April 12-13, 2010 PEÑASQUITO TOUR · In-Pit Crushing & Conveying Identified significant operating...

45

1 1 April 12-13, 2010 PEÑASQUITO TOUR

Transcript of April 12-13, 2010 PEÑASQUITO TOUR · In-Pit Crushing & Conveying Identified significant operating...

1 1

April 12-13, 2010

PEÑASQUITO TOUR

2

FORWARD-LOOKING STATEMENTS

2

This presentation contains “forward-looking statements”, within the meaning of the United States Private Securities Litigation Reform Act of

1995 and applicable Canadian securities legislation, concerning the business, operations and financial performance and condition of

Goldcorp Inc. (“Goldcorp”). Forward-looking statements include, but are not limited to, statements with respect to the future price of gold,

silver, copper, lead and zinc, the estimation of mineral reserves and resources, the realization of mineral reserve estimates, the timing and

amount of estimated future production, costs of production, capital expenditures, costs and timing of the development of new deposits,

success of exploration activities, permitting time lines, hedging practices, currency exchange rate fluctuations, requirements for additional

capital, government regulation of mining operations, environmental risks, unanticipated reclamation expenses, timing and possible outcome

of pending litigation, title disputes or claims and limitations on insurance coverage. Generally, these forward-looking statements can be

identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”,

“estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, “believes” or variations of such words and phrases or statements that

certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. Forward-looking statements are

subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or

achievements of Goldcorp to be materially different from those expressed or implied by such forward-looking statements, including but not

limited to: risks related to the integration of acquisitions; risks related to international operations; risks related to joint venture operations;

actual results of current exploration activities; actual results of current reclamation activities; conclusions of economic evaluations; changes in

project parameters as plans continue to be refined; future prices of gold, silver, copper, lead and zinc; possible variations in ore reserves,

grade or recovery rates; failure of plant, equipment or processes to operate as anticipated; accidents, labour disputes; delays in obtaining

governmental approvals or financing or in the completion of development or construction activities and other risks of the mining industry, as

well as those factors discussed in the section entitled “Description of the Business – Risk Factors” in Goldcorp’s annual information form for

the year ended December 31, 2008 available at www.sedar.com. Although Goldcorp has attempted to identify important factors that could

cause actual results to differ materially from those contained in forward-looking statements, there may be other factors that cause results not

to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and

future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on

forward-looking statements. Goldcorp does not undertake to update any forward-looking statements that are included in this document,

except in accordance with applicable securities laws.

3 3

GROWING:

EFFICIENT:

STRONG:

STABLE:

GROWTH LEADER

LOW-COST PRODUCER

OUTSTANDING BALANCE SHEET

LOW POLITICAL RISK

4

GOLDCORP: THE GROWTH CONTINUES

4

2004 2005 2006 2007 2008 2009 2010* 2011* 2012* 2013* 2014*

3.8 Moz

*Au production estimates 2010 - 2014

5

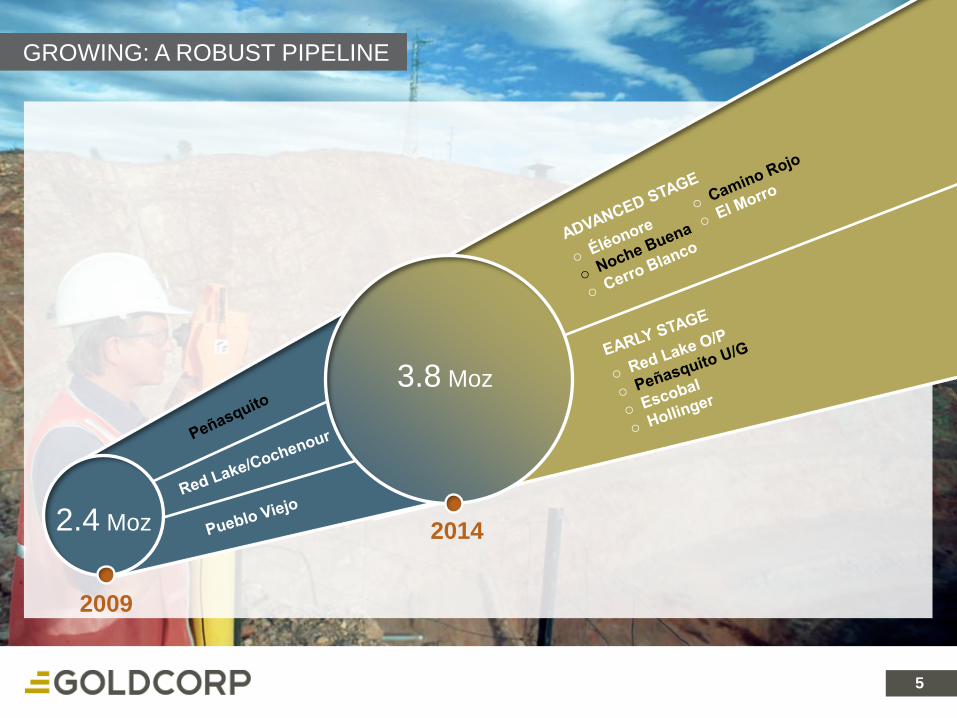

GROWING: A ROBUST PIPELINE

5

2.4 Moz

3.8 Moz

2014

2009

6

STRONG: OUTSTANDING BALANCE SHEET (AS OF DEC. 31, 2009)

Cash

6

$874.6M

Convertible senior notes $862.5M

Available debt facility $1.5B

Average annual cash flow over next 5 years ~$1.5B

Debt : Total capitalization < 0.01 : 1

Exceptionally strong balance sheet

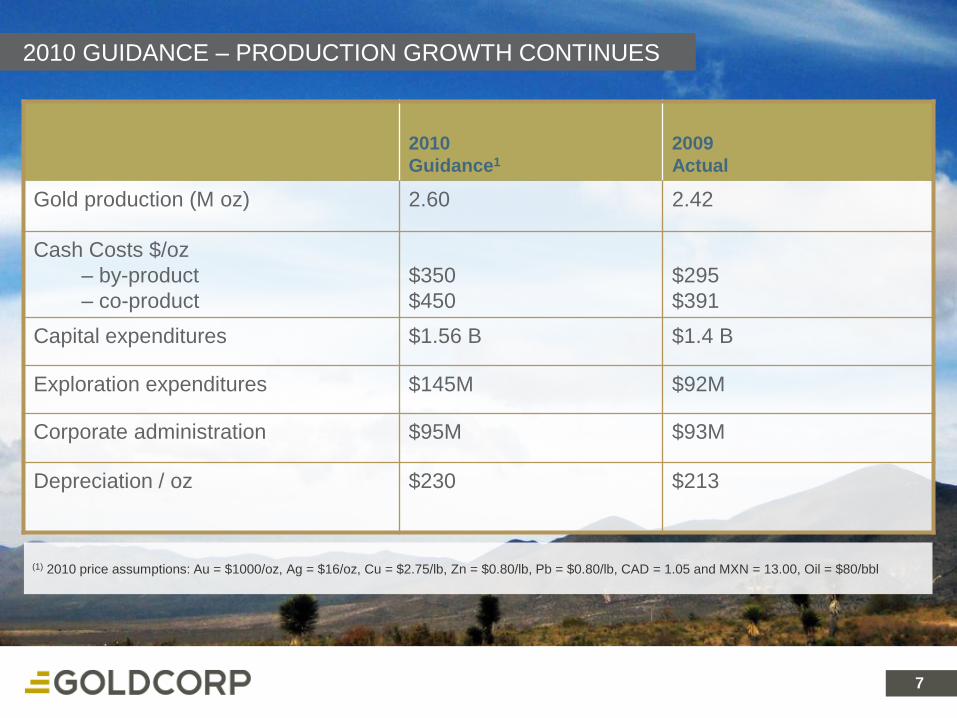

7

(1) 2010 price assumptions: Au = $1000/oz, Ag = $16/oz, Cu = $2.75/lb, Zn = $0.80/lb, Pb = $0.80/lb, CAD = 1.05 and MXN = 13.00, Oil = $80/bbl

2010 GUIDANCE – PRODUCTION GROWTH CONTINUES

2010

Guidance1

2009

Actual

Gold production (M oz) 2.60 2.42

Cash Costs $/oz

– by-product

– co-product

$350

$450

$295

$391

Capital expenditures $1.56 B $1.4 B

Exploration expenditures $145M $92M

Corporate administration $95M $93M

Depreciation / oz $230 $213

7

8

STABLE: LOW POLITICAL RISK PROFILE

8

CANADA

Red Lake 3.4 675,000

Porcupine 2.8 280,000

Musselwhite 2.1 260,000

UNITED STATES

Marigold (66.7%) 1.6 120,000

Wharf 0.2 65,000

MEXICO

Peñasquito 17.8 180,000

Los Filos 5.7 300,000

San Dimas 0.9 110,000

El Sauzal 0.3 155,000

CENTRAL AND SOUTH AMERICA

Marlin 2.1 290,000

Alumbrera (37.5%) 1.5 165,000

2010E Au

(oz)

Au reserves

(Moz)

FOCUS IN THE AMERICAS

2.6 Moz2010E GOLD PRODUCTION

9 8

PEÑASQUITOPROJECT OPTIMIZATION

BACKGROUND

PRODUCTION

EXPLORATION

10

PEÑASQUITO

10

One of the world’s

largest new mines

Inauguration – March 23, 2010

11 11

PEÑASQUITO - INAUGURATION

12 12

PEÑASQUITO - INAUGURATION

13

PEÑASQUITO LOCATION

13

Mazatlan

TorreónSmelter

Herrmosillo

Zacatecas

Saltillo

Mexico City

Chihuahua

Los Mochis

Peñasquito

Los Filos

San Dimas

El Sauzal

BACKGROUND

14

PEÑASQUITO SITE MAP

14

BACKGROUND

15

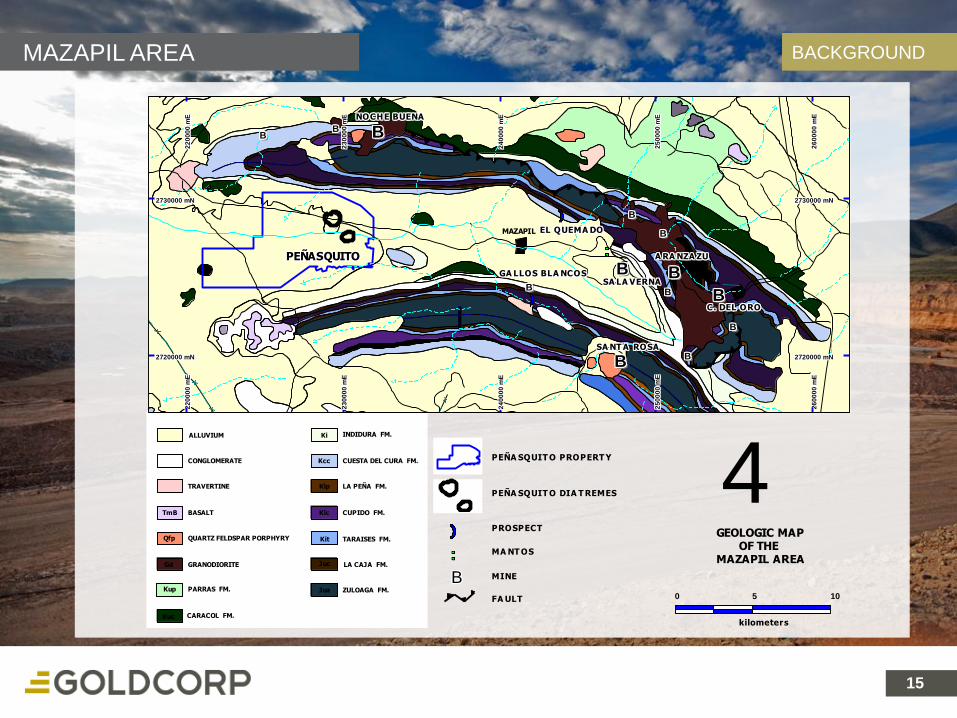

MAZAPIL AREA

15

LA CAJA FM.

TARAISES FM.

CUPIDO FM.

LA PEÑA FM.

Klc

Kit

Juc

Juz

Ki

Klp

KccCONGLOMERATE CUESTA DEL CURA FM.

ALLUVIUM INDIDURA FM.

ZULOAGA FM.

QUARTZ FELDSPAR PORPHYRY

GRANODIORITE

CARACOL FM.

PARRAS FM.

BASALT

TRAVERTINE

Gd

Kuc

Kup

Qfp

TmB

II

BBBBBBBBBB

BBBBBBBBBB

BBBBBBBBBB

BBBBBBBBBB

BBBBBBBBBB

BBBBBBBBBBBBBBBBBBBB

BBBBBBBBBB

BBBBBBBBBB

BBBBBBBBBB

B

BBBBBBBB

B

BBBBBBBBBBBBBBBBBBBBBBBBBBBBBB

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

26

00

00

mE

2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

24

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

25

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN2730000 mN

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

22

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

23

00

00

mE

2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN2720000 mN

0 5 10

kilometers

BBBBBBBBB

PEÑA SQUIT O PROPERT Y

PEÑA SQUIT O DIA T REMES

PROSPECT

MA NT OS

MINE

FA ULT

GA LLOS BLA NCOSGA LLOS BLA NCOSGA LLOS BLA NCOSGA LLOS BLA NCOSGA LLOS BLA NCOSGA LLOS BLA NCOSGA LLOS BLA NCOSGA LLOS BLA NCOSGA LLOS BLA NCOS

PEÑASQUITOPEÑASQUITOPEÑASQUITOPEÑASQUITOPEÑASQUITOPEÑASQUITOPEÑASQUITOPEÑASQUITOPEÑASQUITO

NOCHE BUENANOCHE BUENANOCHE BUENANOCHE BUENANOCHE BUENANOCHE BUENANOCHE BUENANOCHE BUENANOCHE BUENA

EL QUEMA DOEL QUEMA DOEL QUEMA DOEL QUEMA DOEL QUEMA DOEL QUEMA DOEL QUEMA DOEL QUEMA DOEL QUEMA DO

SA LA VERNASA LA VERNASA LA VERNASA LA VERNASA LA VERNASA LA VERNASA LA VERNASA LA VERNASA LA VERNA

A RA NZA ZUA RA NZA ZUA RA NZA ZUA RA NZA ZUA RA NZA ZUA RA NZA ZUA RA NZA ZUA RA NZA ZUA RA NZA ZU

C. DEL OROC. DEL OROC. DEL OROC. DEL OROC. DEL OROC. DEL OROC. DEL OROC. DEL OROC. DEL ORO

SA NT A ROSASA NT A ROSASA NT A ROSASA NT A ROSASA NT A ROSASA NT A ROSASA NT A ROSASA NT A ROSASA NT A ROSA

GEOLOGIC MAP OF THEMAZAPIL AREA

4

MAZAPIL

BACKGROUND

16

GEOLOGY

16

BACKGROUND

17

PEÑASQUITO AT A GLANCE

17

17.8 million ounces gold (proven and probable)1

22-year mine life

500,000 ounces gold - average annual production2

Very low life of mine cash costs

(1) See Endnote

(2) After reaching full design capacity

BACKGROUND

18

FOCUS IN 2010

18

Commissioning of Line 2

Commercial production

Operation refinement

Forecast gold production – 180,000 ounces Au

HPGR start up

BACKGROUND

19 19

SAG LINE 2 BACKGROUND

20

RAMPING UP PRODUCTION

20

Q4/10

Q3/10

Q2/09

130,000 tonnes/day

100,000 tonnes/day

50,000 tonnes/day

THROUGHPUT

High-Pressure Grinding Rolls

SAG Line 2

SAG Line 1

Q2/11

BACKGROUND

21

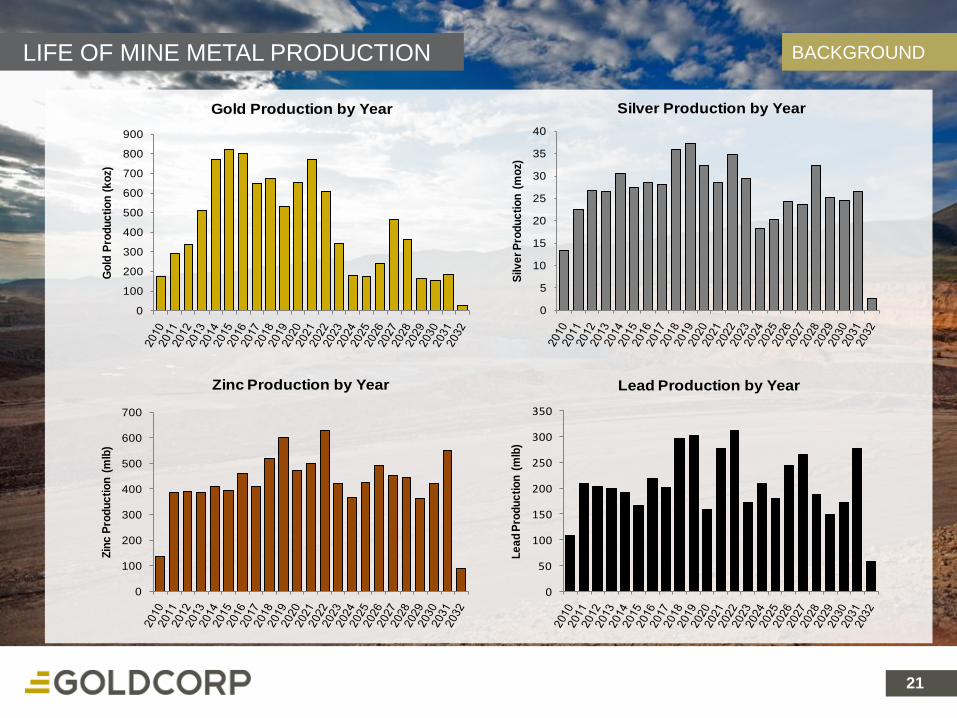

LIFE OF MINE METAL PRODUCTION

21

BACKGROUND

0

100

200

300

400

500

600

700

800

900

Go

ld P

rod

uc

tio

n (

ko

z)Gold Production by Year

0

5

10

15

20

25

30

35

40

Silv

er

Pro

du

cti

on

(m

oz)

Silver Production by Year

0

100

200

300

400

500

600

700

Zin

c P

rod

uc

tio

n (

mlb

)

Zinc Production by Year

0

50

100

150

200

250

300

350

Le

ad

Pro

du

cti

on

(m

lb)

Lead Production by Year

22

FIRST QUARTER PRODUCTION

22

PRODUCTION

Q1-10 Actual

Tonnes Mined – Ore (mt) 6.334

Tonnes Mined – Waste (mt) 36.81

Sulphide Production

Gold (oz) 11,400

Silver (oz) 1,352,900

Zinc (lbs) 17,462,500

Lead (lbs) 11,790,700

Oxide Production

Gold (oz) 19,300

Silver (oz) 725,300

23

MINING

23

PRODUCTION

24

DAILY MINE PRODUCTION

24

PRODUCTION

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

To

nn

es p

er

Day

2008 2009 2010

Daily 30 Day Avg

(1) As of April 6, 2010

25

MINING

25

PRODUCTION

26

PROCESSING

26

PRODUCTION

27

MILL PRODUCTION

27

PRODUCTION

Actual

Jan ‘10 Feb ‘10 Mar ’10 Q1-10

Total Throughput (t) 715,612 859,251 1,427,405 3,002,268

Average

daily throughput (t/d)

23,854 30,688 46,045 33,358

Peak throughput (t/d) 50,145 53,726 59,747 59,747

28

CONCENTRATE GRADES

28

Lead Conc. Expected (1)

Qu

alit

y

Lead 52 – 58% Pb

Gold 20 – 45 g/t Au

Silver 2,000 – 4,000 g/t Ag

Zinc Conc. Expected (1)

Qu

alit

y

Zinc 52 – 57% Zn

Gold 2 – 5 g/t Au

Silver 300 – 400 g/t Ag

2009 Actual Q1-10 Actual

55.3 58.5

33.3 34.2

4,178 3,876

Zn 7.3% 5.5

2009 Actual Q1-10 Actual

54.8 55.7

4.4 3.6

662 567

Pb 3.3% 2.4

(1) From Analyst Day May 2009

PRODUCTION

29

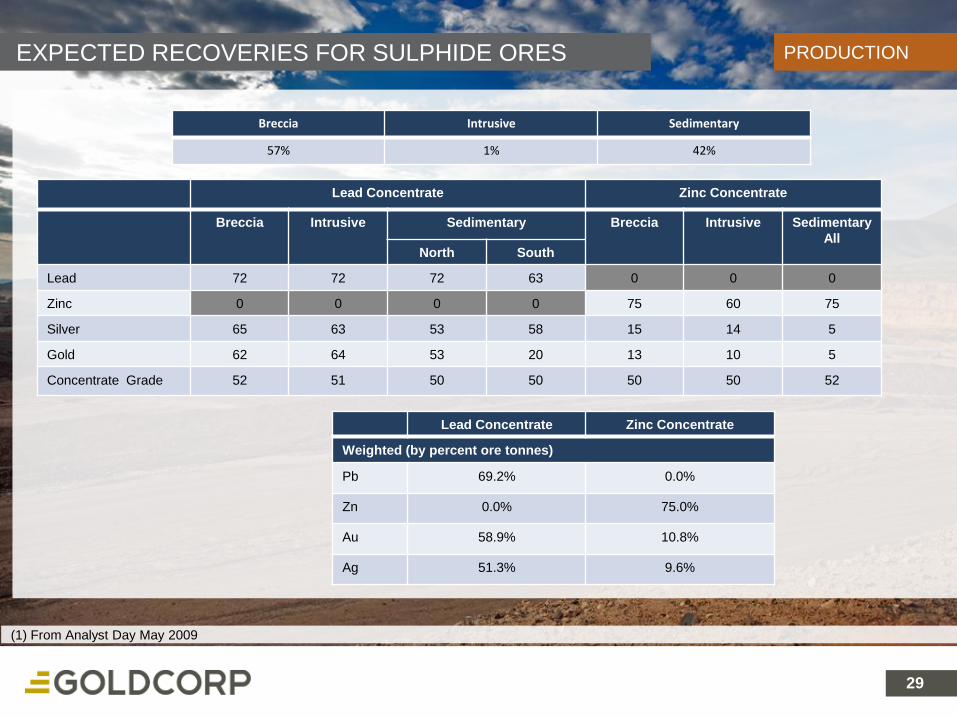

EXPECTED RECOVERIES FOR SULPHIDE ORES

29

Lead Concentrate Zinc Concentrate

Weighted (by percent ore tonnes)

Pb 69.2% 0.0%

Zn 0.0% 75.0%

Au 58.9% 10.8%

Ag 51.3% 9.6%

PRODUCTION

(1) From Analyst Day May 2009

Lead Concentrate Zinc Concentrate

Breccia Intrusive Sedimentary Breccia Intrusive Sedimentary

AllNorth South

Lead 72 72 72 63 0 0 0

Zinc 0 0 0 0 75 60 75

Silver 65 63 53 58 15 14 5

Gold 62 64 53 20 13 10 5

Concentrate Grade 52 51 50 50 50 50 52

Breccia Intrusive Sedimentary

57% 1% 42%

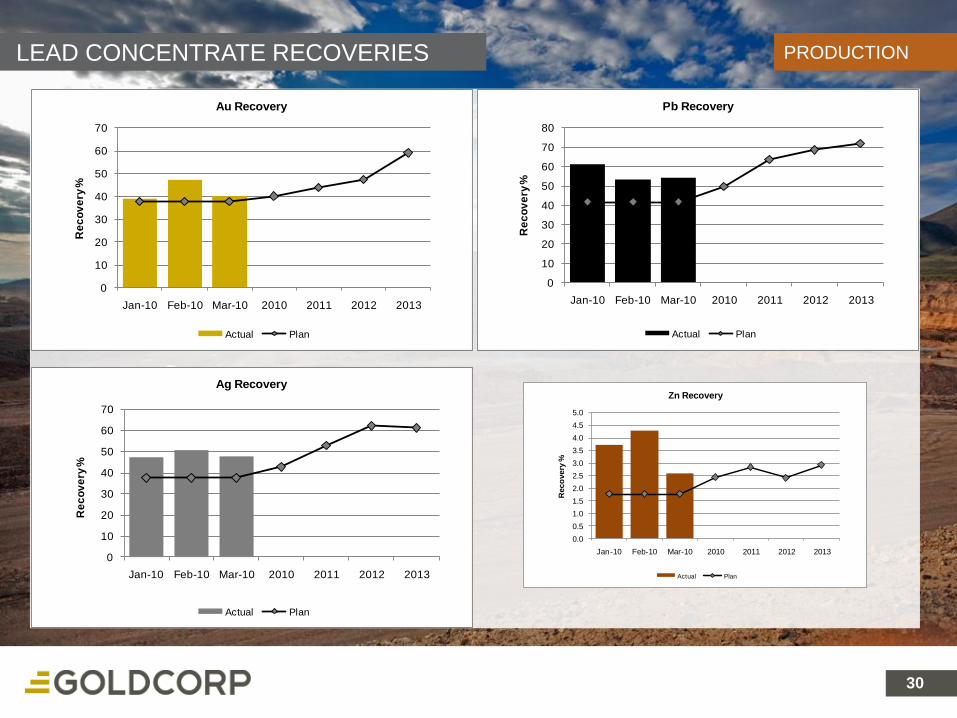

30

LEAD CONCENTRATE RECOVERIES

30

PRODUCTION

0

10

20

30

40

50

60

70

Jan-10 Feb-10 Mar-10 2010 2011 2012 2013

Re

co

ve

ry %

Au Recovery

Actual Plan

0

10

20

30

40

50

60

70

80

Jan-10 Feb-10 Mar-10 2010 2011 2012 2013

Re

co

ve

ry %

Pb Recovery

Actual Plan

0

10

20

30

40

50

60

70

Jan-10 Feb-10 Mar-10 2010 2011 2012 2013

Re

co

ve

ry %

Ag Recovery

Actual Plan

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jan-10 Feb-10 Mar-10 2010 2011 2012 2013

Reco

very

%

Zn Recovery

Actual Plan

31

ZINC CONCENTRATE RECOVERIES

31

PRODUCTION

0

2

4

6

8

10

12

Jan-10 Feb-10 Mar-10 2010 2011 2012 2013

Re

co

ve

ry %

Au Recovery

Actual Plan

0

2

4

6

8

10

12

14

16

Jan-10 Feb-10 Mar-10 2010 2011 2012 2013

Re

co

ve

ry %

Ag Recovery

Actual Plan

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jan-10 Feb-10 Mar-10 2010 2011 2012 2013

Re

co

ve

ry %

Pb Recovery

Actual Plan

0

10

20

30

40

50

60

70

80

Jan-10 Feb-10 Mar-10 2010 2011 2012 2013

Re

co

ve

ry %

Zn Recovery

Actual Plan

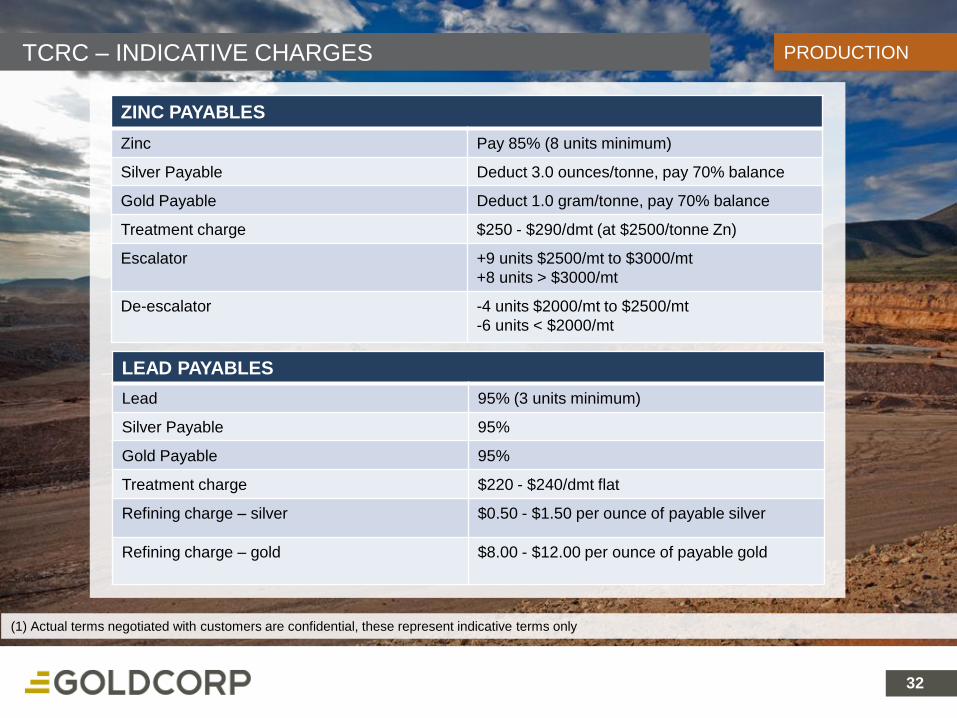

32

TCRC – INDICATIVE CHARGES

32

ZINC PAYABLES

Zinc Pay 85% (8 units minimum)

Silver Payable Deduct 3.0 ounces/tonne, pay 70% balance

Gold Payable Deduct 1.0 gram/tonne, pay 70% balance

Treatment charge $250 - $290/dmt (at $2500/tonne Zn)

Escalator +9 units $2500/mt to $3000/mt

+8 units > $3000/mt

De-escalator -4 units $2000/mt to $2500/mt

-6 units < $2000/mt

LEAD PAYABLES

Lead 95% (3 units minimum)

Silver Payable 95%

Gold Payable 95%

Treatment charge $220 - $240/dmt flat

Refining charge – silver $0.50 - $1.50 per ounce of payable silver

Refining charge – gold $8.00 - $12.00 per ounce of payable gold

PRODUCTION

(1) Actual terms negotiated with customers are confidential, these represent indicative terms only

33

VALUE-ADD INITIATIVES

33

In-Pit Crushing & ConveyingIdentified significant operating savings

Incorporated into mining plan

Underground MiningTargets identified

Further definition required

PROJECT OPTIMIZATION

34

IN-PIT CRUSHING & CONVEYING

34

24 Fewer haul trucks

- Capital savings

Convey 150,000 t/d waste

Lower operating costs increases reserves ~5%

Commence operation 1Q’13- Delivery in 2012

- Arroyo diversion completed

PROJECT OPTIMIZATION

Crusher orders have one year lead-time* Based on $0.55 /litre & $0.08 /kWh

Capital expenditure - $155M

35

IPCC CONVEYOR ROUTE

35

PROJECT OPTIMIZATION

Existing Ore Conveyor

Proposed Conveyor Route

Proposed Waste Dump

36 36

PEÑASQUITO – SW PEÑASCO MANTOS

Peñasco Chile Colorado/Brecha Azul

Mantos

Looking East

PROJECT OPTIMIZATION

37 37

PEÑASQUITO – UNDERGROUND STUDY

Underground Mine Planning

PROJECT OPTIMIZATION

38 38

$16 millionTotal 2010 exploration

investment

EXPLORATION

39 39

PEÑASQUITO REGIONAL TARGETS EXPLORATION

40

NOCHE BUENA: SUPPLEMENTING PEÑASQUITO

40

In-fill drilling and feasibility study

Test bulk and high grade underground resources

Evaluate regional targets

Exploration budget - $6.5 million

EXPLORATION

41

CAMINO ROJO: SUPPLEMENTING PEÑASQUITO

41

3.4 million Au ounces M&I; 0.6 million Au ounces inferred

60.7 million Ag ounces M&I; 7.6 million Ag ounces inferred

Synergies with Peñasquito

Addition of new exploration targets in a core district

EXPLORATION

Exploration budget - $5 million

42 42

ON SCHEDULE, ON BUDGET

SIGNIFICANT UPSIDE REMAINS

DE-RISKING WITH EACH MILESTONE

OPERATIONAL PRODUCTION ACHIEVED

PEÑASQUITO KEY

TAKEAWAYS

43 43

GROWTH LEADER

LOW-COST PRODUCER

OUTSTANDING BALANCE SHEET

LOW POLITICAL RISK

A SUPERIOR INVESTMENT

PROPOSITION

44 44

1. Total cash costs are defined as cost of sales divided by ounces of gold and silver sold or pounds of copper sold. The calculation of totalcash costs per ounce of gold is net of by-product sales revenue (by product copper revenue for Alumbrera; by-product silver revenue forMarlin at market silver prices; and by-product silver revenue for Luismin of $3.95 per silver ounce sold to Silver Wheaton). Goldcorp hasincluded a non-GAAP performance measure, total cash costs per gold ounce, throughout this presentation. Goldcorp reports total cashcosts on a sales basis. In the gold mining industry, this is a common performance measure but does not have any standardizedmeaning, and is a non-GAAP measure. Goldcorp follows the recommendations of the Gold Institute standard. Goldcorp believes that, inaddition to conventional measures, prepared in accordance with GAAP, certain investors use this information to evaluate Goldcorp’sperformance and ability to generate cash flow. Accordingly, it is intended to provide additional information and should not be consideredin isolation or as a substitute for measures of performance prepared in accordance with GAAP

2. All Mineral Reserves and Mineral Resources have been calculated as at December 31, 2009 in accordance with the standards of theCanadian Institute of Mining, Metallurgy and Petroleum and National Instrument 43-101, or the AusIMM JORC equivalent. CautionaryNote to United States Investors Concerning Estimates of Measured, Indicated and Inferred Resources. United States investors areadvised that while such terms are recognized and required by Canadian regulations, the United States Securities and ExchangeCommission does not recognize them. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and as totheir economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to ahigher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or other economicstudies. United States investors are cautioned not to assume that all or any part of Goldcorp’s Measured or Indicated Mineral Resourceswill ever be converted into Mineral Reserves. United States investors are also cautioned not to assume that all or any part of an InferredMineral Resource exists, or is economically or legally mineable. Calculations have been prepared by employees of Goldcorp, its jointventure partners or its joint venture operating companies, as applicable, under the supervision of Maryse Belanger, Director TechnicalServices. Reserve calculations incorporate current and/or expected mine plans and cost levels at each property. Varying cut-off gradeshave been used depending on the mine and type of ore contained in the reserves. Goldcorp’s normal data verification procedures havebeen employed in connection with the calculations. For a breakdown of Reserves and Resources by category and for a more detaileddescription of the key assumptions, parameters and methods used in calculating Goldcorp’s Reserves and Resources, see Goldcorp’sAnnual information Form/ Form 40-F on file with Canadian provincial securities regulatory authorities and the U.S. Securities andExchange Commission.

3. Goldcorp’s exploration programs are designed and conducted under the supervision of Charlie Ronkos, Vice President, Exploration ofGoldcorp. For information on geology, exploration activities generally, and drilling and analysis procedures on Goldcorp’s materialproperties, see Goldcorp’s Annual Information Form/Form 40-F on file with Canadian provincial securities regulatory authorities and theU.S. Securities and Exchange Commission.

ENDNOTES

45