ASC 606 For Software Companies: Step 5 - Recognizing Revenue rec webinar - Step 5 and...Scenario 3...

33

MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS © 2018 Wolf & Company, P.C. ASC 606 For Software Companies: Step 5 - Recognizing Revenue August 16, 2018

Transcript of ASC 606 For Software Companies: Step 5 - Recognizing Revenue rec webinar - Step 5 and...Scenario 3...

MEMBER OF ALLINIAL GLOBAL, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS © 2018 Wolf & Company, P.C.

ASC 606 For Software Companies:

Step 5 - Recognizing Revenue

August 16, 2018

• Today’s presentation slides can be downloaded at

www.wolfandco.com/webinars/2018.

• The session will last about 45 minutes, and we’ll then

have time for Q & A.

• Our audience will be muted during the session.

• Please send your questions in using the “Questions

Box” located on the webinar’s control panel.

2

Before we get started…

About Wolf & Company, P.C.

• Established in 1911

• Offers Audit, Tax, and Risk Management Services

• Offices located in:

– Boston, Massachusetts

– Springfield, Massachusetts

– Albany, New York

– Livingston, New Jersey

• Over 250 professionals

As a leading regional firm founded in 1911, we provide our clients

with specialized industry expertise and responsive service.

3

Introduction

Scott Goodwin, CPAMember of the Firm and Technology Services Team Leader

• E-mail: [email protected]

• Phone: (617) 428-5407

Cecilia Frerotte, CPAAudit Principal and Software Sector Leader

• E-mail: [email protected]

• Phone: (617) 261-8186

4

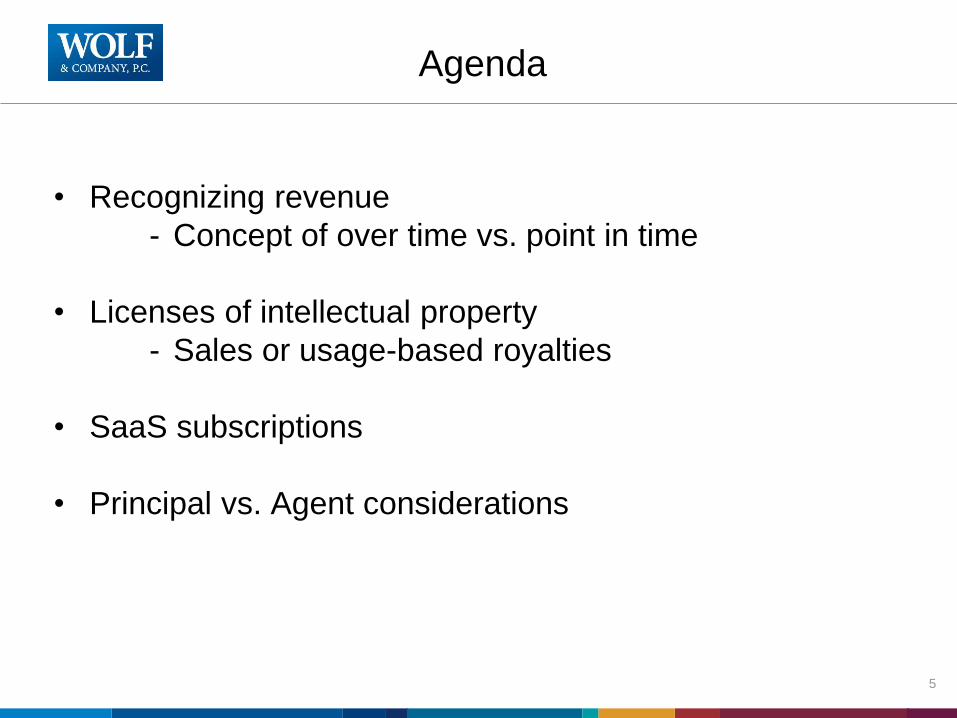

Agenda

• Recognizing revenue

- Concept of over time vs. point in time

• Licenses of intellectual property

- Sales or usage-based royalties

• SaaS subscriptions

• Principal vs. Agent considerations

5

The Five Step Model

6

Core Principle

Recognize revenue to depict the transfer of promised goods or

services to customers in an amount that reflects the consideration

to which the entity expects to be entitled in exchange for those

goods or services

Over time vs. Point in time

An entity transfers control over an asset over time if one of the

following criteria is met:

1. Customer simultaneously receives and consumes the benefits

provided by the entity’s performance as the entity performs

2. Entity’s performance creates or enhances an asset that the

customer controls as the asset is created/enhanced

3. Entity’s performance does not create an asset with an

alternative use to the entity and the entity has an enforceable

right to payment for performance completed to date

7

Transferring a promised good or service to a customer

satisfies a performance obligation occurs either: Over time or

at a point in time

Licenses of Intellectual Property

A license arrangement establishes a customer’s rights

related to a company’s intellectual property and the

obligations of the company to provide those rights.

Critical questions for software companies:

1. Does the arrangement include a license of IP?

2. If so, is that license distinct?

» VSOE is dead

» Consequences of distinct vs. not distinct

3. If so, is the license functional or symbolic?

» Revenue recognition for each

8

Licenses of Intellectual Property

Does the arrangement include a license of IP?

A separate promise of a license exists when:

(1) the customer has the contractual right to take possession

of the software at any time during the hosting period

without significant penalty, and

(2) the customer can run the software on its own hardware or

contract with another party unrelated to the vendor to host

the software

9

Licenses of Intellectual Property

Is that license distinct?

Must be both:

(1) capable of being distinct, and

if a customer can benefit from the license either

on its own or together with other resources that

are readily available to the customer

(2) distinct within the context of the contract

separately identifiable

10

Licenses of Intellectual Property

Is that license distinct?

Vendor-specific objective evidence (VSOE)

• VSOE of fair value is no longer required to

identify the unit of accounting

• May lead to the identification of additional

performance obligations and earlier recognition

of revenue

If not distinct,…11

Scenario 1

Sample Co. enters into a contract with WorkCo

for on-premise data analysis software and cloud

data storage.

The software utilizes WorkCo’s data stored on

the cloud to provide data analysis.

The software can also utilize data stored on the

WorkCo’s premises or data stored by other

vendors.

Is the license distinct?

12

Scenario 1

Yes.

The on-premise software license is distinct from the

cloud data storage service. The software license and

cloud data storage service are not highly interrelated

or interdependent.

If data was stored on WorkCo’s premises or with

another vendor, WorkCo would still get all of the

benefits of the software.

The cloud data storage could be provided by other

vendors and is capable of being distinct.

13

Scenario 2

Sample Co. contracts with WorkCo for

– A perpetual software license,

– installation services,

– 2 years of technical support.

The installation services include significant customization

of the software to interface with WorkCo’s data sources.

The technical support is not critical to maintaining the

ongoing utility of the software.

Is the license distinct?

14

Scenario 2

No. The software license is not distinct from the

installation services because the installation services

significantly customize the software. The software and

installation services create a combined output,

customized software.

Therefore Sample Co. needs to assess whether control

is transferred at a point in time (once the software is

completed) or over time (as the customization is

performed)

The tech support is distinct and should be recognized

over time15

Licenses of Intellectual Property

Is the license functional or symbolic?

Companies provide their customers with either:

• A right to access the entity’s intellectual property as

it exists throughout the license period, including any

changes to that intellectual property

• A right to use the entity’s intellectual property as it

exists at the point in time at which the license is

granted

16

Licenses of Intellectual Property

17

Functional Symbolic

Significant standalone functionality

Derives a substantial portion of its utility from

its significant standalone functionality

Does not have significant standalone

functionality

Substantially all of the utility of symbolic

intellectual property is derived from its

association with the entity’s past or ongoing

activities, including its ordinary business

activities

Software, drug formulas or compounds,

completed media content, specialized and

patents

Brands, logos, team names, and franchise

rights

Functional IP is a right to use IP because the

IP has standalone functionality and the

customer can use the IP as it exists at a

point in time.

Revenue from Functional IP is recognized at

a point in time.

Symbolic IP is a right to access IP because

of the entity’s obligation to support or

maintain the IP over time.

Revenue from symbolic IP is recognized

over the license period, or the remaining

economic life of the IP, if shorter.

Scenario 3

Sample Co provides a 5 year term software license to WorkCo.

The terms of the arrangement allow Work Co to download the

software by using a key provided by Sample Co.

Work Co can use the software on its own server and the software

is functional when it transfers to Work Co. Work Co also

purchases post-contract customer support (PCS) with the

software license.

The license and PCS are distinct as Work Co can benefit from the

license on its own and the license is separable from the PCS.

How should revenue from the license be recognized?

18

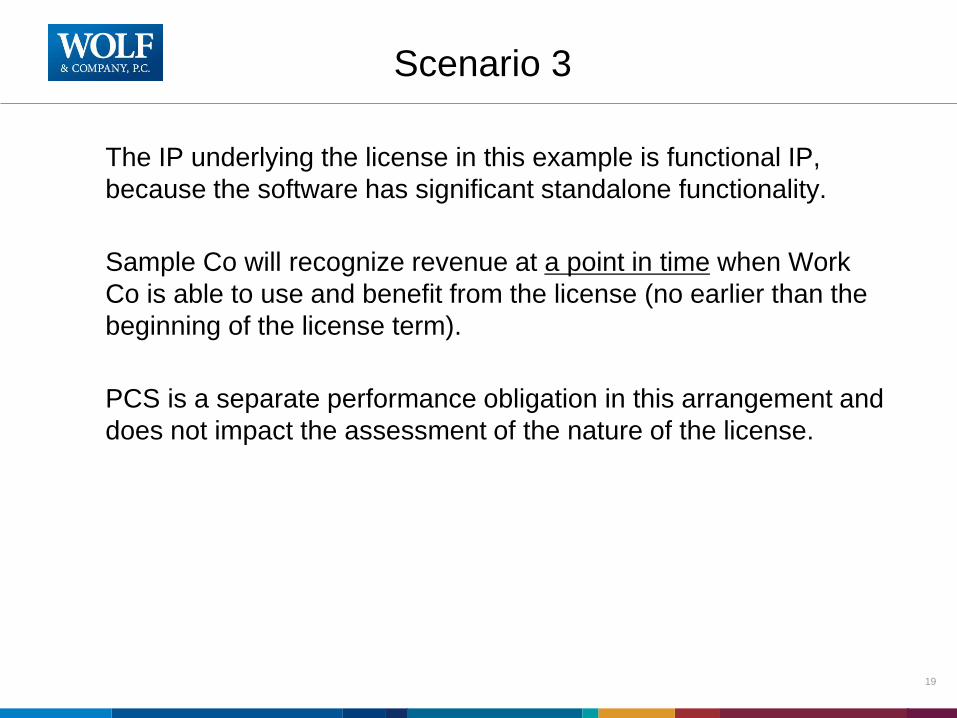

Scenario 3

The IP underlying the license in this example is functional IP,

because the software has significant standalone functionality.

Sample Co will recognize revenue at a point in time when Work

Co is able to use and benefit from the license (no earlier than the

beginning of the license term).

PCS is a separate performance obligation in this arrangement and

does not impact the assessment of the nature of the license.

19

Sales or usage-based royalties

20

Some licenses of IP include sales or usage-based royalties. There is

an exception for revenue recognition for these arrangements as

follows:

• Recognize revenue as the sales or usage occurs unless doing so

accelerates revenue recognition ahead of the entity’s satisfaction

of the performance obligation to which the royalty relates.

• Sales or usage based licenses of IP do not follow variable

consideration rules

• Cannot defer until customer reporting is available, must estimate

sales or usage prior to customer reporting

• Royalty minimum = fixed consideration

Scenario 4

Sample Co. licenses software on an annual basis to its customers and

promises to provide training on the use of the software.

In exchange for the software license and training, the customer promises to

pay Sample Co. $1.00 per transaction processed.

Sample Co. concludes that the software license and training are each distinct.

Does the sales- or usage-based royalty guidance apply to this arrangement?

21

Scenario 4

Yes. The license of IP is predominant in the arrangement because the

customer would ascribe significantly more value to the software license than

to the training.

Therefore Sample Co. will recognize revenue as the usage occurs, assuming

this approach does not accelerate revenue ahead of performance.

22

Scenario 5

Sample Co licenses patented software for a term of 3 years with no upfront

fee and 1% of future product sales. However, Sample Co is entitled to at

least $5 million at the end of each year, regardless of actual sales.

Technology in this area is changing rapidly so the possible consideration

from product sales ranges from $0 to $25 million, depending on whether

new technology is developed.

Management has concluded that the license transfers at a point in time

when the license period commences. Management has also concluded

that it is probable it will collect the consideration to which it is entitled, and

there are no further obligations remaining after the license is transferred.

How should Sample Co account for the transaction?

23

Scenario 5

Sample Co will recognize royalty revenue when the future product sales

occur.

However, since Sample Co is entitled to at least $5 million at the end of

each year, this amount of consideration is not variable. Therefore,

Software Co. should recognize as revenue the fixed amount (the minimum

payment of $15 million) at license inception.

Any consideration from royalties in excess of $5 million in any given year

will be recognized as those sales occur.

24

Licenses of Intellectual Property

25

Does the contract

involving software

include a licenseLicense of IP

SaaSIs the license

distinct?

Apply the general guidance to

the combined bundle Does the customer have a

right to access the entity’s

IP?

If the contract includes a

sales or usage-based

royalty, is the license the

predominant item to which

the royalty relates?

Over-time

perf.

obligation

Point-in-

time perf.

obligation

Yes

No

No Yes

No

Yes

Yes No

Sales or usage-based

royalties are estimated

and subject to variable

consideration (Step 3)

Sales or usage-based

royalties recognized at later

of when sales or usage

occurs and satisfaction of

performance obligation

Apply general

model

SaaS Subscriptions

• Question –

– Is a performance obligation to provide software-as-a-service

satisfied over time?

• Answer –

– Yes (in general)

– Why?

• Customer continuously consumes and receives the benefit

throughout the contract period

– Similar answer to other service-type contracts

26

SaaS Subscriptions

• Question –

– Is a performance obligation to provide implementation

services in conjunction with a software-as-a-service

arrangement satisfied over time?

• Answer –

– Yes (in general)

– Why?

• May create or enhance an asset that the customer controls

• Even if no asset is created, may still be satisfied over time

• But not always!

27

SaaS Subscriptions

• Example - Facts

– SaaS Co enters into a three-year SaaS arrangement with

Customer

– Customer pays fixed quarterly amount for the SaaS

– SaaS Co agrees to provide the following services:

• Training

• Data migration

• Building an interface to Customer’s GL system

– SaaS Co has already concluded that each service meets the

definition of a performance obligation

– Interface will reside on Customer’s network and will

represent an asset for Customer

– Other services do not create assets

28

SaaS Subscriptions

• Example – Analysis

– Interface

• Recognized over time

• Creates an asset controlled by Customer

– Other services

• Recognized over time

• Customer consumes and receives the benefit from each

service as SaaS Co. performs

– SaaS

• Recognized over time

29

Principal versus Agent

• ASC 606 requires a similar analysis as current GAAP

requires

– No longer consider credit risk as an indicator of being a

principal

• Focus of analysis is on obtaining control of the

good/service before transferring it to the customer

• Factors for being a principal

– Primary responsibility for providing good/service

– Assumes inventory risk

– Having discretion in setting prices

• Each promised good/service needs to be evaluated

– Could have some where you are principal and others where

you are agent30

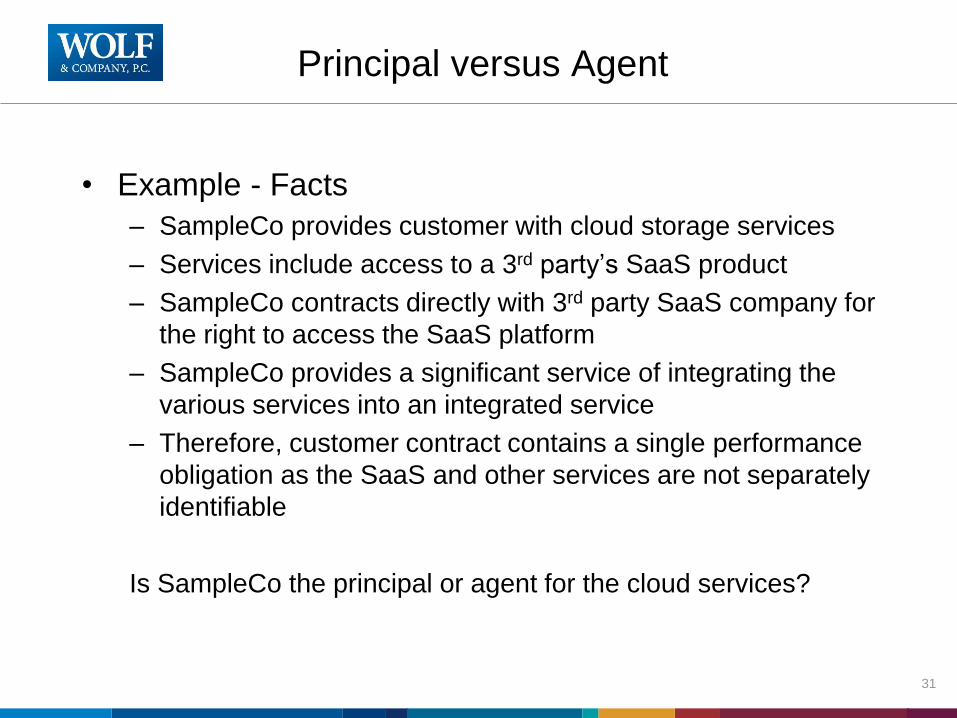

Principal versus Agent

• Example - Facts

– SampleCo provides customer with cloud storage services

– Services include access to a 3rd party’s SaaS product

– SampleCo contracts directly with 3rd party SaaS company for

the right to access the SaaS platform

– SampleCo provides a significant service of integrating the

various services into an integrated service

– Therefore, customer contract contains a single performance

obligation as the SaaS and other services are not separately

identifiable

Is SampleCo the principal or agent for the cloud services?

31

Principal versus Agent

• Example - Analysis

– SampleCo appears to be the principal in this arrangement

• Recognize revenue gross for the fee received from the

customer

– SaaS is one input into the integrated cloud services

– SampleCo obtains control of the inputs, including the SaaS

platform

– SampleCo directs the inputs’ use to deliver a combined

output

32

Questions?

Scott Goodwin, CPAMember of the Firm and Technology Services Team Leader

• E-mail: [email protected]

• Phone: (617) 428-5407

Cecilia Frerotte, CPAAudit Principal and Software Sector Leader

• E-mail: [email protected]

• Phone: (617) 261-8186

33