ANNUAL FINANCIAL STATEMENTS - Robben Island Museum Report 2009/AR_2009_3.pdf · ANNUAL FINANCIAL...

15

ANNUAL FINANCIAL STATEMENTS

Transcript of ANNUAL FINANCIAL STATEMENTS - Robben Island Museum Report 2009/AR_2009_3.pdf · ANNUAL FINANCIAL...

ANNUALFINANCIAL STATEMENTS

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

19

ANNUAL FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 MARCH 2009

Report of the Audit Committee ................................................................................................................................ 20Report of the Auditor-General ................................................................................................................................. 22Statement of Responsibility ..................................................................................................................................... 30Accounting Authority’s Report ................................................................................................................................. 31Statement of Financial Position ............................................................................................................................... 33Statement of Financial Performance ....................................................................................................................... 34Statement of Changes in Net Assets ...................................................................................................................... 35Cash Flow Statement .............................................................................................................................................. 36Notes to the Annual Financial Statements .............................................................................................................. 37

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

20

Report of the Audit Committee for the financial year ended 31 March 2009

We present our report for the financial year ended 31 March 2009.

Membership and attendance

The Audit Committee convened six times during the year under review. Its members and their attendance at meetings were asfollows:

Member Date Appointed

A C Coombe Independent chairperson July 2003 6 out of 6

Position No of meetings attended

C Abdoll Independent member June 2006 5 out of 6

G T Ndlovu Independent member June 2006 6 out of 6

F Mbali Council member October 2007 6 out of 6

E Godongwana Council member August 2008 0 out of 6

The terms of office of Mr A C Coombe and Ms C Abdoll expired during July 2009.

Audit Committee responsibility

The Audit Committee reports that it has complied with its responsibilities arising from section 38 (1)(a) of the Public FinanceManagement Act and Treasury Regulation 3.1.13. The Audit Committee also reports that it has prepared appropriate formal termsof reference in the form of an audit committee charter, which has been duly adopted by the Council, has regulated its affairs incompliance with this charter and, as far as possible, has discharged all its responsibilities as contained therein.

Effectiveness of internal control

Based on our review and evaluation of the work of the Outsourced Internal Auditors and of the Auditor-General of South Africa,as reported to us for the year under review, the Audit Committee is of the opinion that the systems of internal control were generallyinadequate and operated, for the most part, ineffectively during the past year. We have noted numerous areas of weaknessidentified and reported by the Internal Auditors and the Auditor-General of South Africa.

The Audit Committee repeats its concern of the previous year that a risk management committee has not been constituted bythe Council. Management has now appointed a risk and compliance officer and has drafted terms of reference of a risk managementcommittee. However the risk and compliance officer is also acting as the human resources officer, and consequently is not ableto devote sufficient time to the risk management function.

The Audit Committee repeats its recommendation of the previous year that the draft code of conduct and ethics be approved andadopted, and that urgent procedures be introduced to ensure compliance thereto.

The Audit Committee also notes with great concern that the Council, as well as the Interim Chief Executive Officer, resigned on25 May 2009, soon after the financial year end. At the present time the Museum operates without a Council, without a permanentCEO or a permanent Chief Financial Officer and without a Chief Operating Officer. The Committee has communicated its concernsto the Director-General of the Department of Arts and Culture in this regard.

The Audit Committee reports that the Museum has not tabled its budget for the year ending 31 March 2010 to the committee, norhad it approved by the Council.

Quality of quarterly management reports

The Committee was not supplied with copies of quarterly financial reports or performance information, despite requests, until afterthe end of the financial year. The Committee will continue to monitor the quality and timely preparation of these reports and tomake recommendations for improvement, so as to enhance their adequacy, reliability and accuracy.

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

21

Evaluation of financial statements

The Audit Committee has:

• reviewed and discussed with Management the audited annual financial statements to be included in the annual report;• reviewed the Auditor-General of South Africa’s management letter and Management’s response thereto;• reviewed the appropriateness of accounting policies and practices; and,• reviewed adjustments resulting from the annual audit.

The Audit Committee draws attention to the qualified audit report and the reasons why the Auditor-General of South Africa reachedthis conclusion. The Committee concurs with and understands the qualified audit report of the Auditor-General of South Africaon the annual financial statements and recommends that the audited annual financial statements, read together with the reportof the Auditor-General of South Africa thereon, be accepted.

A C CoombeChairperson of the Audit Committee31 July, 2009

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

22

Report of the Auditor-General to Parliament on the Financial Statements and Performance Informationof the Robben Island Museum for the year ended 31 March 2009

Report on the Financial Statements

Introduction

1. I have audited the accompanying financial statements of the Robben Island Museum (RIM) which comprise the statementof financial position as at 31 March 2009, the statement of financial performance, the statement of changes in net assetsand the cash flow for the year then ended, and a summary of significant accounting policies and other explanatory notesas set out on pages 33 to 68.

The accounting authority’s responsibility for the financial statements

2. The accounting authority is responsible for the preparation of these financial statements in accordance with the basis ofaccounting determined by the National Treasury, set out in Note 1 to the financial statements and in the manner requiredby the Public Finance Management Act, 1999 (Act No. 1 of 1999) (PFMA) and for such internal control as the accountingauthority determines is necessary to enable the preparation of financial statements that are free from material misstatement,whether due to fraud or error.

The Auditor-General’s responsibility

3. As required by section 188 of the Constitution of the Republic of South Africa, 1996 read with section 4 of the Public AuditAct, 2004 (Act No. 25 of 2004) (PAA), my responsibility is to express an opinion on these financial statement based onmy audit.

4. I conducted my audit in accordance with the International Standards on Auditing read with General Notice 616 of 2008,issued in Government Gazette No. 31057 of 15 May 2008. Those standards require that I comply with ethical requirementsand plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from materialmisstatements.

5. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financialstatements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of materialmisstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the entity’s preparation and fair presentation of the financial statements in order todesign audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion onthe effectiveness of accounting policies used and the reasonableness of accounting estimates made by management, aswell as evaluating the overall presentation of the financial statements.

6. I believe that the audit evidence I have obtained is sufficient and appropriate to provide a basis for my audit opinion.

Basis of qualified opinion

Comparative figures

7. A disclaimer opinion was issued for the financial year ending 31 March 2008. Comparative figures for property, plant andequipment, deferred revenue and retained earnings were not corrected and restated in the current financial year. I amtherefore still unable to perform the audit procedures I deem necessary to determine the existence, allocation, valuationand completeness of the comparative figures disclosed in the financial statements. There were no satisfactory alternativeaudit procedures that I could perform to obtain reasonable assurance that these comparative figures exist, are correctlyvalued and completely recorded as no corrections were made to these balances.

Property, plant and equipment

8. Upon physical verification between the asset register and the physical assets on the floor, material variances were identified.As a result the existence, valuation and completeness of the closing balance of fixed assets and the related depreciationas disclosed in note 2 of the annual financial statements (AFS) could not be audited. There were no alternative auditprocedures that could be performed to obtain reasonable assurance that the assets disclosed in note 2 of the AFS exists,is correctly valued complete.

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

23

9. As required by South African Statements of Generally Accepted Accounting Practice, IAS 16 (AC 123) Property, Plant andEquipment, boats were componentized but supporting evidence for this could not be presented for audit purposes. As aresult the depreciation charged on the boats could not be recalculated. There were no alternative audit procedures thatcould be performed to obtain reasonable assurance that the depreciation charged is accurate and complete.

10. South African Statement of Generally Accepted Accounting Practice, IAS 16 (AC 123) Property, Plant and Equipmentstates that the residual value and the useful life of an asset shall be reviewed at least at each financial year-end. RIM didnot conduct a useful life and residual value review of assets with a R1 carrying value or less as at 31 March 2009. Therewere no satisfactory audit procedures that I could perform to obtain reasonable assurance that all assets had been recordedat the correct value and that the related depreciation is accurately calculated. Consequently, I was unable to perform theaudit procedures I consider necessary to determine the valuation and allocation of property, plant, and equipment.

Deferred revenue

11. Due to an inadequate control system implemented over the allocation and utilization of the special project income, I wasunable to verify the completeness and valuation of the deferred revenue as disclosed in note 8. There were no alternativeaudit procedures that could be performed to obtain reasonable assurance that the deferred revenue had been recordedcompletely and at the correct value.

12. In accordance with South African Statements of Generally Accepted Accounting Practice, IAS 20 (AC 134) accounting forgovernment grants and disclosure of government assistance, income received for special projects should be releasedthrough the income statement in line with the depreciation charges on the assets purchased with the funds. This treatmentwas not correctly applied as the depreciation charged is not in line with IAS 16 (per paragraph 8 above) and therefore thecorresponding release from the deferred revenue account to the income statement will also be affected. There were nosatisfactory audit procedures that I could perform to obtain reasonable assurance that deferred revenue released had beenaccurately and completely recorded. Consequently, I was unable to perform the audit procedures I consider necessary todetermine the accuracy, occurrence and completeness of the deferred income release to the income statement.

Qualified opinion

13. In my opinion, except for the possible effects of the matters described in the basis for qualified opinion paragraphs, thefinancial statements present fairly, in all material respects, the financial position of the Robben Island Museum as at 31March 2009 and its financial performance and its cash flows for the year then ended, in accordance with the basis ofaccounting determined by National Treasury, as set out in note 1 to the financial statements and in the manner requiredby the PFMA.

Emphasis of matters

14. The entity’s policy is to prepare financial statements in accordance with the basis of accounting as determined by theNational Treasury as set out in note 1 to the financial statements.

Irregular expenditure

15. As disclosed in note 28 to the financial statements, irregular expenditure to the amount of R448 526 was incurred, asappropriate approval for the expenditure incurred was not obtained.

Fruitless and wasteful expenditure

16. As disclosed in note 27 to the financial statements, fruitless and wasteful expenditure to the amount of R242 481was incurred.

Other matters

I draw attention to the following matters that relates to my responsibilities in the audit of the financial statements:

Material inconsistencies

17. I have not obtained the other information included in the annual report and have not been able to identify any materialinconsistencies with the financial statements.

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

24

Unaudited supplementary schedules

18. The supplementary information set out on pages 70 to 92 does not form part of the financial statements and is presentedas additional information. I have not audited these schedules and accordingly I do not express an opinion thereon.

Non-compliance with applicable legislation

Public Finance Management Act

19. Section 51 (1)(b) of the PFMA: RIM did not take effective and appropriate steps to collect all revenue due to the entityas long outstanding debtors existed at year end.

Treasury regulations

20. Section 26.1.1 of the Treasury Regulations: RIM did not submit all the financial quarterly reports in the prescribed timeto the executive authority.

Governance framework

21. The governance principles that impact the auditor’s opinion on the financial statements are related to the responsibilitiesand practices exercised by the accounting authority and executive management and are reflected in the internal controldeficiencies and other key governance requirements addressed below:

Internal control deficiencies

22. Section 51(1)(a)(i) of the PFMA states that the accounting authority must ensure that the public entity has and maintainseffective, efficient and transparent systems of financial and risk management and internal control. The table below depictsthe root causes that gave rise to the deficiencies in the system of internal control, which led to the qualified opinion. Theroot causes are categorized according to the five components of an effective system of internal control (The number listedper component can be followed with the legend below the table). In some instances deficiencies exist in more than oneinternal control component.

Par. No. CE

7 Comparative figures

Basis for qualified opinion RA CA IC M

5

8 Property, plant and equipment 5

9 Property, plant and equipment 7

10 Property, plant and equipment 7

11 Deferred revenue 5

12 Deferred revenue 7

LEGEND

CE = Control environment (ISA 315.14 (b) and A69 - A75)

The organisational structure does not address areas of responsibility and lines of reporting to support effective controlover financial reporting. 1

Management and staff are not assigned appropriate levels of authority and responsibility to facilitate control overfinancial reporting. 2

Human resource policies do not facilitate effective recruitment and training, disciplining and supervision of personnel. 3

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

25

LEGEND

CE = Control environment (ISA 315.14 (b) and A69 - A75)

Integrity and ethical values have not been developed and are not understood to set the standard for financial reporting. 4

The accounting officer/authority does not exercise oversight responsibility over financial reporting and internal control. 5

Management philosophy and operating style do not promote effective control over financial reporting. 6

The entity does not have individuals competent in financial reporting and related matters. 7

RA = Risk assessment

Management has not specified financial reporting objectives to enable the identification of risks to reliable financialreporting. 1

The entity does not identify risks to the achievement of financial reporting objectives. 2

The entity does not analyse the likelihood and impact of the risks identified. 3

The entity does not determine a risk strategy/action plan to manage identified risks. 4

The potential for material misstatement due to fraud is not considered. 5

CA = Control activities

There is inadequate segregation of duties to prevent fraudulent data and asset misappropriation. 1

General information technology controls have not been designed to maintain the integrity of the information systemand security of the data. 2

Manual or automated controls are not designed to ensure that the transactions occurred, are authorised, and arecompletely and accurately processed. 3

Actions are not taken to address risks to the achievements of financial reporting objectives. 4

Control activities are not selected and developed to mitigate risks over financial reporting. 5

Policies and procedures related to financial reporting are not established and communicated. 6

Realistic targets are not set for financial performance measures, which are in turn not linked to an effective rewardsystem. 7

IC = Information and communication

Pertinent information is not identified and captured in a form and time frame to support financial reporting. 1

Information required to implement internal control is not available to personnel to enable internal control responsibilities. 2

Communications do not enable and support the understanding and execution of internal control processes andresponsibilities by personnel. 3

M = Monitoring

Ongoing monitoring and supervision are not undertaken to enable an assessment of the effectiveness of internalcontrol over financial reporting. 1

Reviews by internal audit, the audit committee or self-assessment are not evident. 2

Internal control deficiencies are not identified and communicated in a timely manner to allow for corrective action tobe taken. 3

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

26

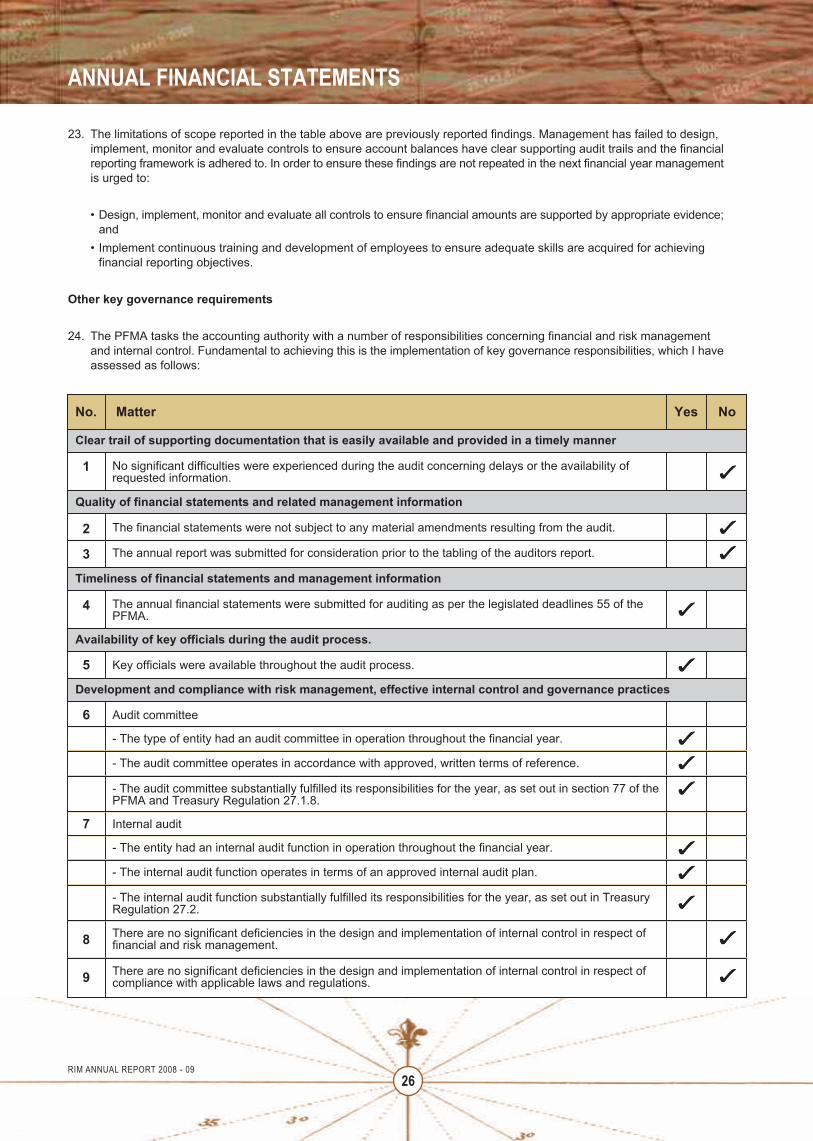

23. The limitations of scope reported in the table above are previously reported findings. Management has failed to design,implement, monitor and evaluate controls to ensure account balances have clear supporting audit trails and the financialreporting framework is adhered to. In order to ensure these findings are not repeated in the next financial year managementis urged to:

• Design, implement, monitor and evaluate all controls to ensure financial amounts are supported by appropriate evidence;and

• Implement continuous training and development of employees to ensure adequate skills are acquired for achieving financial reporting objectives.

Other key governance requirements

24. The PFMA tasks the accounting authority with a number of responsibilities concerning financial and risk managementand internal control. Fundamental to achieving this is the implementation of key governance responsibilities, which I haveassessed as follows:

No.

No significant difficulties were experienced during the audit concerning delays or the availability ofrequested information.

Matter Yes No

1

The financial statements were not subject to any material amendments resulting from the audit.2

The annual report was submitted for consideration prior to the tabling of the auditors report.3

The annual financial statements were submitted for auditing as per the legislated deadlines 55 of thePFMA.

4

Key officials were available throughout the audit process.5

Audit committee6

- The type of entity had an audit committee in operation throughout the financial year.

- The audit committee operates in accordance with approved, written terms of reference.

- The audit committee substantially fulfilled its responsibilities for the year, as set out in section 77 of thePFMA and Treasury Regulation 27.1.8.

Internal audit7

- The entity had an internal audit function in operation throughout the financial year.

- The internal audit function operates in terms of an approved internal audit plan.

- The internal audit function substantially fulfilled its responsibilities for the year, as set out in TreasuryRegulation 27.2.

There are no significant deficiencies in the design and implementation of internal control in respect offinancial and risk management.8

There are no significant deficiencies in the design and implementation of internal control in respect ofcompliance with applicable laws and regulations.9

Clear trail of supporting documentation that is easily available and provided in a timely manner

Quality of financial statements and related management information

Timeliness of financial statements and management information

Availability of key officials during the audit process.

Development and compliance with risk management, effective internal control and governance practices

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

27

25. Although management made an attempt to correct the errors identified during the prior year’s audit, the root causes forthese findings have not been adequately addressed in all instances. Management tends to react on findings raised byinternal and external audit rather than being proactive and implementing preventative controls and establishing a functionalcontrol environment. The entity also does not have enough individuals competent in financial reporting and related mattersto ensure financial reporting objectives are reached.

Investigations

26. The entity initiated 11 separate investigations (3 investigations started in prior year and 8 in the current year) relating toemployee disciplinary procedures. At the date of this report 4 investigations and proceedings have been concluded andthe remainder was still in progress.

REPORT ON OTHER LEGAL AND REGULATORY REQUIREMENTS

Report on performance information

27. I have reviewed the performance information as set out on pages 11 to 17.

The accounting authority’s responsibility for the performance information

28. The accounting authority has additional responsibilities as required by section 55(2)(a) of the PFMA to ensure that theannual report and audited financial statements fairly present the performance against predetermined objectives of thepublic entity.

No.

The information systems were appropriate to facilitate the preparation of the financial statements.

Matter Yes No

10

A risk assessment was conducted on a regular basis and a risk management strategy, which includesa fraud prevention plan, is documented and used as set out in Treasury Regulation 27.2.

11

Powers and duties have been assigned as set out in section 56 of the PFMA.12

Development and compliance with risk management, effective internal control and governance practices

The prior year audit findings have been substantially addressed.13

Follow-up of audit findings

SCOPA resolutions have been substantially implemented.14

The information systems were appropriate to facilitate the preparation of a performance report that isaccurate and complete.15

Issues relating to the reporting of performance information

Adequate control processes and procedures are designed and implemented to ensure the accuracy andcompleteness of reporting performance information.

16

A strategic plan was prepared and approved for the financial year under review for purposes of monitoringthe performance in relation to the budget and delivery by the RIM against its mandate, predeterminedobjectives, outputs, indicators and targets Treasury Regulation 29.1/30.1.

17

There is a functioning performance management system and performance bonuses are only paid afterproper assessment and approval by those charged with governance.18

The Auditor-General’s responsibility29. I conducted my engagement in accordance with section 13 of the PAA read with General Notice 616 of 2008, issued in

Government Gazette No. 31057 of 15 May 2008.

30. In terms of the foregoing my engagement included performing procedures of an audit nature to obtain sufficient appropriateevidence about the performance information and related systems, process and procedures. The procedures selecteddepend on the auditor’s judgement.

31. I believe that the evidence I have obtained is sufficient and appropriate to provide a basis for the findings reported below.

Findings (performance information)

Non-compliance with regulatory requirements

Lack of reporting on all predetermined objectives in annual report

32. The entity has not reported on all the predetermined objectives, as required by section 55(2)(a) of the PFMA. The followingare examples:

• Conservation of the Built Environment and Movable Collection

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

28

Objective

Transform Institutional capacity

Indicator Target

The rehabilitation of "Die Ou Tronk" "Die Ou Tronk is rehabilitated"

Improve public awareness Rehabilitation of the Old Power Station The Old Power Station is rehabilitated;the RI collection adequately protected.

• Conservation of the Natural Environment

Objective

Provide excellence in heritagemanagement

Indicator Target

Waste Management Bins reflect separation/ recyclinginitiatives. Stakeholders more aware

Lack of effective, efficient and transparent systems and internal controls regarding performance management

33. The accounting authority did not ensure that the entity has and maintains an effective, efficient and transparent systemand internal controls regarding performance management, which describe and represent how the entity’s processes ofperformance planning, monitoring, measurement, review and reporting will be conducted, organized and managed, asrequired in terms of section 51(1)(a)(i) of the PFMA.

No or inadequate quarterly reporting on performance information

34. No quarterly reports on the progress in achieving measurable objectives and targets were prepared by the entity to facilitateeffective performance monitoring, evaluation and corrective action, as required by Treasury Regulation 30.2.1.

Inconsistently reported performance information

35. The entity has not reported on its performance with regard to its indicators and targets as per the approved strategic plan.For all objectives reported on in the annual performance report no targets or indicators were included only objectives andactual achievements.

36. The entity reported on objectives, indicators and targets in addition to those as per the approved strategic plan. Furthermore,these additional objectives, indicators and targets were not included in the approved or adjusted budgets or were notapproved subsequent to the strategic planning process. The following are examples of objectives that were reported onbut not included in the strategic plan;

• Conservation of the Built Environment and Movable Collection

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

29

Priorities/Strategic Objective

Harbour Buildings at Murray's Harbour

Achievements

Completed

Jetty 1 Roof Completed

NMG External completed

M-Berth 80% complete

• Maintain, develop and install multi-perspective site specific installation and exhibitions

Priorities/Strategic Objective

Mainland Exhibitions

Achievements

Curated and hosted the Freedom Day Art Against Apartheid,Mandela Birthday Commemorative and the AutshumatoCommemorative Exhibitions

Report performance information not relevant

37. The following targets and indicators with regard to the conservation objectives were not specific in clearly identifying thenature and the required level of performance, measurable in identifying the nature and the required level of performance,measurable in identifying the required performance and time bound in specifying the time period or deadline for delivery:

• Conservation of the built environment and movable collection• Conservation of the natural environment• Maintain develop and install multi-perspective site specific installations and exhibitions

APPRECIATION

38. The assistance rendered by the staff of the RIM during the audit is sincerely appreciated.

Pretoria31 July 2009

Statement of Responsibility

The Public Finance Management Act, 1999 (Act No. 1 of 1999), as amended, requires the accounting authority to ensure thatthe ROBBEN ISLAND MUSEUM keeps full and proper records of its financial affairs. The annual financial statements should fairlypresent the state of affairs of the ROBBEN ISLAND MUSEUM, its financial results, its performance against predetermined objectivesand its financial position at the end of the year in terms of the basis of accounting as set out in note 1 to the financial statements.

The annual financial statements are the responsibility of the accounting authority. The Auditor-General is responsible for independentlyauditing and reporting on the financial statements. The Auditor-General has audited the entity’s financial statements and theAuditor-General’s report appears on pages 22 to 29.

The annual financial statements have been prepared in accordance with the basis of accounting as set out in note 1 to the financialstatements. These annual financial statements are based on appropriate accounting policies, supported by reasonable and prudentjudgements and estimates.

The accounting authority has reviewed the entity’s budgets and cash flow forecasts for the year ended 31 March 2010. On thebasis of this review, and in view of the current financial position, the accounting authority has every reason to believe that the entitywill be a going concern in the year ahead and has continued to adopt the going concern basis in preparing the financial statements.

The accounting authority sets standards to enable management to meet the above responsibilities by implementing systems ofinternal control and risk management that are designed to provide reasonable, but not absolute assurance against materialmisstatements and losses. The entity maintains internal financial controls to provide assurance regarding:

• The safeguarding of assets against unauthorised use or disposition• The maintenance of proper accounting records and the reliability of financial

information used within the business or for publication.

The controls contain self-monitoring mechanisms, and actions are taken to correct deficiencies as they are identified. Even aneffective system of internal control, no matter how well designed, has inherent limitations, including the possibility of circumventionor the overriding of controls. An effective system of internal control therefore aims to provide reasonable assurance with respectto the reliability of financial information and, in particular, financial statement presentation. Furthermore, because of changes inconditions, the effectiveness of internal financial controls may vary over time.

The accounting authority has reviewed the entity's systems of internal control and risk management for the period from 1 April2008 to 31 March 2009. The accounting authority is of the opinion that the entity's systems of internal control have generallyimproved, however certain internal controls and risk management were identified as being inadequate. Steps will be taken toaddress the identified weaknesses in this financial year.

In the opinion of the accounting authority, based on the information available to date, the annual financial statements fairly presentthe financial position of the Museum at 31 March 2009 and the results of its operations and cash flow information for the year.

The annual financial statements for the year ended 31 March 2009, set out on pages 33 to 68, were submitted for auditing on 31May 2009 and are signed on behalf of the accounting authority by:

______________________________Seelan NaidooChief Executive OfficerDate: 31 May 2009

ANNUAL FINANCIAL STATEMENTS

RIM ANNUAL REPORT 2008 - 09

30

RIM ANNUAL REPORT 2008 - 09

Accounting Authority’s Report for the year ended 31 March 2009

The Accounting Authority presents the annual report, which forms part of the audited financial statements of the Museum for theyear ended 31 March 2009.

Principal activity of the Museum

The sustainable operation of a cultural institution and world heritage site.

Council Members

ANNUAL FINANCIAL STATEMENTS

31

Name of Council Member

N Tsiki, Mr

Position Date appointed

Chairperson

Date resigned

1 October 2007 25 May 2009

C Niehaus, Dr Deputy Chairperson 1 October 2007 25 May 2009

F Mbali, Mr Council Member 1 October 2007 25 May 2009

M Mgxashe, Mr Council Member 1 October 2007 6 May 2009

G Singh, Mr Council Member 1 October 2007 6 May 2009

I Ebrahim, Mr Council Member 1 October 2007 6 May 2009

MS Booi, Mr Council Member 1 October 2007 25 May 2009

E Randall, Ms Council Member 1 October 2007 25 May 2009

PM Molefe, Dr Council Member 1 October 2007 13 December 2008

P Dexter, Mr Council Member 1 October 2007 22 May 2009

E Godongwana, Mr Council Member 1 October 2007 16 May 2009

B Mydral, Mr Council Member 1 October 2007 26 February 2008

T Sandwith, Mr Council Member 1 October 2007 26 February 2008

D Stevens, Mr Council Member 1 October 2007 25 May 2009

Council Members

Name of Executive Officers

S Naidoo, Mr

Position Date appointed

Chief Executive Officer (interim)

Date resigned

21 July 2008 25 May 2009

P Langa, Mr Chief Executive Officer 30 November 2008

J O’Hara, Mr Chief Financial Officer (interim) 14 November 2008

IL Masekwameng, Mr Chief Financial Officer 28 February 2009

D Tungwana, Mr Chief Operations Officer

K Holtzhausen, Mrs Company Secretary 1 February 2009 31 May 2009

ANNUAL FINANCIAL STATEMENTS

32

Government Department

Department of Arts and Culture

Address

Robben Island MuseumNelson Mandela Gateway to Robben Island, ClocktowerV&A Waterfront, Cape Town

PO Box 51806, Waterfront, 8002

Telephone: 021 413 4200Fax: 021 425 0206Website: www.robben-island.org.za

Legal Form

The entity is a schedule 3A Public Entity in terms of the Public Finance Management Act No 1 of 1999 and is governed by theNatural Heritage Resources Act No 18 of 1999.

Legislative Mandate

The mandate and core business of the Robben Island Museum (RIM), is underpinned by the Constitution and all other relevantlegislation and policies applicable to government departments.

The specific mandate of Robben Island Museum is derived from the following Acts, Policies, Treaties and Conventions:

The National Heritage Resources Act, 1999The Cultural Institutions Act, 1998The National Monuments Act, 1969The World Heritage Convention Act, 1999The Public Finance Management Act, 1999The National Environmental Management Act, 1998Cape Nature and Environmental Conservation Ordinance, 1974Conservation of Agriculture Resources Act, 1983Marine Living Resources Act, 1998Environment Conservation Act, 1989Sea-shore Act, 1935National Veld and Forest Fire Act, 1998National Water Act, 1998

______________________________Seelan NaidooChief Executive OfficerDate: 31 May 2009

Materiality and Significance Framework for the 2008-09 Financial Year

In terms of the PFMA and National Treasury Regulation 28.1.5, the Council has developed and agreed to a framework of acceptablelevels of materiality and significance.

RIM ANNUAL REPORT 2008 - 09