Annual report 2006

195

CONSOLIDATED FINANCIAL STATEMENTS, STATUTORY FINANCIAL STATEMENTS AND ANNUAL REPORT

-

Upload

archivio-documenti -

Category

Documents

-

view

219 -

download

4

description

2006 CONSOLIDATED FINANCIAL STATEMENTS, STATUTORY FINANCIAL STATEMENTS AND ANNUAL REPORT

Transcript of Annual report 2006

CONSOLIDATED FINANCIAL STATEMENTS,

STATUTORY FINANCIAL STATEMENTS

AND ANNUAL REPORT

CIR S.p.A

. • CO

NSO

LIDATED

FINA

NC

IAL STATEM

ENTS, STATU

TORY FIN

AN

CIA

L STATEMEN

TS AN

D A

NN

UA

L REPOR T • FIN

AN

CIA

L YEAR 2006

C O N T E N T S

ADMINISTRATIVE BODIES 4

LETTER TO THE SHAREHOLDERS 7

MANAGEMENT REPORT 91. PERFOMANCE OF THE GROUP 142. PERFORMANCE OF THE PARENT COMPANY 183. CHART RECONCILING THE FIGURES OF THE PARENT COMPANY WITH THOSE OF THE

CONSOLIDATED FINANCIAL STATEMENTS 194. PERFORMANCE OF THE VARIOUS BUSINESS SECTORS 215. OTHER ACTIVITIES 276. SIGNIFICANT EVENTS WHICH OCCURRED AFTER THE CLOSE OF THE YEAR 297. OTHER INFORMATION 308. PROPOSED ALLOCATION OF NET INCOME FOR THE YEAR 33

CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31 20061. BALANCE SHEET 362. INCOME STATEMENT 373. CASH FLOW STATEMENT 384. STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY 395. EXPLANATORY NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 41

CONSOLIDATED FINANCIAL STATEMENTS OF DIRECTLY CONTROLLED SUBSIDIARIES 93

STATUTORY FINANCIAL STATEMENTS OF THE PARENT COMPANY AS OF DECEMBER 31 20061. BALANCE SHEET 1042. INCOME STATEMENT 1053. CASH FLOW STATEMENT 1064. STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY 1075. EXPLANATORY NOTES TO THE FINANCIAL STATEMENTS 109

FINANCIAL STATEMENTS OF DIRECTLY CONTROLLED SUBSIDIARIES 145

LIST OF INVESTMENTS AT DECEMBER 31 2006 171

REPORT OF THE BOARD OF STATUTORY AUDITORS 179

REPORT OF THE INDEPENDENT AUDITORS 187

0860_CIR_2006 COVER+INDICE.qxd 19-06-2007 9:30 Pagina 1

CIR S.p.A

. • CO

NSO

LIDATED

FINA

NC

IAL STATEM

ENTS, STATU

TORY FIN

AN

CIA

L STATEMEN

TS AN

D A

NN

UA

L REPOR T • FIN

AN

CIA

L YEAR 2006

C O N T E N T S

ADMINISTRATIVE BODIES 4

LETTER TO THE SHAREHOLDERS 7

MANAGEMENT REPORT 91. PERFOMANCE OF THE GROUP 142. PERFORMANCE OF THE PARENT COMPANY 183. CHART RECONCILING THE FIGURES OF THE PARENT COMPANY WITH THOSE OF THE

CONSOLIDATED FINANCIAL STATEMENTS 194. PERFORMANCE OF THE VARIOUS BUSINESS SECTORS 215. OTHER ACTIVITIES 276. SIGNIFICANT EVENTS WHICH OCCURRED AFTER THE CLOSE OF THE YEAR 297. OTHER INFORMATION 308. PROPOSED ALLOCATION OF NET INCOME FOR THE YEAR 33

CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31 20061. BALANCE SHEET 362. INCOME STATEMENT 373. CASH FLOW STATEMENT 384. STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY 395. EXPLANATORY NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 41

CONSOLIDATED FINANCIAL STATEMENTS OF DIRECTLY CONTROLLED SUBSIDIARIES 93

STATUTORY FINANCIAL STATEMENTS OF THE PARENT COMPANY AS OF DECEMBER 31 20061. BALANCE SHEET 1042. INCOME STATEMENT 1053. CASH FLOW STATEMENT 1064. STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY 1075. EXPLANATORY NOTES TO THE FINANCIAL STATEMENTS 109

FINANCIAL STATEMENTS OF DIRECTLY CONTROLLED SUBSIDIARIES 145

LIST OF INVESTMENTS AT DECEMBER 31 2006 171

REPORT OF THE BOARD OF STATUTORY AUDITORS 179

REPORT OF THE INDEPENDENT AUDITORS 187

0860_CIR_2006 COVER+INDICE.qxd 19-06-2007 9:30 Pagina 1

COMPAGNIE INDUSTRIALI RIUNITE

Limited-liability corporation - Share capital € 391,688,733.50 - Registered Office: Strada Volpiano, 53 - 10040 Leinì (Turin) - www.cirgroup.itR.E.A. n. 3933 - Turin Company Register / Fiscale Code / VAT no. 00519120018Company subject to the management and coordination action of COFIDE S.p.A.

Head Office: Via Ciovassino, 1 - 20121 Milan - Tel. +39 02 72270.1Office in Rome: Via del Tritone, 169 - 00187 Rome - Tel. +39 06 692055.1

4

BOARD OF DIRECTORS

Chairman CARLO DE BENEDETTI (1) (5)

Chief Executive Officer RODOLFO DE BENEDETTI (2) and General Manager

Directors GIAMPIO BRACCHI FRANCO DEBENEDETTI PIERLUIGI FERRERO (3) GIOVANNI GERMANO (5) FRANCO GIRARD (3) PAOLO MANCINELLI (6) (7) LUCA PARAVICINI CRESPI (6) CLAUDIO RECCHI (6) (7) MASSIMO SEGRE (4)

GUIDO TABELLINI (8) UMBERTO ZANNI (5)

Secretary to the Board FRANCA SEGRE

BOARD OF STATUTORY AUDITORS

Chairman PIETRO MANZONETTO

Statutory Auditors LUIGI NANI RICCARDO ZINGALES

Reserve Auditors MARCO REBOA GIANLUCA PONZELLINI LUIGI MACCHIORLATTI VIGNAT

INDEPENDENT AUDITORS

PRICEWATERHOUSECOOPERS S.p.A.

Notice pursuant to the recommendation contained in Consob Circular no. DAC/RM/97001574 of February 20 1997:

(1) Power to sign all documents relating to ordinary and extraordinary administration with single signature except for those reserved by law to the Board of Directors (2) Power to sign all documents relating to ordinary administration with single signature (3) Power to sign all documents specified in mandate with joint signature (4) Power to sign all documents specified in mandate with single signature (5) Member of the Compensation Committee (6) Member of the Internal Control Committee (7) Member of the Surveillance Body (8) Lead Independent Director

5

CIR S.p.A. 101st Year of Business

ANNUAL GENERAL MEETING OF SHAREHOLDERS Turin, April 26 2007, 1st call Turin, April 27 2007, 2nd call

NOTICE OF THE ORDINARY AND EXTRAORDINARY ANNUAL GENERAL MEETING OF SHAREHOLDERS

All Shareholders are invited to attend the Ordinary and Extraordinary Meeting of the Shareholders of the Company to be held in the Centro Congressi dell’Unione Industriale di Torino, in Turin - Via Fanti 17, on April 26 2007 at 10.30 a.m., at the first call, and on April 27 2007 at the same time and place, if a second call is necessary, in order to discuss and pass resolution on the following:

AGENDA

Ordinary Session

1. Annual Report and Financial Statements as of December 31 2006 Report of the Board of Statutory Auditors.

Resolutions pertaining to the above

2. Proposal to revoke the resolution adopted on April 27 2006 authorizing the buy-back of the Company’s own shares and the disposal of the same. Proposal for a new authorization.

3. Proposal regarding the approval of the incentive program for the year 2007.

4. Proposal to amend the regulations of Stock Option Plans March 7 2000, September 13 2000 and January 30 2001.

Extraordinary Session

5. Proposal to amend the Company Bylaws partly to bring them into line with Law 262/2005 and subsequent amendments: specifically, the amendment of articles 4, 8, 9, 10, 12, 15, 16, 19 and 20 of the Bylaws. Resolutions pertaining to and resulting from the above.

Shareholders have a right to take part in the Shareholders’ Meeting provided that their intermediaries have notified their attendance, in accordance with the terms of Art. 34-bis of Consob Resolution no. 11768 and subsequent amendments and additions. at least two working prior to the meeting. Any holders of shares that have not yet been dematerialized should present their share certificates to an authorized intermediary for input into the centralized clearing system in electronic form, in accordance with the provisions of Article 51 of Consob Resolution no. 11768 and subsequent amendments and additions, and should request that notification as above be sent within the required time limit. As from April 11 2007 Shareholders may obtain a copy of the documentation relating to the items on the Agenda from the Company offices or from Borsa Italiana S.p.A.. The Financial Statements of the Company as of December 31 2006 and the Consolidated Financial Statements of the Group as of the same date will be available as from March 30 2007 from the Company offices or from Borsa Italiana S.p.A..

THE BOARD OF DIRECTORS

Notice of this meeting was published in the newspapers: "Il Sole-24 Ore" and "la Repubblica"of March 24 2007

7

LETTER TO OUR SHAREHOLDERS

Dear Shareholders,

In November 2006 we celebrated the first thirty years of CIR. Thirty years of building and promoting in CIR and its subsidiaries that which today is recognized as “our” Business Culture, which considers human capital as the most important factor to guarantee lasting success in any business activity. The spirit and values that underpinned the company when it was established are still valid today and are a firm point of reference for all those who have worked with us and those who work with us today.

Thirty years in which we have continued to project ourselves into the future and anticipate some of the great evolutionary trends of industry and the economy, always selecting new investment opportunities with the aim of helping to create fresh value for our shareholders.

The ever faster evolution of the environment surrounding us compels us to adapt our organization and our positioning continually but we never distort their nature. The main objective of our role in allocating investment capital has always been to continue to create value and this we do by defining strategies and checking that business plans are being implemented, in conjunction with the managers of the operating companies. Today we can say that we have completed our transformation from a traditional holding company into a modern Group able to create and sustain new businesses in high-growth sectors following an investment logic of creating deep value in the medium-long term.

Towards our shareholders we take full responsibility for the decisions we make, some big and some small, and we are entirely answerable for the credibility of our business plans and the objectives that we set ourselves. We are committed to achieving successful results so that over time we can build up and strengthen the relationship of trust between CIR and its Stakeholders.

Today CIR holds a portfolio of assets balanced between companies operating in mature business sectors with consolidated positions in the market and good profitability, and businesses that have started up more recently, are interesting opportunities for allocation of capital, have promising growth prospects but with profitability that has not yet reached satisfactory levels due to the relative immaturity of the business.

Every company in our Group has a business plan agreed on with those who are directly responsible for its management and the prerogatives of top management of the investee companies are respected in every way. It is an essential condition if we too are to fulfil the expectations of our shareholders that these business plans contribute to the creation of value in the medium-long term in a realistic and credible way.

We operate in three broad business sectors: Energy (Sorgenia), Media (Espresso), and Automotive components (Sogefi), plus the Healthcare sector, which has been developed more recently, and a new area of investment which is Innovative Finance (Jupiter and Oakwood).

During 2006 the performance of our subsidiaries was very satisfactory and in some cases was better than we had expected.

In particular Sorgenia, which has become our principal investment, has been continuing its expansion in the power generating business: the new Termoli plant has started operating to capacity and work has begun on the construction of the Modugno plant. Recently the new business plan for 2007-2010 was approved, involving further expansion with the construction of new plants with particular attention devoted to those with a low impact on the environment and those using renewable sources. The Espresso Group has confirmed its position both as top newspaper and top private radio broadcaster with good levels of profitability. Sogefi, despite operating in an unfavourable market environment, has again confirmed its leadership in the filter and suspension components sectors and has improved its net profitability for the fifth year running. The acquisition of Anni Azzurri by HSS has enabled us to become the number one private operator in the field of care for the elderly.

Our recent acquisition of 47% of the capital of Oakwood Financial Investments has further strengthened our commitment in the innovative financial service business where our new company Jupiter Finance is already operating in the field of non-performing loans.

Investors who have given us their trust by becoming our shareholders share our medium-long term time horizon for achieving a return on their investment. Calculated in terms of average annual return, our stock has given a return of 22.1% over the last 3 years and of 20.2% over the last 10 years.

Our goal for 2007 is to pursue and give concrete support to the development of our new businesses and at the same time to strengthen our commitment to the successful rollout of the individual business plans of investee companies.

The Chairman Chief Executive Officer Carlo De Benedetti Rodolfo De Benedetti

9

MANAGEMENT REPORT ON THE PERFORMANCE OF OPERATIONS IN FINANCIAL YEAR 2006

Dear Shareholders,

In 2006 the CIR Group reported consolidated net income of € 101.1 million, up by 15.3% from € 87.7 million in 2005. Consolidated revenues came in at € 4,136.8 million, showing an increase of 22.3% from € 3,382.7 million in the previous year.

The year saw further consolidation of the growth strategies of the Group which strengthened con-siderably its presence in the utilities sector and at the end of the year made a new investment in the financial sector.

This confirms the strategy of CIR which is pursuing the objective of creating value for its share-holders in the medium-long term with the launch of new business initiatives in sectors considered to be of potential interest and through the management of its investments in businesses where it already has a presence. This strategy is carried out by constantly developing the business and con-tinually seeking to optimize profitability. In putting this strategy into practice CIR has maintained a prudent approach, following a financial policy that guarantees a balanced ratio of its own resources to those of third parties, thus maintain-ing a solid financial structure.

CIR considers that the most important factor to guarantee lasting success in the business activities in which it has invested and is continuing to invest is having human capital of a very high profes-sional level which with its capabilities, intuition and strategic vision can make a very positive con-tribution to reaching the common objective of the creation of value for the whole Group.

The current configuration of the Group includes four main business sectors: utilities (electricity and gas), media (publishing, radio and television), automotive components (filters and suspension systems) and healthcare (residences for the elderly, hospitals and rehabilitation centres).

The Group has also identified an investment opportunity in a sector considered of potential inter-est, that of non-performing loans. 2006 was the first full year of operation of Jupiter Finance, the company created at the end of 2005, with the aim of acquiring from financial institutions and managing portfolios of non-performing loans. In 2006 the company acquired over 50 portfolios

Management Report

10

for a total amount of approximately € 40 million and a nominal value of approximately € 340 mil-lion.

In January 2007, continuing to implement its strategy of expansion in businesses with a high growth potential and of value creation, the Group made an important investment - the acquisition with a prime financial institution of the standing of Merrill Lynch of joint control of the company Oakwood Financial Investments, specializing in innovative retail financial services aimed at non-conforming or non-prime clients, meaning those who do not fulfil the traditional criteria for being given loans. Oakwood currently operates through five companies: three in Britain, one in Austra-lia and one in Italy. On completion of the deal CIR invested approximately € 100 million, with a commitment to support the development of new initiatives for a further investment estimated at around € 50 million.

All the businesses described above are aimed at achieving the objective of continuing growth in the value of the investments over the medium-long term. The economic results for each period do not always reflect this growth in a linear way and a comparison over a short time frame may not be very representative, considering all the events of an extraordinary nature that can affect the re-sults from time to time.

*****

To make it easier to evaluate the profitability of the Group, the performance of 2006 is presented below through a breakdown of the economic contribution and the balance sheet structures of the operating groups and of the holding company, which contains the figures for CIR and CIR Inter-national.

As has already been mentioned, consolidated net income for 2006 came in at € 101.1 million up from € 87.7 million in 2005. The contribution of the operating groups to this result rose by € 6.9 million (+ 6.6%) from € 104.7 million in 2005 to € 111.6 million in 2006 while the contribution of the financial subsidiaries de-clined from € 16.2 million in 2005 to € 15 million in 2006.

The result of the holding company in 2006 was a negative € 25.5 million and compares with a net loss of € 33.2 million in 2005, which included non-recurring charges of € 16.1 million. Apart from overheads, this result was determined by: - Net financial charges of € 21.1 million due to the higher average cost of the gross debt com-

pared with the average return on financial investments; - Dividends, gains and losses from trading securities for € 4.3 million consisting mainly of

gains on investments in private equity funds for € 20.5 million offset by write-downs of finan-cial assets for € 16.4 million.

The results of the operating groups for financial year 2006 are illustrated below for each of the main business sectors.

In the utilities sector the Energia group adopted the new name of Sorgenia in July 2006 with the aim of giving maximum value to its positioning and to the role that it intends to take in the Italian free market for electricity and gas, defining itself as a provider sensitive to environmental issues. In 2006 the Sorgenia group was engaged in the roll-out of its industrial program which involves investment in the period up to 2010 of over € 1.8 billion in addition to the € 0.9 billion invested up to 2006. This investment will finance a significant expansion in the sector of power generation

Management Report

11

with particular attention being devoted to low environmental impact and renewable sources. In 2006 the consolidated revenues of the group rose by 56.4% reaching € 1,916.1 million thanks to the good performance of sales of both electricity and natural gas and consolidated net income reached € 56.3 million, up from € 29.1 million in the previous year (+93,5%).

In the media sector in 2006 the Espresso group reported consolidated revenues of € 1,102.6 mil-lion (+2.1% from 2005) and posted consolidated net income of € 103.6 million compared with € 116.3 million in the previous year. The rise in advertising and the good performance of circula-tion offset the decline in the sale of add-ons. Again in 2006 the daily news title la Repubblica con-firmed its ranking as number one newspaper in Italy for number of readers and the Espresso group’s radio stations confirmed their leadership in terms of audience.

The Sogefi Group, top Italian producer of automotive components, confirmed its leadership in Europe in the two sectors in which it operates: filters and suspension components. In an unfavour-able market environment due to the decline in business of several important clients, in 2006 the group confirmed sales revenues of over one billion euro (€ 1,018.6 million), while at the same time improving its net profitability for the fifth year running, posting consolidated net income of € 50.8 million, up by 13.7% from € 44.7 million in 2005. In the next few years the group plans to expand its business both in Asian markets (China, Korea and India) and in the North American market, continuing to maintain among its strategic objectives possible acquisitions in the automo-tive components sector.

During 2006 HSS – Holding Sanità e Servizi continued to develop its operations with a view to consolidating its presence in the healthcare sector. In 2006 the Group reported consolidated revenues of € 99.2 million up from € 53.8 million in 2005 (+ 84.4%). The net result was a negative € 4.4 million (due to higher financial expense and non-recurring costs for acquisitions) which compares with a net loss of € 1.4 million in 2005. In June 2006 the company HSS acquired 100% of Anni Azzurri, the company specializing in the construction and management of residences for the elderly and present in four regions with eleven residences and 1,600 beds. This deal together with other smaller acquisitions made during 2006 was an important step for-ward in the roll-out of the strategy of the HSS group which intends to develop further in the Ital-ian healthcare market through fresh acquisitions.

Apart from a breakdown by business sector of the economic and financial results of the Group, the charts on the following pages also show a breakdown of the contribution of the main subsidi-aries to the aggregate results of the holding (CIR and CIR International).

Management Report

12

BREAKDOWN OF INCOME STATEMENT BY BUSINESS SECTOR AND CONTRIBUTIONS TO THE RESULTS OF THE GROUP

(in milllions of euro)2005

CONSOLIDATED Revenues Costs of Other operating Adjustments to Amortization, Net financial Dividends, Income Income (Loss) Net income Net incomeNet income

(loss)productionncome & expense to value of depreciation and income and gains and taxes from assets (loss) Minority (loss) for the for the Group

investments write-downs expenses losses from held for interests Groupvalued at trading and disposal

equity valuationAGGREGATE of securitiesSorgenia group 1,916.1 (1,861.6) 32.6 33.0 (7.7) (8.4) 0.5 (34.8) -- (36.6) 33.1 16.8

Espresso group 1,102.6 (899.8) 0.3 1.4 (41.2) (19.0) (0.6) (39.8) -- (49.8) 54.1 59.1

Sogefi group 1,018.6 (869.8) (15.1) (0.3) (49.3) (11.0) 1.9 (21.6) -- (23.7) 29.7 26.3

HSS group 99.2 (88.4) (4.4) -- (4.1) (3.3) -- (2.9) (0.9) 1.0 (3.8) (1.1)

Other subsidiaries 0.3 (3.5) 0.7 -- (0.1) 0.7 -- 0.5 -- (0.1) (1.5) 3.6

Total operating subsidiaries 4,136.8 (3,723.1) 14.1 34.1 (102.4) (41.0) 1.8 (98.6) (0.9) (109.2) 111.6 104.7

Financial subsidiaries -- (2.2) -- -- -- (0.5) 20.9 -- -- (3.2) 15.0 16.2

Total subsidiaries 4,136.8 (3,725.3) 14.1 34.1 (102.4) (41.5) 22.7 (98.6) (0.9) (112.4) 126.6 120.9

Holding companies (CIR and CIR International)

Revenues -- -- --

Costs of production (22.1) (22.1) (20.7)

Other operating income and expense 4.8 4.8 2.8

Adjustments to the value ofinvestments valued at equity -- -- -- Amortization, depreciation and write-downs (0.5) (0.5) (0.2)

Net financial income and expense (21.1) (21.1) (13.0)

Dividends, gains and losses from trading and valuation of securities 4.3 4.3 8.7

Income taxes 9.1 9.1 5.3

Total holding companies (CIR and CIR International)before non-recurring items -- (22.1) 4.8 -- (0.5) (21.1) 4.3 9.1 (25.5) (17.1)

Non-recurring items -- -- -- -- -- -- -- -- -- (16.1)

Consolidated total for the Group 4,136.8 (3,747.4) 18.9 34.1 (102.9) (62.6) 27.0 (89.5) (0.9) (112.4) 101.1 87.7

2006

Managem

ent Report

CONSOLIDATED BALANCE SHEET FIGURES BY BUSINESS SECTOR

(in millions of euro)31.12.2005

CONSOLIDATED Fixed assets Other net Net working Net financial Total Minority Shareholders' Shareholders'non-current assets capital position shareholders' of which: shareholders' equity - Group equity - Group

AGGREGATE and liabilities equity equitySorgenia group 734.1 222.3 186.1 (596.9) (*) 545.6 293.8 251.8 220.9

Espresso group 907.0 (158.8) 87.8 (262.7) 573.3 279.6 293.7 279.5

Sogefi group 367.2 (58.2) 113.0 (126.3) 295.7 132.4 163.3 145.6

HSS group 170.7 5.0 (0.9) (110.7) 64.1 9.9 54.2 21.2

Other subsidiaries 0.3 11.7 47.6 (12.2) 47.4 4.0 43.4 27.6

Total subsidiaries 2,179.3 22.0 433.6 (1,108.8) 1,526.1 719.7 806.4 694.8

Fixed assets 103.0 103.0 103.0 81.4

Other net non-current assets and liabilities 107.3 107.3 107.3 58.3

Net working capital (14.7) (14.7) (14.7) (9.3)

Net financial position 258.2 258.2 258.2 359.8

Consolidated total - Group 2,282.3 129.3 418.9 (850.6) 1,979.9 719.7 1,260.2 1,185.0

( *) The financial position includes the free cash flow of Energia Holding S.p.A.

31.12.2006

Holding companies (CIR and CIR International)

13M

anagement Report

14 M t R t

1. PERFORMANCE OF THE GROUP

Consolidated revenues for 2006 totalled € 4,136.8 million, up from € 3,382.7 million in 2005, with a rise of € 754.1 million (+22.3%).

Consolidated revenues can be broken down by business sector as follows:

(in millions of euro) Change 2006 % 2005 % absolute %

Utilities Sorgenia Group 1,916.1 46.3 1,225.2 36.2 690.9 56.4

Media Espresso Group 1,102.6 26.7 1,079.9 31.9 22.7 2.1

Automotive components Sogefi Group 1,018.6 24.6 1,023.4 30.3 (4.8) (0.5)

Healthcare HSS Group 99.2 2.4 53.8 1.6 45.4 84.4

Other sectors 0.3 -- 0.4 -- (0.1) (25.0)

Total consolidated revenues 4,136.8 100.0 3,382.7 100.0 754.1 22.3

of which: ITALY 3,213.9 77.7 2,471.2 73.1 742.7 30.1

ABROAD 922.9 22.3 911.5 26.9 11.4 1.3

The highlights of the consolidated income statement are as follows:

(in millions of euro) 2006 % 2005 %

Revenues 4,136.8 100.0 3,382.7 100.0

Consolidated gross operating margin (EBITDA) 442.4 10.7 370.0 10.9

Consolidated operating result (EBIT) 339.5 8.2 275.1 8.1

Financial management result (35.6) (0.9) (20.5) (0.6)

Income taxes (89.5) (2.2) (64.7) (1.9)

Income (loss) from assets held for disposal (0.9) -- -- --

Net income including minority interests 213.5 5.2 189.9 5.6

Minority interests (112.4) (2.7) (102.2) (3.0)

Net result of the Group 101.1 2.4 87.7 2.6

The consolidated gross operating margin (EBITDA) in 2006 was € 442.4 million (10.7% of revenues) compared to € 370 million in 2005 (10.9% of revenues), with a rise of € 72.4 million (+ 19.6%). This result was determined mainly by the following factors:

A significant improvement of approximately € 65 million reported by the Sorgenia group, due to the development of the generating business; The continuing profitability of the Sogefi group; A reduction in the profitability of the Espresso group of around € 18 million, mainly due to the absence of paper subsidies, which were not renewed for financial year 2006.

14 Management Report

15

The consolidated operating margin (EBIT) in 2006 was a positive € 339.5 million (8.2% of revenues) up from € 275.1 million (8.1% of revenues) in 2005, with a rise of 23.4%.

The financial management result was determined by net financial expense that rose from € 48.2 million in 2005 to € 62.6 million mainly due to the rise in debt, and to dividends and net gains from trading securities for € 27 million (€ 27.7 million in 2005).

The consolidated balance sheet highlights of the CIR Group at December 31 2006, prepared according to a “managerial” format with a comparison with the same situation at December 31 2005 is as follows:

(in millions of euro) 31.12.2006 31.12.2005

Fixed assets 2,282.3 1,997.9

Other net non-current assets and liabilities 129.3 74.9

Net working capital 418.9 248.8

Net invested capital 2,830.5 2,321.6

Net financial debt (850.6) (465.2)

Total shareholders’ equity 1,979.9 1,856.4

Shareholders’ equity of the Group 1,260.2 1,185.0

Minority interests 719.7 671.4

Net invested capital at December 31 2006 amounted to € 2,830.5 million compared to € 2,321.6 million at December 31 2005, with a rise of € 508.9 million mainly due to the considerable in-vestment made during the year by the Sorgenia and HSS groups in particular.

The net financial debt position at December 31 2006 showed a balance of € 850.6 million (com-pared to € 465.2 million at December 31 2005), which was the result of the following: - a financial surplus for CIR and CIR International of € 258.2 million which compares with

€ 359.8 million at December 31 2005. The reduction of € 101.6 million which took place dur-ing the year was mainly due to disbursements for the buyback of own shares and for invest-ment in private equity funds and in shareholdings for approximately € 119 million, only par-tially offset by the positive balance of € 14 million between dividends received and those paid out;

- total debt of the operating groups of € 1,108.8 million, up from € 825 million at December 31 2005. The increase of € 283.8 million was mainly due to the investments made by the Sorgenia group for the construction of new power stations and to the acquisition of Anni Azzurri by the HSS group.

Total shareholders’ equity at December 31 2006 stood at € 1,979.9 million compared with € 1,856.4 million at December 31 2005, with a rise of € 123.5 million after the distribution of € 37.5 million of dividends by CIR and a total of € 53.3 million by the subsidiaries to their minor-ity shareholders.

The shareholders’ equity of the Group rose from € 1,185 million at December 31 2005 to € 1,260.2 million at December 31 2006, with a net rise of € 75.2 million.

Minority interests rose from € 671.4 million at December 31 2005 to € 719.7 million at Decem-ber 31 2006, with a rise of € 48.3 million.

Management Report

16

The net financial debt and shareholders’ equity figures at December 31 2006 include € 127.1 mil-lion resulting from the fair value adjustment of available-for-sale securities, which are held mainly by the company Medinvest. In fact the accounting treatment of Medinvest involves recognizing any changes in the fair value of the funds directly to shareholders’ equity. The total net increase during 2006, excluding foreign exchange differences, was € 20.7 million compared to € 13.6 mil-lion in 2005. Since inception (April 1994) performance has been particularly satisfactory up to and including 2006, giving the portfolio a weighted average annual return in dollar terms of 9.7%. In 2006 too, performance gave a positive return, net of commissions, of 11.3%.

The evolution of consolidated shareholders’ equity is given in the Explanatory Notes to the Fi-nancial Statements.

The consolidated cash flow statement for 2006, prepared according to a “managerial” format which, unlike the format used in the statements attached, shows the changes in net financial posi-tion instead of the changes in cash and cash equivalents, and can be broken down as follows:

(in millions of euro) 2006 2005

SOURCES OF FUNDS

Net income for the period including minority interests 213.5 189.9

Amortization, depreciation and write-downs and other non-monetary changes 109.3 79.4

Self-financing 322.8 269.3

Change in working capital (174.0) (89.9)

CASH FLOW GENERATED BY CURRENT OPERATIONS 148.8 179.4

Capital increases 10.4 26.0

TOTAL SOURCES 159.2 205.4

APPLICATIONS

Net investments in fixed assets (434.5) (443.9)

Buy-back of own shares (15.6) (35.9)

Payment of dividends (90.8) (75.9)

Other changes (3.7) (39.4)

TOTAL APPLICATIONS OF FUNDS (544.6) (595.1)

FINANCIAL SURPLUS (DEFICIT) (385.4) (389.7)

NET FINANCIAL POSITION AT THE BEGINNING OF THE PERIOD (465.2) (75.5)

NET FINANCIAL POSITION AT THE END OF THE PERIOD (850.6) (465.2)

The composition of the net financial debt figure, given in the Explanatory Notes to the Financial Statements, includes the following items: the cash and cash equivalents, securities, financial re-ceivables and available-for-sale financial assets (including the hedge funds held by Medinvest) classified as current assets, net of bank liabilities, borrowings and bonds.

Management Report

17

Net financial debt rose from € 465.2 million at the start of the year to € 850.6 million at December 31 2006. The change is mainly attributable to the investment flows to the Sorgenia group and the HSS group in particular.

Self-financing rose by over 20% compared with last year and was partly absorbed by the change in working capital which rose mainly because of the higher turnover of the Sorgenia group.

Also during the year dividends were paid out for € 90.8 million, shares were bought back for € 15.6 million and other “applications” were made for € 3.7 millions.

At December 31 2006 the Group had 11,102 employees.

Management Report

18

2. PERFORMANCE OF THE PARENT COMPANY

The parent company CIR S.p.A. closed financial year 2006 with net income of € 36.7 million (compared with € 4.8 million in 2005 which was penalized for € 16.1 million by tax charges relat-ing to prior periods). Shareholders’ equity at December 31 2006 stood at € 940.7 million compared with € 953.2 mil-lion at December 31 2005.

The key income statement figures of CIR S.p.A. for 2006, with a comparison with those of 2005, are as follows:

(in millions of euro) 2006 2005

Net operating costs (12.5) (12.3)

Other operating costs and amortization (2.3) (1.8)

Financial management result 42.4 29.7

Result before taxes and non-recurring items 27.6 15.6

Taxes from prior periods -- (16.1)

Income taxes 9.1 5.3

Net income 36.7 4.8

Net operating costs for 2006, which amounted to € 12.5 million (€ 12.3 million in 2005), include charges resulting from the IAS/IFRS treatment of stock option plans for € 2.2 million. This com-pares with € 5.7 million in 2005 (of which € 3.8 million referred to extraordinary stock option plans).Other operating costs amounted to € 2.3 million and compare with € 1.8 million in 2005.

The financial management result includes the dividends of subsidiaries, which totalled € 61.1 mil-lion in 2006 compared to € 42.8 million in 2005.

Lastly, 2006 benefited from a positive net tax position of € 9.1 million, compared with € 5.3 mil-lion in 2005, as a result taking part in the group fiscal consolidation as from 2004.

Management Report

19

The key balance sheet figures of CIR S.p.A. at December 31 2006, compared with the situation at December 31 2005, is as follows:

(in millions of euro) 31.12.2006 31.12.2005

Fixed assets 966.7 917.6

Other net non-current assets and liabilities (0.1) 0.0

Net working capital 42.3 15.6

Net invested capital 1,008.9 933.2

Net financial position (68.2) 20.0

Shareholders’ equity 940.7 953.2

The net financial position at December 31 2006 was a position of net debt of € 68.2 million which compares with a net financial surplus of € 20 million at December 31 2005. The change of € 88.2 million was mainly due to an investment in own shares for approximately € 16 million, sharehold-ings for € 47 million, loans made to subsidiaries for approximately € 29 million, net dividends re-ceived for € 23 million and operating costs for € 8 million.

The decrease in shareholders ‘equity from € 953.2 million at December 31 2005 to € 940.7 mil-lion at December 31 2006 was mainly caused by the distribution of dividends for € 37.5 million and the effects of the IAS/IFRS treatment of own share buybacks which were only partially offset by the net income for the period. At December 31 2006 there were 34,094,000 own shares held in the portfolio, equal to 4.37% of capital, for a total value of € 76.9 million, compared with 27,216,642 at December 31 2005.

3. CHART RECONCILING THE ACCOUNTING FIGURES OF THE PARENT COM-PANY AND THOSE OF THE CONSOLIDATED ACCOUNTS

The following chart shows the reconciliation of the results for the year and the shareholders’ eq-uity of the Group with the figures of the parent company.

(in thousands of euro) Shareholders’ equity 31.12.2006

Net result2006

Figures of the parent company CIR S.p.A. 940,738 36,697

- Dividends from companies included in consolidation (61,046) (61,046)

- Reversal of valuations and cover of losses on investments in companies included in the consolidation 1,193 1,193

- Net contribution of consolidated companies 325,534 126,334

- Difference between carrying value of subsidiaries and portion of consolidated shareholders’ equity, net of contributions 55,794 --

- Other consolidation adjustments (2,058) (2,058)

Consolidated figures, Group’s share 1,260,155 101,120

Management Report

(*) Percentage of indirect control through Energia Holding

20

MAIN EQUITY INVESTMENTS OF THE GROUPAS OF DECEMBER 31 2006

Healthcare

Automotive ComponentsSOGEFI58.4%

Media

HSS85.3%

UtilitiesSORGENIA58.2% (*)

ESPRESSO52.2%

Management Report

21

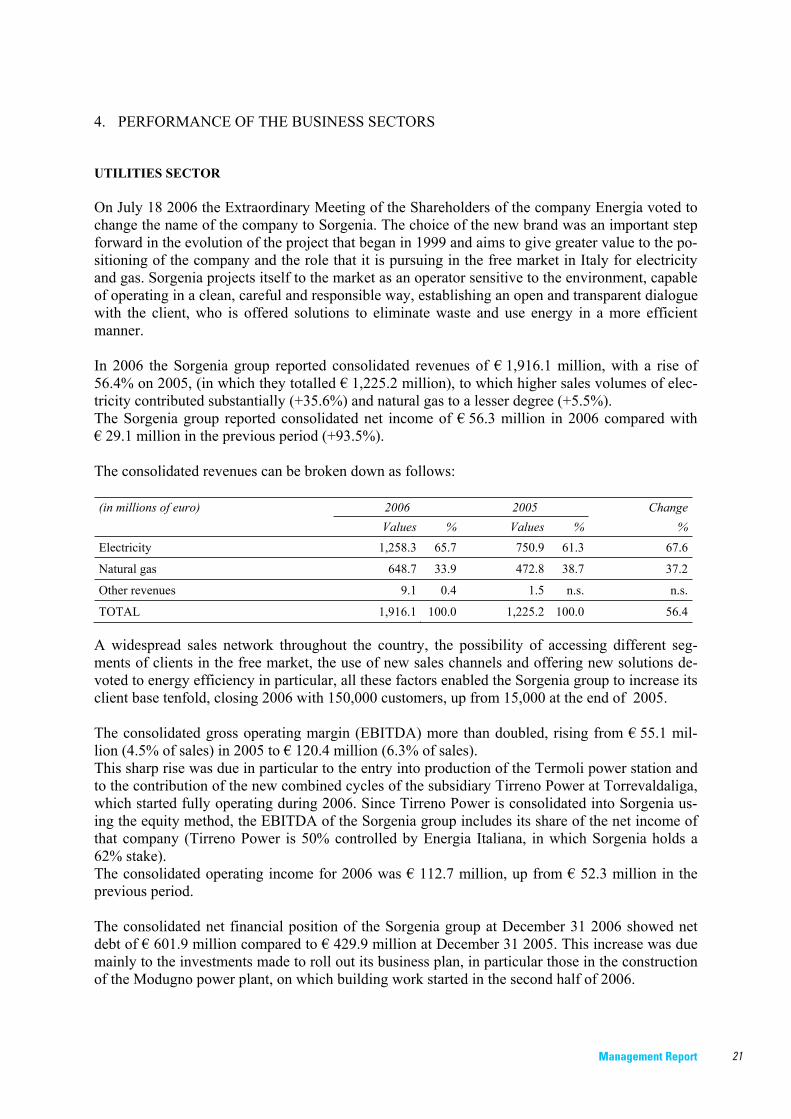

4. PERFORMANCE OF THE BUSINESS SECTORS

UTILITIES SECTOR

On July 18 2006 the Extraordinary Meeting of the Shareholders of the company Energia voted to change the name of the company to Sorgenia. The choice of the new brand was an important step forward in the evolution of the project that began in 1999 and aims to give greater value to the po-sitioning of the company and the role that it is pursuing in the free market in Italy for electricity and gas. Sorgenia projects itself to the market as an operator sensitive to the environment, capable of operating in a clean, careful and responsible way, establishing an open and transparent dialogue with the client, who is offered solutions to eliminate waste and use energy in a more efficient manner.

In 2006 the Sorgenia group reported consolidated revenues of € 1,916.1 million, with a rise of 56.4% on 2005, (in which they totalled € 1,225.2 million), to which higher sales volumes of elec-tricity contributed substantially (+35.6%) and natural gas to a lesser degree (+5.5%). The Sorgenia group reported consolidated net income of € 56.3 million in 2006 compared with € 29.1 million in the previous period (+93.5%).

The consolidated revenues can be broken down as follows:

(in millions of euro) 2006 2005 ChangeValues % Values % %

Electricity 1,258.3 65.7 750.9 61.3 67.6

Natural gas 648.7 33.9 472.8 38.7 37.2

Other revenues 9.1 0.4 1.5 n.s. n.s.

TOTAL 1,916.1 100.0 1,225.2 100.0 56.4

A widespread sales network throughout the country, the possibility of accessing different seg-ments of clients in the free market, the use of new sales channels and offering new solutions de-voted to energy efficiency in particular, all these factors enabled the Sorgenia group to increase its client base tenfold, closing 2006 with 150,000 customers, up from 15,000 at the end of 2005.

The consolidated gross operating margin (EBITDA) more than doubled, rising from € 55.1 mil-lion (4.5% of sales) in 2005 to € 120.4 million (6.3% of sales). This sharp rise was due in particular to the entry into production of the Termoli power station and to the contribution of the new combined cycles of the subsidiary Tirreno Power at Torrevaldaliga, which started fully operating during 2006. Since Tirreno Power is consolidated into Sorgenia us-ing the equity method, the EBITDA of the Sorgenia group includes its share of the net income of that company (Tirreno Power is 50% controlled by Energia Italiana, in which Sorgenia holds a 62% stake). The consolidated operating income for 2006 was € 112.7 million, up from € 52.3 million in the previous period.

The consolidated net financial position of the Sorgenia group at December 31 2006 showed net debt of € 601.9 million compared to € 429.9 million at December 31 2005. This increase was due mainly to the investments made to roll out its business plan, in particular those in the construction of the Modugno power plant, on which building work started in the second half of 2006.

Management Report

22

At December 31 2006 the group had 208 employees compared with 148 at December 31 2005.

The Board of Directors of Sorgenia S.p.A., which met on February 26 2007, proposed distributing dividends for a total of € 9.3 million, against € 8 million the previous year, corresponding to a dividend of € 0.0115 per share up from € 0.010 in 2005.

The Sorgenia group is engaged in the roll-out of its industrial plan which involves significant ex-pansion in the electricity generating sector, with particular attention being devoted to sources with a low environmental impact and to renewables. The industrial objectives of the program include the construction of four combined cycle power plants fired by natural gas, each with an output of 770 MW; the completion of the repowering of the power plants of the subsidiary Tirreno Power; the construction of 450 MW of wind plant and investment in the photovoltaic solar sector. These projects will require investment going forward to 2010 for over € 1.8 billion. The second half of 2006 saw the Termoli (Cb) power plant enter full operation. This is the first of the four power plants planned and work continued on the construction of the Modugno plant in Puglia. In September the authorization process was completed for the Aprilia plant (Lazio), with the favourable opinion expressed by the Service Conference and the issue of the final authoriza-tion decree on October 2 2006 by the Ministry of Economic Development. This authorization joins the one already obtained for the Bertonico-Turano Lodigiano plant (Lombardy).

As far as the Tirreno Power repowering is concerned, the conversion to a 760 MW combined cy-cle of a section of the Vado Ligure plant is going ahead according to schedule and is expected to start operating during 2007. A new 380 MW combined cycle module is also being constructed at Napoli Levante and this one should start operating in 2008.In 2006 Tirreno Power reported revenues of € 988.4 million, up by 27.9% from € 772.7 in 2005, with a net production volume of approximately 11.6 TWh (10.9 TWh in 2005). The gross operat-ing margin rose by 38.9%, coming in at € 229 million compared to € 164.9 million in 2005. Net income more than quadrupled, rising from € 15.4 million in 2005 to € 57.4 million in 2006.

As already indicated, Sorgenia is also developing generating projects from renewable sources, with particular attention being devoted to the construction of wind and photovoltaic solar plants. Soluxia, its wholly owned subsidiary set up to design and build photovoltaic plants, has already obtained from the GSE (Electricity Services Management), admission to incentive feed-in tariffs for 15 new photovoltaic plants each with an output of 1 MW, located in various regions of the South of Italy, with a total installed capacity of approximately 15 MW. On the subject of wind en-ergy, Sorgenia has obtained authorization for projects with a total output of 62 MW – Minervino Murge (Bari) for 18 MW, Castelnuovo di Conza (Salerno) for 10 MW and San Gregorio Magno (Salerno) for 34 MW.

MEDIA SECTOR

The Espresso group closed 2006 with consolidated revenues of € 1,102.6 million up from € 1,079.9 million in 2005 (+2.1%).

Consolidated net income came in at € 103.6 million compared to € 116.3 million in the previous year and benefited this year again (for the last time) from the recognition of deferred tax assets re-lating to the previous losses of the subsidiary Elemedia.

Management Report

23

The revenues of the group can be broken down as follows:

(in millions of euro) 2006 2005 ChangeValues % Values % %

Circulation 458.9 41.6 466.6 43.2 (1.6)

Advertising 615.8 55.9 585.7 54.2 5.1

Other revenues 27.9 2.5 27.6 2.6 1.1

TOTAL 1,102.6 100.0 1,079.9 100.0 2.1

Consolidated advertising revenues, which rose by 5.1%, benefited also from the competitive ad-vantage that the Espresso group derives from being the only company in Italy in the media sector to be able to offer advertisers multimedia advertising, with a portfolio of published titles that are all leaders in their respective markets.

Circulation revenues declined by 1.6% compared with 2005 on account of lower sales of optional products (22 million printed and multimedia add-ons in 2006 compared with almost 26 million in 2005).The negative impact of strikes on revenues was however offset by the good performance of the circulation of la Repubblica, (628 thousand average copies per day) and L’espresso (395 thousand copies per week), and by the rise in price of certain local papers to one euro. This change did not produce any further negative effects on the performance of circulation which reached a total of 452 thousand average copies per issue.

All the media of the group performed well even in terms of readers and traffic. For the fifth time running La Repubblica confirmed its ranking as the most widely read newspaper in Italy with over 3 million readers and the trend is a rising one. The readers of L’espresso are more than 2.3 million and the local papers clocked up 3.2 million readers. In December the group’s internet website network reached 9.5 million unique users and 339 mil-lion page views. The number of visitors to Repubblica.it rose during the year by 45% reaching 6.7 million, more than one third of all Italian users of the web.

The listening figures of the radio stations were also positive, with an overall rise of 4% on 2005: Radio Deejay confirmed its position as the number one private broadcaster in Italy on an average day with 5.8 million listeners which rise to 13.7 million over the whole week; the audience of Ra-dio Capital is now over 2 million people on an average day and 6.6 million over a seven day pe-riod, while m2o now clocks up 1.1 million listeners per day and 2.9 million per week (Audiradio). These listening figures also rewarded the music television channel All Music which in October, according to research carried out by IPSOS, had over 2.8 million viewers in the 15-34 age group, claiming the position as the young people’s broadcaster with the highest audience increase over the last few months.

Consolidated operating income declined from € 177.5 million in 2005 to € 163.3 million in 2006. If the effect of subsidized paper purchases is netted out of the 2005 figures, the operating result for that year would be € 156.9 million giving a rise of 0.8% in 2006 with a ratio to sales stable at over 14%, despite the decline in optional products, the margins of which were still significant but reduced by the declining trend of the market.

Management Report

24

The consolidated net financial position at December 31 2006 showed net debt of € 262.7 million, up from € 252.6 million at December 31 2005 thanks to the good performance of operating cash flow (€ 121.9 million).

Consolidated shareholders’ equity rose from € 550 million at December 31 2005 to € 562.8 mil-lion at December 31 2006.

At December 31 2006 there were 3,384 employees on the group payrolls, down by 13 from 3,397 at December 31 2005.

The Board of Directors of the parent company Gruppo Editoriale L’Espresso, which met on Feb-ruary 21 2007, proposed the distribution of a dividend of € 0.16 per share (€ 0.145 in 2005).

National newspapers Revenues of the national daily sector totalled € 539.8 million, up from € 524 million in 2005 (+3%).The operating result of this area was € 64.9 million and compares with a result for 2005 (net of subsidies for the purchase of paper which were no longer given in 2006) of € 69.7 million with a decline of € 4.8 million due to the cost of designing and launching new titles and to the 4.5% rise in the price of paper.

Local newspapers Consolidated revenues of this sector totalled € 260.5 million, which was in line with the figure for the previous year (+0.2%). The operating result of the area declined from € 49.5 million (19% of revenues) in 2005 to € 46.7 million (17.9% of revenues) in 2006, penalized by the absence of € 2.6 million in the form of sub-sidies. Excluding these subsidies, profitability was unchanged at 18%.

PeriodicalsThe periodicals area reported revenues of € 118.1 million, down by 5.7% from € 125.2 million in 2005.The operating result was € 12.2 million, up from € 6.9 million in 2005. The ratio of operating in-come to sales rose from 9.2% last year to 10.3% in 2006, thanks mainly to the rise in advertising and to the positive contribution of optional products.

RadioIn 2006 the group radio stations increased their revenues by 3.8% from € 75.4 million in 2005 to € 78.3 million. Operating income rose from € 34.1 million in 2005 to € 34.6 million, with a ratio to sales of 44.2%.In 2006 the three broadcasters of the group invested a lot in the circulation of published content on different platforms, confirming their collaboration with the TV group All Music and strength-ening the internet business.

In the early months of this current year advertising revenues have continued to grow for all the media of the group, circulation is performing well, while optional add-ons have declined com-pared with previous years because the market is saturated and competition is becoming more and more aggressive. From the above scenario, management expects advertising revenues to grow while revenues and margins on optional products decline. Consolidated net income for the year 2007 should in any

Management Report

25

case be lower than that of 2006 since there is of no longer the benefit of any deferred tax assets relating to losses of subsidiaries in prior periods.

AUTOMOTIVE COMPONENTS SECTOR

The consolidated revenues of the Sogefi group in 2006 came in at € 1,018.6 million, substantially in line with the previous year’s figure of € 1,023.4 million, in a market environment that was not particularly favourable due to a decline in the business of several important clients. The further growth of sales volumes in South American countries largely offset the decline in revenues in the European and US markets.

Consolidated net income was € 50.8 million, up by 13.7% from € 44.7 million in 2005.

The breakdown of consolidated sales of the Sogefi group by business sector is as follows:

(in millions of euro) 2006 2005 ChangeValues % Values % %

Filters 527.2 51.7 518.5 50.7 1.7

Suspension components and precision springs 491.6 48.3 504.9 49.3 (2.6)

Intercompany elimination (0.2) -- 0.0 -- --

TOTAL 1,018.6 100.0 1,023.4 100.0 (0.5)

The profitability of industrial management actually rose in both divisions (Filters and Suspension components) despite being burdened by rises in energy prices and in the prices of components in aluminium and other alloys used in the special steels for the suspension business.

Consolidated EBITDA was € 128.5 million in 2006 (12.6% of sales), with an improvement of 1.3% from € 126.9 million (12.4% of sales) last year. The latter result was negatively impacted by industrial restructuring charges (€ 5.2 million), write-downs of fixed assets (€ 4.3 million) and non-recurring expense for paying management bonuses for results achieved in recent years (€ 2.3 million). By contrast the year 2006 benefited from capital gains of € 4 million, mainly due to the sale of a factory in Spain.

Consolidated EBIT was € 83.5 million (8.2% of sales), up by 3.1% from € 81 million (7.9% of sales) in 2005.

In 2006 the result before taxes and minority interests was € 74.9 million, up by 11.6% from € 67.1 million in 2005, thanks to lower financial expenses, higher gains from recovering withholding tax on foreign dividends in prior periods and a capital gain from the sale of a shareholding invest-ment.

At December 31 2006 the consolidated net financial position showed net debt of € 126.3 million, with an improvement of € 41 million compared with the figure of € 167.3 million at December 31 2005.

The group had 6,168 employees on its payroll at December 31 2006 compared to 6,171 at De-cember 31 2005.

Management Report

26

The Board of Directors of Sogefi, which met on February 27 2007, proposed distributing a divi-dend of € 0.20 per share (€ 0.175 in 2005).

Sales revenues of the filter division in 2006 came in at € 527.2 million, up from 518.5 million in 2005 (+1.7%). The division improved its economic results both in Europe and in South America, thanks to the good performance of sales in the aftermarket sector during the latter months of the year. EBITDA came to € 70.2 million (13.3% of sales) up from € 68.5 million (13.2% of sales) in 2005, while EBIT rose to € 51.9 million (9.8% of sales) from € 50 million (9.6% of sales) in 2005.

The suspension components division reported sales revenues of € 491.6 million in 2006, down from € 504.9 million in 2005 (-2.6%), following the decline in production volumes of French ve-hicle manufacturers. Despite this, profitability improved: EBITDA rose by 3.6% to € 63.4 million (12.9% of sales) from € 61.2 million in 2005 (12.1% of sales). EBIT reached € 37.4 million (7.6% of sales) with a rise of 8.4% from € 34.5 million (6.8% of sales) in 2005.

No change is expected this year in the main markets in which the group operates: the European market is stable, and the South American market is still growing. In the markets where there is less presence (US and China) the evolution of demand should be positive with orders from new clients. Since, however, there is likely to be more tension on the steel and energy fronts, manage-ment strategy will continue to be based on increasing efficiency and defending profit margins.

HEALTHCARE SECTOR

In 2006 the HSS group continued to develop and manage the new initiatives it has undertaken in this sector. In June a 100% acquisition was made of Anni Azzurri, the company specializing in the construction and management of residences for the elderly, which in 2005 reported consolidated sales revenues of approximately € 50 million and is present in four regions with 11 residences and a total of 1,600 beds. In the second half of 2006 there were two acquisitions – of the companies Meia (which manages four residences for the elderly in Piedmont) and Medipass, which purchases and manages ad-vanced technology in public and private hospitals. At the close of the year the company Physio-clinic, which operates in the development of competitive and amateur sports rehabilitation, was sold to minority shareholders.

In 2006 the HSS group reported revenues of € 99.2 million, up from € 53.8 million in the previous year (+84.4%). Confirming the trend already evident in the final months of 2005, in 2006 the group achieved a positive EBIT figure of € 2.3 million compared with a negative figure of € 0.7 million in 2005.

The net result was a negative € 4.4 million (compared with a net loss of € 1.4 million in 2005) and was affected by higher net financial expense (from € 0.3 million in 2005 to € 3.3 million in 2006) due to the rise in debt and to non-recurring costs for acquisitions made.

At December 31 2006 the HSS group showed net financial debt of € 110.7 million compared with a net financial surplus of € 4.2 million at December 31 2005. The change was mainly due to the acquisition of Anni Azzurri, which involved a disbursement of approximately € 60 million for the shares plus the debt taken on for some € 90 million, to other acquisitions for approximately € 25 million and to a capital increase of € 40 million.

Management Report

27

In line with the strategy followed so far, for part of the properties belonging to Anni Azzurri a preliminary contract of sale was signed in February 2007 for an amount of € 50 million and they were posted to assets held for disposal.

At December 31 2006 consolidated shareholders’ equity amounted to € 63.5 million.

The business of the HSS group is currently directed at managing four kinds of services: 1) Residences and nursing homes (RSAs), through the companies Villa Margherita, which

manages three residences, Casaverde (eight residences), Meia (five residences) and Anni Azzurri (eleven residences);

2) Psychiatric services, with the company Redancia which manages seven psychiatric care communities;

3) Rehabilitation, with the company Rehab specializing in functional recovery and rehabilita-tion;

4) Hospital management, with the company Ospedale di Suzzara (controlled by HSS) which in 2004 was awarded management of the Presidio Ospedaliero F.lli Montecchi di Suzzara (Mantua) and with the company Medipass, which manages diagnostic imaging units in pub-lic and private hospitals.

Currently the HSS group manages a total of 3,400 beds.

The employees of the group totalled 1,302 at December 31 2006.

5. OTHER ACTIVITIES

JUPITER FINANCE – This company was set up on September 2 2005 with the aim of acquiring portfolios of non-performing loans from financial institutions and managing them.The current phase of regulatory discontinuity, following the Basel2 agreements and the introduc-tion of the new international accounting standards, offers an interesting opportunity to enter a business sector with the potential for high growth, as examples of the development of this busi-ness in advanced markets demonstrate (US, Japan, UK and Germany). The company aims to become an independent industrial partner of Italian banks and businesses in the management of non-performing loans, both for bloc sales on a non-recourse basis and for pro-grams of optimization of a credit portfolio over a period of time, acting as services in the broadest sense of the term. Target segments include: distressed bank loans (loan agreements), problem securitized loans, con-sumer credit in arrears (credit cards and personal loans), irrecoverable receivables of industrial companies and public administrations, overdue leasing (with purchase of asset) and mortgage re-ceivables.In line with the scheduled growth plan, in 2006 more than 50 portfolios of non-performing loans were acquired from banks and consumer credit companies for an overall sum of approximately € 40 million and a gross book value of around € 340 million. During 2006 the company started collecting the receivables it had acquired using servicing com-panies. At December 31 2006 the total amount recovered was according to plan.

CIR VENTURES – At the end of 2006 the portfolio of CIR Ventures, the venture capital fund of the Group, contained investments in seven companies of which six in the United States and one in Is-rael. These companies all operate in the sector of information and communications technology. The fair value of these investments at December 31 2006 totalled 14.8 million dollars.

Management Report

28

During 2006 the stake in the Italian company Iriscube was sold to the company Reply and two new investments were made in the Californian companies Active Optical Mems, which operates in the sector of advanced components for fibre optics communication networks, and Home Ro-bots, which develops robotized devices that aid home cleaning. In December 2006 the sale was announced of the stake in Bitfone to Hewlett-Packard and the deal was successfully completed in February 2007. The management activity of the fund is still mainly directed towards supporting the companies in the portfolio and identifying opportunities for taking profit. The prospects for the evolution of the business of these companies remain cautiously optimistic within a scenario of a general improve-ment in the technology sector.

DRY PRODUCTS – The early part of 2006 saw the completion of the sale of the investment in Ric-ciarelli, the only company of the Dry Products group still operating in the sector of machinery for the food industry at a price of € 3.6 million, which was in line with its carrying value. With this transaction the CIR group has now terminated its program of gradual disinvestment from this sec-tor, which was no longer considered strategic.

INVESTMENTS IN PRIVATE EQUITY FUNDS - Through its subsidiary CIR International the CIR group holds a diversified portfolio of funds and minority private equity holdings, of which the fair value determined on the basis of the NAV provided by the various funds was approximately € 87 million at December 31 2006. Remaining commitments outstanding as of the same date amounted to € 20 million. During 2006 approximately € 17.6 million of realized gains were recognized to the accounts.Investors in this kind of fund undertake to provide asset managers with a predetermined amount. The fund managers have a limited time (approximately 5 years) to identify and make the investments following their strategy, requiring from investors the amounts they had paid in. The duration of these investment vehicles is generally limited to about 10 years and proceeds from the sale of investments are immediately distributed to the investors. The investment strategies of these funds follow various procedures, the main one being the acqui-sition of controlling shareholdings often using significant leverage. Risk on private equity investments is reduced by a process of diversification based on criteria that include, among other things, establishing a maximum amount for each individual commitment. At December 31 2006 CIR had invested in some 25 funds mainly denominated in euro and in dol-lars. The exchange rate risk on dollar investments has been hedged.

Management Report

29

6. SIGNIFICANT EVENTS WHICH OCCURRED AFTER THE CLOSE OF THE YEAR

With regard to the principal events which have taken place since December 31 2006 and the out-look for business in this current year, detailed information has already been given in the section of the report on the performance of the business sectors.

In January 2007, through its subsidiary CIR International, CIR finalized the acquisition of a 47.4% shareholding, in joint control with Merrill Lynch, in Oakwood Financial Investments, with a disbursement of approximately € 100 million and a further commitment of € 50 million. The Oakwood Group specializes in the creation, acquisition and management of retail finance companies and concentrates on the non-conforming or non-prime client sector, i.e. those clients that do not meet the traditional criteria for obtaining mortgages, consumer credit, vehicle loans and leasing solutions.Oakwood currently operates in the Australian, British and Italian markets through five companies: three of these were set up between 2001 and 2006 by management (Pepper Homeloans in Austra-lia, One World Leasing and Edeus in Britain), while controlling stakes were acquired in the other two (Ktesios in Italy and Blue Motor Finance in Britain). Details of these are as follows:

1. Pepper Homeloans, founded in 2001, based in Sydney is currently the third largest lender of residential non-conforming mortgages in Australia and to date has issued 5 securitizations;

2. One World Leasing, set up in 2003, based in Manchester UK, specializes in originating small ticket leases;

3. Ktesios, control of which was acquired during 2006, is based in Rome and is one of the lead-ing Italian distributors of salary-secured personal loans;

4. Blue Motor Finance, based in Warrington (UK), originates non-conforming auto loans. The ma-jority stake in this company was also acquired in 2006;

5. Edeus, launched in September 2006, is based in Essington (UK) and specializes in offering non-conforming residential mortgages. Edeus uses highly advanced technology that enables brokers to complete mortgages much faster than they could with traditional methods.

As far as own share deals are concerned, it should be pointed out that between January 1 2007 and today (March 13 2007) CIR bought back 2,950,000 of its own shares for a total of € 8.5 million. As of today, therefore, treasury stock held amounts to 37,044,000 equal to 4.7% of share capital.

It should also be noted that between January 1 2007 and today 2,312,800 shares have been issued in exercise of options by the beneficiaries of existing stock option plans. After this operation the share capital consisted of 782,791,867 shares with a nominal value of € 0.50 each, for a total value of € 391,395,933.50.

Management Report

30

7. OTHER INFORMATION

Information on shares held by Directors, General Managers and Statutory Auditors

The chart below gives the information required by Art. 79 of Consob Resolution no. 11971 of May 14 1999 and subsequent amendments and additions.

SHARES HELD BY DIRECTORS, STATUTORY AUDITORS AND GENERAL MANAGERS

Last name and first name Company in which shares are held Number of shares

Number of shares

Number of shares

Number of shares owned at end

Notes

owned at end bought sold of this year of previous year

DE BENEDETTI CARLO CIR S.p.A. 358,708,621 -- -- 358,708,621 (1)

DE BENEDETTI CARLO GRUPPO EDITORIALE L’ESPRESSO S.p.A. 218,826,235 1,950,000 -- 220,776,235 (2)

DE BENEDETTI CARLO SOGEFI S.p.A. 65,194,962 -- -- 65,194,962 (3)

DE BENEDETTI RODOLFO CIR S.p.A. 6,710,000 337,500 -- 7,047,500

PIASER ALBERTO CIR S.p.A. 94,000 180,000 274,000 --

DEBENEDETTI FRANCO CIR S.p.A. 375,000 -- -- 375,000

FERRERO PIERLUIGI CIR S.p.A. 315,000 100,000 65,000 350,000

FERRERO PIERLUIGI GRUPPO EDITORIALE L’ESPRESSO S.p.A. 30,000 -- -- 30,000

FERRERO PIERLUIGI SOGEFI S.p.A. 10,000 10,000 10,000 10,000

GERMANO GIOVANNI SOGEFI S.p.A. 2,012,000 -- -- 2,012,000

GERMANO GIOVANNI SOGEFI S.p.A. 1,004,312 -- -- 1,004,312 (4)

GIRARD FRANCO CIR S.p.A. 128,000 -- -- 128,000

GIRARD FRANCO SOGEFI S.p.A. -- 10,000 -- 10,000

GIRARD FRANCO GRUPPO EDITORIALE L’ESPRESSO S.p.A. -- 10,000 -- 10,000

PARAVICINI CRESPI LUCA CIR S.p.A. 333,333 -- -- 333,333

SEGRE MASSIMO GRUPPO EDITORIALE L’ESPRESSO S.p.A. 3,000 -- -- 3,000

(1) Indirectly owned through COFIDE S.p.A. (2) At December 31 2006 the shares are owned through the following subsidiaries:

CIR S.p.A. 218,825,235 ROMED S.p.A. 1,000

(3) Indirectly owned through CIR S.p.A. (4) Indirectly owned through Siria S.r.l.

Transactions with companies of the Group and related parties

During the period CIR S.p.A. provided management and strategic support services to its subsidiaries and affiliates which involved, among other things, supplying administrative and financial services, making loans, and issuing guarantees. Transactions with the controlling parent company consisted of providing services of an administrative and financial nature and being supplied with management support and communication services. The main concern of CIR and its counterparties in relation to these services is to ensure quality and a high level of efficiency of the services rendered, which derive from CIR’s specific knowledge of the businesses of the Group. Transactions between companies of the Group are settled at normal market conditions on the basis of the quality and the specific nature of the services rendered.

Management Report

31

The most significant financial transactions between CIR and its subsidiaries are analysed in detail in the Explanatory Notes particularly under the item Miscellaneous receivables, Other payables and Financial receivables with subsidiaries in the Balance Sheet and under the items Miscellaneous revenues and income, Financial expenses and Dividends in the In-come Statement.

Regarding the main equity transactions reference is made to the appropriate sections of the explanatory notes.

It should be pointed out that the CIR Group did not enter into any transactions with related parties, according to Consob’s definition, of a non-typical or unusual nature beyond nor-mal business administration or such as to have any significant impact on the economic, fi-nancial or equity situation of the Group.

The code of conduct governing transactions with related parties was defined by the Board of Directors of the Company in September 2002.

National tax consolidation

As is known, the new Income Tax Consolidation Act (TUIR) introduced the possibility for companies belonging to the same group to determine a single total income figure corre-sponding more or less to the sum of the taxable income of the various companies (parent company and subsidiaries controlled directly and/or indirectly for at least 50% according to certain requisites) and thus to calculate a single income tax figure for the income of the companies of the group. In the last few months of 2004 the Boards of Directors of 28 com-panies belonging to the Espresso, Sorgenia, Sogefi and HSS subgroups voted to take part in the “CIR Tax Consolidation”, signing a general agreement (“General Rules of the CIR Tax Consolidation”), which sets out the rights and obligations of CIR and its subsidiaries, re-sulting from their taking part in the tax consolidation. At December 31 2006 there were 26 companies taking part in the CIR tax consolidation.

Report on Corporate Governance

It should be noted that the full text of the “Annual Report on Corporate Governance” for the year 2006 was approved – in its entirety – by the Board of Directors convened to ap-prove the Financial Statements for the year ended December 31 2006.

This Report will be available to anybody who requests it, according to the conditions stipu-lated by Borsa Italiana for publishing the same. The Report will also be available on the website of the Company.

In relation to D.Lgs. 231/01, issued with the aim of bringing regulations on the subject of the administrative liability of entities into line with international agreements signed by It-aly, on March 7 2003 the Board of Directors of the Company approved the adoption of a Code of Ethics of the CIR Group, published as an attachment to the “Annual Report on Corporate Governance”, which defines the values which the Group follows in the achieve-ment of its objectives and establishes binding principles of conduct for its Directors, em-ployees and those who have a relationship with the Group. Moreover, on September 5 2003, the Board of Directors of the company approved the “Organization Model – the Or-

Management Report

32

ganizational and Management Model as defined by D.Lgs. no. 231/01”, in line with the in-structions laid down in the decree which aimed to ensure correctness and transparency in the conduct of business and corporate activities.

On April 27 2006 the Board of Directors approved an update to the Organizational and Management Model as defined by D.Lgs. no. 231/01 which was needed after law no. 62 of April 18 2005 took effect. This law amended decree 231/2001 inserting art. 25-sexties which establishes fines for offences involving the abuse of privileged information and ma-nipulation of the market.

Lastly it should be noted that the companies of the Group have complied with the provi-sions of Art. 2497-bis of the Civil Code.

Preparation of “Security Policy Document (DPS)”

D.Lgs. no. 196/03, giving instructions on the protection of personal information, stipulates that by March 31 of each year the organization responsible for the treatment of personal in-formation draw up a formal security policy document containing, among other things, ap-propriate information regarding the following: - the list of the types of treatment of personal information carried out by the organiza-

tion;- the distribution of responsibilities and tasks within the sphere of the treatment of such

information; - a description of the measures to be taken to guarantee the integrity and the availability

of the information and the protection of the areas set aside for storing it and making it accessible;

- the description of the criteria and the procedures for restoring access to the said infor-mation in the event of it being destroyed or damaged;

- the description of the criteria to be adopted in order to guarantee that the minimum measures of security are followed when the treatment of personal information is en-trusted, in conformity with the Civil Code, to someone outside the structure of the Of-ficer Responsible.

Article 26 of the Technical Rules states that the preparation or amendment of the Security Policy Document must be mentioned in the Annual Report accompanying the Financial Statements if required. The Security Policy Document was updated with the support of specialist consultants in this field who have been certified as BS7799 lead auditors by the British Standard Institute.

Other

The company CIR S.p.A. – Compagnie Industriali Riunite has its registered office in Strada Volpiano 53, Leinì (To), Italy and its operating headquarters in Via Ciovassino 1, Milan, Italy.

CIR shares, which have been quoted on the Milan Stock Exchange since 1973, since 2004 have been traded on the Blue-chip segment (Reuter code: CIRX.MI, Bloomberg code CIR IM).

This Annual Report for the period January 1 – December 31 2006 was approved by the Board of Directors on March 13 2007.

Management Report

33

PROPOSED ALLOCATION OF NET INCOME FOR THE YEAR

Dear Shareholders,

The Financial Statements for the year ended December 31 2006 that we are submitting to your ap-proval closed with net income of € 36,697,002.36.

We propose:

. making 2.5% of distributable net income, amounting to € 917,425.06, available to the Board of Directors in accordance with Art. 23 of the Company Bylaws.

. distributing a dividend of € 0.050 to each of the shares in circulation with dividend rights as of January 1 2006 (with the exclusion of own shares held as treasury stock), using the distributable part of the net income for the year of € 35,779,577.30, which is equal to € 36,697,002.36 minus the amount of € 917,425.06 made available to the Board of Directors and making up the differ-ence from the item “Retained earnings”.

The proposed allocation of the net income for the year:

¨ takes into account the provisions of Art. 2357 ter, 2nd paragraph, of the Civil Code which stipu-lates that the dividend rights on own shares be allocated pro rata to the other shares;

¨ will take into account the dividend entitlement of the 4,941 shares servicing 810 former Sasib privileged shares, the conversion of which has not yet been requested.

It should be pointed out that the actual amounts allocated to dividends and the withdrawal from the “Retained earnings” reserve will be based on the number of own shares held as treasury stock and the ordinary shares in circulation as of the date of the Shareholders’ Meeting, in case any further shares are bought back in the meantime or any new shares are issued in execution of the exercise of options by beneficiaries of the various stock option plans outstanding.

THE BOARD OF DIRECTORS

Milan, March 13 2007

Management Report

35

CIR Group

Consolidated Financial Statements as of December 31 2006

BALANCE SHEET

INCOME STATEMENT

CASH FLOW STATEMENT

STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

Consolidated Financial Statements

36

1. CONDOLIDATED BALANCE SHEET

(in thousands of euro)

ASSETS Notes 31.12.2006 31.12.2005

NON-CURRENT ASSETS 2,742,536 2,401,558 INTANGIBLE ASSETS (9.a) 951,009 864,436

TANGIBLE ASSETS (9.b) 1,091,030 897,972

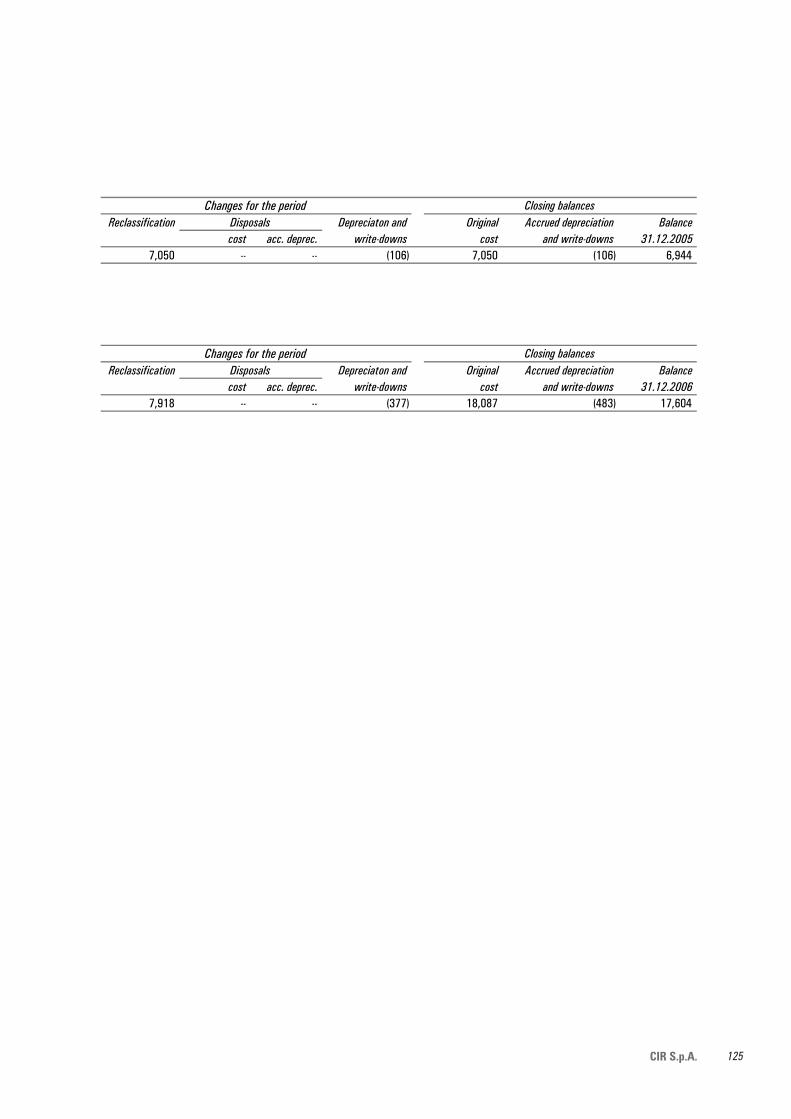

REAL-ESTATE INVESTMENTS (9.c) 17,604 6,944

INVESTMENTS IN COMPANIES VALUED AT EQUITY (9.d) 214,163 221,042

OTHER EQUITY INVESTMENTS (9.e) 8,530 7,529

OTHER RECEIVABLES (9.f) 250,991 261,403

SECURITIES (9.g) 98,583 59,841

DEFERRED TAX ASSETS (9.h) 110,626 82,391

CURRENT ASSETS 2,984,189 2,775,594 INVENTORIES (10.a) 217,082 162,864

WORK IN PROGRESS 1,685 933

TRADE RECEIVABLES (10.b) 996,477 790,744

OTHER RECEIVABLES (10.c) 273,992 201,362

FINANCIAL RECEIVABLES (10.d) 21,354 26,513

SECURITIES (10.e) 654,248 467,959

AVAILABLE-FOR-SALE FINANCIAL ASSETS (10.f) 372,867 362,930

CASH AND CASH EQUIVALENTS (10.g) 446,484 762,289

ASSETS HELD FOR SALE (2.c) 47,589 17,143

TOTAL ASSETS 5,774,314 5,194,295

LIABILITIES AND SHAREHOLDERS' EQUITY 31.12.2006 31.12.2005

SHAREHOLDERS' EQUITY 1,979,912 1,856,383 SHARE CAPITAL (11.a) 390,240 389,621

RESERVES (11.b) 367,779 401,794

RETAINED EARNINGS (LOSSES) (11.c) 401,016 305,945

NET INCOME FOR THE YEAR 101,120 87,675

SHAREHOLDERS' EQUITY - GROUP 1,260,155 1,185,035 MINORITY INTERESTS 719,757 671,348

NON-CURRENT LIABILITIES 2,288,420 2,186,453 BONDS (12.a) 1,187,750 1,199,251

OTHER BORROWINGS (12.b) 758,514 654,785

OTHER PAYABLES 1,178 21

DEFERRED TAX LIABILITIES (9.h.) 137,743 126,260

PERSONNEL OBLIGATIONS (12.c) 166,554 163,671

PROVISIONS FOR RISKS AND LOSSES (12.d) 36,681 42,465

CURRENT LIABILITIES 1,469,640 1,137,983 BANK OVERDRAFT FACILITIES 265,180 54,962

OTHER BORROWINGS (13.a) 134,134 175,881

TRADE PAYABLES (13.b) 748,901 649,766

OTHER PAYABLES (13.c) 273,962 213,768

PROVISIONS FOR RISKS AND LOSSES (12.d) 47,463 43,606

LIABILITIES HELD FOR SALE (2.c.) 36,342 13,476

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY 5,774,314 5,194,295

Consolidated Financial Statements

37Consolidated Financial Statements

2. CONSOLIDATED INCOME STATEMENT

(in thousands of euro)

Notes 2006 2005

REVENUES FROM SALES AND SERVICES (14) 4,136,769 3,382,661

CHANGE IN INVENTORIES 2,206 (1,691)

COSTS FOR PURCHASE OF GOODS (15.a) (2,457,185) (1,818,934)

COSTS FOR SERVICES (15.b) (711,792) (674,847)

PERSONNEL COSTS (15.c) (575,342) (545,777)

OTHER OPERATING INCOME (15.d) 80,263 92,443

OTHER OPERATING EXPENSE (15.e) (66,651) (82,448)

ADJUSTMENTS TO THE VALUE OF INVESTMENTS VALUED AT EQUITY (9.d.) 34,154 18,596

AMORTIZATION, DEPRECIATION AND WRITE-DOWNS (102,938) (94,894)

INCOME BEFORE INTEREST AND TAXES ( E B I T ) 339,484 275,109

FINANCIAL INCOME (16.a) 67,176 83,512

FINANCIAL EXPENSES (16.b) (129,763) (131,657)

DIVIDENDS 1,470 396

GAINS FROM TRADING SECURITIES (16.c) 96,539 93,094

LOSSES FROM TRADING SECURITIES (16.d) (54,030) (65,527)

ADJUSTMENTS TO THE VALUE OF FINANCIAL ASSETS (16,958) (297)

INCOME BEFORE TAXES 303,918 254,630

INCOME TAXES (17) (89,478) (64,753)

INCOME AFTER TAX FROM OPERATING ACTIVITY 214,440 189,877