An Introduction to the Principles of Performance Management · Principles of Performance Management...

65

An Introduction to the Principles of Performance Management Presented to the International Association of Commercial Administrators Copyright © 2000-2014 by Thomas A. Bishop All Rights Reserved.

Transcript of An Introduction to the Principles of Performance Management · Principles of Performance Management...

An Introduction to the Principles of Performance Management

Presented to the International Association of Commercial Administrators

Copyright © 2000-2014 by Thomas A. Bishop

All Rights Reserved.

2

The Theory of

Performance Management

by

Dr. Walter A. Shewhart

and

Dr. W. Edwards Deming

The Shewhart and Deming Performance Management Theory

3

The Shewhart and Deming Performance Management Theory

In 1931, Dr. Walter A. Shewhart introduced a powerful, new theory of management aimed at optimizing the control of manufacturing processes. This event occurred with the publication of his seminal book

“Economic Control of Quality of Manufactured Product”

Over the next 60 years Dr. W. Edwards Deming extended the development and application of Shewhart’s optimization theory to service and administrative processes.

4

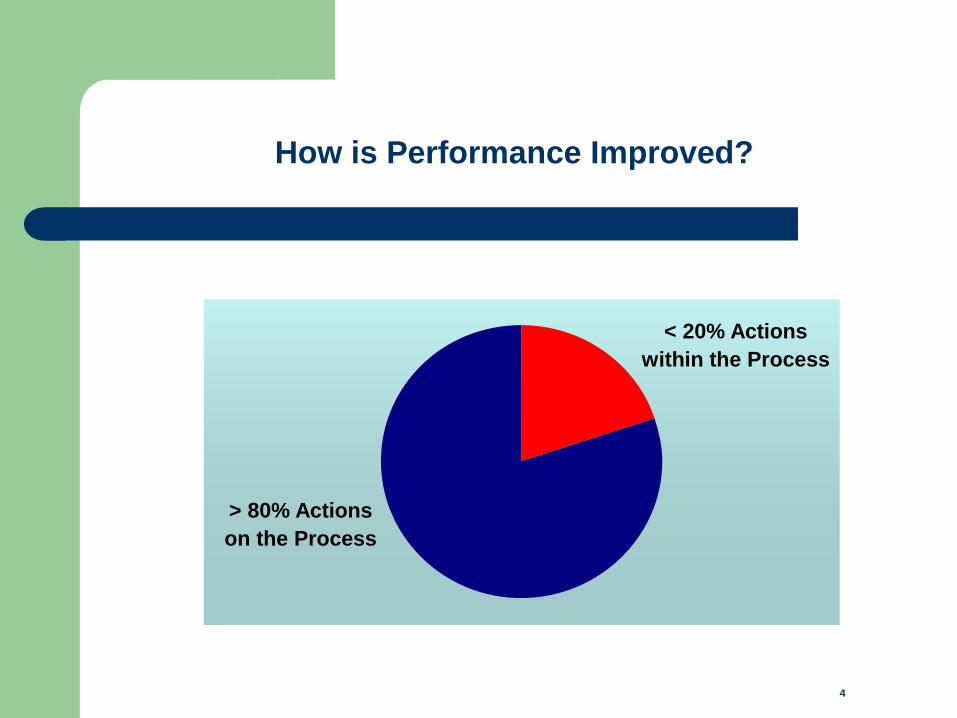

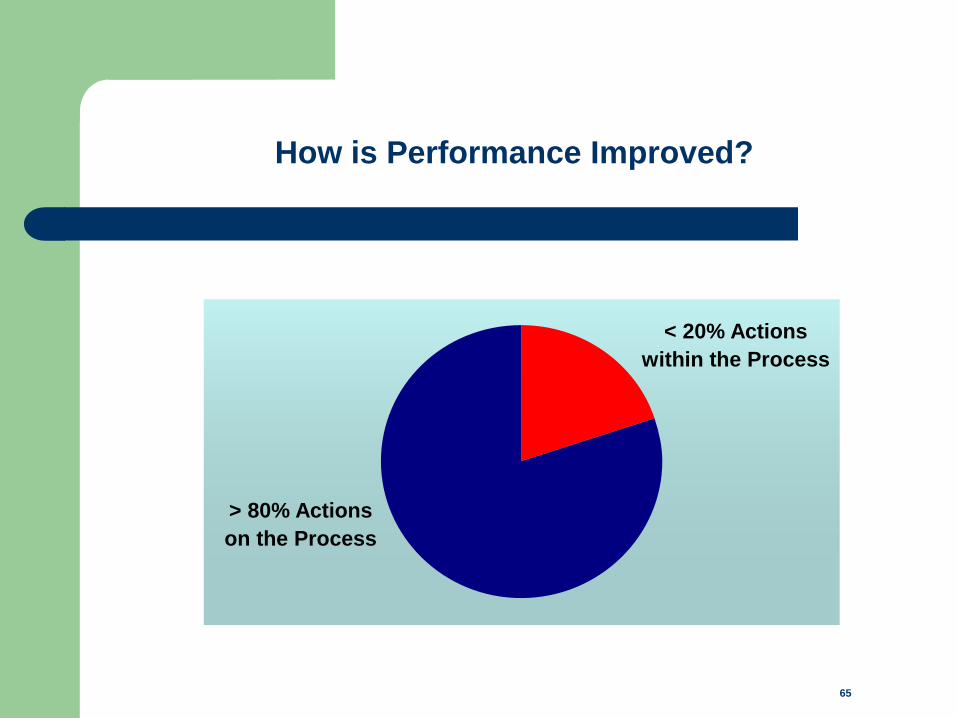

How is Performance Improved?

> 80% Actions

on the Process

< 20% Actions

within the Process

5

The Three Fundamental Axioms of Management

The Axiom of Responsibility

“The primary responsibility of management in any organization is to

create means of producing products and services that meet the wants

and needs of their customers with the minimum amount of human

effort and investment in capital resources.”

In order to meet this responsibility, management must tap and

optimize the inherent capability of the human and capital resources

that have been entrusted to their leadership.

6

The Axiom of Action

“In managing systems and people, data are collected and analyzed

to generate knowledge and insights to form a rational basis for action.”

The Three Fundamental Axioms of Management

7

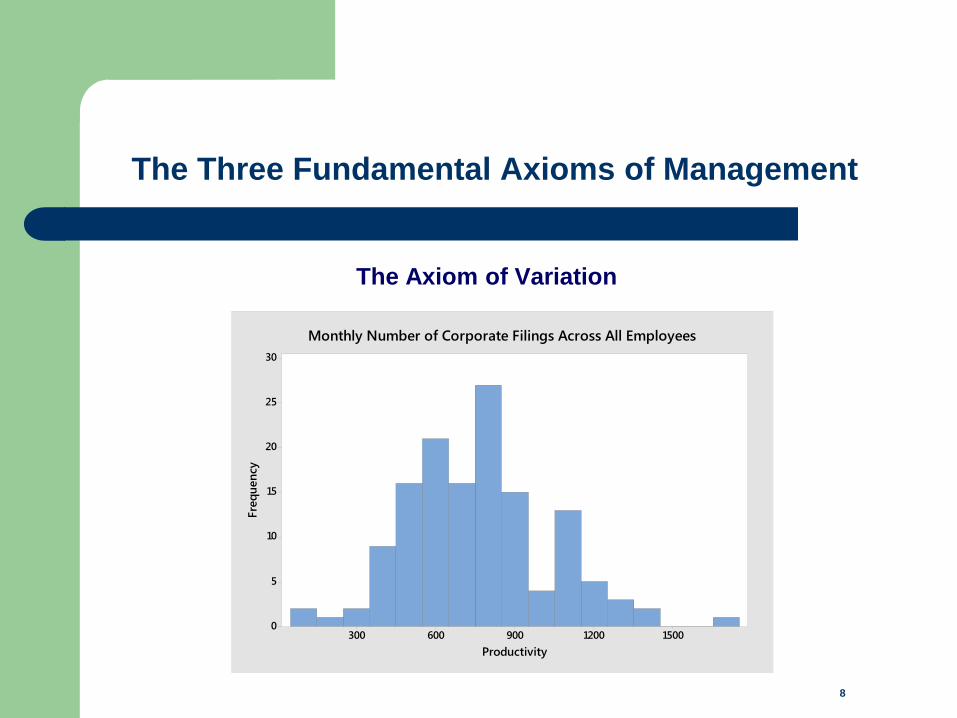

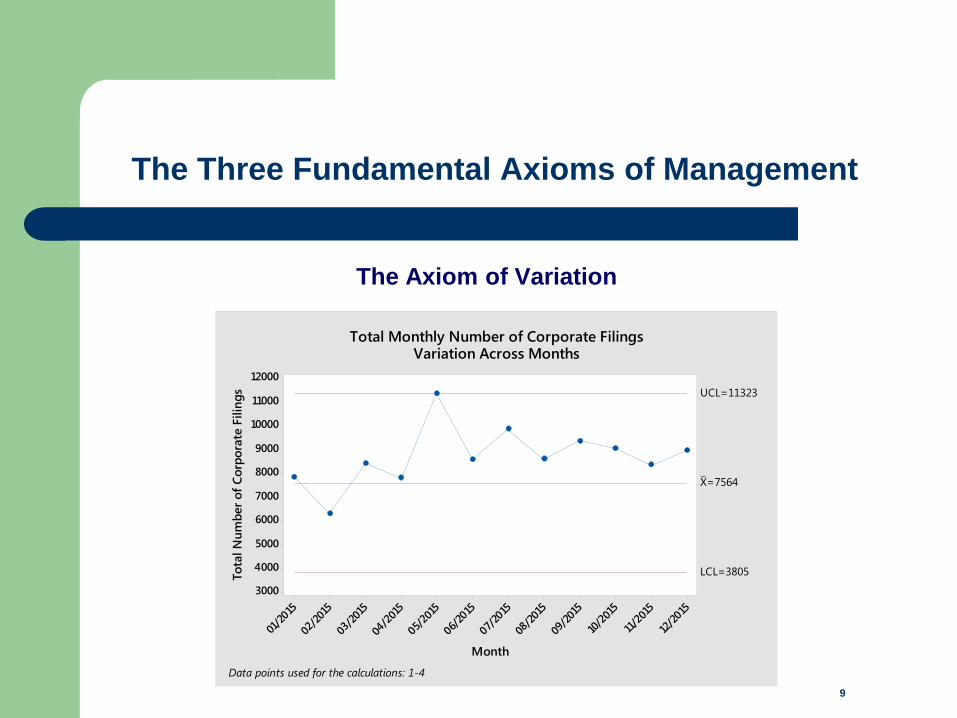

The Axiom of Variation

“Whenever an individual or organization attempts to produce products or

services, their performance will vary over time.”

Therefore, there is inherently a cause system of variation

associated with, and a statistical component to, the

management of both human and fixed assets.

The Three Fundamental Axioms of Management

8

The Axiom of Variation

The Three Fundamental Axioms of Management

15001200900600300

30

25

20

15

10

5

0

Productivity

Fre

qu

en

cy

Monthly Number of Corporate Filings Across All Employees

9

The Axiom of Variation

The Three Fundamental Axioms of Management

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/20

15

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

12000

11000

10000

9000

8000

7000

6000

5000

4000

3000

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=7564

UCL=11323

LCL=3805

Total Monthly Number of Corporate FilingsVariation Across Months

Data points used for the calculations: 1-4

The Bead Box Experiment

Understanding Unexplainable

Random Variation

The Bead Box Experiment

The most famous experiment that demonstrates the effects

of pure common causes of variation, and that also helps us

understand the behavior of constant cause systems of variation,

is Dr. Deming’s bead box experiment.

11

The Components of the Bead Box Experiment

The experiment consists of a box containing beads and a paddle used to draw beads from the box.

There are 1000 beads in the box.

Ten percent of the beads are red

and the remainder are white.

The paddle contains 50 holes.

12

The Experimental Procedure

The beads are thoroughly mixed by hand prior to inserting the paddle.

The paddle is inserted into the box and 50 beads are drawn from the box.

The percent of red beads in the paddle is recorded.

The beads are then returned to the box, the beads are thoroughly mixed again and the experiment is repeated.

This procedure is repeated a large number of times.

13

The Basis for Predictability in the Bead Box Experiment

Why is there such predictability hidden within the

random behavior of the data?

It is due solely to the design of the cause system of variation produced by

the experiment – that is the mechanical process of mixing the beads

thoroughly by hand prior to inserting the paddle.

1009080706050403020101

35

30

25

20

15

10

5

0

Draw

Perc

ent R

ed B

eads

Variation Associated with the Bead BoxData from the First 100 Trials

23%

10%

14

The Student Loan Process Case Study

Evaluating Employee Performance

within the Student Loan Application

Data Entry Process

• In the early 1990’s the Ohio Student Loan Commission (OSLC) was

responsible for the intake and processing of student loan applications for the

state supported colleges.

• Students submitted their loan applications by mail to the OSLC where a staff of

eight data entry clerks, referred to as “keyers” entered the data on the hand

written application forms into the OSLC student loan application database.

• The president of OSLC funded a seminar presenting the Shewhart and

Deming management theory aimed at optimizing organizational and employee

performance.

Project Background

16

16

• During the seminar the supervisor over the data entry process raised

objections to the validity of the concepts being presented relative to the

management and improvement of human performance within administrative

processes.

• This particular supervisor managed the eight keyers who were responsible

for keying the data contained on the student application forms into the OSLC

application database.

• The eight keyers were State of Ohio unionized employees.

Project Background

17

17

• The supervisor was unhappy with what she perceived to be inconsistent and unacceptably high error rates associated with the data entered into the application database by the keyers.

• The supervisor believed that data entry errors were under the control of the keyers and that the data entry errors were due to poor work habits of the keyers.

• She argued that she was helpless to reduce the keying errors because the keyers could not be disciplined or fired because they were members of the union.

• The president of OSLC decided to use the data entry process to test the efficacy of the application of the Deming management theory to the management of the OSLC business departments.

Project Background

18

18

• The goal of this project is to

improve the overall accuracy of

the data entered into the student

loan application database.

• The specific project objectives

include:

the creation of a process analysis

and monitoring system aimed at:

the assessment of the stability of

the process error rates over time

the identification of the causes of

data entry errors

the determination of the appropriate

local and global actions to take to

remove causes of data entry errors

from the process.

Project Goals and Objectives

19

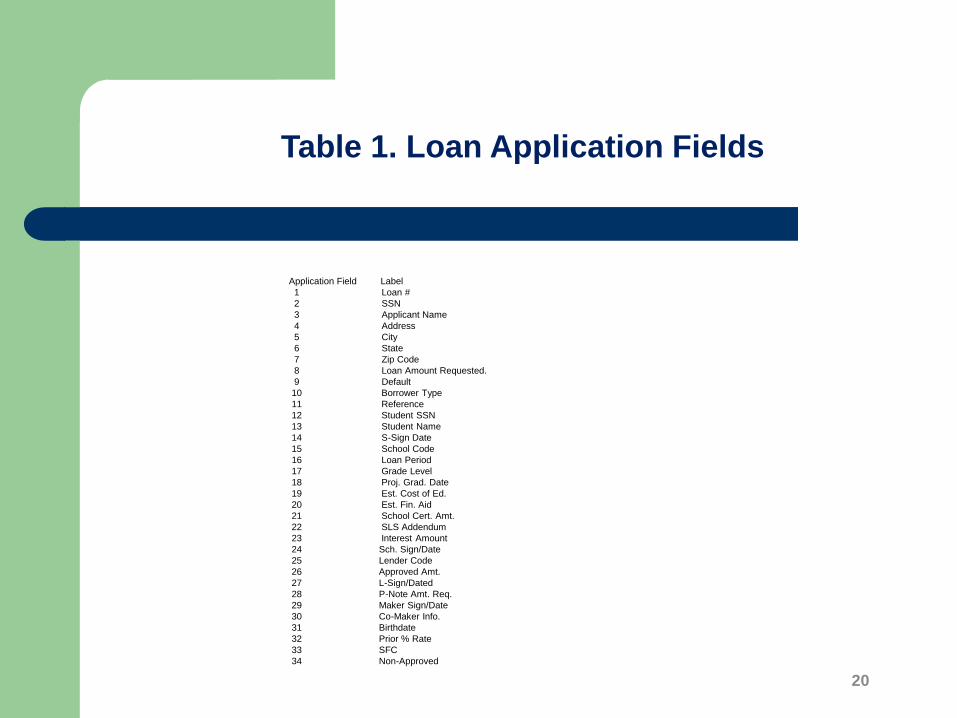

Table 1. Loan Application Fields

20

Application Field Label

1 Loan #

2 SSN

3 Applicant Name

4 Address

5 City

6 State

7 Zip Code

8 Loan Amount Requested.

9 Default

10 Borrower Type

11 Reference

12 Student SSN

13 Student Name

14 S-Sign Date

15 School Code

16 Loan Period

17 Grade Level

18 Proj. Grad. Date

19 Est. Cost of Ed.

20 Est. Fin. Aid

21 School Cert. Amt.

22 SLS Addendum

23 Interest Amount

24 Sch. Sign/Date

25 Lender Code

26 Approved Amt.

27 L-Sign/Dated

28 P-Note Amt. Req.

29 Maker Sign/Date

30 Co-Maker Info.

31 Birthdate

32 Prior % Rate

33 SFC

34 Non-Approved

• Q1: Is the process daily error rate stable over time?

• Q2: Are the keyer daily error rates {ERkd} stable over time?

• Q3: Are there detectable differences in the average daily error rate across the eight keyers?

• Q4: Are there any detectable differences in the volume of keyer errors across the 34 loan application fields?

• Q5: What local and/or global actions can be taken to reduce the future number of application field errors and the keyer daily error rates?

Management Questions of Interest

21 Source: Arial 9 pt. Flush left; Source, e.g. publication name. Title of source document. Date. URL if needed.

Cause System Design Diagram

22

MAIL ROOM

SUPERVISOR

KEYER

VERIFIER

YES

1

Mail Room

Delivers

Application to

Data Entry

2

Keyer Keys

in Data

3

Keyer Passes

Application to

the Verifier

4

5

Verifier Rekeys

Application.

Errors Detected?

6 7

Verifier

Corrects

Application

Error Log

Report

Created

8

Supervisor Reviews

Errors with Each

Keyer Weekly

NO

Data Entry

Supervisor Randomly

Distributes

50 Applications

to Each Keyer

Example of local action

on the individual keyer by

the supervisor in an

attempt to reduce the

errors.

Clear evidence of the

implicit assumption by

the supervisor that the

keying errors are under

the control of the

individual keyers.

22

The control of application

errors is based on an

inspection system.

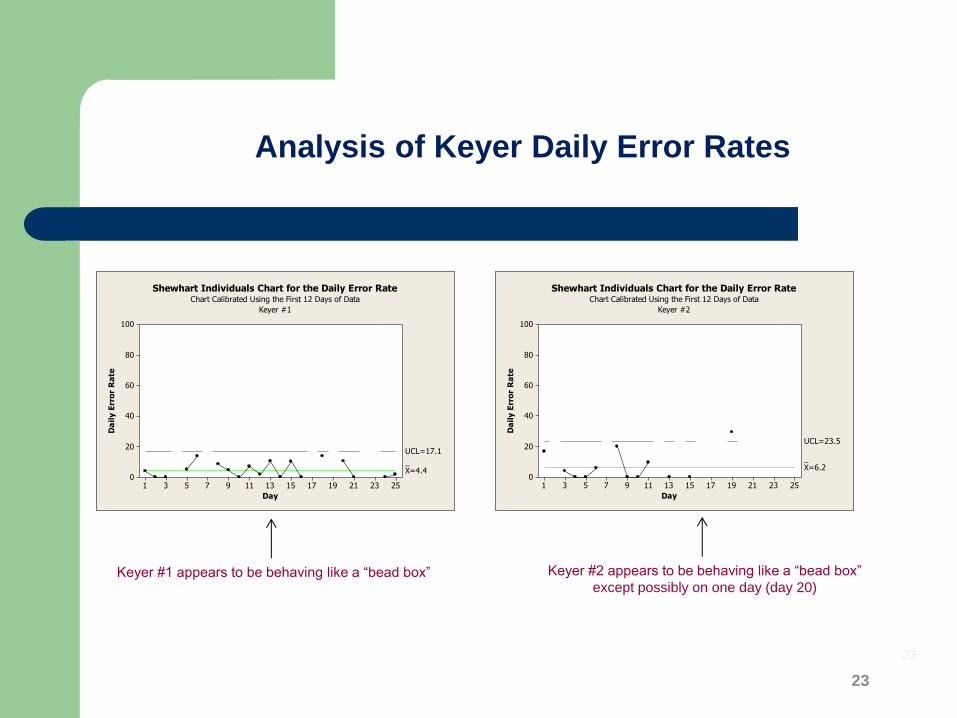

Analysis of Keyer Daily Error Rates

23

Keyer #1 appears to be behaving like a “bead box” Keyer #2 appears to be behaving like a “bead box”

except possibly on one day (day 20)

252321191715131197531

100

80

60

40

20

0

Day

Da

ily E

rro

r R

ate

_X=4.4

UCL=17.1

Shewhart Individuals Chart for the Daily Error RateChart Calibrated Using the First 12 Days of Data

Keyer #1

252321191715131197531

100

80

60

40

20

0

Day

Da

ily E

rro

r R

ate

_X=6.2

UCL=23.5

Shewhart Individuals Chart for the Daily Error RateChart Calibrated Using the First 12 Days of Data

Keyer #2

23

Analysis of Keyer Daily Error Rates

24

Keyer #3 appears to be behaving like a “bead box” Keyer #4 appears to have an upward trend in the

error rate over days 8-13, but then the error rate

drops to 0 on days 14 and 15. And despite this

possible trend, this keyer has the lowest overall

average error rate.

252321191715131197531

100

80

60

40

20

0

Day

Da

ily E

rro

r R

ate

_X=8.0

UCL=24.6

Shewhart Individuals Chart for the Daily Error RateChart Calibrated Using the First 12 Days of Data

Keyer #3

252321191715131197531

100

80

60

40

20

0

Day

Da

ily E

rro

r R

ate

_X=3.1UCL=8.6

Shewhart Individuals Chart for the Daily Error RateChart Calibrated Using the First 12 Days of Data

Keyer #4

24

252321191715131197531

100

80

60

40

20

0

Day

Da

ily E

rro

r R

ate

_X=12.1

UCL=22.8

LCL=1.3

Shewhart Individuals Chart for the Daily Error RateChart Calibrated Using the First 12 Days of Data Excluding Day 7

Keyer #5

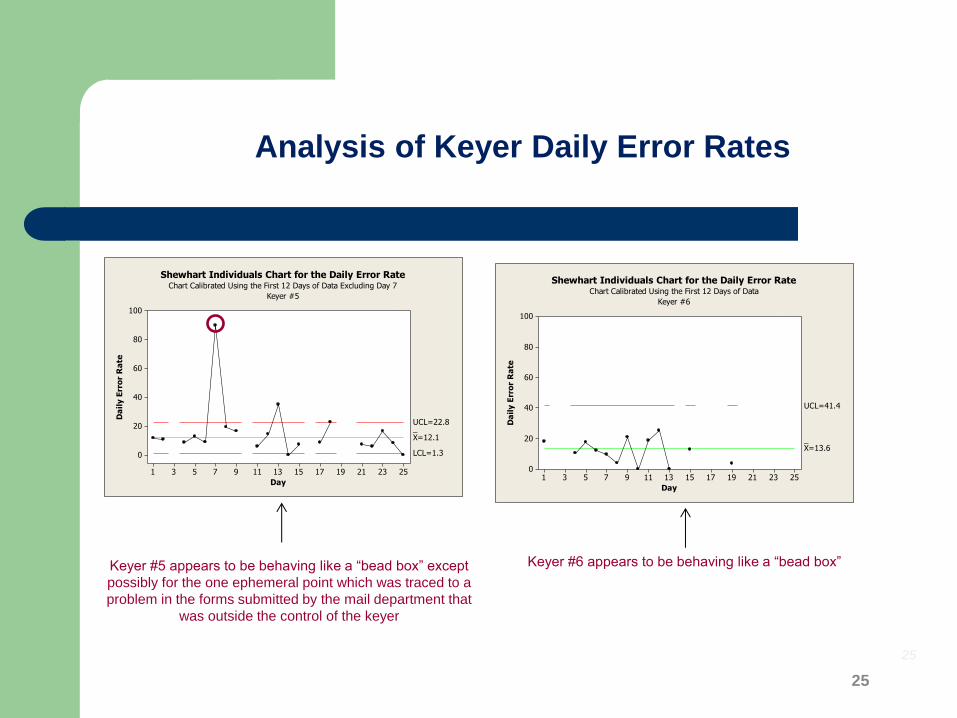

25

Analysis of Keyer Daily Error Rates

Keyer #5 appears to be behaving like a “bead box” except

possibly for the one ephemeral point which was traced to a

problem in the forms submitted by the mail department that

was outside the control of the keyer

Keyer #6 appears to be behaving like a “bead box”

252321191715131197531

100

80

60

40

20

0

Day

Da

ily E

rro

r R

ate

_X=13.6

UCL=41.4

Shewhart Individuals Chart for the Daily Error RateChart Calibrated Using the First 12 Days of Data

Keyer #6

25

26

Analysis of Keyer Daily Error Rates

Keyer #7 appears to be behaving like a “bead box” Keyer #8 appears to be behaving like a “bead box”

252321191715131197531

100

80

60

40

20

0

Day

Da

ily E

rro

r R

ate

_X=4.1

UCL=13.3

Shewhart Individuals Chart for the Daily Error RateChart Calibrated Using the First 12 Days of Data

Keyer #7

252321191715131197531

100

80

60

40

20

0

Day

Da

ily E

rro

r R

ate

_X=6.9

UCL=27.4

Shewhart Individuals Chart for the Daily Error RateChart Calibrated Using the First 12 Days of Data

Keyer #8

26

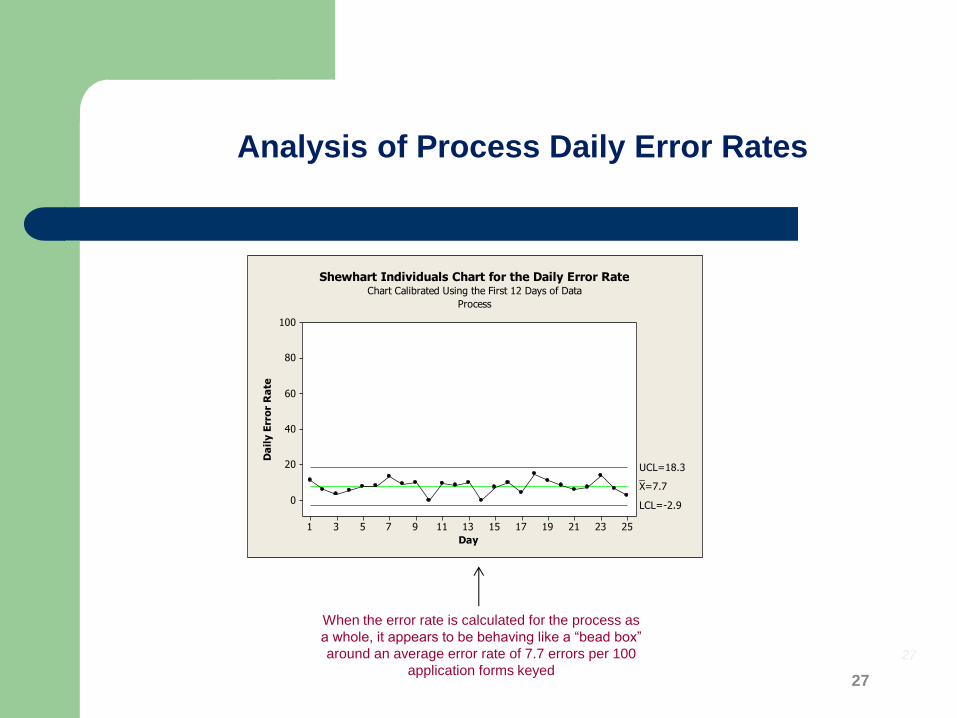

Analysis of Process Daily Error Rates

27

When the error rate is calculated for the process as

a whole, it appears to be behaving like a “bead box”

around an average error rate of 7.7 errors per 100

application forms keyed

252321191715131197531

100

80

60

40

20

0

Day

Da

ily E

rro

r R

ate

_X=7.7

UCL=18.3

LCL=-2.9

Shewhart Individuals Chart for the Daily Error RateChart Calibrated Using the First 12 Days of Data

Process

27

28

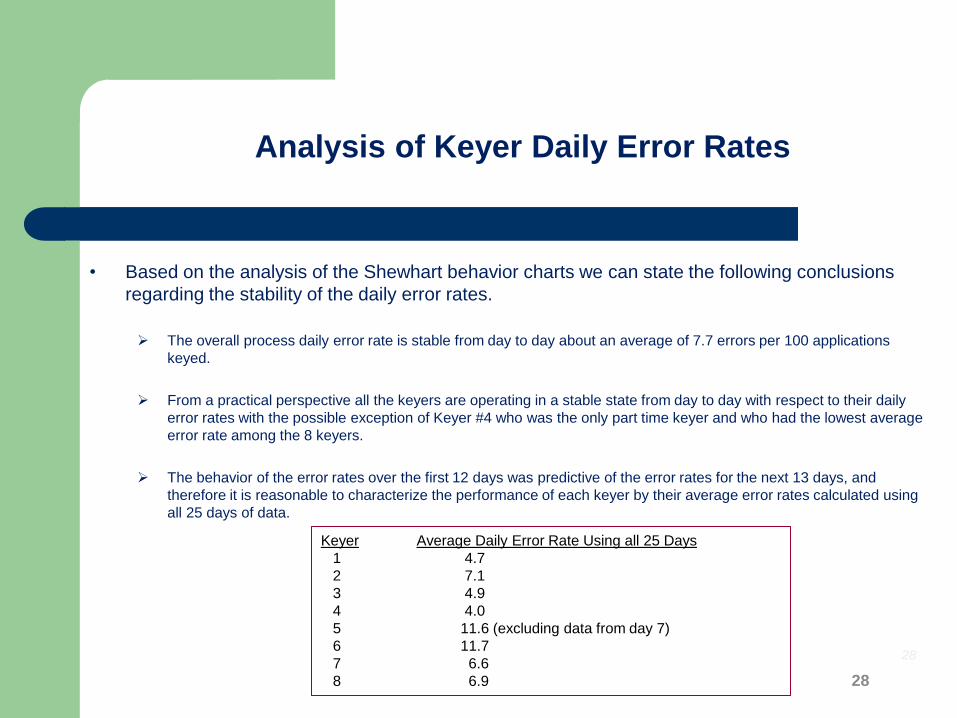

• Based on the analysis of the Shewhart behavior charts we can state the following conclusions

regarding the stability of the daily error rates.

The overall process daily error rate is stable from day to day about an average of 7.7 errors per 100 applications

keyed.

From a practical perspective all the keyers are operating in a stable state from day to day with respect to their daily

error rates with the possible exception of Keyer #4 who was the only part time keyer and who had the lowest average

error rate among the 8 keyers.

The behavior of the error rates over the first 12 days was predictive of the error rates for the next 13 days, and

therefore it is reasonable to characterize the performance of each keyer by their average error rates calculated using

all 25 days of data.

Analysis of Keyer Daily Error Rates

Keyer Average Daily Error Rate Using all 25 Days

1 4.7

2 7.1

3 4.9

4 4.0

5 11.6 (excluding data from day 7)

6 11.7

7 6.6

8 6.9 28

• Given that the keyers daily error rates appear to be stable over days, it is legitimate to ask if

there are any detectable differences in their overall average error rates.

It appears that keyers # 5 and #6 are operating outside the normal system with average error rates that

are greater than those for the remaining six keyers.

• This question can be answered by creating a Shewhart behavior chart using the daily error

rates as the response and the keyer as the rational subgroup.

Comparison of Average Keyer Error Rates

29

87654321

14

12

10

8

6

4

2

0

Keyer

Ave

rag

e E

rro

r R

ate

__X=5.68

UCL=11.07

LCL=0.29

Comparison of Keyer Average Error RatesChart Calibrated Excluding Keyer 5 and Keyer 6 Data

Comparison of Average Keyer Error Rates

30

Source: Arial 9 pt. Flush left; Source, e.g. publication name. Title of source document. Date. URL if needed.

Based on this analysis

there is evidence that

keyer #5 and keyer #6

average error rates are

detectably higher than

the other six keyers.

That is, these two keyers

are operating outside the

capability of the keying

process.

30

• With the analysis of the daily error rates completed, attention was turned to an analysis of the

volume of errors produced by each of the 34 fields on the application form.

• The method of Pareto analysis was used to analyze the volume of errors across the 34 fields

for the process as a whole and by the individual keyers.

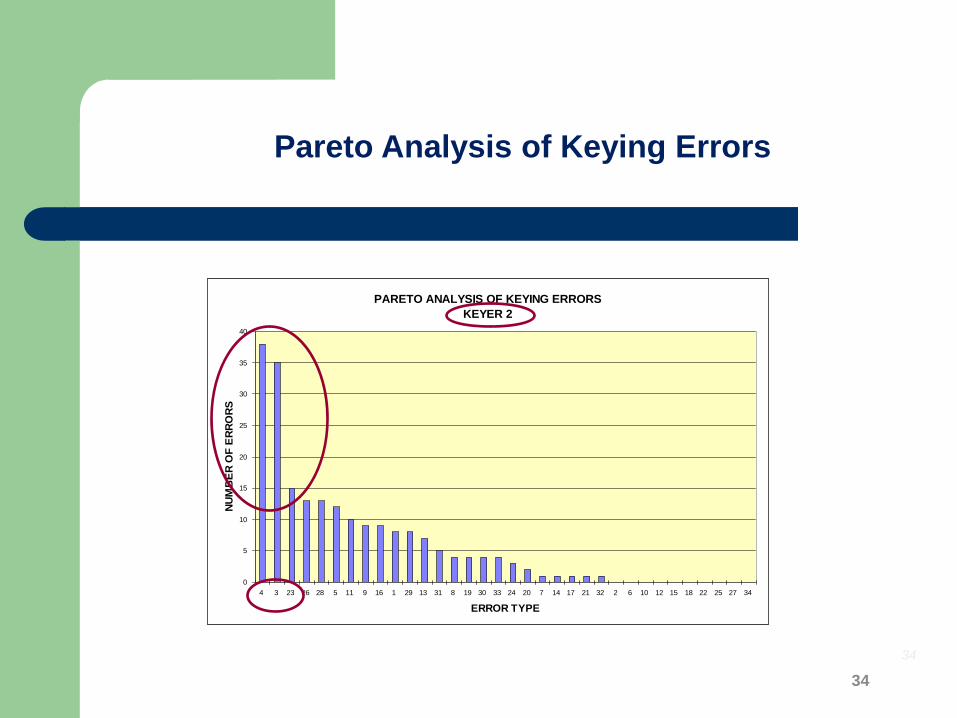

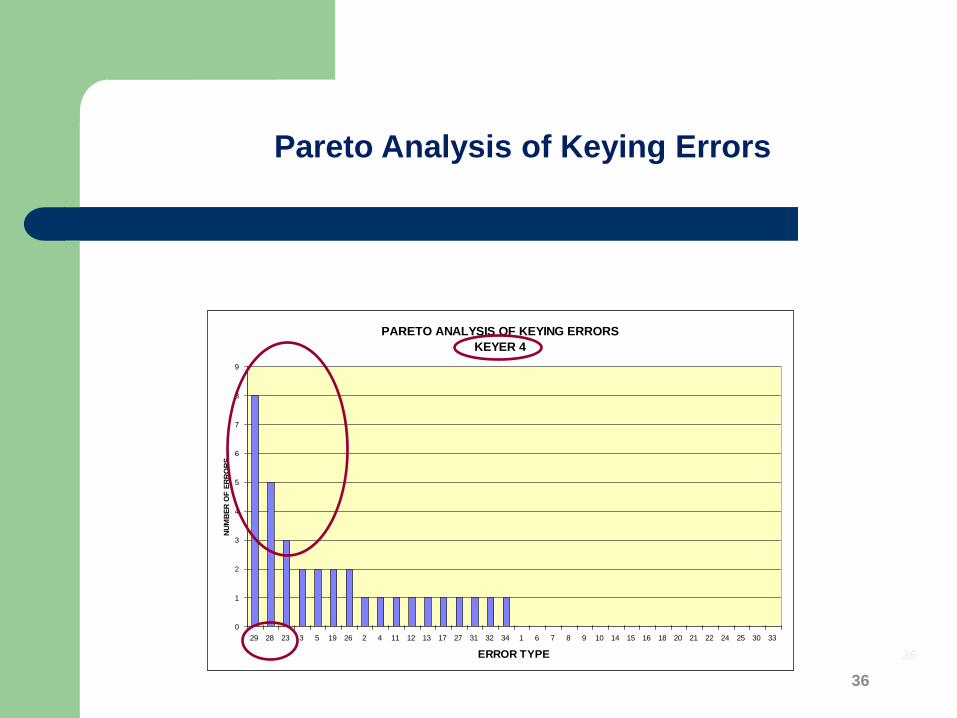

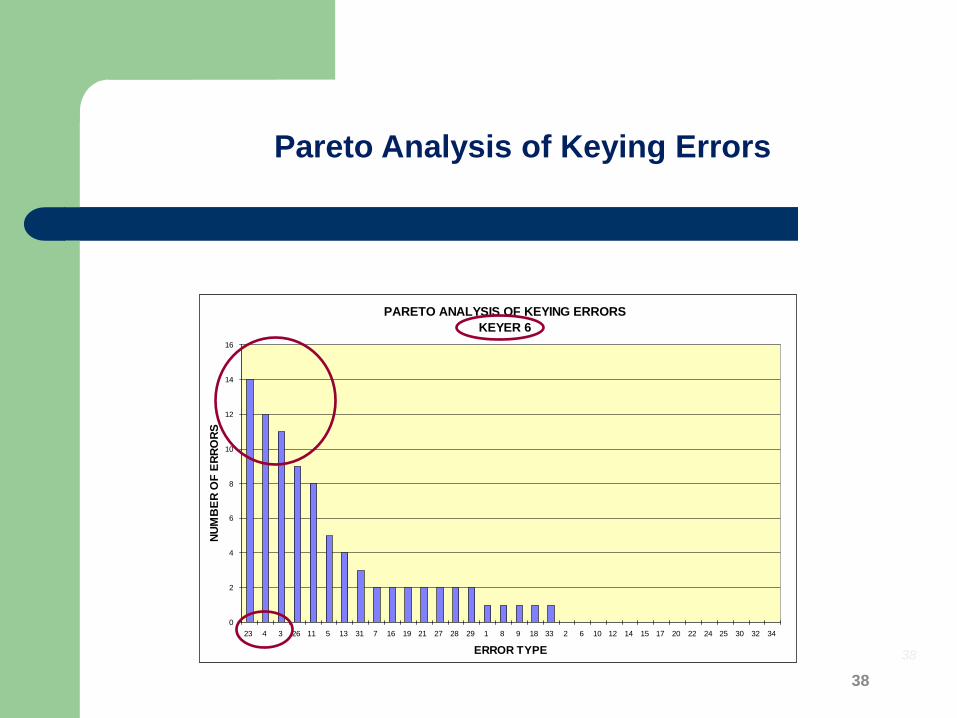

• The following Pareto charts indicate that in all cases, except for keyer #4, who was the only

part-time keyer, the dominate errors occurred for application form fields 3, 4 and 23 which

where the name, address and interest amount fields.

Analysis of Keying Errors by Application Field

31

32

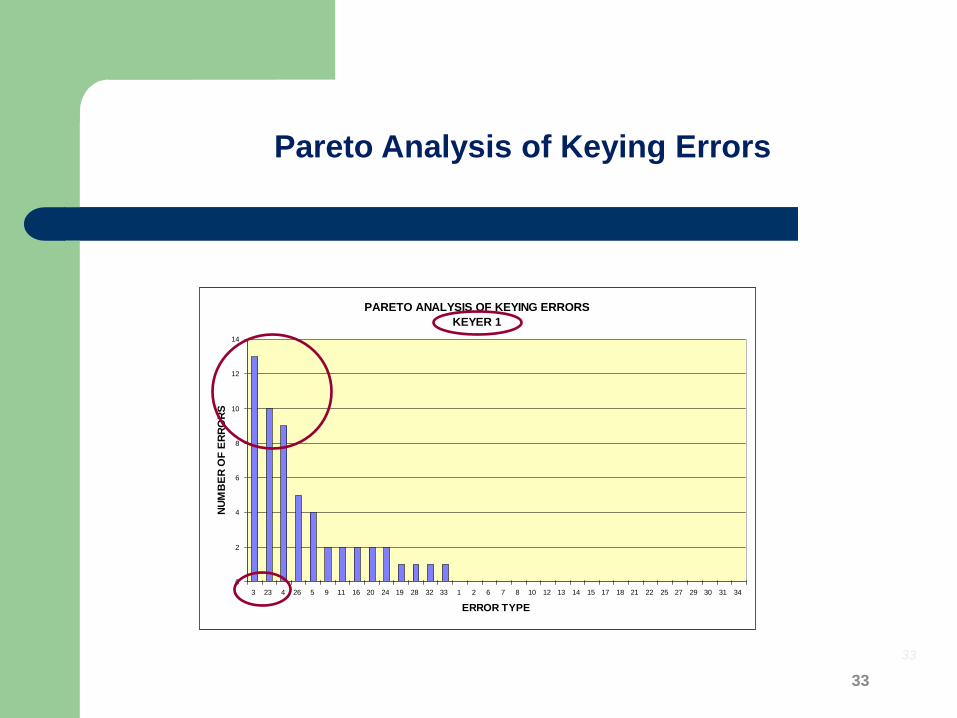

Pareto Analysis of Keying Errors

PARETO ANALYSIS OF KEYING ERRORS

PROCESS

0

20

40

60

80

100

120

3 4 23 26 5 16 11 28 13 1 29 9 31 19 33 7 21 24 8 27 20 2 17 30 32 18 10 14 12 15 22 34 6 25

ERROR TYPE

NU

MB

ER

OF

ER

RO

RS

The Pareto analysis for the process

as a whole demonstrates that

there are 3 of the 34 fields

producing high error volumes.

These are fields 3, 4, and 23.

32

33

Pareto Analysis of Keying Errors

PARETO ANALYSIS OF KEYING ERRORS

KEYER 1

0

2

4

6

8

10

12

14

3 23 4 26 5 9 11 16 20 24 19 28 32 33 1 2 6 7 8 10 12 13 14 15 17 18 21 22 25 27 29 30 31 34

ERROR TYPE

NU

MB

ER

OF

ER

RO

RS

33

34

Pareto Analysis of Keying Errors

PARETO ANALYSIS OF KEYING ERRORS

KEYER 2

0

5

10

15

20

25

30

35

40

4 3 23 26 28 5 11 9 16 1 29 13 31 8 19 30 33 24 20 7 14 17 21 32 2 6 10 12 15 18 22 25 27 34

ERROR TYPE

NU

MB

ER

OF

ER

RO

RS

34

35

Pareto Analysis of Keying Errors

PARETO ANALYSIS OF KEYING ERRORS

KEYER 3

0

2

4

6

8

10

12

14

16

3 23 4 5 26 9 11 13 16 18 2 10 20 31 1 6 7 8 12 14 15 17 19 21 22 24 25 27 28 29 30 32 33 34

ERROR TYPE

NU

MB

ER

OF

ER

RO

RS

35

36

Pareto Analysis of Keying Errors

PARETO ANALYSIS OF KEYING ERRORS

KEYER 4

0

1

2

3

4

5

6

7

8

9

29 28 23 3 5 19 26 2 4 11 12 13 17 27 31 32 34 1 6 7 8 9 10 14 15 16 18 20 21 22 24 25 30 33

ERROR TYPE

NU

MB

ER

OF

ER

RO

RS

36

37

Pareto Analysis of Keying Errors

PARETO ANALYSIS OF KEYING ERRORS

KEYER 5

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

3 26 4 16 5 23 24 27 1 2 6 7 8 9 10 11 12 13 14 15 17 18 19 20 21 22 25 28 29 30 31 32 33 34

ERROR TYPE

NU

MB

ER

OF

ER

RO

RS

37

38

Pareto Analysis of Keying Errors

PARETO ANALYSIS OF KEYING ERRORS

KEYER 6

0

2

4

6

8

10

12

14

16

23 4 3 26 11 5 13 31 7 16 19 21 27 28 29 1 8 9 18 33 2 6 10 12 14 15 17 20 22 24 25 30 32 34

ERROR TYPE

NU

MB

ER

OF

ER

RO

RS

38

39

Pareto Analysis of Keying Errors

PARETO ANALYSIS OF KEYING ERRORS

KEYER 7

0

2

4

6

8

10

12

14

16

18

3 23 1 4 5 16 13 26 7 9 28 31 2 19 21 27 33 8 10 11 15 17 22 24 29 32 6 12 14 18 20 25 30 34

ERROR TYPE

NU

MB

ER

OF

ER

RO

RS

39

40

Pareto Analysis of Keying Errors

PARETO ANALYSIS OF KEYING ERRORS

KEYER 8

0

2

4

6

8

10

12

14

16

18

20

4 3 23 13 16 11 26 28 29 1 5 9 21 31 14 17 19 2 6 7 8 10 12 15 18 20 22 24 25 27 30 32 33 34

ERROR TYPE

NU

NB

ER

OF

ER

RO

RS

40

41

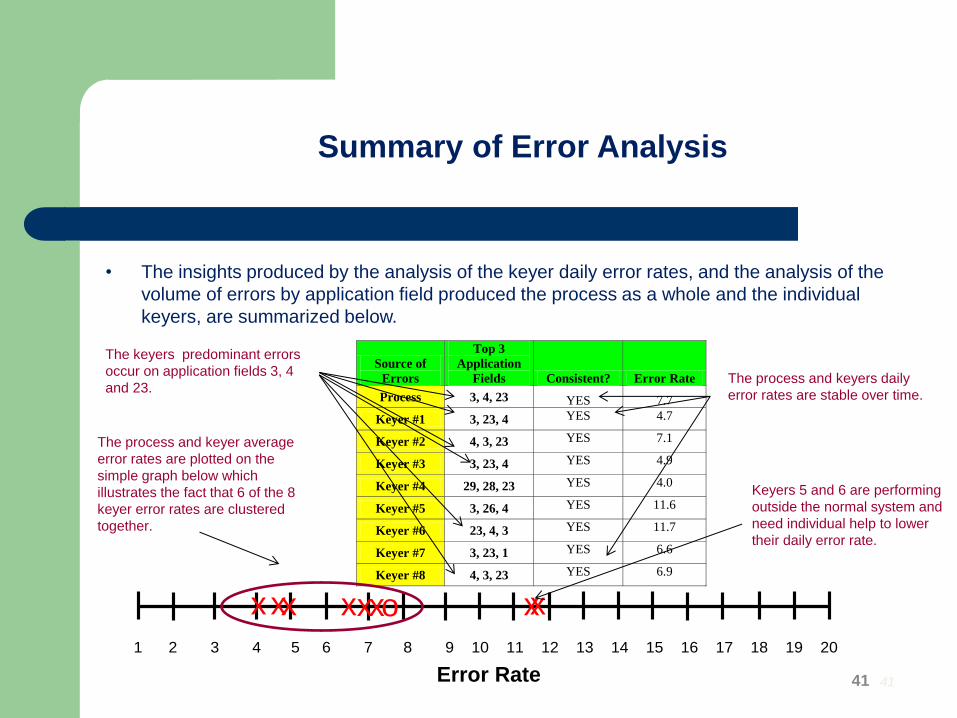

Summary of Error Analysis

• The insights produced by the analysis of the keyer daily error rates, and the analysis of the

volume of errors by application field produced the process as a whole and the individual

keyers, are summarized below.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Error Rate

o x x x x x x x x

Source of

Errors

Top 3

Application

Fields Consistent? Error Rate

Process 3, 4, 23 YES 7.7

Keyer #1 3, 23, 4 YES 4.7

Keyer #2 4, 3, 23 YES 7.1

Keyer #3 3, 23, 4 YES 4.9

Keyer #4 29, 28, 23 YES 4.0

Keyer #5 3, 26, 4 YES 11.6

Keyer #6 23, 4, 3 YES 11.7

Keyer #7 3, 23, 1 YES 6.6

Keyer #8 4, 3, 23 YES 6.9

The process and keyer average

error rates are plotted on the

simple graph below which

illustrates the fact that 6 of the 8

keyer error rates are clustered

together.

The process and keyers daily

error rates are stable over time.

The keyers predominant errors

occur on application fields 3, 4

and 23.

Keyers 5 and 6 are performing

outside the normal system and

need individual help to lower

their daily error rate.

41

Conclusions

42

• C1: In general, the keyers are performing in a stable manner over time.

• C2: Keyers 5 and 6 appear to be operating with higher error rates than the other six keyers

and may need local help to improve their error rates.

• C3: In general the keyers are making the same common errors on fields 3,4, and 23 which

must be due to process design problems because the process design is the only thing the

keyers have in common.

• Fields 3 and 4 are name and address fields which are free form

• Field 23 is the loan interest amount field that is currently manually calculated by

the keyer using daily interest rate tables provided by management.

42

• Q1: Is the process daily error rate stable over time? - Yes

• Q2: Are the keyer daily error rates {ERkd} stable over time? - Yes

• Q3: Are there detectable differences in the average daily error rate across the eight keyers? - Yes, Keyer #5 and Keyer #6 are operating outside the normal system.

• Q4: Are there any detectable differences in the volume of keyer errors across the 34 loan application fields? - Yes, fields 3, 4 and 23 are the dominant fields producing keying errors.

• Q5: What local and/or global actions can be taken to reduce the future number of application field errors and the keyer daily error rates? – See recommendations

Answers to the Research Questions

43

Recommendations

44

• R1: Management should immediately take action to remove the causes of the

errors for application fields 3, 4, and 23 that are common to all keyers.

Fields 3 and 4 are Applicant Name and Address which are currently free text fields.

The application form should be redesigned to block the name and address fields to

force the applicant to print their name and address.

Field 23 is the Loan Interest Amount field that is currently manually calculated by the

keyer using daily interest rate tables provided by management. This calculation should

be automated which will eliminate this error category entirely.

44

Recommendations

45

• R2: Because the keyers are operating in a stable manner over time, and are

subject to making the same common errors associated with application fields 3,

4, and 23, the weekly counseling sessions involving the supervisor are

ineffective at reducing the error rates and should be discontinued.

• These sessions are an attempt to take local action to remove common

causes of variation and will not be successful.

• R3: Management should take local action on Keyer 5 and Keyer 6 in an attempt

to help them reduce their average error rates because although their daily error

rates are stable over time, they are operating at an average error rate that is

outside the capability of the system.

45

Recommendations

46

• R4: Management should use the performance measurement database to create

a monitoring system capable of capturing and analyzing the keyer error rates on

a daily basis.

46

47

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/20

15

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

12000

11000

10000

9000

8000

7000

6000

5000

4000

3000

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=7564

UCL=11323

LCL=3805

Total Monthly Number of Corporate FilingsVariation Across Months

Data points used for the calculations: 1-4

48

15001200900600300

30

25

20

15

10

5

0

Productivity

Fre

qu

en

cy

Distribution of Employee Monthly Corporate Filings

49

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1400

1200

1000

800

600

400

200

0

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=619

UCL=1253

LCL=-15

Number of Monthly Corporate FilingsEmployee - 1

50

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1400

1200

1000

800

600

400

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=824

UCL=1301

LCL=346

Number of Monthly Corporate FilingsEmployee - 2

51

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1200

1000

800

600

400

200

0

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=586

UCL=1181

LCL=-9

Number of Monthly Corporate FilingsEmployee - 3

52

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1200

1100

1000

900

800

700

600

500

400

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=770.3

UCL=1127.8

LCL=412.7

Number of Monthly Corporate FilingsEmployee - 4

53

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1600

1400

1200

1000

800

600

400

200

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=843

UCL=1448

LCL=239

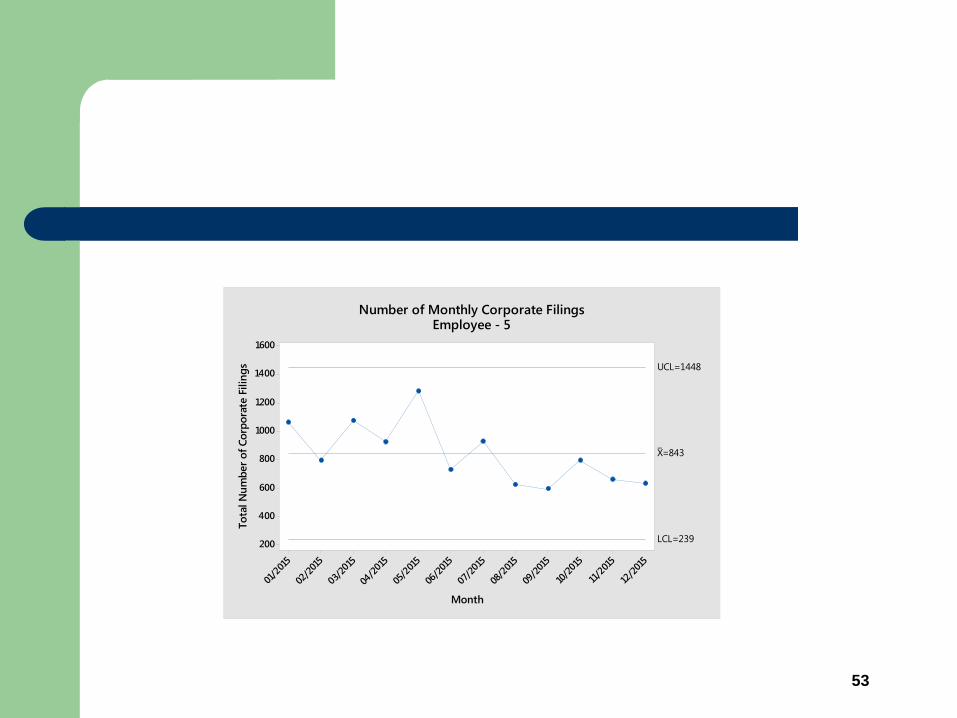

Number of Monthly Corporate FilingsEmployee - 5

54

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1500

1250

1000

750

500

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=906

UCL=1372

LCL=441

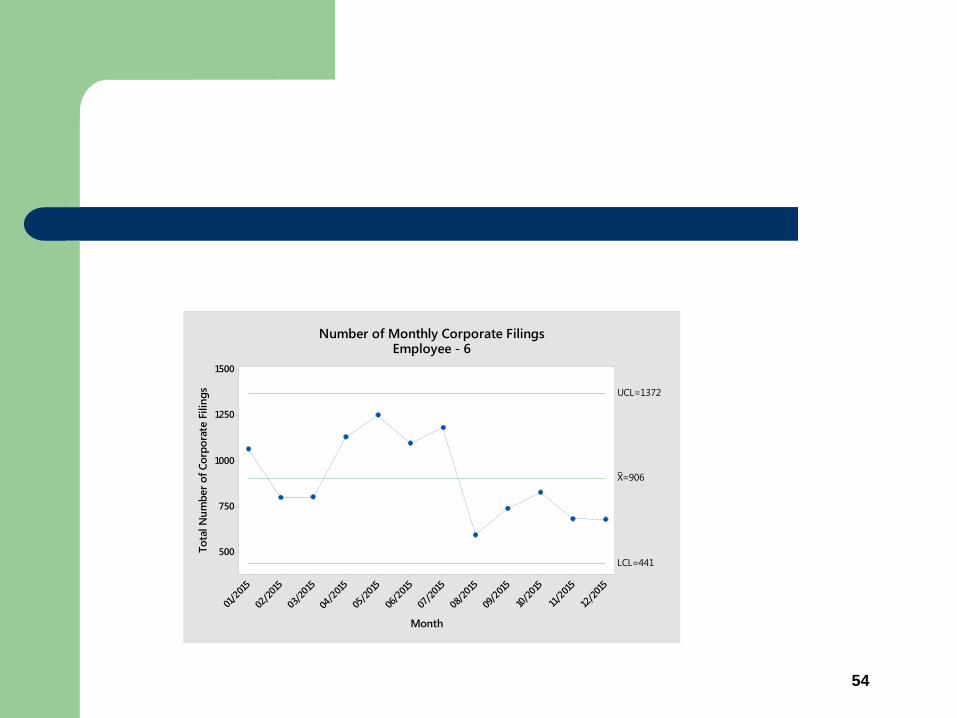

Number of Monthly Corporate FilingsEmployee - 6

55

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1200

1000

800

600

400

200

0

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=589

UCL=1128

LCL=51

Number of Monthly Corporate FilingsEmployee - 7

56

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1000

800

600

400

200

0

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=529

UCL=1029

LCL=30

Number of Monthly Corporate FilingsEmployee - 8

57

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1600

1400

1200

1000

800

600

400

200

0

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=755

UCL=1537

LCL=-27

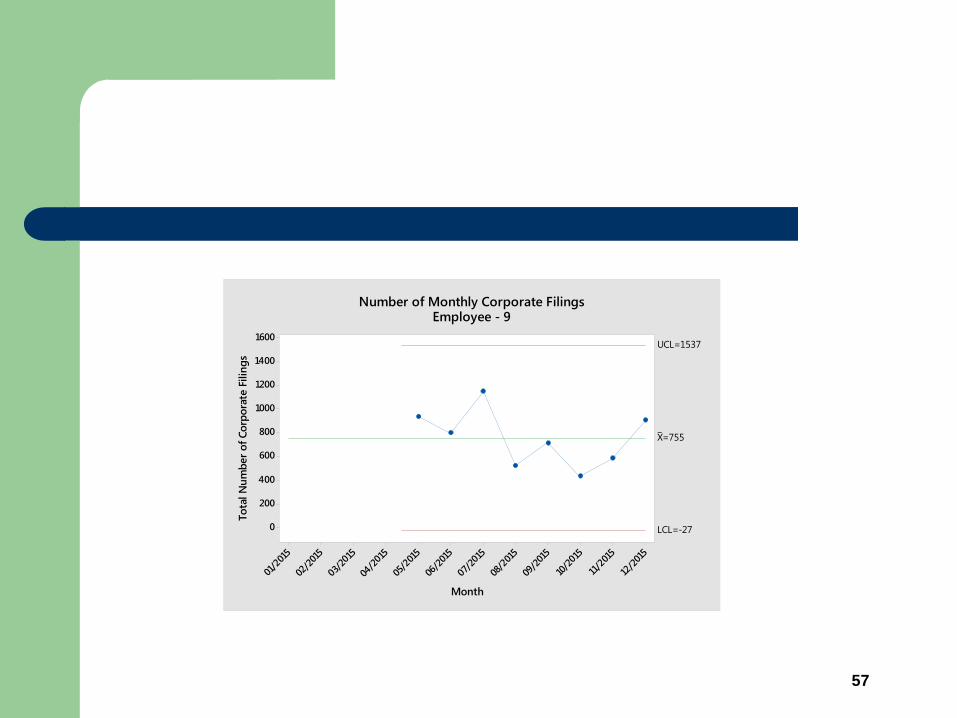

Number of Monthly Corporate FilingsEmployee - 9

58

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1800

1600

1400

1200

1000

800

600

400

200

0

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=912

UCL=1646

LCL=178

Number of Monthly Corporate FilingsEmployee - 10

59

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1400

1200

1000

800

600

400

200

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=798

UCL=1385

LCL=212

Number of Monthly Corporate FilingsEmployee - 11

60

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/2

015

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1800

1600

1400

1200

1000

800

600

400

200

0

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=791

UCL=1451

LCL=132

1

Number of Monthly Corporate FilingsEmployee - 12

61

12/2

015

11/2

015

10/2

015

09/2

015

08/2

015

07/20

15

06/2

015

05/2

015

04/2

015

03/2

015

02/2

015

01/2

015

1500

1400

1300

1200

1100

1000

900

800

700

Month

To

tal N

um

ber

of

Co

rpo

rate

Filin

gs

_X=1111.4

UCL=1465.8

LCL=757.0

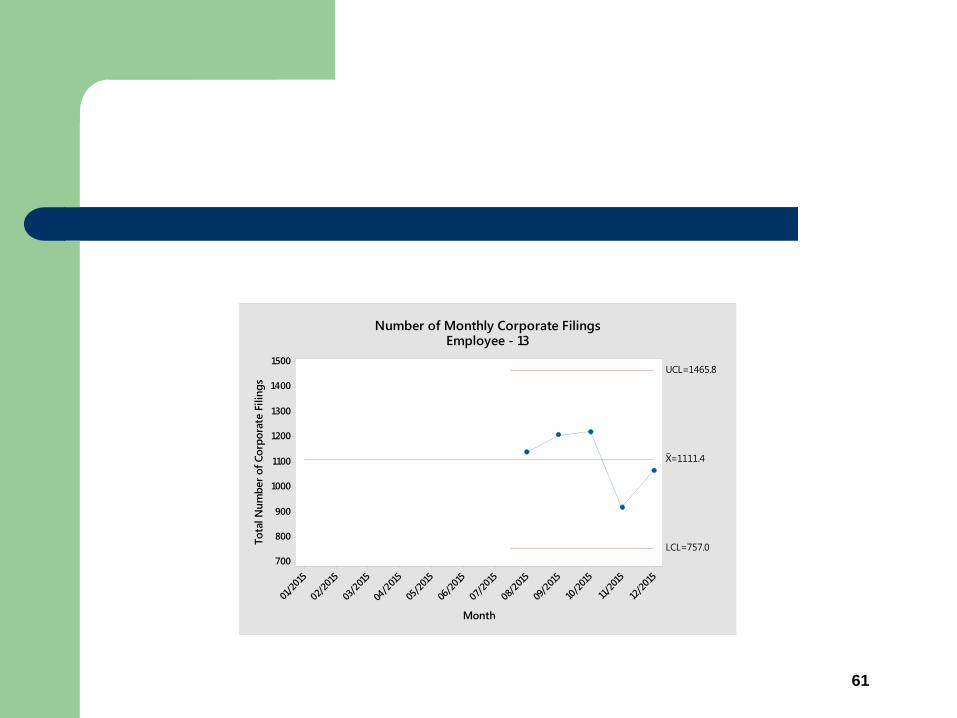

Number of Monthly Corporate FilingsEmployee - 13

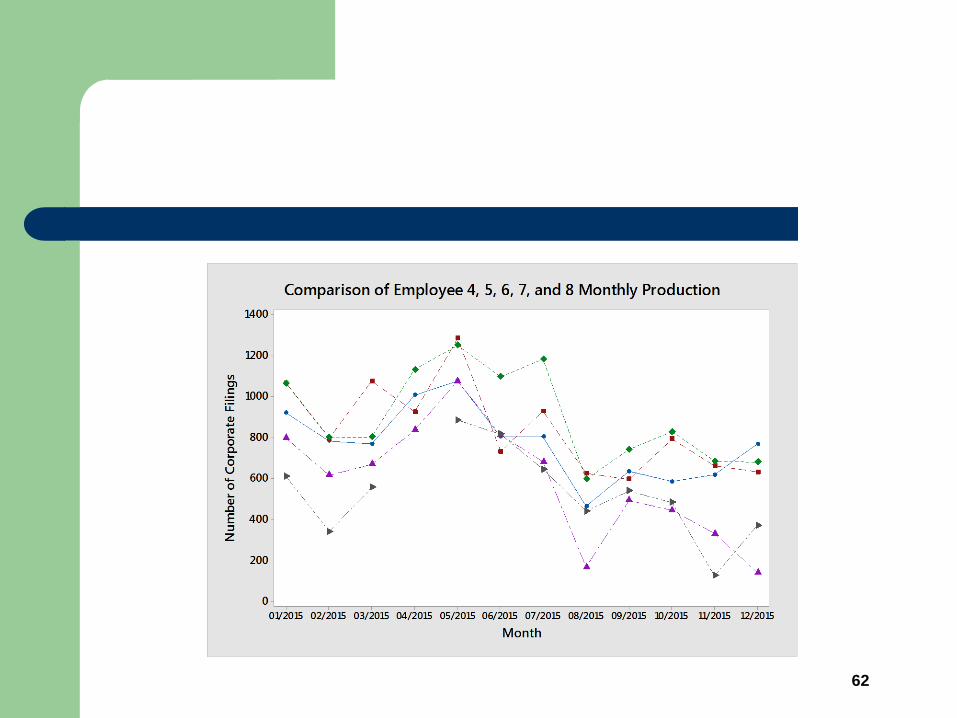

62

63

13121110987654321

1200

1000

800

600

400

Employee ID

Mo

nth

y A

vera

ge C

laim

s P

roce

ssed

__X=760.5

UCL=1076.5

LCL=444.6

13121110987654321

400

300

200

100

0

Employee ID

Mo

nth

y A

vera

ge C

laim

s P

roce

ssed

_S=221.4

UCL=462.4

LCL=0

1

1

Comparison of Employee Productivity Rates

Tests are performed with unequal sample sizes.

64

10

5

01

51

02

52

03

003 006 009 0021 005

N

yc

ne

uq

erF

sgniliF etaroproC fo rebmu

P

elbairaV

ytivitcudorP detsujdA eeyolpmE

ytivitcudor

H ytivitcudorP detsujdA eeyolpmE ,ytivitcudorP fo margotsi

65

How is Performance Improved?

> 80% Actions

on the Process

< 20% Actions

within the Process