ANNUAL FINANCIAL REPORT For the Year Ended District/IL Glen Ellyn Public Library... · MAJOR...

61

GLEN ELLYN PUBLIC LIBRARY GLEN ELLYN, ILLINOIS ANNUAL FINANCIAL REPORT For the Year Ended December 31, 2015

Transcript of ANNUAL FINANCIAL REPORT For the Year Ended District/IL Glen Ellyn Public Library... · MAJOR...

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

ANNUAL FINANCIAL REPORT

For the Year Ended December 31, 2015

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

TABLE OF CONTENTS

Page(s)

INDEPENDENT AUDITOR’S REPORT ............................................................................ 1-2

GENERAL PURPOSE EXTERNAL FINANCIAL STATEMENTS

Management’s Discussion and Analysis .................................................................. MD&A 1-11

Basic Financial Statements

Government-Wide Financial Statements

Statement of Net Position ................................................................................... 3

Statement of Activities ....................................................................................... 4

Fund Financial Statements

Governmental Funds

Balance Sheet ..................................................................................................... 5-6

Reconciliation of Fund Balances of Governmental Funds to

the Governmental Activities in the Statement of Net Position ....................... 7

Statement of Revenues, Expenditures and Changes in Fund Balances ............ 8-9

Reconciliation of the Governmental Funds Statement of Revenues,

Expenditures and Changes in Fund Balances to the Governmental

Activities in the Statement of Activities .......................................................... 10

Notes to Financial Statements ...................................................................................... 11-25

Required Supplementary Information

Schedule of Revenues, Expenditures and

Changes in Fund Balance - Budget and Actual - General Fund ............................ 26

Illinois Municipal Retirement Fund

Schedule of Employer Contributions ................................................................. 27

Schedule of Changes in the Library’s Proportionate Share

Of the Net pension Liability ............................................................................. 28

Notes to Required Supplementary Information ....................................................... 29

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

TABLE OF CONTENTS (Continued)

Page(s)

COMBINING AND INDIVIDUAL FUND

FINANCIAL STATEMENTS AND SCHEDULES

MAJOR GOVERNMENTAL FUNDS

Schedule of Expenditures - Budget and Actual

General Fund ........................................................................................................... 30

Schedule of Revenues, Expenditures and Changes in Fund Balance -

Budget and Actual

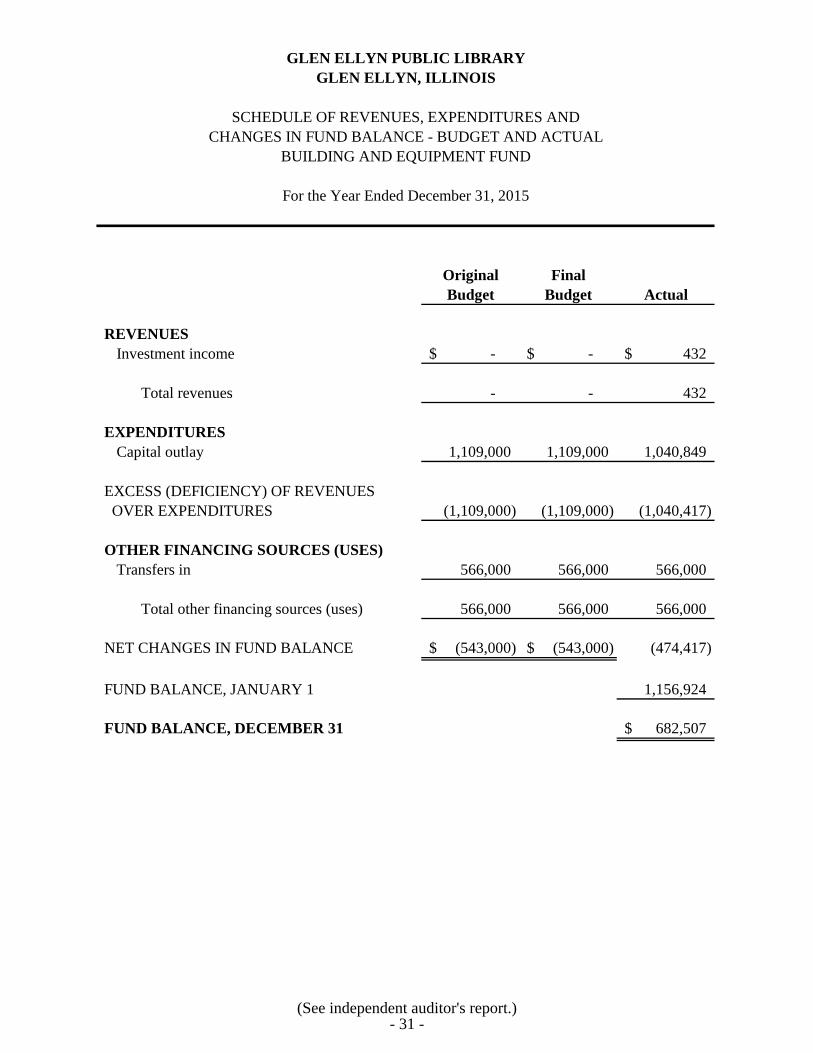

Building and Equipment Fund ................................................................................ 31

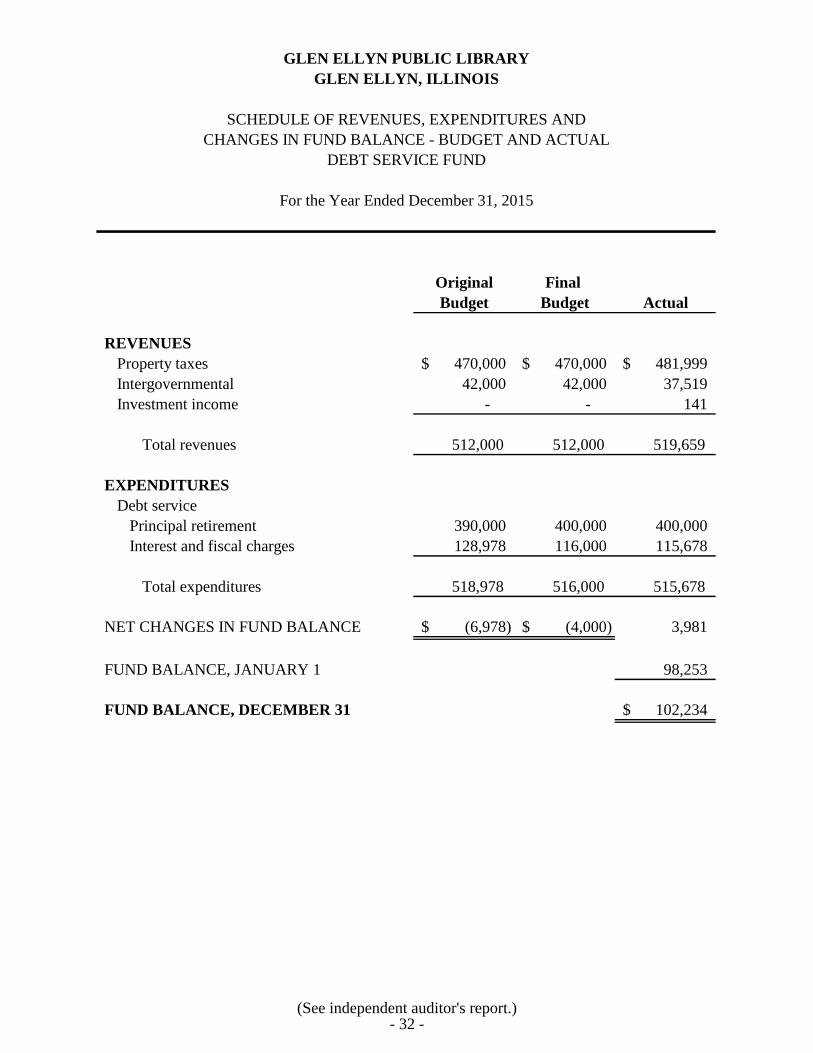

Debt Service Fund ................................................................................................... 32

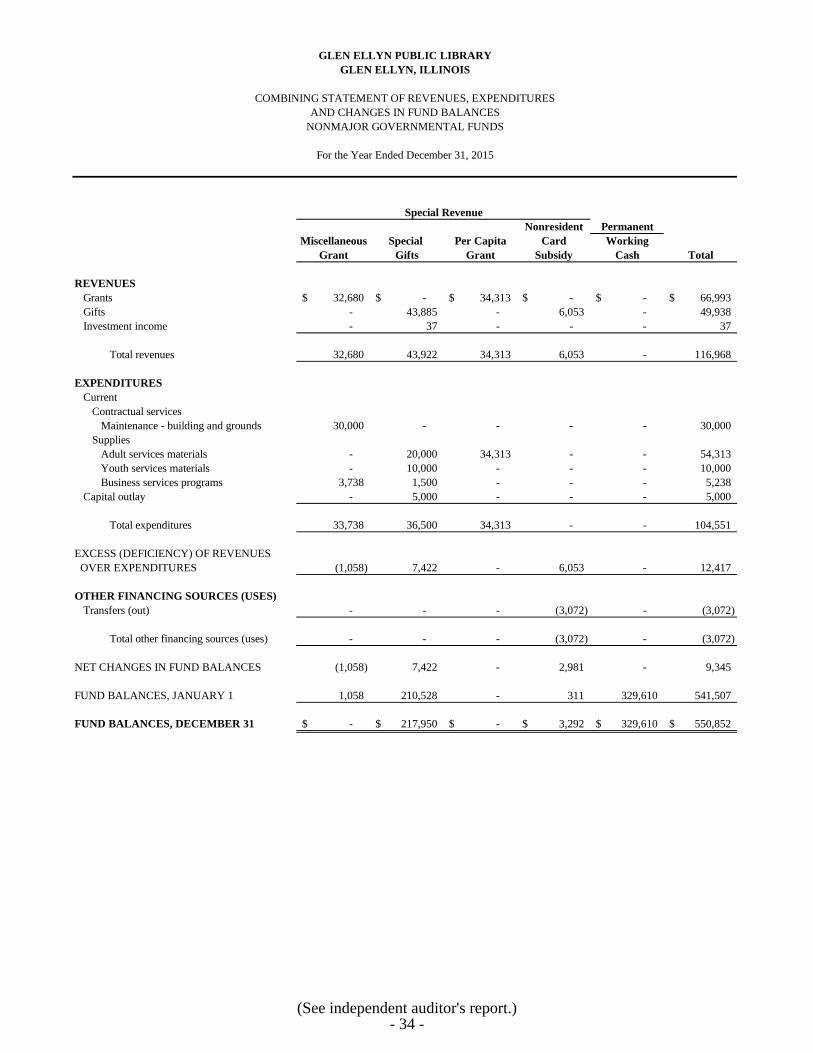

NONMAJOR GOVERNMENTAL FUNDS

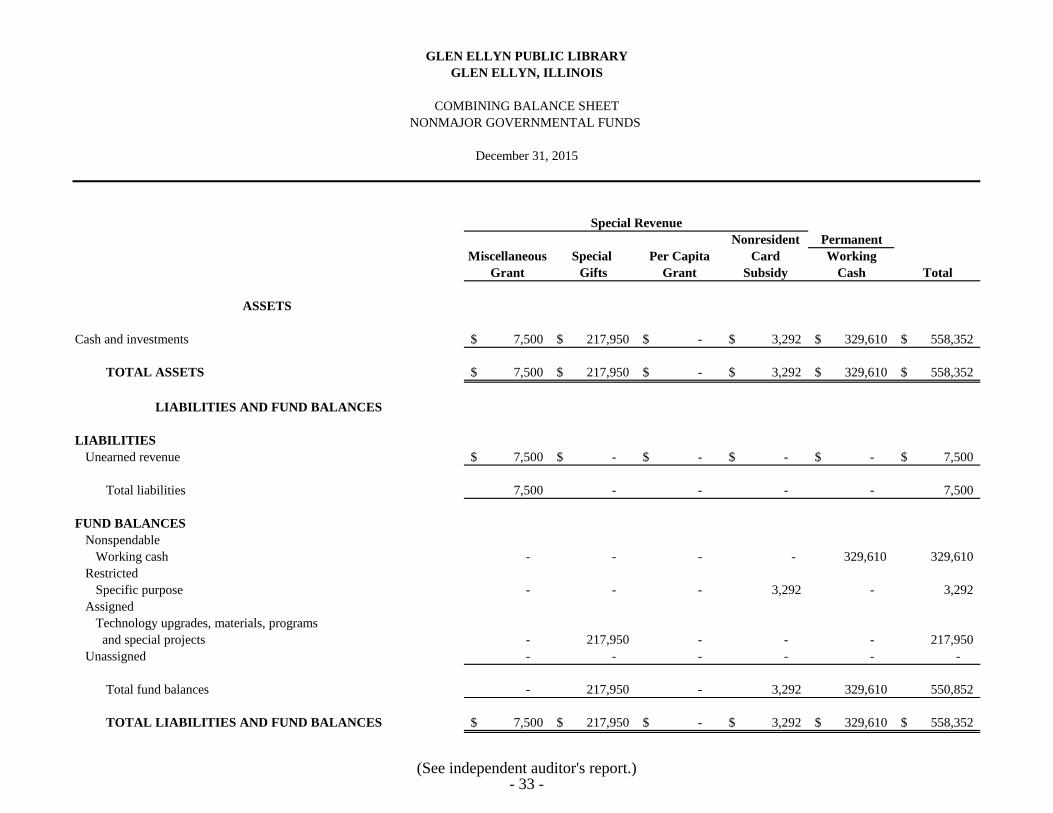

Combining Balance Sheet ............................................................................................ 33

Combining Statement of Revenues, Expenditures

and Changes in Fund Balances .................................................................................. 34

Schedule of Revenues, Expenditures and

Changes in Fund Balance - Budget and Actual

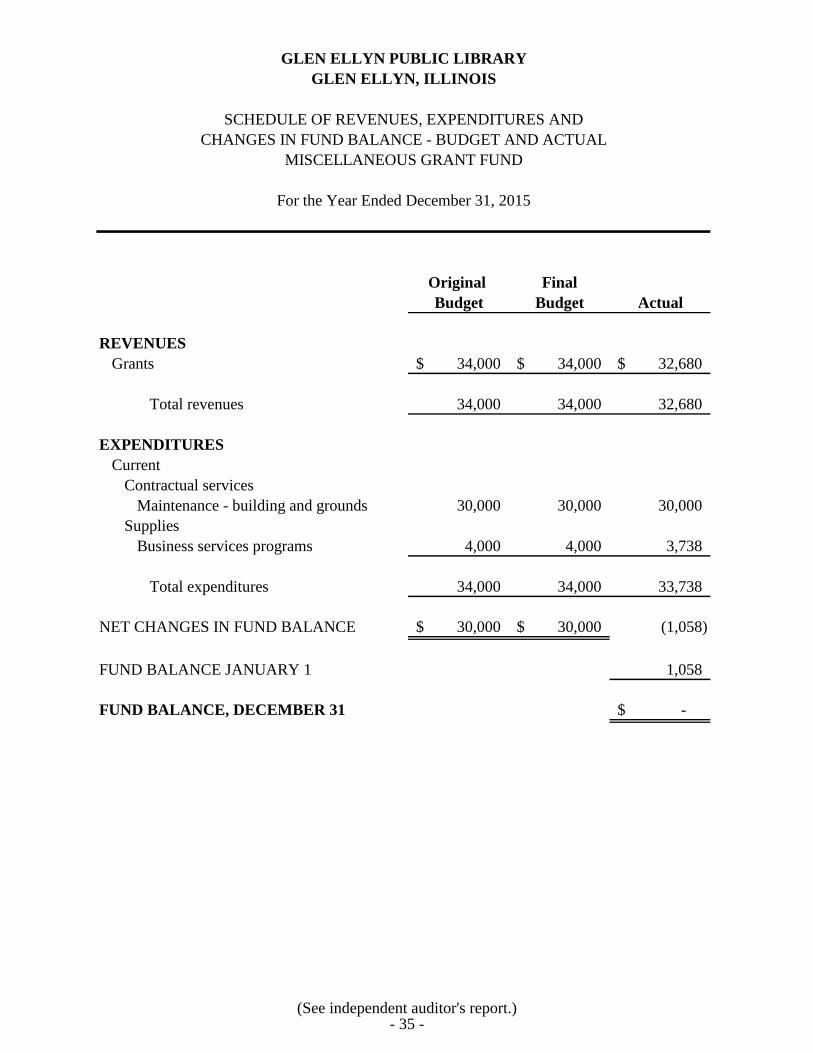

Miscellaneous Grant Fund ...................................................................................... 35

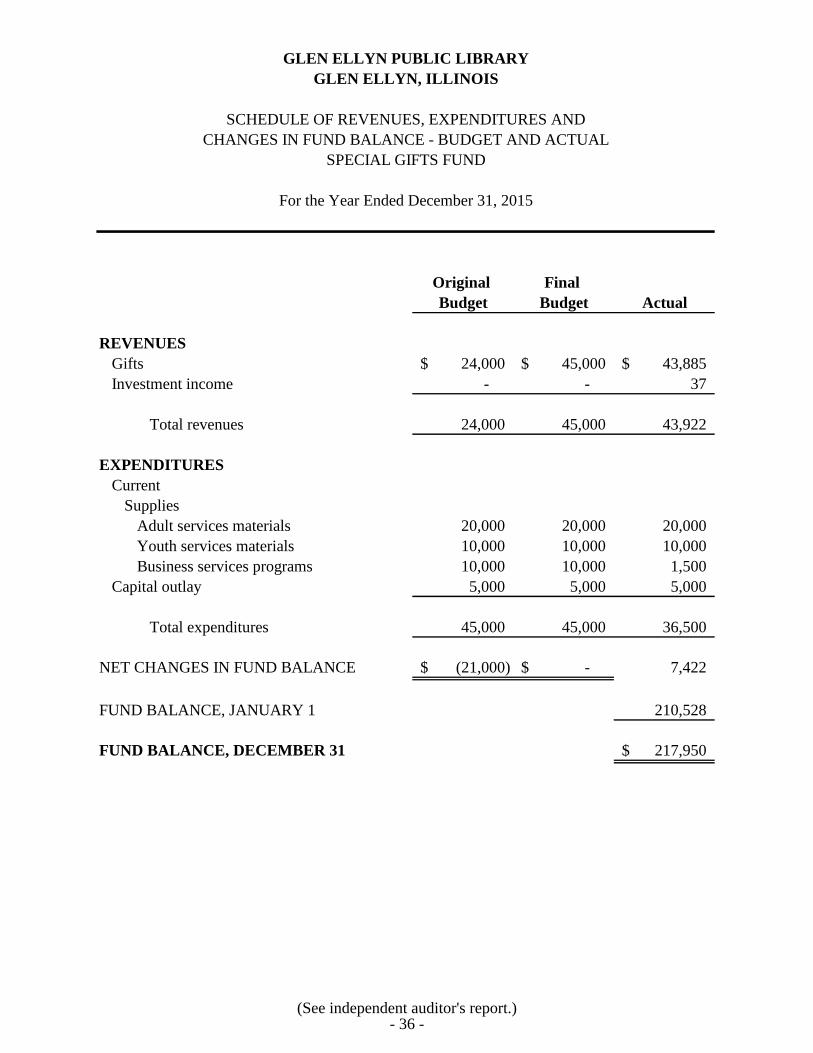

Special Gifts Fund ................................................................................................... 36

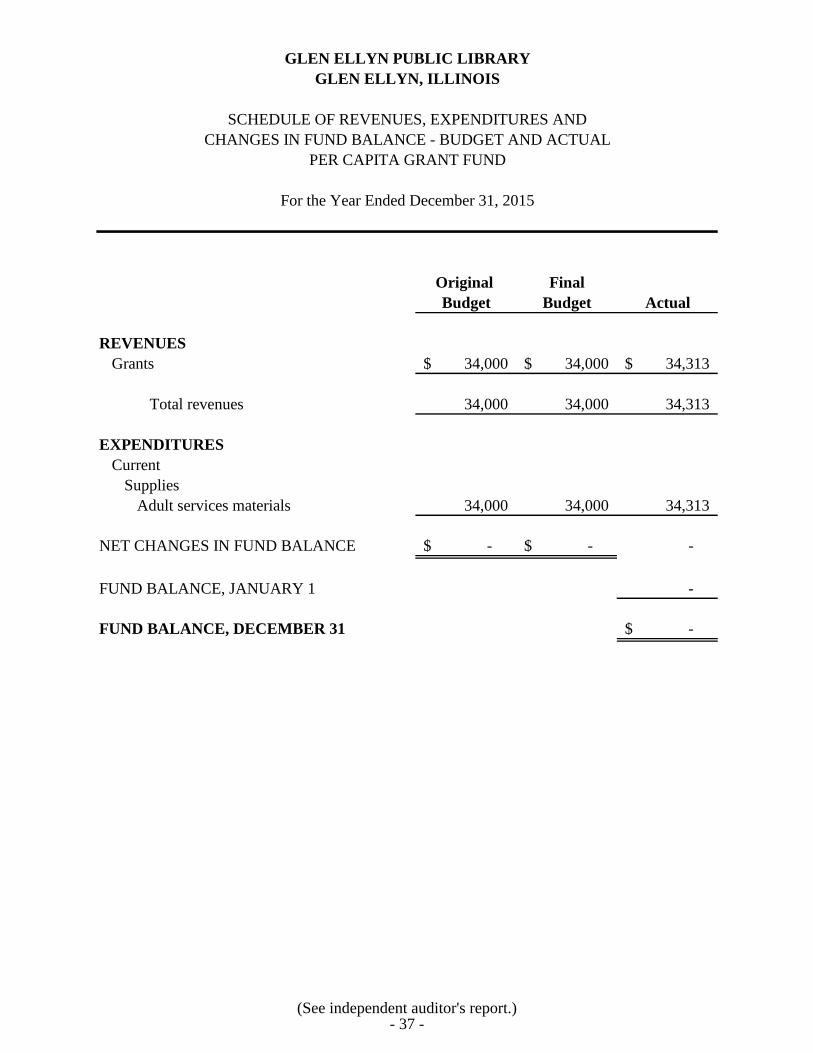

Per Capita Grant Fund ............................................................................................. 37

Nonresident Card Subsidy Fund ............................................................................. 38

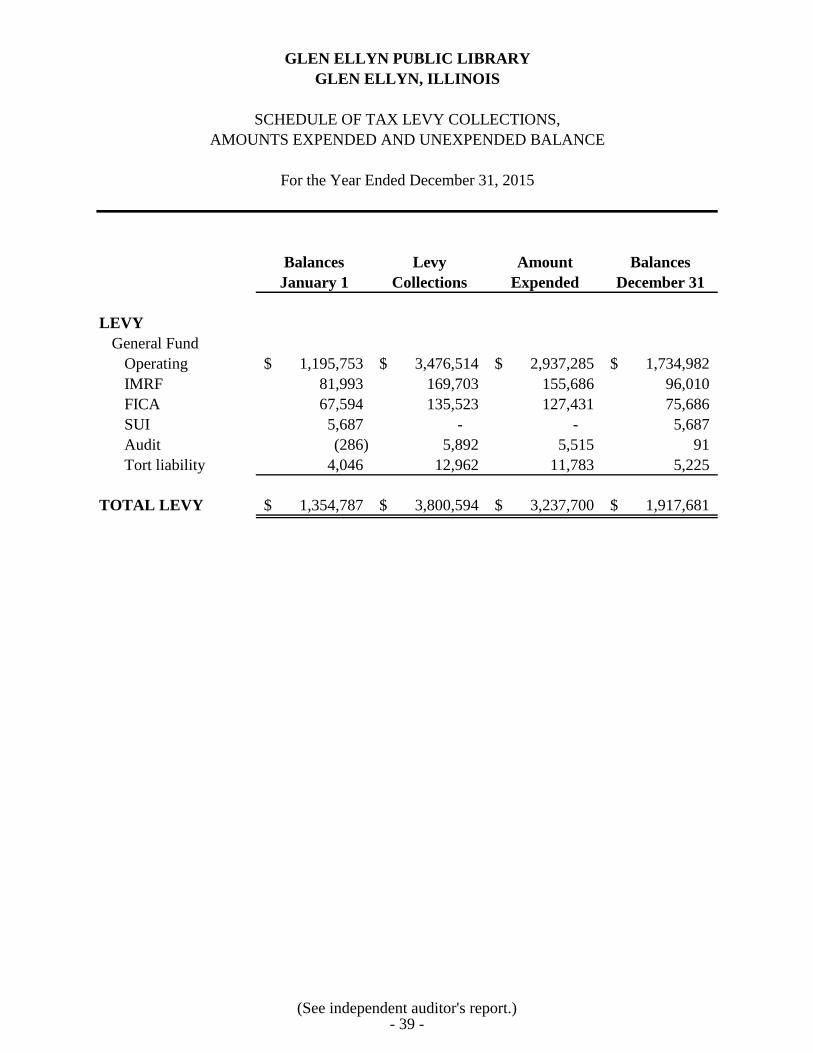

SUPPLEMENTARY INFORMATION

Schedule of Tax Levy Collections, Amounts Expended

and Unexpended Balance ................................................................................................ 39

INDEPENDENT AUDITOR’S REPORT

- 1 -

INDEPENDENT AUDITOR’S REPORT

Members of the Library Board of Trustees

Glen Ellyn Public Library

Glen Ellyn, Illinois

We have audited the accompanying financial statements of the governmental activities, each major

fund and the aggregate remaining fund information of the Glen Ellyn Public Library, Glen Ellyn,

Illinois (the Library), as of the year ended December 31, 2015 and the related notes to financial

statements, which collectively comprise the Library’s basic financial statements as listed in the table

of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with accounting principles generally accepted in the United States of America; this

includes the design, implementation and maintenance of internal control relevant to the preparation

and fair presentation of financial statements that are free from material misstatement, whether due to

fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We

conducted our audit in accordance with auditing standards generally accepted in the United States of

America. Those standards require that we plan and perform the audit to obtain reasonable assurance

about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures

in the financial statements. The procedures selected depend on the auditor’s judgment, including the

assessment of the risks of material misstatement of the financial statements, whether due to fraud or

error. In making those risk assessments, the auditor considers internal control relevant to the

Library’s preparation and fair presentation of the financial statements in order to design audit

procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion

on the effectiveness of the Library’s internal control. Accordingly, we express no such opinion. An

audit also includes evaluating the appropriateness of accounting policies used and the reasonableness

of significant accounting estimates made by management, as well as evaluating the overall

presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis

for our audit opinions.

- 1 -

- 2 -

Opinions In our opinion, the basic financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, each major fund and the aggregate remaining fund information of the Glen Ellyn Public Library, Glen Ellyn, Illinois as of December 31, 2015 and the respective changes in financial position for the year then ended in conformity with accounting principles generally accepted in the United States of America. Change in Accounting Principle As discussed in Note 11, the Library adopted GASB Statement No. 68, Accounting and Financial Reporting for Pensions, which established standards for measuring and recognizing liabilities, deferred inflows and outflows of resources and expenses; modified certain disclosures in the notes to financial statement; and the required supplementary information. Our opinion is not modified with respect to his matter.

Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis and the other required supplementary information listed in the table of contents be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Library’s basic financial statements. The combining and individual fund financial statements and schedules and supplementary information are presented for purposes of additional analysis and are not a required part of the basic financial statements. The combining and individual fund financial statements and schedules and supplementary information are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. The information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the basic financial statements as a whole. Naperville, Illinois June 9, 2016

- 2 -

GENERAL PURPOSE EXTERNAL FINANCIAL STATEMENTS

(See independent auditor’s report)

- MD&A 1 -

GLEN ELLYN PUBLIC LIBRARY

MANAGEMENT’S DISCUSSION AND ANALYSIS

December 31, 2015

As the management of the Glen Ellyn Public Library (the “Library”), we offer readers of

the Library’s financial statements this narrative overview and analysis of the financial

activities of the Library for the fiscal year ended December 31, 2015. We encourage

readers to consider the information presented here in conjunction with additional

information that we have furnished in the Library’s Financial Statements (beginning on

page 3).

This discussion and analysis is designed to (1) assist the reader in focusing on significant

financial issues, (2) provide an overview of the Library’s financial activity, (3) identify

changes in the Library’s financial position (its ability to address the next and subsequent

year’s challenges), (4) identify any material deviations from the financial plan (the

approved budget), and (5) identify individual fund issues or concerns.

It is of the utmost importance when reviewing the information here as well as the

Library’s Financial Statements to take into consideration the fact that the previous fiscal

year being used for comparison includes financial information pertaining to May 1, 2014

thru December 31, 2014 (referred to as SY2014 during the course of this report), and

therefore only reflects eight months of financial data whereas the year closed

December 31, 2015 (referred to as FY2015) contains twelve months of data. Comparing

financial reports or statements to the previous fiscal year will not be a fully accurate

comparison.

USING THE FINANCIAL SECTION OF THIS ANNUAL REPORT

Historically, the primary focus of local government financial statements has been

summarized fund type information on a current financial resource basis. This approach

was modified by Government Accounting Standards Board Statement No. 34 and was

implemented for the first time for FY2004. The Library’s financial statements now

present two kinds of statements, each with a different snapshot of the Library’s finances.

The focus of the financial statements is now on both the Library as a whole (government-

wide) and on the major individual funds. Both perspectives (government-wide and major

fund) allow the user to address relevant questions, broaden a basis for comparison (year

to year or government to government) and enhance the Library’s accountability.

Government-Wide Financial Statements

The government-wide financial statements are designed to provide readers with a broad

overview of the Library’s finances, in a manner similar to a private-sector business. The

focus of the Statement of Net Position presents information on all of the Library’s assets

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 2 -

and liabilities, with the difference between the two reported as net position. This

statement combines and consolidates governmental fund’s current financial resources

(short-term spendable resources) with capital assets and long-term obligations using the

accrual basis of accounting and economic resources measurement focus. Over time,

increases or decreases in net position may serve as a useful indicator of whether the

financial position of the Library is improving or deteriorating.

The Statement of Activities presents information showing how the Library’s net position

changed during the most recent fiscal year. All changes in net position are reported as

soon as the underlying event giving rise to the change occurs, regardless of the timing of

the cash flows. Thus, revenues and expenses are reported in this statement for some

items that will only result in cash flows in future fiscal periods (e.g., earned but unused

compensated absences).

Fund Financial Statements

Traditional users of governmental financial statements will find the Fund Financial

Statements to be more familiar. The focus of the presentation is on major funds rather

than fund types. A fund is a grouping of related accounts that is used to maintain control

over resources that have been segregated for specific activities or objectives. The

Library, like other state and local governments, uses fund accounting to ensure and

demonstrate compliance with finance-related legal requirements. All of the funds of the

Library are in one category: governmental funds.

Governmental Funds. Governmental funds are used to account for essentially the same

functions reported as governmental activities in the government-wide financial

statements. However, unlike the government-wide financial statements, governmental

fund financial statements focus on near-term inflows and outflows of spendable

resources, as well as balances of spendable resources available at the end of the fiscal

year. Such information may be useful in evaluating a government’s near-term financing

requirements.

Because the focus of governmental funds is narrower than that of the government-wide

financial statements, it is useful to compare the information presented for governmental

funds with similar information presented for governmental activities in the government-

wide financial statements. By doing so, readers may better understand the long-term

impact of the government’s near-term financing decisions. Both the governmental fund

balance sheet and the governmental fund statement of revenues, expenditures, and

changes in fund balances provide a reconciliation to facilitate this comparison between

governmental funds and governmental activities.

The Library maintains nine individual governmental funds. Information is presented

separately in the governmental fund balance sheet and statement of revenues,

expenditures, and changes in fund balances for the General Fund, Debt Service Fund, and

Building and Equipment Fund which were considered to be the “major” funds. Data

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 3 -

from the other six governmental funds are combined into a single, aggregate presentation.

Individual fund data for each of these non-major governmental funds is provided in the

form of combining statements elsewhere in this report.

The Library adopts an annual budget for each of its governmental funds. A budgetary

comparison statement has been provided elsewhere in this report to demonstrate

compliance with the budget. The basic governmental fund financial statements can be

found on pages 3 through 10 of this report.

Notes to the Financial Statements

The notes provide additional information that is essential to a full understanding of the

data provided in the government-wide and fund financial statements. The notes to the

financial statements can be found on pages 11 through 25 of this report.

Other Information

In addition to the basic financial statements and accompanying notes, this report also

presents certain required supplementary information concerning the Library’s progress in

funding its obligation to provide benefits to its employees. Required supplementary

information can be found on pages 26 through 29 of this report.

The combining statements referred to earlier in connection with non-major governmental

funds are presented immediately following the required supplementary information.

Combining and individual fund statements and schedules can be found on pages 30

through 38 of this report.

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 4 -

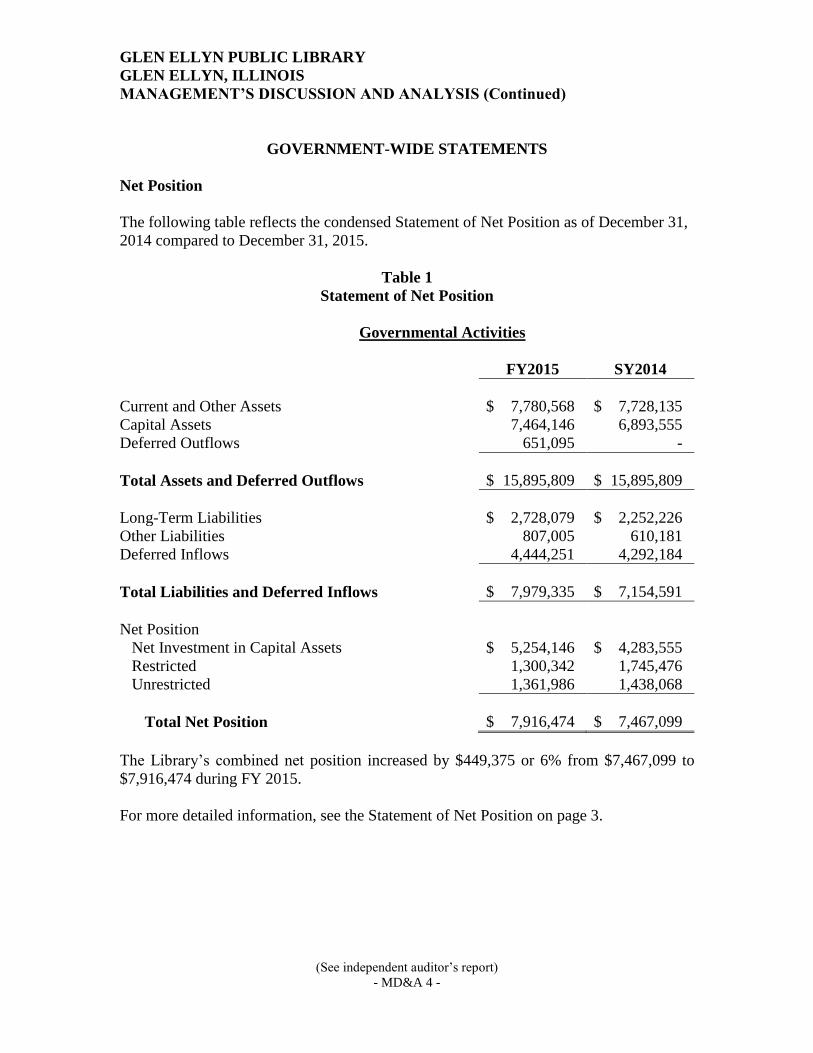

GOVERNMENT-WIDE STATEMENTS

Net Position

The following table reflects the condensed Statement of Net Position as of December 31,

2014 compared to December 31, 2015.

Table 1

Statement of Net Position

Governmental Activities

FY2015 SY2014

Current and Other Assets $ 7,780,568 $ 7,728,135

Capital Assets 7,464,146 6,893,555

Deferred Outflows 651,095 -

Total Assets and Deferred Outflows $ 15,895,809 $ 15,895,809

Long-Term Liabilities $ 2,728,079 $ 2,252,226

Other Liabilities 807,005 610,181

Deferred Inflows 4,444,251 4,292,184

Total Liabilities and Deferred Inflows $ 7,979,335 $ 7,154,591

Net Position

Net Investment in Capital Assets $ 5,254,146 $ 4,283,555

Restricted 1,300,342 1,745,476

Unrestricted 1,361,986 1,438,068

Total Net Position $ 7,916,474 $ 7,467,099

The Library’s combined net position increased by $449,375 or 6% from $7,467,099 to

$7,916,474 during FY 2015.

For more detailed information, see the Statement of Net Position on page 3.

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 5 -

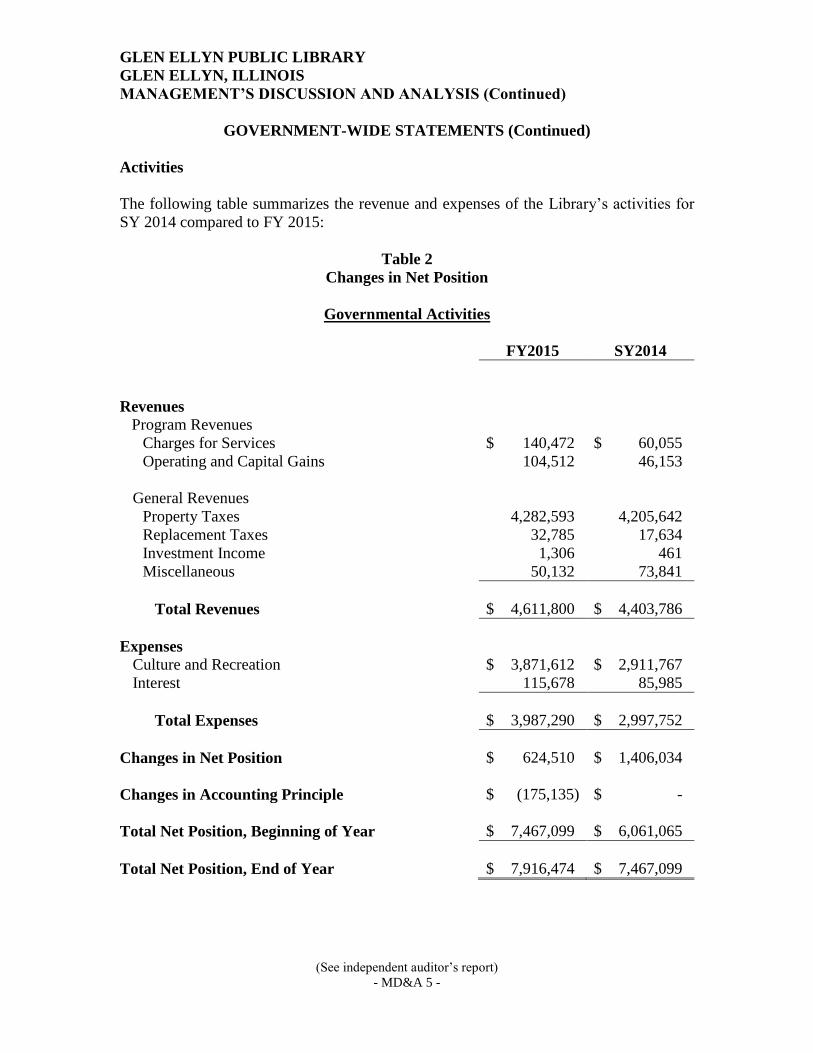

GOVERNMENT-WIDE STATEMENTS (Continued)

Activities

The following table summarizes the revenue and expenses of the Library’s activities for

SY 2014 compared to FY 2015:

Table 2

Changes in Net Position

Governmental Activities

FY2015 SY2014

Revenues

Program Revenues

Charges for Services $ 140,472 $ 60,055

Operating and Capital Gains 104,512 46,153

General Revenues

Property Taxes 4,282,593 4,205,642

Replacement Taxes 32,785 17,634

Investment Income 1,306 461

Miscellaneous 50,132 73,841

Total Revenues $ 4,611,800 $ 4,403,786

Expenses

Culture and Recreation $ 3,871,612 $ 2,911,767

Interest 115,678 85,985

Total Expenses $ 3,987,290 $ 2,997,752

Changes in Net Position $ 624,510 $ 1,406,034

Changes in Accounting Principle $ (175,135) $ -

Total Net Position, Beginning of Year $ 7,467,099 $ 6,061,065

Total Net Position, End of Year $ 7,916,474 $ 7,467,099

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 6 -

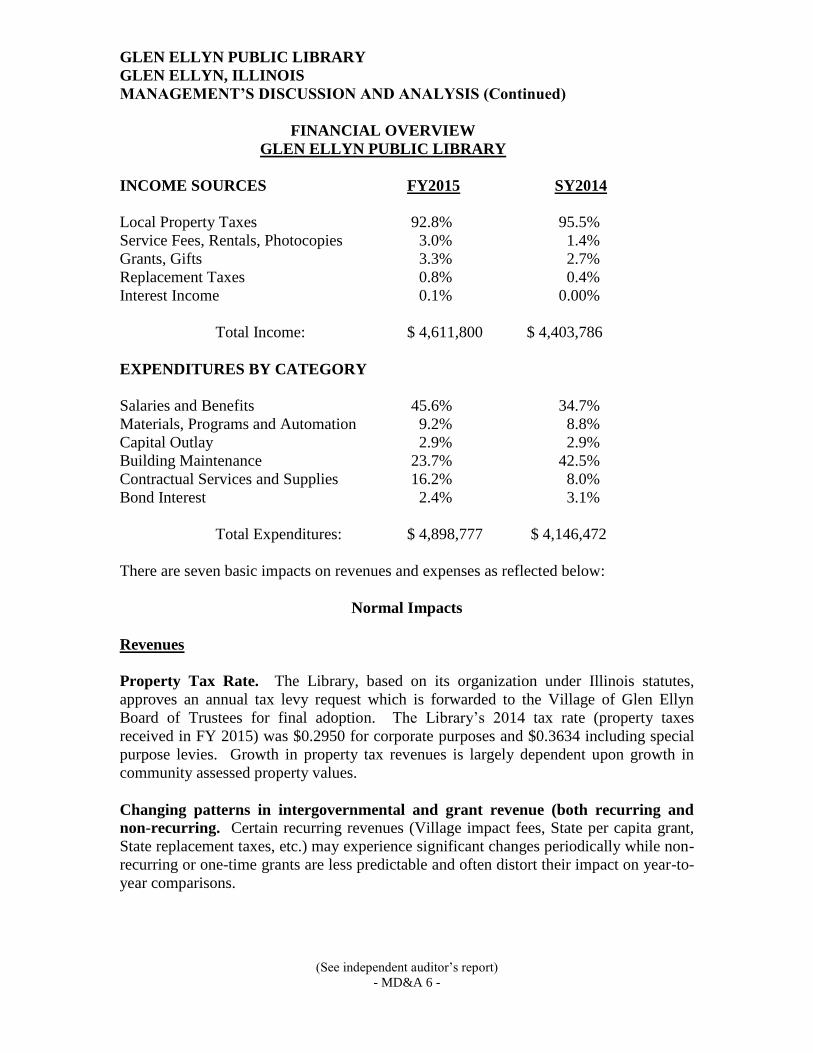

FINANCIAL OVERVIEW

GLEN ELLYN PUBLIC LIBRARY

INCOME SOURCES FY2015 SY2014

Local Property Taxes 92.8% 95.5%

Service Fees, Rentals, Photocopies 3.0% 1.4%

Grants, Gifts 3.3% 2.7%

Replacement Taxes 0.8% 0.4%

Interest Income 0.1% 0.00%

Total Income: $ 4,611,800 $ 4,403,786

EXPENDITURES BY CATEGORY

Salaries and Benefits 45.6% 34.7%

Materials, Programs and Automation 9.2% 8.8%

Capital Outlay 2.9% 2.9%

Building Maintenance 23.7% 42.5%

Contractual Services and Supplies 16.2% 8.0%

Bond Interest 2.4% 3.1%

Total Expenditures: $ 4,898,777 $ 4,146,472

There are seven basic impacts on revenues and expenses as reflected below:

Normal Impacts

Revenues

Property Tax Rate. The Library, based on its organization under Illinois statutes,

approves an annual tax levy request which is forwarded to the Village of Glen Ellyn

Board of Trustees for final adoption. The Library’s 2014 tax rate (property taxes

received in FY 2015) was $0.2950 for corporate purposes and $0.3634 including special

purpose levies. Growth in property tax revenues is largely dependent upon growth in

community assessed property values.

Changing patterns in intergovernmental and grant revenue (both recurring and

non-recurring. Certain recurring revenues (Village impact fees, State per capita grant,

State replacement taxes, etc.) may experience significant changes periodically while non-

recurring or one-time grants are less predictable and often distort their impact on year-to-

year comparisons.

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 7 -

Normal Impacts (Continued) Market impacts on investment income. The Library’s investment portfolio is concentrated in local bank and money market funds similar to many other governments. Market conditions may cause investment income to fluctuate. Most funds are invested in the Illinois Funds accounts, which offer a competitive return, liquidity and safety, requisites of the Library’s investment policy. Expenses Introduction of new programs. Within functional expense categories, individual programs may be added or deleted in order to meet the changing needs of the Library. Changes in authorized personnel. Changes in service demand may cause the Library Board to increase or decrease staffing levels. Personnel costs are the Library’s most significant operating cost. Salary increases (annual adjustments). The ability to attract and retain quality personnel requires the Library to strive to have competitive salary ranges and pay practices. Inflation. While overall inflation has increased, some of the Library’s functions and services may experience unusual commodity-specific increases.

Current Year Impacts

Revenues For the fiscal year ended December 31, 2015, revenues totaled $4,611,800. Property taxes, the Library’s largest single revenue source, amounted to $4,282,593 representing 92.8% of total revenues. Property taxes increased by $76,951 or 1.7% compared to the prior fiscal year 2014. The increase in property tax revenue was used to fund both Library operations and long term capital repairs and replacements. Property values in Glen Ellyn decreased at a rate of .8% in 2014 compared to the 4.2% decrease experienced in 2013. Property taxes received by the Library in FY 2015 represent about 4.2% of the typical Glen Ellyn property tax bill. Expenses The Library’s expenses were $3,987,290 in FY 2015. As required by GASB Statement No. 34, the expense totals include depreciation expense of $378,499 for governmental activities. Because of the Library’s full twelve-month fiscal year cycle, most expense categories increased when compared to the previous short eight-month fiscal year cycle.

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 8 -

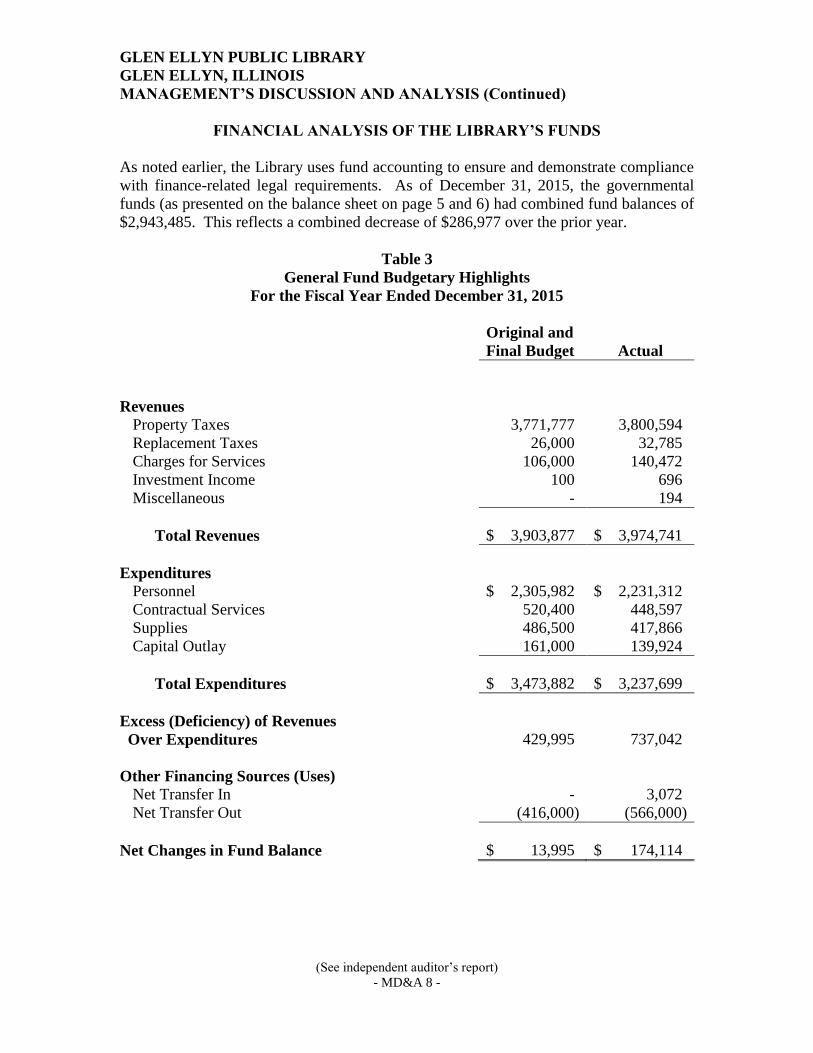

FINANCIAL ANALYSIS OF THE LIBRARY’S FUNDS

As noted earlier, the Library uses fund accounting to ensure and demonstrate compliance

with finance-related legal requirements. As of December 31, 2015, the governmental

funds (as presented on the balance sheet on page 5 and 6) had combined fund balances of

$2,943,485. This reflects a combined decrease of $286,977 over the prior year.

Table 3

General Fund Budgetary Highlights

For the Fiscal Year Ended December 31, 2015

Original and

Final Budget

Actual

Revenues

Property Taxes 3,771,777 3,800,594

Replacement Taxes 26,000 32,785

Charges for Services 106,000 140,472

Investment Income 100 696

Miscellaneous - 194

Total Revenues $ 3,903,877 $ 3,974,741

Expenditures

Personnel $ 2,305,982 $ 2,231,312

Contractual Services 520,400 448,597

Supplies 486,500 417,866

Capital Outlay 161,000 139,924

Total Expenditures $ 3,473,882 $ 3,237,699

Excess (Deficiency) of Revenues

Over Expenditures

429,995

737,042

Other Financing Sources (Uses)

Net Transfer In - 3,072

Net Transfer Out (416,000) (566,000)

Net Changes in Fund Balance $ 13,995 $ 174,114

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 9 -

FINANCIAL ANALYSIS OF THE LIBRARY’S FUNDS (Continued)

General Fund revenues concluded the year over the budgeted amount. Charges for

services exceeded the budgeted amount as well as replacement tax revenue. Impact fees

received from the Village, which are historically difficult to forecast, ended the year

above the budgeted amount due to some new development in the community. Both of

these revenue sources are rather small in relation to the total revenue budget of the

Library.

Transfers were made into the General Fund in the amount of $3,072. The $3,072 was

transferred into the General Fund from the Nonresident Card Subsidy Fund (a special

revenue fund set up to subsidize out of town library cards). This transfer will continue to

occur. Transfers were made out of the General Fund into the Building, Equipment, and

Maintenance Fund in the amount of $566,000. This transfer will continue to occur. The

net amount of transfers equals $562,928.

General Fund expenditures for FY2015 were $236,183 below the adopted expenditure

budget. The largest variance from the General Fund budget was in Personnel. Of the

$2,305,982 budgeted, $2,231,312 was actually spent.

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 10 -

FINANCIAL ANALYSIS OF THE LIBRARY’S FUNDS (Continued)

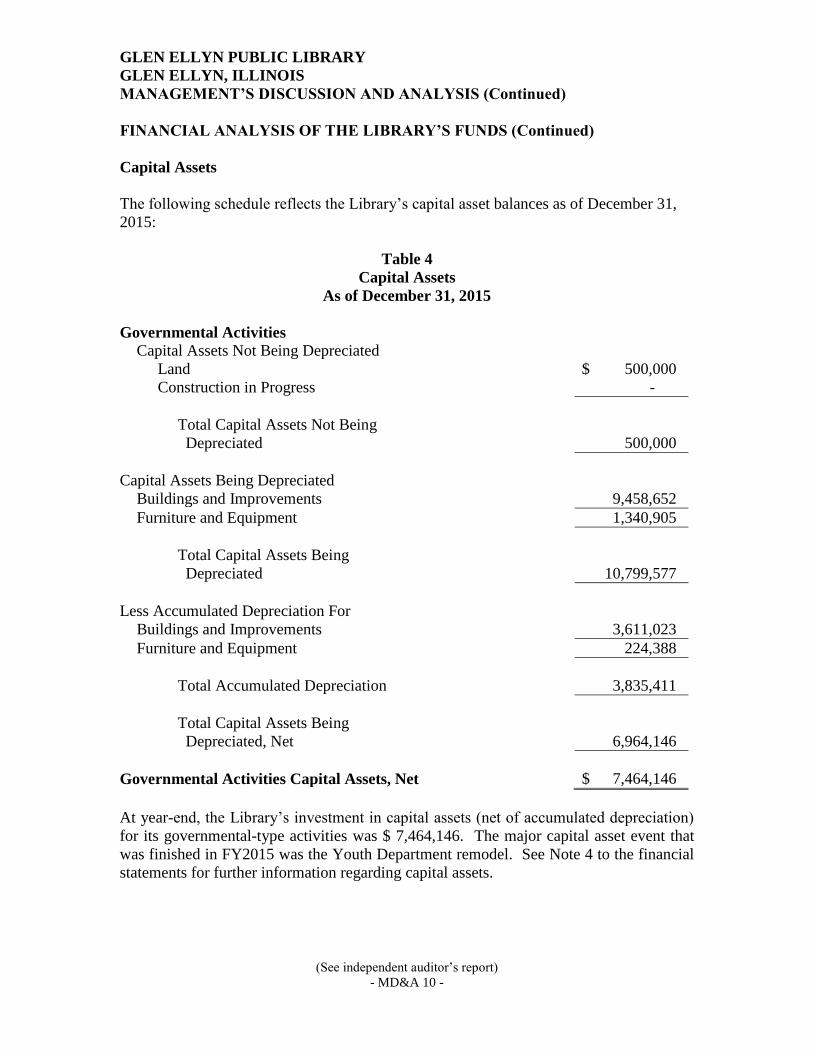

Capital Assets

The following schedule reflects the Library’s capital asset balances as of December 31,

2015:

Table 4

Capital Assets

As of December 31, 2015

Governmental Activities

Capital Assets Not Being Depreciated

Land

Construction in Progress

$ 500,000

-

Total Capital Assets Not Being

Depreciated

500,000

Capital Assets Being Depreciated

Buildings and Improvements 9,458,652

Furniture and Equipment 1,340,905

Total Capital Assets Being

Depreciated

10,799,577

Less Accumulated Depreciation For

Buildings and Improvements 3,611,023

Furniture and Equipment 224,388

Total Accumulated Depreciation 3,835,411

Total Capital Assets Being

Depreciated, Net

6,964,146

Governmental Activities Capital Assets, Net $ 7,464,146

At year-end, the Library’s investment in capital assets (net of accumulated depreciation)

for its governmental-type activities was $ 7,464,146. The major capital asset event that

was finished in FY2015 was the Youth Department remodel. See Note 4 to the financial

statements for further information regarding capital assets.

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

MANAGEMENT’S DISCUSSION AND ANALYSIS (Continued)

(See independent auditor’s report)

- MD&A 11 -

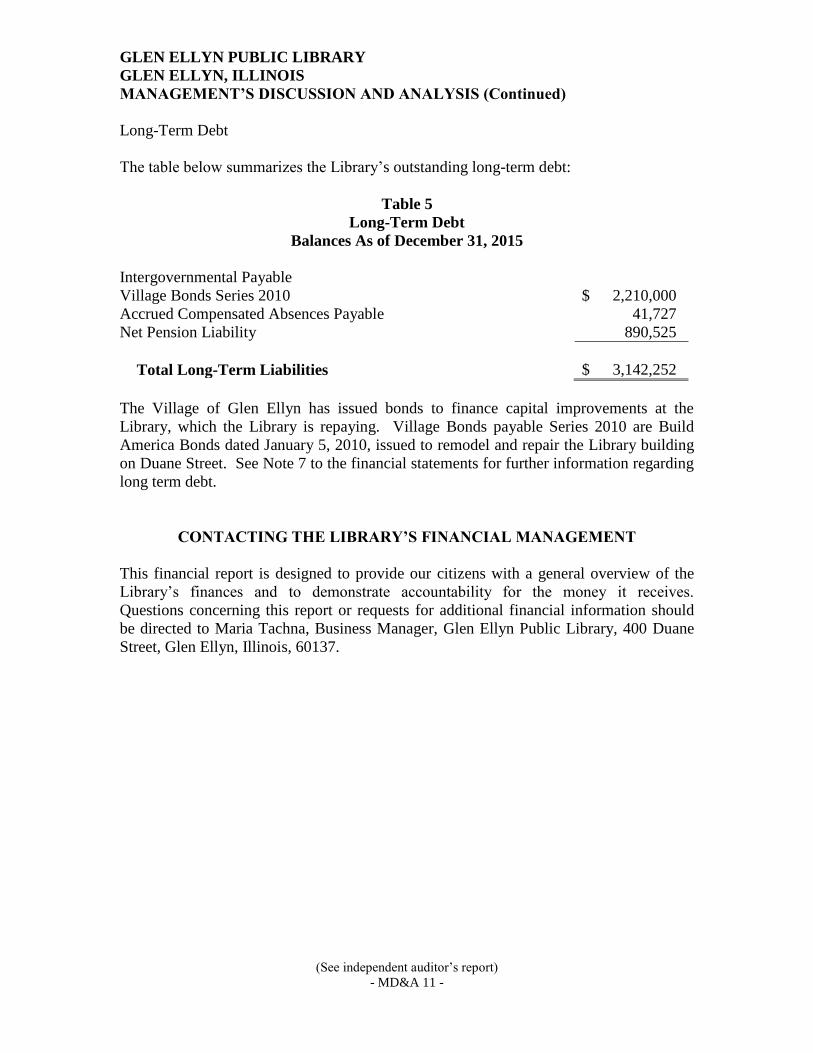

Long-Term Debt

The table below summarizes the Library’s outstanding long-term debt:

Table 5

Long-Term Debt

Balances As of December 31, 2015

Intergovernmental Payable

Village Bonds Series 2010 $ 2,210,000

Accrued Compensated Absences Payable

Net Pension Liability

41,727

890,525

Total Long-Term Liabilities $ 3,142,252

The Village of Glen Ellyn has issued bonds to finance capital improvements at the

Library, which the Library is repaying. Village Bonds payable Series 2010 are Build

America Bonds dated January 5, 2010, issued to remodel and repair the Library building

on Duane Street. See Note 7 to the financial statements for further information regarding

long term debt.

CONTACTING THE LIBRARY’S FINANCIAL MANAGEMENT

This financial report is designed to provide our citizens with a general overview of the

Library’s finances and to demonstrate accountability for the money it receives.

Questions concerning this report or requests for additional financial information should

be directed to Maria Tachna, Business Manager, Glen Ellyn Public Library, 400 Duane

Street, Glen Ellyn, Illinois, 60137.

BASIC FINANCIAL STATEMENTS

Governmental

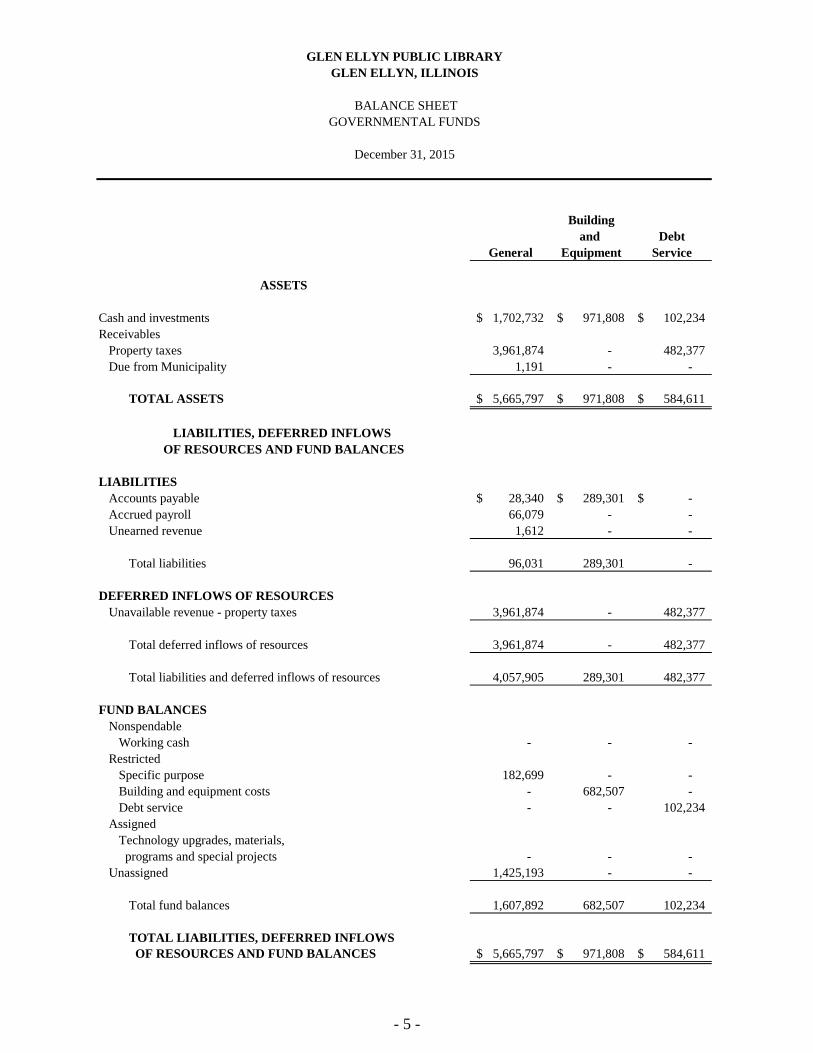

Activities

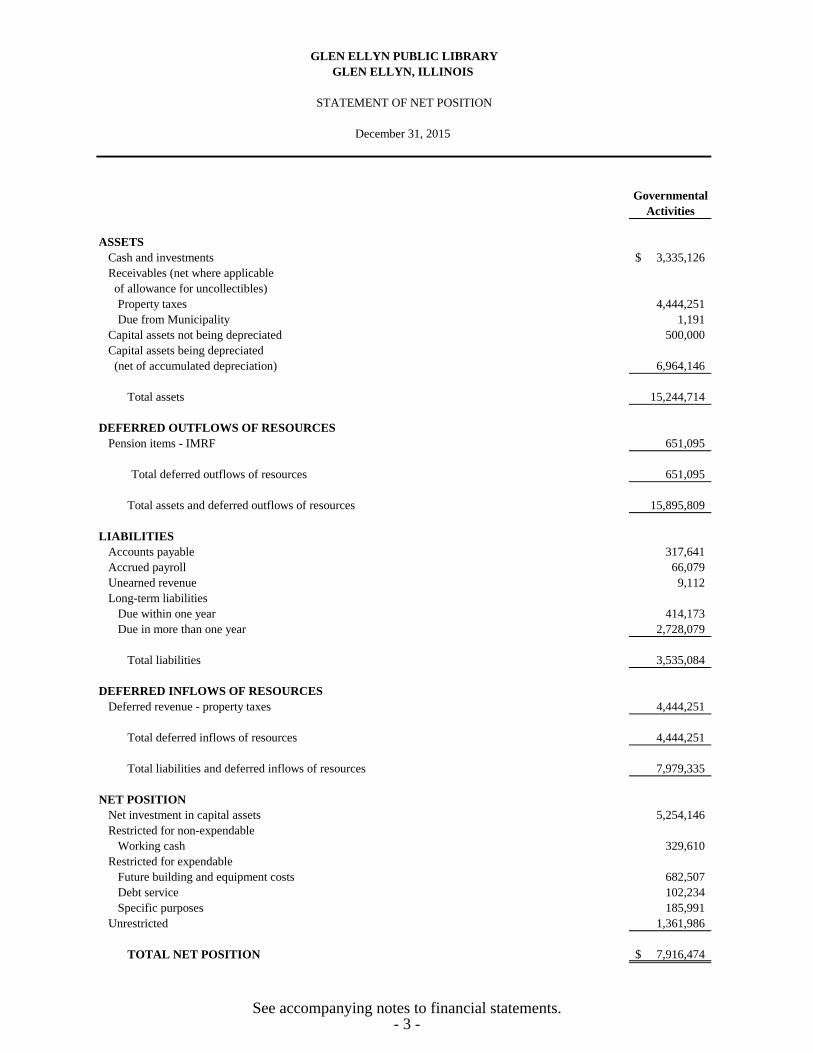

ASSETS

Cash and investments 3,335,126$

Receivables (net where applicable

of allowance for uncollectibles)

Property taxes 4,444,251

Due from Municipality 1,191

Capital assets not being depreciated 500,000

Capital assets being depreciated

(net of accumulated depreciation) 6,964,146

Total assets 15,244,714

DEFERRED OUTFLOWS OF RESOURCES

Pension items - IMRF 651,095

Total deferred outflows of resources 651,095

Total assets and deferred outflows of resources 15,895,809

LIABILITIES

Accounts payable 317,641

Accrued payroll 66,079

Unearned revenue 9,112

Long-term liabilities

Due within one year 414,173

Due in more than one year 2,728,079

Total liabilities 3,535,084

DEFERRED INFLOWS OF RESOURCES

Deferred revenue - property taxes 4,444,251

Total deferred inflows of resources 4,444,251

Total liabilities and deferred inflows of resources 7,979,335

NET POSITION

Net investment in capital assets 5,254,146

Restricted for non-expendable

Working cash 329,610

Restricted for expendable

Future building and equipment costs 682,507

Debt service 102,234

Specific purposes 185,991

Unrestricted 1,361,986

TOTAL NET POSITION 7,916,474$

GLEN ELLYN PUBLIC LIBRARY

STATEMENT OF NET POSITION

December 31, 2015

GLEN ELLYN, ILLINOIS

See accompanying notes to financial statements.- 3 -

Net (Expense)

Revenue and

Change in

Net Position

Operating Capital

Charges Grants and Grants and Governmental

FUNCTIONS/PROGRAMS Expenses for Services Contributions Contributions Activities

PRIMARY GOVERNMENT

Governmental Activities

Culture and recreation 3,871,612$ 140,472$ 71,831$ 32,681$ (3,626,628)$

Interest 115,678 - - - (115,678)

Total governmental activities 3,987,290 140,472 71,831 32,681 (3,742,306)

TOTAL PRIMARY GOVERNMENT 3,987,290$ 140,472$ 71,831$ 32,681$ (3,742,306)

General Revenues

Taxes

Property 4,282,593

Replacement 32,785

Investment income 1,306

Miscellaneous 50,132

Total 4,366,816

CHANGE IN NET POSITION 624,510

NET POSITION, JANUARY 1 7,467,099

Change in accounting principle (175,135)

NET POSITION, MAY 1 - AS RESTATED 7,291,964

NET POSITION, DECEMBER 31 7,916,474$

Program Revenues

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

STATEMENT OF ACTIVITIES

For the Year Ended December 31, 2015

See accompanying notes to financial statements.- 4 -

Building

and Debt

General Equipment Service

Cash and investments 1,702,732$ 971,808$ 102,234$

Receivables

Property taxes 3,961,874 - 482,377

Due from Municipality 1,191 - -

TOTAL ASSETS 5,665,797$ 971,808$ 584,611$

LIABILITIES

Accounts payable 28,340$ 289,301$ -$

Accrued payroll 66,079 - -

Unearned revenue 1,612 - -

Total liabilities 96,031 289,301 -

DEFERRED INFLOWS OF RESOURCES

Unavailable revenue - property taxes 3,961,874 - 482,377

Total deferred inflows of resources 3,961,874 - 482,377

Total liabilities and deferred inflows of resources 4,057,905 289,301 482,377

FUND BALANCES

Nonspendable

Working cash - - -

Restricted

Specific purpose 182,699 - -

Building and equipment costs - 682,507 -

Debt service - - 102,234

Assigned

Technology upgrades, materials,

programs and special projects - - -

Unassigned 1,425,193 - -

Total fund balances 1,607,892 682,507 102,234

TOTAL LIABILITIES, DEFERRED INFLOWS

OF RESOURCES AND FUND BALANCES 5,665,797$ 971,808$ 584,611$

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

BALANCE SHEET

GOVERNMENTAL FUNDS

December 31, 2015

OF RESOURCES AND FUND BALANCES

LIABILITIES, DEFERRED INFLOWS

ASSETS

- 5 -

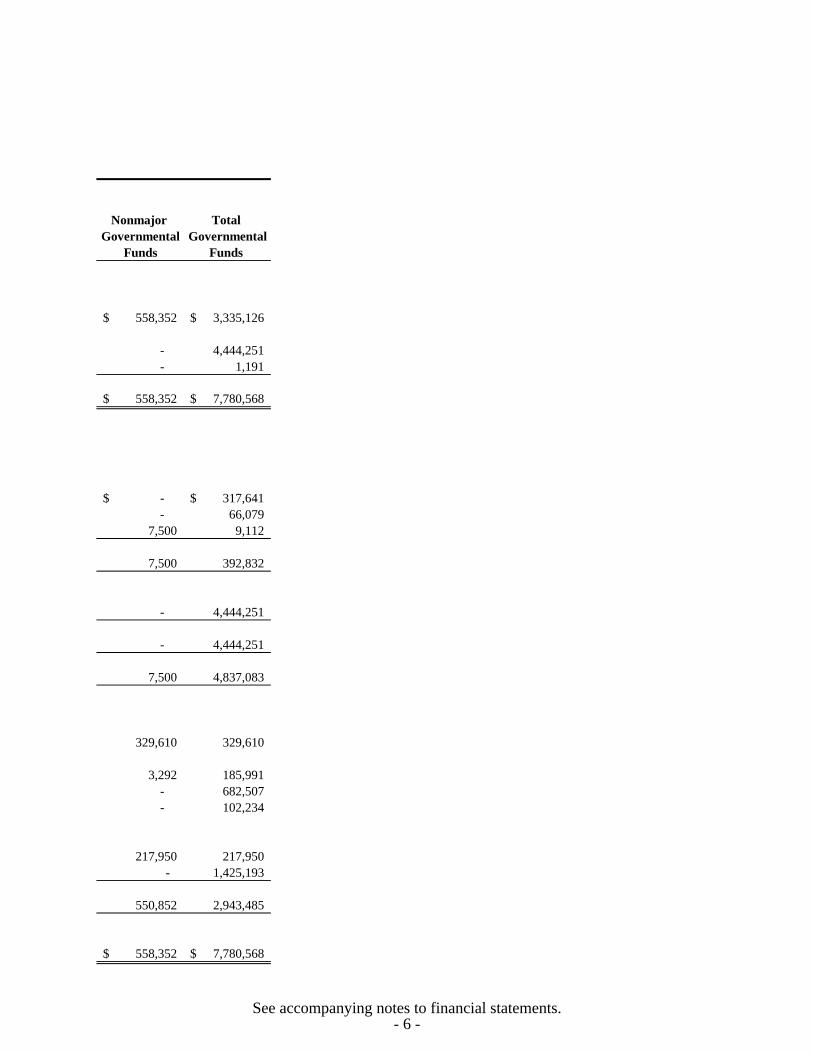

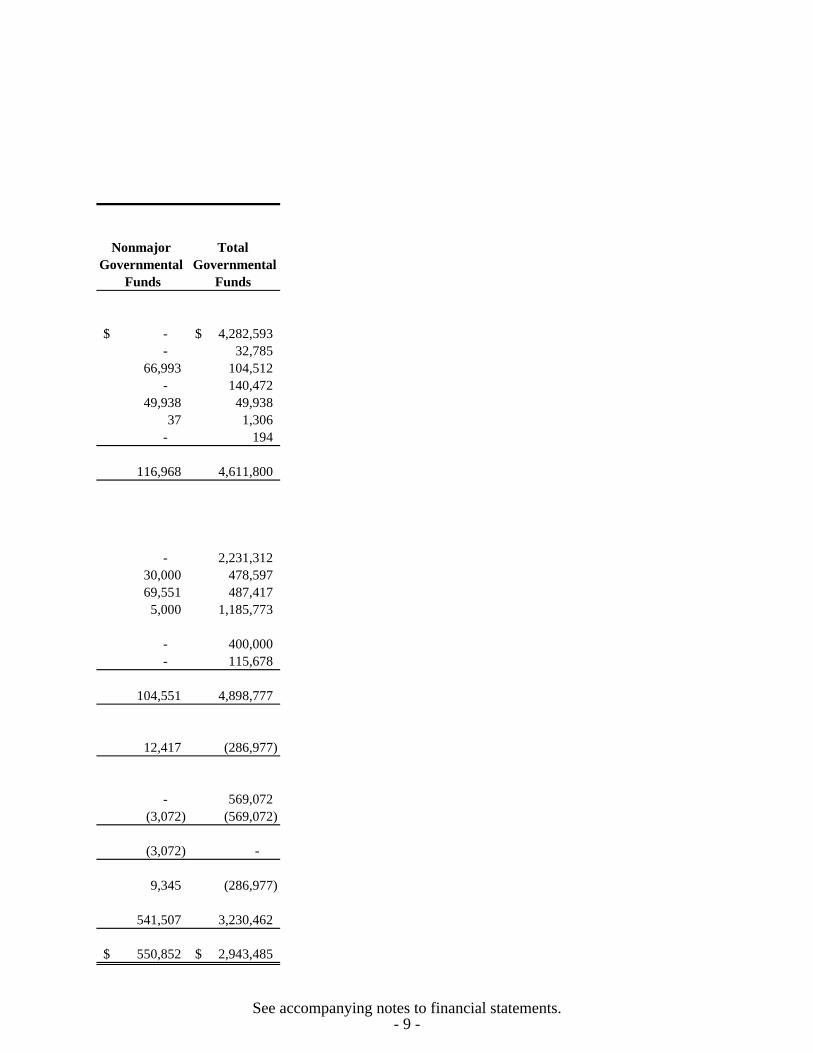

Nonmajor Total

Governmental Governmental

Funds Funds

558,352$ 3,335,126$

- 4,444,251

- 1,191

558,352$ 7,780,568$

-$ 317,641$

- 66,079

7,500 9,112

7,500 392,832

- 4,444,251

- 4,444,251

7,500 4,837,083

329,610 329,610

3,292 185,991

- 682,507

- 102,234

217,950 217,950

- 1,425,193

550,852 2,943,485

558,352$ 7,780,568$

See accompanying notes to financial statements.- 6 -

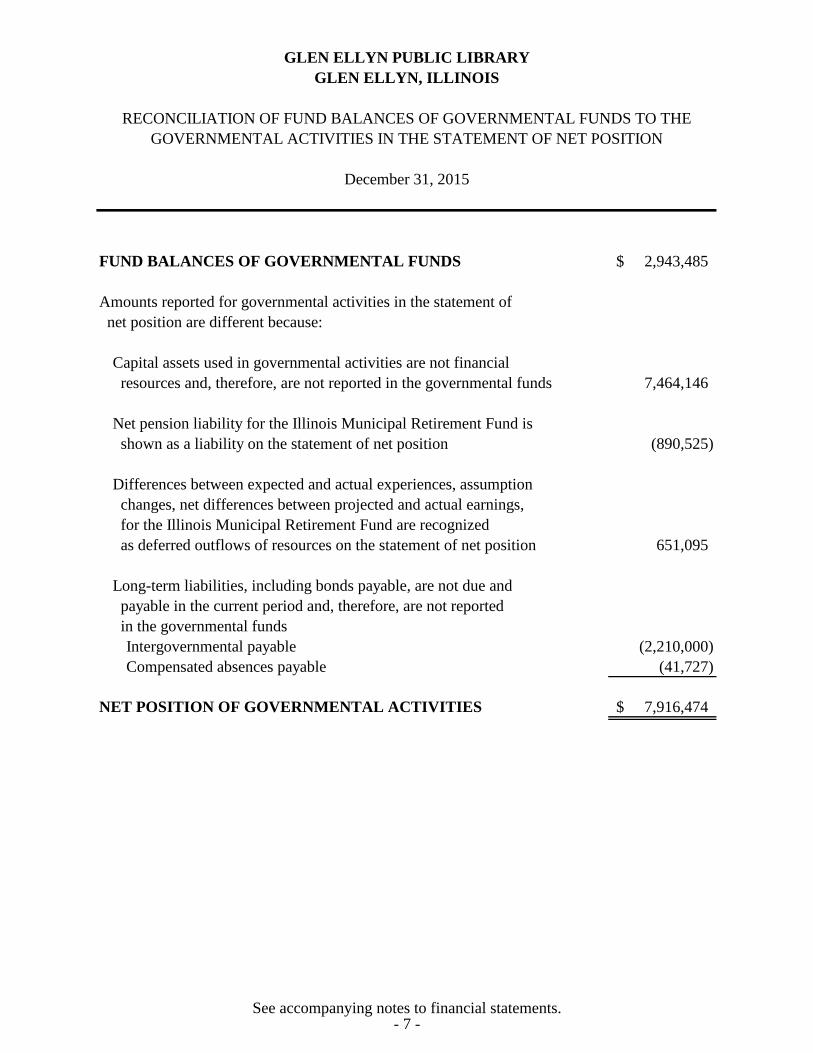

FUND BALANCES OF GOVERNMENTAL FUNDS 2,943,485$

Amounts reported for governmental activities in the statement of

net position are different because:

Capital assets used in governmental activities are not financial

resources and, therefore, are not reported in the governmental funds 7,464,146

Net pension liability for the Illinois Municipal Retirement Fund is

shown as a liability on the statement of net position (890,525)

Differences between expected and actual experiences, assumption

changes, net differences between projected and actual earnings,

for the Illinois Municipal Retirement Fund are recognized

as deferred outflows of resources on the statement of net position 651,095

Long-term liabilities, including bonds payable, are not due and

payable in the current period and, therefore, are not reported

in the governmental funds

Intergovernmental payable (2,210,000)

Compensated absences payable (41,727)

NET POSITION OF GOVERNMENTAL ACTIVITIES 7,916,474$

December 31, 2015

GLEN ELLYN, ILLINOIS

GLEN ELLYN PUBLIC LIBRARY

RECONCILIATION OF FUND BALANCES OF GOVERNMENTAL FUNDS TO THE

GOVERNMENTAL ACTIVITIES IN THE STATEMENT OF NET POSITION

See accompanying notes to financial statements.- 7 -

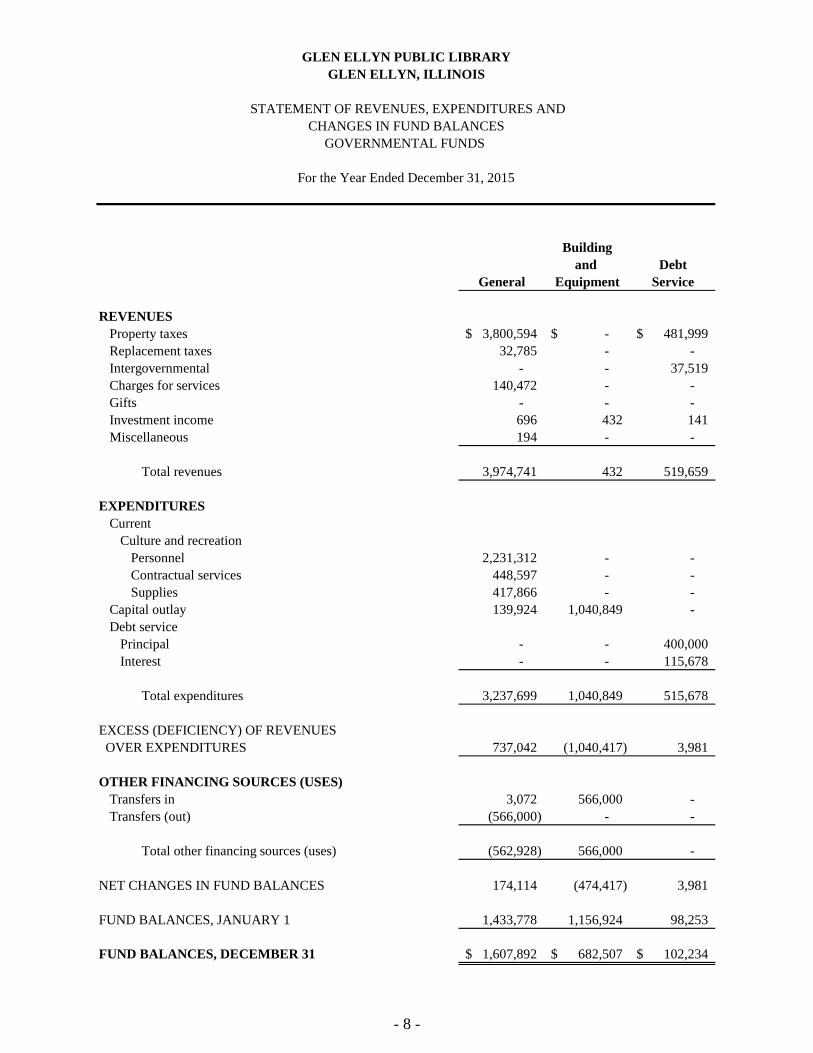

Building

and Debt

General Equipment Service

REVENUES

Property taxes 3,800,594$ -$ 481,999$

Replacement taxes 32,785 - -

Intergovernmental - - 37,519

Charges for services 140,472 - -

Gifts - - -

Investment income 696 432 141

Miscellaneous 194 - -

Total revenues 3,974,741 432 519,659

EXPENDITURES

Current

Culture and recreation

Personnel 2,231,312 - -

Contractual services 448,597 - -

Supplies 417,866 - -

Capital outlay 139,924 1,040,849 -

Debt service

Principal - - 400,000

Interest - - 115,678

Total expenditures 3,237,699 1,040,849 515,678

EXCESS (DEFICIENCY) OF REVENUES

OVER EXPENDITURES 737,042 (1,040,417) 3,981

OTHER FINANCING SOURCES (USES)

Transfers in 3,072 566,000 -

Transfers (out) (566,000) - -

Total other financing sources (uses) (562,928) 566,000 -

NET CHANGES IN FUND BALANCES 174,114 (474,417) 3,981

FUND BALANCES, JANUARY 1 1,433,778 1,156,924 98,253

FUND BALANCES, DECEMBER 31 1,607,892$ 682,507$ 102,234$

GOVERNMENTAL FUNDS

For the Year Ended December 31, 2015

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

STATEMENT OF REVENUES, EXPENDITURES AND

CHANGES IN FUND BALANCES

- 8 -

Nonmajor Total

Governmental Governmental

Funds Funds

-$ 4,282,593$

- 32,785

66,993 104,512

- 140,472

49,938 49,938

37 1,306

- 194

116,968 4,611,800

- 2,231,312

30,000 478,597

69,551 487,417

5,000 1,185,773

- 400,000

- 115,678

104,551 4,898,777

12,417 (286,977)

- 569,072

(3,072) (569,072)

(3,072) -

9,345 (286,977)

541,507 3,230,462

550,852$ 2,943,485$

See accompanying notes to financial statements.- 9 -

NET CHANGES IN FUND BALANCES -

TOTAL GOVERNMENTAL FUNDS (286,977)$

Amounts reported for governmental activities in the statement of

activities are different because:

Governmental funds report capital outlay as expenditures; however,

they are capitalized and depreciated in the statement of activities 949,090

The repayment of the principal portion on long-term debt is reported as

an expenditure when due in governmental funds but as a reduction of

principal outstanding in the statement of activities 400,000

Some expenses in the statement of activities (e.g., depreciation) do not

require the use of current financial resources and, therefore, are not

reported as expenditures in governmental funds (378,499)

The change in compensated absences payable is shown as an expense

on the statement of activities 5,191

The change in the net pension liability for the Illinois Municipal Retirement

Fund is reported only in the statement of activities (715,390)

The change in deferred inflows and outflows of resources for the Illinois

Municipal Retirement Fund is reported only in the statement of activities 651,095

CHANGE IN NET POSITION OF GOVERNMENTAL ACTIVITIES 624,510$

For the Year Ended December 31, 2015

GLEN ELLYN, ILLINOIS

GLEN ELLYN PUBLIC LIBRARY

RECONCILIATION OF THE GOVERNMENTAL FUNDS STATEMENT OF REVENUES,

EXPENDITURES AND CHANGES IN FUND BALANCES TO THE

GOVERNMENTAL ACTIVITIES IN THE STATEMENT OF ACTIVITIES

See accompanying notes to financial statements.- 10 -

- 9 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS

December 31, 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The financial statements of the Glen Ellyn Public Library, Glen Ellyn, Illinois, (the

Library), have been prepared in accordance with accounting principles generally accepted in the United States of America, as applied to governmental units (hereinafter referred to as generally accepted accounting principles (GAAP)). The Governmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing governmental accounting and financial reporting principles. The more significant of the Library’s accounting policies are described below.

a. Reporting Entity The Library is governed by a seven-member Library Board of Trustees that are

separately elected. The Library Board of Trustees selects management staff and directs the affairs of the Library. As required by GAAP, these financial statements include all funds of the Library. Management has also considered all potential component units. Criteria for including a component unit in the Library’s reporting entity principally consist of the potential component unit’s financial interdependency and accountability to the Library. Based upon those criteria, there are no potential component units to be included in the reporting entity.

b. Fund Accounting The accounts of the Library are organized and operated on the basis of funds. A fund

is an independent fiscal and accounting entity with a self-balancing set of accounts. Fund accounting segregates funds according to their intended purpose and is used to aid management in demonstrating compliance with finance related legal and contractual provisions. The minimum numbers of funds are maintained consistent with legal and management requirements.

Funds are classified into the following categories: governmental, proprietary and

fiduciary. All of the Library’s funds are governmental funds. Governmental funds are used to account for all or most of a government’s general

activities, including the collection and disbursement of restricted, committed or assigned monies (special revenue funds), the funds restricted, committed or assigned for the acquisition or construction of capital assets (capital projects funds), the funds committed, restricted or assigned for the servicing of long-term debt (debt service funds) and the management of funds held in trust that can be used for governmental services (permanent fund). The General Fund is used to account for all activities of the Library not accounted for in some other fund.

- 11 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 10 -

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

c. Government-Wide and Fund Financial Statements

The government-wide financial statements (i.e., the statement of net position and the

statement of activities) report information on all of the activities of the Library. The

effect of material interfund activity has been eliminated from these statements.

Governmental activities, which normally are supported by taxes and

intergovernmental revenues, are reported separately from business-type activities,

which rely to a significant extent on fees and charges for support. The Library has no

business-type activities.

The statement of activities demonstrates the degree to which the direct expenses of a

given function, segment or program are offset by program revenues. Direct expenses

are those that are clearly identifiable with a specific function or segment. Program

revenues include (1) charges to customers or applicants who purchase, use or directly

benefit from goods, services or privileges provided by a given function or segment

and (2) grants and standard revenues that are restricted to meeting the operational or

capital requirements of a particular function or segment. Taxes and other items not

properly included among program revenues are reported instead as general revenues.

Separate financial statements are provided for governmental funds. Major individual

governmental funds are reported as separate columns in the fund financial

statements.

The Library reports the following major governmental funds:

The General Fund is the Library’s primary operating fund. It accounts for all

financial resources of the general government, except those accounted for in

another fund.

The Building and Equipment Fund is for the acquisition, construction,

equipping and maintenance of library facilities.

The Debt Service Fund accounts for the accumulation of resources restricted or

assigned for the payment of principal, interest and related costs of general

long-term debt.

The Library reports the following permanent fund:

The Working Cash Fund is used to account for monies used to provide

temporary loans to operating funds during periods of diminished revenue.

- 12 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 11 -

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

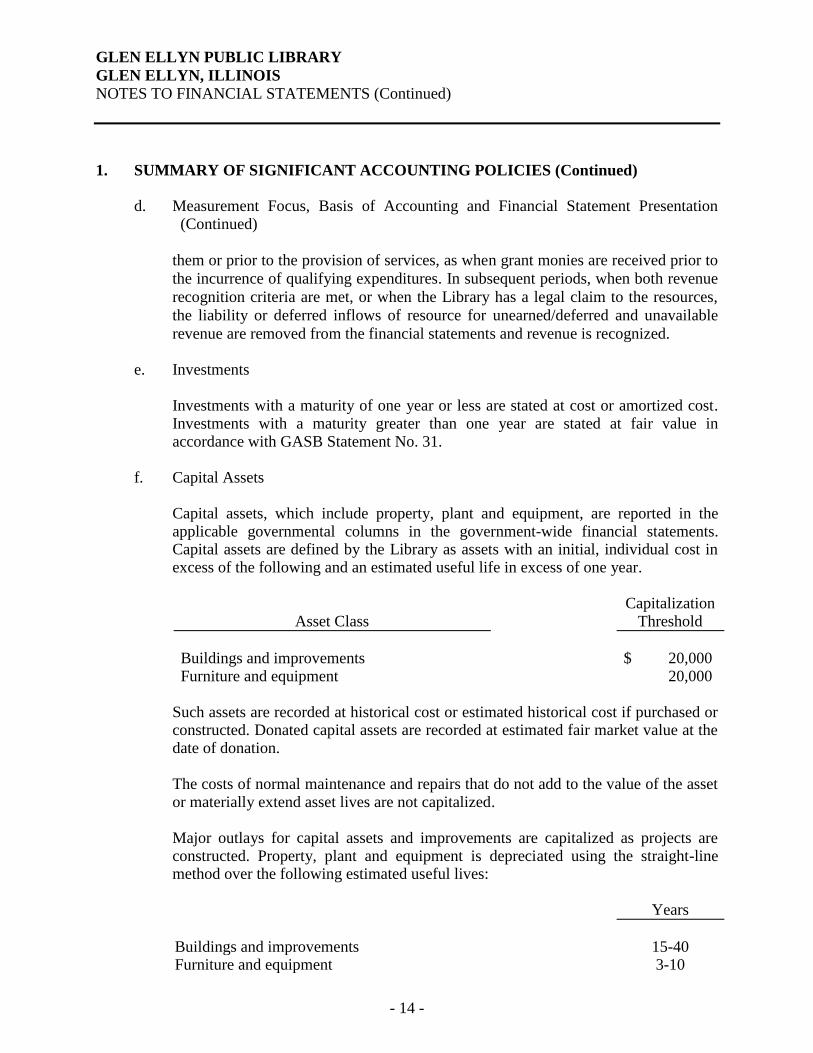

d. Measurement Focus, Basis of Accounting and Financial Statement Presentation

The government-wide financial statements are reported using the economic resources

measurement focus and the accrual basis of accounting. Revenues are recorded when

earned and expenses are recorded when a liability is incurred. The Library

recognizes property taxes when they are measurable in the period the tax is intended

to finance. Grants and similar items are recognized as revenue as soon as all

eligibility requirements imposed by the provider have been met.

Governmental fund financial statements are reported using the current financial

resources measurement focus and the modified accrual basis of accounting.

Revenues are recognized as soon as they are both measurable and available.

Revenues are considered to be available when they are collectible within the current

period or soon enough thereafter to pay liabilities of the current period. The Library

considers revenues to be available if they are collected within 60 days of the end of

the current fiscal period. Expenditures generally are recorded when a fund liability is

incurred. However, debt service expenditures are recorded only when payment is

due.

Property taxes, grants and interest associated with the current fiscal period are all

considered to be susceptible to accrual and are recognized as revenues of the current

fiscal period. Fines and miscellaneous revenues are considered to be measurable and

available only when cash is received by the Library.

In applying the susceptible to accrual concept to intergovernmental revenues (i.e.,

federal and state grants), the legal and contractual requirements of the numerous

individual programs are used as guidance. There are, however, essentially two types

of these revenues. In one, monies must be expended on the specific purpose or

project before any amounts will be paid to the Library; therefore, revenues are

recognized based upon the expenditures recorded. In the other, monies are virtually

unrestricted as to purpose of expenditure and are generally revocable only for failure

to comply with prescribed eligibility requirements, such as equal employment

opportunity. These resources are reflected as revenues at the time of receipt or earlier

if they meet the availability criterion.

The Library reports unearned/deferred and unavailable revenue on its financial

statements. Unavailable revenues arise when a potential revenue does not meet both

the available criteria for recognition in the current period, under the modified accrual

basis of accounting. Unearned/deferred revenue arises when a revenue is measurable

but not earned under the accrual basis of accounting. Unearned/deferred revenues

also arise when resources are received by the Library before it has a legal claim to

- 13 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 12 -

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) d. Measurement Focus, Basis of Accounting and Financial Statement Presentation (Continued)

them or prior to the provision of services, as when grant monies are received prior to

the incurrence of qualifying expenditures. In subsequent periods, when both revenue

recognition criteria are met, or when the Library has a legal claim to the resources,

the liability or deferred inflows of resource for unearned/deferred and unavailable

revenue are removed from the financial statements and revenue is recognized. e. Investments Investments with a maturity of one year or less are stated at cost or amortized cost.

Investments with a maturity greater than one year are stated at fair value in accordance with GASB Statement No. 31.

f. Capital Assets Capital assets, which include property, plant and equipment, are reported in the

applicable governmental columns in the government-wide financial statements. Capital assets are defined by the Library as assets with an initial, individual cost in excess of the following and an estimated useful life in excess of one year.

Asset Class Capitalization

Threshold

Buildings and improvements $ 20,000 Furniture and equipment 20,000

Such assets are recorded at historical cost or estimated historical cost if purchased or

constructed. Donated capital assets are recorded at estimated fair market value at the date of donation.

The costs of normal maintenance and repairs that do not add to the value of the asset

or materially extend asset lives are not capitalized. Major outlays for capital assets and improvements are capitalized as projects are

constructed. Property, plant and equipment is depreciated using the straight-line method over the following estimated useful lives:

Years

Buildings and improvements 15-40 Furniture and equipment 3-10

- 14 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 13 -

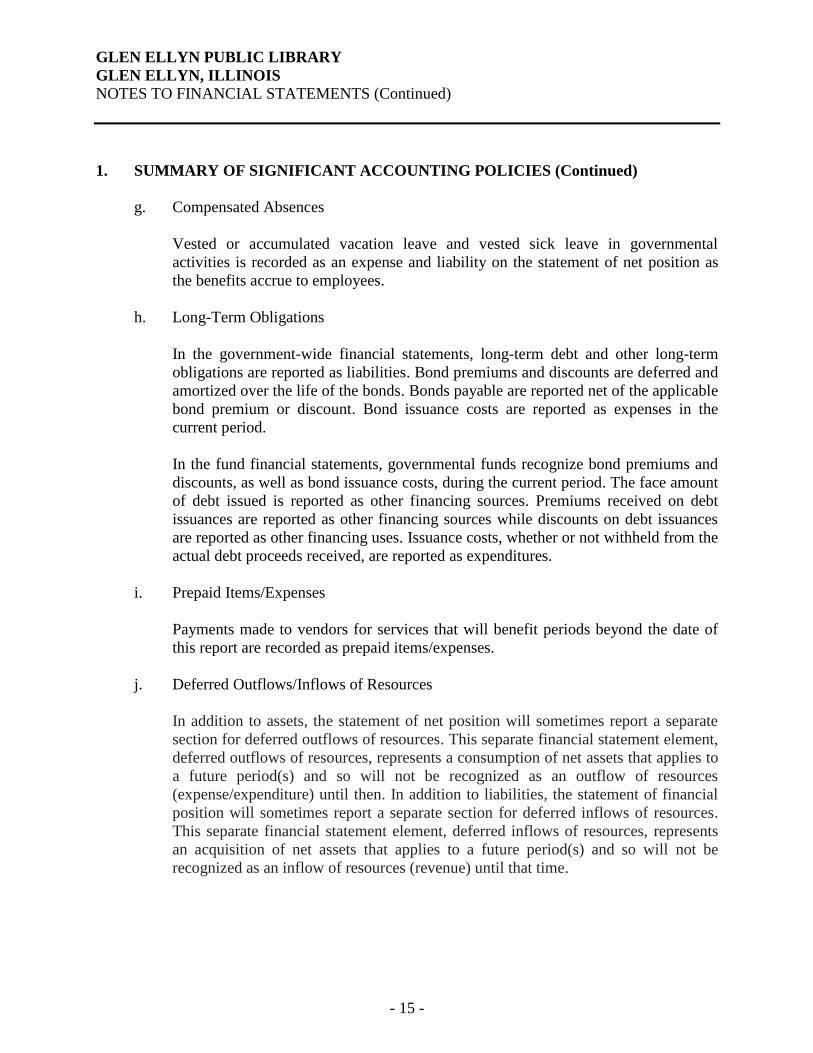

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

g. Compensated Absences

Vested or accumulated vacation leave and vested sick leave in governmental

activities is recorded as an expense and liability on the statement of net position as

the benefits accrue to employees.

h. Long-Term Obligations

In the government-wide financial statements, long-term debt and other long-term

obligations are reported as liabilities. Bond premiums and discounts are deferred and

amortized over the life of the bonds. Bonds payable are reported net of the applicable

bond premium or discount. Bond issuance costs are reported as expenses in the

current period.

In the fund financial statements, governmental funds recognize bond premiums and

discounts, as well as bond issuance costs, during the current period. The face amount

of debt issued is reported as other financing sources. Premiums received on debt

issuances are reported as other financing sources while discounts on debt issuances

are reported as other financing uses. Issuance costs, whether or not withheld from the

actual debt proceeds received, are reported as expenditures.

i. Prepaid Items/Expenses

Payments made to vendors for services that will benefit periods beyond the date of

this report are recorded as prepaid items/expenses.

j. Deferred Outflows/Inflows of Resources

In addition to assets, the statement of net position will sometimes report a separate

section for deferred outflows of resources. This separate financial statement element,

deferred outflows of resources, represents a consumption of net assets that applies to

a future period(s) and so will not be recognized as an outflow of resources

(expense/expenditure) until then. In addition to liabilities, the statement of financial

position will sometimes report a separate section for deferred inflows of resources.

This separate financial statement element, deferred inflows of resources, represents

an acquisition of net assets that applies to a future period(s) and so will not be

recognized as an inflow of resources (revenue) until that time.

- 15 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 14 -

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

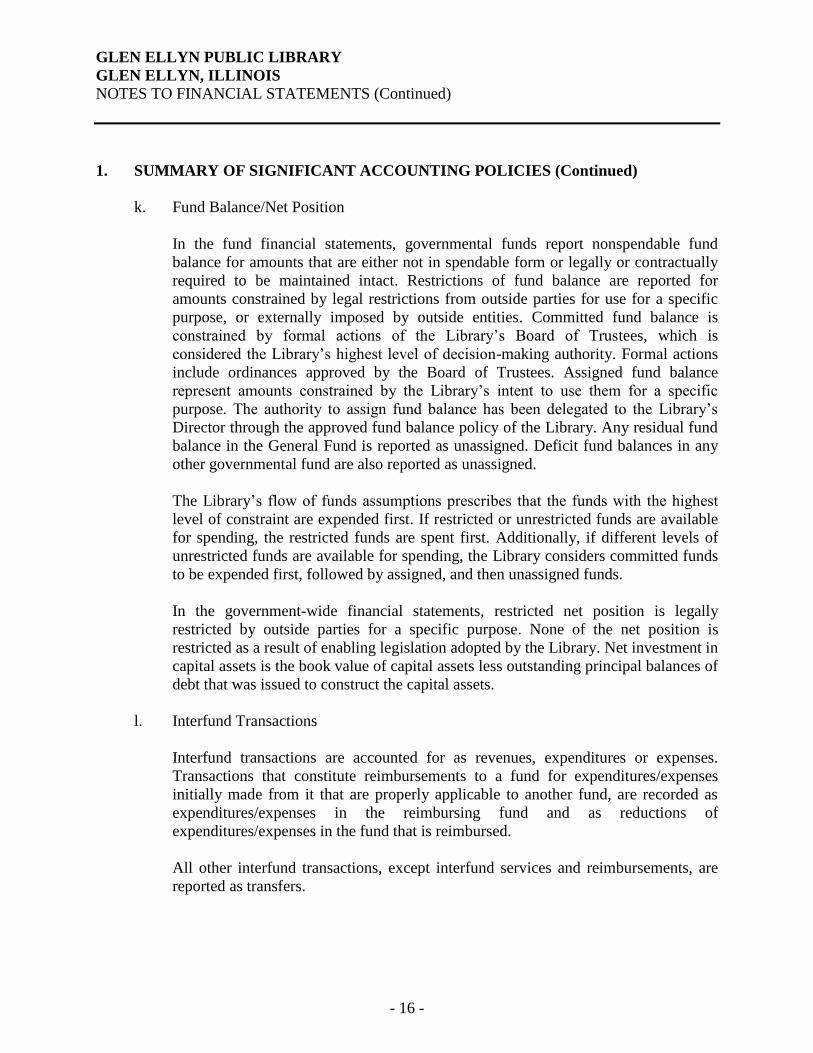

k. Fund Balance/Net Position

In the fund financial statements, governmental funds report nonspendable fund

balance for amounts that are either not in spendable form or legally or contractually

required to be maintained intact. Restrictions of fund balance are reported for

amounts constrained by legal restrictions from outside parties for use for a specific

purpose, or externally imposed by outside entities. Committed fund balance is

constrained by formal actions of the Library’s Board of Trustees, which is

considered the Library’s highest level of decision-making authority. Formal actions

include ordinances approved by the Board of Trustees. Assigned fund balance

represent amounts constrained by the Library’s intent to use them for a specific

purpose. The authority to assign fund balance has been delegated to the Library’s

Director through the approved fund balance policy of the Library. Any residual fund

balance in the General Fund is reported as unassigned. Deficit fund balances in any

other governmental fund are also reported as unassigned.

The Library’s flow of funds assumptions prescribes that the funds with the highest

level of constraint are expended first. If restricted or unrestricted funds are available

for spending, the restricted funds are spent first. Additionally, if different levels of

unrestricted funds are available for spending, the Library considers committed funds

to be expended first, followed by assigned, and then unassigned funds.

In the government-wide financial statements, restricted net position is legally

restricted by outside parties for a specific purpose. None of the net position is

restricted as a result of enabling legislation adopted by the Library. Net investment in

capital assets is the book value of capital assets less outstanding principal balances of

debt that was issued to construct the capital assets.

l. Interfund Transactions

Interfund transactions are accounted for as revenues, expenditures or expenses.

Transactions that constitute reimbursements to a fund for expenditures/expenses

initially made from it that are properly applicable to another fund, are recorded as

expenditures/expenses in the reimbursing fund and as reductions of

expenditures/expenses in the fund that is reimbursed.

All other interfund transactions, except interfund services and reimbursements, are

reported as transfers.

- 16 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 15 -

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

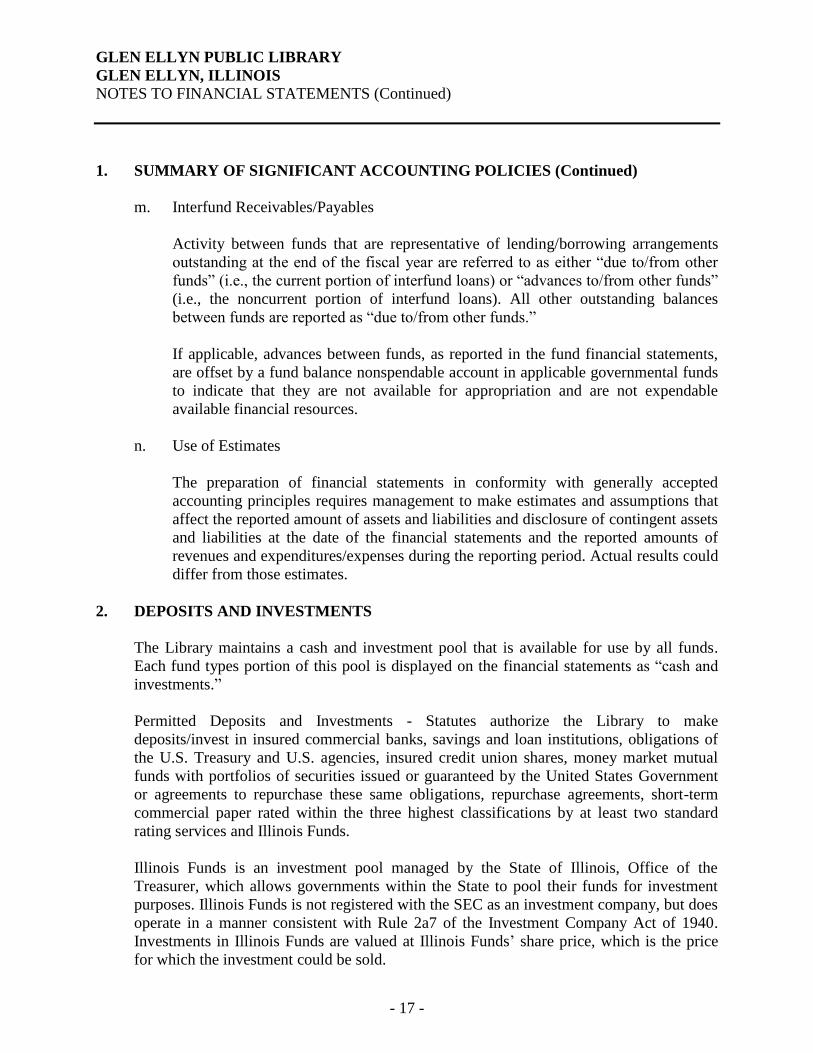

m. Interfund Receivables/Payables

Activity between funds that are representative of lending/borrowing arrangements

outstanding at the end of the fiscal year are referred to as either “due to/from other

funds” (i.e., the current portion of interfund loans) or “advances to/from other funds”

(i.e., the noncurrent portion of interfund loans). All other outstanding balances

between funds are reported as “due to/from other funds.”

If applicable, advances between funds, as reported in the fund financial statements,

are offset by a fund balance nonspendable account in applicable governmental funds

to indicate that they are not available for appropriation and are not expendable

available financial resources.

n. Use of Estimates

The preparation of financial statements in conformity with generally accepted

accounting principles requires management to make estimates and assumptions that

affect the reported amount of assets and liabilities and disclosure of contingent assets

and liabilities at the date of the financial statements and the reported amounts of

revenues and expenditures/expenses during the reporting period. Actual results could

differ from those estimates.

2. DEPOSITS AND INVESTMENTS

The Library maintains a cash and investment pool that is available for use by all funds.

Each fund types portion of this pool is displayed on the financial statements as “cash and

investments.”

Permitted Deposits and Investments - Statutes authorize the Library to make

deposits/invest in insured commercial banks, savings and loan institutions, obligations of

the U.S. Treasury and U.S. agencies, insured credit union shares, money market mutual

funds with portfolios of securities issued or guaranteed by the United States Government

or agreements to repurchase these same obligations, repurchase agreements, short-term

commercial paper rated within the three highest classifications by at least two standard

rating services and Illinois Funds.

Illinois Funds is an investment pool managed by the State of Illinois, Office of the

Treasurer, which allows governments within the State to pool their funds for investment

purposes. Illinois Funds is not registered with the SEC as an investment company, but does

operate in a manner consistent with Rule 2a7 of the Investment Company Act of 1940.

Investments in Illinois Funds are valued at Illinois Funds’ share price, which is the price

for which the investment could be sold.

- 17 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 16 -

2. DEPOSITS AND INVESTMENTS (Continued)

a. Library Deposits with Financial Institutions

Custodial credit risk for deposits with financial institutions is the risk that in the

event of a bank failure, the Library’s deposits may not be returned to it. The

Library’s investment policy requires pledging of collateral with a fair value of at

least 110% of all bank balances in excess of federal depository insurance with the

collateral held by the Library or by a third party or an escrow agent of the pledging

institution.

b. Library Investments

Interest rate risk is the risk that change in interest rates will adversely affect the fair

value of an investment.

In accordance with its investment policy, the Library limits its exposure to interest

rate risk by structuring the portfolio to provide liquidity for operating funds. The

investment policy does not limit the maturity lengths of library investments.

The Library limits its exposure to credit risk, the risk that the issuer of a debt security

will not pay its par value upon maturity, by primarily investing in securities

guaranteed explicitly and implicitly by the United States Government and Illinois

Funds. Illinois Funds are rated AAA by Standard and Poor’s.

Custodial credit risk for investments is the risk that, in the event of the failure of the

counterparty to the investment, the Library will not be able to recover the value of its

investments that are in the possession of an outside party. To limit its exposure, the

Library’s investment policy requires all security transactions that are exposed to

custodial credit risk to be processed on delivery versus payment (DVP) basis with

the underlying investments held by a third party custodian. Illinois Funds are not

subject to custodial credit risk.

Concentration of credit risk is the risk of loss attributed to the magnitude of the

Library’s investment in a single issuer. The Library places no limit on the amount

that may be invested in any one issuer, stating only that the Library diversify its

investments to the best of its ability based on the nature of the funds invested and the

cash flow needs of those funds.

- 18 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 17 -

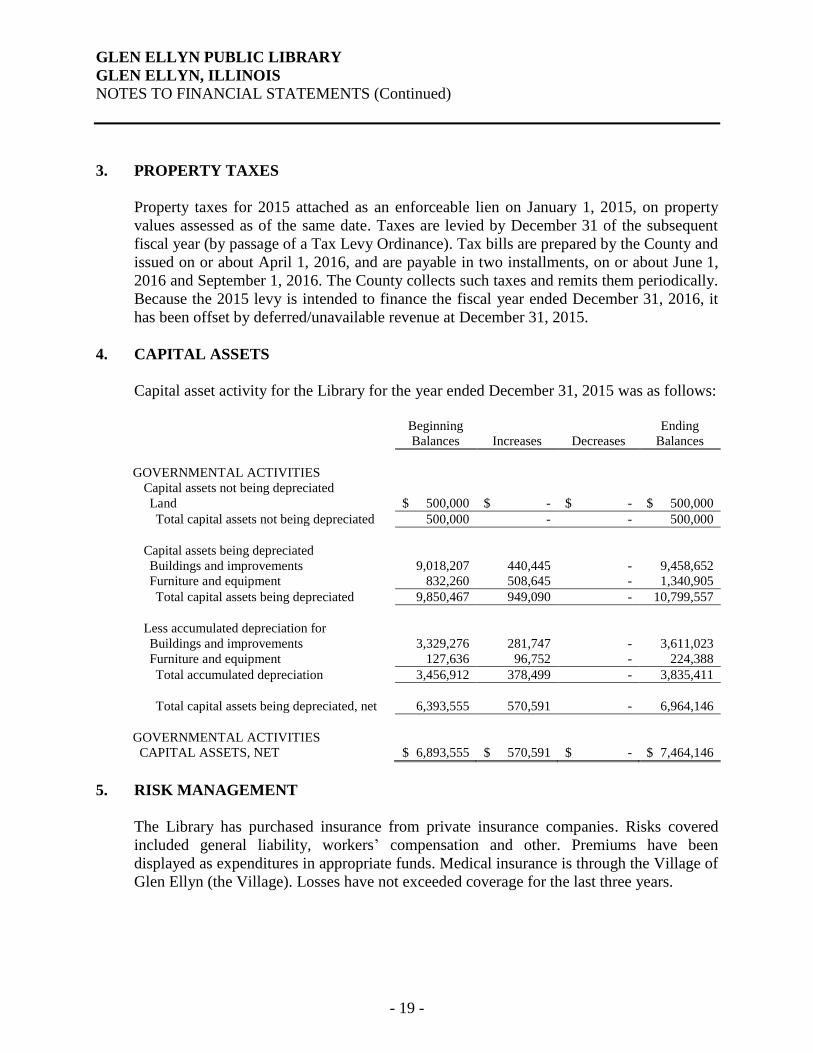

3. PROPERTY TAXES

Property taxes for 2015 attached as an enforceable lien on January 1, 2015, on property

values assessed as of the same date. Taxes are levied by December 31 of the subsequent

fiscal year (by passage of a Tax Levy Ordinance). Tax bills are prepared by the County and

issued on or about April 1, 2016, and are payable in two installments, on or about June 1,

2016 and September 1, 2016. The County collects such taxes and remits them periodically.

Because the 2015 levy is intended to finance the fiscal year ended December 31, 2016, it

has been offset by deferred/unavailable revenue at December 31, 2015.

4. CAPITAL ASSETS

Capital asset activity for the Library for the year ended December 31, 2015 was as follows:

Beginning

Balances

Increases

Decreases

Ending

Balances

GOVERNMENTAL ACTIVITIES

Capital assets not being depreciated

Land $ 500,000 $ - $ - $ 500,000

Total capital assets not being depreciated 500,000 - - 500,000

Capital assets being depreciated

Buildings and improvements 9,018,207 440,445 - 9,458,652

Furniture and equipment 832,260 508,645 - 1,340,905

Total capital assets being depreciated 9,850,467 949,090 - 10,799,557

Less accumulated depreciation for

Buildings and improvements 3,329,276 281,747 - 3,611,023

Furniture and equipment 127,636 96,752 - 224,388

Total accumulated depreciation 3,456,912 378,499 - 3,835,411

Total capital assets being depreciated, net 6,393,555 570,591 - 6,964,146

GOVERNMENTAL ACTIVITIES

CAPITAL ASSETS, NET $ 6,893,555 $ 570,591 $ - $ 7,464,146

5. RISK MANAGEMENT

The Library has purchased insurance from private insurance companies. Risks covered

included general liability, workers’ compensation and other. Premiums have been

displayed as expenditures in appropriate funds. Medical insurance is through the Village of

Glen Ellyn (the Village). Losses have not exceeded coverage for the last three years.

- 19 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 18 -

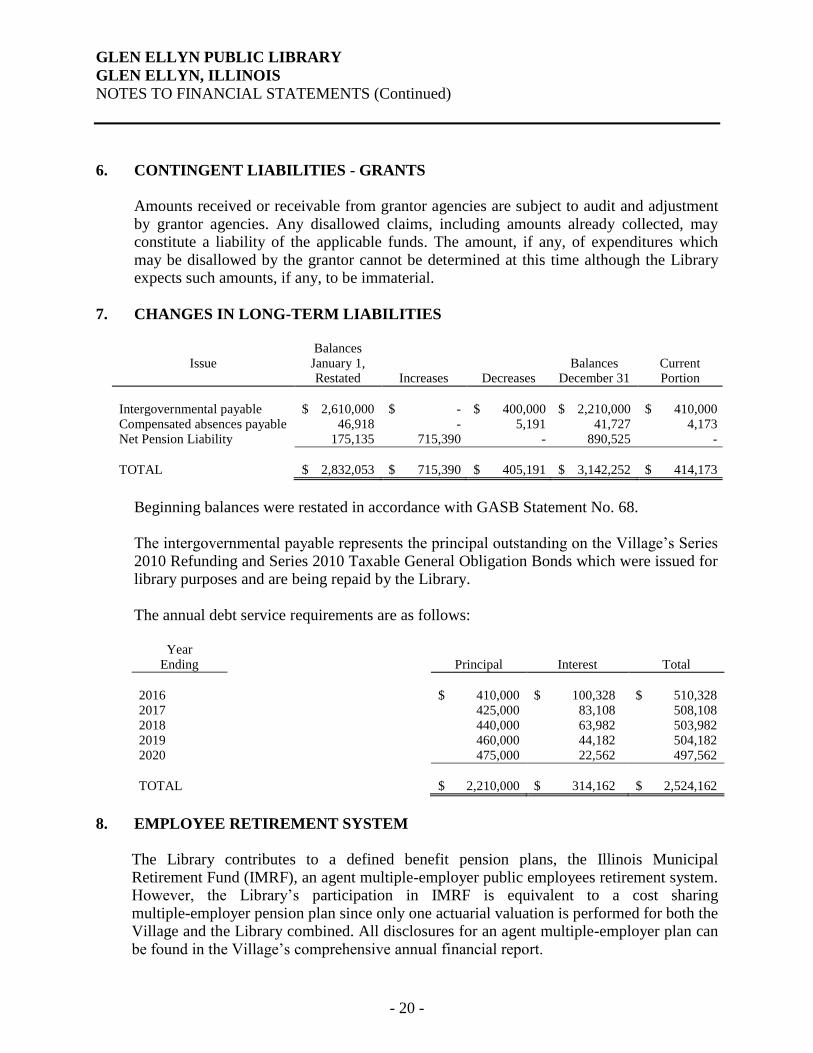

6. CONTINGENT LIABILITIES - GRANTS Amounts received or receivable from grantor agencies are subject to audit and adjustment

by grantor agencies. Any disallowed claims, including amounts already collected, may constitute a liability of the applicable funds. The amount, if any, of expenditures which may be disallowed by the grantor cannot be determined at this time although the Library expects such amounts, if any, to be immaterial.

7. CHANGES IN LONG-TERM LIABILITIES

Issue

Balances January 1, Restated

Increases

Decreases

Balances

December 31

Current Portion

Intergovernmental payable $ 2,610,000 $ - $ 400,000 $ 2,210,000 $ 410,000 Compensated absences payable 46,918 - 5,191 41,727 4,173 Net Pension Liability 175,135 715,390 - 890,525 -

TOTAL $ 2,832,053 $ 715,390 $ 405,191 $ 3,142,252 $ 414,173

Beginning balances were restated in accordance with GASB Statement No. 68. The intergovernmental payable represents the principal outstanding on the Village’s Series

2010 Refunding and Series 2010 Taxable General Obligation Bonds which were issued for library purposes and are being repaid by the Library.

The annual debt service requirements are as follows:

Year Ending Principal Interest Total

2016 $ 410,000 $ 100,328 $ 510,328 2017 425,000 83,108 508,108 2018 440,000 63,982 503,982 2019 460,000 44,182 504,182 2020 475,000 22,562 497,562

TOTAL $ 2,210,000 $ 314,162 $ 2,524,162

8. EMPLOYEE RETIREMENT SYSTEM The Library contributes to a defined benefit pension plans, the Illinois Municipal

Retirement Fund (IMRF), an agent multiple-employer public employees retirement system. However, the Library’s participation in IMRF is equivalent to a cost sharing multiple-employer pension plan since only one actuarial valuation is performed for both the Village and the Library combined. All disclosures for an agent multiple-employer plan can be found in the Village’s comprehensive annual financial report.

- 20 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 19 -

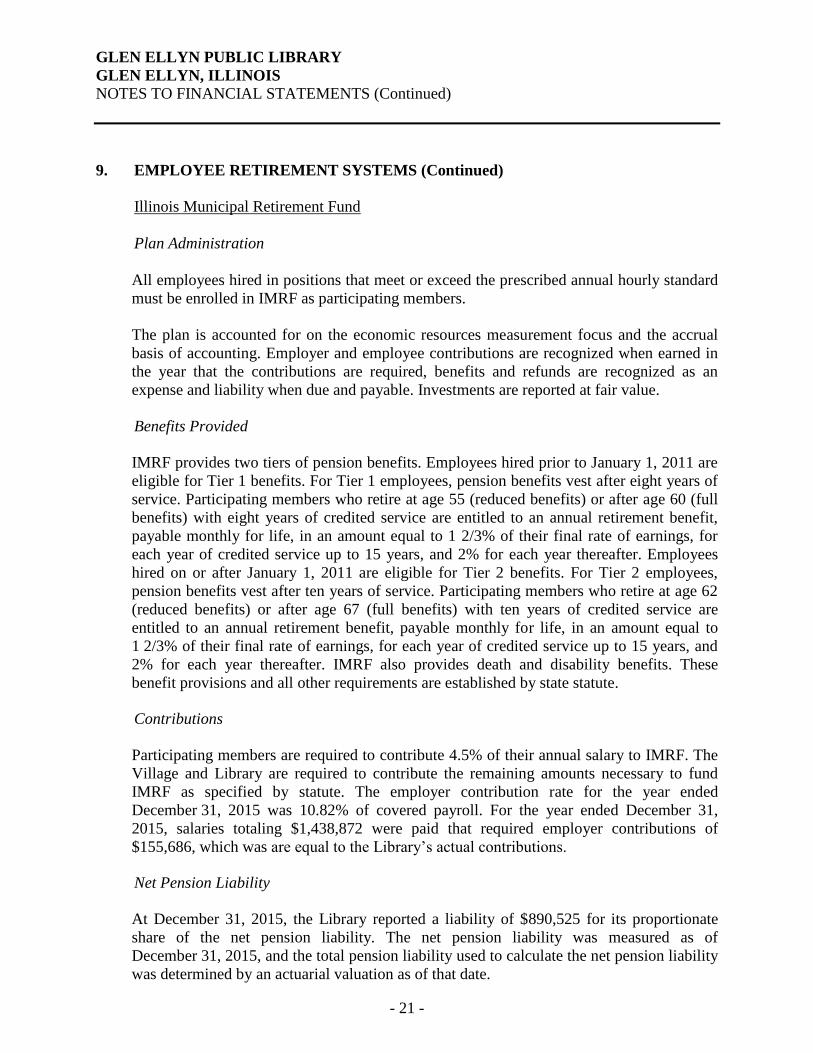

9. EMPLOYEE RETIREMENT SYSTEMS (Continued)

Illinois Municipal Retirement Fund

Plan Administration

All employees hired in positions that meet or exceed the prescribed annual hourly standard

must be enrolled in IMRF as participating members.

The plan is accounted for on the economic resources measurement focus and the accrual

basis of accounting. Employer and employee contributions are recognized when earned in

the year that the contributions are required, benefits and refunds are recognized as an

expense and liability when due and payable. Investments are reported at fair value.

Benefits Provided

IMRF provides two tiers of pension benefits. Employees hired prior to January 1, 2011 are

eligible for Tier 1 benefits. For Tier 1 employees, pension benefits vest after eight years of

service. Participating members who retire at age 55 (reduced benefits) or after age 60 (full

benefits) with eight years of credited service are entitled to an annual retirement benefit,

payable monthly for life, in an amount equal to 1 2/3% of their final rate of earnings, for

each year of credited service up to 15 years, and 2% for each year thereafter. Employees

hired on or after January 1, 2011 are eligible for Tier 2 benefits. For Tier 2 employees,

pension benefits vest after ten years of service. Participating members who retire at age 62

(reduced benefits) or after age 67 (full benefits) with ten years of credited service are

entitled to an annual retirement benefit, payable monthly for life, in an amount equal to

1 2/3% of their final rate of earnings, for each year of credited service up to 15 years, and

2% for each year thereafter. IMRF also provides death and disability benefits. These

benefit provisions and all other requirements are established by state statute. Contributions

Participating members are required to contribute 4.5% of their annual salary to IMRF. The

Village and Library are required to contribute the remaining amounts necessary to fund

IMRF as specified by statute. The employer contribution rate for the year ended

December 31, 2015 was 10.82% of covered payroll. For the year ended December 31,

2015, salaries totaling $1,438,872 were paid that required employer contributions of

$155,686, which was are equal to the Library’s actual contributions.

Net Pension Liability

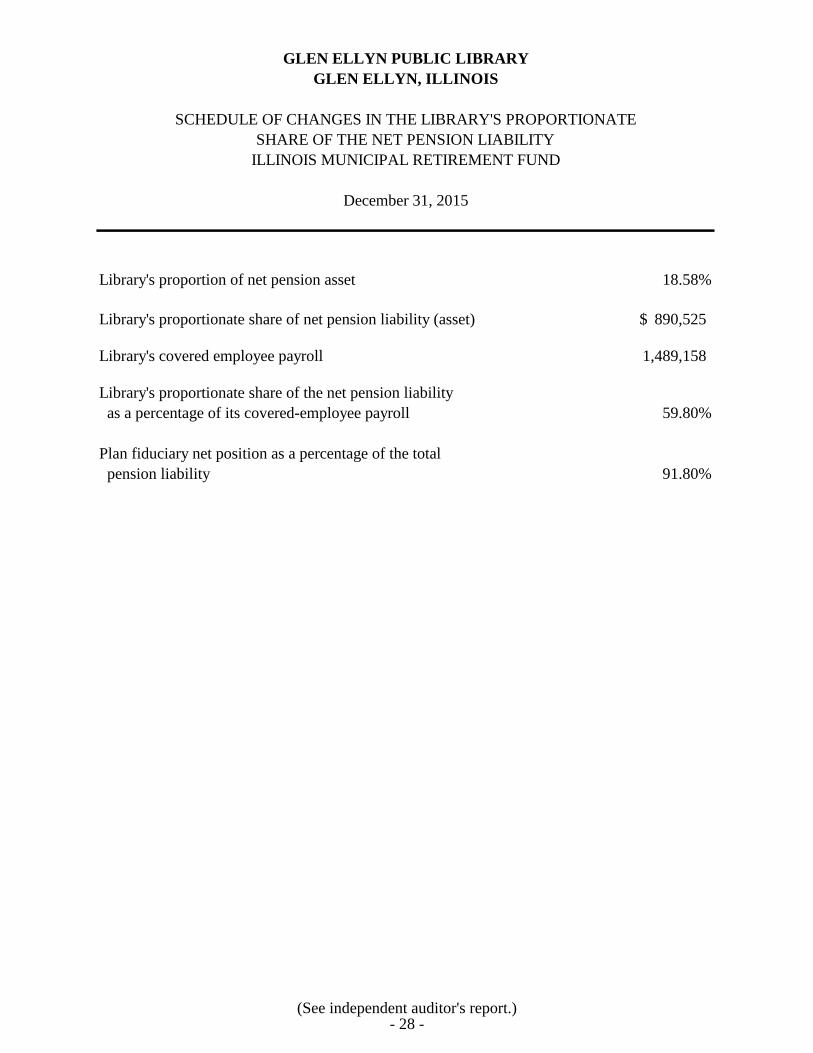

At December 31, 2015, the Library reported a liability of $890,525 for its proportionate

share of the net pension liability. The net pension liability was measured as of

December 31, 2015, and the total pension liability used to calculate the net pension liability

was determined by an actuarial valuation as of that date.

- 21 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 20 -

9. EMPLOYEE RETIREMENT SYSTEMS (Continued)

Illinois Municipal Retirement Fund (Continued)

Net Pension Liability (Continued)

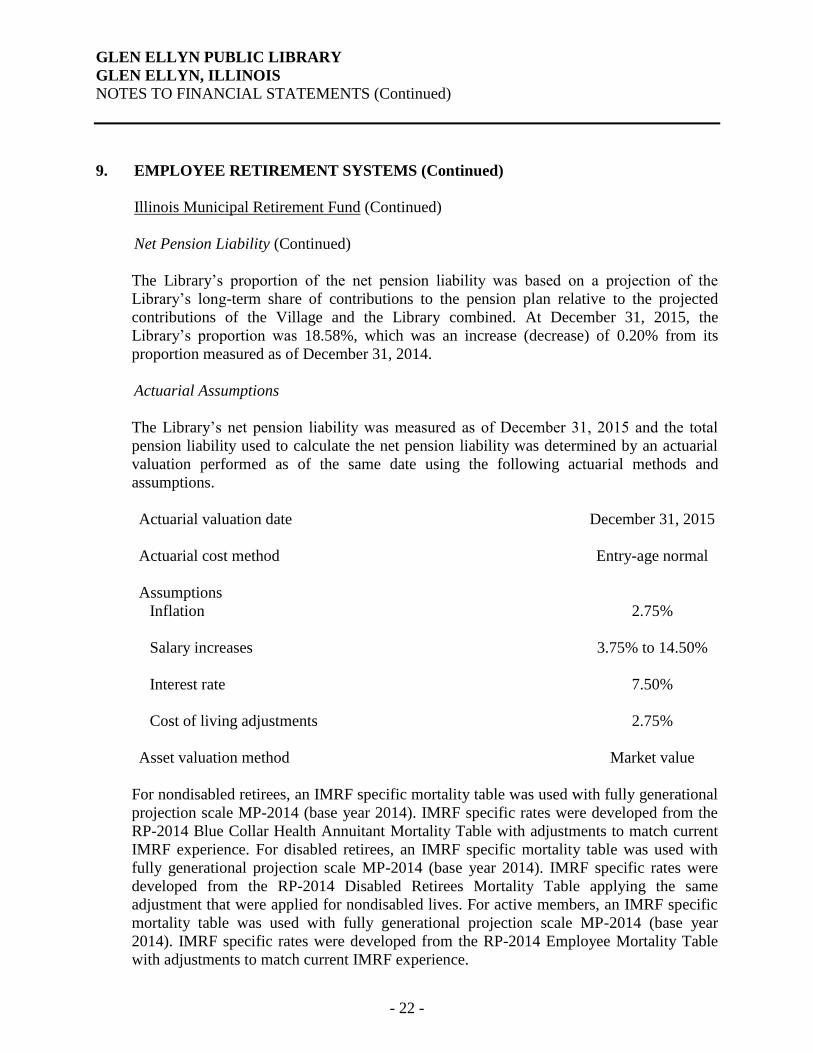

The Library’s proportion of the net pension liability was based on a projection of the

Library’s long-term share of contributions to the pension plan relative to the projected

contributions of the Village and the Library combined. At December 31, 2015, the

Library’s proportion was 18.58%, which was an increase (decrease) of 0.20% from its

proportion measured as of December 31, 2014.

Actuarial Assumptions

The Library’s net pension liability was measured as of December 31, 2015 and the total

pension liability used to calculate the net pension liability was determined by an actuarial

valuation performed as of the same date using the following actuarial methods and

assumptions.

Actuarial valuation date December 31, 2015

Actuarial cost method Entry-age normal

Assumptions

Inflation 2.75%

Salary increases 3.75% to 14.50%

Interest rate 7.50%

Cost of living adjustments 2.75%

Asset valuation method Market value

For nondisabled retirees, an IMRF specific mortality table was used with fully generational

projection scale MP-2014 (base year 2014). IMRF specific rates were developed from the

RP-2014 Blue Collar Health Annuitant Mortality Table with adjustments to match current

IMRF experience. For disabled retirees, an IMRF specific mortality table was used with

fully generational projection scale MP-2014 (base year 2014). IMRF specific rates were

developed from the RP-2014 Disabled Retirees Mortality Table applying the same

adjustment that were applied for nondisabled lives. For active members, an IMRF specific

mortality table was used with fully generational projection scale MP-2014 (base year

2014). IMRF specific rates were developed from the RP-2014 Employee Mortality Table

with adjustments to match current IMRF experience.

- 22 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 21 -

9. EMPLOYEE RETIREMENT SYSTEMS (Continued)

Illinois Municipal Retirement Fund (Continued)

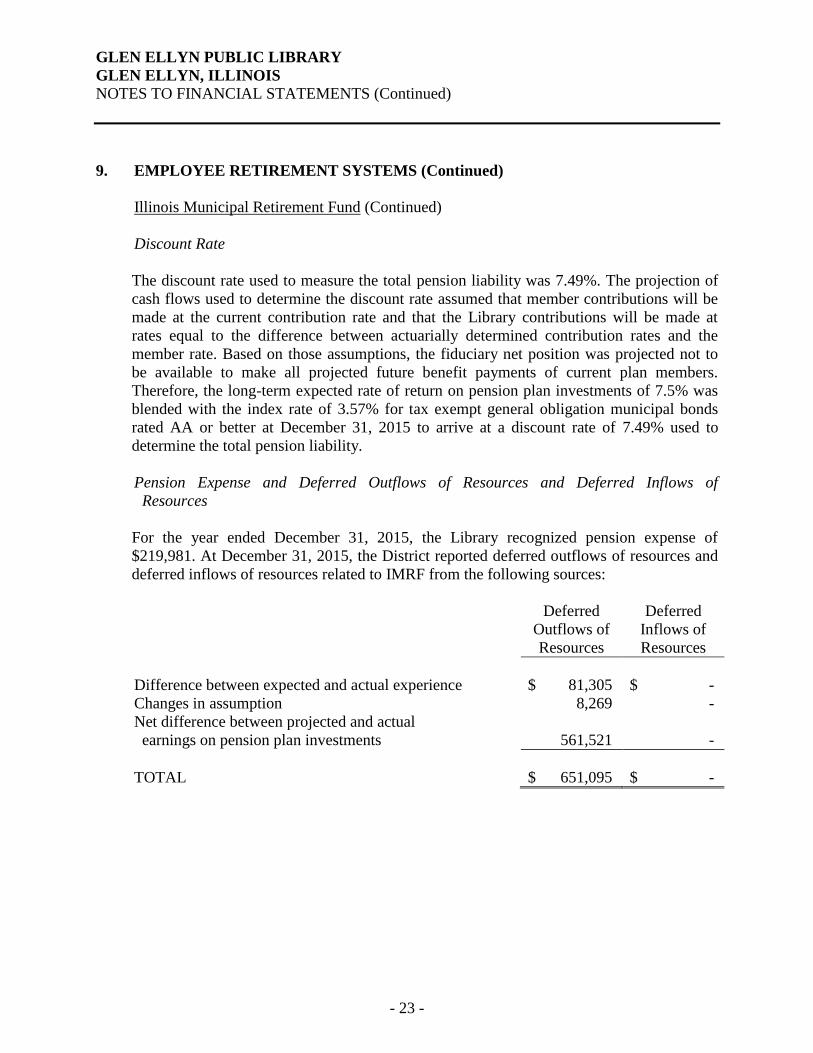

Discount Rate

The discount rate used to measure the total pension liability was 7.49%. The projection of

cash flows used to determine the discount rate assumed that member contributions will be

made at the current contribution rate and that the Library contributions will be made at

rates equal to the difference between actuarially determined contribution rates and the

member rate. Based on those assumptions, the fiduciary net position was projected not to

be available to make all projected future benefit payments of current plan members.

Therefore, the long-term expected rate of return on pension plan investments of 7.5% was

blended with the index rate of 3.57% for tax exempt general obligation municipal bonds

rated AA or better at December 31, 2015 to arrive at a discount rate of 7.49% used to

determine the total pension liability.

Pension Expense and Deferred Outflows of Resources and Deferred Inflows of

Resources

For the year ended December 31, 2015, the Library recognized pension expense of

$219,981. At December 31, 2015, the District reported deferred outflows of resources and

deferred inflows of resources related to IMRF from the following sources:

Deferred

Outflows of

Deferred

Inflows of

Resources Resources

Difference between expected and actual experience $ 81,305 $ -

Changes in assumption 8,269 -

Net difference between projected and actual

earnings on pension plan investments 561,521 -

TOTAL $ 651,095 $ -

- 23 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 22 -

9. EMPLOYEE RETIREMENT SYSTEMS (Continued)

Illinois Municipal Retirement Fund (Continued)

Pension Expense and Deferred Outflows of Resources and Deferred Inflows of

Resources (Continued)

Amounts reported as deferred outflows of resources and deferred inflows of resources

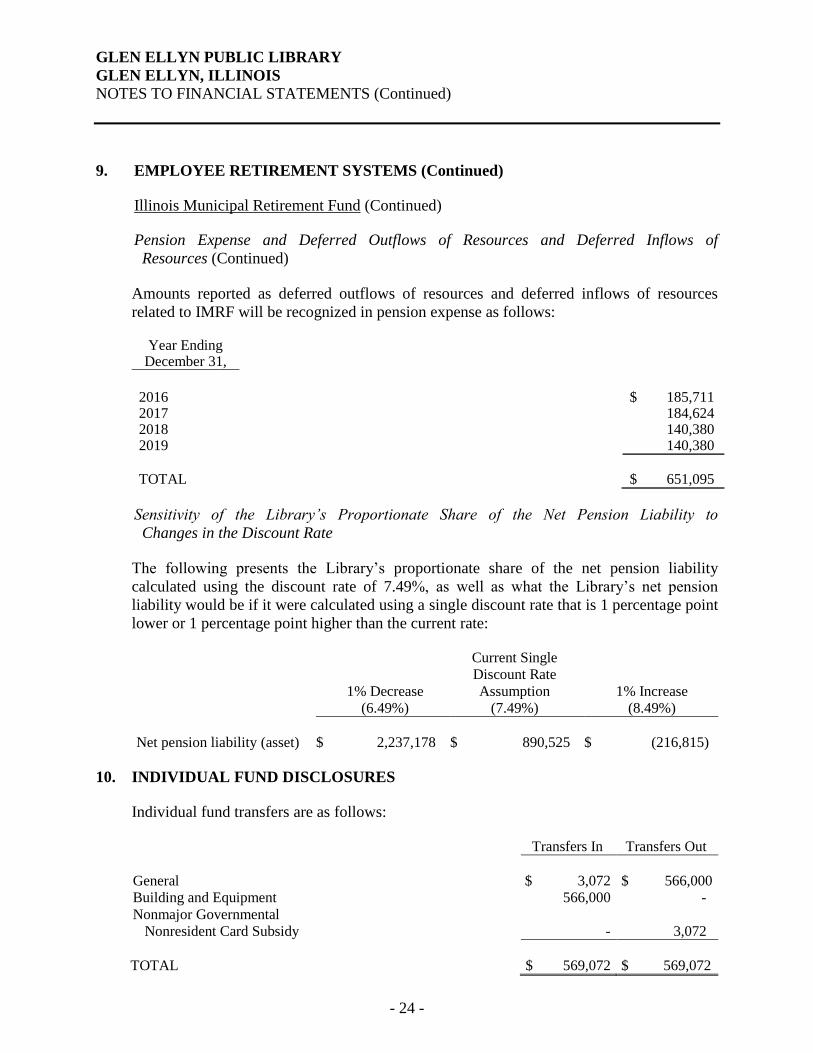

related to IMRF will be recognized in pension expense as follows:

Year Ending December 31,

2016 $ 185,711 2017 184,624 2018 140,380 2019 140,380

TOTAL $ 651,095

Sensitivity of the Library’s Proportionate Share of the Net Pension Liability to

Changes in the Discount Rate

The following presents the Library’s proportionate share of the net pension liability

calculated using the discount rate of 7.49%, as well as what the Library’s net pension

liability would be if it were calculated using a single discount rate that is 1 percentage point

lower or 1 percentage point higher than the current rate:

Current Single

Discount Rate

1% Decrease Assumption 1% Increase

(6.49%) (7.49%) (8.49%)

Net pension liability (asset) $ 2,237,178 $ 890,525 $ (216,815)

10. INDIVIDUAL FUND DISCLOSURES

Individual fund transfers are as follows:

Transfers In Transfers Out

General $ 3,072 $ 566,000

Building and Equipment 566,000 -

Nonmajor Governmental

Nonresident Card Subsidy - 3,072

TOTAL $ 569,072 $ 569,072

- 24 -

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

NOTES TO FINANCIAL STATEMENTS (Continued)

- 23 -

10. INDIVIDUAL FUND DISCLOSURES (Continued)

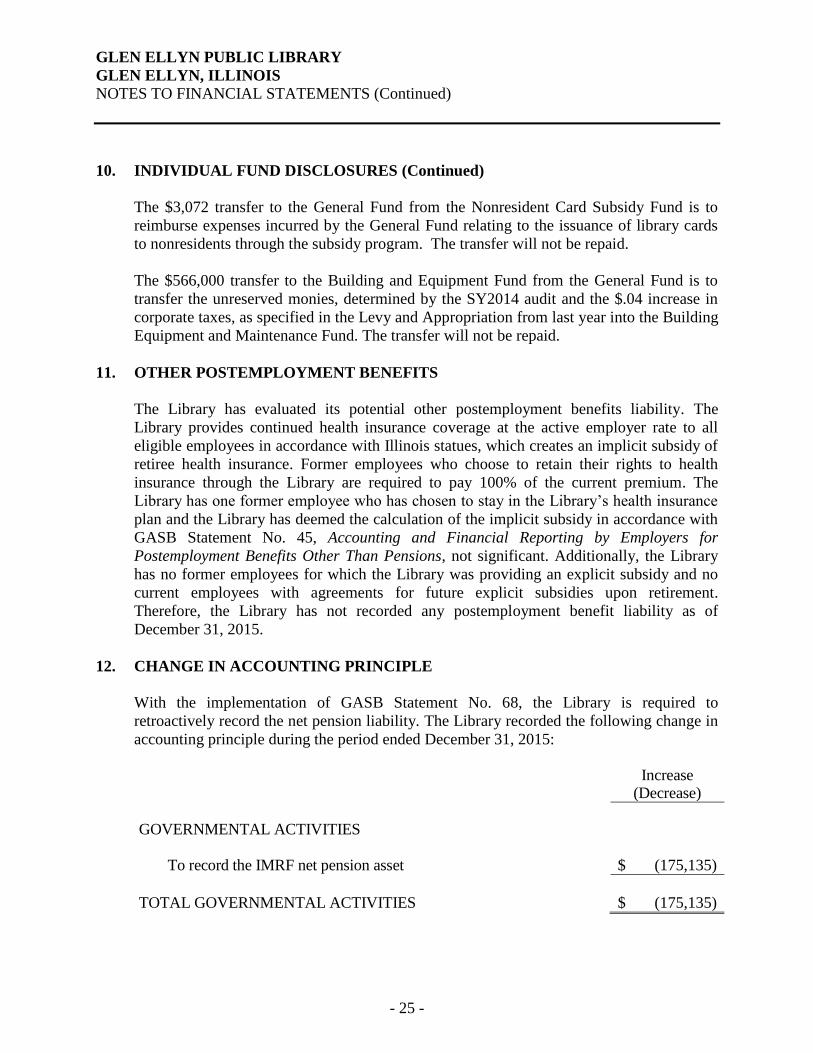

The $3,072 transfer to the General Fund from the Nonresident Card Subsidy Fund is to

reimburse expenses incurred by the General Fund relating to the issuance of library cards

to nonresidents through the subsidy program. The transfer will not be repaid.

The $566,000 transfer to the Building and Equipment Fund from the General Fund is to

transfer the unreserved monies, determined by the SY2014 audit and the $.04 increase in

corporate taxes, as specified in the Levy and Appropriation from last year into the Building

Equipment and Maintenance Fund. The transfer will not be repaid.

11. OTHER POSTEMPLOYMENT BENEFITS

The Library has evaluated its potential other postemployment benefits liability. The

Library provides continued health insurance coverage at the active employer rate to all

eligible employees in accordance with Illinois statues, which creates an implicit subsidy of

retiree health insurance. Former employees who choose to retain their rights to health

insurance through the Library are required to pay 100% of the current premium. The

Library has one former employee who has chosen to stay in the Library’s health insurance

plan and the Library has deemed the calculation of the implicit subsidy in accordance with

GASB Statement No. 45, Accounting and Financial Reporting by Employers for

Postemployment Benefits Other Than Pensions, not significant. Additionally, the Library

has no former employees for which the Library was providing an explicit subsidy and no

current employees with agreements for future explicit subsidies upon retirement.

Therefore, the Library has not recorded any postemployment benefit liability as of

December 31, 2015.

12. CHANGE IN ACCOUNTING PRINCIPLE

With the implementation of GASB Statement No. 68, the Library is required to

retroactively record the net pension liability. The Library recorded the following change in

accounting principle during the period ended December 31, 2015: Increase

(Decrease)

GOVERNMENTAL ACTIVITIES To record the IMRF net pension asset $ (175,135)

TOTAL GOVERNMENTAL ACTIVITIES $ (175,135)

- 25 -

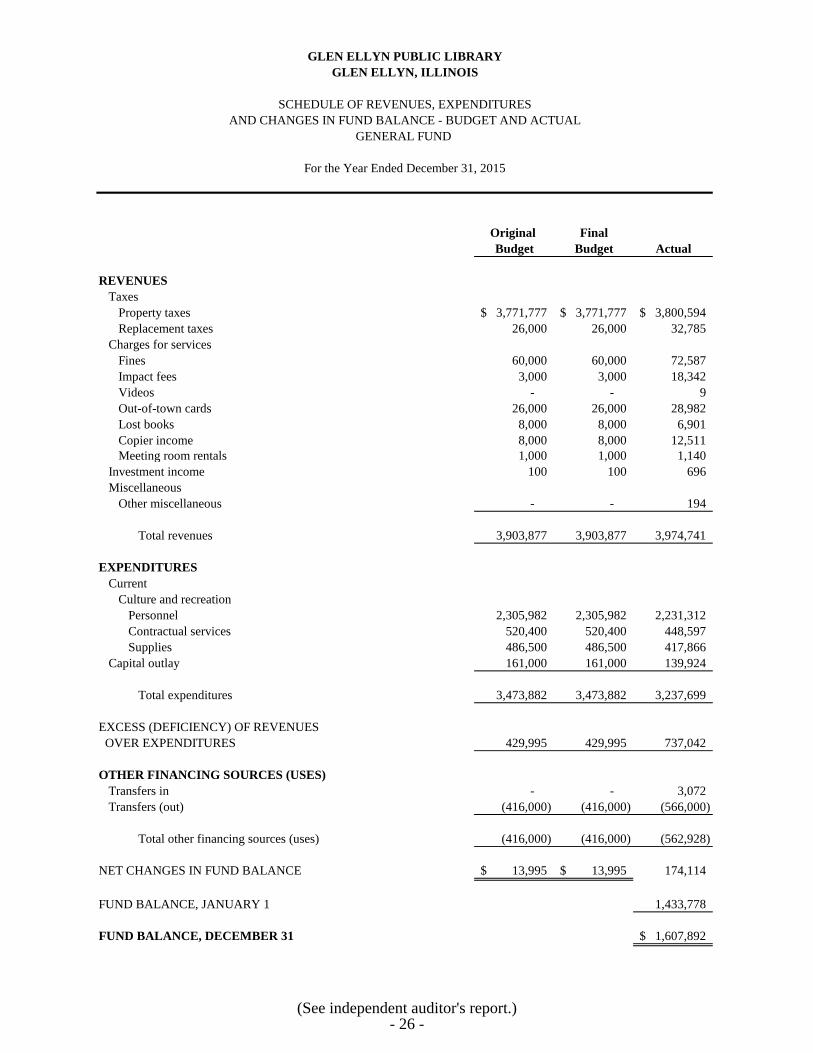

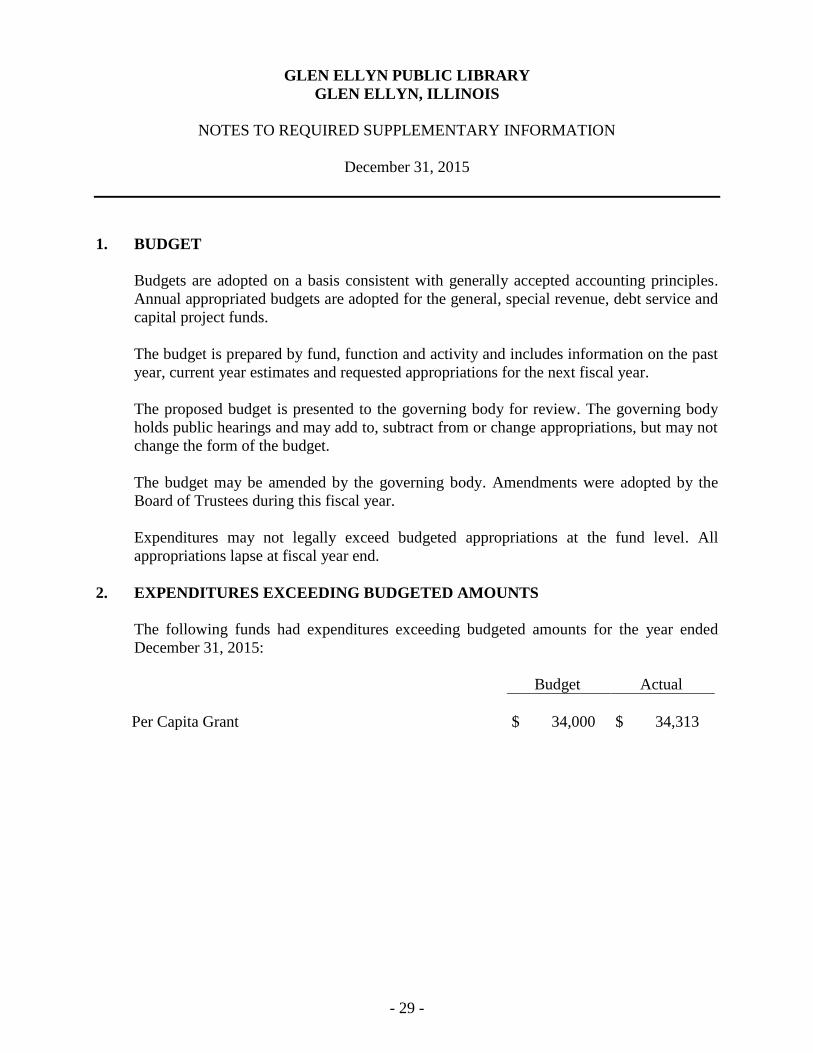

REQUIRED SUPPLEMENTARY INFORMATION

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

SCHEDULE OF REVENUES, EXPENDITURES

AND CHANGES IN FUND BALANCE - BUDGET AND ACTUAL

GENERAL FUND

For the Year Ended December 31, 2015

Original Final

Budget Budget Actual

REVENUES

Taxes

Property taxes 3,771,777$ 3,771,777$ 3,800,594$

Replacement taxes 26,000 26,000 32,785

Charges for services

Fines 60,000 60,000 72,587

Impact fees 3,000 3,000 18,342

Videos - - 9

Out-of-town cards 26,000 26,000 28,982

Lost books 8,000 8,000 6,901

Copier income 8,000 8,000 12,511

Meeting room rentals 1,000 1,000 1,140

Investment income 100 100 696

Miscellaneous

Other miscellaneous - - 194

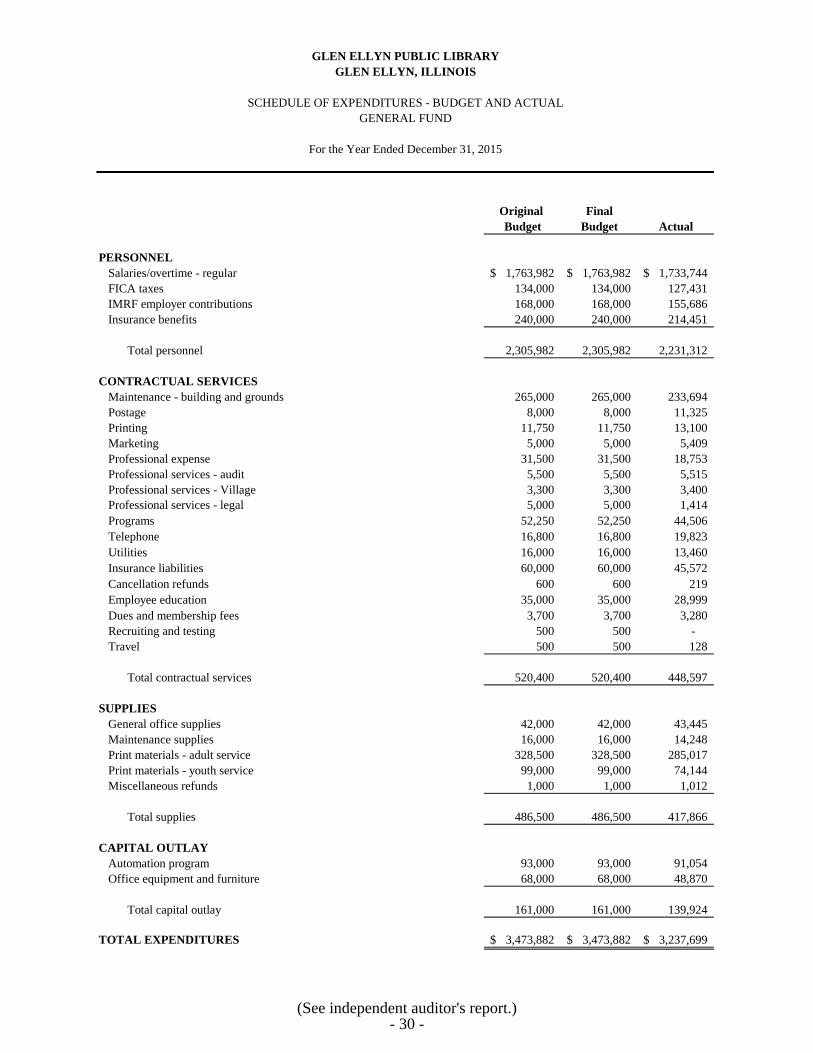

Total revenues 3,903,877 3,903,877 3,974,741

EXPENDITURES

Current

Culture and recreation

Personnel 2,305,982 2,305,982 2,231,312

Contractual services 520,400 520,400 448,597

Supplies 486,500 486,500 417,866

Capital outlay 161,000 161,000 139,924

Total expenditures 3,473,882 3,473,882 3,237,699

EXCESS (DEFICIENCY) OF REVENUES

OVER EXPENDITURES 429,995 429,995 737,042

OTHER FINANCING SOURCES (USES)

Transfers in - - 3,072

Transfers (out) (416,000) (416,000) (566,000)

Total other financing sources (uses) (416,000) (416,000) (562,928)

NET CHANGES IN FUND BALANCE 13,995$ 13,995$ 174,114

FUND BALANCE, JANUARY 1 1,433,778

FUND BALANCE, DECEMBER 31 1,607,892$

(See independent auditor's report.)- 26 -

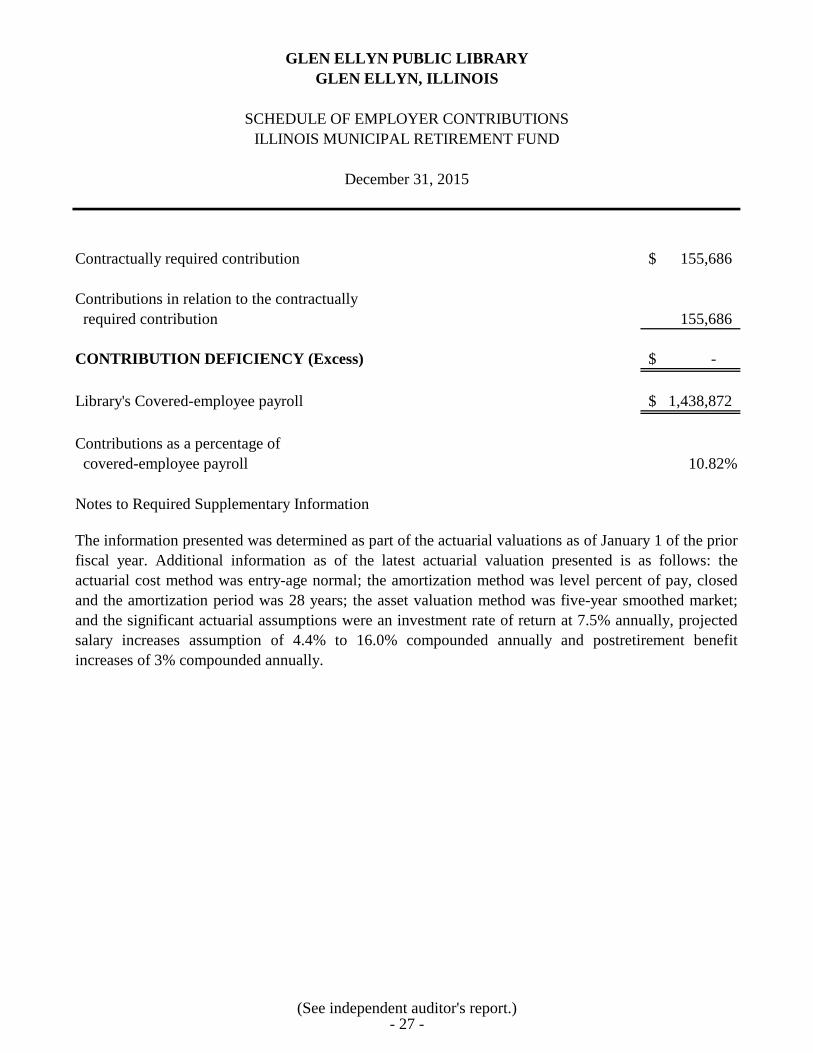

Contractually required contribution 155,686$

Contributions in relation to the contractually

155,686

CONTRIBUTION DEFICIENCY (Excess) -$

Library's Covered-employee payroll 1,438,872$

Contributions as a percentage of

covered-employee payroll 10.82%

Notes to Required Supplementary Information

The information presented was determined as part of the actuarial valuations as of January 1 of the prior

fiscal year. Additional information as of the latest actuarial valuation presented is as follows: the

actuarial cost method was entry-age normal; the amortization method was level percent of pay, closed

and the amortization period was 28 years; the asset valuation method was five-year smoothed market;

and the significant actuarial assumptions were an investment rate of return at 7.5% annually, projected

salary increases assumption of 4.4% to 16.0% compounded annually and postretirement benefit

increases of 3% compounded annually.

GLEN ELLYN PUBLIC LIBRARY

GLEN ELLYN, ILLINOIS

SCHEDULE OF EMPLOYER CONTRIBUTIONS

ILLINOIS MUNICIPAL RETIREMENT FUND