Article New Energy Architecture India Accenture

36

New Energy Architecture India World Economic Forum In partnership with Accenture

description

Smart grid

Transcript of Article New Energy Architecture India Accenture

New Energy Architecture India

World Economic Forum In partnership with Accenture

1New Energy Architecture India

Contents

A note on the creation of this study

This World Economic Forum report was developed by the Forum’s Energy Industry Partnership in collaboration with Accenture.

A series of interviews with stakeholders from across the energy value chain conducted in New Delhi during October 2011, and a private session conducted at the India Economic Summit in Mumbai in November 2011, form the basis of the sections on India’s objectives for a New Energy Architecture and the enabling environments required to achieve them.

The views expressed in this publication do not necessarily reflect those of the World Economic Forum or Accenture.

Contributors

World Economic Forum

• Roberto Bocca, Senior Director, Head of Energy Industry

• Espen Mehlum, Associate Director, Head of Knowledge Management and Integration Energy Industries

Project Adviser: Accenture

• Arthur Hanna, Managing Director, Energy Industry

• James Collins, Senior Manager, Energy Strategy

• Mike Moore, Project Manager, New Energy Architecture, Accenture Secondee

• With further support from Timothy Hendrikz, Bryan Hori, Piush Kothari and Samuel Madden

2 Executive Summary

4 A Methodology for Managing Transition Effectiveness

6 Step 1: Assessing Current Energy Architecture Performance

7 1.1 Introduction to India’s Energy Architecture

8 1.2 India’s Current Energy Architecture Performance

13 1.3 Comparing India’s Current Energy Architecture Performance with the Grow Archetype

16 Step 2: Creating New Energy Architecture Objectives

17 2.1 Defining India’s Objectives for a New Energy Architecture

20 Step 3: Defining the Enabling Environment

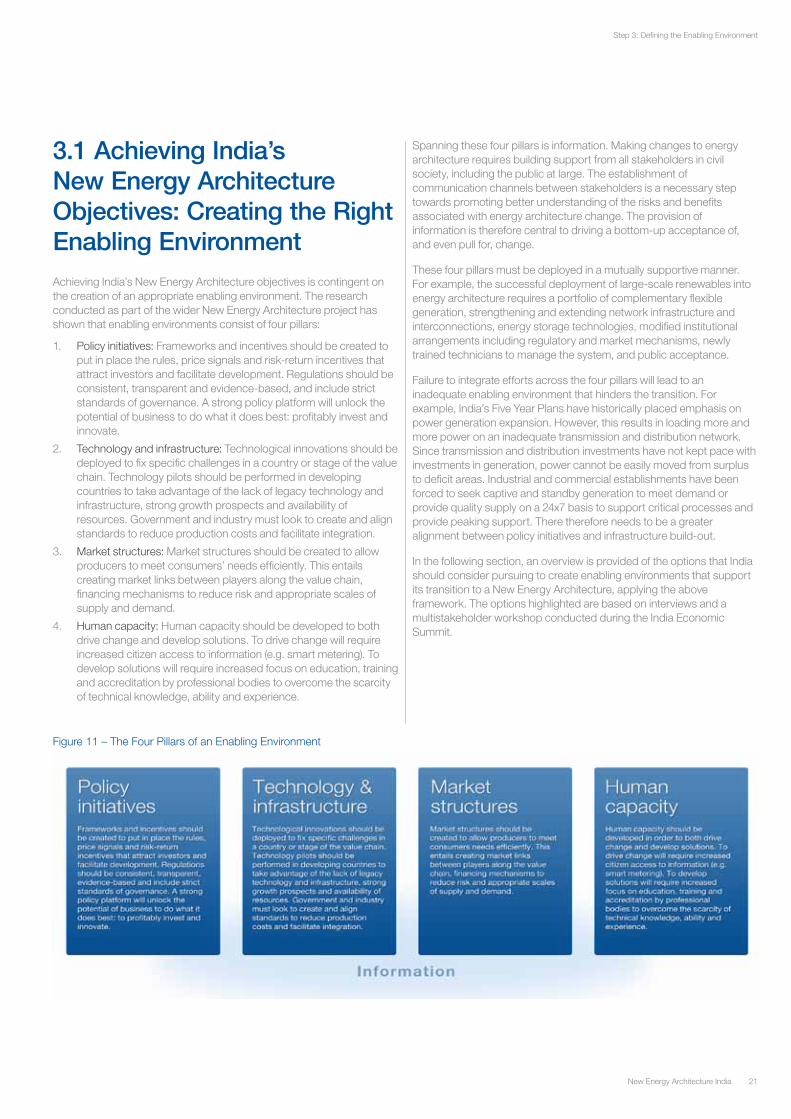

21 3.1 Achieving India’s New Energy Architecture Objectives: Creating the Right Enabling Environment

22 3.2 Defining Enabling Environments for India’s New Energy Architecture

28 Step 4: Defining Areas of Leadership

29 4.1 A Multistakeholder Action Plan

30 Appendices: The Creation of the Energy Architecture Performance Index

31 Appendix A: Computation and Structure of the Energy Architecture Performance Index

32 Appendix B: Technical Notes and Sources for the Energy Architecture Performance Index

2 New Energy Architecture India

Making the Transition

The focus for the coming years will be on supporting economic growth by providing a secure supply of energy. To provide a secure supply of energy – and address further issues of distorted energy pricing, poor air quality, growing water scarcity and import dependence, the unreliability of the grid and continuing energy poverty – require India to bring new forms of supply online, deliver it more effectively to consumers (both urban and rural), and do so at market-based prices (based upon the gradual phase-out of subsidies). To do so, India should consider pursuing the following set of objectives:

• Objective 1 – Augment resources for energy security: India must look to encourage and expand the presence of international coal and oil & gas companies to provide the investment and technical expertise to develop domestic hydrocarbon resources, invest in continuing development of the renewable industry and look to increase efficiency in end use consumption.

• Objective 2 – Provide access to modern forms of energy for all: India must promote the role of the private sector in developing and deploying decentralized distribution and generation and modern cookstove and lighting technologies to rural areas where lack of awareness and state-level bureaucracy is impeding progress.

• Objective 3 –Strengthening energy carriers: The financial health of transmission and distribution companies must be improved to enable investment in strengthening, expanding and developing the power grid while gas infrastructure must continue to expand its small but growing coverage.

• Objective 4 –Rationalize energy prices: To transition to a more efficient economy, India needs a well-instituted market mechanism for energy pricing and must gradually withdraw wide-scale energy subsidies while ensuring that transparent and effective distribution of kerosene and LPG to those below the poverty line is implemented.

Executive Summary

The last decade has been a period of tremendous growth for India. This growth has driven a large increase in energy demand, with India now being the fourth largest consumer of energy globally. Between 1990 and 2008, total demand grew by 95%2 and has put India’s energy architecture under severe strain. India has provisionally set a 9% GDP growth target as part of the 12th Five Year Plan, which will require energy supply to grow 6.5% per year.3 This represents a much more significant growth target for the sector than in previous years. The focus for the coming years will therefore be on supporting economic growth by providing a secure supply of energy. Indeed, “inability to meet energy demand could be the single biggest constraining factor to India’s growth story.”4 This will require India to bring new forms of supply online, deliver it more effectively to consumers (both urban and rural), and do so at a market-based price (based upon the eventual eradication of subsidies) that sends appropriate signals to both the demand and supply sides.

India does have a responsibility to achieve its growth trajectory in an environmentally sustainable manner, and has set a voluntary target to cut the emissions intensity of GDP by 20-25% by 2020 compared with 2005 levels.5 Therefore, the way forward should be to identify common ground between climate change policy and economic growth and pursue measures that achieve both.

Considering that there needs to be a significant expansion in energy infrastructure, India has an opportunity to pursue development while managing emissions growth, enhancing its energy security and creating world-scale clean-technology industries. This would require that India leapfrog inefficient technologies, assets and practices and deploy ones that are more efficient and less emission-intensive. India should therefore not look to copy the Western model of energy infrastructure development, and instead pursue a development path that is particular to its local conditions. This would require that India leapfrog inefficient technologies, assets and practices and deploy ones that are more efficient and less emission intensive, with a key opportunity being the expansion of decentralized distribution and generation.

Inability to meet energy demand could be the single biggest constraining factor

to India’s growth story.1

1 Interviewee, New Delhi, October 20112 World Bank, World Development Indicators3 An Approach to the 12th Five Year Plan, Indian Planning Commission, 20114 Interview participant, New Delhi, October 20115 Natural Resources Defense Council, From Copenhagen Accord to Climate Action: Tracking National Commitments to Curb Global Warming, http://www.nrdc.org/international/copenhagenaccords/

3New Energy Architecture India

The Required Enabling Environment

To enable India to address its objectives, an enabling environment will be needed. The creation of an enabling environment will require support from across all four pillars:

India has a strong policy framework at the national level – but implementation at the state level is often lacking. The public policy regime for the promotion of renewable energy at the national level is viewed as being among the most effective in the world – “a benchmark for all emerging markets”.6 However, success in implementing national targets varies significantly on a state by state basis. Poor performing states should be targeted to promote capacity building and encourage wider economic development.

Development of the power grid is urgently needed. The transmission and distribution network is in urgent need of investment and development and India has the opportunity to leapfrog western countries through the deployment of more efficient, less intensive and smarter technology. India has seen rapid development in its renewables sector, especially in wind energy and this expertise and momentum must be leveraged and applied to other technologies, particularly solar.

Costly and inefficient subsidies are damaging the economy. The energy market must be made more transparent and efficient to attract foreign and private investment. This will require the removal of subsidies and increased separation between the government and state-owned companies. Market structures for the transmission of electricity between states must be rationalized to foster the development of renewable generation and better load balancing.

India can become a centre of excellence for renewable energy R&D. India has a large and growing educated population and this must be leveraged to provide the technical skills that will be required to make the transition to a New Energy Architecture. Society must be more aware of the consequences of energy consumption and the role of decentralized distribution and generation in providing modern forms of energy and bringing opportunities for economic development.

The provision of information is essential for the deployment of new technologies. The effective, transparent and sympathetic dissemination of information will be central in developing India’s energy architecture, from communicating the removal of subsidies to the need to consume energy more efficiently. Honest and upfront communication will also be essential to gaining the involvement of international and private energy companies in the development of India’s hydrocarbon resources.

The government’s role in creating a strong, stable and transparent policy framework is essential. This will require strong political leadership to manage the effective removal of subsidies and enable the benefits from increased private sector participation to be fully passed onto the public. India’s population is growing in size and wealth and private companies must look to exploit this opportunity, this will involve investing in collaborative partnerships to gain access to technology and skills and deploying new technologies to market. The true cost of energy use and waste must be communicated by civil society so that changes in subsidy levels and energy architecture are accepted. Cultural changes such as the acceptability of electricity theft must be altered. The role of modern forms of energy in developing the welfare and economy of rural areas must be imparted.

The New Energy Architecture Project

New Energy Architecture: India builds on the methodology and findings of the World Economic Forum’s wider work, New Energy Architecture: Enabling an effective transition. This project aims to better understand how countries can make the transition to a New Energy Architecture that more effectively underpins economic growth and development, environmental sustainability and energy access and security.

The study provides a basis for discussion and a valuable tool for policy-makers, industry and other stakeholders to use in identifying the current energy architecture challenges for India and the enabling environments that should be created to drive the transition to a New Energy Architecture. We hope it will provide support for any discussion on India’s energy architecture aimed at generating concrete insight and priorities for action.

6 Tulsi R. Tanti, Wind matters: Making the case for wind in India, Suzlon, 2011

Executive Summary

4 New Energy Architecture India

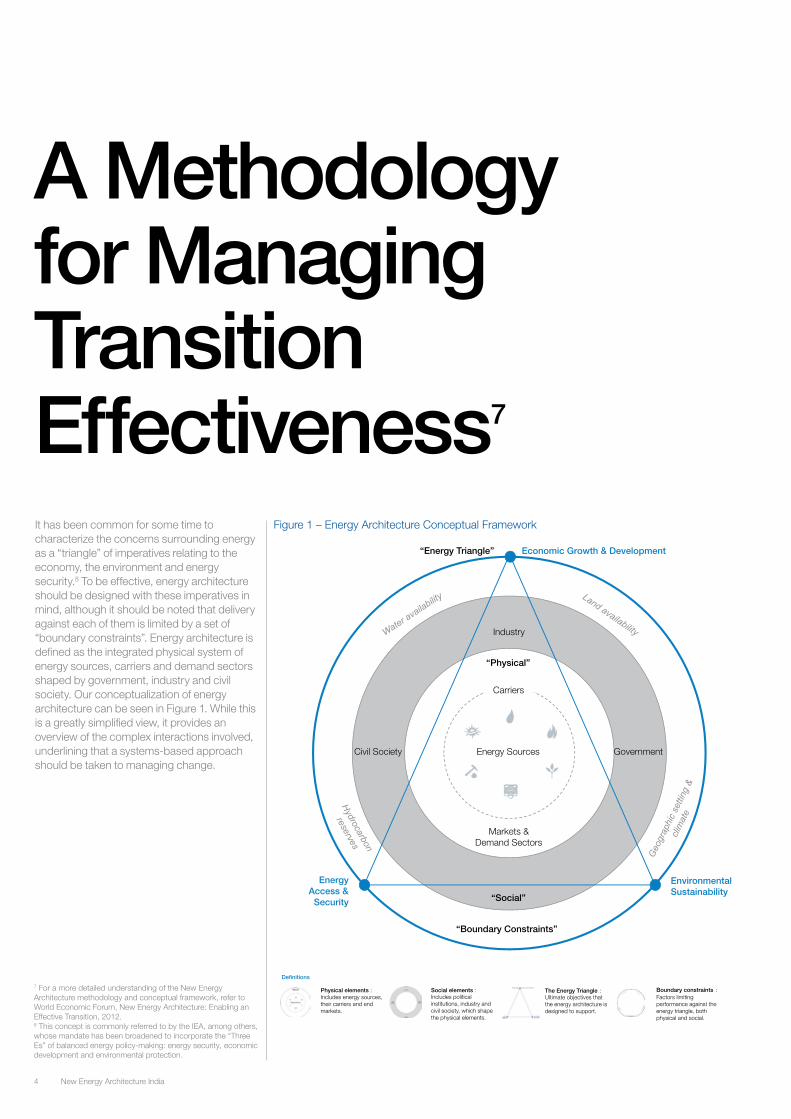

It has been common for some time to characterize the concerns surrounding energy as a “triangle” of imperatives relating to the economy, the environment and energy security.8 To be effective, energy architecture should be designed with these imperatives in mind, although it should be noted that delivery against each of them is limited by a set of “boundary constraints”. Energy architecture is defined as the integrated physical system of energy sources, carriers and demand sectors shaped by government, industry and civil society. Our conceptualization of energy architecture can be seen in Figure 1. While this is a greatly simplified view, it provides an overview of the complex interactions involved, underlining that a systems-based approach should be taken to managing change.

Energy Access &

Security

Economic Growth & Development

Environmental Sustainability

Carriers

Energy Sources

Markets & Demand Sectors

“Social”

“Physical”

Industry

Government Civil Society

“Boundary Constraints”

“Energy Triangle”

Physical elements : Includes energy sources, their carriers and end markets.

Social elements : Includes political institutions, industry and civil society, which shape the physical elements.

The Energy Triangle : Ultimate objectives that the energy architecture is designed to support.

Boundary constraints : Factors limiting performance against the energy triangle, both physical and social.

Definitions

Energy Access &

Security

Economic Growth & Development

Environmental Sustainability

Carriers

Energy Sources

Markets & Demand Sectors

“Social”

“Physical”

Industry

Government Civil Society

“Boundary Constraints”

“Energy Triangle”

Physical elements : Includes energy sources, their carriers and end markets.

Social elements : Includes political institutions, industry and civil society, which shape the physical elements.

The Energy Triangle : Ultimate objectives that the energy architecture is designed to support.

Boundary constraints : Factors limiting performance against the energy triangle, both physical and social.

Definitions

Figure 1 – Energy Architecture Conceptual Framework

A Methodology for Managing Transition Effectiveness7

7 For a more detailed understanding of the New Energy Architecture methodology and conceptual framework, refer to World Economic Forum, New Energy Architecture: Enabling an Effective Transition, 2012.8 This concept is commonly referred to by the IEA, among others, whose mandate has been broadened to incorporate the “Three Es” of balanced energy policy-making: energy security, economic development and environmental protection.

5New Energy Architecture India

This project was initiated to help decision-makers enable a more effective transition to a New Energy Architecture. To do so, a methodology has been created to help them look to the long term and to provide a stable policy environment, based on a holistic and in-depth understanding of the consequences of decisions across the energy value chain. The end result will be a New Energy Architecture that is more responsive to balancing the imperatives of the energy triangle. This process comes in four steps (see Figure 2):

Step 1 – Assessing Current Energy Architecture Performance: This process begins with an assessment of current energy architecture performance using the Energy Architecture Performance Index (EAPI); a composite indicator that considers economic development, energy access and environmental sustainability. This is intended to help countries to monitor the progress of their transition, and guide policy and investment decisions with regard to energy accordingly.

Step 2 – Creating New Energy Architecture Objectives: Based on strengths and weaknesses identified, a set of objectives for a New Energy Architecture that more effectively meets the imperatives of the energy triangle is created. These objectives are tested through in-country interviews with representatives from across the energy value chain.

Step 3 – Defining the Enabling Environment: An enabling environment that supports New Energy Architecture objectives is designed. Interviews are used to identify the enabling environments that should be put in place, with the suggestions further tested through a multistakeholder workshop.

Step 4 – Introducing Areas of Leadership: The ultimate output is the creation of an action plan that details the relative roles of government, industry and civil society in creating an enabling environment for the transition.

In the following sections, the methodology is applied to India. This begins with an overview of India’s current energy architecture and the results of the Energy Architecture Performance Index. India’s objectives for a New Energy Architecture are then identified, based on where its current strengths and weaknesses lie. This is followed by an exploration of the enabling environments that need to be created to achieve objectives. The final section discusses the roles of government, industry and civil society in working collaboratively to create an enabling environment.

Figure 2 – New Energy Architecture Methodology

a) Understand current energy architecture

b) Select KPIs to assess current and historic performance

1. Assessing current energy architecture performance

2. Creating New Energy Architecture objectives

4. Defining areas of leadership

a) Highlight energy architecture challenges

b) Identify New Energy Architecture objectives

a) Develop high-level action plan for steps to be taken by government, industry, the finance community and civil society to shape the transition

• What are the objectives for a New Energy Architecture?

• Who is responsible for implementing enabling environments?

• How is energy architecture currently performing?

Key

que

stio

n A

ctiv

ity

3. Defining the enabling environment

a) Create an enabler “toolkit” that highlights the potential actions that can be taken to accelerate the transition

b) Map enablers to transition objectives

• What enabling environment will achieve transition objectives?

The Energy Architecture Performance Index An archetype approach

The four pillars of an enabling environment

Key considerations for stakeholders

A Methodology for Managing Transition Effectiveness2

6 New Energy Architecture India

Step 1: Assessing Current Energy Architecture Performance

9 The Economic Times, India eyeing 63,000 MW nuclear power capacity by 2032: NPCIL, 11 October 201010 References to India’s energy balance are sourced from the IEA.11 Prayas, Energy Group, An Overview of Indian Energy Trends: Low Carbon Growth and Development Challenges, September 200912 CEA Annual Report 2009-2010; Ministry of Power, Power Sector at a Glance “ALL INDIA”13 ibid14 Ministry of Coal, Annual Report 2009-201015 Ministry of Coal, Provisional Coal Statistics 2009-2010

7New Energy Architecture India

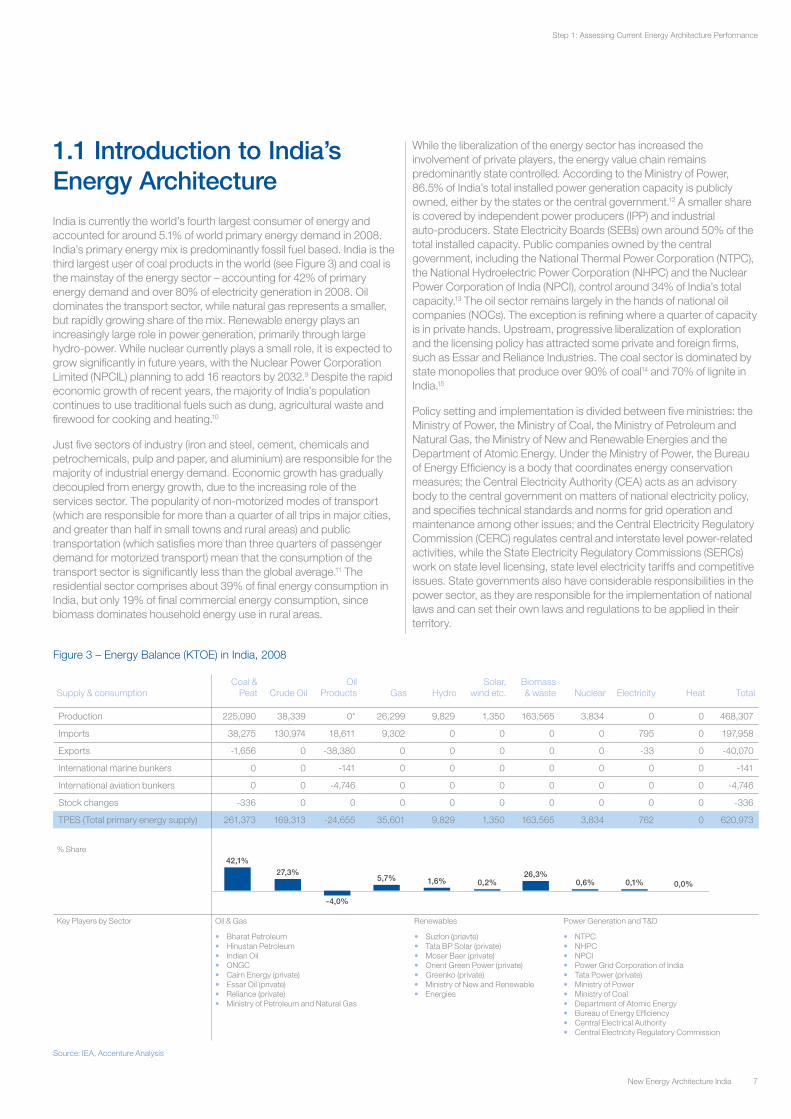

India is currently the world’s fourth largest consumer of energy and accounted for around 5.1% of world primary energy demand in 2008. India’s primary energy mix is predominantly fossil fuel based. India is the third largest user of coal products in the world (see Figure 3) and coal is the mainstay of the energy sector – accounting for 42% of primary energy demand and over 80% of electricity generation in 2008. Oil dominates the transport sector, while natural gas represents a smaller, but rapidly growing share of the mix. Renewable energy plays an increasingly large role in power generation, primarily through large hydro-power. While nuclear currently plays a small role, it is expected to grow significantly in future years, with the Nuclear Power Corporation Limited (NPCIL) planning to add 16 reactors by 2032.9 Despite the rapid economic growth of recent years, the majority of India’s population continues to use traditional fuels such as dung, agricultural waste and firewood for cooking and heating.10

Just five sectors of industry (iron and steel, cement, chemicals and petrochemicals, pulp and paper, and aluminium) are responsible for the majority of industrial energy demand. Economic growth has gradually decoupled from energy growth, due to the increasing role of the services sector. The popularity of non-motorized modes of transport (which are responsible for more than a quarter of all trips in major cities, and greater than half in small towns and rural areas) and public transportation (which satisfies more than three quarters of passenger demand for motorized transport) mean that the consumption of the transport sector is significantly less than the global average.11 The residential sector comprises about 39% of final energy consumption in India, but only 19% of final commercial energy consumption, since biomass dominates household energy use in rural areas.

While the liberalization of the energy sector has increased the involvement of private players, the energy value chain remains predominantly state controlled. According to the Ministry of Power, 86.5% of India’s total installed power generation capacity is publicly owned, either by the states or the central government.12 A smaller share is covered by independent power producers (IPP) and industrial auto-producers. State Electricity Boards (SEBs) own around 50% of the total installed capacity. Public companies owned by the central government, including the National Thermal Power Corporation (NTPC), the National Hydroelectric Power Corporation (NHPC) and the Nuclear Power Corporation of India (NPCI), control around 34% of India’s total capacity.13 The oil sector remains largely in the hands of national oil companies (NOCs). The exception is refining where a quarter of capacity is in private hands. Upstream, progressive liberalization of exploration and the licensing policy has attracted some private and foreign firms, such as Essar and Reliance Industries. The coal sector is dominated by state monopolies that produce over 90% of coal14 and 70% of lignite in India.15

Policy setting and implementation is divided between five ministries: the Ministry of Power, the Ministry of Coal, the Ministry of Petroleum and Natural Gas, the Ministry of New and Renewable Energies and the Department of Atomic Energy. Under the Ministry of Power, the Bureau of Energy Efficiency is a body that coordinates energy conservation measures; the Central Electricity Authority (CEA) acts as an advisory body to the central government on matters of national electricity policy, and specifies technical standards and norms for grid operation and maintenance among other issues; and the Central Electricity Regulatory Commission (CERC) regulates central and interstate level power-related activities, while the State Electricity Regulatory Commissions (SERCs) work on state level licensing, state level electricity tariffs and competitive issues. State governments also have considerable responsibilities in the power sector, as they are responsible for the implementation of national laws and can set their own laws and regulations to be applied in their territory.

1.1 Introduction to India’s Energy Architecture

Step 1: Assessing Current Energy Architecture Performance

Source: IEA, Accenture Analysis

Figure 3 – Energy Balance (KTOE) in India, 2008

Supply & consumptionCoal &

Peat Crude OilOil

Products Gas HydroSolar,

wind etc.Biomass & waste Nuclear Electricity Heat Total

Production 225,090 38,339 0* 26,299 9,829 1,350 163,565 3,834 0 0 468,307

Imports 38,275 130,974 18,611 9,302 0 0 0 0 795 0 197,958

Exports -1,656 0 -38,380 0 0 0 0 0 -33 0 -40,070

International marine bunkers 0 0 -141 0 0 0 0 0 0 0 -141

International aviation bunkers 0 0 -4,746 0 0 0 0 0 0 0 -4,746

Stock changes -336 0 0 0 0 0 0 0 0 0 -336

TPES (Total primary energy supply) 261,373 169,313 -24,655 35,601 9,829 1,350 163,565 3,834 762 0 620,973

% Share

Key Players by Sector Oil & Gas Renewables Power Generation and T&D

• Bharat Petroleum• Hinustan Petroleum• Indian Oil• ONGC• Cairn Energy (private)• Essar Oil (private)• Reliance (private)• Ministry of Petroleum and Natural Gas

• Suzlon (priavte)• Tata BP Solar (private)• Moser Baer (private)• Orient Green Power (private)• Greenko (private)• Ministry of New and Renewable• Energies

• NTPC• NHPC• NPCI• Power Grid Corporation of India• Tata Power (private)• Ministry of Power• Ministry of Coal• Department of Atomic Energy • Bureau of Energy Efficiency• Central Electrical Authority• Central Electricity Regulatory Commission

42,1%27,3%

-4,0%

5,7% 1,6% 0,2%26,3%

0,6% 0,1% 0,0%

8 New Energy Architecture India

KPI 2008 2000 1990 Cumulative index change 1990-2008Index Actual Index Actual Index* Actual

EAPI 1.02 0.84 0.69

Economic Growth and Development 0.42 0.37 0.28

GDP (PPP) per capita (current USD)/capita 0.05 2,064 0.03 1,270 0.01 776

HDI 0.21 0.51 0.09 0.44 0.00 0.39

Cost of energy imports as a share of GDP (%) 0.49 10.23% 0.82 3.88% 0.89 2.40%

Energy intensity GDP (PPP) per toe 0.59 0.19 0.29 0.29 0.00 0.42

Share of mineral products in export (%) 0.65 30.92% 0.67 28.61% 0.67 28.61%

Environmental Sustainability 0.19 0.05 0.05

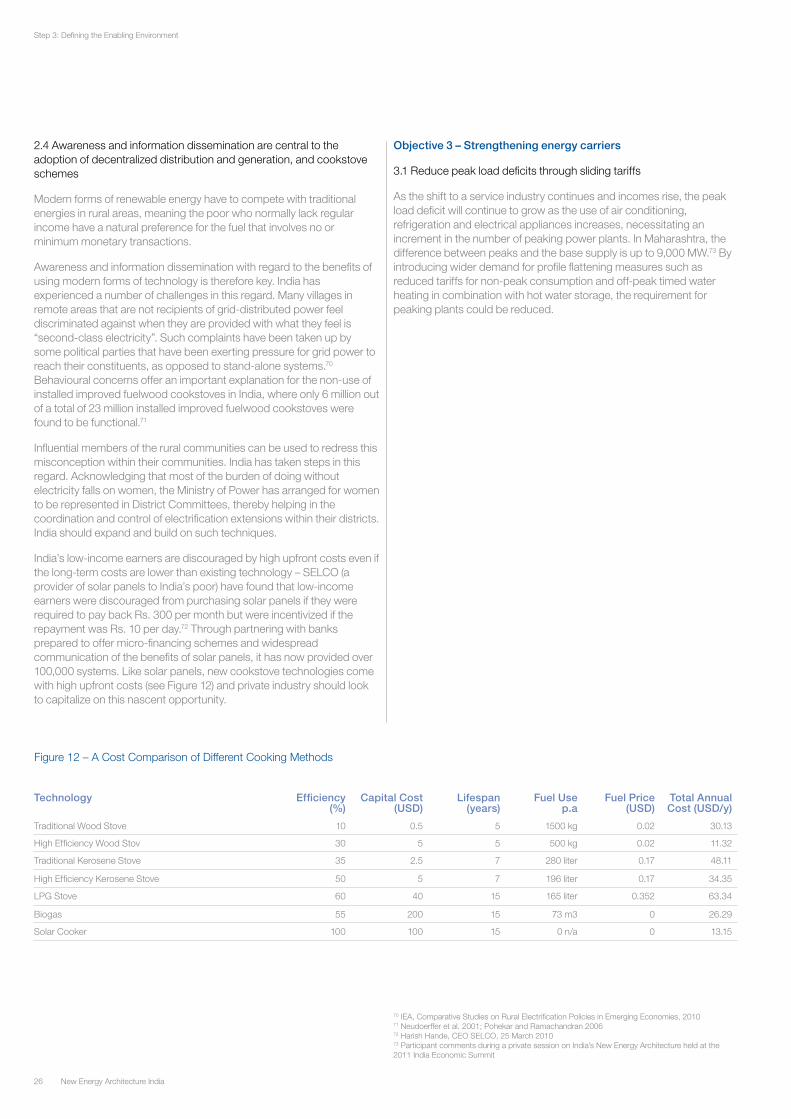

Carbon intensity of energy use (tCO2/2000 USD) 0.26 1.38 0.10 1.67 0.09 1.69

Share of non-carbon energy sources(%) 0.12 2.42% 0.12 2.39% 0.12 2.44%

Outdoor air pollution (PM10 [mg/m3] p.a.) 0.38 59,23 0.00 92.88 0.00 110.55

Water scarcity (withdrawals/internal resources) 0.00 47.84% 0.00 47.84% 0.00 39.18%

Energy Access & Security 0.41 0.41 0.36

Import dependence/TPES (%) 0.32 24.58% 0.34 20.25% 0.38 8.49%

Quality of electricity supply (0-7) 0.24 3.15 0.29 3.20 0.29 3.20

Access to modern forms of energy(%) 0.23 59.69% 0.03 74.00% 0.03 74.00%

Diversity of supply (0-1) 0.83 0.69 0.83 0.69 0.79 0.67

Step 1: Assessing Current Energy Architecture Performance

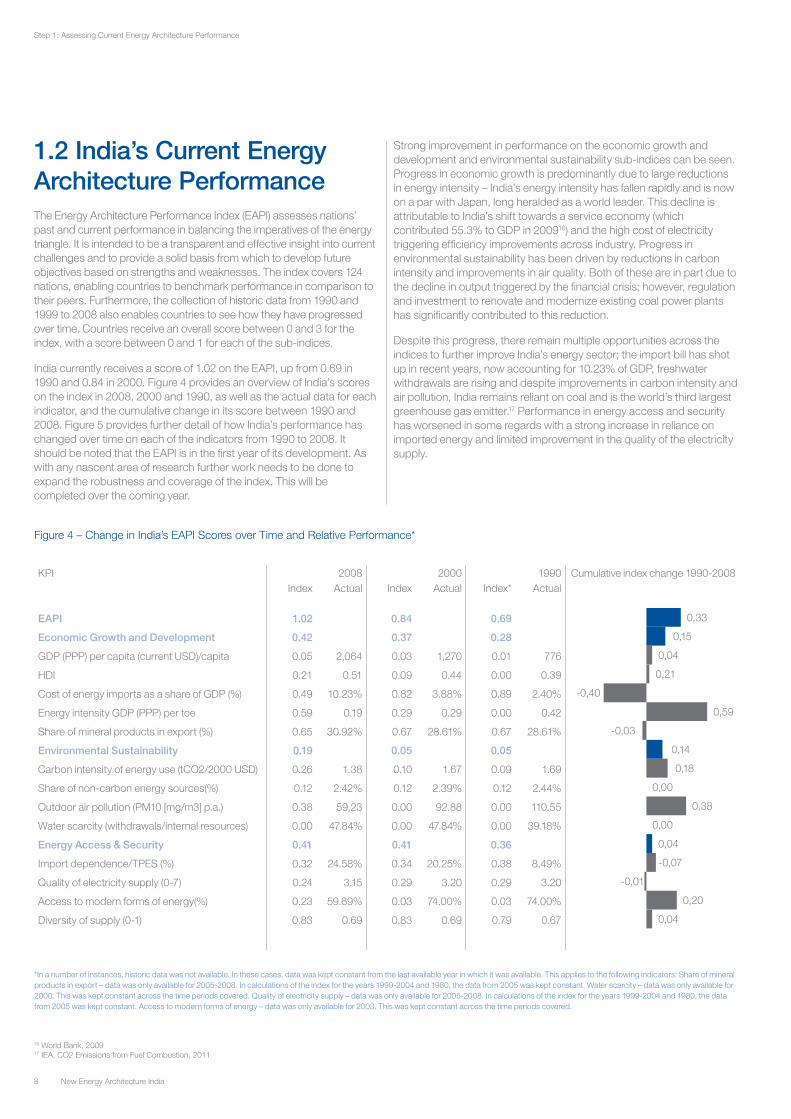

The Energy Architecture Performance Index (EAPI) assesses nations’ past and current performance in balancing the imperatives of the energy triangle. It is intended to be a transparent and effective insight into current challenges and to provide a solid basis from which to develop future objectives based on strengths and weaknesses. The index covers 124 nations, enabling countries to benchmark performance in comparison to their peers. Furthermore, the collection of historic data from 1990 and 1999 to 2008 also enables countries to see how they have progressed over time. Countries receive an overall score between 0 and 3 for the index, with a score between 0 and 1 for each of the sub-indices.

India currently receives a score of 1.02 on the EAPI, up from 0.69 in 1990 and 0.84 in 2000. Figure 4 provides an overview of India’s scores on the index in 2008, 2000 and 1990, as well as the actual data for each indicator, and the cumulative change in its score between 1990 and 2008. Figure 5 provides further detail of how India’s performance has changed over time on each of the indicators from 1990 to 2008. It should be noted that the EAPI is in the first year of its development. As with any nascent area of research further work needs to be done to expand the robustness and coverage of the index. This will be completed over the coming year.

Strong improvement in performance on the economic growth and development and environmental sustainability sub-indices can be seen. Progress in economic growth is predominantly due to large reductions in energy intensity – India’s energy intensity has fallen rapidly and is now on a par with Japan, long heralded as a world leader. This decline is attributable to India’s shift towards a service economy (which contributed 55.3% to GDP in 200916) and the high cost of electricity triggering efficiency improvements across industry. Progress in environmental sustainability has been driven by reductions in carbon intensity and improvements in air quality. Both of these are in part due to the decline in output triggered by the financial crisis; however, regulation and investment to renovate and modernize existing coal power plants has significantly contributed to this reduction.

Despite this progress, there remain multiple opportunities across the indices to further improve India’s energy sector; the import bill has shot up in recent years, now accounting for 10.23% of GDP, freshwater withdrawals are rising and despite improvements in carbon intensity and air pollution, India remains reliant on coal and is the world’s third largest greenhouse gas emitter.17 Performance in energy access and security has worsened in some regards with a strong increase in reliance on imported energy and limited improvement in the quality of the electricity supply.

1.2 India’s Current Energy Architecture Performance

Figure 4 – Change in India’s EAPI Scores over Time and Relative Performance*

*In a number of instances, historic data was not available. In these cases, data was kept constant from the last available year in which it was available. This applies to the following indicators: Share of mineral products in export – data was only available for 2005-2008. In calculations of the index for the years 1999-2004 and 1980, the data from 2005 was kept constant. Water scarcity – data was only available for 2000. This was kept constant across the time periods covered. Quality of electricity supply – data was only available for 2005-2008. In calculations of the index for the years 1999-2004 and 1980, the data from 2005 was kept constant. Access to modern forms of energy – data was only available for 2003. This was kept constant across the time periods covered.

0,33

0,15

0,04

0,21

0,59

0,38

0,14

0,00

0,04

0,18

0,00

-0,07

0,20

0,04

-0,01

-0,40

-0,03

16 World Bank, 200917 IEA, CO2 Emissions from Fuel Combustion, 2011

9New Energy Architecture India

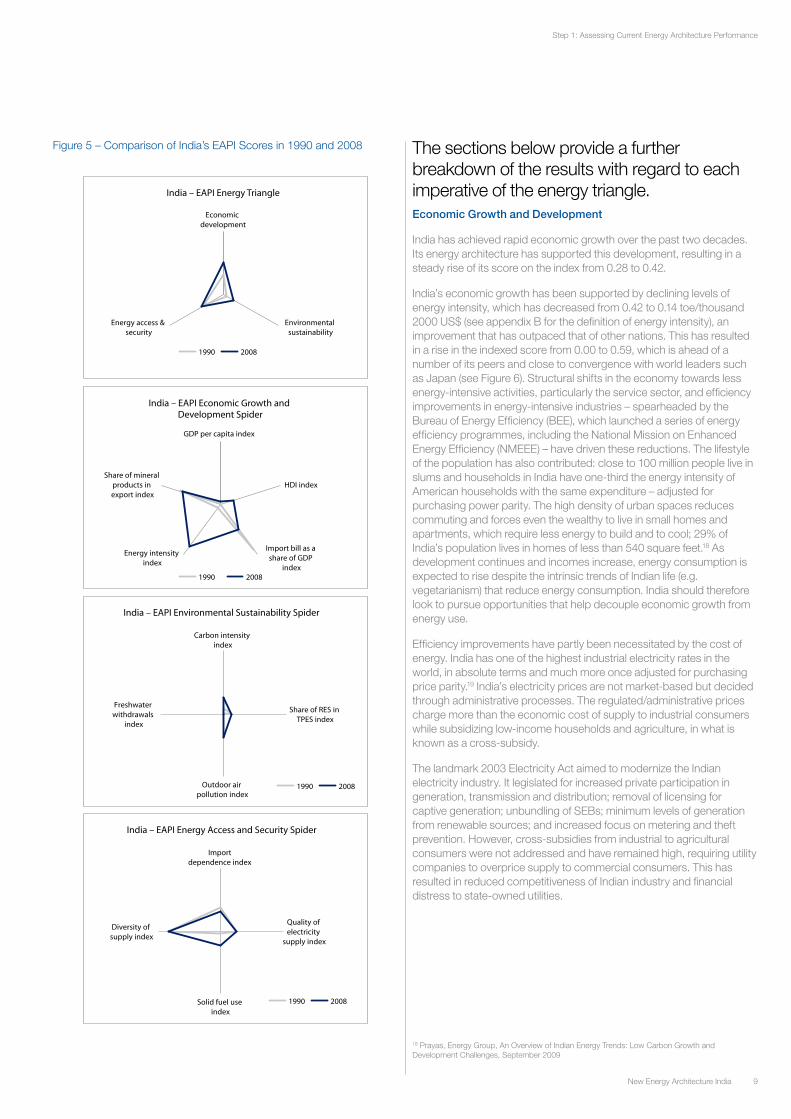

The sections below provide a further breakdown of the results with regard to each imperative of the energy triangle.Economic Growth and Development

India has achieved rapid economic growth over the past two decades. Its energy architecture has supported this development, resulting in a steady rise of its score on the index from 0.28 to 0.42.

India’s economic growth has been supported by declining levels of energy intensity, which has decreased from 0.42 to 0.14 toe/thousand 2000 US$ (see appendix B for the definition of energy intensity), an improvement that has outpaced that of other nations. This has resulted in a rise in the indexed score from 0.00 to 0.59, which is ahead of a number of its peers and close to convergence with world leaders such as Japan (see Figure 6). Structural shifts in the economy towards less energy-intensive activities, particularly the service sector, and efficiency improvements in energy-intensive industries – spearheaded by the Bureau of Energy Efficiency (BEE), which launched a series of energy efficiency programmes, including the National Mission on Enhanced Energy Efficiency (NMEEE) – have driven these reductions. The lifestyle of the population has also contributed: close to 100 million people live in slums and households in India have one-third the energy intensity of American households with the same expenditure – adjusted for purchasing power parity. The high density of urban spaces reduces commuting and forces even the wealthy to live in small homes and apartments, which require less energy to build and to cool; 29% of India’s population lives in homes of less than 540 square feet.18 As development continues and incomes increase, energy consumption is expected to rise despite the intrinsic trends of Indian life (e.g. vegetarianism) that reduce energy consumption. India should therefore look to pursue opportunities that help decouple economic growth from energy use.

Efficiency improvements have partly been necessitated by the cost of energy. India has one of the highest industrial electricity rates in the world, in absolute terms and much more once adjusted for purchasing price parity.19 India’s electricity prices are not market-based but decided through administrative processes. The regulated/administrative prices charge more than the economic cost of supply to industrial consumers while subsidizing low-income households and agriculture, in what is known as a cross-subsidy.

The landmark 2003 Electricity Act aimed to modernize the Indian electricity industry. It legislated for increased private participation in generation, transmission and distribution; removal of licensing for captive generation; unbundling of SEBs; minimum levels of generation from renewable sources; and increased focus on metering and theft prevention. However, cross-subsidies from industrial to agricultural consumers were not addressed and have remained high, requiring utility companies to overprice supply to commercial consumers. This has resulted in reduced competitiveness of Indian industry and financial distress to state-owned utilities.

Figure 5 – Comparison of India’s EAPI Scores in 1990 and 2008

18 Prayas, Energy Group, An Overview of Indian Energy Trends: Low Carbon Growth and Development Challenges, September 2009

Step 1: Assessing Current Energy Architecture Performance

Economic development

Environmental sustainability

Energy access & security

India – EAPI Energy Triangle

1990 2008

GDP per capita index

HDI index

Import bill as a share of GDP

index

Energy intensity index

Share of mineral products in export index

India – EAPI Economic Growth and Development Spider

1990 2008

Carbon intensity index

Share of RES in TPES index

Outdoor air pollution index

Freshwater withdrawals

index

India – EAPI Environmental Sustainability Spider

1990 2008

Import dependence index

Quality of electricity

supply index

Solid fuel use index

Diversity of supply index

India – EAPI Energy Access and Security Spider

1990 2008

10 New Energy Architecture India

Reluctance on the part of some state governments to reduce electricity theft has exacerbated these challenges. Electricity theft has in the past resulted in annual losses amounting to US$ 4.5 billion, roughly 1.5% of GDP.20 The situation has not improved. It is estimated that one-third of generated electricity in 2010 was lost in transmission and distribution at a total cost of US$ 16 billion, the majority through theft.21 The minor repercussions, low likelihood of being caught, ease of colluding with energy company staff and, on a macro scale, the vested political interest in keeping costs down mean that electricity theft is regarded as routine. In some cases, theft is encouraged by a lack of alternative supply options, as opposed to an unwillingness to pay on the part of consumers. Electricity in slums is regularly supplied by an illegal utility company – a connection to the grid is made by simply slinging a wire over the transmission cable and the output sold to slum dwellers, often at above market rates.22

The domestic price of oil-based products remains heavily subsidized. About 60% of the subsidies are spent on holding down the price of diesel and about half of the remainder comes from the long-standing subsidy on kerosene. Gasoline was deregulated in 2010 following the recommendations of the expert group on a viable and sustainable system of pricing of petroleum products led by Kirit Parikh.23 However, this has come with “Indian characteristics”, since the government continues to advise oil companies on the price to set.

Oil subsidies have had serious consequences for domestic upstream and oil marketing companies who have become victims of under recovery and are now reliant on government oil bonds for liquidity. India’s oil product subsidies, calculated on the basis of differences between domestic prices and world prices, surged to around US$ 41billion in 2008, or US$ 36 per capita and 3.4% of GDP, as global oil prices rose.24 Given India’s size, both in terms of population and energy consumption, the absolute value of India’s energy subsidies were the highest among net energy importing economies in 2009. This reflects the growing burden of India’s mineral imports: India’s import bill now accounts for 10.23% of GDP, up from 2.40% in 1990, resulting in a decline in index scores from 0.89 to 0.49.

The central government also subsidizes natural gas via a complex system of differential prices that vary across end users and regions. About 60% of natural gas is sold in an administered pricing mechanism under which the government sets the price for gas produced by the state-owned oil companies. The prices of gas produced from joint venture fields licensed before the New Exploration Licensing Policy (NELP) came into effect in 1997 are determined by production sharing contracts entered into with the government. For gas derived from fields awarded under the NELP, prices are typically set on the basis of a formula linking them to the price of crude oil. The price of natural gas imported as LNG is set on commercial terms.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

toe/

tho

usan

d 2

000U

S$

EA

PI S

core

India – Energy intensity(toe/thousand US$)

India – PM10 level

India – Share of imports in TPES

EAPI China

China

EAPI Scores

EAPI scores

Japan

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

PM

10 [m

g/m

3] p

.a.

EA

PI S

core

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Net

imp

ort

s/T

PE

S (%

)

EA

PI S

core

Figure 6 – Energy Intensity

19 Nagayama, Effects of regulatory reforms in the electricity supply industry on electricity prices in developing countries, Energy policy 200720 World Bank, Reforming the power sector: Controlling electricity theft and improving revenue, September 200421 Power Secretary P. Uma Shankar, Bloomberg Businessweek, Can India’s Power Thieves Be Stopped?, 201122 Clean Distributed Generation for Slum Electrification: The Case of Mumbai, David Schaengold, Woodrow Wilson School Task Force on Energy for Sustainable Development, 200623 Government of India, Report of the expert group on a viable and sustainable system of pricing of petroleum products, 2 February 201024 OECD Economic Surveys: India 2011

Step 1: Assessing Current Energy Architecture Performance

11New Energy Architecture India

Environmental Sustainability

Despite continuing reliance on coal, India has improved the environmental sustainability of its energy architecture. India’s score on the environmental sustainability index has risen from 0.05 in 1990 to 0.19 in 2008. Key drivers include the growth of renewable energy in power generation and reductions in air pollution. India’s per capita emissions (1.25 tons) are also well below the global average.

Progress should not be overstated. India is the fourth largest emitter of global greenhouse gas emissions after China, the US and Russia. Furthermore, recent improvements in carbon intensity can be partially attributed to the affect of the economic downturn. Between 2007 and 2009, the annual growth rate for electricity demand fell from 7.1% to 0.9%, which can be largely attributed to a downturn in industrial output during the global economic crisis.25 Much more can be done to combat carbon emissions: a government report suggests that with a reasonable package of measures, India’s carbon intensity can be reduced by 23 to 25% from its 2005 level.26

Spearheaded by a dedicated Ministry for New and Renewable Energy, renewables have become an integral part of the government’s energy strategy. Since 2000, capacity additions from renewables (excluding large hydro) have comprised nearly one-quarter of total additions in the Indian power sector, and almost half with large hydro.27 However, the share of non-carbon sources in total primary energy supplies as a whole has remained marginal, with gains in the share of renewables in the electricity sector offset by a growing demand for petroleum products in the transportation sector. This has meant that India’s score on this indicator has remained stagnant.

Renovation, modernization and life extension programmes have led to the reduction of air pollution from thermal coal-fired plants. This has resulted in a decrease in air pollution from 110.55 to 59.20 PM10 (mg/m3 per annum), and a concurrent uptick in index performance from 0 to 0.38. Despite this, the overall pollution level remains relatively high due to a rapid increase in the vehicle population and continued use of coal for industrial and energy purposes. According to the Central Pollution Control Board, in 2007 47% of the ambient air pollution monitoring stations reported the level of solid particulate matters exceeding the National Ambient Air Quality Standards by a factor of 1.5.28

Growing water scarcity is being recognized as an important problem facing India. Freshwater withdrawals have increased from 39.18% to 47.84%, giving it a score of 0 on this index, indicating that urgent action is needed. Water use is directly linked to energy supply, availability and price. Water pumping for agriculture accounts for 25-30% of electrical energy consumption in India.29 Low power-tariffs and unmetered supply of power, especially at unregulated times and frequency, lead to wastage of water. The use of water by thermal power plants has shown to be eight times higher per kWh in India than in the world’s most efficient plants.30

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

toe/

tho

usan

d 2

000U

S$

EA

PI S

core

India – Energy intensity(toe/thousand US$)

India – PM10 level

India – Share of imports in TPES

EAPI China

China

EAPI Scores

EAPI scores

Japan

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

PM

10 [m

g/m

3] p

.a.

EA

PI S

core

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Net

imp

ort

s/T

PE

S (%

)

EA

PI S

core

Figure 7 – Outdoor Air Pollution

25 The Impact of the Financial and Economic Crisis on Global Energy Investment, IEA Background paper for the G8 Energy Ministers’ Meeting 24-25 May 200926 Planning Commission, Government of India, Low Carbon Strategies for Inclusive Growth: An Interim Report, May 201127 Prayas, Energy Group, An Overview of Indian Energy Trends: Low Carbon Growth and Development Challenges, September 200928 Central Pollution Control Board, 2007; Annual Report for 2006-2007, New Delhi29 Confederation of Indian Industry, Building a Low-Carbon Economy, 200830 CSE India, Water Use in India, Chandra Bhushan

Step 1: Assessing Current Energy Architecture Performance

12 New Energy Architecture India

Energy Access and Security

The Indian economy faces significant challenges in terms of meeting its energy needs in the coming decade. Although India has extensive steam-coal reserves, its known reserves of oil and gas are limited. Increasing energy requirements, coupled with a slower than expected increase in domestic crude oil and natural gas production, have meant that the share of imports in the energy mix is growing rapidly. Import dependence has risen from 8.49% to 24.58% of GDP. The import component of domestic oil consumption is about 76% (after adjusting for the export of refined petroleum products) and in the case of natural gas, it is about 19%. This has been tempered by India’s diversity of supply and the promotion of alternative fuel sources, and an aggressive policy of exploring its basins for hydrocarbons through its New Exploration and Licensing Policy (NELP). Since the inception of NELP, there have been more than 100 hydrocarbon discoveries, most of them being natural gas, totalling over 30 trillion cubic feet.11

India’s power generation capacity has struggled to keep pace with rapid economic and population growth and urbanization. Despite 50GW of total power generating capacity added over the past five years, peak demand deficits are expected to remain worryingly high during 2011-2012, ranging from 5.9% in the north-eastern region to 14.5% in the southern region.31 In individual states, such as Goa, Daman and Diu, these deficits run at over 40%. Transmission and distribution is also inadequate. Distribution faces substantial technical losses (because of overloading of transformers and conductors, for instance) and, as previously mentioned, commercial losses of electricity (because of low metering efficiency, poor billing and collection and large-scale theft of power).

These losses are among the highest in the world, comparable with some countries in sub-Saharan Africa. According to the World Economic Forum’s Global Competitiveness Index, the quality of electricity supply has actually worsened in recent years, declining from a score of 3.20 in 2005 to 3.15 in 2008. Peak demand deficit surged in 2007-2008 and, despite falling rapidly in 2008-2009, has started rising again. Power shortages are an aspect of everyday life and are having an increasingly negative effect on industrial output and impeding GDP growth; a 2009 study estimated that the downtime cost just to service sector companies was US$ 9.4 billion, an increase of almost 100% from 2003.32

With the biggest rural population in the world, India faces a huge electrification challenge. According to the International Energy Agency (IEA), 25% of the population (289 million) does not currently have access to electricity, while 72% of the population (836 million) relies on the traditional use of biomass for cooking.33 Low energy availability and consumption is reflected in the relatively low Human Development Index (HDI) of India.

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

toe/

tho

usan

d 2

000U

S$

EA

PI S

core

India – Energy intensity(toe/thousand US$)

India – PM10 level

India – Share of imports in TPES

EAPI China

China

EAPI Scores

EAPI scores

Japan

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

PM

10 [m

g/m

3] p

.a.

EA

PI S

core

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Net

imp

ort

s/T

PE

S (%

)

EA

PI S

core

Figure 8 – Import Dependence

31 Central Electricity Authority, Load Generation Balance Report, 2011-201232 MAIT & Emerson Network Power Study, May 200933 IEA, Energy for all: Financing access for the poor, Special early excerpt of the World Energy Outlook 2011

Step 1: Assessing Current Energy Architecture Performance

13New Energy Architecture India

1.3 Comparing India’s Current Energy Architecture Performance with the Grow Archetype

The results of the Energy Architecture Performance Index (EAPI) must be read in context, paying particular heed to the structure of India’s economy. Contextual differences mean that energy architectures will look very different in different countries, affecting performance on the index. For example, India’s large rural population makes issues around the distribution of energy a particular challenge.

To account for such differences, studies on energy transitions often take a regional perspective. However, there is considerable heterogeneity among countries within single regions. In recognition of this, the EAPI has been used to create a series of archetypes, grouping countries that face similar challenges in their current energy architecture, and who therefore have a similar objective for the transition to a New Energy Architecture. This process has resulted in the identification of four archetypes: Rationalize, Capitalize, Grow and Access.

India falls within the Grow archetype. Countries within this archetype have energy architectures that are focused on securing continued and rapid economic growth. Their focus is on alleviating supply bottlenecks, to reduce supply-demand deficits. Key opportunities for these countries lie in bringing new forms of supply online and delivering it more effectively to consumers and doing so at a market-based price. It consists principally of countries that are going through a rapid growth phase, such as those in East Asia and Central and Eastern Europe. They feature growing urban populations, but many also have large rural hinterlands. Due to the growing strain of economic growth, physical infrastructure often falls short of national needs, despite increasing investment. Many of these countries experience peak supply deficits and regular black-outs. The challenge for these countries is to increase reliability, ensure that power supplies keep up with economic growth, and avoid shortfalls that constrain growth.

Figure 9 reports the scores and actual data for India and a select group of Grow nations. Figure 10 is a heat map that complements the raw scores, allowing for a reading of India’s performance in the EAPI in relative terms. It provides a sense of the distance in scores that separates India from other members of the Grow archetype. Blue-shaded cells and grey-shaded cells indicate that India scores or ranks respectively higher or lower than the comparator, while no shading means that there is no significant divergence. The darker the shading, the greater the difference in performance.

The heat map mirrors India’s atypical performance pattern described above. Relative weak points include human development, water scarcity and the proportion of the population using solid fuels, underlining that India faces significant challenges in relation to energy access in comparison to its peers. Relative strengths include energy intensity and diversity of supply. The figure shows that India is outperformed by its peers across the three imperatives of the energy triangle – China is stronger on 10 out of the 17 indicators. This underlines the significant opportunities for improving India’s energy system.

Figure 9 – EAPI Results for India and Selected Comparators from the Grow Archetype

Economic Growth and Development GDP per capita HDI index Import bill as a

share of GDP Energy intensity Share of mineral products in export

Country KPI Raw KPI Raw KPI Raw KPI Raw KPI Raw

Chile 0.30 11277 0.71 0.78 0.57 0.09 0.78 0.14 0.74 23.24

Hungary 0.44 16217 0.76 0.80 0.29 0.14 0.77 0.14 0.96 3.81

India 0.05 2036.9 0.21 0.51 0.49 0.10 0.59 0.19 0.65 30.92

Indonesia 0.08 2983 0.36 0.59 0.62 0.08 0.46 0.24 0.62 33.46

Korea, Rep. 0.59 21630 0.39 0.12 0.64 0.18 0.90 9.45

Mexico 0.31 11646 0.65 0.75 0.90 0.02 0.84 0.12 0.79 18.46

China 0.09 3598.6 0.47 0.65 0.78 0.05 0.29 0.29 0.97 2.66

South Africa 0.21 7992.8 0.36 0.59 0.64 0.07 0.32 0.28 0.72 24.83

Thailand 0.17 6309.3 0.46 0.65 0.30 0.14 0.56 0.21 0.91 7.91

Turkey 0.26 9802 0.52 0.67 0.63 0.08 0.89 0.10 0.92 7.44

Vietnam 0.05 1937.2 0.38 0.13 0.36 0.27 0.77 20.72

Step 1: Assessing Current Energy Architecture Performance

14 New Energy Architecture India

*This heat map allows for a reading of India’s performance in the EAPI in relative terms. It provides a sense of the distance in scores that separates India from other members of the Grow archetype. Blue-shaded cells and grey-shaded cells indicate that India scores or ranks respectively higher or lower than the comparator, while no shading means that there is no significant divergence. The darker the shading, the greater the difference in performance.

Figure 10 – Heat Map Indicating Differences between India and Selected Archetype Comparators*

Environmental Sustainability Carbon intensity Share of non-carbon energy Outdoor air pollution Freshwater

withdrawals

Country KPI Raw KPI Raw KPI Raw KPI Raw

Chile 0.78 0.49 0.34 6.63 0.35 61.55 0.97 1.28

Hungary 0.79 0.48 0.77 15.16 0.90 15.60

India 0.26 1.38 0.12 2.42 0.38 59.23 0.00 47.84

Indonesia 0.37 1.19 0.39 7.68 0.22 72.35 0.87 5.61

Korea, Rep. 0.75 0.55 0.89 17.49 0.72 30.76

Mexico 0.78 0.48 0.34 6.73 0.70 32.69

China 0.00 2.14 0.18 3.53 0.30 65.61

South Africa 0.08 1.70 0.13 2.64 0.82 22.13 0.34 27.86

Thailand 0.32 1.28 0.03 0.57 0.42 55.31

Turkey 0.77 0.50 0.23 4.57 0.64 37.06 0.56 18.50

Vietnam 0.16 1.57 0.19 3.76 0.46 52.71

Energy Access and Security Import dependence Quality of electricity supply Solid fuel use Diversity of supply

Country KPI Raw KPI Raw KPI Raw KPI Raw

Chile 0.12 71.34 0.68 5.33 1.00 5.00 0.70 0.61

Hungary 0.17 60.33 0.68 5.29 1.00 5.00 0.88 0.73

India 0.32 24.58 0.24 3.15 0.23 59.69 0.83 0.69

Indonesia 0.73 -74.65 0.39 3.86 0.25 58.36 0.95 0.77

Korea, Rep. 0.08 80.29 0.85 6.15 1.00 5.00 0.87 0.72

Mexico 0.54 -29.34 0.42 4.03 0.86 15.00 0.66 0.59

China 0.40 5.82 0.56 4.72 0.40 48.00 0.54 0.52

South Africa 0.51 -21.16 0.29 3.36 0.83 17.27 0.46 0.47

Thailand 0.25 40.41 0.71 5.48 0.72 25.00 0.87 0.72

Turkey 0.12 70.58 0.45 4.15 0.88 0.72

Vietnam 0.50 -20.14 0.26 3.22 0.22 61.00 0.86 0.71

Country

India 0.42 0.05 0.20 0.49 0.59 0.65 0.19 0.26 0.12 0.38 0.00 0.41 0.32 0.24 0.23 0.83

Chile -0.22 -0.25 -0.50 -0.08 -0.18 -0.09 -0.42 -0.52 -0.21 0.03 -0.97 -0.22 0.20 -0.44 -0.77 0.13

Hungary -0.24 -0.39 -0.55 0.21 -0.18 -0.31 -0.63 -0.52 -0.64 -0.52 -0.28 0.15 -0.43 -0.77 -0.05

Indonesia -0.01 -0.03 -0.15 -0.13 0.14 0.03 -0.27 -0.11 -0.27 0.16 -0.87 -0.17 -0.42 -0.14 -0.02 -0.12

Korea, Rep. -0.21 -0.54 0.10 -0.05 -0.25 -0.59 -0.48 -0.76 -0.34 -0.29 0.23 -0.61 -0.77 -0.04

Mexico -0.29 -0.26 -0.44 -0.41 -0.25 -0.14 -0.42 -0.52 -0.22 -0.32 -0.22 -0.23 -0.18 -0.63 0.17

China -0.07 -0.04 -0.26 -0.29 0.31 -0.33 0.03 0.26 -0.06 0.08 -0.07 -0.08 -0.32 -0.16 0.29

South Africa -0.01 -0.16 -0.16 -0.15 0.28 -0.07 -0.15 0.18 -0.01 -0.44 -0.34 -0.11 -0.19 -0.04 -0.59 0.38

Thailand -0.07 -0.12 -0.26 0.19 0.04 -0.27 -0.07 -0.06 0.09 -0.05 -0.23 0.07 -0.47 -0.49 -0.04

Turkey -0.25 -0.21 -0.31 -0.14 -0.30 -0.27 -0.36 -0.51 -0.11 -0.27 -0.56 -0.08 0.19 -0.20 -0.05

Vietnam 0.04 0.00 0.12 0.24 -0.12 -0.08 0.11 -0.07 -0.08 -0.05 -0.19 -0.01 0.02 -0.03

Eco

nom

ic g

row

th

& d

evel

op

men

t

Impo

rt b

ill as

a

shar

e of

GD

P

Ene

rgy

inte

nsity

Sha

re o

f min

eral

pr

oduc

ts in

exp

ort

Env

ironm

enta

l su

stai

nab

ility

Car

bon

inte

nsity

Sha

re o

f non

-ca

rbon

ene

rgy

Out

door

air

pollu

tion

Ene

rgy

acce

ss &

se

curi

ty

Impo

rt d

epen

denc

e

Sol

id fu

el u

se

Qua

lity

of e

lect

ricity

su

pply

Fres

hwat

er

with

draw

als

GD

P p

er c

apita

HD

I

Score Difference -0.7 -0.4 -0.1 0.1 0.4 0.7

Div

ersi

ty o

f sup

ply

Step 1: Assessing Current Energy Architecture Performance

15New Energy Architecture India

Summary: Key Challenges for India’s Current Energy Architecture• Distorted energy prices: While some progress has been made in

liberalizing India’s energy sector, industrial energy costs are among the highest in the world, leading to a lack of competitiveness within certain sectors. Meanwhile, residential and agricultural electricity, diesel, kerosene and LPG prices are heavily subsidized, placing a burden on public finances and leading to inefficiencies in use and little motivation for private companies to invest in the industry.

• Air quality: Despite significant improvements, the overall pollution levels remain high due to rapid and sustained increases in vehicle ownership and continued inefficient combustion of low-quality coal.

• Water scarcity: Freshwater withdrawals have increased from 39.18% to 47.84% as energy, agricultural and industrial output rises, a trend that is forecast to continue. Urgent action is required to ensure the continued availability of fresh water to consumers.

• Growing import dependence: Stagnant efficiencies, increasing energy requirements, and a slower than expected increases in domestic fuel production have meant that import dependence has risen from 8.49% to 24.58%.

• Unreliable grid: India has some of the highest transmission and distribution losses in the world. The quality of electricity supply has worsened over recent years with power shortages being routine, continued voltage fluctuations and inability to meet peak demand.

• Energy poverty: 72% of the population continues to rely on biomass-based fuels for cooking, and 289 million people lack access to electricity, giving India a sub-par performance with regard to energy access in comparison to its peers.

Step 1: Assessing Current Energy Architecture Performance

16 New Energy Architecture India

Step 2: Creating New Energy Architecture Objectives

17New Energy Architecture India

Step 2: Creating New Energy Architecture Objectives

A consideration of India’s performance on the EAPI helps highlight the challenges that its energy architecture faces. It helps provide a foundation for identifying a set of objectives for the creation of a New Energy Architecture in India that is more responsive to the imperatives of the energy triangle.35 These objectives were further shaped and tested during a series of interviews with a range of representatives from across the energy value chain, as well as through a multistakeholder workshop conducted during the India Economic Summit. The objectives below therefore represent the participants’ suggestions of the issues that India should focus on.

In shaping these objectives, the existing government targets have been taken into account. India has a core objective of achieving sustainable and inclusive growth and has provisionally set a 9% GDP growth target as part of the 12th Five Year Plan (2012-2017), which will require energy supply to grow at 6.5% per annum.36 This represents a significantly increased growth target for the sector than in the past. The focus for the coming years will therefore be on supporting economic growth by providing a secure supply of energy. Indeed, “inability to meet energy demand could be the single biggest constraining factor to India’s growth story.”37 This will require India to bring new forms of supply online, deliver it more effectively to consumers (both urban and rural), and do so at a market-based price (based upon the eventual eradication of subsidies) that sends appropriate signals to both the demand and supply sides.

India has a responsibility to achieve its growth trajectory in an environmentally sustainable manner, and has set a voluntary target to cut the emissions intensity of GDP by 20-25% by 2020 compared with 2005 levels.38 Therefore, the way forward should be to identify common ground between climate change policy and economic growth and pursue measures that achieve both. Considering that there needs to be a significant expansion in energy infrastructure, India has an opportunity to pursue development while managing emissions growth, enhancing its energy security and creating world-scale clean technology industries. India should therefore not look to copy the Western model of energy infrastructure development, and instead pursue a development path that is particular to its local conditions. This would require that India leapfrog inefficient technologies, assets and practices and deploy ones that are more efficient and less emission intensive, with a key opportunity being the expansion of decentralized distribution and generation.

The following set of objectives are therefore focused on supporting improvement with regard to economic growth and development and energy access and security, but have been tailored to provide co-benefits with regard to environmental sustainability. They are intended to indicate what India’s focus should be in the near to medium term.

2.1 Defining India’s Objectives for a New Energy Architecture

34 Tulsi R. Tanti, Wind matters: Making the case for wind in India, Suzlon, 201135 These transition objectives are intended to indicate the focus that India will have over the course of the next 15-20 years, and are not intended to be exhaustive.36 Government of India, Planning Commission, Faster, Sustainable and More Inclusive Growth: An approach to the 12th Five Year Plan, August 201137 Interview participant, New Delhi, October 201138 Natural Resources Defense Council, From Copenhagen Accord to Climate Action: Tracking National Commitments to Curb Global Warming, http://www.nrdc.org/international/copenhagenaccords/

18 New Energy Architecture India

While [India’s] economic growth has touched millions, without energy security it

cannot be truly sustainable.

Tulsi R. TantiCEO, Suzlon34

Step 2: Creating New Energy Architecture Objectives

New Energy Architecture India18

19New Energy Architecture India

Objective 1 – Augment resources for energy security

India’s principal challenge relates to its supply-demand deficit. Three main actions will enable India to reduce this deficit: more efficient exploitation of indigenous hydrocarbon reserves; the adoption of alternative sources of supply; and, increased energy efficiency across the energy value chain.

India has introduced a number of measures to tackle these issues: oil and gas reserves have been opened up for exploration and production by private and foreign firms under the New Exploration License Policy (NELP), which soon will be replaced with the Open Acreage Licensing Policy (OALP); targets and incentives for renewable energy have been laid out in the Prime Minister’s National Action Plan on Climate Change, which targets a 15% renewable contribution to the electricity generation mix by 2020; the Jawaharlal Nehru National Solar Mission targets the deployment of 20GW of solar power by 2022; and, the National Policy on Biofuels proposes a target of 20% blending of biofuel by 2017.39 Increases in energy efficiency are being targeted by the National Mission on Enhanced Energy Efficiency. These targets need to be further bolstered if India is to reduce its supply bottlenecks.

Objective 2 – Provide access to modern forms of energy for all

Energy poverty continues to blight a significant portion of the population, with fossil fuels currently costing a disproportionate portion of what is for many very modest incomes. Providing energy access for all is therefore a key objective if India is to deliver on its target of 9-9.5% GDP growth in 2012-2017 while achieving the Millennium Development Goals – a set of development targets to be reached by 2015, including reducing the population under the poverty line to below 20%.40 When talking of the transition from traditional to more modern forms of energy in rural communities, “traditional” and “modern” refer to both the type of fuel and the technologies used.

Objective 3 – Strengthening energy carriers41

India may be the world’s second fastest growing economy, but its physical infrastructure continues to fall far short of national needs. Historically, India’s infrastructure investment has averaged about 4% of GDP – half the country’s more than 8% growth rate and half the GDP percentage that China devotes to infrastructure.42 Infrastructure is so poor in some instances that companies are forced to build their own. Infosys, for example, generates much of its own electricity.43

The power supply position prevailing in India is a particular challenge, and is characterized by persistent shortages and unreliability, as utilities struggle to transmit from load centres to demand centres. Additional generating capacity will do little to address India’s increasing demand for power, unless there is significant investment in upgrading transmission and distribution networks. The supporting infrastructure for the gas sector has similarly suffered from a lack of investment, and expansion will be required to enable growth in the sector. Gas pipelines are limited in length (less than 10,000 km) and confined to the north-west corner, supplying just 41 cities with city gas.44

Objective 4 – Rationalize energy prices

A major objective of energy policy is to have an efficient and competitive energy economy that promotes efficient use by consumers, appropriate choice of fuels among substitutes and a proper choice of technique. This is best ensured by a competitive energy sector. India’s energy sector is heavily subsidized. The resultant market perversions lead to a lack of competitiveness in the industrial sector and inefficiencies in use by the residential and agricultural sectors.

In the oil sector, continuing to phase out energy subsidies would facilitate private and joint venture investment and reduce the under recovery of upstream firms and oil marketing companies. A review of subsidies for petroleum products was completed by an expert group led by Kirit Parikh in 2010.45 While some of their recommendations have been pursued, further efforts should be made in this regard.

In electricity markets, the removal of cross-subsidies that reduce the revenues of the distribution utilities to below cost would remove a major barrier to private investment. These measures would improve allocative efficiency in the Indian economy and boost GDP. They would also relieve considerable fiscal pressure and allow revenues to be better directed towards achieving India’s development goals.

Rationalizing prices will accrue co-benefits for environmental sustainability and energy security, as they have a significant role to play in promoting energy efficiency and in ensuring expansion of domestic supply.

Balancing the Energy Triangle

The imperatives of the energy triangle may reinforce or act in tension with one another, and efforts to balance the three require difficult trade-offs to be made.

A particular challenge for India is balancing the needs to promote a more competitive industrial sector through rationalized energy prices, and the need to expand access to modern forms of energy for all. In recognition of this, challenging decisions with regard to the removal of energy subsidies must be carefully made. The solution will be ensuring that energy subsidies reach the appropriate target audience: citizens below or near the poverty line.

39 USDA, India Biofuels Annual, 201140 UNICEF, Millennium Development Goals Country Report: India 200541 Refers to both electricity transmission and distribution, and oil and gas pipeline infrastructure42 Accenture, Helping India on the journey to high performance: Three imperatives for policy-makers and business leaders, 200943 The Economist, The Bollygarchs44 IEA, Natural Gas in India, Anne-Sophie Corbeau, 201045 Government of India, New Delhi, Report of the expert group on a viable and sustainable system of pricing of petroleum products, 2 February 2010

Step 2: Creating New Energy Architecture Objectives

20 New Energy Architecture India

Step 3: Defining the Enabling Environment

21New Energy Architecture India

Step 3: Defining the Enabling Environment

Achieving India’s New Energy Architecture objectives is contingent on the creation of an appropriate enabling environment. The research conducted as part of the wider New Energy Architecture project has shown that enabling environments consist of four pillars:

1. Policy initiatives: Frameworks and incentives should be created to put in place the rules, price signals and risk-return incentives that attract investors and facilitate development. Regulations should be consistent, transparent and evidence-based, and include strict standards of governance. A strong policy platform will unlock the potential of business to do what it does best: profitably invest and innovate.

2. Technology and infrastructure: Technological innovations should be deployed to fix specific challenges in a country or stage of the value chain. Technology pilots should be performed in developing countries to take advantage of the lack of legacy technology and infrastructure, strong growth prospects and availability of resources. Government and industry must look to create and align standards to reduce production costs and facilitate integration.

3. Market structures: Market structures should be created to allow producers to meet consumers’ needs efficiently. This entails creating market links between players along the value chain, financing mechanisms to reduce risk and appropriate scales of supply and demand.

4. Human capacity: Human capacity should be developed to both drive change and develop solutions. To drive change will require increased citizen access to information (e.g. smart metering). To develop solutions will require increased focus on education, training and accreditation by professional bodies to overcome the scarcity of technical knowledge, ability and experience.

Spanning these four pillars is information. Making changes to energy architecture requires building support from all stakeholders in civil society, including the public at large. The establishment of communication channels between stakeholders is a necessary step towards promoting better understanding of the risks and benefits associated with energy architecture change. The provision of information is therefore central to driving a bottom-up acceptance of, and even pull for, change.

These four pillars must be deployed in a mutually supportive manner. For example, the successful deployment of large-scale renewables into energy architecture requires a portfolio of complementary flexible generation, strengthening and extending network infrastructure and interconnections, energy storage technologies, modified institutional arrangements including regulatory and market mechanisms, newly trained technicians to manage the system, and public acceptance.

Failure to integrate efforts across the four pillars will lead to an inadequate enabling environment that hinders the transition. For example, India’s Five Year Plans have historically placed emphasis on power generation expansion. However, this results in loading more and more power on an inadequate transmission and distribution network. Since transmission and distribution investments have not kept pace with investments in generation, power cannot be easily moved from surplus to deficit areas. Industrial and commercial establishments have been forced to seek captive and standby generation to meet demand or provide quality supply on a 24x7 basis to support critical processes and provide peaking support. There therefore needs to be a greater alignment between policy initiatives and infrastructure build-out.

In the following section, an overview is provided of the options that India should consider pursuing to create enabling environments that support its transition to a New Energy Architecture, applying the above framework. The options highlighted are based on interviews and a multistakeholder workshop conducted during the India Economic Summit.

3.1 Achieving India’s New Energy Architecture Objectives: Creating the Right Enabling Environment

Figure 11 – The Four Pillars of an Enabling Environment

22 New Energy Architecture India

3.2 Defining Enabling Environments for India’s New Energy Architecture

Objective 1 – Augment resources for energy security

1.1 Create a policy framework that more effectively supports the involvement of international partners in upstream projects

The New Exploration Licensing Policy (NELP) was formulated in 1997-1998 to boost hydrocarbon exploration in India, providing a level playing field where exploration licenses would be granted on a competitive basis, thereby encouraging the participation of foreign and private oil companies. NELP was first implemented in January 1999, with the Ninth Round launched in October 2010.

The international response to NELP has been mixed, and in recent rounds there has been limited participation by international oil companies. Unstable fiscal policies, particularly the exemption of natural gas from tax breaks46, lack of reliable and comprehensive geologic data, and the opaque structure of the tendering process have driven the poor response – in NELP IX (2011), only eight foreign companies out of a total of 37 participated in NELP IX and out of these only two foreign companies were new entrants to the sector.47

The Open Acreage Licensing Policy (OALP) is designed to replace and overcome some of the issues with NELP but is not expected before 2013. The poor availability and quality of geologic data will be addressed with the creation of a National Resource Database (NDR) to create a definitive view of India’s resources, and four major oilfield service companies have already submitted bids for the work. Companies will bid for blocks that they delineate based on data from the NDR48 and the role of Oil and Natural Gas Corporation (ONGC) in the process will be reduced.

Attracting international partners to the sector is of fundamental importance if India’s oil companies are to build the capacities to exploit indigenous assets, particularly as conventional resources are exhausted and interest turns to more challenging resources (e.g. shale gas). Although Reliance Industries has been able to pursue such a strategy through BP’s acquisition of a stake in 23 exploration blocks, others have been unable to mimic this. Policy must continue to be developed to entice foreign companies to enter India and to govern exploration of non-conventional resources.

1.2 Expand and modernize the coal mining industry to enable foreign participation and full exploitation of indigenous resources

Over the next 20 years, coal will continue to play an important role in India’s energy architecture. Under its New Policies Scenario, the International Energy Agency estimates that India will double its coal use by 2035, displacing the US as the world’s second-largest coal consumer.49 Given the continuing role of coal in the energy mix, it is important that India take steps to ensure that domestic resources are able to meet growing demand, and do so in an environmentally sustainable way.

Coal production has increased dramatically since nationalization and has grown at 4% CAGR over the past decade. However, it has been outstripped by growth in the power industry (which accounts for 80% of consumption) leaving India increasingly reliant on imported coal.50 Coal resources are known to be extensive with a potential resource base of 248GT and proven reserves of 93GT. However, systematic exploration has been based on the coal industry’s perceptions of extraction, leaving extractable proven reserves of only 52GT.50 With increasing numbers of modern coal-fired power plants being built, it is conceivable that they may outlast domestic coal reserves. Without a clear picture of it coal position, India may commit to building power plants now that will affect its long-term dependence on imported coal. It must embark on renewed coal exploration to obtain a conclusive estimate of reserves, which can then be used to inform generation policy and capacity planning.

Shortcomings in exploration can be attributed in some part to the propensity for open cast mining, which has been favoured due to its low cost, quick access and high recovery rate. It accounts for over 80% of production, with 62% of explored areas showing coal at a depth of less than 300 m.50 The focus on open cast mining has led to chronic underinvestment in underground mining, which now lacks modern technology and mechanization.51 This lack of investment means that India is not capable of exploiting its considerable reserves of underground coal. As shallow coal becomes scarcer, this lack of capability may well impede continued growth in coal production.