ANNUAL REPORT 2015 - cellohealthplc.com · 5 Cello Annual Report 2015 CHAIRMAN S STATEMENT OVERVIEW...

52

ANNUAL REPORT 2015

Transcript of ANNUAL REPORT 2015 - cellohealthplc.com · 5 Cello Annual Report 2015 CHAIRMAN S STATEMENT OVERVIEW...

ANNUAL REPORT2015

Highlights 2

Chairman’s Statement 4

Cello Health 10

Cello Signal 20

Cello People 28

Strategic Report 32

Directors’ Report 33

Corporate Governance 36

Report of the Remuneration Committee 38

Consolidated Financial Statements Independent Auditors’ Report 40 Financial Statements 42 Accounting Policies 47 Notes 52

Company Financial Statements Independent Auditors’ Report 76 Financial Statements 78 Accounting Policies 80 Notes 83

Notice of Annual General Meeting 88

Directors 92

Group Directory 94

Advisors 96

Contents

2015 Highlights

£86,681,000

£10,026,000

9292.86p

8.61p

Gross profit

Headline profit before tax

Full year dividend paid (per share) Headcount

Headline basic earnings (per share)

41.6%

Overseas turnover as a % of total

4

Cel

lo A

nnua

l Rep

ort 2

015

CH

AIR

MA

N’S

ST

AT

EM

EN

T

Building a global organisation delivering world-class client solutions

5

Cello A

nnual Report 2015

CH

AIR

MA

N’S ST

AT

EM

EN

T

OVERVIEW

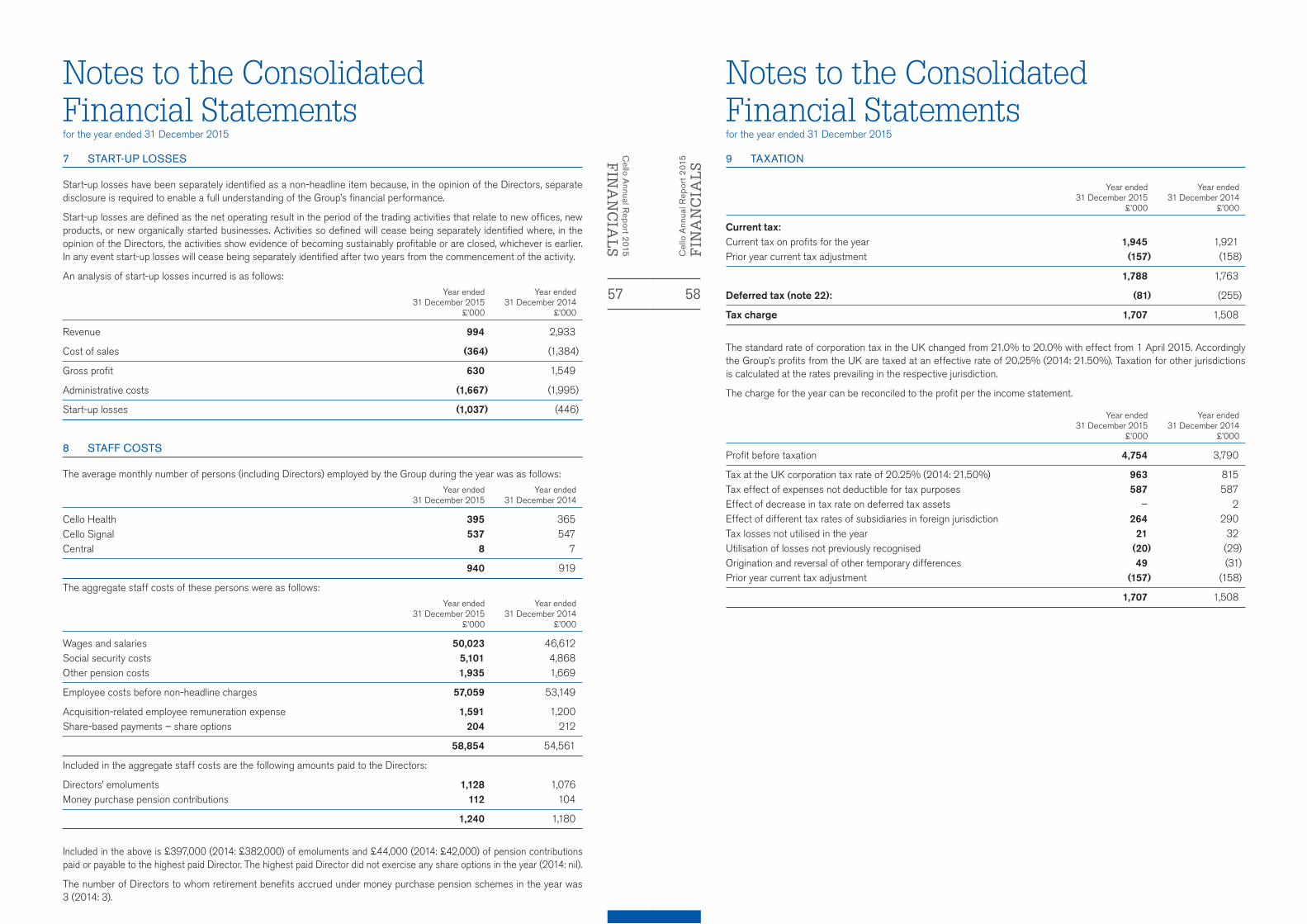

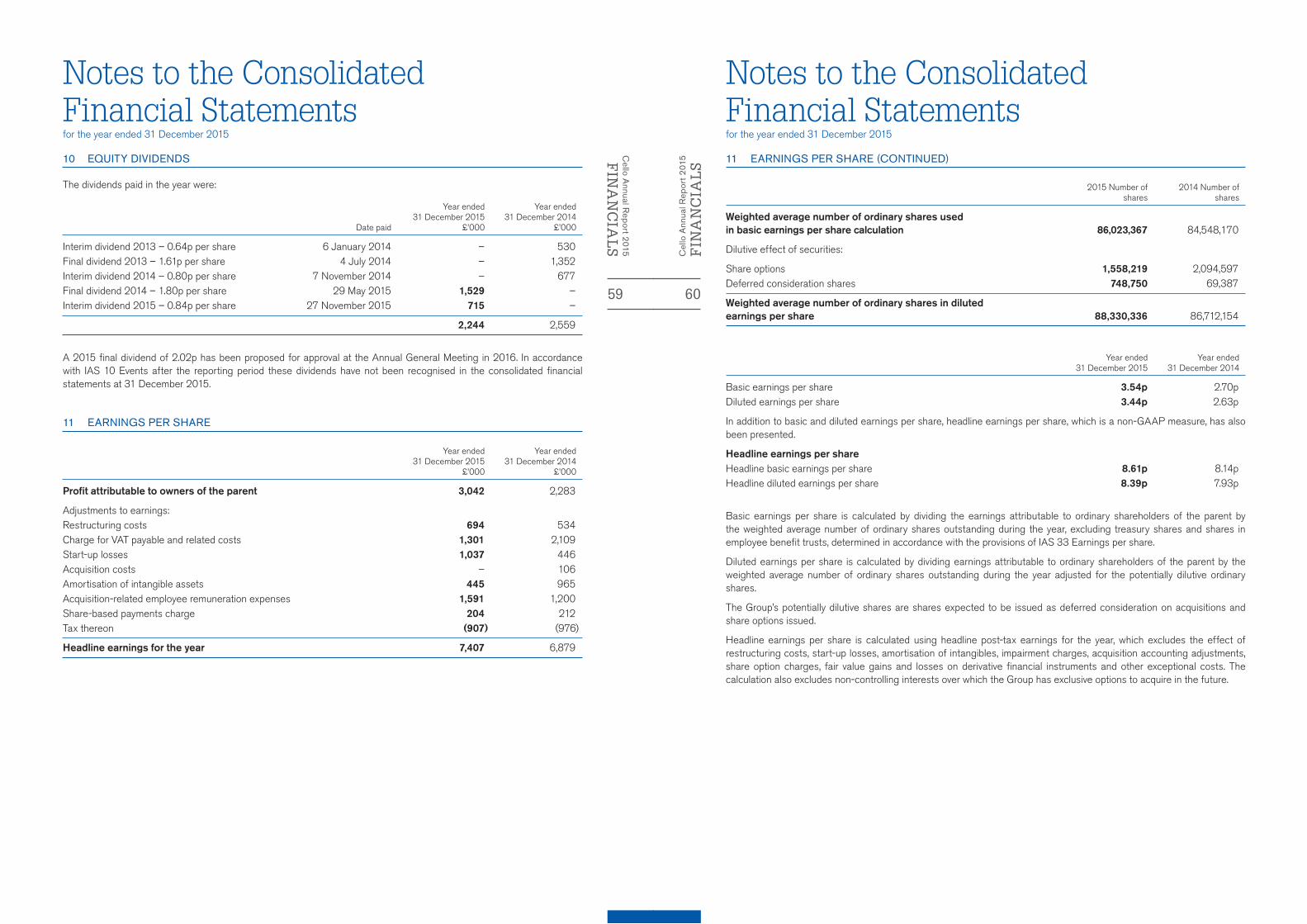

2015 saw a continued strong financial and operational performance. The Group reported a 7.0% increase in gross profit to £86.7m (2014: £81.0m) with headline1 profit before tax up 7.1% to £10.0m (2014: £9.4m).

Both Cello Health and Cello Signal have continued to make great strides towards establishing themselves as leaders in their respective fields. Cello Health completed its integration behind a single brand almost two years ago and the benefits of this have visibly fed into growth prospects for the company. Whilst Cello Health continued to trade well in the UK and in the USA in 2015, the key features of the year were the development of new sources of future global growth based on the Cello Health brand. 2015 saw significant growth from the emerging client base on the West Coast of the USA. It also saw a marked increase in collaboration between the different capabilities of Cello Health to secure new client briefs. In order to secure future growth, the Group continued its significant investment in the development of its biotech offer in Boston, USA.

Cello Signal made significant progress in integrating its offer behind the client-facing Signal brand. By the end of the year a number of larger clients had been won on the basis of the integrated Signal proposition. The fruits of this process also began to show through in revenue growth and margin improvement.

The Group ended the year with a strong balance sheet, with net debt2 at £4.2m. As a result, the Board has raised the full year dividend by 10.0%, reflecting confidence in the Group’s cash flow potential.

Regarding the VAT issue relating to charitable clients of Signal, following the £1.1m provision taken at the half year stage, the Board continues to believe that the total provision of £3.2m is appropriate.

The New Year has started well, with good income visibility and a solid order book from 2015.

The Group reports a7.0% increase in gross

profit to £86.7m

1 Headline measures exclude, where applicable, restructuring costs, amortisation of intangibles, impairment charges, acquisition accounting adjustments, start-up losses and the charge for VAT payable and related costs.

2 Net debt is defined in note 26.

6

Cel

lo A

nnua

l Rep

ort 2

015

CH

AIR

MA

N’S

ST

AT

EM

EN

T

3 Like-for-like measures exclude the results from companies acquired in the year and start-ups, which are defined in note 7.4 Operating margin is calculated by expressing operating profit as a percentage of gross profit.5 Headline earnings per share is defined in note 11.

FINANCIAL REVIEW

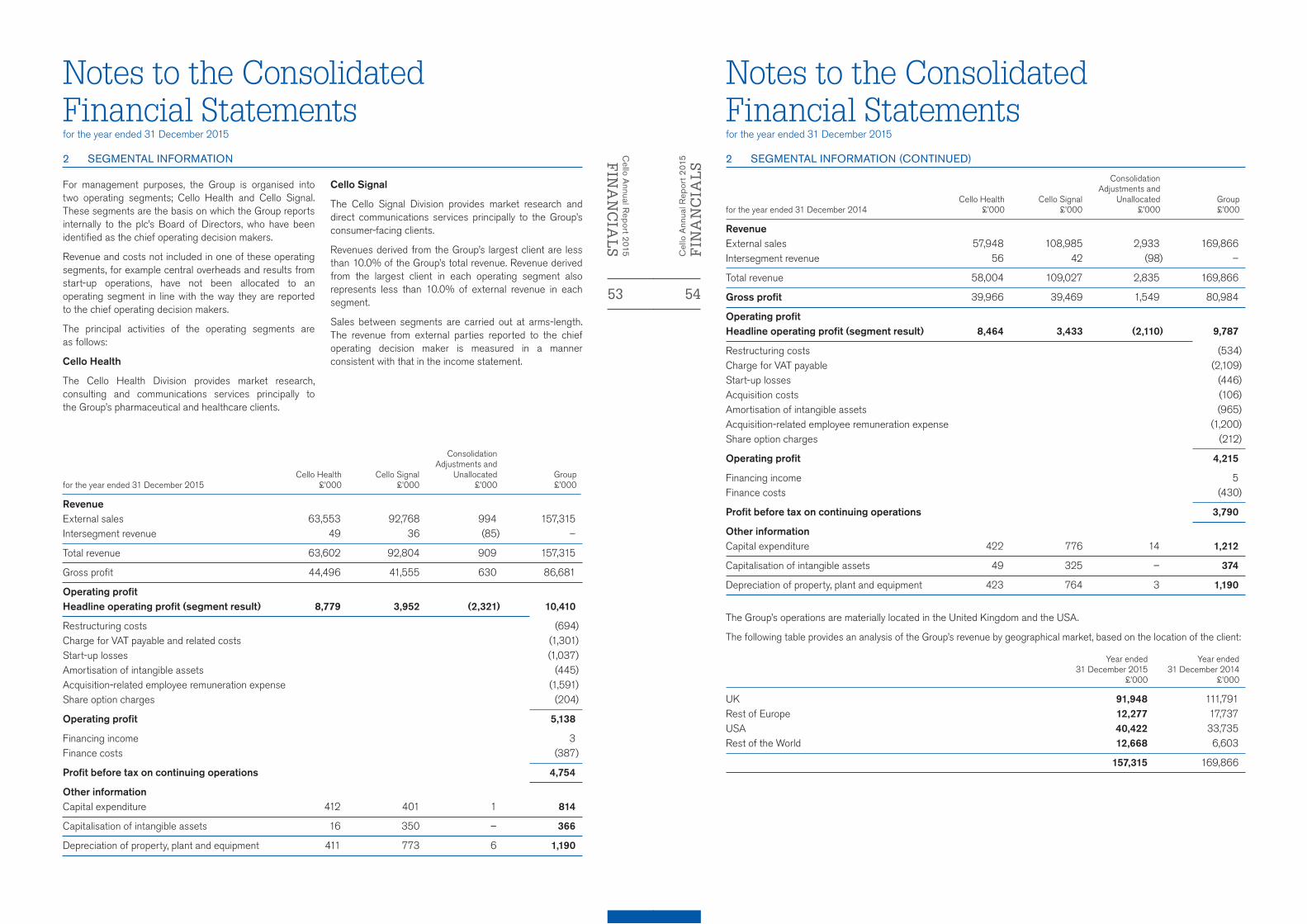

Total Group gross profit was £86.7m (2014: £81.0m) on revenues of £157.3m (2014: £169.9m). Headline profit before tax was £10.0m (2014: £9.4m). The Group’s results reflect a strong performance by Cello Health and an improved performance by Cello Signal, especially in the second half of the year. Like-for-like3 gross profit growth for the whole Group was 4.2%.

The Group’s headline operating margin4 was 12.1% (2014: 12.3%) with a headline operating margin of 19.7% in Cello Health (2014: 21.2%), and 9.5% in Cello Signal (2014: 8.7%).

Headline finance costs were £0.4m (2014: £0.4m).

The Group’s tax charge was £1.7m (2014: £1.5m) with a headline tax rate of 26.1% (2014: 26.5%). The

headline tax rate is dropping as the UK Corporation Tax rate drops.

Headline basic earnings per share5 was up 5.8% to 8.61p (2014: 8.14p).

Statutory profit before tax was £4.8m (2014: £3.8m) after the impact of acquisition-related costs of £1.6m (2014: £1.3m); restructuring costs of £0.7m (2014: £0.5m); amortisation of £0.4m (2014: £1.0m); start-up losses of £1.0m (2014: £0.4m); and the £1.3m charge for VAT payable and related costs.

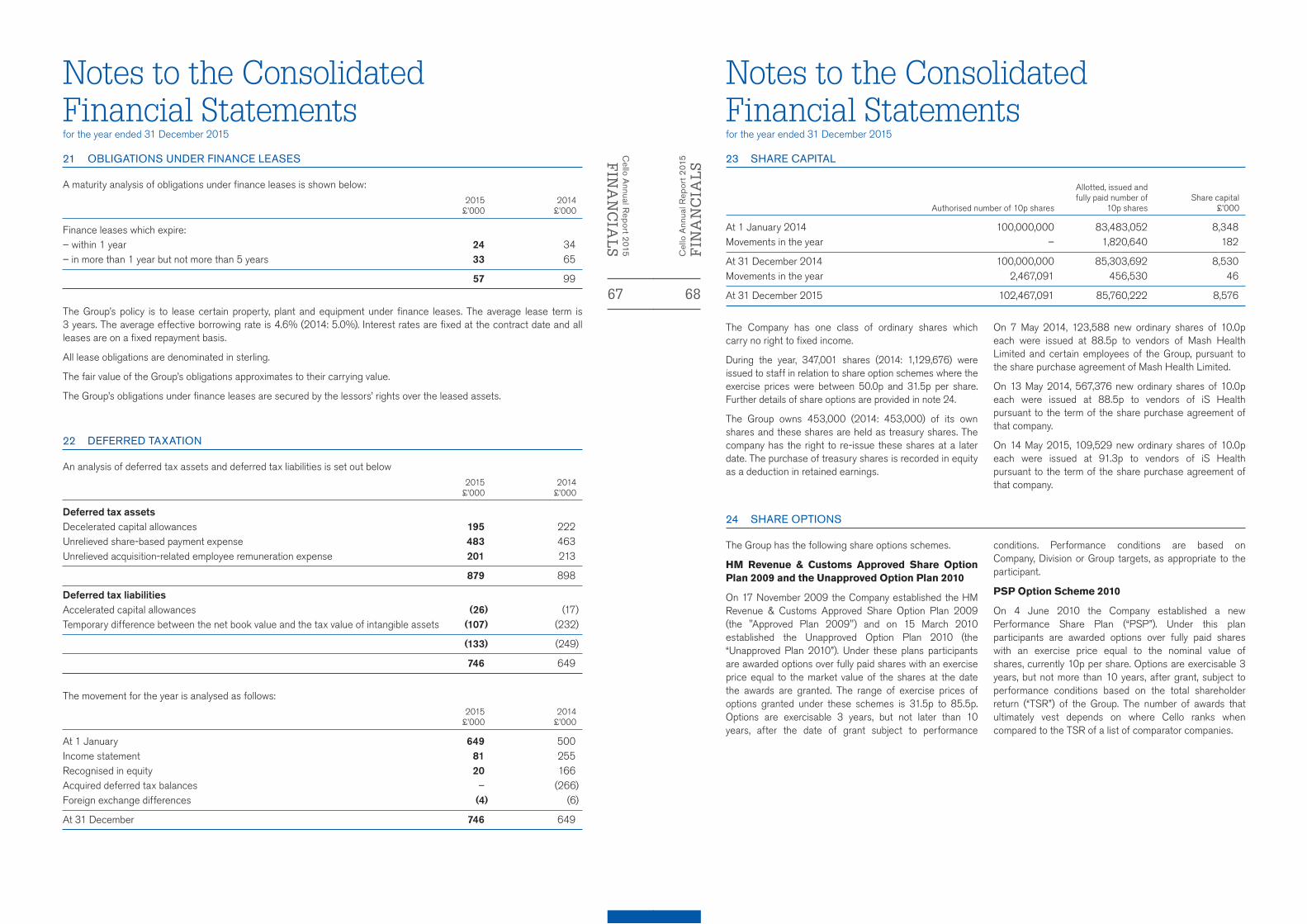

Total Group estimated future acquisition-related obligations are £3.3m, payable from 2016 to 2017, with a maximum of £0.9m payable in new ordinary shares.

Cello Health produced headline operating profit growth of 3.7% on an increase in gross profit of 11.3%, reflecting continued robust demand

from global clients for its highly specialist range of clinically led services. Like-for-like gross profit in Cello Health grew by 4.7%. Operating margins fell slightly to 19.7% (2014: 21.2%). This reflects the tougher trading environment within the consumer offering of Cello Health, where some projects were deferred or cancelled during the year.

Cello Signal continued to make solid progress in 2015. Headline operating profit grew by 15.1% to £4.0m (2014: £3.4m) on gross profits of £41.6m (2014: £39.5m). Like-for-like gross profit growth was 3.7%. Operating margins therefore improved from 8.7% to 9.5%. There was particular strength in the financial services and charity client base. Operating margins were reduced by continued investment in expansion of the business in the USA and in Pulsar.

Robustlike-for-like growth

7

Cello A

nnual Report 2015

CH

AIR

MA

N’S ST

AT

EM

EN

T

These areas are currently delivering lower operating margins as they continue to be expanded.

Pulsar continued to grow impressively, with 191 clients at the end of 2015 (2014: 88). The product continues to evolve. During 2015, Facebook data was incorporated for the first time, vastly increasing the size of the dataset that is analysed. Operating losses of £0.2m for 2015 are absorbed within headline operating profit. Pulsar achieved

break-even on a monthly basis from November 2015. Sales and renewal rates have been strong so far in 2016.

The Group benefitted from a stronger dollar in 2015 compared with 2014, with average US$:£ exchange rates strengthening from 1.65 in 2014 to 1.53 in 2015. The Group currently generates around $3.5m of headline operating profit in the USA. So far in 2016 the dollar has continued to strengthen to around 1.40.

The Board is proposing a final dividend of 2.02p per share (2014: 1.80p), giving a total dividend for the year of 2.86p per share (2014: 2.60p) representing an increase of 10.0%. The dividend has grown every year since 2006 and has grown by 10.0% or more for the past six years. Subject to shareholder approval, the final dividend will be paid on 27 May 2016 to all shareholders on the register at 6 May 2016, and will be recognised in the year ending 31 December 2016.

*No cash flow impact.6 ebitda is defined as headline operating profit before depreciation and amortisation.

The Group incurs a number of charges in the income statement below headline operating profit, which are:

2015 £’000

2014 £’000

Headline operating profit 10,410 9,787

Net interest payable (384) (425)

Headline profit before tax 10,026 9,362

Restructuring costs (694) (534)Charge for VAT payable and related costs (1,301) (2,109)Start-up losses (1,037) (446)Acquisition costs – (106)Amortisation of intangibles* (445) (965)Acquisition related employee remuneration expense (1,591) (1,200)Share option charges* (204) (212)

Statutory profit before tax 4,754 3,790

During 2015, the Group incurred exceptional costs of £0.7m (2014: £0.5m). This related to redundancy payments, predominately within Cello Signal as structural changes were implemented to integrate the offer further and reduce operating costs.

Operating cash flow before tax of £8.2m (2014: £4.8m) during the year represented a 79.2% (2014: 48.7%) conversion of headline operating profit. The Group’s net debt position at 31 December 2015 was £4.2m (2014: £7.2m). The net debt:ebitda6

ratio at 31 December 2015 was 0.35 (2014: 0.64). Group debt facilities are renewable in March 2018. Total debt facilities are £20.0m with a £4.0m overdraft facility.

The VAT issue within a subsidiary of Cello Signal is the subject of ongoing discussions with HMRC. The Board continues to believe the provision made of £3.2m is appropriate. Further updates will be given when there are material developments.

The Group continued to invest in

organic start-up activity. The primary focus was investment in the Boston office of Cello Health that specialises in biotech. While this business has required heavier investment than was originally planned, the Group remains confident about the prospects for the business and the overall opportunity it represents for future growth. In addition, an office in Asia, which was a start-up, was closed during the year. Total start-up costs were £1.0m (2014: £0.4m).

8

Cel

lo A

nnua

l Rep

ort 2

015

CH

AIR

MA

N’S

ST

AT

EM

EN

T

OPERATIONAL REVIEW

Cello Health (www.cellohealth.com)

2015 2014 £’000 £’000

Gross profit 44,496 39,966

Headline operating profit 8,779 8,464

Headline operating margin 19.7% 21.2%

Cello Health had another strong year, delivering headline operating profit of £8.8m (2014: £8.5m) from gross profit of £44.5m (2014: £40.0m). Like-for-like gross profit growth was 4.7%. The business continues to service 23 of the largest 25 pharmaceutical clients7 globally, of which 18 have been clients for 4 years or more, as well as a growing number of biotech clients, particularly in the USA.

The Board of Cello Health has made significant progress in executing its long-term strategy, which consists of four key areas: branding, collaboration, global expansion and innovation.

The migration to the Cello Health brand has now been successfully completed, allowing the business to add more value to each client relationship and enabling more collaboration. Collaboration across Cello Health continued to rise and collaborative projects were commissioned by established and new clients alike in the UK, in Europe and in the USA. The two largest clients of Cello Health grew as the relationship spread to other capabilities. The average contract size of client jobs also continues to increase, improving visibility.

Cello Health has continued to expand in the USA, the primary market for such services globally. The business’s presence on the West Coast of the

USA continues to grow, with a good first full year contribution from Promedica and material new client relationships organically secured during the year by Cello Health. The Group made a material investment in a new start-up venture Cello Health BioConsulting in the Boston area to access the growing USA biotech marketplace. In addition, the office in Chicago continues to expand rapidly. Cello Health now has offices in all the locations required to support core clients’ needs.

The progress achieved by Cello Health BioConsulting in growing our new Boston office has been inhibited by employment restrictions on key employees from their former employer. However, in March 2016, agreement was reached between Cello Health BioConsulting Inc, certain employees of Cello Health BioConsulting Inc and their previous employer, allowing the partial release of these employees from their post-employment

Strategy on track,collaboration drives growth

7 Source Pharmaceutical Executive June 2015.

9

Cello A

nnual Report 2015

CH

AIR

MA

N’S ST

AT

EM

EN

T

restrictions. When this agreement is formally completed, a payment of £0.9m will be made, with additional payments contingent on the financial performance of the Cello Health BioConsulting business over the next 12 months. The Group believe this represents a sensible investment in an important growth area for Cello Health.

The Cello Health product range has continued to expand and develop. ‘IQ’, Cello Health’s quantitative research offering, has grown significantly. eVillage®, Cello Health’s digital research community platform is rapidly becoming a material component of the client proposition. The business is expected to launch Pulsar Health as a social media based solution for clients requiring large datasets in 2016.

Areas of Cello Health’s consumer business experienced a slower year due to deferral of key projects, negatively impacting the overall margin of Cello Health. Excluding this effect, Cello Health’s operating margin was sustained at 20.9% for 2015 (2014: 21.8%) and like-for-like gross profit growth was 7.6%. Appropriate actions have already been taken to address exposure to slower areas of the consumer market.

Notable project wins in 2015 included the following: AbbVie, Abellio, Age UK, Ahlstrom, Algeos, Barchester Healthcare, Bellis-Jones Hill, Boehringer Ingelheim, Boston Scientific, British Lung Foundation, Cancer Research UK, Care Quality Commission, Clark Research, Cooper Vision, Gilead Sciences, Johnson & Johnson, Janssen, Lundbeck, Merz Pharma, NHS Leadership Academy, Reckitt Benckiser, Sanofi, Sennheiser, Sustrans, Symbiota, Tovera and Vertex Pharmaceuticals.

2016 will see further development of Cello Health’s client offer. The business starts the year with a robust order book and is confident about the future growth prospects of the business as it pursues its focused investment strategy.

Cello Signal (www.cellosignal.com)

2015 2014 £’000 £’000

Gross profit 41,555 39,469

Headline operating profit 3,952 3,433

Headline operating margin 9.5% 8.7%

Cello Signal had a good year, with a strong second half. Cello Signal is traditionally a second half weighted business due to its presence in the charity sector whose activity is more weighted towards Christmas. The business delivered headline operating profit of £4.0m (2014: £3.4m) on gross profit of £41.6m (2014: £39.5m) and like-for-like gross profit growth of 3.7%. Operating margins improved from 8.7% to 9.5%.

Cello Signal is following the same path as Cello Health of integrating the core proposition behind a single client-facing brand. This has already begun to bear fruit in the form of material new client wins in late 2015 in the financial services and utility sectors under the Cello Signal banner, underpinned by a digitally-led proposition to clients. Growth in these sectors can be attributed to Cello Signal’s increasing expertise in complex databases and regulated client markets. These sectors have a common requirement to communicate regularly to their large customer bases.

The connectivity of Cello Signal will take a major step forward in 2016 as the majority of the Cello Signal businesses will become connected under a single P&L and single senior bonus structure. This will enable the business to compete more effectively against its large technology-led competitors, as well as other agency groups.

A particularly exciting element of Cello Signal’s 2015 performance was the strengthening of licence sales and renewals for Pulsar, Cello Signal’s social media monitoring and analytics

software platform. The business grew its software licence client base to 191 at the end of 2015 (2014: 88). While there was a headline operating loss of £0.2m, the business is not expected to make losses going forwards. A growing strategic relationship with Facebook may have a significant positive impact on the competitive advantage enjoyed by Pulsar.

In addition, a key strategic imperative for Cello Signal will be to partner with Cello Health to build on its expertise in the public health area, where Cello Signal has produced campaigns relating to cancer screening, alcohol abuse and healthy eating. This will include the application of Cello Signal’s expertise in digital media, which can be readily applied to pharmaceutical solutions for clients. Cello Signal also intends to adapt the Pulsar Platform as a dedicated offer to the healthcare client community.

Major clients wins in 2015 included: AC Hotels (Marriott), Adidas, Autograph Hotels, Bowers & Wilkins, Coty, Courtyard Hotels, De Beers, Drinkaware, EDI Group, Famous Grouse Global BTL, Havas Media, Hershey’s (China), Holiday Inn Express, Home Retail Group, HP, IHG Hotels Group, Jim Beam, Kinross House, Leprino Foods, Marriott, Maxxium Midori, Mazda, Microsoft, Musgrave Group, Nairn's, Prostate Cancer UK, RBS, Renaissance Hotels, Thames Water, The London Clinic, UK2, Unilever and Visit Scotland.

CURRENT TRADING AND OUTLOOK

The Group began 2016 with a robust level of secured forward bookings. It has also seen encouraging levels of new business wins so far this year. At this relatively early stage of the year, the Board is confident that expectations for 2016 will be met.

Allan RichNon-Executive Chairman16 March 2016

10

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O H

EA

LTH

11

Cello A

nnual Report 2015

CE

LL

O H

EA

LTH

Healthcare – our future2015 saw significant progress being made in executing our long-term strategy which consists of four key building blocks:

• Branding – The unification of our business under a core brand to allow us to add more service value to our client relationships and to enable our people to collaborate more readily.

• Global Expansion – To focus on expanding our global footprint, specifically our presence within the US market.

• Innovation – To continue to innovate, develop services and products that our clients need, capitalising wherever possible on the range of technical and digital advances being made.

• Collaboration – To leverage the different assets across Cello Health in terms of product development and meeting clients’ needs.

In 2015 significant progress has been made across all these four areas.

12

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O H

EA

LTH

BRANDING

Back in 2013 the core Health Division consisted of eight different businesses. Client feedback at the time told us very clearly that this did not make sense, especially when the client needed a truly blended set of skills and expertise in the agency team. Cello’s unification of its health businesses under the Cello Health brand was more than skin deep.

Unification involved change in organisation structure, creation of a Board and leadership teams and development of new ways of working to manage the range of services that we provide our clients. This change has taken time to implement. However, the migration to the Cello Health brand represented by our three core capabilities (Consulting, Research and Communications) has now been successfully established.

Customers now have the best of both worlds: best in class capabilities and blended teams that offer powerful integrated solutions, delivered through an organisation that has the bandwidth of a large agency, with the flexibility, tailoring and care of a boutique.

GLOBAL EXPANSION

With the opening up of a new office in Boston and the investment made in a new start-up venture ‘Cello Health BioConsulting’, we have doubled our consulting presence on the East Coast of the USA. Given the importance of the Orphan, Rare and Specialist Disease market, and that over 40% of our consulting revenues are generated from the USA, this will continue to be a focus area for us.

Importantly, with the opening of the Boston office, combined with our existing offices in Chicago, San Francisco, Manhattan and Yardley (PA), we now have offices in all of the important locations in the USA to service our clients’ needs.

The research firm Promedica, acquired at the end of 2014, has performed to expectations in its first full year of contribution within Cello Health.

INNOVATION

Over the last few years we have invested in a range of innovative digital solutions, for example eVillage®, our digital research community platform, IQ our Intelligent Quant offering and the development of mobile apps for research purposes. We are seeing continued success and growth from these initiatives.

Our consulting practice continues to consolidate its IP in a number of areas. Specifically CompetitoRoom™, consisting of competitive management programs and simulations and RedThread Planning™, our cloud-based Strategic Planning software, both have shown growth during 2015. In addition we have further developed FUTURESCOPE™, a key service to help clients reduce commercial uncertainty in early product development.

COLLABORATION

In excess of £5.0m revenue was generated by collaborative projects in 2015 across Cello Health. Collaborative projects were commissioned by both established and completely new clients, confirming that the blended approach we now provide has opened up new opportunities.

SUMMARY

In summary, in 2015 Cello Health made significant progress in executing our long-term strategy. Our client base remains strong, we continue to attract the best people and are successful in developing and retaining talent. Operating performance for our core health operations was in line with expectations.

Our Consumer Health business, which provides services to the wider health and wellbeing market amongst other industry sectors, had a challenging year due to client restructuring and slowness in the commissioning of projects across its non-health client portfolio. Despite this, the business has successfully retained the majority of its well-established blue-chip clients and attracted a range of new clients that should put it back on course for 2016. Importantly, Cello Health in 2015 has established a solid foundation on which we can build long-term growth.

In 2015 significant progress has been made across all these four areas.

13

Cello A

nnual Report 2015

CE

LL

O H

EA

LTH

THE FUTURE

In 2014, Americans alone spent $3 trillion on healthcare and other related products and services.1 Evaluate Pharma is predicting that the worldwide pharmaceutical market in itself will be worth $1 trillion2 in sales by 2020. Continuing major scientific and technological advances, coupled with sociodemographic changes, increasing demand for medicines and the increase in novel new drugs being approved, suggest that this forecast is likely to be exceeded. The clients we serve represent a substantial industry sector and have a healthy future.

The healthcare market is also changing rapidly. A recent PwC paper3 highlighted that 24 of 2013’s Fortune 500 companies are new entrants to healthcare. What is remarkable is their makeup. Eight are technology and telecommunications companies. Seven are retailers. Two are automakers, including Ford Motor Co, which is developing services for chronic condition management while driving.

The market for Cello Health’s services continues to expand at a rapid rate, driven not only by our traditional healthcare client base but also by the vast array of new entrants into the healthcare space. The role of gene therapy, genomics, smart diagnostics, biomarkers, the use of wearable devices, mobile health apps and digital channels and social platforms are changing the market we and our clients operate in.

Our clients still face many challenges. Last year we commented that costs of bringing products to market run into the billions, with many new drugs failing to meet pre-launch expectations. Our clients need to improve on this success rate. They need to progress the right molecules through the R&D process, ensure trials are configured appropriately, and produce the right evidence to support the positioning of the brand with the right commercial strategy to optimise commercial success. Our clients need to get it right first time, which is why they need and see the value in the services we provide.

With their iPhones, iPads, access to apps, websites, and all the various forms of social media, consumers are ever more active and self-directive in how they engage with health issues. This has a major impact on how our clients need to shape how they communicate the value of their brands. This is a key strength of Cello Signal. Cello Signal works across household names in financial services, energy, the public sector and charities helping clients understand how consumers interact with the digital environment. Our healthcare clients share this same need to understand their customers in an increasingly digital world.

The combination of Cello Health’s technical marketing advisory skills, combined with Cello Signal’s digital expertise, we believe sets us apart from our peer set. In 2016, it is our intention to capitalise on this unique combination of skills for the benefit of our healthcare clients and the continued success of Cello Health.

A recent PwC paper highlighted that

24 of 2013’s Fortune 500 companies

are new entrants to healthcare

,,

1 CMS.gov2 World Preview 2015, Outlook to 20203 PwC: Healthcare’s new entrants: Who will be the industry’s Amazon.com

14

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O H

EA

LTH

Cello HealthKey highlights of 2015

CELLO HEALTH INSIGHT

• Strong overall growth in GP and OP vs 2014 with addition of 20 new clients.

• Significant broadening of the USA client base and types of work commissioned.

• Growth in early stage commercial opportunity assessment, doubling the number of engagements in 2015 and setting the stage for continued growth in 2016.

• The IQ quantitative practice delivered 22% year-on-year increase in revenue with investment throughout 2015 allowing the team to expand, bring on board senior analytics expertise and roll-out advanced new software.

• IQ now represents 27% of Cello Health Insight’s revenue, with 25 clients commissioning IQ during 2015.

• Digital offering continued to strengthen, with 11 mobile projects (utilising proprietary app ‘inthemo’) and 33 eVillage® online community platforms commissioned.

CELLO HEALTH CONSULTING

• Continued success across a range of pharmaceutical and biotechnology companies with increasing presence within small to mid-cap biotech companies, building on their developing expertise in biologicals, rare diseases and specialist medicine.

• Remain preferred strategic partner for one of the world’s largest pharmaceutical brands, working with their global and USA commercial teams as they manage new competitive threats as well as developing new indications and pipeline.

• USA continues to be the major growth initiative for Consulting with over 40% of the revenues generated here. 2015 saw Consulting start-up Cello Health BioConsulting, with a doubling of its presence on the East Coast, opening up a new office in Boston.

• One in five consulting projects now delivered collaboratively with Cello Health Insight and Communications, with clients benefiting from their fusion of expertise.

• Continued to consolidate IP, with new extensions to services such as FUTURESCOPE™, CompetitoRoom™ and RedThread Planning™ sold across significantly more clients.

15

Cello A

nnual Report 2015

CE

LL

O H

EA

LTH

CELLO HEALTH COMMUNICATIONS

• A growth year, with 135 communication specialists providing a range of medical and marketing communications transatlantically.

• An increase in collaborative accounts, with 13 new clients added to the Communications roster as a result of partnering with Cello Health Consulting and Insight colleagues.

• Continued focus on leveraging the technical scientific and health outcomes expertise to further deepen and differentiate service offering globally.

• New projects have been won and successfully delivered across territories including Asia, Africa, Eastern Europe and Australia.

• Cello Health Communications projects included innovative digital advisory boards enabling medical experts to discuss, learn and work collaboratively via an online platform from geographically disparate sites. Providing clients with increasing digital solutions offers a key area of growth for 2016.

CELLO HEALTH CONSUMER

Kudos

• A very strong year with substantial growth in revenues.

• Continued growth in B2B research amongst hard-to-reach and C-Suite audiences.

• Continued focus on corporate reputation and thought leadership research for large global consultancies.

• High level of repeat and referred third-party business. Kudos now undertakes specialist B2B data collection for 25% of the UK top 40 market research agencies.

• Further development of qualitative offering this year, with Kudos being awarded Best Qualitative Research 2015 by data-collection industry benchmark quality standards IQCS (Interviewer Quality Control Scheme).

Breaking Blue

• Significant repeat business within core client base despite some budget delays.

• Re-branded and consolidated four sub-brands under one leading brand Breaking Blue – engendering greater market presence and stronger positioning as well as more flexible utilisation of internal resources.

• Tracking business goes from strength to strength, spanning a full range of client sectors.

• Significant new clients in 2015 included: Care Quality Commission, Cancer Research UK, Money Advice Service and NHS Leadership Academy.

The Value Engineers

• A slower year due to a number of key clients undergoing re-structure and budget deferrals.

• The USA office continued to experience high double digit growth, building a strong working relationship with a leading medical device supply company.

• Significant new business wins as a result of concerted business development drive in the UK and USA.

• Growth of B2B brand practice, attracting the likes of Ark Data Centres, Land Securities and Signium.

16

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O H

EA

LTH

CELLO HEALTH CONSULTING

Commercialisation of a phase II biotech asset

CLIENTUS client, a global biotech joint venture on a new personalised oncology asset.

CLIENT CHALLENGETo work with two biotech organisations to understand what it will take to bring their Phase II asset to market given the shift in market and competitive dynamics.

OUR APPROACHAt its core this project was about developing the right Target Product Profile (TPP) for a new asset targeted at a rare oncology population. We quickly recognised that these two clients had a lot less market, competitive and customer insight than we had anticipated and there was a lack of alignment around objectives and ways of working across the joint venture.

We combined two of our proprietary approaches, FUTURESCOPE™ and CompetitoRoom™ in order to achieve the objectives. The first step was to map out the future environment. We enhanced our desk research

using our scientific and research teams from our Communications and Insight capabilities before developing detailed, engaging and tangible potential future scenarios.

Through this process we anticipated the impact of competition. There were meaningful threats posed by one competitor in particular that required focus and planned response. We used another workshop-led process to help teams get under the skin of their competitor to understand what it would take to bring a meaningful innovation to patients and yield business return.

THE RESULTUltimately, our fusion of expertise and proprietary processes forged a stronger partnership between this joint venture, identified areas where they could streamline ways of working, develop new capabilities and also refine clinical trial outcomes to improve market access. Cello Health is now set to work further with this biotech joint venture as the companies build commercial capabilities and move from clinical to commercial.

CELLO HEALTH COMMUNICATIONS

Empowering pharmacies to make a difference to consumer’s health through weight loss/management

CLIENTOmega Pharma (Product: XLS-Medical a weight loss aid, OTC).

CLIENT CHALLENGEFor XLS medical to become the preferred weight management service within pharmacy. Enabling and empowering pharmacies to make a difference to consumer’s health via weight loss/management. The client wanted to promote its brand whilst also achieving its overarching objective of becoming leaders in pharmacy education and support.

OUR APPROACHThe project aimed to design a three-pronged approach to weight loss, including education on a healthy lifestyle and ongoing support delivered via an in-pharmacy weight loss consultation service, positioning the new weight loss

product as a helping hand.

Our goal was to provide pharmacists with the knowledge and tools to launch the in-pharmacy weight loss consultation service in partnership with a well-known retail pharmacy chain.

We did so by creating a suite of resources that gave them the motivation, the knowledge and the tools to deliver against objectives as well as pilot the materials and programme prior to national roll-out.

THE RESULTPilot programme adopted by 18 pharmacies with materials receiving excellent feedback – 80% felt confident at being able to launch an in-pharmacy weight loss consultation service. The client has plans to extend the service to more pharmacies in 2016.

Our work

17

Cello A

nnual Report 2015

CE

LL

O H

EA

LTH

CELLO HEALTH INSIGHT

Understanding the ways in which doctors use digital channels to exchange information and communicate with peers, pharmaceutical sales representatives and their patients

CLIENTSelf-funded study to assess digital engagement among healthcare professionals across the globe.

CLIENT CHALLENGEAdvances in digital technology are delivering breakthroughs in diagnosis through initiatives such as ‘Watson’ from IBM, which claims to combine advanced image analytics with cognitive capabilities to ‘see’ and interpret medical images more like a human would. Advances in smart technology are also providing new ways to manage patients’ treatment through myriad health apps and wearable technologies that promise to include such innovations as Google’s ‘Smart Contact Lens’ that will measure blood glucose levels for people with diabetes. We are all now familiar with an array of digital devices including smartphones, smart watches and tablets that are in turn opening up new digital channels of communication though messenger apps, software applications like Skype and various social media.

Clients in the pharmaceutical industry are increasingly interested in understanding the potential impact that these developments might have on consumers as well as the opportunities they present for marketing pharmaceutical assets.

APPROACHCello Health Insight undertook a self-funded online research project involving over 1,000 doctors across eight global markets to explore in greater depth the ways in which doctors are using digital channels to exchange information and communicate with peers, pharmaceutical sales representatives and their patients. This study went far further than other studies conducted elsewhere as it

looked not just at what was currently happening but the preferences driving this behaviour and expectations for the future.

THE RESULTThe study found that in spite of digital advances, face-to-face information from peers, Key Opinion Leaders (KOLs) and rep visits retain the biggest influence on doctors’ prescribing behaviour. Pharmaceutical companies should not therefore rush to phase out their sales force. Rather they need to look at how digital technologies can be used in tandem to optimise message delivery.

Almost half of physicians regularly share information online across specialist websites such as patient.co.uk and webMD and they are also utilising general consumer social media channels like Facebook and Twitter to share with their peers in a professional capacity. Markets such as Brazil and China are ahead of the curve in their usage of platforms such as WhatsApp to interact with patients and it seems likely this trend will become apparent in other markets. This will provide patients with more immediate interaction with their physicians but will also raise expectations regarding immediacy of response, bringing added pressure to healthcare providers.

Cello Health Insight found that these doctors are sharing precisely the type of information that other doctors are interested in seeing, which makes them highly influential as online KOLs. They should also be a key focus for pharmaceutical marketers, who must now give consideration as to whether the nature of the messages communicated should be the same for online KOLs as it is for offline KOLs.

18

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O H

EA

LTH

CELLO HEALTH INSIGHT

Uncovering and harnessing drivers in ADHD

CLIENTA European based pharmaceutical company.

CLIENT CHALLENGEDespite clinical advantages over the competition, our client’s product had not achieved the expected sales 18 months post-launch. The key objective was to understand psychiatrists’ deeper beliefs and emotions when treating ADHD and the key factors truly driving brand choice.

APPROACHWe utilised our unique psychology-based Kaleidoscope methodology to facilitate our access to participants’ out-of-conscious beliefs and emotional drivers and go beyond rational and clinical thinking. This was moderated by our expert Master Practitioners during a series of interactive groups utilising unusual but highly informative techniques,

the results of which were then interpreted using established psychological models.

THE RESULTThe research clearly showed that a one-size-fits-all approach across different markets was not going to work for the positioning and messaging around the brand. A complex dynamic was shown to be at play between physicians and parents, with physicians locked into a pattern of behaviour driven by previous interactions. We provided the client with clear recommendations on how to support the physicians in these difficult conversations and how to respond with confidence to the challenges the parent may raise. Our insights enabled the client to help develop a revised communication strategy that would more effectively pull physicians towards the brand.

THE VALUE ENGINEERS

Sharpening global brand proposition in the medical devices market

CLIENTGlobal medical device manufacturer.

CLIENT CHALLENGEDuring 2015 we were retained by one of the world’s biggest medical device manufacturers to help sharpen the definition and clarity of its corporate brand proposition. Historically, the company had been a salesforce powerhouse. Deep personal relationships between reps and physicians have served as the bedrock of the company’s reputation and success. However, changes in the healthcare sector are seeing more purchase decisions in the hands of groups like hospital administrators and even patients, who might have limited, or no exposure to sales reps. Consequently, the company needed to deploy a brand with depth and dimension, that connects with a larger and more diverse audience, and that shapes multi-channel communications efforts moving forward. In short, its brand needed to be as strong as its sales team.

APPROACHThe strongest brands play meaningful roles in the lives of their customers. Our client needed to identify the role it sought to play beyond simply supplying great medical devices. Through research we uncovered an insight into what truly motivated healthcare professionals to become physicians, nurses, hospital administrators or medical engineers in the first place, and through the brand development process, positioned our client’s brand in the role of helping them feel they are living up to that higher professional purpose.

RESULTDiscovering a powerful, unifying insight was just one element in crafting a compelling role and story for its brand. We also created a purpose-built brand model, along with a brand architecture designed to provide flexibility for business units to respond to their unique market demands, while at the same time continually building the more enduring aspects of the brand.

Our work

19

Cello A

nnual Report 2015

CE

LL

O H

EA

LTH

BREAKING BLUE

Establishing the hard facts to set the social care agenda for people living with cancer

CLIENTMacmillan Cancer Support.

THE CLIENT CHALLENGEMacmillan was concerned that many people affected by cancer receive inadequate care, relying on informal care networks – family and friends who often lack the time, energy or skills to give them appropriate support. Macmillan needs a robust understanding of the needs of people living with cancer to inform the Macmillan research team, and its policy, campaigning and service delivery workstreams.

OUR APPROACHIt was crucial that we provided insights that were not only robust, but that communicated the ‘human’ dimension, giving people the opportunity to tell their story. We began by conducting a programme of deliberative cognitive testing, working iteratively through proposed terminology and question wordings with different audiences affected by cancer. We structured the quantitative questionnaire in a way that would traditionally be considered unorthodox starting with open-ended questions to allow people to share those issues that were most top-of-mind, before going on to ask questions that would later allow us to

model data quantitatively.

We followed the quantitative phase with in-home depth interviews with representatives of each of the segments combined with an online diary using our platform e-luminate™, where people logged their care needs over a week and also uploaded photos and video clips talking about their experiences. The depth interviews were critical in identifying the inter-relationship between medical and social needs and the need to treat these in tandem.

THE RESULTThe research showed for the first time a full picture of the social care needs of people with cancer. For the first time, Macmillan can quote the proportion of people with unmet needs, and can quantify the impact. Macmillan is now beginning a programme of strategic partnerships with local authorities that will deliver crucial services to those with cancer. The findings were published in March 2015, in a ground-breaking report, Hidden at Home, to extensive media comment. The research won a prize at the National Cancer Intelligence Network (NCIN) 2015 Cancer Outcomes Conference and was a finalist for the MRS Award for Public Policy/Social Research 2015.

20

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O S

IGN

AL

21

Cello A

nnual Report 2015

CE

LL

O SIG

NA

L

Making brands more humanSignal is poised to become a properly integrated business behind a united brand:

We use technology to help clients unlock the value of their brands by achieving more customised and iterative engagement with customers. The combination of technical and communication skills gives Signal a unique advantage globally as we compete to service the world’s leading brands.

22

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O S

IGN

AL

The most important development as we enter 2016 is the migration of our core agency businesses into a unified structure behind the Signal brand as the client-facing proposition. This will also involve a migration to a single P&L for Signal. We have seen the success achieved by Cello Health over the past two years as a result of the same integration process and we are confident Signal will enjoy similar success.

A further key ambition for 2016 will be to partner with Cello Health in developing our existing health-orientated activity into a larger and more developed aspect of our offering. We are already producing campaigns in public health in areas such as cancer screening, alcohol abuse and healthy eating as well as working with a variety of health-related charities. This experience will form the basis of creating stronger links with Cello Health and as a start point for marketing to the Consumer Health and Wellbeing sector.

Given our experience in complex databases and regulated markets it was particularly gratifying to see our utility client base grow across the UK in 2015. This sector, like the Financial Services industry, have a requirement to regularly communicate to their extensive customer base and are acutely aware of their need to be more customer centric. We have now established significant remits and retained relationships with three of the UK’s largest energy providers, across each of our UK offices. Utilities now have the potential to sit alongside Charities and Financial Services as one of our largest and strongest performing sectors.

A significant investment task remains in the USA where we have established offices in New York, San Francisco and Los Angeles. We have an enviable client base and recruited a strong senior team. However, getting to the point of ‘critical mass’ for our US operations has held back our profit delivery. With the team and office network in place, 2016 should see our US profit performance improve and help improve Signal’s overall margin.

Our investment in building our social media software offering, Pulsar, has created a cutting edge lead product for Signal. Pulsar’s client base grew to over 200 by year end. Our close relationship with Facebook opens up exciting opportunities for 2016 and beyond.

INSIGHT AND INNOVATION

Collectively, our Insight and Innovation businesses increased their profit delivery by more than 20%. This profit growth was at its strongest in our UK operations, a particularly exciting element of which was the strengthening performance of the licence sales and renewals for the Pulsar Social Media Monitoring platform. In the closing stages of the year Pulsar started delivering small monthly profits and is set to be a net contributor to our profit performance in 2016.

Another highlight in terms of year-on-year performance was Human Innovation, which enjoyed a full year of activity from the US Hotel and Technology clients it secured in 2014. Its work also resulted in the passing through of a significant web build project for a US Hotel client that will result in further work in 2016.

MARKETING TECHNOLOGY AND DIGITAL BUILD

Our delivery of large digital-build projects that give clients far greater scope to use marketing content in CRM, Web and Mobile has become a key foundation stone of our proposition. The dominating objective of these projects is to deliver a customer centric approach as Banks, Charities and Utilities have clearly learnt the pitfalls of over investing in crude, volume sales techniques. Increasingly, we see our future in helping client brands establish a more empathetic, personalised and intelligent relationship with their audiences.

23

Cello A

nnual Report 2015

CE

LL

O SIG

NA

L

CAMPAIGNS AND CONTENT

Some of the biggest gains in client activity took place in our creative agencies where Edinburgh (Leith) and Cheltenham (Tangible) enjoyed a ‘purple patch’ in the second half of the year, winning new contracts and extended remits from major Banks and Utilities. Leith was also appointed on a global basis to deliver integrated communications for the Edrington Group’s Famous Grouse brand.

Based on the increased client activity out of London, Stripe has opened a London office and taken space with the 2CV offices in Flitcroft Street.

Our skills in Experiential Marketing were recognised by a gold at the MCI European awards for sponsorship for the Bru Store, which was the centrepiece of sponsor activity during the 2014 Commonwealth Games.

PRODUCT DEVELOPMENT

Pulsar Platform is a leading element in our initiative to drive strong health-related revenues through Signal. Pulsar Health will launch in H1 of 2016 as a dedicated offer to pharmaceutical clients who want more insight into how certain conditions are being discussed in social channels.

The learning from Pulsar in terms of shaping and selling a distinct product proposition is also informing the packaging and sales of our CRM automation, UX and Social Media propositions. Centralising our marketing and sales teams is a significant step towards being able to promote our product range more coherently and aggressively in 2016.

THE FUTURE

We have made a major effort over the last three years to drive greater connectivity between our agencies and across our geographies. This will take a major step forward in 2016 when we connect five of our agencies in a single P&L that allows us to access resource and digital expertise more freely, encouraging a single-minded investment strategy and focusing the senior executive team on the overall global outcome.

A significant element of that investment strategy will be putting in place a more clearly demarcated health strategy for Signal with the objective of seeing Health and Wellbeing take up equal prominence to our established sector expertise in Financial Services, Utilities, Charities and Leisure and Travel.

Our skills in

Experiential Marketingwere recognised by a gold at the

MCI European awards for sponsorship for the

Bru Store

,,

24

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O S

IGN

AL

Cello SignalKey highlights of 2015

FACE AND PULSAR

• A healthy profit was maintained in the core Face business and Pulsar passed the break-even barrier in its second full year of trading.

• Pulsar CORE was launched, an analytics tool for measuring the impact of brands owned social media channels, with 50+ clients using the product within 6 months.

• The Department of Health selected Face to help monitor social media feedback from the public around healthcare policies and tracking conversations surrounding clinical diseases.

• Pulsar launched Facebook Topic Data Analytics to enable its hundreds of customers to understand what people share and engage in on the world’s largest social network.

BRIGHTSOURCE

• 14th consecutive year of gross profit growth fuelled by strong organic growth across 18 of 20 largest clients.

• 2014 investment in senior management and digital/tech capability, and focus on larger clients, delivered strong results with operating margin increasing to 14.2%.

• Growth driven by launch of multi-channel communications platforms, TriggerHub and Helios, aimed at brands with complex CRM priorities.

• Helios platform used to deliver the UK’s single largest campaign, to 28 million customers, for one of the UK’s largest regulated brands.

• Instinctiv division won significant new behavioural-planning workstream for British Heart Foundation.

LEITH AGENCY

• A strong year of growth, with three major client wins this year: RBS, ScottishPower and The Famous Grouse global integrated account.

• Excellent year for industry awards. Work for First Great Western (now GWR) picked up CIM Marketing Excellence Marketing Campaign of the Year, Gold at the UK Marketing Society for Effective Marketing, Gold at the Rail Business Awards and Silver at the Travel Marketing Awards.

• IRN-BRU’s sponsorship of the Commonwealth Games lauded across Europe, with major awards including: IMC European Partnerships Gold, IPM Grand Prix, European Sponsorship Awards Excellence Gold, UK Marketing Society Gold, UK Sports Industry Awards Gold, and UK Sponsorship Awards Sponsorship of the Year.

• Another strong year for partnerships/experiential arm, Leith Links, which achieved strong growth following success at the Commonwealth Games.

2CV

• Continued strong growth across the global network, with significant new contract wins.

• Strong performance in the West Coast USA offices, underpinned by dominance in the electronic games sector.

• Strong performance in Asia, with growth in the Singapore office serving multi-national clients.

• Successful retention of the core TfL account through competitive retender.

25

Cello A

nnual Report 2015

CE

LL

O SIG

NA

L

BLONDE

• A strong year of new business, including a number of enterprise scale projects which will define the future shape of Blonde.

• Large scale enterprise builds for organisations including Williams & Glyn Bank, Nando’s, BASF and Scottish National Galleries.

• Closer integration with Tangible, Leith and Brightsource as the core of the new Signal Agency proposition.

STRIPE COMMUNICATIONS

• Continued evolution as a digitally focused PR and Communications Agency – doubling the number of digital accounts through the recruitment of a specialist digital team and upskilling of the agency.

• Won 15 industry awards this year including: Gold Awards at the Social Buzz Awards, CIPR Pride Awards, Marketing Society Excellence Awards including Agency Employer Brand of the Year and the PRCA Dare Awards.

• New material clients secured in 2015 include: BESA, MacSween, Magners, Napiers, Midori, Brodies, Turcan Connell, Scottish Wildlife Trust, Zero Waste Scotland and Robertson Trust.

HUMAN INNOVATION

• Expanded footprint within both IHG and Marriott Group with new brand wins including: Courtyard Hotels, Autograph Hotels, Intercontinental Hotels, Hotel Indigo, Holiday Inn Express, AC Hotels and Moxy Hotels.

• Won a very high profile engagement with Marriott Group to design their new corporate brand architecture across all brands.

• Successfully launched new IP in ‘competitive war gaming and scenario planning’ and successfully delivered a corporate level engagement with HPs senior management team in Europe.

TANGIBLE

• DMA Gold for The Royal British Legion ‘Everyman Remembered Campaign’.

• Four major pitch wins including: npower, Vanguard, EDF, PCUK and retention of The Royal British Legion.

• Two Nudge Awards for application of Behavioural Economics for Lloyds Banking Group.

• Extended remit from Sainsbury’s Bank, following competitive tender.

OPTICOMM

• Won two new clients in two key verticals; not for profit Tearfund and learning Pearson – both with sizeable campaigns running in 2016.

• Won Luton Airport media account, bolstering travel vertical.

• Developed role with NFUM to go beyond econometric modelling and into media planning and management.

TMI

• Commissioned by NHS to help equip its organisations with skills, knowledge and behaviours to revolutionise patient and customer service experience.

• Developed proposition for Travelodge business to improve customer experience. This will now be rolled out across a further 100 hotels.

• Designed and delivered behavioural training for Thames Water throughout 2015 to support its move to end-to-end customer management.

• Designed and delivered a series of workshops for c2c Rail as part of a 3-year behavioural change programme. c2c was awarded Passenger Operator of the Year at this year’s National Rail Awards.

26

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O S

IGN

AL

Our work

FACE AND PULSAR

Understanding female car purchasing behaviour …. using Facebook Topic Data

Aggregated and anonymised Facebook Topic Data allowed us to glean insights from 1.44bn people: an unprecedented scale. We used a Facebook dataset that covered the discussion around BMW, Ford and Honda in the US and UK across 2015. This coincided with the launch of Pulsar’s Audience dashboard, which meant we were able to identify demographic trends within this topic.

One of most interesting insights from our report was that a higher proportion of females discussed the style of cars than males (39% of discussion from women posted or shared content about the attribute, compared to just 28% of men). We also discovered that conversation around style becomes increasingly female-centric through lifestages, with the hypothesis being that as children leave the family home, the choice of cars is less based on functionality and more on aesthetics – particularly as disposable income rises.

2CV

Helping make every journey matter at Transport for London

Everyday more than 30 million journeys are made across the Transport for London network. Over the last few years, TfL has undergone a strategic and cultural change in order to become more focused on the customer and empower staff to embrace the idea that every journey matters. This represents a significant cultural change, from an organisation that historically focused on getting people from A to B in the quickest time possible, to thinking about every aspect of the customer experience.

2CV designed and delivered a pivotal piece of deliberative qualitative research that discovered five levers of the TfL reputation: What It Stands For, Experience, Value for Money, Progress/Innovation and Trust. We worked closely with the TfL Customer Research and Insights team to ensure research built on what was already known (for example ensuring value for money) as well as add fresh customer viewpoints to create a model that worked for both TfL and customers. This model now sits at the heart of the business and continues to evolve with every piece of work we do for TfL.

With the model in place, TfL has been able to focus its efforts on the things that matter to customers: communicating openly and honestly and delivering changes that improve experiences. TfL’s reputation is now at an all-time high.

27

Cello A

nnual Report 2015

CE

LL

O SIG

NA

L

BRIGHTSOURCE

Creating a more personal experience for British Heart Foundation supporters

Many of British Heart Foundation’s new supporters were cancelling their donations within the first year. So BHF set us the challenge of increasing engagement in the crucial early months.

Combining supporter-led planning, with our TriggerHub communications platform, allowed us to transform the experience for BHF’s new supporters – leaving behind the tired, one-size-fits–all direct mail approach that charities have typically relied upon.

We designed the journey around supporter behaviours, using triggers such as direct debit payments as opportunities to be more human, to say ‘thank you’ and learn about their motivations. From there, every subsequent communication builds on the last, providing increasingly tailored content to reflect their interests and improve relevancy.

Additionally, the new welcome message arrives in real-time, rather than taking a month. Content is individualised around location, demographics and direct debit value and points supporters to personalised online surveys to help us gain insight into their interests and preferences.

Using TriggerHub allows dynamic email, personalised landing pages and offline messaging to work together seamlessly, creating a rich, personalised experience where the supporter feels in control. This, in turn, allows British Heart Foundation to enjoy a steeper, more profitable growth trajectory.

LEITH

An integrated approach to promoting Drinkaware

The Leith Agency has been proud to work with Drinkaware on a variety of strategic and creative briefs over the last 12 months. Most recently, Leith successfully delivered fully revised brand guidelines that will act as the foundation reference for all future communications. Included in these guidelines were important tonal references that were developed from the wealth of in-depth knowledge that Leith has on both the Drinkaware brand, as well as the full spectrum of different consumer and health profession audiences.

Each comms brief contains a strong health message, but the key challenge is nailing the tone of the communications to come across in an empathetic, understanding and ultimately human way. Often the lead creative idea will then carry through into a wide variety of compelling digital formats. On the digital front, Leith also teamed up with Blonde to do a full UX review and redesign of the website, the UK’s number one source of alcohol facts and advice online. A fine example of Cello agencies working together to achieve a greater good.

STRIPE COMMUNICATIONS

Social Media solutions for Maxxium

Maxxium tasked Stripe to reinvigorate the Midori UK audience following a period of silence from the brand and in the run up to new branding activity taking place in 2016. The solution was a mix of digital and social strategy development, community management, CRM and influencer outreach as well as traditional consumer and trade PR and communications.

From waking the sleeping giants of its Facebook page, reigniting the Instagram activity and kicking off a new Twitter account, we have used a combination of fan and influencer activity, supported by a strategic paid social approach, to get people re-engaging and discussing the brand.

Recently reporting on our 8th month of activity, the results have been extremely successful with fans increasing steadily across all channels. Specifically we’ve seen Facebook engagements surpassing their 12-month KPI – increasing by 13,000 over just four months.

28

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O P

EO

PL

E

29

Cello A

nnual Report 2015

CE

LL

O P

EO

PL

E

Strong and effective talent management is critical to the success of any organisation. Cello has always recognised that the strength and quality of our people is one of our key differentiators from our competitors. To maintain this competitive advantage, we continue to invest in our people, to build ways to not only attract the best people to the Cello Group, but also to retain the best people within our business.

Over the years we have grown a number of initiatives that focus on the development of employees at different stages of their career, and we will continue to do so moving forward.

We continue to invest in Cello Academy, our flagship programme now in its 11th year. Cello Academy aims to give our new managers access to expert training in key areas. This is fundamentally important to build client service delivery skills and prepare our managers for future senior roles in the organisation. Of particular importance has been the expansion of the programme to cover our US operations. We have also expanded the Academy brand, launching a number of new MasterClasses for Academy Alumni, to continue the training they are exposed to as their careers develop. In total, over 150 people have been through our Academy training programme this year, over 15% of our total employees.

In 2015 we continued the successful BiteSize training sessions – aimed at employees across the Group who want to learn more about topical management issues.

Across the Group we recruit a significant number of

graduates each year. Cello sees this intake as critical to the long-term success of the organisation. In addition, we value the fresh perspective bright young talent can provide in helping improve our services and how we deliver those services to clients. To that end, we will continue to invest in our graduate events each year, aiming to foster collaboration across the Group from their early days in the business.

THE FUTURE

We are constantly reviewing the focus of our training programmes to ensure they are future focused and valuable for the relevant audiences. In 2016 we plan to make a number of changes to the current content, by introducing a range of new initiatives.

A key focus for 2016 will be a focus on continual development of our senior employees. We will be launching a senior leadership development initiative, encompassing a number of modules designed around building the necessary skills and to prepare them for more senior management and leadership roles in the Group.

As well as allowing for continued development, our training also allows us to facilitate networking and collaboration across the Group. 2015 saw significant growth in the level of collaborative projects commissioned by our clients and this will continue to increase. The benefits of investing in our people are clear. In 2016 we are committed to continuing this focus as we move forward and ensuring we attract and retain the best people to best serve our expanding client base.

Investment in professional developmentContinuing to invest in our people

30

Cel

lo A

nnua

l Rep

ort 2

015

CE

LL

O P

EO

PL

E

Cello TalentSuccess stories

Alex KempResearch Executive

I started working at Cello Health Insight in September 2015. After completing my BSc in Pharmacology, I knew (and hoped) that my career path would lead me into the pharmaceutical industry. After deciding that I wanted to work for an agency, Cello Health Insight seemed like the perfect choice for me. I was particularly impressed by the prestige and diversity of its clients, which included all of the top 10 pharmaceutical companies. Immediately, I knew this was a company that I wanted to be a part of. The sheer breadth and variety of the work we do in terms of therapy areas, products and research methodologies has kept me captivated since day one. You are given exciting opportunities early on and there is a great atmosphere which helps you to learn and develop as a researcher.

Lydia JenkinsProject Manager

In July 2014, a month after graduating from Boston University with a degree in Public Relations and Psychology, I uprooted my life to move across the pond as a Project Executive at iS Health in Farnham. I was always fascinated with the pharmaceutical industry and I saw the opportunity to join a medical education company as a great starting point. After 9 months at iS, I was promoted to Project Manager. iS Health offered me the opportunity to learn all about the ins and outs of the industry, get involved with clients of varied functions and work on a multitude of projects, along with bringing my expertise from a different background to build new areas of the business. I couldn’t have pictured a better place to start my career.

31

Cello A

nnual Report 2015

CE

LL

O P

EO

PL

E

Patrick GannonMedical Writer

After completing my PhD in Pharmacology at the University of Pennsylvania, I was resolved to trade in my lab coat and gloves for a suit and tie. My objective was to find a position in the business side of science – one where I would continue to utilise the critical thinking skills and scientific knowledge I had acquired as a graduate student. Rather than devoting my career to the understanding of one disease, I sought knowledge in a wide range of therapeutic areas. Hence, the reason I joined MedErgy.

I was immediately impressed by MedErgy’s dedication to the training of new medical writers, which reinforced their commitment to delivering the highest quality medical communications, while establishing themselves as invaluable strategic partners among their clients. On a more personal level, MedErgy’s commitment to people, both in terms of their happiness and their opportunities to advance within the company, was even more impressive. I look forward to growing within the Cello Health community for years to come.

Megan GoodheadPlanner

I started at Brightsource in January 2012, and moved to Instinctiv in January 2013. I chose the company because it had a good graduate scheme that offered a range of different career paths.

What is great about working here? The diverse range of projects we work on. Being part of the great work we produce for our clients. The trust that is invested in staff. The opportunities to draw on the experience of talented people across the Signal network. An atmosphere that is simultaneously challenging and supportive. The innovative culture. Above all, the people.

Emma PaulAccount Manager

I joined Stripe Communications in 2012 as part of its Stars and Stripes graduate scheme. An ardent English Lit scholar, I was keen to find a profession where I could utilise my skillset; and after a tumultuous time teaching English in Indonesia, I was ready to start a career with a solid future.

I was impressed by Stripe’s client list, but slightly apprehensive about the industry as I’d completed a couple of PR internships at uni, which frankly bored me to tears…but how wrong I was! From day one, Stripe was fast-paced, future focused and bursting at the seams with creativity – exactly what I was looking for.

I’ve worked for a host of high-profile clients including John Lewis, Pizza Express and ScottishPower. Despite our exciting client roster and multiple award wins, for me what’s great about Stripe is the people – we’re young, ambitious and work together to create the best campaigns in the business.

32

Cel

lo A

nnua

l Rep

ort 2

015

FIN

AN

CIA

LS

Strategic Reportfor the year ended 31 December 2015

The Directors present their strategic report on the Group for the year to 31 December 2015.

GENERAL INFORMATION

Cello Group plc (“The Group”) is a healthcare and consumer strategic marketing group of companies. The Group is AIM quoted and is domiciled and registered in the United Kingdom. The Group has offices in the United Kingdom, the United States of America, Singapore and Hong Kong.

REVIEW OF THE BUSINESS AND FUTURE DEVELOPMENTS

The results for the year ended 31 December 2015 are set out in the consolidated income statement on page 42. These show a profit for the year of £3.0m (2014: £2.3m). An interim dividend of 0.84p per share was paid in November 2015 (2014: 0.80p) and a final dividend of 2.02p per share is proposed (2014: 1.80p).

The Directors are required by the Companies Act to present a business review, reporting on the development and performance of the Group and the Company during the year and their positions at the end of the year. A review of the development and future prospects of the business and key performance indicators (“KPIs”) are given in the Chairman’s Statement on pages 4 to 9 which are incorporated in this report by reference.

The Group’s KPIs are outlined in various sections of this review. Whilst there are many financial measures that the Group monitors on a regular basis our core financial objectives are:

• Headline profit before tax

• Headline operating profit

• Headline operating margin

• Like-for-like gross profit

• Headline operating cash flow conversion

• Headline basic earnings per share

RISKS AND UNCERTAINTIES

The Company regularly reviews the risks and uncertainties facing the business through a regular series of board and operational meetings. The Directors believe the current largest risks are as follows:

1. Economic conditionsThe Group’s business is domiciled in the UK but 41% of the Group’s revenues are from clients based overseas. It is clear that income from clients is impacted by the prevailing economic conditions. However, the broad spread of clients across sector and geography mitigates this risk.

2. Loss of the Group’s key clientsClient relationships are crucial to the Group and the strength of them is key to its continued success. The risk is mitigated by our client base being broadly spread and by several of our pharmaceutical clients being subject to longer term master service agreements. The loss of any large client would require replacement. The Group’s client review programmes help mitigate this risk.

3. Loss of key staffThe Group’s Directors and staff are critical to the servicing of existing business and the winning of new accounts and the departure of key staff could be a risk to maintaining client service. With that risk in mind all senior staff are subject to financial lock-ins and long-term incentive arrangements, as well as being under contractual non-compete and non-solicit clauses.

By order of the Board

Mark Bentley Company Secretary 16 March 2016

33

Cello A

nnual Report 2015

FIN

AN

CIA

LS

Directors’ Report

The Directors present their report and audited financial statements for the year ended 31 December 2015.

Information covering the legal constitution of the Group; the location of its branches; dividends, and comments on future developments can be found within the strategic report on page 32.

DIRECTORS

The Directors of the Company who were in office during the year and up to the date of signing the financial statements were:

Mark Scott

Mark Bentley

Stephen Highley

Paul Hamilton

Will David

Allan Rich

Biographical details of the Directors at the date of this report are set out on pages 92 to 93.

DIRECTORS’ INTERESTS IN SHARES AND OPTIONS

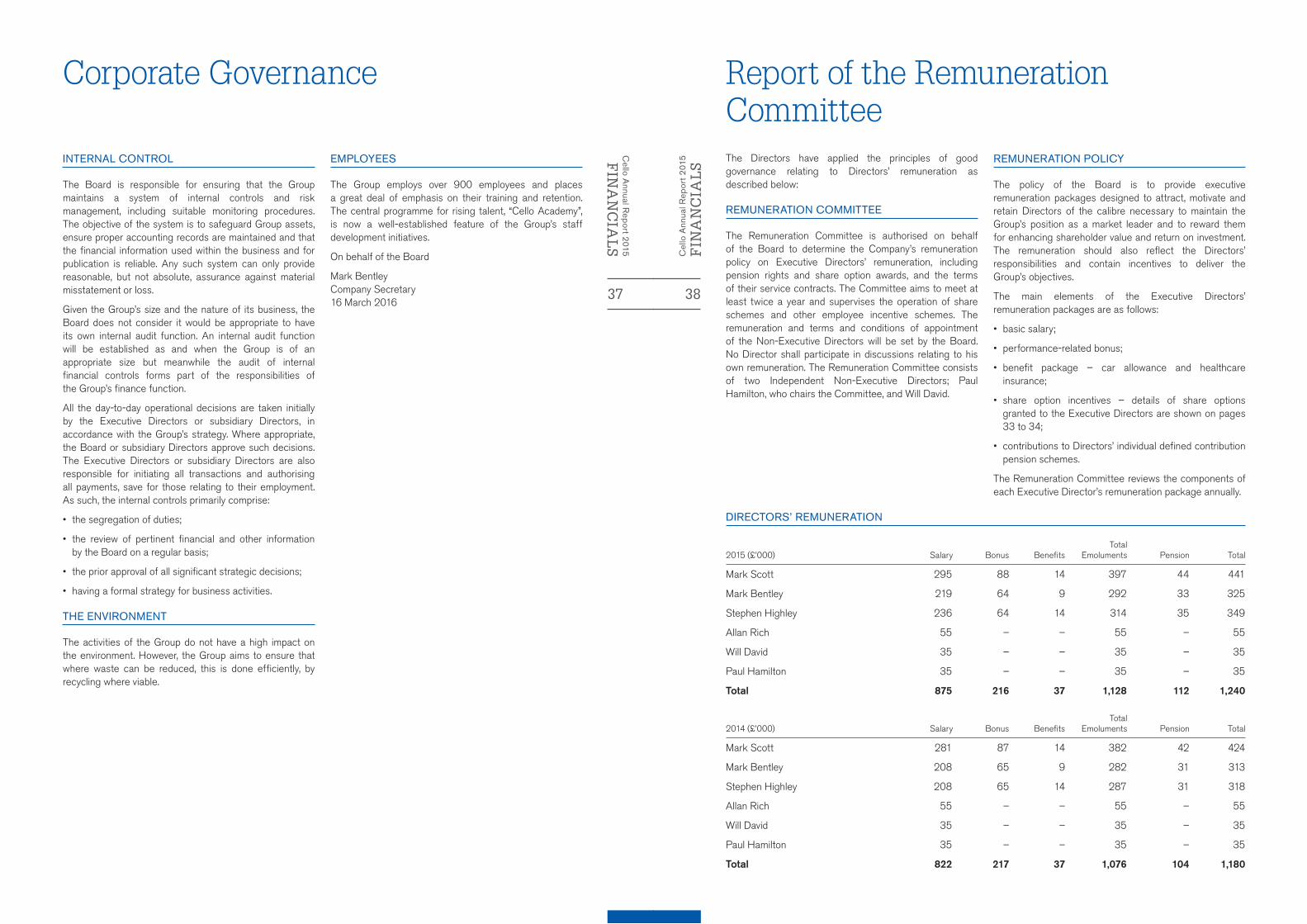

Directors’ interests in the shares of the Company were as follows:

Number of ordinary shares of 10p each Number of ordinary shares of 10p each At 31 December 2015 At 31 December 2014

Mark Scott 964,379 964,379

Mark Bentley 285,479 285,479

Stephen Highley 2,046,889 2,046,889

Paul Hamilton 50,000 50,000

Will David 15,000 15,000

Allan Rich 977,785 977,785

Under the rules of the EMI Share Option Scheme (the “EMI Scheme”), the Unapproved Share Option Scheme 2004 (the “Unapproved Scheme 2004”), the PSP Option Scheme 2010 (the “PSP 2010”) and the Approved Share Option Plan 2009 (the “Approved Plan 2009”), the Executive Directors have been granted an interest in options over ordinary shares of 10p each as follows:

At 1 January 2015

Granted during the

year

Exercised during

the year

Lapsed during

the year

At 31 December

2015

Exercise price

(pence)

Earliest exercise

date Expiry date

Mark Scott

PSP 2010 430,000 – – – 430,000 10.00 June 2013 June 2020

PSP 2010 170,000 – – – 170,000 10.00 June 2014 June 2021

PSP 2010 170,000 – – – 170,000 10.00 July 2015 July 2022

PSP 2010 210,000 – – – 210,000 10.00 July 2016 July 2023

PSP 2010 120,000 – – – 120,000 10.00 June 2017 June 2024

Approved Plan 2009 72,000 – – – 72,000 31.50 June 2013 June 2020

Total Mark Scott 1,172,000 – – – 1,172,000

34

Cel

lo A

nnua

l Rep

ort 2

015

FIN

AN

CIA

LS

Directors’ Report

At 1 January 2015

Granted during the

year

Exercised during

the year

Lapsed during

the year

At 31 December

2015

Exercise price

(pence)

Earliest exercise

date Expiry date

Mark Bentley

EMI Scheme 81,633 – – (81,633) – 122.50 June 2005 June 2015

Unapproved Scheme 2004 81,633 – – (81,633) – 122.50 June 2005 June 2015

PSP 2010 130,000 – – – 130,000 10.00 July 2015 July 2022

PSP 2010 165,000 – – – 165,000 10.00 July 2016 July 2023

PSP 2010 90,000 – – – 90,000 10.00 June 2017 June 2024

Total Mark Bentley 548,266 – – (163,266) 385,000

Stephen Highley

PSP 2010 20,000 – – – 20,000 10.00 July 2015 July 2022

PSP 2010 100,000 – – – 100,000 10.00 July 2016 July 2023

PSP 2010 50,000 – – – 50,000 10.00 June 2017 June 2024

Approved Plan 2009 30,000 – – – 30,000 33.25 July 2015 July 2022

Total Stephen Highley 200,000 – – – 200,000

There were no changes in Directors’ interests between the year end and the date of signing the Group’s accounts.

RESEARCH AND DEVELOPMENT ACTIVITIES

During the year the Group spent £366,000 (2014: £374,000) on the development of new software products which are expected to generate economic benefits in the future. These amounts were capitalised as intangible assets. £373,000 (2014: £309,000) of amortisation on research and development expenditure was charged to the income statement during the year.

DIRECTORS’ THIRD PARTY INDEMNITY PROVISIONS

A qualifying third-party indemnity provision was in place for Directors throughout the year and at the date of approval of the financial statements.

EMPLOYEES

It is the Company’s policy not to discriminate between employees or potential employees on any grounds. Full and fair consideration is given to the recruitment, training and promotion of disabled people and, should staff become disabled during the course of their employment, efforts are made to provide appropriate re-training. The Company places enormous importance on the

contributions of its employees and aims to keep them informed of developments in the Company through a combination of meetings and electronic communication.

TREASURY SHARES

The total number of shares in treasury at 31 December 2015 was 453,000 (2014: 453,000), which represents 0.53% (2014: 0.53%) of the issued share capital. The purpose of the treasury shares is to satisfy future earn out payments and/or share option awards.

SUBSTANTIAL SHAREHOLDINGS