ARVIND LTD ISIN - indianotes-live-04da772e042e45f4b8c979 ...… · ARVIND LTD Result Update...

13

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved ARVIND LTD Result Update (CONSOLIDATED BASIS): Q1 FY19 CMP: 351.30 SEP 27 th , 2018 Overweight ISIN: INE034A01011 Index Details SYNOPSIS Arvind Ltd, one of the largest integrated textile and branded apparel players, with the presence of almost eight decades in this industry. It is among the largest denim manufacturers in the world. The consolidated turnover stood at Rs. 28609.60 million for Q1 FY19 as against Rs. 25942.10 million in Q1 FY18, up by 10.28%. During the quarter, EBIDTA stood at Rs. 2599.40 million as against Rs. 2232.90 million in the corresponding period of the previous year, up by 16.41%. Profit before tax (PBT) increased by 25.71% to Rs. 862.90 million in Q1 FY19 from Rs. 686.40 million in the corresponding quarter of the previous year. During the June quarter, net profit increased by 11.33% to Rs. 665.00 million from Rs. 597.30 million in Q1 FY18. EPS of the company stood at Rs. 2.57 in Q1 FY19 against Rs. 2.31 in the corresponding quarter of the previous year. Net Sales and PAT of the company are expected to grow at a CAGR of 14% and 6% over 2017 to 2020E, respectively. Stock Data Sector Textiles BSE Code 500101 Face Value 10.00 52wk. High / Low (Rs.) 477.85/337.50 Volume (2wk. Avg.) 110000 Market Cap (Rs. in mn.) 90853.21 Annual Estimated Results(A*: Actual / E*: Estimated) Years(Rs in mn) FY18A FY19E FY20E Net Sales 112541.90 122670.67 136164.44 EBITDA 10275.80 11446.27 12666.28 Net Profit 3094.70 3540.21 4017.55 EPS 11.97 13.69 15.53 P/E 29.36 25.66 22.61 Shareholding Pattern (%) As on Jun 2018 As on Mar 2018 Promoter 42.92 42.92 Public 57.08 57.08 Others -- -- 1 Year Comparative Graph ARVIND LTD S&P BSE SENSEX PEER GROUPS CMP MARKET CAP EPS(TTM) P/E (X)(TTM) P/BV(X) DIVIDEND Company Name (Rs.) Rs. in mn. (Rs.) Ratio Ratio (%) Arvind Ltd 351.30 90853.21 12.23 28.73 2.40 24.00 Vardhman Textiles Ltd 1012.40 58156.60 102.97 9.83 1.17 150.00 Orbit Exports Ltd 127.15 3593.00 - - 3.25 26.00 Raymond Ltd 726.50 44593.20 23.12 31.42 2.36 30.00

Transcript of ARVIND LTD ISIN - indianotes-live-04da772e042e45f4b8c979 ...… · ARVIND LTD Result Update...

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

ARVIND LTDResult Update (CONSOLIDATED BASIS): Q1 FY19

CMP: 351.30 SEP 27th, 2018

Overweight ISIN:INE034A01011

Index DetailsSYNOPSIS

Arvind Ltd, one of the largest integrated textile and

branded apparel players, with the presence of almost

eight decades in this industry. It is among the largest

denim manufacturers in the world.

The consolidated turnover stood at Rs. 28609.60

million for Q1 FY19 as against Rs. 25942.10

million in Q1 FY18, up by 10.28%.

During the quarter, EBIDTA stood at Rs. 2599.40

million as against Rs. 2232.90 million in the

corresponding period of the previous year, up by

16.41%.

Profit before tax (PBT) increased by 25.71% to Rs.

862.90 million in Q1 FY19 from Rs. 686.40 million

in the corresponding quarter of the previous year.

During the June quarter, net profit increased by

11.33% to Rs. 665.00 million from Rs. 597.30

million in Q1 FY18.

EPS of the company stood at Rs. 2.57 in Q1 FY19

against Rs. 2.31 in the corresponding quarter of the

previous year.

Net Sales and PAT of the company are expected to

grow at a CAGR of 14% and 6% over 2017 to

2020E, respectively.

Stock DataSector TextilesBSE Code 500101Face Value 10.0052wk. High / Low (Rs.) 477.85/337.50Volume (2wk. Avg.) 110000Market Cap (Rs. in mn.) 90853.21

Annual Estimated Results(A*: Actual / E*: Estimated)Years(Rs in mn) FY18A FY19E FY20ENet Sales 112541.90 122670.67 136164.44EBITDA 10275.80 11446.27 12666.28Net Profit 3094.70 3540.21 4017.55EPS 11.97 13.69 15.53P/E 29.36 25.66 22.61

Shareholding Pattern (%)

As on Jun 2018 As on Mar 2018

Promoter 42.92 42.92

Public 57.08 57.08

Others -- --

1 Year Comparative Graph

ARVIND LTD S&P BSE SENSEX

PEER GROUPS CMP MARKET CAP EPS(TTM) P/E (X)(TTM) P/BV(X) DIVIDEND

Company Name (Rs.) Rs. in mn. (Rs.) Ratio Ratio (%)Arvind Ltd 351.30 90853.21 12.23 28.73 2.40 24.00Vardhman Textiles Ltd 1012.40 58156.60 102.97 9.83 1.17 150.00Orbit Exports Ltd 127.15 3593.00 - - 3.25 26.00Raymond Ltd 726.50 44593.20 23.12 31.42 2.36 30.00

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

QUARTERLY HIGHLIGHTS (CONSOLIDATED BASIS)

Results updates- Q1 FY19,

(Rs in million) Jun-18 Jun-17 % Change

Revenue 28609.60 25942.10 10.28%

Net Profit 665.00 597.30 11.33%

EPS 2.57 2.31 11.29%

EBIDTA 2599.40 2232.90 16.41%

The company’s consolidated net profit stood at Rs. 665.00 million as compared to Rs. 597.30 million in the corresponding

quarter ending of previous year, increased by 11.33%. Revenue for the 1st quarter stood at Rs. 28609.60 million as against

Rs. 25942.10 million, when compared with the prior year period, grew by 10.28%. Reported earnings per share of the

company stood at Rs. 2.57 a share during the quarter, as against Rs. 2.31 per share over previous year period. Profit before

interest, depreciation and tax is Rs. 2599.40 million as against Rs. 2232.90 million in the corresponding period of the

previous year, higher by 16.41%.

Break up of Expenditure

Break up ofExpenditure

Value in Rs. Million

Q1 FY19 Q1 FY18 %Change

Cost of MaterialsConsumed 7682.30 7439.80 3%

Purchase of Stock inTrade 7168.00 1086.90 559%

Project Expenses 169.70 29.80 469%

Employees BenefitExpenses 3430.20 3101.60 11%

Depreciation &Amortization Exp 917.20 863.20 6%

Other Expenses 9034.20 9384.70 -4%

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

Segment Revenue

Business segment highlights

Branded Apparel

EBITDA for Branded Apparel grew by 75% while revenues grew by 13% over Q1 in the previous year. Adjusting for

GST & IndAS, the revenue growth was ~18%.

Power Brands – Arrow, US Polo Association, Flying Machine and Tommy Hilfiger - grew by strong 16% (20%

adjusted for GST). Unlimited – the value retail offering – grew by 20%.

Textiles

Garment volumes up ~20% following the verticalization strategy – greenfield expansion across 3 new states

underway.

Fabric volumes held nearly steady despite GST related base effect and Denim industry overcapacity.

Update on demerger

As stated earlier, the Company is looking to demerge its Branded Apparel and Engineering businesses into separate

companies. This process is progressing as planned, and final approvals are expected in early Q2.

COMPANY PROFILE

Arvind Limited is the largest Textiles, Apparel and Fashion player with revenues exceeding $1.7 billion. The company is

full supply chain partner to world’s leading fashion brands. The domestic fashion business includes the most iconic brands

like US Polo Association, Tommy Hilfiger, Calvin Klein, Arrow, Flying Machine, Gap and Sephora, to name a few.

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

FINANCIAL HIGHLIGHT (CONSOLIDATED BASIS) (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as of March 31, 2017 -2020E

FY17A FY18A FY19E FY20E

ASSETS1) Non-Current Assets

a) Property, Plant and Equipment 34800.70 36255.30 38068.07 39590.79

b) Capital Work In Progress 496.90 897.40 1166.62 1423.28

c) Investment Property 437.40 344.80 303.42 324.66

d) Goodwill 179.20 1370.20 1794.96 2046.26

e) Other Intangible Assets 1304.80 1651.90 1899.69 2203.63

f) Intangible Assets Under Development 459.30 265.00 230.55 260.52

g) Financial Assetsi) Investments 2766.70 761.40 936.52 1067.64

ii) Loans 27.70 25.70 21.85 19.44

iii) Other Financial Assets 2389.00 2605.10 2787.46 2673.17

h) Deferred Tax Assets (Net) 2242.10 2205.10 2094.85 2011.05

i) Other Non-Current Assets 742.30 808.40 870.65 932.46

Sub Total Non- Current Assets 45846.10 47190.30 50174.62 52552.90

2) Current Assetsa) Inventories 23828.00 26193.80 28184.53 30185.63

b) Financial Assets

i) Investments 0.00 0.00 0.00 0.00

ii) Trade Receivables 7948.20 17669.80 22823.51 26567.22

iii) Cash And Cash Equivalents 209.30 394.60 528.76 639.80

iv) Other Bank Balances 329.50 260.30 249.89 259.88

v) Loans 1222.10 1635.60 1897.30 1688.59

vi) Other Financial Assets 1811.80 1071.50 953.64 1020.39

c) Current Tax Assets (Net) 1101.30 1188.40 1307.24 1398.75

d) Other Current Assets 4383.50 6980.00 8445.80 9459.30

Sub Total - Current Assets 40833.70 55394.00 64390.66 71219.56Total Assets (1+2) 86679.80 102584.30 114565.28 123772.47EQUITY AND LIABILITIES

1) EQUITYa) Equity Share Capital 2583.60 2586.20 2586.20 2586.20

b) Other Equity 33086.20 35242.30 38782.51 42800.06

Total Equity 35669.80 37828.50 41368.71 45386.262) Minority Interest 1514.30 3052.80 3754.94 4430.83

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

3) Non Current Liabilitiesa) Financial Liabilities

i) Borrowings 7566.30 8487.10 9250.94 8788.39

ii) Other Financial Liabilities 449.80 440.20 426.99 436.39

b) Provisions 407.20 618.20 704.75 613.13

c) Deferred Tax Liabilities (Net) 1428.80 707.50 495.25 416.01

d) Government Grants 354.60 382.60 405.56 427.86

e) Other Non - Current Liabilities 0.00 19.30 0.00 0.00

Sub Total - Non Current liabilities 10206.70 10654.90 11283.49 10681.78

4) Current Liabilitiesa) Financial liabilities

i) Borrowings 20253.40 22637.80 24675.20 26649.22

ii) Trade Payables 14265.20 21472.20 25337.20 28124.29

iii) Other Financial Liabilities 3373.50 4690.00 5487.30 6145.78

b) Other Current Liabilities 1144.80 1876.10 2213.80 1881.73

c) Provisions 168.20 257.90 309.48 359.00

d) Government Grants 52.30 61.40 68.77 59.14

e) Current Tax Liabilities (Net) 31.60 52.70 66.40 54.45

Sub Total - Current Liabilities 39289.00 51048.10 58158.15 63273.60Total Equity And Liabilities (1+2+3+4) 86679.80 102584.30 114565.28 123772.47Annual Profit & Loss Statement for the period of 2017 to 2020E

Value(Rs.in.mn) FY17A FY18A FY19E FY20EDescription 12m 12m 12m 12mNet Sales 92576.90 112541.90 122670.67 136164.44Other Income 816.90 626.20 651.25 683.81Total Income 93393.80 113168.10 123321.92 136848.26Expenditure -83180.70 -102892.30 -111875.65 -124181.97Operating Profit 10213.10 10275.80 11446.27 12666.28Interest -2883.40 -2578.50 -2913.71 -3175.94Gross profit 7329.70 7697.30 8532.56 9490.34Depreciation -2970.80 -3593.40 -3988.67 -4387.54Exceptional Items -180.60 -227.20 -195.39 -166.08Profit Before Tax 4178.30 3876.70 4348.50 4936.72Tax -988.90 -745.70 -870.13 -987.84Profit After Tax 3189.40 3131.00 3478.36 3948.88Minority Interest -62.20 -63.40 44.50 50.29Share of Profit & Loss of Associate 19.10 27.10 17.34 18.38Net Profit 3146.30 3094.70 3540.21 4017.55Equity capital 2583.60 2586.20 2586.20 2586.20Reserves 33086.20 35242.30 38782.51 42800.06Face value 10.00 10.00 10.00 10.00EPS 12.18 11.97 13.69 15.53

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

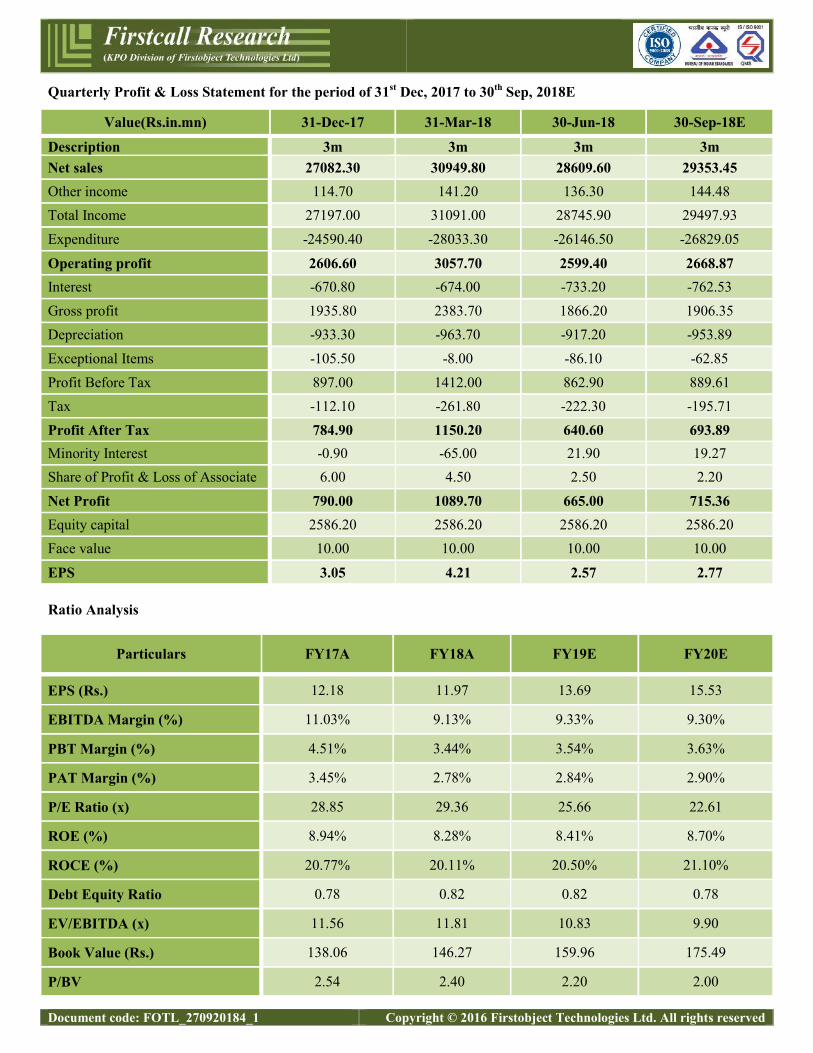

Quarterly Profit & Loss Statement for the period of 31st Dec, 2017 to 30th Sep, 2018E

Value(Rs.in.mn) 31-Dec-17 31-Mar-18 30-Jun-18 30-Sep-18E

Description 3m 3m 3m 3mNet sales 27082.30 30949.80 28609.60 29353.45Other income 114.70 141.20 136.30 144.48Total Income 27197.00 31091.00 28745.90 29497.93Expenditure -24590.40 -28033.30 -26146.50 -26829.05

Operating profit 2606.60 3057.70 2599.40 2668.87Interest -670.80 -674.00 -733.20 -762.53Gross profit 1935.80 2383.70 1866.20 1906.35Depreciation -933.30 -963.70 -917.20 -953.89Exceptional Items -105.50 -8.00 -86.10 -62.85Profit Before Tax 897.00 1412.00 862.90 889.61Tax -112.10 -261.80 -222.30 -195.71Profit After Tax 784.90 1150.20 640.60 693.89Minority Interest -0.90 -65.00 21.90 19.27Share of Profit & Loss of Associate 6.00 4.50 2.50 2.20

Net Profit 790.00 1089.70 665.00 715.36Equity capital 2586.20 2586.20 2586.20 2586.20Face value 10.00 10.00 10.00 10.00

EPS 3.05 4.21 2.57 2.77

Ratio Analysis

Particulars FY17A FY18A FY19E FY20E

EPS (Rs.) 12.18 11.97 13.69 15.53

EBITDA Margin (%) 11.03% 9.13% 9.33% 9.30%

PBT Margin (%) 4.51% 3.44% 3.54% 3.63%

PAT Margin (%) 3.45% 2.78% 2.84% 2.90%

P/E Ratio (x) 28.85 29.36 25.66 22.61

ROE (%) 8.94% 8.28% 8.41% 8.70%

ROCE (%) 20.77% 20.11% 20.50% 21.10%

Debt Equity Ratio 0.78 0.82 0.82 0.78

EV/EBITDA (x) 11.56 11.81 10.83 9.90

Book Value (Rs.) 138.06 146.27 159.96 175.49

P/BV 2.54 2.40 2.20 2.00

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

Charts

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

OUTLOOK AND CONCLUSION

At the current market price of Rs. 351.30, the stock P/E ratio is at 25.66 x FY19E and 22.61 x FY20E, respectively.

Earning per share (EPS) of the company for the earnings for FY19E and FY20E is seen at Rs. 13.69 and Rs. 15.53

respectively.

Net Sales and PAT of the company are expected to grow at a CAGR of 14% and 6% over 2017 to 2020E,

respectively.

On the basis of EV/EBITDA, the stock trades at 10.83 x for FY19E and 9.90 x for FY20E.

Price to Book Value of the stock is expected to be at 2.20 x and 2.00 x for FY19E and FY20E respectively.

Branded Apparel segment is likely to continue its industry leading 20%+ growth momentum and steady margin expansion

is expected. Backed by garment expansion and new products, Textiles segment is likely to grow by 10% with improving

margins. Hence, we say that, we are Overweight in this particular scrip for Medium to Long term investment.

INDUSTRY OVERVIEW

The cyclical upswing that is underway since mid-2016 continued to strengthen global economy in 2017. Global GDP

growth is estimated to have increased from 2.4% in 2016 to 3% in 2017 - the highest growth rate in six years. With

growth increasing in more than half of the world’s economies, it is the broadest synchronized growth since 2010. Global

growth is projected to edge up to 3.1% in 2018, as the cyclical momentum continues.

India had many reasons to cheer in 2017 as the economy made a great comeback in the later part of the year riding on

domestic demand with strong private consumption and push on public infrastructure spending. The country weathered the

aftermath of demonetisation and the disruption post GST roll-out to register strong GDP growth. India regained the title of

fastest growing major economy in the world by registering 7.2% growth in GDP (y-o-y) in the December Quarter of 2017,

after lagging behind China for year. This helped in registering a GDP growth of 6.7% for 2017 and the momentum is

expected to continue with GDP growth projected at 7.2% for 2018 [UN estimate].

Also, despite the revived growth, private investments continue to be sluggish in India. Fresh investment announcements

by Indian companies declined to a 13-year low of Rs 77,000 crores in the December quarter, as per Centre for Monitoring

Indian Economy (CMIE). Low capacity utilization, high leverage and increasing stalled projects are driving the slow-

down in investments. Prevalence of higher NPAs has resulted in slow-down in bank lending for fresh projects and despite

making long strides in ease of doing business index, lack of clearances and problems with raw materials and land

acquisition are contributing to stalling of projects.

Exports grew at 9.8% in FY2017-18, the highest growth in six years. However, it is the lowest as a proportion of GDP

since 2003-04. With a higher rise in imports, overall trade deficit almost doubled to $87 Billion during Apr-Feb FY17-18,

compared to the previous year. With the ongoing global trade recovery, exports can strongly contribute to the growth

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

story; however, this calls for focus on better infrastructure, affordable capital and improved labour productivity. On a

positive note, strong private consumption and services are expected to continue to support economic activity. The private

investment is expected to revive as the corporate sector adjusts to the GST regime and as infrastructure spending

increases.

Global Apparel Market

In 2017, the world apparel market grew by 3.6% driven by ~5% growth in Asia Pac and 8% growth in Rest of the World

markets. China and India have led the growth chart with both countries registering strong growth in 2017. On the other

hand, Western Europe and USA, the two large apparel markets continue to struggle and grew less than 1% in 2017.

After improving steadily in 2017, global fashion industry is expected to continue its recovery in 2018 to register ~5%

growth on the back of continued strong performance in Asia Pacific. Global fashion industry is undergoing a massive shift

due to the changing customer preferences. Large scale adoption of digital technology is changing the paradigm in terms of

consumer expectations. There is increasing focus on convenience, quality, variety and personalisation. Most of the global

brands are already facing challenges on account of fast fashion trends. Changing customer preferences are compelling

them to relook at their supply chain strategy to better compete in the market space. Brands now need to ensure that their

merchandising, logistics and suppliers are more integrated than before to reduce the lead time of sourcing Indian apparel

market picked up growth in the beginning of the year as the impact of demonetisation subsided. However, the euphoria

was short lived as implementation of GST impacted the growth in the industry. Unorganised sector was impacted

disproportionately owing to slower adoption of the new regime. This also marked a gradual movement away from the

unbranded and unorganised market towards the branded and organised apparel, a trend which the company believes will

continue.

Despite the challenges posed by demonetisation, Indian apparel industry delivered strong growth in 2016 by registering a

growth of 14% in value terms, in line with the average growth in the last five years. Children’s wear was the fastest

growing segment, followed by Menswear.

Indian Textile Market Outlook

Textiles and apparel sector plays a major role in the country’s economy by providing direct and indirect employment to

more than 100 million people. The industry went through a bad patch in 2017 as it reeled under the impact of GST roll out

and the reduction of export incentives. The textile exports fell sharply during the year. While GST led disruption is

gradually getting back to normal, reduction in export incentives has had a deeper impact on reducing the export

competitiveness of the country. Indian textile industry continues to be dominated by cotton, accounting for nearly 3/4th of

the total fibre consumption in the country. Cotton production in the country has been estimated to be 360 lakh bales in

2017-18, up from 337 lakh bales produced last year. With last year’s inventory and relatively lower imports, total supply

of cotton is likely to be 410 lakhs bales in FY17-18 vis-à-vis a supply of 401 lakhs bales in FY16-17 Cotton prices

remained volatile through the year impacting the profitability of the industry. With higher prices for seed cotton in the

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

market, area under cotton cultivation is seeing a sharp jump this season with 121 lakh hectares under cotton, a 14%

increase compared to previous year. However, Government of India has announced the MSP to be at least 50% higher

than the cost of production which could lead to strengthening of cotton price. Also, decreasing parity for imported cotton

is likely to drive year-end inventory to a relatively tight position of less than 30 lakh bales and can keep the cotton prices

at elevated levels.

India remains the second largest exporter of Textile and Clothing (T&C) with a global share of ~5%. Overall T&C exports

in key Asian geographies have come down over the last few years primarily driven by lower exports for both China and

India. Driven by rising labour cost and concerns over pollution, China has been losing its competitiveness in the global

market. China’s declining market share has provided an opportunity for other key textile exporters to scale up, primarily

through the garmenting route. Bangladesh’s exports have been growing rapidly and the country is currently the third

largest textile exporter globally.

After falling 5% in previous year, Indian textile export grew by ~1% in FY17-18 primarily led by Cotton textiles. While

the outlook remains positive, there are a few short term challenges facing the sector today.

Government reduced the duty incentives on textile exports w.e.f. October 2017. Sharp reduction in incentives has

impacted the garmenting sector quite negatively and exports saw a double digit decline across both knitted and woven

garments since October. Indian currency also remained strong through the year, impacting the cost competitiveness of

Indian textile players vis-à-vis global peers.

Domestic textile market was also weak post the implementation of GST. The trade channel, which was not subjected to

tax earlier, took time to adjust to the new tax regime, resulting in a sharp fall in domestic demand. While the company

believes that the medium term demand drivers remain intact, it will take a couple of quarters for the demand to normalise.

Over time, the company believe growing Indian economy and higher disposable income will lead to strong domestic

demand which augurs well for textile industry.

Given the challenging environment, Arvind continues to pursue the strategy of being more vertically integrated so as to

shorten the supply chain and become more strategic to the customers. The company is investing in garmenting facilities

globally, the company believe that an integrated offering will not only help us in have better visibility but also create more

stickiness with customers. As announced earlier, Arvind has set up garmenting factories in Ethiopia to take advantage of

lower labour cost, duty savings and lower shipment time to the US and Europe markets. In addition, the company is

setting up garmenting facility in Jharkhand to further expand the company capacities.

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

Disclosure Section

The information and opinions in Firstcall Research was prepared by our analysts and it does not constitute an offer orsolicitation for the purchase or sale of any financial instrument including any companies scrips or this is not an officialconfirmation of any transaction. The information contained herein is from publicly available secondary sources and dataor other secondary sources believed to be reliable but we do not represent that it is accurate or complete and it should notbe relied on as such. Firstcall Research or any of its affiliates shall not be in any way responsible for any loss or damagethat may arise to any person from any inadvertent error in the information contained in this report. Firstcall Research and/or its affiliates and/or employees will not be liable for the recipients’ investment decision based on this document.

Analyst Certification

The following analysts hereby state that their views about the companies and sectors are on best effort basis to the best oftheir knowledge. Unless otherwise stated, the individuals listed on the cover page of this report are research analysts. Theanalyst qualifications, sectors covered and their exposure if any are tabulated hereunder:

Name of the Analyst Qualifications SectorsCovered

Exposure/Interest tocompany/sector UnderCoverage in the CurrentReport

Dr.C.V.S.L. Kameswari M.Sc, PGDCA,M.B.A,Ph.D (Finance)

Pharma &Diversified

No Interest/ Exposure

U. Janaki Rao M.B.A CapitalGoods

No Interest/ Exposure

B. Anil Kumar M.B.A Auto, IT &FMCG

No Interest/ Exposure

M. Vijay M.B.A Diversified No Interest/ ExposureV. Harini Priya M.B.A Diversified No Interest/ ExposureB. Srikanth M.B.A Diversified No Interest/ Exposure

Important Disclosures on Subject Companies

In the next 3 months, neither Firstcall Research nor the Entity expects to receive or intends to seek compensation for anyservices from the company under the current analytical research coverage. Within the last 12 months, Firstcall Researchhas not received any compensation for its products and services from the company under the current coverage. Within thelast 12 months, Firstcall Research has not provided or is providing any services to, or has any client relationship with, thecompany under current research coverage.

Within the last 12 months, Firstcall Research has neither provided or is providing any services to and/or in the past has notentered into an agreement to provide services or does not have a client relationship with the company under the researchcoverage.

Certain disclosures listed above are also for compliance with applicable regulations in various jurisdictions. FirstcallResearch does not assign ratings of Buy, Hold or Sell to the stocks we cover. Overweight, Equal-weight, No-Weight andUnderweight are not the equivalent of buy, hold and sell. Investors should carefully read the definitions of all weightsused in Firstcall Research. In addition, since Firstcall Research contains more complete information concerning theanalyst's views, investors should carefully read Firstcall Research, in its entirety, and not infer the contents from theweightages assigned alone. In any case, weightages (or research) should not be used or relied upon as investment advice.

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

An investor's decision to buy or sell should depend on individual circumstances (such as the investor's own discretion, hisability of understanding the dynamics, existing holdings) and other considerations.

Analyst Stock Weights

Overweight (O): The stock's total return is expected to exceed the average total return of the analyst's industry (orindustry team's) coverage universe, on a risk-adjusted basis, over the next 12-18 months.

Equal-weight (E): The stock's total return is expected to be in line with the average total return of the analyst's industry(or industry team's) coverage universe, on a risk-adjusted basis, over the next 12-18 months.

No-weight (NR): Currently the analyst does not have adequate conviction about the stock's total return relative to theaverage total return of the analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis, over the next12-18 months.

Underweight (U): The stock's total return is expected to be below the average total return of the analyst's industry (orindustry team's) coverage universe, on a risk-adjusted basis, over the next 12-18 months.

Unless otherwise specified, the weights included in Firstcall Research does not indicate any price targets. The statisticalsummaries of Firstcall Research will only indicate the direction of the industry perception of the analyst and theinterpretations of analysts should be seen as statistical summaries of financial data of the companies with perceivedindustry direction in terms of weights.

Firstcall Research may not be distributed to the public media or quoted or used by the public media without the expresswritten consent of Firstcall Research. The reports of Firstcall Research are for Information purposes only and is not to beconstrued as a recommendation or a solicitation to trade in any securities/instruments. Firstcall Research is not abrokerage and does not execute transactions for clients in the securities/instruments.

Firstcall Research - Overall StatementS.No Particulars Remarks1 Comments on general trends in the securities market Full Compliance in Place2 Discussion is broad based and also broad based indices Full Compliance in Place3 Commentaries on economic, political or market conditions Full Compliance in Place4

Periodic reports or other communications not for public appearanceFull Compliance in Place

5 The reports are statistical summaries of financial data of the companies as and whereapplicable

Full Compliance in Place

6 Analysis relating to the sector concerned Full Compliance in Place7 No material is for public appearance Full Compliance in Place8 We are no intermediaries for anyone and neither our entity nor our analysts have any

interests in the reportsFull Compliance in Place

9 Our reports are password protected and contain all the required applicable disclosures Full Compliance in Place

10 Analysts as per the policy of the company are not entitled to take positions either fortrading or long term in the analytical view that they form as a part of their work

Full Compliance in Place

11 No conflict of interest and analysts are expected to maintain strict adherence to thecompany rules and regulations.

Full Compliance in Place

12As a matter of policy no analyst will be allowed to do personal trading or deal andeven if they do so they have to disclose the same to the company and take priorapproval of the company

Full Compliance in Place

Document code: FOTL_270920184_1 Copyright © 2016 Firstobject Technologies Ltd. All rights reserved

13Our entity or any analyst shall not provide any promise or assurance of any favorableoutcome based on their reports on industry, company or sector or group

Full Compliance in Place

14 Researchers maintain arms length/ Chinese wall distance from other employees of theentity

Full Compliance in Place

15No analyst will be allowed to cover or do any research where he has financial interest

Full Compliance in Place

16 Our entity does not do any reports upon receiving any compensation from anycompany

Full Compliance in Place

Firstcall Research Provides

Industry Research on all the Sectors and Equity Research on Major Companiesforming part of Listed and Unlisted Segments

For Further Details Contact:Mobile No: 09959010555

E-mail: [email protected]@firstcallresearch.comwww.firstcallresearch.com