Annual Responsible Investment Report - PGGM · Introduction 9 1. Frameworks for ... indicators of...

68

pggm.nl Annual Responsible Investment Report 2014

Transcript of Annual Responsible Investment Report - PGGM · Introduction 9 1. Frameworks for ... indicators of...

pggm.nl

Annual Responsible Investment Report

2014

15-6959 may 2015

AN

NU

AL R

ESPON

SIBLE IN

VESTMEN

T REPO

RT

2014

2 PGGM

Statements 3

Management Statement 3Statement of the Supervisory Board 3

Foreword 4

Summary 6

Introduction 9

1. Frameworks for Responsible Investment 10

1.1 Beliefs and Principles for Responsible Investment 11 1.2 Policy Advice 11 1.3 Implementation of Responsible Investment 12 1.4 Investing in the Netherlands 14 1.5 Long-term Investment 16

2. Responsible Investment in Areas of Focus 17

2.1 Climate Change and Reduction of Pollution and Emissions 18 2.2 Water Scarcity 22 2.3 Healthcare 25 2.4 Food Security 28 2.5 A Stable Financial System that Serves the Real Economy 31 2.6 Good Corporate Governance 35 2.7 Safeguarding Human Rights 40

3. Responsible Investment in PGGM Funds and Mandates 44

3.1 Application of Responsible Investment in PGGM Funds 45 3.2 Application of Responsible Investment in Mandates 50

Outlook 2015 52

Appendices 53

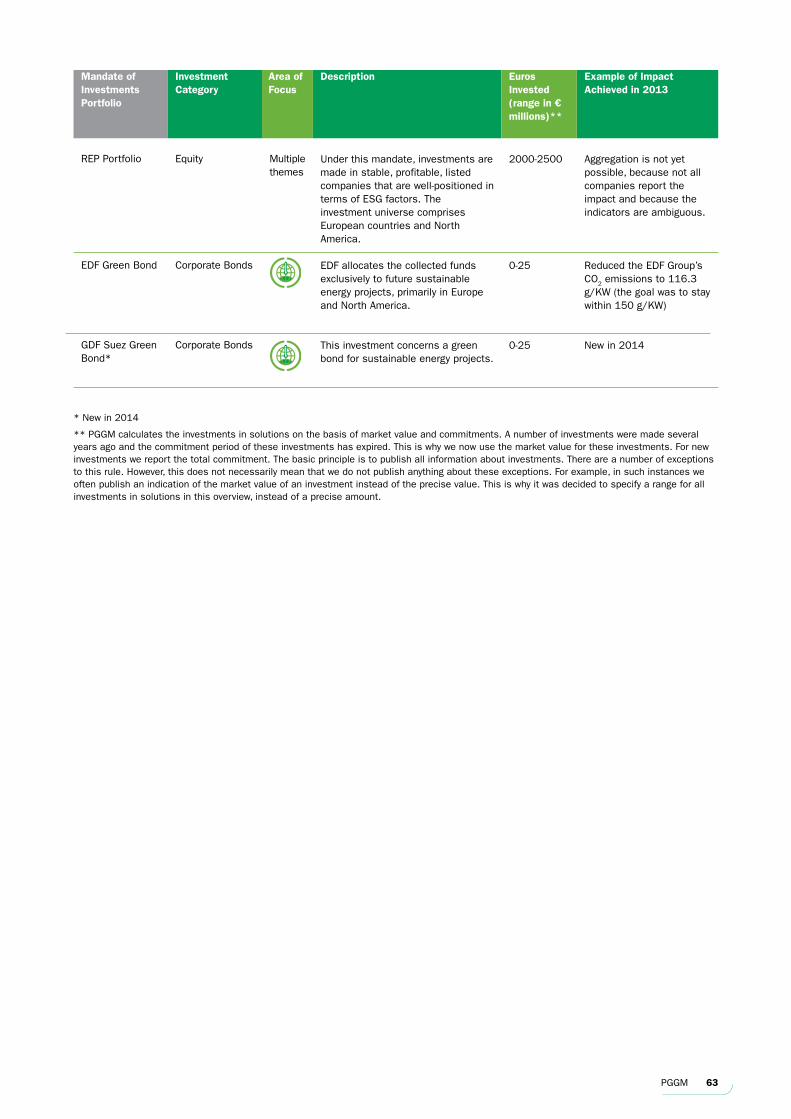

Appendix 1. Abbreviations and Glossary 53Appendix 2. Overview of 2014 Results by Instrument 56Appendix 3. Overview of Instruments by PGGM Fund 57Appendix 4. Overview of Investments in Solutions 60Appendix 5. Engagement Figures 64Appendix 6. Voting Figures 65Appendix 7. Justification 66Appendix 8. Independent Assurance Report 67

Content

3PGGM

Management Statement

As the administrator for investment funds and the asset manager for pension funds, PGGM Vermogensbeheer B.V. (PGGM) supports its clients in their task of providing a stable and high-quality pension for their participants, now and in the future. PGGM is convinced that contributing to a sustainable world is part of building a valuable future for those participants – not only by fulfilling our clients’ wider social responsibility or by complying with laws and regulations or other standards, but also by helping them in fulfilling their primary task. This is why we invest the pension assets of our clients in responsible ways.

This report renders account of the activities carried out in support of responsible investment in 2014. This concerns advisory, as well as implementation-related activities. The policies pursued by our clients and PGGM’s responsible investment framework form the starting point for this. This framework seeks commonality within the PGGM investment funds (PGGM funds), while providing scope to meet clients’ specific policy requirements through internal and external asset management. That means the activities discussed in this report do not always apply to all clients.

In compiling the PGGM 2014 Annual Responsible Investment Report we have adhered to the international reporting principles of the Global Reporting Initiative (GRI) G4 (Appendix 7). In addition, where possible, we have reported on the indicators of the GRI Financial Services Sector Supplement (FSSS Final Version, 2008). We have not followed the GRI to the letter in this report, because it concerns the asset management activities and is not relevant at the PGGM N.V. level.

We have assessed the PGGM 2014 Annual Responsible Investment Report and declare that, to the best of our knowledge and belief, the information in this report presents a true and fair view of reality. The PGGM 2014 Annual Responsible Investment Report has been assessed and provided with an independent assurance report by KPMG Sustainability, an independent external auditor. This assurance report is attached in Appendix 8.

Zeist, 23 March 2015

Management of PGGM Vermogensbeheer B.V.

Eloy LindeijerMarc van den BergArjen PasmaBob Rädecker

Statement of the Supervisory Board

The Supervisory Board of PGGM Vermogensbeheer B.V. was instituted on 7 April 2014. As supervisory directors, we supervised the preparation of the PGGM 2014 Annual Responsible Investment Report and declare that, to the best of our knowledge and belief, the information in this report presents a true and fair view of reality.

Zeist, 31 March 2015

Supervisory Board of PGGM Vermogensbeheer B.V.

Else BosPaul Loven

Statements

PGGM4

In 2014, a number of pension funds whose assets are managed by PGGM took further steps to embed sustainability in their policies. For example, the Pensioenfonds Zorg en Welzijn (PFZW) (Pension Fund for the Healthcare and Social Sectors) published its 2014-2020 Investment Policy. Investments must not only provide for a good pension, but be sustainable, understandable and manageable as well. PFZW has formulated ambitious sustainability objectives, such as halving the investment portfolio’s negative footprint and quadrupling the positive sustainability contribution by 2020. The Stichting Pensioenfonds voor de Architectenbureaus (Pension Fund Foundation for Architecture Firms) also published a new Responsible Investment policy. For PGGM, these developments provide the impetus needed to assess investments in CO2-intensive industries and to look for energy transition opportunities, as well as companies that contribute to solving important social issues in the area of climate change, water scarcity, healthcare, and food security. Furthermore, in 2014, PGGM welcomed two new clients: Stichting Bedrijfstakpensioenfonds voor het Schilders-, Afwerkings- en Glaszetbedrijf (Sector Pension Fund Foundation for Painting, Decorating and Glazier Businesses) and the Stichting Pensioenfonds Smurfit Kappa Nederland (Pension Fund Foundation Smurfit Kappa Netherlands).

Since the financial crisis, the political establishment and society have increasingly called on pension funds to increase investments in the Netherlands as a means of increasing the availability of long-term capital for economic growth and for social themes, such as energy transition, innovation in the healthcare sector and the mortgage market. Because in addition to a good pension, participants also benefit from a healthy economy, we actively participated on behalf of our clients in the Cabinet’s debate with institutional investors on these themes. On 1 October 2014, the Netherlands Investment Institution (NLII or NII) was founded with a large number of institutional investors as its founding fathers, including PGGM and PFZW. The NLII has the task of matching supply and demand for long-term financing and increasing the attractiveness of investing in the Netherlands by consolidating projects. The NLII also is a key platform that together with the Dutch government makes it possible to create clear insight into structural financing issues related to the Dutch economy. PGGM is actively involved in various ways to provide pension funds with access to attractive investments in the Netherlands. For example, we invest in bank capital (risk sharing transactions) designed to facilitate SME financing and we have expanded investments in the private capital of Dutch companies, care homes and infrastructure.

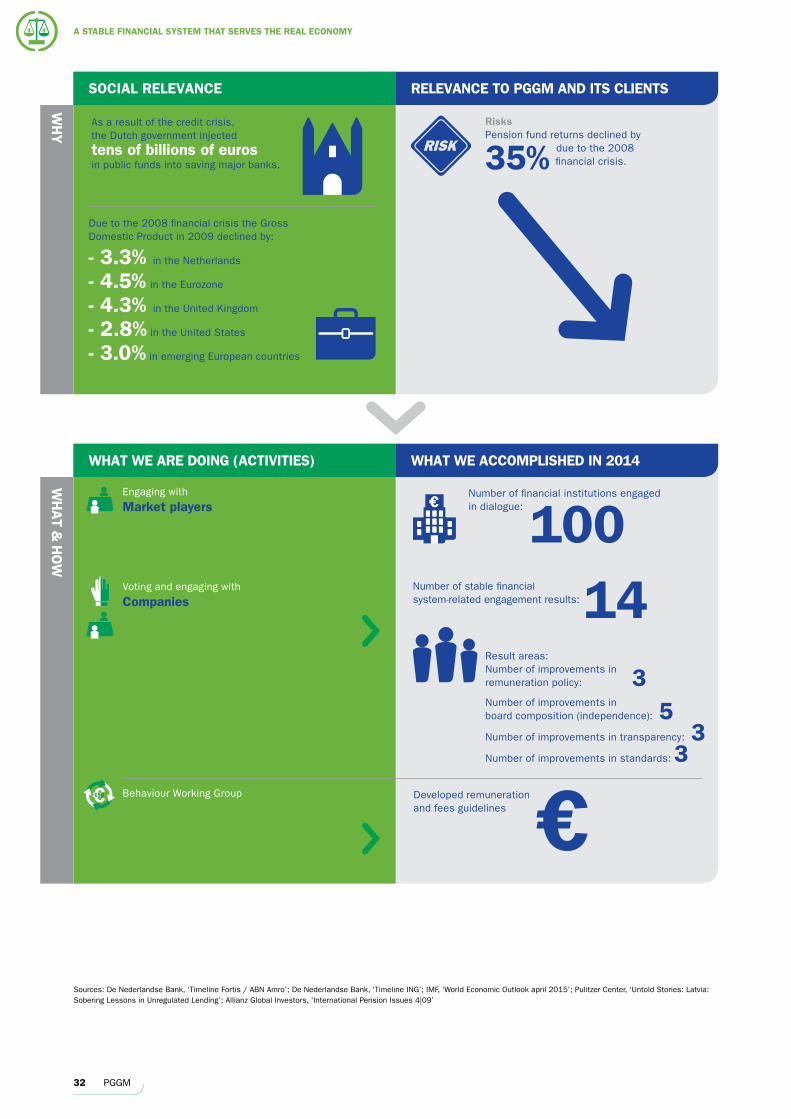

Good corporate governance and well-functioning markets are essential for restoring society’s trust, which was seriously damaged by the financial crisis. This is why PGGM engages with banks and financial institutions on transparency, risk culture and risk management, and on the need for client focus. We have developed new guidelines for acceptable compensation in companies and financial service providers. We observe worldwide improvements in these areas. We are delighted that large Dutch banks, with whom we are in discussion, are actively following up on the recommendations of the Enhanced Disclosure Task Force (EDTF) concerning transparency, and consequently have made substantial improvements in their annual reporting.

In 2015, we continue to work on a sustainable financial system in close cooperation with other institutional investors and initiatives, such as the EDTF, and by actively contributing to the dialogue on new market standards for financial reporting. PGGM consequently joined the Investors Financial Reporting Programme of the International Accounting Standards Board (IASB). In addition, measuring the impact of investments in solutions on social issues is increasingly important, as is the continuous improvement of the integration of sustainability into all investment processes.

Eloy LindeijerChief Investment Management

Foreword

5PGGM

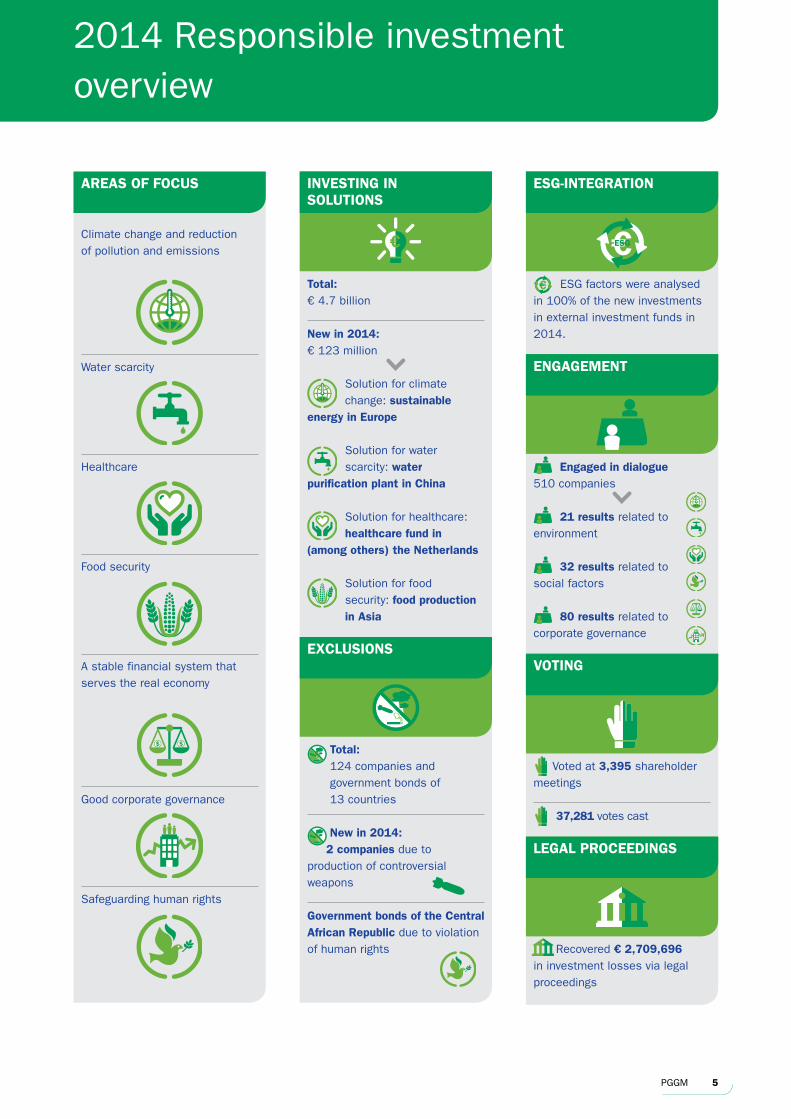

2014 Responsible investment overview

AREAS OF FOCUS INVESTING IN SOLUTIONS

ESG-INTEGRATION

EXCLUSIONS

ENGAGEMENT

Climate change and reduction of pollution and emissions

Water scarcity

Healthcare

Food security

A stable financial system that serves the real economy

Good corporate governance

Safeguarding human rights

Total: € 4.7 billion

New in 2014: € 123 million

Solution for climate change: sustainable energy in Europe

Solution for water scarcity: water purification plant in China

Solution for healthcare: healthcare fund in (among others) the Netherlands

Solution for food security: food production in Asia

Total: 124 companies and government bonds of 13 countries

New in 2014: 2 companies due to production of controversial weapons

Government bonds of the Central African Republic due to violation of human rights

ESG factors were analysed in 100% of the new investments in external investment funds in 2014.

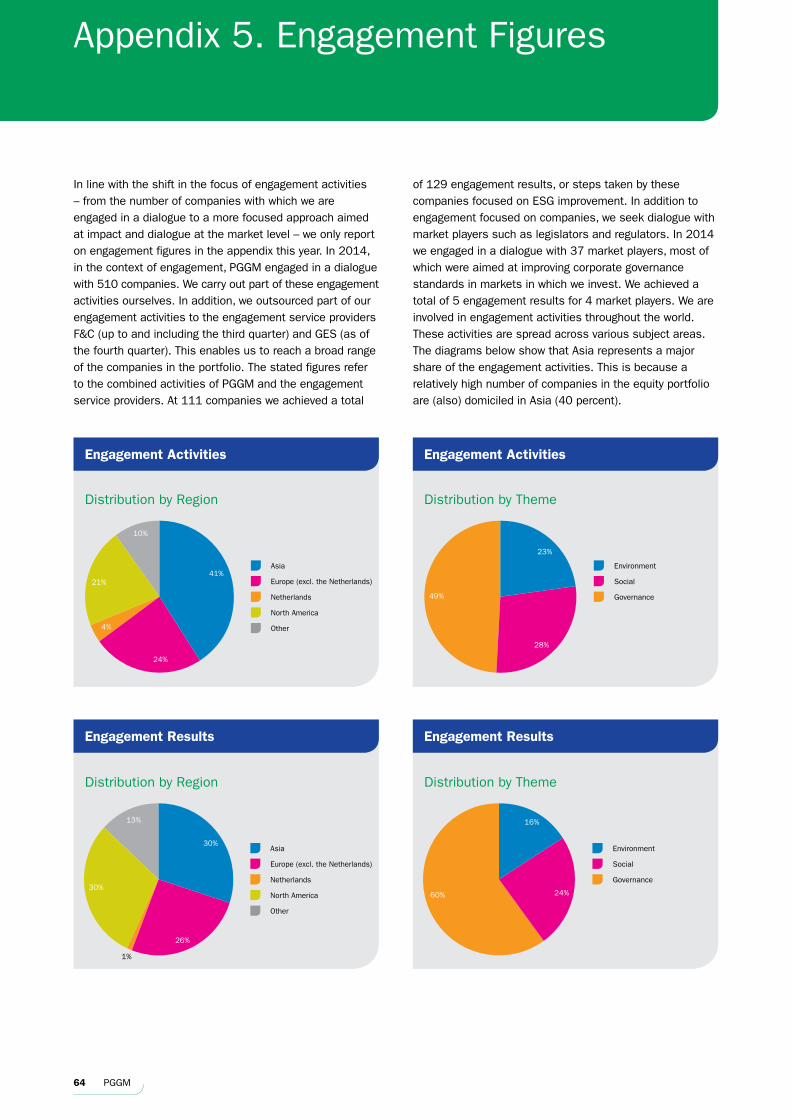

Engaged in dialogue 510 companies

21 results related to environment

32 results related to social factors

80 results related to corporate governance

Voted at 3,395 shareholder meetings

37,281 votes cast

Recovered € 2,709,696 in investment losses via legal proceedings

VOTING

LEGAL PROCEEDINGS

6 PGGM

Through its activities in the field of responsible investment, PGGM

provides responsible, stable and good investment results that are

consistent with our clients’ ambitions for their pensions. These

activities are founded on the beliefs that (1) responsible investment

pays off by producing a positive risk-return profile; (2) sustainable

development results in good and stable returns over the long term;

and (3) capital is a driving force for sustainable development.

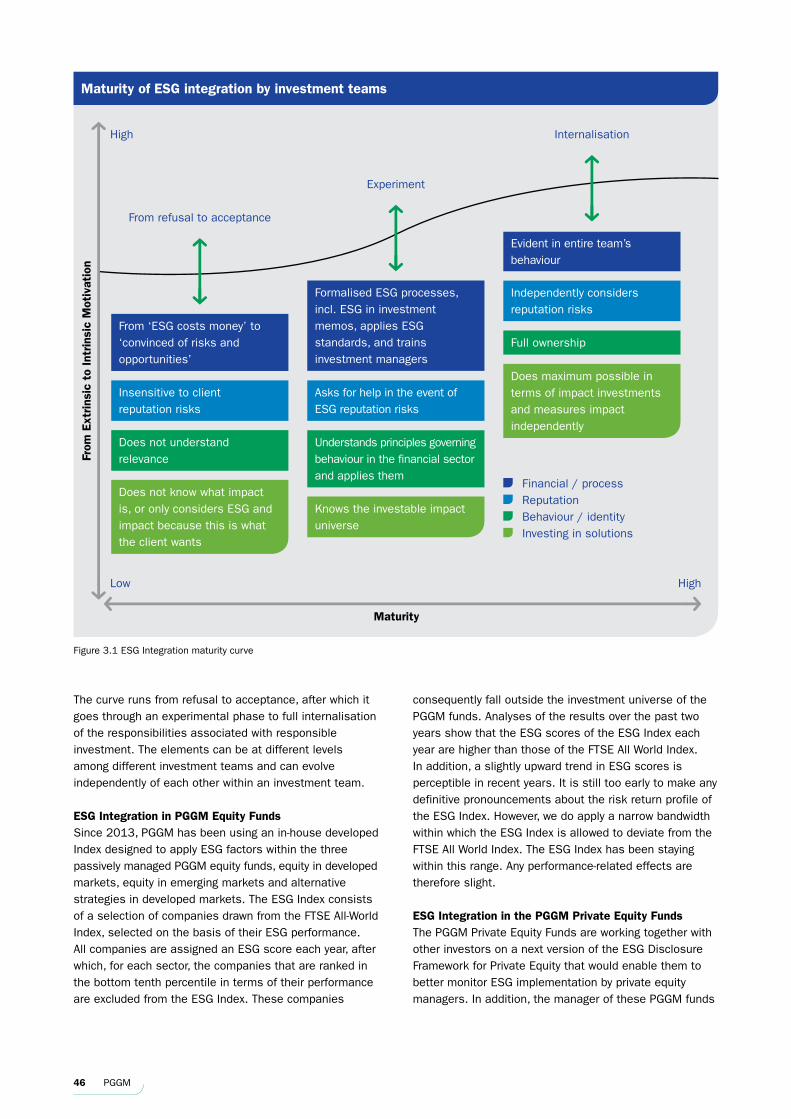

Responsible investment is an integral part of our investment approach. It means that we consciously take account of environmental, social and governance (ESG1) factors in our investment processes. We have developed a number of new instruments in recent years, such as an ESG Index, and are increasingly focusing on the actual social impact of our investments. This annual report is therefore structured on the basis of seven areas of focus selected in consultation with our clients. These areas of focus are material in terms of social impact and in terms of the risk return profile of the investments of our clients. In 2014, the objectives were based on quantitative agree-ments with our clients concerning the use of responsible investment instruments. Appendix 2 presents an overview of the activities associated with each instrument and the results achieved in 2014.

This annual report does not aim for completeness, but is a progress report over 2014. Transactions from previous years, including in sustainable energy, are not covered in this report. Previous annual reports contain additional information on such topics.

Responsible Investment in Areas of Focus

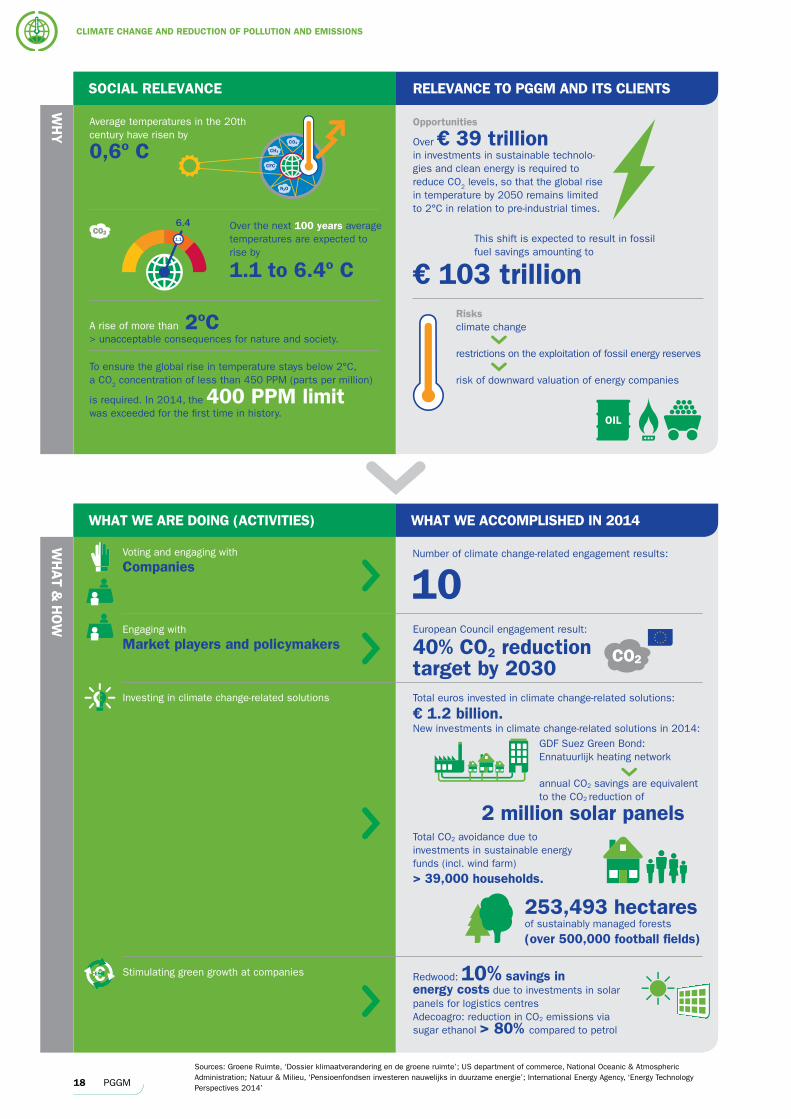

Climate change and reduction of pollution and emissions Reducing the negative effects of climate change requires more green growth, or economic growth based on more sustainable energy and a reduction in the wastage of raw materials. Political leadership is required to create

preconditions that keep investments in green growth attractive. In 2014, we therefore made our voice heard among policymakers throughout the world, for instance at the UN Climate Summit and at the European Commission (EC). The EC presented the ‘2030 Climate and Energy Plan’, calling for a CO2 emission reduction target of 40 percent, the percentage that PGGM had advocated. To limit the risks of climate change for investments, we have started to calculate the CO2 footprint of PGGM’s equity portfolio and we will present a reduction plan in 2015.

Water scarcity Water scarcity not only threatens population health, it also threatens economic growth. PGGM wants to enable economic growth, safeguard the continuity of companies and secure access to clean drinking water. In 2013-2014, PGGM invested in three Chinese water companies that purify industrial waste water and consequently contribute to solving the water scarcity and water pollution issues in North-east China. In addition, PGGM encouraged the CDP, an organisation that sets standards for transparency in water scarcity for listed companies, to increasingly shift the focus of their annual reporting on water to ‘business value at water risk’. This is the business value that is at risk due to exposure to water problems. This information is available effective from 2015. It enables investors to identify water opportunities and risks, and use this information as a basis for making their investment decisions.

1 Appendix 1 contains a list of abbreviations and a glossary.

Summary

7PGGM

Healthcare PGGM wants to contribute to strategic solutions designed to deal with issues concerning population health and access to healthcare. We do this by investing in healthcare solutions and by entering into a dialogue with companies on this issue. In 2014, PGGM invested in Gilde Healthcare Services II, a fund that invests in the healthcare sector, primarily in the Benelux and Germany. In addition, we called on multiple companies to become members of the Japanese non-profit Global Health Innovation and Technology (GHIT) fund, in order to collectively improve access to medicines. Six companies have since joined this fund.

Food securityJust like healthcare, food is a basic necessity and a key engine for social and economic growth. For instance in 2014, we invested via Black River Food Fund II in the Chinese AustAsia dairy farm that each day produces over 80 percent more milk than local farms. This level of efficiency is required to advance food security in China. In addition, PGGM is also engaged in a dialogue with market players and companies in the area of sustainable food production. For example, we successfully continued the engagement project for a sustainable palm oil sector: five palm oil producers have instituted a moratorium on the deforestation and cultivation of peat lands.

A stable financial system that serves the real economy We depend on the health of the financial system in order to achieve returns for our clients. Seven years after start of the financial crisis, trust in the financial sector is still low. As a financial institution, PGGM has a responsibility to contribute to a sustainable financial system that can restore society’s trust, a prerequisite for achieving good returns over the long term. In 2014, we described our role, as well as that of our clients, in a sustainable financial system. In addition, we assess the behaviour of parties in the sector with which we co-operate or in which we invest. We have developed new compensation guidelines, in which we set out what in our view is an acceptable compensation structure for listed companies and financial service providers. As a member of the EDTF, PGGM is working on improving the transparency of international banks concerning risks and risk control measures. In 2014, a number of banks in North America and Europe, including the Netherlands, improved their annual reporting.

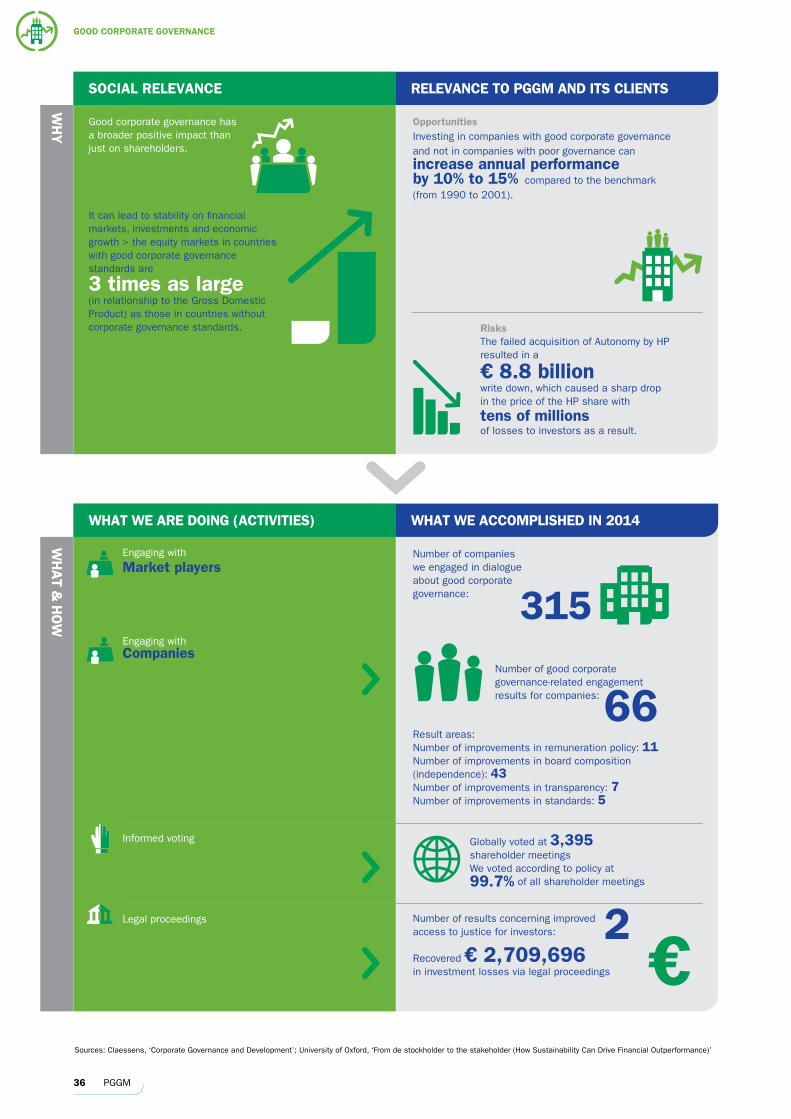

Good corporate governance Good corporate governance is a precondition for the effective operation of a company. The risk and return on investments are highly dependent on efficient companies, markets and social systems. In the markets in which we invest for our clients, we are aiming for a suitable and cohesive system with standards for behaviour, competence and reporting. In 2014, we encouraged a number of companies to develop an acceptable remuneration policy. In addition, we called on various companies to account for a lack of independent supervision. As a result, a number of companies in Asia appointed independent external directors. However, we do not always achieve the desired result. For example, the IT company Oracle once again refused to consider proposals calling for the compensation structure to be adjusted and allowing shareholders to nominate independent directors. If the company continues to refuse to make the necessary adjustments, PGGM, in consultation with its clients, can decide to exclude Oracle.

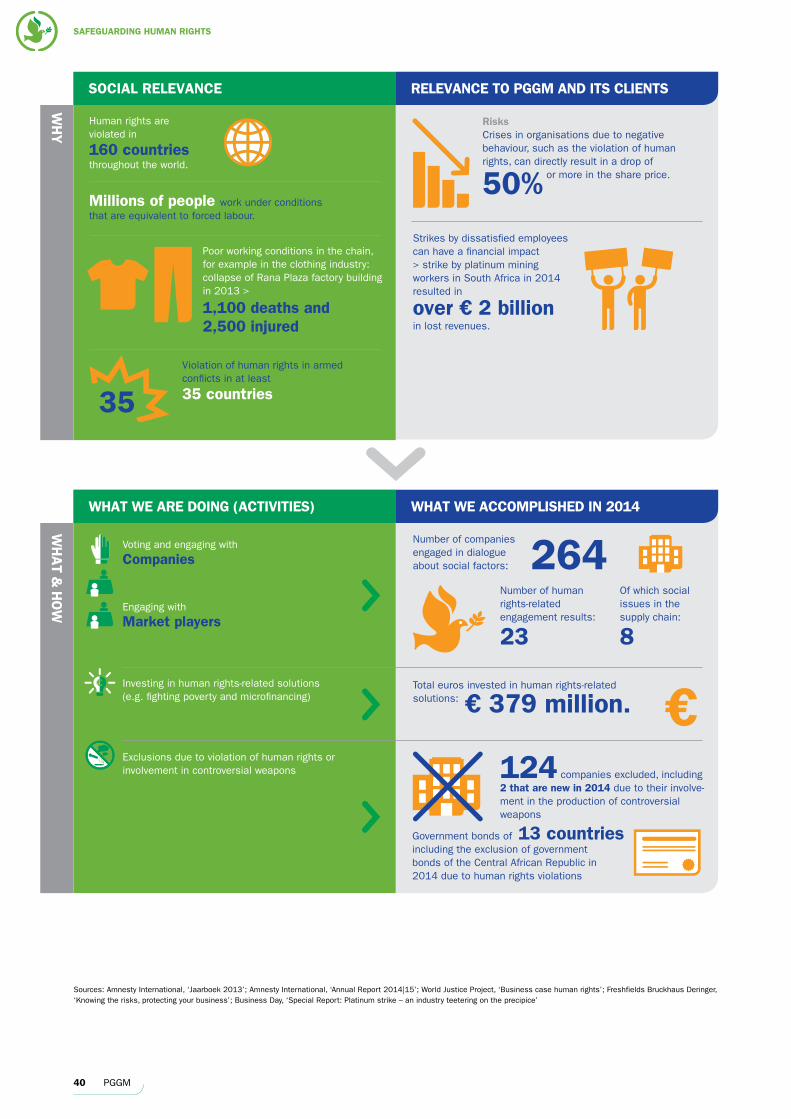

Safeguarding human rights The attainment of fundamental freedoms and human rights is an important condition for achieving sustainable development. We include human rights in the screening process and in the research conducted in support of investment decisions and exert our influence on companies by engaging in dialogue and by voting in order to call them to account for their responsibilities. Parties that are involved in the systematic violation of human rights and that do not show any improvement are excluded in consultation with our clients. At the beginning of 2014, the exclusion of five Israeli banks on behalf of PFZW, on the grounds that they were financing settlements in the occupied Palestinian territories, triggered a series of positive, as well as negative responses. The negative responses suggested that the decision was a politically inspired one. This was not the case; the exclusion is in line with the responsible investment policy frameworks. We evaluated the process and drew lessons learned from it. For example, we need to involve stakeholders more extensively and at an earlier stage in sensitive decisions.

Responsible Investment in PGGM Funds and Mandates

In 2014, we published a new Responsible Investment Implementation Framework. The Implementation Frame-work uses six instruments. We apply ESG integration in all investment processes (1) and stimulate sustainable development by investing in solutions (2). We encourage companies that are in a position to apply ESG improvements to do so by voting (3) and by engaging in a dialogue with them (4). PGGM conducts legal proceedings (5) to recover

8 PGGM

investment losses and enforce good corporate conduct. We exclude companies from PGGM funds that produce controversial weapons or tobacco, or that systematically violate human rights or damage the environment (6). Within PGGM funds we search for commonality with our clients in the guidelines for responsible investment. In client mandates we implement the policy of individual clients. In order to support the differences in the focus of clients and exclusion lists as effectively as possible, the implementation of these instruments can differ somewhat by PGGM fund and mandate.

In relation to investments in solutions, PGGM in 2014 developed proposals for quadrupling investments in solutions over the period leading up to and including 2020 within the climate change, water scarcity, health -care and food security areas of focus. In 2014, these investments amounted to € 4.7 billion. We measured the social impact of all existing investments in solutions. In terms of climate change and water scarcity, we also assess the transition to a circular economy as a problem solving approach. At end 2014, PGGM developed a pilot version of a scan designed to measure the circularity of companies.

With regards to engagement, we increased our focus in the engagement programme in 2014. We primarily enter into a dialogue with legislators and regulators and with companies that have a halo effect in their sector, region or chain. This way we aim to exert greater influence on the improvement of standards at the market level. For example, in the Netherlands we are in discussion with the Ministry of Justice to develop a system of collective compensation proceedings in which a group of misled investors with a shared common interest can instigate legal proceedings. As of the fourth quarter of 2014, PGGM switched from engagement service provider F&C in the UK to GES in Sweden. GES has a focused engage-ment programme that constitutes a good supplement to PGGM’s engagement activities. The programme focuses on companies that do not operate in accordance with international guidelines in the areas of human rights, the environment and corruption. The engage ment activities carried out by PGGM are more focused on strategic areas within the selected themes and on focus markets.

9PGGM

Introduction

Responsible investment is always in development. In recent years we

developed a toolkit with instruments such as voting and engagement,

and we integrated ESG factors into investment activities.

Responsible investment has entered a new phase in which the focus

is shifting from processes to results. PGGM is convinced that financial

and social returns go hand-in-hand. We want to help our clients

realise a valuable future for pension participants on the basis of

sound financial and social returns.

By monitoring the social impact of our investments over multiple years, we will develop the knowledge and experience needed to support the movement toward a more sustainable investment portfolio. In this respect we are continuously looking for points of reference that enable us to take better investment decisions and to actively focus on social added value and on the negative impact of investments, for example on the environment. This approach is not limited to investing in solutions. We apply an integral vision to the entire investment portfolio, a perspective that serves as a basis for taking all investment decisions. In this report we illustrate where we stand in the year 2014.

To give substance to the focused contribution that PGGM as asset manager and administrator of investment funds (the PGGM funds) wants to make to a sustainable world, we identified seven social areas of focus in which we can have an impact, in consultation with our clients. These are areas of focus that our clients and their participants consider important and developments within these themes that we believe will have a material impact on the investments for our clients:

Climate change and reduction of pollution and emissions Water scarcity Healthcare Food security A stable financial system that serves the real economy Good corporate governance Safeguarding human rights

The annual report gets a new look

Due to these developments, the reporting on responsible investment has been given a new look. This year, the report has been structured in accordance with the above-referenced areas of focus and no longer on the basis of our toolkit. For each area of focus we report our targeted social contribution, what we did to accomplish it and what we achieved in 2014 (Section 2). We use all of our responsible investment instruments (Section 1) to make a social contribution within the areas of focus. This Annual Report also provides an overview of the responsible investment developments related to each PGGM fund and related to a number of mandates (Section 3). Quantitative overviews related to the activities are included in the appendices.

10 PGGM

1. Frameworks for Responsible Investment

“As asset manager of

pension funds, we assess

both financial and social

returns over the long term.”

11PGGM

1.1 Beliefs and Principles for Responsible Investment

Although there has been enormous growth in prosperity over the past century, stability and economic development are increasingly threatened by global issues. These include climate change, the scarcity of natural resources such as water and minerals, rising food prices and income inequality. The way in which such issues have been tackled in past decades is no longer viable. This will impact future investment results. Sustainability and viability are therefore key to our activities over the long term. To safeguard this, PGGM, together with its clients, has developed Beliefs and Principles for Responsible Investment and has published them on its website.

BeliefsFor PGGM, responsible investment means not only consciously taking account of ESG factors in investment decisions and exerting positive influence through the investments, but also looking critically at our own behaviour and that of the entities in which PGGM invests or with which it cooperates. Through its responsible investment activities PGGM seeks to contribute to responsible, stable, good investment results for its clients. This objective is based on the following beliefs:

Responsible investment pays off: PGGM firmly believes that sustainability factors materially influence the risk-return profile of the investments and that this influence will steadily increase in the future.

No good and stable return in the long term without sustainable development: PGGM firmly believes that sustainable development is necessary in order to generate good and stable investment returns for our clients in the long term.

The driving force of capital: PGGM firmly believes that by leveraging the driving force of investments for our clients it can and must make a positive contribution to sustainable development through its investment decisions.

PrinciplesPGGM aims to be an excellent cooperative pension fund service provider and to make a substantial contribution on sustainability issues. We have formulated ten basic principles for responsible investment that we implement in making investment decisions.

The basic principles are as follows:1. Responsible investment is an integral part of PGGM’s

investment activities.2. PGGM has a clear focus for responsible investment

activities.3. PGGM critically reviews its own behaviour and the

behaviour of parties in the financial sector with which it cooperates in order to achieve a stable and sustainable financial system.

4. PGGM acts as an active owner on behalf of its clients and on behalf of the investment funds it administers.

5. PGGM critically reviews the behaviour and activities of entities in which it invests on behalf of its clients.

6. PGGM sets a minimum standard for investments for clients. When this standard is not met, we exclude companies or government bonds.

7. Through (part of the) investments for clients PGGM seeks to contribute actively to solutions to societal issues.

8. Collaboration with institutional investors and other market participants leads to synergy and greater impact.

9. PGGM actively seeks methods to demonstrate the financial and social impact of the choices with regard to responsible investment.

10. PGGM is transparent and accountable with regard to responsible investment activities.

1.2 Policy Advice

One of the services provided by PGGM is to advise clients on their responsible investment policy. The Responsible Investment and the Strategy and Fiduciary Advice depart-ments of PGGM Strategic Advisory Services B.V. (PSAS) closely cooperate in this area. As an investment company, PSAS is licensed to provide investment advice. Advice concerning responsible investment policy is substantively reviewed by the Investment Policy Committee. In 2014, we advised several clients concerning the refinement of their policy frameworks. PFZW and the Stichting Pensioenfonds voor de Architectenbureaus (Pension Fund Foundation for Architecture Firms) published a new Responsible Invest-ment policy. In addition, PGGM provided PFZW with advice concerning the translation of its 2014-2020 Policy Framework into a long-term investment policy. A number of ambitious goals designed to anchor sustainability in PFZW’s investments were formulated:

Quadrupling of the positive sustainability contribution. Halving the portfolio’s negative footprint. Systematically integrating sustainability in all steps of

the investment process.

12 PGGM

In 2014, PGGM also provided PFZW with advice concerning a responsible compensation policy. The objective of this policy is to take a position against the most excessive forms of compensation by listed companies and financial service providers. For companies, the remuneration, i.e. the fixed salary, the variable compensation in shares or in cash and the non-financial allowances, was reviewed. For financial service providers, the fees, i.e. the compensation received in exchange for the services provided, and the individual return on investments were reviewed. However, what is considered excessive varies by individual, market, as well as invest ment category. It therefore is a challenge to define this precisely. To implement this policy, PGGM starts off with the most excessive forms of compensation. We compare companies and financial institutions and specifically start from top to bottom with the most excessive compensation practices. PGGM has formulated guidelines for this purpose (Section 2.5.3).

1.3 Implementation of Responsible Investment

We aim to provide optimal support to our clients to help them develop and implement ESG activities. This involves continuously improving ESG integration (Section 3) and developing new activities, such as the expansion of investments in solutions, and measuring and reducing the CO2 footprint (Section 2). The effective implementation of these activities enables our clients to achieve their sustainability objectives. By communicating on these activities to stakeholders we aim to trigger wider interest and growth in the area of responsible investment.

The Responsible Investment Implementation Framework published in 2014 contains detailed implementation guidelines for implementing various activities in the field of responsible investment. Each client has its own policy with particular emphasis in this field. The Implementation Framework seeks commonality within the PGGM funds, while providing scope to meet clients’ specific policy requirements through internal and external asset management. That means that the following activities that we undertake in the field of responsible investment do not always apply to all clients.

PGGM manages various PGGM mutual funds in which multiple clients participate.

PGGM provides asset management services to individual clients.

PGGM advises clients on direct investments through mandates or funds other than those managed by PGGM.

The Beliefs and Principles for Responsible Investment apply to all of PGGM’s investment and advisory activities that fall within these three categories. The Implementation Framework applies to the PGGM mutual funds, to the activities of PGGM Treasury B.V. and to mandates managed internally by PGGM. The individual client’s policy prevails within these mandates. Within PGGM funds we search for commonality with our clients in the guidelines for responsible investment. When taking decisions on and within the Implementation Framework, PGGM goes through an extensive process that takes the clients’ considerations into account, usually through an opinion issued by the Advisory Board Responsible Investment (ABRI) and the Participants’ Meeting.

AIFMD License

In April 2014, we were notified that the Netherlands Authority for the Financial Markets (AFM) had granted PGGM an Alternative Investment Fund Managers Directive (AIFMD) license. PGGM was the first pension fund service provider in the Netherlands to receive this license. The AIFMD license provides investment funds with a ‘European investments passport’. The AIFMD license guidelines co-incided with plans within PGGM to separate investment policy advice and asset management. With this in mind, in 2014, a full-fledged Fiduciary Advice department was set up by the sister company PGGM Strategic Advisory Services (PSAS). This department formulates and evaluates client investment mandates. Accommodating Fiduciary Advice in a separate entity has created a true separation of activities.

13PGGM

PGGM Beliefs and Principles

PGGM Funds

1

Participants’ Meeting

Externally Managed

Mandates & Funds

3

Mandates Managed

Internally by PGGM

2

Responsible Investment

AdvicePGGM Responsible Investment Implementation Framework

(Implementation and Advice)

The assets which PGGM has under management and advice on behalf of its clients amounted to € 181.9 billion at year-end 2014, including € 172 billion within (1) the PGGM funds and (2) the mandates managed internally by PGGM. This report covers only the responsible investment activities carried out by PGGM in respect of the € 172 billion (total of 1 and 2 in Figure 1.1). Section 3 contains a summary of the activities and results for each PGGM fund and a number of internally managed mandates.

ABRI and Participants’ Meeting

The ABRI is an advisory body that consists of five independent external experts from whom PGGM and its clients can obtain advice and with whom they can discuss issues relating to responsible investment. To increase the opportunities for consultation in the PGGM funds, we also organise a Participants’ Meeting for clients, at least once a year. This meeting gives the various participants in a PGGM fund the opportunity to discuss and take decisions on fund-specific subjects with the PGGM fund manager and other participants. This meeting took place on three separate occasions in 2014. Subjects such as the exclusion of the Israeli banks, the conflict between Russia and Ukraine, issues concerning a sustainable financial system, own behaviour and an acceptable remuneration policy were discussed by the ABRI, as well as in the Participants’ Meeting. These subjects are dealt with later in this report.

Clients’ Responsible Investment Policy

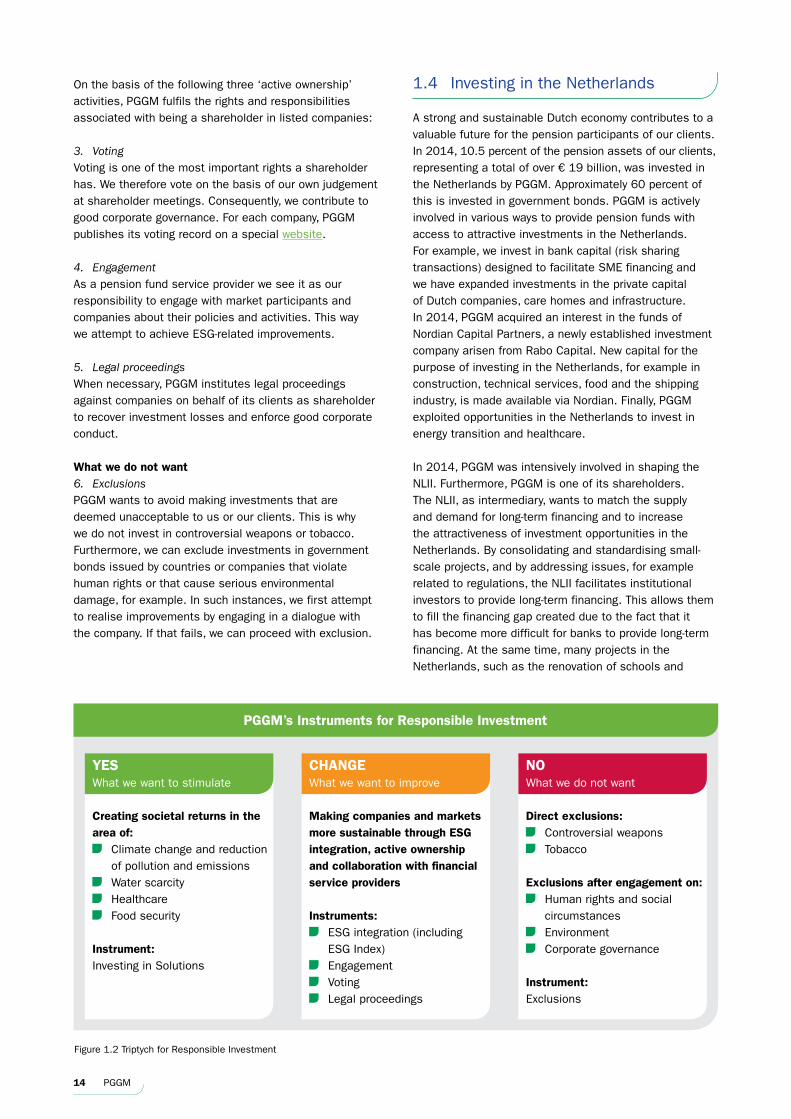

Instruments for Responsible InvestmentWe apply six instruments in support of the implementation of responsible investment activities. We apply these instruments for the purpose of (1) contributing to social solutions; (2) encouraging companies in a position to make ESG improvements to do so; and (3) excluding companies that carry out activities that we do not want to support. Figure 1.2 illustrates the triptych for responsible investment.

What we want to stimulate1. Investments in Solutions Investments in solutions for social development are clearly defined investments that not only contribute to the portfolio’s financial return, but are also intended to generate social added value. We invest in solutions for climate change, water scarcity, healthcare and food security. Section 3 contains additional information about measuring social return.

What we want to improve2. ESG integration into investment processesThe environment, social aspects and the quality of corporate governance can affect our clients’ return on investment. Conversely, the companies and agencies in which we invest can have an impact on the world around them. PGGM therefore firmly believes that taking account of ESG factors in the investment processes contributes to good risk management and can ensure that achieving financial returns is coupled with sustainable social improvements.

Figure 1.1 Framework for Responsible Investment

14 PGGM

On the basis of the following three ‘active ownership’ activities, PGGM fulfils the rights and responsibilities associated with being a shareholder in listed companies:

3. VotingVoting is one of the most important rights a shareholder has. We therefore vote on the basis of our own judgement at shareholder meetings. Consequently, we contribute to good corporate governance. For each company, PGGM publishes its voting record on a special website.

4. EngagementAs a pension fund service provider we see it as our responsibility to engage with market participants and companies about their policies and activities. This way we attempt to achieve ESG-related improvements.

5. Legal proceedingsWhen necessary, PGGM institutes legal proceedings against companies on behalf of its clients as shareholder to recover investment losses and enforce good corporate conduct.

What we do not want6. ExclusionsPGGM wants to avoid making investments that are deemed unacceptable to us or our clients. This is why we do not invest in controversial weapons or tobacco. Furthermore, we can exclude investments in government bonds issued by countries or companies that violate human rights or that cause serious environmental damage, for example. In such instances, we first attempt to realise improvements by engaging in a dialogue with the company. If that fails, we can proceed with exclusion.

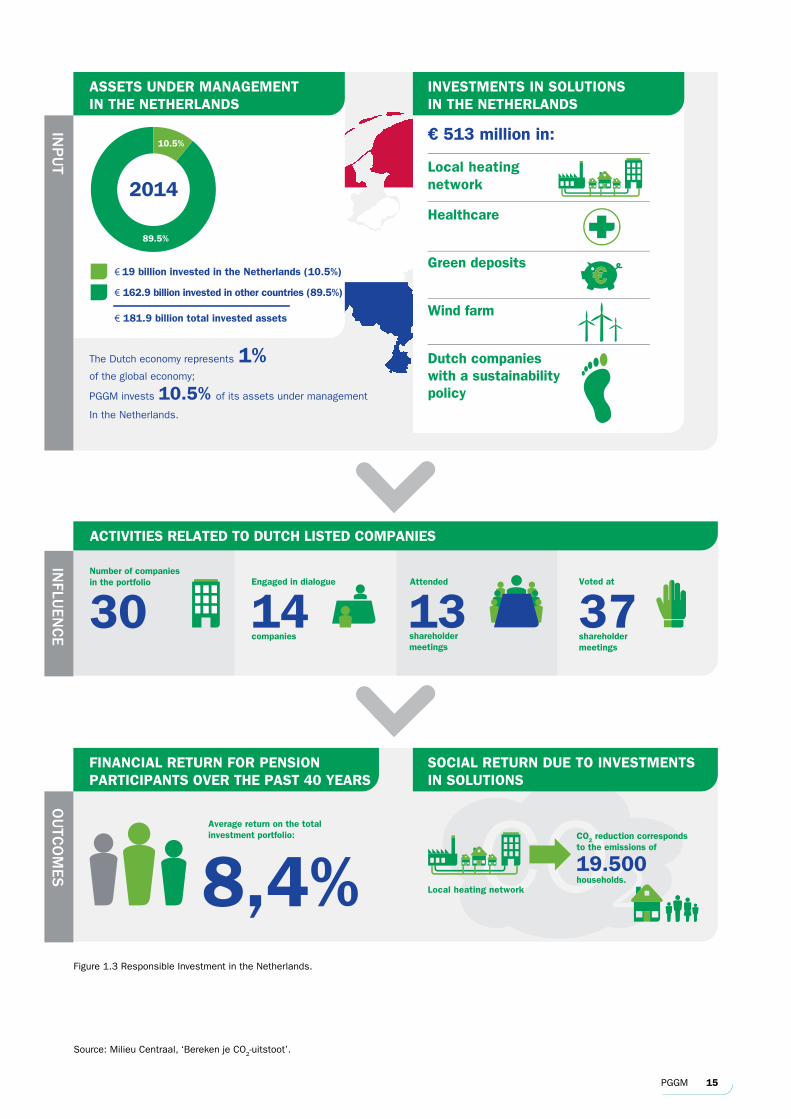

1.4 Investing in the Netherlands

A strong and sustainable Dutch economy contributes to a valuable future for the pension participants of our clients. In 2014, 10.5 percent of the pension assets of our clients, representing a total of over € 19 billion, was invested in the Netherlands by PGGM. Approximately 60 percent of this is invested in government bonds. PGGM is actively involved in various ways to provide pension funds with access to attractive investments in the Netherlands. For example, we invest in bank capital (risk sharing transactions) designed to facilitate SME financing and we have expanded investments in the private capital of Dutch companies, care homes and infrastructure. In 2014, PGGM acquired an interest in the funds of Nordian Capital Partners, a newly established investment company arisen from Rabo Capital. New capital for the purpose of investing in the Netherlands, for example in construction, technical services, food and the shipping industry, is made available via Nordian. Finally, PGGM exploited opportunities in the Netherlands to invest in energy transition and healthcare. In 2014, PGGM was intensively involved in shaping the NLII. Furthermore, PGGM is one of its shareholders. The NLII, as intermediary, wants to match the supply and demand for long-term financing and to increase the attractiveness of investment opportunities in the Netherlands. By consolidating and standardising small-scale projects, and by addressing issues, for example related to regulations, the NLII facilitates institutional investors to provide long-term financing. This allows them to fill the financing gap created due to the fact that it has become more difficult for banks to provide long-term financing. At the same time, many projects in the Netherlands, such as the renovation of schools and

Creating societal returns in the area of:

Climate change and reduction of pollution and emissions

Water scarcity Healthcare Food security

Instrument: Investing in Solutions

Making companies and markets more sustainable through ESG integration, active ownership and collaboration with financial service providers

Instruments: ESG integration (including

ESG Index) Engagement Voting Legal proceedings

Direct exclusions: Controversial weapons Tobacco

Exclusions after engagement on: Human rights and social

circumstances Environment Corporate governance

Instrument: Exclusions

PGGM’s Instruments for Responsible Investment

YESWhat we want to stimulate

CHANGEWhat we want to improve

NOWhat we do not want

Figure 1.2 Triptych for Responsible Investment

15PGGM

CO2

INPUT

ASSETS UNDER MANAGEMENT IN THE NETHERLANDS

The Dutch economy represents 1%of the global economy;

PGGM invests 10.5% of its assets under management

In the Netherlands.

INVESTMENTS IN SOLUTIONS IN THE NETHERLANDS

INFLU

ENCE

ACTIVITIES RELATED TO DUTCH LISTED COMPANIES

OUTC

OMES

€ 19 billion invested in the Netherlands (10.5%)

€ 162.9 billion invested in other countries (89.5%)

€ 181.9 billion total invested assets

2014

89.5%

€ 513 million in:

Local heating network

Healthcare

Green deposits

Wind farm

Dutch companies with a sustainability policy

30Number of companies in the portfolio Engaged in dialogue Attended

companies shareholder meetings

8,4%Average return on the total investment portfolio: CO2 reduction corresponds

to the emissions of

19.500households.

Local heating network

10.5%

14Voted at

shareholder meetings

3713

FINANCIAL RETURN FOR PENSION PARTICIPANTS OVER THE PAST 40 YEARS

SOCIAL RETURN DUE TO INVESTMENTS IN SOLUTIONS

Figure 1.3 Responsible Investment in the Netherlands.

Source: Milieu Centraal, ‘Bereken je CO2-uitstoot’.

16 PGGM

investments in companies, are too small-scale for investors such as PGGM. This causes the costs per investment to be too high for an attractive return. The NLII, in close cooperation with government, is looking for structures that would make it possible to finance such projects.

Figure 1.3 provides an overview of responsible investment in the Netherlands. In total, over € 500 million has been invested in solutions in the Netherlands via PGGM. This includes investments in:

Gilde Healthcare Services, a fund that invests in health-care in various countries, including the Netherlands.

The Rabobank Duurzaam Deposito, a fund used by the Rabobank to make sustainable investments in the Netherlands.

The Ampèrefonds, this fund owns a 32 percent share in the Koegorspolder wind farm in the Province of Zeeland.

Ennatuurlijk local heating network (Section 2.1.3). The Responsible Equity Portfolio (REP), a portion of

which is invested in the Dutch companies Unilever and DSM. Unilever is a leader in the use of sustainable raw materials and the majority of its products meets or exceeds globally recognised nutrition guidelines. Unilever’s goal is to integrate sustainability into normal daily life. DSM too is a key proponent of sustainability and circularity. Together with the World Food Program, DSM is working to increase the nutritional value of emergency aid for 25 to 30 million people in 2015. In addition, DSM is a leader in the development of sustainable and innovative products and solutions with measurable ecological benefits.

In 2015, we will investigate the opportunities to further expand investments in social issues in the Netherlands on behalf of our clients.

1.5 Long-term Investment

Due to their long-term commitments, pension funds are long-term investors. Long-term investments best fit the pension commitments and carry lower risk than short-term investments. In view of the major importance of long-term investments for achieving the pension ambitions of our clients, PGGM develops various initiatives in this area, generally in close cooperation with other institutional investors. For example, PGGM participates in a network of Chief Investment Officers in the Netherlands (the CIO Exchange), in which experiences about long-term investments are exchanged. Furthermore, in 2014, PGGM joined McKinsey’s Focusing Capital on the Long Term initiative and the Canada Pension Plan Investment Board (CPPIB) that, among other things, attempts to stimulate long-term behaviour among investors and among the companies in which it invests. The shareholdership in NLII furthermore is an example of cooperation in the area of long-term investment.

Infrastructure

Various organisations are pointing to the existence of a major infrastructure financing gap throughout the world. This means that the demand for financing infrastructure is significantly larger than the supply. McKinsey estimates the demand for investments in land-based transport, telecom, electricity and water at € 52 billion up to 2030. The Netherlands too is faced with major investments in infrastructure, such as the Delta Plan and the Energy Accord of the Social and Economic Council of the Netherlands (SER), among others. In the letter announcing the NLII on Budget Day 2013, the Minister of Economic Affairs projected a further investment need for infrastructural projects amounting to approximately € 20 billion up to 2020. An increasingly larger portion of this is realised on the basis of Public Private Partnerships (PPP), whereby investors directly finance a project and share the risks.

Infrastructure is an attractive investment for several reasons. It is long-term and has a high, stable expected return, and sometimes includes an inflationary component that matches the obligations of pension funds. Furthermore, in spite of higher interest charges, the taxpayer receives more value for his money because projects are better planned and implemented, and because of optimal risk sharing between public and private partners. In the World Economic Outlook dated October 2014, the IMF contends that good infrastructure pays for itself because it contributes to economic growth. Investments in sustainability are a specific example of this. Investments in infrastructure conse-quently are perfectly suited to combining financial and social returns.

17PGGM

“To give substance to the focused contribution that PGGM

wants to make to a sustainable world, we formulated

seven social areas of focus in which we can have an

impact, in consultation with our clients. These are themes

that our clients and their participants consider important

and that can materially affect the investments made.”

2. Responsible Investment in Areas of Focus

18 PGGM

WH

YW

HA

T & H

OW

SOCIAL RELEVANCE

WHAT WE ARE DOING (ACTIVITIES)

RELEVANCE TO PGGM AND ITS CLIENTS

WHAT WE ACCOMPLISHED IN 2014

Opportunities

Over € 39 trillion in investments in sustainable technolo-gies and clean energy is required to reduce CO2 levels, so that the global rise in temperature by 2050 remains limited to 2°C in relation to pre-industrial times.

A rise of more than 2ºC > unacceptable consequences for nature and society.

To ensure the global rise in temperature stays below 2°C, a CO2 concentration of less than 450 PPM (parts per million)

is required. In 2014, the 400 PPM limit was exceeded for the �rst time in history.

Average temperatures in the 20th century have risen by

0,6º C

This shift is expected to result in fossil fuel savings amounting to

€ 103 trillion

10

Over the next 100 years average temperatures are expected to rise by

1.1 to 6.4º C

Risksclimate change

restrictions on the exploitation of fossil energy reserves

risk of downward valuation of energy companies

Number of climate change-related engagement results:

Engaging with

Market players and policymakers

Investing in climate change-related solutions

Stimulating green growth at companies

European Council engagement result:

40% CO2 reduction target by 2030Total euros invested in climate change-related solutions:

€ 1.2 billion. New investments in climate change-related solutions in 2014:

GDF Suez Green Bond: Ennatuurlijk heating network

annual CO2 savings are equivalent to the CO2 reduction of

Total CO2 avoidance due to investments in sustainable energy funds (incl. wind farm)

> 39,000 households.

253,493 hectares of sustainably managed forests

(over 500,000 football fields)

Redwood: 10% savings in energy costs due to investments in solar panels for logistics centresAdecoagro: reduction in CO2 emissions via sugar ethanol > 80% compared to petrol

2 million solar panels

Voting and engaging with

Companies

N O2

CO2

CH4

CFC

6.41.1

CLIMATE CHANGE AND REDUCTION OF POLLUTION AND EMISSIONS

Sources: Groene Ruimte, ‘Dossier klimaatverandering en de groene ruimte’; US department of commerce, National Oceanic & Atmospheric Administration; Natuur & Milieu, ‘Pensioenfondsen investeren nauwelijks in duurzame energie’; International Energy Agency, ‘Energy Technology Perspectives 2014’

19PGGM

2.1.1 Why Climate Change as an Area of Focus?

Climate change has been a key area of focus for PGGM for years. The warming of the earth by two degrees centigrade can result in extreme weather conditions, drought and floods. This can have an adverse impact on society and on the valuations of companies in which we invest the pension assets of our clients. For example, investment risks could increase because property may become flooded, political instability may increase or because companies may lose value if they are no longer permitted to exploit their coal reserves to limit CO2 emissions (stranded assets). On the other hand, investments in wind farms, for example, can contribute to solving the climate change issue while at the same time creating financial returns.

2.1.2 What Are We Doing in This Area of Focus?

We are convinced that reducing the negative effects of climate change requires more green growth, i.e. economic growth based on more sustainable energy and a reduction in the wastage of raw materials. Green growth offers opportunities. On behalf of our clients, we are currently investing several hundreds of millions of euros in sustainable energy, such as wind energy at sea and on land, and in clean technology that contributes to greater efficiency and reduced wastage of raw materials. Where this is consistent with the pension ambitions of our clients, we want to grow these investments over the coming years. However, green growth does not just happen on its own. Political and executive leadership is also required to create preconditions that keep invest-ments in green growth attractive; policy that over the long term provides greater certainty of stable and high returns. By engaging in a dialogue with policymakers, PGGM attempts to ensure that the emission of greenhouse gases will be assigned a fair price, that innovation in the area of energy efficiency and sustainable energy is supported, that policy is reliable and that the undesirable effects of the supervision of financial institutions that impede investment in green growth are critically assessed.

2.1.3 How Did We Action This in 2014?

Demand for Climate PolicyIn 2014, we regularly made our voice heard by policymakers throughout the world. At the beginning of the year, together with the Institutional Investors Group on Climate Change (IIGCC), we participated in various meetings with EC officers to point out the need for an ambitious climate plan for 2030. A number of items that we lobbied for have been included in the EC’s ‘2030 Climate and Energy Plan’, namely a binding 40 percent reduction target in greenhouse emissions, reform of the CO2 trading system and a greater focus on improvements in the area of energy efficiency. This Plan, which was adopted by the European Council in October 2014, constitutes an important first step in the energy transition at the European level. In September 2014, during the United Nations Climate Summit, together with approximately 350 other major investors throughout the world, we declared that climate change constitutes a risk to investments. We indicated that the lack of leadership and policy for green growth is particularly an area of concern. In a joint declaration, the group of investors promised to make a greater contribution to solutions to climate change by increasing investments in green growth on the one hand, and by encouraging companies in which we invest to adopt behaviour that contributes to green growth, on the other hand. For example, we expect utility companies to develop plans that reduce their dependence on fossil fuels and we ask oil, gas and coal companies to develop strategies designed to use and produce more clean energy. We have asked governments throughout the world to develop policy that truly makes this possible. This is an important message that we will be repeating regularly during the run-up to the Climate Summit in Paris in December 2015.

Measuring and Reducing EmissionsTo further limit the risks of climate change for investments, we have started to identify the CO2 footprint of our equity portfolio. To this end, PGGM signed the ‘Montreal Pledge’ in September. The signatories to this pledge promise to measure and report on the emission of greenhouse gases of their investment portfolio. For years, PGGM and other investors have been asking the companies in which we invest to report their emissions. We have been reporting PGGM N.V.’s footprint for several years. We are now expanding this footprint measurement to include insight into the emissions generated by the investment portfolio. Indeed, we not only want to make an active and focused

2.1 Climate Change and Reduction of Pollution and Emissions

20 PGGM

“The consequences of climate change

constitute risks to investments and

society. It is consequently important

for us to contribute to counteracting

climate change.”

contribution to climate change solutions with a specific portion of our investments; we also want to minimise the contribution of the rest of the portfolio to the CO2 problem and where possible focus on green growth. That starts with knowledge about the size of the footprint and the areas with the highest emissions. In 2014, we started to identify the CO2 footprint of the equity portfolio managed by PGGM. We are developing a method that we will use to calculate PGGM’s share of the total emissions represented by our ownership in each company. We will aggregate the amounts for the total CO2 footprint. We are using the emission data provided by a specialised data supplier for this purpose. In 2015, we will publish the total footprint of the equity portfolio and we will develop a reduction plan. This plan will include the focused use of all existing responsible investment instruments, such as engagement and voting, but we will also look at new instruments that will entail portfolio allocation decisions.

New Investments in Green SolutionsPGGM also made direct investments in climate change solutions in 2014. An example is the investment made by the PGGM Credits Fund in GDF Suez green bonds. These green bonds are used to finance projects in renewable energy, such as wind energy, and in energy efficiency, such as heating networks. The bond finances GDF Suez’ ambitious environmental policy whose objective is to increase the generation of renewable energy by 50 percent between 2009 and 2015, and to increase the energy efficiency of its business activities in Europe by 40 percent by 2018. Utilities are crucial to the growth of the market in green bonds. GDF Suez is a leader by disbursing € 2.5 billion up to date, with additional projects in the pipeline. PGGM wants to contribute to the standardisation of this market, so that green bonds will become a mature investment category. This is why the Fund Manager of the PGGM Credits Fund

has become a member of the Green Bond Principles Group.

In addition, PGGM Infrastructure Funds together with energy service company Dalkia has acquired the Ennatuurlijk heating network from Essent. Ennatuurlijk is a partner for sustainable energy initiatives in the Netherlands and following its acquisition a direction has been set whereby Ennatuurlijk will produce energy locally. It does this by collaborating on various projects, such as efficient heating and cooling, biomass energy plants, and biomass and manure digestion plants. For example, a single cow can provide seven households with sufficient heat on the basis of such digestion plants. In addition, Ennatuurlijk makes optimal use of the residual heat in its network. This way the company, together with its local partners, contributes to making the Netherlands increasingly sustainable. The annual CO2 saving realised by Ennatuurlijk corresponds to approximately two million solar panels.

The investment in Ennatuurlijk made the news several times last year, for example due to the questions asked by residents concerning the connection charges they pay for the heating networks. Ennatuurlijk indicated that it complies with the rates set by the Netherlands Authority for Consumers & Markets (ACM) in line with the Heating Supply Act, with the basic premise being that the costs are equal to central heating using gas. The investment in Ennatuurlijk highlights a dilemma that we more frequently encounter when we invest in solutions. On the one hand we encounter interest groups that encourage energy networks to increase their sustainable energy. These parties value the investment in Ennatuurlijk. On the other hand we encounter (local) interest groups that resist the legislative frameworks and the monopolistic character of the service. The latter group does not agree with

21PGGM

Ennatuurlijk’s pricing in accordance with the Heating Supply Act and consequently has instituted legal proceedings. Ennatuurlijk is prepared to cooperate in the investigation into the fairness of the rates by independent experts. This example demonstrates that investing in solutions to an environmental problem does not mean that there are no ESG risks in other areas, such as the social domain in this case. In making its investments, PGGM tries to take the interests of all stakeholders into account. This is also true of its investment in Ennatuurlijk.

Mexican WindmillsIn our 2013 Annual Report, we indicated that investing in solutions can at times be complex. We illustrated this on the basis of the investment of PGGM Infrastructure Funds in the Mexican Mareña Renovables wind farm. As a result of social and political resistance, the construction of this wind farm has not yet begun. In consultation with federal and local government organisations, opportunities were explored to develop this wind farm at an alternative site. In 2014, a new site was found, approximately 40 kilometres to the north of the original project. To avoid social problems with this project and to safeguard the right to consultation by the indigenous population as provided for in ILO Convention 169, the Mexican government has, for the first time for a project of this nature, initiated a consultation process. On the basis of an elaborate communication programme, the stakeholders were informed on the various aspects of the project, including the benefits and potential negative effects, such as noise pollution. In addition, the parties that are directly involved were given the opportunity to jointly decide on investments in social projects. The consultation is taking place in a complex political and social arena, in which the dissatis-faction about the fact that a similar consultation process did not take place in earlier wind farm projects still plays a key role. PGGM is closely monitoring the consultation process on the basis of regular updates provided by the local management team and by attending various sessions locally. If this process is successfully completed and if a number of conditions are met, we will in all probability invest in the wind farm at the new site.

Green Growth within the Existing PortfolioPGGM also exerts influence to promote green growth within the existing investment portfolio. For example, PGGM’s Private Real Estate team took the initiative to introduce the two real estate managers Investa and Redwood to each other so that they could share their ESG strategies. Redwood was inspired by Investa, a leader in sustainability, and subsequently took the initiative of signing a contract with an energy company for the installation, management and maintenance of solar panels on the roofs of logistics centres. Redwood expects the solar panels to be operational in the first half of 2015. The investment in the energy company is expected

to result in a 10 percent energy savings and thus provides for a higher return on the investments via Redwood.

Another example of green growth in the investment portfolio is Adecoagro, a producer of food and renewable energy in South America. In 2014-2015, Adecoagro will expand its combined sugar and ethanol plant in Brazil. As a shareholder in Adecoagro on behalf of PFZW, we support this development. After the expansion, Adecoagro will be able to process 10.2 million metric tonnes of sugar cane in its three plants. The new plant will be able to store 120,000 tonnes of sugar and 40,000 cubic metres of ethanol. In contrast to the exhaustible energy sources coal and oil, ethanol is a renewable energy source. It is produced from sugar cane plants that accrete year after year, provided they are replanted every six to eight years. The expansion of the production of clean, renewable sugar cane has the potential of significantly reducing global dependence on fossil fuels. In comparison to petrol, sugar cane ethanol reduces the emission of greenhouse gases by more than 80 percent. This represents the largest reduction in greenhouse gases in comparison to any other mass-produced biofuel at the present time. Furthermore, the sugar cane does not originate from land that was used by cereal farmers or for mills. This means that the production of sugar and ethanol does not conflict with safeguarding food security (Section 2.4).

2.1.4 Outlook

In 2015, we will publish a CO2 footprint reduction plan for the equity portfolio. In addition, we will continue to engage in a dialogue with companies in which we have invested in order to encourage them to reduce their CO2 emissions and wastage of raw materials. In addition, in 2015, we will increase our focus of the dialogue with policymakers whereby we will continue to remind them of the necessity of sound climate policy and demonstrate the role investors can play in the realisation of global climate agreements that hopefully will be formulated in Paris at the end of 2015. Finally, we will investigate opportunities to make more investments in climate change solutions over the coming years.

CLIMATE CHANGE AND REDUCTION OF POLLUTION AND EMISSIONS

22 PGGM

WH

YW

HA

T & H

OW

SOCIAL RELEVANCE

WHAT WE ARE DOING (ACTIVITIES)

RELEVANCE TO PGGM AND ITS CLIENTS

WHAT WE ACCOMPLISHED IN 2014

Opportunitiesinvestment opportunities in water supply over the next 15 years:

€ 67,000 billion

Number of water scarcity-related engagement results:

CDP Water ranks companies on ‘business value at water risk’

Total euros invested in water scarcity-related solutions: € 244 millionNew investments in water scarcity-related solutions in 2014:

Chinese water puri�cation plant: > 210 million tonnes of clean water per year

Parkway Parade shopping centre Singapore: annual water savings of 30% through use of rainwater and water-ef�cient taps.

Savings equivalent to consumption by 343 households.

50% of the world population: shortage of clean water by 2030

without drinking water780 million people

2030demand for water will outstrip supply by 40%

Risksdrought results in water shortage for companies, particularly in the power generation, agricultural sector and mining industry

> € 90 billion in annual losses due to water shortages

Voting and engaging with

Companies

Engaging with

Market players

Stimulating water savings by companies

Investing in water scarcity-related solutions

210milliontonnes

3

WATER SCARCITY

Sources: Unicef, ‘Water, sanitatie en hygiëne’; 2030 Water Resources Group, ‘Charting our water future’; UN Food and Agriculture Organization, ‘How to feed the world in 2050’; Bank of America Merrill Lynch, ‘Blue Revolution – global water primer’

23PGGM

2.2 Water Scarcity

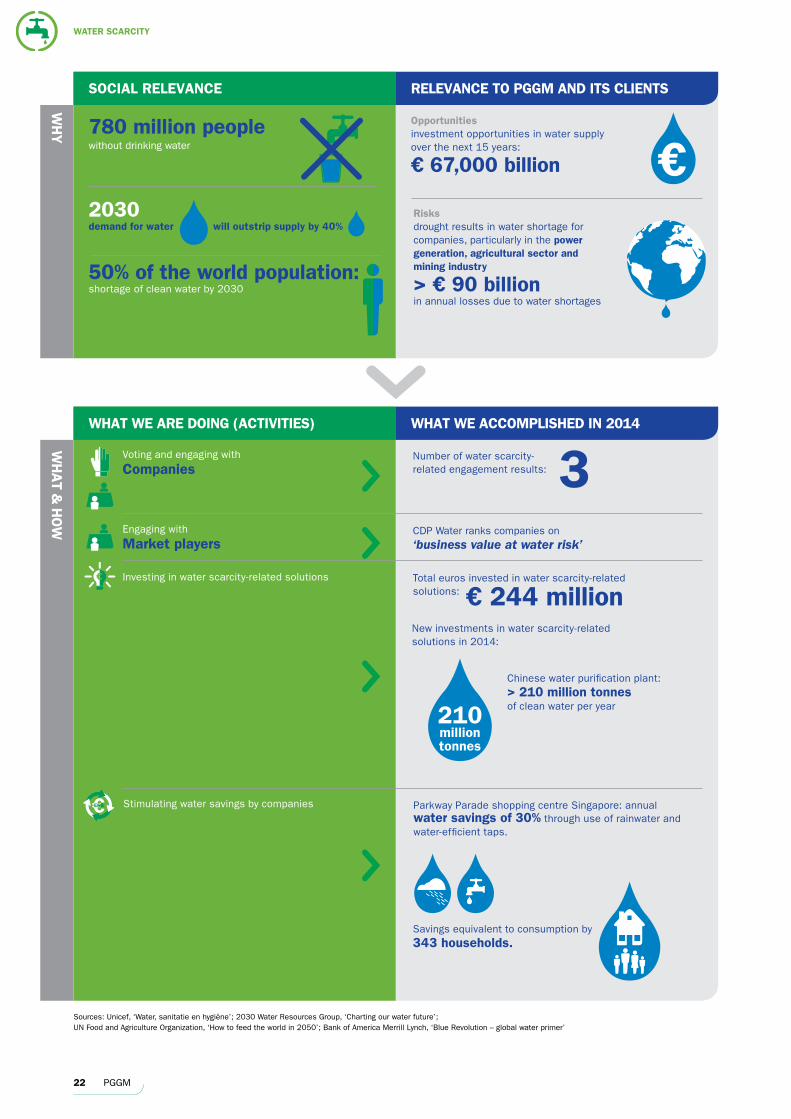

2.2.1 Why Water Scarcity as an Area of Focus?

Water scarcity is an increasing threat to economic growth and to human wellbeing. Insufficient access to clean water has been identified as one of the major global issues by the World Economic Forum. Particularly in dry countries, such as China, India and the United States, the water supply is under high pressure due to the rapidly growing demand for and the declining availability of water. In 2030, the expected demand for water will be 40 percent higher than the supply and almost half of the world population will be faced with shortages of clean water. This also affects the companies in which PGGM invests on behalf of its clients, especially in sectors that are highly dependent on water, such as power generation and agriculture. The continuity and profitability of these companies could be negatively affected by a lack of water. Aside from risks, water scarcity also provides attractive investment opportunities, for example in water purification plants. According to the Organisation for Economic Cooperation and Development (OECD), € 68,000 billion will be required over the coming 15 years for investment in water infrastructure.

2.2.2 What Are We Doing in This Area of Focus?

PGGM can contribute to counteracting water scarcity in order to promote population health and economic growth. The objective is to sustainably increase water security for people and companies in regions where the availability, access to and the quality of the water supply is inadequate. PGGM’s engagement programme is focused on providing better insight into the business value at water risk, that is the business value that is at risk due to exposure to water problems. This involves risks to company production sites, as well as risks within the supply chain ranging from raw

materials to the use of end-products. We encourage market players to develop relevant and comparable water risk data for general information platforms for investors, such as Bloomberg. This would enable investors to assign a lower weight to companies with a high dependency on water and low water security. Relevant, comparable data could also lead to lower capital costs for companies that invest in the efficient use of water and limit water risks. In addition, PGGM invests in water scarcity solutions, in public markets on the basis of equity and bonds, as well as in private markets, for example via infrastructure in private equity. We want to increase the investments in solutions, such as wastewater purification and in water-saving technologies, such as water meters, drought-resistant crops and desalination plants.

2.2.3 How Did We Action This in 2014?

Investment Risks Caused by Water IssuesThe Carbon Disclosure Project (CDP) is the largest platform for voluntarily reporting water-related information by companies. Until now, companies primarily provided information about their water consumption. However, that information is not sufficient for investors. Investors want to know what the water scarcity and pollution-related risks are for a company, and consequently their investment risks. This is why CDP, based on advice received from PGGM and Norges Bank, in 2014 increased the relevance of the annual Water Information Request for investors. PGGM subsequently encouraged the CDP to make the information provided by companies about water risks and the quality of their water risk management comparable. Providing comparable data at the company level makes it possible to rank companies. This also makes it possible for index investors to identify opportunities and threats.

‘To enable economic growth, safeguard the continuity of companies

and secure access to clean drinking water, a significant increase

in investments in water infrastructure and water management is

essential.’

24 PGGM

CDP’s commitment to score and rank companies in terms of water risk is an important step towards a larger platform, such as Bloomberg, where all investors have access to this material information. This information is available from 2015. Not all companies are prepared to release information about water issues, however. A number of companies refuse to share this information and do not wish to be ranked in this respect. An often heard excuse is that companies are, as of yet, unable to measure this information or do not want to measure it because it is not considered relevant business information.

Investing in Clean WaterIn 2013 and at the beginning of 2014, PGGM Infra-structure Funds invested in three Chinese drinking water and wastewater companies, Shenyang Shengyuan Water, Shengyang Zhenxing Environmental and Dahian Hengji Xinrun Water. Collectively they have a total processing capacity of 1.7 million tonnes of water per day. The companies are receiving a great deal of support from local governments because they contribute to solving the major water scarcity and pollution issues in Northeast China due to the fact that the river water in that region is seriously polluted by industrial wastewater. In 2013, one of the water purification plants processed over 200 million tonnes of polluted water.

2.2.4 Outlook

Water scarcity and water pollution are rapidly gaining the attention of investors due to the conspicuous droughts in different parts of the world and due to the investment opportunities, particularly in infrastructure. In 2015, PGGM will make efforts to create better insight into water risks in specific sectors, such as power generation and agriculture. In addition, PGGM will continue to pursue discussions with CDP, Bloomberg and various companies concerning the release of relevant standardised water data, so that investors can include water as a risk factor in their investment decisions. Finally, investments in water security within existing investment categories, such as infrastructure, will be increased. We support the external development of a water bond standard and internally we are designing a mandate for investments in water scarcity solutions.

Circular Economy

PGGM N.V. wants to make a contribution to the transformation of the present-day economy into a circular economy. This is not an objective in itself, but we see the transition to a circular economy as an important solution to climate change, water scarcity and the scarcity of raw materials. In 2014, we started work on developing a scan designed to measure to what extent companies are circular and how they can improve their circularity. The pilot version of this scan has since been completed. The challenge in developing the Circular Scan is that a great deal of information about circularity is still only available at the level of raw materials, rather than at the company’s total level. This makes it difficult to compare and rank companies, which means that the scan is not yet a useful tool for investors. We will continue to work on developing the scan in 2015.

In addition, effective October 2014, PGGM N.V. became a member of the Circular Economy 100 platform of the Ellen MacArthur Foundation (EMF). This is a global platform that brings companies, innovators and regions together in order to accelerate the transition to a circular economy. In an EMF subgroup, together with other financial parties and universities, we are researching the implications of circularity for the financial sector. We assess the implications of the circular economy in terms of the financial issues faced by companies.

WATER SCARCITY

25PGGM

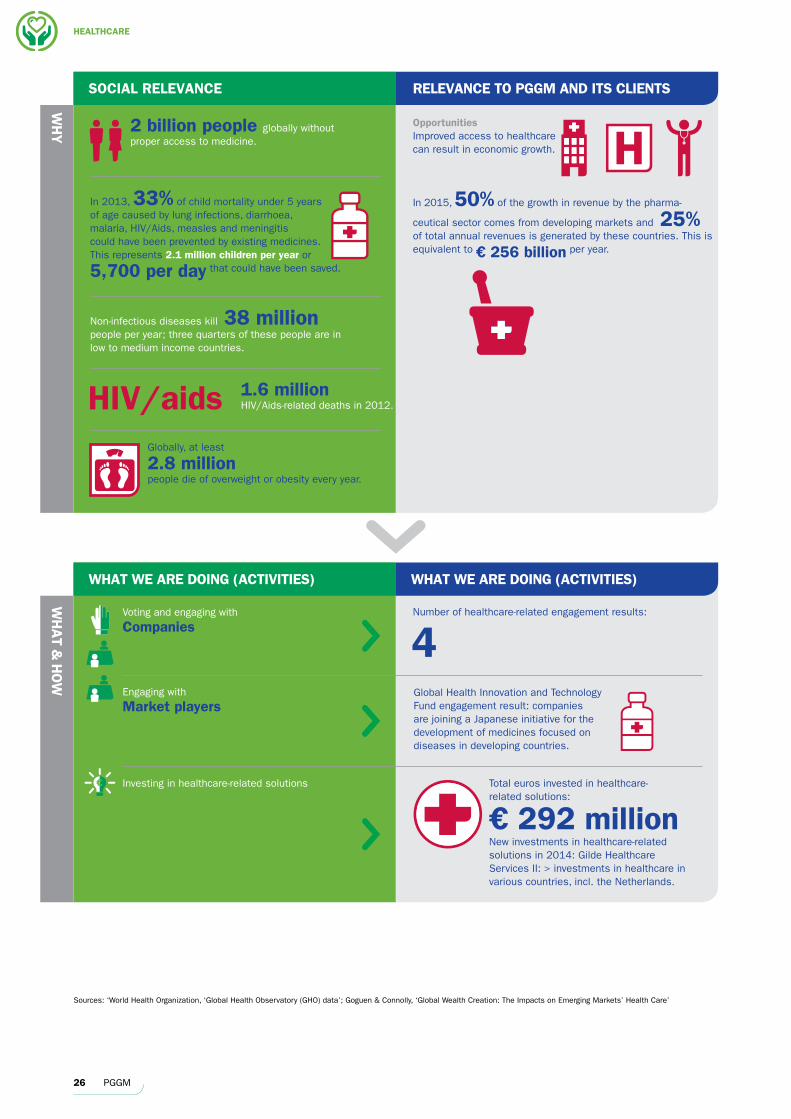

2.3.1 Why Healthcare as an Area of Focus?

Healthcare is an important area of focus due to our historical connection with this sector, that our clients represent. Access to good healthcare is a basic necessity and a human right. In addition, healthcare has our attention because investments in this sector can result in social and financial returns. For example, there are many countries in which a substantial part of the population suffers adverse effects from illnesses that are readily treatable. We believe that improving access to good healthcare in these countries leads to both social return, as well as faster and more stable economic growth. Companies that focus on this area will ultimately be well positioned when economic growth in these countries gathers pace and new sales markets emerge.

2.3.2 What Are We Doing in This Area of Focus?

Companies in the pharmaceutical industry and manufacturers of healthcare equipment play a major role in improving access to good healthcare. At many companies the initiatives are of a philanthropic nature. For example, many companies make one-time product donations in response to human disasters. However, this sector requires strategic solutions designed to deal with the issues. For example, by providing affordable health-care insurance policies companies could improve access to good healthcare for their employees thus reducing the absence due to illness rate. By investing in companies that work on strategic solutions, PGGM on behalf of its clients wants to contribute to improved (access to) healthcare. In addition, as an active shareholder we call companies to account for their behaviour and encourage them to find solutions and develop long-term plans designed to improve access to healthcare. In these discussions we focus on gearing prices to local incomes, sharing patents and researching and developing medicines to treat tropical diseases.

2.3.3 How Did We Action This in 2014?

In 2014, PGGM, on behalf of PFZW, invested in Gilde Healthcare Services II, a fund that invests in the fast-growing, innovative companies, primarily in the Benelux and Germany, which make it possible to provide better care at lower costs. In addition, in 2014, we met with companies to discuss access to medicines in developing countries.

The Access to Medicine (AtM) IndexMany pharmaceutical companies understand the benefits of operating in developing countries. This is also apparent from the biennial AtM Index, which was published for the second time in 2014. PGGM endorses the importance of the AtM Index and its impact on improving access to medicines in developing countries. PGGM invests in the Danish pharmaceutical company Novo Nordisk via its Responsible Equity Portfolio (REP). This is a large manufacturer of medicines for diabetes, a disease that is increasingly affecting people in developing countries as well. PGGM discussed the AtM Index with this company. In the most recent AtM Index, Novo Nordisk, in part due to these discussions, showed the biggest movement, rising from sixth to second place. As such, the company has grown into one of the best performing companies in terms of improving access to medicines.

Access to Medicine in JapanThere also are a number of companies that do not perform well on the AtM Index, or that do not form part of the group of companies analysed. PGGM has engaged in discussions with such companies for many years, for example in Japan. Various companies in the healthcare sector in Japan have decided to form the GHIT non-profit fund. On the basis of their membership in this fund, five Japanese pharmaceutical companies, Eisai, Daiichi Sankyo, Astellas Pharma, Takeda and Shionogi, have provided research budgets for fighting infectious diseases in developing countries and for forgotten tropical diseases. This way they further intensified their AtM programmes. Other participants in the GHIT Fund include the Bill & Melinda Gates Foundation and the Japanese Ministry of Population Health and the Ministry of Foreign Affairs. For some years now, PGGM has been engaged in a dialogue with a number of Japanese companies in the healthcare sector in order to improve the AtM. In the spring of 2014, we also met with these two Ministries to discuss the GHIT Fund, as well as with the GHIT Fund’s CEO and with

2.3 Healthcare

26 PGGM

WH

YW

HA

T & H

OW

SOCIAL RELEVANCE

WHAT WE ARE DOING (ACTIVITIES)

RELEVANCE TO PGGM AND ITS CLIENTS

WHAT WE ARE DOING (ACTIVITIES)

Voting and engaging with

Companies

Engaging with

Market players

Investing in healthcare-related solutions

Global Health Innovation and Technology Fund engagement result: companies are joining a Japanese initiative for the development of medicines focused on diseases in developing countries.

Total euros invested in healthcare-related solutions:

€ 292 million

New investments in healthcare-related solutions in 2014: Gilde Healthcare Services II: > investments in healthcare in various countries, incl. the Netherlands.

OpportunitiesImproved access to healthcare can result in economic growth.

Non-infectious diseases kill 38 million people per year; three quarters of these people are in low to medium income countries.

Globally, at least

2.8 millionpeople die of overweight or obesity every year.

1.6 million HIV/Aids-related deaths in 2012.

In 2013, 33% of child mortality under 5 years of age caused by lung infections, diarrhoea, malaria, HIV/Aids, measles and meningitis could have been prevented by existing medicines. This represents 2.1 million children per year or

5,700 per day that could have been saved.

In 2015, 50% of the growth in revenue by the pharma-

ceutical sector comes from developing markets and 25% of total annual revenues is generated by these countries. This is equivalent to € 256 billion per year.

4Number of healthcare-related engagement results:

2 billion people globally without proper access to medicine.

HEALTHCARE

Sources: ‘World Health Organization, ‘Global Health Observatory (GHO) data’; Goguen & Connolly, ‘Global Wealth Creation: The Impacts on Emerging Markets’ Health Care’

27PGGM

HEALTHCARE