Asasah islamic microfinance

34

-

Upload

alhudacibe -

Category

Documents

-

view

270 -

download

0

Transcript of Asasah islamic microfinance

An Introduction to

Islamic Microfinance

Muhammad Zubair MughalChief Executive Officer,

AlHuda: Centre of Islamic Banking and Economics

www.alhudacibe.com

Contents

• What is Shariah Based Microfinance ?• Difference between Conventional & Islamic MF• Demand of Islamic Microfinance Worldwide• Global Landscape of Islamic Microfinance• Islamic Microfinance Update• The Way Forward

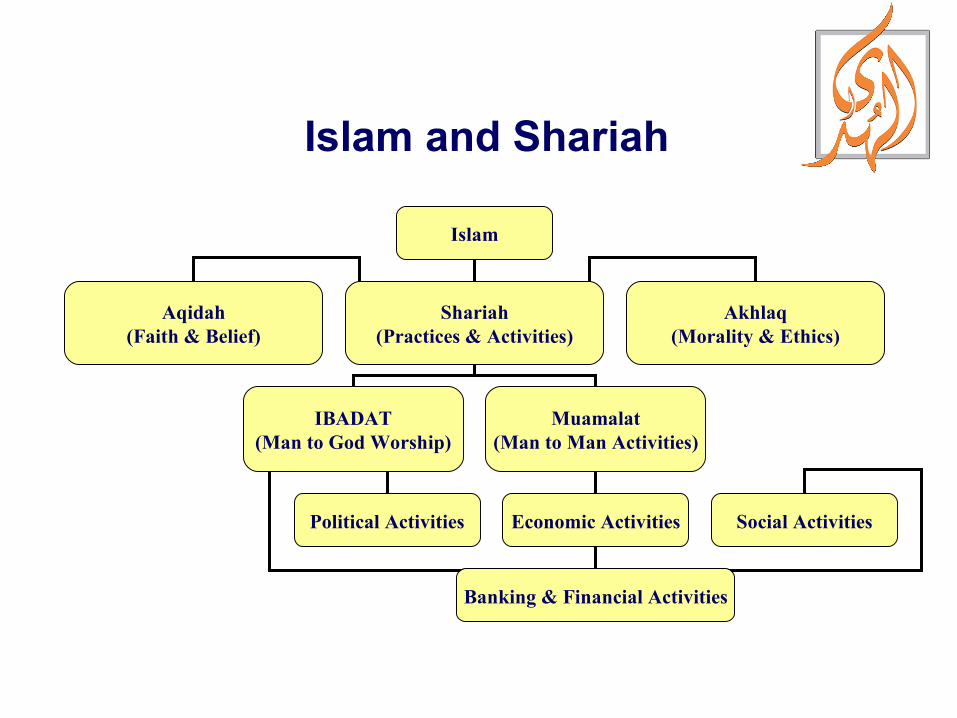

Islam

Aqidah(Faith & Belief)

Shariah(Practices & Activities)

Akhlaq(Morality & Ethics)

IBADAT(Man to God Worship)

Muamalat(Man to Man Activities)

Political Activities Economic Activities Social Activities

Banking & Financial Activities

Islam and Shariah

Sources of Fiq’h in Islam (Islamic Micro Finance)

• Quran

• Sunnah

• Ijtehad / Qiyas

• Ijama’e Ummah

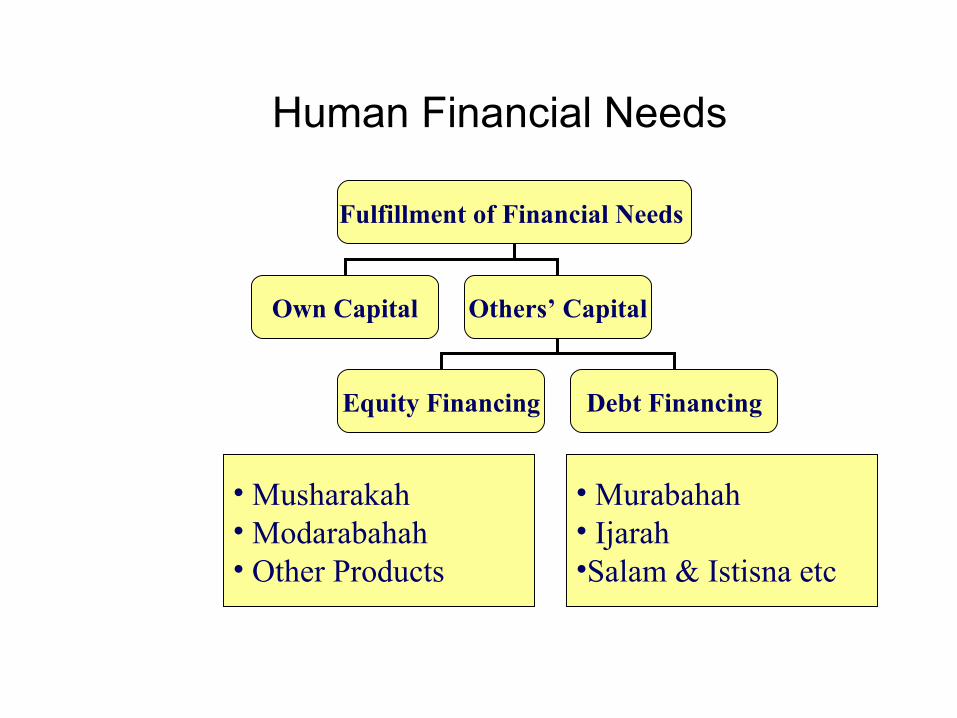

Fulfillment of Financial Needs

Own Capital Others’ Capital

Equity Financing Debt Financing

• Murabahah• Ijarah•Salam & Istisna etc

• Musharakah• Modarabahah• Other Products

Human Financial Needs

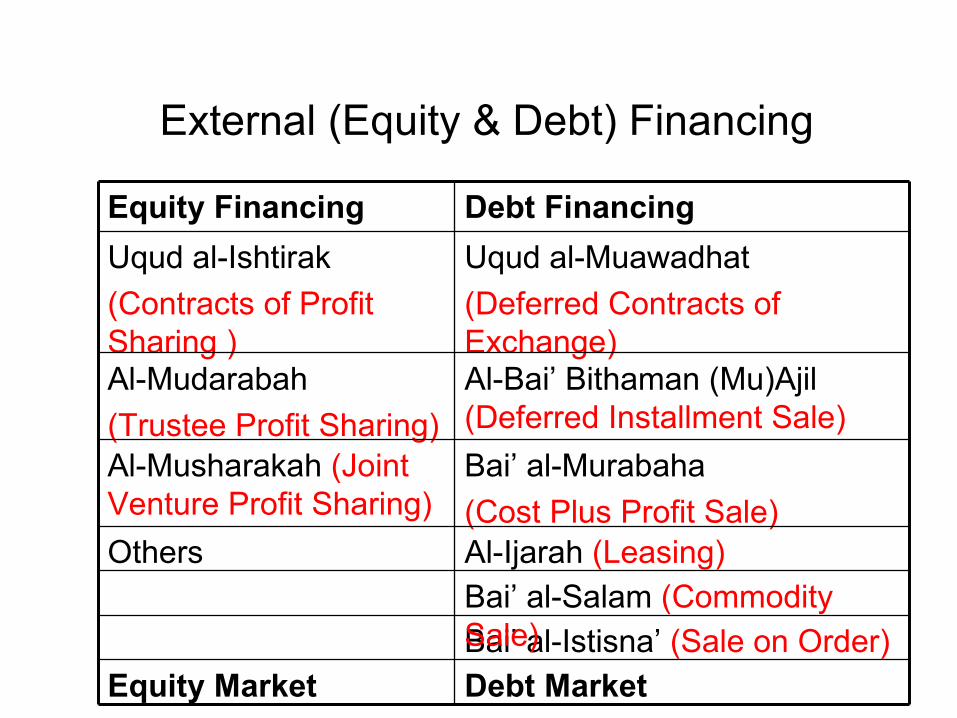

Debt MarketEquity Market

Bai’ al-Istisna’ (Sale on Order)

Bai’ al-Salam (Commodity Sale)

Al-Ijarah (Leasing)Others

Bai’ al-Murabaha

(Cost Plus Profit Sale)

Al-Musharakah (Joint Venture Profit Sharing)

Al-Bai’ Bithaman (Mu)Ajil (Deferred Installment Sale)

Al-Mudarabah

(Trustee Profit Sharing)

Uqud al-Muawadhat

(Deferred Contracts of Exchange)

Uqud al-Ishtirak

(Contracts of Profit Sharing )

Debt FinancingEquity Financing

External (Equity & Debt) Financing

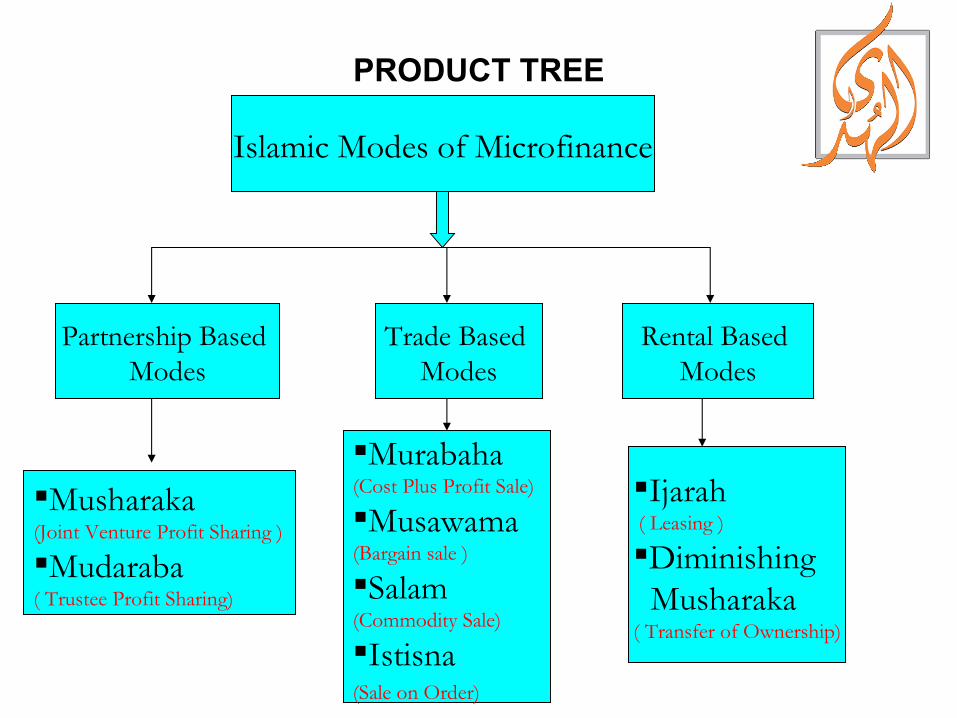

PRODUCT TREE

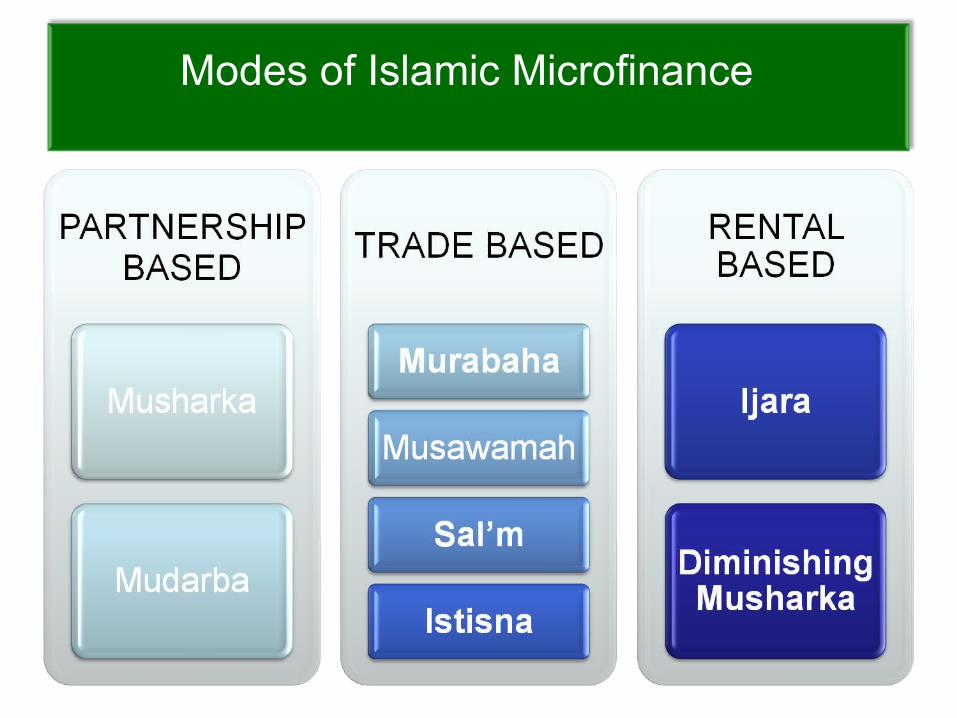

Islamic Modes of Microfinance

Trade Based Modes

Partnership Based Modes

Rental Based Modes

Musharaka(Joint Venture Profit Sharing )

Mudaraba( Trustee Profit Sharing)

Murabaha(Cost Plus Profit Sale)

Musawama(Bargain sale )

Salam(Commodity Sale)

Istisna(Sale on Order)

Ijarah ( Leasing )

Diminishing Musharaka( Transfer of Ownership)

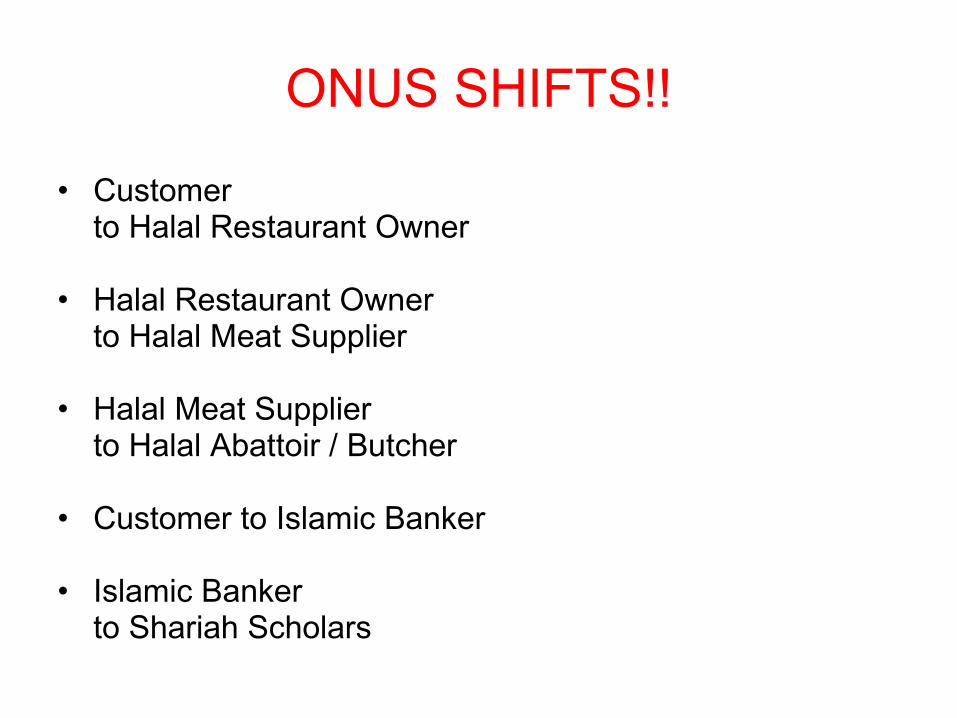

ONUS SHIFTS!!

• Customer to Halal Restaurant Owner

• Halal Restaurant Owner to Halal Meat Supplier

• Halal Meat Supplier to Halal Abattoir / Butcher

• Customer to Islamic Banker

• Islamic Banker to Shariah Scholars

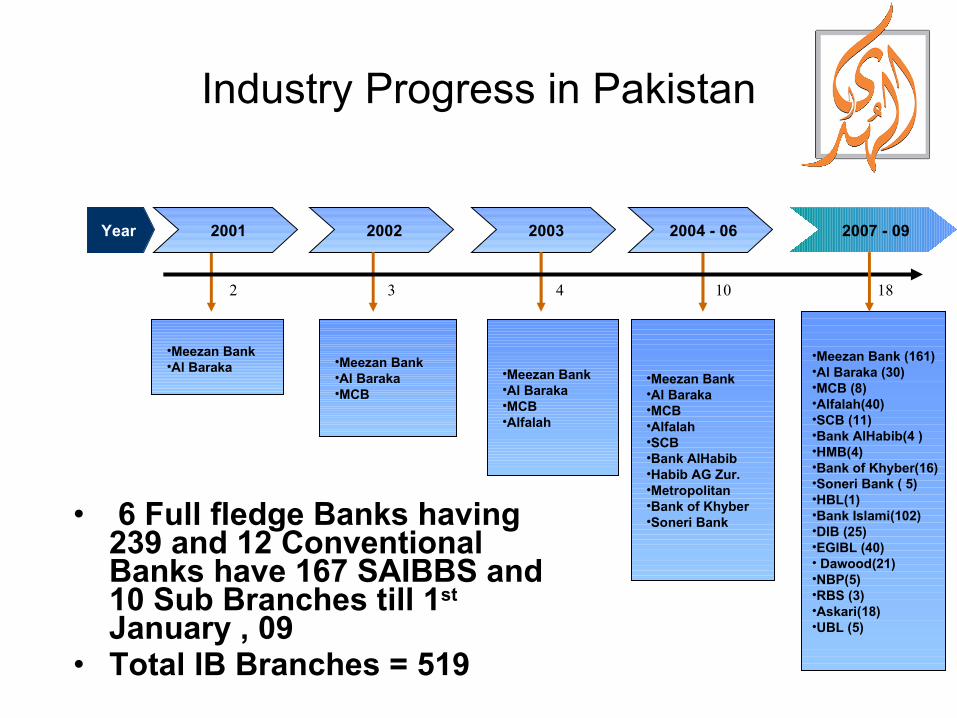

Industry Progress in Pakistan

• 6 Full fledge Banks having 239 and 12 Conventional Banks have 167 SAIBBS and 10 Sub Branches till 1st January , 09

• Total IB Branches = 519

Year 2001

•Meezan Bank•Al Baraka

•Meezan Bank•Al Baraka•MCB•Alfalah•SCB•Bank AlHabib•Habib AG Zur.•Metropolitan•Bank of Khyber•Soneri Bank

2002 2003

•Meezan Bank•Al Baraka•MCB

•Meezan Bank•Al Baraka•MCB•Alfalah

2 10

2007 - 09

•Meezan Bank (161) •Al Baraka (30) •MCB (8) •Alfalah(40) •SCB (11) •Bank AlHabib(4 ) •HMB(4) •Bank of Khyber(16) •Soneri Bank ( 5) •HBL(1) •Bank Islami(102) •DIB (25) •EGIBL (40) • Dawood(21) •NBP(5) •RBS (3) •Askari(18) •UBL (5)

2004 - 06

1843

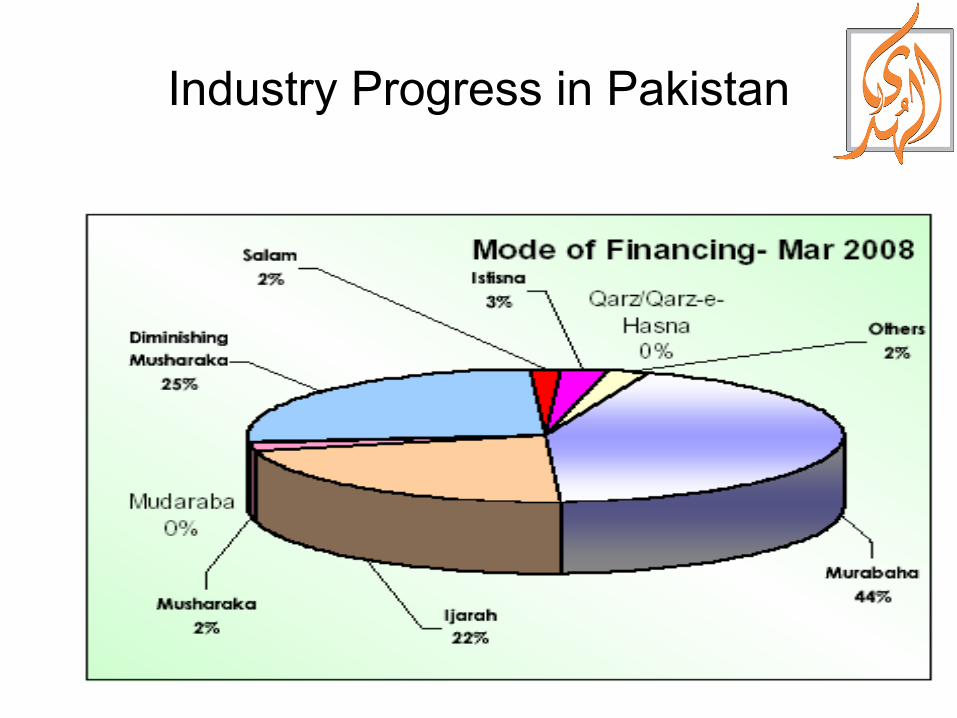

Industry Progress in Pakistan

International Overview

• The size of Islamic Financial Industry has reached US$ 950 Bln.

and its growing annually @ 15% per anum.

• 70 countries have Islamic Banking Institutions

• 37 Muslim countries including Bahrain, UAE, Saudi Arabia,

Malaysia, Brunei and Pakistan

• 34 non-Muslim countries including USA, UK, Canada, Switzerland,

South Africa and Australia

International Overview

• In Feb 1999, Dow Jones introduced the Dow Jones

Islamic Market Index (DJIM) of 600 companies world

wide whose business complies with Islamic Shariah laws

• At present there are more than 170 Islamic Funds

operational through out the world with a total fund base

of over USD 3.50 billion

International Overview

• Governments of Bahrain ,Malaysia and now Pakistan

have issued Islamic Bonds (Sukuk) in order to facilitate

Islamic Banks in managing their liquidity.

• Issuance of these bonds has also paved the way for

Shariah compliant Government borrowings

International Overview

• Institutions like Accounting and Auditing Organization for Islamic

Financial Institutions (AAOIFI) and Islamic Finance Services Board

(IFSB) have been formed.

• These institutions are playing a key role in setting up and

standardizing Shariah , Financial and Accounting standards for

Islamic Financial Institutions.

• Due to these collective efforts Islamic banking is now recognized by

IMF, World Bank and Basel Committee.

Islamic Microfinance

Prohibition of Interest

Risk sharing

Social Development Mission

Prohibition of speculative behaviour

Purity of contracts

Asset Based Financing

Shariah-approved activities.

Principle of Shariah Based Microfinance

And ALLAH has permitted trading and forbidden Riba

(Al Baqara 275)

•Riba means any fixed or guaranteed interest payment on cash advances or on deposits.

•Islam encourages the earning of profits but forbids the charging of interest

Prohibition of Riba ( Interest)

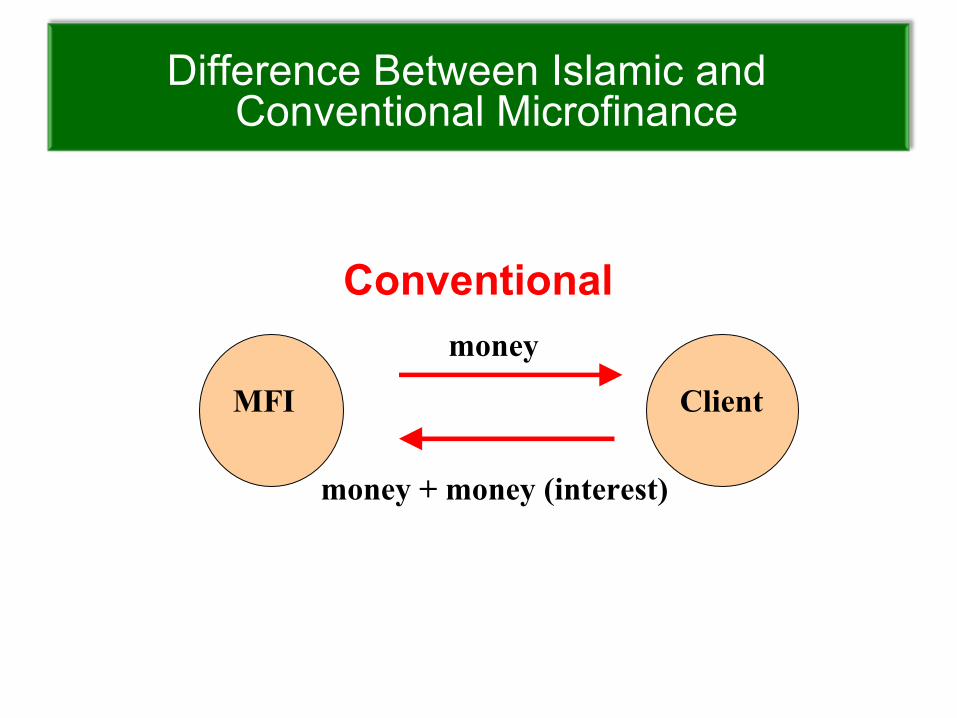

Conventional

MFI Client

money

money + money (interest)

Difference Between Islamic and Conventional Microfinance

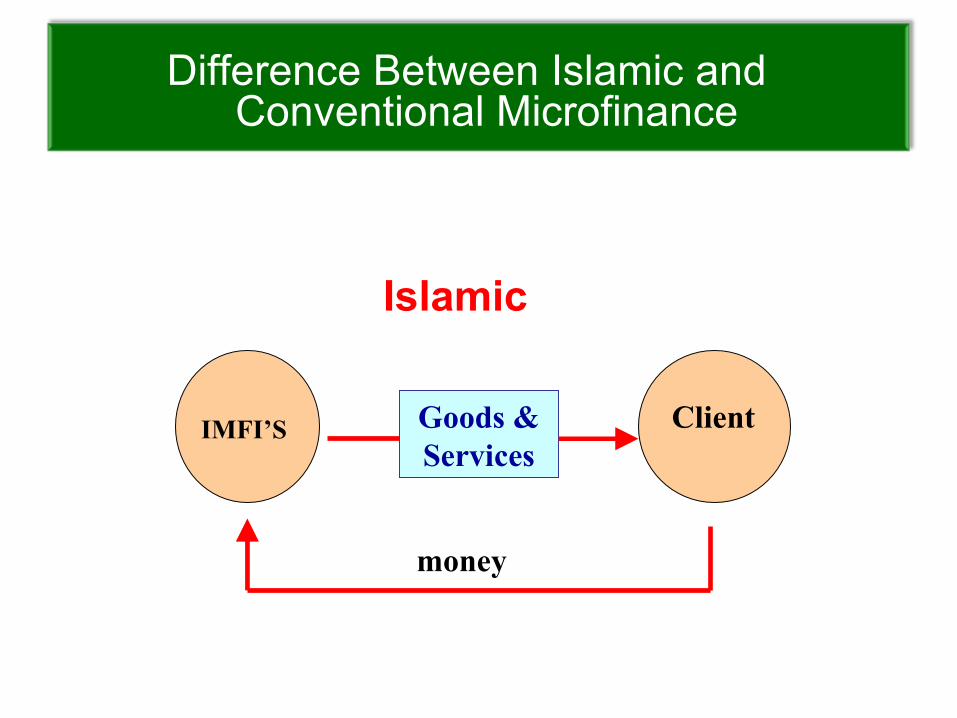

Islamic

IMFI’S ClientGoods & Services

money

Difference Between Islamic and Conventional Microfinance

Modes of Islamic Microfinance

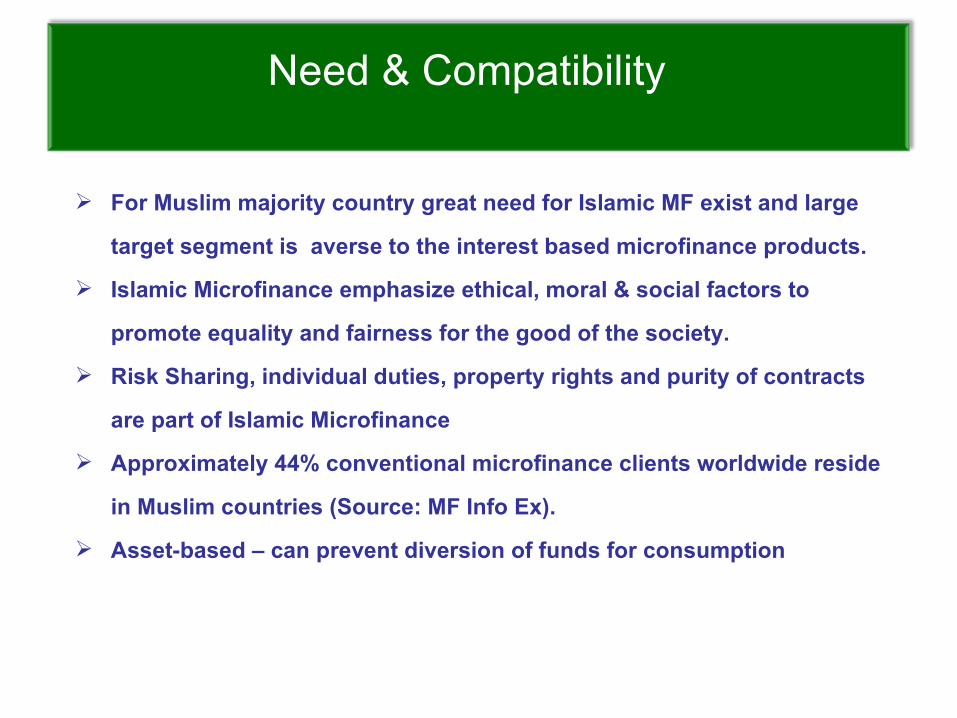

For Muslim majority country great need for Islamic MF exist and large

target segment is averse to the interest based microfinance products.

Islamic Microfinance emphasize ethical, moral & social factors to

promote equality and fairness for the good of the society.

Risk Sharing, individual duties, property rights and purity of contracts

are part of Islamic Microfinance

Approximately 44% conventional microfinance clients worldwide reside

in Muslim countries (Source: MF Info Ex).

Asset-based – can prevent diversion of funds for consumption

Need & Compatibility

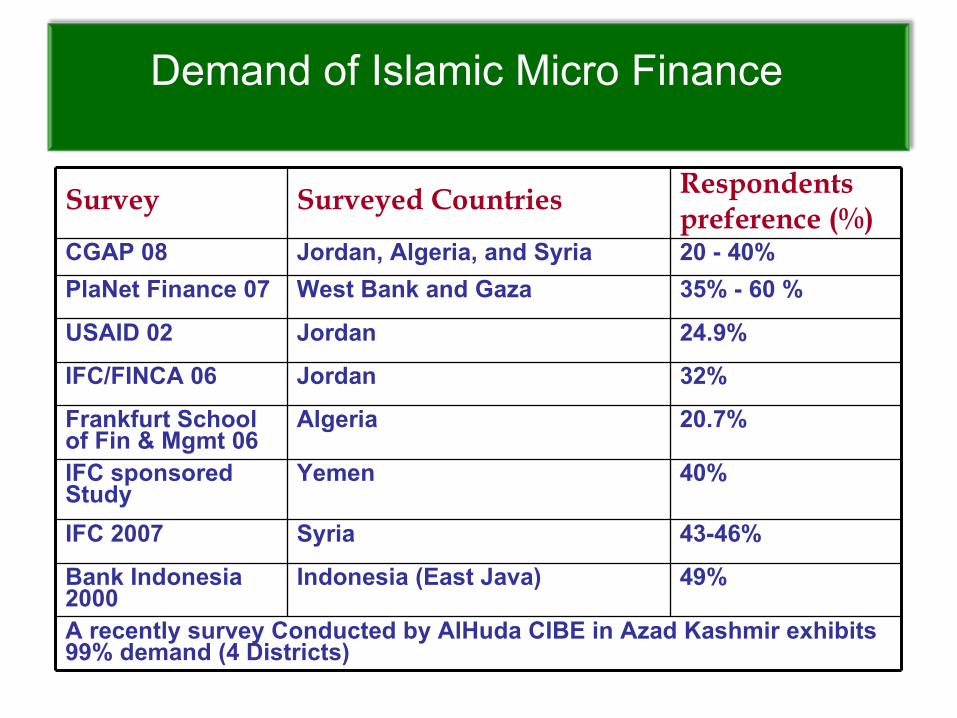

Survey Surveyed Countries Respondents preference (%)

CGAP 08 Jordan, Algeria, and Syria 20 - 40%

PlaNet Finance 07 West Bank and Gaza 35% - 60 %

USAID 02 Jordan 24.9%

IFC/FINCA 06 Jordan 32%

Frankfurt School of Fin & Mgmt 06

Algeria 20.7%

IFC sponsored Study

Yemen 40%

IFC 2007 Syria 43-46%

Bank Indonesia 2000

Indonesia (East Java) 49%

A recently survey Conducted by AlHuda CIBE in Azad Kashmir exhibits 99% demand (4 Districts)

Demand of Islamic Micro Finance

Institution Mode of Finance

7 Sudanese Islamic Banks Murabaha, mudaraba, musharaka, and saving deposit [SIB – Productive Families]

Islamic Cooperatives and Rural Banks of Indonesia

Cooperatives – Members’ Musharaka (integrated with Zakat Fund)

Rural Banks – Various modes

Islami Bank Bangladesh, Social Investment Bank and AlFalah & Rescue

IBB – Mostly bai muajjal

SIBL - Recourse generation - Cash Waqf and Financing through various modes

Jordan Islamic Bank Musharaka and Mudaraba

UNCDF Yemen (HMFP) Murabahah and redeemable Mudarabah

Sanabel (12 Arab countries, 64 MFIs – meeting 80% of MF needs)

Murabaha, mudaraba, musharaka

Amana Ikhtiar Malaysia and Islamic Pawn Broking

AIM – interest free loan

Al Rahnu – short term interest free loan against collateral at market value

International Experience of Islamic Microfinance

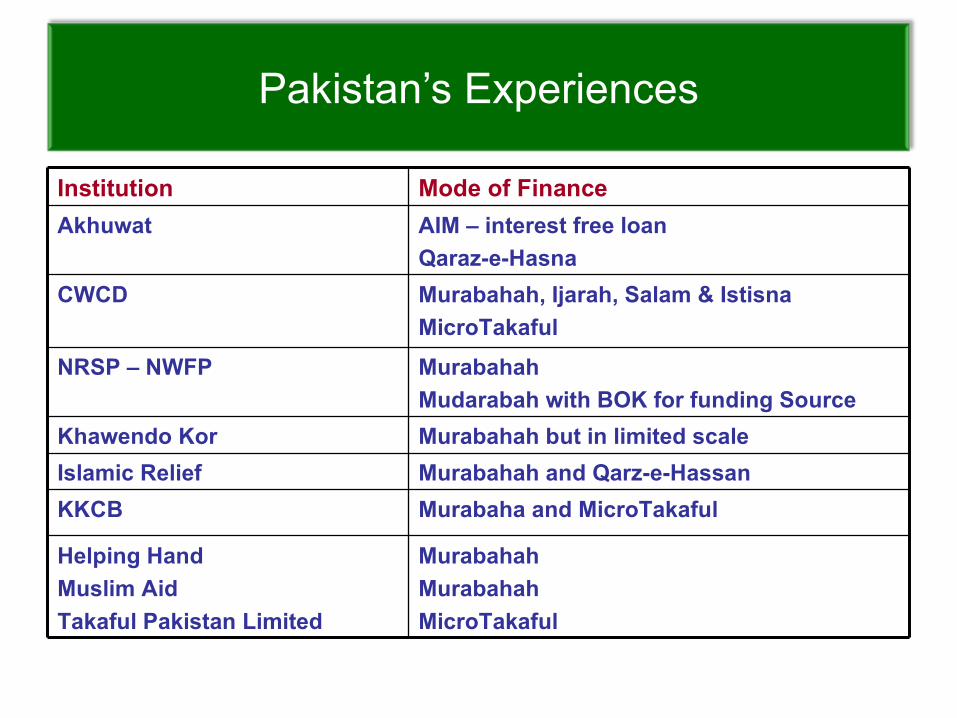

Pakistan’s Experiences

Institution Mode of Finance

Akhuwat AIM – interest free loan

Qaraz-e-Hasna

CWCD Murabahah, Ijarah, Salam & Istisna

MicroTakaful

NRSP – NWFP Murabahah

Mudarabah with BOK for funding Source

Khawendo Kor Murabahah but in limited scale

Islamic Relief Murabahah and Qarz-e-Hassan

KKCB Murabaha and MicroTakaful

Helping Hand

Muslim Aid

Takaful Pakistan Limited

Murabahah

Murabahah

MicroTakaful

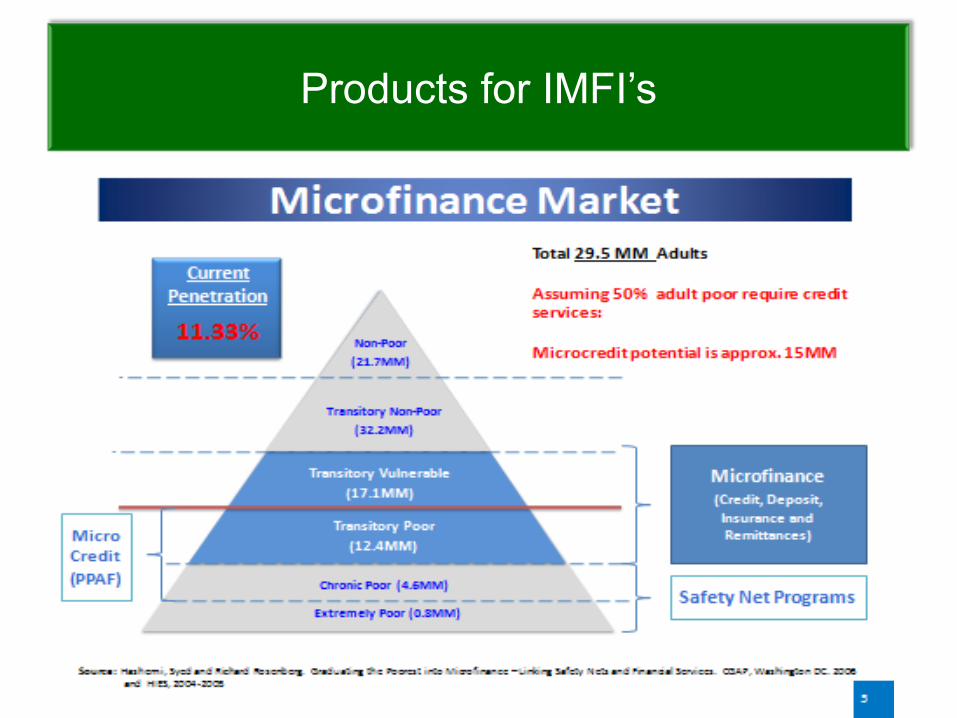

Products for IMFI’s

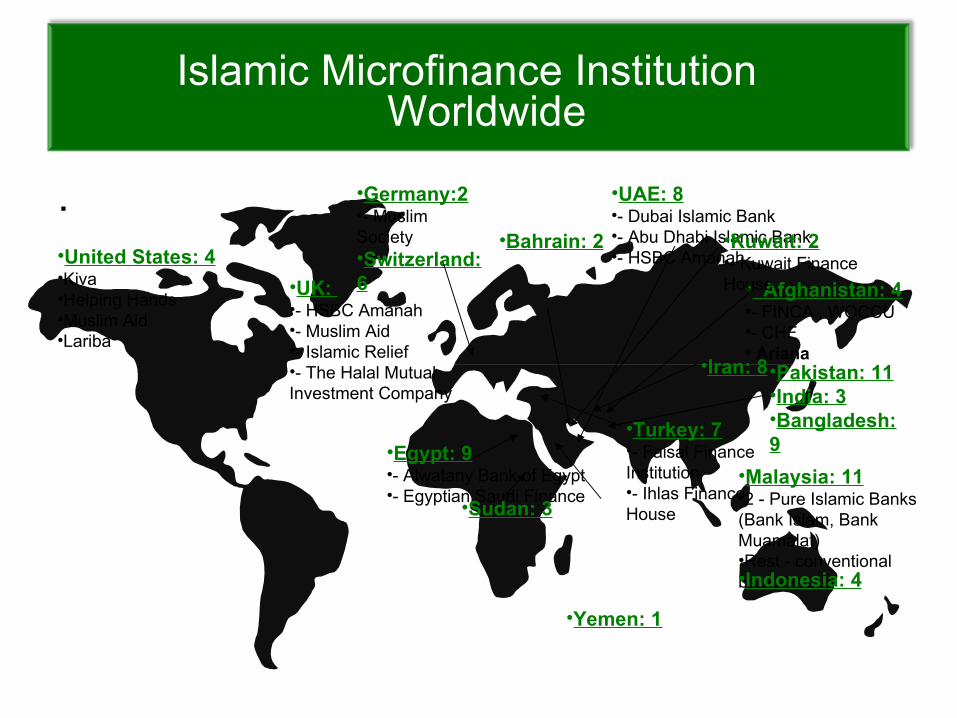

.•United States: 4•Kiva•Helping Hands•Muslim Aid•Lariba

•Germany:2•- Muslim Society•Switzerland: 6•UK:

•- HSBC Amanah•- Muslim Aid •- Islamic Relief•- The Halal Mutual Investment Company

•Bahrain: 2

•Malaysia: 11•2 - Pure Islamic Banks (Bank Islam, Bank Muamalat)•Rest - conventional banks

•UAE: 8•- Dubai Islamic Bank•- Abu Dhabi Islamic Bank•- HSBC Amanah

• Afghanistan: 4•- FINCA , WOCCU•- CHF• Ariana

•Kuwait: 2•- Kuwait Finance House

•Iran: 8

•Egypt: 9•- Alwatany Bank of Egypt•- Egyptian Saudi Finance

•Indonesia: 4

•Sudan: 3

•Pakistan: 11•India: 3•Bangladesh:9

•Turkey: 7•- Faisal Finance Institution•- Ihlas Finance House

•Yemen: 1

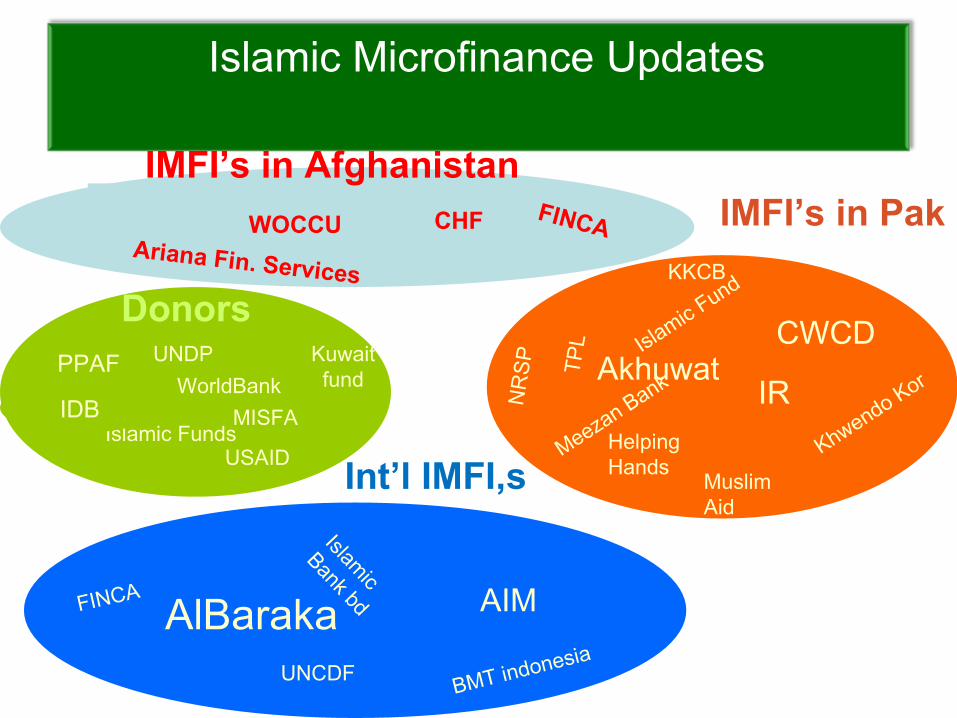

Islamic Microfinance Institution Worldwide

Ariana Fin. Services

FINCAWOCCU

IMFI’s in Afghanistan CHF

Akhuwat

Muslim Aid

NR

SP

Khwendo Kor

CWCD

IMFI’s in Pak

KKCB

Donors

Islamic Funds

PPAF

IDB MISFA

Kuwait fund

Int’l IMFI,s

AlBaraka AIM

UNCDF

FINCA

Islamic

Bank bd

BMT indonesia

Islamic Microfinance Updates

Helping Hands

IR

TP

L

Meezan Bank

Islamic Fund

UNDP

WorldBank

USAID

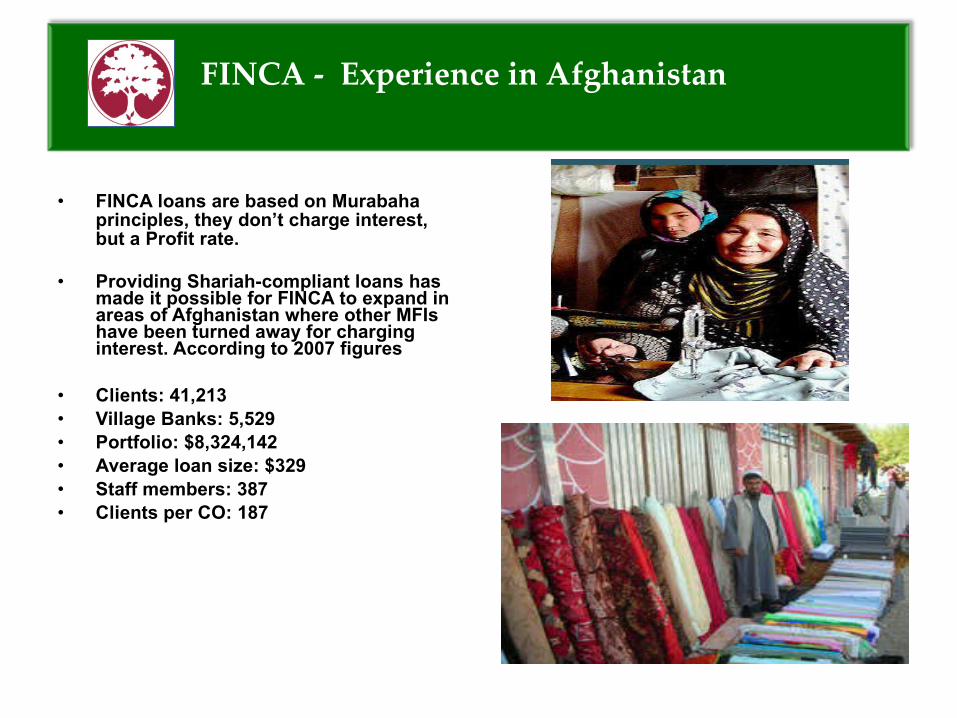

• FINCA loans are based on Murabaha principles, they don’t charge interest, but a Profit rate.

• Providing Shariah-compliant loans has made it possible for FINCA to expand in areas of Afghanistan where other MFIs have been turned away for charging interest. According to 2007 figures

• Clients: 41,213• Village Banks: 5,529• Portfolio: $8,324,142• Average loan size: $329• Staff members: 387• Clients per CO: 187

FINCA - Experience in Afghanistan

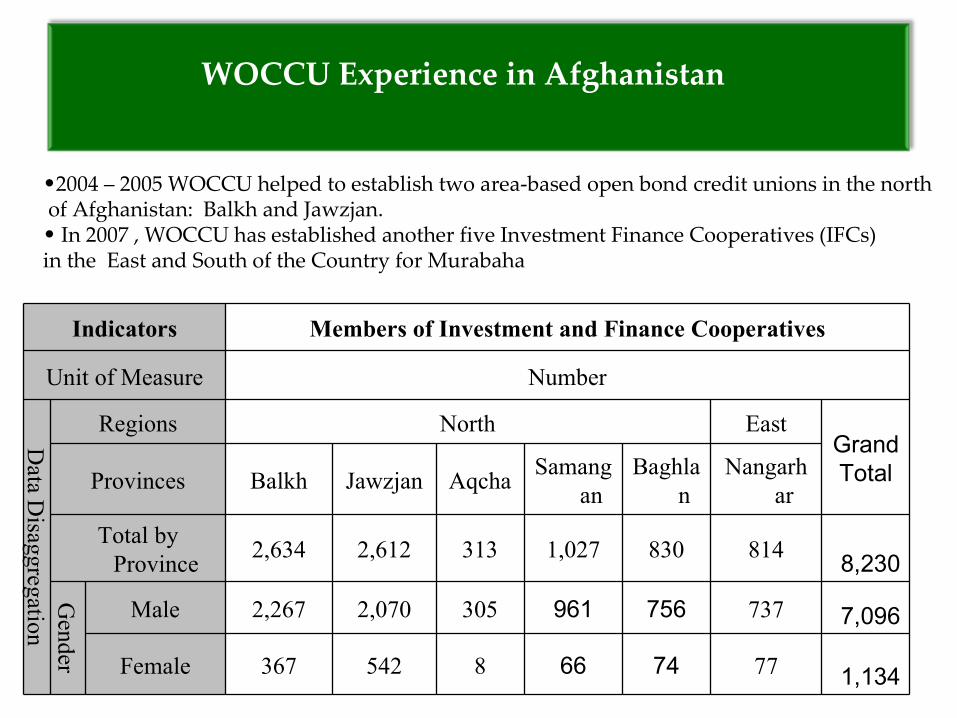

1,1347774668542367Female

7,0967377569613052,0702,267Male

Gender

8,2308148301,0273132,6122,634

Total by Province

Nangarhar

Baghlan

Samangan

AqchaJawzjanBalkhProvinces

GrandTotal

EastNorthRegions

Data D

isaggregation

NumberUnit of Measure

Members of Investment and Finance CooperativesIndicators

•2004 – 2005 WOCCU helped to establish two area-based open bond credit unions in the north of Afghanistan: Balkh and Jawzjan.• In 2007 , WOCCU has established another five Investment Finance Cooperatives (IFCs) in the East and South of the Country for Murabaha

WOCCU Experience in Afghanistan

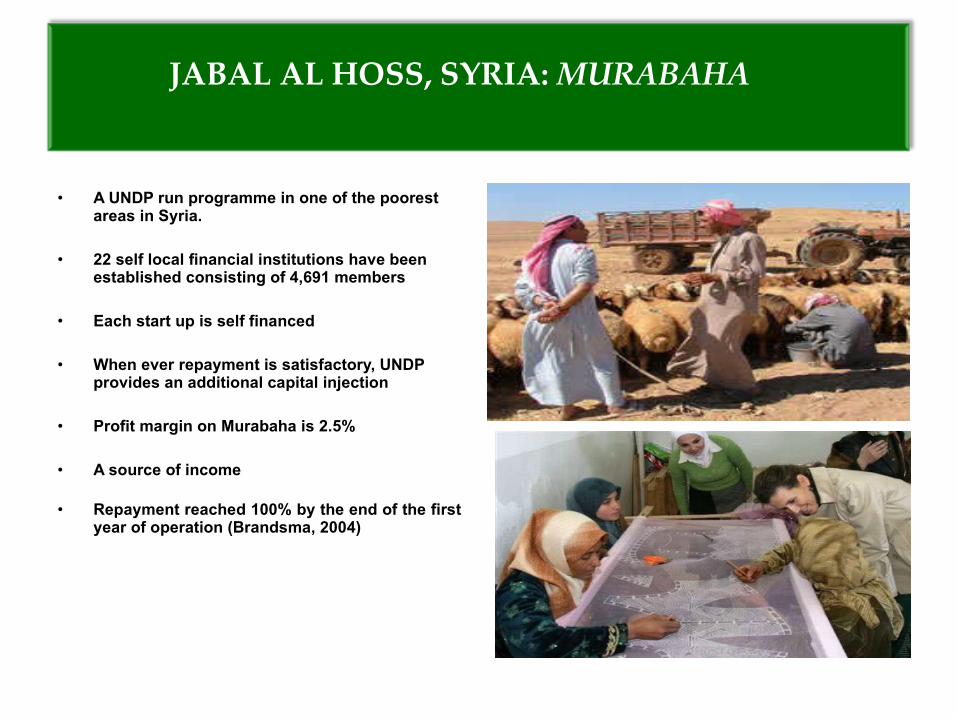

• A UNDP run programme in one of the poorest areas in Syria.

• 22 self local financial institutions have been established consisting of 4,691 members

• Each start up is self financed

• When ever repayment is satisfactory, UNDP provides an additional capital injection

• Profit margin on Murabaha is 2.5%

• A source of income

• Repayment reached 100% by the end of the first year of operation (Brandsma, 2004)

JABAL AL HOSS, SYRIA: MURABAHA

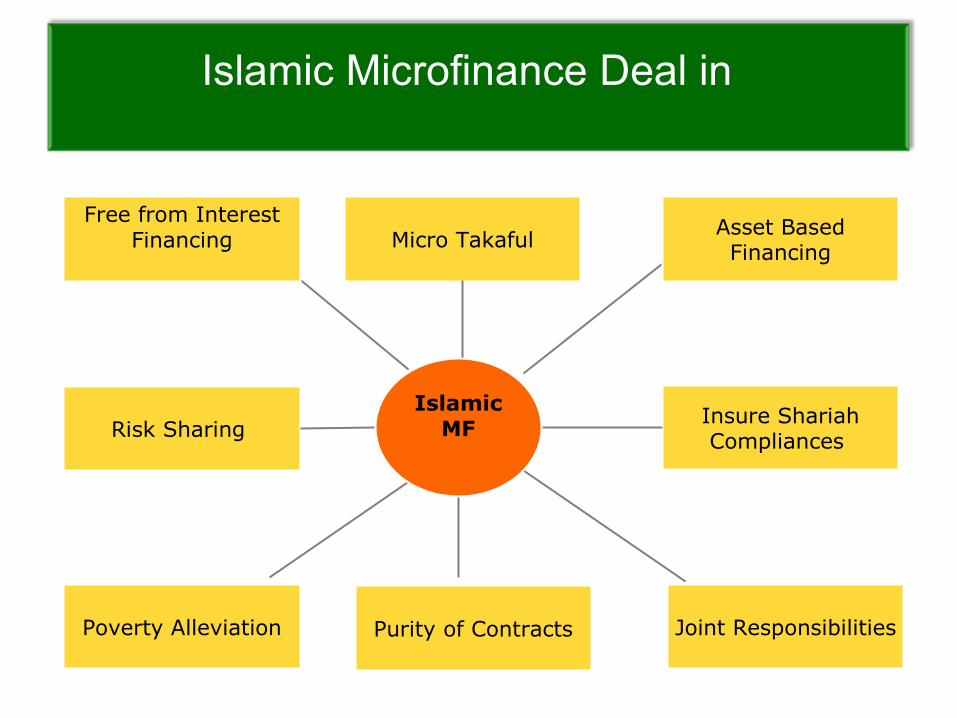

Risk Sharing Insure Shariah Compliances

Poverty Alleviation

Asset Based FinancingMicro Takaful

Free from InterestFinancing

Joint ResponsibilitiesPurity of Contracts

IslamicMF

Islamic Microfinance Deal in

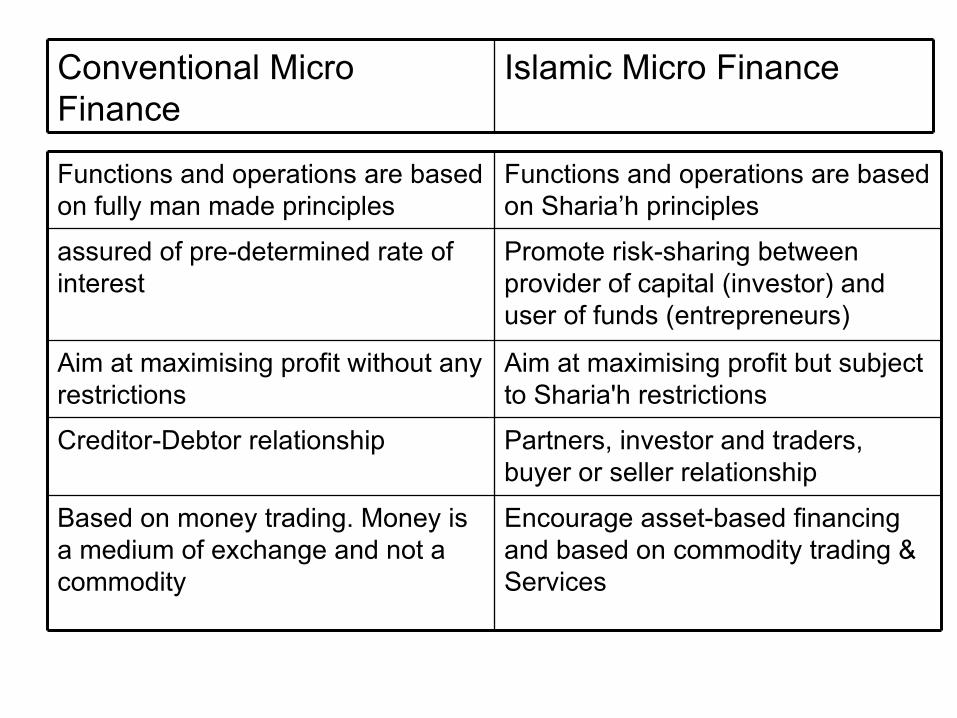

Functions and operations are based on fully man made principles

Functions and operations are based on Sharia’h principles

assured of pre-determined rate of interest

Promote risk-sharing between provider of capital (investor) and user of funds (entrepreneurs)

Aim at maximising profit without any restrictions

Aim at maximising profit but subject to Sharia'h restrictions

Creditor-Debtor relationship Partners, investor and traders, buyer or seller relationship

Based on money trading. Money is a medium of exchange and not a commodity

Encourage asset-based financing and based on commodity trading & Services

Conventional Micro Finance

Islamic Micro Finance

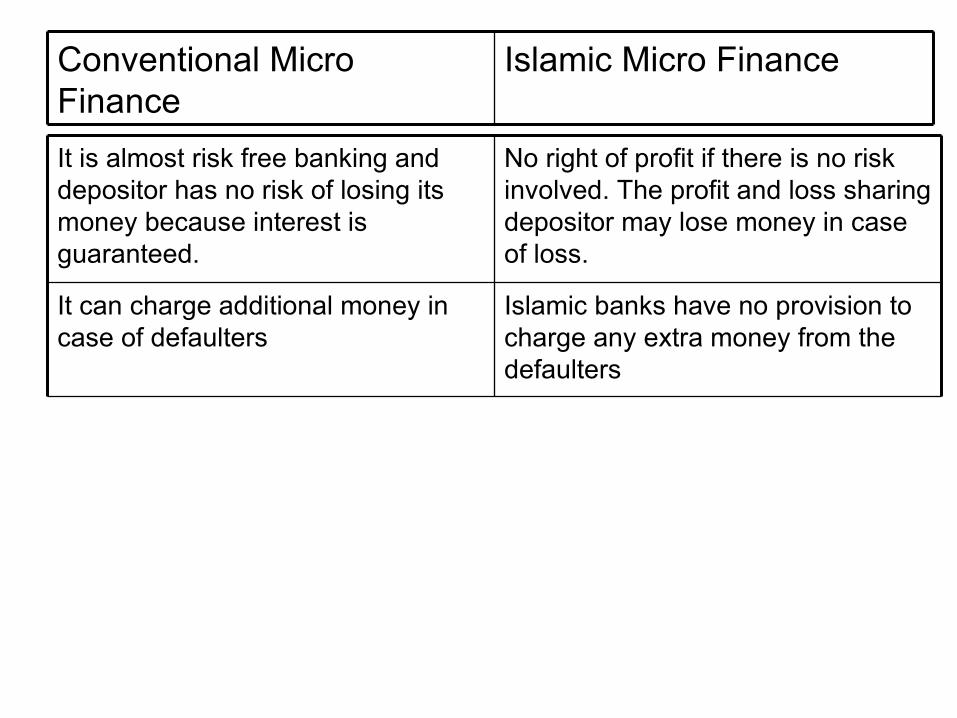

It is almost risk free banking and depositor has no risk of losing its money because interest is guaranteed.

No right of profit if there is no risk involved. The profit and loss sharing depositor may lose money in case of loss.

It can charge additional money in case of defaulters

Islamic banks have no provision to charge any extra money from the defaulters

Conventional Micro Finance

Islamic Micro Finance

![Islamic Microfinance - An Inclusive Approach [M. Khaleequzzaman] Mainstreaming Islamic Microfinance – An Inclusive Approach Muhammad Khaleequzzaman Head.](https://static.fdocuments.net/doc/165x107/56649dc65503460f94ab9fed/islamic-microfinance-an-inclusive-approach-m-khaleequzzaman-mainstreaming.jpg)