Annual Review 2014 - SIBUR – Investor...

241

Annual Review 2014 FROM VISION TO REALITY

Transcript of Annual Review 2014 - SIBUR – Investor...

Annual Review 2014FROM VISION TO REALITY

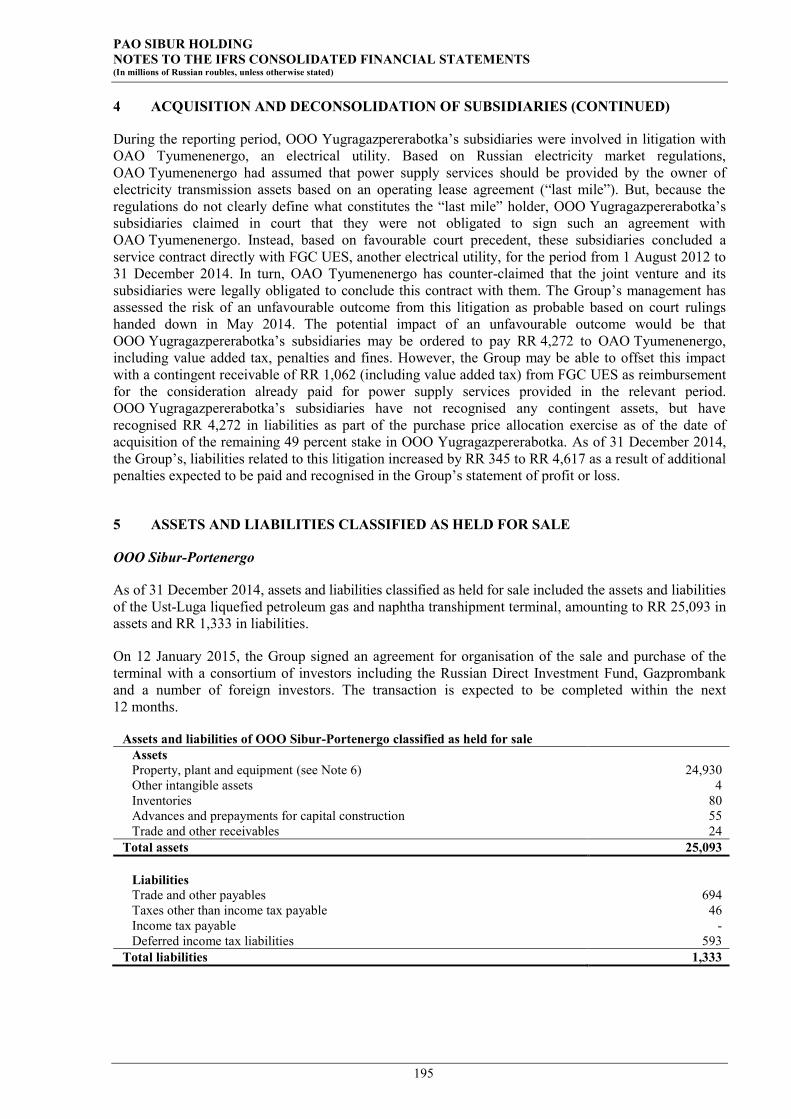

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

02SIBUR 2014 Annual Review

EXCELLENT FINANCIALS

USD 9.4 bln

USD 2.7 bln

revenue

EBITDA

32.2%EBITDA margin(1)

GROWING FEEDSTOCK PROCESSING & PRODUCTION

2.6x

20.1%

PP production y-o-y increase to 395.3 kt

raw NGL fractionation volumes y-o-y increase to 6.3 mt

27.8%LPG production(2)

y-o-y increase to 5.1 mt

SIBUR is Russia’s largest integrated gas processing and petrochemicals company. We are building a strong, internationally competitive and resilient business with unique advantages and opportunities for profitable growth.

We process natural resources in an environmentally sustainable way to produce energy products and petrochemicals demanded by manufacturers to deliver high-quality goods to businesses and consumers. We are a major engine of employment and professional, technological and economic development in the regions and communities where we operate.

SIBUR is building a culture of excellence, integrity and teamwork. We continuously strive to adopt global standards and best practices, recognising that corporate governance, transparency and environmental and social responsibility are the foundations of a successful and sustainable business.

26 production sites in Russia

Over 25,000 employees

Over 1,400 large customersfrom 75 countries representing diverse range of end-customer industries

SIBUR plays a vital role in the country’s economic transformation and the modernisation of its industrial base. In 2014, we completed a major multi-year investment programme to scale our opportunities, drive the benefits of vertical integration and position the Company for its next leg of profitable growth. We have built an integrated value chain that brings together:

Unique feedstock advantages and partnership with oil and gas producers;

An extensive end-to-end transportation network;

World-class gas processing and petrochemicals production facilities;

Access to attractive end markets in Russia and internationally.

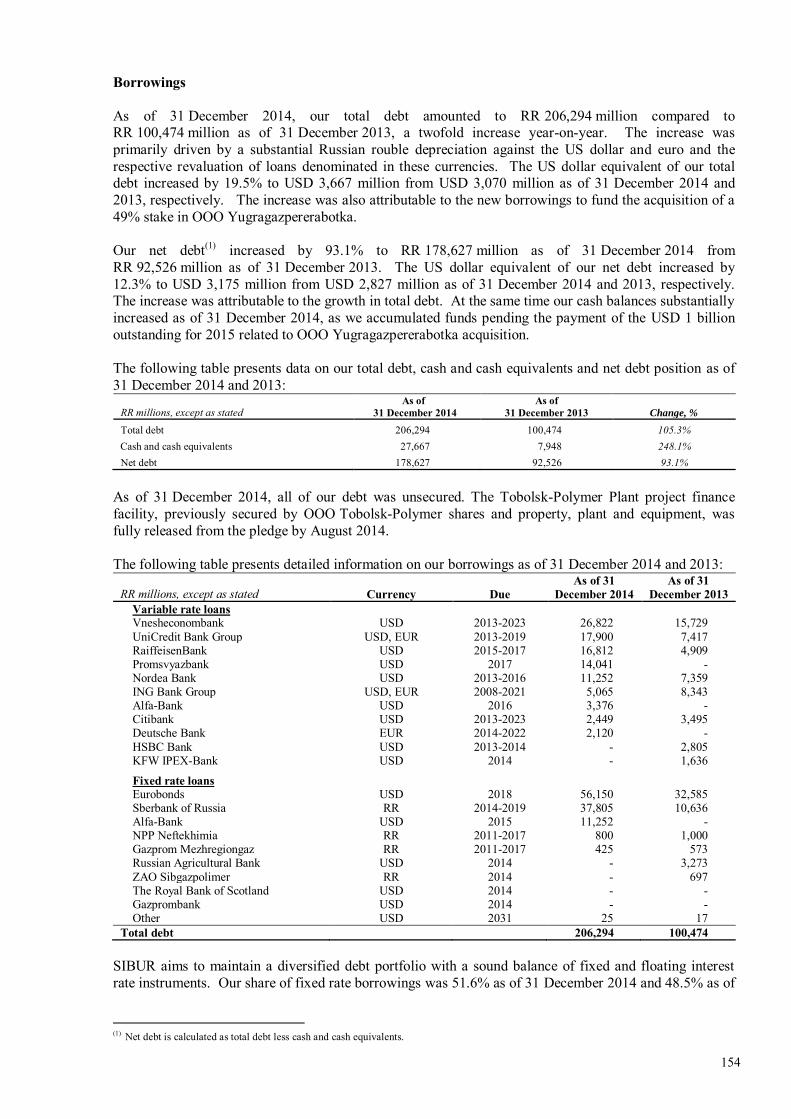

COMFORTABLE DEBT LEVEL

1.19x

1.74x

net debt to EBITDA as of 31 Dec’14(in USD terms)

net debt to EBITDA as of 31 Dec’14(in RR terms)

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.(2) Including production volumes under processing arrangements.

SIBUR in 2014

SIBUR in 2014

03SIBUR 2014 Annual Review

INTRODUCTION

Chairman StatementCEO Letter2014 Highlights

VALUE CHAIN

SIBUR’s Value Chain – From Vision to RealityGeographic FootprintBusiness Model

BUSINESS OVERVIEW

Production FlowsProducts and MarketsFeedstock SourcingTransportation and LogisticsSIBUR Production System

SUSTAINABILITY

Our CommitmentEnvironmentHealth & SafetyEmployeesCommunities and Society

CORPORATE GOVERNANCE

Board of DirectorsBoard CommitteesManagement BoardEquity-Settled Share-Based Payment PlansShare CapitalDividendsRisk Management

FINANCIAL INFORMATION

Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A)IFRS Consolidated Financial Statements

ADDITIONAL INFO

04

060710

14

162628

30

3436545658

60

6263707278

82

87102104

108108109110

118

120

174

REVENUE SPLIT BY PRODUCT

Energy products

Petrochemicals

Other

60%37%3%

1

2

3

2

3

1

REVENUE SPLIT BY MARKET

2

4 53

1

Russia

Europe

Asia

CIS

OtherRevenue from trading operations, ceased in 2015

Revenue from trading operations, ceased in 2015

49%36%8%6%1%

1

2

3

4

5

VERTICALLY INTEGRATED BUSINESS MODEL

Petrochemical products

Intermediates

Plastics & organic synthesis plants

Synthetic rubber plants

Basic polymerplants

Railway loading racks

Steam cracker PDH facility

Transportation infrastructure

PipelinesLPG and naphtha

transshipment facilityRail cars and

tank wagons

Gas processing/fractionation

GPPs

Compressor stations

GFUs

External sourcing of hydrocarbon feedstockWeighted average maturity of our multi-year supply contracts:

16.4 years for APG

17.9 years for NGLs

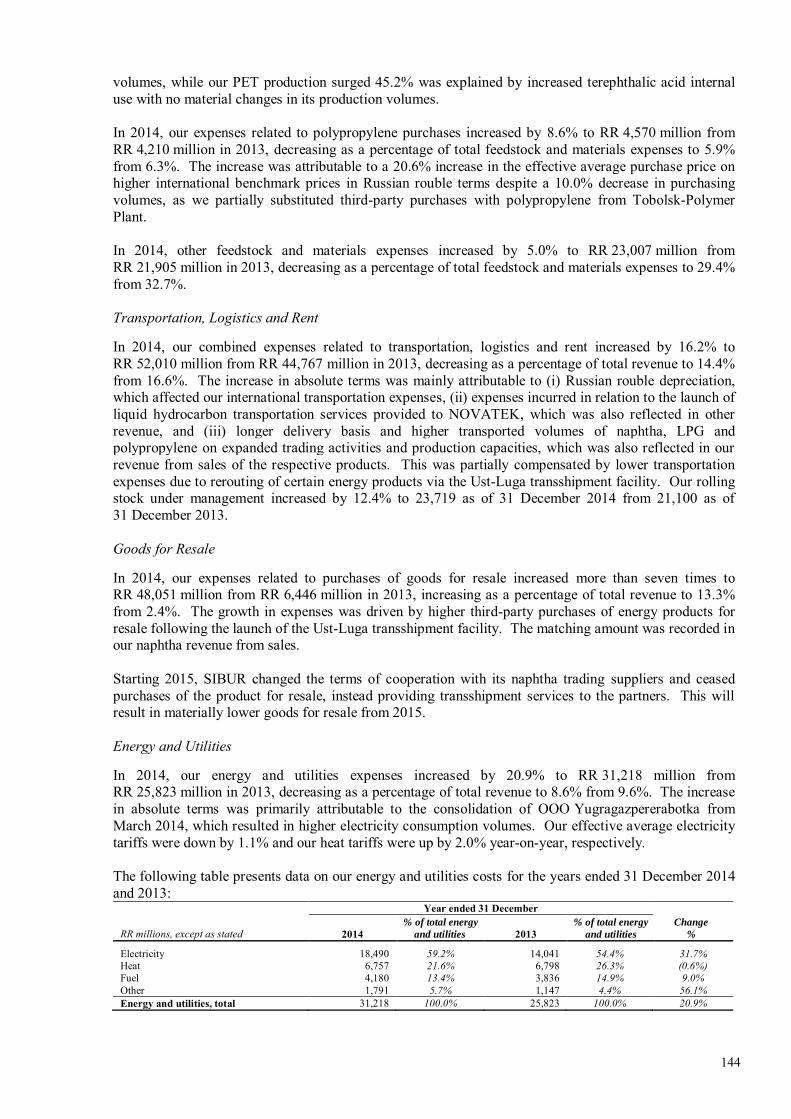

FEEDSTOCK AND ENERGY

EBITDA: USD 2,299 mln

EBITDA margin(1): 41.8%

7 GPPs - 23 bcmpa of APG

3 GFUs - 8 mtpa of raw NGL

2,995 km pipelines

6 railway loading racks

23,719 rail cars and tankwagons

PETROCHEMICALS

EBITDA: USD 542 mlnEBITDA margin: 14.6%

2 basic polymer plants: 875 ktpa3 synthetic rubber plants:573 ktpa13 plastics & organic synthesis plants:1,045 ktpa

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

OUR WEBSITE

http://investors.sibur.com

Oil-based feedstock(APG)

Gas-based feedstock(NGLs)

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

04SIBUR 2014 Annual Review

Introduction

Chairman Statement

CEO Letter

2014 Highlights

Tobolsk-Polymer polypropylene production complex

Content

05SIBUR 2014 Annual Review

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

06SIBUR 2014 Annual Review

Chairman Statement

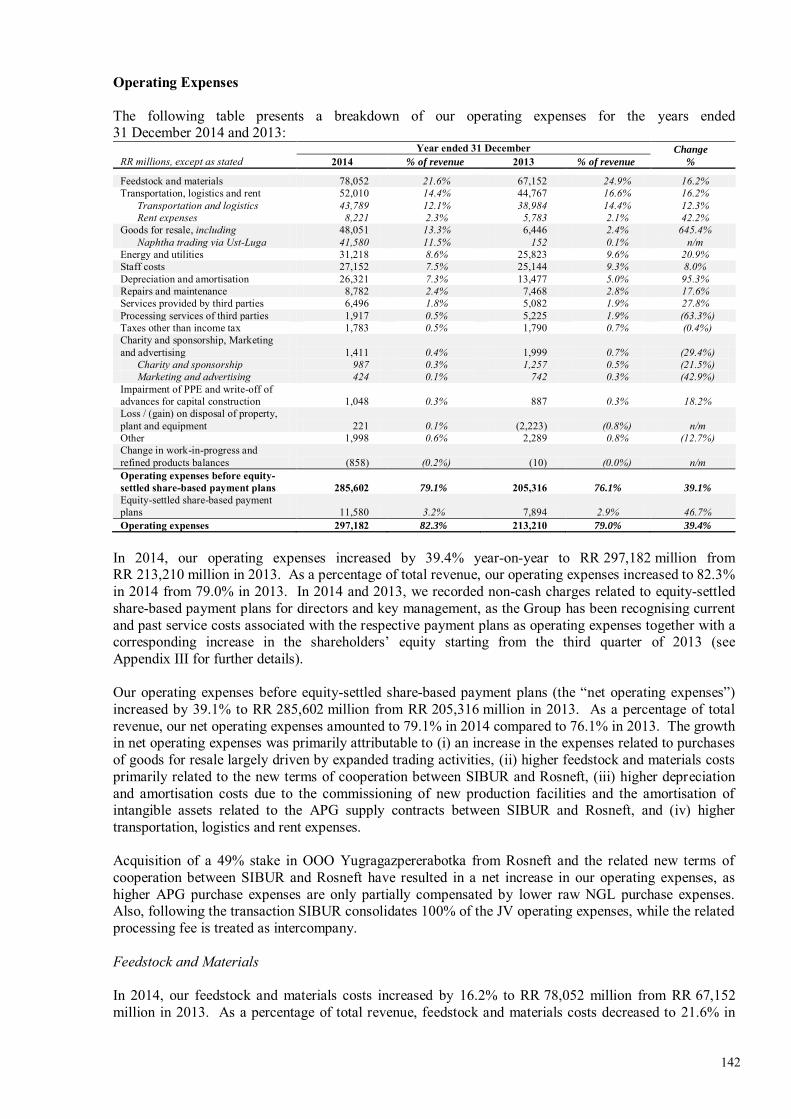

LEONID MIKHELSON

Chairman of the Board of Directors

This was a pivotal year for our strategy to build a world-class integrated gas processing and petrochemicals leader. I am proud to report that we have delivered on all of our key objectives for the multi-year investment cycle completed in 2014 – and the results are evident in our performance.

Our vision for the past several years has been to monetise SIBUR’s most fundamental advantage – access to abundant, attractively priced supplies of Western Siberian feedstock.

Each of our investment projects was conceived as part of a strategic value chain, linking flows of feedstock raw materials to an extensive processing and

transportation infrastructure with the objective of expanding production volumes and profitable growth in domestic and international markets.

This vision is now a reality. The launch and ramp-up of our new pipeline, production and export facilities made possible by the successful completion of strategic projects in 2014 contributed significantly to our growth and profitability. And our increased scale and integration open up large new untapped opportunities for buildingour leadership and generating returns well above the petrochemicals industry average.

Our focus now is to reap the rewards of our investments in 2015 and beyond. The macro environment remains challenging but our performance demonstrates that we have the right business model, the right strategy and that our long-term perspective is paying off.

We also continue to take a longer term view of value creation through increased scale and integration across our business and opportunities to further monetise our feedstock advantage. To that end, in 2014 we approved the ZapSibNeftekhim (ZapSib-2) multi-year investment project to expand petrochemicals production at our world-class integrated complex in Tobolsk.

My number one message is therefore one of optimism and confidence. I would like to thank SIBUR’s management team and employees for delivering strong financial performance and attaining our strategic milestones. We are building a culture of excellence, integrity and teamwork, and are excited about our Company’s opportunities for the future.

Chairman Statement & CEO Letter

07SIBUR 2014 Annual Review

CEO Letter

DMITRY KONOV

CEO and Chairman of the Management Board

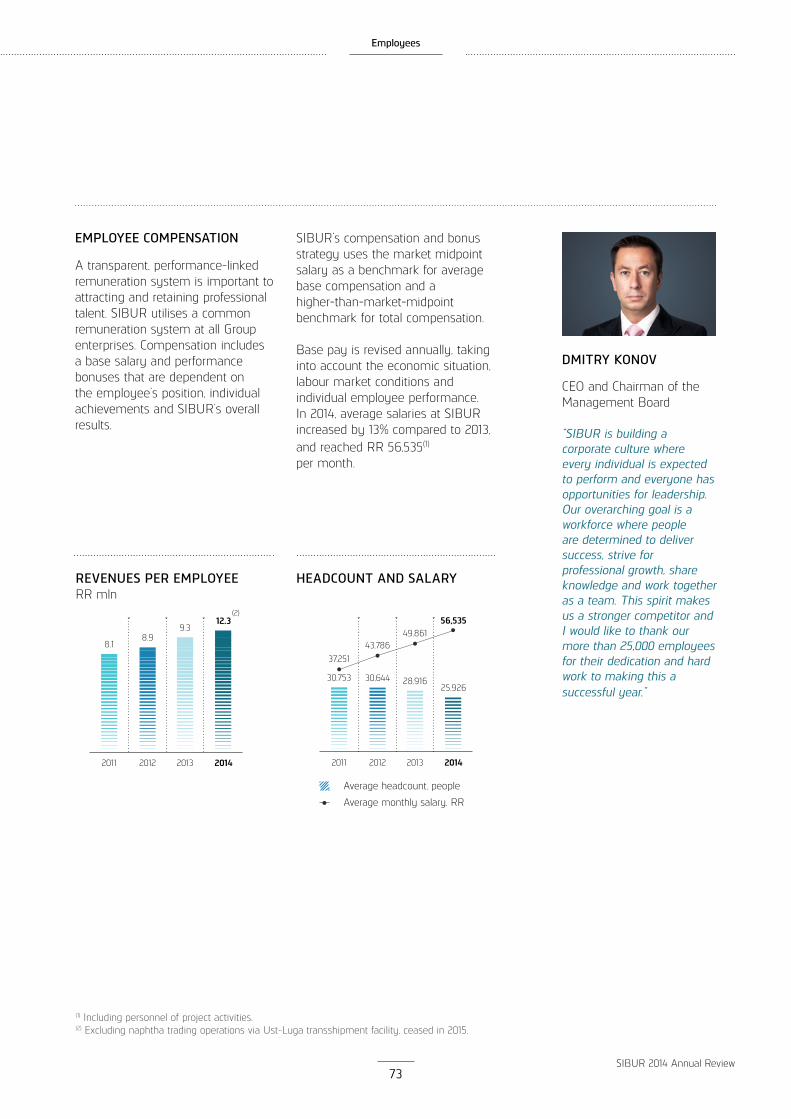

I am pleased to report that SIBUR delivered strong financial performance in 2014 despite a difficult external environment. The arising deterioration of the economic situation in Russia, substantial depreciation of the rouble and a steep decline in global energy prices were a critical test of our endurance.

The perfect storm proved our strategy right. We delivered the Group revenue growth of 34% to RR 361 billion in 2014, or 11% growth in US dollar terms. EBITDA grew by 30% to RR 103 billion, equivalent to an increase of 8% in US dollars. This resulted in an adjusted Group EBITDA margin of 32.2%(1), compared to a 29.2% EBITDA margin in 2013.

SIBUR’s healthy growth and sustained high margins demonstrated the power of our business model in action.

Our increased scale with the ramp-up of new production and transportation infrastructure from completed strategic projects drove our growth. At the same time, SIBUR’s vertically integrated business model enabled us to capture value while offsetting volatility in our key markets.

These trends are evident when looking at our two business segments. In our feedstock and energy business, we vastly increased our capacity to transport and process feedstock and grew LPG exports to newly accessible Western European markets. 2014 was also a breakthrough year for our petrochemicals business, which emerged as an important growth engine for the bottom line thanks to the successful ramp-up of our world-class production complex in Tobolsk.

Looking at SIBUR today, I see a business that is strongly positioned with unique competitive advantages,increasing scale and integration benefits and expanded opportunities for profitable growth. But it is also one that has proven its resilience in bad times. These themes were critical to our success in 2014, and they remain essential elements of our long-term strategy for value creation.

SIBUR’S VALUE CHAIN – FROM VISION TO REALITY

Our multi-year investment programme represents the largest expansion of Russia’s gas processing and petrochemicals infrastructure in decades. Its completion marks a fundamental evolution of our business as we turn to reaping the rewards of these investments. In 2014, SIBUR’s strategy to build an integrated gas processing and petrochemicals leader was validated by our robust financial performance, as the strong results of our expanded petrochemicals business offset the downward pressures on feedstock and energy profitability.

In 2014, we launched the several critical links of our value chain while ramping up commercial operations of other strategic projects that were completed in the previous year. In our feedstock and energy business, this included the opening of the new 1,100 km Purovsk–Pyt-Yakh–Tobolsk pipeline, which provides SIBUR with access to additional available volumes of raw NGL in the northern part of Western Siberia.

(1) Adjusted for low-marginal naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

08SIBUR 2014 Annual Review

The launch was synchronised with the opening of our second gas fractionation unit in Tobolsk, substantially expanding our capacity towards the end of the year.

For 2014 as a whole, SIBUR grew raw NGL feedstock processing volumes by 20%, which enabled a 28% increase in LPG production. These volumes then contributed to an increase in LPG exports to Western Europe through the Ust-Luga transshipment facility, opened in 2013 with the capacity to ship 2.5 million tonnes of light oils and 1.5 million tonnes of LPG per annum in accordance with European Union standards.

We expect continued growth in feedstock and energy production and sales volumes in the coming year as most of the new feedstock supplies and processing capacity came on stream only as of the fourth quarter of 2014. And I would like to underscore that thanks to our integrated Tobolsk complex, this substantial growth in feedstock volumes also powers our growth in petrochemicals.

The strategic progress of our petrochemicals business segment in 2014 was marked by the ramp-up of production at Tobolsk-Polymer, a major new polypropylene production facility with nameplate capacity of 500,000 tonnes per annum. Average capacity load for the year was 53% and utilisation reached 91% in the fourth quarter of 2014. This drove a nearly threefold increase in polypropylene production volumes, with more to come in 2015.

Growth of petrochemicals productionin 2014 also benefited from the launch and commercial ramp-up of several other strategic projects. These included steam cracker upgrade in Kstovo, PET capacity expansion in Blagoveshchensk, new BOPP-films production in Tomsk and Novokuybyshevsk, and SBS production in Voronezh.

EXCELLENCE IN STRATEGIC PROJECT EXECUTION

Our experience in executing strategic projects has resulted in a significant infusion of global best practices and technologies into the Russian market. Our Tobolsk complex is the largest and technologically most advanced project in the Russian petrochemicals industry of the last several years. Its successful launch demonstrated SIBUR’s engineering and project management expertise.

These skills were also on display in the construction and successful launch of the industry’s other major new facility in 2014, the RusVinyl PVC 50/50% joint venture with SolVin Holding Nederland B.V. located in Kstovo, Nizhniy Novgorod region. The new complex comprises a polyvinyl chloride (PVC) plant with an annual capacity of 330,000 of PVC and 225,000 of caustic soda. Feedstock for PVC production at the complex is supplied to the joint venture by SIBUR’s wholly owned steam cracker, which we upgraded to increase ethylene production capacity from 300,000 to 360,000 tonnes per annum.

In September, SIBUR’s Board of Directors approved a major new multi-year project – greenfield construction of the ZapSibNeftekhim(ZapSib-2) ethylene cracking unit and polyolefin production complex within the SIBUR’s Tobolsk petrochemical hub. Project parameters and timelines have been revised to reflect conservative macroeconomic forecasts and meet our financial thresholds. Major contractors were engaged to commence initial stages of construction and we also secured EUR 1.6 billion in committed credit lines for equipment purchases. Our team’s experience and know-how in executing large-scale projects like Tobolsk-Polymer and RusVinyl reinforces our confidence in proceeding with ZapSib-2.

PARTNERSHIP WITH OIL & GAS COMPANIES

Our partnership with major Russianoil and gas producers gives us significant competitive advantages to support our global growth strategy and ability to generate strong financial returns. We have continued to strengthen SIBUR’s access to feedstock through long-term supply contracts with our partners. At the end of 2014, feedstock contracts had weighted average maturities of more than 16 years for APG and nearly 18 years for NGLs.

In March 2014, we revised our format and terms of cooperation with Rosneft with a new agreement that delivers value and efficiency benefits for both companies.

CEO Letter(continued)

CEO Letter

09SIBUR 2014 Annual Review

SIBUR purchased Rosneft’s 49% stake in the Yugragazpererabotka joint venture, giving us full control of its gas processing plants in exchange for commitments by SIBUR to process APG from Rosneft fields and guaranteed supply of APG feedstock to SIBUR through 2032.

I want to underscore SIBUR’s positive impact across the oil and gas industry as a whole. Our extensive infrastructure gives our partners an efficient solution for handling feedstock by-products of oil and gas extraction and an environmentally beneficial alternative to on-field flaring. By processing APG into energy products and petrochemicals, SIBUR enables its partners to earn cash while preventing the release of nearly seven million tonnes of harmful emissions into the atmosphere.

ENVIRONMENTAL AND SOCIAL RESPONSIBILITY

Our goal is not just to operate as a responsible business and reduce risk, but to foster innovation, create a culture of excellence, and deliver benefits for employees, surrounding communities and business partners. A key focus of our modernisation programme has been to drive major improvements in environmental and safety performance.

At each of our production facilities,we have been implementing annualand long-term environmental protection programmes in order to reduce the impact of our operations. Replacement of obsolete equipment and infrastructure and our investments in world-class production facilities and environmental technologies has contributed to substantial improvements in water, air, waste and energy metrics as reported in the Sustainability section of this Annual Review.

We are building a culture where the safety of our employees and communities is everyone’s business. I am proud to say that we had zero fatalities or industrial accidents in 2014. Modern facilities and a focus on continuous improvement and training are prerequisites for delivering on our company-wide commitment to health and safety.

SIBUR is also building a corporate culture where every individual is expected to perform and everyone has opportunities for leadership. Our overarching goal is a workforce where people are determined to deliver success, strive for professional growth, share knowledge and work together as a team. This spirit makes us a stronger competitor and I would like to thank our more than 25,000 employees for their dedication and hard work to make this a successful year.

SIBUR’S NEXT LEG OF GROWTH

SIBUR’s strategy was validated by our strong financial performance last year. The notable trend was increased scale and integration across our business with growth opportunities for our feedstock and energy business coming on stream towards the end of the year and the emergence of petrochemicals as a powerful growth engine for the bottom line.

These achievements have set the stage for continued progress as we reap the gains of our investments during 2015. Looking to the future, we operate in cyclical commoditiesmarkets and are not immune to external shocks, to be sure, but 2014 results demonstrate we are building a more durable and valuable enterprise. With the completion of our investment cycle, our objective is to generate more value from our unique assets and deliver on SIBUR’s next leg of growth.

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

10SIBUR 2014 Annual Review

2014 Highlights

SIBUR’S STRATEGY WAS VALIDATED BY OUR STRONG FINANCIAL PERFORMANCE THIS YEAR.

(1) Adjusted for foreign exchange loss due to the rouble depreciation and the respective revaluation of liabilities, gains on consolidation and deconsolidation of Yugragazpererabotka, and charges related to the equity-settled share-based payment plans.

(2) Source: Russian Federal State Statistics Service, Eurostat, National Bureau of Statistics of the People’s Republic of China.

adjusted profit(1) y-o-y increase

The notable trend was increased scale and integration across our Company with growth opportunities for our feedstock and energy business coming on stream towards the end of the year and the emergence of petrochemicals as a powerful growth engine for the bottom line.

MACRO ENVIRONMENT

In 2014, the macroeconomic environment substantially deteriorated on the back of the sharp decline in oil prices and the significant depreciation of the Russian rouble. The slowdown in the Russian economy continued, with GDP growth of 0.6%(2) compared to 1.3%(2) in 2013 according to government statistics, while consumer and producer price inflation rates nearly doubled year-on-year. Growth in our two main export markets was mixed, with European Union GDP improving but sluggish at 1.2%(2) and China’s economy slowing to a 7.4%(2)

growth rate.

SIBUR also experienced a declining price environment for most of its products. Global oil shocks triggered average energy product price declines in the high single digits to low double digits year-on-year depending on the product.

We benefited from higher natural gas selling prices in Russia due to the 7.4% year-on-year average indexation of regulated prices. In our petrochemicals business, prices for synthetic rubbers and plastics & organic synthesis products experienced sharp double digit declines, while prices for basic polymers were essentially flat.

In this environment SIBUR’s financial results were supported by the depreciation of Russian rouble. The rouble weakened relative to the US dollar by 20.6% on average over the course of 2014 and by 71.9% at the December year-end. Since SIBUR generally earns revenues from commodities priced in US dollars based on international benchmarks, while its operating costs are largely denominated in roubles, our underlying business performance largely benefited from rouble depreciation in 2014.

2014 FINANCIAL PERFORMANCE

Against this negative backdrop, SIBUR delivered strong financial performance in 2014. Group revenue increased 33.8% to RR 361 billion, or 10.9% growth in US dollar terms. If adjusted for the discontinued in 2015 low-marginal naphtha trading operations, total Group revenue increased 18.4% in Russian rouble terms.

30.3%

8.0%

EBITDA y-o-y increase in roubles

EBITDA y-o-y increase in US dollars

26.5%

2014 Highlights

11SIBUR 2014 Annual Review

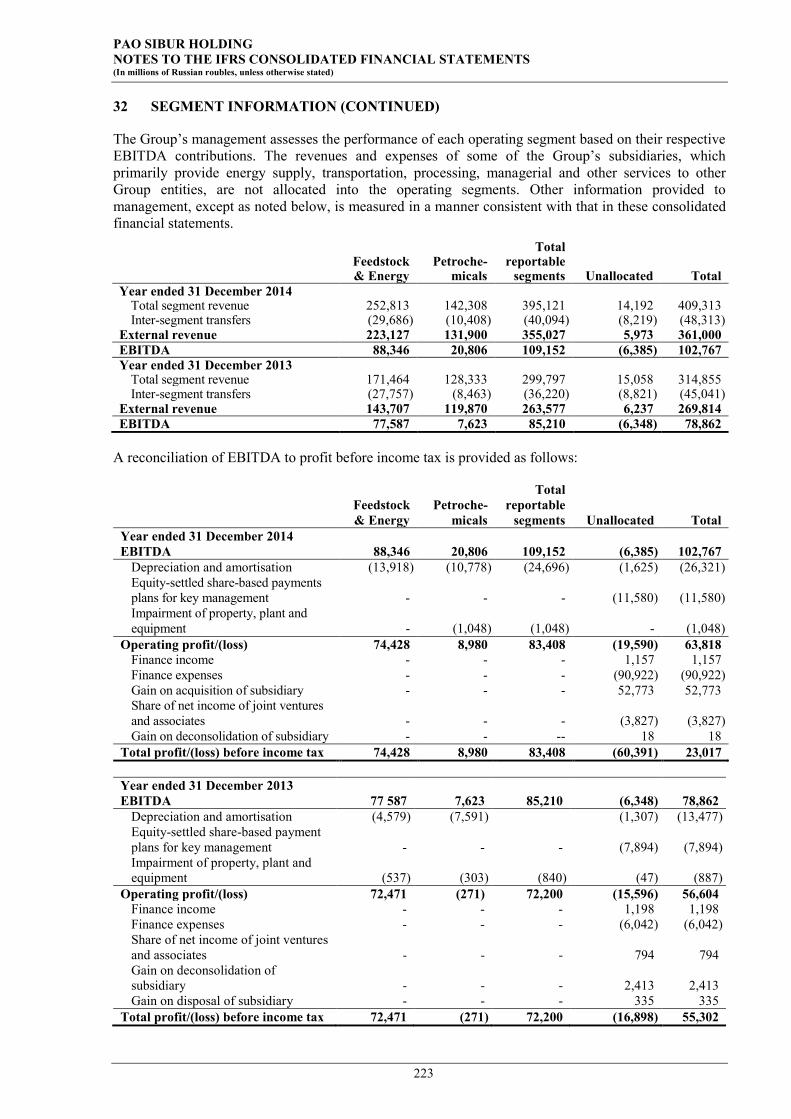

EBITDA grew by 30.3% to RR 103 billion – the highest score in SIBUR history. This is an equivalent to a healthy increase of 8.0% in US dollars, which was driven by threefold growth in the EBITDA of our petrochemicals segment, as well as the higher contribution of our feedstock & energy segment.

This resulted in a total Group EBITDA margin of 28.5% in 2014, or 32.2% adjusted to exclude naphtha trading activities discontinued in 2015, compared to a 29.2% EBITDA margin in 2013.

SIBUR’s revenue and EBITDA growth in rouble terms benefited from the depreciation of the rouble in 2014. At the level of net profit,however, we recorded a 44.8% decrease year-on-year due to foreign exchange effects under IFRS reporting in Russian roubles. In particular, we recorded RR 85.4 billion in foreign exchange loss due to the revaluation of our liabilities primarily denominated in US dollars to match the currency structure of our revenues. Net of one-off non-cash factors(1) our net profit increased 26.5% to RR 69.3 billion.

FEEDSTOCK AND ENERGY SEGMENT

Our feedstock and energy segment remained by far the largest contributor to overall performance. Segment gross revenue grew by 47.4% to RR 253 billion. If adjusted for the low-marginal naphtha trading operations discontinued in 2015, segment revenue increased by 23.2%.

Growth was driven by a number of factors including higher hydrocarbonfeedstock processing volumes, as well as higher natural gas sales volumes due to the full consolidationof Yugragazpererabotka as of March 2014. In 2014, we processed 20.8(2)

billion cubic metres of APG, an increase of 6.3%(2) year-on-year. We also launched an expanded and upgraded integrated feedstock processing and transportation infrastructure in Western Siberia. This enabled a 20.1%(3) increase in raw NGL fractionation volumes to 6.3(3) million tonnes. These factors drove an increase in external sales volumes of LPG of 16.2% to 3.5 million tonnes and of natural gas sales volume of 35.2% year-on-year to 16.0 billion cubic metres.

Profitability, however, was impacted by lower energy product prices in US dollars. Feedstock and energy EBITDA increased 13.9% to RR 88.3 billion, but EBITDA margin declined from 45.2% in 2013 to 41.8%(4) in 2014.

(1) Foreign exchange loss due to the rouble depreciation and the respective revaluation of liabilities, gains on consolidation and deconsolidation ofYugragazpererabotka, and charges related to the equity-settled share-based payment plans.

(2) Including Rosneft’s share in processing volumes of Yugragazpererabotka in 2013 and the first quarter 2014.(3) Including fractionation volumes under processing arrangements. Approach to the treatment of raw NGL production and fractionation volumes at

Nyagan GPP was changed following the acquisition of control in Yugragazpererabotka in March 2014.(4) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

13.9%

41.8%

20.1%

feedstock & energy segmentEBITDA y-o-y increase

feedstock & energy segmentEBITDA margin(4)

raw NGL fractionation volumes(3)

y-o-y increase to 6.3 mt

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

12SIBUR 2014 Annual Review

2014 Highlights2014 Highlights(continued)

PETROCHEMICALS SEGMENT

Petrochemicals gross segment revenue grew 10.9% year-on-year to RR 142.3 billion, while EBITDA nearly tripled to RR 20.8 billion and EBITDA margin improved from 5.9% in 2013 to 14.6% in 2014.

The main drivers were strong growth in volumes and sales from our expanded production capacity – which took market share in Russia by displacing more expensive imports. This strong performance was achieved despite a tough environment for synthetic rubbers, plastics and organic synthesis products and flat prices for polymers.

In particular, petrochemicals products sales volumes increased 5.6% to 2.2 million tonnes. This was achieved thanks to a nearly threefold increase in polypropylene production to 395,309 tonnes due to the ramp-up of Tobolsk-Polymer. Plastics & organic synthesis sales volumes increased 2.4%, benefiting from capacity expansions including a 45.2% increase in PET production to 279,920 tonnes and BOPP-film production growth of 25.6% to 120,386 tonnes. In intermediates, we began to supply ethylene to our RusVinyl joint venture, which we expect to become a reliable source of cash flow. However, these increases were offset by declines in glycols production due to extended shutdowns, and the divestment of Plastic and PVC cable compounds production. In addition, synthetic rubber sales volumes declined 16.3% to 360,038 tonnes due to challenging market conditions.

2.7X

14.6%

5.6%

petrochemicals segment EBITDA y-o-y increase

petrochemicals segment EBITDA margin

petrochemicals sales volumes y-o-y increase to 2.2 mt

2014 Highlights

13SIBUR 2014 Annual Review

Importantly, declining prices for our feedstock and energy products also resulted in lower input costs for our petrochemicals segment. This was one of the key drivers of petrochemicals EBITDA performance and provides a clear demonstration of the benefits of vertical integration.

FINANCIAL STRENGTH

SIBUR was strongly cash generative in 2014. Cash from operations increased 25.2% to RR 91.1 billion, equivalent to a 3.8% increase in US dollar terms. Before working capital changes, operating cash flow increased 35.2% year-on-year. Meanwhile capital expenditures decreased 3.3% to RR 67.7 billion as the result of completion of large-scale projects.

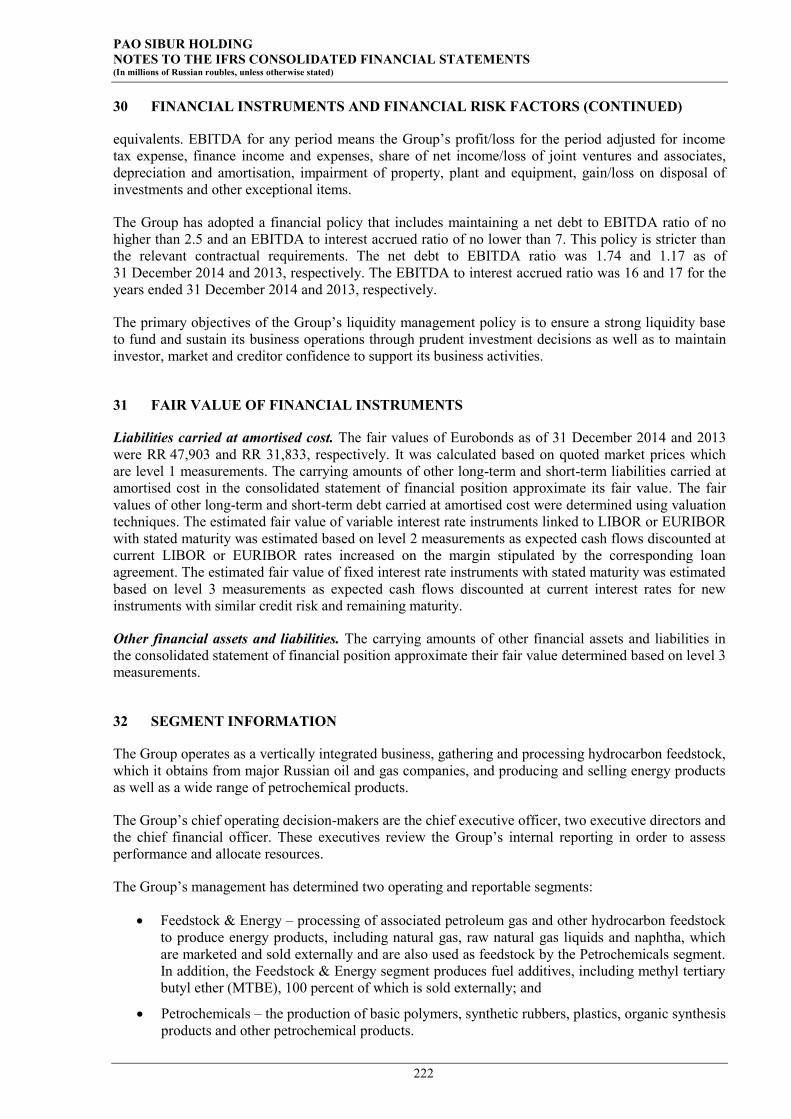

Debt reported on our balance sheet at 31 December 2014 was inflated by rouble depreciation effects. This resulted in a 93.1% increase in net debt to RR 178.6 billion and a net debt to EBITDA ratio of 1.74x compared to 1.17x as of 2013 year-end under IFRS reporting.

Looked at in US dollar terms, SIBUR’s net debt to EBITDA would have been 1.19x as of 2014 year-end, or virtually identical to our leverage ratio a year earlier. We believe this offers a truer picture of our financial position, since we generate EBITDA mainly based on products priced in US dollars, and in addition, a large portion of the Group’s debt is also US dollar-denominated.

The levels reported on the Group’s balance sheet remain well within the limits set by our financial policy. Our strong cash flow from operating activities, declining capital expenditures in US dollar terms and new EUR 1.6 billion line of credit for construction of ZapSibNeftekhim (ZapSib-2) make clear SIBUR’s financial strength.

Please refer to the Management’s Discussion and Analysis and Financial Statements sections of this Annual Review for detailed information on SIBUR’s 2014 performance.

25.2%operating cash flow

y-o-y increase

1.19x

net debt to EBITDA as of 31 Dec’14(in USD terms)

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

14SIBUR 2014 Annual Review

Value Chain

SIBUR’s Value Chain – From Vision to Reality

Geographic Footprint

Business Model

Voronezhsintezkauchuk

Content

15SIBUR 2014 Annual Review

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

16SIBUR 2014 Annual Review

From Vision to Reality SIBUR’s Value Chain

SIBUR’S VISION OVER THE PAST SEVERAL YEARS HAS BEEN TO SCALE OUR OPPORTUNITIES AND BUILD A VALUE CHAIN THAT

BRINGS TOGETHER FOUR KEY ELEMENTS:

THAT VISION IS NOW A REALITY.

Unique feedstock advantages

Extensive end-to-end transportation network

World-class gas processing and petrochemical facilities

Growth in attractive end markets

Over the past six years, we have invested RR 337 billion to build the key components of this integrated whole, and we are proud to say we delivered on all of our commitments. This section of our Annual Review discusses how we will reap the benefits of these investments to position SIBUR as a strong, fast-growing and resilient company.

As we drive near-term performance, we are also focused on longer term opportunities. To that end, SIBUR’s Board of Directors approved a major new multi-year project – the construction of the ZapSibNeftekhim (ZapSib-2) petrochemical facility at our flagship Tobolsk complex – to further monetise our feedstock advantage, leverage the benefits of our scale and integration, and sustain our opportunities for leadership and growth.

2014 has been a transformative year for SIBUR. The successful completion of our multi-year investment programme marks a fundamental evolution of our business and the beginning of our next leg of growth.

With the launch of several major strategic assets we have attained an important milestone in building an integrated value chain that over the coming years will enable:

Unmatched competitive advantages and growth opportunities in Russia and globally;

Expanded access to supplies of abundant, attractively priced feedstock from new sources in Western Siberia as the basic raw material for growing our business;

Significantly increased processing and production capacity to drive growth of production volumes and sales of energy and petrochemical products in both domestic and export markets;

Extensive infrastructure that provides major economies of scale and barriers to entry and positions SIBUR among the lowest cost operators in the world;

A balanced, flexible business able to generate financial returns well above the global petrochemicals industry average.

1

2

3

4

From Vision to Reality - SIBUR’s Value Chain

17SIBUR 2014 Annual Review

2. Extensive, upgraded transportation infrastructure to enable increased flows

Purovsk – Pyt-Yakh – Tobolsk pipeline with up to 8 mtpa annual capacity opened as part of upgraded 2,995 km pipeline network to increase feedstock flows to Tobolsk;

Ramp up of new Ust-Luga transshipment facility with capacity of 1.5 mpta of LPG and 2.5 mpta of light oils for growth of higher margin exports to European markets.

3. World-сlass Tobolsk integrated energy product and petrochemicals complex

Second GFU nearly doubles raw NGL processing capacity to enable vast increases in production of LPG for export growth and a feedstock for petrochemicals growth;

Launch of Tobolsk-Polymer, largest polypropylene complex in Russia, CIS and Eastern Europe, with annual capacity of 500,000 tonnes driving major growth in production;

Decision to proceed with ZapSibNeftekhim (ZapSib-2) greenfield ethylene, polyethylene and polypropylene production site in Tobolsk as part of longer term growth strategy.

4. Opportunities for growth and leadership in attractive end markets

Over 1,400 large customers from 75 countries in a wide range of industries;

Increased opportunities for higher margin exports of energy products and growth as a globally cost-competitive petrochemicals producer;

Growing share of the Russian domestic marketplace driven by import substitution and projected growth in consumption.

1. Access to abundant, attractively priced feedstock stranded in Western Siberia

Long-term supply contracts with the major Russian oil and gas producers for APG and NGLs feedstock;

Ability to monetise abundant new sources of raw NGL feedstock in northern parts of Western Siberia through newly launched transportation and processing infrastructure.

THE COMPLETION OF OUR MULTI-YEAR INVESTMENT CYCLE AND COMMERCIAL RAMP-UP OF STRATEGIC PROJECTS IN 2014

CREATES A POWERFUL INTEGRATED PLATFORM FOR MONETISING SIBUR’S ADVANTAGES.

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

18SIBUR 2014 Annual Review

From Vision to Reality SIBUR’s Value Chain (continued)

1. Access to abundant, attractively priced feedstock stranded in Western Siberia

Our vision for the past several years has been to monetise SIBUR’s most fundamental advantage – access to abundant, attractively priced supplies of Western Siberian feedstock – as the basis for growing our energy products and petrochemicals business. We have invested in the most extensive infrastructure for transporting and processing APG and NGLs feedstock to secure this access and make SIBUR an essential partner for the major Russian oil and gas producers.

Western Siberia has abundant sources of hydrocarbon by-products of the oil and gas extraction process that are difficult for energy companies to use commercially and are thus effectively stranded in the region.

SIBUR has multi-year contracts with oil and gas partners to take these raw materials to produce energy products and petrochemicals. In addition to the cash they generate from supplying feedstock to SIBUR, processing of APG provides our partners with an alternative solution to harmful on-field flaring. In 2014, this prevented the release of more than seven million tonnes of pollutants into the atmosphere.

We continued to cement our long-term access to feedstock in 2014 by agreeing on a new format and terms of cooperation with Rosneft. SIBUR acquired from Rosneft a 49% interest in the joint venture Yugragazpererabotka to gain full ownership of its gas processing plants.

New contracts with an extended tenor through the end of 2032 were signed for APG supplies from Rosneft’s fields with guaranteed supply volumes of approximately 10 billion cubic metres per annum, and natural gas sales from the GPPs to Rosneft.

In addition, SIBUR captured major new flows of raw NGL feedstock from wet gas production in northern parts of Western Siberia in 2014 with the opening of new pipeline and processing capacity.

From Vision to Reality - SIBUR’s Value Chain

19SIBUR 2014 Annual Review

2014 KEY FACTS(1)

(1) As of 31 December 2014.(2) Including fractionation volumes under processing arrangements.

APG NGLs

Purovsk - Pyt-Yakh - Tobolsk raw NGL pipeline

7

20.8 bcm

GPPs

processed volumes

6.3 mt

raw NGL fractionated volumes(2)

Key suppliers:

Key suppliers:

92%

16.4 years

weighted average maturity of our multi-year APG supply contracts

Rosneft, Gazprom neft, RussNeft, LUKOIL

NOVATEK, Gazprom, LUKOIL

of our planned APG supplies for 2015 guaranteed under multi-year

supply contracts

17.9 YEARS

80%

weighted average maturity of our multi-year NGLs supply contracts

of our planned NGLs supplies for 2015 guaranteed under multi-year

supply contracts

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

20SIBUR 2014 Annual Review

From Vision to Reality SIBUR’s Value Chain (continued)

2. Extensive, upgraded transportation infrastructure to enable increased flows

SIBUR operates the largest and most extensive feedstock transportation and processing infrastructure in Western Siberia. This gives us unmatched economies of scale and competitive barriers to entry. We operate 7 of the region’s 9 gas processing plants and our network includes thousands of kilometers of pipelines as well as railway facilities, loading racks and rolling stock needed to bring raw materials to our production facilities and products to end markets.

In 2014, we completed major enhancements to support the growth of our energy products and petrochemicals businesses. Most significant is the 1,100 kilometre Purovsk – Pyt-Yakh – Tobolsk pipeline opened in 2014. Built to coincide with major expansions of production capacity at our Tobolsk complex, the pipeline physically links Tobolsk with supplies of raw NGL feedstock that have risen significantly due to the growth in wet gas production in the northern regions of Western Siberia.

Transportation infrastructure opened in the past two years enabled increased production volumes and flows to end markets. In particular, our Ust-Luga transshipment facility, opened in 2013 with the capacity to ship 2.5 million tonnes of light oils and 1.5 million tonnes of LPG per annum in accordance with European Union standards accommodated a significant increase in exports to Western Europe made possible by the 28% growth in LPG production.

From Vision to Reality - SIBUR’s Value Chain

21SIBUR 2014 Annual Review

2014 KEY FACTS(1)

(1) As of 31 December 2014.

Ust-Luga transshipment facility

62,995 km

pipeline network for APG, natural gas and raw NGL supplies

railway loading racks

23,719rail cars and tank wagons under

management

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

22SIBUR 2014 Annual Review

From Vision to Reality SIBUR’s Value Chain (continued)

3. World-Class Tobolsk integrated energy product and petrochemicals complex

In 2014, we completed and operationalised a number of strategic projects in our feedstock and energy and petrochemicals business segments. Taken together, they will enable us to deliver on our objectives for monetising SIBUR’s feedstock advantage, increasing production volumes and sales, and building a balanced business that is optimally positioned for profitable growth and resilience in global commodities markets.

Our flagship Tobolsk production complex brings together large-scale facilities equipped with the latest technologies and the efficiencies of integrated production and management systems. We have flexibility to shift our production mix between and within each of our business segments based on changing market conditions, price volatility and demand growth in key end markets and products. In short, we can increasingly manage our business as one integrated whole.

This year we completed a major expansion of feedstock processing capacity with the opening of our second gas fractionation unit. This will enable a 75% increase in fractionation of raw NGL supplies in Tobolsk to 6.6 million tonnes per annum that supports significant increase in LPG production, as well as further processing of NGLs into petrochemicals products.

To that end, we ramped up commercial operations at our world-class petrochemicals complex, Tobolsk-Polymer, launched at the end of 2013 with 500,000 tonnes of polypropylene production capacity. The nearly threefold increase in polypropylene sales and petrochemicals segment EBITDA in 2014 are encouraging signs that validate our vertically integrated business model and strategy to build a globally cost-competitive petrochemicals leader.

Growth of petrochemicals production also benefited from the launch and commercial ramp-up of several other strategic projects. These included PET capacity expansion in Blagoveshchensk, new BOPP-films production in Tomsk and Novokuybyshevsk, SBS thermoplastic elastomers production in Voronezh, and opening of the RusVinyl PVC joint venture integrated with the expanded cracking capacity in Kstovo – which increases SIBUR’s revenue from ethylene sales to our JV.

At the end of the year, SIBUR’s Board also approved construction of the ZapSibNeftekhim (ZapSib-2) ethylene cracking unit and polyolefin production facility. This multi-year greenfield project will further leverage our feedstock advantage and integrated production efficiencies of our Tobolsk complex.

From Vision to Reality - SIBUR’s Value Chain

23SIBUR 2014 Annual Review

2014 KEY FACTS

(1) Including production volumes under processing arrangements.

27.8% 2.6x

25.6%

LPG production y-o-y increase to 5.1 mt(1)

PP production y-o-y increase to 395.3 kt

First ethylene supplies

from steam cracker facility in Kstovo to RusVinyl

5.6%petrochemicals products sales

volumes y-o-y increase to 2.2 mt

45.2%PET production

y-o-y increase to 279.9 ktBOPP-film production

y-o-y increase to 120.4 kt

Tobolsk-Polymer polypropylene production complex

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

24SIBUR 2014 Annual Review

From Vision to Reality SIBUR’s Value Chain (continued)

4. Opportunities for growth and leadership in attractive end markets

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.(2) Source: IHS, Market Report, IISPR.

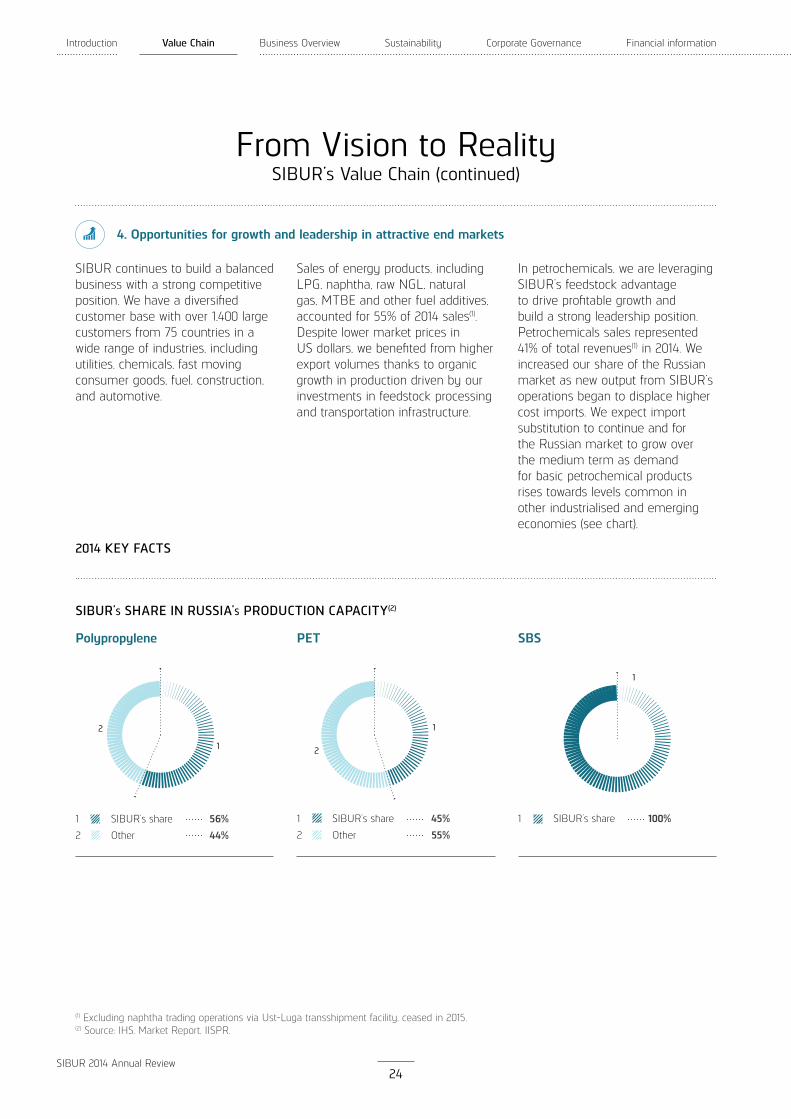

SIBUR continues to build a balanced business with a strong competitive position. We have a diversified customer base with over 1,400 large customers from 75 countries in a wide range of industries, including utilities, chemicals, fast moving consumer goods, fuel, construction, and automotive.

In petrochemicals, we are leveraging SIBUR’s feedstock advantage to drive profitable growth and build a strong leadership position. Petrochemicals sales represented 41% of total revenues(1) in 2014. We increased our share of the Russian market as new output from SIBUR’s operations began to displace higher cost imports. We expect import substitution to continue and for the Russian market to grow over the medium term as demand for basic petrochemical products rises towards levels common in other industrialised and emerging economies (see chart).

Sales of energy products, including LPG, naphtha, raw NGL, natural gas, MTBE and other fuel additives, accounted for 55% of 2014 sales(1). Despite lower market prices in US dollars, we benefited from higher export volumes thanks to organic growth in production driven by our investments in feedstock processing and transportation infrastructure.

SIBUR’s share1SIBUR’s share

Other

1

2

PET Polypropylene SBS

SIBUR’S SHARE IN RUSSIA’S PRODUCTION CAPACITY

2

1

1

SIBUR’s share

Other

1

2

2

1

From Vision to Reality - SIBUR’s Value Chain

25SIBUR 2014 Annual Review

2014 KEY FACTS(1)

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.(2) Source: IHS.

RUSSIA’S CONSUMPTION GROWTH OUTLOOK, CAGR 2013-2020(2)

9.7%

4.1%

4.9%

5.0%

2.4%

1.5%

3.1%

3.7%

MEG

IIR

PVC

LLDPE

PET

LDPE

HDPE

PP

EPS 3.9%

2

34 5

1

GEOGRAPHIC BALANCE (REVENUE SPLIT(1))

Russia

Europe

Asia

CIS

Other

55%28%9%7%1%

1

2

3

4

5

2

3

4

5

87

61

DIVERSE END-MARKETS (REVENUE SPLIT(1))

Utilities

Chemicals

FMCG

Traders

Fuels

Construction

Automotive

Other

21%20%15%13%12%6%6%7%

1

2

3

4

5

6

7

8

over1,400

75 countries

wide range of industries

number of large customers

customer base

utilities, chemicals, fast moving consumer goods, fuel, construction,

and automotive

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

26SIBUR 2014 Annual Review

One Integrated Value ChainGeographic Footprint

Capturing growing domestic marketplace through import substitution

Increased scale and integration of gas processing and petrochemicalsbusinesses

Belgium

Sweden

Poland

Turkey

external sales

Strengthened access to abundant,low-cost feedstock stranded inWestern Siberia through longtermcooperation with oil & gas companies

oil & gasfields

feedstock flows

Extensive upgraded transportation infrastructure supporting increased feedstock volumes and growing export sales of energy products

transshipmentfacility

railway loadingrack

raw NGLpipeline

GPP

GFU

compressorstation

cracker

PDH

petrochemicalsproduction

(1) Based on 2014 numbers. Calculations exclude naphtha trading operations, ceased in 2015. Sales to other geographies totaled 1% in 2014.

Belarus

Finland

4 SALES & MARKETS3 PROCESSING & PRODUCTION

1 FEEDSTOCK SOURCING

4

2 TRANSPORTATION INFRASTRUCTURE

ILLUSTRATIVE

Sales distribution(1):

Russia: 55%Europe: 28%Asia: 9% CIS: 7%

Ukraine

Moscow

Netherlands

Geographic Footprint

27SIBUR 2014 Annual Review

India

China

Kazakhstan

South Korea

APG sourcing

Raw NGL sourcing

APG sourcing

SIBUR PETROCHEMICALSHUB IN TOBOLSK

INVESTMENT PROGRAMME2009 – 2014

Total

Other35

Petrochemicalsproduction

Feedstock processing

199

Transportationinfrastructure

103

337

RUSSIAN FEDERATION

2 3

1 2 3

Moscow

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

28SIBUR 2014 Annual Review

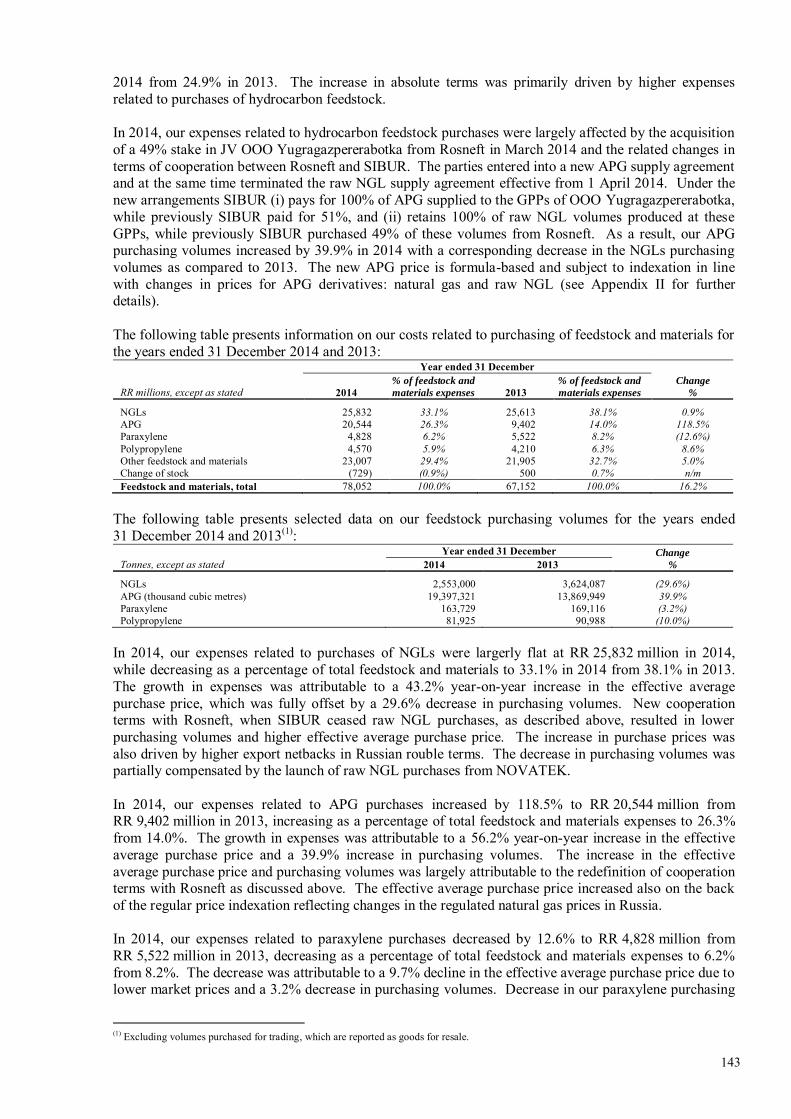

One Integrated Value ChainBusiness Model(1)

FEEDSTOCK SOURCING

For more information on feedstock sourcing refer to Feedstock Sourcing in Business Overview (pp. 54-55)

APGStranded APG purchased from oil companies processed by SIBUR’s GPPs to produce natural gas and raw NGL

Raw NGLRaw NGL producedinternally or purchased from oil & gas companies fractionated at SIBUR GFUs into LPG and naphtha

NaphthaLPG and naphtha produced internally or purchased from oil & gas companies as petrochemical feedstock

Methanol & otherMTBE produced from reaction of methanol with isobutylene as an additive to gasoline

IntermediatesIntermediates polymerised or otherwise processed into higher value-added petrochemical products

LPG, naphtha and raw NGL processed at SIBUR’s crackers / PDH facility into a wide range of intermediate petrochemical products

LPG

PROCESSING & PRODUCTION

For more information on capacities refer to Products and Markets in Business Overview (pp. 39, 47, 49, 51, 53). For more information on production flows refer to Production Flows in Business Overview (pp. 34-35)

PETR

OCH

EMIC

ALS

FEED

STO

CK A

ND

EN

ERGY Oil

companies

Gas companies

Gas processing (GPPs)

18%

82% 52%

NGLs for petrochemicals 30%

Gas fractionation (GFUs)

Cracking/ dehydrogenation/ other chemical processing

40%

20%

1 2 3

(1) Based on 2014 numbers. Calculations exclude naphtha trading operations, ceased in 2015.

External feedstock purchasesInternal feedstock flowsExternal sales

Business Model

29SIBUR 2014 Annual Review

ILLUSTRATIVE

PROCESSING & PRODUCTION

For more information on capacities refer to Products and Markets in Business Overview (pp. 39, 47, 49, 51, 53). For more information on production flows refer to Production Flows in Business Overview (pp. 34-35)

SALES & MARKETS

For more information on products and sales refer to Products and Markets in Business Overview (pp. 36-53)

Natural gas

Raw NGL

LPG

Naphtha

MTBE

Intermediates

Basic polymers

Synthetic rubbers

Plastics & organic

synthesis

Other fuels &

fuel additives

80%

48%

10%

100%

90%

100%

80%

86%

60%

100%

100%NGLs for petrochemicals

30%Other processing

Polymerisation & other processing

Cracking/ dehydrogenation/ other chemical processing

40%

2 4

Share in external revenue; other revenue represented 4% of external revenue in 2014.x%

Utilities

Petrochemicals Fuels

FMCG Construction

Petrochemicals

Fuels Fuel additives and components

Automotive Construction

Petrochemicals UtilitiesFuels

Chemicals

FMCG ConstructionChemicals

12%

7%

24%

12%

3%

6%

9%

9%

14%

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

30SIBUR 2014 Annual Review

Business Overview

Production Flows

Products and Markets

Feedstock Sourcing

Transportation and Logistics

SIBUR Production System

Belozerniy GPP

Content

31SIBUR 2014 Annual Review

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

32SIBUR 2014 Annual Review

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

Business Overview

ASSETS AND INFRASTRUCTURE

7 GPPs

5 compressor stations

3 GFUs

1 LPG and naphtha transshipment facility

6 railway loading racks

SIBUR is a uniquely positioned vertically integrated gas processing and petrochemicals company. We own and operate Russia’s largest gas processing business in terms of APG processing volumes and are a leader in the Russian petrochemicals industry.

We purchase by-products of the oil and gas extraction activities under long-term contracts from major Russian energy companies, and process them into energy products, including LPG, naphtha, natural gas and raw NGL, and into various petrochemical products, including basic polymers, synthetic rubbers, plastics and organic synthesis products, as well as intermediates and other chemicals.

SIBUR operates two business segments: feedstock & energy and petrochemicals. These business segments vary significantly in their end-user markets, supply and demand trends, value drivers, and consequently, near-term and long-term profitability. However, they are highly integrated, with most of feedstock for our petrochemicals segment supplied by our feedstock & energy segment.

20142013

171.5

2012

168.1

2011

149,5

88.377.674.868.1

FINANCIAL PERFORMANCE

42%(1)45%45%46%

Gross revenue, RR bln

EBITDA, RR bln

EBITDA margin

Revenue from trading operations, ceased in 2015

252.8

FEEDSTOCK & ENERGY SEGMENT

SIBUR owns and operates Russia’s largest and most extensive integrated infrastructure for processing and transportation of hydrocarbon feedstock.

SIBUR feedstock & energy segment comprises:

gathering APG from major Russian oil companies and processing it into natural gas and raw NGL at our GPPs;

transportation, fractionation and other processing of NGLs, that we produce internally or purchase from major Russian oil and gas companies;

production, marketing and sales of energy products.

Feedstock & energy segment supplies approximately 30% of NGLs available for sale as a feedstock for our petrochemicals segment.

Business Overview

33SIBUR 2014 Annual Review

ASSETS AND INFRASTRUCTURE

3 steam crackers

1 PDH facility

2 basic polymer production plants

3 syntetic rubber production plants

13 plastics & organic synthesis production plants

FINANCIAL PERFORMANCE

2014

15%12%18%

2013

128.3

20122011

134.2

20.87.624.3

Gross revenue, RR bln

EBITDA, RR bln

EBITDA margin

142.36%

135.6

16.1

PETROCHEMICALS SEGMENT

SIBUR is a leader in the Russian petrochemicals industry, operating an extensive production base across the country and constantly investing in capacity modernisation and expansion.

SIBUR’s petrochemicals segment produces and sells a wide range of petrochemical products:

basic polymers;

synthetic rubbers;

plastics and organic synthesis products;

intermediates and other chemicals.

Our petrochemicals segment benefits from integration with our feedstock & energy segment, which provides a reliable source of attractively priced raw materials.

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

34SIBUR 2014 Annual Review

Production Flows

gas processing

paraxylene acetic acid

APG

raw NGL

acrylic acid

TPA

natural gas

ethylene oxide

glycols LDPE PP

PET EPS acrylates IRBOPP-films

LPG

propylene

naphtha

benzeneethylene

fractionation

dissolution

dehydrogenation

cracking

cracking

cracking

oxidation

alkylation

hydration

polymerisation

polymerisation

catalytic oxidation

liquid state, solid statepolycondensation

dehydrogenation

oxoprocess

polymerisation

extrusion

ethylbenzene isoprenestyrene

alcohols

catalytic oxidation

esterification

Production Flows

35SIBUR 2014 Annual Review

gas processing

APG

BRDMD

natural gas

nd-PBR

IR IIR ESBR SBS SSBR

LPG

propylene BIFmethanol butadieneIIF

BDF

separation

synthesis

dissolution

solution polymerisation

dehydrogenation

dehydrogenation

Energy products

Basic polymers

Synthetic rubbers

Separation Compounding

Plastics and organic synthesis products

Intermediates

Feedstock sourced by SIBUR externally

polymerisation

emulsion copolymerisation

esterification

esterification

hydration & dehydrogenation

emulsion copolymerisation

solution copolymerisation

solution copolymerisation

solution copolymerisation

solution copolymerisation

emulsioncopolymerisation

isoprene isobutylene

MTBE ESBR NBR

alpha-methylstyrene acrylonitrile

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

36SIBUR 2014 Annual Review

Products and Markets

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

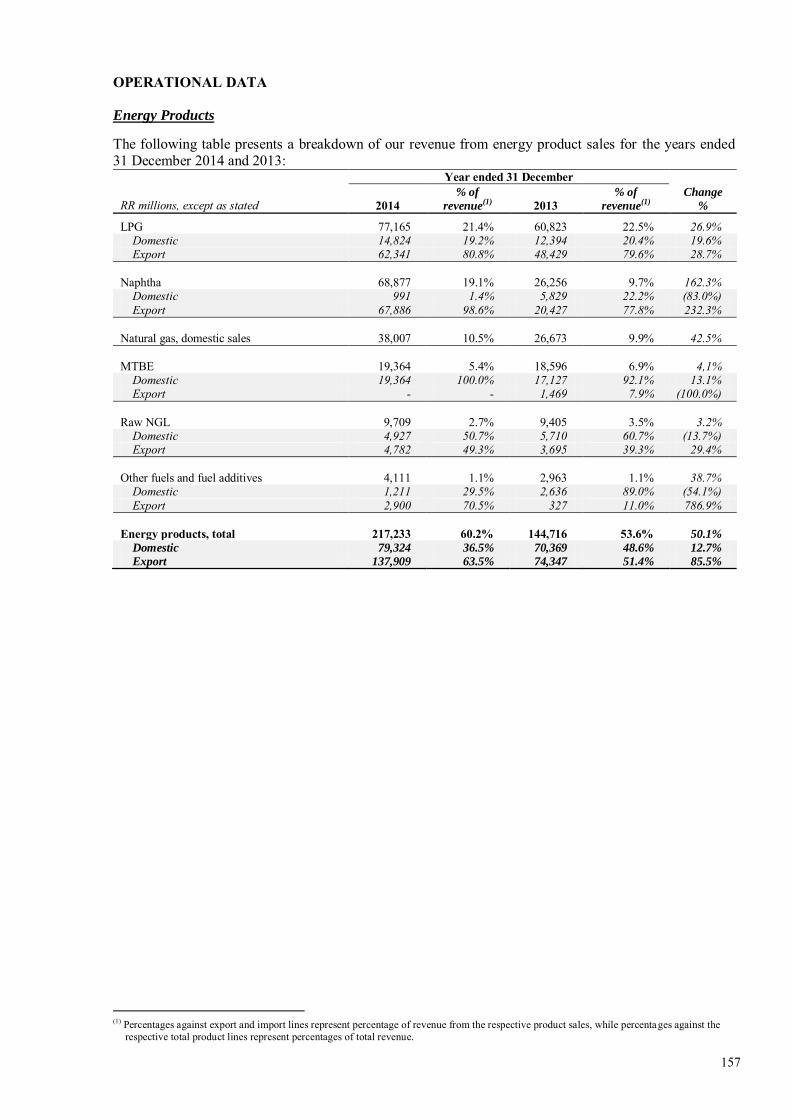

ENERGY PRODUCTS

SIBUR’s energy products, including LPG, naphtha and natural gas are sold primarily to customers in the utilities, fuels and petrochemicals industries both in Russia and internationally. Majority of produced raw NGL is used internally as petrochemical feedstock and raw material for LPG and naphtha. We also produce fuel additives, including MTBE, which we sell to major oil refineries on the domestic market.

In 2014, our revenue from sales of energy products totaled RR 217,233 million, an increase of 50.1% year-on-year, representing 60.2% of total Group revenue for 2014. Domestic sales accounted for 36.5% of total revenue from energy product sales, while 63.5% was attributable to exports.

During 2014 SIBUR conducted naphtha trading operations following the launch of our Ust-Luga transshipment facility. Our revenuefrom sales of energy products adjusted for trading operations increased 21.4% year-on-year, representing 55.0% of the Group’s total revenue for 2014. Domestic sales accounted for 45.2% of total revenue from energy product sales, while 54.8% were derived from exports.

Energy products, such as LPG, naphtha and raw NGL are used as feedstock for internal processing into petrochemical products and sold externally.

KONSTANTIN BELKIN

Member of the Management Board and Managing Director, Hydrocarbon Feedstock Division

“This year we focused on sustaining the profitability of SIBUR’s Feedstock & Energy business amid volatile energy markets, primarily by optimising geographic mix and pursuing high margin distribution channels.”

ENERGY PRODUCTS REVENUE SPLIT(1)

By product

LPG

Natural gas

Naphtha

MTBE

Raw NGL

Other fuels and fuel additives

44%22%16%11%5%2%

1

2

3

4

5

6

3

4

5 6

1

2

30%of NGLs supplied as feedstock to petrochemicals out of volumes

available for sale(1)

Products and Markets

37SIBUR 2014 Annual Review

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

ENERGY PRODUCTS REVENUE SPLIT(1)

By contract/spot

2

1

Contract

Spot

67%33%

1

2

By region By key end-customer industry

Utilities

Petrochemicals

Fuels

Traders

39%25%20%16%

1

2

3

4

3

4

1

2

34 5

1

2

Russia

Europe

Asia

CIS

Other

45%42%7%5%1%

1

2

3

4

5

С1

Methane (gas) Ethane (gas) Propane (gas/liquid)Butane (gas/liquid)

Isobutane (gas/liquid)

Petrochemical feedstock

Oil

Raw natural gas liquids (raw NGL)Natural gas

Liquefied petroleum gas

(LPG) Naphtha

Assosiated petroleum gas (APG)

Pentane (liquid)Isopentane (liquid)

Hexane (liquid)

Heavy fractions

С2 С5-6C3-4 С7+

HYDROCARBON CHAIN

Gubkinskiy GPP

Moscow Vyngapurovskiy GPP

Belozerniy GPPNizhnevartovskiy GPP

Yuzhno-Balykskiy GPPTobolsk-Neftekhim

Nyagan GPP

Uralorgsintez

Yuzhno-Priobskiy GPP

Muravlenkovskiy GPP

SIBUR-Khimprom

Togliattikauchuk

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

38SIBUR 2014 Annual Review

Products and Markets(Energy Products - continued)

Energy productsgas processing & fractionation,MTBE & other fuel additives

Joint venturesinvestment project developed under JV

Petrochemicalssynthetic rubbersplastics & organic synthesis

intermediates

Products and Markets

39SIBUR 2014 Annual Review

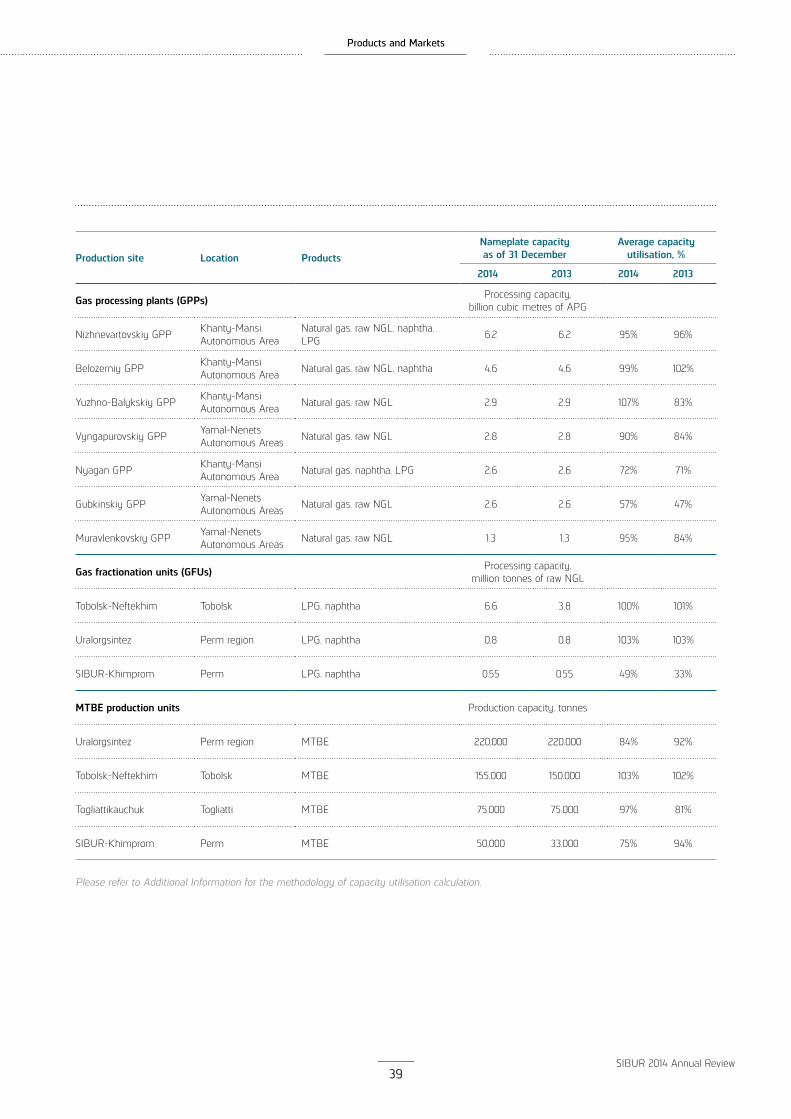

Production site Location ProductsNameplate capacity as of 31 December

Average capacity utilisation, %

2014 2013 2014 2013

Gas processing plants (GPPs) Processing capacity,billion cubic metres of APG

Nizhnevartovskiy GPP Khanty-Mansi Autonomous Area

Natural gas, raw NGL, naphtha, LPG 6.2 6.2 95% 96%

Belozerniy GPP Khanty-Mansi Autonomous Area Natural gas, raw NGL, naphtha 4.6 4.6 99% 102%

Yuzhno-Balykskiy GPP Khanty-Mansi Autonomous Area Natural gas, raw NGL 2.9 2.9 107% 83%

Vyngapurovskiy GPP Yamal-Nenets Autonomous Areas Natural gas, raw NGL 2.8 2.8 90% 84%

Nyagan GPP Khanty-Mansi Autonomous Area Natural gas, naphtha, LPG 2.6 2.6 72% 71%

Gubkinskiy GPP Yamal-Nenets Autonomous Areas Natural gas, raw NGL 2.6 2.6 57% 47%

Muravlenkovskiy GPP Yamal-Nenets Autonomous Areas Natural gas, raw NGL 1.3 1.3 95% 84%

Gas fractionation units (GFUs) Processing capacity,million tonnes of raw NGL

Tobolsk-Neftekhim Tobolsk LPG, naphtha 6.6 3.8 100% 101%

Uralorgsintez Perm region LPG, naphtha 0.8 0.8 103% 103%

SIBUR-Khimprom Perm LPG, naphtha 0.55 0.55 49% 33%

MTBE production units Production capacity, tonnes

Uralorgsintez Perm region MTBE 220,000 220,000 84% 92%

Tobolsk-Neftekhim Tobolsk MTBE 155,000 150,000 103% 102%

Togliattikauchuk Togliatti MTBE 75,000 75,000 97% 81%

SIBUR-Khimprom Perm MTBE 50,000 33,000 75% 94%

Please refer to Additional Information for the methodology of capacity utilisation calculation.

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

40SIBUR 2014 Annual Review

Products and Markets(Energy Products - continued)

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.(2) Including production volumes under processing arrangements.

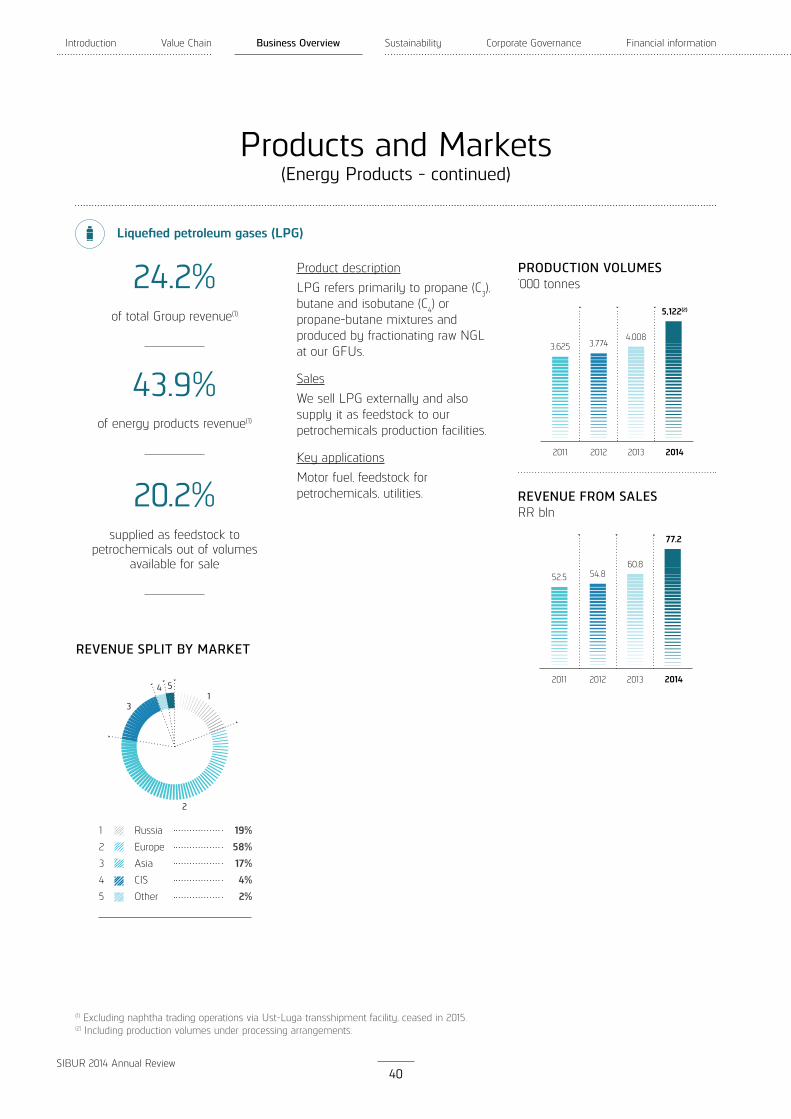

Product descriptionLPG refers primarily to propane (C3), butane and isobutane (C4) or propane-butane mixtures and produced by fractionating raw NGL at our GFUs.

SalesWe sell LPG externally and also supply it as feedstock to our petrochemicals production facilities.

Key applicationsMotor fuel, feedstock for petrochemicals, utilities.

2014

5,122(2)

2013

4,008

2012

3,774

2011

3,625

PRODUCTION VOLUMES‘000 tonnes

2014

77.2

2013

60.8

2012

54.8

2011

52.5

REVENUE FROM SALESRR bln

5

24.2%

43.9%

of total Group revenue(1)

of energy products revenue(1)

20.2%supplied as feedstock to

petrochemicals out of volumes available for sale

REVENUE SPLIT BY MARKET

3

41

2

Russia

Europe

Asia

CIS

Other

19%58%17%4%2%

1

2

3

4

5

Liquefied petroleum gases (LPG)

Products and Markets

41SIBUR 2014 Annual Review

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

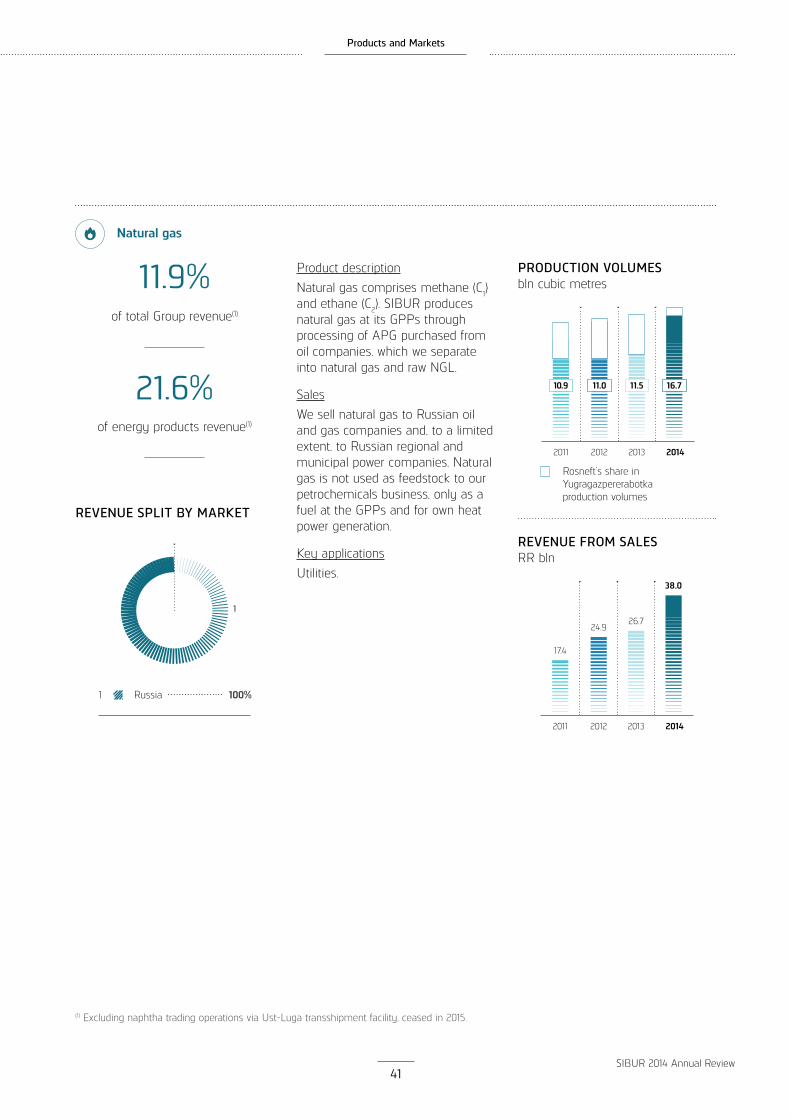

Product descriptionNatural gas comprises methane (C1) and ethane (C2). SIBUR produces natural gas at its GPPs throughprocessing of APG purchased from oil companies, which we separate into natural gas and raw NGL.

SalesWe sell natural gas to Russian oil and gas companies and, to a limited extent, to Russian regional and municipal power companies. Natural gas is not used as feedstock to our petrochemicals business, only as a fuel at the GPPs and for own heat power generation.

Key applicationsUtilities.

11.9%

21.6%

of total Group revenue(1)

of energy products revenue(1)

Rosneft’s share in Yugragazpererabotka production volumes

2014201320122011

PRODUCTION VOLUMESbln cubic metres

16.711.511.010.9

2014

38.0

2013

26.7

2012

24.9

2011

17.4

REVENUE FROM SALESRR bln

REVENUE SPLIT BY MARKET

Russia 100%1

1

Natural gas

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

42SIBUR 2014 Annual Review

Products and Markets(Energy Products - continued)

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

Product descriptionNaphtha (C5+) refers primarily to pentane, isopentane, hexane, heavier fraction hydrocarbons and produced by fractionating raw NGL at our GFUs.

SalesWe sell naphtha externally and supply it as feedstock to our petrochemicals production facilities.

Key applicationsFeedstock for energy and petrochemicals industries.

8.5%

15.5%

of total Group revenue(1)

of energy products revenue(1)

39.4%supplied as feedstock to

petrochemicals out of volumes available for sale(1)

2014

1,460

2013

1,362

2012

1,363

2011

1,295

PRODUCTION VOLUMES‘000 tonnes

Revenue from trading operations, ceased in 2015

2014201320122011

REVENUE FROM SALESRR bln

21.125.7 26.3

68.9

REVENUE SPLIT BY MARKET(1)

Russia

Europe

CIS

3%93%4%

1

2

3

3 1

2

Naphtha

Products and Markets

43SIBUR 2014 Annual Review

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

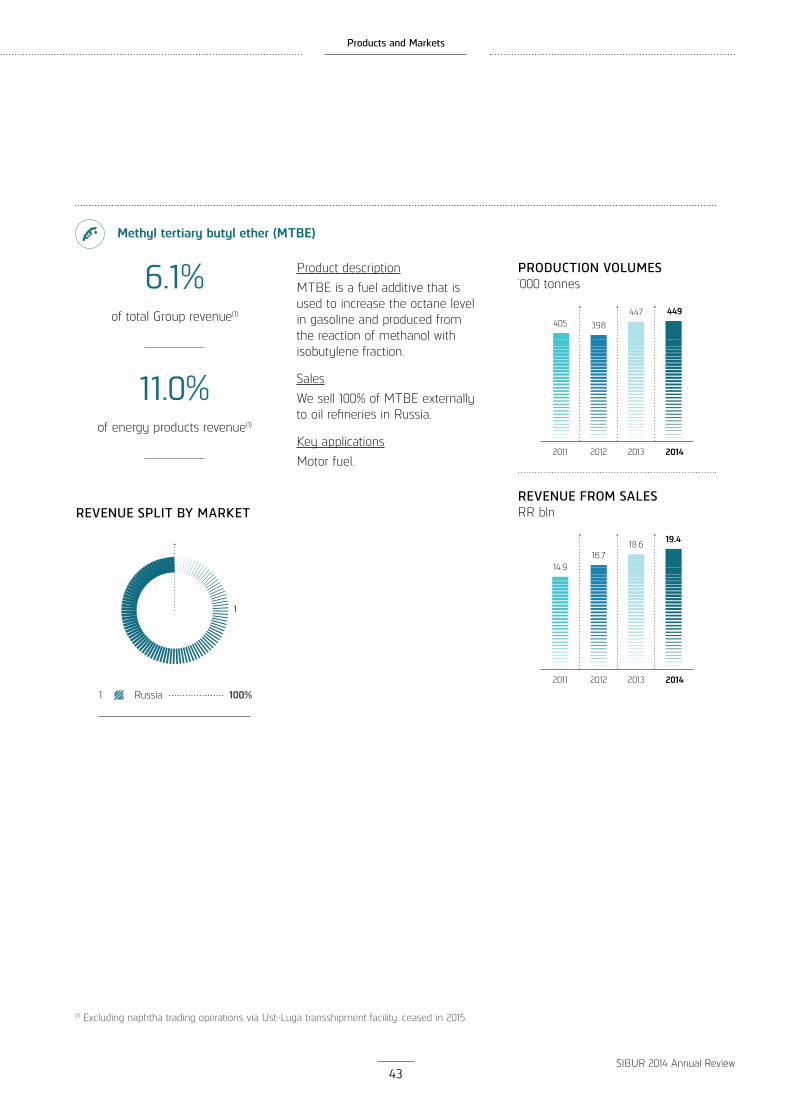

Product descriptionМТBE is a fuel additive that is used to increase the octane levelin gasoline and produced from the reaction of methanol with isobutylene fraction.

SalesWe sell 100% of MTBE externally to oil refineries in Russia.

Key applicationsMotor fuel.

6.1%

11.0%

of total Group revenue(1)

of energy products revenue(1)

REVENUE SPLIT BY MARKET

Russia 100%1

1

2014

449

2013

447

2012

398

2011

405

PRODUCTION VOLUMES‘000 tonnes

2014

19.4

2013

18.6

2012

16.7

2011

14.9

REVENUE FROM SALESRR bln

Methyl tertiary butyl ether (MTBE)

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

44SIBUR 2014 Annual Review

Products and Markets(Energy Products - continued)

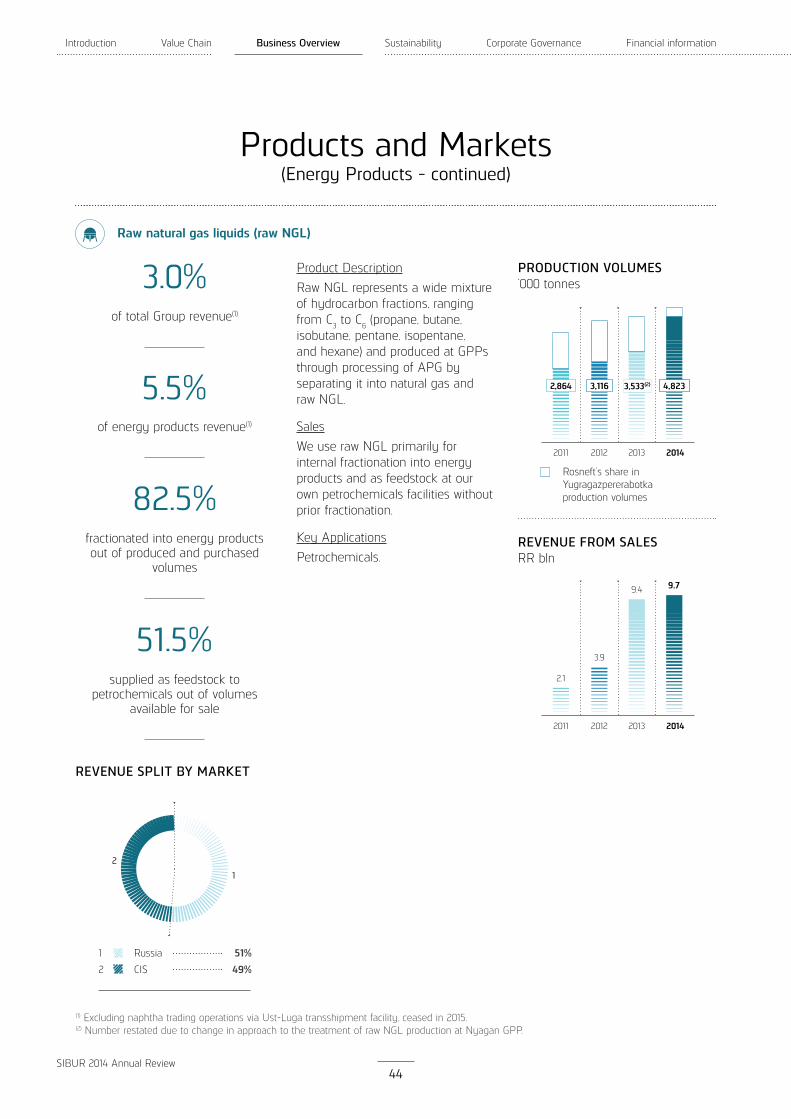

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.(2) Number restated due to change in approach to the treatment of raw NGL production at Nyagan GPP.

Product DescriptionRaw NGL represents a wide mixture of hydrocarbon fractions, ranging from C3 to C6 (propane, butane, isobutane, pentane, isopentane, and hexane) and produced at GPPs through processing of APG by separating it into natural gas and raw NGL.

SalesWe use raw NGL primarily for internal fractionation into energy products and as feedstock at our own petrochemicals facilities without prior fractionation.

Key ApplicationsPetrochemicals.

Raw natural gas liquids (raw NGL)

PRODUCTION VOLUMES‘000 tonnes

Rosneft’s share in Yugragazpererabotka production volumes

2014201320122011

4,8233,1162,864

2014

9.7

2013

9.4

2012

3.9

2011

2.1

REVENUE FROM SALESRR bln

3.0%

5.5%

of total Group revenue(1)

of energy products revenue(1)

82.5%

51.5%

fractionated into energy products out of produced and purchased

volumes

supplied as feedstock to petrochemicals out of volumes

available for sale

REVENUE SPLIT BY MARKET

Russia

CIS

51%49%

1

2

1

2

3,533(2)

Products and Markets

45SIBUR 2014 Annual Review

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

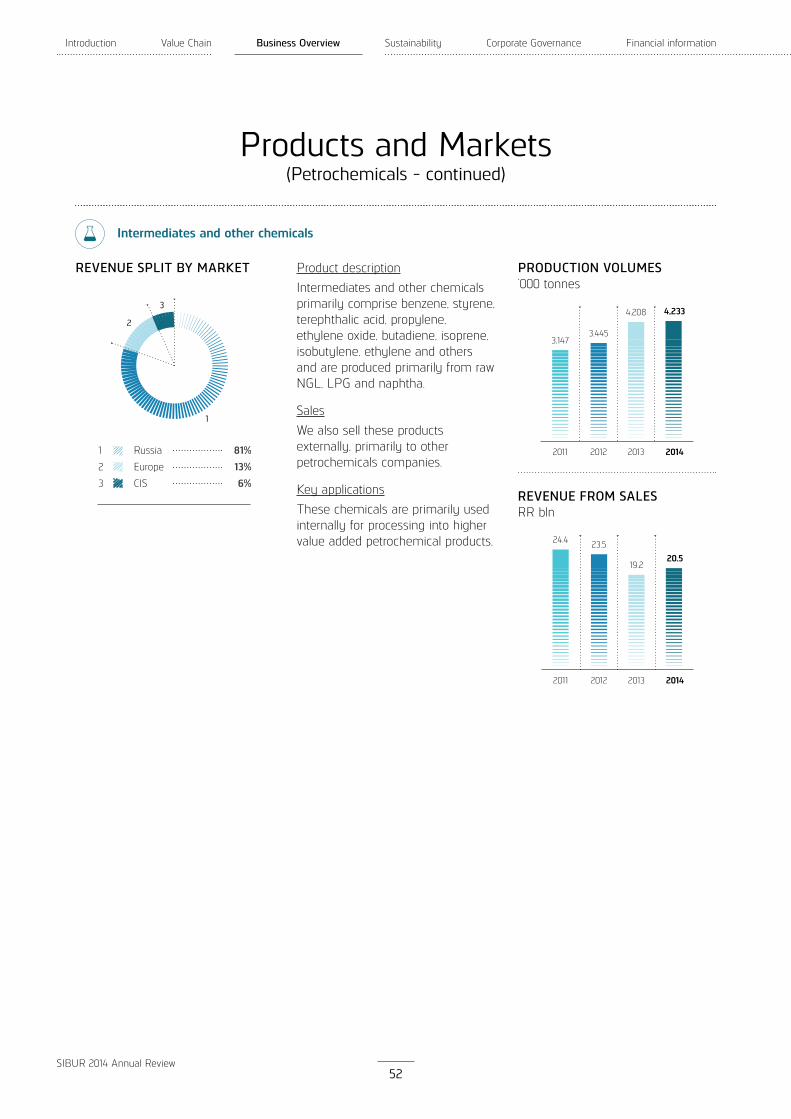

PETROCHEMICALS

SIBUR’s petrochemical products comprise basic polymers, synthetic rubbers, plastics & organic synthesis products as well as intermediates & other chemicals. Each of these product groups has particular characteristics and distinct market fundamentals, however, all are sold to industrial customers in key end-markets, such as fast moving consumer goods (FMCG), construction, chemicals, automotive and other sectors.

In 2014, our revenue from sales of petrochemical products totaled RR 132,513 million, a 14.2% increase year-on-year, and accounted for 41.5% of the total Group revenue for 2014(1). Domestic sales accounted for 65.3% of total revenue from petrochemicals sales, while 34.7% was attributable to exports.

We use a large portion of intermediates & other chemicals internally for processing into higher value added petrochemical products.

SIBUR’s integrated business model enables us to change the composition of our feedstock and product mix to optimise purchasing, production, sales and logistics in order to maximise our blended margins.

PETROCHEMICAL PRODUCTS REVENUE SPLITBy product

Plastic and Organic Synthesis

Basic Polymers

Synthetic Rubbers

Intermediates & Other chemicals

35%

29%21%15%

1

2

3

4

3

4

1

2

By contract/spot

Contract

Spot

41%59%

1

2

1

2

By region

Russia

Europe

Asia

CIS

Other

65%12%11%10%2%

1

2

3

4

5

3

4 5

1

2

By key end-customer industry

FMCG

Construction

Chemicals

Automotive

Traders

Other

35%15%15%13%11%11%

1

2

3

4

5

6

3

4

5

6

1

2

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

46SIBUR 2014 Annual Review

Products and Markets(Petrochemicals - continued)

Basic polymers

SERGEY KOMYSHAN

Member of the Management Board and Managing Director, Basic Polymers Division

“Our aim is to become a leading producer of basic polymers in Russia through organic production expansion and import substitution. The successful launch of Tobolsk-Polymer was a major step forward in executing this strategy.”

Product description SIBUR’s basic polymers products include polypropylene (PP) and polyethylene (LDPE), which are granulated thermoplastic polymers. PP and LDPE are derived from polymerisation of propylene and ethylene, respectively, that are produced internally.

SalesWe sell LDPE and PP to external clients in Russia and abroad and also use certain volumes internally in BOPP-films production.

Key PP applicationsGeneral-purpose consumer goods, packaging, BOPP-films, hygiene products, pipes, fibres and automotive components.

Key LDPE applicationsGeneral-purpose consumer goods, coating materials for electrotechnical and energy industry, film for agricultural industry, various packaging.

2014

656

2013

403

2012

386

2011

373

PRODUCTION VOLUMES‘000 tonnes

2014

38.4

2013

22.8

2012

22.2

2011

21.8

REVENUE FROM SALESRR bln

REVENUE SPLIT BY PRODUCT

PP

PE (LDPE)

60%40%

1

2

1

2

REVENUE SPLIT BY MARKET

3

4 5

1

2

Russia

Europe

Asia

CIS

Other

63%5%

23%8%1%

1

2

3

4

5

Products and Markets

47SIBUR 2014 Annual Review

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.(2) SIBUR’s non-consolidated JV with Gazprom Neft Group and Titan Group.(3) NPP Neftekhimia is the Group’s joint venture with the Gazprom Neft Group. SIBUR does not consolidate production volumes of NPP Neftekhimia, however it purchases all PP produced by the joint venture.

(4) SIBUR’s non-consolidated JV with SolVin Holding Nederland B.V.

Please refer to Additional Information for the methodology of capacity utilisation calculation.

Product Production site LocationNameplate capacity as of 31 December

Capacityutilisation, %

2014 2013 2014 2013

PP Tobolsk-Polymer Tobolsk 500,000 500,000 53% 19%

PP Tomskneftekhim Tomsk 130,000 130,000 99% 99%

PP Poliom (non-consolidated JV(2)) Omsk 210,000 180,000 82% 65%

PP NPP Neftekhimia (non-consolidated JV(3)) Moscow 120,000 120,000 85% 107%

PE (LDPE) Tomskneftekhim Tomsk 245,000 245,000 106% 102%

PVC RusVinyl (non-consolidated JV(4)) Nizhniy Novgorod region 330,000 - 75% -

Caustic soda RusVinyl (non-consolidated JV(4)) Nizhniy Novgorod region 225,000 - 70% -

12.0%

29.0%

of total Group revenue(1)

of petrochemicals revenue

17.3%out of produced and puchased volumes used in BOPP-films

production internally

Petrochemicalsbasic polymersintermediates

Joint venturesfacilities operated under JVs

RusVinyl

NPP Neftekhimia

Poliom

Tobolsk-PolymerTomskneftekhim

Moscow

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

48SIBUR 2014 Annual Review

Products and Markets(Petrochemicals - continued)

Synthetic rubbers

REVENUE SPLIT BY PRODUCT

Commodity rubbers

Speciality rubbers

Thermoplasticelastomers

60%

27%13%

1

2

3

2

3

1

MIKHAIL GORDIN

Member of the Management Board and Managing Director, Synthetic Rubbers Division

“Synthetic rubbers business is facing a challenging external market environment. We are focused on improving operational efficiency and ensure competitive product quality to drive performance.”

Commodity rubbers comprise polyisoprene (IR), polybutadiene (BR) and styrene-butadiene (SBR) rubbers. These are butadiene or isoprene polymers as well asco-polymers of butadiene and styrene, which have elastic and other properties that are partially similar to natural rubbers.

Key applicationsTyres, mechanical rubber goods for automotive and machinebuilding industries, asbestos technical (frictional) goods and adhesives, footwear.

Specialty rubbers comprise co-polymers such as nitrile-butadiene rubber (NBR), which is a complex mixture of unsaturated co-polymers of acrylonitrile and butadiene, and butyl rubber (IIR), which is a co-polymer of isobutylene and a small amount of isoprene. In addition to basic rubber properties, such as elasticity, NBR is characterised by oil and petrol resistance, while IIR is characterised by gas impermeability.

Key applicationsTyre inner tubes and vulcanising diaphragms, mechanical rubber goods for asbestos technical (frictional) goods and adhesives, footwear.

Thermoplastic elastomers represent a mix of polymers (usually plastic and rubber), which consists of materials with both thermoplastic and elastomeric properties.

Key applicationsConstruction, healthcare, automotive and electronics.

SalesWe sell 100% of rubbers to external customers both in Russia and abroad.

2014

353

2013

418

2012

423

2011

426

PRODUCTION VOLUMES‘000 tonnes

2014

27.8

2013

32.4

2012

41.1

2011

51.0

REVENUE FROM SALESRR bln

REVENUE SPLIT BY MARKET

3

4

5

1

2

Russia

Europe

Asia

CIS

Other

36%28%20%9%7%

1

2

3

4

5

Products and Markets

49SIBUR 2014 Annual Review

(1) Excluding naphtha trading operations via Ust-Luga transshipment facility, ceased in 2015.

Please refer to Additional Information for the methodology of capacity utilisation calculation.

8.7%

21.0%

of total Group revenue(1)

of petrochemicals revenue

Product Production site LocationNameplate capacity as of 31 December

Capacityutilisation, %

2014 2013 2014 2013

Commodity rubbers

BR Voronezhsintezkauchuk Voronezh 91,000 91,000 75% 87%

IR Togliattikauchuk Togliatti 82,000 82,000 72% 81%

ESBR Voronezhsintezkauchuk Voronezh 80,000 80,000 59% 78%

ESBR Togliattikauchuk Togliatti 60,000 60,000 53% 89%

PBR-Nd Voronezhsintezkauchuk Voronezh 30,000 30,000 41% 36%

SSBR Voronezhsintezkauchuk Voronezh 23,000 23,000 50% 60%

Specialty rubbers

IIR Togliattikauchuk Togliatti 60,000 53,000 92% 104%

NBR Krasnoyarskiy ZSK Krasnoyarsk 42,500 42,500 76% 86%

Latexes Voronezhsintezkauchuk Voronezh 19,500 19,500 7% 14%

Thermoplastic elastomers

SBS Voronezhsintezkauchuk Voronezh 85,000 85,000 44% 77%

Petrochemicalssynthetic rubbersintermediates

Krasnoyarskiy ZSK

Voronezhsintezkauchuk

Togliattikauchuk

Energy ProductsMTBE & other fuel additives

Moscow

Introduction Value Chain Business Overview Sustainability Corporate Governance Financial information

50SIBUR 2014 Annual Review

Products and Markets(Petrochemicals - continued)

Plastics and organic synthesis products

PAVEL LYAKHOVICH

Member of the Management Board and Managing Director, Plastics and Organic Synthesis Division

“We are successively expanding capacity at our production sites to strengthen our leading positions on the competitive domestic market. Our goal is to meet consumption growth of petrochemicals in Russia being a key supplier of domestic raw materials.”

blocks, packaging materials as well as for decorative elements.Alcohols include 2-ethylhexanol, butyl alcohol and isobutyl alcohol.Key applicationsProduction of plasticisers, acetates, acrylates, oil additives, as solvents for plastics and varnish, as anti-foaming agent, as well as a component for perfume compounds.Glycols include mono-ethylene glycol, diethylene glycol and triethylene glycol.Key applicationsPET, polyester fiber, de-icing liquids, cooling and antifreezing liquids, extragent for aromatic hydrocarbons and reagent for natural gas drying.Acrylates include ethers of acrylic acid, butyl, methyl and ethyl.Key applicationsProduction of acrylic emulsions,superabsorbents, building mixes andadhesives used in the construction and textile industries.SalesWe sell these products to external customers in a variety of industriesin Russia and abroad with a strong focus on domestic market for

majority of the products and also use certain volumes internally, primarily in the production of higher value-added products.

SIBUR produces plastics and organic synthesis products primarilyfrom ethylene and propylene derivatives, as well as a wide range of intermediates, which we also produce as part of our value chain.

PET is a thermoplastic polymer resin of the polyester family.Key applicationsPET packaging for beverages and food, other containers.BOPP-films include coextruded,coated, non-heat sealable or homopolymer films in a variety of finishes.Key applicationsUsed by the retail industry for packaging and production of price tags, as well as labels and adhesive tapes.EPS is a granulated polymer, produced from styrene monomer.Key applicationsProduction of thermoinsulation

REVENUE SPLIT BY MARKET

2

43

1

Russia

Europe

Asia