Annual General Meeting th July 2017 Yverdon-les-Bains ... July 2017 Yverdon-les-Bains, Switzerland 1...

23

company confidential – 2016 0 Annual General Meeting 26 th July 2017 Yverdon-les-Bains, Switzerland

Transcript of Annual General Meeting th July 2017 Yverdon-les-Bains ... July 2017 Yverdon-les-Bains, Switzerland 1...

company confidential – 20160

Annual General Meeting26th July 2017Yverdon-les-Bains, Switzerland

1company confidential – 2017

1

Agenda

▪ 2016 Achievements

▪ 2016 Financial Summary

▪ 2016 Disappointments

▪ Solid foundation for growth

▪ Strategic transformation of the business

▪Outlook

2company confidential – 2017

2

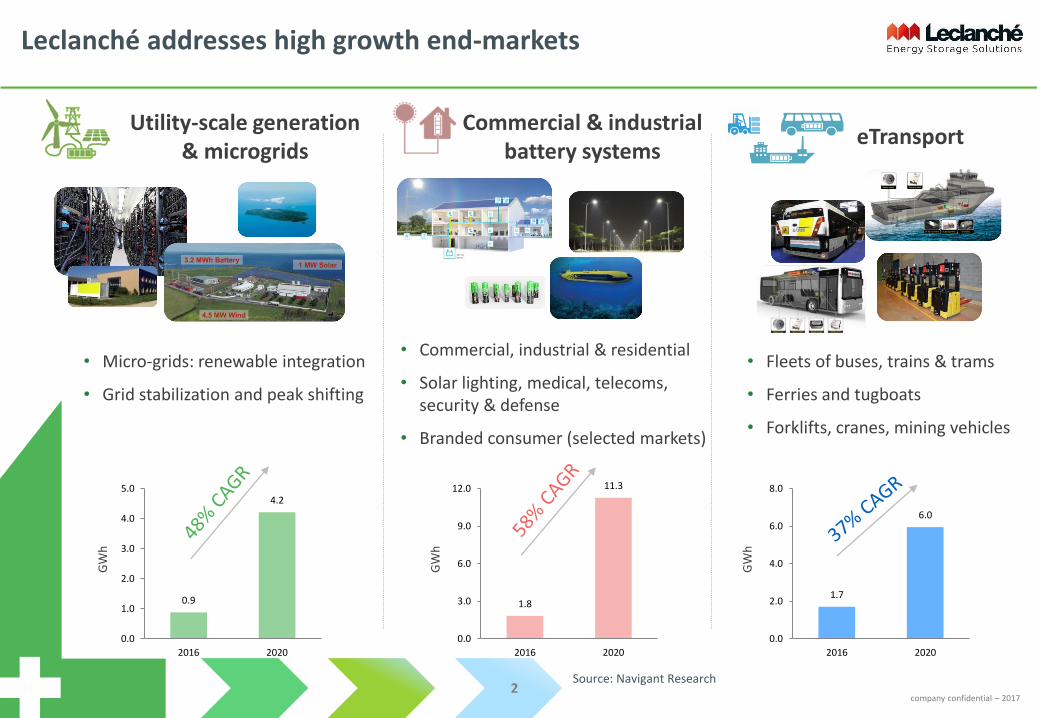

• Micro-grids: renewable integration

• Grid stabilization and peak shifting

Leclanché addresses high growth end-markets

• Commercial, industrial & residential

• Solar lighting, medical, telecoms, security & defense

• Branded consumer (selected markets)

Utility-scale generation & microgrids

Commercial & industrial battery systems

Source: Navigant Research

• Fleets of buses, trains & trams

• Ferries and tugboats

• Forklifts, cranes, mining vehicles

eTransport

0.9

4.2

0.0

1.0

2.0

3.0

4.0

5.0

2016 2020

1.8

11.3

0.0

3.0

6.0

9.0

12.0

2016 2020

1.7

6.0

0.0

2.0

4.0

6.0

8.0

2016 2020

GW

h

GW

h

GW

h

3company confidential – 2017

3

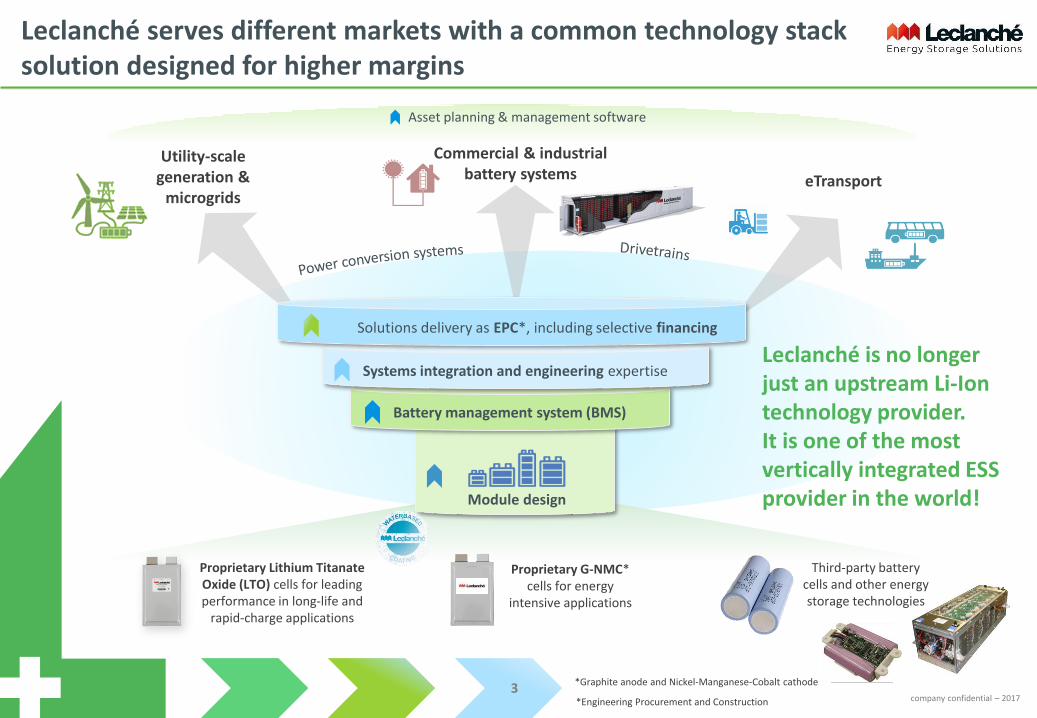

Leclanché serves different markets with a common technology stack solution designed for higher margins

Proprietary Lithium Titanate Oxide (LTO) cells for leading performance in long-life and

rapid-charge applications

Proprietary G-NMC* cells for energy

intensive applications

*Graphite anode and Nickel-Manganese-Cobalt cathode

Module design

eTransport

Asset planning & management software

Leclanché is no longer just an upstream Li-Ion technology provider. It is one of the most vertically integrated ESS provider in the world!

Third-party battery cells and other energy storage technologies

Battery management system (BMS)

Utility-scale generation &

microgrids

Commercial & industrial battery systems

Systems integration and engineering expertise

*Engineering Procurement and Construction

Solutions delivery as EPC*, including selective financing

4company confidential – 2017

4

2016 Achievements

• 56% growth, in line with the guidance given during the interim results

• 2.5x over the year 2014

Revenue

• 16X increase in order intake, currently >85 MWh Orders

• >450 MWh in Order Pipeline

• 22 MWh of projects under construction

Order Book

• Steady-state EBITDA Loss reduced by 54% compared to 2015

• Reduced Capex by 35% over previous year

• Loss per share reduced by 28% vs. 2015

Reduction of loss

Secured USD 23M of project finance fromSGEM, a Golden Partner controlled entity• CHF 8M Equity in Marengo project in

Chicago• USD 15M construction loan for IESO

project in Canada

Project Finance

5company confidential – 2017

5

Agenda

▪ 2016 Achievements

▪ 2016 Financial Summary

▪ 2016 Disappointments

▪ Solid foundation for growth

▪ Strategic transformation of the business

▪Outlook

66

Annual Results 2016

2016 2015 Comments

kCHF kCHF

Sales of goods and services 28 067.1 17 882.5 1First two IESO sites in Canada and Marengo project in

the US

Other income 454.1 325.5

Total income 28 521.2 18 208.0

Raw materials and consumables used -26 162.6 -16 554.1

Personnel costs -19 381.2 -14 297.2 2Ful year impact of Belgium July 2015 acquisition +

Leclanché North America staffing

Other operating expenses -10 501.3 -13 384.3

Earnings Before Interest, Tax, Depreciation and Amortization -27 523.9 -26 027.6 Steady-state loss reduced by 50%, excluding one-time

investments

Depreciation, amortization and Impairment expenses -6 155.5 -5 795.5 3Impairment of Germany machinery damaged by the

April 2016 fire

Operating Loss -33 679.4 -31 823.1

Finance costs -4 091.1 -2 670.2 4Capital raise commissions paid to financial

institutions

Finance income - 0.5

Loss before tax for the year -37 770.5 -34 492.8

Income tax 553.4 -1 084.6

Loss for the year -37 217.1 -35 577.4

Net Loss per share -0.87 -1.21

INCOME STATEMENT

7company confidential – 2017

7

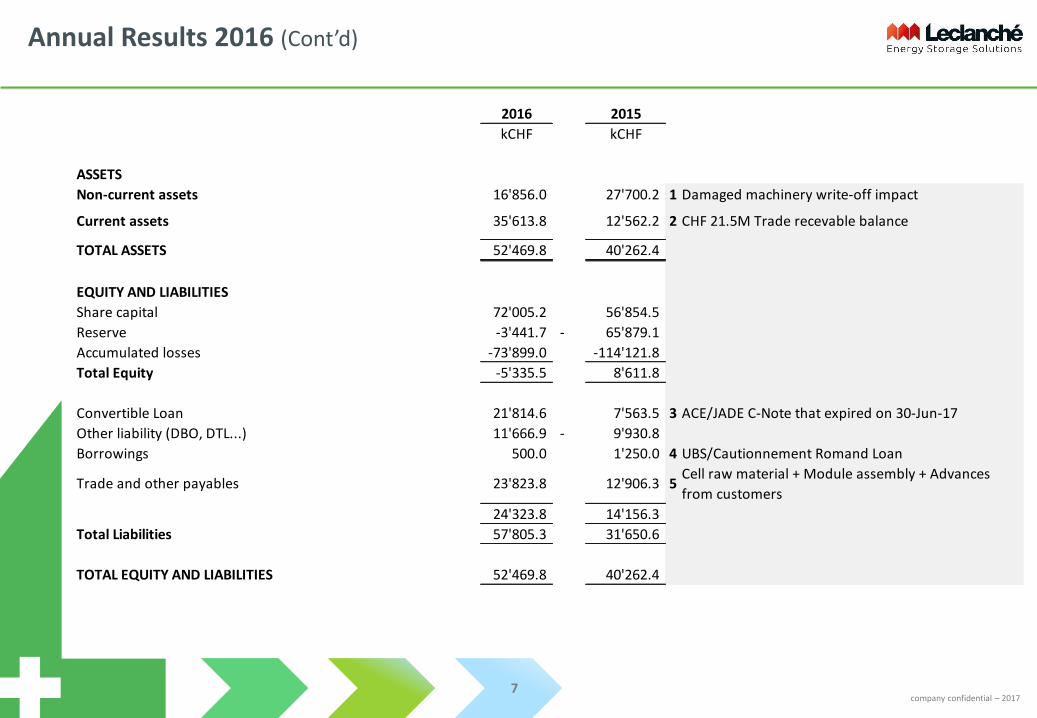

Annual Results 2016 (Cont’d)

2016 2015

kCHF kCHF

ASSETS

Non-current assets 16'856.0 27'700.2 1 Damaged machinery write-off impact

Current assets 35'613.8 12'562.2 2 CHF 21.5M Trade recevable balance

TOTAL ASSETS 52'469.8 40'262.4

EQUITY AND LIABILITIES

Share capital 72'005.2 56'854.5

Reserve -3'441.7 - 65'879.1

Accumulated losses -73'899.0 -114'121.8

Total Equity -5'335.5 8'611.8

Convertible Loan 21'814.6 7'563.5 3 ACE/JADE C-Note that expired on 30-Jun-17

Other liability (DBO, DTL...) 11'666.9 - 9'930.8

Borrowings 500.0 1'250.0 4 UBS/Cautionnement Romand Loan

Trade and other payables 23'823.8 12'906.3 5Cell raw material + Module assembly + Advances

from customers

24'323.8 14'156.3

Total Liabilities 57'805.3 31'650.6

TOTAL EQUITY AND LIABILITIES 52'469.8 40'262.4

8company confidential – 2017

8

Agenda

▪ 2016 Achievements

▪ 2016 Financial Summary

▪ 2016 Disappointments

▪ Solid foundation for growth

▪ Strategic transformation of the business

▪Outlook

9company confidential – 2017

9

The ‘rebuilding and renovation work’ underway from 2015 through to 2017

Temporary slowdown in

1H-2017. Work resumed now

10company confidential – 2017

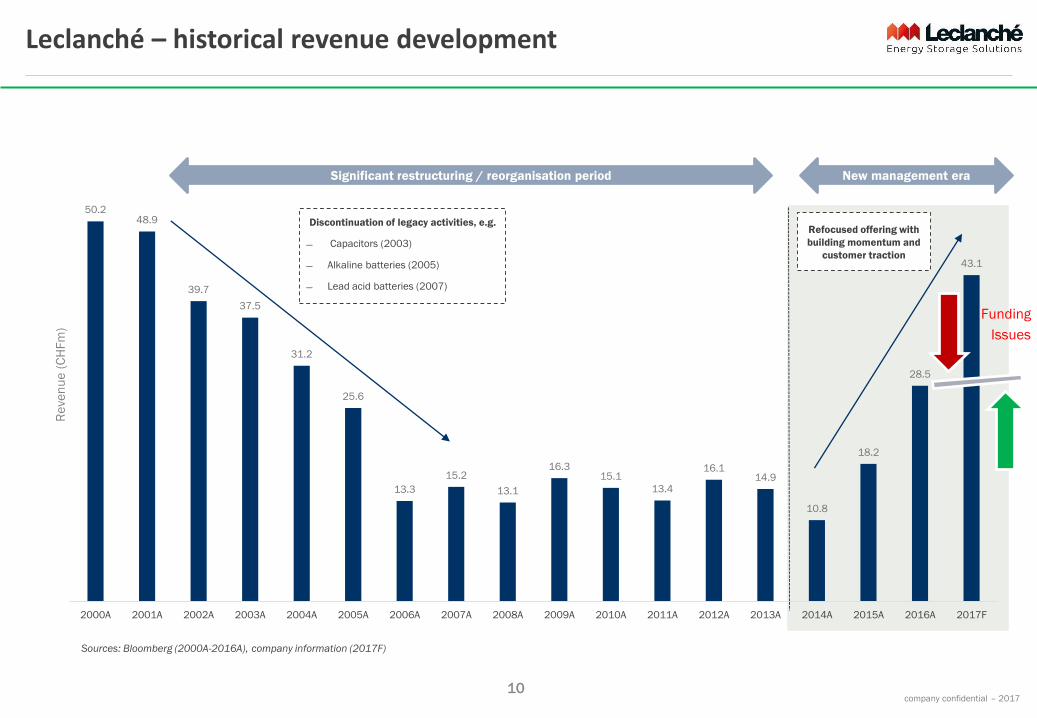

Leclanché – historical revenue development

Sources: Bloomberg (2000A-2016A), company information (2017F)

50.248.9

39.7

37.5

31.2

25.6

13.3

15.2

13.1

16.315.1

13.4

16.114.9

10.8

18.2

28.5

43.1

2000A 2001A 2002A 2003A 2004A 2005A 2006A 2007A 2008A 2009A 2010A 2011A 2012A 2013A 2014A 2015A 2016A 2017F

Re

ven

ue

(C

HF

m)

Significant restructuring / reorganisation period New management era

Discontinuation of legacy activities, e.g.

Capacitors (2003)

Alkaline batteries (2005)

Lead acid batteries (2007)

Refocused offering with

building momentum and

customer traction

Funding

Issues

company confidential – 201711

Leclanché – historical share price performance

Source: Bloomberg as at 25 April 2017

Management enhanced and

investment made to reposition

as vertically integrated energy

storage solution provider

0

5

10

15

20

25

30

35

40

45

Shar

e p

rice

(C

HF)

Leclanché acquires production capacity

for lithium-ion batteries in 2006

Construction of Willstatt

plant in Germany

Expansion of lithium-ion production capacity

and specialisation in high performance

batteries

Discontinuation of small-format

manufacturing at Itzehoe plant

Restructuring towards

integration and modern

technologies

Leclanché rides wave of substantial hype in energy storage sector towards

2009/2010

Cooling of market hype and

Leclanché financial difficulties

Significant restructuring

/ reorganisation

Major capital raise (at a

premium)

Series of further capital

raises (discounted)

Company warns

market it is facing

liquidity issues

2009 capital raise sees speculation by new

institutional investor, driving up Leclanché’s

share price

company confidential – 201712

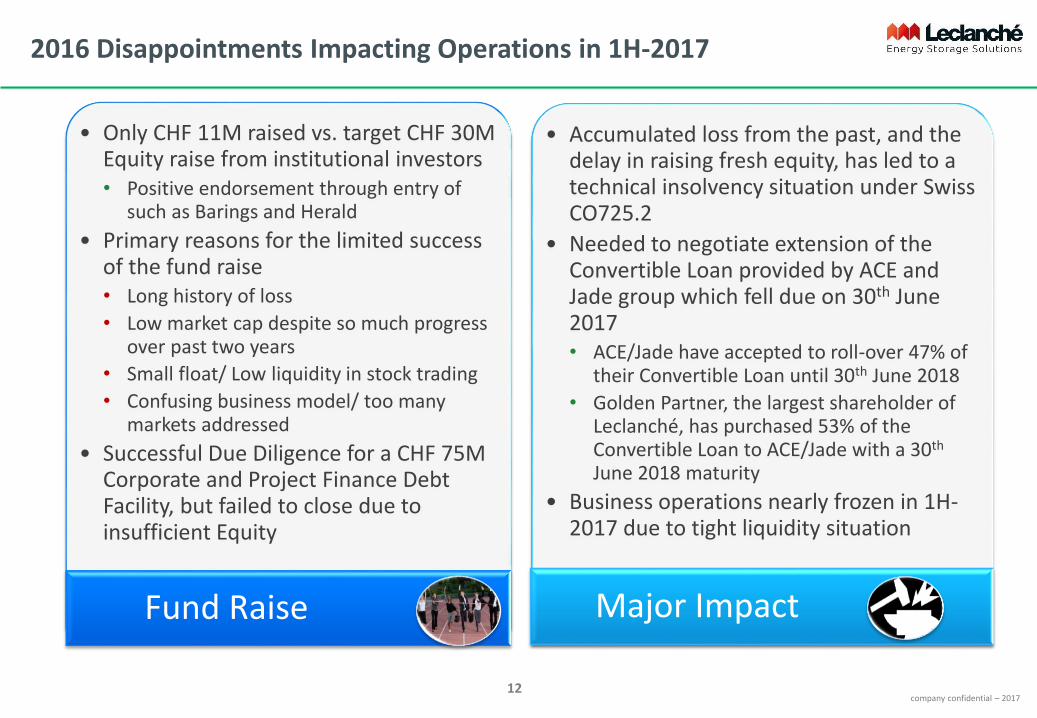

2016 Disappointments Impacting Operations in 1H-2017

• Accumulated loss from the past, and the delay in raising fresh equity, has led to a technical insolvency situation under Swiss CO725.2

• Needed to negotiate extension of the Convertible Loan provided by ACE and Jade group which fell due on 30th June 2017• ACE/Jade have accepted to roll-over 47% of

their Convertible Loan until 30th June 2018

• Golden Partner, the largest shareholder of Leclanché, has purchased 53% of the Convertible Loan to ACE/Jade with a 30th

June 2018 maturity

• Business operations nearly frozen in 1H-2017 due to tight liquidity situation

Major Impact

• Only CHF 11M raised vs. target CHF 30M Equity raise from institutional investors • Positive endorsement through entry of

such as Barings and Herald

• Primary reasons for the limited success of the fund raise • Long history of loss

• Low market cap despite so much progress over past two years

• Small float/ Low liquidity in stock trading

• Confusing business model/ too many markets addressed

• Successful Due Diligence for a CHF 75M Corporate and Project Finance Debt Facility, but failed to close due to insufficient Equity

Fund Raise

13company confidential – 2017

13

Agenda

▪ 2016 Achievements

▪ 2016 Financial Summary

▪ 2016 Disappointments

▪ Solid foundation for growth

▪ Strategic transformation of the business

▪Outlook

14company confidential – 2017

14

‘the bump’ in 1H 2017, doesn’t affect Company's journey to a Profitable High Growth

Golden Partner has undertaken to provide equity of CHF 27.5M comprising of the following:

▪ Investment of CHF 3.5M in equity

▪ New investment of CHF 12M through Mandatory Convertible Note (MCN) and undertaking to convert it by mid-September

▪ Further undertaking to convert CHF 12M of the Convertible Loan and/or inject equivalent equity by end August

Bruellan has undertaken to provide equity of CHF 4.5M comprising of the following:

▪ New investment of CHF 3M through Mandatory Convertible Note (MCN) and undertaking to convert it by end-September

▪ Conversion of CHF 1.5M MCN in July

✓ Order book totalling 95 MWh through 2018

✓ >3x 2016 deliveries planned in 2018

✓ >450 MWh qualified pipeline currently

▪ Rights Issue / Large Private Placement / Asset Sale planned in early October 2017 with aim to raise further CHF 30M (hence the need approve the creation of new shares)

▪ Complete ongoing stationary storage projects and accelerate agreements in the eTransport business

✓ >30 MWh projects under construction and delivery

✓ Significant framework agreements signed in the eTransport business, expected to generate >150 MWh per annum volume or >USD 45M revenue per year, from 2019 onward

Step #1: Cure CO725.2 through capital injectionStep #2: Resume Growth in 2H-2017

15company confidential – 2017

15

Continued growth momentum in the first half of the 2017

Utility-scale generation and micro grid applications - Forecast to grow 48% annually to 4.2 GWh1

▪ EUR 1M order from a leading innovator in the Netherlands for a Hybrid Energy Storage Solution with Leclanché ESS and Flywheel

▪ CAD 17M project for world’s first battery-based Electric Vehicle Charging Station Network in Canada, is being partially funded by a CAD 8M repayable contribution from Natural Resources Canada (NRCan) under the Canadian Energy Innovation Program

▪ EUR 630K order for LTO Battery Packs for EV Chargers in London

“Demand for energy storage from the utility sector will grow more than the marketanticipates by 2019-20…….storage is expected to grow from a less than $300 million a yearmarket to as much as $4 billion in the next two to three years. Ultimately there’s about a $30billion market for storage units, with capacity for around 85 gigawatt-hours of powerstorage. That’s enough electricity to light up most of the New York City metro area for ayear.”- Morgan Stanley’s Utility and Clean Tech analyst, Stephen Byrd and Shared Mobility &

Auto analyst, Adam Jonas: Forbes, July 14th 2017.

(1) According to Navigant Report

16company confidential – 2017

16

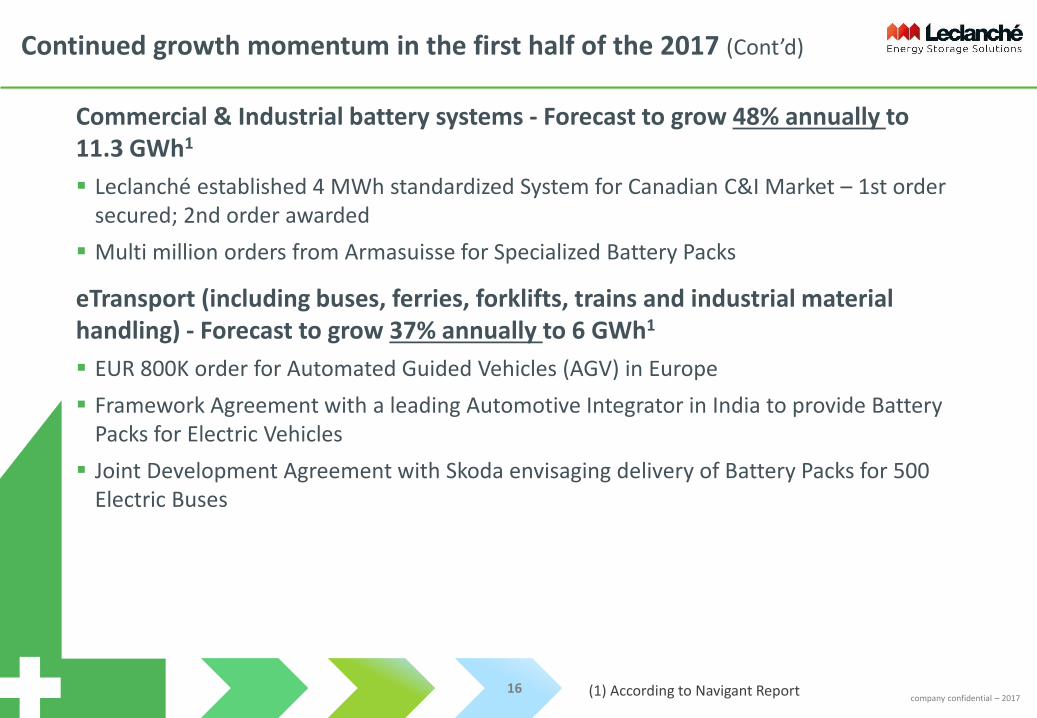

Continued growth momentum in the first half of the 2017 (Cont’d)

Commercial & Industrial battery systems - Forecast to grow 48% annually to 11.3 GWh1

▪ Leclanché established 4 MWh standardized System for Canadian C&I Market – 1st order secured; 2nd order awarded

▪ Multi million orders from Armasuisse for Specialized Battery Packs

eTransport (including buses, ferries, forklifts, trains and industrial material handling) - Forecast to grow 37% annually to 6 GWh1

▪ EUR 800K order for Automated Guided Vehicles (AGV) in Europe

▪ Framework Agreement with a leading Automotive Integrator in India to provide Battery Packs for Electric Vehicles

▪ Joint Development Agreement with Skoda envisaging delivery of Battery Packs for 500 Electric Buses

(1) According to Navigant Report

17company confidential – 2017

17

Agenda

▪ 2016 Achievements

▪ 2016 Financial Summary

▪ 2016 Disappointments

▪ Solid foundation for growth

▪ Strategic transformation of the business

▪Outlook

18company confidential – 2017

18

We have transformed the Company into fully vertically integrated Energy Storage Systems Integrator

Restructure, sharpen focus and increase productivity per person

▪ Wholly owned subsidiary Stationary Storage Business Unit

▪ Wholly owned subsidiary eTransport Storage Business Unit

▪ Considering strategic options for rest of the legacy business

▪ All IP and knowhow held in the parent Leclanché SA

2017 Results will be adversely impacted by

the delayed funding in 1H-2017 and until

completion of the funding underway

Increase margins, increase capital efficiency

▪ Acquire ‘the identified Energy Management Software’ asset, expected to generate additional 3.5% margin

▪ Make & Buy sourcing to optimize gross margin

▪ Senior managers agree to “transform significant portion of their compensation into stock option” until the EBITDA breakeven is reached in 2019

Fully fund the Business Plan

▪ Second listing in North America by Q2 2018

▪ Strategic partnership for non-recourse project finance

▪ Open capital of the operating Business Units to strategic shareholders at an appropriate time

19company confidential – 2017

19

Restructuring framework, organization announcement by Q4-2017

1. Capital Lite: Product Supply Co

2. Opex-optimized organizational structure

3. Unlock the “Value” by market segment: dedicated Business Units focused on Stationary Storage Solution and eTransport

4. Strategic options under consideration for the legacy businesses (Portable, Distribution and Home storage)

Product Supply Division

• Retain ownership of Cell IP; Cell R & D and Production; Module Design

and in-house Module Assembly

• Long-term Master Supply Agreements with committed minimum per

annum volume, initially with Commercial Business Units (BU)

Stationary Storage BU

• 95 MWh Backlog

• In-house EMS and Systems

Integration capabilities

• Turnkey EPC business model,

with strategic partnerships with

‘Owner and Operators’ of ESS

assets

• Project Sales / Liquidity Events

• Secure access to >USD 100M

Project Finance Pool: build on

significant progress in Project

Finance

• Includes C & I and EV Chargers

eTransport BU

• Framework agreements

covering more than 150 MWh

of Battery Pack shipments

from 2019

• In-house BMS and Drive Train

Packaged solution and

integration

• Sales, Marketing and After

Sales Service to and through

OEMs in the automotive sector

• Structured access to Lease/

Rental Financing for Battery

Pack leasing

20company confidential – 2017

20

Agenda

▪ 2016 Achievements

▪ 2016 Financial Summary

▪ 2016 Disappointments

▪ Solid foundation for growth

▪ Strategic transformation of the business

▪Outlook

21company confidential – 2017

21

2017 Outlook shall be provided during Interim Results Announcement in September

Despite funding related constraints in 1H-2017, no major contracts have been lost

▪ Subject to timely completion of the planned funding, the outlook for 2018 is robust

▪ EBITDA breakeven in late 2018/ early 2019

Major breakthrough possible in eTransport business

▪ Framework agreements signed envisage more than 150 MWh or USD 45M revenue per year the year 2019

▪ Joint Development Agreement with Skoda Electric, a world leading integrator

Envisage continued success in non-recourse project finance for Stationary Storage

▪ Advanced Term Sheets in place for both IESO and Marengo project covering Equity and Debt

▪ Exclusivity agreement with a leading European Utility for Cremsow project in Germany

New organization operational from Jan 2018

company confidential – 201622

We thank our Customers, Shareholders, Suppliers and Employees for their continued support