April 16th 2016 The 1.2 billion opportunity€¦ · · 2017-11-29BUSINESS IN AFRICA The 1.2...

15

April 16th 2016 SPECIAL REPORT BUSINESS IN AFRICA The 1.2 billion opportunity

Transcript of April 16th 2016 The 1.2 billion opportunity€¦ · · 2017-11-29BUSINESS IN AFRICA The 1.2...

April 16th 2016

S P E C I A L R E P O R T

B U S I N E S S I N A F R I C A

The 1.2 billionopportunity

20160416_SRBusinesInAfrica.indd 1 04/04/2016 13:48

The Economist April 16th 2016 1

BUSINESS IN AFRIC A

SPECIAL REPOR T

A list of sources is atEconomist.com/specialreports

An audio interview with the author is atEconomist.com/audiovideo/specialreports

CONTENT S

3 The middle classA matter of definition

5 ManufacturingNot making it

6 Exporting flowersComing up roses

7 TradeObstacle course

9 Doing businessIs it worth it?

10 DiasporasSettled strangers

11 Financial technologyOn the move

12 E-commerceVirtual headaches

13 ProspectsFortune favours the brave

1

FOR A LOOK at the African boom at its peak, do as a multitude of foreigninvestors have done and fly into Abidjan, the capital of Ivory Coast. Visi-torsarrive in an air-conditioned hall where a French-style café sellsbeers,snacks and magazines. There is advertising everywhere, for mobile-phone companies, first-class airline tickets and a new Burger King. Thetaxi into the city smoothly crosses over a six-lane toll bridge. On the wayto the Plateau, the city’s commercial core, cranes, new buildings and bill-boards jostle for space on the skyline. In the lagoon, red earth piles upwhere yet another new bridge is under construction.

Just five years ago, Ivory Coast seemed like a lost cause. Havingbeen defeated in an election at the end of 2010, the then president, Lau-rent Gbagbo, refused to leave office. The victorious opposition leaderandnow president, Alassane Ouattara, mounted a military offensive to forceMrGbagbo out. French troops seized the airport to evacuate their citizens(the country used to be a French colony). Protesters were gunned downby troops, foreign businesses were looted and human-rights activistsgave warning about mass graves being dug.

Ivory Coast still has problems, as shown by a terrorist attack inMarch that killed 22 people. But its economy is the second-fastest-grow-ing in Africa (after Ethiopia, which is much poorer), expanding by almost9% per year. Foreign investment is pouring in. As well as the Burger King,Abidjan now has a Carrefour supermarket, a new Heineken brewery, aPaul bakery and plenty of new infrastructure. Sharp-suited, French-edu-cated ministers explain in perfect English what they are doing to “openup”, “improve the ease of doing business” and “sustainably grow themiddle class”. Expensive hotels, such as the reopened $300-a-nightIvoire, are booked up; their bars are full of affluent people striking deals.The country’s three port terminals, the biggest of which is being expand-

1.2 billion opportunities

The commodity boom may be over, and barriers to doing businessare everywhere. But Africa’s market of 1.2 billion people stillholds huge promise, says Daniel Knowles

ACKNOWLEDGMENT S

Apart from those mentioned in thetext, particular thanks for their helpin preparing this report are due toMamadou Diallo, Isidore Kouadio,Zoe Flood, Mairead Cahill, FeyiFawehinmi, Adekunle Adebiyi andNicolas Tesserenc.

2 The Economist April 16th 2016

SPECIAL REPOR TBUSINESS IN AFRIC A

2

1

ed by Bolloré, a French industrial firm, areworking at full capacity, importing carsand electronics and exporting cocoa, cof-fee and cashew nuts.

This is the Africa of business maga-zines and bank ads: a continent that is ris-ingat a prodigious pace and creating prof-itable new markets for multinationalfirms. But Abidjan also has plenty of re-minders that it has been here before. Forall of the new buildings springing up, itsimpressive skyline is still dominated bycrumbling1960s and 1970s concrete mod-ernism. The roads may be new, but theorange taxis that ply them are still ancientfume-spewingToyota Corollas, remnantsof an earlier boom. For the two decadesafter independence from France in 1960,Ivory Coast enjoyed an economic mir-acle. Then, quite suddenly, the price ofco-coa and coffee plunged and the boomfaded as quickly as it had begun.

Reasons to worryThe deepest fearoftoday’s investors

in Africa is that it may be happeningagain. In Ivory Coast’s neighbour, Ghana,thousands of government workers havebeen marching in the streets in the pastfew months to protest against their risingcost of living. Ghana relies on oil andgold, both of which have fallen in price,as well as cocoa. That, plus prodigiousgovernment borrowing, has caused a crisis. One US dollar nowbuys 4 cedi, the local currency; in 2012, it bought not quite two.Growth has halved since 2014, and Ghana is running a budgetdeficit of9% ofGDP and a current-account deficit of13%.

According to the World Bank, in the year to April last yearthe terms of trade deteriorated in 36 out of 48 sub-Saharan Afri-can countries as the price oftheir commodity exports fell relativeto the cost of their imports, mostly manufactured goods. Those36 countries account for 80% of the continent’s population and70% of its GDP. Eight countries, including two giants, Angola andNigeria, derive more than 90% of their export revenues from oil,which has recently plummeted far below the price needed todraw in new investors. Growth across sub-Saharan Africadropped to 3.7% in 2015, far below East Asia’s 6.4% and nowhere

near enough to create enough jobs for the continent with theworld’s youngest and fastest-growing population. The WorldBankexpects it to tickup again, but only to 4.8% in 2017.

Countries that happily borrowed from international inves-tors over the past few years have now found themselves shut outof the markets. The stock of outstanding sovereign bonds in theregion had risen from less than $1 billion in 2009 to over $18 bil-lion in 2014. If growth continues at a decent clip, that should bemanageable. But if it stops, interest ratesof10% ormore on dollar-denominated bonds will make refinancing difficult.

The continent’s two biggest economies, Nigeria and SouthAfrica, are already in deep distress. The reasons are different, butboth have suffered from commodity-price falls as well as fromatrocious economic management. The IMF, although loathed inmuch of Africa, is back, providing a $ 1billion loan to Ghana andpreparing another for Zambia. Some fear a return to 2000, whenthis newspaper described Africa as the “hopeless continent”.

Yet despite that, Nairobi’s thriving malls and Abidjan’shumming ports show that there are plenty of reasons to stay op-timistic. The economic conditions have got worse, but this is avery different continent from two decades ago, when troopsfrom eight African countries were fighting in Congo alone. Warsstill rage in South Sudan, Somalia, Mali and northern Nigeria,and violence bubbles in places like eastern Congo, the CentralAfrican Republic and Burundi. But broadly speaking, most ofsub-Saharan Africa is now peaceful. Elections seem increasinglyless likely to result in strife, even if they still generally return in-cumbents, and more and more often for unconstitutional thirdterms. The governments that come to power are still often cor-rupt and inefficient, but far less brazenly so than those of coldwar despots such as Mobutu Sese Seko of Congo or Jean-BedelBokassa of the Central African Republic.

NAIROBI IS MANY cities in one. In tourist brochures, it is apleasant, laid-back colonial city where you can see giraffes

and lions in the national park before relaxing with a gin andtonic on a verandah. In the literature produced by NGOs andcharities, it suffers from overcrowded slums and brutal crime.But in investors’ pamphlets it is a city ofmalls and highways. Thelatest temple to consumerism, Garden City, just off a new eight-lane motorway, opened in May last year. Inside, well-dressedKenyans enjoy fast food and buy jewellery. The view from theroof-top car park, where SUVs wait under solar-panelled shades,is of terracotta-tiled new suburban houses in all directions.

The mall is the signature investmentofActis, one of Africa’sbiggest private-equity firms. At one end a branch of Game, aSouth African chain now part-owned by Walmart, sells refriger-ators, televisions and everything else needed to furnish those

new semi-detached houses. At the other, an enormous super-market, Nakumatt, sells food to put in the freezers. Duplex apart-ments built alongside it sell for as much as $600,000. It is a pow-erful symbol of investors’ confidence in the emergence ofa largemiddle class in Africa.

And yet across the continent that confidence has taken aknock over the past year or so. Following the collapse in com-modity prices, some are beginning to wonder whether much ofthe apparent growth of a consuming class was simply a productof oil and metals money flowing into the economy. In a part ofthe world where statistics are scarce, and those that exist are of-ten suspect, investorsare nowtryingto decide whether a new, af-fluent class ofconsumers really is emerging.

The fried-chicken testThe idea of such an African middle class, as distinct from

the super-rich, has captured businesspeople’s imagination for atleast a decade. In 2011 the African Development Bank (AfDB)published a report claiming that the middle class at that timenumbered 350m people, or 34% of Africa’s population. In the in-tervening five years, businesspeople across the continent haveused that figure to talkup their prospects.

However, the definition used by the AfDB is very broad. Toreach its figure of 350m, it defined the middle class to include a“floating class” ofpeople earning between $2 and $4 a day. Its de-finition of the middle class proper was of people earning $4 to$20 a day. The sort of people who make the Garden City mallprofitable—the sort who can afford to spend $10 on a fried-chick-en lunch, or $200,000 on a new apartment—would come fromthe top end of what the AfDB called its “rich” category. Theymade up less than 5% of the total African population.

Other studies that have appeared since the AfDB reporthave been more sceptical. In 2014 South Africa’s Standard Banksurveyed 110m households in 11African countries and concludedthat “Africa’s middle class is rising swiftly,” but came up with farmore modest numbers. Using a South African measure of livingstandards that defines middle-class households as those withannual incomes of$5,500 or more, it found that only14% fell intothat category. It also found that by far the fastest growth had beenin oil-rich Nigeria and Angola, where itmaywell tail off now. An-other survey published last year by Pew, an American pollingfirm, found that although poverty in Africa had fallen dramati-cally, “few countries had much ofan increase in the share of mid-dle-income earners” in the decade to 2011.

Such figures help explain why some of the most exuberantboosterism about Africa has deflated. Indeed, some now won-

The middle class

A matter of definition

Who are Africa’s affluent consumers?

The Economist April 16th 2016 3

BUSINESS IN AFRIC A

2

1

Africa’s1.2 billion people also hold plenty ofpromise. Theyare young: south of the Sahara, their median age is below 25everywhere except in South Africa. They are better educatedthan ever before: literacy rates among the young now exceed70% everywhere other than in a band of desert countries acrossthe Sahara. They are richer: in sub-Saharan Africa, the propor-tion ofpeople living on less than $1.90 a day fell from 56% in 1990to 35% in 2015, according to the World Bank. And diseases thathave ravaged life expectancy and productivity are being defeat-ed—gradually for HIV and AIDS, but spectacularly for malaria.Some of the gains may seem modest, but given that living stan-dards across Africa declined during the 30 years after indepen-dence they are sufficiently established to prove lasting.

And forall that oil and metals have come to dominate econ-omies such as Nigeria’s and Congo’s, the boom broadened be-yond natural resources. Mobile telephones have transformedcommerce across Africa, and now smartphones and featurephones (which are halfwaybetween dumb and smart) are takinghold. In 2014, the latestyearforwhich figuresare available, 27% ofNigerians owned a smartphone. In many African countries 4G

mobile-phone infrastructure is the only thing that works well,but it works at least as well as in much richer countries, and a lotcan be built on it. What began with mobile-money systems suchas Kenya’s M-Pesa is now branching into bank accounts, savingsaccounts, loans and insurance. That in turn is helping people riseout ofpoverty and invest in their future.

This special report will argue that despite some deep andentrenched problems, African businesses offer hope too. It isclearly risky to make sweeping judgments about an entire conti-nent with 54 countries and 2,000 languages. This report drawson visits to various countries in sub-Saharan Africa, but four inparticular: South Africa, Nigeria, Kenya and Ivory Coast, allcoastal, urbanised and relatively rich. They certainly do not rep-resent the whole of Africa, but your correspondent picked thembecause they each illustrate a different aspect of business acrossAfrica as a whole. The businesses covered have not yet trans-formed the continent, but they show that African firms are capa-ble ofextraordinary innovation—ifonly they can be set free. 7

SPECIAL REPOR T

4 The Economist April 16th 2016

SPECIAL REPOR TBUSINESS IN AFRIC A

2 der whether African consumers will everbecome a profitable market. “We thoughtthis would be the next Asia, but we haverealised the middle class here in the re-gion is extremely small and it is not reallygrowing,” said Cornel Krummenacher, aNestlé executive, in an interview with theFinancial Times last year. In 2014 Cadburyclosed its chocolate factory in Nairobi, im-porting its products from Egypt and SouthAfrica instead. Last September Diageo, abig drinks firm, announced it was invest-ing in selling more Guinness beer in Nige-ria, quietly giving up on a plan to push itsexpensive vodka and whisky. And eventhose sales of Guinness are falling shortof its hopes.

Yet many investors plough on.Koome Gikunda, a director of Actis, theprivate-equity firm that built Garden City(pictured), says that there most definitelyis a middle class affluent enough to shopat the mall. In the absence of good censusdata, the company conducted its ownrough market research to gauge its size.“We hired a firm who flewover the area ina plane and literally counted TV satellitedishes,” he explains. They concluded thatperhaps as much as a third of their catch-ment area of 1m people could afford toshop at the mall. So far, the firm’s hopesseem to have been vindicated. The 220flats they built alongside the mall sold outin four months. And even on a weekday afternoon the shops arefar from deserted.

The Mara Group, a conglomerate founded by Ashish Thak-kar, a British-born Asian-African businessman (see article ondiasporas later in this report), is also investing in African malls.CFAO, a French firm, plans to construct dozens of malls in eightAfrican countriesover the nextdecade; ithas justopened the firstin Abidjan. And in many African capitals new housing estatesare going up to cater for families with two children and one car.Though in most African countries it is mainly ancient second-hand Toyotas and Peugeots that ply the roads, cardealerships arefull of newer models, and radio stations advertise loans to buy

them with. Are all these firms holding their hopes too high?One plausible explanation for their enthusiasm is that Afri-

ca’s population is so large, and its middle class was so minisculeto begin with, that even modest growth is providing enormousinvestment opportunities. In Ethiopia, where according to Stan-dard Bank 99% of the population are still poor, the middle classhas nonetheless grown tenfold over the past decade or so. Thatmeans a lot more people who buy beer, so in 2014 Heinekenopened a new brewery there, its third in the country. Anotherpossibility is that there has always been money around but itwas goingabroad. SirPaul Collier, an academic at Oxford univer-sity, estimates that in 1990 about 40% ofAfrica’s wealth was held

outside the continent. Thanks to the relative political stability ofthe past two decades, much of that wealth is now returning, andbeing invested in property and African businesses.

But the most probable cause of the optimism is that al-though Africa’s middle class may be small as a proportion of thetotal population, it really is growing fast in the big cities, which iswhere the foreign investors are putting their money. The WorldBank reckons that by 2050 well over half of the continent’s pop-ulation will live in urban areas. Nairobi’s population, which wasabout 3m at the most recent census in 2009, is growing at 5% peryear, halfas fast again as that ofKenya as a whole. The city’s mid-dle-class population needs to grow only slightly faster than the

average to need a bignewmall every year.And even the poor spend money. Theymay not shop at malls but they do buythings like washing powder, processedfood and mobile-phone credit.

In a report published last year Price-waterhouseCoopers, a big consultancy,argued that the best opportunities in Afri-

ca are in cities, because that is where the infrastructure spendinggoes. In big cities, the report said, there is a “constant rise in dis-cretionary spending of a kind that did not exist even a decade ortwo ago…we can safely say it is the result of Africa’s rapidly ex-panding urban middle classes.” Such cities concentrate consum-ers; they also attract returning diaspora Africans.

What would make them expand even faster is industrial-isation. This could replace some imports, as well as provide theforeign exchange needed to pay for the rest. Unlike mining, mak-ing basic things needs lots of people, so the wealth generatedwould be spread widely. But manufacturing in Africa has neverbeen easy, and in some places it is getting harder. 7

Enough customers to go round

Africa’s population is so large, and its middle class wasso miniscule to begin with, that even modest growth isproviding enormous investment opportunities

The Economist April 16th 2016 5

BUSINESS IN AFRIC A

1

BASHIR DANYARO STANDS in dismay in his shoe factoryin Kano, northern Nigeria’s biggest city. In its heyday,

around 15 years ago, up to 200 women operated rows of sewingmachines producing footwear for soldiers and schoolchildren.Now the place is silent and covered in a layer of dust. It has beenalmost two years since the last decent contract came in, Mr Da-nyaro says. Dozens ofhis local competitors have closed up shop;his flailing business is flanked by a deserted leather tannery anda shuttered ceramics plant.

Nigeria’s deindustrialisation is perhaps more visible in thispart of the country than anywhere else. The Sahelian north hasfine leather and agricultural supplies, but its factories are fallinginto disrepair. A once-thriving textile industry is all but extinct.“It’s not profitable. But what else will I do?” asks Mr Danyaro.“This is the only business I know.”

Three thousand miles to the south, in a suburb of Pretoria,South Africa’s capital, things seem better. At the Nissan factorynear Rosslyn, workers in grey overalls and white face masks as-semble pickup trucks. This factory is probably more sophisticat-ed than anything else on the continent, yet it, too, is struggling. Itcurrently produces around 185 pickup trucks a day, mostly for thestagnant South African domestic market. With another shift itcould more than double its output, but managers at the factorygrumble that their bosses in Japan do not want to make full useof their investment.

Manufacturing in Africa is only for the brave. In Nigeria itmakes up about10% ofGDP, according to official statistics, whichmay not be reliable. In South Africa, a far more developed econ-omy, it accounts for13% ofGDP, down from a fifth in 1990. In Thai-

land the equivalent figure is28%. Between 1970 and 2013,says the Brookings Institution,an American think-tank, Afri-ca’s share of global manufac-turing output fell from 3% to2%; as a share of sub-SaharanAfrica’s GDP, manufacturinghas shrunk from almost 20%to about half that. Almost theentire output is for domesticconsumption, not export.

Even though labour isgenerally cheap, making stuffcan be more expensive thanin parts of Europe because ofpoor infrastructure, powerfultrade unions (in South Africa)and pervasive corruption. There is almost nothing like China’selectronics factories or Bangladesh’s textile sweatshops. Every-thing from cornflakes to kettles is imported from Europe or Asia.

Africa boosters say that the fall in commodity prices is adose ofnastybutnecessarymedicine. The waytheysee it, fallingcurrencies will drive up the cost of imports, and governmentswill have to open up to investment and reduce regulation andcorruption in order to increase taxrevenue��et this scenario is fartoo rosy. South Africa and Nigeria are not entirely representativeof the rest of Africa, but together they make up roughly half ofsub-Saharan Africa’s GDP and give some idea of the challengesthe region faces.

PowerlessThe biggest immediate problem is power. Nigeria, which

alone accounts for a third of sub-Saharan Africa’s GDP, has just3,000MW of on-grid power-generating capacity, less than NorthKorea. Mr Danyaro says he gets four hours of power a day atmost. Most factories have to rely on diesel generators to keep go-ing. A new tomato-processing facility belonging to the DangoteGroup, a huge Nigerian conglomerate owned by Africa’s richest

man, has had to import two enormousgenerators which together produce about2MW of electricity. “Every hour they use400 litres of diesel,” says Alhaji Keita,who manages the plant. “It’s by far ourbiggest overhead.” Even the diesel ismostly imported: despite its oil wealth,Nigeria has very little refining capacity.

World Bank figures show that theamount of power consumed per personin Africa has fallen in recent decades be-cause generating capacity has not kept upwith population growth. With 1.2 billionpeople, the continent has a sixth of theworld’s population but only 3% of its gen-erating capacity, which is heavily concen-trated in justa fewcountries. In places likeZambia and Malawi, most of the existingcapacity comes from hydroelectric plantsbuilt in colonial times or shortly after in-dependence, which often do not run inthe dry season. South Africa has manycrumbling power stations from the 1960sthat have not been upgraded or replaced,so people in its big cities suffer blackoutsand factories often come to a halt.

Manufacturing

Not making it

A successful manufacturing sector requires manythings that Africa lacks

Thin on the ground

SPECIAL REPOR T

6 The Economist April 16th 2016

SPECIAL REPOR TBUSINESS IN AFRIC A

2

1

AROUND THE EDGES of Lake Naivasha, underthe shadow of a dormant volcano, Mt Longo-not, one of Kenya’s most successful exportbusinesses of recent years has become estab-lished. All around the lake, and off dirt roadsthat lead from it, are acres and acres of plas-tic tenting in which flowers of all sorts, butespecially roses, are grown for export. At thebiggest operators, thousands of workers goin each day to water, feed, pick and preparethe crop. On average, 360 tonnes of flowersare flown out of Nairobi airport every day,mostly to Europe but also to Asia and theMiddle East. Kenya is the world’s third-largest producer of cut flowers; the crop is itssecond-largest export, after tea. Since 1988the industry has grown more than tenfold.

Africa’s global share of agriculturalexports, as of manufactured exports, hasdeclined in the decades since independence,from over 8% in the 1970s to just 2% in 2009.Nigeria used to be the world’s biggest pro-ducer of palm oil; Ghana of cocoa; and Kenyaand Ethiopia of coffee. All have now beenovertaken by other regions. Yet the plastic-roofed greenhouses of Kenya’s flower farmsare the closest thing the country has to anAsian-style high-tech manufacturing cluster.

Growing flowers and vegetables is acompetitive business, says Mark Low, theboss of Groove Flowers, one of the smalleroutfits around Lake Naivasha. “The marginsare getting smaller and smaller.” Colombia,Ecuador and Ethiopia are all chasing thesame customers. But many of Kenya’s grow-ers are hoping to do better by running ahighly sophisticated operation. Mr Low, anearthy white Kenyan, mostly grows roses,bouvardia and delphiniums. He does not sellto supermarket suppliers because the pricesthey pay do not give him a decent margin.Instead, he goes to a lot of trade fairs to findout what Russian oligarchs will order for theirdaughters’ weddings.

Fashions keep changing, so Mr Low

experiments a great deal. Walking through agreenhouse full of spray roses, with severalflowers growing on one stem, he explainsthat these are much harder to grow than thesingle-flower variety but can fetch higherprices from florists. Sadly, so far they havenot done as well as he had hoped because thedrop in the rouble is making for less lavishwedding budgets. A lot of other factors alsohave to be taken into account. For example, ifa flower is particularly heavy, it may not beworth growing even if it fetches good prices,because air freight is very expensive. Fragileflowers are no good either, because they willget shaken up on his rutted dirt roads.

Flower farming, then, is a bit likefast-fashion manufacturing. To thrive, itneeds an educated workforce; effective, butnot onerous, regulation; good access; adecent airport nearby; and plenty of electric-ity. Indeed, after air freight and labour,power is the main cost: flowers need plenty of

Coming up roses

Kenya’s flower-export business is a rare success

light and carefully controlled air and watersupplies. The industry has settled aroundNaivasha because the area’s volcanic terrainis home to several geothermal power sta-tions, the lake provides water and the airportis not far away. Other parts of Kenya are notso well provided for.

Africa’s agricultural productivity hasimproved immensely over the past decade.Between 2000 and 2013, output of cerealsgrew by 3.3% a year, faster than in any otherregion. But turning farming into a thrivingexport business and a big employer providingwell-paid jobs is harder. In Kenya, flowersmay have bloomed, but production of coffee,a more traditional export, has collapsed,falling from almost 100,000 tonnes a year in2000 to below 40,000 in 2013. Many coffeefarms have succumbed to foreign competi-tion or been swallowed up by housing devel-opment. The success of Kenya’s flower farmswill not easily be replicated by other crops.

Heading for a Russian wedding

Poor roads are another problem. Suleiman Umar owns afactory in Kano that makes relief blankets on ancient-lookinglooms. But only ten of the 68 machines are currently working,and that is not bad for a textile business in Nigeria, he says. Itcostshim more to transporta container from coastal Lagos than itdoes to ship one all the way from China. Even in South Africa,where rail and road connections are generally good, the vast dis-tances make it expensive to move anything across the country.

But fixing these fundamental problems is hard, so many Af-rican countries have tried to foster manufacturing through pro-tectionism. In Nigeria the new government of Muhammadu Bu-

hari has tried to stimulate local production by banning the use offoreign exchange for a list of items including toothpicks andglass. That comes on top oftotal import bans on products such ascloth from China and punitive tariffs on imports of new cars. InSouth Africa, the car industry is sheltered by a 20% tariff on im-ports ofnew cars and an outright ban on importing used cars.

In some ways, this has spurred production. Without the ta-riffs, South Africa’s car industry would have had a harder time.Nigeria became self-sufficient in cement after the governmentruled that only manufacturers could ship it in. At the Dangotegroup’s biggest cement plant, an enormous site looming over the

The Economist April 16th 2016 7

BUSINESS IN AFRIC A

2

1

IT WAS MIDDAYwhen the lorry on which your correspon-dent had hitched a ride pulled out of the factory yard in Yo-

pougon, an industrial suburb ofAbidjan, Ivory Coast’s commer-cial capital. By 7pm, when it reached Bouaké, the second-biggestcity, the driver had been stopped by police nine times and paidseven bribes. And that was the easy part of the six-day journeytaking a cargo of carpets across bumpy, bandit-infested roads toOuagadougou, capital ofnext-door Burkina Faso.

Ivorian ministers give the impression that trade in west Af-rica should be going swimmingly. “We want Ivory Coast to be ahub for the region, we want our goods to go through the countryto Burkina Faso, to Mali, to all of our neighbours,” says Abdou-rahmane Cissé, the country’s budget minister and a formerGoldman Sachs banker. On the face of it, the region seems wellintegrated. Ivory Coast shares its currency, the CFA franc, with itsnorthern neighbours. It belongs to a customs union, UEMOA,that is older than the European Union. Yet according to IMF fig-ures, in 2014 trade between Ivory Coast and Burkina Faso wasworth just €376m, or a mere 2% of Ivory Coast’s total trade.

What is true of Ivory Coast is true ofmuch of the continent.Last year 26 African countries signed an agreement to create a“Tripartite Free Trade Area”, combining the existing eastern andsouthern African trade blocs into one. That ought to be a hugeboon for a continent divided by arbitrary colonial borders. Yetthe trade figures suggest that African cities are mostly not hubs;rather, they are islands with ports. According to the United Na-tions, merchandise trade within the continent made up just 11%of Africa’s total trade between 2007 and 2011. In Asia, intra-con-tinental trade was 50%; in Europe, 70%.

This lack of internal trade helps explain why Africa re-mains poor, and why it has failed to create big firms that straddlenational boundaries. Even though the sub-Saharan part of thecontinent contains overa billion potential customers, in reality itis made up of lots of small markets, each of which has to be con-quered individually. That is what prompted The Economist tohitch a ride with a lorry driver and his brother to get a sense ofthe true barriers to trade, going north from Abidjan via Ferkessé-

Trade

Obstacle course

Africa’s trade suffers from dismal infrastructure, lackof investment and corruption

scrubland of the central Kogi state, managers admit that theywould never have been able to compete under less shelteredconditions. And the profits have allowed Mr Dangote to invest inother businesses, such as his new tomato-canning factory.

But the main industry that thrives thanks to Nigeria’s tradebarriers is corruption. In a Kano hotel, a gap-toothed smugglerexplains that his syndicate has spent a decade manoeuvring fab-ric, rice, pasta and vegetable oil to huge warehouses in Kano viaBenin and Niger. “The official process is tedious and expensive.�ou have to deal with customs, immigration, security, and it

takes so long,” he says in the local Hausa language. “We organisethe illegal route so the products come successfully.” Up to 50 con-tainers might cross the Jibia border post at once, he says, eachyielding a profit ofup to 5 million naira ($15,000). In Lagos’s mar-kets, “west African” fabric is invariably imported from China.The cars on its roads often arrive after being “lost” in transit to Ni-ger, without payment ofNigeria’s hefty duties on imported cars.

And although trade barriers are helpful for those who areprotected, theyhurtotherbusinesses. MrDangote hasmore than60% of Nigeria’s cement market, a near-monopoly. “He has cor-nered the market. He has access to the limestone deposits. He is afriend of every government, he gets cheaper loans and he getstax holidays. Which other business gets that?” says OluseunOnigbinde, founder of BudgIT, a Lagos-based fiscal-analysisgroup. Last year Dangote, which makes one of the world’s mostbasic products, had a profit margin of53%.

In South Africa smuggling is less of a problem, but policy islittle better. The Nissan car factory is one of seven in the country.Broadly defined, the car industry makes up 30% of manufactur-ing output. Demand for cars of all sorts is soaring across the con-tinent, yet South Africa’s huge potential is being wasted by a tox-ic combination of power cuts and poor labour relations. At theNissan factory, stickers plastered all over the machinery encour-age workers to vote for “strong shop stewards to confront thebosses”. Last year a strike shut the plant down for two months.For historical reasons, managers in the car factories tend to bewhite and workersblack. Disputesare politicised, confrontation-al and frequent. Relative to their productivity, South African in-dustrial workers are some of the most expensive in the world. Acheap rand should help, by lowering the cost of labour (althoughit may also raise inflation, which could induce more strikes). Butit would take a fundamental change in South Africa’s rigid la-bour laws to create jobs for the one in four South African adultswho are unemployed.

A local flavourIn the meantime, the best hope comes from locals, who

know how the system works, and from products sold locallyrather than across borders. At Wilson’s Juice, a new factory at theedge of Lagos, lemonade is being bottled on an assembly linemanned by 16 people. On the other side of the room workerschop up pineapples. The business was started by Seun and SeyiAbolaji, two brothers who were raised and educated in Americaand returned to Nigeria, to the bemusementoftheir families. Themarginsare good and the firm isexpandingquickly. The onlyma-terials that have to be imported from outside Africa are for thebottles and the labels, so the shortage of foreign exchange hasnot hurt too much. “A lot of people are apprehensive, but we aresuper-excited. For people who source their own materials local-ly, now is a great time to grow,” says Seyi.

Growth could be speeded up if foreign investors werebuilding factories, too. If this were done on a large scale, as inAsia, it could create millions of export-related jobs. Huge obsta-cles need to be overcome before that can happen. But efforts toimprove Africa’s dire trade links should help. 7

SPECIAL REPOR T

8 The Economist April 16th 2016

SPECIAL REPOR TBUSINESS IN AFRIC A

2

1

dougou, a rough Ivorian border town, towards Ouagadougou. After a couple of hours of waiting for paperwork, with Mi-

chael Jackson blaring through the speakers, the lorry pulled outonto a new, wide, fast-moving road. At the end of 2013 a new tollroad opened that goes all the way from Abidjan to Yamous-soukro, the grandiose official capital that Ivory Coast’s post-inde-pendence president, Félix Houphouët-Boigny, built around hishome town in the 1980s. The road was, as an expat businessmanhad predicted, “like driving in Europe”. As the driver, SounkaloOuattara, revved the engine, he explained that only a few yearsago the 220km journey t��amoussoukro could take six or sevenhours. Now, on the six-lane highway, even a heavily laden lorrycan do it in three.

The good road comes at a cost, though. The official tolls arefairly modest: 5,000 CFA francs, or about $10, for a lorry to travelall the way. But that is only the start. “

�ou have to pay everyone,

even the national-park rangers, you have to pay,” says Sounkalo.“Everyone who has a gun, you have to pay.” His lorry was travel-ling on a Saturday afternoon, a particularly bad time. “At week-ends, all of the senior police officers are not working, so that iswhen the junior ones make their money.” At 1.22pm a police offi-cer gestured the lorry over with his gun. The lorry stopped whileFousseni, Sounkalo’s brother, got out and handed him 1,000francs (about $2). At 1.29pm, another road block and anotherbribe. Then again at 2.21pm, 2.31pm and 3.32pm. Overall, thebribes add up to more than the tolls.

An��amoussoukro is not much of a destination, eventhough it offers one of the world’s most egregiously expensivechurches and one five-star hotel with “presidential” suites for$420 a night. After stoppingbriefly to admire the church, yourcor-respondent squeezed back into the cab for the 100km stretch to

Bouaké, which has a customs checkpoint. From there, the dis-tance to Ferkessédougou, the second night’s stop, is about 200km,yet it took the Ouattaras’ lorry the best part of ten hours to getthere. Just a few miles out of Bouaké the tarmac starts to developpotholes several metres long. At each, the vehicle has to slowdown almost to a standstill to cross it, and then gradually regainspeed. Some go faster, but they take a big risk. At one point the lor-ry passed a group of about 30 people and their luggage, waitingby their crashed bus. A smear of rubber led from a particularlylarge pothole offthe road and into a tree.

As the roads deteriorate, so does the security. Though thereare police checkpoints every 10km or so—generally a couple ofmen and a piece ofa stringora logblocking the road—they mostlygo home at sunse���ehicles travelling after that are often held up

by robbers wieldingAK-47s. Even in the day, there is a risk. Luckilythe Ouattaras’ lorry was not robbed, but Bright Gowonu, a Gha-naian analyst for Borderless Alliance, an NGO which tries to pro-mote more trade, was less fortunate. Travelling from Ouagadou-gouto Abidjan on the same route, the lorryhe wason came acrossan armed robbery of a bus, and was stopped at gunpoint. WhenMr Gowonu and his driver reached a police checkpoint, some-what lighter on cash, they were told that there was nothing thatcould be done. But they were still asked formoney for tea and mo-bile-phone credit.

In the middle of nowhereAccording to a study by Saana Consulting, a development-

economics firm, carried out on behalfof the Danish government,the cost ofmoving a container from a port in west Africa inland isroughly 2.5 times what it would be in America. Bribery generallymakes up about 10% of that (although for perishable goods such

The potholes did for it

The Economist April 16th 2016 9

BUSINESS IN AFRIC A

2

1

LAST OCTOBER MTN, a big South African mobile-tele-coms company, hit a brick wall in Nigeria. The cash-

strapped government there announced that the firm, whichmakes 35% of its revenue in the country, had broken rules aboutregistering SIM cards and would be fined about $1,000 for everyincorrectly registered account. The total came to $5.2 billion,nearly three times MTN’s annual profits in Nigeria. In Novemberthe fine was reduced to $3.9 billion on appeal. Last month thefirm announced that its profits for the year had halved, largelybecause of its poor performance in Nigeria. As this special reportwent to press, the dispute between MTN and the Nigerian gov-ernment had still not been resolved.

MTN’s story illustrates the problems that bigcompanies arelikely to encounter when they invest in new countries in Africa.Wherever they come from, they need to proceed with great care.Taking businesses across borders can be extremely lucrative—butalso extremelyrisky. That isparticularly true ofinvestment inNigeria, where MTN initially did very well. With its youthful andrapidly urbanising population of perhaps 180m, the country is acompelling prospect, but doing business there is fiendishly diffi-cult. Last year the World Economic Forum (WEF) put it 124th outof140 countrieson the qualityofits institutions; 133rd for its infra-structure; and last out of 140 on its primary education. Over thepast five years the country’s position has worsened on almostevery one of the WEF’s measures.

South Africa seems well placed to invest elsewhere on thecontinent. Its firms have access to capital, infrastructure andskilled labour that those in other African countries can onlydream of, but a substantial chunkof its people are as poor as anyAfricans. Many observers therefore expected South Africanbusinesses to be pioneers of direct investment in the rest of thecontinent, especially in consumer market�et over the past de-cade most of them have struggled. It is an ominous warning tocompanies from the rich world trying to follow in their path.

A few South African firms have done well. Standard Bankoperates in 20 countries in Africa and is expanding quickly. “Wewant to go from beinga South African bankwith an African pres-

Doing business

Is it worth it?

For outsiders in particular, investing in Africa isstrewn with hurdles

as fruit it can be much more). But the biggest cost is the sheeramountoftime swallowed up bypoorroads. Justone-third ofAf-ricans in rural areas live within 2km of an all-season road, com-pared with two-thirds ofthose in otherdevelopingregions oftheworld. Some of the statistics are astonishing. The Democratic Re-public of Congo, a country four times the size of France, has few-er miles ofpaved road than Luxembourg.

The costsofthismountup quickly. Astudy in 2010 byAfricaCountry Infrastructure Diagnostic, a research project led by theWorld Bank, found that farmers four hours by road from a city of100,000 people produced only 45% of what their land ought toyield. Those six hours away produced just 20%, and those eighthours away produced a mere 5%. Not only do they find it hard tosell their produce, they cannot easily buy fertilisers and equip-ment or get credit, because doing any of this requires access to areasonably sized city. And what is true for farmers is true foreveryone: being unable to move around means that children donot get educated, job opportunities are missed and businessesare not started.

Things are improving, but not nearly fast enough. In 2009the World Bankestimated that Africa needed an extra $93 billiona year in infrastructure spending. Last year the Brookings Institu-tion argued in a report that a large chunk of this has now materi-alised. New ports, roads, railways and power stations are spring-ing up across the continent. Some rely on private finance, otherson soft Chinese loans. Next year Kenya will open a new railwayline going from Mombasa, its main port, to Nairobi, its capital.Ethiopia has recently opened a new line from Djibouti to AddisAbaba. Both are Chinese-funded.

But progress would be much faster if governments werewilling to let private investors build. Too many African politi-cians favour projects that create opportunities for kickbacks, orwhich mostly help favoured groups. Governments’ unwilling-ness to pay the bills for power generated by private companiesputs investors off. The projects that do get built are either so prof-itable that they can accommodate these risks, or else they arefunded by the World Bank or China. Sovereign-wealth funds aredesperate to invest in long-term projects, but cannot find nearlyenough opportunities for reasonably safe investments to soakup the available capital.

Meanwhile smaller fixes could help boost trade. Onewould be better customs arrangements and more containerisa-tion. At the moment, coastal countries such as Ivory Coast re-peatedly check lorries travelling inland to try to stop tax evasion.Duties provide much of the government’s revenues. As Nigeria’ssmugglers know, a common ruse to avoid them is for goods “intransit” to a landlocked country to go missing en route. But thosechecks also slow things down and provide opportunities for

bribery. If Burkina Faso were able to collect its import duties atIvorian ports, lorries could move inland more quickly.

At the final customs checkpoint at Ouangolodougou thecrew had to negotiate the lorry’s passage into Burkina Faso withan officious man in a khaki uniform who was adamant that theirpaperwork was not in order. It seemed ominous, but within afew hours the official was back and the truck was moving again.Within half an hour the lorry was at the border itself—a thin riv-er, with the final barrier a simple gate guarded by a couple ofsleepy soldiers, where your correspondent descended.

Adecade ago, thiswasrebel-held territoryand there wasnotrade at all, so those carpets crossing the border represent an im-provemen��et barriers to trade in goods are only part of the

story. If Africa is going to become more prosperous, cross-borderinvestment, too, will have to become a lot easier—and that stillseems a long way off. 7

SPECIAL REPOR T

10 The Economist April 16th 2016

SPECIAL REPOR TBUSINESS IN AFRIC A

2

1

LIFE HAS NOT always been easy for AshishThakkar, founder of the Mara Group, a con-glomerate that invests across Africa. He wasborn in 1981in Leicester, about a decadeafter his family settled in Britain after beingkicked out of Uganda (where his forebearshad moved from India in the 1880s) by IdiAmin. The family worked hard and saved, andin 1993 they moved back to Africa.

Ashish was sent to school in Nairobi;the family started a new business in Kigali,Rwanda’s capital. The day after he returnedhome for the Easter holidays in 1994, theRwandan genocide started. “Cutting a longstory short, we came out alive but we losteverything again,” he recalls.

Undeterred, the Thakkars went back toKampala, Uganda’s capital, and started allover yet again. In 1995 the teenage Mr Thak-kar left school, raised a $5,000 loan and setup an IThardware business. After that hemoved to Dubai. Now the Mara Group oper-ates in 25 African countries. Many African-Gujarati businessmen in east Africa havesimilar tales to tell. Doing business in Africamay be difficult, but some groups—Gujaratisin east Africa, Lebanese in west Africa—seem

to be particularly good at it.East Africa’s biggest supermarket

chain, Nakumatt, is mostly owned by theShah family, who also have their origins inGujarat. In Uganda, the leading sugar manu-facturer, Kakira Sugar, is owned by the Madh-vani family, who bought their business backafter it went bankrupt when they were ex-pelled from the country. In Ivory Coast thebiggest retail firm is Prosuma, which is Leba-nese-owned. Lebanese Ivorians claim thatLebanese families control around 40% of theIvory Coasts’s economy.

What is it about these diasporas thatallows them to succeed in business? Largenumbers of Indians came to Kenya and Ugan-da in Victorian times, drawn by the newBritish-built Mombasa-Kampala railway.With the Lebanese, the story goes that theygot lost in Ivory Coast on their way to Braziland decided to stay. Both groups have be-come “settled strangers”, a label used byGijsbert Oonk, a Dutch historian who hasstudied Asian diasporas in east Africa. Thatquality may explain their business success.“It’s a marriage of global ability with localknowledge,” says Aly Khan Satchu, a Kenyan

Settled strangers

Why some diasporas are so successful

financier whose family arrived in east Africain 1884. “These families use their interna-tional relations like a multinational corpo-ration would do,” notes Mr Oonk.

Chadi Srour, a Lebanese propertydeveloper in Abidjan, moved to Ivory Coastfrom Washington, DC, on a recommendationfrom his brother. Lebanese people, he says,“are not afraid of dangerous places as long asthey are making money”. Ivory Coast’s twowars this century were profitable opportuni-ties, he jokes, since many long-establishedFrench expats sold up “and the Lebanesetook over.”

Asian businesses are no longer asdominant in Kenya as they were at indepen-dence. Avaricious governments after in-dependence hurt some; poor successionplanning others. In Ivory Coast, Lebanesebusinesspeople complain that they are beingsqueezed by corrup ���� ��������et the

declining importance of Africa’s businessdiasporas may be a sign of success. Asians didwell because they had strong families andeasy access to education and internationalcapital. These days, such privileges are alsoenjoyed by plenty of Africans.

ence to being a genuinely pan-African bank,” says Peter Schle-busch, one ofthe firm’s top executives. SABMiller, a bigbeercom-pany, has breweries all over Africa, some in difficult places. Lastyear it was bought for $108 billion by Anheuser-Busch InBev, theworld’s largest brewer. Shoprite, a South African supermarketchain, has a quarter of its flagship outlets outside South Africa,including one in Kinshasa, the capital of the Democratic Repub-lic ofCongo, and has done well in Nigeria.�

et hopes that South African companies would dominatethe continent have been disappointed. “A lot of South African

companieshave gone into Nigeria and gotburnt,” saysAlan Hea-ly of Arisaig Partners, a company that invests in many Africanconsumer-goods firms. Last December the Nigerian business ofTiger Brands, South Africa’s biggest food manufacturer, was soldto Dangote for $1 after writing down the business by 1.9 billionrand (roughly $125m at current exchange rates). In 2013 Wool-worths, a South African middle-class retailer, got out of Nigerialess than two years after opening its first store in Lagos. In 2010Telkom, a South African telecomsfirm, announced itwas leavingNigeria after losing 10 billion rand. MTN’s recent travails are justthe latest wave in a sea of troubles.

Some say that South African businesses are at fault, beingunwilling to take risks and commit themselves to difficult partsof the world. “The typical South African business leader is igno-rant and Afro-pessimistic,” says Alan Mukoki, CEO of the SouthAfrican Chamber of Commerce and Industry. “There’s a hugeperception of corruption and a lot of South African businessesthink, if they’re in Kenya or Congo, if there is a dispute, can I takehim to court?”

In reality, though, South African firms have proved moreoptimistic than most about the potential of the African market.

Where they have failed, it has often beenbecause they were too sanguine about in-frastructure and working of the law. Inparticular, they put too much faith in thepower of innovative product design. “

�ou

can come up with an amazing producthere, but that doesn’t help you sell it in Ni-geria if you haven’t got the contacts to get

it out of the port,” says Safroadu�

eboah-Amankwah, the SouthAfrica director ofMcKinsey, a management consultancy.

One reason why Woolworths left was that the goods it wasimporting to sell in its shops were often stuck in the ports formonths. But there were plenty of other vexations that contribut-ed to the company’s decision to quit, including the cost of run-ning generators, finding retail space and paying executivesenough to maintain the sort of lifestyle that they had been usedto in South Africa.

The firm did not mention corruption, but that is a pervasiveproblem. In Kenya, managers claim that demands for bribes are

You can come up with an amazing product, but thatdoesn’t help you sell it in Nigeria if you haven’t got thecontacts to get it out of the port

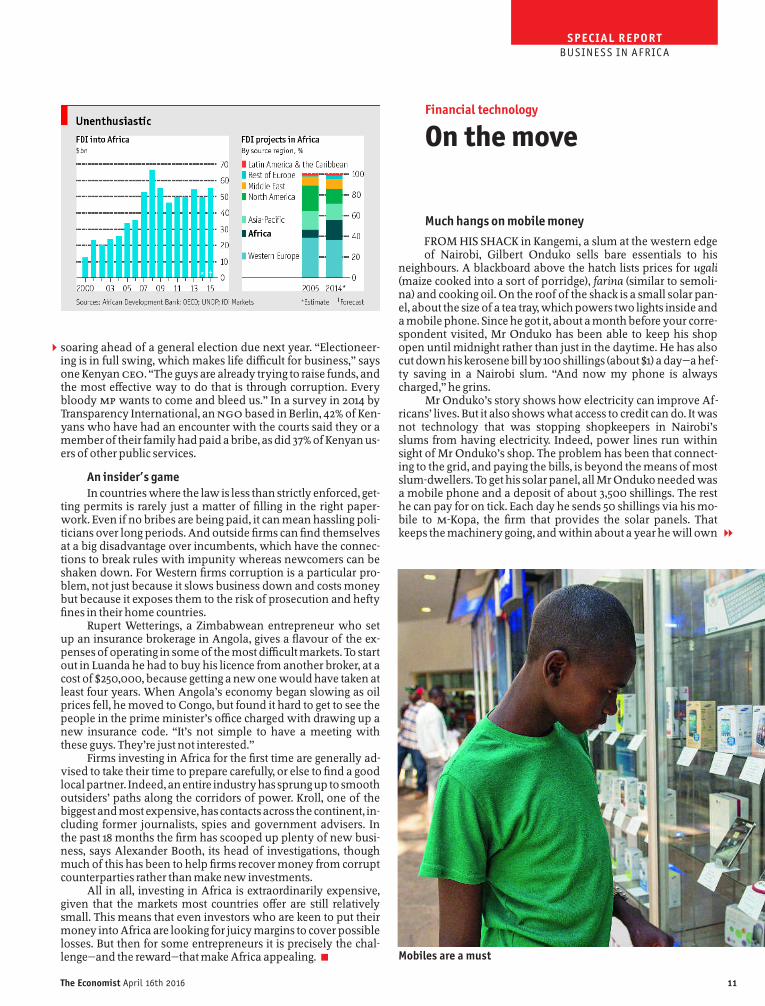

FROM HIS SHACK in Kangemi, a slum at the western edgeof Nairobi, Gilbert Onduko sells bare essentials to his

neighbours. A blackboard above the hatch lists prices for ugali(maize cooked into a sort of porridge), farina (similar to semoli-na) and cooking oil. On the roofof the shack is a small solar pan-el, about the size ofa tea tray, which powers two lights inside anda mobile phone. Since he got it, about a month before your corre-spondent visited, Mr Onduko has been able to keep his shopopen until midnight rather than just in the daytime. He has alsocutdown hiskerosene bill by100 shillings (about$1) a day—a hef-ty saving in a Nairobi slum. “And now my phone is alwayscharged,” he grins.

Mr Onduko’s story shows how electricity can improve Af-ricans’ lives. But it also shows what access to credit can do. It wasnot technology that was stopping shopkeepers in Nairobi’sslums from having electricity. Indeed, power lines run withinsight of Mr Onduko’s shop. The problem has been that connect-ing to the grid, and paying the bills, is beyond the means of mostslum-dwellers. To get his solar panel, all Mr Onduko needed wasa mobile phone and a deposit of about 3,500 shillings. The resthe can pay for on tick. Each day he sends 50 shillings via his mo-bile to M-Kopa, the firm that provides the solar panels. Thatkeeps the machinery going, and within about a yearhe will own

Financial technology

On the move

Much hangs on mobile money

Mobiles are a must

The Economist April 16th 2016 11

BUSINESS IN AFRIC A

2

1

soaring ahead of a general election due next year. “Electioneer-ing is in full swing, which makes life difficult for business,” saysone Kenyan CEO. “The guys are already trying to raise funds, andthe most effective way to do that is through corruption. Everybloody MP wants to come and bleed us.” In a survey in 2014 byTransparency International, an NGO based in Berlin, 42% ofKen-yans who have had an encounter with the courts said they or amemberoftheir familyhad paid a bribe, asdid 37% ofKenyan us-ers ofother public services.

An insider’s gameIn countries where the law is less than strictly enforced, get-

ting permits is rarely just a matter of filling in the right paper-work. Even if no bribes are being paid, it can mean hassling poli-ticians over long periods. And outside firms can find themselvesat a big disadvantage over incumbents, which have the connec-tions to break rules with impunity whereas newcomers can beshaken down. For Western firms corruption is a particular pro-blem, not just because it slows business down and costs moneybut because it exposes them to the risk of prosecution and heftyfines in their home countries.

Rupert Wetterings, a Zimbabwean entrepreneur who setup an insurance brokerage in Angola, gives a flavour of the ex-penses ofoperating in some of the most difficult markets. To startout in Luanda he had to buy his licence from another broker, at acost of$250,000, because getting a new one would have taken atleast four years. When Angola’s economy began slowing as oilprices fell, he moved to Congo, but found it hard to get to see thepeople in the prime minister’s office charged with drawing up anew insurance code. “It’s not simple to have a meeting withthese guys. They’re just not interested.”

Firms investing in Africa for the first time are generally ad-vised to take their time to prepare carefully, or else to find a goodlocal partner. Indeed, an entire industryhassprungup to smoothoutsiders’ paths along the corridors of power. Kroll, one of thebiggestand mostexpensive, hascontactsacross the continent, in-cluding former journalists, spies and government advisers. Inthe past 18 months the firm has scooped up plenty of new busi-ness, says Alexander Booth, its head of investigations, thoughmuch of this has been to help firms recover money from corruptcounterparties rather than make new investments.

All in all, investing in Africa is extraordinarily expensive,given that the markets most countries offer are still relativelysmall. This means that even investors who are keen to put theirmoney into Africa are looking for juicy margins to cover possiblelosses. But then for some entrepreneurs it is precisely the chal-lenge—and the reward—that make Africa appealing. 7

SPECIAL REPOR T

SPECIAL REPOR TBUSINESS IN AFRIC A

2

1

it. M-Kopa, which means “to borrow” in Swahili, has made itsname selling solar panels, but it is rapidly becoming one of eastAfrica’s most innovative financial companies.

Mobile and internet technology is transforming industriesacross the world, but Africa has more potential than most be-cause the existing infrastructure falls so far short of people’sneeds. Executives talk exuberantly about how the continent is“leapfrogging” the West through technology. A lot of this is wish-ful thinking. Drones, for instance, seem unlikely to become a sub-stitute for roads. But the revolution in fi-nance is real. According to the WorldBank, between 2011 and 2014 the propor-tion of adults in sub-Saharan Africa whohave a mobile-money account increasedfrom 24% to 34%.

East Africa is one of the most devel-oped markets. Some 58% of Kenyans usemobile-money services, overwhelminglyM-Pesa. And as M-Kopa shows, such mo-bile services offer more than just a meansto transfer money. Mobile phones canprovide an address book, a credit ratingand a distribution network all in one. To-gether, those things can allow even verypoor people to acquire assets with theirearnings, setting them on the path to be-coming middle-class.

M-Kopa’s offices in Nairobi show allthe signs of a tech startup. Table-footballand table-tennis sets glow in the equatori-al sun. The adjacent call centre is alivewith the sound of employees touting fornew business. When customers arereaching the end of their loan terms, M-Kopa agentscall them to see ifthere isany-thing else the company can sell them. Ifcustomers wish, they can extend theirloans and upgrade their solar set to a big-ger one that can support a television.

M-Kopa also sells fuel-efficient cook-ing pots and smartphones, and wouldlike to supply a small refrigerator, too. Ithas sold around 325,000 solar panels sofar, and 50,000 of their buyers have al-ready paid off their loan and then boughta cooking pot, a television or a smart-phone. The customers’ repayments re-cords offer an effective way of judgingtheir creditworthiness. Pay off your solar

panel quickly and you are probablyworth lending more to, explains JesseMoore, the firm’s American founder.

M-Kopa is far and away the mostsuccessful of the African firms innovatingon top of mobile technology, but it is notthe only one. Insurance is one promisingarea. Milvik, a multinational microfi-nance firm, now sells life insurance infour African countries, Tanzania, Uganda,Ghana and Senegal, partnering with in-surance businesses and telecoms provid-ers. Agents sign up customers, and thepremiums—typically about 2 US cents perday—are taken automatically from mo-bile-phone top-ups. Over 95% of custom-

ers earn less than $10 a day. The policies promise a $1,000 payoutin the event ofan unexpected death.

The mobile-telecoms operators are not doing much to pro-mote innovation. Though most Africans now own mobilephones, these are generally cheap and dumb, and since most Af-ricans are poor, they do not spend much on accessing the inter-net. Unlike in the West, therefore, it ishard to reach a massmarketwith a good app. Instead, mobile operators load apps directlyonto SIM cards and keep the data they generate in-house.

IN A DIRTY warehouse in an industrialdistrict of Abidjan, a few entrepreneurs aretrying to create a version of Amazon forAfricans. At one end, dozens of workers sitat desks making phone calls and confirmingorders. At the other end sit boxes and boxesof deliveries, waiting to go out. Televisions,washing machines, laptops and clothes pileup. The idea is that getting somethingdelivered to your home should be as cheapand easy in Ivory Coast as it is in America.But in a country with no proper addressdatabase, a barely functional postal serviceand hardly any credit cards, that is anambitious goal.

Investors chasing the African middleclass like to build malls, as Actis has done inNairobi, but a growing number are gettinginterested in e-commerce too. The ware-house in Abidjan is run by a firm calledJumia, which started in Lagos but now hasoperations in ten other African countries,including Kenya, Ghana, Cameroon andTanzania. Much of its funding comes fromRocket Internet, a German firm that tries toreplicate successful Western internetbusinesses in countries that do not havethem yet. Rocket Internet also owns Hello-food, a food delivery app similar to Seam-less, and Easy Taxi, rather like Uber.

Jumia is having to learn to adapt to

local conditions. Importing its own goodsand supplying them directly, as Amazondoes in the West, would mean dealing withcustoms officials and facing delays anddemands for bribes. So instead Jumia setsprices, takes payment and arranges deliv-ery, but gets local firms to provide theproducts as they are ordered and send themto Jumia’s warehouse. This means they takea few days to arrive.

Jumia started out using private deliv-ery firms in Ivory Coast, but they were notreliable enough, so now it has its own con-tractors. Processing payments is anotherheadache. The firm would like to take mobilemoney, but many customers prefer to paycash on delivery. All new online orders areconfirmed from a call centre, but even soperhaps a fifth of deliveries end up back atthe warehouse, estimates Francis Dufay, thefirm’s director in Ivory Coast.

It is perhaps unsurprising that so farJumia is not profitable. It has high fixedcosts and has to sell things more cheaplythan shops to compete. But there are rea-sons to be optimistic: on a continent whereproper shopping centres are still rare andtraffic jams are ubiquitous, ordering thingsonline ought to hold wide appeal. AndAmazon itself, after all, still only barelyturns a profit.

Virtual headaches

E-commerce firms like Jumia have to beat multiple handicaps

12 The Economist April 16th 2016

2

1

ON THE EDGE of Kinshasa, the capital of the DemocraticRepublic of Congo, is the Marché de la Liberté, a big whole-

sale market. Kinshasa is Africa’s third-largest city and has a pop-ulation of at least 8m, and perhaps as large as 12m (that nobodyknows for sure tells you much about Congo). And even here, inthe capital of one of the poorest countries on the planet, there isclearly money flowing. At the market’s centre, deafening noiseblares from enormous speakers mounted onto cars, which dou-ble up as stalls selling mobile phones. You can buy anythinghere, from fried fish to Premier League football shirts. Peopleflash cash as they negotiate, and everyone is haggling.

The irony of investing in Africa is that it is both one of theworld’s most difficult regions in which to do business and alsoperhaps its most entrepreneurial. In no other part of the worlddoes such a large share of the population rely on their wits andtheir tradingabilities to get by. Even the most modest stallholdersare smartly dressed and juggle mobile phones, shouting pricesand strikingdeal���et theyalso tell storiesofhardship. “Life is ex-pensive!” exclaims James, who sells plumbing equipment. Copsdemand bribes. Transporting his goods to the market costs a for-tune. And in the neighbourhood where he lives, there is alwaysthe riskofa riot.

What is true for stallholders is also true for the world’s big-gest multinationals. Africa holds promise like no other region.For the first time ever, hundreds ofmillions ofpeople are buyingbeer, washing powder, mobile-phone credit, fast food, insuranceand electricity. But it is also a place to lose yourshirt. Too much ofAfrica’s growth over the past two decades has been sustained bycommodities and little else. It seems perverse that in many Afri-can capitals where most people earn a few dollars a day, it is stillimpossible to find a clean hotel room foranything less than $200a night, or a good Western meal for less than $30. Optimists seethis as evidence ofa spectacular opportunity to enter the marketand make a profit. Pessimists reckon it shows just how difficult it

Prospects

Fortune favours thebraveDoing business in Africa is risky, but potentiallyhighly rewarding

Byfar the most successful is Safaricom. Ithasa loans servicecalled M-Shwari, and has worked with Kenyan banks to try to in-tegrate its service. Buteven the firm’sexecutivesadmit there is farmore it could do. Safaricom has declined to turn itself into abank, but says it is opening up M-Pesa to other developers. Itwants to become a “platform” rather than just a mobile-telecomsprovider, but it has a long way to go, and its monopoly does notprovide the best incentive.

Keep innovatingIn the meantime the best hope is any innovation that gets

around M-Pesa’s monopoly power. The rise ofsmartphones andfeature phones (which can be preloaded with apps) will help. By2020 over half of Africans will have access to smartphones withmobile broadband, reckons the GSMA, which representsmobile-phone operators worldwide. But given the right technology,even dumb phones can be useful. Counterintuitively, a promis-ing source of innovation could be the banking sector, which hasa strong interest in not letting mobile-telecoms operators steal itsactual or potential customers.

In the Democratic Republic ofCongo, one ofAfrica’s largestand least functional countries, the number of people with bankaccounts has increased from just 50,000 in 2005 to over 3m in apopulation ofabout80m. Agovernmentprogramme to paystateemployees by bank transfer instead of in cash has helped. But sotoo has innovation. Trust Merchant Bank (TMB), the country’sbiggest, has developed a voice app for its customers that works alittle like telephone banking in the West: customers can carry outa mobile transaction by making a phone call or sending a textmessage, avoiding the need for an app. In Congo, unlike in muchof east Africa, mobile-money transfers have not so far taken off,probably because the infrastructure is missing. TMB is hopingthat it can beat the telecoms firms to the chase.

Another innovator is Equity Bank, a Kenyan firm with oper-ations across east Africa. In Kenya it has launched its own mo-bile-phone company, Equitel, which uses the network of Airtel,another mobile operator, but exists mainly to provide bankingservices. It offers a “thin SIM” which can be overlaid onto an ex-isting SIM card so that a phone can access two networks at once.That allows banking to be carried out through a dumb-phoneSIM app without giving up the benefits of making phone callsand sending text messages through the dominant provider.

So far, this innovation looks better on paper than in prac-tice. The reason why Equitel’s thin SIM has not been taken up inhuge numbers, observers of the bank reckon, is probably that itcosts 500 shillings to buy, which for most Kenyans is a hefty sum.But Equitel now has some 1.5m subscribers, all of whom alsohave a bank account with Equ-ity. TMB has not released num-bers for users of its app. But in-creasing access to banking—notjust to mobile money—will bekey to opening up other busi-nesses such as M-Kopa.

There are other areas thatphone companies could use-fully tackle. For example, mo-bile money has not yet mademuch progress in internationalmoney transfers, where itcould lower the cost of remit-tances. And even money-trans-fer services within nationalborders are still very expen-sive. Few in the West would

use Safaricom’s M-Pesa to send money to relatives and friends:the transaction fee can eat up as much as 10% of the value of thetransfer. The only place where mobile money is often preferredto cash for small transactions is Somaliland, the autonomousand peaceful northern part ofSomalia. The main system there ison a network run by Dahabshiil, a firm that started as a remit-tances business and bank rather than as a telecoms provider. Incontrast to almost everywhere else in Africa, making paymentsin Somaliland is free.

Mobile money has been one ofeast Africa’s great successesover the past decade. Not only has it created business opportuni-ties, it is a big revenue generator for government: in Kenya, Safa-ricom pays more taxes than any other firm. But if growth is tocontinue, telecoms firms will either have to open up voluntarilyor have their monopolies broken. Most Africans still do not haveaccess to proper loans, insurance or savings facilities. Even thewealthy keep their money in cash and property; the poor rely onbuying physical assets. Firms such as M-Kopa have made a start,but there is plenty more to do. 7

The Economist April 16th 2016 13

BUSINESS IN AFRIC A

SPECIAL REPOR T

war, much of it paid for by su-perpowers competing witheach other. Between 1966 and1993 Nigeria was ruled almostentirely by military leaders andsuffered six coups. That seemsunlikely to happen again. Theleader of one of those Nigeriancoups, Muhammadu Buhari, isnow Nigeria’s president again.But this time he won an electionin which his incumbent oppo-nent, Goodluck Jonathan,stepped down with far moregrace than he ever showed in of-fice. In Burkina Faso, a coup ledby the presidential guard wasoverturned after days of prot-ests in the streets.

Mobile phones do not justcreate consumers. Theyalso linkpeople up and help them shareinformation. A generation agopoliticians could suppress dis-sent just by controlling the radiostations. Now stories of corrup-tion spread quickly by text mes-sage and on WhatsApp. Protestmovements can organise farfaster and more easily than inthe past.

In some places that may bedestabilising. In Burundi, opposition to Pierre Nkurunziza’s at-tempt to hold on to power is being led by just the young urbanand educated people that Western companies most want to sellto. But elsewhere, politicians may come under increased pres-sure to shape up orstand down. Fordecades, the mostcorrupt Af-rican leaders have tried to resist urbanisation lest it threaten theirrule. They are failing.

Even so, the next decade will be more testing than the last.With less money to distribute from the proceeds ofoil, copper or

gold, it will be harder for patronage politi-cians to convince their populations thatthe future is bright. Tanzania’s new presi-dent, John Magufuli, has delighted West-ern diplomats since his election in Octo-ber by prosecuting corrupt officials andrequiring government employees actual-ly to do their jobs. But he has also stokedup xenophobia, expelled foreign workersand shut out imports.

It is only the pluckiest investors whowill brave such choppywaters. Revealing-ly, the biggest private foreign investmentsrecently have been in malls and mobile-phone masts, which are relatively cheap—not roads and railways, which cost bil-lions. But the potential rewards are ex-traordinary. Africa’s population is expect-ed to more than double by 2050, to nearly2.5 billion. Many of these people will stillbe poor, and some will still live in coun-tries torn apart by war. But even if only asmall proportion of them thrive, that willstill be a market worth going for. 7

14 The Economist April 16th 2016

SPECIAL REPOR TBUSINESS IN AFRIC A

2 is to do business here—because if it were easy, somebody wouldhave done it.

The receding commodities boom has made this conun-drum clear. Nigeria, the continent’s most populous country andmany investors’ biggest hope over the past decade, now lookssomewhat less appealing��et not every country is like Nigeria,and not all the money that used to flow so easily has been wast-ed. A decade of investment has given Africa lots of new roads,power stations and telephone towers. The next decade will stillsee new railways, ports and motorways being built, often withChinese money. Even in Kinshasa, a new highway runs throughthe centre of the city. Many African countries have taken on largeamounts of debt, which may prove a problem in the future. Butthey are also acquiring assets, which are already generating newsources ofgrowth.

Build on what you haveOver the next decade, the businesses that succeed in Africa

will be those that can capitalise on thiswithout the help ofcheapmoney and expensive oil—those that can build a genuine middleclass of consumers. Over the past decade, the seeds for this havebeen planted. It is a hopeful sign that African emigrants are re-turning to invest the money they earned overseas. In Kenya lastyear they injected $1.5 billion into an economy that generatedonly $63 billion in all. In Somalia remittance money is rebuildingwar-torn Mogadishu.

From the mobile-phone masts that have spread all over ev-ery big city to the soaring apartment blocks, the desire to changethings is evident. The question for the next decade is whethergovernments can live up to those hopes. In Nigeria, the drop inoil revenues may force the country’s leaders to face up to the factthat for decades they have systematically mismanaged theireconomy. Their attempts to protect the exchange rate and in-crease manufacturing by diktat are doomed to fail. Ghana andZambia, which have spent their windfalls on public-sector sala-ries rather than growth-generating investment, will have tomake tough decisions about the best use of their revenues. Notall these countries will do well.

Yet with a number ofexceptions, Africa has something thatit lacked a generation ago: stability. When commodity prices fellin the 1980s, the result was a series of coups and a generation of

Africa hassomethingthat itlacked agenerationago:stability

Finance in China May 7thMigration May 14thThe Middle East May 28thArtificial intelligence June 25th