Are bonds in a bubble?

20

NEWFOUND RESEARCH 1 Newfound Case #4582249 DEFENSIVE | SIMPLE | CONSISTENT | THOUGHTFUL FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

-

Upload

corey-hoffstein -

Category

Economy & Finance

-

view

696 -

download

0

Transcript of Are bonds in a bubble?

NEWFOUND RESEARCH

1Newfound Case #4582249

DEFENSIVE | SIMPLE | CONSISTENT | THOUGHTFUL

FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

In August 2008, Newfound Research was founded based on a simple, but powerful, premise: investorscare deeply about capital preservation.We believe in portfolio processes that are simple, consistent, and thoughtfully designed.Most of all, we believe that managing risk is paramount to potentially achieving superior risk-adjustedreturns*.Volatility happens. Have a plan with Newfound Research.

OUR INVESTMENT PHILOSOPHYDEFENSIVE | SIMPLE | CONSISTENT | THOUGHTFUL

2

Defensive Simple Consistent ThoughtfulWe view risk management from the investor’s point of view, seeking to participate in bull markets and avoid large losses during bear markets.Volatility will happen: it is the price of admission to the financial markets. We believe investors need a thoughtful plan to deal with this volatility before it happens.

We believe that each strategy should seek to adhere to a simple investment objective, providing transparency both in expected outcome and process. Our research shows that simple processes are more robust to uncertainty than complicated processes – an important factor in delivering consistent and repeatable results.

To meet a simple objective, a strategy must be governed by a guiding policy. At Newfound, we believe that the best way to ensure consistency in our process is through a quantitatively-enabled, rule-based approach, which can help mitigate the behavioral biases that often compound into investment errors.

At Newfound, we recognize the clear distinction between the quantitative models that generate our investment signals and the rules we use to translate those signals into portfolios. We believe that it is with these rules – the design of the portfolio – that we seek to achieve our objective and manage model risk.

There is no guarantee that any investment strategy will achieve its objectives.* Risk-adjusted returns is a measure to find out how much return an investment will provide given the level of risk associated with it.FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Asset BubblesWhat are they?

Asset Bubble: When an asset trades at a price that significantly deviates from its intrinsic value.

Asset bubbles are often difficult to observe in real-time (after all, if they weren’t it would be easy to avoid them) and are instead observed in retrospect after prices crash.

Examples: - 1600s: Tulipmania (single tulip sells for $60,000 in today’s dollars!)

- 1700s: South Sea bubble, Mississippi Bubble

- 1900s: Great Depression (NYC real estate prices down 67% in one quarter), Japan

- 2000s: Dot-com bubble (NASDAQ up 671% from Dec. 1994 to Mar. 2000, subsequently lost 78%, didn’t recover until April 2015), Real estate / global financial crisis

3FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Asset BubblesWhat are their impact?

At their core, asset bubbles lead to depressed future returns. Oftentimes, this is because the bubble pops.

4FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

$0.0

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2 Growth of $1 after all-time high Emerging MarketsReturn: -3.4% Volatility: 37.9%

TechnologyReturn: -1.2% Volatility: 27.9%

FinancialsReturn: -3.2% Volatility: 42.0%

Mortgage REITsReturn: -6.3% Volatility: 31.3%

Private EquityReturn: -5.1% Volatility: 36.4%

Emerging Markets represented by EEM and data is from October 2007 to April 2016. Financials represented by XLF and data is from June 2007 to April 2016. PrivateEquity represented by PSP and data is from June 2007 to April 2016. Mortgage REITs represented by REM and data is from June 2007 to April 2016. Technologyrepresented by XLK and data is from March 2000 to April 2016. Returns i nclude the reinvestment of dividends. Source: Yahoo! Finance. Calculations by NewfoundResearch. Past performance does not guarantee future results.

5

Takeaway:

Bubbles compress future asset returns.

“What the wise do in the beginning, fools do in the end”

FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

0

2

4

6

8

10

12

14

16

18

1953

1954

1956

1957

1958

1960

1961

1963

1964

1966

1967

1968

1970

1971

1973

1974

1975

1977

1978

1980

1981

1983

1984

1985

1987

1988

1990

1991

1992

1994

1995

1997

1998

2000

2001

2002

2004

2005

2007

2008

2009

2011

2012

2014

2015

10-Year Constant Maturity Treasury Rate

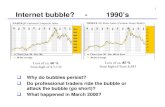

Are Bonds in a Bubble?Historical Bond Yields (Prices)

6FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

March 2016: 1.89%Full Period Average:

5.97%All-Time Low: 1.53%

Rates certainly remain near all-time lows and well below long-term averages.

Source: Federal Reserve Economic Data from the St. Louis Federal Reserve.

Nominal (including inflation) GDP growth is a good rough proxy for interest rate “fair value.”

Why?

- If the economy returns a rate higher than prevailing interest rates, then it makes sense for businesses to borrow and expand. This is a positive return proposition since returns are higher than borrowing costs. More demand for credit should eventually increase interest rates.

- If the economy returns a rate lower than prevailing interest rates, then borrowing to invest is a losing proposition. Credit demand will fall and the cost of borrowing (interest rates) will decline.

Are Bonds in a Bubble?Model for Bond Fair Value

7FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Bonds look to be moderately overvalued relative to nominal GDP growth.

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

1953

1954

1956

1957

1959

1960

1962

1963

1965

1966

1968

1969

1971

1972

1974

1975

1977

1978

1980

1981

1983

1984

1986

1987

1989

1990

1992

1993

1995

1996

1998

1999

2001

2002

2004

2005

2007

2008

2010

2011

2013

2014

Economic Growth vs. Interest Rates

YOY Nominal GDP Growth 10-Year Constant Maturity Treasury Rate

Are Bonds in a Bubble?Model for Bond Fair Value

8FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Dec. 2015 10-Year Rate: 2.2%GDP Growth: 3.1%

Source: Federal Reserve Economic Data from the St. Louis Federal Reserve. Calculations by Newfound Research.

9FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% 4.50% 5.00%Hypo

thet

ical

Ret

urn

on 1

0-Ye

ar C

onst

ant M

atur

ity

Trea

sury

Inde

x

Increase in 10-Year Interest Rates Over the Next Year

Are Bonds in a Bubble?Probably Not in The Traditional Sense

Increase to “Fair Value” in next year would lead to -7.7%.Rates would need to increase to above 6.5% for 30% loss.

Data Source: Federal Reserve Economic Data from the St. Louis Federal Reserve. Calculations by Newfo und Research. Assumes hypothetical 10-year Treasury bondthat pays interest annually and that the rate increase occurs in year one of the bond’s life. Numbers include the benefit from the interest payment in year one.

Interest Rates vs. Forward Bond ReturnsBut Perhaps a Bubble can be Painful Without Popping

10FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1953

1954

1956

1957

1959

1960

1962

1963

1965

1966

1968

1969

1971

1972

1974

1975

1977

1978

1980

1981

1983

1984

1986

1987

1989

1990

1992

1993

1995

1996

1998

1999

2001

2002

2004

2005

2007

2008

2010

2011

2013

2014

10-Year Constant Maturity U.S. Treasury Index (1953 to 2016)

Starting 10-Year Yield Subsequent 10-Year Return

Correlation = 0.93

Data Source: Federal Reserve Economic Data from the St. Louis Federal Reserve. Calculations by Newfound Research. Assumes hypothetical constant maturity 10-year Treasury bond i ndex that is rolled over every month. Retur ns include the reinvestment of interest. Index returns are hypothetical and do not reflect fees ortransaction costs. Past performance does not guarantee future results.

11

Takeaway:

Bonds don’t need to “pop” to disappoint.

“You don’t need to be a rocket scientist. Investing is not a game where the guy with the 160 IQ beats the guy with 130 IQ.”

FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

-5%

0%

5%

10%

15%

20%

25%

1953

.01

1954

.04

1955

.07

1956

.10

1958

.01

1959

.04

1960

.07

1961

.10

1963

.01

1964

.04

1965

.07

1966

.10

1968

.01

1969

.04

1970

.07

1971

.10

1973

.01

1974

.04

1975

.07

1976

.10

1978

.01

1979

.04

1980

.07

1981

.10

1983

.01

1984

.04

1985

.07

1986

.10

1988

.01

1989

.04

1990

.07

1991

.10

1993

.01

1994

.04

1995

.07

1996

.10

1998

.01

1999

.04

2000

.07

2001

.10

2003

.01

2004

.04

2005

.07

2006

.10

2008

.01

2009

.04

2010

.07

2011

.10

2013

.01

2014

.04

2015

.07

U.S. Equities (1953 to 2015)

U.S. Equities Earnings Yield Subsequent 10-Year Return

What About Equities?Earnings Yield vs. Future Equity Returns

12FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Correlation = 0.72

Data Source: Shiller data library (http://www.econ.yale.ed u/~shiller/data.htm). Calculations by Newfound Research. Earnings yield calculated as equity market earningsdividend by price. Index returns are hypothetical and do not reflect fees or transaction costs. Past performance does not guarantee future results.

Nowhere to Hide?U.S. Stocks and Bonds Both Historically Overvalued

13FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Stocks overvaluedBonds overvalued

Stocks undervaluedBonds overvalued

Stocks overvaluedBonds undervalued

Stocks undervaluedBonds undervalued

1999 to 20090.6% per year after inflation

1981 to 199110.5% per year after inflation

2015

Data Source: Shiller data library (http://www.econ.yale.ed u/~shiller/data.htm) and Federal Reserve of St. Louis. Calculations by Newfound Research. Data for the periodfrom 1953 to 2015. Cyclically Adjusted P/E Ratio is a version of the P/E ratio that averages earnings over the prior ten years. The 50/ 50 portfolio is a hypothetical indexthat is rebalanced annually. Index returns are hypothetical and do not reflect fees or transaction costs. Past performance does not guarantee future results.

Colors represent forward 10-year return on a 50/50 stock/bond portfolio. Darker orange indicates lower returns and darker green indicates higher returns.

-

5

10

15

20

25

30

35

40

45

50

0% 2% 4% 6% 8% 10% 12% 14% 16%

Cycl

ical

ly A

djus

ted

P/E

Ratio

10-Year Treasury Rate

Nowhere to Hide?U.S. Stocks and Bonds Both Historically Overvalued

14FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Expected Returns from Research Affiliates

U.S. Large Cap Stocks U.S. Core Bonds 60/40 U.S.

Stock/Bond Portfolio

Yield 2.2% 0.8% 1.6%

Growth 1.3% 0.8%

Roll Return 0.7% 0.3%

Credit Loss -0.3% -0.1%

Valuation -2.2% -0.4% -1.5%

FX 0.0%

10 Yr. Expected Real Return 1.3% 0.8% 1.1%Source: Research Affiliates. Data as of 3/31/16. Expected returns are calculated by Research Affiliates using data from MSCI, Bloomberg, and Barclays. Theseforecasts are forward looking statements based upon the reasonable beliefs of Research Affiliates and are not a guarantee of future performance. This content is notinvestment or tax advice.

15

Takeaway:

Value matters.

“Price is what you pay; value is what you get.”

FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Nowhere to Hide?Expand Your Horizons, Especially With High Income

16FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

-1%0%1%2%3%4%5%6%7%8%9%

10-Year Expected Real Returns from Research Affiliates

Source: Research Affiliates. Data as of 3/31/16. Expected returns are calculated by Research Affiliates using data from MSCI, Bloomberg, and Barclays. Theseforecasts are forward looking statements based upon the reasonable beliefs of Research Affiliates and are not a guarantee of future performance. This content is notinvestment or tax advice.

Nowhere to Hide?Expand Your Horizons, Especially With High Income

17FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Expected Returns from Research Affiliates

60/40 U.S. Stock/Bond Portfolio Diversified

Yield 1.6% 2.3%

Growth 0.8% 0.2%

Roll Return 0.3% 0.6%

Credit Loss -0.1% -0.5%

Valuation -1.5% -0.5%

FX 0.0% 0.5%

10 Yr. Expected Real Return 1.1% 2.7%Source: Research Affiliates. Data as of 3/31/16. Expected returns are calculated by Research Affiliates using data from MSCI, Bloomberg, and Barclays. Theseforecasts are forward looking statements based upon the reasonable beliefs of Research Affiliates and are not a guarantee of future performance. This content is notinvestment or tax advice. The diversified portfolio consists of a 12.5% allocation to U.S. large-cap equities, a 7.5% allocation to EAFE equities, a 5% allocation to EMequities, a 5% allocation to long-term Treasuries, a 10% allocation to U.S. core fixed income, a 10% allocation to global core fixedincome, a 5% allocation to REITs, a 5% allocation to U.S. TIPS, a 10% allocation to high yield, a 10% allocation toUSD EM bonds, a 10% allocation to local currency EM bonds, and a 10% allocation to bank loans.

18

Takeaway:

Opportunity exists globally and in high income asset classes.

“You can get in a whole lot more trouble in investing with a sound premise than with a false premise.”

FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

This document (including the hypothetical/backtested performance results) is provided for informational purposes only and is subject to revision. This document is not an offer to sell or a solicitation of an offer to purchase an interest or shares (“Interests”) in any pooled vehicle. Newfound does not assume any obligation or duty to update or otherwise revise information set forth herein. This document is not to be reproduced or transmitted, in whole or in part, to other third parties, without the prior consent of Newfound.

Certain information contained in this presentation constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of an investment managed using any of the investment strategies or styles described in this document may differ materially from those reflected in such forward-looking statements or in the hypothetical/backtested results included in this presentation. The information in this presentation is made available on an “as is,” without representation or warranty basis.

There can be no assurance that any investment strategy or style will achieve any level of performance, and investment results may vary substantially from year to year or even from month to month. An investor could lose all or substantially all of his or her investment. Both the use of a single adviser and the focus on a single investment strategy could result in the lack of diversification and consequently, higher risk. The information herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. You should consult your investment adviser, tax, legal, accounting or other advisors about the matters discussed herein. These materials represent an assessment of the market environment at specific points in time and are intended neither to be a guarantee of future events nor as a primary basis for investment decisions. The hypothetical/backtested performance results and model performance results should not be construed as advice meeting the particular needs of any investor. Past performance (whether actual, hypothetical/backtested or model performance) is not indicative of future performance and investments in equity securities do present risk of loss. The ability to replicate the hypothetical or model performance results in actual trading could be affected by market or economic conditions, among other things.

Investors should understand that while performance results may show a general rising trend at times, there is no assurance that any such trends will continue. If such trends are broken, then investors may experience real losses. No representation is being made that any account will achieve performance results similar to those shown in this presentation. In fact, there may be substantial differences between backtested performance results and the actual results subsequently achieved by any particular investment program. There are other factors related to the markets in general or to the implementation of any specific investment program which have not been fully accounted for in the preparation of the hypothetical/backtested performance results, all of which may adversely affect actual portfolio management results. The information included in this presentation reflects the different assumptions, views and analytical methods of Newfound as of the date of this presentation.

19

Disclosures

FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.

Performance during the backtested period is not based on live results produced by an investor’s actual investing and trading, but was achieved by the retroactive application of a model designed with the benefit of hindsight, and is not based on live results produced by an investor’s investment and trading, and fees, expenses, transaction costs, commissions, penalties or taxes have not been netted from the gross performance results except as is otherwise described in this presentation. The performance results include reinvestment of dividends, capital gains and other earnings. As the information was backtested, it does not reflect contemporaneous advice or record keeping by an investment adviser. Actual, live client results may have materially differed from the presented performance results.

The Hypothetical Information and model performance assume full investment, whereas actual accounts and funds managed by an adviser would most likely have a positive cash position. Had the Hypothetical Information or model performance included the cash position, the information would have been different and generally may have been lower. While Newfound believes the outside data sources cited to be credible, it has not independently verified the accuracy of any of their inputs or calculations and, therefore, does not warranty the accuracy of any third-party sources or information.

All investing is subject to risk, including the possible loss of the money you invest. Diversification does not ensure a profit or protect against a loss. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income.

These materials represent an assessment of the market environment at specific points in time and are intended neither to be a guarantee of future events nor as a primary basis for investment decisions. The performance results should not be construed as advice meeting the particular needs of any investor. Neither the information presented nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any security. Past performance is not indicative of future performance and investments in equity securities do present risk of loss. Newfound Research LLC’s results are historical and their ability to repeat could be affected by material market or economic conditions, among other things.

This document contains the opinions of the managers and such opinions are subject to change without notice. This document has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. This document does not reflect the actual performance results of any Newfound investment strategy or index. The investment strategies and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation.

No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission from Newfound Research.

© Newfound Research LLC, 2016. All rights reserved.

20

Disclosures

FOR ADVISOR USE ONLY. NOT FOR PUBLIC DISTRIBUTION.