Analyst Presentation 25Aug.ppt - Oil India · This presentation contains certain forward looking...

35

August 25, 2011

Transcript of Analyst Presentation 25Aug.ppt - Oil India · This presentation contains certain forward looking...

August 25, 2011

This presentation contains certain forward looking statements concerning OIL India’s future business

prospects and business profitability, which are subject to a number of risks and uncertainties and the

actual results could materially differ from those in such forward looking statements. The risks and

Disclaimer

actual results could materially differ from those in such forward looking statements. The risks and

uncertainties relating to these statements include, but not limited to, risks and uncertainties, regarding

fluctuations in earnings, our ability to manage growth, competition (both domestic and

international), economic growth in India, ability to attract and retain highly skilled professionals, time and

cost over runs on projects, our ability to manage our international operations, government policies and

actions with respect to investments, fiscal deficits, regulations, etc., interest and other fiscal costs

generally prevailing in the economy. The company does not undertake to make any announcement in case

any of these forward looking statements become materially incorrect in future or update any forward

looking statements made from time to time by or on behalf of the company.

An Overview

Oil India: Brief Overview

� Independent India’s first commercial oil discoveries, with the first made in 1953Rich Heritage

India’s premier Oil & Gas “Navratna” company engaged in the exploration, development, production and

transportation of crude oil and natural gas in India

� Presence across Oil & Gas Value Chain (E&P, Transportation and Downstream)

� Infrastructure to support growth

Integrated O&G

Player

Strong

� Domestic acreage: 127,260 square kilometers;

� International acreage: 38,605 square kilometersLarge Acreage

� Total 2P reserves of over 944 mmboe; with RR ratio of over 142% in FY11 Strong

Reserve Base

� Revenue: 9,549 Cr (FY11), 2,669 Cr. Q1(FY12)

� PAT : 2,888 Cr (FY11), 850 Q1(FY12)

� Market cap : 31,523 Cr1

Strong

Financials

Note:1. As of Aug 19, 2011

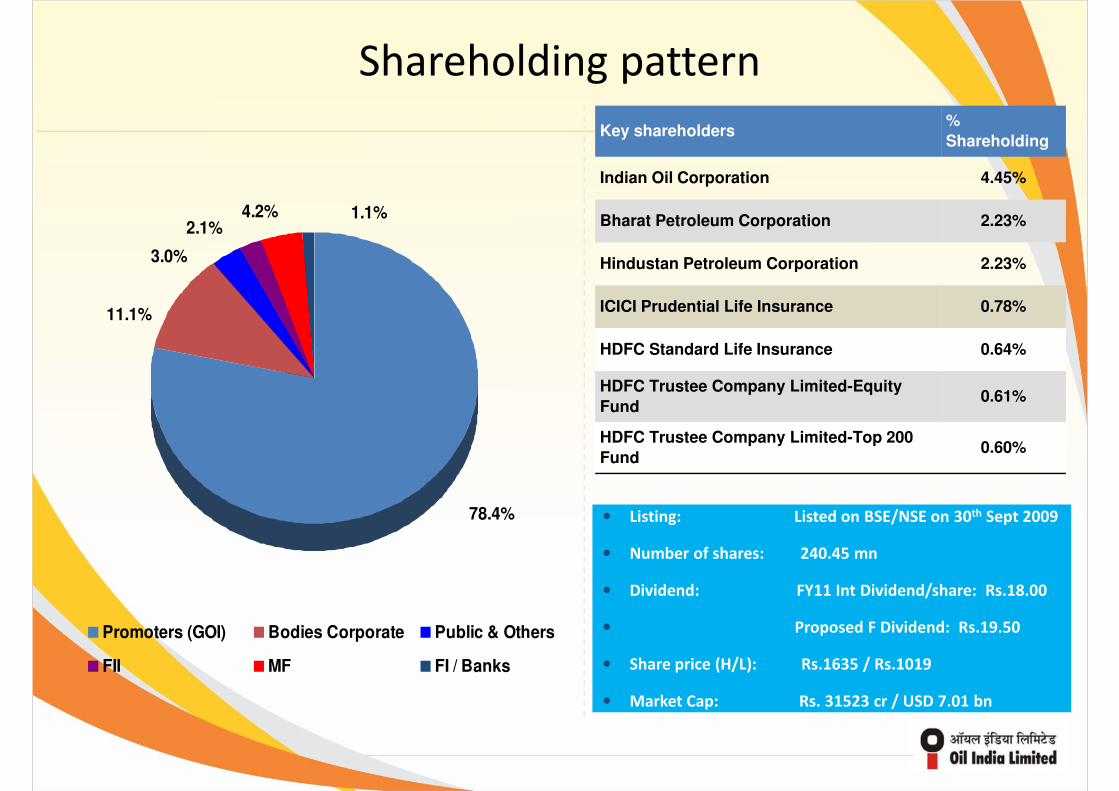

Shareholding pattern

4.2%2.1%

3.0%

1.1%

Key shareholders%

Shareholding

Indian Oil Corporation 4.45%

Bharat Petroleum Corporation 2.23%

Hindustan Petroleum Corporation 2.23%

78.4%

3.0%

11.1%

Hindustan Petroleum Corporation 2.23%

ICICI Prudential Life Insurance 0.78%

HDFC Standard Life Insurance 0.64%

HDFC Trustee Company Limited-Equity

Fund0.61%

HDFC Trustee Company Limited-Top 200

Fund0.60%

• Listing: Listed on BSE/NSE on 30th Sept 2009

Promoters (GOI) Bodies Corporate Public & Others

FII MF FI / Banks

• Number of shares: 240.45 mn

• Dividend: FY11 Int Dividend/share: Rs.18.00

• Proposed F Dividend: Rs.19.50

• Share price (H/L): Rs.1635 / Rs.1019

• Market Cap: Rs. 31523 cr / USD 7.01 bn

Performance of OIL India

1.4

1.5

1.6

0.9

1.0

1.1

1.2

1.3

0.8

0.9

S-0

9

N-0

9

J-1

0

M-1

0

M-1

0

J-1

0

S-1

0

N-1

0

J-1

1

M-1

1

M-1

1

J-1

1

OINL ONGC NIFTY SENSEX OIL & Gas Index

Our Vision

• Fastest growing Energy Company with highest profitability.

• Delight customers with quality products and services at competitive prices

"The fastest growing energy company with a global presence providing value to the

shareholder"

• Delight customers with quality products and services at competitive prices

• Learning Organization, nurturing initiatives, innovations and aspirations with best

practices

• Team, committed to honesty, integrity, transparency and mutual trust creating

employee pride

• Fully committed to safety, health and environment• Fully committed to safety, health and environment

• Responsible corporate citizen deeply committed to socio-economic development in

its areas of operations

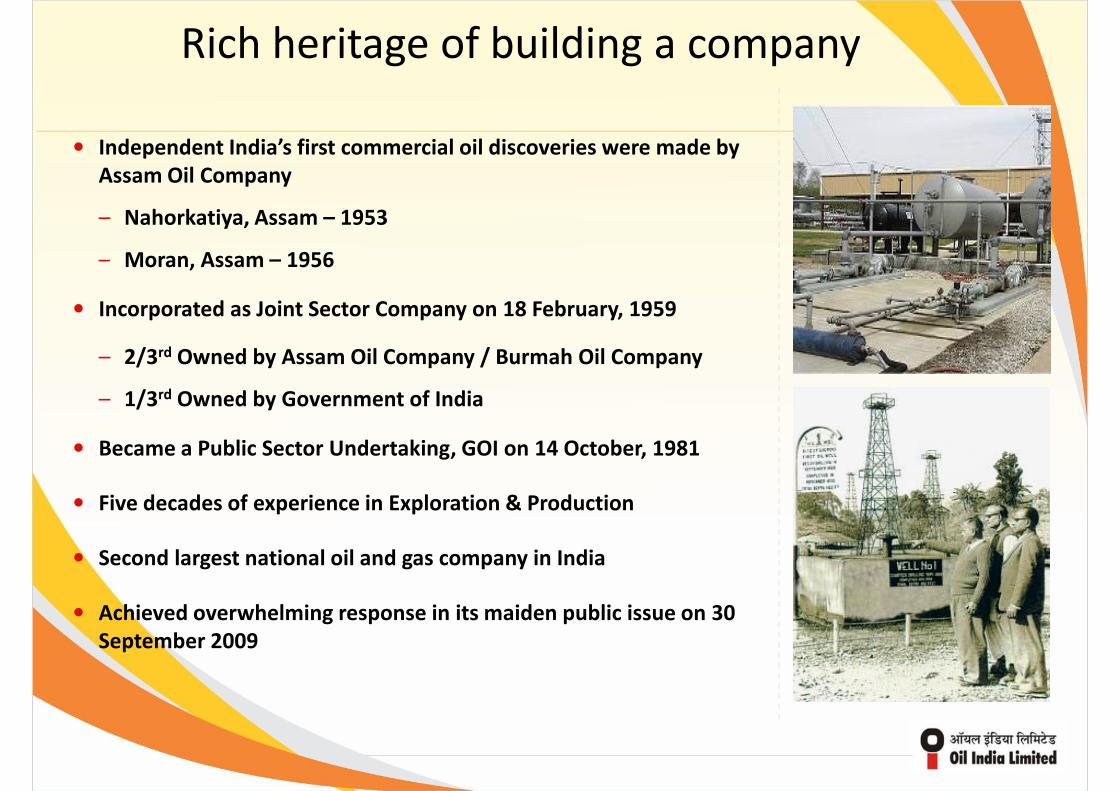

Rich heritage of building a company

• Independent India’s first commercial oil discoveries were made by

Assam Oil Company

– Nahorkatiya, Assam – 1953

– Moran, Assam – 1956 – Moran, Assam – 1956

• Incorporated as Joint Sector Company on 18 February, 1959

– 2/3rd Owned by Assam Oil Company / Burmah Oil Company

– 1/3rd Owned by Government of India

• Became a Public Sector Undertaking, GOI on 14 October, 1981

• Five decades of experience in Exploration & Production

• Second largest national oil and gas company in India

• Achieved overwhelming response in its maiden public issue on 30

September 2009

Integrated Oil & Gas Player

� Domestic: 30 E&P

blocks1

� Refining and marketing

petroleum products:

– 26% equity stake in

� 50 years of experience

� FY’ 11 Produced 25.71

mmbbl of Crude oil:

Exploration DownstreamProduction Transportation

� Crude Oil:

– 1,157 km pipeline ;

~6 MMT capacity� International: Egypt,

Gabon, Iran, Libya,

Nigeria, Timor Leste,

Venezuela and Yemen2

� Discoveries: 16 Small to

Medium3 size discoveries

during last three years

(FY’09 – FY’11)

– 26% equity stake in

NRL1

� Gas cracker project:

– 10% equity stake in

BCPL2

� City gas business –

– Signed MOU with

GAIL, HPCL, IOCL

and BPCL/ONGCL

mmbbl of Crude oil:

– 39 installations

– 1,544 km pipelines

� FY’ 11 Produced 2.35

bcm of Natural gas

– 26 installations

– 583 km pipelines

� Advanced Recovery

techniques to maximize

production

~6 MMT capacity

� Multi-Product:

– 660 km pipeline; 1.72

MMT capacity

� Overseas pipeline:

– 10% stake in 741 km

pipeline (Sudan)

� Natural Gas:

– 23% stake in 192 km

DNPL3 in NE

Note:

1. NRL – Numaligarh Refinery Limited

2. BCPL – Brahmaputra Cracker and Polymer Limited

3. DNPL – Duliajan-Numaligarh Pipeline Limited

Note:

1. 10 blocks have been awarded under NELP IX.

2. Participating interests in exploration and development blocks.

3. Small to Medium size discoveries: Estimated proved plus probable reserves size of less than 30 mn barrels of oil and oil equivalent gas

4. MMBOE – Million Barrels of Oil Equivalent

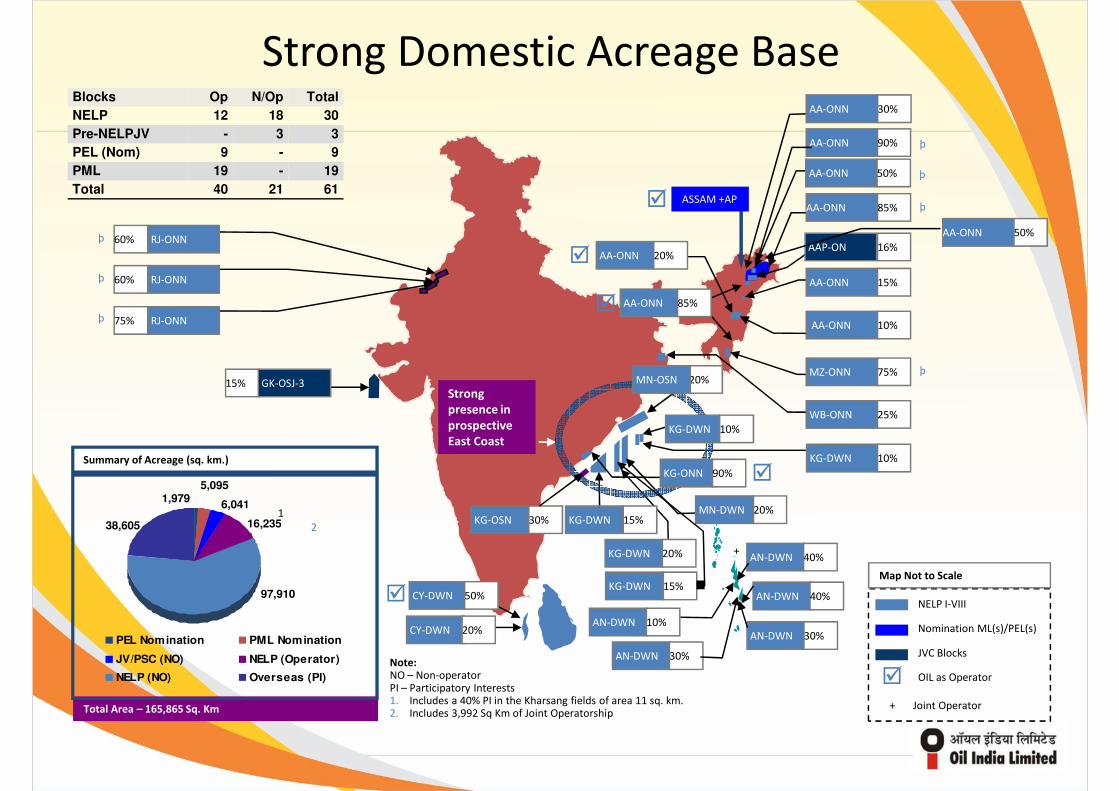

Strong Domestic Acreage BaseBlocks Op N/Op Total

NELP 12 18 30

Pre-NELPJV - 3 3

PEL (Nom) 9 - 9

PML 19 - 19

Total 40 21 61

RJ-ONN

AA-ONN

AA-ONN

AA-ONN

AAP-ONþ

þ

þ

AA-ONN

30%

90%

85%

16%60%

20%

ASSAM +AP

AA-ONN þ50%

AA-ONN 50%

�

�

KG-OSNMN-DWN

AA-ONN

AA-ONN

MZ-ONN

KG-DWN

þ

þ

þ

AA-ONN

WB-ONN

RJ-ONN

RJ-ONN

15%

10%

75%

25%

10%

75%

60%

30%20%

KG-DWN 10%

20%

85%

15%

KG-ONN 90%

GK-OSJ-3 MN-OSN

Summary of Acreage (sq. km.)

1

5,095

38,605

1,9796,041

16,235 KG-DWN 15%2

Strong

presence in

prospective

East Coast

�

�

�

Note:NO – Non-operatorPI – Participatory Interests1. Includes a 40% PI in the Kharsang fields of area 11 sq. km.2. Includes 3,992 Sq Km of Joint Operatorship

KG-DWN

AN-DWNCY-DWN

10%

20%

20%

Total Area – 165,865 Sq. Km

OIL as Operator

NELP I-VIII

Nomination ML(s)/PEL(s)

JVC Blocks

Map Not to Scale

38,605

97,910

16,235

PEL Nomination PML Nomination

JV/PSC (NO) NELP (Operator)

NELP (NO) Overseas (PI)

CY-DWN 50%KG-DWN 15%

AN-DWN 30%

AN-DWN 40%

AN-DWN 40%

AN-DWN 30%

+

+ Joint Operator

2

�

�

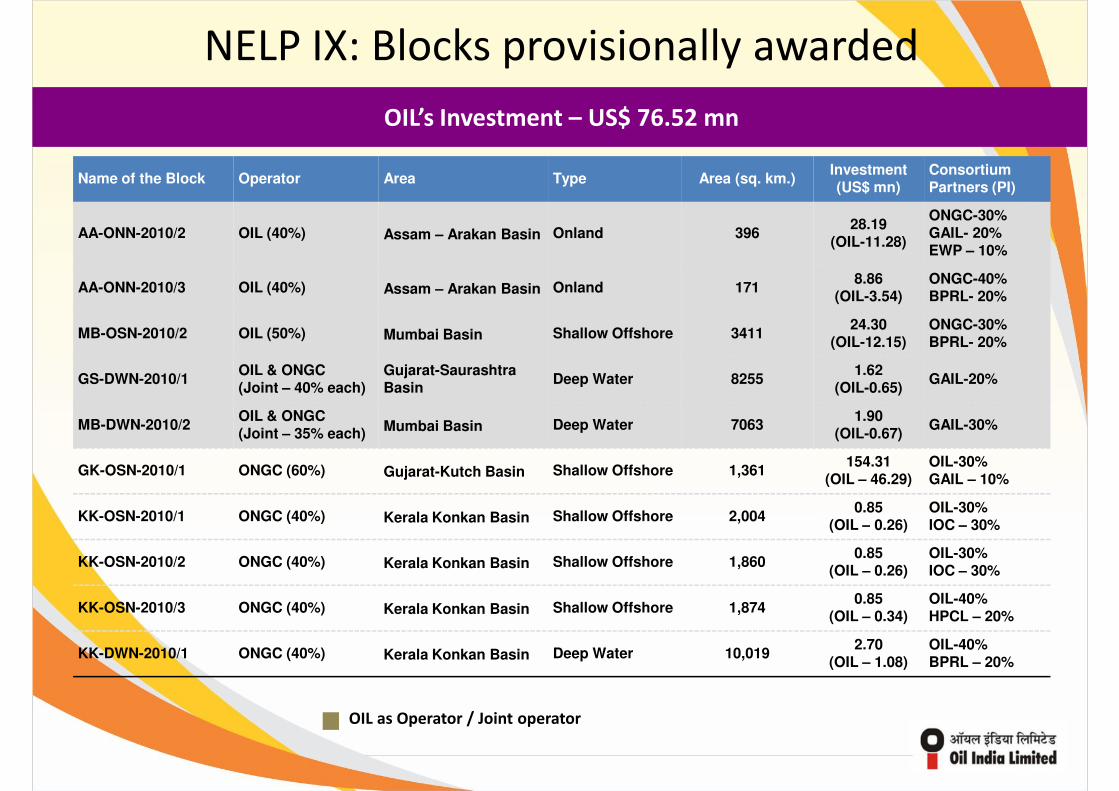

NELP IX: Blocks provisionally awarded

Name of the Block Operator Area Type Area (sq. km.)Investment (US$ mn)

Consortium Partners (PI)

AA-ONN-2010/2 OIL (40%) Assam – Arakan Basin Onland 39628.19

(OIL-11.28)

ONGC-30%GAIL- 20%EWP – 10%

OIL’s Investment – US$ 76.52 mn

AA-ONN-2010/3 OIL (40%) Assam – Arakan Basin Onland 1718.86

(OIL-3.54)ONGC-40%BPRL- 20%

MB-OSN-2010/2 OIL (50%) Mumbai Basin Shallow Offshore 341124.30

(OIL-12.15)ONGC-30%BPRL- 20%

GS-DWN-2010/1OIL & ONGC(Joint – 40% each)

Gujarat-Saurashtra Basin

Deep Water 82551.62

(OIL-0.65)GAIL-20%

MB-DWN-2010/2OIL & ONGC(Joint – 35% each)

Mumbai Basin Deep Water 70631.90

(OIL-0.67)GAIL-30%

GK-OSN-2010/1 ONGC (60%) Gujarat-Kutch Basin Shallow Offshore 1,361154.31

(OIL – 46.29)OIL-30%GAIL – 10%

KK-OSN-2010/1 ONGC (40%) Kerala Konkan Basin Shallow Offshore 2,0040.85

(OIL – 0.26)OIL-30%IOC – 30%(OIL – 0.26) IOC – 30%

KK-OSN-2010/2 ONGC (40%) Kerala Konkan Basin Shallow Offshore 1,8600.85

(OIL – 0.26)OIL-30%IOC – 30%

KK-OSN-2010/3 ONGC (40%) Kerala Konkan Basin Shallow Offshore 1,8740.85

(OIL – 0.34)OIL-40%HPCL – 20%

KK-DWN-2010/1 ONGC (40%) Kerala Konkan Basin Deep Water 10,0192.70

(OIL – 1.08)OIL-40%BPRL – 20%

OIL as Operator / Joint operator

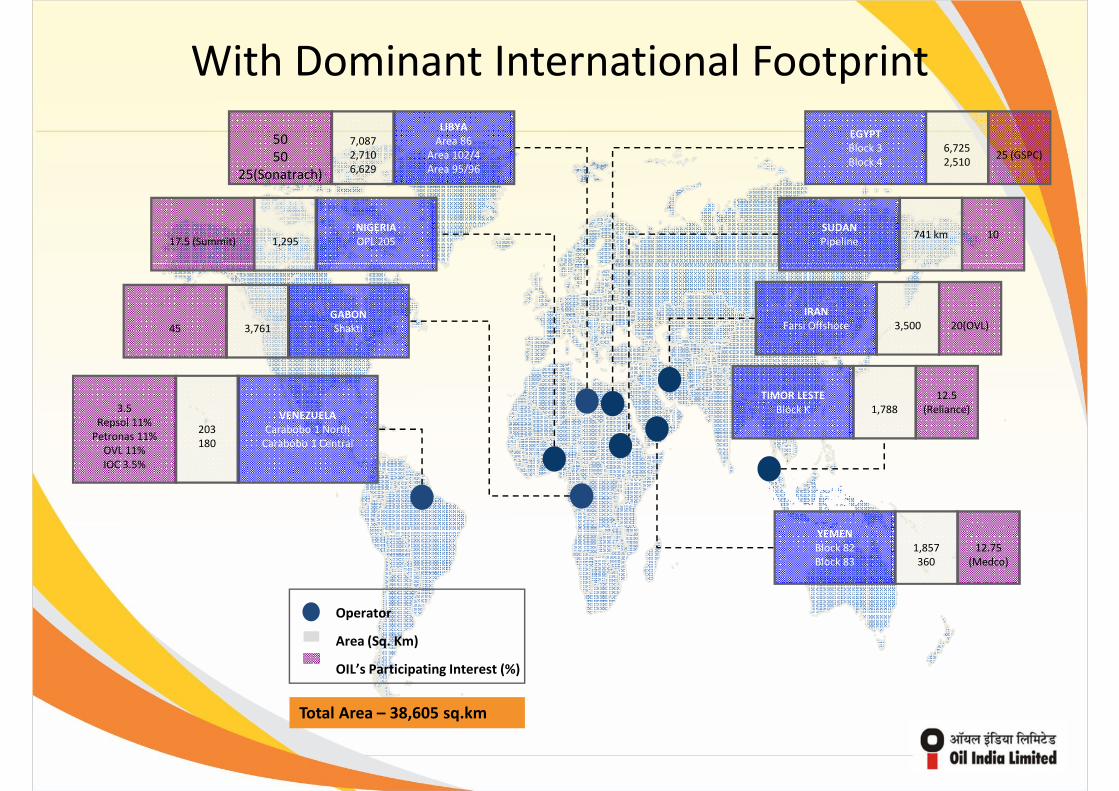

With Dominant International Footprint

6,725

2,51025 (GSPC)

EGYPT

Block 3

Block 4

7,087

2,710

6,629

50

50

25(Sonatrach)

LIBYA

Area 86

Area 102/4

Area 95/96

1,29517.5 (Summit)

NIGERIA

OPL 205741 km 10

SUDAN

Pipeline

3,500 20(OVL)

IRAN

Farsi Offshore3,76145

GABON

Shakti

203

180

3.5

Repsol 11%

Petronas 11%

OVL 11%

IOC 3.5%

VENEZUELA

Carabobo 1 North

Carabobo 1 Central

1,788

12.5

(Reliance)

TIMOR LESTE

Block K

YEMEN

Operator

Area (Sq. Km)

OIL’s Participating Interest (%)

Total Area – 38,605 sq.km

1,857

360

12.75

(Medco)

YEMEN

Block 82

Block 83

5051200

1400

1600

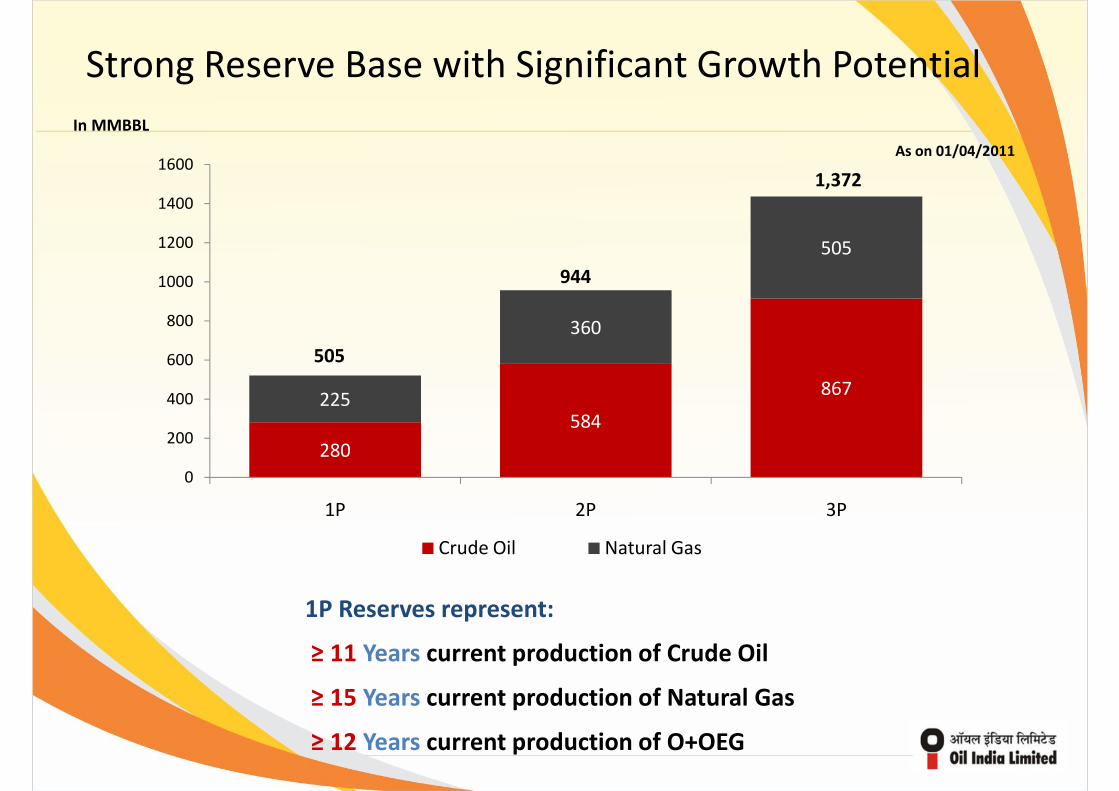

Strong Reserve Base with Significant Growth Potential

In MMBBL

As on 01/04/2011

944

1,372

280

584

867225

360

0

200

400

600

800

1000

1P 2P 3P

505

944

Crude Oil Natural Gas

1P Reserves represent:

≥ 11 Years current production of Crude Oil

≥ 15 Years current production of Natural Gas

≥ 12 Years current production of O+OEG

Healthy and Consistent Reserve Replacement Ratio

2.04 2.04 1.69 1.65

Reserve Replacement Ratio (x)

1.42

Crude Oil and Natural Gas (O+OEG) Production and Reserve Accretion (in MMTOE)

5.1 5.15.6 5.9 5.9

10.4 10.39.4 9.7

8.4

Crude Oil and Natural Gas (O+OEG) Production and Reserve Accretion (in MMTOE)

FY2007 FY2008 FY2009 FY2010 FY2011

Production (O + OEG) Accretion

Adequate reserve replenishment

Integrated In-house E&P Infrastructure To Support Growth

In house Expertise and Integration across Energy Infrastructure

Infrastructure to Support E&P Activities Production & Storage Facilities

Two 2D and One

3D Seismic Crew

Six Logging

Trucks

72 Production

Installations

14 W/over Rigs 11 Drilling Rigs

5,000 Km

O&G

Pipelines

~150k KL

Crude Storage

Strategy to Deliver Long Term Growth and Shareholder Value

Use Advanced Techniques to Improve

Existing Productivity

� Continue to induct world class

technology

1

Further Integrate Business

Portfolio and Diversify

across Geographies

Increase Reserves and

Production in Existing Acreage

� Accelerate exploration efforts

� Develop fields with potential

2

3Vertical Integration4

Explore Non-conventional

energy sources

� Explore alternate energy

opportunities in existing

acreage as well as inorganic

opportunities

5

Inorganic Growth

� Acquire blocks to augment

existing reserve base

� Acquisition of companies that

are value accretive

3Vertical Integration

� Diversify revenues through

downstream investments

� Improve profitability by

extending into higher margin

product value chain

� Providing Oilfield Services

4

Significant Investment Lined Up

M&AOverseas

Significant focus on Exploration and Development of existing acreage potential

2011-2012: 31,803 mn

M&A

1%

Domestic

Assets

9%

Overseas

Projects

11%

Development

27%Exploration &

Appraisal

52%

Planned Activities in FY12

3D Seismic Surveys Exploratory Drilling Development Drilling

Substantial Increase in 3D Surveys, Exploratory and Development Drilling Planned.

16

34

FY11 FY12

25

34

FY11 FY12

672

1,767

FY11 FY12 FY11 FY12 FY11 FY12FY11 FY12

Recent Developments

� Achieved the highest daily rate of crude oil production of 3.93 MTPA (> 27.96 mmbbls/Year)

� Achieved the highest daily rate of natural gas production of 6.67 MMSCMD in North East and

potential of 0.93 MMSCMD in Rajasthan

� Performance up to 31 March 2011:

Select Highlights

* A total loss of 0.127 MMT due to NRL shut-down. However, Highest ever quarterly production of 0.951 MMT achieved in Q2, 2010 .

** Low upliftment by customers of NE & Rajasthan,

� Hydrocarbon discoveries in Assam - 06 Nos. in FY’11

Parameter Unit 2009-10 2010-11

Crude Oil Production MMT 3.572 3.612*

Natural Gas Production BCM 2415 2349**

� Entry in Offshore as Operator and Deep Water Block as Joint Operator

� Entry in CBM Block (Assam)

� Examining Shale Gas potential of Assam-Arakan Basin

� OIL & GAIL( India) Ltd are jointly evaluating US shale gas assets buys

Select Highlights (Contd.)

• Successful commissioning of Duliajan-Numaligarh Pipeline (DNP) w.e.f 28-02-2011

• Completed Preliminary Activities in order to Develop CNG Network in Assam.

• MOUs with BPCL, IOCL & ONGCL executed for CGD. Submitted bids for two cities.

• Received Greentech HR Excellence Gold Award 2010.

• Received Golden Peacock Award & Greentech Gold Award for Environment Management.

• Received Environmental Excellence Award from Indian Chamber of Commerce

• "OIL's Assam Asset won OISD Award in the Oil & Gas Assets (onshore) for the year 2009-10

• Employees Relations Department Accredited with ISO Certification

• Identified Business opportunity in Bangladesh (Pipeline)• Identified Business opportunity in Bangladesh (Pipeline)

• HDD, Telecommunication work & AMC for IOCL’s Guwahati-Siliguri Pipeline

• Cathodic Protection work for DNPL Pipeline

• ODC Project for PDO, Oman

• Marketing of Telecommunication Services

Operating Performance

Crude Oil and Natural Gas Production

22.38

24.9525.7

25.712,341

2,2692,415

2,3490.93

Crude Oil Production (mm bbl) Natural Gas Production (mm scm)

22.38

5.686.81

553641

2007-08 2008-09 2009-10 2010-11 Q1 FY'11 Q1 FY'12 2007-08 2008-09 2009-10 2010-11 Q1 FY'11 Q1 FY'12

~20% increase over last year (QTQ) ~16% increase over last year (QTQ)

Production Cost

1.8 1.41.6

2.0

7.16.8

7.27.6

0.10.2

0.2 0.21.1

1.1

1.21.3

Crude Oil Production Cost (USD/ Barrel) Natural Gas Production Cost (USD/ MMBTU)

3.3

4.9 5.1 5.2 5.3

0.3

0.4 0.4 0.4 0.3

1.2

1.8 1.4

4.8

0.5

0.80.9 0.9 1.0

0.1

0.1

0.10.1 0.1

0.2

0.2

0.2

0.8

2006-07 2007-08 2008-09 2009-10 2010-11

Raising Cost Depreciation Depletion

2006-07 2007-08 2008-09 2009-10 2010-11

Raising Cost Depreciation Depletion

Low Finding & Development Costs

5.56.00

Finding and Development Costs (USD / bbl)

OIL has the Advantage of Low Finding & Development costs.

1.8 1.8

3.02.8

3.8

2.5

3.0

4.1 4.2

5.5

2.00

3.00

4.00

5.00

0.00

1.00

FY2007 FY2008 FY2009 FY2010 FY2011

Finding Costs F&D Costs

Financial Performance

Sharing of Subsidy by Upstream Companies

2007-08 2008-09 2009-10 2010-11 Q1 FY’11 Q1 FY’12

ONGC 22,001 28,226 11,554 24893 5516 12046

OIL 2,307 3,023 1,549 3293 730 1781

GAIL 1,401 1,694 1,326 2111 445 682

Rs. in Crores

Total 25,709 32,943 14,430 30,297 6,691 14,509

% SHARING

2007-08 2008-09 2009-10 2010-11 Q1 FY’11 Q1 FY’12

ONGC 86% 86% 80% 82% 82% 83%

OIL 9% 9% 11% 11% 11% 12%

GAIL 5% 5% 9% 7% 7% 5%

Total 100% 100% 100% 100% 100% 100%

Realized Price

116.3

(USD/barrel)

83.2 81.7

68.5

86.1

78.1

58.1 55.6 56.2 58.5

49.7

59.6

36.239.0 39.8 41.4

33.8

42.1

FY2008 FY2009 FY2010 FY2011 Q1 FY'11 Q1 FY'12

Gross Realized Price Realized Price after Subsidy/Discount Net Realized Price

8,178

8,860

9,549

8,000

9,000

10,000

Revenue and profitability

Revenue and profitability analysis (Rs Crore)

6,010

6,796

1,817

2,669

1640 17892162

26102888

2,000

3,000

4,000

5,000

6,000

7,000

8,000

501850

0

1,000

2,000

FY2007 FY2008 FY2009 FY2010 FY2011 Q1 FY'11 Q1 FY'12

Income PAT

Note: Exchange rate 1 USD = 48.52 INR used for figures upto FY2009; FY10 and FY11, actual exchange rates have been used.

800

900

1000

16,000

18,000

Networth and Book Value

Networth (Rs crores) and Book Value Analysis (Rs)

7,9339,331

13,745 15,602

14,251

16,451 371

436

572

649

593

684

200

300

400

500

600

700

800

4,000

6,000

8,000

10,000

12,000

14,000

0

100

0

2,000

FY2008 FY2009 FY2010 FY2011 Q1 FY'11 Q1 FY'12

Networth (LHS) Book Value (RHS)

Cash Flow and EBITDA Margin

4,380

4,805

49%

50%

52%

50%

60%

4000

4500

5000

2,548

100%

120%

2,500

3,000

Cash Flow (Rs Crores) EBITDA (Rs Crores) and EBITDA MARGIN (%)

2,841

3,568

841

1,387

43%

42%

49%

46%

10%

20%

30%

40%

1000

1500

2000

2500

3000

3500

4000

1,385

1,798

2,135

608

972

20%

40%

60%

80%

500

1,000

1,500

2,000

0%

10%

0

500

FY2008 FY2009 FY2010 FY2011 Q1 FY'11 Q1 FY'12

0%0

FY2008 FY2009 FY2010 FY2011 Q1 FY'11

Q1 FY'12

Consistent and Attractive Cash Flow

EBITDA EBITDA Margin

340

375

305

34

35

300

320

340

360

380

400

0.12x120

140

0.12

0.14

Dividends distribution and Earnings per share highlights

Dividends distribution Earnings per share and Debt-Equity ratio

33.633.9

32.9

30.2

31.3 31.2

275265 260

29

30

31

32

33

40

60

80

100

120

140

160

180

200

220

240

260

280

300

86

7283

104114

1200.07x

0.02x

0.06x

20

40

60

80

100

0.02

0.04

0.06

0.08

0.1

28

FY2006 FY2007 FY2008 FY2009 FY2010 FY2011

0

20

40

Dividend Payout (%) - LHS Dividends (%) - RHS

0.003x0.006x

0

FY2006 FY2007 FY2008 FY2009 FY2010 FY2011

0

Earnings per share (INR) Debt/Equity

The dividend per share has shown a

consistent uptrend

Steady increase in EPS and minimal debt

on the balance sheet

Guidance: FY’12

2009-10 2010-11 2011-12 (Target)

Crude oil production 3.57 mmt 3.61 MMT 3.76 MMT

Natural gas production 2,415 mmscm 2,349 mmscm 2,633 mmscm

� Increase in Exploratory and Development Drilling Meterage

� Increase in Work Overs

� Enhanced Water Injection

� Endeavour to Enhance LPG production through NGL Recycling

� Endeavour to Reduce Gas Flaring by Inducting LNG Technology

� Stable Operations, Looking for Growth

� Company with Good Operating Track Record

� Sound Financial Health

Conclusion

� Sound Financial Health

� Company with more than 5 Decades of E&P Expertise

� Large Prospective E&P Acreage

� Entry into Deepwater/Offshore Blocks as Operator

� Entry into discovered assets in Venezuela, Acquisition Thrust continues

� Spreading its Wings : NE ���� Pan India ���� Global

� Diversifying into New Areas

Thank You