Argent Classic Convertible Arbitrage Fund L.P., et al. v...

20

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 1 of 20 1 2 3 4 5 6 7 8 UNITED STATES DISTRICT COURT 9 CENTRAL DISTRICT OF CALIFORNIA 10 11 ARGENT CLASSIC CONVERTIBLE Case No. CV 07-07097 MRP (MANx) 12 ARBITRAGE FUND L.P., individually and on behalf of all others ORDER Denying Class Certification 13 similarly situated, 14 15 Plaintiff, V. 16 17 COUNTRYWIDE FINANCIAL 18 CORPORATION, el al., 19 Defendants. 20 INTRODUCTION 21 This is a securities action against Countrywide Financial and several other 22 persons and entities (collectively, "Defendants"). For purposes of this order, no 23 distinction among Defendants is necessary. 24 Plaintiff Argent Classic Convertible Arbitrage Fund L.P. ("Argent") brings 25 this action on behalf of those who purchased certain Countrywide convertible 26 debentures ("the Debentures") offered in a private placement under SEC Rule 27 28 -1-

Transcript of Argent Classic Convertible Arbitrage Fund L.P., et al. v...

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 1 of 20

1

2

3

4

5

6

7

8 UNITED STATES DISTRICT COURT

9 CENTRAL DISTRICT OF CALIFORNIA

10

11 ARGENT CLASSIC CONVERTIBLE Case No. CV 07-07097 MRP (MANx)

12 ARBITRAGE FUND L.P.,individually and on behalf of all others ORDER Denying Class Certification

13 similarly situated,14

15Plaintiff,

V.16

17 COUNTRYWIDE FINANCIAL

18 CORPORATION, el al.,

19 Defendants.

20 INTRODUCTION

21 This is a securities action against Countrywide Financial and several other

22 persons and entities (collectively, "Defendants"). For purposes of this order, no

23 distinction among Defendants is necessary.

24 Plaintiff Argent Classic Convertible Arbitrage Fund L.P. ("Argent") brings

25 this action on behalf of those who purchased certain Countrywide convertible

26 debentures ("the Debentures") offered in a private placement under SEC Rule

27

28

-1-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 2 of 20

1 144A. 17 C.F.R. § 230.144A. Two series of Debentures were offered, with a total

2 aggregate principal of approximately $4 billion.'

3 Argent moves to certify a class of Debentures purchasers for the period May

4 16, 2007 through November 21, 2007. Third Amended Compl. ("TAC") at 2. The

5 period starts on May 16, the Debentures' offering date. The period ends on

6 November 21, the date after which Debentures were publicly registered and freely

7 tradable.

8 This order is devoted to a few pertinent facts. Because the issues involved in

9 Argent's motion are so plain and the required analysis so well established, the

10 Court declines to explain every relevant consideration leading to this order.

11 Instead, the Court summarizes and incorporates by reference documents and

12 colloquy in the record in support of its conclusions. No further elaboration should

13 be necessary.

14 There is a factually related securities action before this Court, In re

15 Countrywide Financial Corporation Securities Litigation (referred to herein as

16 "Pappas," after the name of the first-filed case into which other Countrywide-

17 related cases were consolidated). A concurrently filed Memorandum of Decision

18 resolves the class certification issues respecting certain publicly traded securities in

19 the Pappas case (the "Pappas Memorandum"). Parts of the Pappas Memorandum

20 are incorporated by reference to more fully explain the legal standard applied in

21 this case.

22 Argent has failed to demonstrate numerosity, typicality, and adequacy.

23 Argent's motion for class certification is DENIED.

24

25

26

27

28 ^

Countrywide Fin. Corp., Form 8-K (May 22, 2009).

-2-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 3 of 20

1 I.

2 BACKGROUND

3 A. Consolidation

4 In the November 28, 2007 order consolidating Countrywide-related cases,

5 this case was kept separate because the private placement context presents unique

6 issues. See Pappas Memorandum Section I.A (discussing the consolidation order),

7 Introduction n.3 (naming the other Countrywide-related cases before this Court).

8 Most important, the Court anticipated that the issue of reliance would

9 require careful attention. Specifically, the Court was concerned about the private

10 market's implications for fraud on the market and actual reliance. Consol. Order

11 (Nov. 28, 2007) 12-13.

12 B. Second Amended Complaint

13 The Second Amended Complaint ("SAC") asserted only one federal claim

14 (fraud under § 10(b) of the '34 Act) and several California state theories. 2 The

15 Court initially held that the SAC did not adequately plead reliance and dismissed it

16 on November 13, 2008 with leave to amend. 2008 U.S. Dist. LEXIS 103148

17 ("SAC Order"). The SAC Order is incorporated by reference as background

18 material.

19 The SAC Order notes that the SAC pled two reliance theories, both of which

20 sought to invoke the fraud-on-the-market presumption under Basic, Inc. v.

21 Levinson, 485 U.S. 224 (1988). Those theories were (1) that the Debentures'

22 convertibility feature "inextricably link[ed]" the Debentures' price to the common

23 stock price; and (2) "that, at one point $4 billion in [D]ebentures were listed for

24

25

26 2 The parties appear to agree that the Debentures are not "covered securit[ies]"27 under the Securities Litigation Uniform Standards Act ("SLUSA"). SLUSA28 defines "covered security" to exclude "any debt security that is exempt from

registration under" SEC rules for privately traded securities. 15 U.S.C. § 77(f)(3).

-3-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 4 of 20

1 trading, and actively traded in the PORTAL Market of the Nasdaq Stock Market,

2 Inc." Id. at * 5.3

3 Both sides argued strenuously about the reliance allegations. In view of this,

4 and because reliance was inadequately pled, the SAC Order passed only on

5 reliance, observing first that the SAC did not explain how Argent acquired its

6 securities. This omission was important because Argent appeared to have

7 purchased some Debentures in their initial offering—before a private market had

8 developed . 4 As for the aftermarket purchases, the SAC failed to explain which

9 market price (PORTAL or common stock) Argent relied upon—if any. Id. at 8-10.

10 Without relying on one market or another, Argent was plainly not entitled to a

11 fraud-on-the-market presumption for these aftermarket purchases. Id.

12 To the extent the SAC did mention markets, the SAC was held inadequate

13 under Rule 9(b). Id. The SAC merely asserted that the Debentures' convertibility

14 features linked the Debentures to Countrywide's common stock price—but the

15 SAC did not adequately explain how the Debentures' terms linked the prices (and

16 under which conditions the link might be broken). The SAC's PORTAL allegation

17 was a single paragraph. See id. Moreover, Argent is a private investment fund

18 ("hedge fund") and an examination of its late-period Debentures transactions and

19

20

21 3 For background information about PORTAL, see generally Camden Asset22 Mgmt, L.P. v. Sunbeam Corp., 2001 WL 34556527, at *5-11, 2001 U.S. Dist.23 LEXIS 11022, at * 16-36 (S.D. Fla. July 3, 2001) (discussing PORTAL at class

certification); Schwieger, Elena, Redefining the Private Placement Market after24 Sarbanes-Oxley: NASDAQ's PORTAL and Rule 144A, 57 CATH. U. L. REV. 885

25 (2008).

26 4 This is not to say that Argent could not, as a matter of law, have relied upona price set at the offering; this was a private offering from a well established issuer,

27 not a new issuer's initial public offering. SAC Order at * 12-13; accord In re Initial

28 Public Offering Sec. Litig., 471 F.3d 24, 42-43 (2d Cir. 2006) (discussing initialpublic offerings).

-4-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 5 of 20

1 apparent investment strategy enhanced the serious misgivings the Court had about

2 reliance issues. SAC Order at * 12-14.

3 Every one of the SAC Order's holdings were narrow, qualified, and allowed

4 Argent an opportunity to replead facts to establish reliance under any number of

5 possible theories. 5 The SAC was dismissed without prejudice and Argent was

6 granted leave to amend.

7 C. The Third Amended Complaint

8 On December 3, 2008, Argent filed a Third Amended Complaint ("TAC").

9 The TAC is the operative complaint. In a March 3, 2009 order (the "TAC Order"),

10 most of Defendants' motions to dismiss the TAC were denied in their entirety.

11 Docket no. 142. The TAC Order is hereby incorporated by reference as

12 background material.

13 The TAC adequately alleges Argent's actual reliance only on the

14 Debentures' market price. For instance, the TAC alleges that Argent "read and

15 reviewed" the Debentures' offering materials. TAC ¶ 20; see also TAC Order at 9

16 n.7 (dismissing other allegations that could have been intended to plead some form

17 of reliance). It contains no allegation that Argent "relied upon" these offering

18 materials. In some cases, faulting a complaint for omitting "and relied upon" could

19 be an overly technical exercise in pleading. See Fed. R. Civ. Proc. 1 ("[These rules]

20 should be construed and administered to secure the just, speedy, and inexpensive

21

22

23 5 In view of the parties' arguments about reliance, and the possibility of

24 declining supplemental jurisdiction if the federal claim was unsupportable, the25 Court did not address state claims that may lack a reliance element or for which

26 other reliance theories may be available. Instead, Argent was given the opportunityto amend in any appropriate manner. It is also notable that the SAC's "reliance"

27 deficiencies also implicate other necessary elements of all (or most) claims-28 including whether any damages were caused by Defendants' actionable statements

or conduct.

-5-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 6 of 20

1 determination of every action and proceeding."). But this was a serious omission

2 after the SAC Order's discussion of reliance.

3 As for fraud-on-the-market in the Debentures' offering, the TAC, fairly

4 construed, adequately alleges that the Debentures' pricing was efficient based upon

5 their convertibility feature, Countrywide's market prominence, and other factors.

6 TAC Order at 9-13. For example, the convertibility feature may suggest reliance

7 on the common stock market because convertible debt can be "converted" into

8 common stock if certain conditions are met. The Debentures could be converted

9 into common stock at a pre-set price called the "strike price." The more the

10 common stock price exceeds the strike price, the stronger the debtholder's

11 incentive to convert. Thus, though the Debentures have debt features, their value is

12 also linked to the price of the common.

13 As for the aftermarket purchases, one important factor for allowing the TAC

14 to pass the pleading stage as to Argent's aftermarket purchases was the TAC's

15 enhanced pleading about PORTAL. TAC ¶¶ 10, 18, 21, 56-61; TAC Order at 12.

16 The TAC contains specific allegations regarding Argent's trading activity in

17 PORTAL, PORTAL's structure generally, and the Debentures' trading on

18 PORTAL in particular. The TAC Order's reasoning relies in large part on the

19 PORTAL allegations. TAC Order at 10-12.

20 The state claims were allowed to proceed "[b]ecause the surviving federal

21 claims comprise the same facts to which the state claims relate" and, therefore, the

22 state claims would not enlarge Countrywide's discovery burden. Further, there was

23 no need to determine whether exercising supplemental jurisdiction was

24 appropriate. TAC Order at 13. The TAC Order "notes that California does not have

25 a fraud on the market doctrine, Small v. Fritz Cos., 30 Cal. 4th 167, 180 (Cal.

26 2003), but expresses no opinion on any other state reliance doctrines that Argent

27 contends may exist." Id.

28

-6-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 7 of 20

1 In sum, the TAC was allowed to proceed, despite the Court's misgivings.

2 See, e.g., TAC Order at 10:16-11:2 (cautionary language); 12:18-27 (dicta

3 regarding matters Argent could have pled); 12:28-13:7 (cautionary dicta indicating

4 concern about additional facts of the case). Indeed, the TAC Order gave Argent the

5 benefit of several doubts and indicated this Court's hesitance to impose a

6 heightened pleading burden on Argent simply because it is a sophisticated

7 institutional investor suing on nontraditional instruments that traded in

8 nontraditional markets.6

9 II.

10 CLASS CERTIFICATION

11 A full statement of the class certification standard applied in this case is set

12 forth in Section III.A of the Pappas Memorandum of Decision. That section is

13 incorporated by reference. A brief summary follows:

14 A court exercises "broad discretion to certify a class" within Federal Rule of

15 Civil Procedure 23's framework. Zinser v. Accufix Res. Inst., Inc., 253 F.3d 1180,

16 1186 (9th Cir. 2001), as amended on denial of reh g, 273 F.3d 1266 (9th Cir.

17 2001).

18 The proponent of class certification "bears the burden of demonstrating" that

19 all Rule 23 requirements are satisfied. Zinser, 253 F.3d at 1186. To protect due

20 process, the Court is empowered to undertake an analysis as "rigorous" as

21 necessary under the circumstances, such that the Court is "satisfied" that a class

22

23 6 For example, the TAC Order observes that the Debentures' features could

24 "under some circumstances, break the alleged price link with common stock."25 TAC Order at 12-13. In addition, despite the falling price of Countrywide common

26 stock, Argent continued to make large purchases until late in the class period.Further, the TAC Order enumerates a variety of facts that Argent could have

27 pled—because such facts were within Argent's knowledge and its capacity to28 plead—but that Argent, for reasons then unknown to the Court and Defendants, di

not plead. TAC Order at 12.

-7-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 8 of 20

1 action may be properly maintained. Gen. Tel. Co. of the Sw. v. Falcon, 457 U.S.

2 147 9 161 (1982) (discussing the Rule 23(a) prerequisites).

3 Rule 23 has due process implications. Indeed, "[t]he class action device was

4 designed as an exception to the usual rule." Falcon, 457 U.S. at 155. Accordingly,

5 courts should be cognizant of their duty to protect absent class members' interests.

6 The Rule 23 inquiry proceeds in two steps. In this case, only the first step,

7 the Rule 23(a) "prerequisites," need be addressed. The prerequisites are

8 numerosity, commonality, typicality, and adequacy. Argent seeks an opt-out class

9 under Rule 23(b)(3). If the prerequisites were met, the additional requirements of

10 Rule 23(b)(3) would need to be addressed.

11 However, analyzing the prerequisites more than suffices to conclude that

12 Argent cannot represent and, upon judgment, bind absent class members.

13 A. Numerosity

14 Rule 23(a)(1) requires only that the class be so numerous that joinder is

15 "impracticable." Beyond that, little judicial authority exists on this prerequisite.

16 A class size of forty is sometimes offered as a helpful benchmark. See, e.g.,

17 Consol. Rail Corp. v. Town of Hyde Park, 47 F.3d 473, 483 (2d Cir. 1995) (citing 1

18 NEWBERG ON CLASS ACTIONS 2D, (1985 Ed.) § 3.05), cent denied 515 U.S. 1122

19 (1995); Cox v. Am. Cast Iron & Pipe Co., 784 F.2d 1546, 1553 (11th Cir. 1986)

20 (quoting 3B JAMES WM. MOORE, ET AL., MOORE's FEDERAL PRACTICE ¶ 23.05 [ 11

21 n.7 (1978)).

22 A leading treatise notes that (1) the certification proponent "does bear the

23 burden of showing impracticability" and (2) mere "speculation as to the number of

24 parties involved is not sufficient to satisfy" numerosity. 7A FEDERAL PRACTICE &

25 PROCEDURE § 1762 (West 2009); accord Lehocky v. Tidel Techs., Inc., 220 F.R.D.

26 4911, 499 (S.D. Tex. 2004) ("[A] plaintiff need not demonstrate with precision the

27 number of persons in the class to satisfy the requirement that joinder is

28 impracticable where such a conclusion is clear from reasonable estimates."

-8-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 9 of 20

1 (emphasis added)). Further, (3) "difficulty in identifying the class members" may

2 be a factor. AAL High Yield Bond Fund v. Ruttenberg, 229 F.R.D. 676 (N.D. Ala.

3 2005) (citing 7A FEDERAL PRACTICE & PROCEDURE § 1762); Hopson v.

4 Hanesbrands, Inc., 2009 WL 928133, at *3, 2009 U.S. Dist. LEXIS 33900, at *6-7

5 (N.D. Cal. Apr. 3, 2009) (citing WILLIAM W. SCHWARZER, ET AL., FEDERAL CIVIL

6 PROCEDURE BEFORE TRIAL, §§ 10:260-10:264). And (4) geographical dispersion of

7 the class may be relevant. Hopson, 2009 WL 928133, at *3, 2009 U.S. Dist LEXIS

8 33900, at *6.

9 Finally, Rule 23(b)(3) in part serves to aggregate the small claims of

10 dispersed plaintiffs. Where the putative class is small in number, relatively

11 sophisticated, and has potential claims, the class members may be presumed to

12 have incentives to file their own actions. In this situation, there may be less need

13 for the class action device, particularly an opt-out class under Rule 23(b)(3), such

14 as Argent seeks. See Blackie v. Barrack, 524 F.2d 891, 910 n.26 (9th Cir. 1975)

15 "[One of] the primary purposes of the class action device [is] to give small

16 investors a reasonable opportunity to vindicate their claims in a manner which will

17 not place an undue burden upon them." (quoting In re Caesar's Palace Sec. Litig.,

18 360 F. Supp. 366,397-98 (S.D.N.Y. 1973)); In re Worlds of Wonder, 1990 WL

19 61951, at *6, 1990 U.S. Dist. LEXIS 8511 at *20-21 (N.D. Cal. Mar. 23, 1990)

20 (entertaining an argument that because of the size and sophistication of debentures

21 purchasers, the purchasers could maintain their own lawsuits; leaving open the

22 possibility of decertifying a debentures subclass if a "significant number" of the

23 class members opt out).

24 It bears repeating that, even under any set of circumstances most favoring a

25 class in this case, the proposed class would be limited to a six-month period.

26 During that six-month period, the Debentures were tradable only in private markets

27 by large institutional investors. Only a few hundred institutions have been

28 identified as potentially involved with Debentures transactions during this period.

-9-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 10 of 20

1 Despite these few hundred potential class members, Argent has been unable

2 to identify with certainty even one additional class member. The reasons:

3 Countrywide made a tender offer for some Debentures.' Other Debentures include

4 a put right that became exercisable. As a result of the tender and the put right, the

5 vast majority of the outstanding Debentures were repaid after suit was filed . 8

6 Argent identifies institutions that held Debentures at the time of the Debentures'

7 November 2007 registration, as well as some additional institutions that traded in

8 the Debentures. Such institutions may have been damaged if they purchased the

9 Debentures and then sold them before putting or tendering the Debentures—but

10 Argent has not located any such institution besides itself.

11 Further, these institutions presumably engaged in large transactions. The

12 face value of the Debentures' offering was approximately $4 billion-in total. That

13 $4 billion was allocated among a few hundred original purchasers. If another

14 institution was damaged and wishes to seek recovery, it presumably has the means

15 and incentive to file its own suit.

16 The numerosity prerequisite is not met.

17 B. Commonality

18 Commonality requires "questions of law or fact common to the class." Rule

19 23(a)(2). Commonality is not identity. Indeed, the requirement of "shared legal

20 issues with divergent factual predicates is sufficient, as is a common core of salient

21 facts [even if that core is] coupled with disparate legal remedies within the class."

22

23 ' The tender offer was made to settle other litigation. Countrywide Fin. Corp.,

24 Form 8-K (Oct. 14, 2008).25

8 The Debenture holders were repaid their principal and interest unpaid or

26 accrued. Countrywide offers evidence that Bank of America repaid nearly 95% ofthe outstanding principal amount on one series of Debentures and 100% of the

27 outstanding principal amount on the other. Devine Decl. Ex. 60. Of course, the28 initial burden is on Argent to establish numerosity, not on Countrywide to defeat it.

Zinser, 253 F.3d at 1186.

-10-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 11 of 20

1 Hanlon v. Chrysler Corp., 150 F.3d 1011, 1019 (9th Cir. 1998). This standard is

2 somewhat "permissive[]." Id.

3 A further consideration is that choice of law or conflict of laws issues are a

4 possibility on Argent's state claims. Though Countrywide was based in California,

5 Argent's operations appear to be in Connecticut. TAC ¶ 16. Again, no other

6 member of the class has been identified. A small class of entirely out-of-state

7 plaintiffs could raise some choice of law or conflict of laws concerns. See Zinser,

8 253 F.3d at 1186; Worlds of Wonder, 1990 WL 61951, at *5-6, 1990 U.S. Dist.

9 LEXIS 8511, at * 14-19.

10 Nevertheless, under the Ninth Circuit's "permissive[]" commonality

11 standard, it is possible that Argent has satisfied commonality by identifying a

12 common factual course of conduct.

13 Commonality may be satisfied.

14 C. Typicality and adequacy

15 It is sometimes difficult to entirely separate typicality from adequacy; as the

16 Supreme Court recognizes, the two prerequisites "tend to merge" in some

17 situations. Amchem Prods. v. Windsor, 521 U.S. 591, 626 n.20 (1997). In the

18 present case, the facts going to these two prerequisites largely overlap. These

19 prerequisites will therefore be discussed together.

20 1. Legal standard

21 The typicality and adequacy prerequisites, together, are "[t]he due process

22 touchstone." Blackie, 524 F.2d at 910. Typicality must be judged in light of the

23 circumstances. Id. "The purpose of the typicality requirement is to assure that the

24 interest of the named representative aligns with the interests of the class." Hanon v.

25 Dataproducts Corp., 976 F.2d 497, 508 (9th Cir. 1992).

26 Typicality is not identity. Rather, the class' claims need be only "fairly

27 encompassed by" or "reasonably co-extensive with" the proposed representative's

28 claim. Falcon, 457 U.S. at 156 ("fairly encompassed by"); Hanlon, 150 F.3d at

-11-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 12 of 20

1 1020( 66 reasonably coextensive with"). However, typicality is defeated where

2 "there is a danger that absent class members will suffer [because] their

3 representative is preoccupied with defenses unique to it." Hanon, 976 F.2d at 508

4 (internal quotations omitted).

5 Adequacy asks whether "the representative parties will fairly and adequately

6 protect the interests of the class." Fed. R. Civ. Proc. 23(a)(4). The two key

7 inquiries are (1) whether there are conflicts within the class; and (2) whether

8 plaintiffs and counsel will vigorously fulfill their duties to the class. Staton v.

9 Boeing Co., 327 F.3d 938, 957 (9th Cir. 2003).

10 The adequacy inquiry also "factors in competency and conflicts of class

I 1 counsel." Amchem, 521 U.S. at 626 n.20; Local Joint Exec. Bd. of

12 Culinary/Bartender Trust Fund v. Las Vegas Sands, Inc., 244 F.3d 1152, 1162 (9th

13 Cir. 2001). Closely related to the adequacy inquiry, Rule 23(g) governs how class

14 counsel is appointed. A class certification order must address Rule 23(g). Fed. R.

15 Civ. Proc. 23(c)(1)(13). Rule 23(g) requires a court to consider four factors

16 regarding counsel and allows consideration of "any other matter pertinent to

17 counsel's ability to fairly and adequately represent the interests of the class." Id.

18 23(g)(1)(A)-(B).

19 Adequacy is also a due process "touchstone" and, like typicality, must be

20 judged in light of the circumstances. Blackie, 524 F.2d at 910.

21 2. Adequacy: counsel and Argent's course of conduct

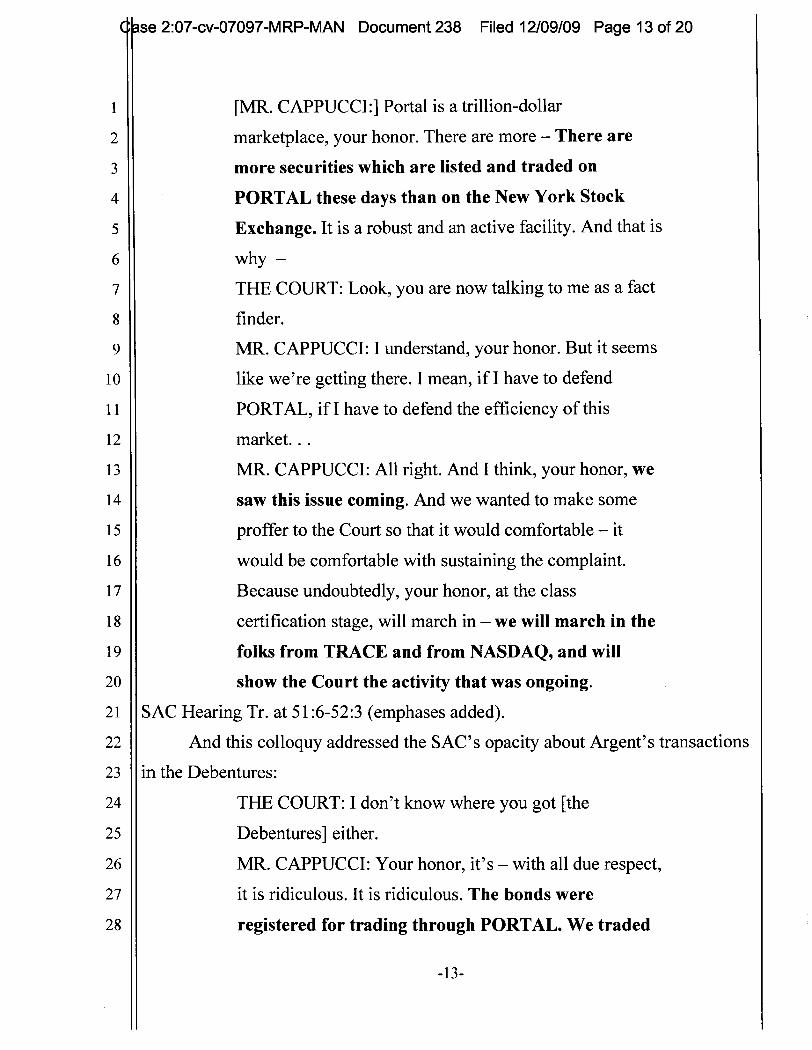

22 Argent's counsel has demonstrated a failure to ascertain and present to the

23 Court accurate facts to support their claims and their arguments. The most

24 important illustrations of this involve counsel's representations to the Court that

25 the Debentures traded on PORTAL. They did not. In fact, at no time in 2007 was

26 PORTAL even available for securities of the Debentures' type.

27 The following exchanges took place at the November 2008

28 hearing on the motions to dismiss the SAC:

-12-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 13 of 20

1 [MR. CAPPUCCI:] Portal is a trillion-dollar

2 marketplace, your honor. There are more — There are

3 more securities which are listed and traded on

4 PORTAL these days than on the New York Stock

5 Exchange. It is a robust and an active facility. And that is

6 why —

7 THE COURT: Look, you are now talking to me as a fact

8 finder.

9 MR. CAPPUCCI: I understand, your honor. But it seems

10 like we're getting there. I mean, if I have to defend

11 PORTAL, if I have to defend the efficiency of this

12 market...

13 MR. CAPPUCCI: All right. And I think, your honor, we

14 saw this issue coming. And we wanted to make some

15 proffer to the Court so that it would comfortable — it

16 would be comfortable with sustaining the complaint.

17 Because undoubtedly, your honor, at the class

18 certification stage, will march in — we will march in the

19 folks from TRACE and from NASDAQ, and will

20 show the Court the activity that was ongoing.

21 SAC Hearing Tr. at 51:6-52:3 (emphases added).

22 And this colloquy addressed the SAC's opacity about Argent's transactions

23 in the Debentures:

24 THE COURT: I don't know where you got [the

25 Debentures] either.

26 MR. CAPPUCCI: Your honor, it's — with all due respect,

27 it is ridiculous. It is ridiculous. The bonds were

28 registered for trading through PORTAL. We traded

-13-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 14 of 20

1 on PORTAL.

2 Id. at 58:12-24 (emphasis added).

3 Argent included the following allegations in the TAC, filed a few weeks

4 later:

5 [D]uring the Class Period, thousands of transactions

6 in each of the Series A and Series B Debentures were

7 executed in the PORTAL Market of the Nasdaq Stock

8 Market, Inc." (the "PORTAL Market") -- a robust and

9 primary market for Rule 144A designated securities --

10 through leading financial institutions which acted as

11 market makers in the securities, as discussed further ....

12 TAC ¶ 10 (emphases added; footnote omitted).

13 Argent also purchased $5,730,000 of Series A and

14 $5,290,000 of Series B Debentures in aftermarket

15 PORTAL transactions.

16 TAC ¶ 18 (emphases added).

17 Argent relied on the integrity of the active and

18 developed market for the Debentures, which had then

19 begun to trade on the PORTAL Market, and the pricing

20 of those securities in PORTAL transactions to

21 concerns that Countrywide was expected to declare

22 bankruptcy in wake of the imploding of its business

23 model), thousands of transactions in the Debentures

24 on the PORTAL Market were cleared electronically

25 through the Depository Trust Clearing Corporation

26 ("DTCC" ).

27 TAC ¶ 21 (emphases added). See also TAC ¶¶ 56-62 (containing

28 more allegations about PORTAL).

-14-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 15 of 20

1 Argent's opposition to the motions to dismiss contains no less than four

2 pages dedicated to PORTAL. At one point, the opposition declares, "Argent did

3 not buy Debentures in traditional over-the-counter transactions." Arg. Opp. to

4 Mots. to Dismiss TAC at 2 (docket no. 116).

5 All these representations were false. The Debentures never traded on

6 PORTAL. Nor was PORTAL even open to securities of the Debentures' type

7 during 2007. And Defendants obtained voluminous evidence in discovery showing

8 that Argent purchased the Debentures in over-the-counter transactions that were

9 nontraditional only in the sense that computer messages were exchanged in

10 addition to telephone negotiations.

11 Counsel explained the representations thus:

12 MR. CAPPUCCI: Your honor, I can only offer my

13 apology to the Court. It is not something that has

14 happened to me much in the past. We were relying on —

15 relying on —

16 THE COURT: It has never happened to me before.

17 Class Cert. Hearing Tr. at 51:14 (Sept. 9, 2009).

18 The most generous inference is that counsel was misinformed. However,

19 counsel stated that they "saw this issue coming." SAC Hearing Tr. at 51:22.

20 Counsel had access to their hedge fund client. That access was used to obtain

21 evidence at the class certification stage; it was apparently not used in the prefiling

22 and pleading stages. At the pleading stage, counsel hired an expert to submit an

23 affidavit regarding the market for Debentures. TAC Order at 6. The expert report

24 was stricken as improper at that stage, id., but the Court reviewed the report after

25 learning that counsel's representations were false. The report states that the expert

26 reviewed data from FINRA's TRACE service (unaffiliated with PORTAL) and

27 that "the Debentures were eligible for trading in the PORTAL Market of the

28 Nasdaq Stock Market, Inc." Nye Aff. ¶j 34, 56 (emphasis added). It is strange to

-15-

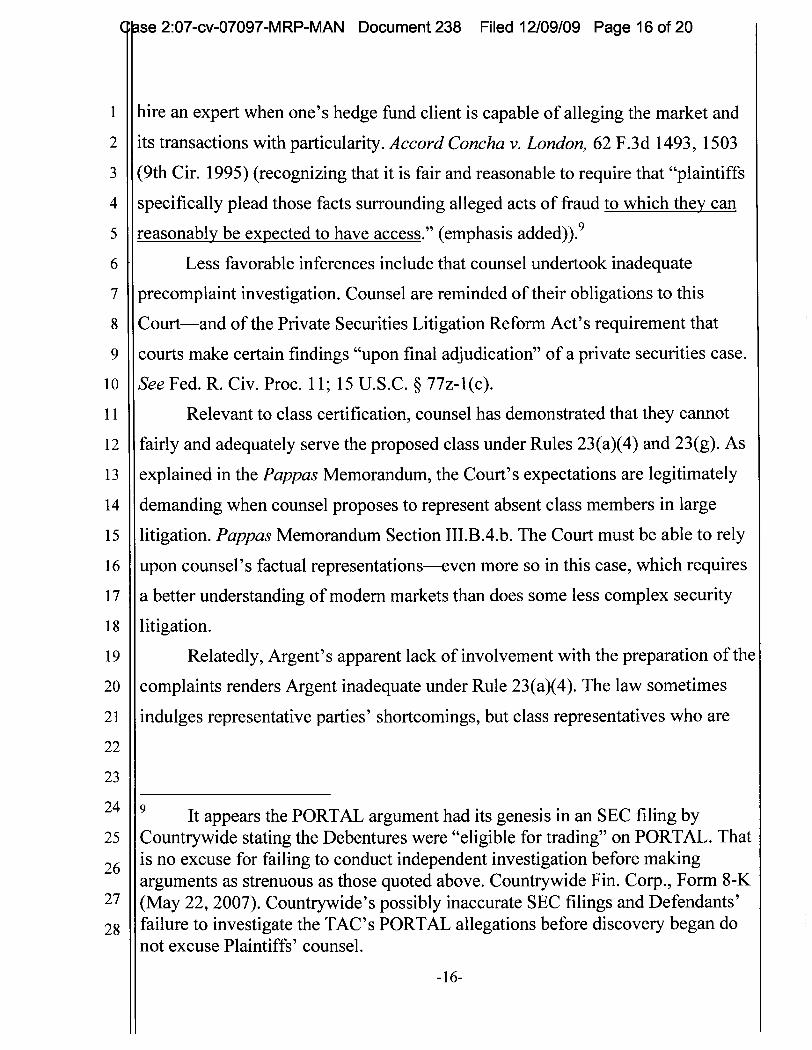

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 16 of 20

1 hire an expert when one's hedge fund client is capable of alleging the market and

2 its transactions with particularity. Accord Concha v. London, 62 F.3d 1493, 1503

3 (9th Cir. 1995) (recognizing that it is fair and reasonable to require that "plaintiffs

4 specifically plead those facts surrounding alleged acts of fraud to which they can

5 reasonably be expected to have access." (emphasis added)).9

6 Less favorable inferences include that counsel undertook inadequate

7 precomplaint investigation. Counsel are reminded of their obligations to this

8 Court—and of the Private Securities Litigation Reform Act's requirement that

9 courts make certain findings "upon final adjudication" of a private securities case.

10 See Fed. R. Civ. Proc. 11; 15 U.S.C. § 77z-1(c).

11 Relevant to class certification, counsel has demonstrated that they cannot

12 fairly and adequately serve the proposed class under Rules 23(a)(4) and 23(g). As

13 explained in the Pappas Memorandum, the Court's expectations are legitimately

14 demanding when counsel proposes to represent absent class members in large

15 litigation. Pappas Memorandum Section III.B.4.b. The Court must be able to rely

16 upon counsel's factual representations—even more so in this case, which requires

17 a better understanding of modern markets than does some less complex security

18 litigation.

19 Relatedly, Argent's apparent lack of involvement with the preparation of the

20 complaints renders Argent inadequate under Rule 23(a)(4). The law sometimes

21 indulges representative parties' shortcomings, but class representatives who are

22

23

24 9 It appears the PORTAL argument had its genesis in an SEC filing by25 Countrywide stating the Debentures were "eligible for trading" on PORTAL. That

26 is no excuse for failing to conduct independent investigation before makingarguments as strenuous as those quoted above. Countrywide Fin. Corp., Form 8-K

27 (May 22, 2007). Countrywide's possibly inaccurate SEC filings and Defendants'28 failure to investigate the TAC's PORTAL allegations before discovery began do

not excuse Plaintiffs' counsel.

-16-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 17 of 20

1 unwilling to monitor counsel's interests—which sometimes oppose the class'

2 interests—are not tolerated. See Pappas Memorandum Section III.B.4.c.

3 3. Typicality & adequacy: the debentures purchasers, Argent's

4 decisionmaking process, and counsel's apparent inattention to the issues

5 As a background consideration, Debentures' purchasers presumably

6 undertook a variety of divergent trading and investment strategies. Under some

7 circumstances, Countrywide's falling common stock prices (due to the alleged

8 corrective disclosures) could have increased the proposed class members' profits.

9 See generally Igor Loncarski, et al., The Rise and Demise of the Convertible

10 Arbitrage Strategy, Social Science Research Network Working Paper Series (Jan.

11 23, 2009 rev.), available at

12 http://papers.ssm.com/sol3/papers.cfm?abstract_id=929951 (collecting empirical

13 data on convertible arbitrage, discussing how certain debentures features affect the

14 strategies of some debentures purchasers, and hypothesizing about some

15 motivations and strategies of some convertible debentures' purchasers). Such funds

16 often take a short position in the common stock in connection with their debentures

17 purchases; if that short position is large enough, falling Countrywide stock could

18 generate a profit—especially when combined with the put right and tender offer.

19 See id.; Cappucci Dec. Ex. 1 at 2-3 (presentation to Countrywide board regarding

20 convertible offering considerations and the "investor base" of "hedge funds" the

21 offering was intended to "[t]ap"). The point is that such investors make typicality

22 more difficult to establish than usual. Accord Welling v. Alexy, 155 F.R.D. 654,

23 660 (N.D. Cal. 1994) ("A review of the[] cases reveals ... that sophistication alone

24 is not sufficient to bar a trader from serving as a class representative. Rather, courts

25 look for sophistication in combination with other factors ...."). Further, counsel's

26 unwillingness to face these complexities and to use its access to Argent to correctly

27 plead the nature of the Debentures' market—and counsel's failure, at class

28 certification, to produce evidence showing why these factors will not hinder

-17-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 18 of 20

1 Argent's typicality—provides additional cause to conclude that counsel is

2 inadequate.' 0

3 More important, Countrywide has obtained and produced additional

4 significant evidence that Argent is inadequate and atypical. On this point, pages

5 8:7-16:18 of the opposition to class certification are incorporated by reference.

6 Two of the most damaging pieces of evidence are:

7 • After Argent filed its complaint, Argent's portfolio manager sent an

8 email referring to a state government's investigation into

9 Countrywide's practices—some of the same practices that the TAC

10 alleges were concealed and destroyed the value of Argent's

11 investments—as "[p]olitical grandstanding." Devine Ex. 30.

12 • After Argent filed its complaint, and apparently as part of a

13 "directive for an overall reduction in ... positions," Argent sold its

14 Debentures. Shortly afterwards, the Bank of America acquisition

15 was announced and Argent's internal emails express "frustrat[ion]"

16 with the decision to liquidate the Debentures. The emails observe

17

18 10 This should not be read to imply any undue categorical skepticism toward19 hedge funds as plaintiffs; nor does it reflect any predisposition to deny legal

protection for fraud in nontraditional markets or nontraditional securities. Indeed,20 at every stage of this litigation, the Court has been cautious not to reach a

21 conclusion that overreaches on these matters. See, e.g., SAC Order, at * 13-14("The Court certainly does not conclude that [a hedge fund with an arbitrage

22 strategy] cannot take advantage of the securities laws. Defendants suggest that23 taking a "contrarian" position (relative to the market) negates all legal protection . .

. The Court disagrees: arbitrageurs have just as much right as anyone else to24 develop a trading strategy based on accurate disclosures."). Accord Argent Class

25 Convertible Arbitrage Fund L.P. v. Rite Aid Corp., 315 F. Supp. 2d 666 (E.D. Pa.

26 2004) (discussing convertible arbitrage generally and Argent specifically). But seeCamden Asset Mgmt., L.P. et al. v. Sunbeam Corp., No. 99-CV -8275, 2001 WL

27 34556527, 2001 U.S. Dist. LEXIS 11022 (S.D. Fla. July 3, 2001) (confronting a28 case with facts similar to the present case; suggesting a much harsher, and perhaps

not entirely warranted, view).

-18-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 19 of 20

1 that Argent would have made a $20-45 million profit on its

2 Debentures transactions had it not liquidated the Debentures. Devin:

3 Exs. 3, 32-37.

4 This second piece of evidence is important for at least three reasons: (1) it

5 illustrates that Argent does not take this litigation seriously, does not appreciate its

6 duties as proposed class representative, and has little interest in monitoring its

7 attorneys' conduct to protect the proposed class' interests; (2) it suggests that

8 Defendants have defenses as to loss causation and damages which threaten to

9 become the focus of this litigation; and (3) it illustrates that this order's foregoing

10 concerns that few, if any, of the conceivable class members were harmed are not

11 merely speculative.

12 Argent is obviously atypical.

13 III.

14 ADDITIONAL STATEMENTS

15 The Court will not reach the Rule 23(b)(3) requirements. However, the

16 entirety of Defendants' class certification opposition is hereby incorporated by

17 reference. The opposition is incorporated without adopting any statement or

18 conclusion of law contained in the opposition. Instead, the opposition points up

19 additional facts in the record. Some of those facts further demonstrate the

20 deficiencies summarized above. Many of those facts go to the difficulties Argent

21 would face in satisfying Rule 23(b)(3); but, again, no conclusion is reached on

22 Rule 23(b)(3)."

23

24

25

26 At times, the opposition borders on arguing that Argent cannot succeed onthe merits of its individual claims—particularly on the federal claim and those state

27 claims with a reliance element. Such arguments are properly made in a motion for28 summary judgment. Finally, as noted above, the Court has, in its prior orders,

withheld discussion of the propriety of supplemental jurisdiction.

-19-

Case 2:07-cv-07097-MRP-MAN Document 238 Filed 12/09/09 Page 20 of 20

1 Finally, there is some authority for the proposition that, even if a proposed

2 class representative makes a showing that marginally satisfies each of Rule 23's

3 prerequisites individually, the "ultimate decision" whether to certify a class, under

4 the totality of the circumstances, is still within a court's sound discretion. See In re

5 Wells Fargo Home Mortgage Overtime Pay Litig., 571 F.3d 953, 957 (9th Cir.

6 2009) (mentioning "judgment in weighing the correct mix of factors"); Yokoyama

7 v. Midland Nat'l Life Ins. Co., 2009 U.S. App. LEXIS 19357 (9th Cir. Aug. 28,

8 2009) ("[T]he ultimate decision as to whether or not to certify the class, must, at

9 least in any nonfrivolous putative class action, involve a significant element of

10 discretion."). The Court concludes that even if Argent did satisfy each of these

11 prerequisites viewed in isolation, under the totality of the circumstances, the

12 ultimate decision would remain the same. This applies both for the federal and for

13 the state claims.

14 IV.

15 CONCLUSION

16 For the foregoing reasons, Argent's motion for class certification is

17 DENIED.

18

19 IT IS SO ORDERED.

20

21 DATED: December 9, 2009 L < </

22 Hon. Mariana R. PfaelzerUnited States District Judge

23

24

25

26

27

28

-20-