Annual General Meeting Thursday 15 April 2010. Carl-Henric Svanberg Chairman.

57

Annual General Meeting Thursday 15 April 2010

-

Upload

alvin-martin -

Category

Documents

-

view

219 -

download

1

Transcript of Annual General Meeting Thursday 15 April 2010. Carl-Henric Svanberg Chairman.

Annual General MeetingThursday 15 April 2010

Carl-Henric SvanbergChairman

3

The Resolutions

1 Annual Report and Accounts

2 Directors’ Remuneration Report

3-16 Election and re-election of Directors

17 Reappointment of Auditors

18 Adoption of new Articles of Association

19 Share buyback

4

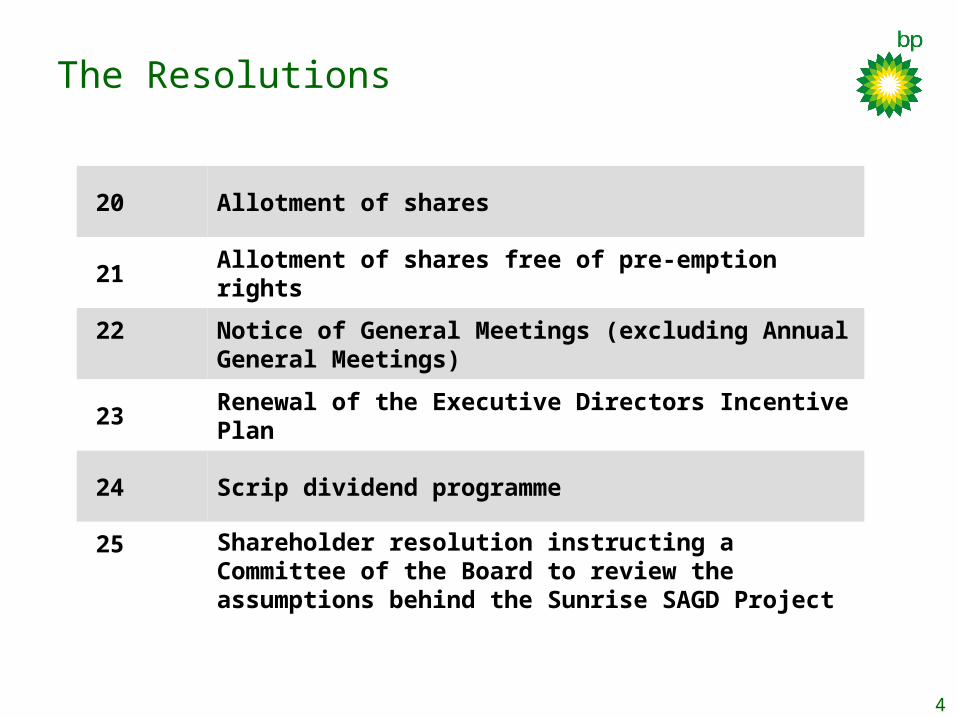

The Resolutions

20 Allotment of shares

21 Allotment of shares free of pre-emption rights

22 Notice of General Meetings (excluding Annual General Meetings)

23Renewal of the Executive Directors Incentive Plan

24 Scrip dividend programme

25 Shareholder resolution instructing a Committee of the Board to review the assumptions behind the Sunrise SAGD Project

5

Resolution 1

Annual Report and AccountsAnnual Report and Accounts

Tony HaywardGroup Chief Executive

7

Long-term energy outlook

Demand

• Growth resumes post recession

• Driven by non-OECD

• Evolution to lower-carbon economy

Supply

• Diverse energy mix required

• Leveraging technology

• Carbon pricing

Energy consumption to 2030

Source: BP estimates

Mb

oed

OECD

Non-OECD

0

100

200

300

400

2000 2010 2020 2030

Renewables

Hydro

Nuclear

Coal

Gas

Biofuels

Oil0

100

200

300

400

2000 2010 2020 2030

Mb

oed

8

BP’s approach to a lower-carbon future

• Energy efficiency within BP operations

• Including the price of carbon in investment decisions

• Promoting lowest-cost energy pathways e.g. gas for power generation

• Continued investment in Alternative Energy

− biofuels

− wind

− solar

− carbon capture and sequestration

• Investing in research and technology

9

Forward Agenda

Safe and reliable operations

• Continue journey in personal safety

• Implement Operating Management System

• Compliance

People

• Building capability

• Leadership and behaviours

Performance

• Restore revenues

• Reduce complexity and cost

10

Safe, reliable and efficient operations

Loss of Primary Containment Incidents

0

50

100

150

200

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

(1) Data for 2008 and 2009 is aligned to incident impact severity rather than volume released

Integrity Management Major Incidents(1)

0

5

10

15

20

25

30

35

2004 2005 2006 2007 2008 2009

Recordable Injury Frequency

0.0

0.5

1.0

1.5

2000200120022003200420052006200720082009

Industry range - six majors

11

People and organization

• Leadership and culture

• Restructuring and delayering

• Skills and capability

• Diversity and inclusion

• Reward for performance

Changing the culture

12

2004

2005

2006

2007

2008

2009

Restoring revenues

Refining availability(1)Production Rolling 4-quarters to 4Q09

Shell

Total

Chevron

ExxonMobil

BP

mb

oed

2000

2500

3000

3500

4000

4500

1Q

00

1Q

01

1Q

02

1Q

03

1Q

04

1Q

05

1Q

06

1Q

07

1Q

08

1Q

09

Note: Chevron includes Texaco, prior to the mergerBarrels of oil equivalent as reported in company disclosures (1) Solomon availability

70%

75%

80%

85%

90%

95%

100%

13

Controlling cash costs

Cash costs - indexed(Total BP Group)

A definition of cash costs can be found on our website at www.bp.com

80

90

100

110

120

130

140

150

2004 2005 2006 2007 2008 2009

14

2009 momentum versus peers

Underlying Net Income $bn(1) 14.6 19.2 11.6 9.5 Year on Year % -44% -56% -59% -58%

Cash from Operations $bn 27.7 28.4 21.0 Year on Year % -27% -52% -52% -35%

Reported Volumes mboed 3998 3932 3152 2704 Year on Year % 4% 0% -3% 7%

Market Capitalisation $bn(2)

vs. end 2008 %

Capital Expenditure $bn(3) 20.0 27.1 30.6 22.2 Year on Year % -8% 4% 2% -2%

10.9-47%

17.2-37%

2281-3%

18.6-7%

(1) For BP underlying net income is replacement cost for the year adjusted for non-operating items and fair value accounting effects. For other companies, underlying includes adjustments for all identified non-recurring items.

(2) as at 31/12/2009(3) BP organic; ExxonMobil, Royal Dutch Shell, Chevron and Total as disclosed

181 323 185 15424% -21% 13% 3%

15015%

19.4

15

BP vs peers – since January 2009

Conoco Phillips

Exxon Mobil

BP

ChevronRDSB

Total

Source: Datastream, 14 April 2010

J F M A M J J A S O N D J F M A60

70

80

90

100

110

120

130

140

16

Strategic progress in 2009

E&P• New access: Iraq, Indonesia, Jordan, new acreage in US Gulf of Mexico and

Egypt • Exploration and appraisal success: Tiber, Mad Dog South, Angola Block 31• Major projects: 7 start-ups and 2 sanctioned developments• Resource replacement: over 250%• Reserves replacement: 129%• Production growth: 4%

R&M• Revenues restored: US refining portfolio fully operational• Simplification: US convenience retail, reduced marketing footprint• Cost efficiency: cash costs down by more than 15% on 2008

Alternative Energy• Focused and disciplined: $4bn invested since 2006

Corporate Simplification• Headcount: reduced by ~ 7500 to date• Cash costs: down by more than $4bn in 2009

Reserve replacement as reported on a combined basis of subsidiaries and equity accounting entities, excluding acquisitions and divestments

17

2009 exploration and access

ANGOLALeda, Oberon, TebeBlock 31BP (27%) and operatorNineteen discoveries in block

US GULF OF MEXICOTiberBP (62%) and operatorGiant oil discovery

CANADAEllice J-27BP (25%)

EGYPTNile Delta2,900km2 net in two

blocks

IRAQRumailaRedevelopment of supergiant

PAKISTANOnshore5,000km2 in two blocks

INDONESIAKalimantanNet 640km2 of Coal Bed Methane

INDONESIAWest Papua2620km2 net in two blocks

US GULF OF MEXICO61 leases from OCS 208, 210

US SHALE GASEagle FordNew ~5tcf position

ExplorationAccess

JORDANRisha7,000km2 block

18

Growth to 2015

2010-2015 BP projections at $60/bbl

TNK-BP

Angola

Gulf of Mexico

Asia Pacific

South America

N. Africa, Middle Eastand Caspian

Trinidad & Tobago

North Sea

North America Onshore0

1,000

2,000

3,000

4,000

5,000

2008 2009 2010 2011 2012 2013 2014 2015

mboed

19

Project start-ups 2010–2015

AlaskaLiberty *

* BP Operated

2010 Start Ups

2011 Start Ups

2012-2015 Start Ups

Canada Canada Noel * Sunrise

Gulf of MexicoGreat WhiteGalapagos *Na Kika Phase 3 *Mad Dog Phase 2 *Na Kika Phase 4 * Tubular Bells *Freedom Kaskida *Mars B Horn Mountain Phase 2 *Atlantis Phase 3 *

Trinidad & TobagoSerrette *Trinidad Compression *Juniper *

AngolaB31 PSVM *PazflorClochas MavacolaAngola LNGKizomba Satellites Phase 2B18 West *CLOV

Asia PacificNorth Rankin 2Tangguh Expansion *Sanga Sanga Coal Bed Methane

AzerbaijanChirag Oil *

North SeaSkarv *Valhall Redevelopment * Devenick *Kinnoull *Clair Ridge *WoS Q204 *

EgyptWND Gas *

Algeria & LibyaIn Salah Gas CompressionIn Salah Southern FieldsIn Amenas Compression

Middle EastOman FFD *

Russia (TNK-BP)RusskoyeSuzunVerkhnechonskoye FFD

2012 and 2015 BP projections at $60/bbl

2012 2015

400

1000

20

Total oil and gas initially in place

Portfolio qualityEfficient and successful

explorer

High quality refining

RDSCVX

BP

XOM

COP

TOT

0

1

2

3

4

5

5 10 15Exploration spend $bn

Dis

covere

d r

eso

urc

e b

nb

oe

Majors' relative performance 2004 - 2008

Leverage to improved recovery

Strong reserve replacement track record (1)

+1% = 2 bnboe

18

45

41

bn boe

Currently unrecoverabl

e hydrocarbon

Produced

Proved

Non-proved

World class international businesses

0%

20%

40%

60%

80%

100%

120%

5-Y

ear

Avera

ge O

rgan

ic R

RR

’0

4-’

08

(excl

ud

ing

oil

san

ds,

usi

ng

year-

en

d p

rici

ng

)

(1) BP estimates using company disclosure

Robust medium-term growth

2010-2015 BP projections at $60/bbl

1,000

2,000

3,000

4,000

5,000

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

TNK-BP

Angola

Gulf of Mexico

Asia Pacific

South America

N Africa, Middle East and CaspianTrinidad

North Sea

North America Onshore

mb

oed

0

Source: Oil & Gas Journal 2010

Avera

ge R

efin

ery

Siz

e (

kbd

)

Alliance MombasaCoryton ReichstettGrangemouthSalt LakeLavera Singapore Mandan Yorktown

BP Divestments ’00-’09

Divested

100

150

200

250

7 8 9 10 11Nelson Complexity

• Material market shares

• 40% of capital employed in growth markets

• Leading technologies

• Strong customer relationships

• Premium brands

• Margin share growth

21

The opportunity

Project Cost Performance

Inflation ProjectManagement

120% 5%15%

SanctionEstimate

100%

ROACE vs PeersEarnings vs Peers

Projects efficiencyPerformance gap in US Fuels Value

Chains

Drilling efficiency

Underlying net income gap $bn

(25)

(20)

(15)

(10)

(5)

0

5

BP gap to Shell BP gap to ExxonMobil(absolute)

2001 2002 2003 2004 2005 2006 2007 2008 2009 0%

5%

10%

15%

20%

25%

30%

35%

40%

2003 2004 2005 2006 2007 2008 20092003 2004 2005 2006 2007 2008 2009

Underlying ROACE

BP

Other Supermajors

Dril

ling

Cap

ital $

m

Industry Average

Best in

Basin

$500m Opportunity

2009 BP Actual

Performance

Pre-tax RCOP per barrel, rolling 4Q indexed

US Peers

BP

Refining efficiency

YearBP portfolio average Top 3 R&M refinery sites

Solo

mon

Availab

ilit

y %

70

75

80

85

90

95

100

R&M refining cost efficiency(1)

2012

2007

2009

140 120 100130 110

2004

Refining performance

(1) Based on Solomon non-energy operating expense per Effective Distillation Capacity (indexed to top three R&M refineries)

(100)

(50)

0

50

100

150

200

1Q

05

2Q

05

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

4Q

06

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

Source: Benchmarking data based on BP internal and industry

Data based on BP Operated Major Projects portfolio in 2004-2008

22

Realising the opportunity

• Capital efficiency

• Cost efficiency

• Technology

• Culture

23

Strategy

• Upstream profit growth, cost and capital efficiency

• Downstream turnaround, cost efficiency

• Alternative Energy focused and disciplined

• Corporate efficiency

Carl-Henric SvanbergChairman

25

Resolution 1

Annual Report and AccountsAnnual Report and Accounts

26

Resolution 12009 Annual Report and Accounts

Voted For 11,079,621,694

Voted Against 21,499,097

Vote Withheld 66,436,113

For

Against

Results to date:

99.8%

0.2%

27

Resolution 2

Directors’ Remuneration Report

Directors’ Remuneration Report

28

Resolution 2Directors’ Remuneration Report

Voted For 9,398,720,859

Voted Against 931,578,571

Vote Withheld 837,212,009

Results to date:

For

Against

91.0%

9.0%

29

Resolutions 3-15Election or re-election of Directors

Mr P Anderson

Mr A Burgmans

Mrs C B Carroll

Sir William Castell

Mr I C Conn

Mr G David

Mr I E L Davis

Mr R Dudley

Mr D J Flint

Dr B E Grote

Dr A B Hayward

Mr A G Inglis

Dr D S Julius

30

Resolutions 3-15Election or re-election of Directors

Vote for Vote against Vote withheld

Mr P Anderson 10,977,409,512 151,066,543 38,993,692

Result to date: For 98.6% Against 1.4%

Mr A Burgmans 10,965,134,434 164,050,721 38,302,403

Result to date: For 98.5% Against 1.5%

Mrs C B Carroll 11,027,057,453 102,533,368 37,902,173

Result to date: For 99.1% Against 0.9%

Sir William Castell 11,025,041,912 103,761,424 38,702,079

Result to date: For 99.1% Against 0.9%

31

Resolutions 3-15Election or re-election of Directors

Vote for Vote against Vote withheld

Mr I C Conn 10,938,403,093 191,087,047 38,041,584

Result to date: For 98.3% Against 1.7%

Mr G David 10,733,392,610 395,475,212 38,614,107

Result to date: For 96.4% Against 3.6%

Mr I E L Davis 10,975,611,000 152,716,758 39,155,414

Result to date: For 98.6% Against 1.4%

32

Resolutions 3-15Election or re-election of Directors

Vote for Vote against Vote withheld

Mr R Dudley 10,940,166,275 188,849,910 38,478,595

Result to date: For 98.3% Against 1.7%

Mr D J Flint 10,899,035,276 102,425,031 166,033,213

Result to date: For 99.1% Against 0.9%

Dr B E Grote 10,939,048,013 190,239,704 38,228,537

Result to date: For 98.3% Against 1.7%

33

Resolutions 3-15Election or re-election of Directors

Vote for Vote against Vote withheld

Dr A B Hayward 11,024,928,701 104,948,195 37,664,239

Result to date: For 99.1% Against 0.9%

Mr A G Inglis 10,939,126,761 190,109,903 38,288,567

Result to date: For 98.3% Against 1.7%

Dr D S Julius 10,809,445,155 320,094,978 37,952,418

Result to date: For 97.1% Against 2.9%

34

Resolution16

Election of Mr C-H SvanbergElection of Mr C-H Svanberg

35

Resolution 16Election of Mr C-H Svanberg

Voted For 10,930,203,696

Voted Against 198,508,861

Vote Withheld 38,772,903

Results to date:

For

Against

98.2%

1.8%

36

Resolution17

Reappointment of AuditorsReappointment of Auditors

37

Resolution 17Reappointment of Auditors

Voted For 11,033,820,135

Voted Against 82,465,621

Vote Withheld 51,260,548

Results to date:

For

Against

99.3%

0.7%

38

Resolution18

Special Resolution:Adoption of New Articles

Special Resolution:Adoption of New Articles

39

Resolution 18Adoption of New Articles

Voted For 10,875,402,957

Voted Against 100,262,826

Vote Withheld 191,793,500

Results to date:

For

Against

99.1%

0.9%

40

Resolution19

Special Resolution:Authority to repurchase

shares

Special Resolution:Authority to repurchase

shares

41

Resolution 19Authority to repurchase shares

Voted For 11,049,776,527

Voted Against 54,030,655

Vote Withheld 63,742,541

Results to date:

For

Against

99.5%

0.5%

42

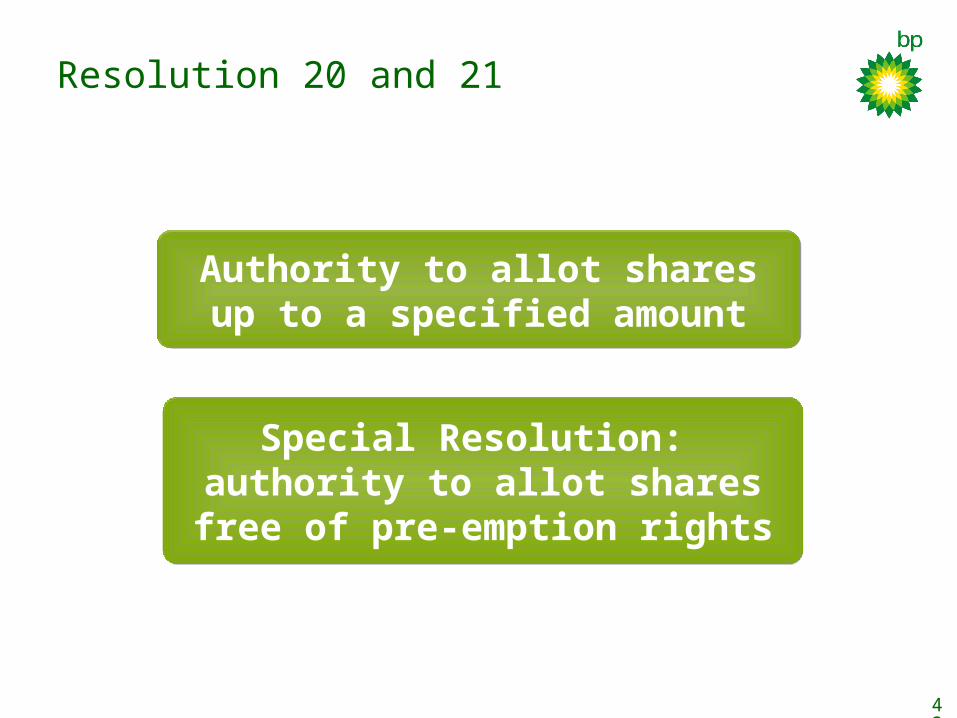

Resolution 20 and 21

Authority to allot shares up to a specified amount

Authority to allot shares up to a specified amount

Special Resolution: authority to allot shares free

of pre-emption rights

Special Resolution: authority to allot shares free

of pre-emption rights

43

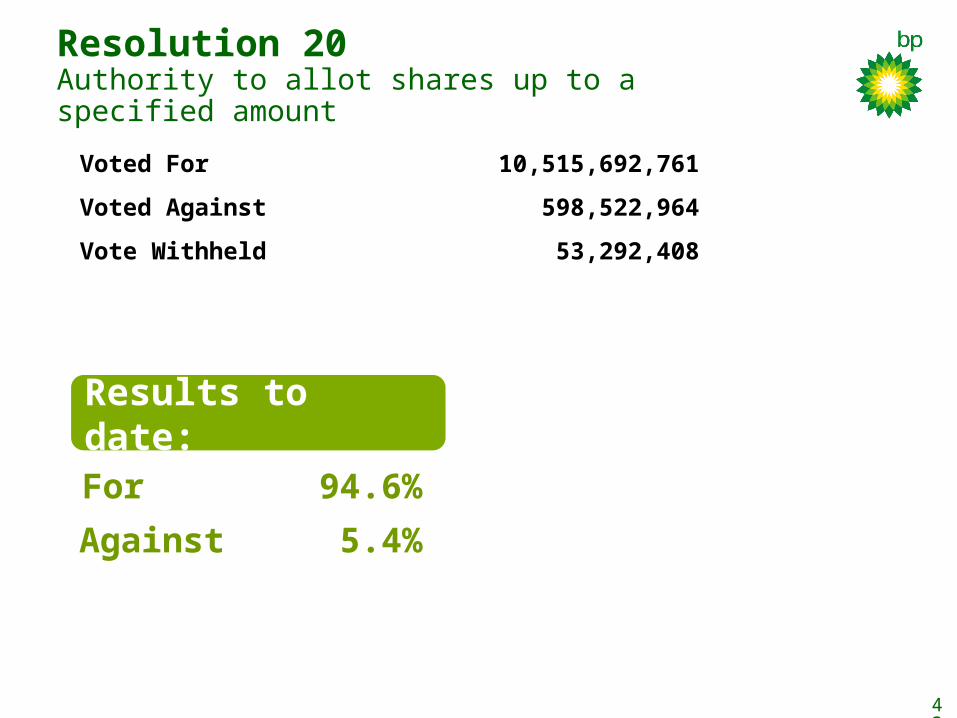

Resolution 20Authority to allot shares up to a specified amount

Voted For 10,515,692,761

Voted Against 598,522,964

Vote Withheld 53,292,408

Results to date:

For

Against

94.6%

5.4%

44

Resolution 21Authority to allot shares free of pre-emption rights

Voted For 10,936,954,354

Voted Against 172,496,006

Vote Withheld 58,061,690

Results to date:

For

Against

98.4%

1.6%

45

Resolution 22

Special Resolution:Notice of General Meetings

(excluding AGMs)

Special Resolution:Notice of General Meetings

(excluding AGMs)

46

Resolution 22Notice of General Meetings (excluding AGMs)

Voted For 10,531,741,736

Voted Against 591,822,173

Vote Withheld 44,000,807

Results to date:

For

Against

94.7%

5.3%

47

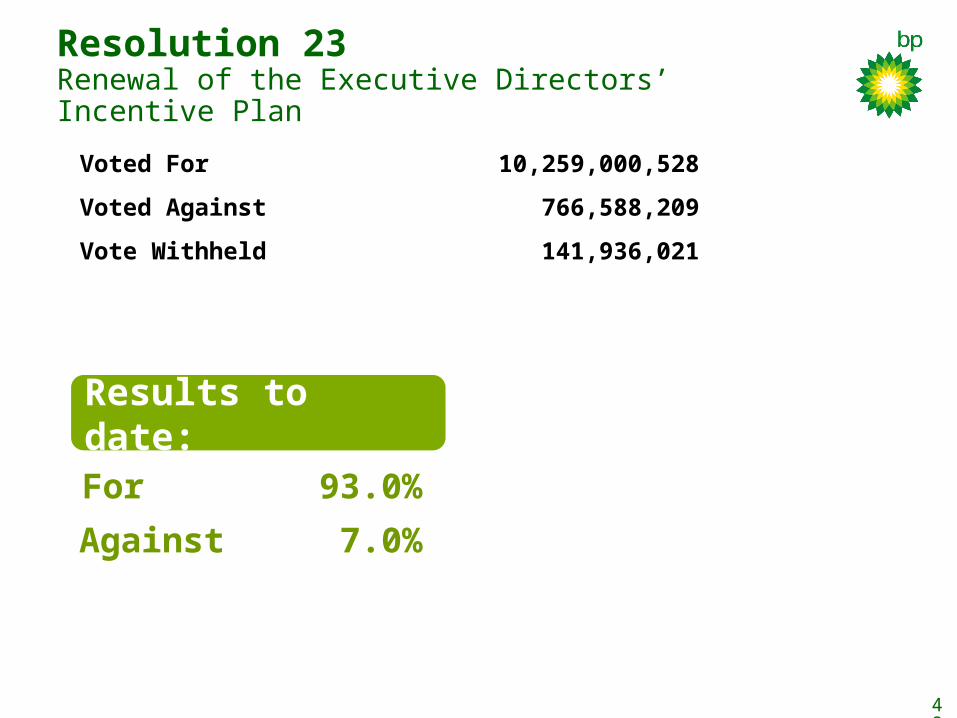

Resolution 23

Renewal of the Executive Directors’ Incentive PlanRenewal of the Executive Directors’ Incentive Plan

48

Resolution 23Renewal of the Executive Directors’ Incentive Plan

Voted For 10,259,000,528

Voted Against 766,588,209

Vote Withheld 141,936,021

Results to date:

For

Against

93.0%

7.0%

49

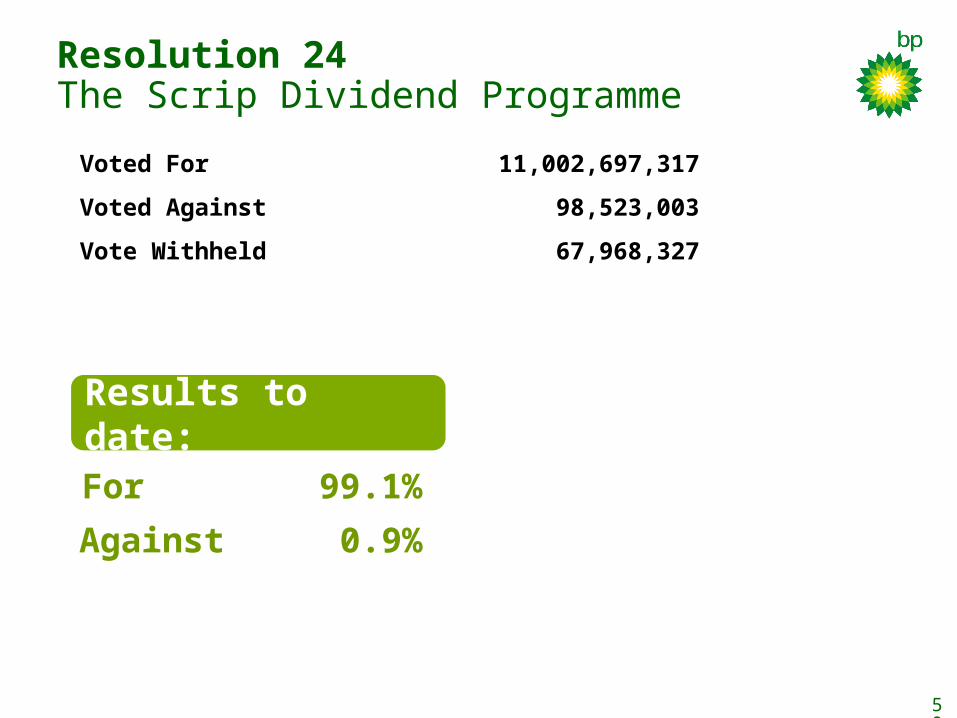

Resolution 24

The Scrip Dividend Programme

The Scrip Dividend Programme

50

Resolution 24The Scrip Dividend Programme

Voted For 11,002,697,317

Voted Against 98,523,003

Vote Withheld 67,968,327

Results to date:

For

Against

99.1%

0.9%

51

Resolution 25

Shareholder ResolutionShareholder Resolution

Special Resolution: Instructing a Committee of

the Board to review the assumptions behind the

Sunrise SAGD Project

Special Resolution: Instructing a Committee of

the Board to review the assumptions behind the

Sunrise SAGD Project

52

A typical Steam Assisted Gravity Drainage (SAGD) Well Pad

53

SAGD Schematic

54

Resolution 25Instructing a Committee of the Board to review the assumptions behind the Sunrise SAGD Project

Voted For 622,272,418

Voted Against 9,497,638,714

Vote Withheld 1,020,301,075

Results to date:

For

Against

6.1%

93.9%

55

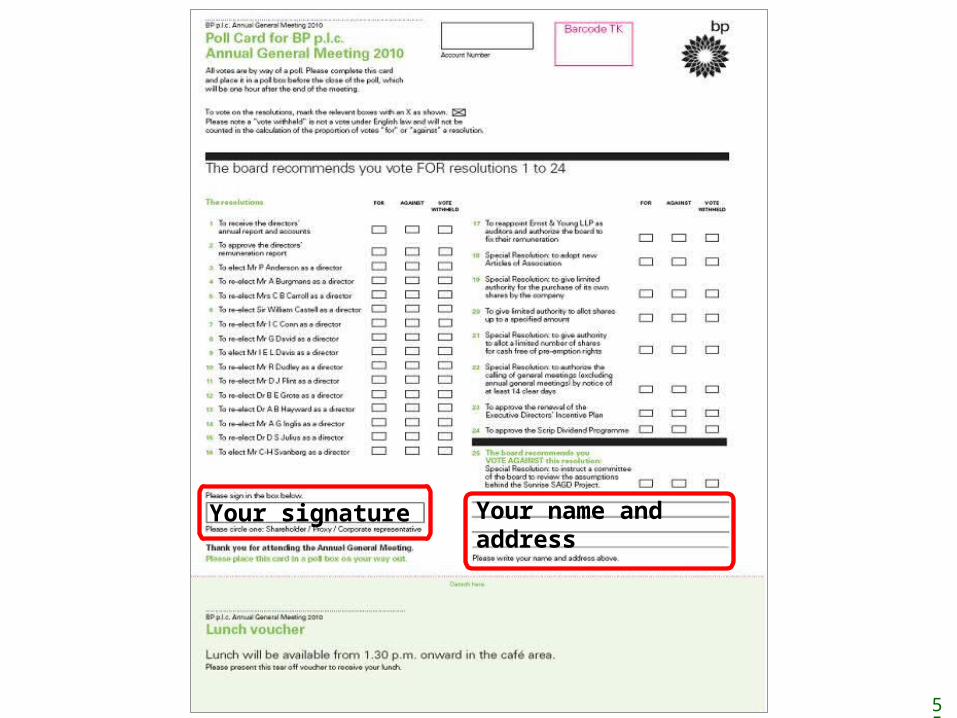

Your signature Your name and address

56

Please complete your

poll cards and place

them in the boxes

provided

57

The BP p.l.c. AGM 2010 is now concluded

Thank you for your attendance