Amlak Finance PJSC · AMLAK FINANCE PJSC Investor Relations Annual Information Pack December 2015...

30

1 AMLAK FINANCE PJSC Investor Relations Annual Information Pack December 2015 1 Investor Relations Unit, Amlak Finance PJSC, P O Box 2441, Dubai Web: http://www.amlakfinance.com/en/investor-relations.html Email: [email protected] Contact Us:

Transcript of Amlak Finance PJSC · AMLAK FINANCE PJSC Investor Relations Annual Information Pack December 2015...

1

AMLAK FINANCE PJSC

Investor Relations Annual Information Pack

December 2015

1

Investor Relations Unit, Amlak Finance PJSC, P O Box 2441, Dubai

Web: http://www.amlakfinance.com/en/investor-relations.html

Email: [email protected]

Contact Us:

2

Disclaimer

2

The information set out in this presentation is being made available to recipients for information purposes only. It does not constitute, nor is it intended to be an offer to sell, or an invitation to subscribe for, or purchase, any securities in the Company. Neither this presentation nor anything in it shall form the basis of any contract or commitment.

This presentation may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to Company’s businesses and operations, market conditions, results of operation and financial condition, capital adequacy, specific provisions and risk management practices. Readers are cautioned not to place undue reliance on these forward looking statements.

The information contained herein has been prepared to assist the Recipients in making their own evaluation on the Company and does not purport to contain all information that they may desire. In all cases, the Recipients should conduct their own investigation and analysis of the Company, its business, prospects, results of operations and financial condition as well as any other information the Recipients may deem relevant to their decision making.

The Presentation is at the date hereof. Neither the delivery of this Presentation nor any further discussions in relation to the Company or the contemplated issue of shares with any of the Recipients shall, under any circumstances, create any implication that there has been no change in the affairs of the Company since the date of this Presentation.

Without the express prior written consent of the Company, the Presentation and any information contained within it may not be (i) reproduced (in whole or in part), (ii) copied at any time, (iii) used for any purpose other than your evaluation of the Company.

3 3

Sections

UAE & DUBAI ECONOMY

REAL ESTATE MARKET

MORTGAGE MARKET

AMLAK AT A GLANCE

FINANCIAL HIGHLIGHTS

STRATEGY

STOCK INFORMATION

AWARDS

4 4

UAE & DUBAI ECONOMY

5

UAE & Dubai Economy - Overview

5

The United Arab Emirates (UAE) continues to drive regional change with an economy that has remained relatively

buoyant throughout the last couple years.

The country boasts one of the most agile economies in the world and has witnessed strong growth. As a result, the

UAE consistently scores high across all global competitiveness indices compiled by both regional and international

organizations.

President His Highness Sheikh Khalifa Bin Zayed Al Nahyan calls the Emirates’ economic model both sustainable

and responsible and expressed confidence that, as such, current policy ensures the long-term prosperity of the

nation.

Despite sharp fall in oil prices recently, UAE economy has shown resilience and capable in accommodating

changes to market dynamics, open new frontiers, and diversity thanks to the country’s strong infrastructure,

technology, and logistics.

UAE, mainly Dubai, seeks to create new sustainable and competitive economic models and adopt more flexible

approaches that boost cooperation between the public and private sector, which particularly suits the country’s

international position as a main economic player in the MENA hub. Dubai has adopted diversity in its economy and

whilst oil prices do have an undeniable effect, the variety of business activities, to a large extend, mitigate oil price

fluctuations.

Despite, many geo-political and economic challenges in Middle East, the UAE and Dubai have consistently provided

an investment oasis for professional and non-professional investors. With the 2020 Expo set for Dubai, the city is

expected to attract further attention and direct regional and foreign investment over the next few years.

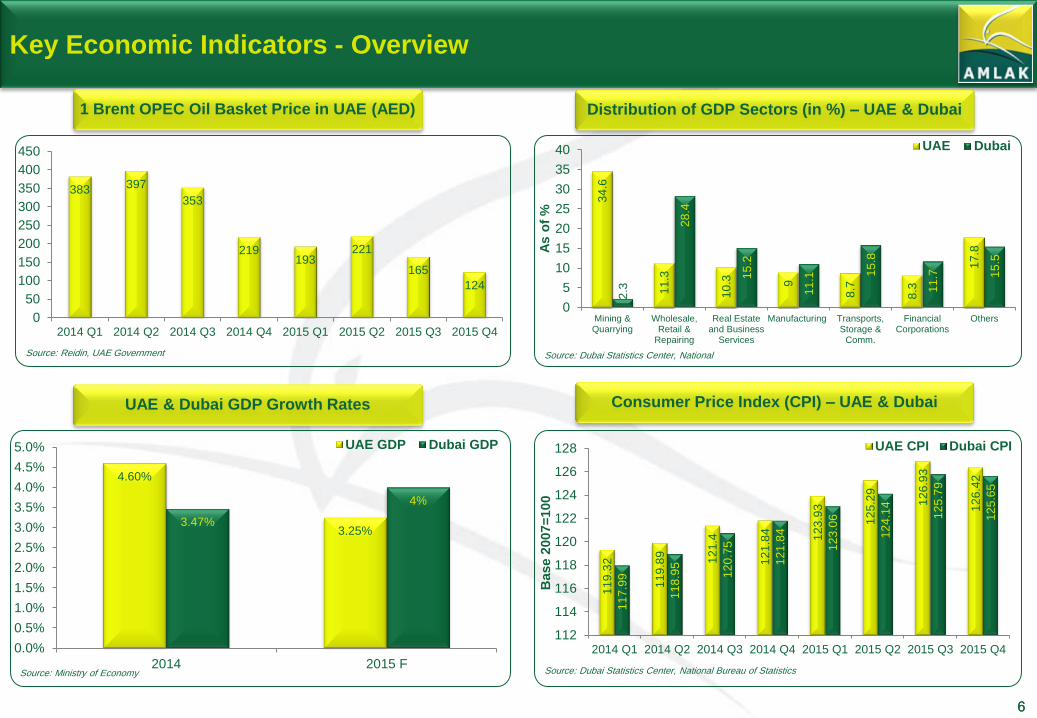

6

Key Economic Indicators - Overview

6

1 Brent OPEC Oil Basket Price in UAE (AED)

383 397

353

219 193

221

165

124

0

50

100

150

200

250

300

350

400

450

2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4

Source: Reidin, UAE Government

UAE & Dubai GDP Growth Rates

4.60%

3.25% 3.47%

4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2014 2015 F

UAE GDP Dubai GDP

Source: Ministry of Economy

Distribution of GDP Sectors (in %) – UAE & Dubai

34

.6

11

.3

10

.3

9

8.7

8.3

17

.8

2.3

28

.4

15

.2

11

.1 15

.8

11

.7

15

.5

0

5

10

15

20

25

30

35

40

Mining &Quarrying

Wholesale,Retail &

Repairing

Real Estateand Business

Services

Manufacturing Transports,Storage &

Comm.

FinancialCorporations

Others

As o

f %

UAE Dubai

Source: Dubai Statistics Center, National

Consumer Price Index (CPI) – UAE & Dubai

11

9.3

2

11

9.8

9

12

1.4

12

1.8

4

12

3.9

3

12

5.2

9

12

6.9

3

12

6.4

2

11

7.9

9

11

8.9

5

12

0.7

5

12

1.8

4

12

3.0

6

12

4.1

4

12

5.7

9

12

5.6

5

112

114

116

118

120

122

124

126

128

2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4

Base 2

007=

100

UAE CPI Dubai CPI

Source: Dubai Statistics Center, National Bureau of Statistics

7 7

REAL ESTATE MARKET

8

Real Estate Market - Overview

8

The real estate market is an important and integral part of Dubai economy. The city is famous for its community

living, commercial district and leisure projects. Major developers have retuned to the market in earnest over the last

3 years with many off plan launches, many of which have shown great success. Many lessons have also been

learnt. New laws and regulations, property registration and strata management have helped stabilize the real estate

market in Dubai allowing better visibility for investors and end users in this market segment.

However, given signs of recession in many parts of the global and regional economies, the Dubai real estate market

has cooled down since the beginning of 2015 after expanding significantly in 2013 and 2014. Coupled with lower oil

prices and the appreciation of the US dollar, has dented demand for real estate by foreign investors with

repercussions on other of key sectors such as retail and tourism.

According to the Dubai Land Department, there appears to be marked shift of investors recently, to GCC and Arab

investors with a drop in other foreigner investors who traditionally were from India, Pakistan, and United Kingdom.

2016 is likely to see fresh supply of completed properties ready for hand over which could create further price

pressure in the market. Residential sales prices are expected to decline further in 2016 but at a diminishing rate

compared to 2015, as Dubai is in the maturity phase of its real estate cycle. Rentals, on the other hand, are

expected to stay relatively stronger and robust due to the fairly more steady demand.

The commercial rent prices are expected to stabilize given the number of quality office projects scheduled to be

delivered in 2016.

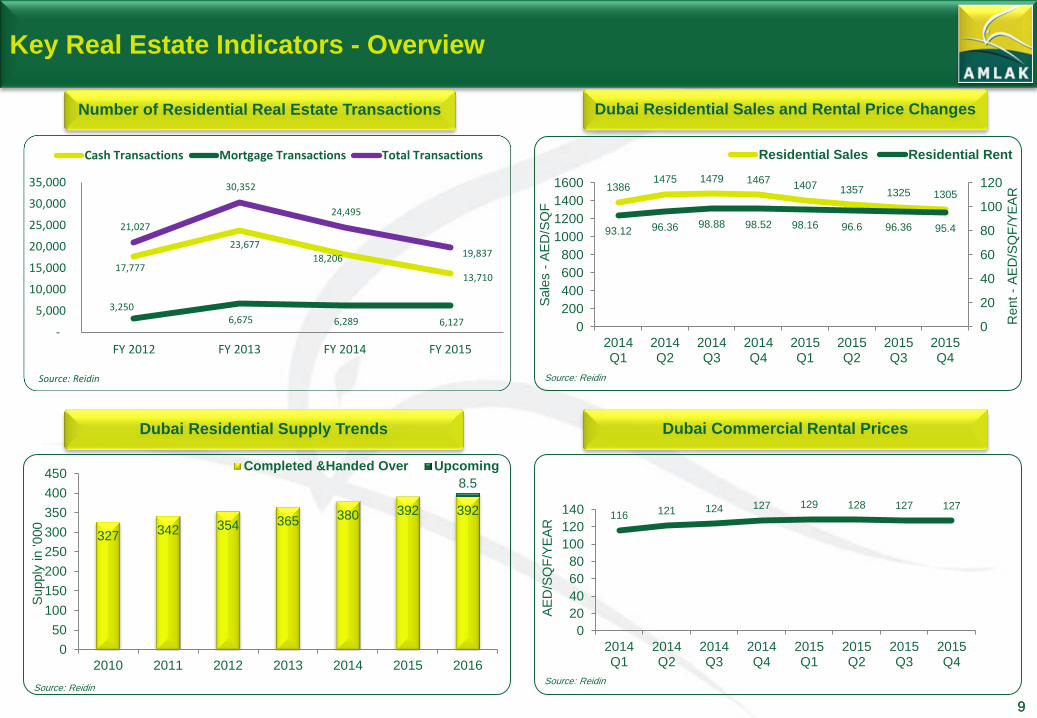

9

Key Real Estate Indicators - Overview

9

Number of Residential Real Estate Transactions

Dubai Residential Supply Trends

327 342 354 365 380 392 392

8.5

0

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014 2015 2016

Supply

in '000

Completed &Handed Over Upcoming

Source: Reidin

Dubai Residential Sales and Rental Price Changes

Dubai Commercial Rental Prices

1386 1475 1479 1467

1407 1357 1325 1305

93.12 96.36 98.88 98.52 98.16 96.6 96.36 95.4

0

20

40

60

80

100

120

0

200

400

600

800

1000

1200

1400

1600

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

Rent

- A

ED

/SQ

F/Y

EA

R

Sale

s -

AE

D/S

QF

Residential Sales Residential Rent

Source: Reidin

116 121 124 127 129 128 127 127

0

20

40

60

80

100

120

140

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

AE

D/S

QF

/YE

AR

Source: Reidin

17,777

23,677

18,206

13,710

3,250 6,675 6,289 6,127

21,027

30,352

24,495

19,837

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

FY 2012 FY 2013 FY 2014 FY 2015

Cash Transactions Mortgage Transactions Total Transactions

Source: Reidin

10 10

MORTGAGE MARKET

11

Dubai Mortgage Market - Overview

11

Historically, cash transactions have dominated residential acquisitions in the Dubai real estate market over the

mortgage transactions for the last decade. This trend highlights that Dubai real estate market has been more investor-

oriented than end-users.

Mortgage penetration rates (mortgage debt as a percentage of GDP) in GCC countries are low at 5-10%. In contrast,

developed countries like the US and UK, have mortgage penetration rates of more than 70%.

Overall value of Dubai mortgage market is estimated to be around AED 66 billion per annum over the last few years.

Out of this value, around AED 12.5 billion relates to the residential unit mortgage transactions per year.

When Dubai is compared to other real estate markets, Dubai was among the top cities in terms of price appreciation in

2013 and 2014, registering double digit increases, has now become a more affordable place to buy real estate after

prices declined around 10 - 15%. The real estate market in Dubai offers an average yield of 7%, about 2-3% above the

average yield in international property markets, especially when compared to the modest yields that mature markets like

London, Paris or New York offer.

There have been a number of changes in the Dubai mortgage market over the past year by Dubai Land Department and

Central Bank of UAE such as a new mortgage law and higher property transaction fees.

These recent changes have protected Dubai’s rebounding property market from pure speculators.

Although these recent changes may have created a short term negative effect in the market among investors in 2014,

mortgage market remained stagnant in the following years despite the overall market softening in terms of prices and

transactions.

Amlak’s main competitors in the property financing market are both local and international banks. Recently, banks have

offered lower mortgage profit/interest rates to expand their customer base in today’s slower market conditions. However,

Amlak as a specialized property financier has developed a number of innovative products which are unique and appeal

to the investor segment more prominently. Our Istithmari product which is a “Buy-to-Let” package is a clear example.

12

Mortgage Transactions and Rental Yields

12

Number of Transactions Over the Years Rental Yields in Dubai

0

2,000

4,000

6,000

8,000

10,000

12,000

2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4

Total Transactions Sales Transactions Mortgage Transactions

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4

Apartment Villa

There has been a decrease in number of sales transactions over the past two years as the Dubai real estate market experienced a healthy

correction period. Mortgage transactions, over past couple of years, have shown stable movement during this correction period. While

number of sales transactions dropped around 35% over the last two years, mortgage transactions were almost flat.

This trend is likely to continue in the near future, with some potential increase in number of transactions as market is expected to pick up

once again over the next couple of year.

Also, new project launches and a positive market outlook are expected to create further demand for mortgage financing. Combining the

new investment opportunities towards Expo 2020 and relatively low mortgage interest rates, mortgage transactions are expected to start

increasing in the medium and longer terms.

Overall, Dubai rental yields are a major attraction for property investors which is set to continue as property prices remain tight.

13 13

AMLAK AT A GLANCE

14

About Amlak

14

Amlak Finance was established in 2000 as a leading specialized real estate financier under the regulation of UAE Central Bank.

Amlak became a listed company in 2004 on the Dubai Financial Market (DFM) under the regulation of Securities and Commodities Authority (SCA) and UAE Central Bank.

Amlak became a Sharia Compliant Finance Company in 2004.

Amlak operates in UAE and Egypt with affiliation in Saudi Arabia.

In the UAE, Amlak’s focus is on Dubai property market, in both freehold and leasehold areas.

Amlak provides innovative, Shari’a-compliant property financing products and solutions for end-users and investors for both ready and off-plan/under-construction properties.

To learn more about Amlak Finance, please visit our website: http://www.amlakfinance.com

15

Vision & Mission Statements

15

“To be the specialized and customer centric real estate financing institution in the UAE”

Our Mission Our Vision

“To provide niche financial solutions, customized to fit our customers’ needs while maximizing

shareholders’ value and nurturing our employees”

Business

Segments

Real Estate Finance

Retail Customers - ready & off plan financing

Developers - project financing

Real Estate Investments

Land bank – with selected development

Ready proprietary property

Under development projects

Corporate Investments

Fully owned subsidiary in Egypt and associate company in KSA engaged in real estate financing activity

16

Board

Business (Financing and RE investments)

Finance & Investments Operations & IT Corporate Services Strategy & Organization

Development Legal, Compliance

&Sharia

Zakat

Committee

Audit

Committee

Internal

Audit

Managing Director & Chief Executive Officer

Organization Structure

16

Board Committees:

Zakat Committee

Audit Committee

Corporate Governance

Executive Committees:

MANCO (Management Committee)

ALCO (Assets Liability Committee)

Risk Committee

17

Key Products and Services

17

Amlak ‘Tatweer’ is an off plan financing product for a Buy To Let property as well as

for end users. Finance is supplemented by a complimentary full suite of property

management services that comes into effect post completion of the property.

Our basic home finance product aimed towards end users for residential as well as

commercial property in both ready and under-construction projects. Under Ijarah,

Amlak buys the property from the developer/seller and leases it out to the customer

with a promise to sell at the end of the lease term. The customer pays monthly

rentals that comprise of fixed, variable and supplementary rentals.

Amlak’s ‘Istithmari’ is the first-of-its-kind Buy-To-Let property finance (Ijarah) product

in the region, designed for investors looking to invest in completed residential and

commercial properties. Customers are also provided with a complimentary full suite

of Property Management Services.

End User Ijarah

Istithmari

Tatweer

‘Platinum Lifestyle Takaful’ is a comprehensive Takaful plans package exclusively

designed for all customers. The plans give protection against most property finance

related perils and other value added lifestyle benefits.

Platinum

Lifestyle Takaful

Developer Finance’ is given for Amlak approved unfinished projects as an advance

payment against future receivables or as an independent finance facility to complete

the project.

Developer Finance

18

Recent Developments

18

Completed Financial Restructuring in November 2014

Amlak completed its financial restructuring in 2014 which

allowed for the company to re-start business and trading

activity and relist its shares on the DFM.

Profit growth since completion of restructuring

The company’s profits grew sharply post restructuring and

have now stabilized under normal business activity cycle.

Resumed Share Trading on DFM June 2015

Amlak shares were re-admitted to Dubai Financial Market

after seven years of suspension, giving company the

opportunity to again deliver long-term value to our

shareholders. Company witnessed strong market interest in

our stock afterwards.

19 19

FINANCIAL HIGHLIGHTS

20

Group Performance Analysis

20

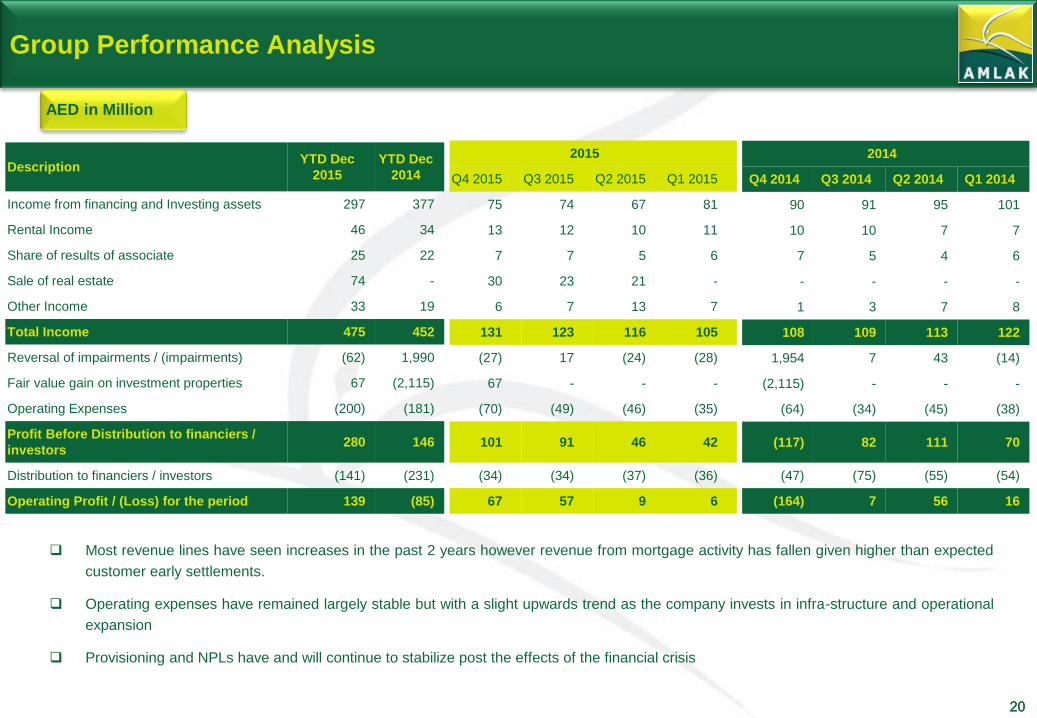

Description YTD Dec

2015

YTD Dec

2014

Income from financing and Investing assets 297 377

Rental Income 46 34

Share of results of associate 25 22

Sale of real estate 74 -

Other Income 33 19

Total Income 475 452

Reversal of impairments / (impairments) (62) 1,990

Fair value gain on investment properties 67 (2,115)

Operating Expenses (200) (181)

Profit Before Distribution to financiers /

investors 280 146

Distribution to financiers / investors (141) (231)

Operating Profit / (Loss) for the period 139 (85)

2015

Q4 2015 Q3 2015 Q2 2015 Q1 2015

75 74 67 81

13 12 10 11

7 7 5 6

30 23 21 -

6 7 13 7

131 123 116 105

(27) 17 (24) (28)

67 - - -

(70) (49) (46) (35)

101 91 46 42

(34) (34) (37) (36)

67 57 9 6

AED in Million

2014

Q4 2014 Q3 2014 Q2 2014 Q1 2014

90 91 95 101

10 10 7 7

7 5 4 6

- - - -

1 3 7 8

108 109 113 122

1,954 7 43 (14)

(2,115) - - -

(64) (34) (45) (38)

(117) 82 111 70

(47) (75) (55) (54)

(164) 7 56 16

Most revenue lines have seen increases in the past 2 years however revenue from mortgage activity has fallen given higher than expected

customer early settlements.

Operating expenses have remained largely stable but with a slight upwards trend as the company invests in infra-structure and operational

expansion

Provisioning and NPLs have and will continue to stabilize post the effects of the financial crisis

21

Group Performance – Quarterly Trends

21

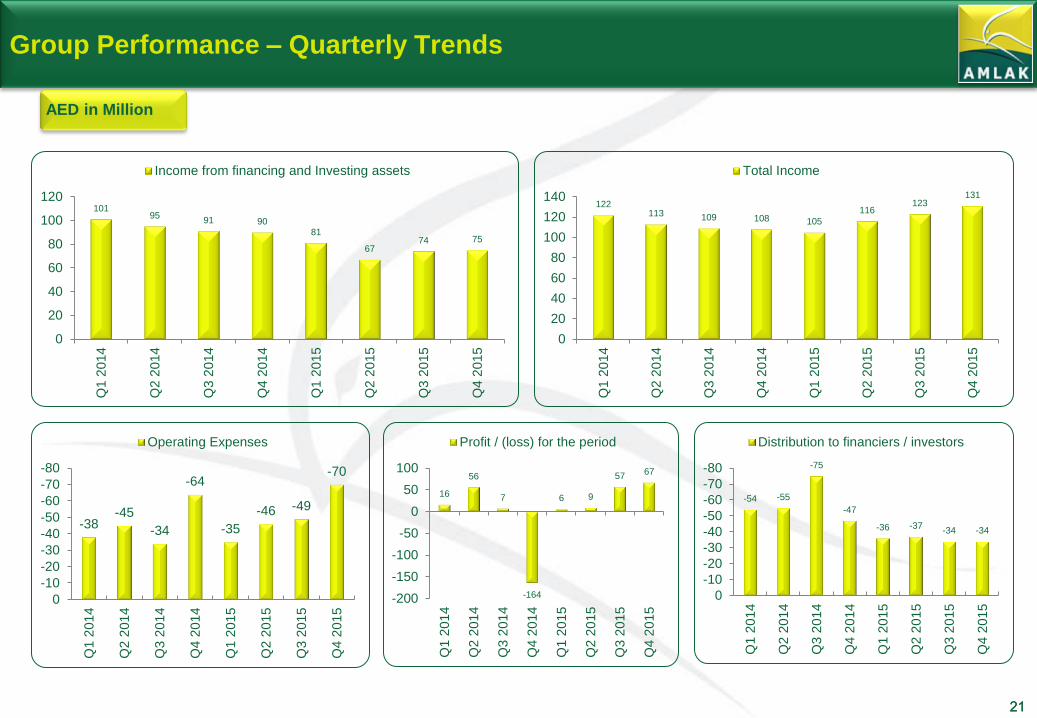

AED in Million

101 95

91 90 81

67 74 75

0

20

40

60

80

100

120

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Income from financing and Investing assets

122 113 109 108 105

116 123

131

0

20

40

60

80

100

120

140

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Total Income

-38 -45

-34

-64

-35

-46 -49

-70 -80

-70

-60

-50

-40

-30

-20

-10

0

Q1 2

014

Q2 2

014

Q3 2

014

Q4

20

14

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Operating Expenses

16

56

7

-164

6 9

57 67

-200

-150

-100

-50

0

50

100

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Profit / (loss) for the period

-54 -55

-75

-47

-36 -37 -34 -34

-80

-70

-60

-50

-40

-30

-20

-10

0

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Distribution to financiers / investors

22

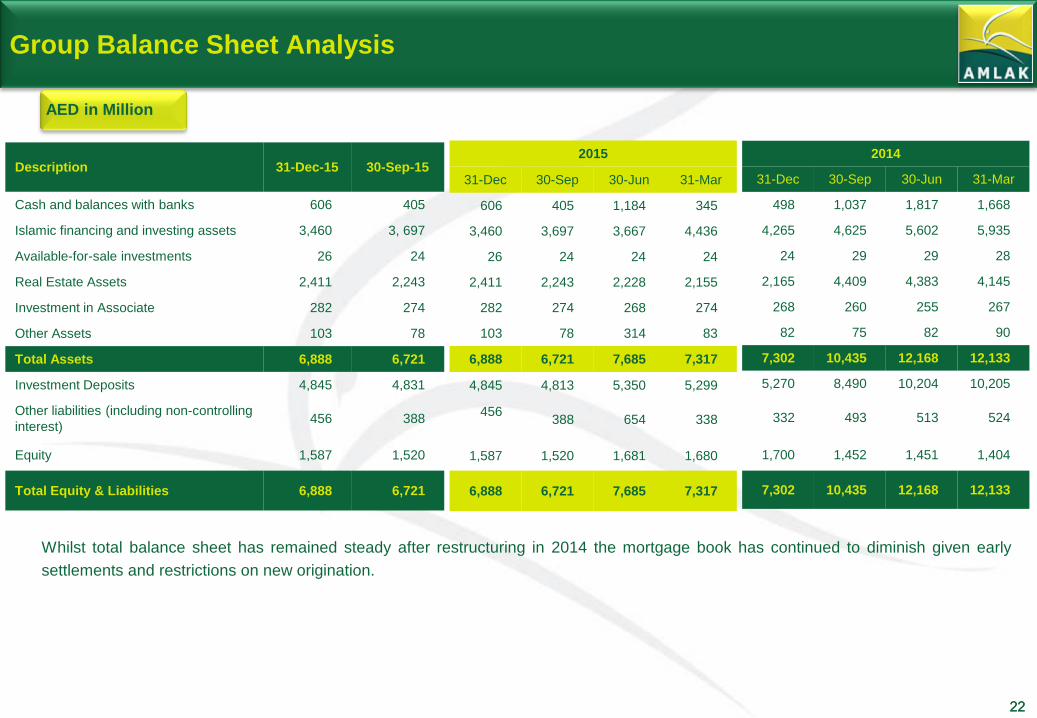

Group Balance Sheet Analysis

22

Description 31-Dec-15 30-Sep-15

Cash and balances with banks 606 405

Islamic financing and investing assets 3,460 3, 697

Available-for-sale investments 26 24

Real Estate Assets 2,411 2,243

Investment in Associate 282 274

Other Assets 103 78

Total Assets 6,888 6,721

Investment Deposits 4,845 4,831

Other liabilities (including non-controlling

interest) 456 388

Equity 1,587 1,520

Total Equity & Liabilities 6,888 6,721

2015

31-Dec 30-Sep 30-Jun 31-Mar

606 405 1,184 345

3,460 3,697 3,667 4,436

26 24 24 24

2,411 2,243 2,228 2,155

282 274 268 274

103 78 314 83

6,888 6,721 7,685 7,317

4,845 4,813 5,350 5,299

456

388 654 338

1,587 1,520 1,681 1,680

6,888 6,721 7,685 7,317

Whilst total balance sheet has remained steady after restructuring in 2014 the mortgage book has continued to diminish given early

settlements and restrictions on new origination.

AED in Million

2014

31-Dec 30-Sep 30-Jun 31-Mar

498 1,037 1,817 1,668

4,265 4,625 5,602 5,935

24 29 29 28

2,165 4,409 4,383 4,145

268 260 255 267

82 75 82 90

7,302 10,435 12,168 12,133

5,270 8,490 10,204 10,205

332 493 513 524

1,700 1,452 1,451 1,404

7,302 10,435 12,168 12,133

23

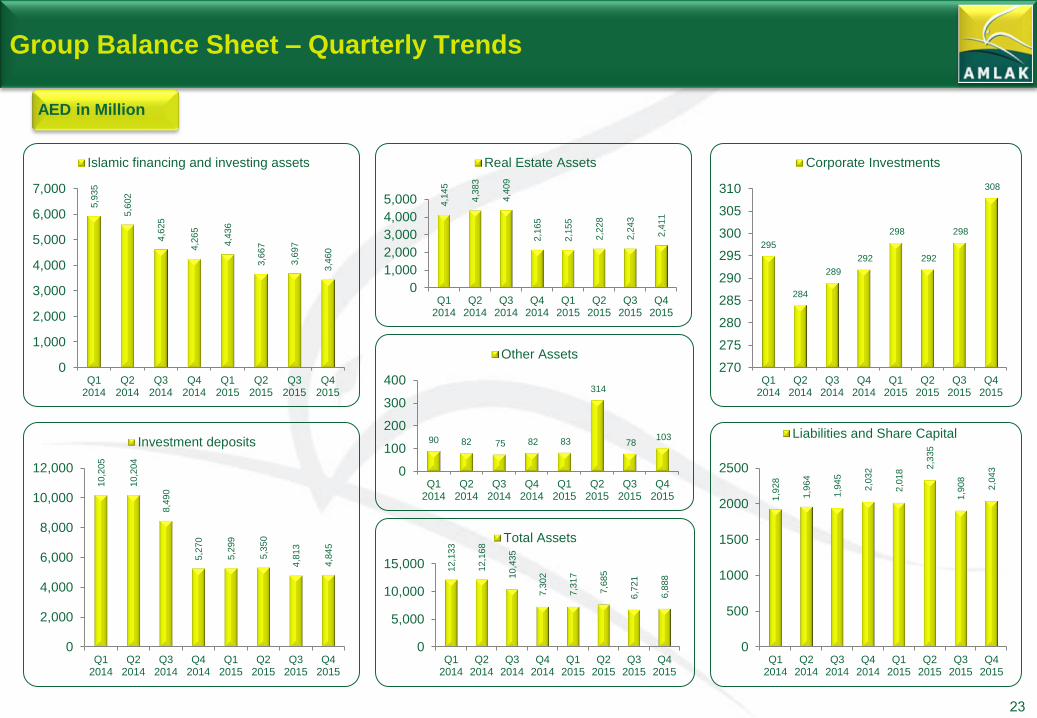

Group Balance Sheet – Quarterly Trends

AED in Million

12,1

33

12,1

68

10,4

35

7,3

02

7,3

17

7,6

85

6,7

21

6,8

88

0

5,000

10,000

15,000

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Total Assets

5,9

35

5,6

02

4,6

25

4,2

65

4,4

36

3,6

67

3,6

97

3,4

60

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Islamic financing and investing assets

4,1

45

4,3

83

4,4

09

2,1

65

2,1

55

2,2

28

2,2

43

2,4

11

0

1,000

2,000

3,000

4,000

5,000

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Real Estate Assets

295

284

289

292

298

292

298

308

270

275

280

285

290

295

300

305

310

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Corporate Investments

90 82 75 82 83

314

78 103

0

100

200

300

400

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Other Assets

10,2

05

10,2

04

8,4

90

5,2

70

5,2

99

5,3

50

4,8

13

4,8

45

0

2,000

4,000

6,000

8,000

10,000

12,000

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Investment deposits

1,9

28

1,9

64

1,9

45

2,0

32

2,0

18 2,3

35

1,9

08

2,0

43

0

500

1000

1500

2000

2500

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Liabilities and Share Capital

24 24

STRATEGY

25

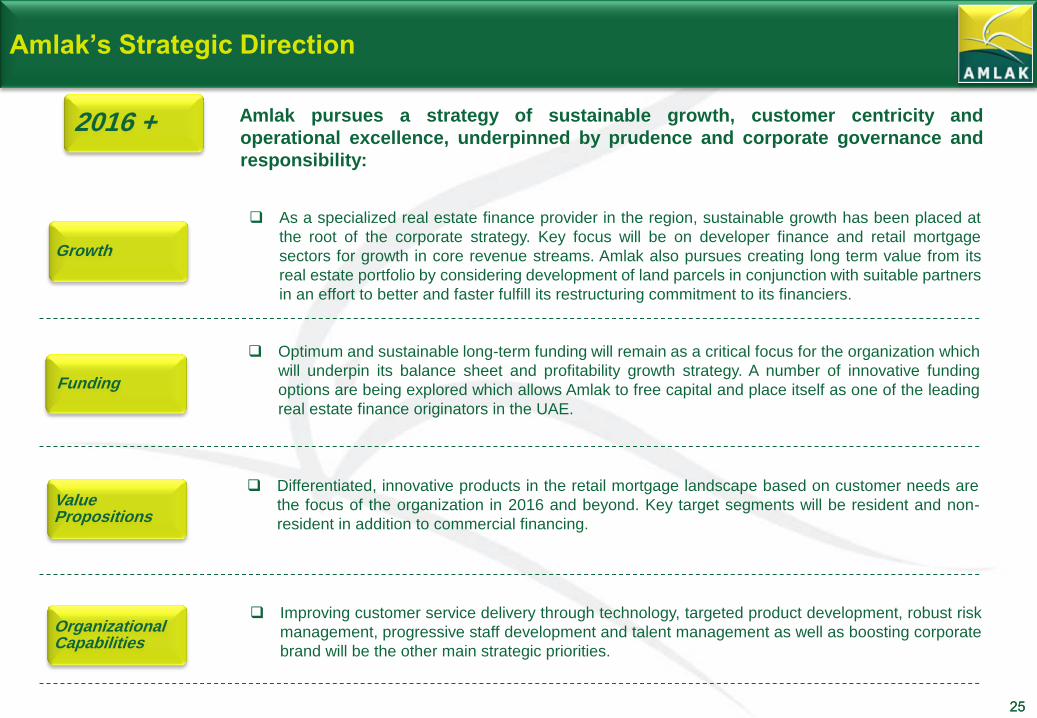

Amlak’s Strategic Direction

25

Optimum and sustainable long-term funding will remain as a critical focus for the organization which

will underpin its balance sheet and profitability growth strategy. A number of innovative funding

options are being explored which allows Amlak to free capital and place itself as one of the leading

real estate finance originators in the UAE.

Differentiated, innovative products in the retail mortgage landscape based on customer needs are

the focus of the organization in 2016 and beyond. Key target segments will be resident and non-

resident in addition to commercial financing.

As a specialized real estate finance provider in the region, sustainable growth has been placed at

the root of the corporate strategy. Key focus will be on developer finance and retail mortgage

sectors for growth in core revenue streams. Amlak also pursues creating long term value from its

real estate portfolio by considering development of land parcels in conjunction with suitable partners

in an effort to better and faster fulfill its restructuring commitment to its financiers.

Growth

Funding

Value Propositions

Improving customer service delivery through technology, targeted product development, robust risk

management, progressive staff development and talent management as well as boosting corporate

brand will be the other main strategic priorities.

Organizational Capabilities

2016 + Amlak pursues a strategy of sustainable growth, customer centricity and

operational excellence, underpinned by prudence and corporate governance and

responsibility:

26

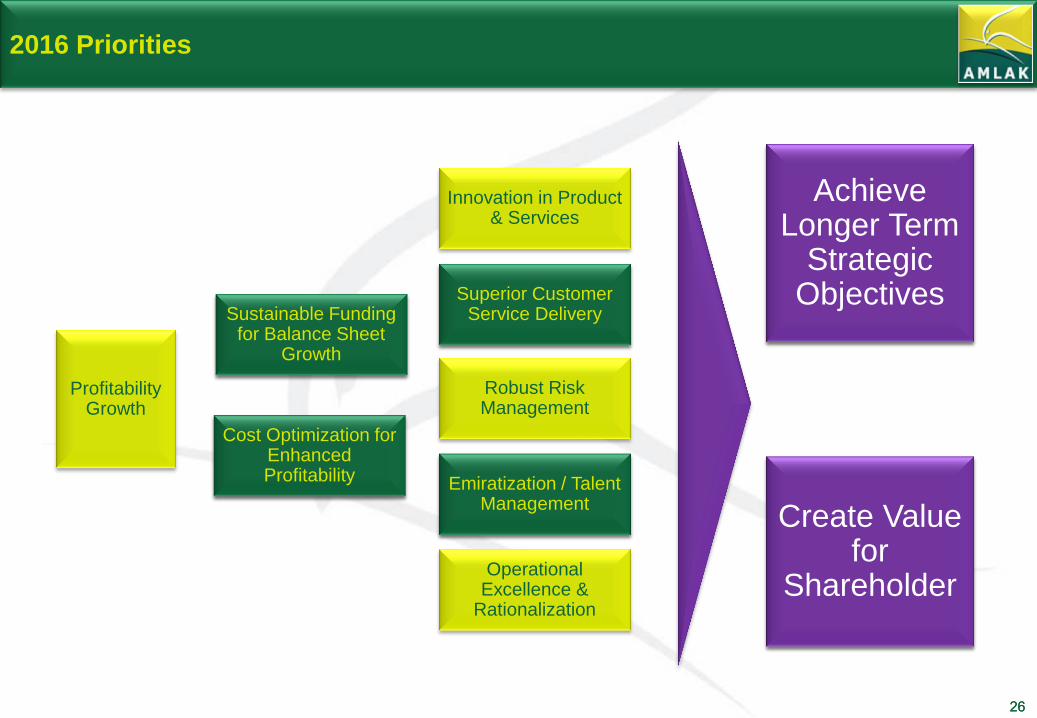

2016 Priorities

26

Innovation in Product & Services

Superior Customer Service Delivery

Robust Risk Management

Emiratization / Talent Management

Operational Excellence &

Rationalization

Sustainable Funding for Balance Sheet

Growth

Cost Optimization for Enhanced Profitability

Profitability Growth

Achieve Longer Term

Strategic Objectives

Create Value for

Shareholder

27 27

STOCK INFORMATION

28

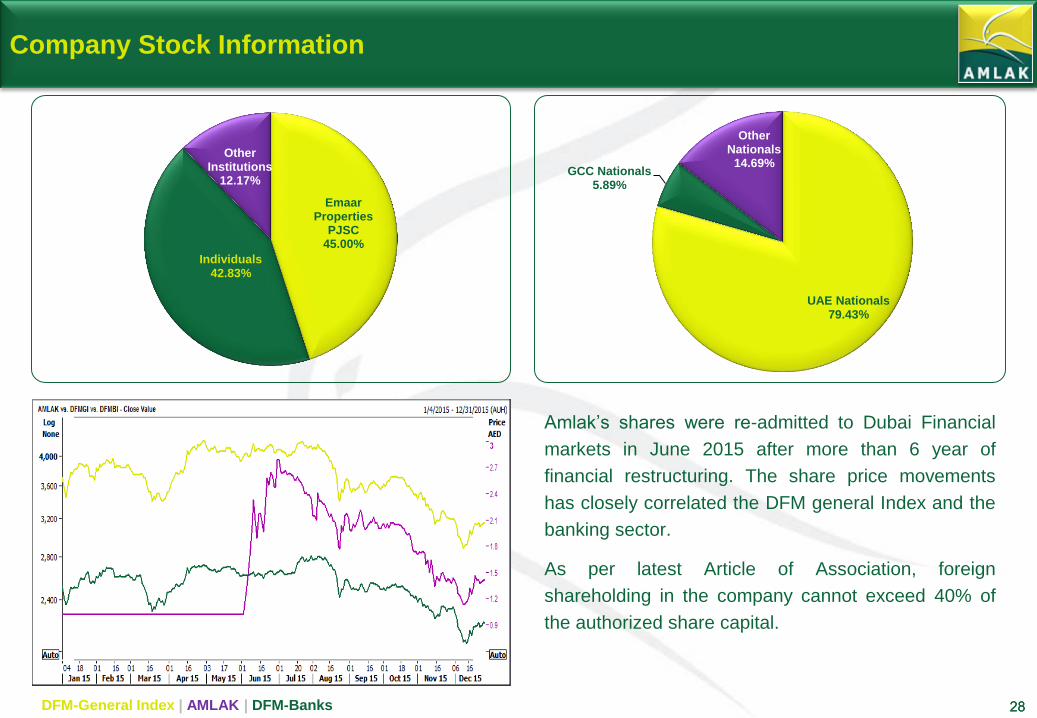

Company Stock Information

28

Emaar Properties

PJSC 45.00%

Individuals 42.83%

Other Institutions

12.17%

UAE Nationals 79.43%

GCC Nationals 5.89%

Other Nationals

14.69%

DFM-General Index | AMLAK | DFM-Banks

Amlak’s shares were re-admitted to Dubai Financial

markets in June 2015 after more than 6 year of

financial restructuring. The share price movements

has closely correlated the DFM general Index and the

banking sector.

As per latest Article of Association, foreign

shareholding in the company cannot exceed 40% of

the authorized share capital.

29 29

AWARDS

30

Awards - 2015

30