Ascend Aircraft Investment Index -...

20

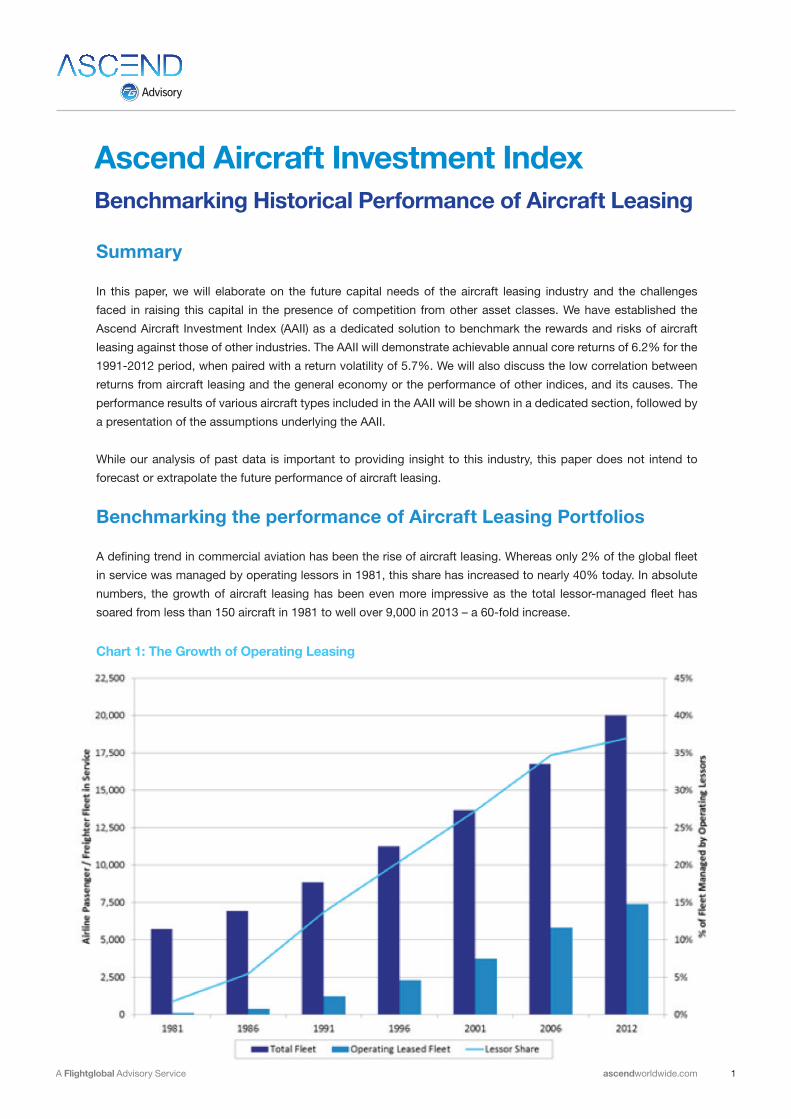

1 A Flightglobal Advisory Service ascendworldwide.com Ascend Aircraft Investment Index Summary In this paper, we will elaborate on the future capital needs of the aircraft leasing industry and the challenges faced in raising this capital in the presence of competition from other asset classes. We have established the Ascend Aircraft Investment Index (AAII) as a dedicated solution to benchmark the rewards and risks of aircraft leasing against those of other industries. The AAII will demonstrate achievable annual core returns of 6.2% for the 1991-2012 period, when paired with a return volatility of 5.7%. We will also discuss the low correlation between returns from aircraft leasing and the general economy or the performance of other indices, and its causes. The performance results of various aircraft types included in the AAII will be shown in a dedicated section, followed by a presentation of the assumptions underlying the AAII. While our analysis of past data is important to providing insight to this industry, this paper does not intend to forecast or extrapolate the future performance of aircraft leasing. Benchmarking the performance of Aircraft Leasing Portfolios A defining trend in commercial aviation has been the rise of aircraft leasing. Whereas only 2% of the global fleet in service was managed by operating lessors in 1981, this share has increased to nearly 40% today. In absolute numbers, the growth of aircraft leasing has been even more impressive as the total lessor-managed fleet has soared from less than 150 aircraft in 1981 to well over 9,000 in 2013 – a 60-fold increase. Benchmarking Historical Performance of Aircraft Leasing Chart 1: The Growth of Operating Leasing

-

Upload

phungquynh -

Category

Documents

-

view

352 -

download

5

Transcript of Ascend Aircraft Investment Index -...

1A Flightglobal Advisory Service ascendworldwide.com

Ascend Aircraft Investment Index

Summary

In this paper, we will elaborate on the future capital needs of the aircraft leasing industry and the challenges

faced in raising this capital in the presence of competition from other asset classes. We have established the

Ascend Aircraft Investment Index (AAII) as a dedicated solution to benchmark the rewards and risks of aircraft

leasing against those of other industries. The AAII will demonstrate achievable annual core returns of 6.2% for the

1991-2012 period, when paired with a return volatility of 5.7%. We will also discuss the low correlation between

returns from aircraft leasing and the general economy or the performance of other indices, and its causes. The

performance results of various aircraft types included in the AAII will be shown in a dedicated section, followed by

a presentation of the assumptions underlying the AAII.

While our analysis of past data is important to providing insight to this industry, this paper does not intend to

forecast or extrapolate the future performance of aircraft leasing.

Benchmarking the performance of Aircraft Leasing Portfolios

A defining trend in commercial aviation has been the rise of aircraft leasing. Whereas only 2% of the global fleet

in service was managed by operating lessors in 1981, this share has increased to nearly 40% today. In absolute

numbers, the growth of aircraft leasing has been even more impressive as the total lessor-managed fleet has

soared from less than 150 aircraft in 1981 to well over 9,000 in 2013 – a 60-fold increase.

Benchmarking Historical Performance of Aircraft Leasing

Chart 1: The Growth of Operating Leasing

2 ascendworldwide.com A Flightglobal Advisory Service

Aircraft leasing is expected to grow even further, with the fleet under management to double over the next 15

years. As regular fleet renewals are necessary to keep up with market requirements, the aircraft leasing industry

will require hundreds of billions of US dollars in capital investment. These needs are unlikely to be matched by

the current capital providers for aircraft leasing, as the aviation sector would weigh significantly higher on their

balance sheets. Therefore, attracting new, yet untapped, capital sources will be a key factor for the future success

of the aircraft leasing industry.

There are a number of factors which make aircraft leasing an interesting investment proposition: the asset is highly

mobile yet protected by international agreements, operator risk is reduced by high lessee diversification paired

with good asset management, and the large-ticket nature of aircraft paired with expected fleet growth allow for

investment of large sums.

Before the Lehman shock, the focus of investors was on the reward potential of investments, but this has undeniably

shifted towards aspects such as investment risk, the steadiness of returns and counter-cyclical behavior. This

is understandable since the heralded benefits of diversification proved non-existent when several, seemingly

unrelated, asset classes collapsed in unison during the crash. There was nothing to provide support for investors’

equity as many of these asset classes were not backed by physical collateral.

In order to attract new capital sources, the aircraft leasing industry needs to prove its appeal in the face of

competition from other more established investment sectors. But how can this be done in the absence of any

industry-wide transparent metric? The creation of a credible industry benchmark is important for potential investors

to make informed investment decisions when comparing aircraft leasing and its alternatives. The acute need for

such a benchmark has led Ascend to create the Ascend Aircraft Investment Index (AAII), an unlevered monthly

index based on the performance of an aircraft leasing portfolio.

Ascend Aircraft Investment Index – Methodology

Indices have proven to be effective instruments that track and benchmark the performances of various

business sectors or investment strategies (e.g. S&P MidCap 400, S&P SmallCap, S&P 500). In addition,

they can capture aspects such as return volatility and return correlation with the performance of the general

economy or other assets.

In order to create an index, we have to adopt an underlying model that simulates the way an aircraft leasing

portfolio functions and its respective returns over the period of measurement. We also need to specify assumptions

concerning the investment strategy that will be undertaken for the hypothetical aircraft leasing portfolio.

The aircraft portfolio model underlying the AAII is able to simulate the various strategies pursued by an aircraft

leasing company.

3A Flightglobal Advisory Service ascendworldwide.com

In this paper, we will analyse the case of the so-called “passive strategy” and will refer to the index as “AAII

Passive”. The passive strategy precludes any active trading in the portfolio in reaction to temporary market

developments. It allows us to measure the core returns from leasing, which can be used as a yardstick for the

performance of any active strategy. The details of the passive strategy are explained in depth in the next section

and in the Appendix.

The aircraft portfolio leasing model underlying the AAII is based on the way a real aircraft leasing portfolio functions.

The model simulates the essential processes in a leasing portfolio, such as acquisitions and disposals of aircraft,

and the placement of aircraft on consecutive leases. Its inputs are based on Ascend’s historical Market Values and

Lease Rates to accurately mirror past circumstances.

When calculating the monthly returns from the portfolio, the model includes factors such as asset appreciation/

depreciation, lease stream, lessor fees, capital expenditure for new acquisitions and capital gains from asset

disposals (if any).

The Total Rate of Return for a single month is derived as follows:

= (PortƒCMVt – PortƒCMVt-1 ) – (NewAcquist + Disposalst ) + (LeaseRentalst – Feest) x 100

(PortƒCMVt-1 + NewAcquist)

where PortƒCMVt denotes the portfolio Market Value at the end of month t

PortƒCMVt-1 denotes portfolio Market Value at the end of month t-1

NewAcquist is the capital expenditure of investing in new aircraft in month t

Disposalst is the revenue earned from the disposal of aircraft in month t

LeaseRentalst denotes the monthly lease income

Feest denotes management and lessor fees and other expenses (e.g. for reconfiguration)

Passive Strategy – Annual Acquisition Process

When employing a passive strategy, new aircraft are acquired at Market Values at the beginning of each year,

irrespective of the economic cycle, after which the aircraft are placed on a series of leases at Market Lease Rates

and are kept in the portfolio for 25 years. This implies that no aircraft disposals are made until the aircraft spend

25 years within the portfolio.

Annual acquisitions are done in January of each year, when up to five aircraft between the ages zero to four years

old (one aircraft at each age) of each type are purchased. There are no limits on the acquisition budget. Therefore,

should all five ages of a type be in existence in a given year, they will be added to the portfolio.

When calculating the portfolio return, the AAII model assumes that assets are purchased, held and sold at Full-Life

Market Values.

It is assumed that the aircraft will be returned in full-life condition at the end of a lease. A more detailed description

of the acquisition process is presented in the Appendix.

4 worldwide.com A Flightglobal Advisory Service

Passive Strategy – Lease Placement Cycle and Associated Costs

When an aircraft is acquired, it is leased at the historical Market Lease Rate for that aircraft type and vintage. The

calculated lease rate is the actual rent recorded for this aircraft in the market when purchased and will only change

when a new lease occurs after the initial term.

To reflect the leasing market, the lease term is defined as 10 years for twin-aisle aircraft and seven years for

single-aisle aircraft in the index, while all subsequent leases are defined as five years, regardless of the aircraft

classification. Each aircraft is assumed to operate for 25 years, after which it will be sold at its Market Value at

that point in time.

The associated costs of transitioning aircraft between operators are included in this index and detailed in the

Appendix.

The contribution of each aircraft to the portfolio’s performance is determined by the acquisition process (which

determines the number of each type’s aircraft in the portfolio), the aircraft’s Market Value and Market Lease Rates.

It is not weighted by the historical composition of the general aircraft leasing market, although it can be simulated

by the model.

Comparative performance of AAII

Using the passive strategy, the AAII index shows the following returns:

Table 1: AAII Results

Chart 2: Ascend Aircraft Investment Index (1991-2012)

Period ReturnStandard deviation

1991-2000 7.1% 2.4%

2000-2013 5.4% 7.5%

1991-2013 6.2% 5.7%

5A Flightglobal Advisory Service ascendworldwide.com

The chart below shows the performance of AAII Passive (black curve), as well as general stock indices (S&P 500,

MSCI World Index) and sector indices (S&P 500 Airlines Index, Dow Jones Transportation Index, S&P Railroads

Index, S&P Global Property Index).

The remarkably smooth shape of the AAII Passive curve contrasts with the more volatile lines for the other

benchmarks. The dips in the AAII Passive curve after the recessions of 2001 and 2008 are small compared with

the steep falls for other indices, while the growth for the rest of the period is noticeably stable and devoid of any

sudden rises. This suggests a low volatility of returns provided by the underlying aircraft leasing portfolio. Where

does such low volatility stem from?

The inherent characteristic of a properly structured aircraft leasing portfolio is the stacked re-lease process, where

only a certain portion of aircraft require new lessees each year. This is modeled by the AAII underlying portfolio,

where around 15-18% of a narrowbody fleet is re-leased in each year as a result of the continuous acquisition

process and a five to seven year lease term (depending on whether it is a first or a later lease).

As a longer first lease term is assumed for widebodies (10 years for the first lease, five years for subsequent

lease-terms), this ratio will be even lower for widebody assets. Since lease rates are typically agreed upon at

the beginning of the lease and continue until their expiration, one of the main components of the profitability

Chart 3: Ascend Aircraft Investment Index – Comparative Performance Benchmark

6 worldwide.com A Flightglobal Advisory Service

equation is insulated from market conditions for 85-90% of the portfolio fleet. Although lease rates are sometimes

renegotiated, mainly if a lessee runs into significant financial troubles, this is not the norm.

Good returns, paired with low volatility, promise a favourable profit-to-risk return. Low volatility also implies that

the returns from the portfolio are largely independent of cyclical movements. The fact that the AAII curve has

a visibly different shape from other curves, which largely have a similar profile, suggests that the AAII has a

low correlation with other indices. This would be a highly desired characteristic that allows for genuine portfolio

diversification and insulation of returns from temporary market swings. It is important to note that this does not

appear to be as achievable with other indices, since they all move in the same direction and closely track the

general economy to a high degree.

A comparison with alternative investment benchmarks, such as shipping or precious metal indices, tells a similar

story. The AAII has had the steadiest growth path and clearly outperformed the shipping indices. Although it was

outpaced by the precious metal indices in 2010, this could be a transitory development as investors rallied to

gold and silver in the wake of the global financial crisis and European sovereign debt crisis. While the AAII has

continued to increase, the precious metal indices have remained stagnant since mid-2011.

A popular finance approach used to compare investments in different assets is the Sharpe ratio. The Sharpe ratio

is calculated as the asset class return, less US Treasuries, divided by the asset class standard deviation.

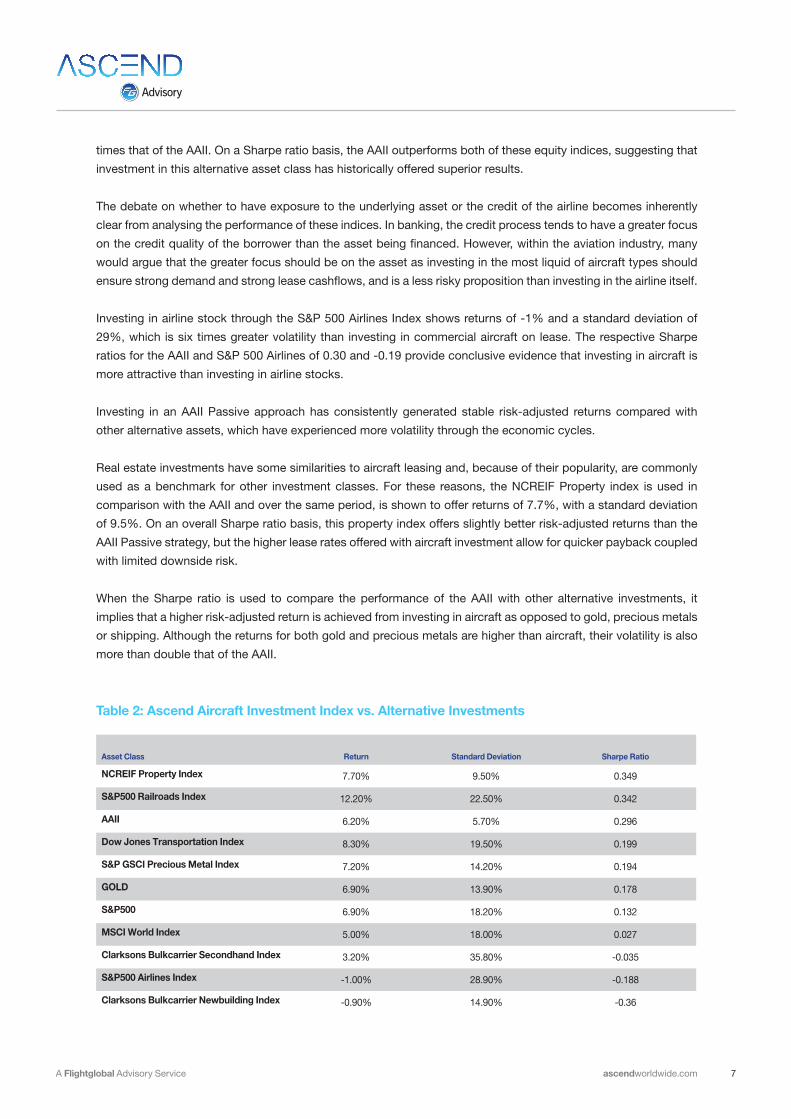

The passive strategy shows that investment in commercial aircraft offers an attractive risk- adjusted return as

compared with other investment classes. The unleveraged return of 6.2% over the 21-year period compares

favorably to returns offered by the S&P 500 (6.9%) and MSCI World Index (5%), whose volatility is almost four

Chart 4: Ascend Aircraft Investment Index vs. Alternative Investments

7A Flightglobal Advisory Service ascendworldwide.com

times that of the AAII. On a Sharpe ratio basis, the AAII outperforms both of these equity indices, suggesting that

investment in this alternative asset class has historically offered superior results.

The debate on whether to have exposure to the underlying asset or the credit of the airline becomes inherently

clear from analysing the performance of these indices. In banking, the credit process tends to have a greater focus

on the credit quality of the borrower than the asset being financed. However, within the aviation industry, many

would argue that the greater focus should be on the asset as investing in the most liquid of aircraft types should

ensure strong demand and strong lease cashflows, and is a less risky proposition than investing in the airline itself.

Investing in airline stock through the S&P 500 Airlines Index shows returns of -1% and a standard deviation of

29%, which is six times greater volatility than investing in commercial aircraft on lease. The respective Sharpe

ratios for the AAII and S&P 500 Airlines of 0.30 and -0.19 provide conclusive evidence that investing in aircraft is

more attractive than investing in airline stocks.

Investing in an AAII Passive approach has consistently generated stable risk-adjusted returns compared with

other alternative assets, which have experienced more volatility through the economic cycles.

Real estate investments have some similarities to aircraft leasing and, because of their popularity, are commonly

used as a benchmark for other investment classes. For these reasons, the NCREIF Property index is used in

comparison with the AAII and over the same period, is shown to offer returns of 7.7%, with a standard deviation

of 9.5%. On an overall Sharpe ratio basis, this property index offers slightly better risk-adjusted returns than the

AAII Passive strategy, but the higher lease rates offered with aircraft investment allow for quicker payback coupled

with limited downside risk.

When the Sharpe ratio is used to compare the performance of the AAII with other alternative investments, it

implies that a higher risk-adjusted return is achieved from investing in aircraft as opposed to gold, precious metals

or shipping. Although the returns for both gold and precious metals are higher than aircraft, their volatility is also

more than double that of the AAII.

Asset Class Return Standard Deviation Sharpe Ratio

NCREIF Property Index 7.70% 9.50% 0.349

S&P500 Railroads Index 12.20% 22.50% 0.342

AAII 6.20% 5.70% 0.296

Dow Jones Transportation Index 8.30% 19.50% 0.199

S&P GSCI Precious Metal Index 7.20% 14.20% 0.194

GOLD 6.90% 13.90% 0.178

S&P500 6.90% 18.20% 0.132

MSCI World Index 5.00% 18.00% 0.027

Clarksons Bulkcarrier Secondhand Index 3.20% 35.80% -0.035

S&P500 Airlines Index -1.00% 28.90% -0.188

Clarksons Bulkcarrier Newbuilding Index -0.90% 14.90% -0.36

Table 2: Ascend Aircraft Investment Index vs. Alternative Investments

8 worldwide.com A Flightglobal Advisory Service

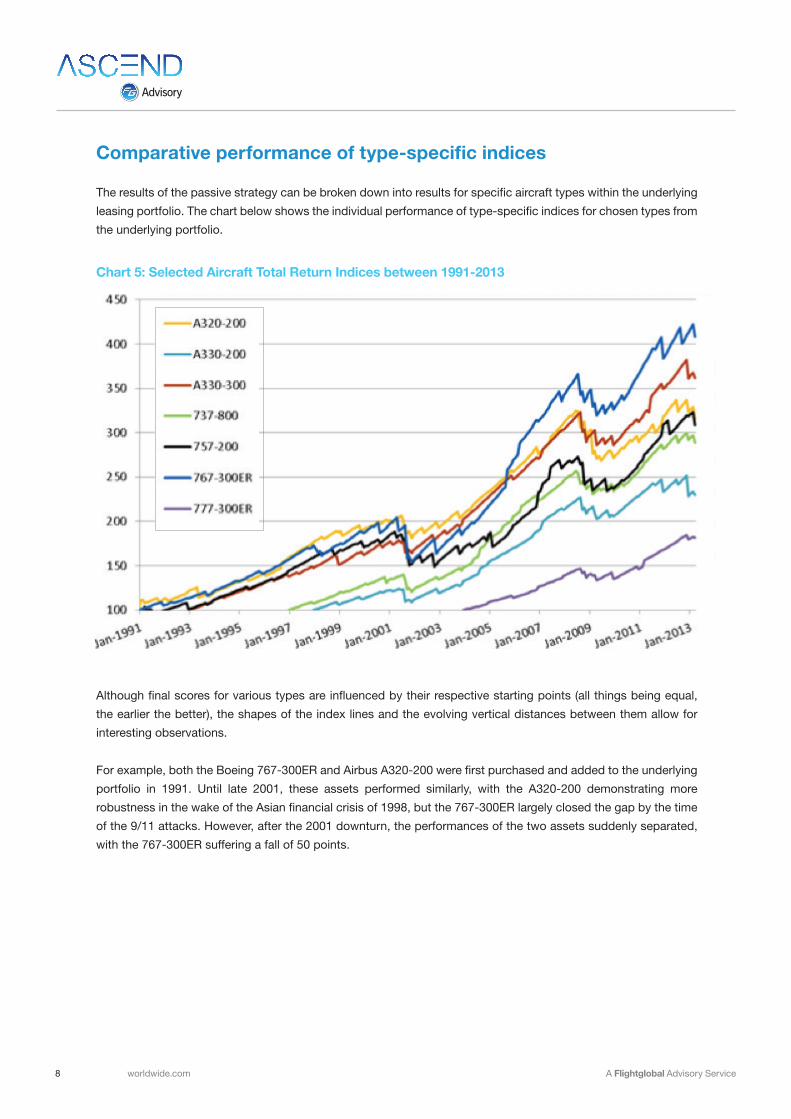

Comparative performance of type-specific indices

The results of the passive strategy can be broken down into results for specific aircraft types within the underlying

leasing portfolio. The chart below shows the individual performance of type-specific indices for chosen types from

the underlying portfolio.

Although final scores for various types are influenced by their respective starting points (all things being equal,

the earlier the better), the shapes of the index lines and the evolving vertical distances between them allow for

interesting observations.

For example, both the Boeing 767-300ER and Airbus A320-200 were first purchased and added to the underlying

portfolio in 1991. Until late 2001, these assets performed similarly, with the A320-200 demonstrating more

robustness in the wake of the Asian financial crisis of 1998, but the 767-300ER largely closed the gap by the time

of the 9/11 attacks. However, after the 2001 downturn, the performances of the two assets suddenly separated,

with the 767-300ER suffering a fall of 50 points.

Chart 5: Selected Aircraft Total Return Indices between 1991-2013

9A Flightglobal Advisory Service ascendworldwide.com

This fall was due to greater volatility in the 767-300ER’s Market Values, which fell by 20-25% during Q3 2001.

The value loss for the A320-200 was much more moderate and in the region of 10%. As the market started to

recover around 2003, so did the values of the 767-300ER. And with the extra lift from the Boeing 787 delays, the

depreciation of the 767-300ER values was effectively arrested for the next five years, until late 2008.

During that time, the 767-300ER index caught up again and in 2005, overtook that of the A320-200. Despite this

dynamic convergence and recent robust performance, the presence of steep value falls suggests that the 767-

300ER has been a volatile asset.

On the other hand, the Airbus A330-300 index, which started two years later than the A320-200 and the 767-

300ER indices, converges with them by 2004. Although its current level is still below the level of the 767-300ER

index (but above the A320-200 curve), its line displays the smoothest profile of the three. This suggests that the

A330-300 returns had the lowest volatility, and possibly outperformed the 767-300ER and the A320-200 indices

in terms of risk-adjusted returns.

By benchmarking the Boeing 737-800 and Boeing 757-200 returns, we are provided some interesting insights.

The 757-200 index started in 1991, while the 737-800 began in 1997 when the 757-200 index already had risen to

166 points. However, after seven years the difference between the two disappeared, indicating that performance

of the 757-200 in the period of 2001-2005 has been weak, and the 737-800 has proven to be a stellar investment.

Since 2005, these two indices have moved in tandem. The recession following 9/11 has shifted the 757-

200 values to such a point that when combined with a more robust lease rate, it was able to offer attractive

profitability from 2005.

This demonstrates that aircraft assets can have periods of poor performance followed by strong returns

once different components (Market Values or Market Lease Rates) of the lease return formula move to

appropriate levels.

10 worldwide.com A Flightglobal Advisory Service

Charting the results in a scatter chart will allow us to remove the bias introduced by the differing starting points of

the indices and to get a better understanding of return-to-risk profiles. The graph below shows the returns (Y axis)

and volatility (standard deviation of returns on X axis).

In the chart above, we can see the clear winners and losers of the 1991-2012 period. The 737-800 has been the

best performing asset in terms of profitability and has had medium volatility. The A330-300 and the 777-300ER

have scored well on returns and even better in terms of volatility. The 767-300ER provides a mixed picture, with

returns comparable to that of the A330-300 but with double the volatility.

One of those apparent losers is the A320-200, with below-average returns and average volatility. The 757-200

has scored even worse with lower average returns and higher volatility than the A320-200. However, if we only

consider the 2005-2012 period, the 757-200 would have been one of the winners in terms of profitability, with an

average return of 7% (although coupled with an elevated volatility of 9.3%).

Chart 6: Historical Returns / Standard Deviation for Selected Types, 1991-2012

11A Flightglobal Advisory Service ascendworldwide.com

A complete table with the returns and risk profiles for all types included in the underlying portfolio can be found

in the Appendix.

Market volatility driving stronger correlations between asset classes

When selecting asset classes to invest in, investors are not only concerned with expected return and risk but

must also look at the correlation between their investments. Correlation is a statistical measure which indicates

the degree to which the prices of two assets move together. Correlation between two assets is 1.0 when the two

assets move completely in tandem. It is -1.0 if the price of asset A always goes up when the price of asset B goes

down. Correlation is 0 if the two assets move completely independently of each another.

Holding assets that have no correlation or low positive or negative correlation can offer investors some protection

against downside. The importance of correlation has intensified since the 2008 downturn, where increased market

volatility has increased the correlation between asset classes. The focus on holding a diversified portfolio means

that investors are now seeking out new opportunities that offer stable and uncorrelated returns.

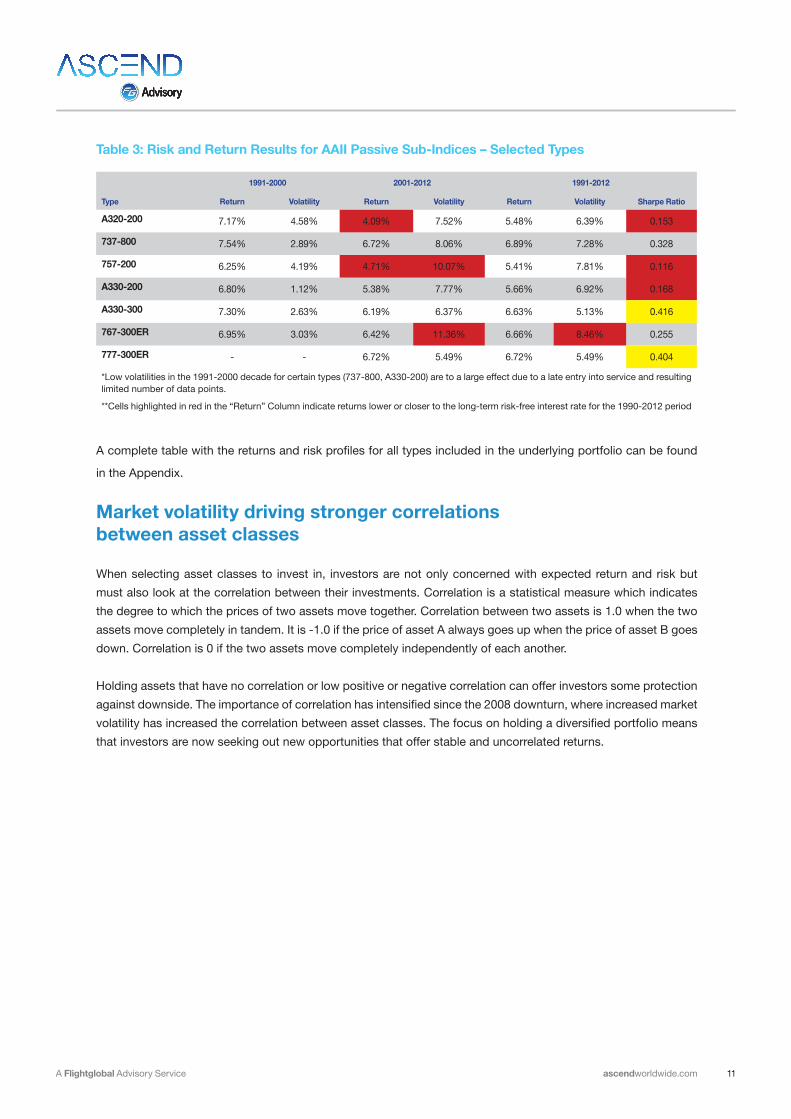

Table 3: Risk and Return Results for AAII Passive Sub-Indices – Selected Types

1991-2000 2001-2012 1991-2012

Type Return Volatility Return Volatility Return Volatility Sharpe Ratio

A320-200 7.17% 4.58% 4.09% 7.52% 5.48% 6.39% 0.153

737-800 7.54% 2.89% 6.72% 8.06% 6.89% 7.28% 0.328

757-200 6.25% 4.19% 4.71% 10.07% 5.41% 7.81% 0.116

A330-200 6.80% 1.12% 5.38% 7.77% 5.66% 6.92% 0.168

A330-300 7.30% 2.63% 6.19% 6.37% 6.63% 5.13% 0.416

767-300ER 6.95% 3.03% 6.42% 11.36% 6.66% 8.46% 0.255

777-300ER - - 6.72% 5.49% 6.72% 5.49% 0.404

*Low volatilities in the 1991-2000 decade for certain types (737-800, A330-200) are to a large effect due to a late entry into service and resulting limited number of data points.

**Cells highlighted in red in the “Return” Column indicate returns lower or closer to the long-term risk-free interest rate for the 1990-2012 period

12 worldwide.com A Flightglobal Advisory Service

To this end, the AAII Passive strategy satisfies these requirements as it has low positive/negative correlation with

all asset classes listed in the tables below. The correlation ranges are broken into four groupings;

1. Red represents high correlation less than or equal to -70% and greater than or equal to 70%

2. Yellow represents medium correlation less than or equal to -50% and greater than or equal to 50%

3. Green represents low correlation less than or equal to -15% and greater than or equal to 15%

4. White represents no correlation

To protect against the downside, investing in a combination of assets that fall between the ranges identified in 2-4

above are best. The tables below show the correlations between asset classes for the periods of 1991-2000 and

2001-2012.

During the 1991-2000 period there was low correlation between the AAII Passive index and all other asset classes.

Table 4: Correlation from 1991 to 2000

Type

Ascend Aircraft Investment Index

S&P 500

MSCI World Index

Dow Jones Transportation Index

S&P 500 Railroads Sub Industry Index

S&P 500 Airlines Index

S&P Global Property Index

Baltic Dry Index Gold

S&P GSCI Precious Metal Index

NCREIF Property Index

Clarkson - Bulkcarrier Newbuilding Price

Ascend Aircraft Investment Index

1 -13% -18% 3% 48% 9% 12% 15% -20% -6% -5% 20%

S&P 500 -13% 1 77% 63% -7% 36% 6% -47% -26% -33% 25% 2%

MSCI World Index

-18% 77% 1 31% -4% -2% -10% -19% 27% 22% 20% 6%

Dow Jones Transportation Index

3% 63% 31% 1 -2% 69% 25% -55% -30% -32% -26% 54%

S&P 500 Railroads Sub Industry Index

48% -7% -4% -2% 1 -46% -9% -15% -5% -5% -47% -31%

S&P 500 Airlines Index

9% 36% -2% 69% -46% 1 29% -39% -49% -40% 29% 49%

S&P Global Property Index

12% 6% -10% 25% -9% 29% 1 -14% 19% 17% -13% 48%

Baltic Dry Index

15% -47% -19% -55% -15% -39% -14% 1 6% 10% -1% 24%

Gold -20% -26% 27% -30% -5% -49% 19% 6% 1 96% -27% 8%

S&P GSCI Precious Metal Index

-6% -33% 22% -32% -5% -40% 17% 10% 96% 1 -22% 12%

NCREIF Property Index

-5% 25% 20% -26% -47% 29% -13% -1% -27% -22% 1 -30%

Clarkson - Bulkcarrier Newbuilding Price Index

20% 2% 6% 54% -31% 49% 48% 24% 8% 12% -30% 1

13A Flightglobal Advisory Service ascendworldwide.com

Table 5: Correlation from 2001 to 2012

The increased volatility in the markets following 9/11 and the liquidity crisis in 2008 have resulted in stronger

correlation between different asset classes in the 2001-2012 cycle. While the relationship between the AAII

Passive index and other assets remains in the medium-to-low range, there has been an increase in its correlation

with other assets. However, from assessing both periods, it is evident that by adding the AAII Passive Index to a

portfolio of equities, property or other alternative assets, it would reduce the overall volatility of a total portfolio

investment, and provide higher returns and lower risk.

Type

Ascend Aircraft Investment Index

S&P 500

MSCI World Index

Dow Jones Transportation Index

S&P 500 Railroads Sub Industry Index

S&P 500 Airlines Index

S&P Global Property Index

Baltic Dry Index Gold

S&P GSCI Precious Metal Index

NCREIF Property Index

Clarkson - Bulkcarrier Newbuilding Price

Ascend Aircraft Investment Index

1 40% 45% 52% 29% 13% 34% -1% 38% 42% 64% 69%

S&P 500 40% 1 98% 90% -26% 80% 88% 58% 43% 53% 1% 26%

MSCI World Index

45% 98% 1 90% -33% 80% 90% 63% 48% 57% 0% 33%

Dow Jones Transportation Index

52% 90% 90% 1 -24% 80% 84% 35% 31% 45% 8% 40%

S&P 500 Railroads Sub Industry Index

29% -26% -33% -24% 1 -48% -25% -70% -16% -13% 70% 7%

S&P 500 Airlines Index

13% 80% 80% 80% -48% 1 72% 52% 41% 54% -40% -3%

S&P Global Property Index

34% 88% 90% 84% -25% 72% 1 58% 34% 46% -3% 28%

Baltic Dry Index

-1% 58% 63% 35% -70% 52% 58% 1 53% 50% -53% -4%

Gold 38% 43% 48% 31% -16% 41% 34% 53% 1 98% 2% 18%

S&P GSCI Precious Metal Index

42% 53% 57% 45% -13% 54% 46% 50% 98% 1 3% 19%

NCREIF Property Index

64% 1% 0% 8% 70% -40% -3% -53% 2% 3% 1 63%

Clarkson - Bulkcarrier Newbuilding Price Index

69% 26% 33% 40% 7% -3% 28% -4% 18% 19% 63% 1

Appendix

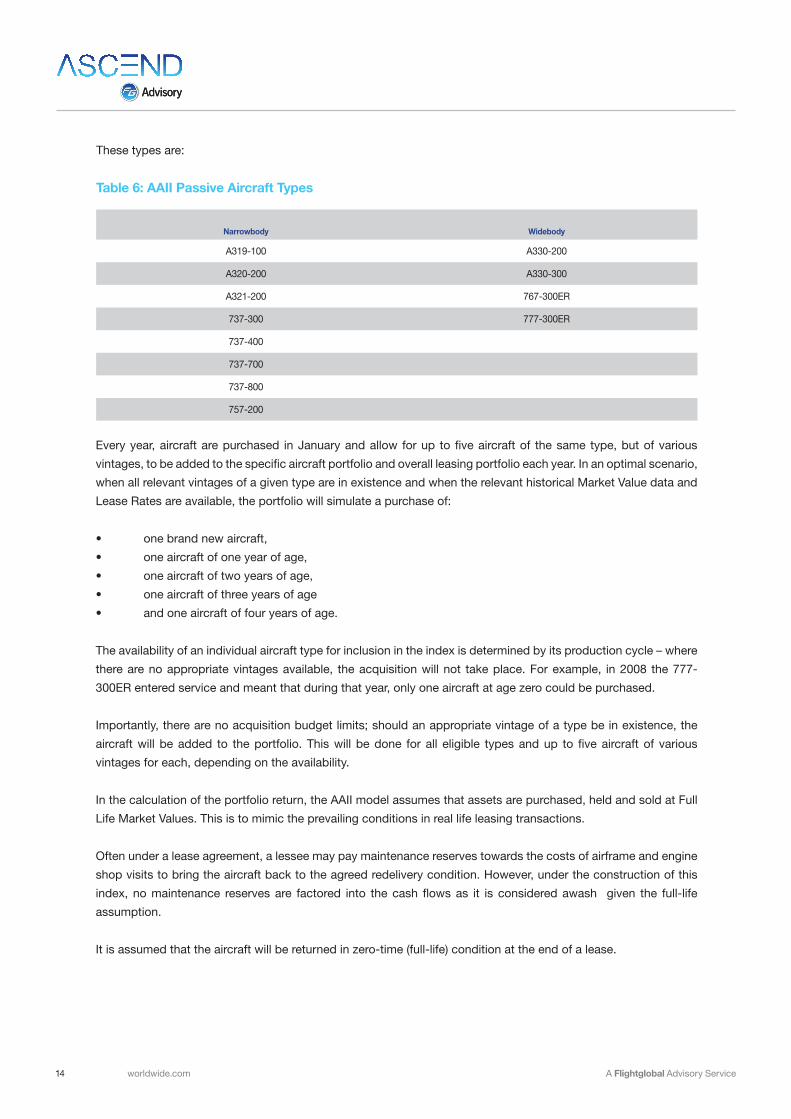

Annual Acquisition Process

The annual acquisition is limited to aircraft in the early life cycle stage (zero to four years) and are conducted for

the most popular aircraft types held by the leasing community over the past 20 years. These aircraft cover the four

categories of narrowbodies, widebodies, regional jets (RJs) and turboprops.

14 worldwide.com A Flightglobal Advisory Service

These types are:

Table 6: AAII Passive Aircraft Types

Narrowbody Widebody

A319-100 A330-200

A320-200 A330-300

A321-200 767-300ER

737-300 777-300ER

737-400

737-700

737-800

757-200

Every year, aircraft are purchased in January and allow for up to five aircraft of the same type, but of various

vintages, to be added to the specific aircraft portfolio and overall leasing portfolio each year. In an optimal scenario,

when all relevant vintages of a given type are in existence and when the relevant historical Market Value data and

Lease Rates are available, the portfolio will simulate a purchase of:

• one brand new aircraft,

• one aircraft of one year of age,

• one aircraft of two years of age,

• one aircraft of three years of age

• and one aircraft of four years of age.

The availability of an individual aircraft type for inclusion in the index is determined by its production cycle – where

there are no appropriate vintages available, the acquisition will not take place. For example, in 2008 the 777-

300ER entered service and meant that during that year, only one aircraft at age zero could be purchased.

Importantly, there are no acquisition budget limits; should an appropriate vintage of a type be in existence, the

aircraft will be added to the portfolio. This will be done for all eligible types and up to five aircraft of various

vintages for each, depending on the availability.

In the calculation of the portfolio return, the AAII model assumes that assets are purchased, held and sold at Full

Life Market Values. This is to mimic the prevailing conditions in real life leasing transactions.

Often under a lease agreement, a lessee may pay maintenance reserves towards the costs of airframe and engine

shop visits to bring the aircraft back to the agreed redelivery condition. However, under the construction of this

index, no maintenance reserves are factored into the cash flows as it is considered awash given the full-life

assumption.

It is assumed that the aircraft will be returned in zero-time (full-life) condition at the end of a lease.

15A Flightglobal Advisory Service ascendworldwide.com

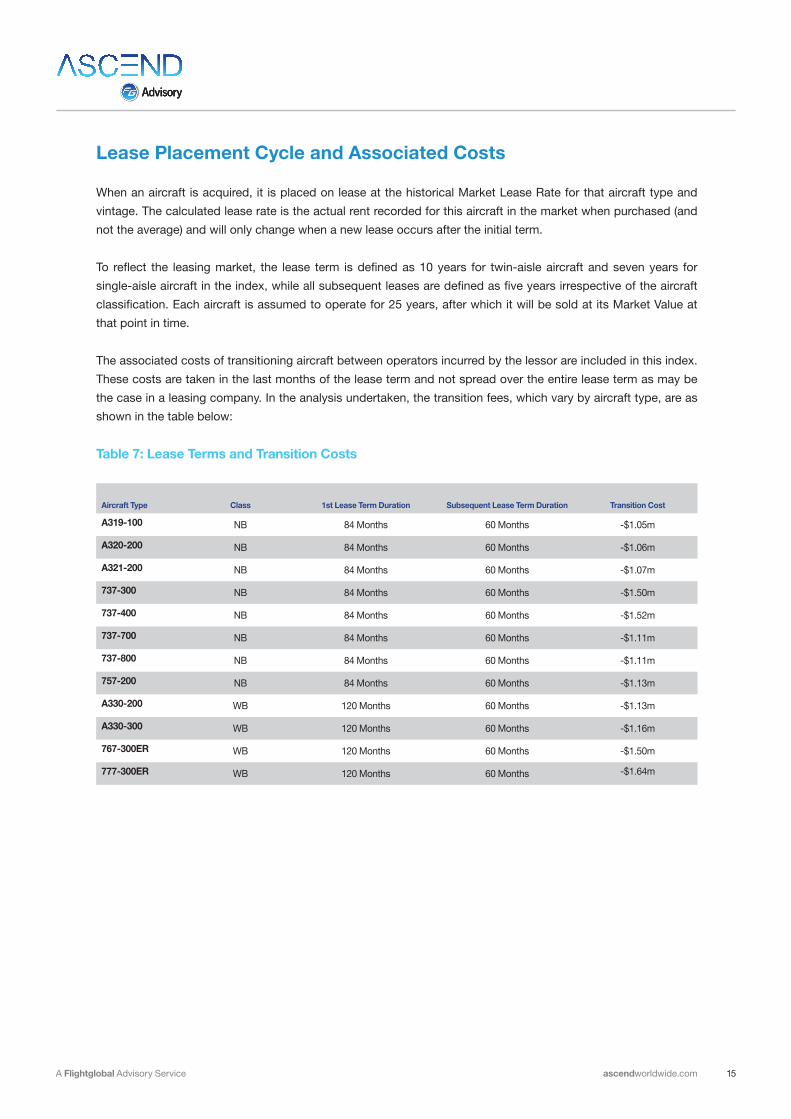

Lease Placement Cycle and Associated Costs

When an aircraft is acquired, it is placed on lease at the historical Market Lease Rate for that aircraft type and

vintage. The calculated lease rate is the actual rent recorded for this aircraft in the market when purchased (and

not the average) and will only change when a new lease occurs after the initial term.

To reflect the leasing market, the lease term is defined as 10 years for twin-aisle aircraft and seven years for

single-aisle aircraft in the index, while all subsequent leases are defined as five years irrespective of the aircraft

classification. Each aircraft is assumed to operate for 25 years, after which it will be sold at its Market Value at

that point in time.

The associated costs of transitioning aircraft between operators incurred by the lessor are included in this index.

These costs are taken in the last months of the lease term and not spread over the entire lease term as may be

the case in a leasing company. In the analysis undertaken, the transition fees, which vary by aircraft type, are as

shown in the table below:

Table 7: Lease Terms and Transition Costs

Aircraft Type Class 1st Lease Term Duration Subsequent Lease Term Duration Transition Cost

A319-100 NB 84 Months 60 Months -$1.05m

A320-200 NB 84 Months 60 Months -$1.06m

A321-200 NB 84 Months 60 Months -$1.07m

737-300 NB 84 Months 60 Months -$1.50m

737-400 NB 84 Months 60 Months -$1.52m

737-700 NB 84 Months 60 Months -$1.11m

737-800 NB 84 Months 60 Months -$1.11m

757-200 NB 84 Months 60 Months -$1.13m

A330-200 WB 120 Months 60 Months -$1.13m

A330-300 WB 120 Months 60 Months -$1.16m

767-300ER WB 120 Months 60 Months -$1.50m

777-300ER WB 120 Months 60 Months -$1.64m

16 worldwide.com A Flightglobal Advisory Service

As a result of the nature of leasing, the risk of downtime between leases is factored in by applying an adjustment

multiplier to the lease stream during the lease term. For example a 1% discount (multiplier of 0.99) for a 60-month

lease term is equivalent to 0.6 months of lease stream. Storage costs are accounted for in the transition costs in

the table above.

In developing this passive strategy, a management fee of 3% of lease rates was taken into account, to be charged

on monthly lease revenue.

AAII Result Tables and Charts

The graph below shows the returns and volatilities of each aircraft type and their development over the periods of

1991-2000 and 2001-2012. For each of the selected types, these two periods are represented individually by the

smaller symbols (with labels), while the combined 1991-2012 period is represented by a larger symbol (no label)

between the two. As shown, there has been a noticeable dip in performance during the second period for each

aircraft type.

Table 8: Downtime and Market Lease Rates Adjustment Factors

Aircraft Type1st Lease Term MLR Adjustment factor

2nd Lease Term MLR Adjustment factor

3rd Lease Term MLR Adjustment factor

4th Lease Term MLR Adjustment factor

A319-100 1.00 0.985 0.965 0.965

A320-200 1.00 0.985 0.965 0.965

A321-200 1.00 0.985 0.965 0.965

737-300 1.00 0.985 0.965 0.965

737-400 1.00 0.985 0.965 0.965

737-700 1.00 0.985 0.965 0.965

737-800 1.00 0.985 0.965 0.965

757-200 1.00 0.985 0.965 0.965

A330-200 1.00 0.985 0.965 0.965

A330-300 1.00 0.985 0.965 0.965

767-300ER 1.00 0.985 0.965 0.965

777-300ER 1.00 0.985 0.965 0.965

17A Flightglobal Advisory Service ascendworldwide.com

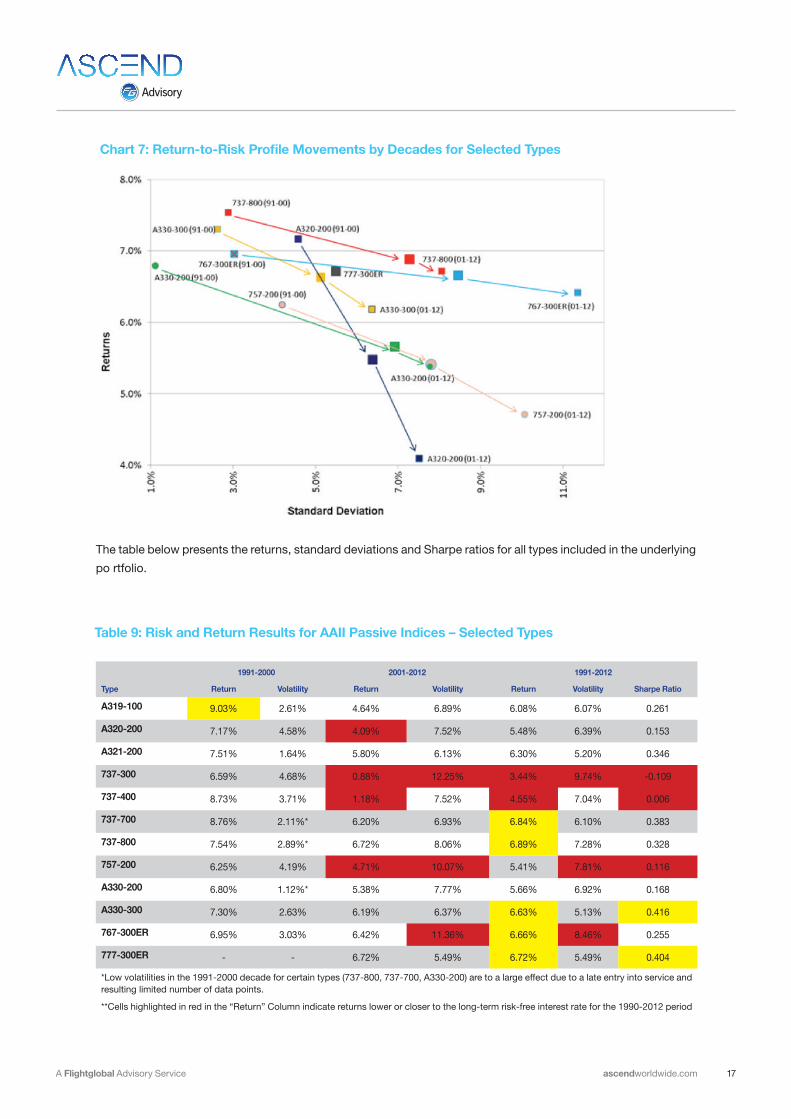

The table below presents the returns, standard deviations and Sharpe ratios for all types included in the underlying

po rtfolio.

Chart 7: Return-to-Risk Profile Movements by Decades for Selected Types

Table 9: Risk and Return Results for AAII Passive Indices – Selected Types

1991-2000 2001-2012 1991-2012

Type Return Volatility Return Volatility Return Volatility Sharpe Ratio

A319-100 9.03% 2.61% 4.64% 6.89% 6.08% 6.07% 0.261

A320-200 7.17% 4.58% 4.09% 7.52% 5.48% 6.39% 0.153

A321-200 7.51% 1.64% 5.80% 6.13% 6.30% 5.20% 0.346

737-300 6.59% 4.68% 0.88% 12.25% 3.44% 9.74% -0.109

737-400 8.73% 3.71% 1.18% 7.52% 4.55% 7.04% 0.006

737-700 8.76% 2.11%* 6.20% 6.93% 6.84% 6.10% 0.383

737-800 7.54% 2.89%* 6.72% 8.06% 6.89% 7.28% 0.328

757-200 6.25% 4.19% 4.71% 10.07% 5.41% 7.81% 0.116

A330-200 6.80% 1.12%* 5.38% 7.77% 5.66% 6.92% 0.168

A330-300 7.30% 2.63% 6.19% 6.37% 6.63% 5.13% 0.416

767-300ER 6.95% 3.03% 6.42% 11.36% 6.66% 8.46% 0.255

777-300ER - - 6.72% 5.49% 6.72% 5.49% 0.404

*Low volatilities in the 1991-2000 decade for certain types (737-800, 737-700, A330-200) are to a large effect due to a late entry into service and resulting limited number of data points.

**Cells highlighted in red in the “Return” Column indicate returns lower or closer to the long-term risk-free interest rate for the 1990-2012 period

18 worldwide.com A Flightglobal Advisory Service

Chart 8: Ascend aircraft investment index – comparative performance benchmark

Chart 9: Selected narrowbody aircraft total return indices between 1991-2013

19A Flightglobal Advisory Service ascendworldwide.com

Chart 10: Widebody aircraft total return indices between 1991-2013

Chart 11: Chart 8: Return-ro-risk profiles – narrowbodies (1991-2012)

20 worldwide.com A Flightglobal Advisory Service

Chart 8: Return-ro-risk profiles – widebodies (1991-2012)