Amylin Pharmaceuticals, Inc. Financial Analysis...

89

Amylin Pharmaceuticals, Inc. Financial Analysis Report Prepared by: Danielle Davis and Liz Van Hemel Presented to: Dr. Mohammed Ahmed December 15, 2009

Transcript of Amylin Pharmaceuticals, Inc. Financial Analysis...

Amylin Pharmaceuticals, Inc.

Financial Analysis Report

Prepared by: Danielle Davis and Liz Van Hemel

Presented to: Dr. Mohammed Ahmed

December 15, 2009

Amylin Pharmaceuticals, Inc. Financial Analysis Report 1

Table of Contents

EXECUTIVE SUMMARY 5 INTRODUCTION 6 Company Background 6 Mission 7 Goals and Objectives 7 Revenues 8 Assets 11 Growth Rate 14 Market Position 15 Company Strategies/Products 16 Management and Corporate Culture 18 Strategic Partnerships 19 MARKET OUTLOOK 20 General Overview 20 Historical Performance 21 Future Outlook 23 INDUSTRY OUTLOOK 23 Nature of the Industry 23 Industry Composition 26 Industry Growth 26 Opportunities and Threats 27 Future Outlook 29 FINANCIAL STATEMENT ANALYSIS 31 Income Statement 31 Common Size Income Statement 32 Balance Sheet 34 Common Size Balance Sheet 35 Statement of Cash Flows 37 Cash Flow Analysis 40 Financial Ratio Analysis 43

Amylin Pharmaceuticals, Inc. Financial Analysis Report 2

STRENGTHS AND WEAKNESSES ANALYSIS 54 Financial Ratios Industry Comparison 54 Strengths 57 Weaknesses 57 Reasons for Level of Performance 61 FINANCIAL FORECASTING 62 Growth Rate Data 62 Pro Forma Income Statement 68 Pro Forma Balance Sheet 70 CAPITAL STRUCTURE ANALYSIS 72 VALUATION ANALYSIS 77 Book Value 77 Market Value 77 Common Stock Valuation 77 Liquidation Value 78 BANKRUPTCY ANALYSIS 79 VALUE-BASED FINANCIAL ANALYSIS 81 RECOMMENDATIONS 82 REFERENCES 84 APPENDIX 88

Amylin Pharmaceuticals, Inc. Financial Analysis Report 3

List of Tables

Table 1: Product Sales (2006-2008) 8

Table 2: Revenues from Collaborative Agreements (2006-2008) 9

Table 3: Total Revenues (2004-2008) 10

Table 4: First Six Months Total Revenue Comparison (2008 & 2009) 10

Table 5: Amylin & Top Competitors Total Revenue Comparison (2006-2008) 11

Table 6: Summary of Current and Long-Term Assets (2006-2008) 12

Table 7: Mid-year Assets (2008 & 2009) 12

Table 8: Amylin and Top Competitors Asset Comparison (June 30, 2009) 13

Table 9: Product Sales & Total Revenue Growth (2006-2008) 14

Table 10: Amylin Management Team 18

Table 11: Outline of Strategic Collaborations 19

Table 12: Disease Trends 27

Table 13: Company Financial Ratio Comparisons 55

Table 14: Summary of Financial Weaknesses 58

Table 15: Biotechnology Industry Revenue Growth (2005-2008) 63

Table 16: Biotechnology Industry Expected Revenue Growth (2009-2011) 63

Table 17: Weighted Average Cost of Capital 76

Table 18: Bankruptcy Analysis Ratios 80

Table 19: Altman’s Bankruptcy Model Z-Score Computation 80

Amylin Pharmaceuticals, Inc. Financial Analysis Report 4

List of Figures

Figure 1: Historical Performance of Major Market Indices 22

Figure 2: Income Statement (2006-2008) 31

Figure 3: Common Size Income Statement (2006-2008) 32

Figure 4: Operations Overview (2006-2008) 33

Figure 5: Balance Sheet (2006-2008) 34

Figure 6: Common Size Balance Sheet (2006-2008) 35

Figure 7: Asset Structure (2006-2008) 36

Figure 8: Liability & Equity Structure (2006-2008) 36

Figure 9: Statement of Cash Flows (2006-2008) 37

Figure 10: Cash Flow Balances (2006-2008) 39

Figure 11: Cash Flow by Activity (2006-2008) 39

Figure 12: Company Comparisons of ROA, ROE, and ROI (Year ended 12/31/08) 56

Figure 13: Growth Rate Determination 65

Figure 14: Pro Forma Income Statement for 2009 68

Figure 15: Pro Forma Balance Sheet for 2009 70

Figure 16: Capital Structure (2006-2009) 74

Amylin Pharmaceuticals, Inc. Financial Analysis Report 5

EXECUTIVE SUMMARY

Amylin Pharmaceuticals, Inc. is a relatively young and small company operating in the

biotechnology industry. The company was founded upon the discovery of the peptide hormone amylin

and its role in the maintenance of normal glucose concentrations in the human body. In September 1987

Amylin Pharmaceuticals was incorporated with founding Chief Executive Officer, Howard E. Greene,

Jr., and a team of scientists leading the way towards the development of a drug that would be a synthetic

analogue of amylin and would be used in the management of diabetes. After nearly two decades of

research and development, the company finally introduced two first-in-class diabetes medications:

BYETTA® and SYMLIN®. Currently, these are the only two products that Amylin has on the market.

Financial analyses have indicated that Amylin Pharmaceuticals is in poor financial health and

represents a great risk to investors. While net product sales and total revenues over the past three years

have grown by 17.1% and 17.8% respectively, the company has yet to turn a profit. Moreover, in 2008

the company’s return on assets and return on equity were -18.09% and -69.80% respectively. These and

other ratios consistently show the troubled financial condition that Amylin is in.

Amylin’s common stock is traded on the NASDAQ under the ticker symbol AMLN. As might

be expected based on the financial analyses, the company has significantly decreased the wealth of its

stockholders. As of December 1, 2009, the closing price of Amylin common stock was $14.38. While

this is up compared to recent months, it is way down from $45.33, the closing price on August 31, 2006.

This report provides a complete analysis of Amylin’s internal and external environments.

General company information, a stock market outlook, and a discussion on the biotechnology industry

will collectively provide a foundation for further analysis. The final sections of the report will consist of

evaluations of company financial statements, an analysis of company strengths and weaknesses,

financial forecasting, analyses of capital structure and bankruptcy risk, a company valuation, and

recommendations for increasing the value of the firm.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 6

INTRODUCTION

Company Background

In the late 1980s, groundbreaking research was being carried out by a group of Oxford

University scientists that involved the discovery of the peptide hormone amylin and its role in

the maintenance of normal glucose concentrations in the human body. These scientists

discovered that amylin is created in and secreted from the same pancreatic beta cells that produce

insulin. In a normal, healthy individual these two hormones, in conjunction with another

pancreatic hormone, glucagon, would work together to preserve normal glucose levels; however,

in people with diabetes, the collaborative functions of these three hormones are thrown out of

balance. These research findings were the inspiration behind Amylin Pharmaceuticals, Inc. In

September 1987 Amylin Pharmaceuticals was incorporated in the state Delaware, with Howard

E. Greene, Jr. as the founding Chief Executive Officer. Greene had two decades of experience

with eleven different medical technology companies and was compelled to carry on the research

begun at Oxford with the realization that this revelation could lead to significant improvements

in the treatment of diabetes. So Greene and a team of scientists began efforts to develop a drug

that would be a synthetic analogue of amylin and would be used in the management of the

disease (Funding Universe, 2005).

The company struggled and toiled away for nearly 18 years (relying on R&D funding

from venture capitalists), until finally in 2005 it successfully introduced two first-in-class

diabetes medications: BYETTA® and SYMLIN® (products will be discussed in detail later in the

text). It was at this point in time that the company transformed from a research organization into

an “integrated biopharmaceutical company with capabilities in research, development,

manufacturing, and commercialization” (Amylin, 2009).

Amylin Pharmaceuticals, Inc. Financial Analysis Report 7

In 1992, five years after its inception, the company went public and has since been

trading on the National Association of Securities Dealers Automated Quotations (NASDAQ)

National Market under the ticker symbol AMLN. Amylin Pharmaceuticals is headquartered in

San Diego, California. The company ends its fiscal year on December 31st, and its website

address on the World Wide Web is www.amylin.com.

Mission

“Amylin Pharmaceuticals is a biopharmaceutical company committed to improving the lives of people with diabetes, obesity and other diseases through the discovery, development and commercialization of innovative medicines.”

—Amylin Pharmaceuticals’ 2008 Annual Report

Although Amylin Pharmaceuticals does not layout a specific mission statement, the

following maxim is clearly stated on its company website, in its Annual Report, and throughout

other company documentation, and it certainly serves the purpose of an effective mission

statement in that it identifies who they are (a biopharmaceutical company), who their customers

are (people with diabetes, obesity, and other diseases), and their reason for existence (improve

lives through the discovery, development and commercialization of innovative medicines).

Goals and Objectives

Amylin has outlined a five-point plan to generate value in 2009 (following points taken

directly from www.amylin.com):

• Growing revenue from BYETTA® (exenatide) injection, our first-in-class marketed product for type 2 diabetes;

• Bringing exenatide once weekly to patients as quickly as possible;

• Growing revenue from our second marketed diabetes product, SYMLIN® (pramlintide acetate) injection;

• Continuing development of potentially breakthrough therapies for obesity; and

Amylin Pharmaceuticals, Inc. Financial Analysis Report 8

• Lowering our cost structure to improve operating results and shorten our path to profitability.

Moreover, in a press release dated July 21, 2009 and titled “Amylin Pharmaceuticals Reports

Second Quarter Financial Results,” the company’s senior vice president of finance and chief

financial officer, Mark G. Foletta, made the following statement: “We set a goal of becoming

operating cash flow positive by the end of 2010, and we have taken considerable steps toward

achieving that goal.” This goal reiterates the plan to improve operating results as revealed in the

last point mentioned above while attaching a target deadline to this plan.

While the company is unclear about its specific objectives for growing revenues from

BYETTA® and SYMLIN® and its objectives for swiftly bringing exenatide to market, its 2008

Annual Report does address its goal for lowering its cost structure to boost operating results and

curtail its path to profitability. This will be discussed later in the company strategies section.

Revenues

As mentioned before, Amylin Pharmaceuticals is currently selling only two products,

BYETTA® and SYMLIN®. Table 1 below shows the sales (in millions) from each of these

products over the past 3 years as well as the net product sales (in millions) for the two products

combined.

Table 1: Product Sales (2006-2008)

Year ended December 31, 2008 2007 2006 BYETTA® $678.5 $636.0 $430.2 SYMLIN® 86.8 65.5 43.8 Net Sales $765.3 $701.5 $474.0 Source: Amylin Pharmaceuticals, 10-K, February 27, 2009

What can be gleaned from the above table is that sales for both products have been on the

rise, and clearly BYETTA® accounts for a significant portion of net sales. BYETTA® sales as a

Amylin Pharmaceuticals, Inc. Financial Analysis Report 9

percentage of net product sales were 88.7%, 90.7%, and 90.8% for the years 2008, 2007, and

2006 respectively. On the other hand, SYMLIN® sales as a percentage of net product sales were

11.3%, 9.3%, and 9.2% for those same years.

For a look at individual and net product sales for the current year, attention is turned to

the company’s quarterly report for the quarter ended June 30, 2009. According to this latest

report, revenues for the six months ended June 30, 2009 for BYETTA® and SYMLIN® were

$332.8 million and $44.0 million respectively; these revenues are combined to reach net product

revenues of $376.8 million. Revenues for the same period in 2008 were $336.0 million from

BYETTA® and $43.1 million from SYMLIN® for a total of $379.1 million.

In addition to the product sales discussed above, Amylin also receives revenues from its

collaborative agreements. These revenues are a result of a collaborative agreement with Eli Lilly

and Company for shared development of exenatide (refer to Strategic Partnerships). In order to

equalize development expenses, Lilly made up-front payments to Amylin and has made

milestone payments and cost-sharing payments. The revenues (in millions) over the past few

years from these payments are shown in the following table.

Table 2: Revenues from Collaborative Agreements (2006-2008)

Year ended December 31, 2008 2007 2006 Amortization of up-front payments $4.3 $4.3 $4.3 Recognition of milestone payments -- 15.0 -- Cost-sharing payments 70.5 60.2 32.5 Total Revenues under collaborative agreements

$74.8 $79.5 $36.8

Source: Amylin Pharmaceuticals, 2008 Form 10K Next, these revenues under collaborative agreements are added to revenues from net

product sales to obtain the total revenues for Amylin Pharmaceuticals, as shown in the following

table (all values in thousands).

Amylin Pharmaceuticals, Inc. Financial Analysis Report 10

Table 3: Total Revenues (2004-2008)

Years Ended December 31, 2008 2007 2006 2005 2004 Net Product Sales

$765,342

$701,450

$474,038

$86,713

---

Revenues under collaborative agreements

74,767

79,547

36,837

53,761

34,268

Total Revenues $840,109 $780,997 $510,875 $140,474 $34,268 Source: Amylin Pharmaceuticals, Form 10-K, February, 27, 2009 Note: Amylin’s products were first launched in 2005; thus, no product sales exist for 2004.

It is apparent that Amylin has experienced significant growth in revenues over this five

year period. In fact, the compound annual growth rate (CAGR) is equal to 90% (calculated as

CAGR = [(Ending Value/Beginning Value) ^ (1/#of years)] – 1).

Finally, we’ll take a look at total revenues for the first six months of 2009 compared to

total revenues for the same period in 2008 as provided by Amylin’s quarterly report for the

quarter ended June 30. Again, all values are in thousands of U.S. dollars.

Table 4: First Six Months Total Revenue Comparison (2008 & 2009)

Six Months Ended June 30, 2009 2008 Net Product Sales

$376,829

$379,056

Revenues under collaborative agreements 26,217 40,200 Total Revenues $403,046 $419,256 Source: “Amylin Pharmaceuticals Reports Second Quarter Financial Results,” 2009

Now, in order to have an understanding of how Amylin’s revenues compare to those of

other firms in the Biotechnology industry, attention is turned to Amylin’s top competitors as

defined by Hoover’s and Yahoo Finance: GlaxoSmithKline, Merck & Co., Inc., and Novo

Nordisk. Revenues (in millions of US Dollars) over the past three years for each of these

companies are presented in Table 5 below. Amylin’s total revenues are shown once again to aid

in comparisons.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 11

Table 5: Amylin & Top Competitors Total Revenue Comparison (2006-2008)

December 2008 December 2007 December 2006 GlaxoSmithKline 35,244.6 45,347.9 45,479.2 Merck 23,850.3 24,197.7 22,636.0 Novo Nordisk 8,627.7 8,257.4 6,853.6 Amylin Pharmaceuticals 840.1 781.0 510.9 Source: Hoover’s Company Records

As these numbers reveal, Amylin’s revenues are minimal compared to those of its top

competitors. The most likely reasons for these significant differences in revenues are history and

number of products on the market. Merck and Novo Nordisk were founded in 1891 and 1923

respectively, and while GlaxoSmithKline was only recently established in 2000, its history goes

as far back as the early eighteenth century (“About Merck,” “About Novo Nordisk” & “Our

history-About GlaxoSmithKline,” 2009). With Amylin’s history only tracing back to the late

1980s, it is like a baby in the industry.

Because Amylin’s competitors have been in the industry for a greater length of time, they

have many more products on the market. For instance, Merck markets nearly a hundred different

products and GlaxoSmithKline sells even more (numerous prescription medicines, vaccines, and

consumer healthcare products). Novo Nordisk, on the other hand, currently has nine products on

the market (“About Novo Nordisk,” 2009); this is reflected in their considerably lower revenues

compared to GlaxoSmithKline and Merck. All in all, since Amylin is presently selling only two

products, it is easy to see why their revenues are meager in comparison to its competition.

Assets

The information in the subsequent table shows a summary of Amylin Pharmaceuticals’

current and long-term assets as drawn from its consolidated balance sheets from the years 2006,

2007, and 2008. All values are in thousands of US Dollars.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 12

Table 6: Summary of Current and Long-Term Assets (2006-2008)

December 31, 2008 2007 2006 Current Assets: Cash & cash equivalents $237,263 $422,232 $66,640 Short-term investments 579,575 708,183 700,691 Accounts receivable, net 62,369 73,579 58,089 Inventories, net 115,823 100,214 59,299 Other current assets 41,038 32,100 22,098 Total Current Assets 1,036,068 1,336,308 906,817 Property, plant and equipment, net 636,922 390,301 146,779 Other long-term assets 23,755 28,082 2,870 Debt issuance costs 15,884 19,520 3,920 Total Assets $1,712,629 $1,774,211 $1,060,386 Source: Amylin Pharmaceuticals, 2008 and 2007 Form 10K Between the year 2006 and the year 2007, Amylin had increases in both current assets

and long-term assets. Particularly, the company had a significant increase in cash and cash

equivalents, net inventories, property, plant and equipment, and other long-term assets.

However, by 2008, the company had a nearly 44% decrease in cash and cash equivalents and

about an 18% decrease in short-term investments. Another notable change was the significant

increased investment in property, plant, and equipment between the years 2007 and 2008

(roughly a 63% change).

For a more recent snapshot of Amylin’s current and long-term assets, we turn to its

consolidated balance sheet presented in its most recent quarterly report.

Table 7: Mid-year Assets (2008 & 2009)

June 30, 2009 2008 Current Assets: Cash & cash equivalents $111,272 $237,263 Short-term investments 533,166 579,575 Accounts receivable, net 76,405 62,369 Inventories, net 109,803 115,823 Other current assets 64,839 41,038

Amylin Pharmaceuticals, Inc. Financial Analysis Report 13

Total Current Assets 895,485 1,036,068 Property, plant and equipment, net 714,541 655,444 Other long-term assets 30,077 23,755 Debt issuance costs 10,264 11,786 Total Assets $1,650,367 $1,727,053 Source: Form 10-Q, 2009

Finally, Amylin’s top competitors’ (GlaxoSmithKline, Merck, and Novo Nordisk) assets

will be evaluated to facilitate an understanding of how the company’s assets stack-up relative to

its competition. All values (in millions of US Dollars) are taken from the consolidated balance

sheets of each of the companies’ most recent quarterly reports in order to reflect the most up-to-

date asset information.

Table 8: Amylin and Top Competitors Asset Comparison (June 30, 2009)

GlaxoSmithKline Merck Novo Nordisk

Amylin

06/30/09 06/30/09 06/30/09 06/30/09 Current Assets: Cash & cash equivalents $5,346.0 $12,457.6 $8,863.0 $111.272 Short-term investments 573.0 4,474.7 1,091.0 533.166 Accounts receivable, net 5,363.0 3,663.4 7,254.0 76.405 Inventories, net 3,910.0 2,155.3 9,900.0 109.803 Other current assets 2.0 - - 6.037 Total Current Assets 15,249.0 29,233.9 29,727.0 895.485 Property, plant and equipment, net 8,875.0 11,711.3 18,760.0 714.541 Other long-term assets 3,063.0 6,331.7 1,489.0 40.341 Total Assets $35,961.0 $49,407.1 $51,246.0 $1,650.367 Source: Business & Company Resource Center, 2009

Clearly, the value of Amylin’s assets (current and long-term) is significantly less than

those of its competitors. As aforementioned when differences in revenues were discussed,

Amylin is relatively young and small compared to its competition. This fact accounts for the

sharp contrast between the company’s assets and its top competitors’ assets.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 14

Growth Rate

Amylin continues to grow as a leader in diabetes research and development. In October

2008, the American Diabetic Association (ADA) and its European counterpart, the EASD,

updated guidelines regarding treatment for diabetes establishing BYETTA® (exenatide) as the

only approved secondary treatment option for diabetes type II (Amylin, 2009). In August 2008,

the Food and Drug Administration (FDA) updated a warning for BYETTA®, sighting a link

between the drug and pancreatitis. This resulted in fewer prescriptions of the drug in the second

half of 2008. However, it appears that this trend has stabilized, as Amylin sent out field

representatives to educate about the product's safety profile and prescribing recommendations

(Amylin, 2009). The decrease in prescriptions and product demand is likely the cause of net

sales dropping from $379,056,000 in the six months ending June 30, 2008 to $376,829,000

during the same period in 2009 (Amylin, 2009).

Amylin has also developed a new class of medication under the trade name SYMLIN®.

This medication also focuses on diabetes mellitus type I/II treated with insulin that has not met

glycemic goals. This product utilizes pre-filled pen injections to deliver simple fixed doses at

mealtimes (Amylin, 2009). Product sales in the first six months of 2009 ending June 30 were

$44 million, up from $43.1 million during the same period in 2008 (Amylin, 2009).

Overall, Amylin has experienced significant growth in individual product sales and total

revenues over the past several years. This growth over the past few years is highlighted in Table

9 below.

Table 9: Product Sales & Total Revenue Growth (2006-2008)

Year ended 12/31/08 Year ended 12/31/06 CAGR* BYETTA® sales $678.5M $430.2M 16.3% SYMLIN® sales 86.8M 43.8M 25.3% Net product sales 765.3M 474.0M 17.1% Total Revenues 840.109M 510.875M 17.8%

Amylin Pharmaceuticals, Inc. Financial Analysis Report 15

Source: Form 10-K, 2009 *CAGR=Compound Annual Growth Rate=[(Ending Value/Beginning Value)^(1/#of years)] – 1) Clearly there has been positive growth in sales and revenues for Amylin across the board,

with the most growth seen in product sales of SYMLIN®. However, despite these revenue

growths, Amylin has been unable to grow owner earnings. Investors have seen a dramatic

decrease in stock price over the past few years. As of August 31, 2009, the closing price of

Amylin common stock was $12.60. This is way down from $45.33, the closing price on August

31, 2006 (Yahoo! Finance, 2009). Lack of growth in stockholder wealth will be further

expressed in the financial statement analysis section.

Market Position

As aforementioned, Amylin Pharmaceuticals is a relatively small and young company in

the market. It also has only two products on the market, both for the treatment of diabetes. This

is in sharp contrast to industry leaders who have numerous drugs on the market, often times in

multiple different treatment areas. For example, a leading competitor, GlaxoSmithKline, has its

roots traced back to the 18th century and has over a hundred products on the market ranging from

prescription medications for treatment of osteoporosis to oral health care products (“Our history-

About GlaxoSmithKline,” 2009). Another large-cap company in the industry is Genzyme

Corporation. Genzyme has over twenty diverse products on the market and has been operating

since 1981 (“About Genzyme,” 2009).

While large-cap firms such as the two mentioned above obviously overshadow Amylin, it

is important to understand that they are the exception, rather than the rule. In the biotechnology

industry there are only about a dozen such large-cap companies. The numbers of smaller scale

firms significantly outweigh the number of large firms (Silver, 2009). In this light, it can be

concluded that while Amylin is not a big player in the industry, it is not uncommonly small.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 16

Company Strategy/Products

BYETTA®

Plans with BYETTA® include continued promotion of the product as the first and only

FDA approved product of its class and publicizing data reassuring patients and physicians of the

product safety (over one million users) when compared to other common diabetic medications

(Amylin, 2009). There will be continued emphasis of the ADA guidelines recommending

BYETTA® and continued collaboration with Eli Lilly for product commercialization.

Exenatide Once Weekly

Exenatide once weekly is in the advanced stages of research trials with promising data

and results. Patients have lower incidences of hypoglycemia (low blood sugar), even when used

in combination with other commonly prescribed diabetes medications (Amylin, 2009). The once

weekly administration of exenatide has shown an average 9.5 pound weight loss and lowered

A1C levels by 2% in trials (Amylin, 2009). If approved, this medication will be marketed as the

"opportunity to transform diabetes therapy" (Amylin, 2009). The clinical trials to date have met

FDA requirements to allow for a new drug application (NDA), and the NDA will be submitted

by the end of 2009.

Anticipating approval of once weekly exenatide, Amylin invested with Lilly and

Alkermes Inc. in a manufacturing facility in Ohio in 2008 with the ability to produce commercial

levels of the product ready for immediate distribution. This product will rely on the safety

profile of BYETTA® and unique value proposition to patients, doctors, and payers (Amylin,

2009).

Amylin Pharmaceuticals, Inc. Financial Analysis Report 17

SYMLIN®

Amylin intends to focus growth for the product SYMLIN® on the unmet needs of patients

on insulin who have not been able to meet therapy goals. The product has been used for four

years and assists with glucose fluctuations, weight loss, and over A1C reduction. It is 100%

wholly owned by Amylin and has been used by over 100,000 patients.

OBESITY

Amylin has appropriately identified obesity as a major contributor to diabetes and is

focusing efforts to educate health providers and patients as to the important relationship between

excessive weight and high blood sugar as well as the risks of cardiovascular disease associated

with these conditions. In the research and development pipeline, Amylin is focusing on the

peptides amylin and leptin, as they are related to appetite, saity, and weight management. A new

agent, davalintide, is in clinical trials for weight management (Amylin, 2009).

In response to the FDA warning on BYETTA®, Amylin carefully restructured its sales

force to specifically target medical doctors that write BYETTA® and SYMLIN® prescriptions.

This lead to an actual reduction in sales force, including managed care and the government

affairs sections of the organization. The workforce in San Diego was trimmed by 25%. Amylin

plans to continue to work with Eli Lilly to enhance effectiveness of the sales and marketing

organization. With continued surveillance of the changing marketplace, new products in

development, and anticipatory planning for once weekly exenatide with a commercial

production facility in place, Amylin anticipates positive cash flow by 2010 (Amylin Annual

Report, 2008).

Amylin Pharmaceuticals, Inc. Financial Analysis Report 18

Management and Corporate Culture

The following table represents the management team at Amylin Pharmaceuticals.

Table 10: Amylin Management Team

Daniel M. Bradbury

President and Chief Executive Officer

Mark G. Foletta

Senior VP, Finance and Chief Financial Officer

Mark J. Gergen

Senior VP, Corporate Development

Orville G. Kolterman, MD

Senior VP, Research & Development

Marcela B. Lloyd

Senior VP, Government & Corporate Affairs and General Counsel

Roger Marchetti

Senior VP, Human Resources & Information Management

Paul Marshall

Senior VP, Operations

Vincent P. Mihalik Senior VP, Sales & Marketing and Chief Commercial Officer Source: Amylin, 2009

This leadership team is diverse with individuals from recognized pharmaceutical

companies, medical doctors, and expert researchers. This diversity reflects an important part of

Amylin’s corporate culture. Furthermore, the workplace and corporate culture values

“commitment and talent, and a fast-paced, stimulating environment that encourages creativity,

open-mindedness, collaboration and results” (Amylin, 2009). In particular, with a high value

placed on collaboration, and management’s understanding of the benefits received from it,

Amylin has entered into strategic alliances with Eli Lilly and Company, Alkermes, Inc., and

Psylin Neurosciences, Inc. See the next section for a brief overview of these strategic

partnerships.

Amylin also embraces community responsibility through scholarships, internships, and

grants. Moreover, the company embraces LEED (Leadership in Energy and Environmental

Amylin Pharmaceuticals, Inc. Financial Analysis Report 19

Design) Green Buildings for its California locations and the Ohio plant. Employees of Amylin

have won several awards for environmental care and management (Amylin, 2009).

Strategic Partnerships

Table 11 provides a concise outline of the three strategic collaborations that Amylin has

entered into.

Table 11: Outline of Strategic Collaborations

Partnering Company Nature/Purpose of Partnership Eli Lilly and Company • Collaboration on development of exenatide (since 2002)

• Has led to successful commercialization of BYETTA (exenatide) injection

• Shared commercialization efforts/costs of BYETTA in US; foreign commercialization efforts & costs are responsibility of Lilly

• Currently working on development of exenatide once weekly

Alkermes, Inc. • Worked together on development of exenatide once weekly

• Continue to work on prospective long-acting forms of exenatide

Psylin Neurosciences, Inc. • Formed out of venture between Amylin & PsychoGenics Inc. in January 2007

• Will “evaluate the potential of peptide hormones as novel therapeutic approaches to psychiatric disorders”

Source: Amylin, 2009 Collaborative efforts with these companies promote the development of novel therapeutic

medications to better assist target patients.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 20

MARKET OUTLOOK

General Overview

Securities exchanges are the marketplaces where stocks are traded. The New York Stock

Exchange (NYSE) is the most famous and lists more than 3,000 common and preferred stocks

(Boone & Kurtz, 2007). The NYSE has a trading floor in an open auction fashion for stocks that

meet the listing requirements.

The National Association of Securities Dealers Automated Quotations (NASDAQ)

System is a computerized network that links member investment firms (Brigham & Ehrhardt,

2008). While the NYSE occupies a physical place, all trading on the NASDAQ takes place on

the NASDAQ intranet. There are approximately 5,000 stocks traded on the NASDAQ, many of

these being technology company listings and smaller, less well known companies that do not

meet criteria for listing on the NYSE. Amylin has had its stock traded on the NASDAQ (under

the ticker symbol AMLN) since its initial public offering (IPO) in 1992 (Funding Universe,

2005).

In addition to the two aforementioned stock markets, there is the American Stock

Exchange and various regional stock exchanges; however, daily trading volume on these other

stock markets is minimal when compared to the NYSE and NASDAQ.

The securities markets are regulated by the Securities and Exchange Commission (SEC),

which was created in 1934. It is the principal federal overseer of the securities markets and

carries the responsibility of administering securities laws and protecting investors in public

securities transactions. The SEC requires that all new public issues of corporate securities be

registered. Securities laws also require public corporations to issue an annual report called a 10-

K form with the SEC. Moreover, these public corporations must submit reports each time there

Amylin Pharmaceuticals, Inc. Financial Analysis Report 21

is a change in company officers, whenever stock is bought or sold directors, and if there is an

investor that accumulates more than 5% of the company's outstanding stock (Boone & Kurtz,

2007).

Historical Performance

The general performance of the different securities markets are described by the Dow

Jones Industrial Average. It is an index that shows how publicly traded companies have traded

during a session and is considered a gauge of economic activity (Boone & Kurtz, 2007). The

Standard and Poor's (S&P) 500 Index is also used as a stock market indicator. These

performance indices historically fluctuate with economic variables that affect businesses, banks,

and consumers. Most company securities are compared to these indices to assist investors in the

evaluation of their stock purchases with a given company. Historically, the Dow Jones Industrial

Average and the S&P 500 have fluctuated and have had ups and downs. These fluctuations are

due to the rising and falling of the prices of the pooled stocks that make up the indices. To

understand why stock prices are subject to such instability, it is important to remember the basic

fact that it is expectations over the future course of a company’s earnings and the economy that

lead an investor to sell or buy stock. And of course it is the selling and buying (supply and

demand) of the stock that determine its price. Every day, new information is disseminated

through the market which changes investors’ expectations about the future of either the company

or the economy, or both. The changing outlook in turn causes supply and demand for various

stocks to fluctuate. Thus, in a free market such as that of the U.S., the market will always be

fluctuating. Figure 1 below illustrates the performance of Dow Jones Industrial Average (^DJI),

the S&P 500 Index (^GSPC), and the NASDAQ Composite Index (^IXIC) over the past ten

Amylin Pharmaceuticals, Inc. Financial Analysis Report 22

years in terms of price (or value). Collectively viewing the activity of these three key indices

provides a fair understanding of the overall market’s performance.

Figure 1: Historical Performance of Major Market Indices

Source: Yahoo! Finance, 2009

As is evident by the figure above, the market has had its highs and lows over the past

decade. In this time frame, the market was at its highest performance in late 1999 to early 2000

and at its lowest in late 2008 to early 2009 (not surprising given the deep economic recession we

were in).

Amylin Pharmaceuticals, Inc. Financial Analysis Report 23

Future Outlook

The stock market in the past year has experienced extreme volatility. To date, the

economy has been stagnant with various economic changes made to assist with improving the

current conditions. These changes have included lowered interest rates, "Cash for Clunkers,”

various government bailouts, financial institution re-structuring, credit card law changes,

mortgage refinances, etc. The results of these activities have yet to be seen and their outcome

remains uncertain.

The market has seen significant improvements over the past seven months, and the

market is generally expected to improve as the economy recovers. An article posted on

CNNMoney.com on November 2, 2009 stated that, “The first and second quarters of next year

are expected to move toward a more moderate rate of growth, rising 37.6% and 20.9%

respectively” (Twin, 2009). So much of the market performance outlook hinges upon how

quickly the economy recovers. Different analysts have different opinions as to the speed and

strength of recovery, making predictions about the near future market performance challenging.

However, it seems that the general consensus is that the market will be experiencing moderate

growth over the next few years.

INDUSTRY OUTLOOK Nature of the Industry

Amylin Pharmaceuticals, Inc. operates in the biotechnology industry. According to

Standard & Poor’s (S&P’s) survey on the industry, “Biotechnology refers to the application of

biological and biochemical science to large-scale production of products to modify human

health, food supplies, or the environment” (Silver, 2009, 19). While many of the fundamental

Amylin Pharmaceuticals, Inc. Financial Analysis Report 24

foundations of the industry can be traced back thousands of years (i.e. the use of living

organisms such as bacteria and fungus to process foods and beverages), pioneering research in

genetics and molecular biology in recent years has resulted in significant advances for the

industry. Such industry advances and innovations have typically focused on treatment in the

following areas: cancer, infectious diseases (such as HIV and AIDS), auto-immune disorders,

osteoporosis and diabetes. Into the future, it is expected that the industry will continue to

develop and produce cutting-edge drugs in these particular areas. Other advances in areas such

as stem-cell research and human cloning face a more turbulent future due to public and political

opposition. The industry currently faces, and will continue to face, many developmental

obstacles in such areas. However, the biotechnology industry is no stranger to challenges and

obstacles. The industry is highly regulated and vulnerable to legal and political conditions.

Because this is such a major element of the nature of the industry, it merits a brief discussion.

The U.S. Food and Drug Administration (FDA) is the primary overseer of this industry

and are responsible for drug approvals and management of drug safety. The regulatory process

for new drugs is extremely costly and time consuming and represents a critical hurdle that all

potential new products in the industry must pass. Many products fail to get approval from the

FDA, resulting in significant losses for the developing company. Unfortunately, a number of

factors are making FDA approval even more difficult for this industry. First and foremost, the

FDA is inundated with petitions for new product approvals, yet they lack funding and resources

to meet this demand. As a result, the administration often misses deadlines, lengthening the time

for new drug approvals. Moreover, elevated safety concerns are slowing the process due to new

and more guidelines and extended clinical studies. Essentially, it is important to understand here

Amylin Pharmaceuticals, Inc. Financial Analysis Report 25

that the FDA plays a critical role in this industry, and the heavy regulations make for a

challenging industry climate in which significant losses are common.

Extraordinary costs are another aspect of the biotech industry that is inherent in its nature.

Most of these costs arise throughout a drug’s discovery and development process. Typically, this

process consists of the following steps: early discovery, preclinical development, clinical trials,

and regulatory filing and review. A 2006 study conducted by Tufts Center for the Study of Drug

Development estimated that the average cost to develop a new drug in this industry is about $1.2

billion dollars. For small, young biotech firms, this is particularly challenging. These firms

depend heavily on funds from private, wealthy investors, small groups of investors, and venture

capitalists. These high costs also make partnerships critical (and common) in this industry.

Smaller firms join together with larger firms to benefit from shared expenditures. Often times

the larger firms have deep pockets that enable them to cover up-front fees for the smaller firms

as well as provide research and development (R&D) funding. Moreover, these larger companies

typically have greater manufacturing capabilities that the smaller companies can benefit from.

Funding for R&D is perhaps one of the most critical ways that larger companies can help smaller

ones because R&D is very much the backbone of the industry. R&D is necessary in this industry

to stay competitive and for the development of innovative new drugs. Its importance is

supported by the fact that R&D spending as a percentage of revenues in the industry is among

the highest of any U.S. industry. According to Ernst & Young LLP, U.S. public biotech

companies spent approximately $25.3 billion (47% of product sales) on R&D in 2008, compared

to $21 billion (48%) in 2007.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 26

A final point to be made about the nature of the biotechnology industry is that it is very

volatile. Some of the issues discussed above contribute to its volatility, while other reasons will

be addressed in the later section on industry opportunities and threats.

Industry Composition

The biotechnology industry is composed of numerous companies varying in size from

small start-ups to multibillion-dollar firms. There are relatively few multibillion-dollar firms in

the industry, yet these industry leaders (i.e. Amgen Inc., Biogen Idec Inc., Celgene Corp.,

Genzyme Corp., etc.) account for the bulk of industry revenues, profits, and market

capitalization. Moreover, there is a downtrend in the number of large-cap companies due to

industry consolidation. In fact, consolidation through mergers and acquisitions (M&A) is the

name of the game in this industry. This is reflected in the recent decrease in the number of

biotech-related, publicly traded companies in the U.S. There are approximately 350 of these

companies currently trading, versus about 380 in 2008 (Silver, 2009). Bankruptcies and the

absence of initial public offerings since 2008 have also contributed to this trend.

Industry Growth

Industry growth is believed to be slowing; however, evidence still shows overall growth.

“According to BioPharm Insight, a newsletter that focuses on the life sciences business,

biotechs accounted for 42% of preclinical candidates and 26% of submissions for US marketing

approval in 2007 (latest available), up from 34% and 18%, respectively, in 2006” (Silver, 2009,

11). Moreover, it is expected that 50% of the top 100 drugs in 2014 will be biotech drugs.

According to Ernst and Young, industry product sales grew from $52.7 billion in 2007 to

$57.0 billion in 2008, representing an 8.2% change. Revenues grew slightly less (8.0%), from

$64.9 billion in 2007 to $70.1 billion in 2008 (Silver, 2009).

Amylin Pharmaceuticals, Inc. Financial Analysis Report 27

Growth prospects remain positive for this industry in part because industry demand is

predominantly linked to the population’s health, rather than to economic cycles. An aging

population, an increase in average life-expectancy, and the mounting cases of chronic disease all

point to increased demand for biotech drugs (Silver, 2009). A growing market will likely

translate into growth for the industry if companies can continue to develop and produce

innovative, safe, and effective new drugs.

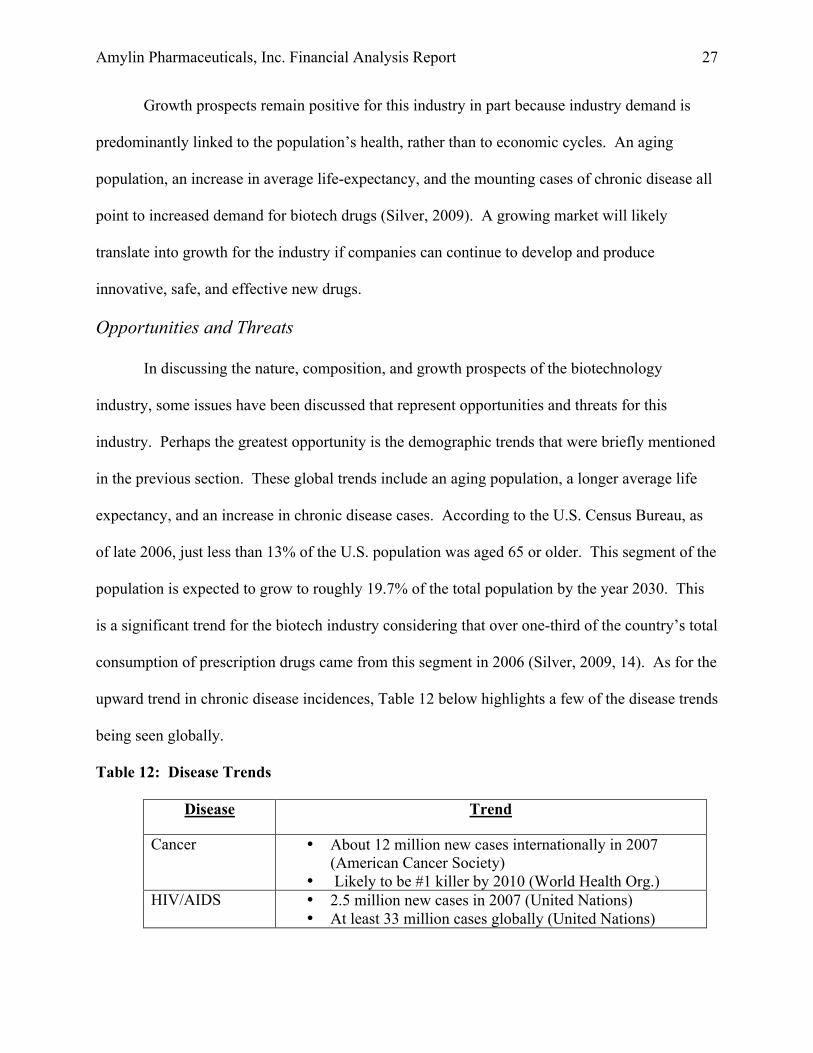

Opportunities and Threats

In discussing the nature, composition, and growth prospects of the biotechnology

industry, some issues have been discussed that represent opportunities and threats for this

industry. Perhaps the greatest opportunity is the demographic trends that were briefly mentioned

in the previous section. These global trends include an aging population, a longer average life

expectancy, and an increase in chronic disease cases. According to the U.S. Census Bureau, as

of late 2006, just less than 13% of the U.S. population was aged 65 or older. This segment of the

population is expected to grow to roughly 19.7% of the total population by the year 2030. This

is a significant trend for the biotech industry considering that over one-third of the country’s total

consumption of prescription drugs came from this segment in 2006 (Silver, 2009, 14). As for the

upward trend in chronic disease incidences, Table 12 below highlights a few of the disease trends

being seen globally.

Table 12: Disease Trends

Disease Trend

Cancer • About 12 million new cases internationally in 2007 (American Cancer Society)

• Likely to be #1 killer by 2010 (World Health Org.) HIV/AIDS • 2.5 million new cases in 2007 (United Nations)

• At least 33 million cases globally (United Nations)

Amylin Pharmaceuticals, Inc. Financial Analysis Report 28

Hepatitis C • 170 million people in the world are infected (Hepatitis Foundation International)

• Market for treatment of the disease likely to grow from $2 billion in 2008 to about $8 billion in 2013 (Decision Resources, a pharmaceutical industry research advisory firm)

Diabetes • Approximately 24 million cases exist in the U.S. (The American Diabetes Association)

• U.S. diabetic population is likely to grow by almost 50% by the year 2020 (The American Diabetes Association)

Source: Silver, 2009, pp.15-18

Of course these are just a few of the many chronic diseases plaguing the global

population; however, they do represent some of the most serious epidemics. While these trends

are distressing, they do represent opportunities for growth for the biotech industry.

Another opportunity in this industry is the recent merger and acquisition (M&A) activity,

which is expected to continue. For the large-cap companies in the industry, merging or acquiring

a smaller firm represents an opportunity to expand into new areas of treatments and therapies and

can help build its product portfolio. For some small firms in the industry who are struggling to

stay afloat and cannot receive enough capital, this vigorous M&A activity represents an

opportunity to avoid bankruptcy. However, this escalating number of mergers and acquisitions

may represent a threat to some. In particular, small firms that can manage on their own and

choose not to merge with or be acquired by a larger firm will find it increasingly difficult to

compete with the ever growing large-cap companies.

More obvious and critical threats facing the biotech industry include the following, each

of which have already been briefly addressed.

• Health care reform putting greater pressure on prescription drug pricing

• Health care reform making the entry of generic drugs easier (representing increased competition for the biotech industry)

• Health care reform encouraging the performance of comparative effectiveness

studies

Amylin Pharmaceuticals, Inc. Financial Analysis Report 29

• Political and regulatory uncertainty (refer to previous discussion of FDA

problems) • Current economic conditions are making it very difficult for firms to receive

necessary capital (particularly troubling for smaller firms); as a result, companies are reducing their R&D expenditures, and some small firms are going bankrupt.

• Many large firms are centering R&D on fewer therapies, rather than looking to

expand into new therapies. This limits smaller firms’ chances for partnership with them.

• An arduous and costly approval process for new drugs and therapies (see

discussion on FDA problems).

These threats should be a concern to all companies operating in the biotechnology

industry. Yet, some should be more concerned than others. Most large-cap firms are likely to

overcome these barriers and challenges due to their size and abundant resources; on the other

hand, many of the smaller companies (which represent a greater proportion of the industry) will

struggle greatly, and many may not survive.

Future Outlook

The overall future outlook of the biotechnology industry is positive. There is ample room

for companies to grow as demand is expected to increase, given the global demographic trends

aforementioned. In this industry, an individual company’s future success will depend on the

following:

• Its investment in R&D • Its product pipeline • Its ability to develop patentable products (and to obtain those patents) • The quality of its management and scientific teams • Its effective use of alliances • How well it works with the FDA and complies with regulatory requirements • Its ability to generate adequate funding

Finally, continued industry consolidation (due to the M&A activity) will presumably lead

to an industry that is run by a small number of very large firms, while most of the smaller firms

Amylin Pharmaceuticals, Inc. Financial Analysis Report 30

will be weeded out. Moreover, because this M&A activity is not isolated within the industry, but

is also occurring between this industry and the pharmaceutical industry, the distinction between

the two industries will be increasingly blurred.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 31

FINANCIAL STATEMENT ANALYSIS

Figure 2: Income Statement (2006-2008)

Amylin Pharmaceuticals, Inc. Consolidated Income Statements (Years 2006-2008)

(in thousands, except per share data) Year ended December 31, 2008 2007 2006 Revenues:

Net Product Sales $ 765,342 $ 701,450 $ 474,038 Revenues under collaborative agreements 74,767 79,547 36,837

Total Revenues 840,109 780,997 510,875 Costs and expenses:

Costs of goods sold 91,596 65,457 50,073 Selling, general, and administrative 395,112 390,982 281,950 Research and development 293,095 276,600 222,053 Collaborative profit-sharing 302,600 290,934 194,191 Restructuring 54,926 — —

Total costs and expenses

(1,137,329)

(1,023,973) (748,267) Operating loss (297,220) (242,976) (237,392) Make-whole payment on debt redemption — — (7,875) Interest and other income 26,561 46,969 34,903 interest and other expense (29,803) (15,129) (8,492) Loss on impairment of investments (14,943) — —

Net loss $ (315,405.00) $(211,136.00) $ (218,856.00)

Net loss per share--basic & diluted $ (2.30) $ (1.59) $ (1.78) Shares used in computing net loss per share, basic & diluted 137,006 132,621 122,647

Amylin Pharmaceuticals, Inc. Financial Analysis Report 32

Figure 3: Common Size Income Statement (2006-2008)

Amylin Pharmaceuticals, Inc. Common Size Income Statements (Years 2006-2008)

Year ended December 31, 2008 2007 2006 Revenues:

Net Product Sales 91.10% 89.81% 92.79% Revenues under collaborative agreements 8.90% 10.19% 7.21%

Total Revenues 100% 100% 100% Costs and expenses:

Costs of goods sold 10.90% 8.38% 9.80% Selling, general, and administrative 47.03% 50.06% 55.19% Research and development 34.89% 35.42% 43.47% Collaborative profit-sharing 36.02% 37.25% 38.01% Restructuring 6.54% — —

Total costs and expenses -135.38% -131.11% -146.47% Operating loss -35.38% -31.11% -46.47% Make-whole payment on debt redemption — — -1.54% Interest and other income 3.16% 6.01% 6.83% interest and other expense -3.55% -1.94% -1.66% Loss on impairment of investments -1.78% — — Net loss -37.54% -27.03% -42.84%

Amylin Pharmaceuticals, Inc. Financial Analysis Report 33

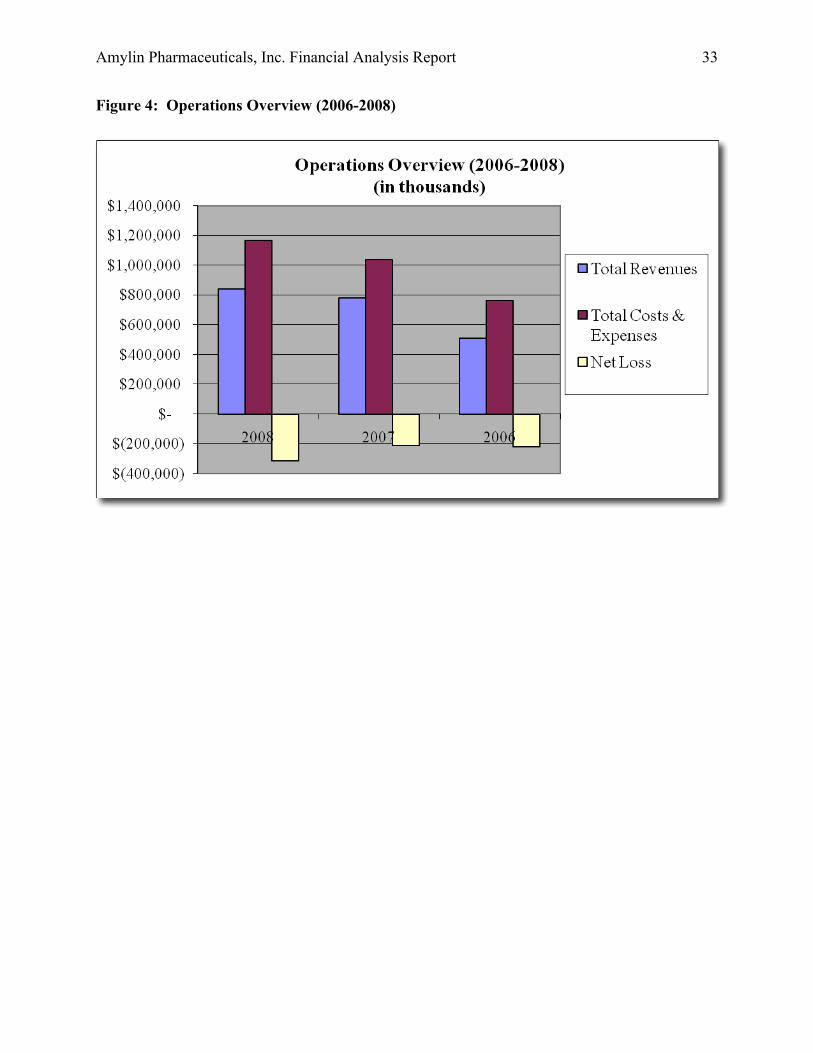

Figure 4: Operations Overview (2006-2008)

Amylin Pharmaceuticals, Inc. Financial Analysis Report 34

Figure 5: Balance Sheet (2006-2008)

Amylin Pharmaceuticals, Inc.

Consolidated Balance Sheets (Years 2006-2008) (in thousands, except per share data)

December 31, 2008 2007 2006 ASSETS Current assets:

Cash and cash equivalents $ 237,263 $ 422,232 $ 66,640 Short-term investments 579,575 708,183 700,691 Accounts receivable, net 62,369 73,579 58,089 Inventories, net 115,823 100,214 59,299 Other current assets 41,038 32,100 22,098

Total current assets 1,036,068 1,336,308 906,817 Property, plant and equipment, net 636,922 390,301 146,779 Other long-term assets 23,755 28,082 2,870 Debt issuance costs 15,884 19,520 3,920

Total Assets $1,712,629 $ 1,774,211 $1,060,386

LIABILITIES AND EQUITY Current liabilities:

Accounts payable $ 39,467 $ 37,530 $ 36,834 Accrued compensation 65,145 56,428 39,251 Payable to collaborative partner 60,470 66,116 52,338 Other current liabilities 90,125 122,924 71,178 Restructuring liability, current portion 24,235 — — Notes payable, current portion 31,250 — — Deferred revenue, current portion 3,086 4,286 4,286

Total current liabilities 313,778 287,284 203,887 Deferred revenue, net of current portion — 3,086 7,372 Long-term deferred credit 125,000 — — Restructuring liability, net of current portion 22,503 — — Other long-term obligations, net of current portion 31,724 31,023 13,836 Notes payable, net of current portion 93,750 125,000 — Convertible senior notes 775,000 775,000 200,000 Stockholders' equity:

Common stock, $.001 par value, 450,000 shares, 137,623 & 135,044 issued & outstanding at Dec. 31, 2008 & 2007 138 135 130

Additional paid-in capital 2,111,473 1,987,453 1,857,194 Accumulated deficit (1,749,725) (1,434,320) (1,223,184) Accumulated other comprehensive loss (11,012) (450) (1,151)

Total stockholders' equity 350,874 552,818 635,291

Total Liabilities and Stockholder's Equity

$1,712,629 $ 1,774,211 $1,060,386

Amylin Pharmaceuticals, Inc. Financial Analysis Report 35

Figure 6: Common Size Balance Sheet (2006-2008)

Amylin Pharmaceuticals, Inc. Common Sized Balance Sheets (Years 2006-2008)

December 31, 2008 2007 2006 ASSETS Current assets:

Cash and cash equivalents 13.85% 23.80% 6.28% Short-term investments 33.84% 39.92% 66.08% Accounts receivable, net 3.64% 4.15% 5.48% Inventories, net 6.76% 5.65% 5.59% Other current assets 2.40% 1.81% 2.08%

Total current assets 60.50% 75.32% 85.52% Property, plant and equipment, net 37.19% 22.00% 13.84% Other long-term assets 1.39% 1.58% 0.27% Debt issuance costs 0.93% 1.10% 0.37% Total Assets 100% 100% 100% LIABILITIES AND EQUITY Current liabilities:

Accounts payable 2.30% 2.12% 3.47% Accrued compensation 3.80% 3.18% 3.70% Payable to collaborative partner 3.53% 3.73% 4.94% Other current liabilities 5.26% 6.93% 6.71% Restructuring liability, current portion 1.42% — — Notes payable, current portion 1.82% — — Deferred revenue, current portion 0.18% 0.24% 0.40%

Total current liabilities 18.32% 16.19% 19.23% Deferred revenue, net of current portion — 0.17% 0.70% Long-term deferred credit 7.30% — — Restructuring liability, net of current portion 1.31% — — Other long-term obligations, net of current portion 1.85% 1.75% 1.30% Notes payable, net of current portion 5.47% 7.05% — Convertible senior notes 45.25% 43.68% 18.86% Stockholders' equity:

Common stock, $.001 par value, 450,000 shares authorized, 137,623 & 135,044 issued & outstanding at December 31, 2008 & 2007 0.0% 0.01% 0.01% Additional paid-in capital 123.29% 112.02% 175.14% Accumulated deficit -102.17% — — Accumulated other comprehensive loss — — 0.01%

Total stockholders' equity 20.49% 31.16% 59.91% Total Liabilities and Stockholder's Equity 100% 100% 100%

Amylin Pharmaceuticals, Inc. Financial Analysis Report 36

Figure 7: Asset Structure

Figure 8: Liability & Equity Structure (2006-2008)

Amylin Pharmaceuticals, Inc. Financial Analysis Report 37

Figure 9: Statement of Cash Flows (2006-2008)

Amylin Pharmaceuticals, Inc. Consolidated Statements of Cash Flows

(in thousands) Years ended December 31, 2008 2007 2006 OPERATING ACTIVITIES: Net loss $(315,405) $(211,136) $ (218,856) Adjustments to reconcile net loss to net cash used in operating activities:

Depreciation and amortization 33,348 21,563 16,228 Stock-settled compensation accruals 25,109 21,696 5,869 Employee stock-based compensation 55,115 59,064 51,838 Loss on impairment of investments 14,943 — —

Restructuring (including $786 of employee stock-based compensation) 9,483 — —

Make-whole payment on debt redemption — — 7,875 Other non-cash expenses 5,718 3,028 1,247

Changes in operating assets and liabilities: Accounts receivable, net 11,210 (15,490) (32,389) Inventories, net (15,609) (40,915) (32,549) Other current assets (13,005) (10,016) (3,995) Accounts payable and accrued liabilities 8,641 28,101 38,293 Accrued compensation 4,888 1,300 7,071 Payable to collaborative partner (5,646) 13,778 35,660 Deferred revenue 111,498 (4,286) (4,286) Deferred collaborative profit sharing 9,216 — — Restructuring liabilities 46,738 — — Other assets and liabilities, net (5,752) 8,153 1,987

Net cash used in operating activities (19,510) (125,160) (126,007) INVESTING ACTIVITIES: Purchases of short-term investments (1,015,811) (392,155) (714,772) Sales and maturities of short-term investments 1,132,017 383,076 386,840 Purchases of property, plant and equipment (295,060) (268,674) (97,925) Increase in other long-term assets (3,299) (18,348) (33) Net cash used in investing activities (182,153) (296,101) (425,890) FINANCING ACTIVITIES: Proceeds from issuance of common stock, net 16,694 64,687 546,511 Proceeds from issuance of convertible debt, net — 558,670 —

Amylin Pharmaceuticals, Inc. Financial Analysis Report 38

Proceeds from long-term note payable — 123,496 — Proceeds from contingent share settled obligation — 30,000 — Principal payments on capital leases — — — Net cash provided by financing activities 16,694 776,853 546,511 Increase (decrease) in cash and cash equivalents (184,969) 355,592 (5,386) Cash and cash equivalents at beginning of year 422,232 66,640 72,026 Cash and cash equivalents at end of year $ 237,263 $ 422,232 $ 66,640 Supplemental disclosures of cash flow information: Interest paid, net of interest capitalized $ 17,701 $ 9,477 $ 6,409 Interest capitalized $ 11,867 $ 4,483 $ 560 Property, plant & equipment additions in other current liabilities at year end $ 6,057 $ 15,559 $ 21,219 Common stock issued upon conversion of senior convertible notes — — $ 175,000

Reclassification of debt issuance costs to additional paid-in capital upon conversion of convertible senior notes — — $ 1,980 Non-cash financing activities: Issuance of common stock upon milestone conversion $ 30,000 — — Shares contributed as employer 401(k) match $ 4,284 $ 2,811

Issuance of common stock for employee stock ownership plan $ 16,996 — —

Amylin Pharmaceuticals, Inc. Financial Analysis Report 39

Figure 10: Cash Flow Balances (2006-2008)

Figure 11: Cash Flow by Activity (2006-2008)

Amylin Pharmaceuticals, Inc. Financial Analysis Report 40

Cash Flow Analysis

An evaluation of cash flows is a critical step in gauging a company’s financial health. As

the name implies, a cash flow is a flow of cash either out of or into a company. These cash flows

are reflected on the statement of cash flows, which shows how a company raised and spent funds

over a given period of time (investopedia.com). When assessing a company, it is often tempting

to focus on the net income reported on the income statement to determine if a company is

profitable or not. This can be very misleading and is subject to manipulation with different

accounting methods. However, cash either exists or does not on the cash flow statements.

Perhaps most importantly, cash is used to maintain a company and to determine whether a

company has enough liquidity to maintain the business and meet its financial obligations. This is

the ultimate measure of potential success or failure.

There are three principal parts of a cash flow statement: cash flows from operations, cash

flows from investment activities, and cash flows from financing activities (Marshall &

McManus, 2007). Cash flow from operations is the key source of cash generation; it is the

primary source of money made by the company from production, as opposed to funds from

outside investors and other financial activities (investopedia.com). The cash flow from investing

activities usually demonstrates an outflow of cash. Investments such as property, plant and

equipment as well as business acquisitions are listed here. Noting capital expenditures is very

relevant, as it is a priority for a business to maintain equipment, plants, et cetera for efficient

operations. The third section is the cash flows from financing. This part shows debt and equity

transactions, as most businesses are constantly borrowing and paying off debt. For investors, a

key item for stock issues is the cash dividends paid (investopedia.com).

Amylin Pharmaceuticals, Inc. Financial Analysis Report 41

The reported financial statements (balance sheet, income statement, and statement of cash

flows) all provide pieces of data that explain a company’s financial position. An analysis of the

cash flows year to year, as well as reviewing certain relevant data from the balance and income

statements, can provide insight into where a company has placed funds, if there is enough

liquidity, how well the business is managed, and if it “measures up” to companies with similar

profiles.

On initial evaluation of Amylin’s cash flow statement, an immediate observation is made.

The net cash used from operating activities is -$19,510,000, yet the net loss is -$315,405,000.

This bears further investigation. Where did the rest of the money go? The following ratio

analyses should provide useful information for answering this question. The operating cash flow

ratio (OCF) provides information as to how well current liabilities are covered by the cash flows

from company operations (investopedia.com). The formula is: OCF = cash flow from current

operations/current liability. For Amylin this is -0.0621 (-19.51/313.778). Typically a number

greater than 1.0 indicates that a company has enough cash flows from operations to cover

expenses. This ratio is one of several tools to evaluate the financial strength of a company.

Comparing a very similar company to Amylin is also beneficial. The company used in this

section for comparison is The Medicines Company (MDCO). Also a bio/pharmaceutical

company with two primary products and traded on the NASDAQ, The Medicines Company is

similar in industry, size, number of products, and research endeavors. The calculated OCF for

The Medicines Company is 0.4260, less than 1.0 but not a negative number. For both

companies, current liabilities may not be covered by the cash flows from current operations.

This appears to be especially concerning for Amylin.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 42

Another ratio is termed flow ratio (fool.com). This ratio compares year to year changes

in cash flows to obtain a sense of improvement/worsening of cash utilization. The formula is:

(current assets - cash + market securities)/current liabilities - short term debt. In 2008, Amylin’s

flow ratio was 0.775 (1036.068 - 816.836/313.778 – 31.25). In 2007, the ratio was 0.716,

indicating an increase in the cash flow ratio. This rising ratio indicates a cash drain on the

company. This is also concerning for Amylin because it represents poor cash management.

The cash flow statement portion regarding investments for Amylin is of particular

interest. Upon review it is apparent that Amylin has been placing significant resources in short

term investments as well as focusing on property, plant, and equipment. This is verified by

reviewing the SEC 10K report filed by Amylin citing the purchase and construction of a

manufacturing and research facility in Ohio (Amylin, 2009). Amylin appears to have

concentrated on raising cash through sales of stock options in the years 2006-2008, as evidenced

by the financing activities section.

When evaluating the cash flow statement and trying to determine where the money has

been utilized between the cash from operating activities and the net loss, the income statement

for Amylin provides information suggested by the ratio analysis as well. The income statement

for 2008 lists selling, general, and administrative (SG&A) expenses at $395.112 million, and a

comparison to The Medicines Company lists SG&A expenses at $164.903 million. Amylin

simply lists these costs as “increased expenses” in its 2008 annual report.

In summary, the cash flow analysis of Amylin provides concerning data that suggests

poor financial management by its leadership and questionable investment in property, plant and

equipment. The investment in the new Ohio facility is especially concerning considering the

company may not even obtain FDA approval for its anticipated long acting product.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 43

Financial Ratio Analysis

When analyzing a company’s financial statements, whether as an investor or as a

manager, an ideal place to start is with financial ratios. Each of these ratios fall into one of the

following five categories: liquidity, asset management, debt management, profitability, or

market value ratios. We will utilize these ratios to begin our analysis of the financial

performance of Amylin Pharmaceuticals over the past three years. We will then proceed into an

evaluation of the company’s common size statements and cash flow statements.

Liquidity Ratios

As the name implies, liquidity ratios help to determine the liquidity of a company’s

assets. As defined in Financial Management: Theory and Practice, “a liquid asset is one that

trades in an active market and hence can be quickly converted to cash at the going market price”

(Brigham & Ehrhardt, 2008, p. 123). Essentially, these ratios assist in answering this question:

“Will the firm be able to pay off its debts as they come due over the next year or so?” (Brigham

& Ehrhardt, 2008, p. 123).

Current Ratio [Formula: Current assets/Current liabilities] The current ratio is used to determine if the company is able to pay-off its short-term

financial obligations (debt and payables) using its short term assets (cash, inventory, &

receivables). A ratio of 1 or greater indicates that the company would be able to meet all of its

current financial obligations given its current assets. Moreover, the higher the ratio, the higher

the firm’s ability to pay-off its short-term liabilities. Generally speaking, the higher the current

ratio, the better; however, one must realize that a very high current ratio could also suggest that

too much is invested in current assets. Amylin’s calculated current ratios for the years 2006

through 2008 are as follows.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 44

2008 2007 2006 3.30 4.65 4.45

As the above ratios indicate, Amylin had the ability to pay off its current liabilities using

its current assets 3.3 times over in 2008. Likewise, the company was able to do so 4.65 times

over and 4.45 times over in 2007 and 2006, respectively. Theses current ratios are adequate, but

a drop is seen from 2007 to 2008. This is most likely due to decreased sales at the end of 2008.

Amylin appears to be fairly liquid.

Quick Ratio [Formula: (Current assets-inventory)/Current liabilities] The quick ratio (also known as the acid-test ratio), is very similar to the current ratio, and

it essentially measures the same thing. However, with the quick ratio, inventories have been

subtracted from current assets. Some believe this provides a more accurate gauge of a firm’s

liquidity because inventory is usually the least liquid current asset (Brigham & Ehrhardt, 2008, p.

126).

2008 2007 2006 2.93 4.30 4.16

In 2008, Amylin had the ability to pay-off its current liabilities using its current assets

(excluding inventories) 2.93 times over. In 2007 and 2006, they were able to do so 4.3 times

over and 4.16 times over, respectively. Again, one can determine that Amylin is fairly liquid and

has the ability to meet its’ short-term financial obligations. Because there was not a significant

drop between the current ratio and the quick ratio, another observation can be made: inventories

do not count for a significant portion of Amylin’s current assets.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 45

Asset Management Ratios

Using asset management ratios, one can determine how effectively the firm is managing

its assets. This set of ratios help to answer this question: “Does the total amount of each type of

asset as reported on the balance sheet seem reasonable, too high, or too low in view of current

and projected sales levels?” (Brigham & Ehrhardt, 2008, p. 126). Generally speaking, does the

firm have the right amount invested in assets?

Inventory Turnover [Formula: Sales/Inventory]

This ratio refers to how quickly product is moved in relation to sales, and the higher the

number the better (Brigham & Ehrhardt, 2008, pp. 126-127). Specifically, inventory turnover

measures how many times a firm’s inventory is sold and replenished over a period.

2008 2007 2006 6.61 7.00 7.99

In 2008, Amylin sold and replaced its inventory 6.61 times. In 2007 and 2006, the

company sold and replaced its inventory 7 and 7.99 times, respectively. It is a clear that there

has been a negative trend. Normally this can suggest a decrease in sales, but Amylin’s income

statement shows an increase in sales. Thus, it is assumed that Amylin has become less effective

in purchasing the right amount of inventories, given its sales.

Days Sales Outstanding (DSO) [Formula: Receivables/(Annual sales/365)] Days sales outstanding is sometimes referred to as “average collection period.” By

comparing accounts receivables to average daily sales, this ratio shows how long it takes to

collect accounts receivables, or how many days between the time a sale is made and the time a

Amylin Pharmaceuticals, Inc. Financial Analysis Report 46

firm receives cash from that sale (Brigham & Ehrhardt, 2008, p. 127). The lower this ratio is the

better.

2008 2007 2006 29.74 38.29 44.73

In 2008, it took Amylin 29.74 days to collect its accounts receivables. In other words,

there was, on average, about a one month gap between the time a sale was made and the time

Amylin received cash from the sale. This is very good, and suggests that Amylin is efficient in

managing its accounts receivables. Moreover, a downward trend can be observed from the years

2006 to 2008, indicating that the company has improved.

Fixed Assets Turnover [Formula: Sales/Net fixed assets] The fixed assets turnover ratio evaluates how effectively a company uses its fixed assets

(property, plant and equipment) by measuring how much sales are generated from its given net

fixed assets (Brigham & Ehrhardt, 2008, p. 128). The higher this ratio is the better.

2008 2007 2006 1.16 1.68 3.17

In 2008, Amylin generated $1.16 for every dollar invested in net fixed assets. In 2007

and 2006, the company generated $1.68 and $3.17 for every dollar invested in net fixed assets,

respectively. This downward trend (particularly a large drop between the years 2006 and 2007)

is discouraging and suggests decreased efficiency in management of its fixed assets. The sharp

increase in net fixed assets (the new plant in Ohio) explains this. While Amylin’s sales have

increased, in relation to net fixed assets, they have not increased enough. Simply put, net fixed

Amylin Pharmaceuticals, Inc. Financial Analysis Report 47

assets increased more than sales. This further supports the questionability of the company’s new

plant.

Total Assets Turnover [Formula: Sales/Total assets] The total assets turnover ratio measures how effectively the firm uses its total assets

(current and fixed) to produce sales. A high ratio means that the firm is able to generate a lot of

revenues given its total assets and indicates effective management of assets.

2008 2007 2006 0.45 0.40 0.45

Evidently, Amylin has maintained a relatively stable total assets turnover ratio over the

past few years; however, it is very low and this suggests poor asset management. In 2008,

Amylin was only able to generate 45 cents in revenue for every dollar in total assets. The ratios

for 2007 and 2006 can be similarly interpreted.

Debt Management Ratios

Debt management ratios are critical to investors and creditors alike because they help

appraise a firm’s long-term solvency by measuring its level of debt financing (also referred to as

financial leverage). Financial leverage, to a certain extent, can be a positive thing for investors

because their returns can be enhanced, or “leveraged,” when the company receives more on

investments financed with debt that it pays in interest. Furthermore, shareholders can preserve

their control of a company without increasing their investment. However, the greater the extent

of a firm’s financial leverage, the greater the risk. This risk is of concern to the investor, but it is

of particular concern to creditors.

Amylin Pharmaceuticals, Inc. Financial Analysis Report 48

Debt Ratio [Formula: Total liabilities/Total assets] The debt ratio compares current and long-term liabilities (debt) to current and long-term

assets and reveals the percentage of a firm’s total assets that are funded by debt. As the ratio

increases, so does the firm’s risk (Brigham & Ehrhardt, 2008, p.129). Creditors favor a fairly

low debt ratio, as it indicates they are more likely to get paid in the event of liquidation.

However, shareholders tend to like a little higher of a ratio because it means they have greater

leverage. Thus, firms have to find their ideal balance between risk and the benefits of financial

leverage. Amylin’s debt ratios for the years 2006 through 2008 are shown below.

2008 2007 2006

79.51% 68.84% 40.09%

Amylin’s debt ratio for 2006 was actually very good. That year, only about 40% of their

assets were financed with debt. This indicates a fair level of financial leverage without too much

risk. However, by 2007 the ratio had increased significantly. It continued to increase in 2008, at

which point nearly 80% of the company’s assets were financed with debt. This is an undue

amount of risk that is very unappealing to both investors and creditors. Amylin will likely have

trouble continuing to get funds through loans, as creditors will be very hesitant to provide them.

Moreover, Amylin will have to borrow at a much higher interest rate, because naturally, creditors

will require a greater return for taking on the high risk.

Times Interest Earned (TIE) [Formula: EBIT/Interest]

Simply put, the times interest earned ratio indicates a firm’s ability to pay interest. It

measures how many times a firm can make its interest payments based on its pre-tax earnings. A

very low TIE ratio means that the company may not be able to meet these financial obligations

Amylin Pharmaceuticals, Inc. Financial Analysis Report 49

and thus could be forced into bankruptcy (Brigham & Ehrhardt, 2008, p.130). So, the higher this

ratio is the better. Naturally, this ratio is of particular significance to creditors. Amylin’s TIE

ratios for the years 2006 through 2008 are presented below.

2008 2007 2006

-10.75 -4.17 -6.03

The above ratios are very disheartening in that they are negative and increasingly so. It

has become more negative due to the company’s increased use of debt financing (which

translates into greater interest charges) and increasing loss before interest and taxes. These

negative TIE ratios indicate that Amylin will be unable to meet its financial obligations if its

creditors came calling for their money. As a result, Amylin could be forced into bankruptcy.

Profitability Ratios

Up to this point we have examined ratios that help indicate the effectiveness of a firm’s

operations. This next set of ratios, the profitability ratios, takes our analysis a step further to

show the combined effects of what we have looked at so far (liquidity, asset management, and