Application Of Modified Porters’ Five Forces Model In ...

66

1 APPLICATION OF MODIFIED PORTERS’ FIVE FORCES MODEL IN ASSESSING ATTRACTIVENESS OF INSURANCE INDUSTRY IN KENYA SHARIFF NHAAMAN O.ABUOR. A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILLMENT FOR THE REQUIREMENT OF THE DEGREE OF MASTERS OF BUSINESS ADMINSTRATION (MBA) , SCHOOL OF BUSINESS,UNIVERSITY OF NAIROBI NOVEMBER, 2014

Transcript of Application Of Modified Porters’ Five Forces Model In ...

1

APPLICATION OF MODIFIED PORTERS’ FIVE FORCES

MODEL IN ASSESSING ATTRACTIVENESS OF INSURANCE

INDUSTRY IN KENYA

SHARIFF NHAAMAN O.ABUOR.

A RESEARCH PROJECT SUBMITTED IN PARTIAL

FULFILLMENT FOR THE REQUIREMENT OF THE DEGREE

OF MASTERS OF BUSINESS ADMINSTRATION (MBA) ,

SCHOOL OF BUSINESS,UNIVERSITY OF NAIROBI

NOVEMBER, 2014

2

DECLARATION

This is to declare that this research project is my original work and has not been

submitted for a degree course in this or any other University or Institution of higher

learning for examination.

Signed ……………………………… Date……………..…………

SHARIFF NHAAMAN O. ABUOR

REG. No.D61/68125/2011

This Management Research Project has been submitted for examination with my

approval as the University supervisor.

Signed …………………………... Date …………………………..

DR. JACKSON MAALU

SUPERVISOR, SCHOOL OF BUSINESS

UNIVERSITY OF NAIROBI.

3

ACKNOWLEDGEMENTS

I give all to God for guidance. Sincere gratitude to Dr. J. Maalu; my supervisor for

constantly advising and perfecting my project and Mr.S.Odongo, who spared his busy

schedule to guide and moderate the project. Without you precious people, i would

have not made it.

I would also like to acknowledge great support from MBA classmates, friends and

relatives. Madam RoselyneSamo who tirelessly typed this piece. Her devotion and

dedication throughout the project work was incredible.

Deepest appreciation to my wife Millicent, daughters; Shehnaz, Vennezar, Zainab and

Aisha-Tabby. Your understanding and support was abundant, i adore you. To all the

people not mentioned here, take pride.

May God bless the work of your hands, God bless you All

ALHAMDULILLAH

4

DEDICATION

To my parents and heroes, the late father and mother (Abuor Jakoguta &Tabitha

Nyakadiang‟a) you instilled sense of love, endurance and hard work. Your memory is

forever engraved in my heart. My beloved wife Milly,, daughters; Sheh, Veh, Zah

and Aisha-Tabby. You literally endured life without a father when I used to burn the

mid night oil studying. To my brother, late Wilson, sister late Dorine and brother-in-

law Salim Musa: you financially facilitated my early education. Take pride.

5

ABSTRACT

The insurance industry in Kenya has undergone a lot of changes in the recent past.

Many companies have closed shops while others have cropped up on equal measure.

There has not been a clear predictable trend on suitability of insurance industry in

Kenya. The purpose of this study was to apply the modified porters five forces model

in assessing attractiveness of insurance industry in Kenya. This was to shed light on

an industry which has witnessed death of as many companies as birth of others.

Porter‟s five forces model has been used world over to understand the competitive

forces in an industry. In specific terms, the study sought to determine how

attractiveness of insurance industry in Kenya is influenced by bargaining power of

suppliers & buyers, threat of new entrants, threat of substitute products or services,

competitive rivalry in the industry, politics, government and others. A descriptive

survey design was undertaken based on self-competition questionnaires. Data was

collected from 33 respondents out of the targeted population of 47 insurance

companies registered in Kenya. Completed questionnaires were collected and results

analyzed using descriptive statistics. Tables, mean score and standard deviation were

used for presentation and analysis. The findings of this research revealed that

Politics/Government was a minimal force with a mean of 3.44, Industry rivalry 3.59,

Barrier to entry 3.63, Threat of substitutes 3.68, bargaining power of suppliers 3.88,

and finally bargaining power of buyers 3.98. The research further identified the

Presence of Substitute Suppliers Scored a mean of 4.24, Supplier concentration 3.73,

impact of supplier on cost 3.97, supplier difference 3.48 and Importance of Volume of

business to the suppliers mean of 3.97. The study concluded that the insurance

industry in Kenya is growing and looks vibrant as perceived externally.

6

TABLE OF CONTENTS

DECLARATION………………………….………………....................ii

ACKNOWLEDDGEMENTS…………………………………………..iii

DEDICATION……..………….….……………………...……………...iv

ABSTRACT………………………….…………….……………………v

LIST OFTABLES……………………………………………...………viii

CHAPTER ONE: INTRODUCTION ..................................................................................... 1

1.1Background of the Study ...................................................................................................... 1

1.1.1 Industry Attractiveness ..................................................................................................... 2

1.1.3 Insurance Industry in Kenya ............................................................................................. 3

1.2 Research Problem ................................................................................................................ 4

1.3 Research Objective .............................................................................................................. 6

1.4 Value of the Study ............................................................................................................... 6

CHAPTER TWO: LITERATURE REVIEW .......................................................................... 15

2.1 Introduction ........................................................................................................................ 15

2.2. Theoretical Review..................................................................................................7

2.2.1 Competitive Theory………...…………………...……………………………….7

2.2.2 Industry Theory……………………………………………………………….…7

2.3 Porter‟s five forces Model……………………………...………………………….8

2.3.1 Threat of Substitute Products or Services ....................................................................... 16

2.3.2 Threat of New Entrant ...................................................................................................... 8

2.3.3 Rivarly among existing firms.......................................................................................... 10

2.3.4 Bargaining powers of suppliers ...................................................................................... 10

2.3.5 Bargaining power of buyers ............................................................................................ 19

2.4 Modified Porter's Framework…..…..…………………………………………….12

2.5 Empirical literature on industry analysis 21

2.6 Summary of the Literature……………………………………………………..14

CHAPTER THREE: RESEARCH METHODOLOGY .......................................................... 23

3.1 Introduction ........................................................................................................................ 23

3.2 Research Design................................................................................................................. 23

3.3 Population of study ............................................................................................................ 23

3.4 Data Collection .................................................................................................................. 23

3.5 Data Analysis ..................................................................................................................... 24

7

CHAPTER FOUR: DATA ANALYSIS, RESULTS AND DISCUSSIONS ……….17

4.1 Introduction ……………………………………………………………….....17

4.2 The Response Rate…………………………………………………………...17

4.3 Organisational Information………………………………………..………....17

4.3.1 Ownership Structure……………………………………………………….....18

4.3.2 Products or Service Offered ……………………………….……………...…18

4.3.3 Organisation's years in operation…………....…………………………….....19

4.4 Attractiveness of the Insurance Industry ……………………..…………......20

4.4.1 Supplier Bargaining Power ……………………………………………….....20

4.4.2 Bargaining Power of Customer/Buyers ………………………………….......22

4.4.3 Threats of New Entrants/Barrier to Entry ……………………….…….........24

4.4.4 Threat of Substitutes ……………………………………………………...…28

4.4.5 Degree of Rivalry Among Existing Firms ……………………………..........29

4.4.6 Politics/Government/Power of Other Stakeholders ……………………........32

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND

RECOMMENDATIONS ........................................................................36

5.1 Introduction …………….…………………………………………..………..36

5.2 Summary ……………………………………………………….……………36

5.3 Conclusion …………………………………………………………….…….39

5.4 Limitations of the study…………..……………………………….………….39

5.5 Recommendation …………………………….………………….…………...40

5.6 Suggestion for Policy and Practices………………………………………….40

5.7 Suggestion for Further Studies……………………………………………….40

REFERENCE ………………………………………………..…………41

APPENDIX…………………………………………………….……….44

8

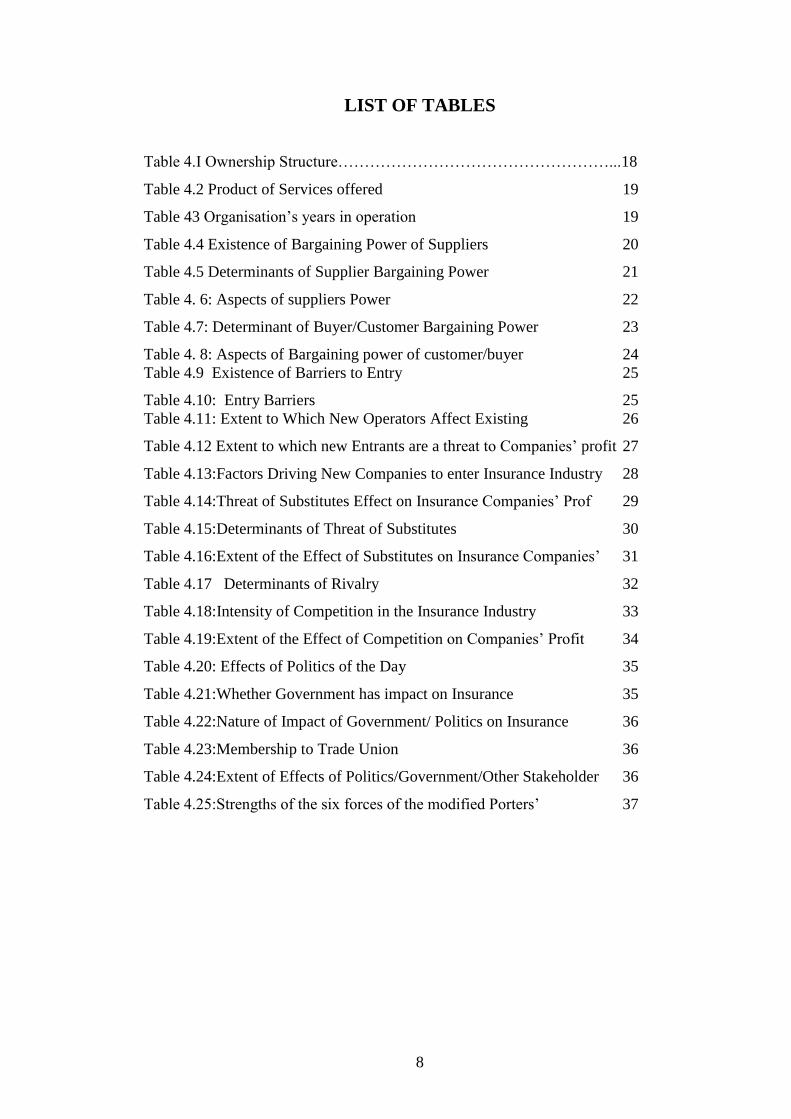

LIST OF TABLES

Table 4.I Ownership Structure……………………………………………...18

Table 4.2 Product of Services offered 19

Table 43 Organisation‟s years in operation 19

Table 4.4 Existence of Bargaining Power of Suppliers 20

Table 4.5 Determinants of Supplier Bargaining Power 21

Table 4. 6: Aspects of suppliers Power 22

Table 4.7: Determinant of Buyer/Customer Bargaining Power 23

Table 4. 8: Aspects of Bargaining power of customer/buyer 24

Table 4.9 Existence of Barriers to Entry 25

Table 4.10: Entry Barriers 25

Table 4.11: Extent to Which New Operators Affect Existing 26

Table 4.12 Extent to which new Entrants are a threat to Companies‟ profit 27

Table 4.13:Factors Driving New Companies to enter Insurance Industry 28

Table 4.14:Threat of Substitutes Effect on Insurance Companies‟ Prof 29

Table 4.15:Determinants of Threat of Substitutes 30

Table 4.16:Extent of the Effect of Substitutes on Insurance Companies‟ 31

Table 4.17 Determinants of Rivalry 32

Table 4.18:Intensity of Competition in the Insurance Industry 33

Table 4.19:Extent of the Effect of Competition on Companies‟ Profit 34

Table 4.20: Effects of Politics of the Day 35

Table 4.21:Whether Government has impact on Insurance 35

Table 4.22:Nature of Impact of Government/ Politics on Insurance 36

Table 4.23:Membership to Trade Union 36

Table 4.24:Extent of Effects of Politics/Government/Other Stakeholder 36

Table 4.25:Strengths of the six forces of the modified Porters‟ 37

9

CHAPTER ONE: INTRODUCTION

1.1 Background of the Study

Industry attractiveness is the value generated by economic activity of the industry

participants as well as the ability to share in the wealth created thereof called Profit,

(Hax & Maljuf 1983). The business world is encountering an unprecedented speed of

change, radical technologies and massive entry of new competitors. The key concern

of organizations is to continue existing over time at a profit. For this to be achieved,

organizations have to constantly adjust to their environment. In such a rapidly

changing environment, the only competitive advantage is the ability to continuously

create new sources of competitive advantage. It is imperative that organizations

continuously adopt their activities in order to ensure survival (Porter 1980, Pearce &

Robinson 1997, Hamel & Prahalad, 1999). Organizations develop & implement

competitive strategies to succeed. Competitive strategy specifies the distinctive

approach which the firm intends to use in order to succeed in each strategic business

areas. Competitive strategy gives a company an advantage over its rivals in attracting

customers and defending against competitive forces (Ansoff 1985).

Every Industry has unique structures and the greater the threat posed by an industry

force, the lesser attractive the industry becomes. Clear understanding of what forces

are on play enables business owners to formulate and implement corresponding

strategies to deal with them and consequently develop unique ways to satisfy

customers in order to obtain competitive advantage over industry rivals. Cook (1995)

notes that in any particular industry, not all the five forces will be equally

important. The five forces frame work do not eliminate the need for creativity in

finding new methods of dealing with competition within the industry but helps

managers to focus on aspects of industry structure that brings long term profitability.

Increased competition is one of the challenges presented by a dynamic environment.

The theory of competition in economics is heavily focused on price competition. A

company can gain a competitive advantage through charging lower prices than its

rivals (Murphy 2005). This is a complex phenomenon which determines whether a

firm‟s activities are appropriate and how much it contributes to profit.

10

Porters famous five forces of competitive positioning model provides a simple but

powerful perspective tool for assessing and analyzing the competitive strength and

position of a business, organization or corporation in a given industry (Porter,

1980).Firms wishing to gain a competitive edge should consider building defenses

against these forces and formulate specific courses of competitive action that can

directly influence these forces (Grundy, 2006; Grant and Jordan (2012).

1.1.1 Assessment Of Industry Attractiveness

An industry is a group of firms that market products which are close substitute for

each other (Grant 2012). For a firm to succeed in business, it is necessary to evaluate

the attractiveness of various industries in terms of their potential to generate suitable

profit. Industry attractiveness is the relative future profit potential of a market which

can be established by industry analysis. According to Hax & Majluf (1996), Industry

analysis is an orderly process that attempts to capture those structural factors that

define the long term profitability prospects of an Industry, and to identify and

characterize the behavior of the most significant competitors. Pearce and Robinson

(2005) say that industry analysis is the basis of intelligent planning. It is a systematic

process of gathering and analyzing information about an industry on a domestic and

global scope.

According to Porter (1980) a company can out-perform rivals only if it can establish a

difference that it can preserve. This is done by creating a unique and valuable

position involving a different set of activities and making trade-offs in competitive

environment. Porters (1980) notes that a firm can change the industry‟s structure

through the adopted strategies and that if the firm can shape the industry structure, it

can fundamentally change the industry attractiveness either negatively or positively.

The reasons why some companies make more profit than others lie in understanding

of competitive structure and strategic plans. Strategy is the way by which a firm

achieves its mission and attains its objectives. According to Drucker (1961), strategy

is the pattern of major objectives, purpose or goals and essential policies or plans for

achieving these goals; stated in such a way that it defines what business the company

is in or to be in and the kind of company it is or is to be. According to Barney (1997),

strategy is a pattern of resource allocation that enables firms to maintain or improve

11

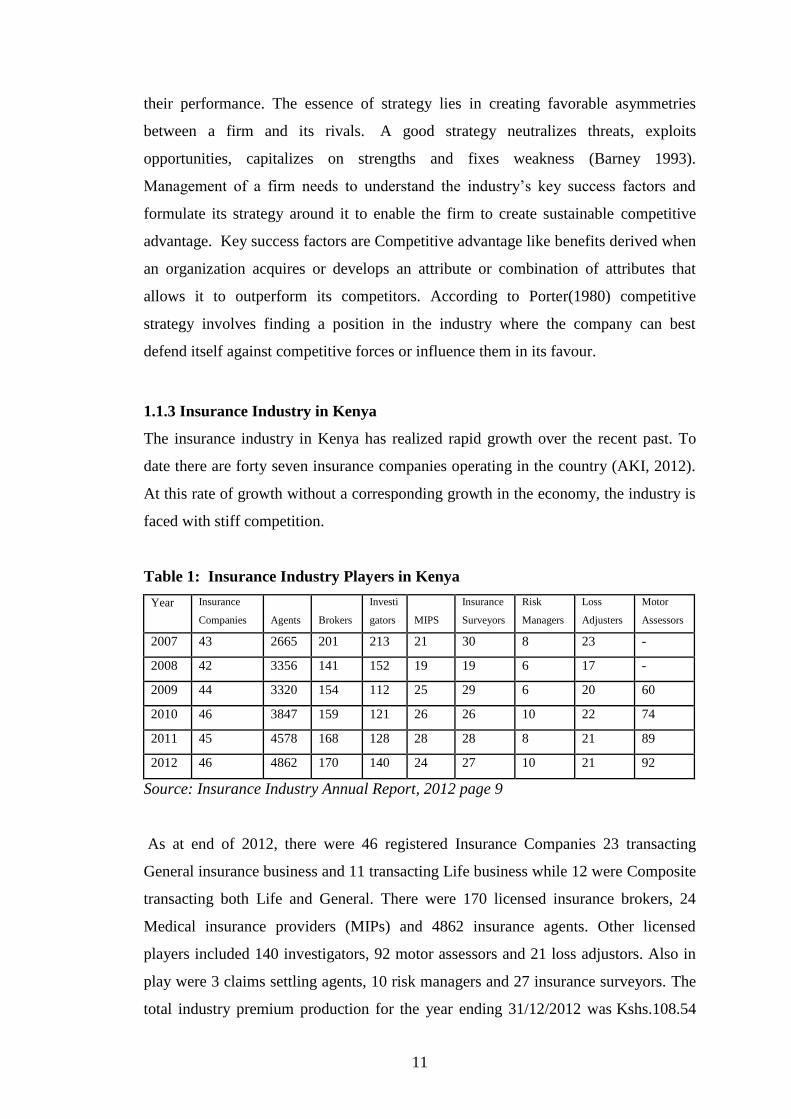

their performance. The essence of strategy lies in creating favorable asymmetries

between a firm and its rivals. A good strategy neutralizes threats, exploits

opportunities, capitalizes on strengths and fixes weakness (Barney 1993).

Management of a firm needs to understand the industry‟s key success factors and

formulate its strategy around it to enable the firm to create sustainable competitive

advantage. Key success factors are Competitive advantage like benefits derived when

an organization acquires or develops an attribute or combination of attributes that

allows it to outperform its competitors. According to Porter(1980) competitive

strategy involves finding a position in the industry where the company can best

defend itself against competitive forces or influence them in its favour.

1.1.3 Insurance Industry in Kenya

The insurance industry in Kenya has realized rapid growth over the recent past. To

date there are forty seven insurance companies operating in the country (AKI, 2012).

At this rate of growth without a corresponding growth in the economy, the industry is

faced with stiff competition.

Table 1: Insurance Industry Players in Kenya

Year Insurance

Companies

Agents

Brokers

Investi

gators

MIPS

Insurance

Surveyors

Risk

Managers

Loss

Adjusters

Motor

Assessors

2007 43 2665 201 213 21 30 8 23 -

2008 42 3356 141 152 19 19 6 17 -

2009 44 3320 154 112 25 29 6 20 60

2010 46 3847 159 121 26 26 10 22 74

2011 45 4578 168 128 28 28 8 21 89

2012 46 4862 170 140 24 27 10 21 92

Source: Insurance Industry Annual Report, 2012 page 9

As at end of 2012, there were 46 registered Insurance Companies 23 transacting

General insurance business and 11 transacting Life business while 12 were Composite

transacting both Life and General. There were 170 licensed insurance brokers, 24

Medical insurance providers (MIPs) and 4862 insurance agents. Other licensed

players included 140 investigators, 92 motor assessors and 21 loss adjustors. Also in

play were 3 claims settling agents, 10 risk managers and 27 insurance surveyors. The

total industry premium production for the year ending 31/12/2012 was Kshs.108.54

12

billion which was composed of Life Kshs.37.08 billion (34.16%) and Non-life

Kshs.71.46 billion (65.84%). Production in 2015 is projected to be Kshs.200 billion

(AKI 2012). The penetration of insurance in Kenya is estimated at 3.16%. Initiatives

such as improved regulatory framework, innovative products, adoption of alternative

distribution channels, enhanced public education and use of technology have

contributed to the improved penetration level in Kenya.

The Kenyan Insurance Industry is the leader in East Africa (Uganda, Tanzania, DRC

Congo, Rwanda) and COMESA region (Common Market for East and Southern

Africa) employing over 10,000 people. Total Annual premium in 2012 was 108.54

Billion with net claims paid being over Kshs.48.36 Billion (AKI 2012). On the top ten

by premium production (not in any order) are Jubilee, Kenindia, Heritage, APA,

ICEALION, CIC, UAP, AIG, British America and Pan Africa. They command over

50% of the market share. Insurance Industry in Kenya is regulated by the Insurance

Act Cap 487 as amended. In 2007, sections of the Act were amended which allowed

conversion of the former Office of Commissioner of Insurance under the ministry of

finance into an autonomous authority called Insurance Regulatory Authority (IRA). It

is mandated to provide general control and guidance i.e. licensing, registration,

supervision, consumer education/protection and so on.

1.2 Research Problem

Porter‟s modified “Five Forces” model is a widely used managerial tool for analyzing

potential industry margins and for classifying features which affect the competitive

environment. According to Porter (2002) Industry structures are determined by the

interplay of five forces thus; bargaining power of buyers, bargaining power of

suppliers, threat of new entrants, threat of substitute products, and intensity of

industry rivalry. Other scholars like Aosa (1997) added other forces like government,

logistics and power play. All competitive forces and their interactions are governed by

a regulatory framework that sets the „rules of the game‟ for all participants.An

industry‟s economic traits and competitive conditions and how they are expected to

change determine whether its future prospects will be poor, average, or excellent.

Industry and competitive conditions differ so much that leading companies in

unattractive industries can find it hard to earn respectable profits while weak

13

companies in attractive industries can report good performances (Porter, 1980;

Thompson and Strickland, 2003; Pearce and Robinson, 2005).

Insurance Industry in Kenya is one of the most volatile industries undergoing drastic

changes. The industry has witnessed the collapse of giant firms e.g. Kenya National

Assurance co. Ltd in 1990, Lakester, United and Blue shield among others. Over the

last 15 years, eight (8) new insurance firms have entered the industry. The rapid

collapse of existing firms and equally rapid entry of new ones sends mixed signals

about this industry. For some companies, the industry looks attractive while for others

it is bleak. In Kenya, only 8 out of the current registered 47 insurance firms

underwrite Public Service Vehicles (PSV) and out of the 6 collapsed companies 4

were underwriting PSVs ( AKI 2012). The legislation; the Insurance Act cap 487 vide

legal notice No.58 is a major barrier to entry as it stipulates that Kshs. 500M must be

deposited with the government before being licensed to carry on general and Kshs.

300M for life insurance respectively. The public perception of the industry is negative

as they always perceive insurance firms as organizations which hide under small

prints to avoid settlement of claims. Unscrupulous lawyers and fraudulent public see

the industry as cash cow while employees especially managers in public service

vehicles (PSV) underwriters view the industry as very unattractive.

.

Past studies on application of Porters five forces model have limited the scope to the

missionary five forces only without consideration to modifications. Further, no studies

have been done specifically on insurance industry in Kenya. Aosa (1997) included

three other additional forces thus government, logistics, and power play only. His

work was neither in the insurance industry nor exhaustive in terms of the modifying

factors. Muchiri (2008) studied porter‟s five forces application to assess attractiveness

of the mailing industry in Kenya while Langat (2009) anchored her studies on how the

forces shape competition in handcraft industry in Kenya. Nyale (2007) researched on

mobile telephone and Olouch (2003) applied the concept while studying the perceived

attractiveness in freight and forwarding industry Muhu (2008) researched on

perception of attractiveness of public service vehicles (PSV) insurance business in

Kenya. Kiandiko (2007) narrowed down to one of the five forces; the Entry Barrier

and studies its extent to profitability in the air pressure Industry in Kenya. All the

other known studies were therefore different in context and time. This leaves a

14

remarkable knowledge gap in terms of context and time which this research will

satisfy. This study will try to assess how attractive Insurance industry in Kenya is

using the Porters modified five forces

1.3 Research Objective

The objective of the study is to apply the Modified Porter‟s Forces Model to assess

the attractiveness of insurance industry in Kenya

1.4 Value of the Study

The study will help the current insurance companies in Kenya and those companies or

individual aspiring to invest in the insurance market to assess potentiality of the

industry

For scholars, the study will not only increase the level of literature available in

understanding how attractive Insurance Industry in Kenya is but also help in critically

analyzing and appreciating porter‟s forces model and its applicability in Kenya‟s

insurance industry.

It will also help the statutory authorities (Insurance Regulatory Authority – IRA) and

(Association of Kenya Insurers –AKI) to better understand the viability of the

industry for policy formulation and decision making.

15

CHAPTER TWO: LITERATURE REVIEW

2.1 Introduction

This chapter discusses relevant literature information on the study topic and in line

with the research objectives. The chapter begins with the theoretical foundation of the

study. The chapter ends with empirical review on attractiveness in an industry and

concluding summary of the same.

2.2 Theoretical Review

2.2.1 Competitive Theory

Industry analysis is an orderly process that attempt to capture the structural factors

that define the long-term profitability prospects to an industry. Rowe et al (1994)

define industry analysis as an environmental scan to determine what forces in a firm‟s

external environment have direct impact on its competitive position and what

competitive actions need to be taken to achieve competitive advantage. It focuses on

industries in which the firm competes (Comeford & Callagham. 1990).There is an

established relationship between business strategy, innovation and organizational

performance. In response to new technology driven global markets, companies have

increased their use of advanced technologies as well as their innovation efforts (Zahra

& Covin, 1993). The increasingly competitive environment in the financial services

market has resulted in pressure to develop and utilize alternative delivery channels

(Pearson & Robinson, 2007).

2.2.2 Industry Theory

The survival and success of an organization occurs when the organization creates and

maintains a match between its strategy and the environment and also between its

internal capability and its strategy (Grant, 2002). In order to achieve new gains for its

stakeholders and fulfill their needs and requirements, organizations must

continuously search for the development of its product and services through

marketing innovation and creativity. This will play a very important role in achieving

competitive advantage especially in the insurance industry where competition is

intense, through the forces of change brought into the industry by recapitalization and

consolidation (Business Monitor International, 2012).

16

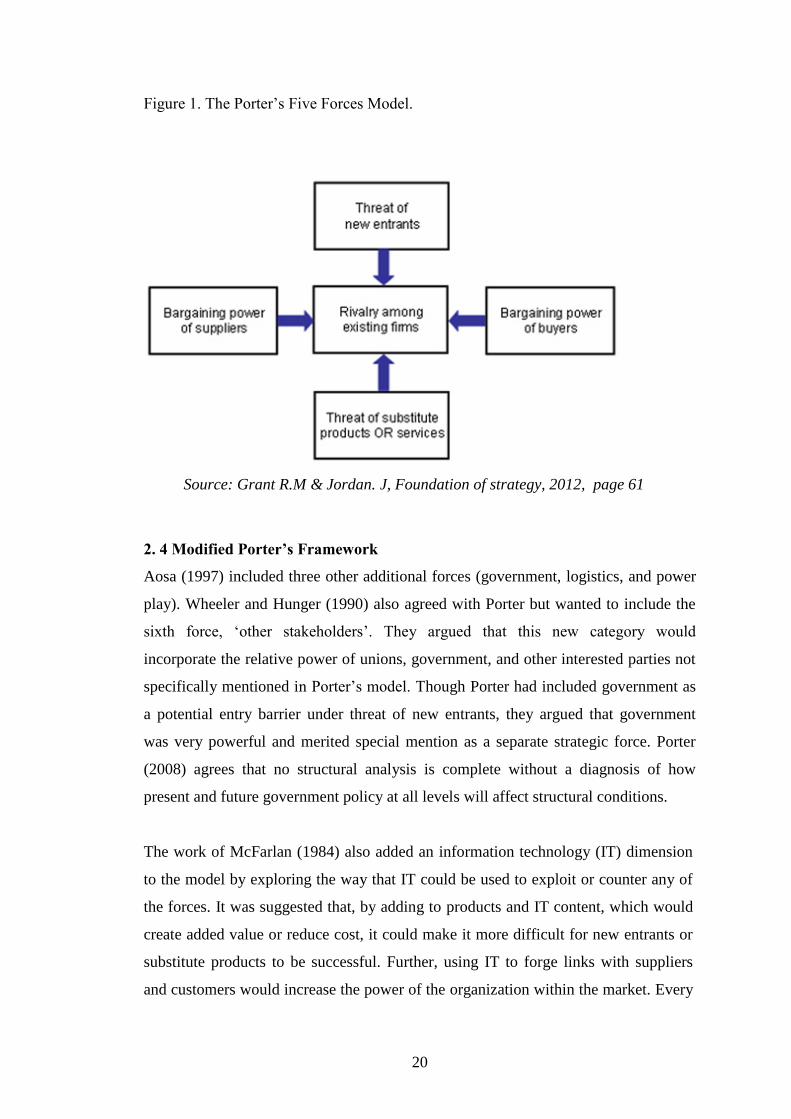

2.3 Porter’s Five Forces Model

2.3.1 Threat of Substitute Products or Services

Price to customers willing to pay for a product depends partly on the availability of

substitute products. The absence of close substitutes for a product as in the case of

Petrol or cigarettes means that consumers are comparatively insensitive to price

hence demand is inelastic with respect to price. Existence of close substitute‟s means

that customers will switch to substitutes in response to price increases for the product

hence demand is elastic with respect to price. If an industry earns a return on capital

in excess of capital, it acts like a magnet to attract firms outside the industry. If entry

of new firms is unrestricted, the rate of profit will fall towards its competitive

level. Threat of entry rather than actual entry may be sufficient to ensure that

established firms constrain their prices to the competitive level.

New entrants in an industry contribute to extra capacity, technology, desire to gain

market share and so on. In microeconomics theory, the entry is a response to the

prevailing industry attractiveness as manifested in profit margin enjoyed by the

industry operating companies. However, according to Geroski (1995), there is

evidence that entry reacts slowly to high expected profits and that only important

differences of expected profits among industries may lead to different rates of entry

hence profits are a sign of industry attractiveness only if they are relatively high and

the response by potential entrants is slow. One may therefore reason that speed of

entry as a reaction to high profit may depend on other factors connected with an entry

of new firms such as capital and technology requirements, transaction costs and so

on. However, these factors are mainly industry specific hence leading to a conclusion

that entry reaction to high profit industry may depend on industry itself, (Barbot,

2001).

2.3.2 Threat of New Entrant

Entry barrier is the major factor determining the speed and magnitude of threat of

new entrants and can also be considered to be low or high depending on the resources

and competencies of the potential entrants. With high sustainable profits, new

entrants will be attracted in large numbers and will highly be motivated to commit

any level of needed resources to negate the barriers to entry. In this case, relevance

17

of entry barrier diminishes. According to Keegan (1995), the entry of new players

disrupts the level of Industry‟s profitability by increasing the industry capacity and

reducing the price leading to reduced profit margin; the law of demand and supply.

The barrier can be maintained by having unique capabilities which cannot be copied

by competitor making it easy for the firm to enter the industry but unacceptably

difficult for everybody else.(Hax & Majluf, 1996). Industry growth is another

important determinant of entry as growing industries attract new firms and vice

versa. An industry where no barriers to entry or exit exists is contestable; prices and

profits tend towards the competition level regardless of the number of firms within

the industry (Grant & Jordan, 2012). Contestability depends on the absence of sunk

costs i.e. investments whose values cannot be recovered. Absence of such costs make

an industry vulnerable to „hit-and-run‟ entry wherever established firms raise their

prices above the competitive level (Grant & Jordan, 2012).

Capital cost of getting established may also be a hindrance to entry. Product

differentiation is another entry deterrent. In an industry where products are highly

differentiated, established firms possess the advantage of brand recognition and

customer loyalty. This will force new entrants to spend heavily on promotion and

advertisement to gain brand awareness and goodwill. Control of channel of

distribution may also work as a barrier to entry. Limited capacity within distribution

channels example. Brokers, Agents, and Banks. Big Brokers and Agents have already

placed their loyalty in some few companies. Economists from the Chicago school

theorize that the only effective barriers to entry are those created by government

(Legal barriers) (Grant & Jordan, 2012). Barriers to entry also depends on the

entrants expectations as to possible retaliation by established firms. This may take the

firm of increased advertising, price cutting or even litigation.

For most industries, the major determinant of the overall state of competition and the

general level of probability is competition among the firms within the industry. In

some industries, firms compete aggressively pushing prices below cost hence

industry wide losses. In other industries, price competition is muted and rivalry

focuses on advertising, innovation and service quality. Concentration of sellers; as

measured by concentration ratio is one of the methods of measuring intensity of

competition between established firms. Seller‟s concentration refers to the number

18

and size distribution of firms competing within a market. Diversity of competitors

and product differentiation also helps in measuring the inter industry rivalry. The

more similar the offerings among rival firms, the more willing are customers to

switch between them and the greater inducements for firms to cut prices to boost

sales. Where products of rival firms are virtually indistinguishable, price is the sole

basis for competition. Excess capacity and exit barriers also help to ascertain the

intensity of intra industry competition. Unused capacity encourages firms to offer

price cuts to attract new business while barrier to exits are costs associated with

capacity leaving an industry e.g. where resources are durable and specialized and

employees entitled to Job protection, emotional ties, government or social restrictions

and the like.

2.3.3 Rivalry among existing firms

Competitive strategy aims to establish a sustainable profitable position against the

forces that determine industry competition (Porter 2002). The choice of competitive

strategy depends on attractiveness for long-term profitability and factors that

determine it, not all industries offer equal opportunity for sustained profitability

which is an essential ingredient in determining the profitability of a

firm. Determinants of relative competitive position within an industry helps to

explain why some firms are more profitable than others regardless of average

profitability of the industry. A firm in a very attractive industry may still not earn

attractive profit if it has chosen a poor competitive position. Conversely, a firm in an

excellent competitive position may be in such a poor industry, that it is not very

profitable. Industries become more or less attractive over time and competitive

position reflects a sustained war among competitors. Even long period of stability

can be ended abruptly by competitive moves (Anker, 1998).

2.3.4 Bargaining powers of suppliers

There are a number of strategic options for high performance and success. These are

product and service innovation, super customer service, geographical expansion &

product differentiation, sales promotion and so on. The intensity of competition

tends to increase when an industry is characterized by a number of well balanced

competitors, a slow rate of industry growth, high fixed costs and lack of

differentiation between products. According to Cook (1995) supplies to organizations

19

refer to all those sources of inputs that the organization need to provide goods and

services. Powerful suppliers can connive to bring down profits in an industry by

raising prices or reducing quality of supplied goods and services. Suppliers

bargaining power is high when; market is dominated by a few powerful large

suppliers as opposed to small and weak fragmented source, when there are no

substitute to a product or service, high switching costs, high possibility of forward

integration.

Singh and Wah (1997) concluded that firms and their suppliers needed to have a good

relationship for their mutual benefit. Leverick and Cooper (1998) observed that

organizations have tended to move away from adversarial relationship with suppliers

towards a more cooperative way of doing business. The bargaining power of

suppliers determines the costs of raw materials and other inputs. Suppliers power can

affect the relationship between a small business and its customers by influencing the

quality and price of the final product (Porter 2003). In the insurance industry, effect

of suppliers are seen in computer hardware and software, office equipment,

stationery and so on.

2.3.5 Bargaining power of buyers

Buyers are those who use the products or services of an organization. Before buying

a product, a consumer collects information from various sources which then goes

through the consumer buying process till decision to buy is made. Buyers will

normally compete with the industry by bargaining for lower prices, high quality

products or services. Buyer power is high when the volume of purchase of the

buyer is high, there are alternative source of supply, cost of switching supplies is low,

there is threat of backward integration; buyers have full information of demand,

actual market price and supplies costs. Powerful buyers can exert pressure on

business by demanding lower prices, higher quality services and even playing off

competitors against one another. The strength of buying power that firms face from

their customers depends on two factors thus buyer‟s price sensitivity and relative

bargaining power. Price sensitivity is the extent to which buyers respond to a firm‟s

price changes in an industry.

20

Figure 1. The Porter‟s Five Forces Model.

Source: Grant R.M & Jordan. J, Foundation of strategy, 2012, page 61

2. 4 Modified Porter’s Framework

Aosa (1997) included three other additional forces (government, logistics, and power

play). Wheeler and Hunger (1990) also agreed with Porter but wanted to include the

sixth force, „other stakeholders‟. They argued that this new category would

incorporate the relative power of unions, government, and other interested parties not

specifically mentioned in Porter‟s model. Though Porter had included government as

a potential entry barrier under threat of new entrants, they argued that government

was very powerful and merited special mention as a separate strategic force. Porter

(2008) agrees that no structural analysis is complete without a diagnosis of how

present and future government policy at all levels will affect structural conditions.

The work of McFarlan (1984) also added an information technology (IT) dimension

to the model by exploring the way that IT could be used to exploit or counter any of

the forces. It was suggested that, by adding to products and IT content, which would

create added value or reduce cost, it could make it more difficult for new entrants or

substitute products to be successful. Further, using IT to forge links with suppliers

and customers would increase the power of the organization within the market. Every

21

industry feels the influence of other forces like politics of the day, government,

employees and special groups, the public, lobby groups and registered trade unions

and so on hence called the sixth force. The sixth force either influence industry

attractiveness through all the main five forces or act as a separate force

2.5 Empirical literature on industry analysis

Illangakon (2010) on Analysis of Industry attractiveness using Porter's five forces in

UK music Industy examined and concluded that the universal applicability of music

as a form of entertainment may remain to be the largest selling proposition for this

industry and is the largest reason behind the high profitability of the industry. In

conclusion therefore, it can be said that applying five forces theory is extremely

important in industry analysis as it allows firms to develop better strategies through

identification of forces operating in the market and understanding of overall

attractiveness of the industry.

Cafferky (2005) in The Porter Five-forces Industry Analysis Framework For

Religious Nonprofits in the USA contends that the profitability (and correspondingly

attractiveness) of an industry is a function of the cumulative effect of the five forces.

Profitability of the religious “industry” is not meaningful if discussed in terms of

marginal costs versus marginal revenues. What is needed is a better description of the

outcome of the five forces in the religious industry. Share of world-view and mind-set

advantages versus the tradeoffs for the consumer may offer descriptions of outcomes

more relevant than profit though exceedingly difficult to measure. Aldrichs (1979)

concept of environmental capacity, richness and leanness may be helpful in

understanding the environment in which religious non profit organizations operate.

Vengesayi (2009) on A conceptual model of tourism destination Competitiveness and

Attractiveness examined that there have been advances in modeling competitiveness

in tourism but there is little empirical evidence to support the models proposed by

researchers. The symmetrical approach to tourism destination evaluation should be a

starting point in harmonizing the interests of the destination as well as those of the

tourists. The results of such an approach could be used to sell the destination interests

to visitors as well as the interests of visitors to the destination operators. Researchers

22

now need to move from conceptual to empirical validation of the proposed models.

Initially the challenge should be to investigate the relationship between the identified

variables and how strongly they influence the attractiveness and competitiveness of

tourism destinations.

In Kenya, studies that have been conducted focused only on the application of the

ordinary Porter‟s Five Forces Model without the modification. However, Waithaka

(2001), studied funeral industry attractiveness and adopted the modified model

advanced by Aosa (1997), which included three other additional forces (government,

logistics, and power play). These forces were found to define the structure of the

funeral industry. The same modified model has been applied by Oluoch (2003) in

studying the perceived attractiveness of the freight and forwarding industry. Other

studies that have adopted Porter‟s Five Forces Model include those of Nyale (2007)

who researched on mobile telephony and Wachira (2008) in the insurance industry.

The studies are also in support of the views advanced by Aosa, (1997) Osigweh,

(1989) Hussey,(1990) and Austin, (1991) that management is sensitive to the context

in which it is practiced and that strategic management models advanced in developed

countries where strategic management originated may not be directly applicable in

developing African countries.

2.6 Summary of the literature Review

The Kenyan insurance industry is experiencing intensified competition and

regulations. This study will analyze the „big picture‟ of the insurance industry in

Kenya through Porter‟s Modified Five Forces model of competition. It will also

examine the key players aligned with the Modified Five Forces and their impact on

competition and industry Profitability in Kenya. Finally, it will assess attractiveness

of the insurance industry in Kenya through the modified porter‟s model.

23

CHAPTER THREE: RESEARCH METHODOLOGY

3.1 Introduction

This chapter focuses on the methodology that will be employed in the research

project. It details the research design, population under study, sampling technique

used, nature of the data collected and method of data analysis.

3.2 Research Design

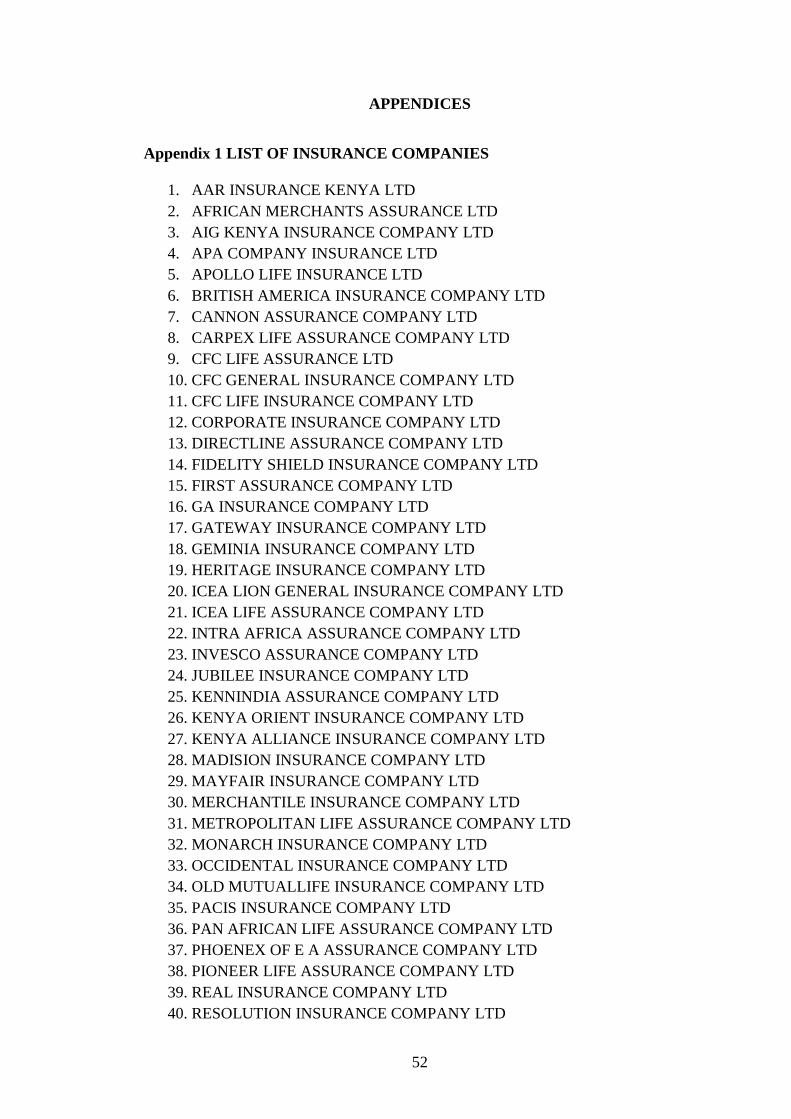

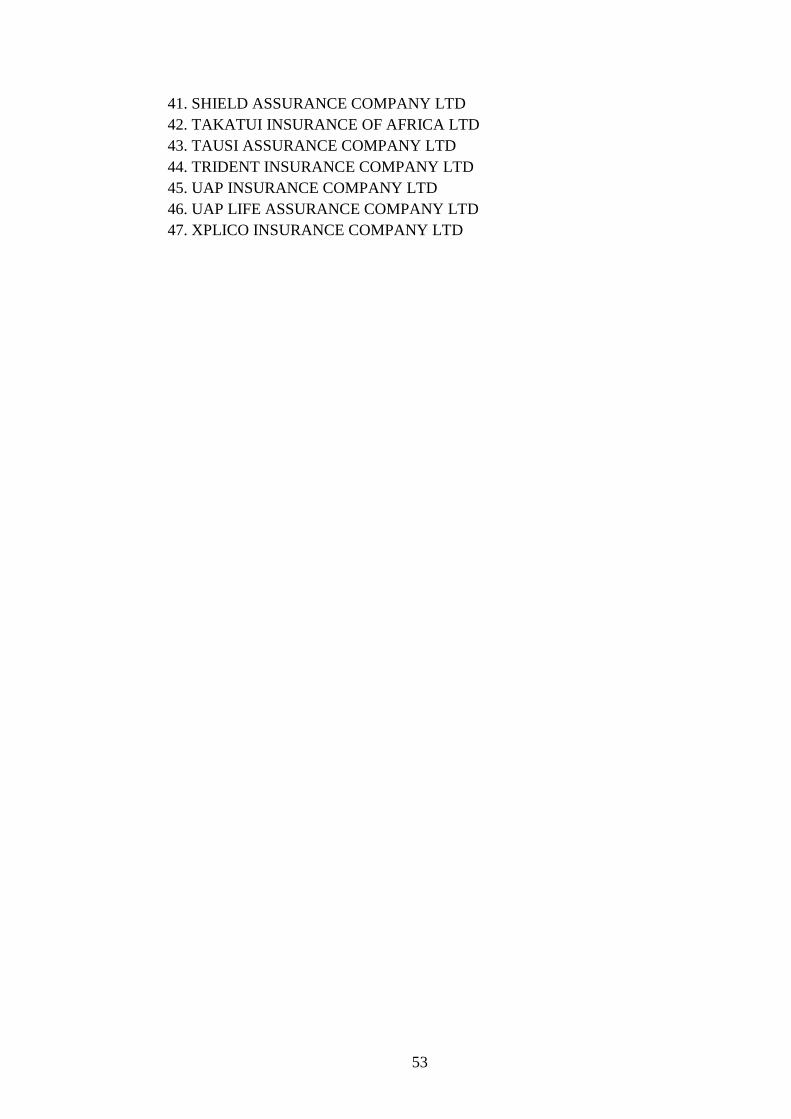

The study was a descriptive survey of all the 47 Insurance companies registered in

Kenya and are members of The Association of Kenya Insurers (Appendix 2). It was

carried out by descriptive survey design which is favoured because it

describes the state of affairs as it exist at present (Kothari 2003). The researcher

wanted to assess the attractiveness of insurance industry at the moment.

According to Donald and Pamela (1998) a descriptive study was concerned with

finding out the what, where and how of a phenomenon, hence the how, or how not

attractive the insurance industry in Kenya is and due to what forces. The design

involved primary research methods and field research involved collection of primary

data.

3.3 Population of study

Population of interest in this Study was all the Insurance companies registered in

Kenya comprising 47 companies which are registered with the Association of Kenya

Insurers (Appendix 1).

3.4 Data Collection

A population is defined as a complete set of elements with some common observable

characteristics, Mugenda and Mugenda (1999). The study used primary data which

are largely descriptive in nature. Data was collected by Structured questionnaire due

to convenience of facilitating collection of large amount of data in a given sector of

the economy. It captures respondense‟s feeling and makes comparison and analysis

easy (Kibera and Wariunge). The researcher identified the targeted individual

respondents from each insurance company and wrote introductory letter together with

24

questionnaire to them. The questionnaire dwelt on the modified Porter‟s five forces

model which was regarded as variables. Question format embraced Five Point likert

scale. It targeted Chief Executive Officers because the research is intended for

officers at policy formulation levels who are able to appreciate the industry

challenges. Method of distribution was by hand delivery to respondents and

collecting later. This method is favored due to its convenience.

3.5 Data Analysis

Descriptive statistical method was used because the research questions are descriptive

in nature. The data was presented using tables for further analysis and to facilitate

comparison. Quantitative data was analyzed using descriptive statistics such as

frequencies, percentages, mean score and standard deviation. Data from open ended

questions was analyzed thematically according to objectives and research questions

after categorizing and allocating points for each answer. Inferences and conclusions

were then drawn from the analyzed data. The mean of the points was computed by

use of Statistics for Practices of Social and Sciences ( SPSS). While mean scores

measures the average, Standard deviation connotes the disparity from the central

tendency.

25

CHAPTER FOUR: DATA ANALYSIS, RESULTS AND DISCUSSIONS

4.1 Introduction

This chapter presents analysis and findings of the study as set out in the research

methodology. The results are presented in line with objectives of the study which was

to assess attractiveness of insurance industry in Kenya by application of Porter‟s

modified five forces model. The data was gathered using questionnaires which was

designed in two sections. The first section covered brief background information of

the insurance companies while second section covered the information on Porter‟s

modified five forces. The likert scale of 1 to 5 points was used in which I meant No

or low effect while 5 meant very high effect. Statistical tools like means, percentages

were employed to analysed data and presentation done in table form.

4.2 The Response Rate

The response rate is the return rate expressed as a percentage of total number of

questionnaires the researcher gave out. The study targeted the 47 Insurance

Companies operation in Kenya and registered as members of the Association of

Kenya Insurers (AKI). Out of the 47 questionnaires given out, 33 were completed

and returned in good time for analysis. The response rate was therefore 70.2% which

was considered fair and representative. According to Mugenda and Mugenda (1999)

a responses rate of 50% is considered adequate for reporting, 60% is good and 70% is

very good. The researcher initially called respective managing directors in advance to

request for their assistance in completing the questionnaire. After a short period soft

copies were sent followed by hard copies dropped for those who alleged to had not

received the soft copies. Respondents who did not respond to the questionnaire cited a

number of reasons including busy schedules, targeted personnel being out of the

country and some deliberately refused to divulge any information.

4.3 Organisational Information

This aspect was analysed based on ownership structure, age of the company and the

products and/or services offered. This aspect of organization information was

considered relevant as it facilitates proper understanding of the insurance industry.

26

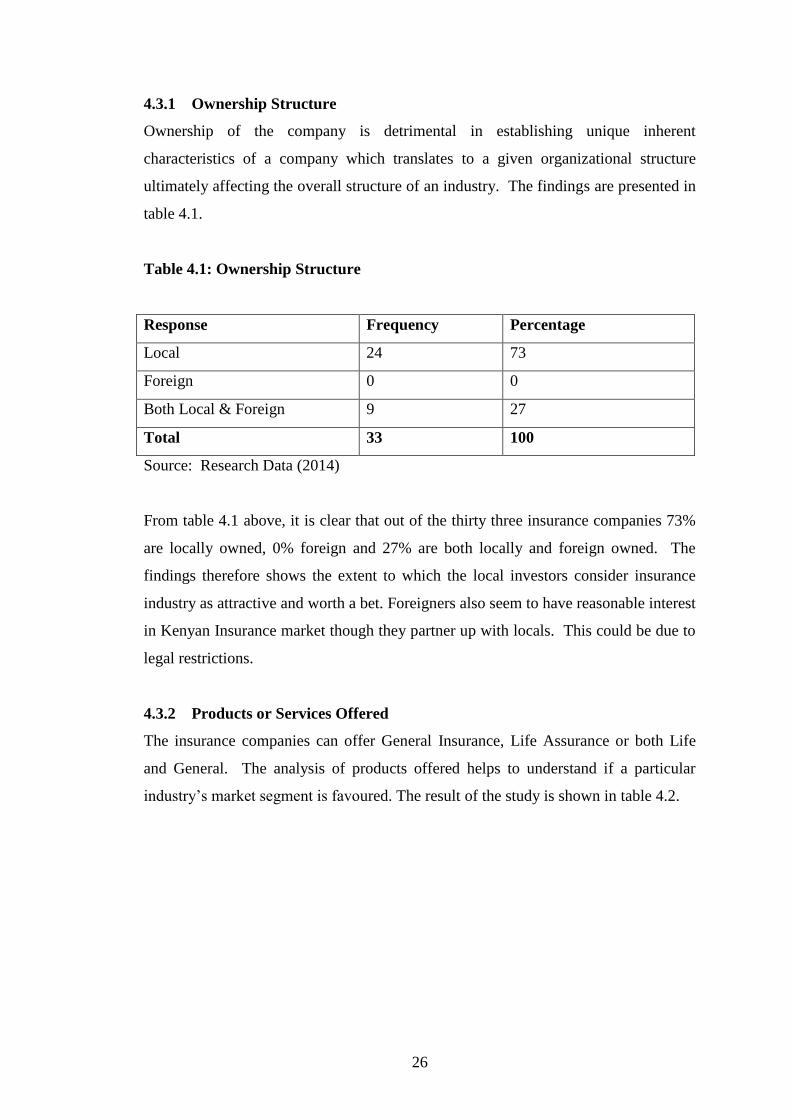

4.3.1 Ownership Structure

Ownership of the company is detrimental in establishing unique inherent

characteristics of a company which translates to a given organizational structure

ultimately affecting the overall structure of an industry. The findings are presented in

table 4.1.

Table 4.1: Ownership Structure

Response Frequency Percentage

Local 24 73

Foreign 0 0

Both Local & Foreign 9 27

Total 33 100

Source: Research Data (2014)

From table 4.1 above, it is clear that out of the thirty three insurance companies 73%

are locally owned, 0% foreign and 27% are both locally and foreign owned. The

findings therefore shows the extent to which the local investors consider insurance

industry as attractive and worth a bet. Foreigners also seem to have reasonable interest

in Kenyan Insurance market though they partner up with locals. This could be due to

legal restrictions.

4.3.2 Products or Services Offered

The insurance companies can offer General Insurance, Life Assurance or both Life

and General. The analysis of products offered helps to understand if a particular

industry‟s market segment is favoured. The result of the study is shown in table 4.2.

27

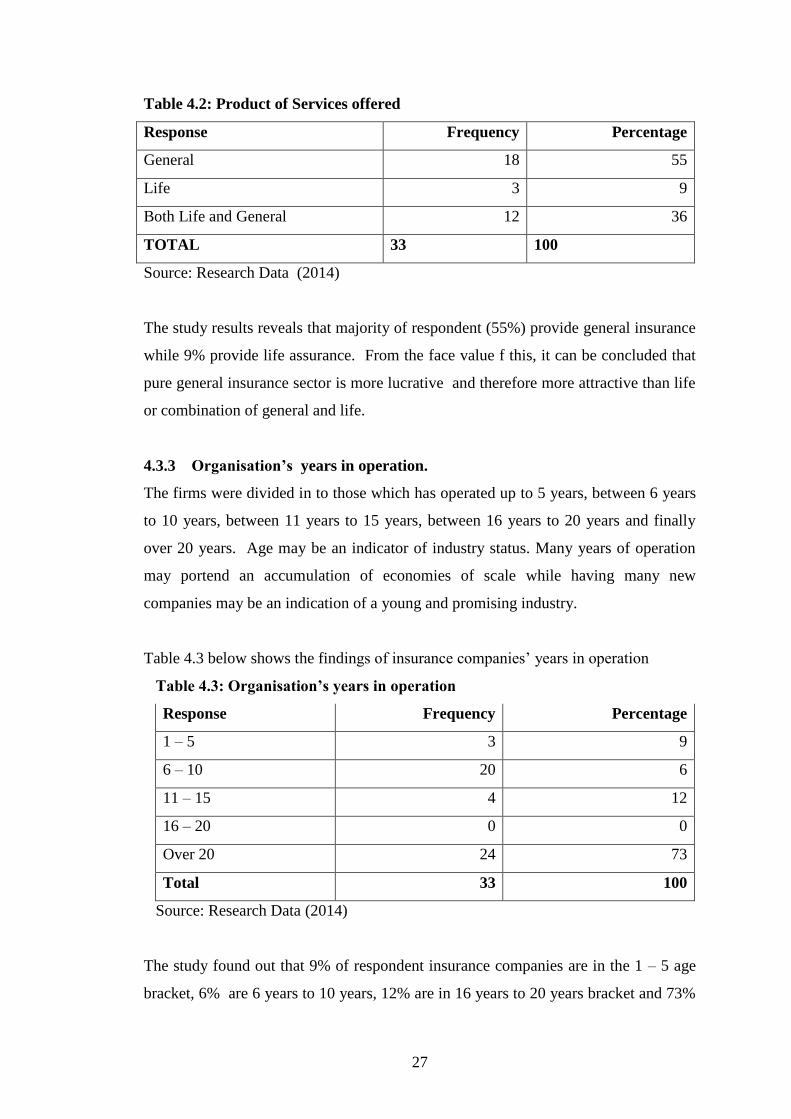

Table 4.2: Product of Services offered

Response Frequency Percentage

General 18 55

Life 3 9

Both Life and General 12 36

TOTAL 33 100

Source: Research Data (2014)

The study results reveals that majority of respondent (55%) provide general insurance

while 9% provide life assurance. From the face value f this, it can be concluded that

pure general insurance sector is more lucrative and therefore more attractive than life

or combination of general and life.

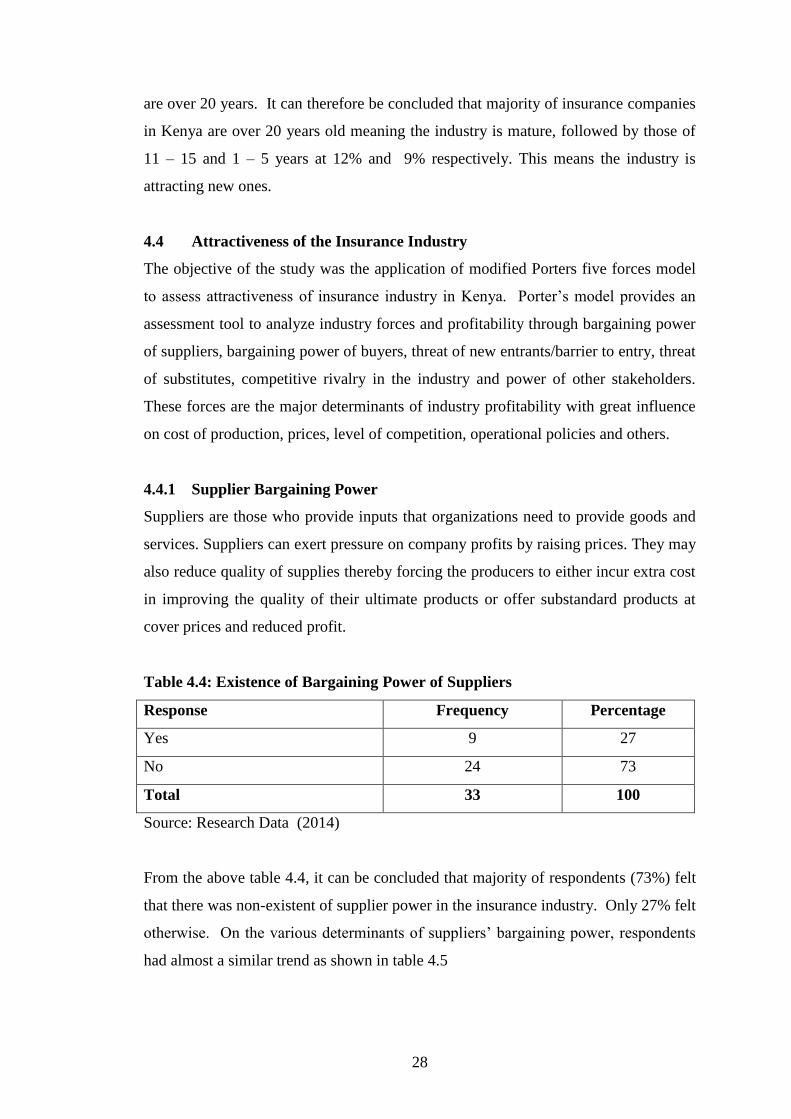

4.3.3 Organisation’s years in operation.

The firms were divided in to those which has operated up to 5 years, between 6 years

to 10 years, between 11 years to 15 years, between 16 years to 20 years and finally

over 20 years. Age may be an indicator of industry status. Many years of operation

may portend an accumulation of economies of scale while having many new

companies may be an indication of a young and promising industry.

Table 4.3 below shows the findings of insurance companies‟ years in operation

Table 4.3: Organisation’s years in operation

Response Frequency Percentage

1 – 5 3 9

6 – 10 20 6

11 – 15 4 12

16 – 20 0 0

Over 20 24 73

Total 33 100

Source: Research Data (2014)

The study found out that 9% of respondent insurance companies are in the 1 – 5 age

bracket, 6% are 6 years to 10 years, 12% are in 16 years to 20 years bracket and 73%

28

are over 20 years. It can therefore be concluded that majority of insurance companies

in Kenya are over 20 years old meaning the industry is mature, followed by those of

11 – 15 and 1 – 5 years at 12% and 9% respectively. This means the industry is

attracting new ones.

4.4 Attractiveness of the Insurance Industry

The objective of the study was the application of modified Porters five forces model

to assess attractiveness of insurance industry in Kenya. Porter‟s model provides an

assessment tool to analyze industry forces and profitability through bargaining power

of suppliers, bargaining power of buyers, threat of new entrants/barrier to entry, threat

of substitutes, competitive rivalry in the industry and power of other stakeholders.

These forces are the major determinants of industry profitability with great influence

on cost of production, prices, level of competition, operational policies and others.

4.4.1 Supplier Bargaining Power

Suppliers are those who provide inputs that organizations need to provide goods and

services. Suppliers can exert pressure on company profits by raising prices. They may

also reduce quality of supplies thereby forcing the producers to either incur extra cost

in improving the quality of their ultimate products or offer substandard products at

cover prices and reduced profit.

Table 4.4: Existence of Bargaining Power of Suppliers

Response Frequency Percentage

Yes 9 27

No 24 73

Total 33 100

Source: Research Data (2014)

From the above table 4.4, it can be concluded that majority of respondents (73%) felt

that there was non-existent of supplier power in the insurance industry. Only 27% felt

otherwise. On the various determinants of suppliers‟ bargaining power, respondents

had almost a similar trend as shown in table 4.5

29

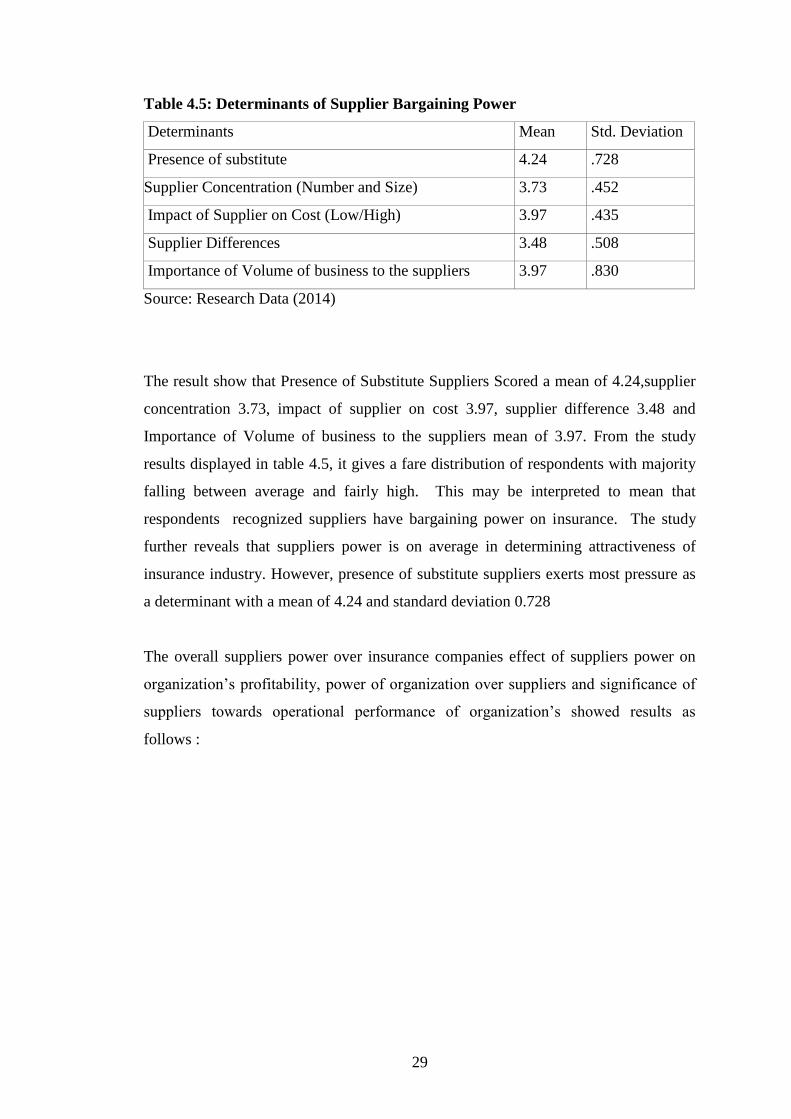

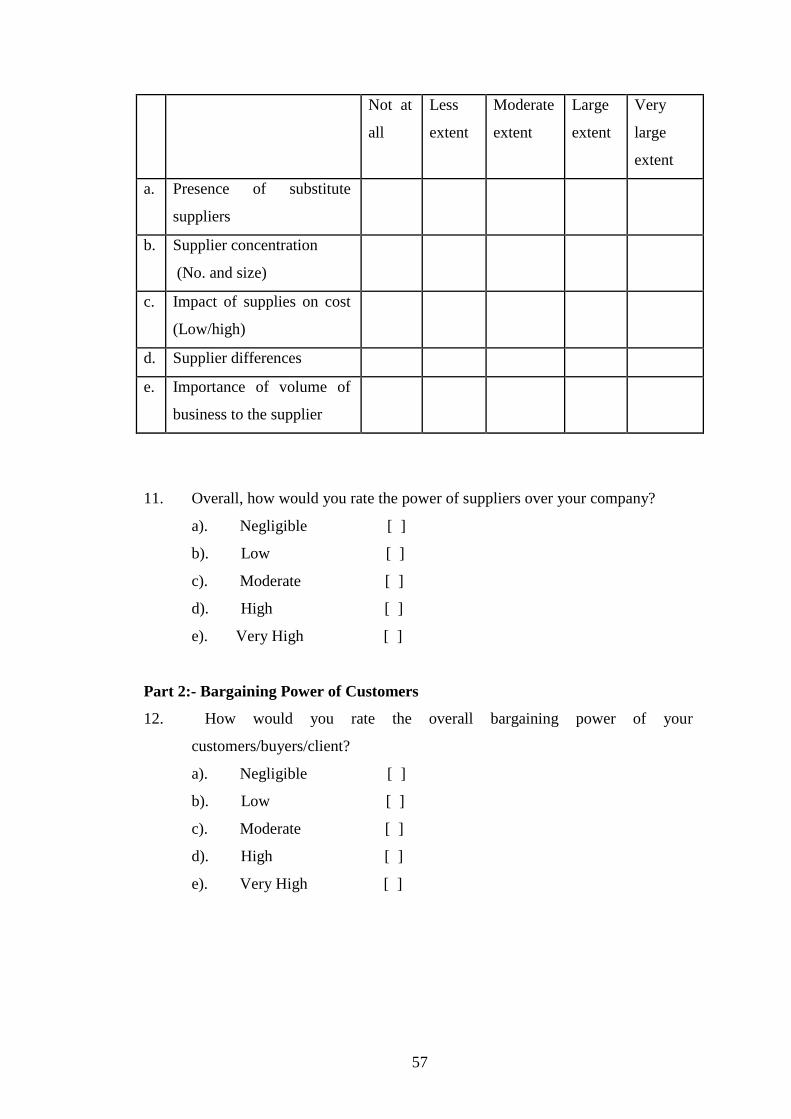

Table 4.5: Determinants of Supplier Bargaining Power

Determinants Mean Std. Deviation

Presence of substitute 4.24 .728

Supplier Concentration (Number and Size) 3.73 .452

Impact of Supplier on Cost (Low/High) 3.97 .435

Supplier Differences 3.48 .508

Importance of Volume of business to the suppliers 3.97 .830

Source: Research Data (2014)

The result show that Presence of Substitute Suppliers Scored a mean of 4.24,supplier

concentration 3.73, impact of supplier on cost 3.97, supplier difference 3.48 and

Importance of Volume of business to the suppliers mean of 3.97. From the study

results displayed in table 4.5, it gives a fare distribution of respondents with majority

falling between average and fairly high. This may be interpreted to mean that

respondents recognized suppliers have bargaining power on insurance. The study

further reveals that suppliers power is on average in determining attractiveness of

insurance industry. However, presence of substitute suppliers exerts most pressure as

a determinant with a mean of 4.24 and standard deviation 0.728

The overall suppliers power over insurance companies effect of suppliers power on

organization‟s profitability, power of organization over suppliers and significance of

suppliers towards operational performance of organization‟s showed results as

follows :

30

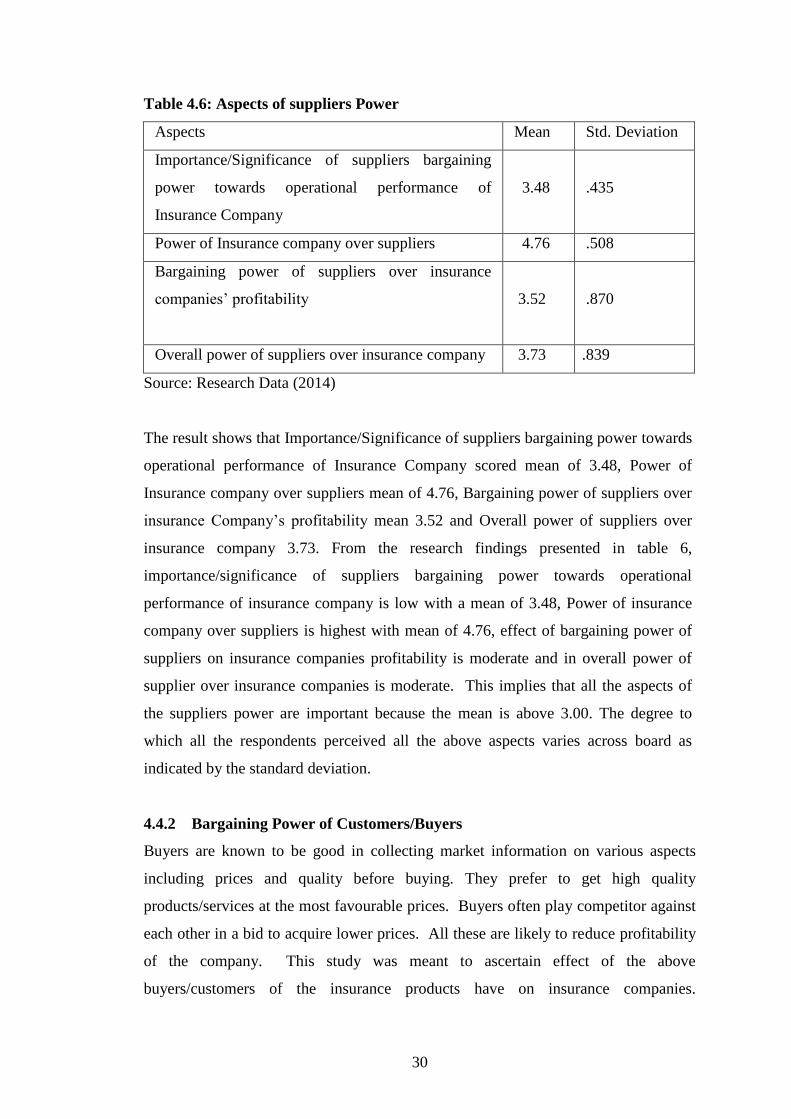

Table 4.6: Aspects of suppliers Power

Aspects Mean Std. Deviation

Importance/Significance of suppliers bargaining

power towards operational performance of

Insurance Company

3.48 .435

Power of Insurance company over suppliers 4.76 .508

Bargaining power of suppliers over insurance

companies‟ profitability

3.52 .870

Overall power of suppliers over insurance company 3.73 .839

Source: Research Data (2014)

The result shows that Importance/Significance of suppliers bargaining power towards

operational performance of Insurance Company scored mean of 3.48, Power of

Insurance company over suppliers mean of 4.76, Bargaining power of suppliers over

insurance Company‟s profitability mean 3.52 and Overall power of suppliers over

insurance company 3.73. From the research findings presented in table 6,

importance/significance of suppliers bargaining power towards operational

performance of insurance company is low with a mean of 3.48, Power of insurance

company over suppliers is highest with mean of 4.76, effect of bargaining power of

suppliers on insurance companies profitability is moderate and in overall power of

supplier over insurance companies is moderate. This implies that all the aspects of

the suppliers power are important because the mean is above 3.00. The degree to

which all the respondents perceived all the above aspects varies across board as

indicated by the standard deviation.

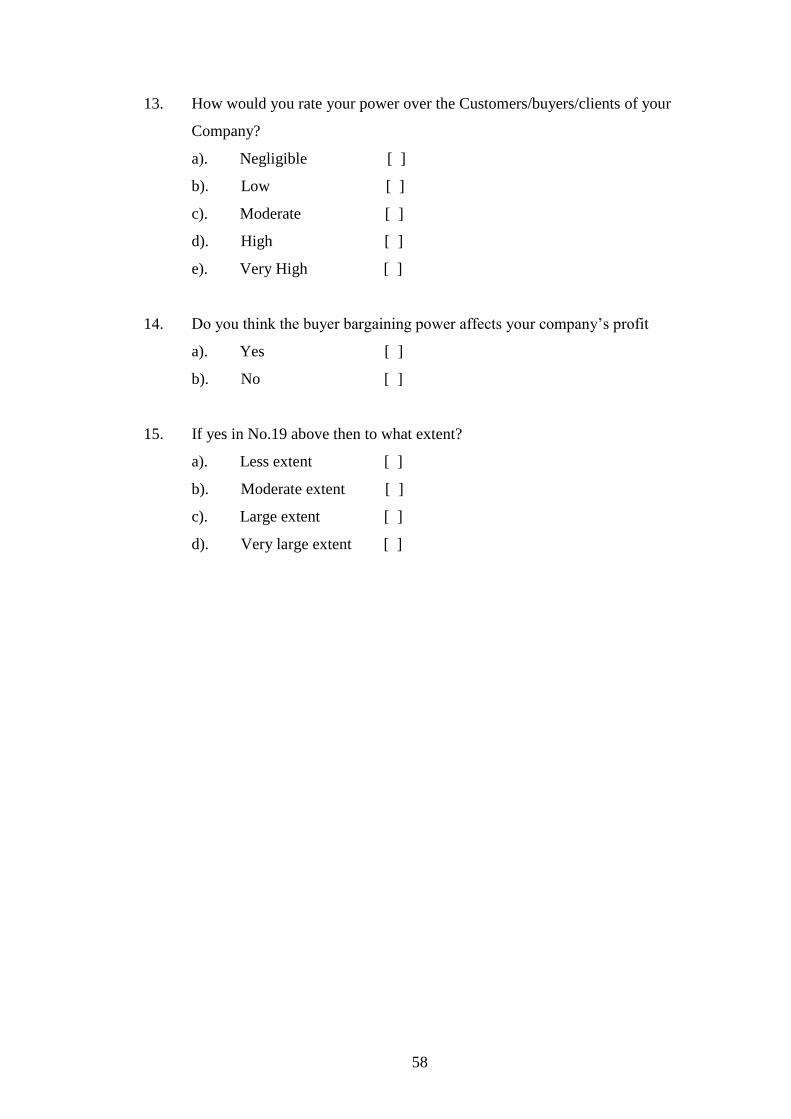

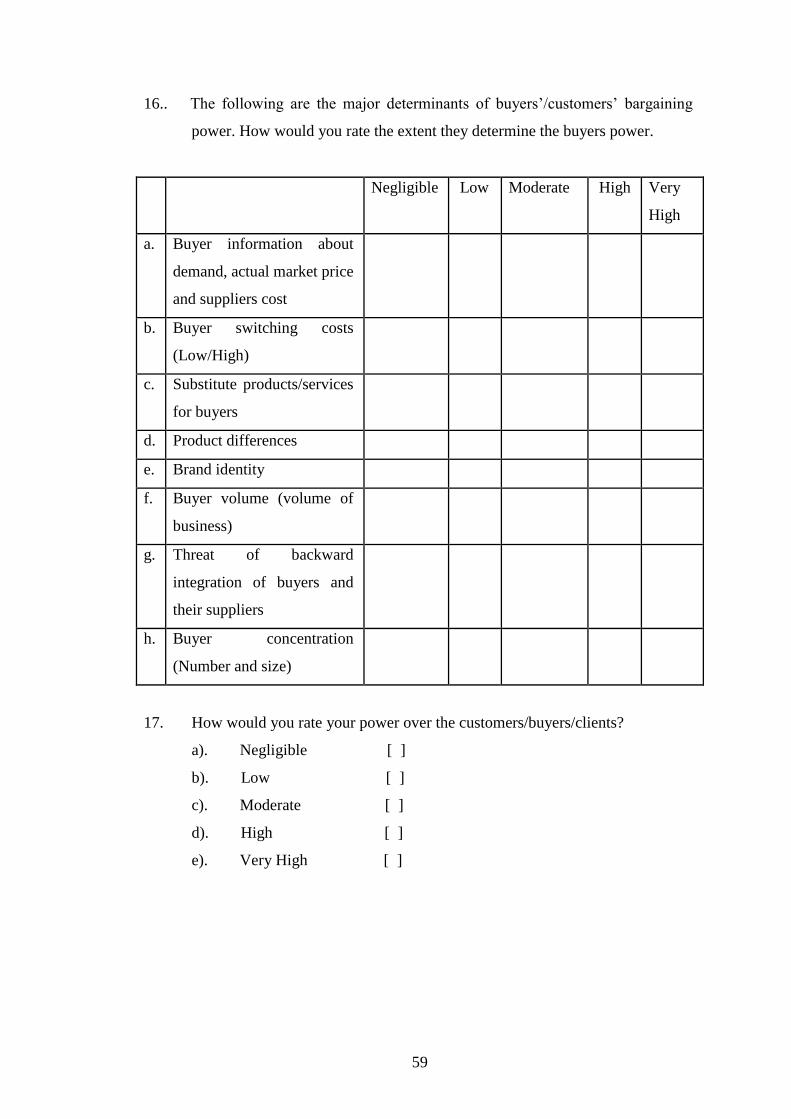

4.4.2 Bargaining Power of Customers/Buyers

Buyers are known to be good in collecting market information on various aspects

including prices and quality before buying. They prefer to get high quality

products/services at the most favourable prices. Buyers often play competitor against

each other in a bid to acquire lower prices. All these are likely to reduce profitability

of the company. This study was meant to ascertain effect of the above

buyers/customers of the insurance products have on insurance companies.

31

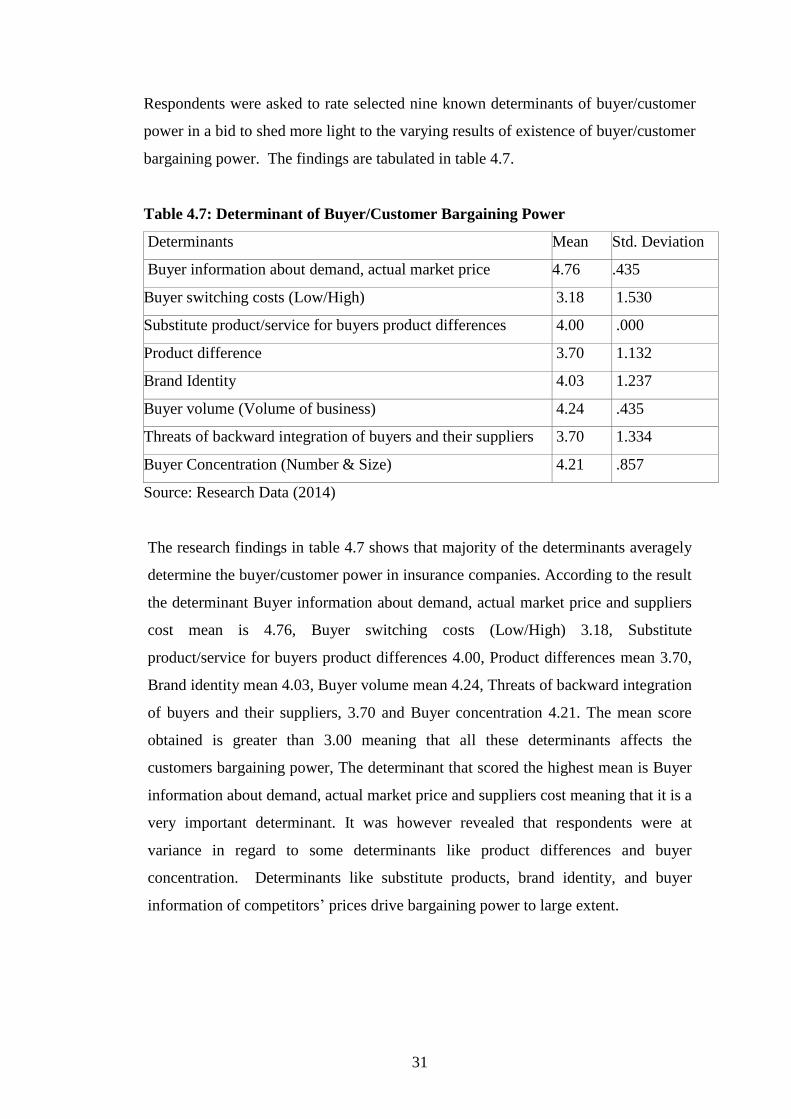

Respondents were asked to rate selected nine known determinants of buyer/customer

power in a bid to shed more light to the varying results of existence of buyer/customer

bargaining power. The findings are tabulated in table 4.7.

Table 4.7: Determinant of Buyer/Customer Bargaining Power

Determinants Mean Std. Deviation

Buyer information about demand, actual market price 4.76 .435

Buyer switching costs (Low/High) 3.18 1.530

Substitute product/service for buyers product differences 4.00 .000

Product difference 3.70 1.132

Brand Identity 4.03 1.237

Buyer volume (Volume of business) 4.24 .435

Threats of backward integration of buyers and their suppliers 3.70 1.334

Buyer Concentration (Number & Size) 4.21 .857

Source: Research Data (2014)

The research findings in table 4.7 shows that majority of the determinants averagely

determine the buyer/customer power in insurance companies. According to the result

the determinant Buyer information about demand, actual market price and suppliers

cost mean is 4.76, Buyer switching costs (Low/High) 3.18, Substitute

product/service for buyers product differences 4.00, Product differences mean 3.70,

Brand identity mean 4.03, Buyer volume mean 4.24, Threats of backward integration

of buyers and their suppliers, 3.70 and Buyer concentration 4.21. The mean score

obtained is greater than 3.00 meaning that all these determinants affects the

customers bargaining power, The determinant that scored the highest mean is Buyer

information about demand, actual market price and suppliers cost meaning that it is a

very important determinant. It was however revealed that respondents were at

variance in regard to some determinants like product differences and buyer

concentration. Determinants like substitute products, brand identity, and buyer

information of competitors‟ prices drive bargaining power to large extent.

32

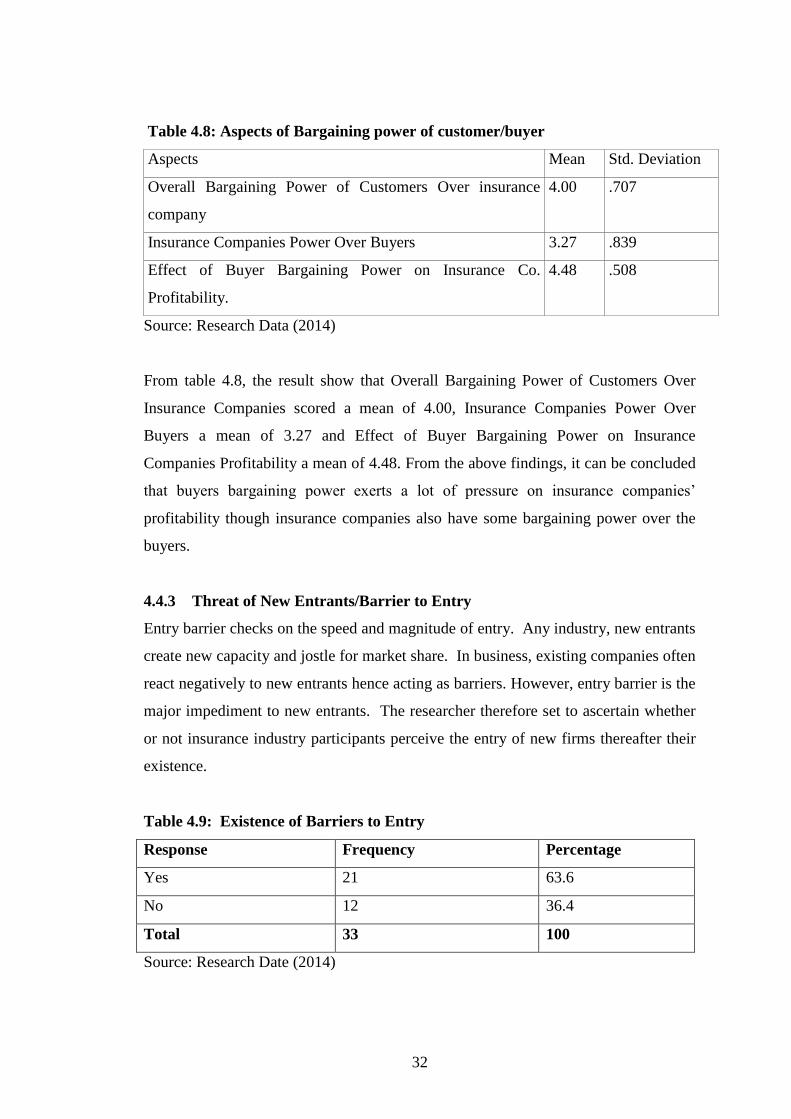

Table 4.8: Aspects of Bargaining power of customer/buyer

Aspects Mean Std. Deviation

Overall Bargaining Power of Customers Over insurance

company

4.00 .707

Insurance Companies Power Over Buyers 3.27 .839

Effect of Buyer Bargaining Power on Insurance Co.

Profitability.

4.48 .508

Source: Research Data (2014)

From table 4.8, the result show that Overall Bargaining Power of Customers Over

Insurance Companies scored a mean of 4.00, Insurance Companies Power Over

Buyers a mean of 3.27 and Effect of Buyer Bargaining Power on Insurance

Companies Profitability a mean of 4.48. From the above findings, it can be concluded

that buyers bargaining power exerts a lot of pressure on insurance companies‟

profitability though insurance companies also have some bargaining power over the

buyers.

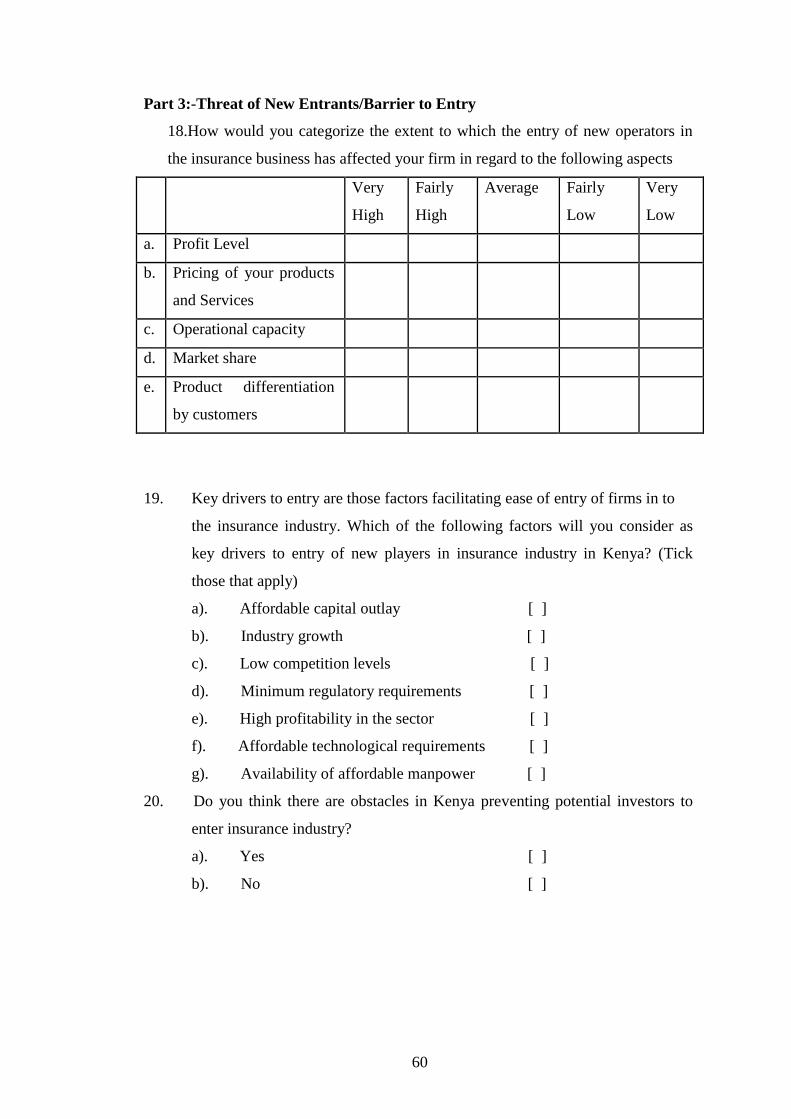

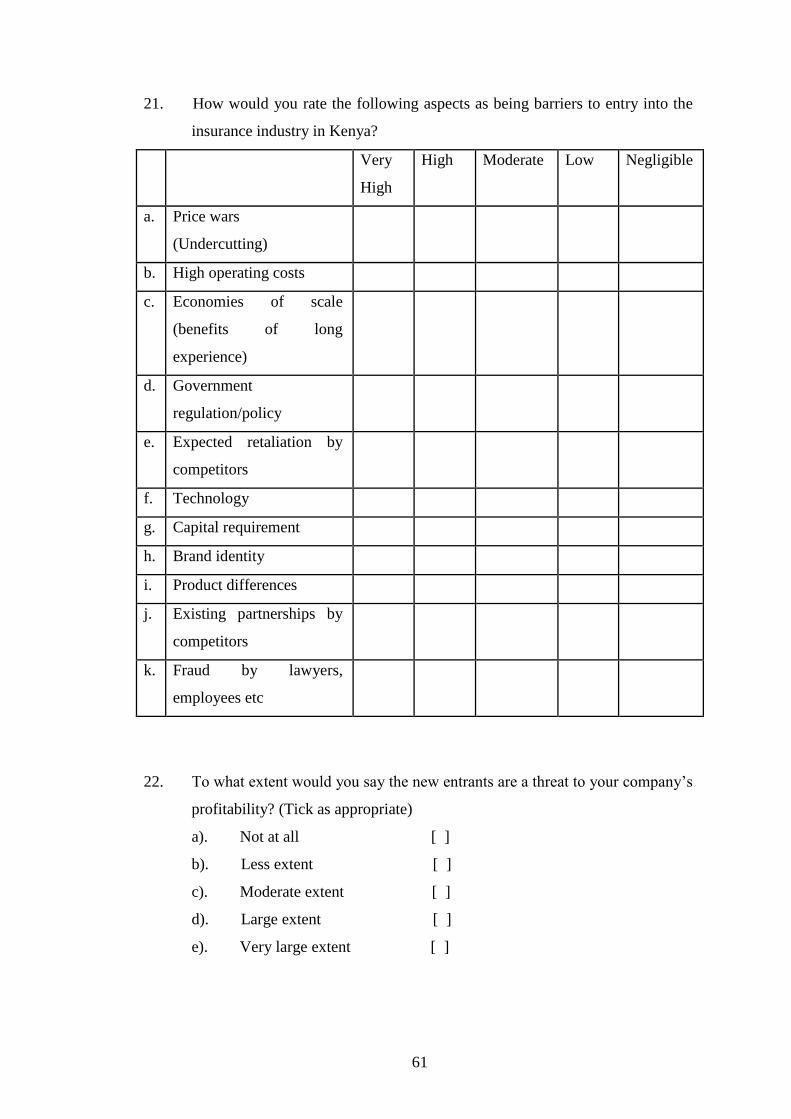

4.4.3 Threat of New Entrants/Barrier to Entry

Entry barrier checks on the speed and magnitude of entry. Any industry, new entrants

create new capacity and jostle for market share. In business, existing companies often

react negatively to new entrants hence acting as barriers. However, entry barrier is the

major impediment to new entrants. The researcher therefore set to ascertain whether

or not insurance industry participants perceive the entry of new firms thereafter their

existence.

Table 4.9: Existence of Barriers to Entry

Response Frequency Percentage

Yes 21 63.6

No 12 36.4

Total 33 100

Source: Research Date (2014)

33

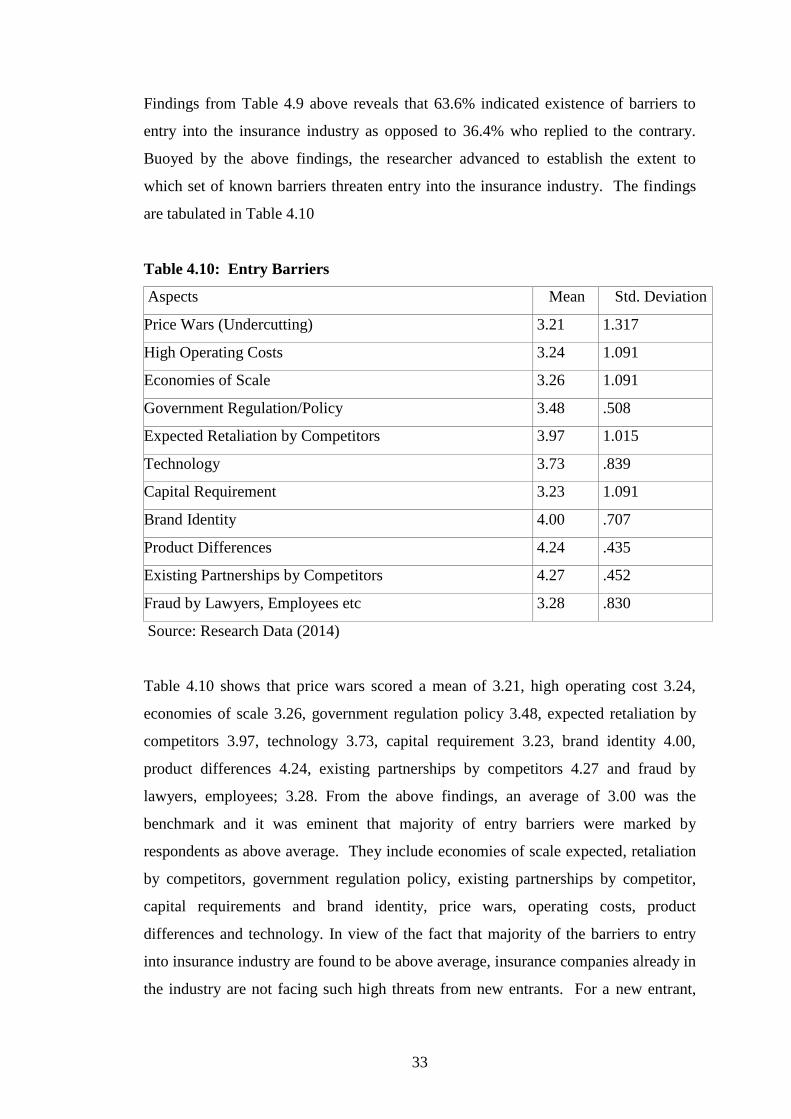

Findings from Table 4.9 above reveals that 63.6% indicated existence of barriers to

entry into the insurance industry as opposed to 36.4% who replied to the contrary.

Buoyed by the above findings, the researcher advanced to establish the extent to

which set of known barriers threaten entry into the insurance industry. The findings

are tabulated in Table 4.10

Table 4.10: Entry Barriers

Aspects Mean Std. Deviation

Price Wars (Undercutting) 3.21 1.317

High Operating Costs 3.24 1.091

Economies of Scale 3.26 1.091

Government Regulation/Policy 3.48 .508

Expected Retaliation by Competitors 3.97 1.015

Technology 3.73 .839

Capital Requirement 3.23 1.091

Brand Identity 4.00 .707

Product Differences 4.24 .435

Existing Partnerships by Competitors 4.27 .452

Fraud by Lawyers, Employees etc 3.28 .830

Source: Research Data (2014)

Table 4.10 shows that price wars scored a mean of 3.21, high operating cost 3.24,

economies of scale 3.26, government regulation policy 3.48, expected retaliation by

competitors 3.97, technology 3.73, capital requirement 3.23, brand identity 4.00,

product differences 4.24, existing partnerships by competitors 4.27 and fraud by

lawyers, employees; 3.28. From the above findings, an average of 3.00 was the

benchmark and it was eminent that majority of entry barriers were marked by

respondents as above average. They include economies of scale expected, retaliation

by competitors, government regulation policy, existing partnerships by competitor,

capital requirements and brand identity, price wars, operating costs, product

differences and technology. In view of the fact that majority of the barriers to entry

into insurance industry are found to be above average, insurance companies already in

the industry are not facing such high threats from new entrants. For a new entrant,

34

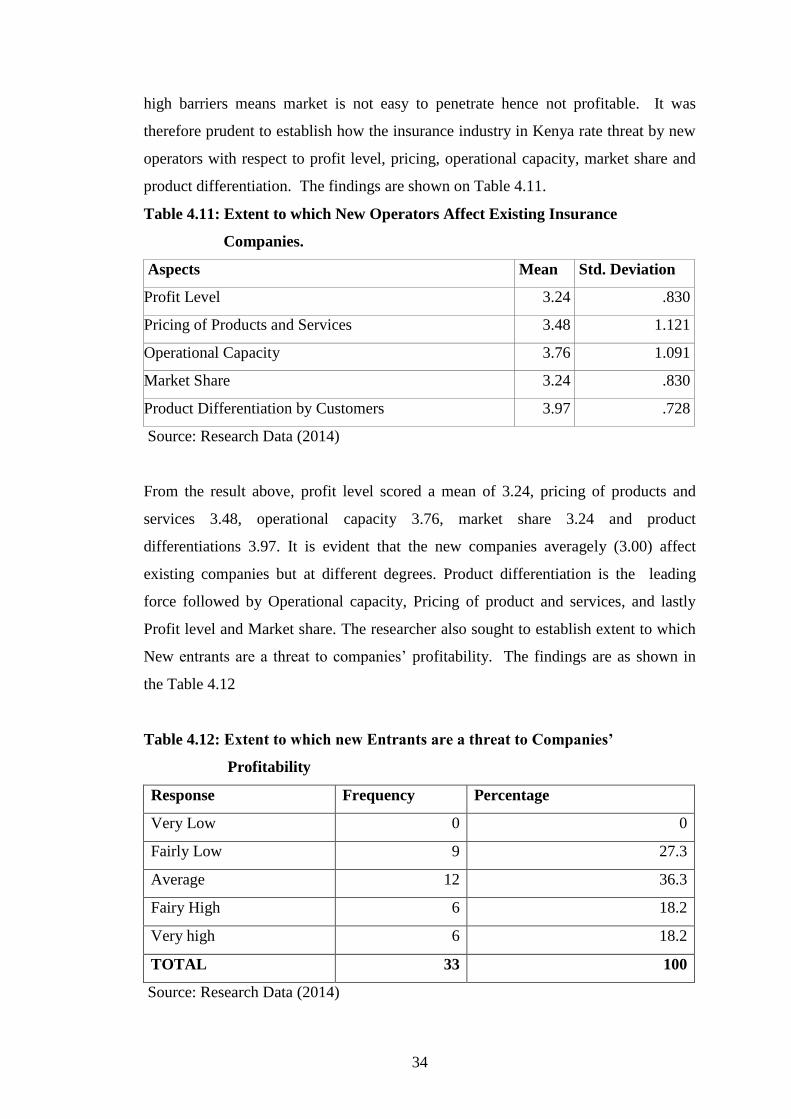

high barriers means market is not easy to penetrate hence not profitable. It was

therefore prudent to establish how the insurance industry in Kenya rate threat by new

operators with respect to profit level, pricing, operational capacity, market share and

product differentiation. The findings are shown on Table 4.11.

Table 4.11: Extent to which New Operators Affect Existing Insurance

Companies.

Aspects Mean Std. Deviation

Profit Level 3.24 .830

Pricing of Products and Services 3.48 1.121

Operational Capacity 3.76 1.091

Market Share 3.24 .830

Product Differentiation by Customers 3.97 .728

Source: Research Data (2014)

From the result above, profit level scored a mean of 3.24, pricing of products and

services 3.48, operational capacity 3.76, market share 3.24 and product

differentiations 3.97. It is evident that the new companies averagely (3.00) affect

existing companies but at different degrees. Product differentiation is the leading

force followed by Operational capacity, Pricing of product and services, and lastly

Profit level and Market share. The researcher also sought to establish extent to which

New entrants are a threat to companies‟ profitability. The findings are as shown in

the Table 4.12

Table 4.12: Extent to which new Entrants are a threat to Companies’

Profitability

Response Frequency Percentage

Very Low 0 0

Fairly Low 9 27.3

Average 12 36.3

Fairy High 6 18.2

Very high 6 18.2

TOTAL 33 100

Source: Research Data (2014)

35

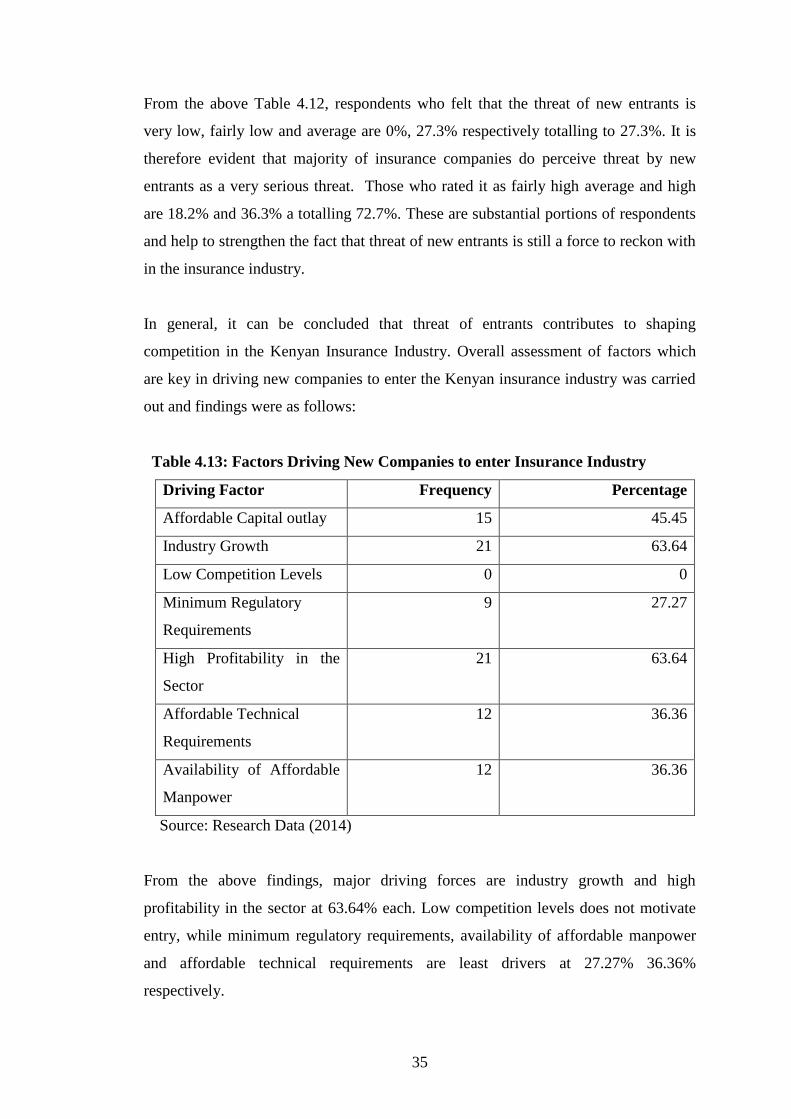

From the above Table 4.12, respondents who felt that the threat of new entrants is

very low, fairly low and average are 0%, 27.3% respectively totalling to 27.3%. It is

therefore evident that majority of insurance companies do perceive threat by new

entrants as a very serious threat. Those who rated it as fairly high average and high

are 18.2% and 36.3% a totalling 72.7%. These are substantial portions of respondents

and help to strengthen the fact that threat of new entrants is still a force to reckon with

in the insurance industry.

In general, it can be concluded that threat of entrants contributes to shaping

competition in the Kenyan Insurance Industry. Overall assessment of factors which

are key in driving new companies to enter the Kenyan insurance industry was carried

out and findings were as follows:

Table 4.13: Factors Driving New Companies to enter Insurance Industry

Driving Factor Frequency Percentage

Affordable Capital outlay 15 45.45

Industry Growth 21 63.64

Low Competition Levels 0 0

Minimum Regulatory

Requirements

9 27.27

High Profitability in the

Sector

21 63.64

Affordable Technical

Requirements

12 36.36

Availability of Affordable

Manpower

12 36.36

Source: Research Data (2014)

From the above findings, major driving forces are industry growth and high

profitability in the sector at 63.64% each. Low competition levels does not motivate

entry, while minimum regulatory requirements, availability of affordable manpower

and affordable technical requirements are least drivers at 27.27% 36.36%

respectively.

36

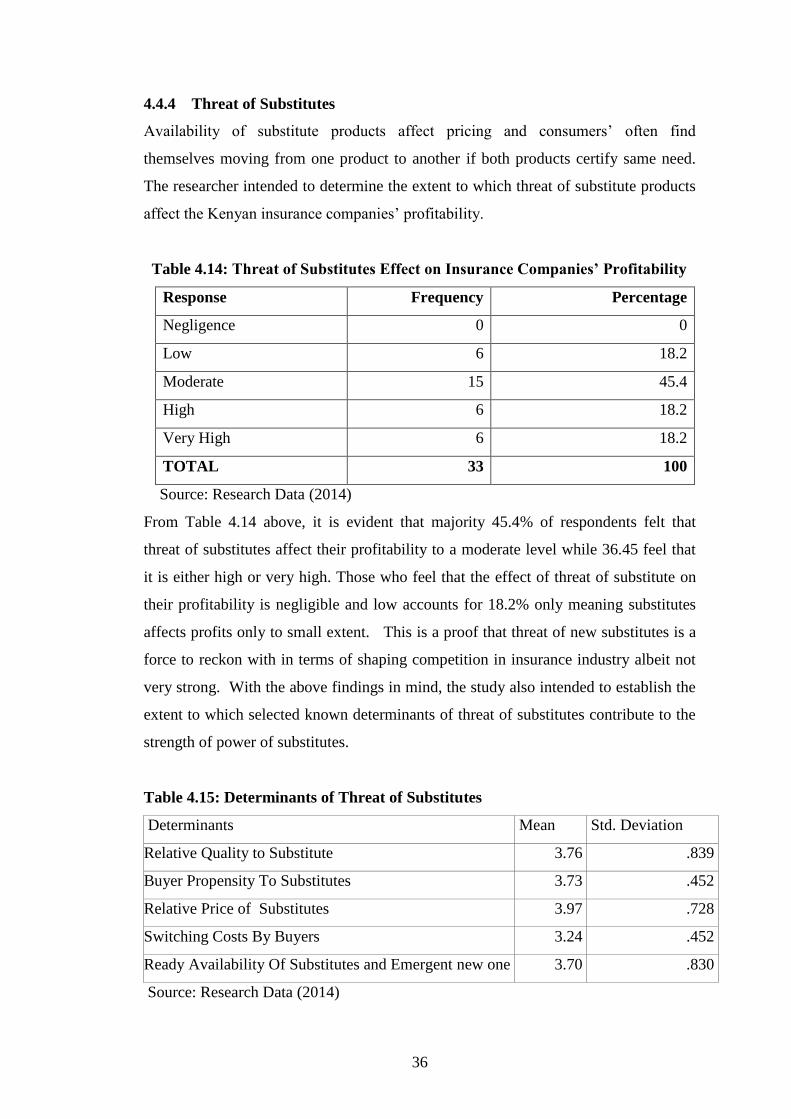

4.4.4 Threat of Substitutes

Availability of substitute products affect pricing and consumers‟ often find

themselves moving from one product to another if both products certify same need.

The researcher intended to determine the extent to which threat of substitute products

affect the Kenyan insurance companies‟ profitability.

Table 4.14: Threat of Substitutes Effect on Insurance Companies’ Profitability

Response Frequency Percentage

Negligence 0 0

Low 6 18.2

Moderate 15 45.4

High 6 18.2

Very High 6 18.2

TOTAL 33 100

Source: Research Data (2014)

From Table 4.14 above, it is evident that majority 45.4% of respondents felt that

threat of substitutes affect their profitability to a moderate level while 36.45 feel that

it is either high or very high. Those who feel that the effect of threat of substitute on

their profitability is negligible and low accounts for 18.2% only meaning substitutes

affects profits only to small extent. This is a proof that threat of new substitutes is a

force to reckon with in terms of shaping competition in insurance industry albeit not

very strong. With the above findings in mind, the study also intended to establish the

extent to which selected known determinants of threat of substitutes contribute to the

strength of power of substitutes.

Table 4.15: Determinants of Threat of Substitutes

Determinants Mean Std. Deviation

Relative Quality to Substitute 3.76 .839

Buyer Propensity To Substitutes 3.73 .452

Relative Price of Substitutes 3.97 .728

Switching Costs By Buyers 3.24 .452

Ready Availability Of Substitutes and Emergent new one 3.70 .830

Source: Research Data (2014)

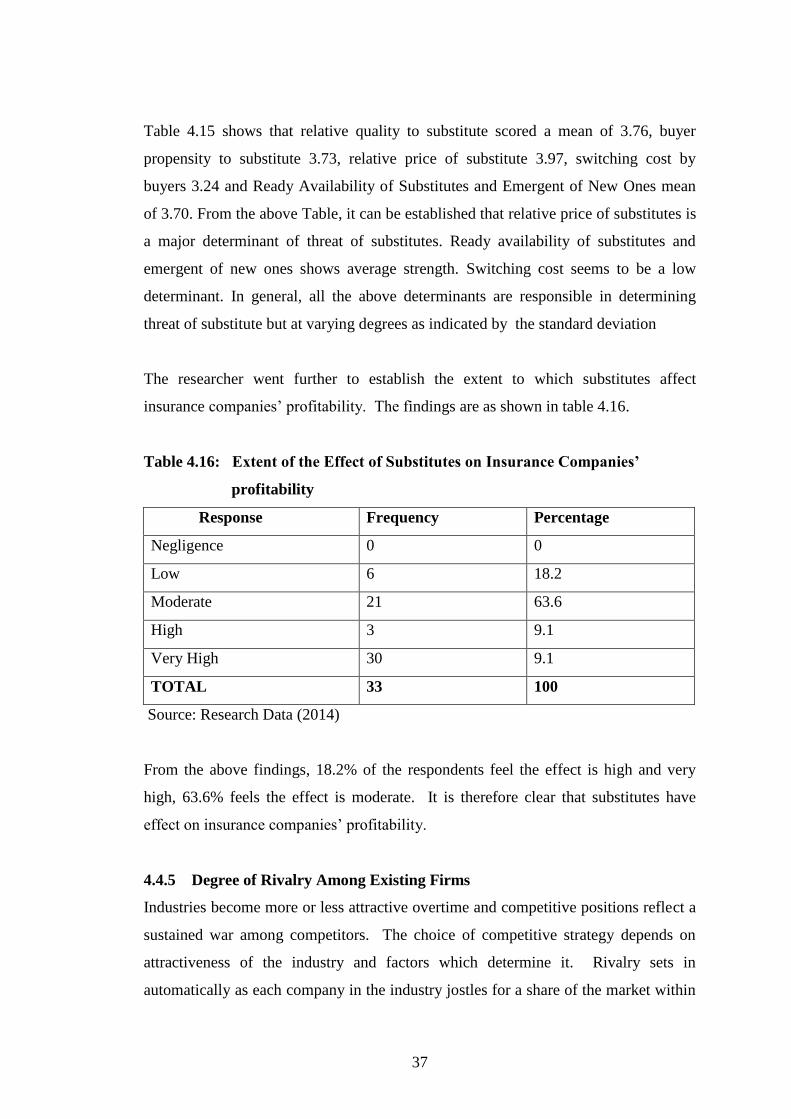

37

Table 4.15 shows that relative quality to substitute scored a mean of 3.76, buyer

propensity to substitute 3.73, relative price of substitute 3.97, switching cost by

buyers 3.24 and Ready Availability of Substitutes and Emergent of New Ones mean

of 3.70. From the above Table, it can be established that relative price of substitutes is

a major determinant of threat of substitutes. Ready availability of substitutes and

emergent of new ones shows average strength. Switching cost seems to be a low

determinant. In general, all the above determinants are responsible in determining

threat of substitute but at varying degrees as indicated by the standard deviation

The researcher went further to establish the extent to which substitutes affect

insurance companies‟ profitability. The findings are as shown in table 4.16.

Table 4.16: Extent of the Effect of Substitutes on Insurance Companies’

profitability

Response Frequency Percentage

Negligence 0 0

Low 6 18.2

Moderate 21 63.6

High 3 9.1

Very High 30 9.1

TOTAL 33 100

Source: Research Data (2014)

From the above findings, 18.2% of the respondents feel the effect is high and very

high, 63.6% feels the effect is moderate. It is therefore clear that substitutes have

effect on insurance companies‟ profitability.

4.4.5 Degree of Rivalry Among Existing Firms

Industries become more or less attractive overtime and competitive positions reflect a

sustained war among competitors. The choice of competitive strategy depends on

attractiveness of the industry and factors which determine it. Rivalry sets in

automatically as each company in the industry jostles for a share of the market within

38

the industry. Different companies see different opportunities at different times hence

scramble for a superior competitive position. Major tools used in the scramble are

price competition, customer service, product differentiation, promotions and

innovations. The study is intended to establish the degree of rivalry in Kenya and also

the strength of such rivalry in determining industry attractiveness. Selected

determinants were paused to the respondents who were asked to rate them on basis of

extent to which they determine competition. The results were as shown on Table 4.17

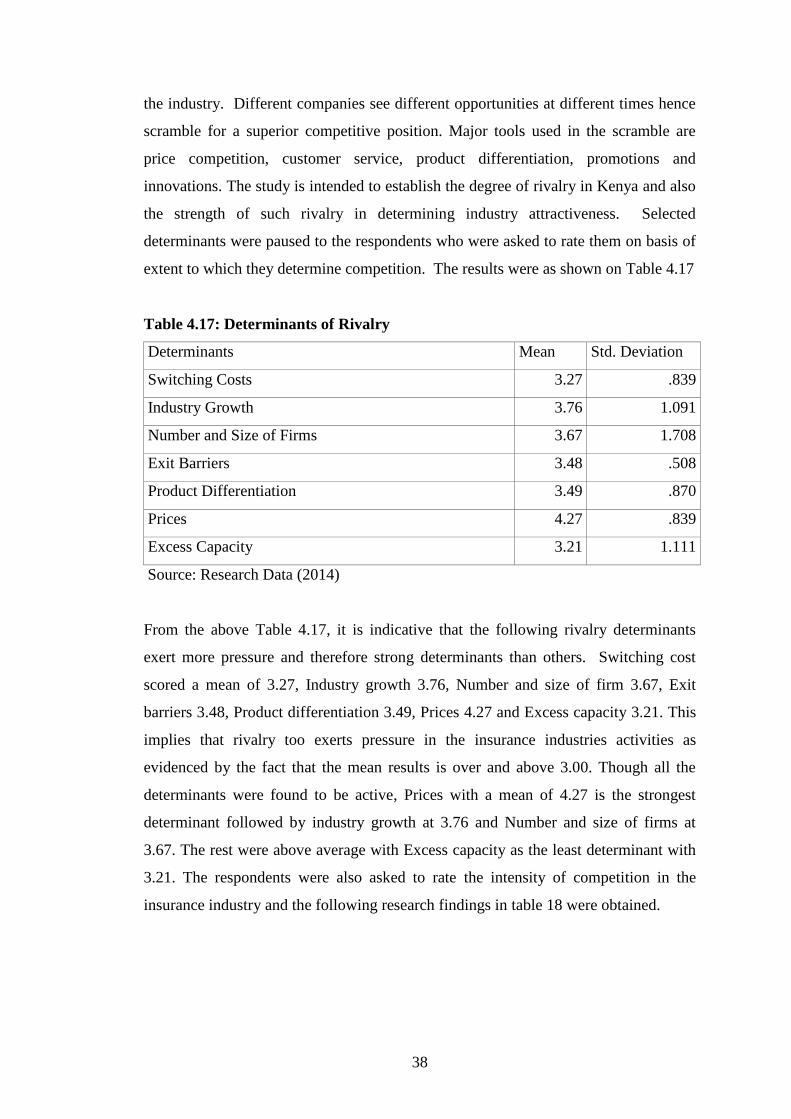

Table 4.17: Determinants of Rivalry

Determinants Mean Std. Deviation

Switching Costs 3.27 .839

Industry Growth 3.76 1.091

Number and Size of Firms 3.67 1.708

Exit Barriers 3.48 .508

Product Differentiation 3.49 .870

Prices 4.27 .839

Excess Capacity 3.21 1.111

Source: Research Data (2014)

From the above Table 4.17, it is indicative that the following rivalry determinants

exert more pressure and therefore strong determinants than others. Switching cost

scored a mean of 3.27, Industry growth 3.76, Number and size of firm 3.67, Exit

barriers 3.48, Product differentiation 3.49, Prices 4.27 and Excess capacity 3.21. This

implies that rivalry too exerts pressure in the insurance industries activities as

evidenced by the fact that the mean results is over and above 3.00. Though all the

determinants were found to be active, Prices with a mean of 4.27 is the strongest

determinant followed by industry growth at 3.76 and Number and size of firms at

3.67. The rest were above average with Excess capacity as the least determinant with

3.21. The respondents were also asked to rate the intensity of competition in the

insurance industry and the following research findings in table 18 were obtained.

39

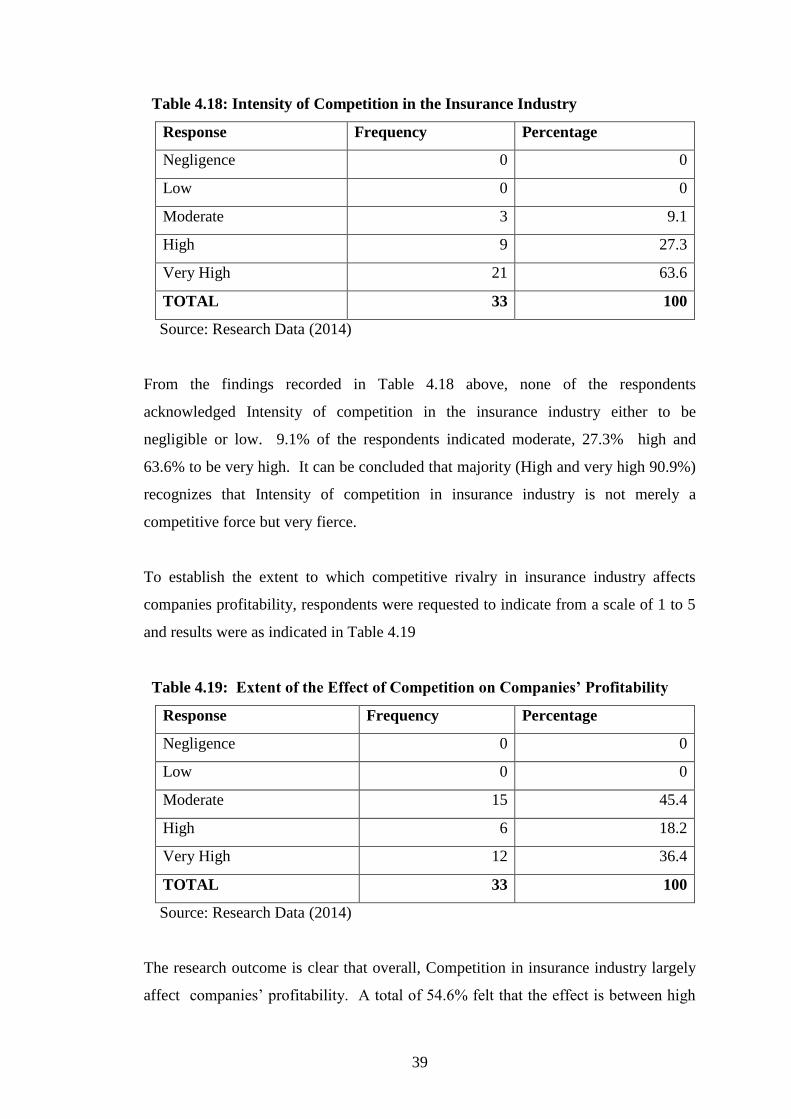

Table 4.18: Intensity of Competition in the Insurance Industry

Response Frequency Percentage

Negligence 0 0

Low 0 0

Moderate 3 9.1

High 9 27.3

Very High 21 63.6

TOTAL 33 100

Source: Research Data (2014)

From the findings recorded in Table 4.18 above, none of the respondents

acknowledged Intensity of competition in the insurance industry either to be

negligible or low. 9.1% of the respondents indicated moderate, 27.3% high and

63.6% to be very high. It can be concluded that majority (High and very high 90.9%)

recognizes that Intensity of competition in insurance industry is not merely a

competitive force but very fierce.

To establish the extent to which competitive rivalry in insurance industry affects

companies profitability, respondents were requested to indicate from a scale of 1 to 5

and results were as indicated in Table 4.19

Table 4.19: Extent of the Effect of Competition on Companies’ Profitability

Response Frequency Percentage

Negligence 0 0

Low 0 0

Moderate 15 45.4

High 6 18.2

Very High 12 36.4

TOTAL 33 100

Source: Research Data (2014)

The research outcome is clear that overall, Competition in insurance industry largely

affect companies‟ profitability. A total of 54.6% felt that the effect is between high

40

and very high; an indication of serious impact of competition on profits. Though

there is remarkable variation of extent on the strength of the effect, the actual effect

on the profit is quite significant.

When the respondents were asked to briefly explain in what other way rivalry in the

industry influence performance, they gave various reasons including undercutting of

rates, and when asked for recommendations to make insurance industry more

attractive, respondents gave various reasons like competition on service delivery not

on price, product development, training of insurance personnel and strict adherence to

the rule of law.

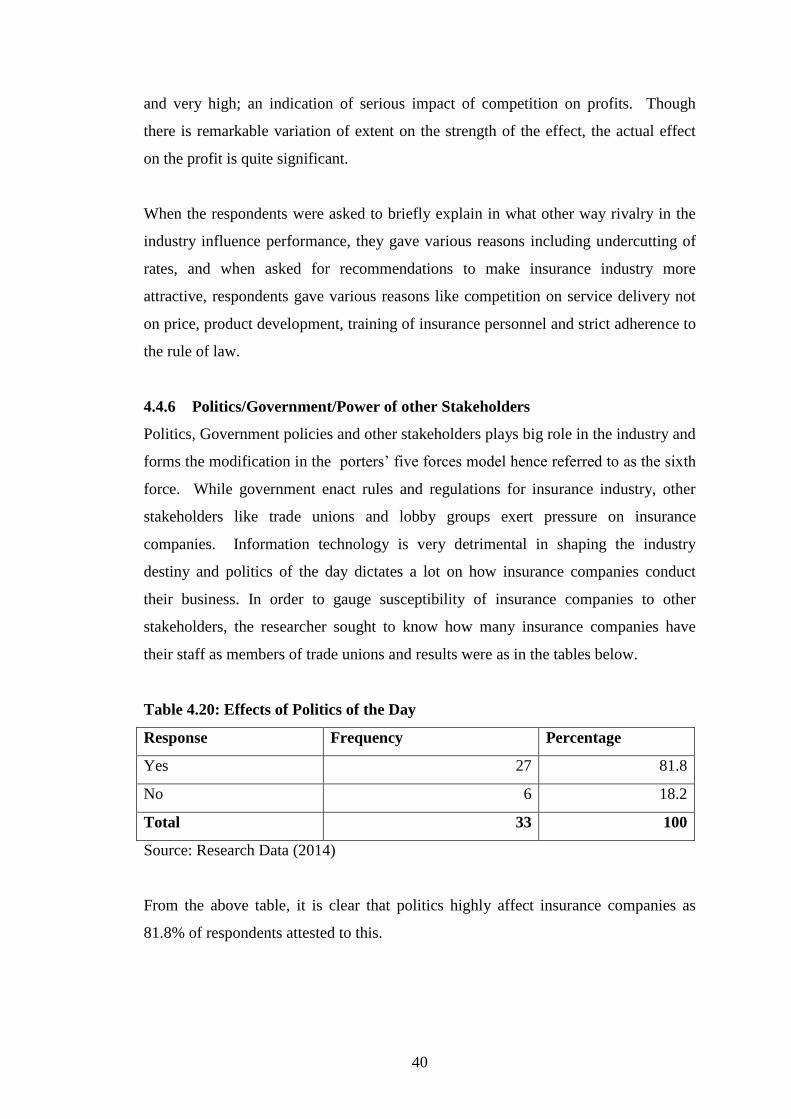

4.4.6 Politics/Government/Power of other Stakeholders

Politics, Government policies and other stakeholders plays big role in the industry and

forms the modification in the porters‟ five forces model hence referred to as the sixth

force. While government enact rules and regulations for insurance industry, other

stakeholders like trade unions and lobby groups exert pressure on insurance

companies. Information technology is very detrimental in shaping the industry

destiny and politics of the day dictates a lot on how insurance companies conduct

their business. In order to gauge susceptibility of insurance companies to other

stakeholders, the researcher sought to know how many insurance companies have

their staff as members of trade unions and results were as in the tables below.

Table 4.20: Effects of Politics of the Day

Response Frequency Percentage

Yes 27 81.8

No 6 18.2

Total 33 100

Source: Research Data (2014)

From the above table, it is clear that politics highly affect insurance companies as

81.8% of respondents attested to this.

41

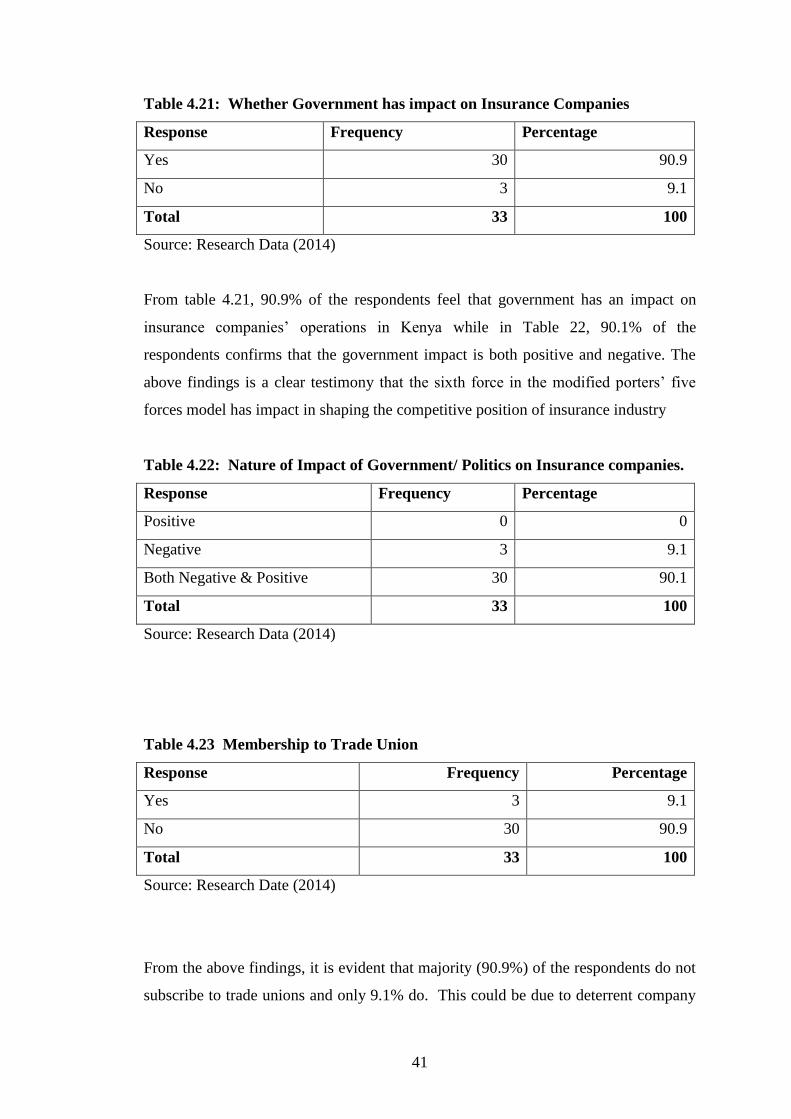

Table 4.21: Whether Government has impact on Insurance Companies

Response Frequency Percentage

Yes 30 90.9

No 3 9.1

Total 33 100

Source: Research Data (2014)

From table 4.21, 90.9% of the respondents feel that government has an impact on

insurance companies‟ operations in Kenya while in Table 22, 90.1% of the

respondents confirms that the government impact is both positive and negative. The

above findings is a clear testimony that the sixth force in the modified porters‟ five

forces model has impact in shaping the competitive position of insurance industry

Table 4.22: Nature of Impact of Government/ Politics on Insurance companies.

Response Frequency Percentage

Positive 0 0

Negative 3 9.1

Both Negative & Positive 30 90.1

Total 33 100

Source: Research Data (2014)

Table 4.23 Membership to Trade Union

Response Frequency Percentage

Yes 3 9.1

No 30 90.9

Total 33 100

Source: Research Date (2014)

From the above findings, it is evident that majority (90.9%) of the respondents do not

subscribe to trade unions and only 9.1% do. This could be due to deterrent company

42

policies or general fair treatment to the extent that staff do not perceive viability of

unionism. The research further intended to establish the extent to which the above

stakeholders affect operation of insurance companies in Kenya. The findings are as

shown in table 4.24.

Table 4.24: Extent of Extent of Politics/Government/Other

Stakeholders

Factors Mean Std. Deviation

Effect of Trade Union Movement in Company‟s Performance 3.03 1.661

Effect of Politics of the Day in Company‟s Performance 3.52 .728

Effect of Government Policies on Profit 3.76 .435

Source: Research Data (2014)

From table 4.24 the results show that Effect of Trade Union Movement in Company‟s

Performance scored a mean of 3.03, Effect of Politics of the day in Company‟s

Performance a mean of 3.52 and Effect of Government Policies on Profit a mean of

3.76. This implies that politics/government/other stakeholders to some extent have

effects in the insurance industries‟ activities

Table 4.25: Strengths of the six forces of the modified Porters’ model

Force Mean Rank

Bargaining Power of customers 3.98 1

Bargaining power of suppliers 3.88 2

Threats to substitute 3.68 3

Threats of new entry 3.63 4

Competitive Rivalry 3.59 5

Politics/Government/Other stakeholders 3.44 6

Source: Research Data (2014)

Table 4.25 shows that Bargaining power of customers exert more pressure in the

insurance industry with mean of 3.98, followed by Bargaining power of Suppliers

with mean of 3.88, Threat of substitute 3.68 mean, Barrier to entry 3.63 mean,

Competitive rivalry 3.59 while Politics/Government/Others had the least mean of

43

3.44. This implies that customers still have the strongest powers in influencing the

Insurance industry and should therefore be treated with great care.

44

CHAPTER FIVE

SUMMARY, CONCLUSION AND RECOMMEDATIONS

5.1 Introduction