRUST. Any discrepancies in the figures included herein between the individual amounts and total thereof are due to rounding.

Contents

Key Highlights

Financial Performance

Portfolio Performance

Capital Management

Outlook

4

Key Highlights

2Q FY2013/14 results included new contributions from Ibis Beijing Sanyuan and Park Hotel Clarke Quay:

Gross Revenue: S$53.1 million

Net property income (“NPI”): S$21.3 million

Distribution per unit (“DPU”): 1.41 cents

Revenue per available room (“RevPAR”) of the Australia hotels increased following completion of asset enhancement works

Latest acquired Park Hotel Clarke Quay won “Singapore’s Leading City Hotel” at the 20th Annual World Travel Awards in October 2013

In current advanced discussions on refinancing the loans of the Australia and Japan portfolio, which upon completion, will extend the debt maturity profile from 2.2 years to more than 3.0 years

Financial Performance

5

6

Results Highlights

2Q FY2013/14 2Q FY2012/13(1)

S$’ mil Actual IPO

Forecast Variance Actual Variance

Gross Revenue 53.1 59.0 (10.1%) 38.1 39.4%

Net Property Income 21.3 20.7 2.9% 12.6 68.7%

NPI Margin 40.1% 35.0% 5.1pp 33.2% 6.9pp

Distribution Income 14.6 14.9 (2.1%) 8.7 67.3%

Distribution Per Unit (cents)

1.41 1.85 (23.8%) 1.26(2) 11.9%

(1) 2Q FY2012/13 financial results included 65-days income contribution from 27 July 2012 (IPO date) to 30 Sept 2012; while 2Q FY2013/14 financial results included 92-days income contribution and income from Park Hotel Clarke Quay and Ibis Beijing Sanyuan.

(2) Taking into account waiver sponsor distribution

7

2Q FY2013/14 2Q FY2012/13(1)

S$’ mil Actuals IPO Forecast Variance(2) Actuals Variance(2)

Australia

Revenue 39.4 47.7 (17.4%) 31.7 24.4%

Net Property Income 13.0 15.6 (16.6%) 9.9 31.6%

China

Revenue 5.5 5.4 0.2% 2.2 146.9%

Net Property Income 1.9 1.5 23.1% 0.6 222.9%

Japan

Revenue 4.7 5.9 (20.4%) 4.2 12.4%

Net Property Income 2.9 3.6 (18.3%) 2.4 22.2%

Singapore

Revenue 3.5 - nm - nm

Net Property Income 3.5 - nm - nm

(1) Computation is based on the financials rounded to the nearest dollar. (2) 2Q FY2012/13 results included 65-days income contribution from 27 July 2012 (IPO date) to 30 Sept 2012; while 2Q

FY2013/14 results included 92-days income contribution and income from Park Hotel Clarke Quay and Ibis Beijing Sanyuan.

8

Distribution Details

Distribution Period 10 June 2013 to 30 September 2013 (1)

1Q FY2013/14 0.26 cents

2Q FY2013/14 1.41 cents

Total 1.67 cents

(1) An Advance Distribution for the period 1 April 2013 to 9 June 2013 was paid to Stapled Securityholders on 30 July 2013.

Notice of Books Closure Date 12 November 2013

Ex-Date 18 November 2013, 9.00 am

Books Closure Date 20 November 2013, 5.00 pm

Distribution Payment Date 20 December 2013

Timetable

9

Portfolio Performance

10

Foreign Exchange Impact

NPI for 2Q FY2013/14 exceeded the IPO Forecast by S$0.6 million or 2.9%, mainly due to contribution from Park Hotel Clarke Quay

Adjusting to exclude the unfavourable currency movements, NPI exceeded the IPO Forecast by S$2.2 million or 10.4%

Actual

IPO Forecast

Variance Attributable to

Assets Performance

FX Movement

S$’ mil S$’ mil S$’ mil %

S$’ mil % S$’ mil %

Australia 13.0 15.6 (2.6) (16.6%) (1.7) (11.0%) (0.9) (5.6%)

China 1.9 1.5 0.4 23.1% 0.3 18.4% 0.1 4.7%

Japan 2.9 3.6 (0.7) (18.3%) 0.1 2.9% (0.8) (21.2%)

17.8 20.7 (2.9) (14.0%) (1.3) (6.5%) (1.6) (7.5%)

Singapore 3.5 - 3.5 nm 3.5 nm - nm

Total 21.3 20.7 0.6 2.9% 2.2 10.4% (1.6) (7.5%)

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Jul- 12 Aug- 12 Sep- 12 Oct- 12 Nov- 12 Dec- 12 Jan- 13 Feb- 13 Mar- 13 Apr- 13 May- 13 Jun- 13 Jul- 13 Aug- 13 Sep- 13 Oct- 13

AUD/SGD JPY/SGD CNY/SGD

11

Foreign Exchange Movements

Exchange rate movements from IPO to 30 September 2013

AUD/SGD

JPY/SGD

RMB/SGD

9.4%

3.0%

21.3%

Source: OANDA

33.9

11.2

33.0

24.4

7.6

31.1

38.4

12.6

32.7

2Q FY2013/14

2Q FY2012/13

IPO Forecast

82.8

159 132

84.3

160 135

83.4

176 147

NPI Margin (%)

Revenue (AUD’mil)

NPI (AUD’mil)

RevPAR (AUD)

Occupancy (%)

ADR (AUD)

12

Australia Asset Performance

1.5pp

2.2% 0.6%

39.1%

47.4%

1.9pp

87.6

404

350

80.5

535

431

85.2

419

354

26.5

9.2

34.7

11.3

3.0 26.5

27.5

7.8

28.3

2Q FY2013/14

2Q FY2012/13

IPO Forecast

13

China Asset Performance

NPI Margin (%)

Revenue (RMB’mil)

NPI (RMB’mil)

RevPAR (RMB)

Occupancy (%)

ADR (RMB)

134.8%

8.2pp

207.2%

7.1pp

24.5%

18.8%

14

Japan Asset Performance

Revenue (JPY’mil)

NPI Margin (%)

NPI (JPY’mil)

369.6

225.9

61.1

266.6

138.7

52.0

368.4

219.6

59.6

2Q FY2013/14

2Q FY2012/13

IPO Forecast

38.6%

62.9%

9.1pp

15

A-HTRUST Asset Portfolio Net property income by segments for 2Q FY2013/14

By geography By type of contracts

Australia 61.0%

China 8.9%

Japan 13.6%

Singapore 16.5%

Master Lease 30.0%

Management Contracts 70.0%

16

A-HTRUST Asset Portfolio Valuation by property and geography(1)

Tokyo 16%

Beijing 8%

Sydney 26%

Brisbane 14%

Cairns 3%

Singapore 23%

Australia(2) 53% Courtyard by Marriott Sydney – North Ryde 4%

Pullman Sydney 9% Novotel Sydney Central 8%

Novotel Sydney Parramatta 5% Pullman and Mercure Albert Park 10%

Pullman and Mercure Brisbane KGS 14% Pullman Cairns International 3%

China(3) 8% Ibis Beijing 4%

Novotel Beijing 4%

Japan(3) 16%

Hotel Sunroute Ariake & B:Conte 16%

Singapore(4) 23%

Park Hotel Clarke Quay 23%

(1) The valuation refers to the revaluated net asset value of the properties, which includes the revaluation of land use rights of the China hotels (2) Valuation by Jones Lang LaSalle and Knight Frank as of 31 March 2013 (3) Valuation by DTZ as of 31 March 2013 (4) Valuation by Colliers International as of 31 March 2013

Melbourne 10%

Completed Asset Enhancements

17

Completed rebranding and refurbishment works of six Australia hotels

managed by Accor

Media Coverage

18

Pullman Melbourne Albert Park

“To sum up my stay at the Pullman Melbourne Albert Park all I can say is that it far surpassed my expectations and my one night stay was too short to fully appreciate all it has to offer. It is a stylish modern five-star hotel that offers the best in guest rooms, leisure facilities and dining options….It is the ideal upscale hotel for business and leisure in Melbourne.”

The Holiday & Travel Magazine

Travel Daily, 4 Sept 2013 The Holiday & Travel Magazine,

7 Oct 2013 Weekend Australian, 5 Oct 2013 Sydney Morning Herald, 5 Oct

2013 The Saturday Age, 5 Oct 2013 West Australian, 13 Oct 2013

19

Asset Enhancements Impact

RevPAR Before AEI After AEI Change

Pullman Sydney Hyde Park July – Sep 12 July – Sep 13

12.7% 138 155

Novotel Sydney Parramatta July – Sep 12 July – Sep 13

6.1% 119 126

Pullman Brisbane King George Square

May – Sep 12 May – Sep 13 -3.1%

167 161

Pullman Cairns International Mar – Sep 12 Mar – Sep 13

-2.5% 117 114

Novotel Sydney Central & Pullman Melbourne Albert Park only completed the

refurbishment works in August 2013

Media Coverage

20

Award-winning Hotel Park Hotel Clarke Quay won “Singapore’s Leading City Hotel” at the 20th Annual World

Travel Awards in October 2013 - an award hailed as the “Oscars of the travel industry” and

recognised worldwide as the hallmark of industry excellence

World Travel Awards is hailed as the “Oscars of the travel industry” and recognised worldwide as the hallmark of industry excellence….

21

Park Hotel Clarke Quay

July – August 2013

against mid-tier market(1)

Occupancy +1.0pp

Average Daily Rate (ADR) +6.7%

Revenue per Available Room (RevPAR) +7.3%

(1) Source: STB’s survey on ‘Return of Tourist Hotel on Room Lettings and Food & Beverage Sales Turnover’ as at 26 Sep 2013.

22

Capital Management

23

Healthy Balance Sheet

As of 30 September 2013

Total Debt S$485.6 million

Total Assets S$1,357.1 million

A-HTRUST Gearing (1) 35.8%

- A-HREIT Gearing (1) 30.5%

- A-HBT Gearing (1) 39.2%

Effective Borrowing Rate 2.9%

Weighted Average Debt to Maturity 2.2 years

Net Asset Value per unit S$0.76

(1) Gearing is computed based on total debt over total assets

1

62

13

256

49

53

53

0

50

100

150

200

250

300

2013 2014 2015 2016 2017 2018

JPY100m Bond Japan Hotel S$13m RCF

Australia Hotels China Hotels Singapore Hotel

24

Debt Profile

Debt Maturity Profile Debt Currency Profile

Interest Rate Profile

Weighted average debt maturity of 2.2 years S$’mil

Refinancing of loans for the Australia and Japan portfolio in progress, which will extend the weighted debt maturity to more than 3.0 years

SGD 62.3%

AUD 26.3%

RMB 4.8%

JPY 6.6%

Fixed 97.4%

Floating 2.6%

25

Currency Hedging

Distributable Income

The Managers hedges 100% of A-HTRUST’s distributable income as soon as the amount has been earned from foreign assets and can be reasonably estimated.

In view of the continued volatility in foreign currency movements, the Managers have reviewed its existing income hedging strategy of hedging the earned income on a monthly basis.

Estimated distributable income is now hedged up to 15 months forward to allow a longer coverage period and reduce the exposure of A-HTRUST’s distributable income to forex risks.

Balance Sheet

The Managers do not hedge its equity.

Currently, 50% of A-HTRUST’s borrowings are in local currencies (AUD, JPY & RMB) for its foreign assets.

The Managers are currently in advanced discussions to refinance 100% of the loans for Australia and Japan assets in local currencies.

26

Outlook

27

Market Outlook

Australia economy is expected to remain soft with the continuing rise in unemployment rate and substantial drag from weaker mining investment

Managers are working closely with hotel managers on various initiatives (e.g. advertising & promotional activities) to increase revenue

Positive signs that the Japan economy is turning around Winning the bid to host the 2020 Olympics should boost

business and consumer sentiment Weaker Japanese Yen should trigger growth of domestic

and international accommodation demand

28

China economy expanded 7.8% year-on-year (“y-o-y”) in 3Q 2013, up from 7.5% in 2Q 2013(1)

Decline in international visitor arrivals to Beijing, but domestic visitor arrivals remain strong

Oversupply of hotel accommodation, mainly in upscale segment

Based on advance estimates released by the MITI(2), Singapore economy grew 5.1% on a y-o-y basis in 3Q 2013, as compared to 4.2% growth in 2Q 2013

8.5% y-o-y growth in international visitor arrivals from Jan to Aug 2013; and hotel occupancy rates remains strong above 85% from Jan to Sept 2013 (3)

Hospitality prospects are expected to remain healthy with the expected opening of Singapore Sports Hub and the National Art Gallery

Market Outlook

(1) Source: National Bureau of Statistics of China (2) The Ministry of Trade & Industry (3) Singapore Tourism Board

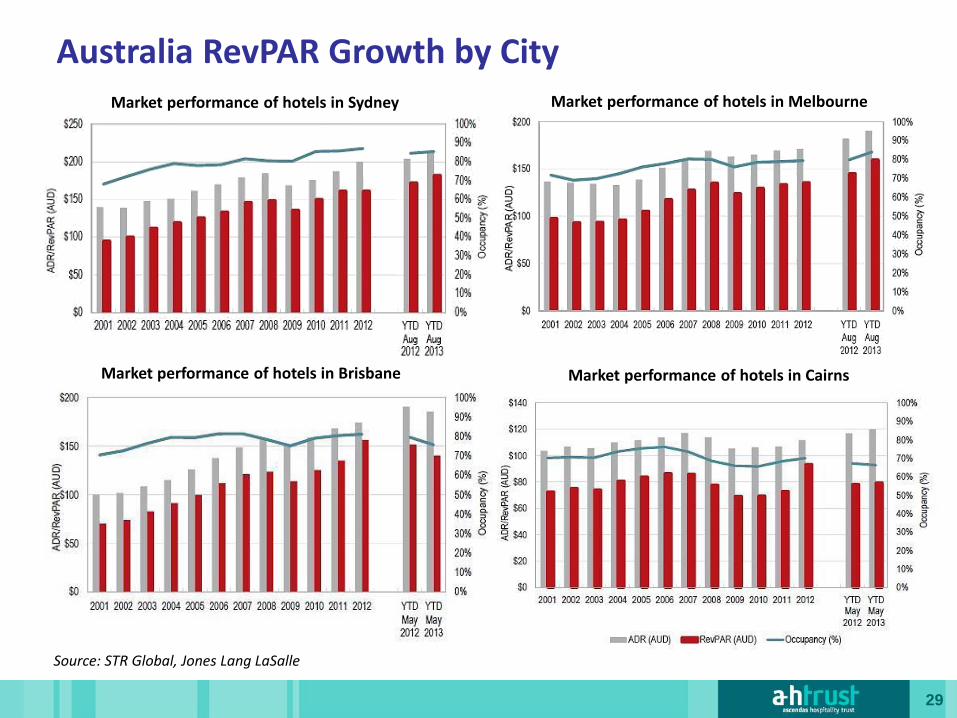

Australia RevPAR Growth by City

29

Market performance of hotels in Sydney Market performance of hotels in Melbourne

Source: STR Global, Jones Lang LaSalle

Market performance of hotels in Brisbane Market performance of hotels in Cairns

30

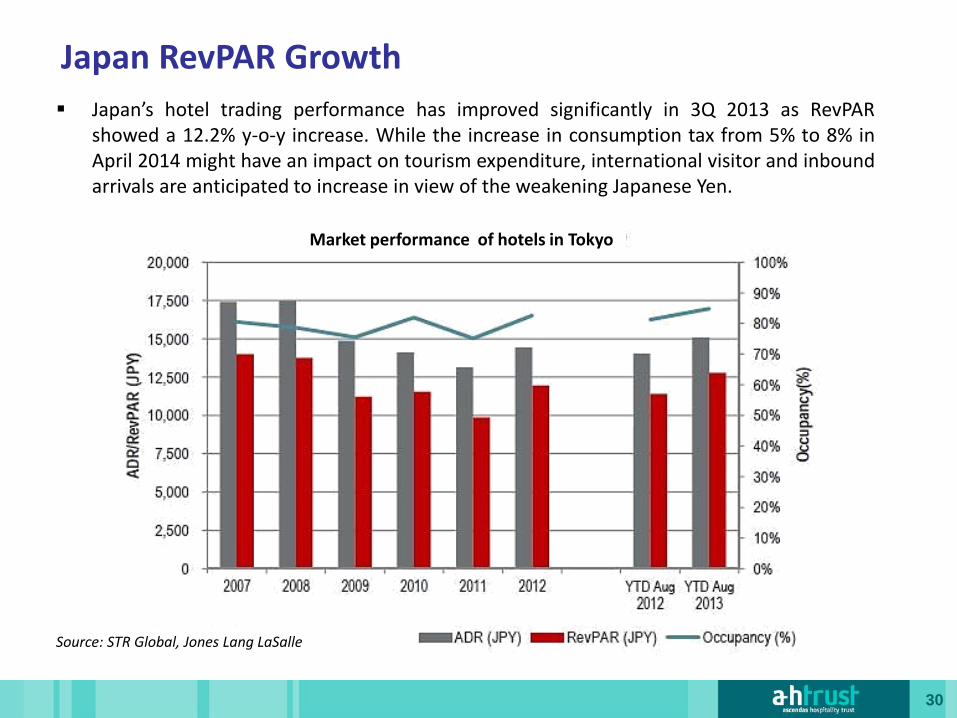

Japan RevPAR Growth

Japan’s hotel trading performance has improved significantly in 3Q 2013 as RevPAR showed a 12.2% y-o-y increase. While the increase in consumption tax from 5% to 8% in April 2014 might have an impact on tourism expenditure, international visitor and inbound arrivals are anticipated to increase in view of the weakening Japanese Yen.

Market performance of hotels in Tokyo

Source: STR Global, Jones Lang LaSalle

31

Beijing RevPAR Growth

Beijing four-star hotels’ performance recorded a decline in 3Q 2013 due to the reduction in visitor arrivals during 3Q 2013. As at YTD August 2013, occupancy declined 3.0 percentage points to 68.1%, ADR decreased 3.3% y-o-y and RevPAR decreased 7.4% y-o-y.

Market performance of four-star hotels in Beijing

Source: STR Global, Jones Lang LaSalle

32

Source: STR Global, Jones Lang LaSalle

Performance of midscale hotels in Singapore declined in 3Q 2013 due to increase in hotel supply. As at YTD August 2013, occupancy declined 0.6 percentage points to 86.6%, ADR decreased 0.7% y-o-y and RevPAR declined 3.8% y-o-y.

Market performance of midscale hotels in Singapore

Singapore RevPAR Growth

33