ANDHRA PRADESH TAX ON ENTRY OF MOTOR...

60

STATEMENT OF OBJECTS AND REASONS It is observed that proper tax is not being realised by the State on all the Motor Vehicles, which are being used in Andhra Pradesh. Many Vehicles are purchased at low tax in the neighbouring States and brought and used in the State. Since no sales took place within our State the Government is not getting any revenue on such vehicles. To overcome such problem, neighbouring States like, Tamil Nadu and Kerala have introduced Entry Tax on Motor Vehicles and in Karnataka it is being levied on all the commodities except 35 specified items. Entry Tax was introduced in our State in the year 1987 on Textiles, Tobacco and Sugar and it was subsequently withdrawn from 1st April, 1990. It is decided to levy Entry Tax on Motor Vehicles only to arrest tax evasion. The rate of tax on the local sales on motor vehicles is increased from 4% to 8% on the first sales and Entry Tax is levied at the rate of 8%. Entry Tax is not leviable if the motor vehicles suffer tax under local Sales Tax Act. The levy of entry tax on motor vehicles is therefore mainly meant to plug the leakage of revenue. To achieve the above object, Government have decided to enact, a separate law for the purpose. As the Legislative Assembly of the State was not then in session, having been prorogued and it has been decided to give effect to the above decision immediately, the Andhra Pradesh Tax on Entry of Motor Vehicles into Local Areas Ordinance, 1996 (Andhra Pradesh Ordinance No.22 of 1996) has been promulgated by the Governor on 1st August, 1996. _______________ ANDHRA PRADESH TAX ON ENTRY OF MOTOR VEHICLES INTO LOCAL AREAS ACT, 1996 879

Transcript of ANDHRA PRADESH TAX ON ENTRY OF MOTOR...

879

STATEMENT OF OBJECTS AND REASONS

It is observed that proper tax is not being realised by the State on all theMotor Vehicles, which are being used in Andhra Pradesh. Many Vehicles arepurchased at low tax in the neighbouring States and brought and used in theState. Since no sales took place within our State the Government is not gettingany revenue on such vehicles. To overcome such problem, neighbouring Stateslike, Tamil Nadu and Kerala have introduced Entry Tax on Motor Vehicles andin Karnataka it is being levied on all the commodities except 35 specified items.Entry Tax was introduced in our State in the year 1987 on Textiles, Tobaccoand Sugar and it was subsequently withdrawn from 1st April, 1990. It isdecided to levy Entry Tax on Motor Vehicles only to arrest tax evasion. Therate of tax on the local sales on motor vehicles is increased from 4% to 8% onthe first sales and Entry Tax is levied at the rate of 8%. Entry Tax is not leviableif the motor vehicles suffer tax under local Sales Tax Act. The levy of entry taxon motor vehicles is therefore mainly meant to plug the leakage of revenue. Toachieve the above object, Government have decided to enact, a separate lawfor the purpose.

As the Legislative Assembly of the State was not then in session, havingbeen prorogued and it has been decided to give effect to the above decisionimmediately, the Andhra Pradesh Tax on Entry of Motor Vehicles into LocalAreas Ordinance, 1996 (Andhra Pradesh Ordinance No.22 of 1996) has beenpromulgated by the Governor on 1st August, 1996.

_______________

dc

dc

ANDHRA PRADESHTAX ON ENTRY OF

MOTOR VEHICLES INTOLOCAL AREAS ACT, 1996

879

880

ANDHRA PRADESH TAX ONENTRY OF MOTOR VEHICLESINTO LOCAL AREAS ACT, 1996

[Act No. 26 of 1996]

[17th October, 1996]

The following Act of the Andhra Pradesh Legislative Assembly receivedthe assent of the Governor on the 15th October, 1996 and the said assent ishereby first published on the 17th October, 1996 in the Andhra Pradesh Gazettefor general information :—

An Act to provide for the levy of tax on entry of Motor Vehicles intoLocal Areas in the State of Andhra Pradesh and for the matters connectedtherewith or incidental thereto.

Be it enacted by the Legislative Assembly of the State of Andhra Pradeshin the Forty-seventh year of the Republic of India, as follows :—

CHAPTER - I

1. Short title, extent and commencement.— (1) This Act may becalled the Andhra Pradesh Tax on Entry of Motor Vehicles into Local AreasAct, 1996.

(2) It extends to the whole of the State of Andhra Pradesh.

(3) It shall be deemed to have come into force with effect from 1stAugust, 1996.

2. Definitions.— (1) In this Act, unless the context otherwiserequires,—

(a) “accessories” means car air conditioner, music system or anyother article fitted to a motor vehicle, which is not included in theoriginal invoice;

(b) “appellate authority” means an appellate authority appointedunder section 6;

(c) “assessing authority” means an assessing authority appointedunder section 5;

(d) “entry of motor vehicle into a local area” with all its grammaticalvariations and cognate expressions, means entry of motor vehicle

A.P. Tax on Entry of M.V. into Local Areas Act, 1996 [S. 2

880

881

into a local area from any place outside the State for use or saletherein;

1[(e) “Value Added Tax Act” means the Andhra Pradesh Value AddedTax Act, 2005];

(f) “Government” means the State Government;

(g) “Importer” means a person who brings a motor vehicle into alocal area from any place outside the State for use or sale thereinor who owns the vehicle at the time of its entry into the localarea;

(h) “local area” means the area of jurisdiction of a local authority;

(i) “local authority” means the area within the limits of, a city asdeclared under the Hyderabad Municipal Corporation Act, 1955,or the Visakhapatnam Municipal Corporation Act, 1979, or theVijayawada Municipal Corporation Act, 1981 or any otherMunicipal Corporation in the State, as in force or a municipalityas constituted or deemed to have been constituted under theAndhra Pradesh Municipalities Act, 1965, or any notified area,as declared under Section 389-A of the Andhra PradeshMunicipalities Act, 1965 or the area within the limits of GramPanchayats, under Andhra Pradesh Panchayat Raj Act, 1994.

(j) “Motor vehicle” means a motor vehicle defined in Clause (28) ofSection 2 of the Motor Vehicles Act, 1988 (Central Act 59 of 1988);

(k) “notification” means a notification published in the “Gazette”;

(l) “person” includes any company or association or body ofindividuals whether incorporated or not, a firm, a local authority,a Hindu undivided family, society, club, an individual, the CentralGovernment or the Government of any other State or UnionTerritory;

(m) “prescribed” means prescribed by rules made under this Act;

(n) “purchase value” means the value of a motor vehicle, asascertained from the original invoice and includes the value of

1. The clause (e) was subs. by Act 4 of 2006 w.e.f. 1st April, 2005. The earlier clausewas follows:

“(e) “General Sales Tax Act” means the Andhra Pradesh General Sales TaxAct, 1957 (Act No. VI of 1957)”;

S. 2] A.P. Tax on Entry of M.V. into Local Areas Act, 1996

882

accessories fitted to the vehicle, insurance, excise dutiescountervailing duties, sales tax, transport fee, freight charges andall other charges incidentally levied on the purchase of a motorvehicle :

Provided that, where the purchase value of a motor vehicle is notascertainable on account of non-availability or non-production of the originalinvoice or when the invoice produced is proved to be false or if the motorvehicle is acquired or obtained otherwise than by way of purchase, then thepurchase value shall be the value or price at which a motor vehicle of like kindor quality is sold or is capable of being sold, in open market;

(o) ‘State’ means the State of Andhra Pradesh;

(p) ‘tax’ means tax payable under this Act.

(2) Words and expressions used, but not defined in this Act, anddefined in the 1[the Value Added Tax Act], shall have the meanings respectivelyassigned to them under that Act.

CHAPTER - II

LEVY OF TAX

3. Levy of tax.— (1) Subject to the provisions of this Act, there shallbe levied and collected tax on the entry of any motor vehicle into any localarea for use or sale therein which is liable for registration in the State underthe Motor Vehicles Act, 1988 (Central Act 59 of 1988). The tax levied shall be atsuch rate or rates as may be fixed by the Government, by notification, on thepurchase value of the motor vehicle but not exceeding 2[the rates specified formotor vehicles in the Fifth Schedule to the Value Added Tax Act, 2005] :

Provided that no tax shall be levied and collected in respect of anymotor vehicle which was registered in any Union Territory or any other Stateunder the provisions of the Motor Vehicles Act, 1988, prior to period of fifteenmonths or more from the date on which, it is registered in the State :

Provided further that no tax shall be levied and collected in respect ofany motor vehicle, which is owned by Central Government and is usedexclusively for the purposes relating to the Defence of India.

1. Subs. for the words “General Sales Tax” by Act 4 of 2006 w.e.f. 1st April, 2005.

2. Subs. for the words “the rates specified for motor vehicles in the First Scheduleto the General Sales Tax Act, 1957” by Act 4 of 2006 w.e.f. 1st April, 2005.

A.P. Tax on Entry of M.V. into Local Areas Act, 1996 [S. 3

883

(2) The tax shall be payable by the importer in such manner andwithin such time as may be prescribed.

(3) Where the motor vehicle is taken delivery of, on its entry into alocal area or brought into a local area by a person other than an importer, theimporter who takes delivery of the motor vehicle from such person shall bedeemed to have brought or caused to have brought the motor vehicle into thelocal area.

4. Reduction in tax liability.— (1) Where an importer of a motorvehicle liable to pay tax under this Act, being a dealer in motor vehicles,becomes liable to pay tax under 1[the Value Added Tax Act], as a result, of thesale of such motor vehicle, then the amount of tax payable under 1[the ValueAdded Tax Act], shall be reduced by the amount of the tax paid under this Act.

(2) An importer, other than a dealer, liable to pay tax under this Act,causes entry of motor vehicle into a local area for use or sale therein, shall paytax to such authority, as Commissioner may notify within fifteen days fromthe date of entry of such vehicle into a local area or before an application ismade for registration of the said vehicle or assignment of a new registrationmark to such vehicle under the Motor Vehicles Act, 1988, whichever is earlier.

(3) Where an importer who, not being a dealer in motor vehicles,had purchased a motor vehicle for his own use in any Union Territory or anyother State, then the tax payable by him under this Act, shall, subject to suchconditions as may be prescribed, be reduced by the amount of tax paid, if any,under the law relating to 1[the Value Added Tax Act], in force in that UnionTerritory or State.

CHAPTER - III

ASSESSING AND APPELLATE AUTHORITIES

5. Assessing Authorities.— The Government, may by notificationappoint the officers of the Commercial Taxes Department not below the rankof Deputy Commercial Tax Officer to be the assessing authority for the purposesof this Act, and may assign to them such local area or local areas as may bespecified in such notification.

6. Appellate Authorities.— The Government may, by notificationappoint such officers of the Commercial Taxes Department of the rank of DeputyCommissioner of Commercial Taxes to be the appellate authorities for the

1. Subs. for the words “General Sales Tax Act” by Act 4 of 2006 w.e.f. 1st April,2006.

S. 6] A.P. Tax on Entry of M.V. into Local Areas Act, 1996

884

purposes of this Act, and may assign to them such local area or local areas asmay be specified in such notification.

CHAPTER - IV

RETURNS, ASSESSMENT, PAYMENT,RECOVERY AND REFUND OF TAX

7. Returns.— Every importer who is a dealer liable to pay tax underthis Act, shall furnish returns in such form, for such period, by such dates andto such authority, as may be prescribed.

8. Assessment.— (1) The amount of tax due from a person liable topay tax under this Act, shall be assessed separately for such period as may beprescribed.

(2) If the assessing authority is satisfied that the return furnished bya person liable to pay tax is correct and complete, he shall assess the amountof tax due from the person on the basis of such return.

(3) If the assessing authority is of the opinion that the returnfurnished by a person liable to pay tax is not correct and complete, he shallserve on such person, in the prescribed manner a notice requiring him, toattend on a date and at a place specified therein, and produce or cause to beproduced, all evidence on which the said person relies in support of his returnor to produce such evidence as specified in the notice and on the date specifiedin the notice, and as soon as may be, thereafter, the assessing authority shallafter considering all the evidence which may be produced, assess the amountof tax due from the person.

(4) If a person fails to comply with the requirements of anynotice issued under sub-section (3), the assessing authority shall determinethe purchase value of the motor vehicle under the proviso to clause (n) ofsection 2 to the best of his judgment and assess the amount of tax due fromhim and may direct the importer to pay in addition to the tax so assessedpenalty as specified in sub-section (1) of section 18.

(5) No order of assessment under sub-section (3) or sub-section (4)or any period shall be made after the expiry of three years from the last dateprescribed for filing of returns for that period. If, for any reason such order isnot made within the period aforesaid, then the return so filed shall be deemedto have been accepted as correct and complete for assessing the tax due fromsuch person.

9. Reassessment.— If, after a person liable to pay tax has beenassessed under section 8 for any period, the assessing authority has reason to

A.P. Tax on Entry of M.V. into Local Areas Act, 1996 [S. 9

885

believe that any purchase value or part thereof has, in respect of that period,escaped assessment or has been under assessed or assessed at a lower rate,then the assessing authority may within four years from the date of the orderof assessment of the particular period and after giving the person a reasonableopportunity of being heard, reassess the tax due from him and may direct himto pay in addition to the tax so assessed, penalty as specified in sub-section (1)of section 18.

10. Payment of Tax.— (1) The tax shall be paid in the mannerhereinafter provided.

(2) A person liable to pay the tax shall, before furnishing returns asrequired by sub-section (1) of section 7, pay into the Government Treasury, inthe prescribed manner, the whole of the amount of tax due from him accordingto such return.

(3) The amount of—

(i) the tax due, where return has been furnished without fullpayment thereof;

(ii) the difference in the tax assessed under section 8 or reassessedunder section 9 for any period, and the sum already paid by theperson in respect of such period; and

(iii) the penalty, if any, levied under Section 18, shall be paid by theperson into the Government Treasury by such date, which shallbe after twenty one days from the date of service of the notice, asmay be specified in the notice issued by the assessing authorityfor this purpose.

(4) Any tax or penalty, which remains unpaid after the date specifiedin the notice for payment, shall be recoverable as if it were an arrear of landRevenue.

11. Refund of Tax.— (1) The assessing authority shall refund to aperson the amount of the tax and the penalty, if any, paid by such person inexcess of the amount due from him for any period and the refund may beeither by cash payment or at the option of the person, by reduction of suchexcess from the amount of the tax and the penalty, if any, due from that personin respect of any other period :

Provided that the assessing authority shall first apply such excesstowards the recovery of any amount due in respect of which a notice undersub-section (4) of section 10 has been issued, and shall then refund the balance,if any.

A.P. Tax on Entry of M.V. into Local Areas Act, 1996S. 11]

886

(2) Where as a result of any order passed in appeal or other proceedingunder this Act, refund of any amount becomes due to the importer, theassessing authority shall refund the amount to the importer without hishaving to make any claim in that behalf, or adjust or apply, such amount asprovided in sub-section (1).

(3) Where a levy and collection of tax is held invalid by any judgmentor order of a Court or Tribunal, it shall not be necessary to refund any such taxto the importer unless it is proved by the importer to the satisfaction of theassessing authority that the tax has not been collected from the purchaser ofthe motor vehicle.

11-A. Refund on appeal etc.— Where as a result of any order passed inappeal or other proceeding under this Act, refund of any amount becomes dueto the importer, the assessing authority shall refund the amount to the importerwithout his having to make any claim in that behalf, or adjust or apply, suchamount as provided in section 11.

11-B. Non-refund of tax in certain cases.— Where a levy and collectionof tax is held invalid by any judgment or order of a Court or Tribunal, it shallnot be necessary to refund any such tax to the importer unless it is proved bythe dealer to the satisfaction of the assessing authority that the tax has notbeen collected from the purchaser of the Motor Vehicle.

12. Exemptions and Reductions.— Subject to such conditions as theymay impose, the Government may, if it is necessary so to do in the publicinterest, by notification, reduce the rate of tax on any type of Motor Vehicle orexempt any specified class of importers or type of Vehicles from payment ofthe whole or part of the tax payable under this Act.

CHAPTER - V

APPEALS AND REVISION

13. Appeals.— (1) An appeal from every original order under thisAct shall lie to the appellate authority.

(2) No appeal shall be entertained by the appellate authority unlessit is filed within thirty days from the date of receipt of the order appealedagainst by the assessee, and unless the entire amount of tax and penalty, ifany, has been remitted by the assessee in the Government Treasury.

(3) Subject to such rules as may be made in this behalf everyappellate authority referred to in sub-section (1) shall have the following

A.P. Tax on Entry of M.V. into Local Areas Act, 1996 [S. 13

887

powers, namely :—

(a) in an appeal against an order of assessment to confirm, reduce,enhance or annul the assessment, or set aside the assessment andrefer the case back to the assessing authority for making a freshassessment in accordance with the direction given by it or him;and

(b) in any other case, to pass such orders in the appeal as may bedeemed just and proper.

14. Revision.— (1) The Commissioner of Commercial Taxes may suomotu call for and examine the records of the proceedings of any order made byany authority, officer or person subordinate to it under the provisions of thisAct including sub-section (2) of this section and if such order or proceedingrecorded is prejudicial to the interests of revenue and may make such enquiryor cause such enquiry to be made and subject to the provisions of this Act,may initiate proceedings to revise, modify or set aside such order or proceedingand may pass such order in reference thereto as it thinks fit.

(2) Powers of the nature referred to in sub-section (1) may also beexercised by the Additional Commissioner, Joint Commissioner and DeputyCommissioner in the case of orders passed or proceedings recorded byauthorities, officers or persons subordinate to them.

(3) The powers conferred by sub-section (1) shall be exercised withina period of four years from the date on which the said order was served on theImporter.

15. Appeal to Appellate Tribunal.— (1) Any importer objecting toan order passed or proceeding recorded :—

(a) by any appellate authority on appeal under section 13; or

(b) by a Joint Commissioner or Deputy Commissioner suo motu undersub-section (2) of section 14 may appeal to the Appellate Tribunalwithin sixty days from the date on which the order or proceedingwas served on him.

(2) The Appellate Tribunal may admit an appeal preferred after theperiod of sixty days mentioned in sub-section (1), if it is satisfied that theimporter had sufficient cause for not preferring the appeal within thatperiod.

(3) The appeal shall be in the prescribed form shall be verified in theprescribed manner and shall be accompanied by such fee, calculated at the

A.P. Tax on Entry of M.V. into Local Areas Act, 1996S. 15]

888

rate of two per cent of the tax or penalty under dispute subject to a minimumof one hundred rupees and a maximum of two thousand rupees.

(4) The Appellate Tribunal may, after giving both parties to theappeal a reasonable opportunity of being heard :—

(i) confirm, reduce, enhance or annul the assessment or the penaltyor both;

(ii) set aside the assessment or the penalty or both and direct theassessing authority to pass fresh order after such further inquiryas may be directed; or

(iii) pass such order as it may think fit :

Provided that if the appeal involves a question of law, decision on whichis pending in any proceeding before the High Court or the Supreme Court, theAppellate Tribunal may defer the hearing of the appeal before it, till suchproceeding is disposed of.

(5) Before passing any order under sub-section (4), the AppellateTribunal may make such inquiry as it deems fit or remand the case to theappellate authority against whose order the appeal was preferred or to theassessing authority concerned for an inquiry and report on any specified pointor points.

(6) Notwithstanding anything in sub-section (4), where the importerwho has filed an appeal under this section to the Appellate Tribunal fails toappear before the Appellate Tribunal, either in person or by counsel when theappeal is called on for hearing, it shall be open to the Appellate Tribunal tomake an order dismissing the appeal :

Provided that the Appellate Tribunal, may on an application made bythe importer within thirty days from the date of communication of the orderof dismissal and on sufficient cause being shown by him for his non-appearance when the appeal was called on for hearing, re-admit the appealon such terms as it thinks fit, after giving notice thereof to the authority againstwhose order or proceeding the appeal is preferred.

(7) Except as provided in the rules made under this Act, the AppellateTribunal shall not have power to award costs to either of the parties to theappeal.

(8) Every order passed by the Appellate Tribunal under sub-section (4) shall be communicated by it to the importer, the authority against

A.P. Tax on Entry of M.V. into Local Areas Act, 1996 [S. 15

889

whose order the appeal was preferred, the Commissioner and such otherauthorities as may be prescribed.

(9) Every order passed by the Appellate Tribunal under sub-section (4) shall, subject to the provision of section 14, be final.

16. Revision by High Court.— (1) Within ninety days from the dateon which an order under sub-section (4) of Section 15 was communicated tohim, the importer or the authority prescribed in this behalf may prefer apetition to the High Court against the order on the ground, that the AppellateTribunal has either decided erroneously, or failed to decide, any question oflaw :

Provided that the High Court may admit a petition preferred after theperiod of ninety days aforesaid if it is satisfied that the petitioner had, sufficientcause for not preferring the petition within that period.

(2) The petition shall be in the prescribed form, shall be verified inthe prescribed manner, and shall, where it is preferred by the importer, beaccompanied by a fee of five hundred rupees.

(3) If the High Court, on perusing the petition considers that there isno sufficient ground for interfering, it may dismiss the petition summarily :

Provided that no petition shall be dismissed unless the petitioner hashad a reasonable opportunity of being heard in support thereof.

(4) (a) If the High Court does not dismiss the petition summarily, itshall, after giving both parties to the petition, a reasonable opportunity ofbeing heard, determine the question or questions of law raised and eitherreverse, affirm or amend the order against which the petition was preferredor remit the matter to the Appellate Tribunal with the opinion of the HighCourt on the question or questions of law raised, or pass such other order inrelation to the matter as the High Court thinks fit.

(b) Where the High Court remits the matter to the Appellate Tribunalunder clause (a) with its opinion on the question or questions oflaw raised, the Appellate Tribunal shall amend the order passedby it in conformity with such opinion.

(5) Before passing an order under sub-section (4), the High Courtmay, if it considers it necessary so to do, remit the petition to the AppellateTribunal and direct it to return the petition with its finding on any specificquestion or issue.

A.P. Tax on Entry of M.V. into Local Areas Act, 1996S. 16]

890

(6) Notwithstanding that a petition has been preferred under sub-section (1) tax shall be paid in accordance with the assessment made in thecase :

Provided that the High Court may, in its discretion, permit the petitionerto pay the tax in such number of instalments, or give such other direction inregard to the payment of tax as it thinks fit :

Provided further that if, as a result of the petition any change becomesnecessary in such assessment, the High Court may authorise the assessingauthority to amend, the assessment and on such amendment being made theexcess amount paid by the importer shall be refunded to him without interest,or the further amount of tax due from him shall be collected in accordancewith the provisions of this Act, as the case may be.

(7) (a) The High Court may, on the application of the importer or theprescribed authority review any order passed by it under sub- section (4) onthe basis of facts which were not before it when it passed the order.

(b) The application for review shall be preferred within such timeand in such manner as may be prescribed, and shall, where it ispreferred by the importer, be accompanied by a fee of five hundredrupees.

(8) The payment of tax and penalty if any due in accordance withthe order of the Appellate Tribunal in respect of which a petition has beenpreferred under sub-section (1) shall not be stayed pending the disposal of thepetition but if such amount is reduced as a result of such petition, the excesstax paid shall be refunded in accordance with the provisions of section 11.

(9) In respect of every petition or application preferred under sub-section (1) or sub-section (7) the costs shall be in the discretion of the HighCourt.

17. Appeal to High Court.— (1) Any importer objecting to an orderrelating to assessment passed by the Commissioner suo motu under sub-section(1) of Section 14 may appeal to the High Court within sixty days from the dateon which the order was communicated to him :

Provided that the High Court may admit an appeal preferred after theperiod of sixty days aforesaid if it is satisfied that such importer had sufficientcause for not preferring the appeal within that period.

(2) The appeal shall be in the prescribed form, shall be verified in theprescribed manner and shall be accompanied by a fee calculated at the rate of

A.P. Tax on Entry of M.V. into Local Areas Act, 1996 [S. 17

891

two per cent of tax or penalty under dispute subject to a minimum of onehundred rupees and a maximum of two thousand rupees.

(3) The High Court shall, after giving both parties to the appeal areasonable opportunity of being heard, pass such order thereon as it thinksfit.

(4) The provisions of sub-sections (6), (7), (8) and (9) of section 16shall apply in relation to appeal preferred under sub-section (1) as they applyin relation to petitions preferred under sub-section (1) of Section 16.

CHAPTER - VI

PENALTY AND CHECKING OF MOTOR VEHICLES

18. Penalty.— (1) Where any person liable to pay tax under this Act,fails to comply with any of the provisions of this Act, the assessing authoritymay, after giving such person a reasonable opportunity of being heard, byorder, in writing, impose on him, in addition to any tax payable, a sum byway of penalty not exceeding twice the amount of the tax due.

(2) If any person liable to pay tax under this Act, does not, withoutreasonable cause, pay the tax within the time he is required by or under theprovisions of this Act, to pay it, the assessing authority may, after giving suchperson a reasonable opportunity of being heard by order, in writing, imposeupon him by way of penalty, in addition to the amount of tax and penaltyunder sub-section (1), a sum equal to :—

(a) one and a half per cent of the amount of tax for each month for thefirst three months after the last date by which the person shouldhave paid the tax; and

(b) two per cent of amount of tax per each month thereafter duringthe time the person continues to make default in the payment ofthe tax.

19. Officers competent to check Motor Vehicles in Local areas.—(1) Any officer of the Commercial Taxes Department authorised by theGovernment under sub-section (3) shall have power to stop any motor vehiclethat is being brought into any local area for sale or use and examine thedocuments relating to purchase of the vehicle and payment of tax due thereonunder this Act.

(2) The person incharge of the vehicle shall stop the vehicle and keepthe vehicle stationary so long as it is necessary for examination mentioned in

A.P. Tax on Entry of M.V. into Local Areas Act, 1996S. 19]

892

sub-section (1) and shall give the details about the purchase of the vehicle andpayment of tax under this Act.

(3) The Government may authorise any officer of the CommercialTaxes Department, not below the rank of Commercial Tax Officer to exercisethe powers specified in sub-section (1) in such local areas or part thereof asmay be notified from time to time.

20. Impounding of Motor Vehicle on Import of which Tax is notpaid.— If a person liable to pay tax in the manner as laid down under sub-section (2) of Section 4 fails to pay tax within 15 days from the entry of motorvehicle into the local area or before an application is made for registration ofthe vehicle under the Motor Vehicles Act, 1988, whichever is earlier, then thedesignated officer shall forthwith impound the vehicle in respect of which taxhas remained unpaid and keep the vehicle impounded till the amount of taxand penalty due and payable is paid in full :

Provided that, if the amount of tax and penalty is not paid within onemonth of impounding of the vehicle, the designated officer shall have powerto sell the vehicle in the prescribed manner, by auction and apply the saleproceeds towards recovery of the tax, penalty and costs. The remainder, ifany, shall be refunded to the importer :

Provided further that, if, at any time before the auction of the vehicle,the importer pays the tax, penalty and costs, if any, incurred towards holdingthe auction, then, the designated officer may, after satisfying that all the duesas aforesaid have been fully paid by the importer cancel the auction and returnthe vehicle to the importer.

CHAPTER - VII

MISCELLANEOUS

21. Officers and Employees to be Public Servants.— All officers andemployees acting under the provisions of this Act, shall be deemed to be publicservants within the meaning of section 21 of the Indian Penal Code, 1860(Central Act 45 of 1860).

22. Protection of action taken in good faith.— No suit, prosecutionor other legal proceeding shall lie against the Government or any officer oremployee for anything which is, in good faith, done or intended to be doneunder this Act.

23. Restriction on registration.— Notwithstanding anythingcontained in any other law for the time being in force, where the liability to

A.P. Tax on Entry of M.V. into Local Areas Act, 1996 [S. 23

893

pay tax in respect of a motor vehicle arises under this Act, and such motorvehicle is required to be registered in the State under the Motor Vehicles Act,1988 (Central Act 59 of 1988), no registration authority shall register suchmotor vehicle, unless payment of such tax has been made by the personconcerned in respect of that vehicle.

24. Offences.— (1) Any person, who—

(a) fails to pay, within the time allowed any tax assessed or anypenalty imposed on him under this Act; or

(b) wilfully acts in contravention of the provisions of this Act or therules made thereunder; shall, on conviction, be liable to bepunished with fine which may extend to two thousand rupees.

(2) Any person, who,—

(a) wilfully submits an untrue return or fails to submit a return asrequired by the provisions of this Act or the rules madethereunder; or

(b) fraudulently evades the payment of any tax, and other amountdue from him under this Act, shall on conviction, be liable to bepunished, if it is a first offence, with fine which may extend totwo thousand rupees, and if it is a second or subsequent offence,with simple imprisonment which may extend to six months orwith fine which may extend to two thousand rupees or withboth.

(3) Any person who makes any statement or declaration in any ofthe records or documents which statement or declaration he knows or hasreason to believe to be false shall, on conviction, be liable to be punished withsimple imprisonment which may extend to six months or with fine whichmay extend to two thousand rupees or with both.

(4) Any person, who is in any way knowingly concerned in anyfraudulent evasion or attempt at evasion or abetment of evasion of any taxpayable under this Act, shall, on conviction, be liable to be punished withsimple imprisonment which may extend to six months or with fine whichmay extend to two thousand rupees or with both.

25. (1) No Court other than the Court of a Magistrate of the FirstClass shall take cognizance of, or try, an offence under this Act.

(2) No prosecution for an offence under sub-section (2) of section 24or for any second or subsequent offence under sub-section (2) of that section

A.P. Tax on Entry of M.V. into Local Areas Act, 1996S. 25]

894

shall be instituted except with the written consent of the Deputy Commissionerhaving jurisdiction over the local area.

26. (1) The prescribed authority may accept from any person, whohas committed or is reasonably suspected of having committed an offenceunder this Act by way of composition of such offence :—

(a) where the offence consists of failure to pay, or the evasion of, anytax recoverable under this Act, in addition to the tax sorecoverable a sum of money not exceeding two thousand rupeesor double the amount of the tax recoverable, whichever is greater;and

(b) in other cases, a sum of money not exceeding two thousandrupees.

(2) Any order passed or proceeding recorded by the prescribedauthority under sub-section (1), shall be final and no appeal or application forrevision shall lie therefrom.

27. An assessing authority, an appellate authority or a revisionauthority shall, for the purpose of this Act, have power :—

(a) to summon and enforce the attendance of any person to examinehim on oath or affirmation; and

(b) to require the production of any document.

28. Save as otherwise expressly provided in this Act, no Court shallentertain any suit or other proceeding to set aside or modify or question thevalidity of an assessment order or decision made or passed by any officer orauthority under this Act or any rules made thereunder or in respect of anyother matter falling within its or his scope.

29. No assessment made, penalty or compounding fee levied or otherorder passed by any officer or authority under this Act, shall be set asidemerely on account of any defect or irregularity in the procedure relating thereto,unless it appears that such defect or irregularity has in fact occasioned materialhardship or failure of justice.

30. Power to make Rules.— (1) The Government may, by notification,make rules, either prospectively or retrospectively, for carrying out thepurposes of this Act.

(2) In particular and without prejudice to the generality ofthe foregoing power, such rules may provide for the following matters,

A.P. Tax on Entry of M.V. into Local Areas Act, 1996 [S. 30

895

namely:—

(a) the duties and powers of officers appointed for the purpose ofenforcing the provisions of this Act;

(b) all matters expressly required or allowed by this Act, to beprescribed;

(c) generally regulating the procedure to be followed and the formsto be adopted in the proceedings under this Act;

(d) any other matter including levy of fees for which there is nospecific provision in this Act, and for which provision is in theopinion of the Government, necessary for giving effect to thepurposes of this Act; and

(e) the procedure for any other matter incidental to the disposal ofappeal and the value of Court-Fee Stamp, which a memorandumof appeal or revision should bear.

(3) Every rule made under this section shall immediately after it ismade, be laid before the Legislative Assembly of the State if it is in session andif it is not in session, in the session immediately following for a total period offourteen days which may be comprised in one session, or in two successivesessions and if before the expiration of the session in which it is so laid or thesession immediately following the Legislative Assembly agrees in makingany modification in the rule or in the annulment of the rule, the rule shall fromthe date on which the modification or annulment is notified have effect only insuch modified form or shall stand annulled as the case may be; so however,that any such modification or annulment shall be without prejudice to thevalidity of anything previously done under that rule.

31. Repeal of Ordinance 22 of 1996.— The Andhra Pradesh Taxon Entry of Motor Vehicles into Local Areas Ordinance, 1996 is herebyrepealed.

D D D D D

A.P. Tax on Entry of M.V. into Local Areas Act, 1996S. 31]

896

ANDHRA PRADESH TAX ONENTRY OF MOTOR VEHICLES

INTO LOCAL AREAS RULES, 1996

[G.O.Ms.No.849, Revenue (CT.II) Department, dt.18-10-1996]

In exercise of the powers conferred by Section 30 of the AndhraPradesh Tax on Entry of Motor Vehicles into Local Areas Act, 1996 (A.P. ActNo. 26 of 1996), the Governor of Andhra Pradesh hereby makes the followingRules.

1. Title and Commencement.— (i) These rules may be called theAndhra Pradesh Tax on Entry of Motor Vehicles into Local Areas Rules, 1996.

(ii) They shall come into force with effect on and from the 1st August,1996.

2. Definitions.— (1) In these Rules, unless the context otherwiserequires :—

(a) “Act” means the Andhra Pradesh Tax on Entry of Motor Vehiclesinto Local Areas Act, 1996.

(b) “Form” means a form appended to these rules.

(c) “Government Treasury” means a Treasury or Sub-Treasury ofthe Government.

(d) “Month” means a calendar month.

(e) “Section” means a Section of the Act.

(2) Words and expressions used but not defined in these rules shallhave the same meaning respectively assigned to them in the Act.

3. Returns.— (1) Every Importer other than those falling under sub-rule (6), liable to pay tax under Section 3 of the Act, shall submit, so as to reachthe assessing authority on or before the 20th of every month, a return in FormM-1 in duplicate showing the total and net purchase price of all or any of themotor vehicles on which tax is payable for the preceeding month and alongwith the return he shall submit a receipt from the Government Treasury or acrossed demand draft in favour of the assessing authority for the full paymentof tax payable for the month to which the return is related.

896

897

(2) In the case of an importer having more than one place of businessin the local area, all returns prescribed by these rules shall be submitted bythe principal place of business in the local area in the State and shall includethe total purchase value of all or any of the motor vehicles of all the places ofhis business. Each place of business in any local area shall also :—

(a) submit to the assessing authority of the local area in which it issituated a return of the total and net purchase value of the motorvehicles of the place of business in Form M-1; and

(b) intimate to such authority the fact that the return of the total andnet purchase value of all motor vehicles is included in the returnsubmitted by its principal place of business in the local area andspecify the name and address of such principal place of businessin the local area.

(3) The returns so filed shall subject to the provisions of sub-rules (4)and (5) be provisionally accepted.

(4) Where any importer fails to submit the return in respect of anymonth before the date prescribed in that behalf or if the return submittedappears to be incorrect or incomplete the assessing authority shall afterfollowing the procedure prescribed in Rule 4 determine the purchase value tothe best of the judgment and provisionally assess the tax or taxes payable forthe month and shall serve upon the dealer a notice in Form D-1 and the importershall pay the sum demanded within the time and in the manner prescribed inthe notice.

(5) Where any importer submits a return without a GovernmentTreasury receipt or crossed demand draft for the full amount of the tax payablethe assessing authority shall provisionally assess the taxes payable for themonth and shall serve upon the dealer a notice in Form D-1 for the tax due andthe importer shall pay the sum demanded within the time specified in thenotice.

(6) (a) An importer other than a dealer shall file a return in FormM-2 along with the proof of payment of tax due thereon before such authority,as may be notified by the Commissioner, within fifteen days from the date ofEntry of such vehicle into a local area or before an application is made forregistration of the said vehicle or assignment of a new registration mark tosuch vehicle under the Motor Vehicles Act, 1988, whichever is earlier.

(b) Tax due thereon shall be paid by tendering a challan or a demanddraft or payment order issued in favour of such authority.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996R. 3]

898

(c) If such authority is satisfied that return is true, correct andcomplete he shall pass an order in Form M-3 and a copy shall bemarked to the importer.

(d) If the return filed in Form M-2 does not appear to be correct andcomplete the designated authority shall determine the purchasevalue of motor vehicle and tax to be paid thereon and serve onthe importer a notice in Form M-4 and the importer shall pay thesum demanded within the time and in the manner specified inthe notice.

4. Assessment.— (1) After the close of the year for which returnshave been submitted under Rule 3 or in the course of the year, where animporter has discontinued business, the assessing authority shall if he issatisfied after such scrutiny of the accounts and making such enquiry as heconsiders necessary that the returns filed are correct and complete, finallyassess in a single order on the basis of the return(s), the tax payable for theyear to which the return(s) relate.

(2) Where any importer fails to submit return or returns before thedate prescribed in that behalf or if any return or returns submitted by himappears to the assessing authority to be incorrect or incomplete, the assessingauthority shall after giving the dealer an opportunity as mentioned in sub-section (3) of Section 8 determine the purchase value of motor vehicles to thebest of his judgment and finally assess in a single order the tax or taxes payable.

(3) If on final assessment under sub-rule (1) or sub-rule (2), any tax isfound to be due from the importer after deducting the tax or taxes paid by himtowards the provisional assessment made under Rule 3, the assessing authorityshall serve on the importer a notice in Form D-2, and the dealer shall pay thesum demanded in the notice therein. If, however, any refund of tax, is found tobe due to the dealer, the assessing authority shall serve on him a notice inForm R.

5. (1) Where any business carried on by a firm, a Hindu undividedfamily or an association has been discontinued or dissolved, the assessingauthority shall make an assessment under Section 8 of the Act on the firm, theHindu undivided family or association as if no such discontinuance ordissolution had taken place, and all the provisions of the Act including theprovisions relating to the levy of penalty or any other sum chargeable underthe provisions of the Act shall apply, so far as may be to such assessment.

(2) Every person who was at the time of such discontinuance ordissolution, a partner of such firm or a member of such Hindu undivided

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [R. 5

899

family or association and legal representative of any such persons who isdeceased shall be jointly and severally liable for the amount of the tax, penaltyor other sum payable, and all the provisions of the Act, so far as may be, shallapply to any such assessment or levy of penalty or other sum.

6. (1) Subject to provisions of Section 13 any person aggrieved byan order passed or proceedings recorded under the provisions of the Act mayappeal to the Appellate Deputy Commissioner of Commercial Taxes havingjurisdiction over the area :

Provided that the Commissioner may, either suo motu or on anapplication, for the reasons to be recorded in writing, transfer an appealpending before an Appellate Deputy Commissioner of Commercial Taxes toanother Appellate Deputy Commissioner of Commercial Taxes :

Provided further that the order of transfer shall be communicated tothe appellant or petitioner, to every person affected by the order, the authorityagainst whose order the appeal or petition was preferred and to the AppellateDeputy Commissioner of Commercial Taxes.

(2) (i) Every such appeal shall be in Form-I and verified in themanner specified therein.

(ii) It shall be in duplicate.

(iii) It shall be accompanied by the following documents namely :—

(a) where it is an appeal against an order of assessment, by aGovernment Treasury receipt in support of having paidthe fee calculated at the rate of two per cent of the disputedtax or penalty subject to a minimum of fifty rupees and amaximum of rupees one thousand;

(b) where it is an appeal against an order not being an order ofassessment or penalty by Court fee stamps of the value ofthree rupees affixed to one of the copies.

(3) The appeal may be sent to the appellate authority by registeredpost or be presented to that authority or to such officer as the appellateauthority may appoint in this behalf by the appellant or by his authorisedagent or a legal practitioner.

(4) The appellate authority after giving the appellant reasonableopportunity of being heard pass such orders as laid down in sub-section (3) ofsection 13 of the Act.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996R. 6]

900

7. For the purpose of the exercise of the powers of the nature referredto in sub-section (1) of Section 14, the authorities specified in Column (1) of theTable below shall be deemed to be subordinate to the authority specified inthe corresponding entry in Column (2) thereof.

TABLE

(1) (2)

Commissioner of CommercialTaxes.

Commissioner of CommercialTaxes.

Additional Commissioner ofCommercial Taxes.

Deputy Commissioner of Commer-cial Taxes of the Division concerned.

1. Additional Commissioners ofCommercial Taxes

2. Joint Commissioner ofCommercial Taxes includingAppellate Deputy Commi-ssioner of Commercial Taxes,Assistant Commissionersof Commercial Taxes andCommercial Tax Officers.

3. Deputy Commissioner ofCommercial Taxes (includingAppellate Deputy Commi-ssioners of Commercial Taxes,Assistant Commissioners ofCommercial Taxes andCommercial Tax Officers).

4. Assistant Commissioners ofCommercial Taxes and Com-mercial Tax Officers.

8. Every order of an Appellate or Revising Authority undersection 13 or Section 14 respectively, as the case may be, shall be communi-cated to the Appellant or the party affected by the order, to the assessingAuthority against whose order the appeal was filed or to any authorityconcerned.

9. (1) (i) Every appeal preferred under Section 15 to the AppellateTribunal shall be in Form-II and shall be verified in the manner specifiedtherein.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [R. 9

901

(2)(i) Every such appeal shall clearly set forth the grounds ofappeal and the relief prayed for; and shall be accompanied by the following;namely :—

(a) four spare copies thereof;

(b) five copies of the order appealed against (one of which shallbe the original or the authenticated copy); and

(c) four copies of the order of the assessing authority.

(ii) it shall be accompanied by a Treasury receipt in support of havingpaid :—

(a) in cases where the levy of tax or penalty is disputed; a feecalculated at the rate of two per cent of the disputed taxsubject to a minimum of rupees one hundred and amaximum of rupees two thousand; and

(b) a fee of rupees one hundred in all other cases.

(2) If the Appellate Tribunal allows any appeal preferred by anassessee under Section 15, it may in its discretion, by order refund eitherwholly or partly the fees paid by the assessee under sub-section (3) ofSection 15.

(3) Every order passed by the Appellate Tribunal under Section 15shall be communicated to the Appellate Deputy Commissioner and to theState Representative before the Appellate Tribunal, in addition to thosespecified in the sub-section (8) of Section 15.

10. (1) Within ninety days from the date on which the order of theAppellate Tribunal, under sub-section (4) of Section 15 was communicated tothe importer, he or the State Representative may prefer a petition to the HighCourt of Andhra Pradesh under Section 16 against the order on the groundthat the Appellate Tribunal has decided either erroneously or has failed todecide any question of law.

(2) Every petition under sub-section (1) of Section 16 of the Act toHigh Court shall be in Form-III and shall be verified in the manner specifiedtherein.

(3) Such petition shall be accompanied by a certified copy of theorder of the Appellate Tribunal and where it is preferred by the proprietor beaccompanied by a fee of rupees five hundred.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996R. 10]

902

11. Every appeal under sub-section (1) of Section 17 to the High Courtshall be in Form-IV and shall be verified in the manner specified therein. Itshall be preferred within sixty days from the date on which the order wascommunicated and shall be accompanied by a certified copy of the order ofthe Commissioner appealed against and a fee calculated at the rate of twopercent of tax or penalty under dispute subject to a minimum of one hundredrupees and a maximum of two thousand rupees.

12. (1) Every application for review under Section 16 or Section 17 tothe High Court shall be in either Form-V or in Form-VI respectively and shallbe verified in the manner specified therein.

(2) It shall be preferred within one year from the date of communi-cation to the petitioner of the order sought to be reviewed, and where it ispreferred by the importer be accompanied by a fee of Rupees five hundred.

Accounts

13. (1) Every importer who is a dealer in motor vehicle and who isliable to pay tax under the Act shall keep and maintain a true and correctaccount promptly in any of the languages specified in the Eighth Schedule tothe Constitution of India, or in English language showing :—

(i) the value of motor vehicle bought by him;

(ii) names and addresses of each of the person from whom motorvehicles were purchased and supported by a bill or delivery noteissued by the seller; and

(iii) the descriptive and quantitative particulars of motor vehicles. Incase they are not bought but received into or a godown of theimporter with the names and addresses of the owners supportedby necessary vouchers and the circumstances under which theyare received or kept.

2. An importer not being a dealer shall keep minimum accounts toindicate the details such as purchase value etc., in respect of the entry of motorvehicle into local area effected by him.

Miscellaneous

14. (1) Any Assessing, Appellate or Revising Authority may, at anytime within four years from the date of any order passed by him, rectify anyclerical or arithmetical mistake apparent from the record :

Provided that no such rectification which has the affect of enhancing anassessment or any penalty shall be made unless the assessing or appellate

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [R. 14

903

authority has given notice to the dealer of his intention to do so, and hasallowed him a reasonable opportunity of being heard.

15. If an importer enters into a partnership in regard to his business,he shall report the fact to the assessing authority within thirty days of hisentering into such partnership. The importer and the partner shall jointlyand severally be responsible for the payment of the tax or renewal of penaltyleviable under the Act.

16. In case of default of payment of the tax or penalty leviable underthe Act, the properties of the firm may be proceeded against, in the first instancefor the recovery of the amount due from the firm.

17. If a partnership is dissolved, every person who as a partner shallsend a report of the dissolution to the assessing authority within thirty daysof such dissolution.

18. If at any time a dealer :—

(a) discontinues or sells or otherwise disposes of the whole or anypart of any business carried on by him; or

(b) changes his place of business or any of his places of business;or

(c) opens a new place of business; or

(d) changes the name of any business carried on by him, the dealeror if he is dead, the legal representative of the deceased, shallnotify the fact to the assessing authority concerned within thirtydays thereafter.

19. Any assessing, or revising authority may issue summons inForm IX for the production of any document or for the appearance of anyperson.

20. The service on a dealer of any notice, summon, order orproceedings under the Act or under these rules, may be effected in any of thefollowing ways, namely :—

(a) by delivering or tendering it to such importer or to his manageror to his agent who is concerned with the business; or

(b) if such importer or his manager or agent is not found, by leavingit at his last known place of business or residence or by deliveringor tendering to some adult member of his family; or

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996R. 20]

904

(c) if the address of such importer is known to the assessing authority,by sending it to him by registered post with acknowledgmentdue; or

(d) if any or all of the modes aforesaid is not practicable, by affixingit in some conspicuous place at his last known place of businessor residence.

Designated Officer to ascertain payment of amount of tax

21. The Designated Officer, who is notified under sub-section (2) ofSection 4 of the Act, shall ascertain whether the importer not being a dealerhas paid the amount of tax due in full within the period of fifteen days fromthe date of entry of the motor vehicle into a local area or before an applicationis made for registration under the Motor Vehicles Act, 1988 whichever is earlier,by obtaining from the Assessing Authority a copy of the order in Form M-3issued by the Assessing Authority to the importer. If the Importer has notpaid the tax, then the Designated Officer shall impound the vehicle forthwith.”

22. Reduction of tax paid by an importer under the *General SalesTax Law in force in any other State or Union Territory :—

(1) In assessing the amount of tax payable in respect of any periodby an importer, who is not a dealer in motor vehicles the AssessingAuthority shall, in respect of his purchase of motor vehicle, theentry of which into the local area of the State is liable to tax, as thecase may be, reduce the following amounts; namely :—

(a) the sum collected separately by way of sales tax from theimporter by the manufacturer/authorised dealer, situatedin any other State or Union Territory in respect of the motorvehicle so purchased under the law relating to *GeneralSales Tax as may be in force in that State or Union Territory,or,

(b) in case not covered in Clause (a) above, the sum assessedby a competent authority and in fact paid into theGovernment Treasury of any other State or Union Territoryin respect of a motor vehicle which is subsequentlypurchased by the importer :

Provided that, no reduction under Clause (b) shall be granted unlessthe importer proves that the said tax has in fact been assessed by a competent

*. Now see Value Added Tax Act.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [R. 22

905

authority and has in fact been paid into the Government Treasury of theconcerned State or Union Territory.

23. Notice for payment of penalty as specified in Section 18, shall beissued in Form-VII.

FORM - M1

MONTHLY RETURN OF PURCHASE VALUE

(To be filled by Importer who is a dealer)

[See Rules 3(1) and (4)]

To

The Commercial Tax Officer.

I..............................Son/Daughter/Wife of ............................being the importeron behalf of dealer carrying on business known as ..........................furnishherewith the statement of total and net purchase value of the motor vehiclesentered into local area(s) during the ......................(month/year) and give thefollowing connected particulars:—

(1) Name and address of the manager of the business.

(2) Status or relationship of the person who signs this form............................ (Manager/Partner/Proprietor etc.,)

(3) Name and address of the Principal place of business withparticulars of registration.

Name ......................................

A.P.T.E.M.V. into Local Areas Act. A.P.G.S.T. Act C.S.T. Act

Registration Certificate No.

Address:

....................................................

....................................................

....................................................

(4) Name (s) of the other places of business in notified local areas andthe address of every such place (if space provided for is notsufficient, information shall be furnished in a separate sheet andenclosed to this return)

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996F. M1]

906

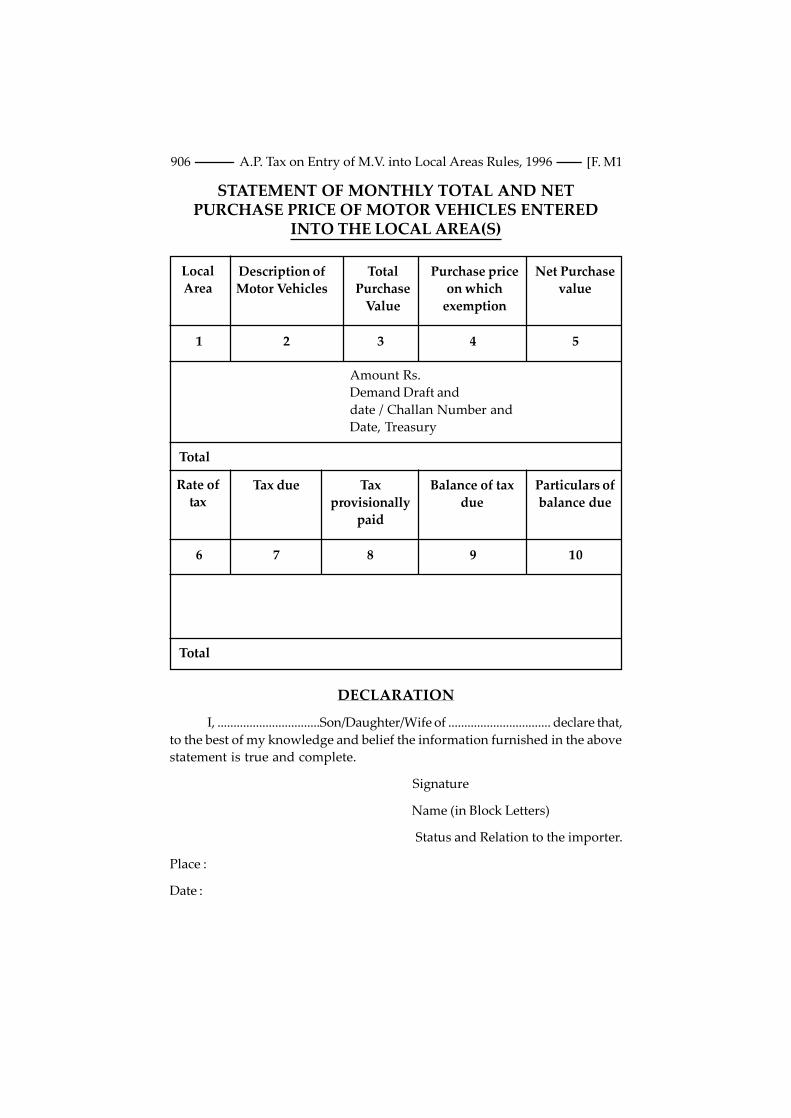

STATEMENT OF MONTHLY TOTAL AND NETPURCHASE PRICE OF MOTOR VEHICLES ENTERED

INTO THE LOCAL AREA(S)

DECLARATION

I, ................................Son/Daughter/Wife of ................................ declare that,to the best of my knowledge and belief the information furnished in the abovestatement is true and complete.

Signature

Name (in Block Letters)

Status and Relation to the importer.

Place :

Date :

LocalArea

Description ofMotor Vehicles

TotalPurchase

Value

Purchase priceon which

exemption

Net Purchasevalue

1 2 3 4 5

Rate oftax

Tax due Taxprovisionally

paid

Balance of taxdue

Particulars ofbalance due

6 7 8 9 10

Amount Rs.Demand Draft anddate / Challan Number andDate, Treasury

Total

Total

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [F. M1

907

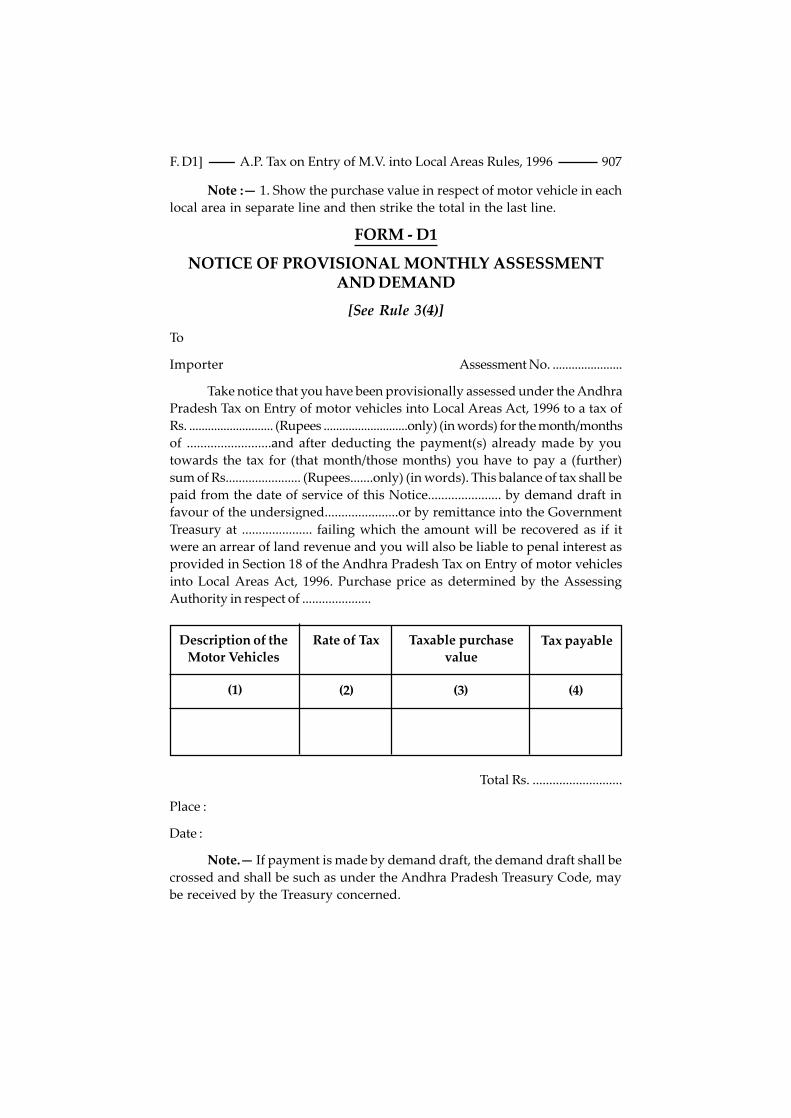

Note :— 1. Show the purchase value in respect of motor vehicle in eachlocal area in separate line and then strike the total in the last line.

FORM - D1

NOTICE OF PROVISIONAL MONTHLY ASSESSMENTAND DEMAND

[See Rule 3(4)]

To

Importer Assessment No. ......................

Take notice that you have been provisionally assessed under the AndhraPradesh Tax on Entry of motor vehicles into Local Areas Act, 1996 to a tax ofRs. ........................... (Rupees ...........................only) (in words) for the month/monthsof .........................and after deducting the payment(s) already made by youtowards the tax for (that month/those months) you have to pay a (further)sum of Rs....................... (Rupees.......only) (in words). This balance of tax shall bepaid from the date of service of this Notice...................... by demand draft infavour of the undersigned......................or by remittance into the GovernmentTreasury at ..................... failing which the amount will be recovered as if itwere an arrear of land revenue and you will also be liable to penal interest asprovided in Section 18 of the Andhra Pradesh Tax on Entry of motor vehiclesinto Local Areas Act, 1996. Purchase price as determined by the AssessingAuthority in respect of .....................

Description of theMotor Vehicles

Rate of Tax Taxable purchasevalue

Tax payable

(1) (2) (3) (4)

Total Rs. ...........................

Place :

Date :

Note.— If payment is made by demand draft, the demand draft shall becrossed and shall be such as under the Andhra Pradesh Treasury Code, maybe received by the Treasury concerned.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996F. D1]

908

FORM - D2

[See Rule 4(3)]

NOTICE OF ANNUAL ASSESSMENT AND DEMAND

To

Importer Assessment No. ..............

Take notice that you have been finally assessed under the AndhraPradesh Tax on Entry of motor vehicles into Local Areas Act, 1996 to a tax ofRs........................... (Rupees................................................. only (in words) for the yearending ..................... and that after deducting the total amount of the monthlypayment(s) already made by you towards the tax for that year, you have topay a (further) sum of Rs..................... (Rupees ...................................... only) (inwords). This balance of tax shall be paid within (.............days) from the date ofservice of this notice ........................by demand draft in favour of the undersignedor by remittance into the Government Treasury at .............................failing whichthe amount will be recovered as if it were an arrear of land revenue and youwill also be liable to penal interest as provided in Section 18 of the AndhraPradesh Tax on Entry of motor vehicles into Local Areas Act, 1996.

Purchase price as determined by the Assessing Authority in respectof .......................................

Description of theMotor Vehicles

Rate of Tax Taxablepurchase value

Tax payable

(1) (2) (3) (4)

Total Rs. ...........................

Place :

Date :

Assessing Authority

Note.— If payment is made by demand draft, the demand draft shallbe crossed and shall be such as under the Andhra Pradesh Treasury Code,may be received by the Treasury concerned.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [F. D2

909

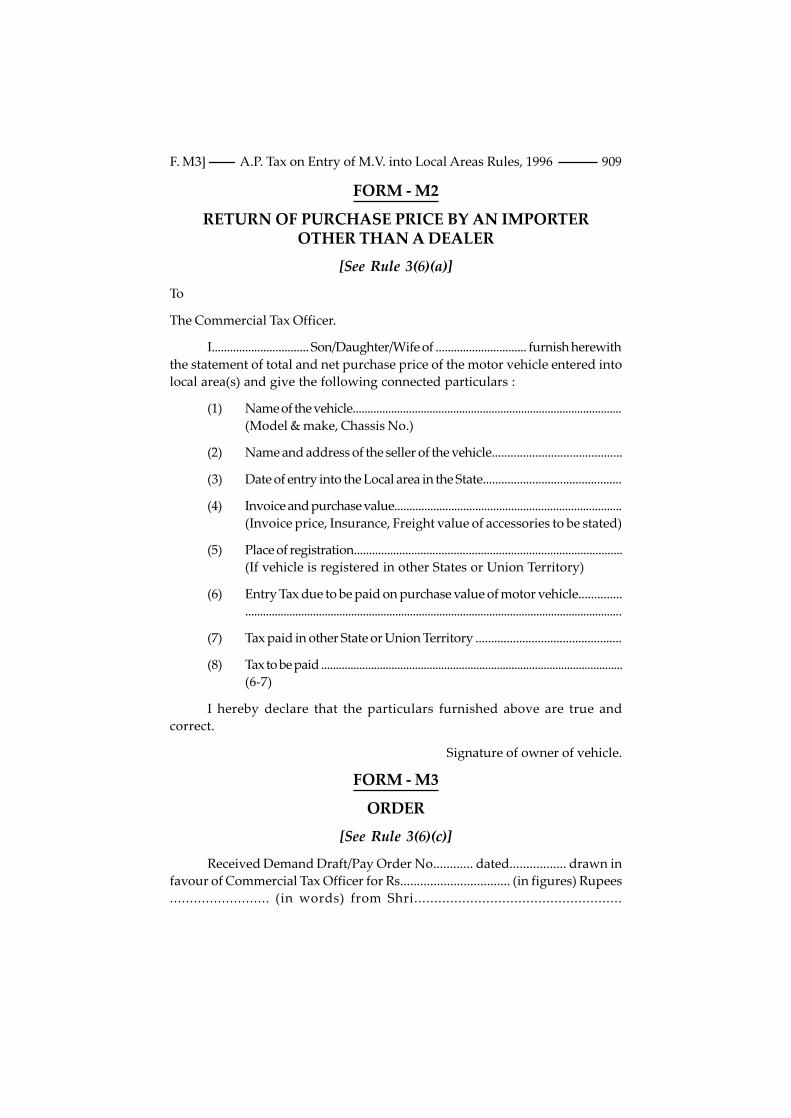

FORM - M2

RETURN OF PURCHASE PRICE BY AN IMPORTEROTHER THAN A DEALER

[See Rule 3(6)(a)]

To

The Commercial Tax Officer.

I................................ Son/Daughter/Wife of .............................. furnish herewiththe statement of total and net purchase price of the motor vehicle entered intolocal area(s) and give the following connected particulars :

(1) Name of the vehicle...........................................................................................(Model & make, Chassis No.)

(2) Name and address of the seller of the vehicle..........................................

(3) Date of entry into the Local area in the State.............................................

(4) Invoice and purchase value............................................................................(Invoice price, Insurance, Freight value of accessories to be stated)

(5) Place of registration.........................................................................................(If vehicle is registered in other States or Union Territory)

(6) Entry Tax due to be paid on purchase value of motor vehicle..............................................................................................................................................

(7) Tax paid in other State or Union Territory ...............................................

(8) Tax to be paid .......................................................................................................(6-7)

I hereby declare that the particulars furnished above are true andcorrect.

Signature of owner of vehicle.

FORM - M3

ORDER

[See Rule 3(6)(c)]

Received Demand Draft/Pay Order No............ dated................. drawn infavour of Commercial Tax Officer for Rs................................. (in figures) Rupees......................... (in words) from Shri....................................................

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996F. M3]

910

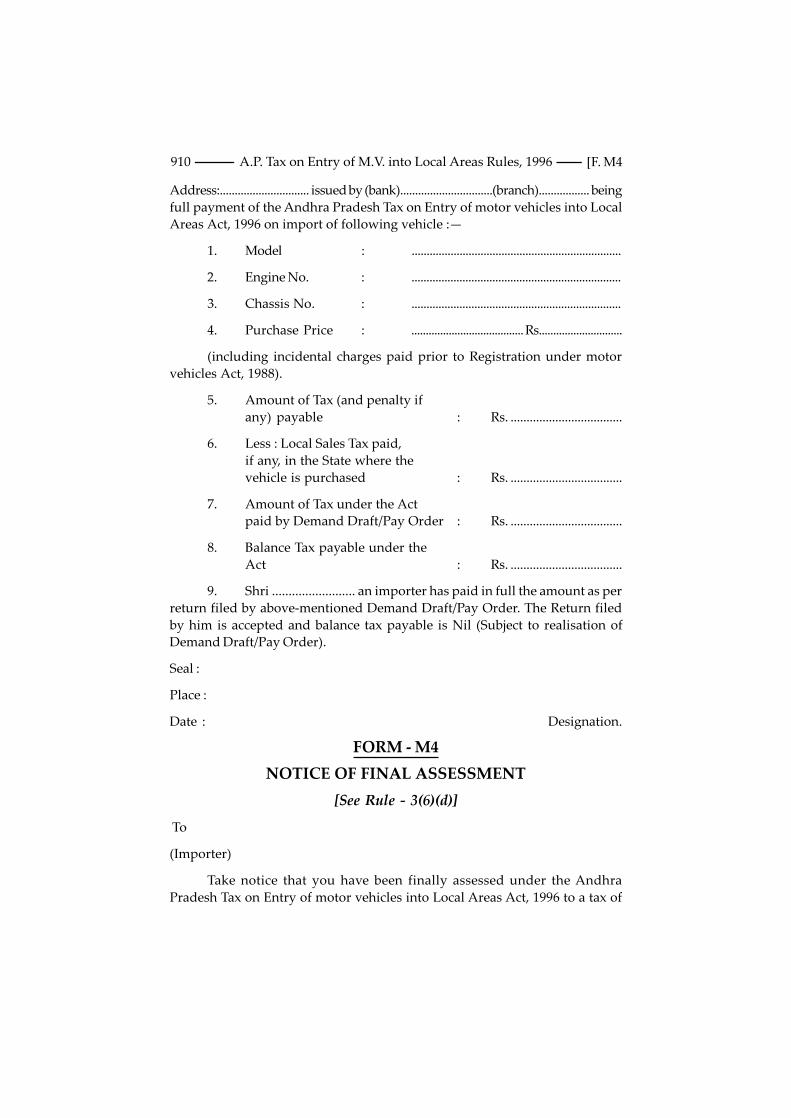

Address:.............................. issued by (bank)...............................(branch)................. beingfull payment of the Andhra Pradesh Tax on Entry of motor vehicles into LocalAreas Act, 1996 on import of following vehicle :—

1. Model : ......................................................................

2. Engine No. : ......................................................................

3. Chassis No. : ......................................................................

4. Purchase Price : ....................................... Rs.............................

(including incidental charges paid prior to Registration under motorvehicles Act, 1988).

5. Amount of Tax (and penalty ifany) payable : Rs. ...................................

6. Less : Local Sales Tax paid,if any, in the State where thevehicle is purchased : Rs. ...................................

7. Amount of Tax under the Actpaid by Demand Draft/Pay Order : Rs. ...................................

8. Balance Tax payable under theAct : Rs. ...................................

9. Shri ......................... an importer has paid in full the amount as perreturn filed by above-mentioned Demand Draft/Pay Order. The Return filedby him is accepted and balance tax payable is Nil (Subject to realisation ofDemand Draft/Pay Order).

Seal :

Place :

Date : Designation.

FORM - M4

NOTICE OF FINAL ASSESSMENT

[See Rule - 3(6)(d)]

To

(Importer)

Take notice that you have been finally assessed under the AndhraPradesh Tax on Entry of motor vehicles into Local Areas Act, 1996 to a tax of

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [F. M4

911

Rs.................. (Rupees................ only) (in words).The total amount of tax paid byyou already is Rs.....(Rupees.........only) (in words). You have to pay a furthersum of Rs................. (Rupees .............only) (in words). This balance of tax shall bepaid within............. days from the date of service of this notice by Cheque/D.D.in favour of undersigned or by remittance into the Government Treasury at............ failing which the amount will be recovered as if it were an arrear ofland revenue and you will also be liable to interest.

Purchase value and total tax payable as determined by the assessingauthority in respect of :—

Descriptionof the Motor

Vehicles

Rate ofTax

Taxablepurchase

value

Taxpayable

(1) (2) (3) (4)

Tax paid Balance tobe paid

(5) (6)

Total Rs. ....................

Place :

Date : Assessing Authority.

Note: If payment is made by demand draft, the demand draft shall becrossed and shall be such as under the Andhra Pradesh Treasury Code, maybe received by the Treasury concerned.

FORM - R

NOTICE OF ANNUAL ASSESSMENT ANDREFUND ORDER

[See Rule - 4(3)]

To

(Importer)

Take notice that you have been finally assessed under the AndhraPradesh Tax on Entry of motor vehicles into Local Areas Act, 1996 to a tax ofRs..................... (Rupees .................... only) (in words) for the year ending the .............The total amount of tax paid by you already is Rs............. (Rupees ............... only)(in words) that is Rs................... in excess of the tax due.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996F. R]

912

(2) Out of the above excess a sum of Rs.............. will be adjustedtowards tax due from you for the period.

A refund order for the amount of Rs.................... is enclosed. You shouldapply to the Government Treasury at ............. (for the refund of the sum).................. within three months from the date of issue of this notice failingwhich the amount will lapse to the Government.

Purchase value as determined by the assessment authority in respectof .............................

Description of theMotor Vehicles

Rate of Tax Taxable purchasevalue

Tax payable

(1) (2) (3) (4)

Place :

Date : Assessing Authority.

*in Para 3 the in applicable portion shall be scored out.

FORM - I

FORM OF APPEAL UNDER SECTION 13

[See Rule 6(2)(i)]

To

The Appellate Deputy Commissioner of

Commercial Taxes of ....................................

The ...................... day of ................. 19 .........

1. Name(s) of appellant(s)

2. Assessment Year

3. Authority passing the order or proceeding disputed.

4. Date on which the order or proceeding was communicated.

5. Address to which notice may be sent to the Applicant.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [F. I

913

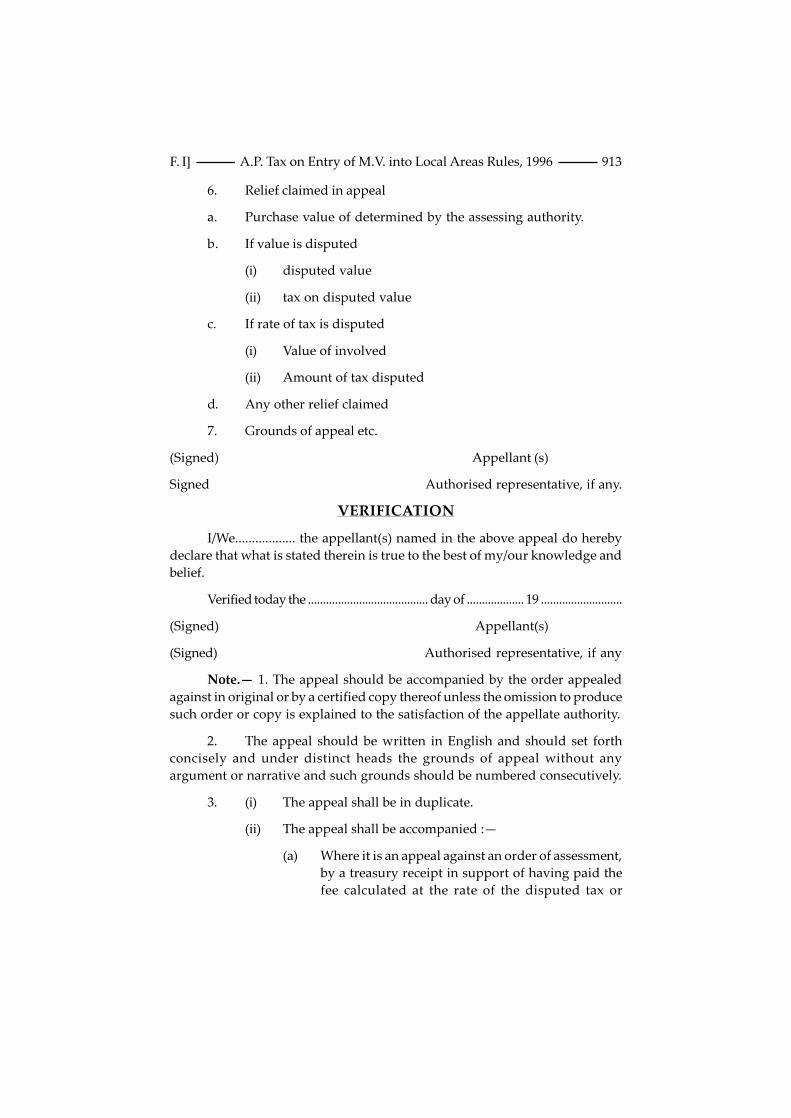

6. Relief claimed in appeal

a. Purchase value of determined by the assessing authority.

b. If value is disputed

(i) disputed value

(ii) tax on disputed value

c. If rate of tax is disputed

(i) Value of involved

(ii) Amount of tax disputed

d. Any other relief claimed

7. Grounds of appeal etc.

(Signed) Appellant (s)

Signed Authorised representative, if any.

VERIFICATION

I/We.................. the appellant(s) named in the above appeal do herebydeclare that what is stated therein is true to the best of my/our knowledge andbelief.

Verified today the ........................................ day of ................... 19 ...........................

(Signed) Appellant(s)

(Signed) Authorised representative, if any

Note.— 1. The appeal should be accompanied by the order appealedagainst in original or by a certified copy thereof unless the omission to producesuch order or copy is explained to the satisfaction of the appellate authority.

2. The appeal should be written in English and should set forthconcisely and under distinct heads the grounds of appeal without anyargument or narrative and such grounds should be numbered consecutively.

3. (i) The appeal shall be in duplicate.

(ii) The appeal shall be accompanied :—

(a) Where it is an appeal against an order of assessment,by a treasury receipt in support of having paid thefee calculated at the rate of the disputed tax or

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996F. I]

914

penalty subject to a minimum fifty rupees and amaximum of one thousand rupees. The fee shall becredited into a Government Treasury to thefollowing Account “.....................”

(b) Where it is an appeal against an order not being anassessment, by Court fee stamps of the value of threerupees affixed to one of the copies.

FORM - II

FORM OF APPEAL MEMORANDUM TOTHE APPELLATE TRIBUNAL

[See Rule 9(1)(i)]

Appeal Memorandum to the Appellate TribunalIn the Appellate Tribunal, Andhra Pradesh.

No. ............. of 19 ...........

...................................... ...................................... Appellant (s)

Versus

...................................... ....................................... Respondent (s)

1. District in which assessment was made.

2. Assessment Year.

3. Authority passing the original order indispute.

4. Appellate Deputy Commissioner ofCommercial Taxes passing the order underSection 13(3) or the Deputy Commissioner orJoint Commissioner/Additional Commi-ssioner passing an order under Section 14(2).

5. Date of Communication of the order nowappealed against.

6. Address to which notice may be sent to theappellant.

7. Address to which notices may be sent to therespondent.

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [F. II

915

8. Relief claimed in appeal:

(a) Purchase Value of motor Vehicledetermined by the assessing authoritypassing the assessing order disputed.

(b) Purchase value of motor vehicle confir-med by the Appellate Deputy Commi-ssioner of Commercial Taxes or byDeputy Commissioner or Joint Commi-ssioner/ Additional Commissioner asthe case may be.

(c) If purchase value is disputed—

(i) Disputed value

(ii) Tax due on the dispute value

(d) If rate of tax is disputed—

(i) Purchase value involved

(ii) Amount of the tax

(e) Specify, if any, other relief claimed.

9. Grounds of appeal etc.

(Signed) Appellant(s)

(Signed) Authorised representative, if any.

VERIFICATION

I/We.......................... the appellant(s) do hereby declare that what is statedabove is true to the best of my/our knowledge and belief.

Verified today the ........... day of ........19 ...................

(Signed) Appellant(s)

(Signed) Authority representative, if any.

Note.— 1. The appeal should be in quadruplicate and should beaccompanied by four copies (atleast one of which should be the original or anauthenticated copy) of the order appealed against and also three copies of theorder of the assessing authority.

2. The appeal shall be accompanied by a Treasury receipt in supportof having paid a fee calculated at the rate of two per cent of the disputed tax or

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996F. II]

916

penalty subject to a minimum of Rs.100/- and maximum of Rs.2,000/- incases where the levy of tax is disputed and fee of Rs.100/- in all other cases. Thefee should be credited in a Government Treasury to the following head ofaccount :—

“.........................................”

3. The appeal should be written in English and should set forthconcisely and under distinct heads the grounds of appeal without anyargument or narrative and such grounds should be numbered consecutively.

FORM - III

REVISION PETITION

In the High Court of Andhra Pradesh at Hyderabad[Appellate Side]

Memorandum of Civil Revision Petition

[Under Section 16(1)]

[See Rule 10(2)]

Civil Revision Petition No. ..................................

...................................... ...................................... Petitioner

Versus

...................................... ....................................... Respondent

Revision/Petition presented to the High Court to revise the Order of theAppellate Tribunal.

Date ................................ and passed in ..................................

1. District in which the assessment was made.

2. Assessment year.

3. The designation of the Officer whose orderswere appealed against before the AppellateTribunal.

4. Date of Communication of the order of theAppellate Tribunal.

5. Findings of the Appellate Tribunal (State inserial and appropriate order the relevantfindings arrived at by the Tribunal).

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996 [F. III

917

6. Question of law raised for decision by the HighCourt (here formulate the question of lawraised concisely, etc.)

(Signed) Petitioner(s)

(Signed) Authorised representative, if any.

VERIFICATION

I/We................................ the petitioner(s) do hereby declare that what isstated above is true to the best of my/our knowledge and belief.

Verified today the ...................... day of ................... 19

(Signed) Petitioner(s)

(Signed) Authorised representative, if any

Note.— 1. The petition should be accompanied by a certified copy ofthe order of the Appellate Tribunal.

2. The petition should (if preferred by a dealer) be accompanied bya fee of Rs. 500/-

3. The petition should be written in English and should be set forthconcisely and under distinct heads the facts of the case, the findings arrived atby the Tribunal, and the questions of law, raised consecutively. There shouldbe no argument or narrative.

FORM - IV

APPEAL

In the High Court of Andhra Pradesh at Hyderabad (Appellate Side)Memorandum of appeal against order

[Under Section 17]

[See Rule 11]

Appeal against order No. ..................

...................................... ...................................... Appellant (s)

Versus

...................................... ....................................... Respondent (s)

Appeal against the order of the Commissioner of Commercial Taxes -dated ................and .............. passed in ................................................

A.P. Tax on Entry of M.V. into Local Areas Rules, 1996F. IV]

918

1. District in which the assessment was made

2. Assessment year

3. Assessing Authority passing the originalorder.