(APICORP) – Aa3 stable Arab Petroleum Investments Corporation · (APICORP) – Aa3 stable Annual...

22

SOVEREIGN AND SUPRANATIONAL ISSUER IN-DEPTH 10 October 2017 RATINGS APICORP Rating Outlook Long-Term Issuer Aa3 STA Short-Term Issuer P-1 STA Long-Term Unsecured Debt (P)Aa3 TABLE OF CONTENTS OVERVIEW AND OUTLOOK 1 Organizational structure and strategy 2 CREDIT PROFILE 5 Capital adequacy: High 5 Liquidity: High 9 Strength of member support: Very High 12 Rating range 14 Comparatives 15 DATA AND REFERENCES 16 Contacts Steffen Dyck 49-697-073-0942 VP-Sr Credit Officer [email protected] Eugeniu Croitor 971.423.795.74 Associate Analyst [email protected] Christian de Guzman 65-6398-8327 VP-Sr Credit Officer [email protected] Matt Robinson 44-20-7772-5635 Associate Managing Director [email protected] Yves Lemay 44-20-7772-5512 MD-Sovereign Risk [email protected] Alastair Wilson 44-20-7772-1372 MD-Global Sovereign Risk [email protected] Arab Petroleum Investments Corporation (APICORP) – Aa3 stable Annual credit analysis OVERVIEW AND OUTLOOK APICORP's (Aa3 stable) credit strengths include its robust capital adequacy, a high-quality investment asset portfolio, de facto preferred creditor status and strong shareholder support – APICORP is wholly owned by the 10 member states of the Organization of Arab Petroleum Exporting Countries (OAPEC). APICORP has maintained a high level of equity relative to its risk assets, and its corresponding capital adequacy ratios exceed regulatory guidelines, specifically those of the Central Bank of Bahrain, where the corporation maintains a wholesale banking branch. Relatively low leverage also contributes to APICORP’s high intrinsic financial strength while the increase in callable capital in 2016 underlines shareholder support. By contrast, APICORP's credit challenges include a funding profile marked by a high share of short-term wholesale deposits, an improving but still comparatively large asset-liability maturity mismatch, and high geographic and sector concentration relative to peers. Efforts to diversify its funding sources are ongoing and there was a further moderation of the short- term maturity gap in 2016. Nevertheless, the degree to which the corporation remains reliant on wholesale deposits adversely affects our assessment of its liquidity. In addition, APICORP's operating environment is challenging given the political turmoil in a number of member countries since 2011, more prominent geopolitical risks recently and sustained low oil prices, which saw net profit decline 13.2% year-on-year in 2016. That said, asset quality and capital adequacy have not been materially impacted yet. APICORP's ratings could gain upward momentum should it make further material progress in addressing liquidity risk by diversifying its funding base and reducing maturity mismatches, while maintaining its capital adequacy despite the challenging operating environment. Conversely, downward pressure on its ratings could emerge should: (1) a prolonged period of very low oil prices or a regional political shock significantly impair asset quality; (2) its main shareholders experience further rating downgrades indicating a weaker ability to financially support APICORP; (3) any other indication emerge that shareholders' willingness to support APICORP was weakening; or (4) liquidity risk increase or any funding pressures emerge as a result of a worsening of the operating environment. This credit analysis elaborates on APICORP's credit profile in terms of capital adequacy, liquidity and strength of member support, which are the three main analytical factors in Moody’s Supranational Rating Methodology .

Transcript of (APICORP) – Aa3 stable Arab Petroleum Investments Corporation · (APICORP) – Aa3 stable Annual...

SOVEREIGN AND SUPRANATIONAL

ISSUER IN-DEPTH10 October 2017

RATINGS

APICORPRating Outlook

Long-Term Issuer Aa3 STA

Short-Term Issuer P-1 STA

Long-Term Unsecured Debt (P)Aa3

TABLE OF CONTENTSOVERVIEW AND OUTLOOK 1Organizational structure and strategy 2CREDIT PROFILE 5Capital adequacy: High 5Liquidity: High 9Strength of member support: VeryHigh 12Rating range 14Comparatives 15DATA AND REFERENCES 16

Contacts

Steffen Dyck 49-697-073-0942VP-Sr Credit [email protected]

Eugeniu Croitor 971.423.795.74Associate [email protected]

Christian de Guzman 65-6398-8327VP-Sr Credit [email protected]

Matt Robinson 44-20-7772-5635Associate [email protected]

Yves Lemay 44-20-7772-5512MD-Sovereign [email protected]

Alastair Wilson 44-20-7772-1372MD-Global [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

Arab Petroleum Investments Corporation(APICORP) – Aa3 stableAnnual credit analysis

OVERVIEW AND OUTLOOK

APICORP's (Aa3 stable) credit strengths include its robust capital adequacy, a high-qualityinvestment asset portfolio, de facto preferred creditor status and strong shareholdersupport – APICORP is wholly owned by the 10 member states of the Organization ofArab Petroleum Exporting Countries (OAPEC). APICORP has maintained a high level ofequity relative to its risk assets, and its corresponding capital adequacy ratios exceedregulatory guidelines, specifically those of the Central Bank of Bahrain, where the corporationmaintains a wholesale banking branch. Relatively low leverage also contributes to APICORP’shigh intrinsic financial strength while the increase in callable capital in 2016 underlinesshareholder support.

By contrast, APICORP's credit challenges include a funding profile marked by a high shareof short-term wholesale deposits, an improving but still comparatively large asset-liabilitymaturity mismatch, and high geographic and sector concentration relative to peers. Effortsto diversify its funding sources are ongoing and there was a further moderation of the short-term maturity gap in 2016. Nevertheless, the degree to which the corporation remainsreliant on wholesale deposits adversely affects our assessment of its liquidity. In addition,APICORP's operating environment is challenging given the political turmoil in a number ofmember countries since 2011, more prominent geopolitical risks recently and sustained lowoil prices, which saw net profit decline 13.2% year-on-year in 2016. That said, asset qualityand capital adequacy have not been materially impacted yet.

APICORP's ratings could gain upward momentum should it make further material progress inaddressing liquidity risk by diversifying its funding base and reducing maturity mismatches,while maintaining its capital adequacy despite the challenging operating environment.

Conversely, downward pressure on its ratings could emerge should: (1) a prolonged period ofvery low oil prices or a regional political shock significantly impair asset quality; (2) its mainshareholders experience further rating downgrades indicating a weaker ability to financiallysupport APICORP; (3) any other indication emerge that shareholders' willingness to supportAPICORP was weakening; or (4) liquidity risk increase or any funding pressures emerge as aresult of a worsening of the operating environment.

This credit analysis elaborates on APICORP's credit profile in terms of capital adequacy,liquidity and strength of member support, which are the three main analytical factors inMoody’s Supranational Rating Methodology.

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Organizational structure and strategyAPICORP is an OAPEC company

APICORP was established as a multilateral development bank (MDB) on 23 November 1975 in accordance with an internationalagreement (“Establishing Agreement of APICORP”) signed and ratified by the 10 member states of the OAPEC.1

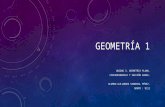

Exhibit 1 shows the distribution of fully paid-in capital, with the largest shareholders being the governments of Saudi Arabia (A1 stable),the United Arab Emirates (Aa2 stable) and Kuwait (Aa2 stable). APICORP’s headquarters are located in Dammam, Saudi Arabia, and ithas a wholesale banking branch in Manama, Bahrain (B1 negative).

Exhibit 1

APICORP's shareholding structureFully paid-in capital shares (as of 31 December 2016)

Kuwait (Aa2)17%

UAE (Aa2)17%

17%

17%

17%

15%

10%

10%

5%

3%

3%

3%

Saudi Arabia (A1)

Kuwait (Aa2)

UAE (Aa2)

Libya (NR)

Iraq (Caa1)

Qatar (Aa3)

Algeria (NR)

Bahrain (B1)

Egypt (B3)

Syria (NR)

AlgeriaLibya

Egypt

Kuwait

Saudi

Arabia

Iraq

Syria

UAE

Qatar

Bahrain

Note: Sovereign ratings in brackets are as of 10 October 2017.Sources: APICORP, Moody's Investors Service

APICORP is independent in its administration and in the performance of its activities. Unlike many other MDBs, it carries out itsoperations on a commercial basis, in accordance with its statutes. APICORP allocates 10% of annual net income to its statutory reserveand has the option of distributing the remainder as dividends to its shareholders. There is no dividend policy in place and dividenddistribution is mainly driven by surplus liquidity considerations. The corporation has not paid out dividends in seven out of last 10 years.Dividends were paid in 2007, 2011, and 2015.

The Establishing Agreement of APICORP explicitly grants the corporation privileges throughout OAPEC member countries. Theseprivileges include (1) the pledge and undertaking to support APICORP, jointly and severally; (2) the granting of rights and privileges ofnationality within any member country of OAPEC; (3) support for APICORP’s personnel in entry and residency throughout OAPEC;(4) exemption from payment of duties and all public and financial costs within OAPEC; (5) protection of assets against appropriation;(6) immunity from political risks; and (7) exemption from currency controls, including from convertibility and transfer restrictions.Membership in APICORP is explicitly limited to member countries of OAPEC, and any country that withdraws its membership fromOAPEC is obliged to withdraw from APICORP.

Fulfills mandate through lending and equity investment operations

APICORP’s mandate is to assist in financing petroleum projects and industries, and associated fields of activity of OAPEC members inorder to strengthen member states’ economic and financial potential. In order to achieve its purpose, APICORP makes direct equityinvestments in (16% of total assets as of year-end 2016) and extends debt financing (syndicated and direct loans, 48% of assets) tolocal, regional, and international entities in the energy and petrochemical sectors, as well as the trading activities of first-tier Arabexporters and global traders with creditworthy importing countries.

APICORP may conduct investments or financing proposals located outside the Arab region if it sees potential association with theinterest and development of the wider energy industry in the Arab region. The rest of the assets consist of cash and cash equivalents,

2 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

bank deposits, property and equipment, and are invested in liquid instruments. APICORP also provides advisory related to oil and gasfinance and project development, and publishes macro-economic research with a focus on the oil and gas sector.

APICORP’s development mandate and its multilateral shareholding structure are typical of most MDBs. But it differs from other highly-rated MDBs in that it fulfils its mandate by investing in the private sector, although a significant portion of its assets is indirectlyassociated with governments, through government-owned entities. We therefore consider APICORP’s business model slightly morevulnerable than those of most other MDBs, whose assets are largely characterized by direct sovereign exposure. The high concentrationof assets in the oil and gas sector is also a difference between APICORP and some other MDBs.

In the context of heightened country risk in the Middle East, the corporation’s strategy for its project & trade finance loans is tomaintain the current volume and contain the average maturity of its loan portfolio, while shifting focus to advisory services and tradeand commodity finance, with a focus on the Gulf Cooperation Council (GCC) countries.

According to its five-year business plan, loan growth will be moderate. Some of this growth will be done in partnership with otherlarge MDBs. APICORP has well-established co-financing relationships with the European Investment Bank (EIB), International FinanceCorporation (IFC), and the Islamic Development Bank (IsDB) and is working towards broadening its relationships with the EuropeanBank for Reconstruction and Development (EBRD) and the African Development Bank (all rated Aaa). In October 2016, APICORPannounced its expansion in Egypt (B3 stable) through a 3-year financing facility worth $100 million for Egyptian General PetroleumCorporation (EGPC, unrated).

Regarding its equity operations, APICORP’s strategy is to grow and diversify investments. Compared to its 2012 level of $318 million,equity investments have more than doubled in 2013, to $822 million, although most of this increase was the result of portfoliorevaluation. Equity investments continued to rise further, hitting $987 million in 2016 or approximately 33% of loan operations.Consequently, the Corporation has added to its personnel to handle the increased volume. It also usually partners with publicinstitutions and aims at occupying at least one seat on the Board of the investee, although with a planned exit strategy.

APICORP continues to diversify its investments across regions and sectors, following a selective investment approach. Key activities in2016 include the acquisition of a 35% stake in Ashtead Technology (unrated), a leading independent provider of sub-sea equipmentand services to the offshore oil and gas industry, with operations in the UK, Houston and Singapore, and in late 2016, the corporationannounced the acquisition of a 30% share in Bahrain's largest cement producer Falcon Cement Company (FCC, unrated). Investmentsin 2017 to date were focused on utilities and the fracking sector in the US.

Exhibit 2

APICORP’s direct equity investments, as of 31 December 2016

Company name Domiciled in Value (US$ million)

Saudi European Petrochemical Company (IBN ZAHR) Saudi Arabia 459.5

Egyptian Methanex Methanol Company (EMETHANEX) Egypt 109.0

National Petroleum Services (NPS) United Arab Emirates 107.3

Yanbu National Petrochemical Company (YANSAB) Saudi Arabia 107.1

Industrialization and Energy Services Company (TAQA) Saudi Arabia 97.5

Saudi Mechanical Industries (SMI) Saudi Arabia 46.1

Falcon Cement Company (FCC) Bahrain 25.5

Ashtead Technology (ASHTEAD)) Great Britain 13.0

Misr Fertilizers Production Company (MOPCO) Egypt 12.6

Tankmed Tankage Mediterranee (TANKMED) Tunisia 3.6

Note: Yansab is the only listed company. Direct equity investments are measured at fair value, except in case of certain unlisted companies where reliable fair value measures are notavailable; those are carried at cost less impairment allowances (if any).Source: APICORP

As of year-end 2016, APICORP’s largest equity holding was Saudi European Petrochemical Company (Ibn Zahr), a polypropylenemanufacturer majority-owned by Saudi Basic Industries Corporation (SABIC, A1 stable), at a book value of $459.5 million, or 52.2% ofall the corporation’s equity investments (see Exhibit 2).

3 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Wholesale deposit operations position APICORP as a unique MDB

APICORP, unlike most MDBs, accepts wholesale deposits. The few other Moody’s-rated MDBs that take deposits – Corporacion Andinade Fomento (CAF, Aa3 stable), Central American Bank for Economic Integration (CABEI, A1 stable), Fondo Latinoamericano de Reservas(FLAR, Aa2 stable) – take the deposits primarily from shareholders, and they do not use the deposits as a source of funding for theirbanking operations. The African Export-Import Bank (Afrexim, Baa1 stable) has also introduced a deposit facility in late 2015 which canserve as cash collateral facility to fund trade finance operations on the asset side.

APICORP’s business model differs from other MDBs, while sharing some characteristics with commercial banks in that it uses wholesaledeposits to fund: (1) primarily, treasury operations for profit and liquidity purposes; and (2) a small portion of investment operations(around 10%). From the period 1998-2005, deposits from banks accounted for an average 65% of the corporation's funding source,with term financing loans comprising the remainder.

In 2006, APICORP started diversifying its deposit client base with the opening of its conventional wholesale bank branch in Bahrain,operating under a Conventional Wholesale Bank License granted by the Central Bank of Bahrain (CBB). The branch is governed by theregulations of the CBB, but like other offshore banks operating in Bahrain, it does not have access to central bank liquidity facilities. Thepurpose of the branch is to complement the treasury and capital market activities of the corporation and provide banking facilities –predominantly letter-of-credit – to clients.

At the end of 2016, deposits from private sector corporates and government-related entities (GRE) accounted for 27.4% of APICORP'stotal liabilities, down from 36.9% in 2015 and 38% reported in 2014. Deposits from banks amounted to 6.9% of total liabilities, upfrom 4.6% in the year before. These shares are in contrast with longer-term trends, where the share of corporate and GRE deposits hasrisen significantly, while the proportion of deposits from banks has shrunk.

4 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

CREDIT PROFILEOur determination of a supranational’s rating is based on three rating factors: Capital adequacy, liquidity and strength of membersupport. For Multilateral Development Banks, the first two factors combine to form the assessment of intrinsic financial strength,which provides a preliminary rating range. The strength of member support can provide uplift to the preliminary rating range. For moreinformation please see our Supranational Rating Methodology.

Capital adequacy: HighStrong capital position and very low leverage

Scale

+ -

Capital adequacy assesses the solvency of an institution. The capital adequacy assessment considers the availability of capital to

cover assets in light of their inherent credit risks, the degree to which the institution is leveraged and the risk that these assets

could result in capital losses.

Very LowVery High High Medium Low

Factor 1

Our assessment of capital adequacy measures an MDB’s capacity to absorb credit or market losses stemming from its operations, andthus preserve its ability to repay debt holders. MDBs hold capital as a buffer against potential credit losses as a consequence of theirlending and investment operations in sectors or regions that are naturally risky, in line with their mandates. In addition, most MDBs(including APICORP) do not have access to central bank liquidity facilities, given their supranational status. Hence, MDBs typically havesignificantly higher levels of capital adequacy than similarly rated commercial banks.

High levels of usable equity and relatively low leverage support capital adequacy

The capital adequacy ratio we use in our analysis of MDBs is the asset coverage ratio (ACR), which is the ratio of usable equity2 to thesum of loans, equity operations, and risk-weighted treasury assets. As of 2016, APICORP is in line with its peer group3 median, withan ACR of 47.7%. Despite the increase in usable equity, APICORP’s ACR fell for the first time last year since 2008 on account of thecorporation's accelerated expansion of loan operations (see Exhibit 3), which increased by 17.6% in 2016. At the same time, its leverageratio has also increased in 2016 but remains similar to the peer group median, as debt-to-usable equity stood at 127% in 2016 (seeExhibit 4), a bit lower than the median for Aa-rated peers (136%).

Exhibit 3

The upward trend in ACR was reversed in 2016%

Exhibit 4

Asset coverage and leverage ratios are broadly in line with similar-rated peersYear-end 2016, %

0

20

40

60

80

100

120

140

160

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Assets Coverage Ratio (ACR) Debt / Usable Equity

ACR: Usable Equity / (Gross Loans+Equity+Expected Loss on Liquid Assets)Source: APICORP, Moody's Investors Service

0

50

100

150

200

250

CDB(Aa1/STA)

IIC (Aa1/STA) APICORP(Aa3/STA)

Aa Median CABEI(A1/STA)

CAF(Aa3/STA)

Assets Coverage Ratio (ACR) Debt / Usable Equity

Source: Respective Financial Statements, Moody's Investors Service

5 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Nevertheless, as is our common practice for other deposit-taking MDBs, this ratio excludes deposits, which constitute a large sourceof funding for APICORP (37% of total liabilities in 2016). If we were to include deposits, APICORP’s leverage ratio would reach around200% at the end of 2016, similar to the (unadjusted) leverage ratio for CAF and CABEI.

APICORP calculates its capital adequacy ratio (Tier 1 + Tier 2 Capital/Total Risk-Weighted Exposure) at 28.9% as of June 2017, up from27.6% at year-end 2016 and broadly in line with levels recorded in 2015 and 2014. This ratio exceeds the Basel II and Central Bank ofBahrain guidelines of 8% and 12%, respectively. According to APICORP’s minimum capital adequacy guideline, the ratio should not fallbelow 20%.

APICORP’s capital position is also supported by the strong quality of its asset portfolio, reflected in comparatively high weightedaverage credit ratings for different asset classes. Based on the corporation’s internal calculations, the weighted average credit rating ofits total asset portfolio is in the A sphere, slightly lower than Aa-range for previous year. This breaks down into Corporate Finance GrossLoans,4 Direct Equity Investments and Treasury Assets (all with a weighted average rating in the A-range).5

The share of corporate loans in non-investment grade countries has increased in 2016 to 14.6% from 9.5% one year ago due tonew projects in Egypt (B3 stable), Azerbaijan (Ba2 stable) and Bahrain (B1 negative). However, the share of guaranteed loans hasincreased to almost 31% in 2016 from around 25% one year ago, most of which are guaranteed by governments and government-related entities. As of end-2016, almost 54% of the guarantees are provided by government-related entities, while 27% are providedgovernment. The rest are guaranteed by private sector third-party entities – in many cases parent companies. Compared to 2014, thecombined share of guarantees from governments and government-related entities has decreased a bit to 81% of all guarantees from87%.

Asset performance is relatively high

Our assessment of high asset performance reflects the relatively high quality of APICORP’s asset portfolio combined with graduallydeclining levels of non-performing loans (NPL). Nevertheless, the share of NPL in total gross loans remains higher than for its peers.

At year-end 2016, gross NPLs represented 2.06% of gross corporate finance loans. The ratio has come down from 2.4% in 2015 and isestimated to have decreased further to 2% as of June 2017 due to no loans entering non-performing status during last and this year. 6

Current NPLs include loans granted to the Iraqi Ministry of Oil and a Libyan asset. Exhibit 5 shows a comparison of APICORP’s problemloans with its peers. While APICORP’s point-in-time and seven-year average NPL ratio is higher than for its peer group, it is worthmentioning that the seven-year average NPL ratio has been continuously declining.

Exhibit 5

APICORP has higher NPL ratios than its peers% of gross loans

0.0 0.5 1.0 1.5 2.0 2.5 3.0

CAF (Aa3/STA)

CDB (Aa1/STA)

CABEI (A1/STA)

IIC (Aa1/STA)

APICORP (Aa3/STA)

2016 7-year average

Sources: Respective financial statements, Moody's Investors Service

In 2016, the amount of gross NPLs remained unchanged at $63.6 million after it was reduced by $4.8 million in 2015 as APICORPwrote off a $16.5 million NPL from the Government of Sudan (unrated) and had a new entry of $11.8 million from a Libyan exposure.APICORP had planned to write-off its NPL from Iraq’s Ministry of Oil ($51.8 million) but has not done so yet as the corporation expects

6 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

to recover at least part of total amount. Should the institution decide to write-off the loan and assuming no new NPL entries and basedon the June 2017 total loans of $3.19 billion, this would reduce the NPL ratio to 0.4% of total corporate finance loans, more in line withthe peer group.

In terms of peer comparison, despite having an asset base generally regarded as less creditworthy than that of APICORP, CAF has astrong track-record of maintaining low levels of NPLs. CABEI makes loans and guarantees primarily to governments and governmentalentities with a sovereign guarantee. The CDB lends to the public sector and therefore preferred creditor status can have significantpositive impact on asset performance. The IIC, on the other hand, lends only to the private sector and therefore receives very limitedbenefit from preferred creditor status.

APICORP’s relatively weaker asset performance in its corporate finance loan book reflects, in part, the challenging geopoliticalenvironment in which it operates. However, while APICORP’s relative position is weak, the absolute size of NPLs remains fairly smalland stable, and is fully provisioned (see Exhibit 6), mitigating any corresponding credit concern. Specific provisions were increased in2014, in order to cover geopolitical uncertainties in Iraq and Libya.

Exhibit 6

APICORP’s NPLs are more than fully provisionedUS$ million, as of end-2016

63.6

-18.8

-25.9

-45.5

-25.2

-30

-20

-10

0

10

20

30

40

50

60

70

Gross NPLs Cash Collateral Specific Impairment Provision Collective Impairment Provision Net NPLs

Sources: APICORP, Moody's Investors Service

APICORP’s de facto preferred creditor status on its public-sector backed lending helps to keep NPLs at a moderate and manageablelevel, although it does not eliminate credit losses. Given that almost 80% of loans as of end-2016 are to governments or government-related entities – up from 68% in 2013 – preferred creditor status has the potential to boost the performance of a significant portion ofits exposures. However, preferred creditor status is not incorporated into any loan documentation, which is common practice amongMDBs. Indeed, the current stock of NPLs in Libya and Iraq are loans to government-related entities.

According to Articles 6 & 12 of the Establishing Agreement, the corporation must “preserve and protect APICORP’s assets, rights andprivileges of nationality, as well as its interests [held] internationally by its members.” Article 15 grants APICORP preferential access toforeign exchange in the event of a country’s foreign-exchange crisis.

Consistent with these preferences, APICORP’s loans are exempt from country risk provisioning when applicable, and its loans havenever been included in general country debt rescheduling. APICORP has only once been involved in a Paris Club rescheduling7 (Algeriain 1995) and it subsequently recovered 100% of its outstanding loan balance. Similarly, APICORP has never been subject to mandatorynew money obligations under any country debt rescheduling. Examples of this include Paris Club rescheduling and debt-forgivenessof Iraqi sovereign obligations in 2003: APICORP’s outstanding loans to government-related entities were not included in any of itsprovisions.

Concentration of assets indicates potential for sizeable impact on capital adequacy

Given its mandate to finance energy-related projects in OAPEC member states, APICORP’s asset portfolio is inevitably concentratedin the energy sector and in the Middle East region. This concentration is not atypical for regional MDBs. APICORP’s concentration

7 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

based on the top five country exposures is high, but not inconsistent with its peers, with the exception of the IIC which has a largerregional scope than the others. However, APICORP’s assets are concentrated even within the country and sectorial buckets, with aparticularly high geographic concentration in Saudi Arabia and Qatar (57% of loans) – with an additional 20% in UAE and Oman – andin hydrocarbon-related8 projects (around 65% of loans).

We also note that APICORP’s portfolio of treasury investments at end-2016 had significant exposure to members, either directlythrough government bonds or indirectly through state-owned entities, with close to 80% of fixed income investments in GCCcountries. While these instruments tend to be highly rated, investing treasury assets in members further compounds the geographicconcentration of assets.

Having said that, APICORP is making progress in diversifying its assets portfolio across regions and sectors. With the acquisition of theUK-based Ashtead Technology in 2016, the corporation increased its exposure to regions outside-GCC. At the same time, APICORPincreased its exposure to the US through higher investment in US T-bills as well as direct equity investment.

Track record of profitability directly supports capital adequacy

Despite having a development mandate, APICORP, unlike many other MDBs, operates on a commercial basis, and, at times, paysdividends to shareholders. We typically assess the profitability of an MDB in terms of the contribution that it makes to building ordepleting the institution’s capital base. This analysis is particularly relevant in the case of APICORP, where the board decided to forgodividend distributions in seven out of the past 10 years to strengthen the corporation’s balance sheet.

APICORP has a strong track record of profitability that has bolstered the capital base over time. However, on the back of low oil pricesnet income dropped to $93.4 million in 2016 from $107.6 million one year earlier and slightly below the budgeted $95.6 million. Thereduction was driven by a 36.8% drop in income from equity investment, which more than offset the increase in net interest incomeand other investment income. Following a sharp rise in 2013, general administrative expenses declined for a third straight year to $35.5million in 2016 from $37.7 million the year before. For the first eight months of 2017, net income was $68.1 million9, slightly behind thebudgeted $69 million, and about 69% of the full year target of $99.2 million.

Return on assets for 2016 was 1.5%, down from 1.9% in 2015. In the first eight months of 2017 the ratio improved again slightly to1.7% Return on equity has been very strong, with an average of 6.9% since 2007 and year-end 2016 results of 4.8%.

Challenging operating environment but no material impact on asset quality and capital adequacy

In the recent past, APICORP has faced new challenges in its operating environment given political unrest in a number of membercountries and the subsequent deterioration in their respective sovereign risk profiles. However, the corporation does not have anyloan exposure to Syria (unrated), while its loan portfolio in Libya (unrated), Iraq (Caa1 stable) and Egypt (B3 stable) represents anaggregate 8.1% of total country exposure. For its investments in these countries, APICORP has fully provisioned for expected losseswhere applicable, preempting a significant deterioration on the corporation’s financial performance. The diplomatic conflict of Qatarwith neighboring countries has not had an impact on APICORP's credit profile so far.

Developments in global energy markets, which have been characterized by lower global benchmark oil prices, pose a potential threat toAPICORP’s credit profile given the sectoral concentration of its assets in petroleum-related projects. Low energy prices predominantlyaffect dividend payments from direct equity investments. APICORP has taken into consideration these developments by lowering thebudgeted direct equity income share in its 2016 and 2017 budget and reducing operating expenses. According to the corporation,an environment of prolonged low oil prices will clearly be detrimental to prospects of investee companies. As such, the ongoingdiversification of the investment portfolio is a positive.

From a lending perspective, lower oil and gas prices could potentially affect the debt-service capacity of projects, but APICORPmaintains that current oil prices are still above the historically calculated project-specific breakeven prices. The corporation seespotential positive impact from low oil prices on trade financing for net oil importers, and advisory and financing opportunities relatedto debt restructuring and refinancing.

Sustained low oil prices could put pressure on funding and liquidity conditions in the region where APICORP is operating in, particularlyfor oil exporters.

8 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Liquidity: HighImproving maturity mismatch but deposits still account for a sizable share of funding

Scale

+ -

A financial institution’s liquidity is important in determining its shock absorption capacity. We evaluate the extent to which liquid

assets cover debt service requirements and the stability of the institution’s access to funding.

Very High High Medium Low Very Low

Factor 2

Use of short-term wholesale deposit funding leads to balance sheet maturity mismatch…

The degree to which APICORP’s funding is reliant on wholesale deposits is unusual for an MDB. APICORP uses short-term wholesaledeposits to fund its sizeable treasury operations for the purposes of profit generation and liquidity. In addition, it uses them as asource of funding for a portion of its loan operations. At end-2016, 33.3% of its total liabilities were short-term deposits from banks,corporates and member states. While this share has been decreasing from 51.7% reported in 2013, within the small group of deposit-taking MDBs, APICORP remains amongst the most reliant on short-term funding.

By contrast, 75.1% of APICORP’s assets were long term (remaining maturity over one year), with 41.6% of assets having a remainingmaturity of five years or more, up from 70.5% and 34.6%, respectively in 2014. This balance sheet maturity mismatch is a challengefor the corporation and constrains creditworthiness. Balance sheet maturity mismatches of this magnitude are uncommon in the MDBsector, and we therefore make an adjustment to our liquidity score adjustment.

Exhibit 7

APICORP is among a small group of MDBs that take deposits

Deposits/Total Liabilities, end-2016

African Export-Import Bank (Afreximbank, Baa1/STA) 3.44%

Corporacion Andina de Fomento (CAF, Aa3/STA) 12.3%

Central American Bank for Economic Integration (CABEI, A1/STA) 15%

Arab Petroleum Investments Corporation (APICORP, Aa3/STA) 36.9%

Fondo Latinoamericano de Reservas (FLAR, Aa2/STA) 99.80%

Sources: Respective financial statements, Moody's Investors Service

We view wholesale deposits as a potentially volatile source of funding and vulnerable to market confidence, owing to their greaterconcentration and correlation to economic cycles relative to retail deposits. Moreover, because MDBs tend to engage in medium tolong-term lending activity, relying on deposit funding can lead to a balance sheet maturity mismatch.

Whereas we acknowledge that APICORP’s deposits exhibit some stability based on the corporation’s own definition of threeconsecutive months of renewal, APICORP’s overall funding profile is somewhat weaker than for its peers.

…which is partly mitigated by stability of deposits and term financing program

There are some mitigating factors to this mismatch: deposits from corporates and government-related entities (which accounted for60% of the deposit base in 2016) are relatively stable because they are mainly deposited by companies owned by member statesthrough their state-owned oil & gas companies, or other entities with ties to one or more member states. In addition, a significantportion of these companies also have a loan or direct equity investment client relationship with APICORP, which presumably makesthem somewhat more stable than typical wholesale deposits, based on existing loan or equity relationships in place or a history ofregular renewal. Deposits from corporates have increased since the opening of the Bahrain branch in 2006, when they comprised only18% of total deposits.

9 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Another mitigating factor is that deposits from shareholders, which amounted to $107.5 million and accounted for 6.4% of the depositbase at year-end 2016, have been stable over the past three years. Indeed, despite significant transition and stress starting in 2011,Libya and Syria have not withdrawn their deposits.

Over the past couple of years, efforts have focused on lengthening the average maturity of debt to mitigate the mismatches resultingfrom the short-term nature of deposits. As of end-2016, long-term funding – equity, term financing, bonds and shareholder deposits –made up 76% of the corporation’s net stable funding requirements (for corporate finance loans and equity investments).10 Achieving ahigher ratio in 2013 was helped by the 2012 closing of three Islamic term financings with maturities of three to five years.

In addition to contributing to a maturity lengthening, the three facilities also helped diversify APICORP’s creditor base, facilitatingaccess to Islamic pools of liquidity. Although it did not issue long-term debt in 2013, APICORP transacted its first term repo of$173 million with a 15-month maturity. In March 2014, it also engaged in a SAR1 billion ($267 million) five-year bilateral long termfinancing. This was followed by another SAR3 billion five-year Islamic Club Term Facility in December, which included refinancingand additional borrowing. Also, in December 2014, APICORP raised $150 million through a three-year Islamic Club Term Facility.In June 2015, APICORP established a $3 billion medium-term sukuk program (rated (P)Aa3), with the aim of further lengthening itsdebt maturity, which was tapped for the first time in October 2015 with a $500 million five-year sukuk issuance. In August 2016, theinstitution issued a SAR250 million ($66 million) three-year private sukuk bond, followed by the first Formosa bond on the Taiwanesemarket in September 2016 ($300 million with maturity of five years). In early October 2017, APICORP announced another five-yearFormosa bond and the Corporation will most likely re-tap its existing medium-term sukuk programme again in 2017.

Liquidity management consistent with business model, different from most MDBs

APICORP manages liquidity by grouping maturing assets and liabilities into five time buckets: up to one month, one month to threemonths, three months to one year, one to five years, and over five years. The associated cash inflows and outflows are matched (Exhibit8) and the cumulative gap between the cash flows as a percentage of liabilities is the relevant ratio that is managed by APICORP. As aresult of the corporation’s willingness to reduce the short-term maturity mismatch, the cash flow gap up to one year was down to 5%as of end-2015 from an average of 21% between 2012 and 2014. However, as of end-2016, the cumulative mismatch had increasedagain, to 7.5%. APICORP has set thresholds for the ratio in most of the time buckets11 and at end-2016 was within the applicablethresholds for all of the buckets.

Exhibit 8

Maturity profile of assets and liabilities as of 31 December 2016

% of Total < 1 month 1-3 months 3-12 months 1-5 years >5 years

Assets 12.8% 5.0% 7.1% 33.5% 41.6%

Liabilities 13.2% 11.5% 7.6% 34.7% 33.0%

Absolute Maturity Gap (US$ million) -28.021 -401.124 -29.703 -72.064 530.912

Sources: APICORP, Moody's Investors Service

Most MDBs do not have a maturity mismatch, and manage liquidity primarily through a policy dictating the holding of a minimumlevel of liquid assets, such that a certain number of forthcoming months’ net cash outflow demands are covered. While APICORPmanagement does have such a policy, the methodology used for the calculations differs from other MDBs and as a result it is notmeaningful to make comparisons with its peers. There are several ratios that APICORP is using to manage liquidity risk. The LiquidityCoverage Ratio measures total high quality liquid assets as percent of total net cash outflow over the next three months. The ratio fellin 2016 to 172% from 381% a year earlier. However, it increased in the first half of this year and reached 624% in June 2017 due toadditional investment in T-bills this year. The second ratio is the Liquidity Asset Ratio, which measures total discounted liquid assetsas percent of net cash requirements for the next 12 months. It has also decreased in 2016 to 68% from 74% but recovered to 83%in the first half of 2017, which is still below the target of 100%. This year, the corporation added the Survival Horizon metrics, whichmeasures the number of months APICORP is able to fullfil all its payment obligations under a stress scenario, which assumes loss ofmarket access and a haircut up to 32% on treasury assets. As of end-June 2017, this ratio stood at 9.9 months.

10 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

As shown in Exhibit 9, APICORP’s liquidity position is the weakest in its direct peer group when its deposits are incorporated intothe analysis. The exhibit illustrates that in the extremely unlikely event that APICORP loses market access for refinancing—and issimultaneously challenged by a run on deposits—APICORP could face challenges fulfilling its debt service requirements over the courseof a full year.

Exhibit 9

If deposits are included APICORP has the weakest debt service coverage ratio in its peer group(Short-term debt + currently maturing long-term debt) / discounted liquid assets (end-2016)

0

10

20

30

40

50

60

70

80

90

100

CDB (Aa1/STA) IIC (Aa1/STA) CAF (Aa3/STA) CABEI (A1/STA) APICORP (Aa3/STA)

Base Ratio Including Short-Term Deposits in the Numerator

Sources: Respective financial statements, Moody's Investors Service

APICORP’s portfolio of treasury investments are entirely funded by short-term deposits. We do not consider the quality of theseinvestments to offset the risks to liquidity in full from the wholesale and short-term nature of the funding. That said, APICORP hasdiversified its treasury investment to include G-7 countries' 12 government paper, which remain highly liquid even during times offinancial market turmoil. As of June 2017, APICORP had invested $200 million in US T-bills to improve portfolio's quality and liquidity.This adds to sovereign fixed income investment in the UK and Germany.

11 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Strength of member support: Very HighVery strong shareholder base, reinforced by incremental capitalization from retained earnings

Scale

+ -

Contractual support primarily manifests itself in the callable capital pledge, which is a form of emergency support. Extraordinary

support is a function of shareholders’ ability and willingness to support the institution in ways other than callable capital. Strength of

member support can increase the preliminary rating range determined by combining factors 1 and 2 by as many as three scores.

Very High High Medium Low Very Low

Factor 3

Renewed capital increase underlines shareholder support

In May 2011, APICORP’s shareholders agreed to change the capital structure by introducing callable capital in the amount of $750million. Callable capital is an unconditional and full-faith obligation of each member country to provide additional capital within twomonths when called. Along with sustained strong financial performance, this led to the upgrade of APICORP’s rating to Aa3 from A1 inSeptember 2012.13 In April 2016, the shareholders' $1 billion line of credit was replaced with additional callable capital of $500 millionwhich increased total callable capital to $1 billion. The introduction of callable capital demonstrates stronger support than the line ofcredit made available by shareholders in 2008.

As a result of the increase in capital, the callable capital coverage of the corporation’s debt stock has increased, putting contractualsupport at ”Medium” from “Low” in our methodological scorecard, with debt representing 4.3 times the amount of discounted callablecapital, lower than peers like CAF and CABEI.

Likelihood of extraordinary support demonstrated by high shareholder ratings, capital increase

The weighted median rating of APICORP’s shareholders was A1 as of end-2016 reflecting a strong ability to provide extraordinarysupport. In comparison, the corresponding indicators for peers were much lower, with CABEI at Ba2, CAF at Baa3, CDB at Baa3.

Of APICORP’s 10 member countries, seven are rated by Moody’s (United Arab Emirates – Aa2 stable, Kuwait – Aa2 stable, Qatar – Aa3negative, Saudi Arabia – A1 stable, Bahrain – B1 negative, Egypt – B3 stable, Iraq - Caa1 stable).14 The capital base is held primarily byinvestment-grade countries (61%) – although none are Aaa-rated – with the remainder held by non-investment-grade (16%) or non-rated countries (23%).

APICORP’s track record of receiving capital increases demonstrates a strong propensity for shareholders to provide support. At the timecallable capital was introduced in 2011, the amount of paid in capital was also increased by $200 million, all of which was funded bythe capitalization of dividends and reallocation from reserves. Similarly, the previous capital increase exercises in 1981, 1996, and 2003were funded by reallocation from reserves and capitalization of dividends rather than by new funds from shareholders.

In line with the decision to forego dividend distributions for 2016, APICORP’s shareholders further demonstrated their support for thecorporation by allowing for the use of reserves to gradually fulfill each shareholder’s capital subscription. As such, in the absence offurther capital increases, APICORP’s capital structure will gradually shift as paid in capital increases, while callable capital decreases.

Moreover, the strategic importance of the energy sector to the OAPEC economies backs our view that APICORP benefits from a highpriority of support.

Very liberal terms in relation to callable capital

APICORP’s shareholders have explicitly committed to support the institution on a “joint and several” basis. Article 6 of the Articles ofAgreement states: “The Member States undertake, jointly and severally, to support the Corporation, protect it and embrace its causesin every way that ensures the protection of its rights and interests internationally and otherwise and undertake to facilitate all theactivities related to its objectives and to adopt all possible measures to that end.”

12 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Although we do not regard the wording of this pledge as a full financial guarantee for creditors, it does indicate a stronger willingnessto support as compared to the pro rata wording of support pledges of other MDBs. Typically, each member’s fulfillment of the callablecapital obligation is independent of the action of the other shareholders.

While it is rare for an MDB to have shareholder support in this more collective form, the language in the Articles of Agreement isopen to interpretation and is not explicitly linked to callable capital. Hence, we monitor the capital adequacy ratios amended forconsideration of joint and several callable capital (i.e., including all callable capital because the highest-rated shareholder is rated Aa2).At the same time, the key ratio we use in our analysis of contractual support—the callable capital coverage ratio—continues to includeonly the callable capital provided by those members rated Baa3 or higher.

Another unique feature of APICORP’s callable capital is that the conditions under which APICORP can request callable capital is notrestricted to debt service. Management can request callable capital in order to service debt, to expand development operations (whilemaintaining capital adequacy ratios), or to absorb losses from treasury or development-related assets. These very liberal callable capitalguidelines differ from other MDBs, which can only request callable capital to service debt. Once requested, APICORP’s callable capital isexpected to be paid in by members within two months.

13 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Rating rangeCombining the scores for individual factors provides an indicative rating range. While the information used to determine the grid mapping is mainly historical, our ratings incorporateexpectations around future metrics and risk developments that may differ from the ones implied by the rating range. Thus, the rating process is deliberative and not mechanical,meaning that it depends on peer comparisons and should leave room for exceptional risk factors to be taken into account that may result in an assigned rating outside the indicativerating range. For more information please see our Supranational Rating Methodology.

Supranational rating metrics: Arab Petroleum Investments Corporation

+ -

+ -

+ -

+ -

Very LowVery High High Medium Low

High Medium Low Very LowVery High

Very High High Medium Low Very Low

Aa3

Aaa-Aa2

Very High High Medium Low Very Low

Capital Adequacy

How strong is the capital buffer?

How strong is the institutions' shock absorption capacity?

Sub-Factors: Position, Funding

Assigned Rating:

Strength of Member Support

Intrinsic Financial Strength

Sub-Factors: Capital Position, Leverage, Asset Performance

How strong is members' support of the institution?

Sub-Factors: Contractual Support, Extraordinary Support

Rating Range:

Liquidity

Source: Moody's Investors Service

14 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

ComparativesThis section compares credit relevant information regarding APICORP with other supranationals rated by Moody’s Investors Service. Itfocuses on a comparison with supranationals within the same rating range and shows selected credit metrics and factor scores.

APICORP benefits from a solid capital position and relatively low leverage, placing the corporation’s capital adequacy in the samecategory as CAF and higher than CABEI, although CDB and IIC have stronger equity and asset quality. APICORP’s liquidity positionis hampered by a relatively large level of short-term debt due to its reliance on deposits, which is partially offset by a lower cost offunding than CDB or CAF. Finally, shareholder support is a key credit strength that places APICORP in a favorable position relative topeers, with a high median shareholder rating of A1 and the existence of callable capital.

Exhibit 12

Arab Petroleum Investments Corporation's key peersYear APICORP CDB CAF IIC CABEI Aa Median

Rating/Outlook Aa3/STA Aa1/STA Aa3/STA Aa1/STA A1/STA --

Total Assets (US$ million) 2016 6,142 1,599 35,669 2,147 9,194 6,472

Factor 1 High Very High High Very High Medium --

Usable Equity/Gross Loans Outstanding + Equity Operations (%)[1] 2016 47.7 88.4 46.8 115.3 41.9 47.7

Debt/Usable Equity (%)[1] 2016 126.6 73.0 197.4 104.0 199.0 136.2

Gross NPLs/Gross Loans Outstanding (%)[2] 2016 2.1 0.5 0.0 1.0 0.0 0.0

Factor 2 High Very High Very High Very High Very High --

ST Debt + CMLTD/Liquid Assets (%)[3] 2016 27.3 1.7 34.6 33.7 30.1 22.4

Bond-Implied Ratings (Long-Term Average) 2010-2016 -- A3 A3 -- A3 Aa3

Intrinsic Financial Strength (F1+F2) High Very High High Very High High --

Factor 3 Very High Very High Low Medium Medium --

Total Debt/Discounted Callable Capital (%)[4] 2016 426.0 111.9 2828.8 -- 544.7 111.9

Weighted Median Shareholder Rating (Year-End) 2016 A1 Baa3 Baa3 A3 Ba2 A1

Rating Range (F1+F2+F3) Aaa-Aa2 Aaa-Aa2 Aa2-A1 Aaa-Aa2 Aa1-Aa3 --

Notes:[1] Usable equity is total shareholder's equity and excludes callable capital[2] Non performing loans[3] Short-term debt and currently maturing long-term debt[4] Callable capital pledge by members rated Baa3 or higher, discounted by Moody's 30-year expected loss rates associated with ratingsSources: Moody's Investors Service, respective MDB financial statements

15 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

DATA AND REFERENCESRating history

Exhibit 13

Arab Petroleum Investments Corporation

16 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Annual statistics

Exhibit 14

Arab Petroleum Investments Corporation

2010 2011 2012 2013 2014 2015 2016

Balance Sheet, USD Thousands

Assets

Cash & Equivalents 455,265 661,717 809,473 570,776 982,912 995,068 838,575

Securities 903,353 794,491 952,170 1,183,464 1,181,092 1,068,980 1,203,518

Net Loans 2,541,968 2,803,489 2,897,046 2,923,135 2,690,803 2,510,060 2,951,598

Net Equity Investments 365,634 324,284 318,002 822,607 865,957 922,530 987,249

Other Assets 45,403 45,523 100,884 175,181 163,237 156,050 160,794

Total Assets 4,311,623 4,629,504 5,077,575 5,675,163 5,884,001 5,652,688 6,141,734

Liabilities

Borrowings 1,338,854 1,369,142 1,832,887 1,698,413 2,114,878 2,010,395 2,533,078

Other Liabilities 1,831,791 2,041,577 1,936,649 2,172,175 1,912,140 1,733,008 1,607,912

Total Liabilities 3,170,645 3,410,719 3,769,536 3,870,588 4,027,018 3,743,403 4,140,990

Equity

Subscribed Capital 550,000 1,500,000 1,500,000 1,500,000 1,500,000 1,500,000 2,000,000

Less: Callable Capital 0 750,000 750,000 750,000 500,000 500,000 1,000,000

Equals: Paid-In Capital 550,000 750,000 750,000 750,000 1,000,000 1,000,000 1,000,000

Retained Earnings (Accumulated Loss) 85,580 94,854 97,931 100,605 93,953 96,511 83,822

Reserves 505,398 373,931 460,108 953,970 763,030 812,774 916,922

Total Equity 1,140,978 1,218,785 1,308,039 1,804,575 1,856,983 1,909,285 2,000,744

Exhibit 15

Arab Petroleum Investments Corporation

2010 2011 2012 2013 2014 2015 2016

Income Statement, USD Thousands

Net Interest Income 16,849 27,202 40,206 42,863 40,114 44,907 53,814

Interest Income 60,580 77,500 104,729 109,084 106,701 106,662 125,758

Interest Expense 43,731 50,298 64,523 66,221 66,587 61,755 71,944

Net Non-Interest Income 104,180 109,666 99,542 107,797 102,692 100,359 75,084

Net Commissions/Fees Income 1,802 1,224 1,076 2,935 1,460 1,218 117

Income from Equity Investments 67,048 96,411 71,624 71,218 86,530 85,883 54,251

Other Income 35,330 12,031 26,842 33,644 14,702 13,258 20,716

Other Operating Expenses 25,849 31,514 30,857 38,603 37,773 37,664 35,474

Administrative, General, Staff 25,849 31,514 30,857 38,603 37,773 37,664 35,474

Pre-Provision Income 95,180 105,354 108,891 112,057 105,033 107,602 93,424

Loan Loss Provisions (Release) 0 0 0 0 0 0 0

Net Income (Loss) 95,180 105,354 108,891 112,005 104,953 107,511 93,322

Other Accounting Adjustments and Comprehensive Income 0 0 0 0 0 0 0

Comprehensive Income (Loss) 95,180 105,354 108,891 112,005 104,953 107,511 93,322

17 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Exhibit 16

Arab Petroleum Investments Corporation

2010 2011 2012 2013 2014 2015 2016

Financial Ratios

Capital Adequacy, %

Usable Equity / (Loans + Equity) 37.1 36.5 38.0 45.8 48.8 52.0 47.7

Debt/Usable Equity 117.3 112.3 140.1 94.1 113.9 105.3 126.6

Allowance For Loan Losses / Gross NPLs 34.8 41.8 65.6 69.1 81.9 73.9 69.2

NPL Ratio: Non-Performing Loans / Gross Loans 2.6 3.3 2.3 2.3 2.4 2.4 2.1

Return On Average Assets 2.3 2.4 2.2 2.1 1.8 1.9 1.6

Interest Coverage Ratio (X) 3.2 3.1 2.7 2.7 2.6 2.7 2.3

Liquidity, %

St Debt + CMLTD / Liquid Assets 30.1 57.5 20.1 9.8 63.7 0.0 27.3

Bond-Implied Rating 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Liquid Assets / Total Debt 101.5 106.4 96.1 103.3 102.3 102.7 80.6

Liquid Assets / Total Assets 31.5 31.5 34.7 30.9 36.8 36.5 33.2

Strength of Member Support, %

Callable Capital (CC) of Baa3-Aaa Members/Total CC - 64.0 64.0 64.0 64.0 64.0 61.0

Total Debt/Discounted Callable Capital - 290.5 388.9 360.9 674.1 669.2 426.0

Weighted Median Shareholder Rating (Year-End) Aa3 Aa3 Aa3 Aa3 Aa3 Aa3 A1

18 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Moody’s related research

» Rating Action: Moody's assigns provisional (P)Aa3 rating to APICORP's proposed Formosa bond, 5 October 2017

» Credit Opinion: Arab Petroleum Investments Corporation – Aa3 Stable: Regular update, 31 May 2017

» Rating Action: Moody's affirms APICORP at Aa3; maintains stable outlook, 23 September 2016

» Rating Methodology:Multilateral Development Banks and Other Supranational Entities, 29 March 2017

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of thisreport and that more recent reports may be available. All research may not be available to all clients.

Related websites and information sources

» APICORP

MOODY’S has provided links or references to third party World Wide Websites or URLs (“Links or References”) solely for yourconvenience in locating related information and services. The websites reached through these Links or References have not necessarilybeen reviewed by MOODY’S, and are maintained by a third party over which MOODY’S exercises no control. Accordingly, MOODY’Sexpressly disclaims any responsibility or liability for the content, the accuracy of the information, and/or quality of products or servicesprovided by or advertised on any third party web site accessed via a Link or Reference. Moreover, a Link or Reference does not imply anendorsement of any third party, any website, or the products or services provided by any third party.

Authors

Steffen DyckVice President - Senior Credit Officer

Eugeniu CroitorAssociate Analyst

19 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

Endnotes1 The principal objective of the OAPEC Agreement is the development of regional cooperation in the petroleum industry. In pursuit of this objective, OAPEC

sponsored the creation of four companies: APICORP, the Arab Maritime Petroleum Transport Company, the Arab Shipbuilding and Repair Yard Company,and the Arab Petroleum Services Company.

2 Paid-in capital + reserves + retained earnings.

3 Caribbean Development Bank (CDB, Aa1); Corporacion Andina de Fomento (CAF, Aa3); Inter-American Investment Corporation (IIC, Aa1) and CentralAmerican Bank for Economic Integration (CABEI, A1).

4 Loans account for 50% of APICORP’s assets, direct equity 18%, and treasury 20%.

5 Treasury investment policy does not allow for investments in securities rated below Baa3.

6 The corporation’s practice is to remove a loan from NPL status once all late payments have been paid.

7 Debt rescheduling by official/bilateral creditors.

8 Includes petrochemical, petroleum refineries, production and storage, gas processing, and other petroleum-related loans.

9 According to unaudited results.

10 The net stable funding ratio (NSFR) is calculated by APICORP as the available amount of stable funding over the required amount of stable funding. TheNSFR should be equal to or exceed 100% and will become a minimum standard by 1 January 2018.

11 Thresholds are -30% in the ‘up to one month’, ‘one month to three months’, ‘three months to one year’, respectively. No thresholds are assigned for the‘one to five years’ and ‘over five years’ buckets.

12 United States (Aaa stable), United Kingdom (Aa2 stable), France (Aa2 stable), Germany (Aaa stable), Italy (Baa2 negative), Canada (Aaa stable), and Japan(A1 stable).

13 See Moody’s upgrades APICORP to Aa3, outlook stable, 25 September 2012.

14 Ratings as of 10 October 2017.

20 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

REPORT NUMBER 1092179

21 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis

MOODY'S INVESTORS SERVICE SOVEREIGN AND SUPRANATIONAL

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

22 10 October 2017 Arab Petroleum Investments Corporation (APICORP) – Aa3 stable: Annual credit analysis