Annual Report 2015 - Central Bank of Bahrain R/CBB ANNUAL REPORT 2015... · 4.4 ATM Network...

58

. Annual Report 2015

Transcript of Annual Report 2015 - Central Bank of Bahrain R/CBB ANNUAL REPORT 2015... · 4.4 ATM Network...

.

Annual Report

2015

Central Bank of Bahrain Annual Report 2015

Table of Contents i

Table of Contents

1. Monetary Policy Developments .............................................................................. 1

1.1 Overview ........................................................................................................ 2 1.2 Monetary Policy Management ....................................................................... 2 1.3 Domestic Interest Rates ................................................................................. 2 1.4 Public Debt Issuance ...................................................................................... 3

2. Banking Developments ............................................................................................ 6

2.1 The Aggregate Balance Sheet of the Banking System .................................. 7 2.2 Retail Banks ................................................................................................... 7 2.3 Wholesale Banks ........................................................................................... 8

3. Regulatory and Supervisory Developments ........................................................ 10

3.1 Regulatory Developments ............................................................................ 11 3.2 Supervisory Developments .......................................................................... 14

4. Other CBB Projects and Activities ...................................................................... 34

4.1 New Licenses ............................................................................................... 35 4.2 Payment System (“SSS” & “RTGS”) .......................................................... 36 4.3 Cheque Clearing........................................................................................... 36 4.4 ATM Network (“BENEFIT”) ...................................................................... 36 4.5 Electronic Fund Transfer System (EFTS).................................................... 36 4.6 Currency Issue ............................................................................................. 37 4.7 CBB Training Programs .............................................................................. 38 4.8 IT Projects .................................................................................................... 38 4.9 External Communications Unit.................................................................... 39 4.10 CBB’s Organisational Chart ........................................................................ 43

5. FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015 ......................................................................................................................... 44

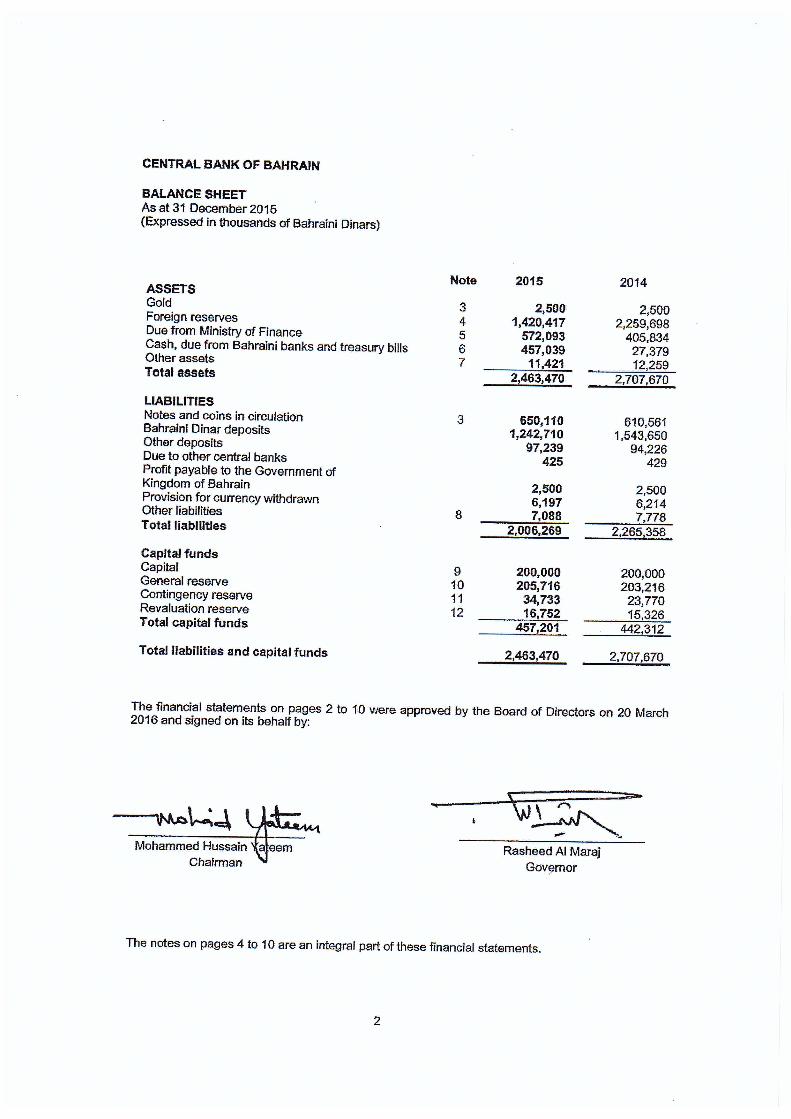

BALANCE SHEET (As at 31 December 2015) ...................................................... 44 PROFIT AND LOSS ACCOUNT AND APPROPRIATION (For the year ended 31 December 2015) ....................................................................................................... 44

Central Bank of Bahrain Annual Report 2015

Chapter 1: Monetary Policy Developments 1

1. Monetary Policy Developments

Overview

Monetary Policy Management

Domestic Interest Rates

Public Debt Issuance

Chapter

1

Central Bank of Bahrain Annual Report 2015

Chapter 1: Monetary Policy Developments 2

1.1 Overview During 2015, the Central Bank of Bahrain (“CBB”) continued to use a number of monetary policy measures aimed at maintaining the smooth functioning of financial markets in Bahrain. These measures included a range of monetary policy instruments as well as interest rate actions. 1.2 Monetary Policy Management Monetary Policy Committee The CBB Monetary Policy Committee (“MPC”) met on a weekly basis throughout 2015. The MPC closely evaluated economic and financial developments, monitored liquidity conditions, provided recommendations for monetary policy instruments and set interest rates on facilities offered by the CBB. Reserve Requirements All retail banks are required to maintain, on a monthly basis, a specific percentage of their non-bank deposits (denominated in Bahraini dinars), in a non-interest-bearing account at the CBB. During 2015, the reserve requirement did not change from 5%. 1.3 Domestic Interest Rates Key Policy Interest Rates

Based on the US Federal Reserve Bank's decision to raise interest rates on December 17, 2015, the Central Bank of Bahrain, on the same date, raised interest rates for the facilities provided by the CBB for retail banks by 0.25%, as follows: The interest rate for the overnight deposit facility was raised to 0.50% and for the one-week maturity to 0.75%, during the period from October to December 2015. There has been no change in the overnight lending rate offered by the CBB for borrowing against government treasury bills, deposits of retail banks and the return against Islamic Ijara Sukuk was 2.25% during the same period. Wakalah

As part of the ongoing efforts towards the development of Islamic banking and promoting investment opportunities for Islamic retail banks, the Central Bank of Bahrain (CBB) launched a new Sharia compliant Wakalah investment tool. This tool, which was approved by the Shariah Board of the CBB, is aimed at absorbing excess liquidity of the local Islamic retail banking through the Wakalah agreement. The agreement has been developed, based on a standard

Central Bank of Bahrain Annual Report 2015

Chapter 1: Monetary Policy Developments 3

contract of the International Islamic Financial Market (IIFM), that is currently used by all Islamic banks in Bahrain. The Wakalah is an investment opportunity for Islamic retail banks who wish to deposit excess liquidity with the CBB. Islamic retail banks need to sign a Wakalah agreement which appoints the CBB as an agent (Wakil) to invest cash on behalf of the bank (Muwakkil). Accordingly, the Wakil will invest these funds in the investment portfolio allocated in advance, and contains international Islamic Sukuks in US dollars and cash in Bahraini dinars. The duration of the Wakalah is one week and is available for retail Islamic banks every Tuesday. Interbank Rates As at end-2015, the 3 month BHIBOR rate was 1.62 %, compared to 1% at end-2014. The 6 month BHIBOR rate 1.77% at end-2015 compared to 1.25 % at end-2014. 1.4 Public Debt Issuance In accordance with the CBB Law, the CBB issues, on behalf of the Government of Bahrain, short and long-term debt instruments, including Treasury Bills, Government Bond, Sukuk AlSalam and Ijarah Sukuk. The issuance of all government debt securities is executed in coordination with the Ministry of Finance (MOF). The Central Bank of Bahrain, at the request of the Ministry of Finance, increased the amount of the short-term government issues in February 2015, as follows:

x Increase the amount of the 3 month treasury bills from BD 35 million to BD 70 million.

x Increase the amount of the 6 month treasury bills from BD 30 million to BD 35 million.

x Increase the amount of the 12 month treasury bills from BD 150 million to BD 200 million.

x Increase the amount of the 6 month Ijara sukuk from BD 20 million to BD 26 million.

x Increase the amount of 3 month Sukuk AlSalam from BD 36 million to BD 43 million.

Central Bank of Bahrain Annual Report 2015

Chapter 1: Monetary Policy Developments 4

During 2015, the CBB issued conventional 3-month treasury bills, denominated in Bahraini dinars, on a weekly basis, with an issue amount of BHD 70 million. Six (6)-month Treasury Bills were also issued, on a monthly basis, with an issue amount of BHD 35 million. In addition, the CBB issued 12-month Treasury Bills on a quarterly basis, with an issue amount of BHD 200 million. The CBB also issued, on a monthly basis, three-month Sukuk AlSalam for BHD 43 million. In addition, the CBB issued, on a monthly basis, six-month Ijara Sukuk for BHD 26 million. In addition, the CBB issued long-term Ijarah Sukuk in various denominations and for different maturities, upon the request of the Kingdom of Bahrain’s government, represented by the Ministry of Finance. The Central Bank of Bahrain, during 2015, at the request of the Ministry of Finance, issued domestic and international government development bonds of different periods, as follows:

x Local development bonds with an issue amount of BD 100 million on July 14, 2015, with a maturity of two years, fixed-rate of 2.75%.

x Local development bonds with an issue amount BD 150 million on July

30, 2015, with a maturity of 5 years, at a fixed rate of 4%.

x Local development bonds with an issue amount of BD 100 million on August 4, 2015, with a maturity of 3 years, at a fixed rate of 3%.

x International development bonds with an issue amount of US $ 800

million on November 24, 2015, with a maturity of 10 years and two months, at an interest rate of 7%.

x International development bonds with issue amount of US $ 700

million on November 24th, 2015, with a maturity of 5 years and two months, at a fixed rate of 5.875%.

The CBB also issued long-term Ijara Sukuks with different amounts and maturities, according to the needs of the Government of the Kingdom of Bahrain, represented by the Ministry of Finance, in coordination with the CBB from within and outside Bahrain. The CBB issued three Islamic issuances which were as follows:

Central Bank of Bahrain Annual Report 2015

Chapter 1: Monetary Policy Developments 5

x Ijara Sukuk with an issue amount of BD 100 million on January 8, 2015, for a period of 3 years, fixed return of 3%.

x Ijara Sukuk with an issue amount of BD 250 million on January 19,

2015, for a period of 10 years, fixed return of 5.5%.

x Ijara Sukuk with an issue amount of BD 200 million on July 9, 2015, for a period of 10 years, fixed return of 5%.

Central Bank of Bahrain Annual Report 2015

Chapter 2: Banking Developments 6

2. Banking Developments

The Aggregate Balance Sheet of the Banking System

Retail Banks

Wholesale Banks

Chapter

2

Central Bank of Bahrain Annual Report 2015

Chapter 2: Banking Developments 7

2.1 The Aggregate Balance Sheet of the Banking System Total aggregate balance sheet for the banking system (retail and wholesale banks) increased to USD 191.0 billion by the end of 2015, compared to USD 189.3 billion at the end of 2014, an increase of 0.9%. Wholesale banks represented 57.7% of total assets, whilst retail banks accounted for 42.3%. Domestic banking assets amounted to USD 52.6 billion at the end of 2015 compared to USD 49.3 billion at the end of 2014, representing an increase of USD 3.3 billion (6.7%). Foreign assets amounted to USD 138.4 billion, compared to USD 140.0 billion at the end of 2014, a decrease of USD 1.6 billion (1.1%). Domestic liabilities increased to USD 52.6 billion at the end of 2015 compared to USD 51.9 billion at the end of 2014, an increase of USD 0.7 billion (1.3%). Total foreign liabilities increased by USD 1.0 billion (0.7%) to reach USD 138.4 billion against USD 137.4 billion at the end of 2014. 2.2 Retail Banks1 The aggregate balance sheet of retail banks increased by 2.7% to BD 30.9 billion at the end of 2015, compared to BD 30.1 billion at the end of 2014. Total domestic assets grew by BD 0.9 billion (5.8%) to reach BD 16.5 billion, with claims on private non-banks sector increasing by BD 0.6 billion (7.5%) and claims on general government securities growing by 0.3 billion (9.1%). Foreign assets recorded a decrease of BD 0.1 billion (0.7%), reaching a total of BD 14.4 billion at the end of 2015 compared to BD 14.5 billion at the end of 2014. Claims on foreign non-banks increased by BD 0.3 billion (3.4%) from BD 8.7 billion at the end of 2014 to BD 9.0 billion at the end of 2015, while claims on foreign banks decreased by BD 0.4 billion (6.9%), reaching a total of BD 5.4 billion at the end of 2015. Total domestic liabilities of retail banks increased by BD 0.5 billion (3.2%) from BD 15.7 billion at the end of 2014 to BD 16.2 billion at the end of 2015. This was due to an increase in liabilities to private non-banks by BD 0.3 billion (3.2%) and liabilities to capital and reserves by BD 0.2 billion (8.3%). Total foreign liabilities increased to reach BD 14.8 billion at the end of 2015. Liabilities to foreign banks decreased by BD 0.1 billion (1.2%) and liabilities to foreign non-banks increased by BD 0.5 billion (8.2%). 1 This includes conventional and Islamic retail banks.

Central Bank of Bahrain Annual Report 2015

Chapter 2: Banking Developments 8

Loans and Credit Facilities Outstanding loans and credit facilities of retail banks stood at BD 7.8 billion at the end of 2015, a 9.9% increase compared to the BD 7.1 billion at the end of 2014. The business sector accounted for 53.0% of total loans and credit facilities, while individuals and the government sector represented 43.2% and 3.8% respectively. Deposits Retail banks’ total domestic deposits increased to BD 11.4 billion at the end of 2015 compared to BD 11.1 billion at the end of 2014, an increase of BD 0.3 billion (2.7%). This was due to higher private sector deposits which increased by BD 0.3 billion (2.8%) while general government deposits decreased by BD 0.02 billion (1.5%) Domestic deposits in Bahraini Dinar increased by BD 0.1 billion (1.1%) to BD 9.1 billion at the end of 2015. Domestic foreign currency deposits increased BD 0.2 billion (9.5%) to BD 2.3 billion from BD 2.1 million. Bahraini Dinar deposits and foreign currency deposits constituted 79.8% and 20.2% of total domestic deposits respectively. Geographical and Currency Distribution of Assets The share of total assets accounted for by the member countries of the Gulf Cooperation Council (GCC) (excluding Bahrain) reached a total of 20.6% while Asia accounted for 10.2%, Western Europe accounted for 5.5%, North and South America for 6.1%, and other Arab countries for 2.7%. In terms of currency, the share of US dollar denominated assets was 45.4%, while the GCC currencies (excluding Bahraini dinar) accounted for 5.8% of total assets. The Euro represented 2.4% of total assets. 2.3 Wholesale Banks2 3

The aggregate balance sheet of wholesale banks fell by USD 0.5 billion or 0.5% to USD 108.8 billion at the end of 2015, compared with USD 109.3 billion at the end of 2014. Total domestic assets grew to USD 8.6 billion at 2015, compared with USD 7.8 billion at the end of 2014. Foreign assets decreased by USD 1.3 billion (1.3%) to USD 100.2 billion at the end of 2015. This was due to decreases in claims on Securities by USD 1.5 billion (7.5%), and in claims on banks by USD 2.6 billion (15.3%).

2 This includes conventional and Islamic wholesale banks. 3 The balance sheets of wholesale banks are usually denominated in USD.

Central Bank of Bahrain Annual Report 2015

Chapter 2: Banking Developments 9

Total domestic liabilities of wholesale banks declined by USD 0.5 billion (5.0%) to USD 9.6 billion at the end of 2015 compared with USD 10.1 billion at the end of 2014. Foreign liabilities increased slightly by USD 0.04 billion to reach USD 99.2 billion at the end of 2015. This increase was mainly due to an increase in liabilities on banks which increased by USD 2.7 billion (8.5%) Geographical and Currency Distribution of Assets The share of total assets accounted for by the GCC (excluding Bahrain) reached a total of 32.8%, while Western Europe accounted for 34.7%, North and South America for 8.4%, Asia for 10.8%, and other Arab countries for 3.6%. As for currency, the share of GCC currencies (excluding Bahraini dinar) of total assets was 12.2% with the dollar accounting for 68.1% of total assets and the Euro comprising 7.6% of total assets.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 10

3. Regulatory and Supervisory Developments

Regulatory Developments

Supervisory Developments

Chapter

3

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 11

3.1 Regulatory Developments As part of CBB’s continuing development of the regulatory framework for the financial system, work was carried out during the year 2015 to strengthen regulatory policies and to develop appropriate prudential regulations, in order to maintain financial stability and market integrity. 3.1.1 Updates to CBB Rulebook Basel III adoption In January 2015, the CBB started implementing the new capital adequacy rules in accordance with the requirements of Basel III & Islamic Financial Services Board (IFSB) for conventional & Islamic Banks respectively. The CBB has also issued in March 2015 the revised Prudential Information Returns (PIRs) in its final form for conventional banks as per Basel III requirements, and for the Islamic banks as per the IFSB requirements. The first updated PIRs were submitted formally by banks for the quarter ending 31st March 2015. Moreover, the CBB has issued a consultation paper on Basel III Leverage Requirements in March 2015. The CBB is currently studying the received comments and feedback thereof internally. In May 2015, the CBB has issued its requirements on Public Disclosure in accordance with Basel III and started receiving the financial reports according to these requirements from conventional banks in June 2015. In addition, the CBB has issued a consultation paper on its requirements on the Public Disclosure for Islamic banks in accordance with Basel III in November 2015. The CBB is currently working on developing the Liquidity Risk Management requirements according to Basel III. Resolution No. (20) of the year 2015 in respect of the establishment of a Centralized Shari’a Supervisory Board Resolution No. (20) of the year 2015 in respect of the establishment of a Centralized Shari’a Supervisory Board was issued on the 23rd April 2015 in the Official Gazette. This Board shall operate under the supervision of the CBB. The objective of the resolution is to develop the Islamic financial industry and to implement a unified Islamic Shari’a standards and practices across the Islamic financial industry. The Resolution includes, but not limited to, the roles and responsibilities of the Board, formation of the Board, term of membership, membership requirements and the binding force of the Board’s fatwas and opinions.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 12

Consultation papers on proposed directives for Ancillary Service Providers

The CBB intends to issue new directives soon for Ancillary Service Providers as part of Rulebook Volume 5 for Specialized Licensees following the consultation conducted with the financial sector and the concerned parties in this regard. These new directives cover the Authorization, General Requirements and the CBB Reporting Modules. Proposed amendments to the Operational Risk Management Module (OM) for banks and financing companies The CBB has issued a consultation paper in May 2015 on proposed amendments to the Operational Risk Management Module (OM) for retail banks and financing companies introducing rules related to outsourcing of services which contains customers’ information. The CBB received all comments from retail banks and financing companies and is currently studying them internally to be discussed and issued in the final form. Resolution No. (23) of the year 2015 with respect to the Conditions and Procedures for Obtaining Approval for members of the board of directors and Controlled Functions within Licensees

The CBB has issued Resolution No. (23) in May 2015 which stipulates the terms and conditions for the CBB’s approval requirements of licensees’ memberships on the board of directors and for any executive position in accordance with Article 65(a) of the CBB Law. Proposed directives on ATM Security for retail banks

As part of the CBB’s objectives to protect the depositors and customers of financial institutions, the CBB has issued in May 2015 a consultation paper to retail banks that includes new proposed requirements with regards to ATMs security which are in line with the best international practices as part of the security measures for retail banks. The CBB received retail banks comments in this regard and is currently studying them internally in order to discuss and issue such directives in the final form. Proposed amendments to Module HC for Volume 2 Islamic banks The CBB has issued a consultation paper in May 2015 to align the High Level Controls Module of Volume 2 for Islamic banks with the following international standards:

x Principles for enhancing corporate governance issued by the Basel Committee in October 2010.

x Guiding Principles on Corporate Governance for institutions offering only Islamic financial services issued by the IFSB in December 2006.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 13

x Compliance and compliance function in banks issued by the Basel Committee in April 2005.

In addition, the CBB is currently studying the comments received from the Islamic banks on the consultation paper.

The CBB is also updating the paper to include the recent update issued by Basel Committee in July 2015 titled “Guidelines – Corporate Financial Governance Principles for banks” in order to be issued as a second consultation paper. Early Repayment Charges for Murabaha Corporate Financing Facilities The CBB issued in August 2015 a circular to all Islamic banks with regards to early repayment charges for murabaha corporate financing facilities aiming to identify the current related practices in order to standardize the process of dealing with early settlements of such facilities so that Islamic banks would maintain their competitive advantage compared to the conventional banks. The CBB has studied banks’ comments and is currently developing a proposed directive in this regard. Proposed directives on offering banking and financial services to the disabled customers The CBB has issued a consultation paper in November 2015 with regards to proposed directives on offering banking and financial services to the disabled customers to all retail banks, financing companies, Ministry of Labour and Social Development and Societies of the disabled. The CBB received the feedback and comments from all parties which are currently being studied internally.

The proposed directives include special measures and procedures to deal with the disabled customers to safeguard their rights of accessing banking and financial services on an equal basis with others, using appropriate methods of communication, and by creating the appropriate environment according to their needs. For the purpose of the above stated proposed directives, “disabled” is defined as the customers who have the ability to make their own decisions but they need assistance to do so due to their circumstances. Disabled includes visual impairments and blind, hearing impairments and physical impairments. Consultation paper on the Proposed Changes to Credit Risk Management Module (CM) concerning the CBB’s prior approval requirements on writing-off exposures

The CBB has issued in November 2015 a consultation paper with regards to proposed changes to Credit Risk Management Module (CM) which include widening the scope of obtaining the CBB’s prior written approval before writing-off any exposure that is more than BD100, 000 or equivalent in foreign currency to include all branches of foreign banks operating in the Kingdom, which was previously applied only to locally incorporated banks.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 14

The new proposals include also the requirement of obtaining the CBB’s prior written approval for approved person’s exposures within the licensees. Legislative Decree No. (34) of the year 2015 on the amendment of some provisions of The Central Bank of Bahrain and Financial Institutions Law No. (64) of 2006 “the Law”

In line with the CBB’s efforts on enhancing credit risk management process within the financial institutions to support financial stability in the Kingdom, an amendment of some provisions of The Central Bank of Bahrain and Financial Institutions Law No. (64) Of 2006 has been issued introducing a new Chapter in Part 2 of the Law with regards to the Credit Information Centers. The amendment includes several main aspects, namely: 1. Expansion of the membership of the Credit Information Centers to include some

government agencies and certain types of commercial companies along with the current financial institutions members.

2. Adding controlling measures to govern the process of exchanging credit information among the concerned parties in terms of:

a) Providing and receiving credit information. b) Maintaining information confidentiality. c) Receiving and processing any complaints raised by customers. d) Protecting the rights of both members and customers.

3. Increasing the limit of the administrative fines to BD100,000 instead of 20,000, in

the case of violation of any of the provisions of this Law. The fine shall be multiplied by the number of violations.

Credit Reports requested by pensioners

The CBB has issued in August 2015 a circular to all retail banks and financing companies with regards to waiving any administrative fees or charges required from pensioners in return of issuing a credit report or similar document to establish their credit standing in order to alleviate the financial burdens on such citizens. 3.2 Supervisory Developments Compliance Directorate During the year 2015, the Central Bank of Bahrain continued its efforts with particular emphasis on upgrading the Kingdom’s regulatory framework specific to AML/CFT through the Policy Committee, which is a national committee chaired by the CBB and is responsible for formulating AML/CFT policies, procedures and coordinating with relevant internal and external bodies.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 15

In light of the FATF recommendations introduced in February 2012, the Policy Committee continued to work with ministries and government authorities on a unified strategic plan with regards to anti money laundering and terrorist financing. The national plan aimed to implement the FATF recommendations within the specified time frame based on country’s risk assessment. As the revised FATF 40 recommendations require a systematic, risk-based AML/CFT assessment at both country level and institutional level, ministries and regulatory authorities will be responsible for thoroughly analysing and addressing the recommendations based on their relevance and applicability. It was decided in the Plenary meeting held in June 2015 that Bahrain will undergo the mutual evaluation based on the new FATF methodology. The assessment will commence in 2017 and will be discussed in 2018. As part of its systematic program to improve the AML/CFT framework in Bahrain, the CBB has continued to carry out examinations on relevant licensees to ensure compliance with the CBB’s regulations, to further enhance the on-site AML/CFT supervision and to help the licensees improve their systems of internal controls with respect to the prevention, detection, monitoring and reporting of suspicious transactions. Such examination visits help upgrade the level of AML/CFT awareness within banks, moneychangers, insurance firms and the capital market sector. The Kingdom of Bahrain has reached an agreement in substance with the United States of America relating to the Foreign Account Tax Compliance Act (FATCA) Intergovernmental Agreement “IGA” and have consented to be included on the Treasury and US Internal Revenue Service “IRS” list. In this regard, the US authorities have agreed on extending the FATCA reporting deadline from 30th September 2015 to 30th September 2016. The Compliance Directorate has been coordinating with the licensees to ensure their readiness for FATCA. The licensees were requested to register with the IRS to obtain their Global Intermediary Identification Numbers “GIINs” and provide detailed implementation plans outlining the steps that have been taken to ensure that all systems and procedures are in place to meet FATCA requirements by the proposed deadline. Banking Supervision Directorates The CBB continued its efforts towards achieving its objectives of ensuring financial stability and soundness of the banking sector as well as protecting the interests of consumers of banking services. To achieve these objectives, the CBB pursued proactive supervisory approach including enhanced monitoring of the banks and financial institutions, provided adequate assurance to the consumers of the banking sector through initiating measures that provide positive signals to the market and facilitate the development of the market and implemented rules based on international best practices which facilitate enhanced transparency and disclosures. Accordingly, the following measures were taken by the CBB during the year:

x Sound Remuneration Practices: The implementation of the CBB rules on ‘Remuneration of Approved Persons and Material Risk Takers’ (required to be implemented for the bonuses accruing for 2014) was monitored and reviewed

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 16

to ensure their timely and effective implementation by banks. The relevant rules in this regard align the bonuses of the employee with risks taken by them and encouraged long term relationship between the bank and the employee.

x Related Party Exposures: The CBB as part of its efforts towards limiting any risk concentration and ensuring compliance with its rules continued with its monitoring of related party exposures on a monthly basis.

x Monitoring the Level of Real Estate Exposures: The central bank with the intention of controlling risk concentration to volatile sector like the real estate sector, continued to monitor banks’ exposures to real estate on a quarterly basis.

x Monitoring of Impaired Loans Portfolio: The CBB on a quarterly basis persisted with its monitoring of the impaired loans portfolio of banks. Based on the assessment, the banks were advised, to take pre-emptive measures to limit the growth in impaired loans portfolio.

x Meeting on Financial Statements: The banking supervision directorates conducted annual trilateral meetings with locally incorporated banks and financing companies, and their external auditors to discuss the annual financial results for 2014, before these are submitted to the Board of Directors of the respective licensee for approval. The issues pertaining to impaired assets, adequacy of provisions, recognition of income, valuation practices, and proposed dividends etc were also deliberated in the meeting. In addition, the CBB conducted quarterly meetings with banks and financing companies to review their interim financial performance for the quarter during 2015.

x Monitoring of Board Performance and Organization Structure: The CBB reviewed the annual corporate governance reports submitted by banks and financing companies with the aim of evaluating the performance of Board of Directors. Such assessment included reviewing the Directors attendance in Board meetings, their participation in the discussions in Board meetings, Board sub-committees structure and the appointment of independent directors among others. Furthermore, a review of organization structure as well as succession plan of banks and financing companies was undertaken with the objective of monitoring implementation of effective corporate governance in these institution. The CBB’s representatives also attended the AGM/EAGM of licensees as observers as part of its monitoring of licensees corporate governance.

x Prudential Meetings: During the year, the conventional banking supervision directorates conducted 62 prudential meetings with the licensees under their

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 17

supervision. The deliberations in these meetings encompassed inter alia the licensees previous years financial performance, strategic direction for the future and other supervisory issues of relevance for the CBB. In addition, the banking supervision directorates also held quarterly meetings with Domestic Systemically Important Banks or D-SIBs.

x Bahrain Credit Reference Bureau (BCRB): The CBB in its endeavour to enhance the credit quality in the banking system and thereby promote financial soundness of institutions continued its efforts towards facilitating effective credit referencing services in the country through the BCRB. In this regard, banks were encouraged to ensure that the data shared in the BCRB system is devoid of any errors and is updated regularly.

x Studies/Surveys: The CBB conducted a number of surveys during the year as part of its proactive supervisory approach. The surveys included interest charged on credit cards among others.

x Domestic-Systematically Important Banks (D-SIBs): The domestic systematically important banks (D-SIBs) submitted their revised Recovery and Resolution Plans (RRPs) which were reviewed by the CBB in line with the Financial Stability Board guidance and specific requirements of the financial industry in Bahrain.

x Appointed Experts Assignments: As part of its efforts for enhancing the effectiveness of its supervisory practices the CBB appoints qualified “Appointed Experts” to conduct ‘Agreed upon Procedures’ through onsite Examination of its licensees. Accordingly, “Appointed Experts” handled 2 assignments during the year for conventional bank licensees.

x Consolidated Supervision: The CBB continuing with its consolidated supervision approach, visited Jordan and Malaysia to participate in the supervisory college meetings hosted by the home country regulator of banks in these respective countries, having their presence in Bahrain. Besides, such interaction facilitated cross border exchange of information between the CBB and the respective home country regulatory authority.

x Basel III Implementation: The CBB had earlier announced the timelines for implementing Basel III commencing from January 2015 onwards. The concerned directorates at the CBB monitored the implementation of Basel III by locally incorporated banks in accordance with the set timeline for the year 2015.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 18

x Electronic Submission of Returns and Analysis of Data (ESRAD): The supervision directorates monitored and facilitated in smoothening the online submission of data by licensees through the electronic system called ESRAD. The system is aimed at enabling the licensees to submit prudential returns online and bring efficiency in submission of information by licensees. The banking supervision directorates continued enhancing the ESRAD system to cater to the requirements of Basel III implementation.

Other activities undertaken by the Supervision Directorates include:

x Compliance with the “Code of Best Practice on Consumer Credit and Charging”: The CBB continued with its monitoring of the adherence with the provisions of the Code by retail banks and financing companies. The aim was to ensure that licensees act fairly, responsibly and reasonably in their dealings with consumers and are transparent in their dealings.

x Public Disclosure by Banks: The CBB continuously monitored banks

disclosures to its stakeholders including its compliance with the CBB Rules on public disclosures. As such, the banks were required to submit their public disclosures report duly reviewed by their external auditors. Non-compliance by banks with the CBB’s rules or any delays in submission of the required information to the CBB attracted enforcement actions including imposition of penalty on the bank. The banks were required to disclose in their annual reports the imposition of any fines/penalties by the CBB.

x Enforcement actions: The CBB endeavours to ensure high standards of compliance by its licensees with aim of reducing the risks to customers and the financial system as well as to ensure market discipline. It believes that effective enforcement facilitates effective supervision. Therefore, and in accordance with Article 38 of the CBB Law, the CBB has taken 21 enforcement measures against conventional banks and financing companies including imposition of penalties, during the year 2015.

Islamic Financial Institutions Supervision The Directorate is responsible for the supervision of the Islamic Financial Institutions that provide regulated banking services. These include 14 Wholesale Banks, 6 Retail Banks, 1 Financing Companies, 3 Branch of a Foreign Bank and 1 Microfinance Institution . The following are the key milestones achieved during the year 2015:

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 19

x Submitted a working paper on the experience of the Kingdom of Bahrain in the field of Shari’a corporate governance in the Islamic Banking industry during the 14th Annual Shari’a Conference of AAOIFI.

x Visited Japan to share the experience of the Kingdom of Bahrain in the development and support of the Islamic Banking sector with the Japanese Ministry of Finance and the Financial Institutions Supervision.

x Received a number of delegations from various countries around the world including South Africa, Tunisia, France, and Libya to share with them the experience of the Kingdom of Bahrain in the development and support of the Islamic Banking sector.

x Trained a delegate from The National Bank of the Republic of Kazakhstan for a period of two weeks.

x Participated in the Sharia scholars’ meetings and seminars conducted by Waqf Fund.

x Participated in a number of international training courses and seminars to cope with the latest developments in the financial sector. In addition, some staff were enrolled in Advanced Islamic Banking Diploma program.

x Participated in the IFSB annual meeting held in Jakarta and Jeddah.

x Conducted meetings with all Islamic Banks’ management team in order to discuss their strategies and future business plans.

x Implementation of Basel III and IFSB-15 standards on Capital Adequacy for Islamic Financial Institutions, and conducting related internal awareness programs for all Banking Supervisors.

x Implementing the Electronic Submission of Returns and Analysis of Data (ESRAD) system for electronic filing of returns by Licensees.

Inspection Directorate The Inspection Directorate completed its planned programs of onsite inspection visits to CBB licensees including full scope and subject specific visits. The Directorate employed a risk focused examination approach using the CMORTALE methodology focused on the following assessment elements- capital adequacy, management quality, operational risk, risk Management, transparency and disclosure, asset quality, liquidity and earnings. This methodology assesses the risk profile of the CBB’s

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 20

licensees with the ultimate objective of promoting the safety and soundness of financial institutions through onsite procedures aimed at identifying regulatory action required to reduce the risk of insolvency, the potential loss of market confidence, and losses to depositors or investors. During the year, the Directorate continued its effort to develop an enhanced risk profiling methodology to assess the business, control failure and systemic risks of the licensees. The updated risk profiling methodology shall enable enhanced assessment of probability of default and systemic risk of CBB licensees, in alignment with international best practices. In response to the greater focus towards the assessment of risk within the financial sector, the Directorate identified and implemented training and development programmers designed to provide inspection staff with the skills and experience necessary to assess the extent to which best practice risk management had been effectively embedded in the financial sector. The trainings included a dedicated forensic review skills training for the CBB examiners. During 2015, the Directorate participated in the discussions hosted in Riyadh by GCC Payment Committee, which focused on promoting enhanced networking and communication solutions. Capital Markets Supervision The CBB worked during 2015, to complete the implementation of its plan for the development and updating of the legislative, regulatory and supervisory framework for the capital market sector, in line with international standards and best practices in consultation with the stakeholders and interested parties in this sector and all other financial sector components in Bahrain. Developments & Achievements Development of the Rules and Regulations During this period, the CMSD worked to complete the regulatory and legal framework, including Volume 6 of the CBB Rulebook relating to the capital market, with its main objectives being to enhance transparency and develop the capital markets, and protect investors. These included the following activities:

x Unifying CBB Powers related to Listed Companies In order to consolidate and simplify the procedures relating to the control and supervision of the listed shareholding companies, and after the CBB’s completion of the regulatory and legal framework relating to the capital market in the Kingdom of Bahrain, the amendments on the Commercial Companies Law under Law No. (50) for the year 2014, came to provide for the identification of CBB powers in all matters relating to the control and supervision of listed companies, and in particular the text in Article (119 modified) which states that: " The dealing of the Company’s shares, its registration, transfer, depository, pledge, mortgage

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 21

and the Company’s purchase of its own shares shall be undertaken in accordance with the provisions of the Central Bank of Bahrain and Financial Institutions Law promulgated by Law No. (64) and any of its regulations issued pursuant to it.” In cooperation with the relevant stakeholders especially the Economic Development Board and the Ministry of Industry and Commerce, the CBB has issued Resolution No. (30) for the year 2015 to amend certain articles from Resolution No. (59) for the year 2011 pertaining to the procedures to be followed for the registration of pledges and liens on securities and the discharge and lifting of such pledges and liens.

These amendments stipulate the measures to be followed for the registration of pledges and liens on securities and their discharge as outlined in Resolution No. (59) for the year 2011 in relation to securities issued by public shareholding companies and ordinary shares issued by closed joint-stock companies. To activate the amendments, the CBB issued Circular No. CMS/202/15 dated 9th July, 2015 to all relevant stakeholders to ensure awareness to and compliance with the implementation of the same. x Development of Disclosure Standards The Central Bank of Bahrain issued Resolution No. (54) for the year 2015 in respect of Dissemination of Listed Companies’ Financial Statements and Board of Directors’ Meetings, issued in official Gazette No. (3242) dated 31st December 2015, which included some fundamental changes to the Resolution No. (49) for the year 2007, and in particular to allow for the boards of directors to hold meetings during the trading session , and therefore the use of appropriate mechanisms to disclose such a change, through the specimens provided by the resolution. x Amendments to the Annual Licensing Fees The issuance of Resolution No. (1) for the year 2016, on the amendment of Resolution No. (1) for the year 2007, in respect of determination of the licensing fees and services provided by the Central Bank of Bahrain (CBB) in the Official Gazette No. 3247 on Thursday 4th February 2016, regarding the method of calculating the total annual license fees for various categories of market intermediaries operating in the capital markets based on the total volume of transactions undertaken during a year on a pro-rata basis rather than on a predetermined fixed amount.

x Diversification of Financial Products and Instruments 1. The CBB approved Bahrain Bourse’s amendment to the listing requirements on Main Board of Bahrain Bourse (BHB) vide its letter Ref. No. CMS/L305/15 dated 15th November 2015, which has been approved by the Board of Directors of BHB under Resolution No. 5/2015 dated 11th November 2015, which included substantial changes, especially regarding the criteria of measuring the liquidity of

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 22

the shares of the listed companies, as well as the adoption of electronic registration on the Central registry and depository i.e. enabling title to securities to be evidenced and transferred without the need to produce written instrument in accordance with Article (178 ) of the CBB Law. 2. The CBB issued a letter Ref. No. CMS/L137/2015 dated 16th April 2015, regarding its final approval to the regulatory procedures and rules of listing and dealing of Real Estate Investment Trusts (REITs), and mandating Bahrain Bourse to publish those rules on its website before 21 day of the effective application for transparency purposes. In addition, the BHB issued the REITs listing rules on the 15th June 2015. 3. In order to achieve the goal of creating depth and diversity in the nature of the financial products and instruments that can be provided by the capital markets sector in the Kingdom of Bahrain, the CBB issued its in-principle approval to Bahrain Bourse to regulate and operate a market for listing and trading of securities issued by closed, small and medium-sized companies as an independent market from the main market, in order to attract these companies and dealers in their shares, whether inside or outside the Kingdom of Bahrain. The CBB expects the aforementioned rules to be finalized shortly. 4. Furthermore, the CBB approved the BHB’s request for provision of Murabaha through Equities service in accordance with the principles and requirements of Islamic Shariah and after coordinating with the concerned financial institutions. This service will hopefully be announced and implemented in the next phase. x Short Selling, Lending and Borrowing of Securities and Margin Trading Rules Complementing the legislative and regulatory framework for the capital markets sector and in accordance with the requirements of the CBB Law in general and Articles (91) and (92) in particular, the CBB has prepared the initial draft of the requirements and criteria of lending, borrowing, short selling and margin trading for securities traded as an initial draft to be developed in coordination with Bahrain Bourse and hopefully issue it as a consultation paper in the next phase. x Updating Technical Infrastructure

In accordance with the legislative, regulatory and supervisory development plans that the CBB has worked towards achieving during the previous years, and based on the achievements of the Bahrain Bourse (BHB) during the year 2014, the BHB succeeded in updating its Automated Trading System as well as the regulations relating to the settlement, clearing, central depository and central registry in line with the best international practices. The BHB has introduced the remote trading service during the year 2015, after coordinating and attaining approval of the CBB. This service will be provided to licensed members that are operating in securities markets outside the Kingdom of Bahrain, provided that their home market securities regulator is a member of the International Organization of Securities Commissions (IOSCO).

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 23

In addition, the central depository at the BHB is working on developing the technical infrastructure to improve system-specific requirements, particularly on the licensed members, through a personalized electronic link which will hopefully be offered during the next phase.

x Exchanges, Clearing, Settlement and Central Depositories

a) The CBB granted its in-principle and conditional approval to Bahrain Bourse

on 25th March 2013, for establishing an independent, Single Person Company that will offer clearing, settlement and central depository services. The main objective for setting up the new Company is to segregate the clearing, settlement and central depository operations from trading operations of Bahrain Bourse. The BHB is currently working on completing the procedures and formalities of setting up the Company.

b) The Capital Markets Supervision (CMS) Directorate issued its final approval to Bahrain Bourse Market Rules vide letter Ref. CMS/165/2014 dated 11th May 2014 and BHB started implementing the Rules on 1st September 2014. BHB members were given a six month transitional period from the date of implementation to meet the requirements of the new Rules. Currently, Bahrain Bourse is working on finalizing its draft Listing Rules as well as the Clearing, Settlement and Central Depository (CSD) Rules.

c) Based on the agreement with the CBB, the Bahrain Financial Exchange (BFX) is working on the implementation of an agreed upon action plan to recommence its market operations during the year 2016, vide CBB’s letter Ref. No. EDFIS/248/2015 dated 28th December 2015.

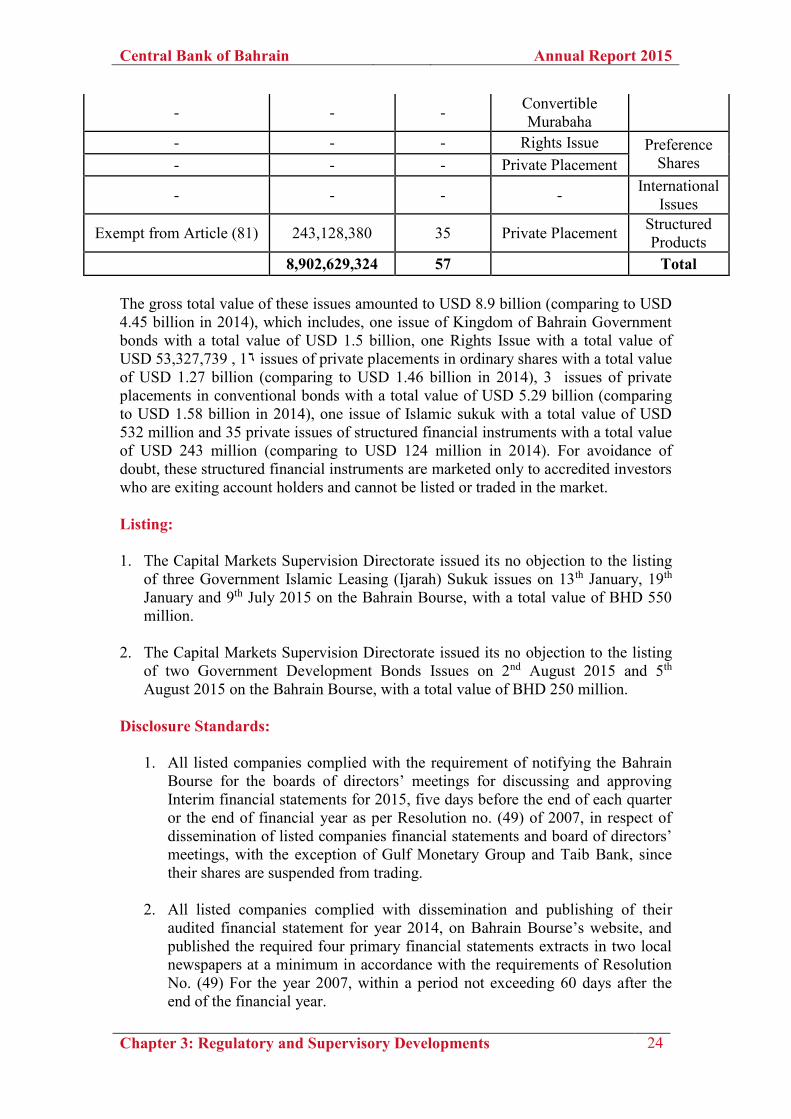

Primary Market: In 2015, the CMS Directorate issued its no objection to the use of 57 public and private offering documents (comparing to 44 offering documents in 2014) after ensuring the completeness of all the information and details as per the CBB Law, Offering of Securities Module of CBB Rulebook Volume 6, as follows:

Type of CBB Approval $Issues Value No. of Issues Offering Method Type of

Security - - - Public Offering

Ordinary Shares Registration – Article (81) 53,327,740 1 Rights Issue

Registration – Article (81) 1,274,100,905 16 Private Placement - - - Public Offering

Conventional Bond

Filing - Exempt from Article (81) 5,299,243,380 3 Private Placement

Registration – Article (81) 1,500,000,000 1 Governmental - - - Governmental Islamic

Sukuk Filing - Exempt from Article (81) 532,828,920 1 Private Placement

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 24

- - - Convertible Murabaha

- - - Rights Issue Preference Shares - - - Private Placement

- - - - International Issues

Exempt from Article (81) 243,128,380 35 Private Placement Structured Products

8,902,629,324 57 Total The gross total value of these issues amounted to USD 8.9 billion (comparing to USD 4.45 billion in 2014), which includes, one issue of Kingdom of Bahrain Government bonds with a total value of USD 1.5 billion, one Rights Issue with a total value of USD 53,327,739 , 16 issues of private placements in ordinary shares with a total value of USD 1.27 billion (comparing to USD 1.46 billion in 2014), 3 issues of private placements in conventional bonds with a total value of USD 5.29 billion (comparing to USD 1.58 billion in 2014), one issue of Islamic sukuk with a total value of USD 532 million and 35 private issues of structured financial instruments with a total value of USD 243 million (comparing to USD 124 million in 2014). For avoidance of doubt, these structured financial instruments are marketed only to accredited investors who are exiting account holders and cannot be listed or traded in the market. Listing:

1. The Capital Markets Supervision Directorate issued its no objection to the listing

of three Government Islamic Leasing (Ijarah) Sukuk issues on 13th January, 19th January and 9th July 2015 on the Bahrain Bourse, with a total value of BHD 550 million.

2. The Capital Markets Supervision Directorate issued its no objection to the listing

of two Government Development Bonds Issues on 2nd August 2015 and 5th August 2015 on the Bahrain Bourse, with a total value of BHD 250 million.

Disclosure Standards:

1. All listed companies complied with the requirement of notifying the Bahrain Bourse for the boards of directors’ meetings for discussing and approving Interim financial statements for 2015, five days before the end of each quarter or the end of financial year as per Resolution no. (49) of 2007, in respect of dissemination of listed companies financial statements and board of directors’ meetings, with the exception of Gulf Monetary Group and Taib Bank, since their shares are suspended from trading.

2. All listed companies complied with dissemination and publishing of their

audited financial statement for year 2014, on Bahrain Bourse’s website, and published the required four primary financial statements extracts in two local newspapers at a minimum in accordance with the requirements of Resolution No. (49) For the year 2007, within a period not exceeding 60 days after the end of the financial year.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 25

All listed companies complied to convene the Annual General Meetings within 90 days of the end of 2014 , with the exception of a Gulf Monetary Group and Taib Bank.

3. All listed companies complied with publishing their 2014 quarterly financial

results within the prescribed deadline of (45) days following the end of the first, second and third quarter of the same year, on Bahrain Bourse’s website and in two local newspapers and included the required four primary financial statements extracts at a minimum, in accordance with resolution no. (49) for the year 2007, with the exception of Gulf Monetary Group and Taib Bank.

Compliance and Enforcement:

1. Liquidation of Brokerage Firm: As a result of TAIB Securities being unable to continue to provide brokerage services, the CBB worked on the protection of the rights and assets of the customers through the transfer of these assets and money to a licensed brokerage firm licensed by the CBB, Mubasher. These measures have been fully disclosed through the announcement in the market and through direct contact with the customers concerned and through the publication in the local newspapers.

Consequently, the appointment of a legal consultancy offices and attorneys has been announced, as liquidators of the company TAIB Securities, in accordance with the decision of the Company’s Extraordinary General Meeting dated 27th May 2014. Currently the necessary procedures are being taken to complete the final liquidation.

2. Cancelation of license of Brokerage firm dealing in securities and

financial instruments As a result of ceasing to providing brokerage services on the BFX market, and ceasing to provide settlement and clearance services in the clearing house BCDC, and at the request of the company, the CBB has issued Resolution No. 16 dated 4th June 2014, on the cancelation of the license granted to the company Grrans Commodities BSC (c), which has been published in local newspapers.

3. Circular regarding the necessity to fulfill all the required data about

customers

The CMSD issued a circular to all listed companies, clearing house, central depository, brokerage firms and other capital market service providers, under letter Ref, CMS/292/15 dated 12th November 2015, obligates all parties to fulfil all data and information related to the investor and customer dealing in the market, and specifically while opening securities accounts and deposit, as it contained in the account application form.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 26

4. Referral to the Disciplinary Board In accordance to the Capital Market Supervision Directorate’s issued letter Ref. CMS/293/15, the BHB was mandated to convene a meeting of its Disciplinary Board to decide on the conduct of violating and/or non-compliance with the CBB’s requirements by one of the listed companies. 5. Cancellation of Suspicious Transactions As a result of violation of the CBB’s disclosure standards, the Capital Market Supervision Directorate issued a letter Ref. CMS/269/15 to BHB, instructing the cancellation of transactions executed on Batelco’s shares. 6. Notification of Non-compliance to Submission of the Monthly Statement

of the Register of Interest In accordance with the requirement to disclose of ownership interests by shareholders owning 5% or more in shares of listed companies within 5 business days from the end of the month, the following companies have been notified for failing to deliver the report during the required timeframe: United Gulf Investment Corporation, TAIB Bank, Al Ahlia Insurance Company, Banader Hotel Company, Ithmaar Bank, Takaful International Company, United Gulf Bank, Al Salam Bank and GFH Financial Group. 7. Notification of Non-Compliance to Disclosure Standards In accordance with the requirement to publicize financial statements for the period in question (quarterly review/ annually audited) with the comparative period for each period separately through the dissemination in press releases for companies, the Directorate issued non-compliance letters to the following companies: Bahrain Cinema Company, Bahrain Flour Mills, Khaleeji Commercial Bank, Bahrain Islamic Bank, Arab Insurance Group and Gulf Hotel Group B.S.C. 8. Notification of Non-Compliance to Submission of Annual Verification of

the Insiders’ and the Key Persons’ Data Register In accordance with Article (2.15.6) of the Prohibition of Market Abuse and Manipulation (MAM) Module of Volume 6, on the provision of the annual verification of the insiders’ and the key persons’ data register, which is to be reviewed by the company’s Internal Auditor, to be submitted no later than 10 days after the company’s Annual General Meeting date, the Directorate issued non-compliance letters to Al Salam Bank, United Gulf Investment Corporation, Banader Hotels Company, GFH Financial Group and Inovest. 9. Notification of Non-Compliance with Requirements Regarding the

Announcement of Dividend Declaration

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 27

In accordance with the CBB’s Disclosure Standards requirements, particularly Article (32.5) of the same, pertaining to requirements pertaining to dividend declaration announcements, the Directorate issued a Notice letter to Zain Bahrain and Arab Insurance Group emphasizing the necessity of this publication. 10. Temporary Suspension of Trading

a. The Directorate issued a resolution to suspend trading on the shares of Ithmaar

Bank on March 1st, 2015, as a result of the Bank's non-adherence to the publication of its annual audited financial statements for the year 2014 within 60 days from the end of the year, in accordance with Resolution No. (49) of the year 2007. Trading on the Bank’s shares was resumed on March 8th, 2015, after the Bank’s publication of its annual audited financial statements.

b. Trading on GFH Financial Group shares was suspended on April 19th, 2015, as a result of its capital reduction plan. Trading was resumed on April 21st, 2015.

c. The Directorate issued a resolution to suspend trading on Bahrain Islamic Bank on October 20th, 2015, as a result of the Bank’s request based on its capital reduction plan. Trading was suspended on October 27th, 2015 and resumed on November 1st, 2015.

d. Trading of GFH Financial Group shares was suspended on 8th November 2015 as a result of non-disclosure of the developments relating to their ongoing litigations in Bahrain’s courts as announced on BHB’s website. Trading resumed on 9th November 2015.

11. Delisting The Capital Markets Supervision Directorate issued its no objection to the delisting on Bahrain Bourse, as follows:

The Capital Markets Supervision Directorate issued its no objection to the delisting on Bahrain Bourse, as follows:

1. On 14th May 2015, the Ijara Government Sukuk Issue (20th Issue) was delisted

due to the maturity of the sukuk. 2. On 1st November 2015, the Government Development Bonds (GDEV.BND)

was delisted due to the maturity of the Bonds. 3. On 22nd November 2015, Al Ahli United Bank B.S.C Preference Class (A)

Shares was delisted based on the bank’s early redemption resolution.

4. On 24th November 2015, SICO Arab Financial Fund (SICO.AFF) was delisted due to liquidation of the fund.

5. On 30th November 2015, SICO Money Market Fund (SICO.MM.F) was delisted due to liquidation of the fund.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 28

Joint Work of the Gulf Cooperation Council (GCC)

1. The CBB’s Capital Markets Supervision Directorate participated during 2015 in the meetings of the Gulf Cooperation Council (GCC) Taskforces to complete the drafting and approving of uniform rules for the Capital markets in the GCC, in particular, in the 19th meeting for the Issuance and Public Offering Taskforce, the 11th meeting for the Market Surveillance and Supervision over the exchanges in the GCC, and in the 3rd meeting for the Working Group Responsible for Training Organization approaching the financial markets in the GCC countries.

2. Signed the memorandum of understanding between the (GCC) Financial Markets

Authorities, on the sidelines of the 6th meeting of the Ministerial Committee of the Heads of Councils Regulators of Financial Markets in the GCC countries on September 15, 2015.

3. Participated in the 12th and 13th meeting of the Heads of Securities Commissions

on 4th May 2015 and 14th September 2015, respectively.

4. A delegation from the CBB headed by His Excellency, the Governor, participated in the 6th meeting of the Ministerial Committee of the Heads of Councils Regulators of Financial Markets in the GCC countries, which was held on 15th September 2015 and the outcome of the meeting was as follows:

x Approval of "the uniform rules for acquisitions in the financial markets in the

GCC countries," and endorsing these rules to the Ministerial Council for adoption by the Supreme Council as an advisory paper until the completion of the preparation of the full uniform rules and principles for the integration of capital markets and make sure that they are consistent and compatible with each other.

x The final approval of the amendments to the uniform rules for the issuance and offering of shares in the financial markets in the GCC countries, after adding the articles pertaining to the private placement in the GCC financial markets, and adopting it as an advisory paper.

x The formation of a joint technical group between the supervision and oversight of the banking system committee related to the Committee of Governors of Monetary Agencies and Central Banks in the GCC countries and the Market Surveillance and Supervision over the exchanges Taskforce related to the Committee of the Heads of Securities Commissions in the GCC countries, to study the topics proposed to be discussed between the two Ministerial committees and to propose a date to meet and prepare for it.

x The final approval of the amendments to the uniform rules for the issuance and offering of investment funds in the GCC financial markets, and adopting it as an advisory paper.

x The final approval of the amendments to the uniform rules for the issuance and offering of bonds/Sukuk in the GCC financial markets, and adopting it as an advisory paper.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 29

x The final approval of the proposed amendments to the uniform rules for the

supervision and oversight of trading in the GCC financial markets, and adopting it as an advisory paper.

The Supreme Council decided at its (36th) annual meeting, which was held on December 9 to 10, 2015: "the adoption of uniform rules for acquisitions in the financial markets in the GCC countries, as an advisory paper until the completion of the preparation of the full uniform rules and principles for the integration of capital markets, and make sure that they are consistent and compatible with each other.”

Financial Institutions Supervision Directorate (“FISD”) Overall responsibilities of FISD as part of CBB The Financial Institutions Supervision Directorate (FISD) supervises financial institutions, other than banks, namely, Investment Business Firms Categories 1, 2 and 3, Money Changers, Trust Service Providers, Ancillary Service Providers, Representative Offices of Investment Firms and Fund Administrators/Registrars. In carrying out its responsibilities, the FISD ensures that all of the licensees under its supervision adhere to CBB Law and their respective regulations through CBB Rulebook Volumes 4 and 5. Additionally, the FISD is responsible for the authorization and registration of Bahrain domiciled and overseas funds, as appropriate, and the supervision of Bahrain domiciled funds through the implementation of the rules within CBB Rulebook Volume 7. Routine Responsibilities During 2015 During the course of 2015, FISD continued to fulfil its responsibilities by implementing rules and regulations and using various supervisory tools, including in-depth financial analysis, prudential meetings with management of licensees, formal requests for information from the sector, liaising internally with other Directorates at the CBB, in addition to the ongoing monitoring of licensees through regular communication and exchange of correspondence. As part of its supervisory role in monitoring the Collective Investment Undertakings (CIUs’) sector, FISD also continued to use its supervisory tools to monitor the industry and ensure adherence to the rules and regulations stipulated in CBB Rulebook Volume 7 (CIUs) and other relevant regulatory requirements. Developments achieved/or and new regulations/circulars issued during 2015. Being vigilant of the continuous developments in the local, regional and international financial centers, the CBB continuously enhances its existing regulations to ensure

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 30

parity with best market practice, and identifies gaps based on industry demand and international developments. As a result of such strategy, the FISD identifies certain areas for development and sets at the beginning of each year objectives which are then executed. Several consultations were issued to FISD licensees during the course of 2015, in order to get their views on proposed regulations and incorporate them within the existing regulatory framework. Such consultations included the following:

x On 20th August 2015, a consultation was issued to all investment firm licensees, regarding the proposed Memorandum of Understanding between the CBB and the Alternative Investment Funds Managers (AIFMD), in order to become a member of the European Securities and Markets Authority (ESMA). The purpose of the consultation was to receive the licensees’ comments on the proposal.

x Another consultation was issued on 16th November 2015, to all Money Changer Licensees, regarding the proposed amendments to the Money Changers High Level Controls Module. The proposed amendments aim at aligning the Module with the corporate governance code issued by the Ministry of Industry and Commerce and the other CBB requirements, while taking into consideration the unique features related to the money changer activities.

During 2015, FISD continued, in accordance with its objectives, to develop the rules and regulations pertaining to its licensees, either by way of updating or introducing new rules. A number of initiatives commenced and updates to Regulations were issued throughout the course of the year, as follows:

x A Royal Decree No. (34) of the year 2015 amending some of the provision of the Central Bank and Financial Institutions Law No. (64) of the year 2006 was issued.

x In order for licensees to ensure full compliance with the amendments, a circular dated 29th December 2015, notifying licensees of the amendments was sent to all Investment Firm Licensees, Money Changers, Trust Service Providers, Administrator / Registrars, Ancillary Service Providers and Representative Offices.

Insurance Sector Supervision The Insurance Supervision Directorate released the Insurance Market Review Report of 2014. The Report presents the financial performance of the insurance industry in Bahrain for the years 2013 and 2014 (both ‚conventional insurance & reinsurance and Takaful & Retakaful business) by class of business in the Kingdom, highlighting the origin and the historical background of the insurance market in Bahrain. The total

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 31

gross premiums of the Bahrain insurance market increased to BD 271 million in 2014. Insurance penetration (ratio of gross premiums to GDP) stood at 2.13% in 2014. Furthermore, the Insurance Supervision Directorate at the CBB has applied a range of measures to enhance/endorse the stability of the Insurance sector: x The CBB receives and reviews various prudential reports as per the requirement

of the CBB Rulebook (Volume 3) in order to efficiently supervise and assess the Licensees compliance with the CBB and Financial Institutions Law No. (64) of 2006 and the CBB Rulebook (Volume 3).

x The CBB requested Insurance Firms’ management to submit their year-end financial statements and attend a meeting at the CBB with their external auditors prior to the submission of the financial statements for approval to the Board of Directors.

x The CBB continued to receive monthly investment reports and assess the performance of the investment portfolio.

x Ad-hoc reporting is implemented when needed in order to implement risk based supervision on Licensee(s) and/or to handle specific market concern.

x The CBB has implemented the new Takaful model after consulting with the

Takaful industry and other interested parties. The new model reaffirms the Kingdom of Bahrain as the jurisdiction of choice for the Takaful and Retakaful industry.

x The new model enhances measuring and assessing the solvency status of Takaful and Retakaful Firms. It is expected that the new module will increase the ability of Takaful and Retakaful firms to distribute surpluses to participants and dividends to shareholders. As part of the consultation process, the CBB has been proactive in liaising with not just the Takaful industry for their views and comments on the proposed rules, but also with the Shariah Supervisory Boards of a number of Takaful companies to ensure conformity of the revised rules and guidance with Shariah requirements.

x In October 2014, Motor Insurance Compensation Fund Law No. 61 of 2014 was

issued after approval by Shura Council and Council of Representatives. The Fund was an initiative of the CBB which is designed to compensate the injured parties in the following circumstances:

o Absence of a valid insurance policy for the vehicle that caused the accident (Uninsured vehicle);

o The vehicle that caused the accident or the owner and/or the driver of the vehicle were not identified (Hit & Run);

o In the event of the insurer being insolvent; and o In case of no other party to compensate as per relevant laws and

regulations.

x The CBB has worked closely with the Bahrain Insurance Association (BIA) in this respect.

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 32

x During 2015, the Board of Directors of the Motor Compensation Fund have met

several times to discuss various issues related to the Fund. Furthermore, the Fund received the contribution of 1% of the Gross Motor Insurance Premiums from the Insurance Firms for the years 2014 and 2015.

x The CBB in cooperation with the Bahrain Insurance Association have finalized the Standard Policy Document of Compulsory Insurance for Motors (Third Party Insurance) and the procedures for dealing with motor claims. Such documents will be issued in a form of a resolution in the Official Gazette, in order to ensure that high quality insurance services and fair treatments are offered to the policyholders and claimants.

x The CBB has continued to register appointed representatives during 2015. The

total number of the registered appointed representatives as of the end of 2015 were as follows:

No. of Companies No. of Registered Licensed Banks 10 172 Commercial Companies 5 24 Individuals - 53 Total 15 249

Financial Stability Directorate During 2015, the Financial Stability Directorate (“FSD”) continued conducting research and analysis on issues relating to financial stability. The FSD also continued to perform the following core functions:

x Issuing various publications such as the Financial Stability Report (semi-annual), Financial Soundness Indicators Report (semi-annual), the Economic Report (annual), Sensitivity Testing Report, along with other periodical publications that monitor domestic and international macro-financial developments.

x Undertaking general research on issues relating to financial stability in

Bahrain and conducting a number of presentations on financial stability developments.

x Collecting, compiling and disseminating statistical information and releasing financial data that is published through its Monthly Statistical Bulletin and quarterly Economic Indicators.

x Conducting annual surveys such as the Manpower Survey, Coordinated Portfolio Investment (“CPIS”) Survey, Locational International Banking surveys (quarterly).

Central Bank of Bahrain Annual Report 2015

Chapter 3: Regulatory and Supervisory Developments 33

x Maintaining CBB’s relations with major international institutions and agencies

(IMF, World Bank, and rating agencies) and acting as a point of contact for other third parties, both domestic and overseas.

In 2015, the FSD focused on enhancing its publications and statistical data. For the Financial Stability and Financial Soundness Indicators Reports, there was focus on making them more effective analytical reports, ensuring their clarity and consistency, enhancing the overall assessments, and making sure they are up to date with covering current issues to financial stability. The FSD also enhanced some of its statistical returns to capture data on SME’s, investment business firms, Islamic windows and financial institutions. The CBB also conducted its sensitivity stress testing exercises in 2015 based on the locally incorporated and Systemically Important Banks (D-SIBs). In order to further develop its stress testing strategy, the FSD started the process of developing other model based stress tests to assess other risks and the involvement of banks in further exercises. The FSD was also involved in conducting the CBB’s ‘Women in the Financial Sector Survey’ in 2015 as part of the initiative of the Supreme Council for Women to celebrate women in Bahrain’s financial sector for this year. The FSD continues to be involved in the Electronic Submission of Returns and Data (ESRAD) system and is working with other CBB directorates and licensee as since the launch of the system. FSD was able to publish a number of returns in 2015 and started receiving submissions from various licenses. The FSD continues to continue to provide licensees with information and training with regards to the use of the system and submission of period data.

Central Bank of Bahrain Annual Report 2015

Chapter 4: CBB Projects and Activities 34

4. Other CBB Projects and Activities New Licenses

Payment System (“SSS” & “RTGS”)

Cheque Clearing

ATM Network (“BENEFIT”)

Currency Issue

CBB Training Programs

IT Projects

External Communications Unit

CBB’s Organisational Chart

Chapter

4

Central Bank of Bahrain Annual Report 2015

Chapter 4: CBB Projects and Activities 35

4.1 New Licenses The Central Bank of Bahrain (“CBB”) has issued 11 new licenses in 2015 compared to 9 new licenses issued in 2014, reaching to a total of 403 licensees to provide financial services as of 31st December 2015 compared to a total of 404 licensees as of 31st December 2014. Those new licenses were issued for different financial sectors, as shown in the list below:

1- JS Bank Limited - Conventional Wholesale Bank, Branch

2- Turkiye Finans Katilim Banakasi A.S. - Wholesale Bank (Islamic Principles),

Branch

3- BOK – International - Wholesale Bank (Islamic Principles), Branch

4- Orient Insurance P.J.S.C. – Overseas Insurance Firms

5- Braxtone Insurance Management W.L.L. – Insurance Manager

6- Trust Insurance Management W.L.L. – Insurance Manager

7- Mr. Jabran Noor - Registered Actuary

8- Mr. Luis Portugal - Registered Actuary

9- Mr. Olivier Quesnel - Registered Actuary

10- Mr. Hatim Nuruddin Maskawala - Registered Actuary

11- Mr. Sumedh Sadashiv Aher – Registered Loss Adjuster

The main growth of new licenses issued in 2015 was in the insurance sector as shown in the graph below:

New Licensees Growth by Sector

0

1

2

3

4

5

6

7

8

9

Banks Insurance InvestmentBusiness

SpecilisedLicenses

CapitalMarkets

New

Lic

ense

s

Year 2015

Year 2014

Central Bank of Bahrain Annual Report 2015

Chapter 4: CBB Projects and Activities 36

4.2 Payment System (“SSS” & “RTGS”) Bank transfers through the Real Time Gross Settlement System (“RTGS”) were 693,370 in 2015, for a total amount of BD 59.7 billion with a daily average of 2,796 and BD 240.9 million, broken down as follows:

x The volume of bank transfers among retail banks through RTGS was 103,386 for a value of BD 49.4 billion.

x The volume of customer transfers through the RTGS totalled 589,984 with a

value of BD 9.8 billion during 2015.