APAS MONTHLY - Ashvin Parekh Advisory Services LLP Monthly_May 2019.pdf · opens allotment ‘on...

33

2019 Volume 5 THIS MONTH Season’s greetings! In this issue, Mr. Amit Tandon, Founder & MD, IiAS, has presented his thoughts on ‘Corporate Governance: The Journey to 4G’. We thank Mr. Amit Tandon for his contribution to the APAS Monthly. This month, the APAS column presents its views on ‘Impact of US-China and US-Iran relations’. The economic indicators showed mixed performance. Manufacturing PMI fell to an 8-month low of 51.8 in April from 52.6 in March. India’s annual infrastructure output in April grew at 2.6%. India's Index of Industrial Production (IIP) slowed to a 21-month low of 0.1% in March. PMI services fell to a 7-month low of 51 in April from 52 in March, while composite PMI dipped to 51.7 in April from 52.7 in March. CPI inflation rose to a 6-month high of 2.92% in April from 2.86% in March. WPI inflation slipped to 3.07% in April from 3.18% in March. The Gross Domestic Product (GDP) growth rate for the fourth quarter (January-March) of 2018-19 slipped to a 20-quarter low of 5.8%. For the full year 2018-19, GDP slumped to a 5-year low of 6.8%. The Reserve Bank of India (RBI) released Second Bi-monthly Monetary Policy Statement, 2019-20. The RBI notified the revised Voluntary Retention Route for Investments by Foreign Portfolio Investors (FPIs) and opened allotment ‘on tap’. The RBI also released guidelines on Extension of Timings for Customer Transactions on Real Time Gross Settlement (RTGS) System. APAS MONTHLY

Transcript of APAS MONTHLY - Ashvin Parekh Advisory Services LLP Monthly_May 2019.pdf · opens allotment ‘on...

2019

Volume 5

THIS MONTH

Season’s greetings!

In this issue, Mr. Amit Tandon, Founder & MD, IiAS, has presented his thoughts on ‘Corporate

Governance: The Journey to 4G’. We thank Mr. Amit Tandon for his contribution to the APAS

Monthly.

This month, the APAS column presents its views on ‘Impact of US-China and US-Iran relations’.

The economic indicators showed mixed performance. Manufacturing PMI fell to an 8-month low of

51.8 in April from 52.6 in March. India’s annual infrastructure output in April grew at 2.6%. India's

Index of Industrial Production (IIP) slowed to a 21-month low of 0.1% in March. PMI services fell to

a 7-month low of 51 in April from 52 in March, while composite PMI dipped to 51.7 in April from

52.7 in March. CPI inflation rose to a 6-month high of 2.92% in April from 2.86% in March. WPI

inflation slipped to 3.07% in April from 3.18% in March.

The Gross Domestic Product (GDP) growth rate for the fourth quarter (January-March) of 2018-19

slipped to a 20-quarter low of 5.8%. For the full year 2018-19, GDP slumped to a 5-year low of 6.8%.

The Reserve Bank of India (RBI) released Second Bi-monthly Monetary Policy Statement, 2019-20.

The RBI notified the revised Voluntary Retention Route for Investments by Foreign Portfolio

Investors (FPIs) and opened allotment ‘on tap’. The RBI also released guidelines on Extension of

Timings for Customer Transactions on Real Time Gross Settlement (RTGS) System.

APAS

MONTHLY

The Insurance Regulatory and Development Authority of India (IRDAI) released guidelines on

Reconciliation of Co-Insurers Balance from ETASS. IRDAI also released guidelines on Preparation

of Financial statements for FY 2019-20 and Onwards.

Ministry announced PM-KISAN Scheme extension to include all eligible farmer families irrespective

of the size of land holdings. Ministry also announced Pension scheme to secure lives of 5 crore farmers

in three years.

Securities Exchange Board of India (SEBI) released norms on Participation of Mutual Funds in

Commodity Derivatives Market in India.

We hope that this APAS Monthly is insightful. We welcome your inputs and thoughts and encourage

you to share them with us.

Ashvin parekh

On the cover

GUEST COLUMN

Mr. Amit Tandon Founder & MD IiAS Corporate Governance: The Journey to 4G

ECONOMY

➢ Index of Industrial Production – March

➢ Inflation update – April

➢ PMI update – April

➢ Core Sector – April

➢ GDP – Q4 – FY 18-19

APAS COLUMN

Impact of US-China and US-Iran relations

INSURANCE ➢ Reconciliation of Co-Insurers Balance from ETASS

➢ Preparation of Financial Statements for FY 2019-20

and Onwards

INFRASTRUCTURE & OTHER

GOVT. INITIATIVES

➢ PM-KISAN Scheme extension to include all eligible

farmer families irrespective of the size of land

holdings

➢ Pension scheme to secure lives of 5 crore farmers in

three years

BANKING

➢ Second Bi-monthly Monetary Policy Statement, 2019-20

Resolution of the Monetary Policy Committee (MPC),

Reserve Bank of India

➢ RBI notifies the revised Voluntary Retention Route for

Investments by Foreign Portfolio Investors (FPIs) and

opens allotment ‘on tap’

➢ Real Time Gross Settlement (RTGS) System – Extension of

Timings for Customer Transactions

CAPITAL MARKETS SNAPSHOT

➢ CNX Nifty, BSE Sensex, India VIX, $/₹, GIND 10Y

CAPITAL MARKETS

➢ Participation of Mutual Funds in Commodity

Derivatives Market in India

ECONOMIC DATA SNAPSHOT

➢ Global GDP, CPI, Current account balance, budget

balance, Interest rates

It is convenient to characterize telecom technology from 1G (voice), to 2G (SMS, MMS), 3G (data, mobile

internet), 4G (videoconferencing, mobile TV, gaming). We can similarly label India’s corporate governance

(CG) journey, which is described below:

First generation

India’s journey began in 1997 with the Confederation of Indian Industry setting up a task force, under Rahul

Bajaj, to look at CG. This was within five years of the UK setting up "The Committee on the Financial Aspects

of Corporate Governance," since known as the Cadbury Committee - after its chairman Adrian Cadbury, to

look at ‘the arrangement of company boards and accounting systems to mitigate corporate governance risks

and failures.’ The final CII report, with a quirky title ‘Desirable Corporate Governance: A Code’ was presented

a year later, in 1998 and it introduced the concept of CG to Indian markets. The committee did not define CG

and instead focused on a few elements – transparency, disclosures, boards, etc. It did recognize that

‘corporate governance goes far beyond company law’ – something that is usually forgotten.

A year later, SEBI formed a committee with Kumar Mangalam Birla in the chair. Its recommendations focused

on two aspects, focusing on Boards’ responsibilities and pushing for better disclosures. It introduced the audit

committee, the board composition with the need for independent directors. It highlighted the need for

quarterly reporting and the annual report containing an MD&A section.

Importantly, most of the recommendations were presented as mandatory - enforced on companies in a

phased manner - as the committee was of the view that ‘a statutory rather than a voluntary code would be

far more purposive and meaningful’.

These recommendations, better known as Clause 49, were incorporated into the listing agreement and rolled

out between 2000 and 2003.

Corporate Governance:

The Journey to 4G Mr. Amit Tandon Founder & MD IiAS

Second Generation

Even as the Listing Agreement was being adopted Enron and a number of other accounting scandals rocked

the US corporate establishment. The US quickly overhauled their accounting rules and investor protection

oversight through the Sarbanes-Oxley Act of 2002.

This resulted in a series of reviews of the CG landscape in India. First the Naresh Chandra Committee, with a

strong focus on the accounting framework – auditors, their appointment, fees, audit committees etc.). This

was followed by the 2003 Narayan Murthy Committee tasked to review the progress of the Kumar Mangalam

Committee and strengthen disclosures and then the 2005 JJ Irani Committee, to look at CG in the context of

the proposed revision to the Companies Act, 1956. The recommendations broadened the remit of what was

included in governance eg. risk management, related party transactions and deepened our understanding of

issues.

Third Generation

The next wave of reforms hit after the Satyam scam in 2009. While industry viewed Satyam as one-off and

cautioned against over-regulation, a series of regulatory changes, including the appointment of a qualified

CFO, timelines on disclosures and rotation of auditor (albeit voluntary) were brought in.

Satyam was important because it highlighted the primacy of good governance practices. Till the scam

happened governance had remained an amorphous idea. Satyam quantified the cost of its failure.

Fourth generation

The fourth generation of CG are driven by two specific themes: The first is the emphatic use of regulation to

enforce governance practices; the other is in empowering different stakeholders to assert their rights.

The Companies Act 2013, implemented in 2014 has completely modernized corporate law in India. It is far

more current that half-a-century-old predecessor and focuses very strongly on the corporate governance

agenda and in aligning these to the G20-OECD guidelines.

Some of what has been incorporated includes:

• Roles and responsibilities of the board

• Definition of an independent director

• Granular disclosures regarding CEO compensation

• Mandatory auditor rotation

• Tenure of independent directors

• E-voting

• Approval of related party transactions by the audit committee, and of majority of minority

shareholders under specified situations

• 2% of profits to be spent on Corporate Social Responsibility (comply or explain)

• One woman director on the board

• Permits class-action suits against the board

• National Financial Reporting Authority

Some of these like a mandatory woman director, and auditor rotation or on CSR spend are generating a global

debate.

This period also saw the listing guidelines being replaced by Listing Obligation and Disclosure Requirements

Regulation 2015 (LODR): The LODR is the consolidation of the compliance requirements by every listed entity

into one single document across various types of securities listed on a stock exchange. While many of the

requirements are aligned with the Companies Act 2013, there are several provisions that are more stringent.

The SEBI Committee on Corporate Governance, chaired by Uday Kotak, also examined CG Practices. Its

recommendations were aimed at achieving the dual objective of shareholder protection and long-term value

creation. The proposals covered a diverse set of items and push corporates towards improving board

effectiveness, enhancing oversight over group entities, tightening control over related party transactions,

providing timely disclosures, increasing focus on audit quality, and facilitating investor participation. The

proposed recommendations were grounded in market realities, and benchmark governance practices with

local and global practices.

Stepping back and looking at the arc of regulatory changes, three elements stand out. One, initially regulators

viewed CG as something you cannot regulate and have usually prescribing best practices. Companies pushed

back citing the letter, and not spirit of then law. It is only then that CG practices have had to be codified. Two,

regulations have increasingly come rely on disclosure as an enforcement tool: publicly disseminating

information will create comparability, thereby fostering an environment of competitive behavior that serves

shareholders and the corporate governance agenda. In addition, they propagate robust internal controls to

provide stronger oversight over on reign in the promoters. Three, there is a shift in thinking about how better

governance will be achieved. In the first blush regulations dealt with the rights and responsibilities of

companies. Today the focus is on the rights of stakeholders, as witnessed by the adopting of Stewardship

Codes by institutional investors.

In telecom, we are now gearing up to a transition to 5G. In a parallel move, I expect focus to shift to ESG –

environment, social and governance. This will be the next upgrade for regulators, investors and companies.

*Views are personal. Neither APAS nor any of its employees endorse any view, product or services mentioned in the article

US-China

On May 10, the US raised tariffs from 10% to 25% on USD 200 billion worth of imports from China and is

threatening tariffs on an additional USD 325 billion worth of Chinese goods. China retaliated by promising to

raise tariffs further on USD 60 billion in US exports.

Renewed talks of escalating tariffs and trade tensions between the US and China unnerved markets in India.

Indian benchmarks ended down for the ninth consecutive session on Monday, May 13, 2019. On the same

day, the rupee slipped to an over-two-month-low as foreign funds extended their share sale. With the latest

string of losses, the Sensex has equalled its nine-session losing streak in February this year. Nifty equalled its

2011 losing streak with this fall.

However, India was not alone in this fall. Global stock markets have tumbled after the US threat to impose

new tariffs on Chinese exports. As on May 13, the month-to-date change in the various indices was: China

Shcomp (-5.67%), India Sensex (-4.97%), Japan Nikkei (-4.8%), South Korea Kospi (-5.65%), Singapore STI (-

4.88%) and Hong Kong HSI (-3.87%).

The impact on US producers with significant exposure to Chinese markets was also captured in stock market

valuations. The equity price performance of US companies with high sales to China underperformed relative

to the US businesses exposed to other international markets, after retaliatory tariffs by China were

implemented.

There could be implications for the world at large. With Chinese goods being taxed at a higher rate in the US,

other countries can pitch in and fill the gap. This opens up opportunities for other exporters, including India.

India needs to make use of this opportunity to significantly enhance its exports.

To substantively benefit from this situation, India requires a strategic approach to convert this opportunity

into a major gain. India needs to focus on becoming a new powerhouse as a global hub for exports, with a

major positive impact on competitiveness and job creation. India needs to take its vision of ease of doing

business and Make in India to the next level.

At the same time, China is likely to get more aggressive with exports and the world should watch out for

dumping of goods as it seeks to regain markets. There is also a possibility of China depreciating its currency

Impact of US-China and

US-Iran relations

so as to get a competitive edge, like in 2015. This would have ramifications for other countries as China has

enough power to move the currencies.

Meanwhile, US government also intends to terminate India’s designation as a beneficiary developing country

under the Generalised System of Preference (GSP) programme. However, a group of 25 influential American

lawmakers has urged the US Trade Representative not to terminate the GSP programme with India, saying

the country’s companies seeking to expand their exports to India could be affected. The final decision of the

US remains to be seen.

Overall, the repercussions can be – more volatility in both commodity prices and currencies as the trade war

escalates. Global trade would get more volatile and also affect investment flows.

US-Iran

In another development from the US, on May 2, the Trump administration brought to an end the waiver the

US had granted to 8 countries, including India, of sanctions on imports of oil from Iran.

Even with the waivers, sanctions had significantly reduced global oil supply. According to the International

Energy Agency, Iran’s oil exports had fallen to 1.1 million barrels per day in March 2019, as compared with 2.3

million barrels in June 2018, just after the US sanctions were announced.

That shortfall worsened an oil supply situation that was already affected by a host of other factors. One was

the political standoff in Venezuela, which drastically reduced production in and exports from there. Another

factor was Saudi Arabia, which decided to join other OPEC nations and enter into an alliance with Russia and

10 other non-OPEC countries to cut production and hold back from the market more than half a million barrels

of crude every day. In little more than a year, the spot price of Brent crude rose from around USD 45 a barrel

to around USD 85 a barrel.

The removal of Iranian oil from India’s energy sourcing basket may have major implications, given that India

has been a major importer of Iranian oil. India imported 23.5 million tonnes in 2018-19 from Iran. India would

need to come up with options that offer terms as attractive as those offered by Iran, including 60-day credit,

free insurance and shipping. Finding an alternative supplier at competitive terms quickly for India may be

tough.

While Saudi Arabia, UAE and other OPEC countries would likely fill the gap created by lower Iranian exports,

it would come at the cost of a significant reduction in the spare capacity and also increase the risks of a

potential conflict in the Middle East.

Oil prices are expected to rise in the foreseeable future. That is not likely to be good news for the government

that is taking control now. The price of India’s crude import basket, which was in decline, has been rising since

the end of last year.

While consumption of crude and petroleum products in India has been continually rising, touching 212 billion

tonnes in 2018-19, the share of net imports in consumption has hovered around 93% for the last 4 years.

So, the trade and current account deficits on India’s balance of payments are expected to widen, creating

uncertainty among foreign investors even when the political landscape cleared. There is also the possibility of

higher inflation, as the effects of higher oil prices pass through.

As mentioned earlier, the threat of the US-China trade war can be converted into an opportunity by India to

increase its exports. Increasing exports would bring in more foreign exchange for India. This foreign exchange

could then be used by India to purchase oil from alternative sources.

-APAS

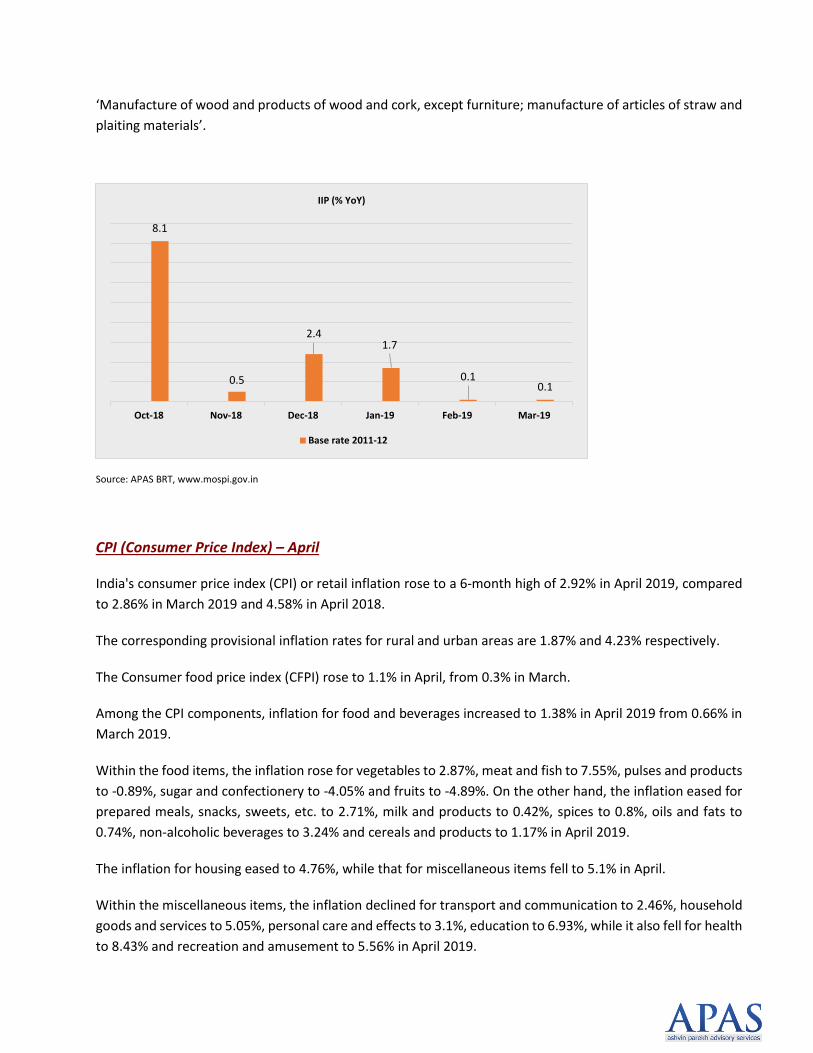

IIP (Index of Industrial Production) – March

Index of Industrial Production (IIP) or factory output for the month of March 2019 slowed to a 21-month low

of 0.1%, compared to 0.1% in February 2019 and 5.3% in March 2018.

The General Index for the month of March 2019 stands at 140.2, which is 0.1% lower as compared to that in

March 2018.

The growth slowed, mainly due to a slowdown in consumption and investment.

The cumulative growth for the period April-March 2018-19 over the corresponding period of last year stood

at 3.6%, as against 4.4% last year.

As per Use-based classification, the growth rates in March 2019 over March 2018 are 2.5% in primary goods,

(-) 8.7% in capital goods, (-) 2.5% in intermediate goods and 6.4% in infrastructure/construction goods.

Consumer durables and non-durables have recorded growth rates of (-) 5.1% and 0.3% respectively.

The manufacturing sector, which constitutes 77.63% of the index, contracted by 0.4% in March, compared to

5.7% growth last year.

Electricity generation grew by 2.2% in March, compared to 5.9% last year.

Mining sector output grew 0.8% in March, compared to 3.1% last year.

In terms of industries, 12 out of 23 industry groups in the manufacturing sector have shown decline in March

2019 from March 2018.

The industry group ‘Manufacture of furniture’ has declined most by 24.6%, followed by 18.5% in ‘Manufacture

of other transport equipment’ and 15.3% in ‘Manufacture of fabricated metal products, except machinery and

equipment’.

On the other hand, the industry group ‘Manufacture of tobacco products’ has shown the highest growth of

13.5%, followed by 10.6% in ‘Manufacture of computer, electronic and optical products’ and 9.3% in

ECONOMY

‘Manufacture of wood and products of wood and cork, except furniture; manufacture of articles of straw and

plaiting materials’.

Source: APAS BRT, www.mospi.gov.in

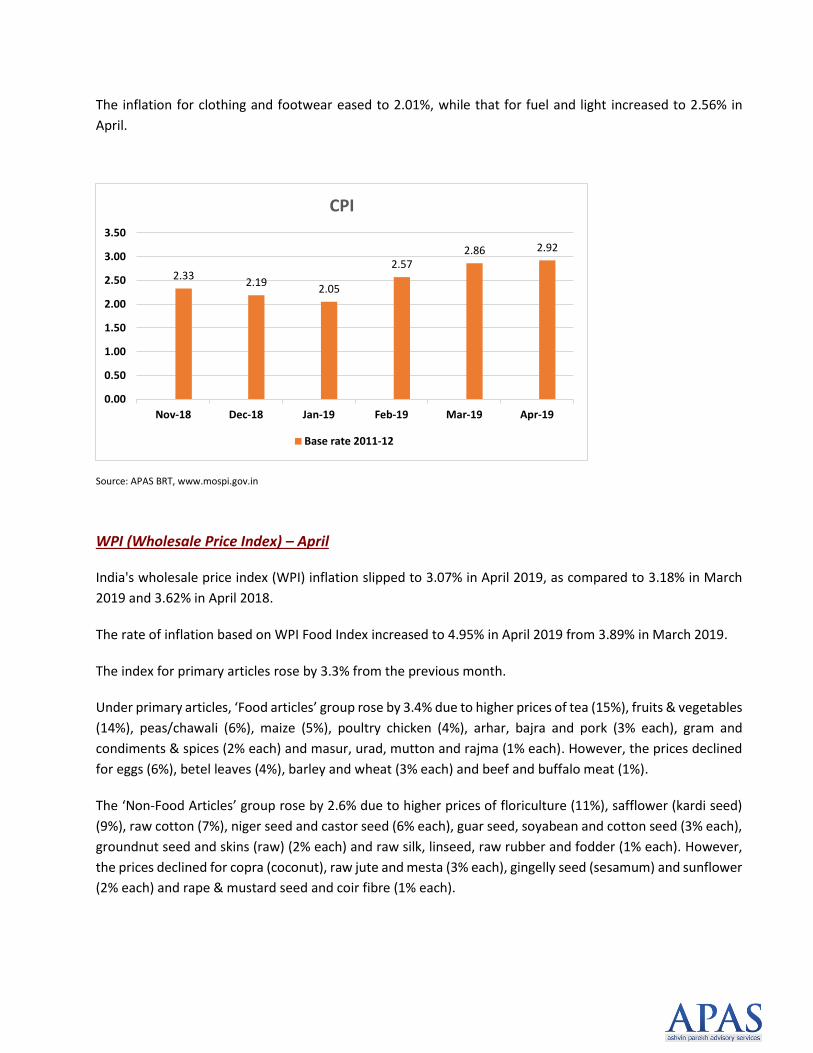

CPI (Consumer Price Index) – April

India's consumer price index (CPI) or retail inflation rose to a 6-month high of 2.92% in April 2019, compared

to 2.86% in March 2019 and 4.58% in April 2018.

The corresponding provisional inflation rates for rural and urban areas are 1.87% and 4.23% respectively.

The Consumer food price index (CFPI) rose to 1.1% in April, from 0.3% in March.

Among the CPI components, inflation for food and beverages increased to 1.38% in April 2019 from 0.66% in

March 2019.

Within the food items, the inflation rose for vegetables to 2.87%, meat and fish to 7.55%, pulses and products

to -0.89%, sugar and confectionery to -4.05% and fruits to -4.89%. On the other hand, the inflation eased for

prepared meals, snacks, sweets, etc. to 2.71%, milk and products to 0.42%, spices to 0.8%, oils and fats to

0.74%, non-alcoholic beverages to 3.24% and cereals and products to 1.17% in April 2019.

The inflation for housing eased to 4.76%, while that for miscellaneous items fell to 5.1% in April.

Within the miscellaneous items, the inflation declined for transport and communication to 2.46%, household

goods and services to 5.05%, personal care and effects to 3.1%, education to 6.93%, while it also fell for health

to 8.43% and recreation and amusement to 5.56% in April 2019.

8.1

0.5

2.41.7

0.10.1

Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19

IIP (% YoY)

Base rate 2011-12

The inflation for clothing and footwear eased to 2.01%, while that for fuel and light increased to 2.56% in

April.

Source: APAS BRT, www.mospi.gov.in

WPI (Wholesale Price Index) – April

India's wholesale price index (WPI) inflation slipped to 3.07% in April 2019, as compared to 3.18% in March

2019 and 3.62% in April 2018.

The rate of inflation based on WPI Food Index increased to 4.95% in April 2019 from 3.89% in March 2019.

The index for primary articles rose by 3.3% from the previous month.

Under primary articles, ‘Food articles’ group rose by 3.4% due to higher prices of tea (15%), fruits & vegetables

(14%), peas/chawali (6%), maize (5%), poultry chicken (4%), arhar, bajra and pork (3% each), gram and

condiments & spices (2% each) and masur, urad, mutton and rajma (1% each). However, the prices declined

for eggs (6%), betel leaves (4%), barley and wheat (3% each) and beef and buffalo meat (1%).

The ‘Non-Food Articles’ group rose by 2.6% due to higher prices of floriculture (11%), safflower (kardi seed)

(9%), raw cotton (7%), niger seed and castor seed (6% each), guar seed, soyabean and cotton seed (3% each),

groundnut seed and skins (raw) (2% each) and raw silk, linseed, raw rubber and fodder (1% each). However,

the prices declined for copra (coconut), raw jute and mesta (3% each), gingelly seed (sesamum) and sunflower

(2% each) and rape & mustard seed and coir fibre (1% each).

2.332.19

2.05

2.572.86 2.92

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19

CPI

Base rate 2011-12

‘Minerals’ group rose by 5.3% due to higher prices of sillimanite (27%), copper concentrate (16%) and

chromite (3%). However, the prices declined for iron ore and lead concentrate (5% each), garnet and

manganese ore (3% each) and limestone (1%).

‘Crude petroleum and natural gas’ group rose by 2.4% due to higher prices of natural gas (6%) and crude

petroleum (1%).

The index for fuel and power declined by 0.5% from the previous month.

Under fuel and power, ‘Mineral oils’ group rose by 0.4% due to higher prices of LPG (5%), naphtha (3%), petrol

and kerosene (2% each) and ATF (1%). However, the prices declined for petroleum coke (3%), furnace oil (2%)

and HSD (1%).

The index for manufactured products remained unchanged from the previous month.

Source: APAS BRT, www.eaindustry.nic.in

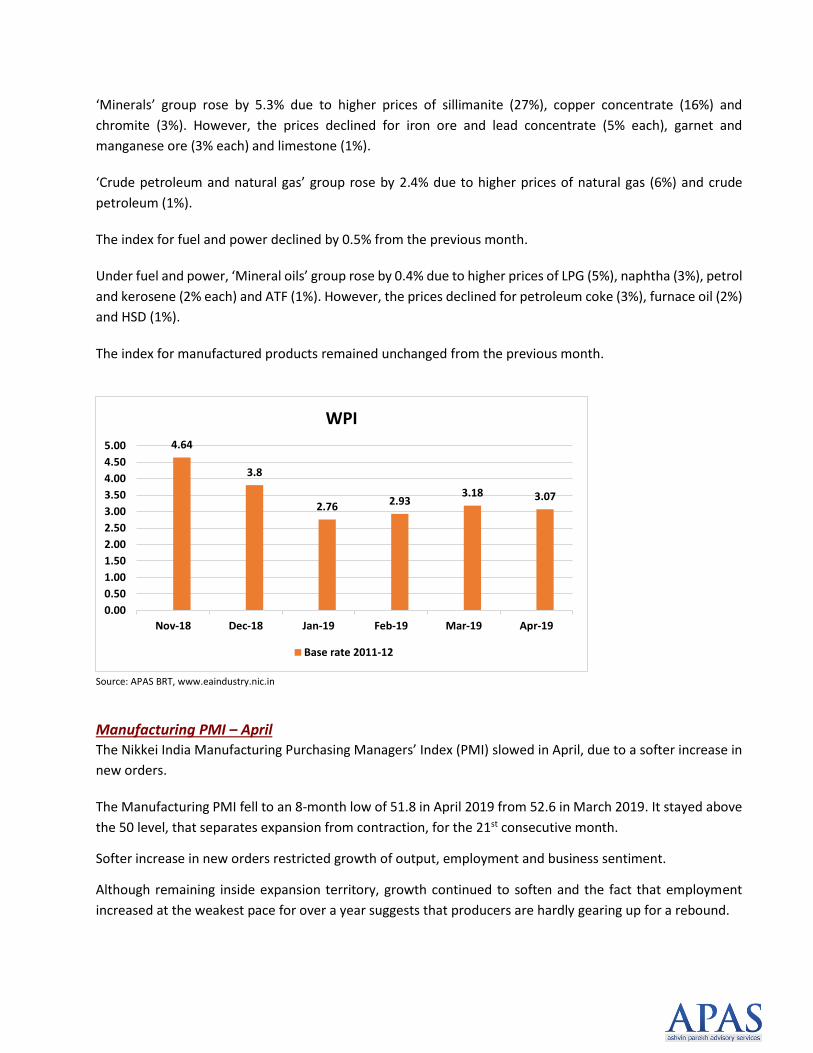

Manufacturing PMI – April The Nikkei India Manufacturing Purchasing Managers’ Index (PMI) slowed in April, due to a softer increase in

new orders.

The Manufacturing PMI fell to an 8-month low of 51.8 in April 2019 from 52.6 in March 2019. It stayed above

the 50 level, that separates expansion from contraction, for the 21st consecutive month.

Softer increase in new orders restricted growth of output, employment and business sentiment.

Although remaining inside expansion territory, growth continued to soften and the fact that employment

increased at the weakest pace for over a year suggests that producers are hardly gearing up for a rebound.

4.64

3.8

2.76 2.933.18 3.07

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19

WPI

Base rate 2011-12

On the prices front, input cost inflation eased to a 43-month low, while the rate of charge inflation was

marginal and below its long-run average.

The one bright spot in April was exports, which expanded solidly and at a slightly quicker pace than in March.

Source: www.tradingeconomics.com

Services PMI – April

The Indian services sector activity eased in April, with rates of new business and output growth, both cooling

to 7-month lows.

The Nikkei India Services Purchasing Managers’ Index (PMI) Business Activity Index fell to a 7-month low of 51

in April 2019 from 52 in March 2019. The index remained above the neutral mark of 50, which separates

expansion from contraction, for the eleventh month in a row.

The moderation was partially due to slower increases in output and new business orders, with both growth

rates falling back to lows last seen in September and weighed on by uncertainty leading up to the general

elections.

Meanwhile, export sales increased the most in 10 months and employment growth accelerated.

At the same time, firms continued to report greater levels of unfinished business as clients delayed payments.

On the price front, rates of inflation for input costs and output charges remained weak by historical standards.

Input price inflation moderated to the second slowest rate in almost 2 years and output inflation remained

subdued.

Looking ahead, sentiment strengthened, supported by marketing initiatives, the upcoming launch of low-cost

services and efforts to expand capacity. In terms of the next 12 months, business confidence among service

providers rose in April to the highest in 7 months, supported by predictions that economic conditions will

improve after the elections.

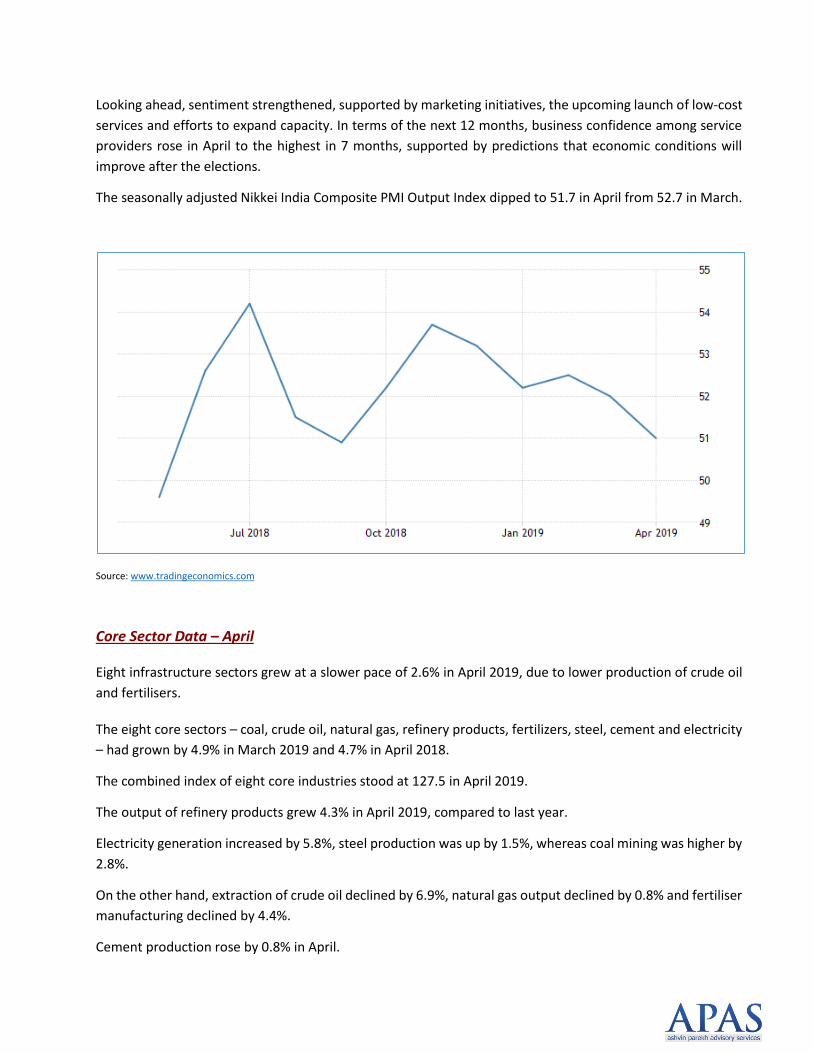

The seasonally adjusted Nikkei India Composite PMI Output Index dipped to 51.7 in April from 52.7 in March.

Source: www.tradingeconomics.com

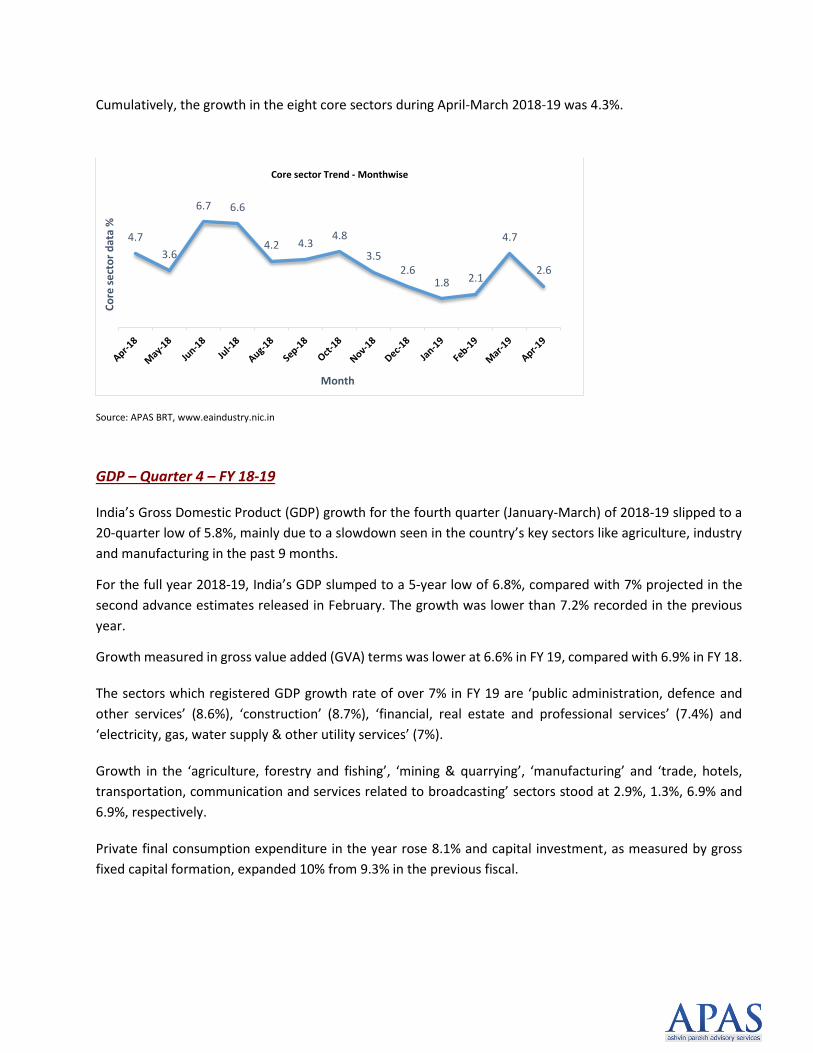

Core Sector Data – April

Eight infrastructure sectors grew at a slower pace of 2.6% in April 2019, due to lower production of crude oil

and fertilisers.

The eight core sectors – coal, crude oil, natural gas, refinery products, fertilizers, steel, cement and electricity

– had grown by 4.9% in March 2019 and 4.7% in April 2018.

The combined index of eight core industries stood at 127.5 in April 2019.

The output of refinery products grew 4.3% in April 2019, compared to last year.

Electricity generation increased by 5.8%, steel production was up by 1.5%, whereas coal mining was higher by

2.8%.

On the other hand, extraction of crude oil declined by 6.9%, natural gas output declined by 0.8% and fertiliser

manufacturing declined by 4.4%.

Cement production rose by 0.8% in April.

Cumulatively, the growth in the eight core sectors during April-March 2018-19 was 4.3%.

Source: APAS BRT, www.eaindustry.nic.in

GDP – Quarter 4 – FY 18-19

India’s Gross Domestic Product (GDP) growth for the fourth quarter (January-March) of 2018-19 slipped to a

20-quarter low of 5.8%, mainly due to a slowdown seen in the country’s key sectors like agriculture, industry

and manufacturing in the past 9 months.

For the full year 2018-19, India’s GDP slumped to a 5-year low of 6.8%, compared with 7% projected in the

second advance estimates released in February. The growth was lower than 7.2% recorded in the previous

year.

Growth measured in gross value added (GVA) terms was lower at 6.6% in FY 19, compared with 6.9% in FY 18.

The sectors which registered GDP growth rate of over 7% in FY 19 are ‘public administration, defence and

other services’ (8.6%), ‘construction’ (8.7%), ‘financial, real estate and professional services’ (7.4%) and

‘electricity, gas, water supply & other utility services’ (7%).

Growth in the ‘agriculture, forestry and fishing’, ‘mining & quarrying’, ‘manufacturing’ and ‘trade, hotels,

transportation, communication and services related to broadcasting’ sectors stood at 2.9%, 1.3%, 6.9% and

6.9%, respectively.

Private final consumption expenditure in the year rose 8.1% and capital investment, as measured by gross

fixed capital formation, expanded 10% from 9.3% in the previous fiscal.

4.7

3.6

6.7 6.6

4.2 4.34.8

3.52.6

1.8 2.1

4.7

2.6

Co

re s

ect

or

dat

a %

Month

Core sector Trend - Monthwise

Source: APAS BRT, www.mospi.gov.in

6.1 5.76.3

7.27.7

8.27.1

6.65.8

Q4 16-17 Q1 17-18 Q2 17-18 Q3 17-18 Q4 17-18 Q1 18-19 Q2 18-19 Q3 18-19 Q4 18-19

GD

P %

Quarter

GDP Trend

Second Bi-monthly Monetary Policy Statement, 2019-20 Resolution of the Monetary Policy

Committee (MPC), Reserve Bank of India

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy

Committee (MPC) at its meeting decided to:

• Reduce the policy repo rate under the liquidity adjustment facility (LAF) by 25 basis points to 5.75 per cent

from 6.0 per cent with immediate effect.

Consequently, the reverse repo rate under the LAF stands adjusted to 5.50 per cent, and the marginal standing

facility (MSF) rate and the Bank Rate to 6.0 per cent. The MPC also decided to change the stance of monetary

policy from neutral to accommodative. These decisions are in consonance with the objective of achieving the

medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent,

while supporting growth. The main considerations underlying the decision are set out in the statement below.

Assessment:

Global Economy

Global economic activity has been losing pace after a somewhat improved performance in Q1:2019, reflecting

further slowdown in trade and manufacturing activity. Leading indicators point to a further slowdown in the

Euro area in Q2. In the UK, GDP growth for Q1 picked up on high retail sales and government expenditure.

However, the outlook is clouded by uncertainty relating to Brexit.

Economic activity has slowed in many emerging market economies (EMEs). In Q1:2019, the Chinese economy

grew at the same pace as in the previous quarter, though slightly above consensus expectations. However,

incoming data on industrial production and retail sales suggest that the growth momentum may weaken in

Q2.

Crude oil prices remained volatile, reflecting evolving demand-supply conditions underpinned by the

production stance of the OPEC plus, rising shale output, weakening global demand and geopolitical concerns.

The strengthening of the US dollar had weakened gold prices; however, prices picked up since the last week

of May on escalating trade tensions, reviving its demand as a safe haven asset. Inflation remains below target

in several economies, though it has shown an uptick since March. In many EMEs, bond yields have been falling

with central banks adopting accommodative monetary policy to boost economic growth.

BANKING

Domestic Economy

Moving beyond Q4, the India Meteorological Department (IMD) has predicted that south-west monsoon

rainfall (June to September) is likely to be normal at 96 per cent of the long period average (LPA). The current

weak El Niño conditions over the Pacific are likely to continue during the monsoon. However, currently

prevailing neutral Indian Ocean Dipole (IOD) conditions may turn positive in the middle of the monsoon season

and persist thereafter, which augur well for the rainfall outlook.

Transmission of the cumulative reduction of 50 bps in the policy repo rate in February and April 2019 was 21

bps to the weighted average lending rate (WALR) on fresh rupee loans. However, the WALR on outstanding

rupee loans increased by 4 bps as the past loans continue to be priced at high rates. Interest rates on longer

tenor money market instruments remained broadly aligned with the overnight WACR, reflecting near full

transmission of the reduction in policy rate.

Outlook

In the bi-monthly monetary policy resolution of April 2019, CPI inflation was projected at 2.4 per cent for

Q4:2018-19, 2.9-3.0 per cent for H1:2019-20 and 3.5-3.8 per cent for H2:2019-20, with risks broadly balanced.

The headline inflation outcome in Q4 at 2.5 per cent was largely in alignment with the April policy projections.

RBI notifies the revised Voluntary Retention Route for Investments by Foreign Portfolio Investors

(FPIs) and opens allotment ‘on tap’

Reserve Bank of India introduced the Voluntary Retention Route for Investments by Foreign Portfolio

Investors (FPIs) on March 01, 2019. Limits for investment in debt by Foreign Portfolio Investors (FPIs) were

offered for allotment ‘on tap’ during March 11 – April 30, 2019. Based on the feedback received, and in

consultation with the Government, the Bank has made certain changes in the scheme to increase its

operational flexibility.

The revised VRR scheme shall be open for allotment from May 27, 2019 as per the following details:

1. The investment limit shall be ₹ 54,606.55 crores, under the VRR–Combined category, which allows

investment in both government securities and corporate debt.

2. The minimum retention period shall be three years. During this period, FPIs shall maintain a minimum

of 75% of the allocated amount in India.

3. Investment limits shall be available ‘on tap’ and allotted on ‘first come, first served’ basis.

4. The ‘tap’ shall be kept open till the limit is fully allotted or till December 31, 2019, whichever is earlier.

5. FPIs may apply for investment limits online to Clearing Corporation of India Ltd. (CCIL) through their

respective custodians.

6. CCIL will separately notify the operational details of application and allotment.

7. FPIs that were allotted investment limits under the tap that was open during March 11-April 30, 2019,

may, at their discretion, opt to convert their full allotment to ‘VRR-Combined’ by advising CCIL through

their custodians. Such conversions shall not use up the investment limit of ₹ 54,606.55 crores

indicated above

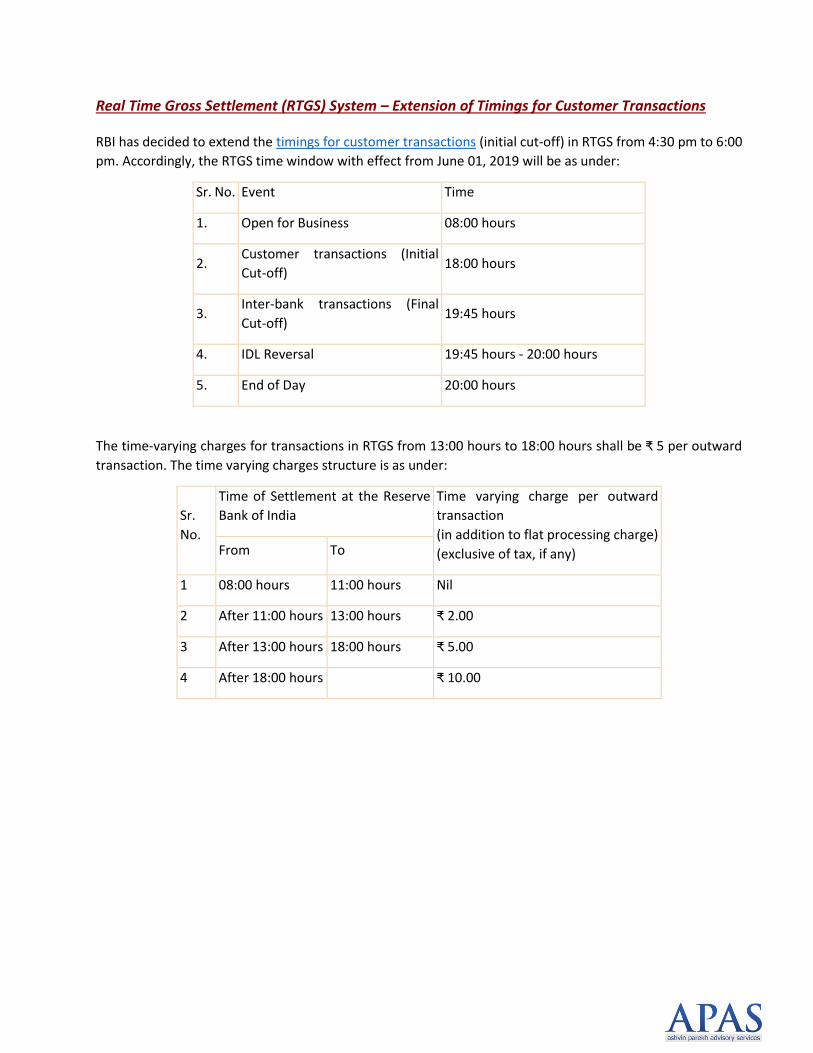

Real Time Gross Settlement (RTGS) System – Extension of Timings for Customer Transactions

RBI has decided to extend the timings for customer transactions (initial cut-off) in RTGS from 4:30 pm to 6:00

pm. Accordingly, the RTGS time window with effect from June 01, 2019 will be as under:

Sr. No. Event Time

1. Open for Business 08:00 hours

2. Customer transactions (Initial

Cut-off) 18:00 hours

3. Inter-bank transactions (Final

Cut-off) 19:45 hours

4. IDL Reversal 19:45 hours - 20:00 hours

5. End of Day 20:00 hours

The time-varying charges for transactions in RTGS from 13:00 hours to 18:00 hours shall be ₹ 5 per outward

transaction. The time varying charges structure is as under:

Sr.

No.

Time of Settlement at the Reserve

Bank of India

Time varying charge per outward

transaction

(in addition to flat processing charge)

(exclusive of tax, if any) From To

1 08:00 hours 11:00 hours Nil

2 After 11:00 hours 13:00 hours ₹ 2.00

3 After 13:00 hours 18:00 hours ₹ 5.00

4 After 18:00 hours ₹ 10.00

Reconciliation of Co-Insurers Balance from ETASS

General Insurance Council has been implementing ETASS (Electronic Transaction Administration and

Settlement System) for capturing of Co-insurance transactions, reconciliation and settlement of balances

between member insurance companies. The system has been in operation from April 2017 for all lines of

Business and GI Council agreed that from 1st April 2018, the system would be treated as live and all co-

insurance transactions will be settled between member insurers only on the basis of ETASS statement.

The Authority had noticed that the inter-company balances in re-insurance and co-insurance business are

significantly high and are on the rise. The re-insurance and co-insurance transactions typically involve multiple

organizations across various geographies giving rise to following issues:

1. Inability of parties to the transactions to agree, resulting in growing inter-company balances;

2. Lack of cooperation between the companies and inadequate documentation, posing a problem towards

the efforts to minimize these balances;

3. Lack of a common platform to handle the re-insurance and co-insurance transactions;

4. Delayed settlement of balances;

5. High turnaround times.

In this regard, IRDAI has directed that:

I. For all the co-insurance transactions that took place after 1st April 2018, the balances due to/from

co-insurers shall be reconciled with the balances as per ETASS;

II. A certificate from the statutory auditor shall be submitted to the Authority, in the format as

prescribed in Annexure A(Enclosed below), along with the annual financial statements certifying that there is

no difference in books of accounts and ETASS with regard to co-insurance transactions that relate to policies

with a risk start date on or after 1st April 2018;

III. In case of differences, the co-insurer wise differences shall be reported in the Auditor’s certificate;

IV. Balances for the transactions that took place before 1st April 2018 shall be reconciled by the insurer

and the same shall be submitted to the Authority on or before 30th September 2019 without fail.

INSURANCE

Preparation of Financial Statements for FY 2019-20 and Onwards

In order to bring uniformity, comparability and fair presentation of Financial Statements filed by the insurers,

the Authority, has issued the following directions:

1. Presentation of Excess Expenses of Management (EoM) in Operating Expenses:

The Authority vide Insurance Regulatory and Development Authority of India (Expenses of Management of

Insurers transacting General or Health Insurance business) Regulations, 2016 have prescribed the limits of

expenses of management. In case expenses of management exceed the limits prescribed by the Regulations,

the excess is required to be charged to Shareholders Account i.e. Profit and Loss Account.

It is observed that some insurers are disclosing the operating expenses net of excess EoM charged to

shareholders account, in Revenue Account. This leads to distorted picture of the Underwriting Results of the

Insurers. In light of the same, all Insurers are advised to present the excess of EoM in Financial Statements, as

under:

I. Report the gross amount of Operating expenses in Schedule-4 and Revenue Account without

deducting ‘Excess of allowable expenses’;

II. Report excess of allowable expenses as income under Revenue account under separate sub line item

as “Contribution from Shareholders Funds towards Excess EoM” in the line item “Others”;

III. Report excess of allowable expenses as expenses under Profit & Loss account under separate sub line

item, “Contribution to policyholders Funds towards Excess EoM” in line item “Other Expenses”;

2. Personal Accident Policies in Health Segment

In terms of Section 2(6C) of the Insurance Act, 1938, Personal Accident and Travel (Including domestic as well

as overseas) are part of Health Insurance.

2.1 In order to have uniformity in case of business from Personal Accident and Travel, it is hereby specified

that in Financial Statements:

I. Personal Accident shall continue to be shown as a separate sub-segment within “Miscellaneous

segment”;

II. As the Insurance Regulatory and Development Authority (Preparation of Financial Statements and

Auditor’s Report of Insurance Companies) Regulations, 2002 do not provide a separate segment/sub segment

for Travel (including domestic as well as overseas) insurance, it shall be clubbed with “Health Segment”;

2.2 For computation of Expenses of Management, Personal Accident and Travel shall be clubbed with Health

Segment.

3. Deviation from Formats prescribed:

It is observed that some insurers have modified the formats as prescribed by the by IRDA (Preparation of

Financial Statements and Auditor’s Report of Insurance Companies) Regulations, 2002 by way of

addition/deletion of line items.

All insurers are advised to strictly adhere to the formats prescribed by the Regulations. Any new line item, if

so warranted to be disclosed separately, may be shown under “Others” in Revenue Account, P&L Account

and/or relevant schedule of the financial statements by giving the break-up.

4. Creation of UPR and Outstanding Claims Reserve (Including IBNR/IBNER) for Premium Ceded under Clean-

cut Reinsurance Treaties

It is observed that some insurers enter into one-year Quota Share Reinsurance Treaty on Clean-cut basis. The

provision towards the unexpired premium reserve / IBNR / IBNER, on such treaties, is neither provided by

Direct insurer (cedant) nor by the reinsurer(s).

It is hereby advised that Direct insurers (cedant) shall create the adequate reserves, as follows, in accordance

with the IRDAI (Assets, Liabilities and Solvency Margin of General Insurance Business) Regulations, 2016:

I. Unearned Premium Reserve and Premium Deficiency Reserve towards the unexpired risk at the end

of the treaty period; and

II. Outstanding Claims Reserve (including IBNR/IBNER) towards the outstanding claims on the date of

expiry of the treaty.

5. Rewards and Remuneration to Agents/Brokers/Other intermediaries

In order to bring the consistency, uniformity and fair presentation, it is hereby advised that rewards and/or

remuneration to agents, brokers or other intermediaries shall be shown as part of Commission.

6. Segregation of Policyholders’ and Shareholders’ Funds

The Authority has issued to Circular IRDA/F&A/CIR/CPM/010/01/2017 dated 12th January 2017 which

mandates the insurers to segregate Policyholders’ Funds and Shareholders’ Funds. The provisions of the

Circular, which was hitherto applicable till 31stMarch 2018, are now extended for FY2018-19 and onwards, till

further orders. All other provisions of the above referred Circular shall continue to be applicable.

7. Corporate Social Responsibility Expenditure

In order to bring the consistency, uniformity and fair presentation, it is hereby advised that expenditure

towards Corporate Social Responsibility shall be shown in Profit and Loss Account.

PM-KISAN Scheme extension to include all eligible farmer families irrespective of the size of land

holdings

The Union Cabinet, chaired by the Prime Minister Narendra Modi, has approved that the ambit of the Pradhan

Mantri Kisan Samman Nidhi (PM-KISAN) would be comprehensively extended. With this decision, all land

holding eligible farmer families (subject to the prevalent exclusion criteria) would avail of the benefits under

this scheme.

More beneficiaries, greater progress:

The revised Scheme is expected to cover around 2 crore more farmers, increasing the coverage of PM-KISAN

to around 14.5 crore beneficiaries, with an estimated expenditure by Central Government of Rs. 87,217.50

crores for year 2019-20.

Speed, scale and a major promise delivered:

Today’s Cabinet decision pertaining to expanding the ambit PM-KISAN marks the fulfilment of a major promise

made by the Prime Minister to the people of India in the run-up to the 2019 Parliamentary elections. The BJP

manifesto too mentioned this major policy decision.

It may also be noted that certain operational issues like lack of updated land records in Jharkhand and lack of

Aadhaar penetration in states of Assam, Meghalaya and J&K have also been resolved.

PM-KISAN: A path-breaking support incentive for farmers:

The genesis of the PM-KISAN Yojana dates back to the interim Budget for the year 2019-2020.

The key element of PM-KISAN is income support of Rs. 6000/- to the small and marginal landholder farmer

families with cultivable land holding upto 2 hectare across the country. (This has been expanded today)

The amount is being released in three 4-monthly instalments of Rs.2000/- each over the year, to be credited

into the bank accounts of the beneficiaries held in destination banks through Direct Benefit Transfer mode.

The scheme was launched in a record time of 3 weeks, on 24th February at a huge programme in Gorakhpur,

Uttar Pradesh where the first rounds of instalments was paid to several farmers.

INFRASTRUCTURE &

OTHER GOVT.

INITIATIVES

So far, 1st instalment to 3.11 crore beneficiaries and 2nd instalment to 2.66 crore beneficiaries have been

credited directly to the bank accounts of the farmer families.

Serving India’s Annadatas with renewed vigour:

Time and again, PM Narendra Modi has spoken with great reverence for India’s farmers. He has described

India’s farmers as our Annadatas who undertake great efforts to feed 1.3 billion Indians.

Between 2014 to 2019, numerous measures were taken to empower the hardworking farmer. This includes

increase in the Minimum Support Prices (MSP) for 22 crops, Soil Health Cards, PM Krishi Sinchai Yojana, PM

Kisan Sampada Yojana, e-NAM for better markets and more. These steps have made agriculture more

prosperous and ensured greater productivity for farmers. They will go a long way in fulfilling the Prime

Minister’s dream of doubling farmer incomes by 2022, when India marks 75 years of freedom.

Pension scheme to secure lives of 5 crore farmers in three years

The Union Cabinet, chaired by the Prime Minister Narendra Modi, has approved new Central Sector Scheme,

a historic decision that will empower farmers across India. This is a path breaking scheme that will provide

pension cover to our industrious farmers who toil day and night to keep our nation fed. It is also for the first

time since independence that such a pension coverage has been envisioned for farmers.

It is estimated that 5 crore small and marginal farmers will benefit in the first three years itself. The Central

Government would spend Rs. 10774.50 crore for a period of 3 years towards its contribution (matching share)

for providing social security cover as envisaged under the scheme.

The salient features of this scheme are:

A voluntary and contributory pension scheme for all Small and Marginal Farmers (SMF) across the country.

Entry age of 18 to 40 years with a provision of minimum fixed pension of Rs.3,000/- on attaining the age of 60

years.

For example, a beneficiary farmer is required to contribute Rs 100/ - per month at median entry age of 29

years. The Central Government shall also contribute to the Pension Fund an equal amount as contributed by

the eligible farmer.

After the subscriber’s death, while receiving pension, the spouse of the SMF beneficiary shall be entitled to

receive 50% of the pension received by the beneficiary as family pension, provided he/she is not already an

SMF beneficiary of the Scheme. If, the death of the subscriber happens during the period of contribution, the

spouse shall have the option of continuing the Scheme by paying regular contribution.

Synergy between schemes, prosperity for farmers:

An interesting feature of the Scheme is that the farmers can opt to allow his/her monthly contribution to the

Scheme to be made from the benefits drawn from the Pradhan Mantri Kisan Samman Nidhi (PM-KISAN)

Scheme directly. Alternatively, a farmer can pay his monthly contribution by registering through Common

Service Centres (CSCs) under MeitY.

Participation of Mutual Funds in Commodity Derivatives Market in India

In order to promote institutional participation in Exchange Traded Commodity Derivatives (ETCDs), SEBI has

permitted Category III Alternative Investment Funds to participate in exchange traded commodity derivatives

and also permitted Eligible Foreign Entities (EFE) having actual exposure to Indian commodity markets, to

participate in the commodity derivative segment of recognized stock exchanges for hedging their exposure.

In furtherance to this objective, it has been decided to permit mutual funds to participate in ETCDs.

The participation of mutual funds in ETCDs would be subject to the following:

1. Mutual funds are permitted to participate in ETCDs in India, except in commodity derivatives on

‘Sensitive Commodities’ as defined by SEBI

2. ETCDs having gold as the underlying, shall also be considered as ‘gold related instrument’ for Gold

Exchange Traded Funds (Gold ETFs).

3. No Mutual fund schemes shall invest in physical goods except in ‘gold’ through Gold ETFs. Further, as

mutual fund schemes participating in ETCDs may hold the underlying goods in case of physical

settlement of contracts, in that case mutual funds shall dispose of such goods from the books of the

scheme, at the earliest, not exceeding 30 days from the date of holding of the physical goods.

4. No mutual fund scheme shall have net short positions in ETCDs on any particular good, considering

its positions in physical goods as well as ETCDs, at any point of time

5. Mutual funds are permitted to participate in ETCDs through the following schemes:

a. Hybrid schemes

b. Gold ETFs.

6. All the existing schemes shall comply with provisions of Regulation 18(15A) of SEBI (Mutual Funds)

Regulations, 1996, as this will lead to change in fundamental attributes of the scheme and all

unitholders shall be given a time-period of at least 30 days to exercise the option to exit at prevailing

NAV without charging of exit load, if any.

7. Prior to participation in ETCDs, the AMCs shall adhere to compulsions such as Appointing fund

manager, appointing custodian, drafting investment policy, valuation policy, etc.

The mutual funds shall follow certain investment limits and disclosure as applicable to the fund.

CAPITAL MARKETS

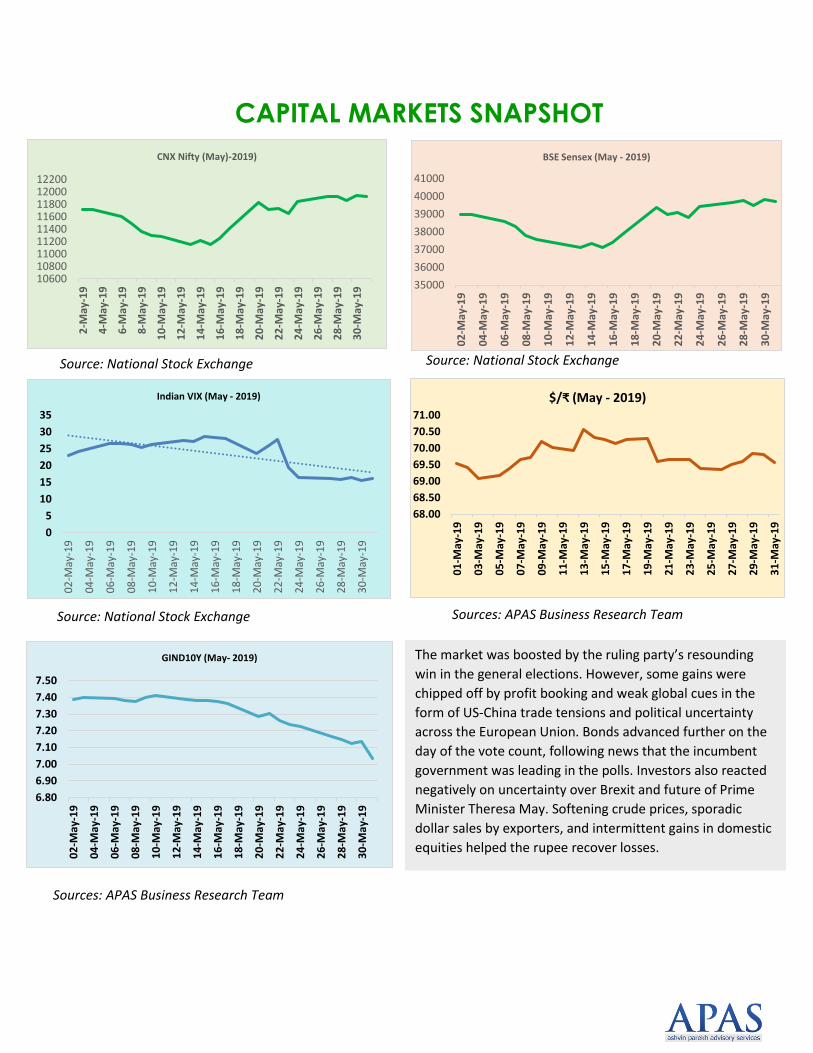

CAPITAL MARKETS SNAPSHOT

Source: National Stock Exchange

Sources: APAS Business Research Team

Source: National Stock Exchange Source: Bombay Stock Exchange

Source: National Stock Exchange Source: National Stock Exchange

Sources: APAS Business Research Team

The market was boosted by the ruling party’s resounding

win in the general elections. However, some gains were

chipped off by profit booking and weak global cues in the

form of US-China trade tensions and political uncertainty

across the European Union. Bonds advanced further on the

day of the vote count, following news that the incumbent

government was leading in the polls. Investors also reacted

negatively on uncertainty over Brexit and future of Prime

Minister Theresa May. Softening crude prices, sporadic

dollar sales by exporters, and intermittent gains in domestic

equities helped the rupee recover losses.

0

5

10

15

20

25

30

35

02

-May

-19

04

-May

-19

06

-May

-19

08

-May

-19

10

-May

-19

12

-May

-19

14

-May

-19

16

-May

-19

18

-May

-19

20

-May

-19

22

-May

-19

24

-May

-19

26

-May

-19

28

-May

-19

30

-May

-19

Indian VIX (May - 2019)

68.00

68.50

69.00

69.50

70.00

70.50

71.00

01

-May

-19

03

-May

-19

05

-May

-19

07

-May

-19

09

-May

-19

11

-May

-19

13

-May

-19

15

-May

-19

17

-May

-19

19

-May

-19

21

-May

-19

23

-May

-19

25

-May

-19

27

-May

-19

29

-May

-19

31

-May

-19

$/₹ (May - 2019)

6.80

6.90

7.00

7.10

7.20

7.30

7.40

7.50

02

-May

-19

04

-May

-19

06

-May

-19

08

-May

-19

10

-May

-19

12

-May

-19

14

-May

-19

16

-May

-19

18

-May

-19

20

-May

-19

22

-May

-19

24

-May

-19

26

-May

-19

28

-May

-19

30

-May

-19

GIND10Y (May- 2019)

106001080011000112001140011600118001200012200

2-M

ay-1

9

4-M

ay-1

9

6-M

ay-1

9

8-M

ay-1

9

10

-May

-19

12

-May

-19

14

-May

-19

16

-May

-19

18

-May

-19

20

-May

-19

22

-May

-19

24

-May

-19

26

-May

-19

28

-May

-19

30

-May

-19

CNX Nifty (May)-2019)

35000

36000

37000

38000

39000

40000

41000

02

-May

-19

04

-May

-19

06

-May

-19

08

-May

-19

10

-May

-19

12

-May

-19

14

-May

-19

16

-May

-19

18

-May

-19

20

-May

-19

22

-May

-19

24

-May

-19

26

-May

-19

28

-May

-19

30

-May

-19

BSE Sensex (May - 2019)

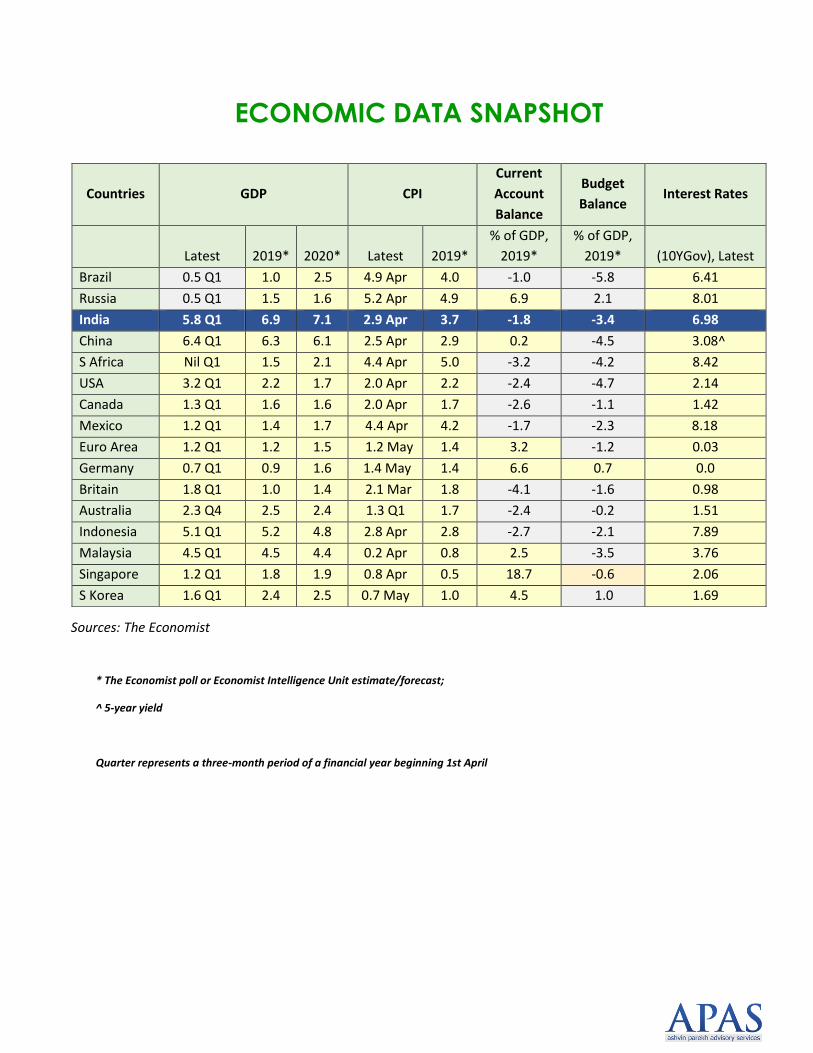

ECONOMIC DATA SNAPSHOT

* The Economist poll or Economist Intelligence Unit estimate/forecast;

^ 5-year yield

Quarter represents a three-month period of a financial year beginning 1st April

Countries GDP CPI

Current

Account

Balance

Budget

Balance Interest Rates

Latest 2019* 2020* Latest 2019*

% of GDP,

2019*

% of GDP,

2019* (10YGov), Latest

Brazil 0.5 Q1 1.0 2.5 4.9 Apr 4.0 -1.0 -5.8 6.41

Russia 0.5 Q1 1.5 1.6 5.2 Apr 4.9 6.9 2.1 8.01

India 5.8 Q1 6.9 7.1 2.9 Apr 3.7 -1.8 -3.4 6.98

China 6.4 Q1 6.3 6.1 2.5 Apr 2.9 0.2 -4.5 3.08^

S Africa Nil Q1 1.5 2.1 4.4 Apr 5.0 -3.2 -4.2 8.42

USA 3.2 Q1 2.2 1.7 2.0 Apr 2.2 -2.4 -4.7 2.14

Canada 1.3 Q1 1.6 1.6 2.0 Apr 1.7 -2.6 -1.1 1.42

Mexico 1.2 Q1 1.4 1.7 4.4 Apr 4.2 -1.7 -2.3 8.18

Euro Area 1.2 Q1 1.2 1.5 1.2 May 1.4 3.2 -1.2 0.03

Germany 0.7 Q1 0.9 1.6 1.4 May 1.4 6.6 0.7 0.0

Britain 1.8 Q1 1.0 1.4 2.1 Mar 1.8 -4.1 -1.6 0.98

Australia 2.3 Q4 2.5 2.4 1.3 Q1 1.7 -2.4 -0.2 1.51

Indonesia 5.1 Q1 5.2 4.8 2.8 Apr 2.8 -2.7 -2.1 7.89

Malaysia 4.5 Q1 4.5 4.4 0.2 Apr 0.8 2.5 -3.5 3.76

Singapore 1.2 Q1 1.8 1.9 0.8 Apr 0.5 18.7 -0.6 2.06

S Korea 1.6 Q1 2.4 2.5 0.7 May 1.0 4.5 1.0 1.69

Sources: The Economist

ABOUT APAS

APAS is a management advisory firm specializing in banking, financial services and the insurance space. APAS

assists business leaders of some of the leading domestic and global organizations, acting as an extended arm

to the management in coping with the ever changing internal and external dynamics. Leveraging deep

business insights APAS develops business and operational strategy for its clients. APAS provides transaction

advisory services (Buy, sell and merge), and also specializes in governance and board training. APAS facilitates

investors and sellers with directional guidelines of pursuing transactions, by utilizing subject knowledge, vast

experience and deep market outreach. APAS has capability to identify and analyze key transaction drivers,

recognize possible partnerships, and initiate discussions with them for possible growth opportunity. We help

major insurance companies, payment institutions, and other financial organizations to identify their growth

potential, innovative opportunity and possible benefits of consolidation, and hence comprehend the possible

merger or acquisition. Buying or selling a major asset or a business, undertaking a merger, or performing an

IPO can be risky and complex especially in this globalization era. Hence, the need of a trusted advisor who can

help clients preserve, create and enhance value in transactions.

Contact Us: 022-6789 1000

www.ap-as.com

Disclaimer – This informative APAS Monthly has been sent only for reader’s reference. Contents have been

prepared on the basis of publicly available information which has not been independently verified by APAS.

Neither APAS, nor any person associated with it, makes any expressed or implied representation or warranty

with respect to the sufficiency, accuracy, completeness or reasonableness of the information set forth in this

note, nor do they owe any duty of care to any recipient of this note in relation to this APAS Monthly. Reader

should not pursue any information provided in the Monthly as an investment advice. Neither APAS nor any

person associated with it are responsible for any loss due to such persuasion.