Chlitina Holding Limited 1 Chlitina Holding Limited Group Introduction.

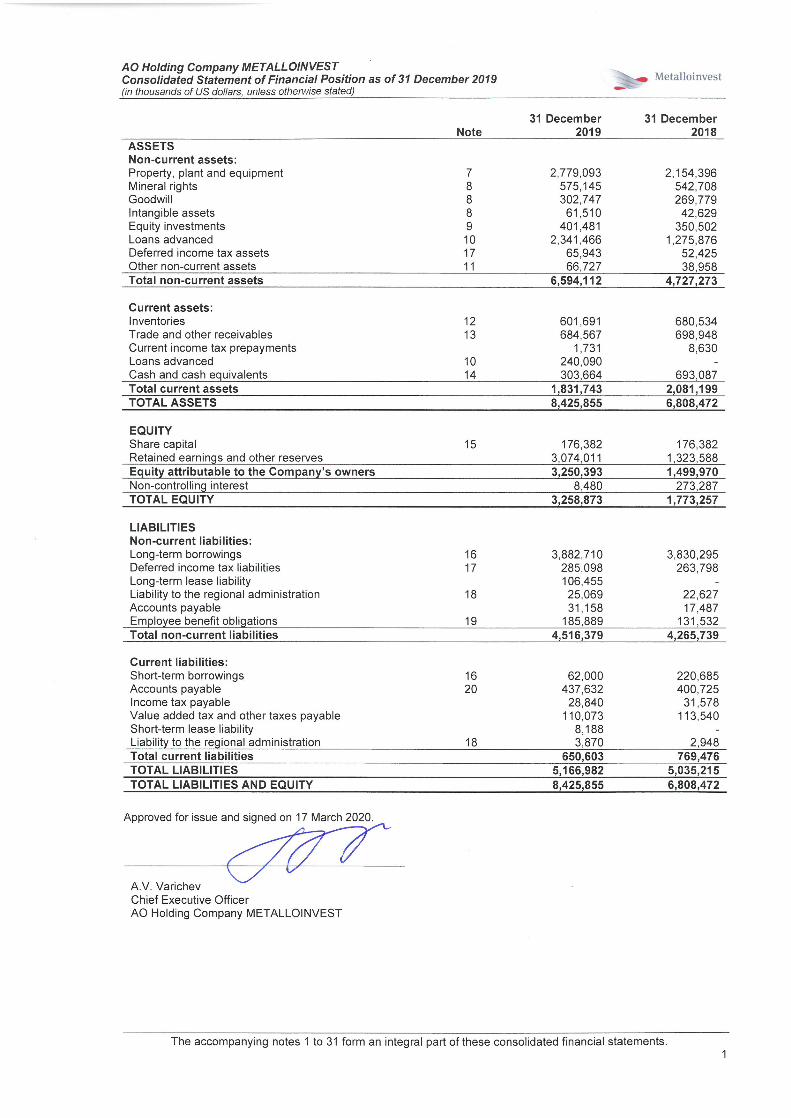

AO Holding Company METALLOINVEST

International Financial Reporting Standards Consolidated Financial Statements and Independent Auditor’s Report

31 December 2019

AO Holding Company METALLOINVEST Consolidated Financial Statements for the year ended 31 December 2019

Contents

INDEPENDENT AUDITOR’S REPORT CONSOLIDATED FINANCIAL STATEMENTS

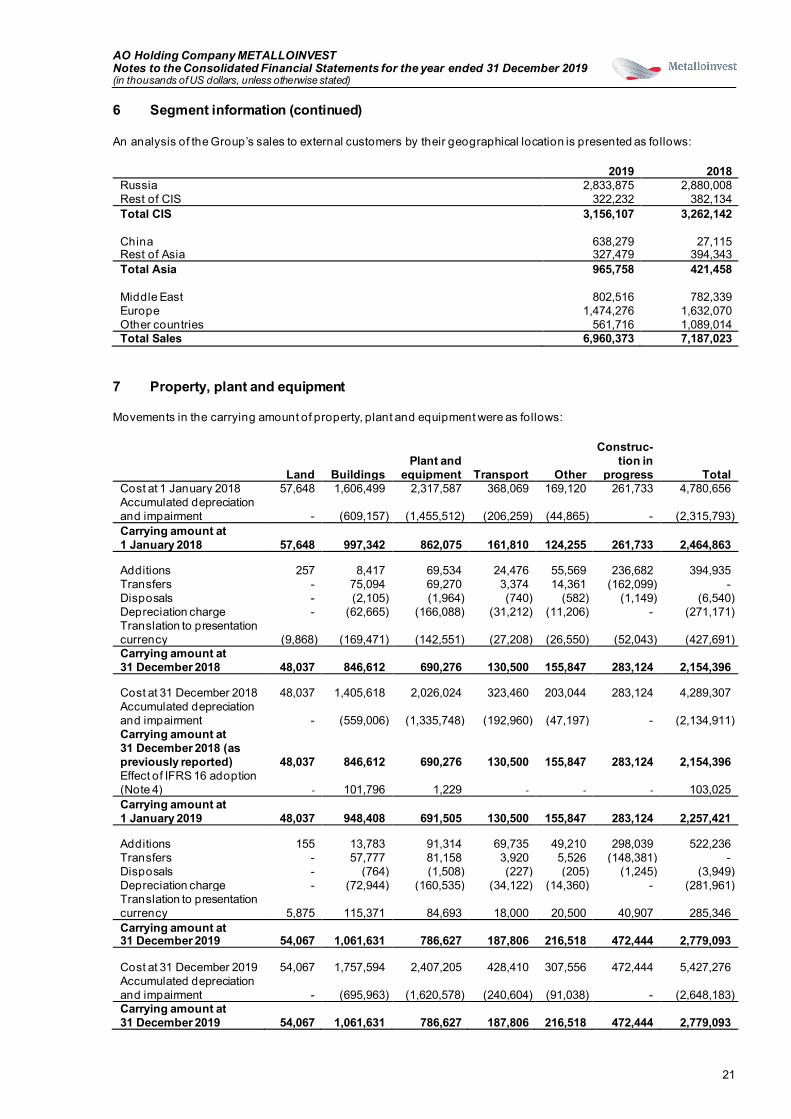

Consolidated Statement of Financial Position......................................................................................................................1 Consolidated Statement of Profit or Loss and Other Comprehensive Income...................................................................2 Consolidated Statement of Cash Flows................................................................................................................................3 Consolidated Statement of Changes in Equity.....................................................................................................................4 Notes to the Consolidated Financial Statements 1 General information....................................................................................................................................................5 2 Basis of preparation and summary of significant accounting policies .....................................................................5 3 Critical accounting estimates and judgements .......................................................................................................15 4 Adoption of new or revised standards and interpretations.....................................................................................17 5 New accounting pronouncements ...........................................................................................................................18 6 Segment information ................................................................................................................................................18 7 Property, plant and equipment ................................................................................................................................21 8 Intangible assets and goodwill.................................................................................................................................22 9 Equity investments ...................................................................................................................................................24 10 Loans advanced .......................................................................................................................................................25 11 Other non-current assets .........................................................................................................................................26 12 Inventories ................................................................................................................................................................27 13 Trade and other receivables ....................................................................................................................................27 14 Cash and cash equivalents......................................................................................................................................28 15 Share capital and other reserves ............................................................................................................................29 16 Short-term and long-term borrowings .....................................................................................................................30 17 Income taxes ............................................................................................................................................................31 18 Liability to the regional administration .....................................................................................................................33 19 Employee benefit obligations...................................................................................................................................33 20 Accounts payable .....................................................................................................................................................35 21 Sales .........................................................................................................................................................................35 22 Cost of sales .............................................................................................................................................................35 23 Distribution expenses...............................................................................................................................................35 24 General and administrative expenses.....................................................................................................................36 25 Operating income/(expenses) – net ........................................................................................................................36 26 Finance income and costs .......................................................................................................................................36 27 Earnings per share ...................................................................................................................................................37 28 Balances and transactions with related parties ......................................................................................................37 29 Contingencies, commitments and operating risks..................................................................................................38 30 Financial risk management and fair value of financial instruments .......................................................................39 31 Events after the reporting date ................................................................................................................................44

AO PricewaterhouseCoopers Audit White Square Office Center 10 Butyrsky Val Moscow, Russian Federation, 125047 T: +7 (495) 967 6000, F:+7 (495) 967 6001, www.pwc.ru

Independent Auditor’s Report To the Shareholders of AO Holding Company METALLOINVEST:

Our opinion In our opinion, the consolidated financial statements present fairly, in all material respects, the consolidated financial position of AO Holding Company METALLOINVEST (the “Company”) and its subsidiaries (together – the “Group”) as at 31 December 2019, and its consolidated financial performance and its consolidated cash flows for the year then ended in accordance with International Financial Reporting Standards (IFRS). What we have audited The Group’s consolidated financial statements comprise:

• the consolidated statement of financial position as of 31 December 2019; • the consolidated statement of profit or loss and other comprehensive income for the year then

ended;

• the consolidated statement of cash flows for the year then ended; and • the consolidated statement of changes in equity for the year then ended;

the notes to the consolidated financial statements, which include significant accounting policies and other explanatory information.

Basis for opinion We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the consolidated financial statements section of our report. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Independence We are independent of the Group in accordance with the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants (IESBA Code) and the ethical requirements of the Auditor’s Professional Ethics Code and Auditor’s Independence Rules that are relevant to our audit of the consolidated financial statements in the Russian Federation. We have fulfilled our other ethical responsibilities in accordance with these requirements and the IESBA Code.

ii

Our audit approach Overview

Overall Group materiality: USD 80,000 thousand, which represents 5% of weighted average profit before tax.

• We conducted audit work at all significant reporting units in both the Russian Federation and abroad.

• Each significant reporting unit was audited by component teams based in the Russian Federation, Switzerland and Cyprus.

• Our audit scope addressed 96% of the Group’s revenues and 96% of the Group’s absolute value of underlying profit before tax.

Introduction of a new automated accounting system.

As part of designing our audit, we determined materiality and assessed the risks of material misstatement in the consolidated financial statements. In particular, we considered where management made subjective judgments; for example, in respect of significant accounting estimates that involved making assumptions and considering future events that are inherently uncertain. As in all of our audits, we also addressed the risk of management override of internal controls, including among other matters consideration of whether there was evidence of bias that represented a risk of material misstatement due to fraud. Materiality The scope of our audit was influenced by our application of materiality. An audit is designed to obtain reasonable assurance whether the consolidated financial statements are f ree from material misstatement. Misstatements may arise due to fraud or error. They are considered material if individually or in aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of the consolidated financial statements. Based on our professional judgment, we determined certain quantitative thresholds for materiality, including the overall Group materiality for the consolidated financial statements as a whole as set out in the table below. These, together with qualitative considerations, helped us to determine the scope of our audit and the nature, timing and extent of our audit procedures and to evaluate the effect of misstatements, if any, both individually and in aggregate on the consolidated financial statements as a whole.

Overall Group materiality USD 80,000 thousand (2018: USD 62,000 thousand)

How we determined it 5% of five year weighted average profit before tax giving a higher weight to the current year and lower weight to the preceding years

Rationale for the materiality benchmark applied

We chose profit before tax as the benchmark because, in our view, it is the benchmark against which the performance of the Group is commonly measured by users, and is a generally accepted benchmark. Due to fluctuations of profit in different years, we considered it more appropriate to use a five-year weighted average as a benchmark. We chose 5% which is consistent with quantitative materiality thresholds used for profit-oriented companies in this sector. This is consistent with the basis for our materiality calculation in the previous year.

Materiality

Group scoping

Key audit matters

iii

How we tailored our Group audit scope Considering our ultimate responsibility for the opinion on the Group’s consolidated financial statements we are responsible for the direction, supervision and performance of the Group audit. In this context, we tailored the scope of our audit and determined the nature and extent of the audit procedures for components of the Group to ensure that we performed sufficient work to enable us to provide an opinion on the consolidated financial statements as a whole. Determining factors were the structure of the Group, the financial significance and/or risk profile of the Group entities and activities, the accounting processes and controls, and the industry in which the Group operates. On this basis, we selected Group entities for which an audit of financial information or specific balances was considered necessary. We also included tax, valuation and actuarial specialists in our group audit team. The group audit was focused on the significant components in the Russian Federation and abroad. These components include Group entities which are individually financially significant. Each of these components required an audit of their complete set of financial information. For components that are not individually financially significant, but that are important to achieve sufficient coverage on individual items, we performed an audit of a complete set of financial information or an audit of one or more account balances and disclosures. For the significant components in the Russian Federation, including the four main production plants based in Kursk, Belgorod and Orenburg regions, we performed the audit work ourselves. For the foreign components located in Switzerland and Cyprus, we used component auditors from other PwC network firms who are familiar with the local laws and regulations to perform this audit work. Where the work was performed by the component auditors, we as the group auditor determined the level of involvement we needed to have in the audit work at those components to be able to conclude whether suf ficient appropriate audit evidence had been obtained as a basis for our opinion on the Group’s consolidated financial statements as a whole. We issued specific instructions to the audit teams of the components in our audit scope. These instructions included our risk analysis, materiality and audit approach for key audit areas. The group engagement team regularly communicated with all component auditors and in the current year, the group audit team visited local management of Metalloinvest Trading AG and the related PwC component auditors in Switzerland. The Group’s consolidation, financial statements disclosures and a number of complex items were audited by the group engagement team. The group engagement team audited the accounting treatment of significant reporting items such as financial assets measured at fair value, annual goodwill impairment testing, segment information, pension liabilities and others. By performing the above procedures at components, combined with additional procedures at the Group level, we have obtained sufficient and appropriate audit evidence regarding the financial information of the Group as a whole to provide a basis for our opinion on the consolidated financial statements.

iv

Key audit matters Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Key audit matter How our audit addressed the key audit matter

Introduction of a new automated accounting system In 2018, the Group’s subsidiaries AO Lebedinsky GOK and PAO Mikhailovsky GOK (mining segment) introduced a new integrated f inancial and business management system using the SAP S/4HANA business suite. In 2019, the Group continued the implementation and since 1 July 2019, the new system was introduced at the remaining major Group’s subsidiaries: AO Oskol Electrometallurgical Plant, AO Ural Steel (steel segment) and Metalloinvest Trading AG (trading segment). This year we focused on the implementation of SAP system on Metalloinvest Trading AG due to significance of changes in financial reporting processes, specifics and difference in business processes of the trading company comparing to the production entities of the Group and, consequently, potential risks of material misstatements that may arise in case of system malfunction.

We performed the following audit procedures for Metalloinvest Trading AG: Understand and evaluate control environment We obtained an understanding of IT general controls and determined whether they have been implemented. We obtained an understanding of controls relevant to our audit, evaluated the design of those controls, and determined whether they have been implemented. Migration of data We tested the completeness and accuracy of data migration to the new accounting system, in particular, we: • checked the migration of all balances on

accounts; • analysed the classification of balances on

accounts in the new accounting system. Substantive testing We paid special attention to the accounting for inventories as one of the most complex areas and, in particular, we performed: • reconciliation of all purchased inventory with

the sales data of production entities of the Group for 2019;

• sample testing with a higher level of assurance of railway freight transportation expenses for the second half of 2019;

• sample testing with a higher level of assurance of the year-end inventory costing including transportation costs incurred before the moment of sale;

• testing of finished goods net realizable value calculation.

Based on the procedures performed we did not identify any material misstatements in financial statements arising from the transition to the new automated accounting system.

v

Other information Management is responsible for the other information. The other information comprises the Group’s annual report for the year ended 31 December 2019 and the issuer’s report for the 1st quarter 2020 (but does not include the consolidated financial statements and our auditor’s report thereon), which are expected to be made available to us after the date of this auditor’s report. Our opinion on the consolidated financial statements does not cover the other information and we do not and will not express any form of assurance conclusion thereon. In connection with our audit of the consolidated financial statements, our responsibility is to read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the consolidated financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. When we read the other information identified above, if we conclude that there is a material misstatement therein, we are required to communicate the matter to those charged with governance.

Responsibilities of management and those charged with governance for the consolidated financial statements Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with IFRS, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are f ree from material misstatement, whether due to fraud or error. In preparing the consolidated financial statements, management is responsible for assessing the Group’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so. Those charged with governance are responsible for overseeing the Group’s financial reporting process.

Auditor’s responsibilities for the audit of the consolidated financial statements Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are f ree from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if , individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements. As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional scepticism throughout the audit. We also: • Identify and assess the risks of material misstatement of the consolidated financial statements,

whether due to f raud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as f raud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

AO Holding Company METALLOINVEST Consolidated Statement of Profit or Loss and Other Comprehensive Income for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

The accompanying notes 1 to 31 form an integral part of these consolidated financial statements. 2

Note 2019 2018 Sales 21 6,960,373 7,187,023 Cost of sales 22 (3,194,572) (3,267,838) Gross profit 3,765,801 3,919,185 Distribution expenses 23 (1,084,135) (856,080) General and administrative expenses 24 (328,312) (347,718) Other operating income/(expenses), net 25 (217,093) 6,805 Operating profit 2,136,261 2,722,192 Finance income 26 203,558 118,454 Finance costs 26 (361,554) (333,182) Change in credit loss allowance on loans advanced, net 14,419 (19,429) Foreign exchange gain/(loss) from borrowings and loans advanced, net 225,868 (379,476) Profit before income tax 2,218,552 2,108,559 Income tax charge 17 (487,552) (461,378) Profit for the year 1,731,000 1,647,181 Other comprehensive income: Items that will not be reclassified to profit or loss: Fair value gain/(loss) arising on equity investments 9,15 14,089 (16,603) Remeasurements of employee benefit obligations (31,535) 13,190 Currency translation differences 293,995 (293,648) Total other comprehensive income/(loss) for the year 276,549 (297,061) Total comprehensive income for the year 2,007,549 1,350,120 Profit is attributable to: Owners of the Company 1,676,897 1,602,348 Non-controlling interests 54,103 44,833 1,731,000 1,647,181 Total comprehensive income is attributable to: Owners of the Company 1,953,446 1,305,287 Non-controlling interests 54,103 44,833 2,007,549 1,350,120 Basic and diluted earnings per ordinary share for profit attributable to the owners of the Company (in USD per share) 27 0.0224 0.0214

AO Holding Company METALLOINVEST Consolidated Statement of Cash Flows for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

The accompanying notes 1 to 31 form an integral part of these consolidated financial statements. 3

Note 2019 2018 Cash flows from operating activities: Profit before income tax 2,218,552 2,108,559 Reconciliation between profit before income tax and net cash from operating activities:

Depreciation of property, plant and equipment 269,285 252,894 Amortisation of intangible assets and mineral rights 43,023 37,437 Finance costs, net 26 157,996 214,728 Foreign exchange (gain)/loss (132,551) 281,643 Change in credit loss allowance on loans advanced, net (14,419) 19,429 Other (18,359) 18,980

Changes in: Inventories 155,409 (211,417) Trade and other receivables 78,347 (275,619) Trade and other payables (26,054) 44,896 Employee benefit obligations (6,267) (18,766)

Income tax paid (503,619) (460,056) Interest paid (283,564) (316,500) Premium paid on early redemption of guaranteed notes and unsecured corporate bonds 16 (6,558) - Other finance charges (4,882) (648) Net cash from operating activities 1,926,339 1,695,560 Cash flows from investing activities: Purchases of property, plant and equipment and intangible assets (516,812) (441,020) Loans advanced (1,181,972) (1,802,372) Repayments of loans advanced 146,093 1,234,708 Interest received 13,549 69,855 Other 365 69 Net cash used in investing activities (1,538,777) (938,760) Cash flows from financing activities: Repayment of borrowings 16 (1,178,901) (725,523) Lease payments 16 (5,161) - Proceeds from borrowings 16 931,827 640,289 Acquisition of additional interest in subsidiaries (222,547) (74,215) Proceeds from disposal of interest in subsidiaries - 166,045 Transaction costs on disposal of interest in subsidiaries - (2,270) Dividends paid by the Group’s subsidiaries to non-controlling interests (279) (956) Dividends paid to the owners of the Company 15 (302,863) (434,682) Net cash used in financing activities (777,924) (431,312) Effect of exchange rate changes on cash and cash equivalents 939 (22,773) Net (decrease)/increase in cash and cash equivalents (389,423) 302,715 Cash and cash equivalents at the beginning of the year 693,087 390,372 Cash and cash equivalents at the end of the year 303,664 693,087

AO Holding Company METALLOINVEST Consolidated Statement of Changes in Equity for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

The accompanying notes 1 to 31 form an integral part of these consolidated financial statements. 4

Attributable to owners of the Company

Note Share

capital Other

reserves Retained earnings Total

Non-controlling

interests Total

equity Balance at 1 January 2018 176,382 (1,684,846) 2,278,404 769,940 1,088 771,028 Profit for the year - - 1,602,348 1,602,348 44,833 1,647,181 Other comprehensive income/(loss) Fair value loss on equity investments 9,15 - (16,603) - (16,603) - (16,603) Remeasurements of employee benefit obligations - - 13,190 13,190 - 13,190 Currency translation differences 15 - (293,648) - (293,648) - (293,648) Total other comprehensive income/(loss) - (310,251) 13,190 (297,061) - (297,061) Total comprehensive income/(loss) for the year ended 31 December 2018 - (310,251) 1,615,538 1,305,287 44,833 1,350,120 Acquisition of additional interest in subsidiaries - - (101,160) (101,160) 26,545 (74,615) Disposal of interest in subsidiaries - - (34,743) (34,743) 201,921 167,178 Cancellation of treasury shares in subsidiary - - (262) (262) 262 - Dividends declared by the Group’s subsidiaries to non-controlling interests - - - - (1,362) (1,362) Dividends declared by the Company 15 - - (439,092) (439,092) - (439,092) Balance at 31 December 2018 176,382 (1,995,097) 3,318,685 1,499,970 273,287 1,773,257 Profit for the year - - 1,676,897 1,676,897 54,103 1,731,000 Other comprehensive income/(loss) Fair value gain on equity investments 9,15 - 14,089 - 14,089 - 14,089 Remeasurements of employee benefit obligations - - (31,535) (31,535) - (31,535) Currency translation differences 15 - 293,995 - 293,995 - 293,995 Total other comprehensive income/(loss) - - 308,084 (31,535) 276,549 - 276,549 Total comprehensive income for the year ended 31 December 2019 - - 308,084 1,645,362 1,953,446 54,103 2,007,549 Acquisition of additional interest in subsidiaries - - 96,179 96,179 (318,910) (222,731) Cancellation of unclaimed dividends to non-controlling interests to retained earnings - - 1,707 1,707 - 1,707 Dividends declared by the Company 15 - - (300,909) (300,909) - (300,909) Balance at 31 December 2019 176,382 (1,687,013) 4,761,024 3,250,393 8,480 3,258,873

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

5

1 General information

These consolidated financial statements have been prepared in accordance with International Financial Reporting Standards for the year ended 31 December 2019 for AO Holding Company METALLOINVEST (the “Company”) and its subsidiaries (the “Group”). The Group’s principal business activity is the production and sale of iron ore products and ferrous metals. These products are sold both in Russia and abroad. The Company is incorporated and domiciled in Russia. The address of its registered office is Rublyovskoye shosse, 28, Moscow, Russia. The Group’s manufacturing facilities are primarily based in the Kursk, Belgorod and Orenburg regions.

At 31 December 2019 and 2018, USM Metalloinvest LLC (a 100%-owned direct subsidiary of HС USM LLC) owned a 100% stake in the Company.

At 31 December 2019 and 2018, the major beneficial owner of the Company was Alisher B. Usmanov, who owned a 49% stake in HC USM LLC.

The following table sets out the major subsidiaries of the Group:

Entity Activity

Nominal ownership, % 31 December

2019 31 December

2018 OOO Management Company METALLOINVEST Management company 100% 100% AO Lebedinskiy Mining and Processing Works (“LGOK”) Production and sale of iron ore products 100% 100% AO Oskol Electrometallurgical Plant (“OEMK”)

Production and sale of ferrous metal products 100% 100%

PAO Mikhailovsky Mining and Processing Works (“MGOK”) Production and sale of iron ore products 100% 89.317%

AO Ural Steel (“Ural Steel”) Production and sale of ferrous metal products 100% 100%

OOO Ural Scrap Company Collection and processing of scrap 100% 100% Metalloinvest Trading AG (Switzerland) Iron ore and steel products trading 100% 100%

2 Basis of preparation and summary of significant accounting policies

Basis of preparation. These consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) under the historical cost convention except as described below. The principal accounting policies applied in the preparation of these consolidated financial statements are set out below. Apart from the accounting policy changes resulting from the adoption of IFRS 16 effective from 1 January 2019, these policies have been consistently applied to all the periods presented.

Consolidated financial statements. Subsidiaries are those investees, including structured entities, that the Group controls because the Group (i) has power to direct the relevant activities of the investees that significantly affect their returns, (ii) has exposure, or rights, to variable returns from its involvement with the investees, and (iii) has the ability to use its power over the investees to affect the amount of the investor’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether the Group has power over another entity. For a right to be substantive, the holder must have a practical ability to exercise that right when decisions about the direction of the relevant activities of the investee need to be made. The Group may have power over an investee even when it holds less than the majority of the voting power in an investee. In such a case, the Group assesses the size of its voting rights relative to the size and dispersion of holdings of the other vote holders to determine if it has de-facto power over the investee. Protective rights of other investors, such as those that relate to fundamental changes of the investee’s activities or apply only in exceptional circumstances, do not prevent the Group from controlling an investee. Subsidiaries are consolidated from the date on which control is transferred to the Group (acquisition date) and are deconsolidated from the date that control ceases.

The acquisition method of accounting is used to account for the acquisition of subsidiaries. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured at their fair values at the acquisition date, irrespective of the extent of any non-controlling interest.

The Group measures non-controlling interest on a transaction by transaction basis, either at: (a) fair value, or (b) the non-controlling interest's proportionate share of net assets of the acquiree.

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

6

2 Basis of preparation and summary of significant accounting policies (continued)

Goodwill is measured by deducting the net assets of the acquiree from the aggregate of the consideration transferred for the acquiree, the amount of non-controlling interest in the acquiree and the fair value of an interest in the acquiree held immediately before the acquisition date. Any negative amount (“negative goodwill”) is recognised in profit or loss, after management reassesses whether it identified all the assets acquired and all the liabilities and contingent liabilities assumed and reviews the appropriateness of their measurement.

The consideration transferred for the acquiree is measured at the fair value of the assets given up, equity instruments issued and liabilities incurred or assumed, including the fair value of assets or liabilities from contingent consideration arrangements, but excludes acquisition related costs such as advisory, legal, valuation and similar professional services. Transaction costs incurred for issuing equity instruments are deducted from equity; transaction costs incurred for issuing debt are deducted from its carrying amount and all other transaction costs associated with the acquisition are expensed.

Intercompany transactions, balances and unrealised gains on transactions between Group companies are eliminated; unrealised losses are also eliminated unless the transaction provides evidence of an impairment of the asset transferred. The Company and all of its subsidiaries use uniform accounting policies consistent with the Group’s policies.

Non-controlling interest is that part of the net results and of the equity of a subsidiary attributable to interests, which are not owned, directly or indirectly, by the Company. Non-controlling interest forms a separate component of the Group’s equity.

When the group ceases to consolidate or equity account for an investment because of a loss of control or significant influence, any retained interest in the entity is remeasured to its fair value with the change in carrying amount recognised in profit or loss. This fair value becomes the initial carrying amount for the purposes of subsequently accounting for the retained interest as an associate, joint venture or financial asset. In addition, any amounts previously recognised in other comprehensive income in respect of that entity are accounted for as if the group had directly disposed of the related assets or liabilities. This may mean that amounts previously recognised in other comprehensive income are reclassified to profit or loss.

Transactions with non-controlling interests. The Group treats transactions with non-controlling interests as transactions with equity owners of the Group. For purchases from non-controlling interests, the difference between any consideration paid and the relevant share acquired of the carrying value of net assets of the subsidiary is recorded in equity. Gains or losses on disposals to non-controlling interests are also recorded in equity.

Foreign currency translation. The functional currency of each of the Group’s consolidated entities is the currency of the primary economic environment in which the entity operates. The Company’s functional currency is the national currency of Russia, Russian roubles (“RUB”); the Group’s presentation currency is US Dollar (“USD”) as it is considered by management to be more relevant presentation currency for users of the consolidated financial statements of the Group.

Monetary assets and liabilities are translated into each entity’s functional currency at the official exchange rate of the Central Bank of Russia (the “Central Bank”) at the respective end of the reporting period. Foreign exchange gains and losses resulting from settlement of transactions and from translation of monetary assets and liabilities into each entity’s functional currency at year-end official exchange rates of the Central Bank are recognised in profit or loss. Translation at year-end rates does not apply to non-monetary items that are measured at historical cost.

Non-monetary items measured at fair value in a foreign currency, including equity investments, are translated using the exchange rates at the date when the fair value was determined. Effects of exchange rate changes on non-monetary items measured at fair value in a foreign currency are recorded as part of the fair value gain or loss.

The results and financial position of each Group entity (the functional currency of none of which is a currency of a hyperinflationary economy) are translated into the presentation currency as follows:

(i) assets and liabilities for each statement of financial position are translated at the closing rate at the end of the respective reporting period;

(ii) income and expenses are translated at average exchange rates (unless this average is not a reasonable approximation of the cumulative effect of the rates prevailing on the transaction dates, in which case income and expenses are translated at the dates of the transactions);

(iii) components of equity are translated at the historical rate; and

(iv) all resulting exchange differences are recognised in other comprehensive income.

When control over a foreign operation is lost, the previously recognised exchange differences on translation to a different presentation currency are reclassified from other comprehensive income to profit or loss for the year as part of the gain or loss on disposal. On partial disposal of a subsidiary without loss of control, the related portion of accumulated currency translation differences is reclassified to non-controlling interest within equity.

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

7

2 Basis of preparation and summary of significant accounting policies (continued)

Goodwill and fair value adjustments arising on the acquisition of a foreign entity are treated as assets and liabilities of the foreign entity and translated at the closing rate.

At 31 December 2019, the principal exchange rates used for translating foreign currency balances were USD 1 = RUB 61.9057 (31 December 2018: USD 1 = RUB 69.4706), EUR 1 = RUB 69.3406 (31 December 2018: EUR 1 = RUB 79.4605).

Income and expenses for the year were translated to presentation currency at quarterly average exchange rates.

Quarterly average exchange rates/ Year

For the three months ended

31 March

For the three months ended

30 June

For the three months ended 30 September

For the three months ended

31 December 2019 66.1271 64.5584 64.5685 63.7192 2018 56.8803 61.7998 65.5323 66.4822

Segment reporting. Operating segments are reported in a manner consistent with the internal reporting provided to the Group’s chief operating decision maker. Segments whose revenue, result or assets are 10% or more of all the segments are reported separately.

Property, plant and equipment. Property, plant and equipment are stated at historical acquisition or construction cost less accumulated depreciation and provision for impairment, where required.

Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the Group and the cost of the item can be measured reliably. The carrying amount of any replaced part is derecognised. All other repairs and maintenance are recognised in profit or loss in the financial period in which they are incurred.

At each end of the reporting period management assesses whether there is any indication of impairment of property, plant and equipment. If any such indication exists, management estimates the recoverable amount, which is determined as the higher of an asset’s fair value less costs to sell and its value in use. The carrying amount is reduced to the recoverable amount and the impairment loss is recognised in profit or loss. An impairment loss recognised for an asset in prior years is reversed if there has been a change in the estimates used to determine the recoverable amount. Gains and losses on disposals determined by comparing proceeds with carrying amount are recognised in profit or loss.

Depreciation. Land is not depreciated. Depreciation on other items of property, plant and equipment is calculated using the straight-line method to allocate their cost to their residual values over their estimated useful lives:

Useful lives in years Buildings 7 to 135 Plant and equipment 3 to 30 Transport 5 to 20 Other 2 to 10

Included into Buildings group are tailings embankments which estimated useful lives vary from 60 to 135 years, useful life of the other buildings items vary from 7 to 50 years.

The residual value of an asset is the estimated amount that the Group would currently obtain from disposal of the asset less the estimated costs of disposal, if the asset was already of the age and in the condition expected at the end of its useful life. The residual value of an asset is nil if the Group expects to use the asset until the end of its physical life. The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at the end of each reporting period.

Capitalisation of borrowing costs. Borrowing costs directly attributable to the acquisition, construction or production of assets that necessarily take a substantial time to get ready for intended use or sale (qualifying assets) are capitalised as part of the costs of those assets.

Capitalisation of borrowing costs continues up to the date when the assets are substantially ready for their use or sale.

The Group capitalises borrowing costs that could have been avoided if it had not made capital expenditure on qualifying assets. Borrowing costs capitalised are calculated at the Group’s average funding cost (the weighted average interest cost is applied to the expenditures on the qualifying assets), except to the extent that funds are borrowed specifically for the purpose of obtaining a qualifying asset. Where this occurs, actual borrowing costs incurred less any investment income on the temporary investment of those borrowings are capitalised.

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

8

2 Basis of preparation and summary of significant accounting policies (continued)

Stripping costs. The Group separates two different types of stripping costs that are incurred in surface mining activity: a) stripping activity asset; and b) current stripping costs. Stripping activity asset is created as part of usual surface activity in order to obtain improved access to further quantities of minerals that will be mined in future periods. Current stripping costs are costs that are incurred in order to mine the mineral ore only in current period.

The Group recognises a stripping activity asset if, and only if, all of the following are met: 1) it is probable that the future economic benefit (improved access to the ore body) associated with the stripping activity will flow to the entity; 2) the entity can identify the component of the ore body for which access has been improved; and 3) the costs relating to the improved access to that component can be measured reliably.

After initial recognition, stripping activity assets are carried at cost less accumulated depreciation and impairment loss. Depreciation is calculated using the units of production method. Stripping asset is recognised within property, plant and equipment.

Right-of-use assets. The Group recognises a right-of-use asset and a corresponding lease liability at the commencement date of the lease. The right-of-use asset is initially measured at cost comprising of the lease liability, lease payments made at or before the commencement date, any initial direct costs and other lease related costs.

Contracts may contain both lease and non-lease components. The Group allocates the consideration in the contract to the lease and non-lease components based on their relative stand-alone prices.

The right-of-use asset is depreciated on a straight-line basis from the commencement date to the earlier of: the end of the useful life of the underlying asset or the end of the lease term. The lease term may include periods covered by an option to extend (or terminate) the lease, whenever the lease is reasonably certain to be extended (or not terminated). Management assesses extension and termination options of the leases on a regular basis.

Right-of-use assets are accounted for within "Property, plant and equipment" in the consolidated statement of financial position and are subject to testing for impairment, whenever there are indications that the asset may be impaired.

The right-of-use assets mainly comprised administrative offices lease contracts and are depreciated over 2 to 15 years.

Intangible assets. The Group’s intangible assets other than goodwill have finite useful lives and primarily include acquired computer software licences, licenced technology and customer relationships acquired in business combinations. Intangible assets are amortised using the straight-line method over their estimated useful lives of three to ten years for acquired computer software licences and customer relationships, and of twenty five to thirty years for licenced technology. Intangible assets are assessed for impairment whenever there is an indication that the intangible assets may be impaired.

If impaired, the carrying amount of intangible assets is written down to the higher of value in use and fair value less costs to sell.

Goodwill. Goodwill on acquisitions of subsidiaries is presented separately in the consolidated statement of financial position. Goodwill on acquisitions of associates is included in investment in associates. Goodwill is carried at cost less accumulated impairment losses, if any.

The Group tests goodwill for impairment at least annually and whenever there are indications that goodwill may be impaired. Goodwill is allocated to the cash-generating units, or groups of cash-generating units, that are expected to benefit from the synergies of the business combination. Such units or group of units represent the lowest level at which the Group monitors goodwill and are not larger than an operating segment. Gains or losses on disposal of an operation within a cash generating unit to which goodwill has been allocated include the carrying amount of goodwill associated with the operation disposed of, generally measured on the basis of the relative values of the operation disposed of and the portion of the cash-generating unit which is retained.

Mineral rights. In accordance with provisions of IFRS 3 Business Combinations mineral rights acquired in business combinations are recorded at their fair values at the date of acquisition, based on their appraised fair value. Other mineral rights and licences are recorded at cost.

Mineral rights stated at 31 December 2019 and 2018 represent mainly mineral rights recognised as a result of acquisition of MGOK in December 2006, which grant access to reserves that will be extracted over periods in excess of 100 years. The appraised value of these rights reflects expected cash flows over thirty years from the date of acquisition, since the impact of cash flows beyond this period is not material. The Group's production plans for these reserves are such that there is no material difference between amortisation calculated using the units of production and using the straight-line method. These rights are therefore amortised on a straight line basis over thirty years.

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

9

2 Basis of preparation and summary of significant accounting policies (continued)

Advances issued. Advances issued are carried at cost less provision for impairment. An advance issued is classified as non-current when the goods or services relating to the advance issued are expected to be obtained after one year, or when the advance issued relates to an asset, which will itself be classified as non-current upon initial recognition. If there is an indication that the assets, goods or services relating to an advance issued will not be received, the carrying value of the advance issued is written down accordingly and a corresponding impairment loss is recognised in profit or loss.

Inventories. Inventories are stated at the lower of cost and net realisable value. Cost of inventory is determined using the weighted average method. The cost of finished goods and work in progress comprises raw material, direct labour, other direct costs and related production overheads (based on normal operating capacity) but excludes borrowing costs. Net realisable value is the estimated selling price in the ordinary course of business, less the cost of completion and distribution expenses.

Financial instruments – key measurement terms. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The best evidence of fair value is the price in an active market. An active market is one in which transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis.

Fair value of financial instruments traded in an active market is measured as the product of the quoted price for the individual asset or liability and the number of instruments held by the entity. This is the case even if a market’s normal daily trading volume is not sufficient to absorb the quantity held and placing orders to sell the position in a single transaction might affect the quoted price.

Valuation techniques such as discounted cash flow models or models based on recent arm’s length transactions or consideration of financial data of the investees are used to measure fair value of certain financial instruments for which external market pricing information is not available. Fair value measurements are analysed by level in the fair value hierarchy as follows: (i) level one are measurements at quoted prices (unadjusted) in active markets for identical assets or liabilities, (ii) level two measurements are valuations techniques with all material inputs observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices), and (iii) level three measurements are valuations not based on solely observable market data (that is, the measurement requires significant unobservable inputs). Transfers between levels of the fair value hierarchy are deemed to have occurred at the end of the reporting period.

Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of a financial instrument. An incremental cost is one that would not have been incurred if the transaction had not taken place. Transaction costs include fees and commissions paid to agents (including employees acting as selling agents), advisors, brokers and dealers, levies by regulatory agencies and securities exchanges, and transfer taxes and duties. Transaction costs do not include debt premiums or discounts, financing costs or internal administrative or holding costs.

Amortised cost (“AC”) is the amount at which the financial instrument was recognised at initial recognition less any principal repayments, plus accrued interest, and for financial assets less any allowance for expected credit losses (“ECL”). Accrued interest includes amortisation of transaction costs deferred at initial recognition and of any premium or discount to the maturity amount using the effective interest method. Accrued interest income and accrued interest expense, including both accrued coupon and amortised discount or premium (including fees deferred at origination, if any), are not presented separately and are included in the carrying values of the related items in the consolidated statement of financial position.

The effective interest method is a method of allocating interest income or interest expense over the relevant period, so as to achieve a constant periodic rate of interest (effective interest rate) on the carrying amount. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts (excluding future credit losses) through the expected life of the financial instrument or a shorter period, if appropriate, to the gross carrying amount of the financial instrument. The effective interest rate discounts cash flows of variable interest instruments to the next interest repricing date, except for the premium or discount which reflects the credit spread over the floating rate specified in the instrument, or other variables that are not reset to market rates. Such premiums or discounts are amortised over the whole expected life of the instrument. The present value calculation includes all fees paid or received between parties to the contract that are an integral part of the effective interest rate. For assets that are purchased or originated credit impaired (“POCI”) at initial recognition, the effective interest rate is adjusted for credit risk, i.e. it is calculated based on the expected cash flows on initial recognition instead of contractual payments.

Financial instruments – initial recognition. Financial instruments at fair value though profit or loss (“FVTPL”) are initially recorded at fair value. All other financial instruments are initially recorded at fair value adjusted for transaction costs. Fair value at initial recognition is best evidenced by the transaction price. A gain or loss on initial recognition is only recorded if there is a difference between fair value and transaction price which can be evidenced by other observable current market transactions in the same instrument or by a valuation technique whose inputs include only data from observable markets. After the initial recognition, an ECL allowance is recognised for financial assets measured at AC and investments in debt instruments measured at fair value though other comprehensive income (“FVOCI”), resulting in an immediate accounting loss.

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

10

2 Basis of preparation and summary of significant accounting policies (continued)

All purchases and sales of financial assets that require delivery within the time frame established by regulation or market convention (“regular way” purchases and sales) are recorded at trade date, which is the date on which the Group commits to deliver a financial asset. All other purchases are recognised when the entity becomes a party to the contractual provisions of the instrument.

The Group uses discounted cash flow valuation techniques to determine the fair value of loans to related parties that are not traded in an active market. Differences may arise between the transaction price and fair value at initial recognition, which is determined using a valuation technique. Such differences are amortised using effective interest method over the term of the loans to related parties.

Financial assets – classification and subsequent measurement – measurement categories. The Group classifies financial assets in the following measurement categories: FVTPL, FVOCI and AC. The classification and subsequent measurement of debt financial assets depends on: (i) the Group’s business model for managing the related assets portfolio and (ii) the cash flow characteristics of the asset.

Financial assets – classification and subsequent measurement – business model. The business model reflects how the Group manages the assets in order to generate cash flows – whether the Group’s objective is: (i) solely to collect the contractual cash flows from the assets (“hold to collect contractual cash flows”,) or (ii) to collect both the contractual cash flows and the cash flows arising from the sale of assets (“hold to collect contractual cash flows and sell”) or, if neither of (i) and (ii) is applicable, the financial assets are classified as part of “other” business model and measured at FVTPL.

Business model is determined for a group of assets (on a portfolio level) based on all relevant evidence about the activities that the Group undertakes to achieve the objective set out for the portfolio available at the date of the assessment. Factors considered by the Group in determining the business model include the purpose and composition of a portfolio, past experience on how the cash flows for the respective assets were collected.

Financial assets – classification and subsequent measurement – cash flow characteristics. Where the business model is to hold assets to collect contractual cash flows or to hold contractual cash flows and sell, the Group assesses whether the cash flows represent solely payments of principal and interest (“SPPI”). Financial assets with embedded derivatives are considered in their entirety when determining whether their cash flows are consistent with the SPPI feature. In making this assessment, the Group considers whether the contractual cash flows are consistent with a basic lending arrangement, i.e. interest includes only consideration for credit risk, time value of money, other basic lending risks and profit margin.

Where the contractual terms introduce exposure to risk or volatility that is inconsistent with a basic lending arrangement, the financial asset is classified and measured at FVTPL. The SPPI assessment is performed on initial recognition of an asset and it is not subsequently reassessed.

Financial assets – reclassification. Financial instruments are reclassified only when the business model for managing the portfolio as a whole changes. The reclassification has a prospective effect and takes place from the beginning of the first reporting period that follows after the change in the business model. The entity did not change its business model during the current and comparative period and did not make any reclassifications.

Financial assets impairment – credit loss allowance for ECL. The Group assesses, on a forward-looking basis, the ECL for debt instruments measured at AC and FVOCI and for the exposures arising from loan commitments and for contract assets. The Group measures ECL and recognises Net impairment losses on financial and contract assets at each reporting date. The measurement of ECL reflects: (i) an unbiased and probability weighted amount that is determined by evaluating a range of possible outcomes, (ii) time value of money and (iii) all reasonable and supportable information that is available without undue cost and effort at the end of each reporting period about past events, current conditions and forecasts of future conditions.

The Group applies a three stage model for impairment, based on changes in credit quality since initial recognition. A financial instrument that is not credit-impaired on initial recognition is classified in Stage 1. Financial assets in Stage 1 have their ECL measured at an amount equal to the portion of lifetime ECL that results from default events possible within the next 12 months or until contractual maturity, if shorter (“12 Months ECL”).

If the Group identifies a significant increase in credit risk (“SICR”) since initial recognition, the asset is transferred to Stage 2 and its ECL is measured based on ECL on a lifetime basis, that is, up until contractual maturity but considering expected prepayments, if any (“Lifetime ECL”). If the Group determines that a financial asset is credit-impaired, the asset is transferred to Stage 3 and its ECL is measured as a Lifetime ECL. For financial assets that are purchased or originated credit-impaired (“POCI Assets”), the ECL is always measured as a Lifetime ECL.

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

11

2 Basis of preparation and summary of significant accounting policies (continued)

Financial assets – write-off. Financial assets are written-off, in whole or in part, when the Group exhausted all practical recovery efforts and has concluded that there is no reasonable expectation of recovery. The write-off represents a derecognition event. Indicators that there is no reasonable expectation of recovery include: a significant financial difficulty of the counterparty as evidenced by its financial information that the Group obtains; the considered bankruptcy of the counterparty or a financial reorganisation; an adverse change in the payment status of the counterparty as a result of changes in the national or local economic conditions that impact the counterparty; or the value of collateral, if any, significantly decreases as a result of deteriorating market conditions. The Group may write-off financial assets that are still subject to enforcement activity when the Group seeks to recover amounts that are contractually due, however, there is no reasonable expectation of recovery.

Financial assets – derecognition. The Group derecognises financial assets when (a) the assets are redeemed or the rights to cash flows from the assets otherwise expire or (b) the Group has transferred the rights to the cash flows from the financial assets or entered into a qualifying pass-through arrangement whilst (i) also transferring substantially all the risks and rewards of ownership of the assets or (ii) neither transferring nor retaining substantially all the risks and rewards of ownership but not retaining control.

Control is retained if the counterparty does not have the practical ability to sell the asset in its entirety to an unrelated third party without needing to impose additional restrictions on the sale.

Financial assets – modification. The Group sometimes renegotiates or otherwise modifies the contractual terms of the financial assets. The Group assesses whether the modification of contractual cash flows is substantial considering, among other, the following factors: any new contractual terms that substantially affect the risk profile of the asset, significant change in interest rate, change in the currency denomination, new collateral or credit enhancement that significantly affects the credit risk associated with the asset or a significant extension of a loan when the borrower is not in financial difficulties.

If the modified terms are substantially different, the rights to cash flows from the original asset expire and the Group derecognises the original financial asset and recognises a new asset at its fair value. The date of renegotiation is considered to be the date of initial recognition for subsequent impairment calculation purposes, including determining whether a SICR has occurred. The Group also assesses whether the new loan or debt instrument meets the SPPI criterion. Any difference between the carrying amount of the original asset derecognised and fair value of the new substantially modified asset is recognised in profit or loss, unless the substance of the difference is attributed to a capital transaction with owners.

In a situation where the renegotiation was driven by financial difficulties of the counterparty and inability to make the originally agreed payments, the Group compares the original and revised expected cash flows to assets whether the risks and rewards of the asset are substantially different as a result of the contractual modification. If the risks and rewards do not change, the modified asset is not substantially different from the original asset and the modification does not result in derecognition. The Group recalculates the gross carrying amount by discounting the modified contractual cash flows by the original effective interest rate (or credit-adjusted effective interest rate for POCI financial assets), and recognises a modification gain or loss in profit or loss.

Financial liabilities – measurement categories. Financial liabilities are classified and subsequently measured at AC, except for (i) financial liabilities at FVTPL: this classification is applied to derivatives, financial liabilities held for trading (e.g. short positions in securities), contingent consideration recognised by an acquirer in a business combination and other financial liabilities designated as such at initial recognition and (ii) financial guarantee contracts and loan commitments.

Financial liabilities – derecognition. Financial liabilities are derecognised when they are extinguished (i.e. when the obligation specified in the contract is discharged, cancelled or expires).

An exchange between the Group and its original lenders of debt instruments with substantially different terms, as well as substantial modifications of the terms and conditions of existing financial liabilities, are accounted for as an extinguishment of the original financial liability and the recognition of a new financial liability. The terms are substantially different if the discounted present value of the cash flows under the new terms, including any fees paid net of any fees received and discounted using the original effective interest rate, is at least 10% different from the discounted present value of the remaining cash flows of the original financial liability. In addition, other qualitative factors, such as the currency that the instrument is denominated in, changes in the type of interest rate, new conversion features attached to the instrument and change in loan covenants are also considered. If an exchange of debt instruments or modification of terms is accounted for as an extinguishment, any costs or fees incurred are recognised as part of the gain or loss on the extinguishment. If the exchange or modification is not accounted for as an extinguishment, any costs or fees incurred adjust the carrying amount of the liability and are amortised over the remaining term of the modified liability.

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

12

2 Basis of preparation and summary of significant accounting policies (continued)

Modifications of liabilities that do not result in extinguishment are accounted for as a change in estimate using a cumulative catch up method, with any gain or loss recognised in profit or loss, unless the economic substance of the difference in carrying values is attributed to a capital transaction with owners.

Offsetting financial instruments. Financial assets and liabilities are offset and the net amount reported in the statement of financial position only when there is a legally enforceable right to offset the recognised amounts, and there is an intention to either settle on a net basis, or to realise the asset and settle the liability simultaneously. Such a right of set off (a) must not be contingent on a future event and (b) must be legally enforceable in all of the following circumstances: (i) in the normal course of business, (ii) in the event of default and (iii) in the event of insolvency or bankruptcy.

Cash and cash equivalents. Cash and cash equivalents includes cash in hand, deposits held at call with banks, and other short-term highly liquid investments with original maturities of three months or less. Bank deposits held for longer than three months that are repayable on demand within several working days without penalties or that can be redeemed/withdrawn, subject to the interest income forfeited, are classified as cash equivalents if the deposits are held to meet short-term cash needs and there is no significant risk of a change in value as a result of an early withdrawal. Other term deposits are included into short-term investments.

Restricted balances are excluded from cash and cash equivalents for the purposes of the cash flow statement. Balances restricted from being exchanged or used to settle a liability for at least twelve months after the end of the reporting period are included in other non-current assets. Bank overdrafts are shown within borrowings in current liabilities. Cash flows arising from overdrafts movements are reported on a net basis in cash flow statement within financing activities.

Trade and other receivables. Trade and other receivables are initially recognised at fair value and are subsequently carried at AC using the effective interest method.

Trade and other payables. Trade payables are accrued when the counterparty performs its obligations under the contract and are recognised initially at fair value and subsequently carried at AC using the effective interest method.

Equity investments. Equity investments that are not held for trading are initially recognised at fair value and designated at FVOCI. Fair value gains and losses on equity investments are presented in OCI, there is no subsequent reclassification of fair value gains and losses to profit or loss following the impairment or derecognition of the investment.

Loans advanced. Loans advanced are initially recognised at fair value and are subsequently measured depending on business model applied by the Group for each particular loan advanced and cash flow characteristics. As at 31 December 2019 and 2018 the Group hold loans advanced measured at AC and FVTPL.

Share capital. Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares are shown in equity as a deduction, net of tax, from the proceeds.

Where the Company or its subsidiaries purchase the Company’s equity instruments (treasury shares), the consideration paid, including any directly attributable incremental costs, net of income taxes, is deducted from retained earnings until the equity instruments are reissued, disposed of or cancelled. Where such shares are subsequently sold or reissued, any consideration received, net of any directly attributable incremental transaction costs and the related income tax effects, is included in retained earnings.

Dividends. Dividends are recognised as a liability and deducted from equity in the period in which they are declared and approved. Any dividends declared after the reporting period and before the financial statements are authorised for issue are disclosed in the subsequent events note.

Short-term employee benefits. Wages, salaries, contributions to the Russian state medical and social insurance funds, paid annual leave and sick leave, bonuses, and non-monetary benefits (such as health services and kindergarten services) are accrued in the year in which the associated services are rendered by the employees of the Group and are included within labour costs in operating expenses. Contributions to the Russian state pension fund are treated as defined contribution plan.

Pension and other post-employment benefits. Group companies operate both funded and unfunded post-employment benefits plans. Typically, defined benefit plans define an amount of pension benefit that an employee will receive on retirement, usually dependent on one or more factors such as age, years of service and compensation.

The liability recognised in the statement of financial position in respect of defined benefit pension plans is the present value of the defined benefit obligation at the end of the reporting period date less the fair value of any plan assets. The defined benefit obligation is calculated annually by independent actuaries using the projected unit credit method.

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

13

2 Basis of preparation and summary of significant accounting policies (continued)

The present value of the defined benefit obligation is determined by discounting the estimated future cash outflows using interest rates of government bonds that have maturities approximating those of the related pension liability.

Actuarial gains and losses arising from experience adjustments and changes in actuarial assumptions are recognised immediately in other comprehensive income as they arise.

Past-service costs are recognised immediately in profit or loss.

Income taxes. The income tax charge is calculated on the basis of the tax laws enacted or substantively enacted by the end of the reporting period in the countries where the company’s subsidiaries and associates operate and generate taxable income, primarily Russia. The income tax charge/credit comprises current tax and deferred tax and is recognised in profit or loss for the year, except to the extent that it relates to transactions that are recognised in other comprehensive income or directly in equity. In this case, the tax is also recognised in other comprehensive income or directly in equity, respectively.

Current tax is the amount expected to be paid to or recovered from the taxation authorities in respect of taxable profits or losses for the current and prior periods. Taxes, other than on income, are recorded within operating expenses.

Deferred income tax is provided using the balance sheet liability method for tax loss carry forwards and temporary differences arising between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes. In accordance with the initial recognition exemption, deferred taxes are not recorded for temporary differences arising on initial recognition of an asset or a liability in a transaction other than a business combination if the transaction, when initially recorded, affects neither accounting nor taxable profit. Deferred tax liabilities are not recorded for temporary differences arising on initial recognition of goodwill or subsequently for goodwill which is not deductible for tax purposes. Deferred tax balances are measured at tax rates enacted or substantively enacted at the end of the reporting period which are expected to apply to the period when the temporary differences will reverse or the tax loss carry forwards will be utilised. Deferred tax assets and liabilities are netted only within the individual companies of the Group. Deferred tax assets for deductible temporary differences and tax loss carry forwards are recorded only to the extent that it is probable that future taxable profit will be available against which the deductions can be utilised.

Deferred income tax is provided on temporary differences arising from investments in subsidiaries and associates, except where the timing of the reversal of the temporary difference is controlled by the Group and it is probable that the temporary difference will not reverse in the foreseeable future.

The Group's uncertain tax positions are reassessed by management at the end of each reporting period. Liabilities are recorded for income tax positions that are determined by management as more likely than not to result in additional taxes being levied if the positions were to be challenged by the tax authorities. The assessment is based on the interpretation of tax laws that have been enacted or substantively enacted by the end of the reporting period and any known court or other rulings on such issues. Liabilities for penalties, interest and taxes other than on income are recognised based on management’s best estimate of the expenditure required to settle the obligations at the end of the reporting period.

Value added tax. Output value added tax related to sales is payable to tax authorities on the earlier of (a) collection of receivables from customers or (b) delivery of goods or services to customers. Input VAT is generally recoverable against output VAT upon receipt of the VAT invoice. The tax authorities permit the settlement of VAT on a net basis. VAT related to sales and purchases is recognised in the consolidated statement of financial position on a gross basis and disclosed separately as an asset and liability. Where provision has been made for the ECL of receivables, the impairment loss is recorded for the gross amount of the debtor, including VAT.

Provisions for liabilities and charges. Provisions for liabilities and charges are non-financial liabilities of uncertain timing or amount. They are accrued when the Group has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources will be required to settle the obligation, and a reliable estimate of the amount can be made. Where there are a number of similar obligations, the likelihood that an outflow will be required in settlement is determined by considering the class of obligations as a whole. A provision is recognised even if the likelihood of an outflow with respect to any one item included in the same class of obligations may be small.

Where the Group expects a provision to be reimbursed, for example under an insurance contract, the reimbursement is recognised as a separate asset, but only when the reimbursement is virtually certain.

Provisions are measured at the present value of the expenditures expected to be required to settle the obligation using a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the obligation. The increase in the provision due to passage of time is recognised as interest expense.

AO Holding Company METALLOINVEST Notes to the Consolidated Financial Statements for the year ended 31 December 2019 (in thousands of US dollars, unless otherwise stated)

14

2 Basis of preparation and summary of significant accounting policies (continued)

Lease liabilities. The lease liability is initially measured at the present value of fixed lease payments that are not paid at the commencement date. Lease payments are discounted using the interest rate implicit in the lease. If that rate cannot be readily determined, the lessee's individual incremental borrowing rate is used.