ANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE,...

102

ANNUAL REPORT FOR THE YEAR ENDED 30 TH JUNE, 2015

Transcript of ANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE,...

ANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

THE UNITED REPUBLIC OF TANZANIA

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

January, 2016

Energy and Water Utilities Regulatory Authority (EWURA)7TH Floor, LAPF Pension Fund Tower, Opposite Makumbusho Village, Kijitonyama

P.O. Box 72175, Dar es Salaam, Tanzania

Tel: +255 (0)22 2923513 -18, Fax: +255 (0)22 2923519,

E-mail: [email protected] • Website: www.ewura.go.tz

iv

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

ABBREVIATIONS

ACL : Armstone Company LimitedAFUR : African Forum for Utility RegulatorsBOD : Biochemical Oxygen DemandCOD : Chemical Oxygen DemandDTWSSA : District and Township Water Supply and Sanitation AuthorityEPP : Emergency Power ProducerEWURA : Energy and Water Utilities Regulatory AuthorityFCT : Fair Competition TribunalFOB : Free On BoardGEPF : Government Employees Provident FundGIZ : Deutsche Gesellschaft für Internationale ZusammenarbeitGPA : Group Personal AccidentGWh : Giga Watt hourHIV/AIDS : Human Immunodefi ciency Virus/Acquired Immune Defi ciency SyndromeHFO : Heavy Furnace OilIAS : International Accounting StandardsIASB : International Accounting Standards BoardICT : Information and Communication TechnologyIDA : International Development AssociationIFRS : International Financial Reporting StandardsIK : Illuminating KeroseneIPP : Independent Power ProducerISA : International Standards on AuditingISO : International Standardization OrganizationKASHWASA : Kahama Shinyanga Water Supply and Sanitation AuthorityLAPF : Local Authorities Pensions FundLOIS : Licensing and Order Information SystemMajIs : Water Utilities Information SystemMEM : Ministry of Energy and MineralsMT : Metric TonnesMW : Mega WattNPWSSA : National Project Water Supply and Sanitation AuthorityNSSF : National Social Security FundPAA : Public Audit Act 2008PICL : Petroleum Importers Coordinators LtdPPF : Parastatal Pension FundPPSDP : Privatization and Private Sector Development ProjectPSPF : Public Service Pensions FundRERA : Regional Electricity Regulators AssociationRWSSA : Regional Water Supply and Sanitation AuthoritySPP : Small Power ProducerTANESCO : Tanzania Electric Supply CompanyTBS : Tanzania Bureau of StandardsTZS : Tanzania ShillingsWSSA : Water Supply and Sanitation AuthorityZECO : Zanzibar Electric CompanyZESCO : Zambia Electricity Corporation

v

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

LETTER OF TRANSMITTAL

Hon. Gerson Lwenge (MP),Minister for Water,Ministry of Water,426 Morogoro Road,14473 Dar es Salaam.

Honourable Minister,

I have the honour to submit to you the Annual Report and Audited Accounts of the Energy and Water Utilities Regulatory Authority (EWURA) for the fi nancial year ended 30th June, 2015 as per Section 48 of the EWURA Act, Cap 414.

The report outlines the major activities accomplished by the Authority during the year under review.

I submit.

Prof. Eng. Jamidu KatimaChairman, EWURA Board of DirectorsJanuary 2016

vi

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

VISION, MISSION AND CORE VALUES

Vision: To be a world class regulator of energy and water services.

Mission: To regulate the energy and water services in a transparent, effective and effi cient manner that promotes investments and enhances the socio-economic welfare of the Tanzanian society.

Core Values:

(a) Transparency EWURA operates in a fully transparent manner. All regulatory decisions are conducted without prejudice,

with respect for the interests of all stakeholders and in a fair and completely transparent manner. Information on regulatory decisions is openly communicated to all stakeholders using various media.

(b) Integrity EWURA Board members and staff are not allowed to solicit or accept gifts, favours or inducements, fi nancial

or otherwise, in the course of discharging their duties. In addition, EWURA Board members and staff shall not offer gifts, improper favors or inducements.

(c) Courtesy EWURA Board members and staff treat their clients and colleagues with courtesy and regard themselves

as servants of the people; and will be particularly considerate when dealing with vulnerable members of the public such as the elderly, the poor, the sick and people with disabilities and disadvantaged groups in society.

(d) Accountability EWURA Board members and staff discharge duties including making decisions with which they are bound

and answerable. Their conduct is in a manner that shows readiness to take full liability and responsibility for the outcome of their decisions.

(e) Professionalism EWURA Board members and staff attend to their duties with the highest degree of professionalism.

(f) Equity EWURA Board members and staff treat all stakeholders with impartiality and fairness. The duty of EWURA

as a regulator is to set a level playing fi eld and balance interests of all stakeholders. The conduct of all staff and their individual decisions as well as those of the Authority at all times should refl ect this value.

Strategic Objectives

The Authority is determined to increase its contribution to national economic development and improve the welfare of the Tanzanian society through delivery of regulated services. It is within this drive that the Authority set out fi ve objectives in its Strategic Plan (2012/13 - 2016/17) with a view to enabling it to address imminent and medium-term regulatory challenges in all the sectors it regulates. These strategic objectives are:

(a) least cost investments in the regulated sectors promoted; (b) quality and access of regulated services improved;(c) public knowledge, awareness and understanding of regulatory functions in the regulated sectors enhanced;(d) EWURA functions effectively and effi ciently managed; and(e) interventions against HIV/AIDS enhanced.

vii

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

TABLE OF CONTENTS

ABBREVIATIONS ..................................................................................................................................................iv

LETTER OF TRANSMITTAL .....................................................................................................................................v

VISION, MISSION AND CORE VALUES ...............................................................................................................vi

INTRODUCTION ..................................................................................................................................................1

CHAIRMAN’S STATEMENT ....................................................................................................................................2

DIRECTOR GENERAL’S STATEMENT ......................................................................................................................7

Board of Directors ..................................................................................................................................................8Board Committees ..................................................................................................................................................8Director General ....................................................................................................................................................8Internal Monitoring System .....................................................................................................................................8Litigation ................................................................................................................................................................8Finance and Budget Administration ........................................................................................................................8Procurement Management ......................................................................................................................................9Code of Conduct ....................................................................................................................................................9Internal Audit and Risk Management ......................................................................................................................9

1.0 GENERAL INSTITUTIONAL PERFORMANCE REVIEW ...........................................................................101.1 Staffi ng and Institutional Capacity Building .............................................................................................101.2 Regional Co-operation and Collaboration ...............................................................................................101.3 Information and Communication Technology (ICT) .................................................................................111.4 Public Register ........................................................................................................................................111.5 Financial Performance Review ................................................................................................................111.6 Key Achievements and Challenges ..........................................................................................................12

2.0 ELECTRICITY SECTOR PERFORMANCE AND REGULATION .................................................................142.1 Overview ................................................................................................................................................142.2 Performance Monitoring .........................................................................................................................152.3 Tariff and Power Purchase Agreement .....................................................................................................172.4 Regulatory ..............................................................................................................................................182.5 Complaints and Dispute Resolutions .......................................................................................................182.6 Litigation ................................................................................................................................................182.7 Health, Safety and Environmental Matters ...............................................................................................182.8 Key Achievements and Challenges ..........................................................................................................19

3.0 PETROLEUM SECTOR PERFORMANCE AND REGULATION .................................................................203.1 Overview ................................................................................................................................................203.2 Performance Monitoring .........................................................................................................................203.3 Petroleum Products Quality Monitoring ..................................................................................................293.4 Monitoring adherence to Health, Safety and Environmental (HSE) requirements .....................................323.5 Licensing Activities .................................................................................................................................343.6 Legislative Regulatory Tools ....................................................................................................................343.7 Complaints Handling and Dispute Resolution .........................................................................................35

viii

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

3.8 Litigation ................................................................................................................................................353.9 Key Challenges and Achievements ..........................................................................................................35

4.0 NATURAL GAS SECTOR PERFORMANCE AND REGULATION ..............................................................364.1 Overview ................................................................................................................................................364.2 Performance Monitoring .........................................................................................................................364.3 Level of Investment in Gas Infrastructure Development ...........................................................................394.4 Health, Safety and Environment ..............................................................................................................404.5 Licensing ................................................................................................................................................404.6 Determination of Rates and Charges .......................................................................................................404.7 Legislative Matters ..................................................................................................................................404.8 Disputes and Complaints ........................................................................................................................414.9 Litigation ................................................................................................................................................414.10 Achievements and Challenges ................................................................................................................41

5.0 WATER SUPPLY AND SANITATION SERVICES REGULATION ...............................................................425.1 Overview ................................................................................................................................................425.2 Performance Monitoring .........................................................................................................................425.3 Review of WSSAs’ Business Plans ...........................................................................................................435.4 Review of WSSAs’ Client Service Charters ..............................................................................................435.5 Water Utilities Performance Review Report .............................................................................................435.6 Licensing ................................................................................................................................................435.7 Determination of Rates and Charges .......................................................................................................445.8 Complaints Handling and Dispute Resolution .........................................................................................445.9 Litigation ................................................................................................................................................455.10 Health, Safety and Environmental Matters ...............................................................................................455.11 Capacity Building ...................................................................................................................................455.12 Other Interventions in the Water Sector ..................................................................................................455.13 Key Achievements and Challenges ..........................................................................................................46

6.0 COMMUNICATIONS AND PUBLIC AWARENESS PROGRAMME ..........................................................476.1 Overview ................................................................................................................................................476.2 Public Awareness Campaign ...................................................................................................................476.3 Press Conferences and Media Coverage ..................................................................................................476.4 Advertisements .......................................................................................................................................476.5 Publicity Materials ..................................................................................................................................476.6 Exhibitions ..............................................................................................................................................486.7 Impact of Public Awareness Campaigns ..................................................................................................486.8 Donations and Contributions ..................................................................................................................486.9 Key Achievement and Challenges ...........................................................................................................48

7.0 STAKEHOLDERS CONSULTATIONS .......................................................................................................49

8.0 DECLARATION OF CONFLICT OF INTEREST ........................................................................................49

9.0 CONCLUSION AND FUTURE OUTLOOK .............................................................................................49

10.0 REPORT FROM THE CONTROLLER AND AUDITOR GENERAL .............................................................51

1

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

INTRODUCTION

This is the 9th Annual report that presents the performance of the Energy and Water Utilities Regulatory Authority (EWURA) for the year that ended on 30th June, 2015. The report summarizes the executed activities, challenges encountered and achievements attained during the period under review.

The Authority was established under the EWURA Act, Cap. 414 of the Laws of Tanzania, and started its operations in June 2006 as a multi-sector regulatory authority. The Authority carries out economic and technical regulation of the energy (electricity, petroleum, and natural gas) and water sectors. The functions of the Authority as spelt out in the Act are to: (a) perform all functions conferred on it by sector legislation and Cap. 414;(b) issue, renew and cancel licences;(c) establish standards for goods and services;(d) establish standards for terms and conditions of supply of goods and services;(e) regulate rates and charges;(f) make rules;(g) monitor performance of regulated sectors in relation to availability, quality, standards of services, cost of

services, effi ciency of production, investment levels and distribution of services; (h) facilitate resolution of complaints and disputes; and(i) disseminate information about matters relevant to its functions.

Further, Section 6 of the EWURA Act requires the Authority to assume the following duties in the course of carrying out its functions:(a) promote effective competition and economic effi ciency;(b) promote the interests of consumers;(c) protect the fi nancial viability of effi cient suppliers;(d) promote the availability of regulated services to all consumers, including low income, rural and disadvantaged

consumers;(e) enhance public knowledge, awareness and understanding of the regulated sectors including the rights and

obligations of consumers and regulated suppliers, the ways in which complaints and disputes may be initiated and resolved, and the duties, functions and activities of the Authority; and

(f) take into account the need to protect and preserve the environment.

Objectives of the ReportThis annual report for 2014/15 fulfi ls the following objectives:(a) to comply to the requirements of Section 48 of EWURA Act, Cap. 414;(b) to inform the public on the Authority’s performance in regulation of energy and water sectors;(c) to educate stakeholders of regulated sectors and the general public on regulatory matters; and(d) to provide a source of credible information on the regulated sectors.

2

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

CHAIRMAN’S STATEMENT

On behalf of the Board of Directors of the Energy and Water Utilities Regulatory Authority (EWURA), I am pleased to give a brief overview of EWURA’s performance for the Financial Year ending June 30th 2015, which is the 9th Annual Report since the commencement of the Authority’s operations way back in 2006.

For the fi nancial year 2014/2015, EWURA has proved its stability by demonstrating a strong performance in its regulatory activities to the sectors that fall under its mandate and jurisdiction. Such sectors are Energy (Electricity, Petroleum, Natural Gas) and Water and Sanitation.

During the period under review, the Authority received many awards; but one of them is a famous award that the Authority won as the best Energy Regulator in Africa at the Africa Energy Forum held in June,2015 in Dubai, thus proving the Authority’s ability to regulate the sectors that it regulates.

Although there are still some challenges in the quality of service, especially in Water and Electricity, the Authority has managed to put more efforts in making sure that it accelerates the development of services in terms of availability and quality of services. The Authority has continued to protect the interests of the consumers and the service providers.

During the fi nancial year 2014/2015, the Authority monitored the fl uctuations of petroleum products prices in the world market and translated its effects in Tanzania, where the country experienced lowest prices during the period between September 2014 and March 2015.

This was the last fi nancial year for the founding Board Chairman, Mr. Simon Sayore who completed his 8 years tenure on 26th June 2015 as stipulated in the EWURA Act Cap. 414. I am pleased to note that Mr. Sayore has left behind a powerful institution which stands fi rm in implementing and defending various regulatory principles and values, through which the Authority steers towards the right direction in attaining its objectives.

I wish to extend my sincere appreciation to the Government of Tanzania, and especially to His Excellence, Dr. Jakaya Mrisho Kikwete, the President of the United Republic of Tanzania, who has pioneered the operationalization of EWURA and leaving his legacy of founding the Authority that has achieved a lot.

I also wish to extend my appreciation to the Minister for Water, Hon. Prof. Jumanne Maghembe and the Minister for Energy and Minerals, Hon. George Simbachawene for supporting the Authority in achieving its intended goals. Finally, let me take this opportunity to congratulate EWURA Board Members, Management and Staff for their unwavering commitment, dedication and hardworking during the year under review.

Mr. Omar Shane BenderaDeputy Chairman

3

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

BOARD AND MANAGEMENT STRUCTURE

The Authority has a cost-effective organisation structure that facilitates effi cient regulation of the energy (electricity, petroleum, natural gas) and water sectors; good corporate governance; and effi cient provision of cross-cutting services. The structure has the Board of Directors as the top decision-making body, the Director General as the overall overseer of the day to day activities of the Authority and eight Divisions headed by Directors. There are also heads of units who report directly to the Director General, namely, Manager Procurement Management and Manager, Communications and Public Relations. The organisation structure is as shown in FIGURE 1.

Board of DirectorsEWURA is governed by a Board of Directors which is the highest decision-making organ of the Authority established under section 8 of the EWURA Act. The Board consists of the non-executive Chairman appointed by the President of the United Republic of Tanzania, fi ve (5) non-executive members and the Director General who are appointed by the Minister responsible for EWURA after consultation with the Minister for Energy and Minerals.

In order to fulfi l its oversight responsibilities, the Board has established fi ve (5) Board Committees based on sectoral and cross-cutting issues. These are Audit, Legal and Corporate Affairs, Electricity and Natural Gas, Petroleum, and Water Board Committees.

Director GeneralThe Director General is appointed under section 14 of the EWURA Act and is responsible for the day-to-day operations of the Authority, subject to the directions of the Board of Directors.

Divisional DirectorsThe Director General is assisted by seven (7) Divisional Directors, namely Director of Electricity, Director of Petroleum, Director of Natural Gas, Director of Water and Sanitation, Director of Regulatory Economics, Director of Legal Services and Director of Corporate Affairs. The Director of Internal Audit reports to the Board’s Audit Committee on audit functions and to the Director General on administrative matters. Communications and Public Relations, and Procurement Management are functions headed by managers under the Director General’s Offi ce.

Offi ce of the AuthorityThe offi ce of the Authority is currently located at 7th Floor, LAPF Pension Fund Tower, Opposite Makumbusho Village, Kijitonyama in Dar es Salaam. The Authority also operates one zonal offi ce in Mwanza.

4

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

Dir

ec

tor

of

Co

rpo

rate

Aff

air

s

Bo

ard

of

Dir

ec

tors

Dir

ec

tor

of

Inte

rna

l A

ud

it

Dir

ec

tor

Ge

ne

ral

Ma

na

ge

r

Co

mm

un

ica

tio

n a

nd

Pu

blic

Re

lati

on

s

Ma

na

ge

r

Pro

cu

rem

en

t

Ma

na

ge

me

nt

Fin

an

ce

an

d

Ad

min

istr

ati

on

Ma

na

ge

r

Info

rma

tio

n a

nd

Co

mm

un

ica

tio

n

Te

ch

no

log

y M

an

ag

er

Hu

ma

n R

eso

urc

es

Ma

na

ge

r

Zo

na

l M

an

ag

er

Ma

na

ge

r G

as

Dis

trib

uti

on

Te

ch

nic

al

Ma

na

ge

r

Te

ch

nic

al

Ma

na

ge

r

Te

ch

nic

al

Ma

na

ge

r

Ma

na

ge

r F

ina

nc

ial

An

aly

sis

an

d

Mo

de

llin

g

Ma

na

ge

r L

ice

nsin

g

an

d E

nfo

rce

me

nt

Ma

na

ge

r G

as

Tra

nsm

issio

n

Co

mm

erc

ial

Ma

na

ge

r

Co

mm

erc

ial

Ma

na

ge

rC

om

me

rcia

l

Ma

na

ge

r

Ma

na

ge

r E

co

no

mic

An

aly

sis

an

d

Re

se

arc

h

Ma

na

ge

r L

eg

al

Se

rvic

es

Dir

ec

tor

of

Na

tura

l G

as

Dir

ec

tor

of

Pe

tro

leu

m

Dir

ec

tor

of

Wa

ter

an

d S

ew

era

ge

Dir

ec

tor

of

Ele

ctr

icit

y

Dir

ec

tor

of

Re

gu

lato

ry

Ec

on

om

ics

Dir

ec

tor

of

Le

ga

l

Se

rvic

es

Figu

re 1

: Org

aniz

atio

n St

ruct

ure

5

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

BOARD OF DIRECTORS

Mr. Simon F. Sayore Chairman

Mr. Richard M. KayomboMember

Mr. Omar S. BenderaDeputy Chairman

Mr. Ahmed S.K. KilimaMember

Mr. Oswald R. MutaitinaMember

Ms Juliana A. MwalongoMember up to October,

2014

Mr. Nicholas H.MbwanjiMember

Mr. Felix M. NgamlagosiMember

6

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

MANAGEMENT

Mr. Felix M. NgamlagosiDirector General

Ms. Miriam G. Mahanyu

Director of Legal Services

Eng. Anastas MbawalaDirector of Electricity

Ms. Naiungishu S. MollelDirector of Corporate

Affairs

Eng. Mutaekulwa Mutegeki

Director of Water and Sanitation

Eng. Godwin SamwelDirector of Petroleum

Eng. Charles OmujuniDirector of Natural Gas

Mr. George KabelwaAg. Director of

Regulatory Economics

Mr. Giniva SangaAg. Director of Internal Audit

Mr. Deogratius KumalijaManager Procurement

Management

Mr. Titus KaguoManager

Communications and Public Relations

7

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

DIRECTOR GENERAL’S STATEMENT

On behalf of Management and Members of staff of the Energy and Water Utilities Regulatory Authority (EWURA), I am honoured to present EWURA’s Annual Report for the Financial Year 2014/2015. This is the ninth year of operation since the Authority was established. The report contains details on achievements made from the efforts and commitments of the Authority’s Board of Directors, Management, members of staff and stakeholders. Furthermore, the report contains the challenges that were encountered during the reporting period.

Before I proceed, let me fi rst congratulate the founding Board Chairman, Mr. Simon Sayore, whose 8 years tenure with the Authority, as the Board Chairman, ended effectively on 26th June 2015. Mr Sayore has served as the Board Chairman for eight years since 2006, bringing the Authority to new heights of professional performance that transcended to global levels. During his leadership, EWURA registered notable success, for instance emerging as the best energy regulator of Africa for the year 2015 namely the Energy Regulator of the Year 2015, Award for Excellence 2015.

I would like to recognise and applaud the noble leadership of the Deputy Chairman Mr. Omar Shane Bendera during the time under review. Also, would like to welcome and congratulate, the new Board Chairman, Professor Eng. Jamidu Katima, who has just been appointed by His Excellency, the President of the United Republic of Tanzania, Dr. Jakaya Mrisho Kikwete. On behalf of EWURA Board, Management and staff, I wish him all the best in his new responsibilities and assure him of our continued cooperation.

During the fi nancial year 2014/2015, the Authority continued to discharge its mandate in the regulation of energy and water sectors. Specifi cally, the Authority registered notable successes in the regulation of tariffs and charges for regulated goods and services by, inter alia, focusing on the value for money and the quality of services offered.

Furthermore, the Authority participated in the preparation of Model Power Purchase Agreements for seven energy technologies which are hydro, natural gas, oil, coal, geothermal, solar and wind, for use in negotiating power projects in Mainland Tanzania. These models will be applicable for power projects of above 10MW. These models have been approved by the Ministry of Energy and Minerals and will be used in negotiations between project developers and power off-takers in a bid to attract investments in the electricity sector. Likewise, during the period under review the second generation Small Power Producers Framework has been developed for hydro generation of electricity and biomass technologies for generating electricity.

For the fi nancial year 2014/15 the Authority participated in the drafting of the Petroleum Act 2015. The Petroleum Act, which was passed by the Parliament of Tanzania in July 2015 and assented by H.E President of the United Republic of Tanzania, once enacted will facilitate management and regulation of petroleum and natural gas sub-sectors in Tanzania.

Last but not least, I would like to thank the EWURA Board of Directors, Management, staff and all our stakeholders for the highest commitment and support extended to us during the fi nancial year 2014/2015.

Felix M. NgamlagosiDirector General

8

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

CORPORATE GOVERNANCE

Board of DirectorsThe Board of Directors of EWURA as the highest decision making organ, is established under Section 8 of the EWURA Act, Cap 414. The Board consists of six (6) non-executive members including the Chairman and one (1) executive member who is also the Director General. The Chairman is appointed by the President of the United Republic of Tanzania while the remaining fi ve (5) non-executive members and the Director General are appointed by the Minister responsible for EWURA after consultation with the relevant sector Ministers. During the year under review a total of 32 Board Meetings were conducted, out of which 12 were ordinary and 20 were extraordinary.

Board CommitteesThe committees of the Board of Directors are established in accordance with Section 21 of the EWURA Act, Cap 414 to fulfi l its oversight responsibilities. The Board has fi ve (5) Committees based on sectoral and cross-cutting issues. These are Audit, Legal and Corporate Affairs, Electricity and Natural Gas, Petroleum, and Water Committees. During the period under review, eighteen (18) meetings were conducted by these Committees as shown in Table 1.

Table 1: Board Committees Meetings

S/N Board Committee Number of Meetings

1 Audit 7

2 Legal and Corporate Affairs 5

3 Electricity and Natural Gas 4

4 Petroleum 1

5 Water 1

Total 18

Director GeneralThe Director General of the Authority is appointed by the Minister responsible for EWURA as per section 14 of the EWURA Act, Cap 414 and shall discharge day-to-day operations of the Authority, subject to the directions of the Board of Directors.

Internal Monitoring SystemThe Authority has established an Internal Monitoring System in line with relevant public sector legislation, regulations, rules and procedures. The internal administrative monitoring system is achieved through, among other things, fi nancial controls, and the Code of Conduct and Internal Audit functions.

LitigationDuring the year under review, in relation to Corporate Governance, the Authority was a party to one labour dispute at the Commission of Mediation and Arbitration (CMA). In this dispute, one former employee of the Authority is challenging EWURA’s decision not to confi rm him to the post. Hearing of the matter is still pending. Furthermore, the Authority was a party to two Civil Suits at the Resident Magistrate Court of Dar es Salaam at Kisutu. The nature of the Suit was on recovery of unpaid regulatory levy by some regulated suppliers.

Finance and Budget AdministrationThe fi nancial matters of the Authority are governed by the Public Finance Act, 2002 and international fi nancial best practices. The Authority’s Annual Plan and Budget are prepared in accordance with the fi ve years strategic plan (2012/13 – 2016/17) of the Authority.

9

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

Pursuant to Section 21 of the Budget Act, 2014, the Authority is required to prepare budget estimates and submit to the Permanent Secretary of the Ministry of Finance for scrutiny and approval. After being approved the budget is submitted to the Minister responsible for EWURA in line with the provisions of section 49 of the EWURA Act. Resources used to implement the Annual Budget are derived from regulatory levies and fees collected from regulated utilities and consumers. The outcome of the implementation of annual budget is presented to the Minister responsible for the Authority through an Annual Report and Accounts in line with the provisions of section 48 of the EWURA Act.

Procurement ManagementThe Authority has a Tender Board and a Procurement Management Unit (PMU) established in accordance with the Public Procurement Act Cap 410. In order to comply with the requirements of the Public Procurement Act and its related Regulations, members of the Tender Board, Staff of the Procurement Management Unit and user departments attend various training courses being conducted by the Public Procurement Regulatory Authority (PPRA).

During the audit on the implementation of the system for checking and monitoring procurement activities conducted by the Public Procurement Regulatory Authority in February 2015, the Authority was assessed to have performed very well with a compliance level of 88.5%.

Code of ConductThe Authority’s Code of Conduct binds both Members of the Board of Directors and Staff. The Code of Conduct explicitly underlines that the Authority has zero tolerance to fraud and corruption. All incidents of fraud and corruption are reported to appropriate Authorities. During the year under review, the Authority did not encounter any incident of fraud or corruption.

Internal Audit and Risk ManagementThe Internal Audit functions that entail giving assurance on risk management, control processes and governance processes, were carried out in accordance with the Internal Audit Charter, Annual Audit Plan and International Standards for Professional Practices of Internal Auditing.

During the period under review, the Authority witnessed a smooth running of various processes under the guidance of the oversight bodies which include the Board of Directors and its committees. The Internal Audit activity continued to assist the Board and Management in ensuring that there is improvement in the effectiveness of risk management, control and governance processes.

10

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

1.0 GENERAL INSTITUTIONAL PERFORMANCE REVIEW

During the period under review, the Authority performed various activities related to regulatory matters as summarised below:

1.1 Staffi ng and Institutional Capacity Building 1.1.1 Recruitment The Authority maintained its recruitment policy by providing equal opportunity to all. In so doing, the

Authority recruited the most appropriate candidates available in the market in a competitive and transparent manner in order to ensure that the functions and duties of the Authority are performed effi ciently and effectively.

During the period under review, the Authority’s workforce was further strengthened. A total of 11 staff were recruited thus bringing the number of staff to 104 out of 113 in the approved establishment. Staff gender structure is as indicated in Table 2 below:

Table 2: Staff as at 30th June 2015

Item Male Female Total

Staff Compliment 70 34 104

Proportion 67% 33% 100%

1.1.2 Capacity Building EWURA believes in having well educated and motivated staff. The Authority encourages distance learning,

development and growth of its staff. The learning and development programmes support the retention initiatives of the Authority that aims at ensuring that the Authority has adequate professional and skilled staff.

During the year under review, the Authority enhanced knowledge of its staff in relevant regulatory, managerial and operational competencies. The new senior staff attended general courses on Public Utility Regulation and Strategy. Also, several staff attended local training on general management courses, professional courses, secretarial practices and advanced drivers and offi ce attendants courses in order to improve their performance. Additionally the Authority in collaboration with Public Service College and Tanzania Fire and Rescue Force Unit conducted awareness training on HIV/ AIDS and working life skills, and fi re- fi ghting and protection respectively to all the Authority staff.

1.2 Regional Co-operation and Collaboration The Authority subscribed and participated in the activities of fi ve Regional Associations namely, Regional

Electricity Regulators Association (RERA), African Forum for Utility Regulators (AFUR), Energy Regulators Association of East Africa (EREA), Eastern and Southern Africa Water and Sanitation Regulators Association (ESAWAS) and African Refi ners Association (ARA). The main objective is to exchange regulatory experiences within the International and Regional setting, and allow the Authority to have access to information necessary for regulation and performance benchmarking. Furthermore, the Authority has participated in various meetings convened to establish the regional power pool regulatory body, the Eastern Africa Power Pool Independent Regulatory Body (EAPP-IRB).

11

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

1.3 Information and Communication Technology (ICT)

1.3.1 Regulatory and Management Information Systems The Authority’s Information Communication and Technology (ICT) System continued to support regulatory

functions. It is the Authority’s policy to ensure that the public is provided with timely and accurate information. The Authority’s website provides access to regulatory information including publications of all decisions made by the Board.

Pursuant to the Petroleum Act, 2008, the Authority continued with testing and training on the National Petroleum Information System (NPIS). The system consist of an integrated and centralized information system using modern data processing technology and covering all petroleum supply operations and installations, the principal market activities and statistics of the country as well as international reference data. In ensuring that the system works well and meets the expectations of all users, the Authority conducted training to Oil Marketing Companies (OMCs) on the use of NPIS.

The Authority continued to monitor the performance of Water Supply and Sanitation Authorities (WSSA) by using the Water Utilities Information System (MajIs). MajIs serves to improve accessibility to data and information for monitoring, planning and decision-making.

Likewise, the Authority maintained the Electricity Regulatory Information System (ERIS) and Asset Register (AR). The system is used to collect information from electricity service providers.

Furthermore, the Authority was in the fi nal stages of commissioning the Licensing and Order Information System (LOIS) under the support of GIZ. LOIS has been designed to facilitate online application, issuing, revocation and transfer of licences.

Finance and accounting activities of the Authority are managed through EPICOR accounting software which provides accurate data and timely reporting. A remote data recovery centre has been improved to strengthen the security of the Authority’s data in the event of a disaster to ensure business continuity.

1.4 Public Register Public Register is maintained by the Authority for public inspection at all times during business hours

at the Head Quarters in Dar es Salaam. Some of the information from the public access registry can be obtained from the Authority’s website. The register provides access to the Code of Conduct adopted by the Authority, regulatory information and all regulatory decisions made by the Authority and published in the Government Gazette such as rules, tariff Orders, awards and licences. The public has the right to get correct and accurate information from the Authority relating to the regulated entities. The main objective of the Public Registry is to ensure transparency and provision of timely information to all stakeholders on the Authority’s regulatory activities.

1.5 Financial Performance Review The Authority’s operations are fi nanced mainly through collection of levies from regulated service

providers in the energy, (electricity, petroleum, natural gas) and water and sanitation sectors. Other sources of fi nancing include licence fees, application fees, penalties and interest income from fi xed deposits.

Total operating revenue in 2014/15 amounted to TZS 38.7 billion indicating an increase of 15.7% when compared to the previous year as shown in Table 3

12

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

Table 3: Summary of Financial Performance

Item Amount for the Year Ended 30th June, 2015

Amount for the Year Ended 30th June, 2014

%Increase Over Previous Year

TZS’000 TZS’000 %

Income from Levy and Licences 34,823,343 30,077,848 15.8

Other Income 4,866,718 3,076,257 58.2

Total Income 38,690,061 33,154,105 16.7

Re-current Expenditure 27,490,594 25,347,854 8.5

Capital Expenditure 1,243,174 612,443 103.0

Total Expenditure 28,733,768 25,960,297 10.7

1.6 Key Achievements and Challenges Key achievements made and challenges experienced by the Authority during the year under review are

discussed below.

1.6.1 Key Achievements During the year under review, the key achievements of the Authority included: (a) The Authority continued to sustain fi nancial self-suffi ciency to run its operations without depending

on grants from the Government or Development Partners. (b) In a bid to bring regulatory services closer to consumers, the Authority’s Zonal Offi ce in Mwanza

for the Lake Zone has started its operations. (c) The Authority continued with petroleum products marking system which has signifi cantly reduced

adulteration and dumping of transit petroleum products. This has improved the quality of petroleum products and competition in the sector. In addition the system has reduced tax evasion on transit petroleum products.

(d) The standard of retail outlets infrastructure, quality of service and compliance to Health Safety and Environment (HSE) throughout the country has signifi cantly improved because of compliance monitoring, enforcement and measures taken by the Authority.

(e) The Authority prepared and disseminated the fi rst Downstream Petroleum Sub-Sector Performance Review Report. The report covers performance of the sector between years 2007 to 2014.

(f) The Authority participated in the preparation of Petroleum Act, 2015 which enables the Authority to regulate the mid and downstream of the petroleum and natural gas sectors

(g) In a bid to promote investments in the power sector, the Authority participated in the preparation of technology based Model Power Purchase Agreements for hydro, natural gas, oil, coal, geothermal, solar and wind.

(h) The Authority conducted training on the use of Water Utilities Information System (MajIs) to District, Township and National Project Water Supply and Sanitation Authorities (WSSAs). As a result, additional 60 water utilities started reporting through MajIs.

(i) The Authority prepared Licensing and Order Information System (LOIS) under the support of GIZ to facilitate online application, issuing, revocation and transfer of licences.

(j) The Authority developed regulatory tools which include 19 rules, guidelines, codes and licence templates.

(k) The Authority issued Water Quality Monitoring Guidelines, 2014 which provide guidance to water utilities in developing own quality monitoring programs for water supply and wastewater disposal.

(l) The Authority developed and implemented a Communication Policy and Strategy.

13

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

(m) The Authority continued to conduct public awareness campaigns and seminars on the roles and responsibilities of the Authority, rights and obligations of the service providers and consumers and complaints handling mechanism, for editors and journalists of Dar es Salaam based media houses. A similar training was conducted to TANESCO employees in Dar es Salaam, Coast, Lindi, Mtwara, Tabora, Kigoma, Kagera, Shinyanga, Mwanza and Mara regions.

1.6.2 Key Challenges The key challenges and their respective mitigation measures are as outlined below. (a) The Authority is faced with offi ce accommodation challenges which include frequent increases in

rent and insuffi cient space. However, efforts are under way to enable the Authority to construct its own offi ce building.

(b) Insuffi cient knowledge by the general public and key stakeholders in understanding the concept of regulation. This causes some of the key stakeholders to misunderstand the Authority’s decision making process. The Authority shall continue to implement its Public Awareness Programme to address this challenge.

(c) The delay in making regulatory decisions to some crosscutting issues that require approval from other Government Institutions like land use and environmental requirements.

14

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

2.0 ELECTRICITY SECTOR PERFORMANCE AND REGULATION

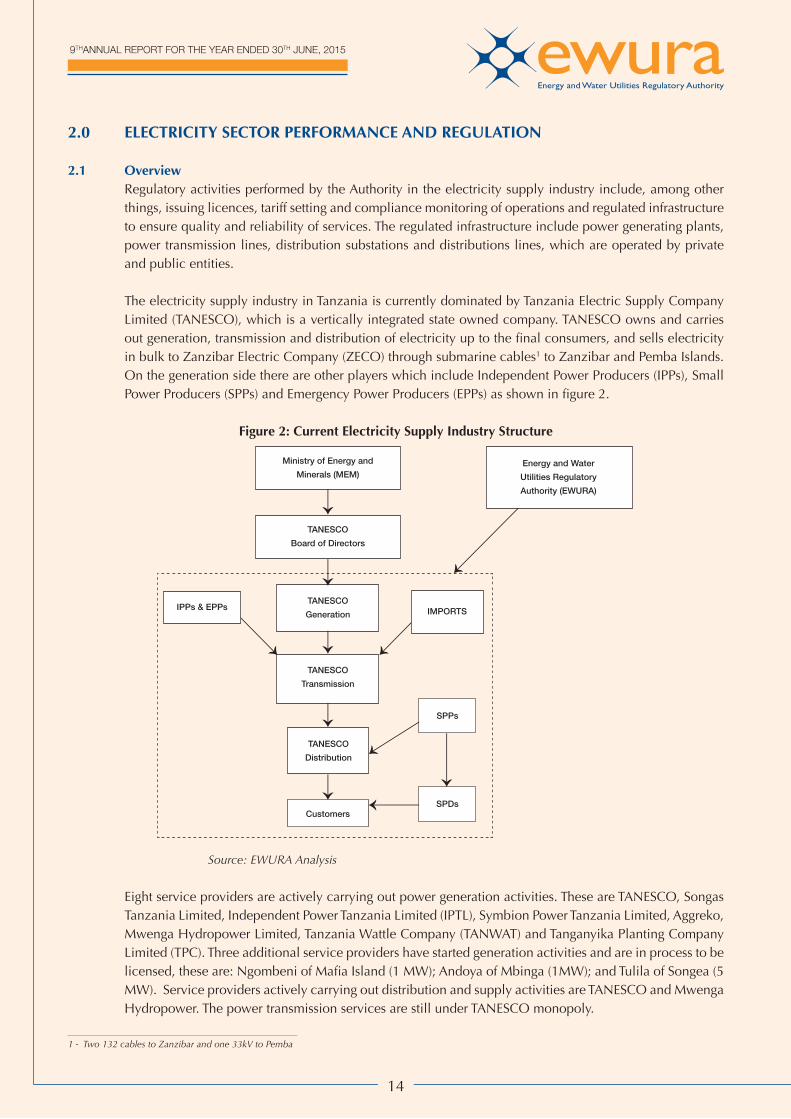

2.1 Overview Regulatory activities performed by the Authority in the electricity supply industry include, among other

things, issuing licences, tariff setting and compliance monitoring of operations and regulated infrastructure to ensure quality and reliability of services. The regulated infrastructure include power generating plants, power transmission lines, distribution substations and distributions lines, which are operated by private and public entities.

The electricity supply industry in Tanzania is currently dominated by Tanzania Electric Supply Company Limited (TANESCO), which is a vertically integrated state owned company. TANESCO owns and carries out generation, transmission and distribution of electricity up to the final consumers, and sells electricity in bulk to Zanzibar Electric Company (ZECO) through submarine cables1 to Zanzibar and Pemba Islands. On the generation side there are other players which include Independent Power Producers (IPPs), Small Power Producers (SPPs) and Emergency Power Producers (EPPs) as shown in fi gure 2.

Figure 2: Current Electricity Supply Industry Structure

Source: EWURA Analysis

Eight service providers are actively carrying out power generation activities. These are TANESCO, Songas Tanzania Limited, Independent Power Tanzania Limited (IPTL), Symbion Power Tanzania Limited, Aggreko, Mwenga Hydropower Limited, Tanzania Wattle Company (TANWAT) and Tanganyika Planting Company Limited (TPC). Three additional service providers have started generation activities and are in process to be licensed, these are: Ngombeni of Mafi a Island (1 MW); Andoya of Mbinga (1MW); and Tulila of Songea (5 MW). Service providers actively carrying out distribution and supply activities are TANESCO and Mwenga Hydropower. The power transmission services are still under TANESCO monopoly.

Ministry of Energy and

Minerals (MEM)

Energy and Water

Utilities Regulatory

Authority (EWURA)

TANESCO

Board of Directors

TANESCO

Generation

TANESCO

Transmission

IPPs & EPPsIMPORTS

SPPs

TANESCO

Distribution

CustomersSPDs

1 - Two 132 cables to Zanzibar and one 33kV to Pemba

15

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

2.2 Performance Monitoring

2.2.1 Reporting System Pursuant to Section 15(4) of the Electricity Act, 2008, every electricity service provider is required to

submit to the Authority, data and information relating to performance of its functions. During the period under review, the Authority continued to receive and maintain periodic data submitted by licensed power utilities and suppliers directly and through the Electricity Regulatory Information System (ERIS). Also, daily system reports were submitted by TANESCO through email distribution list.

2.2.2 Monitoring and Inspection During the period under review the Authority conducted routine inspection on Low Voltage (LV) and

Medium Voltage (MV) distribution networks. The inspections were conducted for Electricity Distribution infrastructure’s in nine Regions namely Arusha, Mwanza, Kagera, Morogoro, Dodoma, Tabora, Kigoma, Mara and Iringa. Among the defects found during inspection were leaning and rotten poles, defective switchgears, leaning insulators, transformer oil leakages and unrated fuse wires. Also some areas were observed to have low voltage caused by lines extended beyond the standard limit and overloaded transformers. The Authority instructed TANESCO to rectify the anomalies as detailed in the inspection reports given to them.

2.2.3 Quality and Standard of Services The Authority continued to monitor quality of service with reference to the quality of supply and services

standards with a focus on system disturbances such as unacceptable frequencies and voltage fl uctuations, power outages and load shedding. It was revealed that the system experienced voltages and frequencies fluctuations because of aged equipment and lack of maintenance. In this regard, the Authority has started planned utility infrastructure inspections through which identifi ed anomalies are communicated to the utility operators for rectifi cation. Furthermore, the Authority allows funds through the multi-year tariff order for capital investment projects to address such problems.

2.2.4 Generation Capacity The installed capacity in the Isolated Grid was 78 MW, while installed capacity in the main grid was 1,261

MW. The Maximum Demand attained was 934.62 MW, recorded on 12th December 2014. During the period under review, a total of 6,164 GWh as were available for sale as shown in Table 4, which implies a 1.3% increase as compared to 6,085.92 GWh reported during the previous year. These units were received from TANESCO plants, IPPs, SPPs and imports from neighbouring countries.

Table 4: Electricity Generation and Imports

S/N Utility GWh: 2014-2015 Contribution (%)1 TANESCO 4,028,567 65.4%

2 Songas 1,358,260 22.0%

3 IPTL 588,244 9.5%

4 Aggreko 125,672 2.0%

5 SPPs 34,230 0.6%

6 Symbion 0 0.0%

7 Imports 63,345.82 1.0%

Total 6,164,089 100.0%

Source: EWURA

16

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

2.2.5 Generation Mix During the reporting period, the electricity generation mix consisted of hydropower 42%, natural gas 41%

and liquid fuel 17% as shown in Figure 3. In comparison to the previous years there is an increase of hydropower contribution in the generation mix. This increase was mainly due to improved rainfall in the catchment areas during rainy season of 2014, which resulted in having suffi cient water for the dry season of 2014 (August to November). During the review period, the Authority ensured that, the utility operates the available generation resources while adhering to least-cost merit order in order to minimize the cost of energy generation.

In 2014/15 thermal power plants including the emergency ones had dispatched less due to insuffi cient fund for fuel and good water level in the reservoirs. The emergency plants of 105 MW (Symbion Arusha and Dodoma) and 30 MW of Aggreko Tegeta had were decommissioned. Furthermore, there has been reduction of natural gas generation from 47% to 41%. After decommissioning of the emergency power plants, the remaining generating plants were able to fulfi l demand requirements up to the end of the review period. The new gas pipeline from Mtwara was expected to be completed in September 2015.

Figure 3: Electricity Generation Mix 2014-15

Source: EWURA

2.2.6 Customer Base During the year under review, the number of connected TANESCO customers was 1,502,474 as compared

to 1,298,468 customers recorded the previous year. The growth in customer connections was on record high due to an extensive grid extension of the distribution network funded by the Rural Energy Fund. This has increased access to electricity to about 36%, surpassing the Government target of 30% access by end of 2015.

2.2.7 Licensing

2.2.7.1 Power Supply Licensing During the period under review the Authority approved six generation licences (4 provisional and 2

operational) with potential generation capacity of up to 164MW as shown in Table 5 below. There were no transmission and distribution licences issued during the period under review.

17

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

Table 5: New Electricity Generation Licences

S/N Licensee Project Area

Capacity [MW]

Use Duration - Months

Date Issued

1 Dangote Industries Ltd Mtwara 75.00 Own Use 12 19-Mar-15

2 Aggreko Ubungo & Tegeta 70.00 Supply 6 16-May-15

3 East Coast Oils Kurasini 10.00 Supply 12 10-Feb-15

4 TEXPOL Development Co. Ltd Ilungu Ward Mbeya 6.20 Supply 36 4-Jun-15

5 Ulaya Hydro and Windmill Technology Ltd - Uzia Small Hydro Power

Uzia - Sumbawanga

1.12 Supply 36 16-Jun-15

6 Ulaya Hydro and Windmill Technology Ltd - Kalumbaleza Small Hydro Power

Kalumbaleza - Sumbawanga

1.20 Supply 36 16-May-15

Total 163.52Source: EWURA

2.2.8 Electrical Installation Contractors and Wiremen During the year under review, the Authority received a total of 209 licence applications for wiremen

and electrical contractors. Table 6 shows that 203 licences were issued to successful applicants while six licence applications were rejected mainly due to insuffi cient qualifi cations. Furthermore, in order to bring awareness on the Electricity Act, 2008 on licensing matters, the Authority conducted one Electrical Installation Contractors and Wiremen seminar in Dodoma which was attended by 83 registered contractors and wiremen from Singida, Morogoro, Dodoma, and Tabora. EWURA in collaboration with TANESCO continued to require electrical installation personnel to be licensed and refrain from doing work in breach of the law.

Table 6: Electrical Contractors and Wiremen license applied and issued

S/N CLASSNUMBER OF

APPLICATIONSLICENCESISSUED

REJECTEDAPPLICATION

1 A 14 14 0

2 B 26 24 2

3 C 60 58 2

4 D 56 55 1

5 W 53 52 1

TOTAL LICENCES ISSUED 209 203 6Source: EWURA

2.3 Tariff and Power Purchase Agreement

2.3.1 Tariff Review During the period under review, the Authority reviewed and approved Tariff Application from Armstone

Company Limited (ACL) for provision of electricity distribution services at Kyerwa District in Kagera region. The approved ACL’s interim tariff is shown in the Table 7.

18

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

Table 7: Approved ACL’s Interim Tariff

Customer Category ParticularsRequested Tariff

(in TZS)

Approved Tariff

(in TZS)

ST – Schools and Hospital Basic Monthly Charge - - Energy Charge per kWh 252 309

T1 – Household Customers Basic Monthly Charge 5,400 5,400

Energy Charge per kWh 342 235

T2 – Small, Middle and Large Entities

Monthly Charge 12,600 12,600

Energy Charge per kWh 342 267

Monthly Demand Charge per KVA 13,500 13,500

Source: EWURA

2.3.2 Power Purchase Agreements The Authority reviewed and approved the following PPAs between: (a) TANESCO and Aggreko International Projects Limited for a 50MW emergency power plant and an

additional capacity of 20 MW located at Ubungo and Tegeta in Dar es Salaam, respectively. (b) TANESCO and Geo Wind Power Limited for 50MW Singida wind power project was reviewed and

approved by the Board in August 2014. Furthermore, EWURA has completed review of a PPA between TANESCO and Zambia Electricity

Corporation (ZESCO), and the parties have been instructed to work on comments before signing the contract. The PPA is for electricity supply to the border town of Sumbawanga through the 66 kV Mbala - Sumbawanga Interconnector Transmission Line.

2.4 Regulatory Tools During the period under review, the Authority developed the Electricity (Development of Small Power

Projects) Rules, 2015 – GN No. 321 of 2015 and Electricity (Electrical Installation Services) Rules, 2015, - GN No. 404 of 2015. These rules were approved by the Authority and published in the Government Gazette. Also during the same period the Authority worked on the draft Electricity (Accident Reporting) Rules 2015 and Electricity Distribution Code. These documents are being reviewed and be circulated to stakeholders’ for comments.

2.5 Complaints and Dispute Resolutions A total of 88 complaints were brought forward from the previous fi nancial year while the number of

complaints received during the fi nancial year 2014/2015 were 51, resolving 59 complaints, and the remaining 80 are in progress.

2.6 Litigation During the period under review, the Authority was a party in six appeals in the electricity sub-sector all

of which were pending at the Fair Competition Tribunal. All appeals were against the decisions of the Authority in the complaints which were fi led by consumers to EWURA against TANESCO. Judgements for four out of six appeals were made in favour of the Authority while two are pending determination.

2.7 Health, Safety and Environmental Matters The Authority continued to sensitize electricity service providers on the need to keep their power supply

facilities and workplaces at highest level of safety. Furthermore, the service providers were reminded to disseminate information to the public on the dangers of electricity, and safe ways of using electricity, and have their workers maintain a high level of safety when working in the field. The Authority carried out

19

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

inspection of the power supply facilities, including power stations, substations, and distribution lines and service line entries, in order to check safety and environmental issues. Several challenges were noted, including old equipment, low hanging distribution lines, unprotected transformers, and unsatisfactory dangerous clearance of electricity conductors from building structures thus posing risk of electrocutions. The findings of the Authority during inspections were forwarded to the service providers for rectification. During the period under review there were no fatal accidents recorded, however there was one fi re incident recorded whereby a grid transformer at Mufi ndi was destroyed, causing power interruptions for a period of more than one month.

2.8 Key Achievements and Challenges

2.8.1 Achievements The achievements made by the Authority during the period under review include the following: (a) Development of Second Generation SPP Framework which included technology based Renewable

Feed-in Tariffs (REFITs) for Small Power Projects meant to attract investments in renewable energy. Solar and wind projects will be procured through competitive bidding process that is being developed and be available for use beginning 2016.

(b) Development of technology based Model Power Purchase Agreements(MPPAs) (c) Increased level of awareness of the need for licence for electrical installation personnel.

2.8.2 Challenges The major challenges that the Authority faced in the electricity sector during the year under review were; (a) Delay in decision making by other institutions than EWURA. The Authority experienced the delay in

the approval of model PPA and the Electricity (Approval of Power Purchase Agreements) Regulations, 2015. Also delay in gazetting the Electricity (Small Power Projects) Rules, 2015. The Authority will continue to make close follow up on issues submitted other institutions.

(b) TANESCO late payments to SPPs currently in operation has made it diffi cult to operate and new projects have diffi culty in getting fi nance. The Authority is working on a possibility to establish liquidity support facility in collaboration with World Bank.

(c) Unreliable electricity supply due to infrastructure related problems and lack of generation reserves. The Authority is carrying out regular infrastructure inspections and advise TANESCO to take corrective measures to improve the network. The Authority will also continue to take measures to improve the investment climate so as to attract more investments in electricity generation especially by private sector.

(d) Despite the fact that the Authority has developed regulatory tools to attract private investment, the pace of private investment in the electricity sector is not suffi cient to meet the rapid growing demand of electricity in the country. The Authority, in collaboration with the Government, is working on strategies developed under the Big Results Now initiatives to enable increased electrification and increased involvement of the private sector.

20

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

3.0 PETROLEUM SECTOR PERFORMANCE AND REGULATION

3.1 Overview The Authority continued to regulate the downstream petroleum sub-sector in Mainland Tanzania, covering

technical and commercial aspects. The regulated service providers include Oil Marketing Companies, Retail Outlets, Lubricants and Liquefi ed Petroleum Gas (LPG) Wholesalers.

EWURA is committed to continuously improve standards of petroleum products and facilities. Furthermore, the Authority continued with its efforts to ensure that there is all times, adequate and stable supplies of petroleum products in the country, and that these products are not sold above the monthly published cap prices.

3.2 Performance Monitoring

3.2.1 Petroleum Products Supply and Consumption Monitoring

(a) Petroleum Products Supply All Oil Marketing Companies (OMCs) submitted to the Authority their stocks on weekly basis as required.

This was done to ensure that there was at all times adequate supplies of petroleum products in the country. The Authority continued to prepare weekly stock reports which were shared with various key stakeholders such as the Ministry of Energy and Minerals, PICL inter alia.

Throughout the period under review, there was no critical stock out, except for few incidents of which some operators were hoarding stocks in anticipation of price increase. The Authority responded by taking punitive measures to all those who caused such artifi cial shortages.

During the period under review, a total of 4.60 billion litres of petroleum products were imported into the country through Dar es Salaam port and Sirari border. That included 2.99 billion litres for the local market and 1.61 billion litres as transit to neighbouring countries. Total imported volume for the fi nancial year 2014/15 decreased by two percent (2%) when compared to 4.71 billion litres which were imported in the previous fi nancial year of 2013/14.

On the other hand, the total imported volume for local consumption was 2.99 billion litres, an increase of one percent (1%) when compared to 2.97 billion litres imported in the previous fi nancial year 2013/14. As for the transit products, imported volume was 1,61 billion litres, a decrease of eight percent (8%) when compared to 1.74 billion litres imported in the previous fi nancial year 2013/14.

Dar es Salaam port continued to be the main entry point of petroleum products and accommodated 99% of all imports, leaving the remaining 1% to Sirari border. Table 8 and Table 9 show the volume of petroleum products imported for the local and transit markets respectively, under 2014/15 fi nancial year.

It is clear from the tables that local market petroleum products imports were 65% of the total imported petroleum products and the remaining 35% were imported for the transit market (Zambia, Democratic Republic of Congo, Rwanda, Malawi and Burundi).

21

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

Table 8: Petroleum Products Imports for the Local Market (Litres)

Month Diesel Petrol IK Jet A1 HFO TotalJul-14 104,786,808 74,541,954 4,245,527 13,133,375 12,501,797 209,209,461

Aug-14 117,068,219 73,401,147 5,333,889 13,959,038 12,893,044 222,655,337

Sep-14 112,070,244 70,882,584 1,545,590 13,919,977 21,370,493 219,788,888

Oct-14 103,309,470 85,479,929 1,915,867 27,862,603 - 218,567,869

Nov-14 101,995,448 46,174,386 2,090,095 28,057,185 30,160,444 208,477,558

Dec-14 80,762,196 56,668,921 3,084,276 15,751,045 30,827,758 187,094,196

Jan-15 92,315,101 48,446,376 2,077,751 26,739,386 - 169,578,614

Feb-15 97,150,812 25,705,755 2,254,423 16,498,531 14,530,516 156,140,037

Mar-15 107,133,807 68,338,677 1,621,533 14,173,368 - 191,267,386

Apr-15 97,061,973 48,640,231 1,337,819 12,117,285 36,733,130 195,890,439

May-15 127,004,653 73,273,833 611,430 12,572,769 6,880,626 220,343,311

Jun-15 124,252,829 62,443,068 2,082,846 12,879,658 32,422,880 234,081,281

Add localized-Jul-2014 to May 2015 321,232,388 197,871,368 12,606,598 - 27,959,772 559,670,126

Total 1,586,143,949 931,868,231 40,807,644 207,664,220 226,280,459 2,992,764,502

Source: EWURA

Table 9: Transit Petroleum Products Imports (Litres)

Month Diesel Petrol IK HFO TotalJul-14 78,418,458 68,931,510 4,206,193 - 151,556,161

Aug-14 132,484,057 80,929,699 7,375,995 508,258 221,298,009

Sep-14 92,509,330 75,462,606 4,902,782 - 172,874,718

Oct-14 85,108,875 69,966,370 5,935,722 - 161,010,967

Nov-14 123,007,591 56,017,114 4,759,925 1,039,327 184,823,957

Dec-14 123,871,331 54,313,496 6,319,670 8,135,096 192,639,593

Jan-15 92,574,434 45,229,139 5,870,114 - 143,673,687

Feb-15 123,886,590 42,117,569 5,127,659 - 171,131,818

Mar-15 98,120,090 88,111,352 6,342,209 - 192,573,650

Apr-15 98,257,512 73,959,658 4,913,481 11,381,774 188,512,424

May-15 93,445,929 89,942,056 4,137,172 - 187,525,156

Jun-15 120,179,563 71,974,861 4,671,014 3,115,716 199,941,154

Less localized (Jul-2014 to May-2015) (298,313,605) (220,790,151) (12,606,598) (27,959,772) (559,670,126)

Total 963,550,154 596,165,278 51,955,337 (3,779,600) 1,607,891,169

Source: EWURA

Furthermore, during the year under review, a total of 69,148 MT of LPG were imported into the country as compared to 69,257 MT which was imported in the previous fi nancial year of 2013/14. The noted decrease of 0.2% in the LPG imports was because of a substantial decrease in the re-exported volume. It may be noted that consumption of the product in the local market is increasing.

(b) Petroleum Products Consumption During the fi nancial year 2014/15, the industry recorded sales of 3.1billion litres of petroleum products, an

increase of 5% when compared to previous fi nancial year performance which was 2,938,896,450 litres. The petroleum market in the country is competitive and fairy distributed among different oil marketing

22

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

companies, as shown in Figure 4. There are only two companies with market shares of above 10%, namely PUMA Energy (12%) and Oryx Energies (12%), the rest have market shares below 10% (Figure 4). Companies that attained market shares of less than 10% but higher than 5% are Camel Oil (9%), Total (9%), Star Oil (8%), Oil Com (8%), GBP(6%) Gapco (6%) and Lake Oil (5%).

Figure 4: OMCs Market Shares

Source: EWURA

In terms of consumption, as it can be seen in Figure 5 Diesel outperformed all other products by registering 54% of total annual consumption, followed by Petrol (31%), Jet A1(7%), Fuel Oil(7%) and Kerosene(1%). The overall fuel consumption for petroleum products went up by 5% during the period under review when compared to the previous fi nancial year. Diesel dropped by 4% and this was attributed by improved power supply from hydro and natural gas that was used for power generation.

Petrol consumption increased signifi cantly during the period under review and this was probably because of increased number of vehicles using petrol in the country as well as the motorcycles commonly known as (boda boda). Kerosene continued to drop, possibly due to progressive measures exercised by the Authority to curb fuel adulteration, but also increased number of households connected to the supply of electricity, particularly in rural areas under the REA (Rural Energy Agency) scheme.

Figure 5: Local Consumption by Product

Source: EWURA

23

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

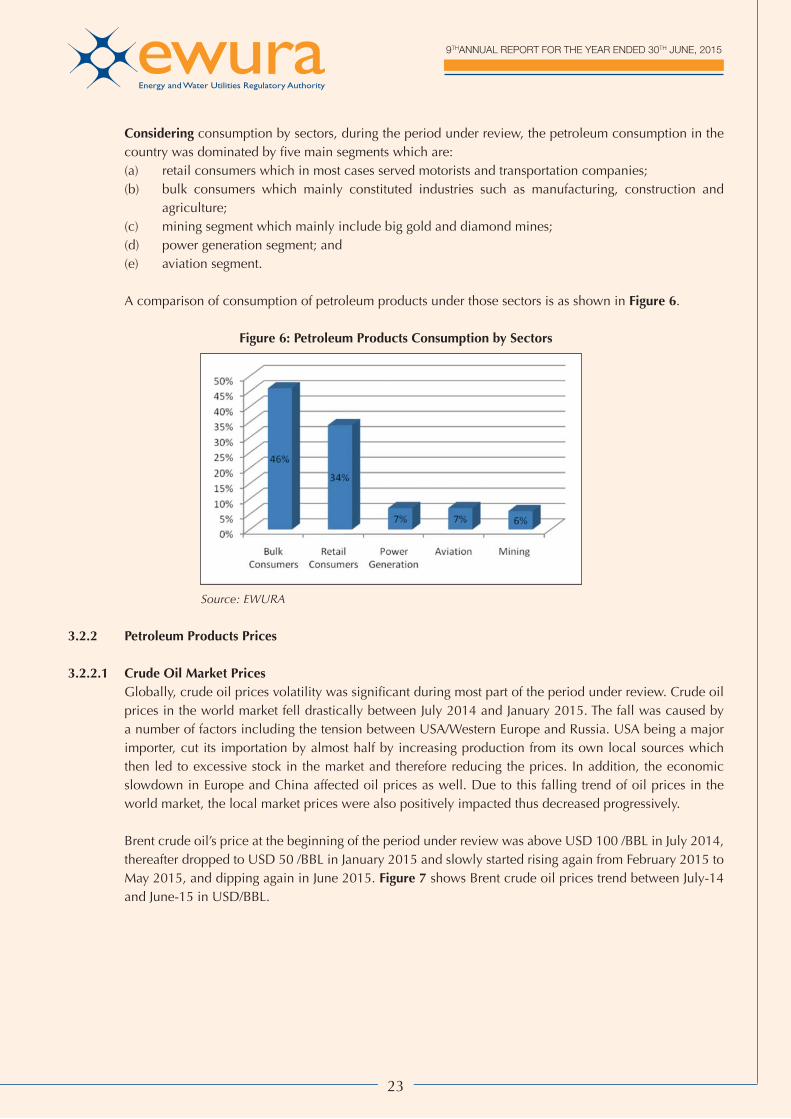

Considering consumption by sectors, during the period under review, the petroleum consumption in the country was dominated by fi ve main segments which are:

(a) retail consumers which in most cases served motorists and transportation companies; (b) bulk consumers which mainly constituted industries such as manufacturing, construction and

agriculture; (c) mining segment which mainly include big gold and diamond mines; (d) power generation segment; and (e) aviation segment.

A comparison of consumption of petroleum products under those sectors is as shown in Figure 6.

Figure 6: Petroleum Products Consumption by Sectors

Source: EWURA

3.2.2 Petroleum Products Prices

3.2.2.1 Crude Oil Market Prices Globally, crude oil prices volatility was signifi cant during most part of the period under review. Crude oil

prices in the world market fell drastically between July 2014 and January 2015. The fall was caused by a number of factors including the tension between USA/Western Europe and Russia. USA being a major importer, cut its importation by almost half by increasing production from its own local sources which then led to excessive stock in the market and therefore reducing the prices. In addition, the economic slowdown in Europe and China affected oil prices as well. Due to this falling trend of oil prices in the world market, the local market prices were also positively impacted thus decreased progressively.

Brent crude oil’s price at the beginning of the period under review was above USD 100 /BBL in July 2014, thereafter dropped to USD 50 /BBL in January 2015 and slowly started rising again from February 2015 to May 2015, and dipping again in June 2015. Figure 7 shows Brent crude oil prices trend between July-14 and June-15 in USD/BBL.

24

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

Figure 7: Crude Price trend from Jul-14 to Jun-15 in USD/BBL

Source: PLATTS Arab Gulf

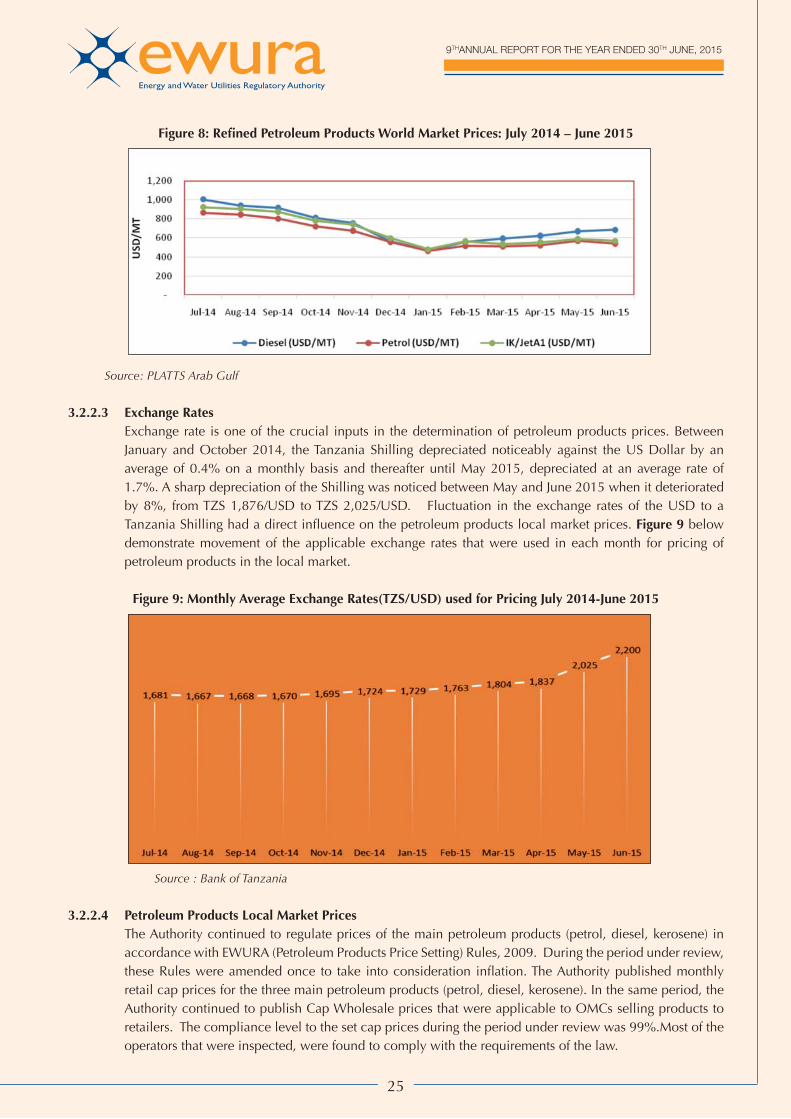

3.2.2.2 Refi ned Petroleum Products Prices in the World Market During the period under review, average monthly prices of refi ned petroleum products in the world market

ranged between USD 1,004/MT and USD 468/MT. This was a very volatile trend that was caused by falling crude oil prices in the market. Lowest prices were recorded in January 2015, thereafter a slight upward trend was experienced through June 2015. Monthly average World Market FOB prices are shown in Table 10 Error! Reference source not found.and Figure 8 below.

Table 10: Refi ned Petroleum Products World Market Prices from July 2014- June 2015

Month Diesel (USD/MT) Petrol (USD/MT) IK/JetA1 (USD/MT)

Jul-14 1,004 865 923

Aug-14 938 847 907

Sep-14 914 803 875

Oct-14 809 721 783

Nov-14 755 676 744

Dec-14 564 561 600

Jan-15 468 465 483

Feb-15 556 517 567

Mar-15 592 511 537

Apr-15 622 522 556

May-15 669 570 590

Jun-15 683 544 571

Avg 2014/15 715 633 678

Avg 2013/14 894 979 952

% Change -20% -35% -29%

Source: PLATTS Arab Gulf

25

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

Figure 8: Refi ned Petroleum Products World Market Prices: July 2014 – June 2015

Source: PLATTS Arab Gulf

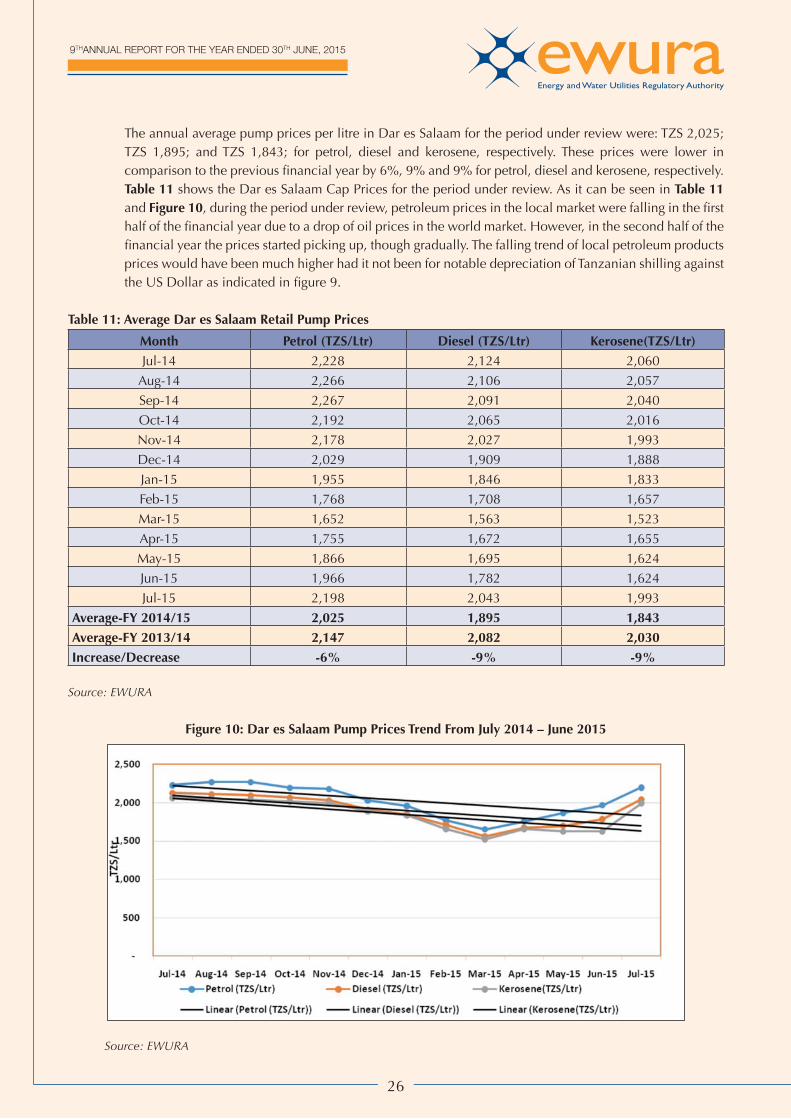

3.2.2.3 Exchange Rates Exchange rate is one of the crucial inputs in the determination of petroleum products prices. Between

January and October 2014, the Tanzania Shilling depreciated noticeably against the US Dollar by an average of 0.4% on a monthly basis and thereafter until May 2015, depreciated at an average rate of 1.7%. A sharp depreciation of the Shilling was noticed between May and June 2015 when it deteriorated by 8%, from TZS 1,876/USD to TZS 2,025/USD. Fluctuation in the exchange rates of the USD to a Tanzania Shilling had a direct infl uence on the petroleum products local market prices. Figure 9 below demonstrate movement of the applicable exchange rates that were used in each month for pricing of petroleum products in the local market.

Figure 9: Monthly Average Exchange Rates(TZS/USD) used for Pricing July 2014-June 2015

Source : Bank of Tanzania

3.2.2.4 Petroleum Products Local Market Prices The Authority continued to regulate prices of the main petroleum products (petrol, diesel, kerosene) in

accordance with EWURA (Petroleum Products Price Setting) Rules, 2009. During the period under review, these Rules were amended once to take into consideration infl ation. The Authority published monthly retail cap prices for the three main petroleum products (petrol, diesel, kerosene). In the same period, the Authority continued to publish Cap Wholesale prices that were applicable to OMCs selling products to retailers. The compliance level to the set cap prices during the period under review was 99%.Most of the operators that were inspected, were found to comply with the requirements of the law.

26

9THANNUAL REPORT FOR THE YEAR ENDED 30TH JUNE, 2015

The annual average pump prices per litre in Dar es Salaam for the period under review were: TZS 2,025; TZS 1,895; and TZS 1,843; for petrol, diesel and kerosene, respectively. These prices were lower in comparison to the previous fi nancial year by 6%, 9% and 9% for petrol, diesel and kerosene, respectively. Table 11 shows the Dar es Salaam Cap Prices for the period under review. As it can be seen in Table 11 and Figure 10, during the period under review, petroleum prices in the local market were falling in the fi rst half of the fi nancial year due to a drop of oil prices in the world market. However, in the second half of the fi nancial year the prices started picking up, though gradually. The falling trend of local petroleum products prices would have been much higher had it not been for notable depreciation of Tanzanian shilling against the US Dollar as indicated in fi gure 9.

Table 11: Average Dar es Salaam Retail Pump Prices